UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-23297

————————

Infinity Long/Short Equity Fund, LLC.

—————————————————

(Exact name of registrant as specified in charter)

c/o UMB Fund Services, Inc.

235 West Galena Street

Milwaukee, WI 53212

—————————————————————

(Address of principal executive offices) (Zip code)

Terrance P. Gallagher

235 West Galena Street

Milwaukee, WI 53212

—————————————————————

(Name and address of agent for service)

Registrant’s telephone number, including area code: (414) 299-2270

—————

Date of fiscal year end: March 31

———

Date of reporting period: March 31, 2019

—————

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-1090. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

The Report to The Members is attached herewith.

INFINITY LONG/SHORT EQUITY FUND, LLC

(a Delaware Limited Liability Company)

Annual Report

For the Year Ended March 31, 2019

Beginning on January 1, 2021 as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Infinity Long/Short Equity Fund, LLC’s shareholder reports, like this one, will no longer be sent by mail, unless you specifically request paper copies of the reports from the Fund [or from your financial intermediary, such as a broker-dealer or bank]. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund c/o UMB Fund Services at 235 West Galena Street, Milwaukee, WI 53212, or by calling toll-free at 1-(877)-775-7751. If you own your shares through a financial intermediary (such as a broker-dealer or bank), you must contact your financial intermediary.

You may elect to receive all future reports in paper free of charge. You can inform the Fund or your financial intermediary that you wish to continue receiving paper copies of your shareholder reports by contacting them directly. Your election to receive reports in paper will apply to the Fund and all funds held through your financial intermediary, as applicable

INFINITY LONG/SHORT EQUITY FUND, LLC

(a Delaware Limited Liability Company)

For the Year Ended March 31, 2019

Table of Contents

|

grant thornton llp | |

| Grant Thornton Tower | |

| 171 N. Clark Street, Suite 200 | |

| Chicago, IL 60601-3370 |

| D | +1 312 856 0200 | |

| F |

+1 312 565 4719 |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Board of Managers and Members of

Infinity Long/Short Equity Fund, LLC

Opinion on the financial statements

We have audited the accompanying statement of assets, liabilities and members’ equity of Infinity Long/Short Equity Fund, LLC (the “Fund”), including the schedule of investments, as of March 31, 2019, the related statements of operations and cash flows for the year then ended, and the statement of changes in members’ equity and the financial highlights for each of the two years in the period then ended, and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of March 31, 2019, and the results of its operations and its cash flows for the year then ended, and its financial highlights for each of the two years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. The financial highlights for the period from October 1, 2016 (commencement of operations) to March 31, 2017, were audited by other auditors whose report thereon dated September 30, 2017, expressed an unqualified opinion on those financial highlights.

Basis for opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

| GT.COM | Grant Thornton LLP is the U.S. member firm of Grant Thornton International Ltd (GTIL). GTIL and each of its member firms are separate legal entities and are not a worldwide partnership. |

| 1 |

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. Our procedures included confirmation of securities owned as of March 31, 2019, by correspondence with the custodian. We believe that our audits provide a reasonable basis for our opinion.

/s/ GRANT THORNTON LLP

We have served as the Fund’s auditor since 2018.

Chicago, Illinois

May 30, 2019

| 2 |

| Infinity Long/Short Equity Fund, LLC |

| (a Delaware Limited Liability Company) |

| Schedule of Investments |

| March 31, 2019 |

| Redemptions | Redemption | Investment | Original | |||||||||||||

| Investment Funds (95.42%) | Permitted | Notice Period | Strategy | Cost | Fair Value | Acquisition Date | ||||||||||

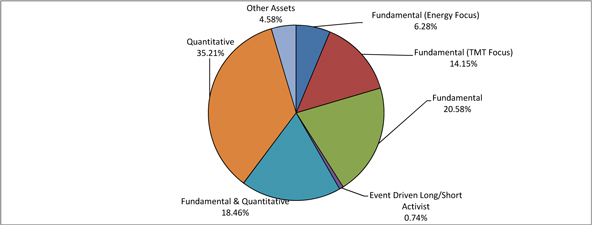

| BAM Zie Fund, LLC a,b,c | Quarterly | 65 Days | Fundamental (Energy Focus) | $ | 1,494,992 | $ | 1,183,867 | 10/1/2016 | ||||||||

| Coatue Qualified Partners, L.P. a,b,c | Quarterly | 45 Days | Fundamental (TMT Focus) | 2,300,000 | 2,670,098 | 10/1/2016 | ||||||||||

| Hoplite Partners, L.P. a,b,c | Quarterly | 45 Days | Fundamental | 2,300,000 | 2,440,284 | 10/1/2016 | ||||||||||

| Jana Partners Qualified, L.P. Class A a,b | Quarterly | 60 Days | Event Driven Long/Short Activist | 150,500 | 140,543 | 10/1/2017 | ||||||||||

| MW Eureka (US) Fund Class A2 a,b | Monthly | 30 Days | Fundamental & Quantitative | 3,117,145 | 3,482,915 | 10/1/2016 | ||||||||||

| Renaissance Institutional Equities Fund LLC a,b | Monthly | 45 Days | Quantitative | 2,935,253 | 3,682,788 | 10/1/2016 | ||||||||||

| Swiftcurrent Offshore, Ltd. a,b,c | Semi-Annually | 90 Days | Fundamental | 1,400,000 | 1,442,000 | 10/1/2017 | ||||||||||

| Two Sigma Spectrum Cayman Fund, Ltd. a,b,d | Quarterly | 55 Days | Quantitative | 2,640,560 | 2,959,332 | 1/1/2018 | ||||||||||

| Total Investment Funds (cost $16,338,450) (95.42%) | 18,001,827 | |||||||||||||||

| Total Investment (cost $16,338,450) (95.42%) | $ | 18,001,827 | ||||||||||||||

| Other assets in excess of liabilities (4.58%) | 864,032 | |||||||||||||||

| Members' Equity - 100.00% | $ | 18,865,859 | ||||||||||||||

a Non-income producing.

b Investment Funds are issued in private placement transactions and as such are restricted as to resale.

c Early redemption penalties may apply.

d The investment fund can institute a gate provision on redemptions at the fund level of 10% of the fair value of investment in the investment fund.

INVESTMENT STRATEGIES OF INVESTMENT FUND HOLDINGS AS A PERCENTAGE OF TOTAL NET ASSETS

Percentages as a percentage of total net assets are as follows:

The accompanying notes are an integral part of these Financial Statements.

| 3 |

| Infinity Long/Short Equity Fund, LLC |

| (a Delaware Limited Liability Company) |

| Statement of Assets, Liabilities and Members' Equity |

| March 31, 2019 |

| Assets | ||||

| Investments, at fair value (cost $16,338,450) | $ | 18,001,827 | ||

| Cash | 1,175,962 | |||

| Receivable for investments sold | 412,478 | |||

| Total Assets | 19,590,267 | |||

| Liabilities | ||||

| Payable for shares repurchased | 674,999 | |||

| Accounting and administration fees payable | 18,765 | |||

| Professional fees payable | 27,262 | |||

| Custody fees payable | 667 | |||

| Other fees payable | 2,715 | |||

| Total Liabilities | 724,408 | |||

| Members' Equity | $ | 18,865,859 | ||

| Members' Equity consists of: | ||||

| Members' Equity paid-in | $ | 17,643,014 | ||

| Total distributable earnings | 1,222,845 | |||

| Total Members' Equity | $ | 18,865,859 | ||

| Number of Shares Outstanding | 17,246.690 | |||

| Members' Equity per Share | $ | 1,093.88 | ||

The accompanying notes are an integral part of these Financial Statements.

