As filed with the Securities and Exchange Commission on August 29, 2022

No. 333-

UNITED STATES SECURITIES AND EXCHANGE COMMISSION | ||

| Washington, D.C. 20549 | ||

FORM

S-3 | ||

| Ramaco

Resources, Inc. (Exact name of registrant as specified in its certificate of incorporation) | ||

Delaware (State or other jurisdiction of incorporation or organization) |

38-4018838 (I.R.S. Employer Identification No.) | |

250 West Main Street, Suite 1800 Lexington, Kentucky 40507 (859) 244-7455 (Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Randall W. Atkins Chairman and Chief Executive Officer 250 West Main Street, Suite 1800 Lexington, Kentucky 40507 (859) 244-7455 | ||

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies of all communications, including communications sent to agent for service, should be sent to: | ||

Matthew R. Pacey, P.C. Kirkland & Ellis LLP 609 Main Street Houston, TX 77002 (713) 836-3334 | ||

Approximate date of commencement of proposed sale to the public: From time to time after the effective date of the Registration Statement as determined by market conditions. | ||

| If the only securities being registered on this Form are being offered pursuant to dividend or interest reinvestment plans, please check the following box. ¨ |

| If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, other than securities offered only in connection with dividend or interest reinvestment plans, check the following box. ¨ |

| If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨ |

| If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨ |

| If this Form is a registration statement pursuant to General Instruction I.D. or a post-effective amendment thereto that shall become effective upon filing with the Commission pursuant to Rule 462(e) under the Securities Act, check the following box. ¨ |

| If this Form is a post-effective amendment to a registration statement filed pursuant to General Instruction I.D. filed to register additional securities or additional classes of securities pursuant to Rule 413(b) under the Securities Act, check the following box. ¨ |

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. |

| Large accelerated filer | ¨ | Accelerated filer | x |

| Non-accelerated filer | ¨ | Smaller reporting company | x |

| Emerging growth company | x | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. x

| |||

| The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine. | |||

The information in this preliminary prospectus is not complete and may be changed. We may not distribute these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction where an offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | Subject to completion, dated August 29, 2022 |

Ramaco Resources, Inc.

shares of

Class B Common Stock

This prospectus is being furnished in connection with the distribution by Ramaco Resources, Inc. (the “Company”) to holders of existing common stock, par value $0.01 (the “existing common stock”), of shares of Class B common stock, par value $0.01 per share (the “Class B common stock”). Concurrent with the Distribution (as defined below) the existing common stock will be reclassified as shares of Class A common stock, par value $0.01 per share (the “Class A common stock”), pursuant to our Second Amended and Restated Certificate of Incorporation approved by our stockholders on , 2022 (the “Amended Charter”). The Class B common stock would be a newly authorized and issued series of common stock of the Company that we anticipate will pay a dividend based on the separate economic performance of the business, assets and liabilities to be attributed to Ramaco Coal, LLC. We refer to the businesses associated with these assets, collectively as “CORE,” which is an abbreviation for “Carbon Ore-Rare Earth.” Holders of Class B common stock are common stockholders of the Company and will not have any legal rights related to the CORE Assets (as defined herein). Please see “Risk Factors–Holders of Class B common stock are common stockholders of the Company and, therefore, are subject to risks associated with an investment in the Company as a whole, even if a holder does not own shares of Class A common stock.” We refer to the Class B common stock as the “securities” in this prospectus and the Class A common stock and Class B common stock collectively as the “common stock” in this prospectus.

Shares of our Class B common stock will be distributed to holders of existing common stock of record as of the close of business, New York City time, on , 2022, which will be the record date. Each such holder will receive 0.2 shares of Class B common stock for every one share of existing common stock held on the record date (with cash in lieu of any fractional share interests). We refer to this distribution of securities as the “Distribution.” The Distribution is subject to the tracking stock proposal (as defined herein), which will be effective at New York City time, on , 2022. For Company stockholders who own existing common stock in registered form, in most cases the transfer and distribution agent will credit their shares of Class B common stock to their book entry accounts. Our transfer and distribution agent will send these stockholders a statement reflecting their Class B common stock ownership shortly after , 2022. For stockholders who own existing common stock through a broker or other nominee, their shares of Class B common stock will be credited to their accounts by the broker or other nominee.

Company stockholders will not be required to pay for shares of our Class B common stock received in the Distribution, or to surrender or exchange shares of existing common stock in order to receive our Class B common stock, or to take any other action in connection with the Distribution.