| 4 |

| Infinity Long/Short Equity Fund, LLC |

| (a Delaware Limited Liability Company) |

| Statement of Operations |

| For the Year Ended March 31, 2019 |

| Expenses | ||||

| Investment management fee | $ | 244,204 | ||

| Professional fees | 100,362 | |||

| Accounting and administration fees | 96,492 | |||

| Managers' fees | 28,000 | |||

| Offering costs | 20,836 | |||

| Other expenses | 14,008 | |||

| Insurance fees | 12,008 | |||

| Chief Compliance Officer fees | 10,650 | |||

| Excise tax | 10,189 | |||

| Custody fees | 9,786 | |||

| Blue sky fees | 921 | |||

| Total Operating Expenses | 547,456 | |||

| Expense Waivers | (244,204 | ) | ||

| Net Expenses | 303,252 | |||

| Net Investment Loss | (303,252 | ) | ||

| Realized and Unrealized Gain (Loss) on Investments | ||||

| Net realized loss from investments | (130,283 | ) | ||

| Net change in unrealized appreciation on investments | 559,896 | |||

| Net Realized and Unrealized Gain on Investments | 429,613 | |||

| Net Increase in Members' Equity from Operations | $ | 126,361 |

The accompanying notes are an integral part of these Financial Statements.

| 5 |

| Infinity Long/Short Equity Fund, LLC |

| (a Delaware Limited Liability Company) |

| Statements of Changes in Members' Equity |

| Year Ended | Year Ended | |||||||

| March 31, 2019 | March 31, 2018* | |||||||

| Operations | ||||||||

| Net investment loss | $ | (303,252 | ) | $ | (174,980 | ) | ||

| Net realized gain (loss) on investments | (130,283 | ) | 233,924 | |||||

| Net change in unrealized appreciation on investments | 559,896 | 910,719 | ||||||

| Net change in Members' equity from operations | 126,361 | 969,663 | ||||||

| Distributions to Members | ||||||||

| Distributions1 | (198,332 | ) | ||||||

| From net investment income | (16,970 | ) | ||||||

| Net change in Members' equity from distributions to Members | (198,332 | ) | (16,970 | ) | ||||

| Capital Share Transactions | ||||||||

| Sale of shares | 75,000 | 11,682,700 | ||||||

| Reinvested distributions | 198,332 | 16,970 | ||||||

| Shares repurchased | (1,131,831 | ) | - | |||||

| Net change in Members' equity from capital transactions | (858,499 | ) | 11,699,670 | |||||

| Total Increase (Decrease) | (930,470 | ) | 12,652,363 | |||||

| Members' Equity | ||||||||

| Beginning of period | 19,796,329 | 7,143,966 | ||||||

| End of period2 | $ | 18,865,859 | $ | 19,796,329 | ||||

* As of October 4, 2017 the Fund registered as an investment company under the Investment Company Act of 1940, as amended.

1 The SEC eliminated the requirement to disclose components of distributions paid to Members in 2018.

2 End of period Members' equity includes accumulated undistributed net investment income of $123,108 for the year ended March 31, 2018. The requirement to disclose undistributed net investment income was eliminated in 2018.

The accompanying notes are an integral part of these Financial Statements.

| 6 |

| Infinity Long/Short Equity Fund, LLC |

| (a Delaware Limited Liability Company) |

| Statement of Cash Flows |

| For the Year Ended March 31, 2019 |

| CASH FLOWS FROM OPERATING ACTIVITIES | ||||

| Net Increase in Members' Equity from Operations | $ | 126,361 | ||

| Adjustments to reconcile Net Increase in Members' Equity from | ||||

| Operations to net cash provided by operating activities: | ||||

| Net realized loss from investments | 130,283 | |||

| Net change in unrealized appreciation on investments | (559,896 | ) | ||

| Purchases of Investment Funds | (800,000 | ) | ||

| Proceeds from Investment Funds sold | 2,600,537 | |||

| Changes in operating assets and liabilities: | ||||

| Decrease in prepaid offering costs | 20,836 | |||

| Decrease in due from adviser | 867 | |||

| Decrease in other assets | 921 | |||

| Decrease in accounting and administration fees payable | (5,470 | ) | ||

| Increase in professional fees payable | 1,862 | |||

| Decrease in custody fees payable | (191 | ) | ||

| Decrease in Chief Compliance Officer fees payable | (1,591 | ) | ||

| Increase in other fees payable | 416 | |||

| Net Cash Provided by Operating Activities | 1,514,935 | |||

| CASH FLOWS FROM FINANCING ACTIVITIES | ||||

| Proceeds from sale of shares, including sale of shares received in advance | 75,000 | |||

| Payments for shares repurchased | (456,832 | ) | ||

| Net Cash Used in Financing Activities | (381,832 | ) | ||

| Net change in cash | 1,133,103 | |||

| Cash at beginning of period | 42,859 | |||

| Cash at end of period | $ | 1,175,962 | ||

| Supplemental disclosure of reinvested distributions | $ | 198,332 |

The accompanying notes are an integral part of these Financial Statements.

| 7 |

| Infinity Long/Short Equity Fund, LLC |

| (a Delaware Limited Liability Company) |

| Financial Highlights |

| Period from | ||||||||||||

| October 1, 2016 | ||||||||||||

| (Commencement | ||||||||||||

| Year Ended | Year Ended | of Operations) | ||||||||||

| March 31, 2019 | March 31, 2018* | to March 31, 2017 | ||||||||||

| Members' Equity, Beginning of Period | $ | 1,098.86 | $ | 1,022.61 | $ | 1,000.00 | ||||||

| Income from investment operations: | ||||||||||||

| Net investment loss (1) | (17.02 | ) | (13.97 | ) | (5.31 | ) | ||||||

| Net realized and unrealized gain on investments | 23.27 | 91.18 | 27.92 | |||||||||

| Total from investment operations: | 6.25 | 77.21 | 22.61 | |||||||||

| Distributions to Members | ||||||||||||

| From net investment income | (0.74 | ) | (0.96 | ) | - | |||||||

| From net realized gains | (10.49 | ) | - | - | ||||||||

| Net change in Members' equity due to distributions to Members | (11.23 | ) | (0.96 | ) | - | |||||||

| Members' Equity, End of Period | $ | 1,093.88 | $ | 1,098.86 | $ | 1,022.61 | ||||||

| Total Return (2) | 0.61 | % | 7.55 | % | 2.26 | %(3) | ||||||

| Members' Equity, end of period (in thousands) | $ | 18,866 | $ | 19,796 | $ | 7,144 | ||||||

| Net investment loss to average Members' equity | (1.56 | )% | (1.29 | )% | (1.06 | )%(4) | ||||||

| Ratio of gross expenses to average Members' equity (5) | 2.81 | % | 2.68 | % | 2.26 | %(4) | ||||||

| Ratio of expense waiver to average Members' equity | (1.25 | )% | (1.39 | )% | (1.20 | )%(4) | ||||||

| Ratio of net expenses to average Members' equity | 1.56 | %(6) | 1.29 | % | 1.06 | %(4) | ||||||

| Portfolio Turnover | 4.20 | % | 24.27 | % | 0.18 | %(3) | ||||||

* As of October 4, 2017 the Fund registered as an investment company under the Investment Company Act of 1940, as amended.

(1) Based on average shares outstanding for the year.

(2) Total Return based on Members' equity is the combination of changes in Members' equity and reinvested dividend

income in Members' equity, if any. Total Return does not reflect the impact of any applicable sales charges.

(3) Not annualized.

(4) Annualized.

(5) Represents the ratio of expenses to average Members' equity absent fee waivers and/or expense reimbursement by the Adviser.

(6) The Fund's operating expenses include an excise tax , which is excluded from the Expense Limitation calculation. If the excise tax was excluded from operating expenses, the net expense ratio would be 1.50%.

The accompanying notes are an integral part of these Financial Statements.

| 8 |

| INFINITY LONG/SHORT EQUITY FUND, LLC |

| (a Delaware Limited Liability Company) |

| Notes to Financial Statements – March 31, 2019 |

| 1. | ORGANIZATION |

Infinity Long/Short Equity Fund, LLC (the “Fund”) is a Delaware limited liability company organized under a Limited Liability Company Agreement dated June 22, 2016, and commenced operations on October 1, 2016. On October 4, 2017, the Fund filed its initial registration statement with the Securities and Exchange Commission (the “SEC”) under the Investment Company Act of 1940, as amended (the “1940 Act”), as a non-diversified, closed-end management investment company. The Fund’s amended registration statement was filed with the SEC on December 22, 2017. Infinity Capital Advisors, LLC serves as the investment adviser (the “Adviser”) of the Fund. The Adviser is an investment adviser registered with the SEC under the Investment Advisers Act of 1940, as amended.

The investment objective of the Fund is to seek long-term capital growth. The Fund is a “fund of funds” that invests primarily in general or limited partnerships, funds, corporations, trusts or other investment vehicles collectively, “Investment Funds”) based primarily in the United States that invest or trade, both long and short, in a wide range of securities, and, to a lesser extent, other property and currency interests. Certain of the Investment Funds in which the Fund may invest are commonly referred to as hedge funds. The Fund may also make investments outside of Investment Funds to hedge exposures deemed too risky or to invest in strategies not employed by the Fund’s Investment Funds. Such investments could also be used to hedge a position in an Investment Fund that is locked-up or difficult to sell. Direct investments could include U.S. and foreign equity securities, debt securities, exchange-traded funds and derivatives related to such instruments, including futures and options thereon.

The Board of Managers of the Fund (the “Board”) has overall responsibility for the management and supervision of the business operations of the Fund.

| 2. | SIGNIFICANT ACCOUNTING POLICIES |

The following is a summary of the significant accounting policies consistently followed by the Fund in the preparation of its financial statements. The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America (“U.S. GAAP”) requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from these estimates. The Fund is an investment company and follows the accounting and reporting guidance in Financial Accounting Standards Board (“FASB”) Accounting Standards Codification Topic 946.

a. Valuation of Investments

The Board has established a Valuation Committee to oversee the valuation of the Fund’s investments on behalf of the Fund. The Board has approved valuation procedures for the Fund (the “Valuation Procedures”). The Valuation Procedures provide that the Fund will value its investments in direct investments and Investment Funds at fair value.

The valuations of investments in Investment Funds are supported by information received from the Investment Funds such as monthly net asset values, investor reports, and audited financial statements, when available.

In accordance with the Valuation Procedures, fair value as of each month-end or other applicable accounting periods, as applicable, ordinarily will be the value determined as of such date by each Investment Fund in accordance with the Investment Fund’s valuation policies and reported at the time of the Fund’s valuation. As a general matter, the fair value of the Fund’s interest in an Investment Fund will represent the amount that the Fund could reasonably expect to receive from the Investment Fund if the Fund’s interest was redeemed at the time of valuation, based on information reasonably available at the time the valuation is made and that the Fund believes to be reliable. Generally, the fair value of an Investment Fund is its net asset value. In the event that the Investment Fund does not report a month-end net asset value to the Fund on a timely basis, the Fund will determine the fair value of such Investment Fund based on the most recent final or estimated value reported by the Investment Fund, as well as any other relevant information available at the time the Fund values its portfolio. Using the nomenclature of the hedge fund industry, any values reported as “estimated” or “final” are expected to reasonably reflect fair market values of securities when available or fair value as of the Fund’s valuation date. A substantial amount of time may elapse between the occurrence of an event necessitating the pricing of the Fund’s assets and the receipt of valuation information from the underlying manager of an Investment Fund.

| 9 |

| INFINITY LONG/SHORT EQUITY FUND, LLC |

| (a Delaware Limited Liability Company) |

| Notes to Financial Statements – March 31, 2019 (continued) |

| 2. | SIGNIFICANT ACCOUNTING POLICIES (continued) |

a. Valuation of Investments (continued)

If it is probable that the Fund will sell an investment at an amount different from the net asset valuation or in other situations where the month-end valuation of the Investment Fund is not available, or when the Fund believes alternative valuation techniques are more appropriate, the Adviser and the Valuation Committee may consider other factors, including subscription and redemption rights, expected discounted cash flows, transactions in the secondary market, bids received from potential buyers, and overall market conditions in determining fair value.

The Fund classifies its assets and liabilities into three levels based on the lowest level of input that is significant to the fair value measurement. Estimated values may differ from the values that would have been used if a ready market existed or if the investments were liquidated at the valuation date.

The three-tier hierarchy distinguishes between (1) inputs that reflect the assumptions market participants would use in pricing an asset or liability developed based on market data obtained from sources independent of the reporting entity (observable inputs) and (2) inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing an asset or liability developed based on the best information available in the circumstances (unobservable inputs) and to establish classification of fair value measurements for disclosure purposes. Various inputs are used in determining the value of the Fund’s investments. The inputs are summarized in the three broad levels listed below:

|

|

· | Level 1 - quoted prices (unadjusted) in active markets for identical assets and liabilities | |

| · | Level 2 - other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, ability to redeem in the near term (generally within the next calendar quarter for Investment Funds), etc.) | ||

| · | Level 3 - significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) or investments that cannot be fully redeemed at the net asset value in the “near term” (these are investments that generally have one or more of the following characteristics: gated redemptions, suspended redemptions, or have lock-up periods greater than 90 days). | ||

In April 2015, the FASB issued Accounting Standards Update (“ASU”) 2015-7, Disclosures for Investments in Certain Entities That Calculate Net Asset Value per Share (or Its Equivalent), modifying Accounting Standards Codification 946 Financial Services – Investment Companies. Under the modifications, investments in affiliated and private investment funds valued at the net asset value as practical expedient are no longer included in the fair value hierarchy. As a result of adopting ASU 2015-7, investments in Investment Funds with a fair value of $18,001,827 are excluded from the fair value hierarchy as of March 31, 2019.

As of March 31, 2019, the Fund does not hold any investments that have to be included in the fair value hierarchy.

The Adviser generally categorizes the investment strategies of the Investment Funds into investment strategy categories. The investment objective of the long/short hedge funds is to outperform the equity markets with half to two-thirds of the indices’ volatility. The investment strategy of the fundamental, bottoms-up long/short equities managers is to perform balance sheet analysis, along with many other layers of company and industry specific analysis to uncover intrinsic values that does not match where the market is currently priced. They will buy stocks that are below their intrinsic value and they will short stocks they feel are above their intrinsic value. The sector specific Investment Fund managers rely on their deep expertise within their sector of focus and work to provide alpha through the active management of their sectors through deep fundamental analysis. The quantitative approach uses internally developed and tested algorithms and models that use market data to trade in the equity space.

The Investment Funds compensate their respective Investment Fund managers through management fees currently ranging from 0.50% to 2.0% annually of average net asset value of the Fund’s investment and incentive allocations typically ranging between 10.0% and 25.0% of profits, subject to loss carryforward provisions, as defined in the respective Investment Funds’ agreements.

| 10 |

| INFINITY LONG/SHORT EQUITY FUND, LLC |

| (a Delaware Limited Liability Company) |

| Notes to Financial Statements – March 31, 2019 (continued) |

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

b. Investment Income

Interest income is recorded on an accrual basis. Investment transactions are accounted for on a trade date basis. The Fund determines the gain or loss realized from the investment transactions by comparing the original cost of the security lot sold with the net sale proceeds.

c. Fund Expenses

The Fund will pay all of its expenses, or reimburse the Adviser or their affiliates to the extent they have previously paid such expenses on behalf of the Fund. The expenses of the Fund include, but are not limited to, any fees and expenses in connection with the offering and issuance of shares of beneficial interest (“Shares”) of the Fund; all fees and expenses directly related to portfolio transactions and positions for the Fund’s account such as direct and indirect expenses associated with the Fund’s investments, and enforcing the Fund’s rights in respect of such investments; and all fees and expenses reasonably incurred in connection with the operation of the Fund, such as investment management fee, legal fees, auditing fees, accounting, administration, and tax preparation fees, custodial fees, fees for data and software providers, costs of insurance, registration expenses, managers’ fees, and expenses of meetings of the Board.

d. Income Tax Information & Distributions to Members

The Fund's policy is to comply with the requirements of Subchapter M of the Internal Revenue Code of 1986, as amended, that are applicable to regulated investment companies (“RICs”) and to distribute substantially all of its net investment income and any net realized gains to its members (“Members”). Therefore, no provision is made for federal income or excise taxes. Due to the timing of dividend distributions and the differences in accounting for income and realized gains and losses for financial statement and federal income tax purposes, the fiscal year in which amounts are distributed may differ from the year in which the income and realized gains and losses are recorded by the Fund.

Accounting for Uncertainty in Income Taxes (the “Income Tax Statement”) requires an evaluation of tax positions taken (or expected to be taken) in the course of preparing the Fund’s tax returns to determine whether these positions meet a “more-likely-than-not” standard that, based on the technical merits, have a more than fifty percent likelihood of being sustained by a taxing authority upon examination. A tax position that meets the “more-likely-than-not” recognition threshold is measured to determine the amount of benefit to recognize in the financial statements. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations.

The Income Tax Statement requires management of the Fund to analyze tax positions expected to be taken in the Fund’s tax returns, as defined by Internal Revenue Service (the “IRS”) statute of limitations for all major jurisdictions, including federal tax authorities and certain state tax authorities. During fiscal the year ended March 31, 2019, the Fund did not have a liability for any unrecognized tax benefits. At March 31, 2019, the tax years ended March 31, 2017, March 31, 2018, and March 31, 2019 remain open to examination by the IRS. The Fund has no examination in progress and is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months.

The Regulated Investment Company Modernization Act of 2010 (the "Act") was signed into law on December 22, 2010. The Act makes changes to a number of the federal income and excise tax provisions impacting RICs, including simplification provisions on asset diversification and qualifying income tests, provisions aimed at preserving the character of the distributions made by the RIC and coordination of the income and excise tax distribution requirements, and provisions for allowing unlimited years carryforward for capital losses.

The character of distributions made during the year from net investment income or net realized gain may differ from the characterization for federal income tax purposes due to differences in the recognition of income, expense and gain/(loss) items for financial statement and tax purposes. Where appropriate, reclassifications between net asset accounts are made for such differences that are permanent in nature.

Additionally, U.S. GAAP requires certain components of net assets relating to permanent differences be reclassified between financial and tax reporting. Permanent differences between book and tax basis are attributable to partnerships and passive foreign investment companies adjustments. These reclassifications have no effect on Members’ Equity or Members’ Equity per Share. For the tax year ended March 31, 2019, the following amounts were reclassified:

| 11 |

| INFINITY LONG/SHORT EQUITY FUND, LLC |

| (a Delaware Limited Liability Company) |

| Notes to Financial Statements – March 31, 2019 (continued) |

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

d. Income Tax Information & Distributions to Members (continued)

| Members’ Equity paid-in | $ | (182,027 | ) | |

| Total distributable earnings | 182,027 |

At March 31, 2019, the federal tax cost of investment securities and unrealized appreciation (depreciation) as of the year-end were as follows:

| Gross unrealized appreciation | $ | 1,744,639 | ||

| Gross unrealized depreciation | (243,797 | ) | ||

| Net unrealized appreciation | $ | 1,500,842 | ||

| Cost of investments | $ | 16,500,985 |

The difference between cost amounts for financial statement and federal income tax purposes is due primarily to timing differences in recognizing certain gains and losses in security transactions.

As of March 31, 2019, the components of accumulated earnings on a tax basis were as follows:

| Undistributed ordinary income | $ | - | ||

| Undistributed long-term capital gains | - | |||

| Tax accumulated earnings | - | |||

| Accumulated capital and other losses | (82,728 | ) | ||

| Unrealized appreciation | 1,500,842 | |||

| Other differences | (195,269 | ) | ||

| Distributable net earnings | $ | 1,222,845 |

At March 31, 2019, the Fund had $82,728 of accumulated capital loss carryforward which consisted of $82,728 short-term and $0 long-term. To the extent that a fund may realize future net capital gains, those gains will be offset by any of its unused capital loss carryforward. Future capital loss carryover utilization in any given year may be subject to Internal Revenue Code limitations.

The tax character of distributions paid during the tax year ended March 31, 2019 and 2018 was as follows:

| Distributions paid from: | 2019 | 2018 | ||||||

| Ordinary income | $ | 66,637 | $ | 16,970 | ||||

| Net long-term capital gains | 131,692 | - | ||||||

| Total taxable distributions | 198,329 | 16,970 | ||||||

| Total distributions paid | $ | 198,329 | $ | 16,970 | ||||

For Federal income tax purposes, the Fund designated long-term capital gain dividends of $131,692 for the year ended March 31, 2019.

e. Cash

Cash, if any, includes amounts held in interest bearing money market accounts. Such deposits, at times, may exceed federally insured limits. The Fund has not experienced any losses in such accounts and does not believe it is exposed to any significant credit risk on such accounts.

f. Use of Estimates

The preparation of financial statements in conformity with U.S. GAAP requires the Fund’s management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of increases and decreases in Members’ Equity from operations during the reporting period. Actual results could differ from those estimates.

| 12 |

| INFINITY LONG/SHORT EQUITY FUND, LLC |

| (a Delaware Limited Liability Company) |

| Notes to Financial Statements – March 31, 2019 (continued) |

3. INVESTMENT MANAGEMENT AND OTHER AGREEMENTS

The Fund pays the Adviser a management fee (“Investment Management Fee”) at an annual rate of 1.25%, payable monthly in arrears, based upon the Fund’s Members’ Equity as of month-end. The Investment Management Fee is paid to the Adviser before giving effect to any repurchase of Shares in the Fund effective as of that date, and will decrease the net profits or increase the net losses of the Fund that are credited to its Members.

The Adviser has entered into an expense limitation and reimbursement agreement (the “Expense Limitation and Reimbursement Agreement”) with the Fund, whereby the Adviser has agreed to waive fees that it would otherwise have been paid, and/or to assume expenses of the Fund (a “Waiver”), if required to ensure the Total Annual Expenses (excluding taxes, interest, brokerage commissions, certain transaction-related expenses, commitment or non-use fees related to the Fund’s line of credit, extraordinary expenses, and any Acquired Fund Fees and Expenses) do not exceed 1.50% on an annualized basis (the “Expense Limit”).

For a period not to exceed three years from the date on which a Waiver is made, the Adviser may recoup amounts waived or assumed, provided they are able to effect such recoupment and remain in compliance with the Expense Limit. The Expense Limitation Agreement is in effect until December 31, 2019, and will automatically renew for consecutive one-year terms thereafter. Neither the Fund nor the Adviser may terminate the Expense Limitation Agreement during its current term. For the year ended March 31, 2019, the Adviser waived fees and reimbursed expenses of $244,204. At March 31, 2019, $187,082 is subject for recoupment through March 31, 2021, $244,204 is subject for recoupment through March 31, 2022.

Foreside Fund Services, LLC acts as distributor to the Fund.

For the fiscal year ended March 31, 2019, the Fund’s allocated fees incurred for the Fund’s Managers are reported on the Statement of Operations.

Vigilant Compliance Services, LLC provides CCO services to the Fund. The Fund’s allocated fees incurred for CCO services for the year ended March 31, 2019 were $10,650.

| 4. | RELATED PARTY TRANSACTIONS |

At March 31, 2019, Members who are affiliated with the Adviser owned approximately $2,380,771 (or approximately 13% of Members’ Equity) of the Fund.

| 5. | ADMINISTRATION AND CUSTODY AGREEMENT |

UMB Fund Services, Inc. serves as administrator (the “Administrator”) to the Fund and provides certain accounting, administrative, record keeping and investor related services. The Fund pays a monthly fee to the Administrator based upon average Members’ Equity, subject to certain minimums. UMB Bank, N.A. (the “Custodian”), an affiliate of the Administrator, serves as the primary custodian of the assets of the Fund, and may maintain custody of such assets with U.S. and non-U.S. sub-custodians, securities depositories and clearing agencies.

| 6. | INVESTMENT TRANSACTIONS |

For the year ended March 31, 2019, the purchase and sale of investments, excluding short-term investments and U.S. Government securities were $800,000 and $2,048,412, respectively.

| 13 |

| INFINITY LONG/SHORT EQUITY FUND, LLC |

| (a Delaware Limited Liability Company) |

| Notes to Financial Statements – March 31, 2019 (continued) |

| 7. | CAPITAL SHARE TRANSACTIONS |

Shares are generally offered for purchase as of the first day of each calendar month at the Fund’s then-current Members’ Equity per Share (determined as of the close of the preceding month), except that Shares may be offered more or less frequently as determined by the Board in its sole discretion. Transactions in Shares were as follows:

| Shares outstanding, March 31, 2017 | 6,986.022 | |||

| Shares issued | 11,013.537 | |||

| Shares reinvested | 15.779 | |||

| Shares redeemed | - | |||

| Shares outstanding, March 31, 2018 | 18,015.338 | |||

| Shares issued | 69.234 | |||

| Shares reinvested | 188.505 | |||

| Shares redeemed | (1,026.387 | ) | ||

| Shares outstanding, March 31, 2019 | 17,246.690 |

| 8. | REPURCHASE OF SHARES |

At the discretion of the Board and provided that it is in the best interests of the Fund and Members to do so, the Fund intends to provide a limited degree of liquidity to the Members by conducting repurchase offers generally quarterly with a Valuation Date (as defined below) on or about March 31, June 30, September 30 and December 31 of each year. In each repurchase offer, the Fund may offer to repurchase its Shares at their net asset value as determined as of approximately March 31, June 30, September 30 and December 31, of each year, as applicable. Each repurchase offer ordinarily will be limited to the repurchase of approximately 25% of the Shares outstanding, but if the value of Shares tendered for repurchase exceeds the value the Fund intended to repurchase, the Fund may determine to repurchase less than the full number of Shares tendered. In such event, Members will have their Shares repurchased on a pro rata basis, and tendering Members will not have all of their tendered Shares repurchased by the Fund. Members tendering Shares for repurchase will be asked to give written notice of their intent to do so by the date specified in the notice describing the terms of the applicable repurchase offer, which date will be approximately 95 days prior to the date of repurchase by the Fund.

| 9. | CREDIT FACILITY |

The Fund may enter into one or more credit agreements or other similar agreements negotiated on market terms (each, a “Borrowing Transaction”) with one or more banks or other financial institutions which may or may not be affiliated with the Adviser (each, a “Financial Institution”) as chosen by the Adviser and approved by the Board. The Fund may borrow under a credit facility for a number of reasons, including without limitation, to pay fees and expenses, to make annual income distributions and to satisfy certain repurchase offers in a timely manner to ensure liquidity for the investors. To facilitate such Borrowing Transactions, the Fund may pledge its assets to the Financial Institution.

| 10. | INDEMNIFICATION |

In the normal course of business, the Fund enters into contracts that provide general indemnifications. The Fund’s maximum exposure under these agreements is dependent on future claims that may be made against the Fund, and therefore cannot be established; however, the Fund expects the risk of loss from such claims to be remote.

| 11. | RISK FACTORS |

The Fund is subject to substantial risks — including market risks, strategy risks and Investment Fund manager risks. Investment Funds generally will not be registered as investment companies under the 1940 Act and, therefore, the Fund will not be entitled to the various protections afforded by the 1940 Act with respect to its investments in Investment Funds. While the Adviser will attempt to moderate any risks of securities activities of the Investment Fund managers, there can be no assurance that the Fund’s investment activities will be successful or that the Members will not suffer losses. The Adviser will not have any control over the Investment Fund managers, thus there can be no assurances that an Investment Fund manager will manage its Investment Funds in a manner consistent with the Fund’s investment objective.

| 14 |

| INFINITY LONG/SHORT EQUITY FUND, LLC |

| (a Delaware Limited Liability Company) |

| Notes to Financial Statements – March 31, 2019 (continued) |

| 12. | OTHER |

As of March 31, 2019, the Fund has a member that holds 76% of the outstanding shares of the Fund. A significant redemption by this member could affect the Fund’s liquidity and the future viability of the Fund.

| 13. | NEW ACCOUNTING PRONOUNCEMENT |

In August 2018, the Securities and Exchange Commission (the "SEC") adopted regulations that eliminated or amended disclosure requirements that were redundant or outdated in light of changes in SEC requirements, GAAP, International Financial Reporting Standards, or changes in technology or the business environment. These regulations were effective November 5, 2018, and the Fund is complying with them effective with these financial statements.

| 14. | SUBSEQUENT EVENTS |

Management has evaluated the impact of all subsequent events on the Fund through the date the financial statements were issued and has determined that there were no subsequent events to report.

| 15 |

| INFINITY LONG/SHORT EQUITY FUND, LLC |

| (a Delaware Limited Liability Company) |

| Fund Management – March 31, 2019 (unaudited) |

The identity of the members of the Board and the Fund’s officers and brief biographical information as of March 31, 2019 is set forth below. The Fund’s Statement of Additional Information includes additional information about the membership of the Board.

INDEPENDENT MANAGERS

| Name, Address and YEAR OF BIRTH |

Position(s) Held with the Fund |

Length of Time Served |

Principal Occupation(s) During Past 5 Years and |

NUMBER OF PORTFOLIOS

IN |

Other Directorships Held By MANAGERS |

|

David G. Lee Year of Birth: 1952

c/o UMB Fund Services, Inc. 235 W. Galena St. Milwaukee, WI 53212 |

Manager | Since Inception | President and Director, Client Opinions, Inc. (2003 - 2012); Chief Operating Officer, Brandywine Global Investment Management (1998-2002) | 6 | None |

|

Robert Seyferth Year of Birth: 1952

c/o UMB Fund Services, Inc. 235 W. Galena St. Milwaukee, WI 53212 |

Manager | Since Inception | Chief Procurement Officer/Senior Managing Director, Bear Stearns/JP Morgan Chase (1993-2009) | 6 | None |

|

Gary E. Shugrue Year of Birth: 1954

c/o UMB Fund Services, Inc. 235 W. Galena St. Milwaukee, WI 53212 |

Advisory Board Member | Since December 2018 | Managing Director, Veritable LP (2016-Present); Founder/ President, Ascendant Capital Partners, LP (2001 – 2015) | 6 | Trustee, Quaker Investment Trust (5 portfolios) (registered investment company); Scotia Institutional Funds (2006-2014) (3 portfolios) (registered investment company |

| 16 |

| INFINITY LONG/SHORT EQUITY FUND, LLC |

| (a Delaware Limited Liability Company) |

| Fund Management – March 31, 2019 (unaudited) (continued) |

INTERESTED MANAGERS AND OFFICERS

| Name, Address and YEAR OF BIRTH |

Position(s) Held with the Fund |

Length of Time Served |

Principal Occupation(s) During Past 5 Years |

NUMBER OF PORTFOLIOS IN FUND COMPLEX* OVERSEEN BY manager |

Other Director- ships Held By MANAGERS |

|

Anthony Fischer** Year of Birth: 1959 c/o UMB Fund Services, Inc. 235 W. Galena St. Milwaukee, WI 53212 |

Chairman and Manager | September 2017 | Executive Director – National Sales of UMB Bank for Institutional Banking and Asset Servicing (Until 2018); President of UMB Fund Services (2014 – 2018); Executive Vice President in charge of Business Development, UMB Fund Services (2013 – 2014); Senior Vice President in Business Development, UMB Fund Services (2008 – 2013). | 6 | None |

|

Jeffrey Vale Year of Birth: 1969

c/o UMB Fund Services, Inc. 235 W. Galena St. Milwaukee, WI 53212 |

President | Since Inception | Partner and Chief Investment Officer of Adviser (2002 – present); Senior Analyst, Long Bow Capital Management, LLC (2000 - 2002). | N/A | N/A |

|

Phillip Jarrell Year of Birth: 1970

c/o UMB Fund Services, Inc. 235 W. Galena St. Milwaukee, WI 53212 |

Treasurer | Since Inception | Partner and Head of Business Development (2010 – present); Vice President and Major Account Manager, Thomson Reuters (2002 – 2010). | N/A | N/A |

| 17 |

| INFINITY LONG/SHORT EQUITY FUND, LLC |

| (a Delaware Limited Liability Company) |

| Fund Management – March 31, 2019 (unaudited) (continued) |

| Name, Address and YEAR OF BIRTH |

Position(s) Held with the Fund |

Length of Time Served |

Principal Occupation(s) During Past 5 Years |

NUMBER

OF PORTFOLIOS IN FUND COMPLEX* OVERSEEN BY manager |

Other Director- ships Held By MANAGERS |

|

Perpetua Seidenberg Year of Birth: 1990 c/o UMB Fund Services, Inc. 235 W. Galena St. Milwaukee, WI 53212 |

Chief Compliance Officer |

Since June 5, 2018 |

Compliance Director, Vigilant Compliance, LLC (an investment management services company) (2014 – Present); Auditor, PricewaterhouseCoopers (2012 – 2014). | N/A | N/A |

|

Ann Maurer Year of Birth: 1972 c/o UMB Fund Services, Inc. 235 W. Galena St. Milwaukee, WI 53212 |

Secretary | Since September 5, 2018 | Senior Vice President, Client Services (2017 –Present); Vice President, Senior Client Service Manager (2013 – 2017), Assistant Vice President, Client Relations Manager (2002 – 2013); UMB Fund Services, Inc. | N/A | N/A |

* The fund complex consists of the Fund, Infinity Core Alternative Fund, The Relative Value Fund, Vivaldi Opportunities Fund, Variant Alternative Income Fund, and Cliffwater Corporate Lending Fund.

** Mr. Fischer is deemed an interested person of the Fund because of his prior affiliation with an affiliate of the Fund’s Administrator.

| 18 |

| INFINITY LONG/SHORT EQUITY FUND, LLC |

| (a Delaware Limited Liability Company) |

| Other Information – March 31, 2019 (unaudited) |

Proxy Voting

The Fund is required to file Form N-PX, with its complete proxy voting record for the twelve months ended June 30, no later than August 31. The Fund’s Form N-PX filing is available: (i) without charge, upon request, by calling the Fund at 1-877-775-7751 or (ii) by visiting the SEC’s website at www.sec.gov.

Availability of Quarterly Portfolio Schedules

The Fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Form N-Q is available, without charge and upon request, on the SEC’s website at www.sec.gov.

Dividend Reinvestment Program

Each Member whose Units are registered in its own name will automatically be a participant under the Fund’s dividend reinvestment program (the “DRIP”) and have all income dividends and/or capital gains distributions automatically reinvested in Units unless such Member, at any time, specifically elects to receive income dividends and/or capital gains distributions in cash. Distributions are taxable whether they are received in cash or reinvested in Fund Units.The Fund reserves the right to cap the aggregate amount of any income dividends and/or capital gain distributions that are made in cash (rather than being reinvested) at a total amount of not less than 20% of the total amount distributed to Members. In the event that Members submit elections in aggregate to receive more than the cap amount of such a distribution in cash, any such cap amount will be pro rated among those electing Members. For additional information about the DRIP, please contact UMB Fund Services at 1-(877)-775-7751.

| 19 |

| INFINITY LONG/SHORT EQUITY FUND, LLC |

| (a Delaware Limited Liability Company) |

| Other Information – March 31, 2019 (unaudited) (continued) |

Privacy Policy

|

FACTS |

WHAT DOES THE FUND DO WITH YOUR PERSONAL INFORMATION? | ||

| Why? | Financial companies choose how they share your personal information. Federal law gives consumers the right to limit some but not all sharing. Federal law also requires us to tell you how we collect, share, and protect your personal information. Please read this notice carefully to understand what we do. | ||

| What? |

The types of personal information we collect and share depend on the product or service you have with us. This information can include: · Social Security number · account balances · account transactions · transaction history · wire transfer instructions · checking account information Even when you are no longer our customer, we continue to share your information as described in this notice. | ||

| How? | All financial companies need to share customers' personal information to run their everyday business. In the section below, we list the reasons financial companies can share their customers' personal information; the reasons funds choose to share; and whether you can limit this sharing. | ||

| Reasons we can share your personal information | Does the Fund share? | Can you limit this sharing? | |

| For our everyday business purposes – such as to process your transactions, maintain your account(s), respond to court orders and legal investigations, or report to credit bureaus |

Yes | No | |

| For our marketing purposes – to offer our products and services to you |

No | We don’t share | |

| For joint marketing with other financial companies | No | We don’t share | |

| For our affiliates’ everyday business purposes – information about your transactions and experiences | Yes | No | |

| For our affiliates’ everyday business purposes – information about your creditworthiness | No | We don’t share | |

| For our affiliates to market to you | No | We don’t share | |

| For nonaffiliates to market to you | No | We don’t share | |

| Questions? | Call 1-877-775-7751. |

| 20 |

| INFINITY LONG/SHORT EQUITY FUND, LLC |

| (a Delaware Limited Liability Company) |

| Other Information – March 31, 2019 (unaudited) (continued) |

| What we do | |

| How does the Fund protect my personal information? |

To protect your personal information from unauthorized access and use, we use security measures that comply with federal law. These measures include computer safeguards and secured files and buildings.

|

| How does the Fund collect my personal information? |

We collect your personal information, for example, when you

▪ open an account ▪ provide account information ▪ give us your contact information ▪ make a wire transfer ▪ tell us where to send money

We also collect your information from others, such as credit bureaus, affiliates, or other companies.

|

| Why can’t I limit all sharing? |

Federal law gives you the right to limit only

▪ sharing for affiliates’ everyday business purposes – information about your creditworthiness ▪ sharing for affiliates from using your information to market to you ▪ sharing for nonaffiliates to market to you

State laws and individual companies may give you additional rights to limit sharing.

|

| Definitions | |

| Affiliates |

Companies related by common ownership or control. They can be financial and nonfinancial companies.

▪ Our affiliates include companies such as Infinity Capital Advisors, LLC and Infinity Core Alternative Fund. |

| Nonaffiliates |

Companies not related by common ownership or control. They can be financial and nonfinancial companies.

▪ The Fund doesn’t share with nonaffiliates so they can market to you.

|

| Joint marketing |

A formal agreement between nonaffiliated financial companies that together market financial products or services to you.

▪ The Fund doesn’t jointly market.

|

| 21 |

ITEM 2. CODE OF ETHICS.

(a) The registrant, as of the end of the period covered by this report, has adopted a code of ethics that applies to the registrant's principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions, regardless of whether these individuals are employed by the registrant or a third party.

(c) There have been no amendments, during the period covered by this report, to a provision of the code of ethics that applies to the registrant's principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions, regardless of whether these individuals are employed by the registrant or a third party, and that relates to any element of the code of ethics description.

(d) The registrant has not granted any waivers, during the period covered by this report, including an implicit waiver, from a provision of the code of ethics that applies to the registrant's principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions, regardless of whether these individuals are employed by the registrant or a third party, that relates to one or more of the items set forth in paragraph (b) of this item's instructions.

ITEM 3. AUDIT COMMITTEE FINANCIAL EXPERT.

As of the end of the period covered by the report, the registrant's board of managers has determined that Mr. David G. Lee and Mr. Robert Seyferth are qualified to serve as the audit committee financial experts serving on its audit committee and that they are "independent," as defined by Item 3 of Form N-CSR.

ITEM 4. PRINCIPAL ACCOUNTANT FEES AND SERVICES.

Audit Fees

———

(a) The aggregate fees billed for each of the last two fiscal years for professional services rendered by the principal accountant for the audit of the registrant's annual financial statements or services that are normally provided by the accountant in connection with statutory and regulatory filings or engagements for those fiscal years are $39,900 for 2018 and $40,300 for 2019.

Audit-Related Fees

——————

(b) The aggregate fees billed for each of the last two fiscal years for assurance and related services by the principal accountant that are reasonably related to the performance of the audit of the registrant's financial statements and are not reported under paragraph (a) of this Item are $0 for 2018 and $0 for 2019. The fees listed in item 4 (b) are related to out-of-pocket expenses in relation to the annual audit of the registrant.

Tax Fees

———

(c) The aggregate fees billed for each of the last two fiscal years for professional services rendered by the principal accountant for tax compliance, tax advice, and tax planning are $6,000 for 2018 and $7,350 for 2019.

All Other Fees

—————

(d) The aggregate fees billed for each of the last two fiscal years for products and services provided by the principal accountant, other than the services reported in paragraphs (a) through (c) of this Item are $0 for 2018 and $0 for 2019.

(e)(1) Disclose the audit committee's pre-approval policies and procedures described in paragraph (c)(7) of Rule 2-01 of Regulation S-X.

The Registrant's Audit Committee must pre-approve the audit and non-audit services of the Auditors prior to the Auditor's engagement.

(e)(2) The percentage of services described in each of paragraphs (b) through (d) of this Item that were approved by the audit committee pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X are as follows:

(b) 0%

(c) 0%

(d) 0%

(f) The percentage of hours expended on the principal accountant's engagement to audit the registrant's financial statements for the most recent fiscal year that were attributed to work performed by persons other than the principal accountant's full-time, permanent employees was less than fifty percent.

(g) The aggregate non-audit fees billed by the registrant's accountant for services rendered to the registrant, and rendered to the registrant's investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by, or under common control with the adviser that provides ongoing services to the registrant for each of the last two fiscal years of the registrant 6was $0 for 2018 and $0 for 2019.

(h) The registrant's audit committee of the board of managers has considered whether the provision of non-audit services that were rendered to the registrant's investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant that were not pre-approved pursuant to paragraph (c)(7)(ii) of Rule 2-01 of Regulation S-X is compatible with maintaining the principal accountant's independence.

ITEM 5. AUDIT COMMITTEE OF LISTED REGISTRANTS.

Not applicable.

ITEM 6. SCHEDULE OF INVESTMENTS.

Schedule of Investments in securities of unaffiliated issuers as of the close of the reporting period is included as part of the report to members filed under Item 1 of this form.

ITEM 7. DISCLOSURE OF PROXY VOTING POLICIES AND PROCEDURES FOR CLOSED-END MANAGEMENT INVESTMENT COMPANIES.

PROXY VOTING POLICIES AND PROCEDURES

The Fund invests substantially all of its investable assets in Investment Funds. While it is unlikely that the Fund will receive notices or proxies from Investment Funds (or receives proxy statements or similar notices in connection with any other portfolio securities), to the extent that the Fund does receive such notices or proxies and the Fund has voting interests in such Investment Funds, the Board has delegated responsibility for decisions regarding proxy voting for securities held by the Fund to the Adviser. The Adviser will vote such proxies in accordance with its proxy policies and procedures.

The Adviser’s proxy policies and procedures require that the Adviser vote proxies received in a manner reasonably believed to be in the best interests of the Fund and its Members and not affected by any material conflict of interest. The Adviser considers Members’ best economic interests over the long term (i.e. addresses the common interest of all Members over time). Although Members may have differing political or social interests or values, their economic interest is generally uniform.

The Adviser has adopted proxy voting guidelines to assist in making voting decisions on common issues. The guidelines are designed to address those securities in which the Fund generally invests and may be revised in the Adviser’s discretion. Any non-routine matters not addressed by the proxy voting guidelines are addressed on a case-by-case basis, taking into account all relevant facts and circumstances at the time of the vote, particularly where such matters have a potential for major economic impact on the issuer’s structure or operations. In making voting determinations, the Adviser may conduct research internally and/or use the resources of an independent research consultant. The Adviser may also consider other materials such as studies of corporate governance and/or analyses of Member and management proposals by a certain sector of companies and may engage in dialogue with an issuer’s management.

The Adviser acknowledges its responsibility to identify material conflicts of interest related to voting proxies. The Adviser’s employees are required to disclose to the chief compliance officer any personal conflicts, such as officer or director positions held by them, their spouses or close relatives, in any publicly traded company. Conflicts based on business relationships with the Adviser or any affiliate will be considered only to the extent that the Adviser has actual knowledge of such relationships. The Adviser then takes appropriate steps to address identified conflicts.

In some cases, the cost of voting a proxy may outweigh the expected benefits. For example, casting a vote on a foreign security may involve additional costs such as hiring a translator or traveling to the foreign country to vote the security in person. The Adviser may abstain from voting a proxy if the effect on Members’ economic interests or the value of the portfolio holding is indeterminable or insignificant.

In certain cases, securities on loan as part of a securities lending program may not be voted. Nothing in the proxy voting policies shall obligate the Adviser to exercise voting rights with respect to a portfolio security if it is prohibited by the terms of the security or by applicable law or otherwise.

The Adviser will not discuss with members of the public how they intend to vote on any particular proxy proposal.

The Fund will be required to file Form N-PX, with its complete proxy voting record for the twelve months ended June 30, no later than August 31 of each year. The Fund’s Form N-PX filing will be available: (i) without charge, upon request, by calling the Fund at 1-877-775-7751 or (ii) by visiting the SEC’s website at www.sec.gov.

ITEM 8. PORTFOLIO MANAGERS OF CLOSED-END MANAGEMENT INVESTMENT COMPANIES.

(a)(1) Identification of Portfolio Manager(s) or Management Team Members and Description of Role of Portfolio Manager(s) or Management Team Members

The following table provides biographical information about the members of Infinity Capital Advisors, LLC (the "Adviser"), who are primarily responsible for the day-to-day portfolio management of the Infinity Long/Short Equity Fund, LLC as of June 6, 2019:

| Name of Portfolio Management Team Member |

Title | Length of Time of Service to the Fund |

Business Experience During the Past 5 Years |

Role of Portfolio Management Team Member |

| Jeffrey J. Vale | Partner & Chief Investment Officer | Since Inception | Partner and Chief Investment Officer, Infinity Capital Partners, LLC (2002-present). | Portfolio Management |

| Milton L. Williams, III | Partner & Chief Operating Officer | Since Inception | Partner and Chief Operating Officer, Infinity Capital Partners, LLC (2002-present). | Portfolio Management |

| R. Phillip Jarrell, Jr. | Partner & Head of Business Development | Since Inception | Partner and Head of Business Development, Infinity Capital Partners, LLC (2010-present); Major Account Manager, Thomson Reuters Corp. (2002-2010). | Portfolio Management |

| Steven P. Barth | Partner & Portfolio Manager | Since Inception | Partner and Portfolio Manager, Infinity Capital Partners, LLC (2013-present); Partner, President and Chief Investment Officer, BT Wealth Management (2008-2013). | Portfolio Management |

(a)(2) Other Accounts Managed by Portfolio Manager(s) or Management Team Member and Potential Conflicts of Interest

The following table provides information about portfolios and accounts, other than the Infinity Long/Short Equity Fund, LLC, for which the members of the Investment Committee of the Adviser are primarily responsible for the day-to-day portfolio management as of March 31, 2019:

| Number of Accounts and Total Value of Assets for Which Advisory Fee is Performance-Based: |

Number of Other Accounts Managed and Total Value of Assets by Account Type for Which There is No Performance-Based Fee: | |||||

| Registered investment companies |

Other pooled investment vehicles |

Other accounts |

Registered investment companies |

Other pooled investment vehicles |

Other accounts | |

| Jeffrey J. Vale | Zero accounts | Seven pooled investment vehicles with $338 million |

Zero accounts

|

Zero accounts | Twelve pooled vehicle with $223 million | Zero accounts |

|

Milton L. Williams, III |

Zero accounts | Zero pooled investment vehicles. |

Zero accounts |

Zero accounts | Zero accounts | Zero accounts |

|

R. Phillip Jarrell, Jr. |

Zero accounts | Zero pooled investment vehicles. |

Zero accounts |

Zero accounts | Zero accounts | Zero accounts |

|

Steven P. Barth |

Zero accounts | Seven pooled investment vehicles with $338 million |

Zero accounts |

Zero accounts | Twelve pooled vehicle with $223 million | Zero accounts |

Conflicts of Interest

Actual or apparent conflicts of interest may arise when a portfolio manager has day-to-day management responsibilities with respect to more than one fund or other account. More specifically, portfolio managers who manage multiple funds and/or other accounts may be presented with one or more of the following potential conflicts:

The management of multiple funds and/or other accounts may result in a portfolio manager devoting unequal time and attention to the management of each fund and/or other account. The Adviser seeks to manage such competing interests for the time and attention of a portfolio manager by having the portfolio manager focus on a particular investment discipline. Most other accounts managed by a portfolio manager are managed using the same investment models that are used in connection with the management of the Fund.

If a portfolio manager identifies a limited investment opportunity which may be suitable for more than one fund or other account, a fund may not be able to take full advantage of that opportunity due to an allocation of filled purchase or sale orders across all eligible funds and other accounts. To deal with these situations, the Adviser has adopted procedures for allocating portfolio transactions across multiple accounts.

The Adviser has adopted certain compliance procedures which are designed to address these types of conflicts. However, there is no guarantee that such procedures will detect each and every situation in which a conflict arises.

Compensation of the Investment Committee

The members of the Investment Committee are not directly compensated for their work with respect to the Fund; however, each member of the Investment Committee is an equity owner of the parent company of the Sub-Adviser and therefore benefits indirectly from the revenue generated from the Sub-Advisory Agreement.

Portfolio Management Team’s Ownership of Shares

| Name of Portfolio Management Team Member: |

Dollar Range of Shares Beneficially Owned by Portfolio Management Team Member: |

| Jeffrey J. Vale | $100,001-$500,000 |

| Milton L. Williams, III | $100,001-$500,000 |

| R. Phillip Jarrell, Jr. | $100,001-$500,000 |

| Steven P. Barth | $100,001-$500,000 |

(b) Not Applicable

ITEM 9. PURCHASES OF EQUITY SECURITIES BY CLOSED-END MANAGEMENT INVESTMENT COMPANY AND AFFILIATED PURCHASERS.

Not applicable.

ITEM 10. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS.

There have been no material changes to the procedures by which the members may recommend nominees to the registrant's board of managers, where those changes were implemented after the registrant last provided disclosure in response to the requirements of Item 407(c)(2)(iv) of Regulation S-K (17CFR 229.407), or this Item.

ITEM 11. CONTROLS AND PROCEDURES.

(a) The registrant's principal executive and principal financial officers, or persons performing similar functions, have concluded that the registrant's disclosure controls and procedures (as defined in Rule 30a-3(c) under the Investment Company Act of 1940, as amended (the "1940 Act") (17 CFR 270.30a-3(c))) are effective, as of a date within 90 days of the filing date of the report that includes the disclosure required by this paragraph, based on their evaluation of these controls and procedures required by Rule 30a-3(b) under the 1940 Act (17 CFR 270.30a-3(b)) and Rules 13a-15(b) or 15d-15(b) under the Securities Exchange Act of 1934, as amended (17 CFR 240.13a-15(b) or 240.15d-15(b)).

(b) There were no changes in the registrant's internal control over financial reporting (as defined in Rule 30a-3(d) under the 1940 Act (17 CFR 270.30a-3(d)) that occurred during the registrant's second fiscal quarter of the period covered by this report that has materially affected, or is reasonably likely to materially affect, the registrant's internal control over financial reporting.

ITEM 12. DISCLOSURE OF SECURITIES LENDING ACTIVITIES FOR CLOSED-END MANAGEMENT INVESTMENT COMPANIES.

Not applicable

ITEM 13. EXHIBITS.

(a)(1) Code of ethics or any amendments thereto, that is subject to disclosure required by item 2 is attached hereto.

(a)(2) Certifications pursuant to Rule 30a-2(a) under the 1940 Act and Section 302 of the Sarbanes-Oxley Act of 2002 are attached hereto.

(a)(3) Not applicable.

(a)(4) Not applicable.

(b) Certifications pursuant to Rule 30a-2(b) under the 1940 Act and Section 906 of the Sarbanes-Oxley Act of 2002 are attached hereto.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| (registrant) | Infinity Long/Short Equity Fund, LLC | |

| By (Signature and Title)* | /s/ Jeff Vale | |

| Jeff Vale, President | ||

| (Principal Executive Officer) | ||

| Date | June 6, 2019 |

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

| By (Signature and Title)* | /s/ Jeff Vale | |

| Jeff Vale, President | ||

| (Principal Executive Officer) | ||

| Date | June 7, 2019 | |

| By (Signature and Title)* | /s/ Phillip Jarrell | |

| Phillip Jarrell, Treasurer | ||

| (Principal Financial Officer) | ||

| Date | June 6, 2019 |

* Print the name and title of each signing officer under his or her signature.