Our existing common stock is listed on the NASDAQ Global Select Market (“NASDAQ”) under the symbol “METC.” We intend to apply to list our Class B common stock on the NASDAQ under the symbol “METCB.”

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 and have elected to comply with certain reduced public company reporting requirements.

Investing in the securities involves risks that are described in the “Risk Factors” section beginning on page 19 of this prospectus and in the documents incorporated by reference herein.

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2022.

TABLE OF CONTENTS

Page

i

Under this prospectus, we are registering shares of our Class B common stock to be distributed to holders of our existing common stock. You should rely only on the information provided or incorporated by reference in this prospectus or any applicable prospectus supplement. We are not making an offer to sell these securities in any jurisdiction where the offer or sale of these securities is not permitted. You should not assume that the information appearing in this prospectus or any applicable prospectus supplement or the documents incorporated by reference herein or therein is accurate as of any date other than their respective dates. Our business, financial condition, results of operations and prospects may have changed since those dates. You should carefully read the entirety of this prospectus and any applicable prospectus supplement, as well as the documents incorporated by reference in this prospectus and any applicable prospectus supplement, before making an investment decision. You should also read and consider the information in the documents we have referred you to in the sections of this prospectus entitled “Incorporation of Certain Information by Reference” and “Where You Can Find Additional Information.”

In this prospectus, unless otherwise specified or the context requires otherwise, we use the terms “Ramaco Resources,” “Company,” “we,” “us” and “our” to refer to Ramaco Resources, Inc. and its consolidated subsidiaries.

1

This summary highlights selected information appearing elsewhere in, or incorporated by reference into, this prospectus. This summary is not complete and does not contain all of the information that you should consider before investing in our common stock. You should carefully read the entire prospectus and information incorporated by reference in this prospectus, including the section entitled “Risk Factors” on page 19 of this prospectus, our Annual Report on Form 10-K for the year ended December 31, 2021, and the financial data and related notes and the other documents that we incorporate by reference into this prospectus.

About Ramaco Resources, Inc.

Ramaco Resources, Inc. is a Delaware corporation formed in October 2016. Our existing common stock is listed on the NASDAQ under the symbol “METC.” Our 9.00% Senior Notes due 2026 are listed on the NASDAQ under the symbol “METCL.”

We are an operator and developer focused on high-quality, low-cost metallurgical coal in southern West Virginia, southwestern Virginia, and southwestern Pennsylvania. Historically, we have been a pure play metallurgical coal company with 39 million reserve tons and 769 million resource tons of high-quality metallurgical coal. We believe our advantaged reserve geology provides us with higher productivities and industry leading lower cash costs.

In April 2022, we acquired 100% of the equity interests of Ramaco Coal, LLC (“Ramaco Coal”), an entity owned by an investment fund managed by Yorktown Partners, LLC and certain members of the Company’s management, through the Company’s subsidiary, Ramaco Development, LLC (the “Acquisition”). Ramaco Coal’s current income producing assets primarily consist of land holding and coal royalty producing subsidiaries, including fee ownership of approximately 42 million tons of metallurgical coal. The vast majority of Ramaco Coal’s metallurgical coal is currently leased to the Company. Merging the Ramaco Coal land and royalty interests into the Company will have a positive and immediately accretive financial impact on the Company’s Central Appalachian coal mining operations.

The Acquisition will allow the Company to avoid ongoing minimum royalty and production royalty expense for the entire life of production from the acquired reserves. It will provide significant near and long-term financial benefit, ensuring that the Company remains among the lowest cost producers of metallurgical coal in the U.S. for the foreseeable future.

Description of the Class B Common Stock

The Class B common stock is being issued to provide holders of existing common stock direct participation in the financial performance of the CORE Assets on a standalone basis separate from our coal mining operations, which are primarily metallurgical coal. The Class B common stock is expected to pay a dividend based on the financial performance of the CORE Assets. Subject to the discretion of our Board and the requirements of Delaware law, we expect to pay an initial cash dividend of $2.84 million per quarter ($11.4 million annualized) on the Class B common stock for the balance of 2022 and $4.83 million per quarter ($19.3 million annualized) in 2023 based on the anticipated dividend of 20% of the revenue attributable to the CORE Assets. We will adjust the amount of our Class B common stock dividend for the period from the closing of the Distribution through December 31, 2022, based on the actual length of the period. See “Cash Dividend Policy and Restrictions on Dividends.” The CORE assets include (collectively, the “CORE Assets”):

| · | Coal Royalties: Royalty interests in 38 million tons of coal reserves and 473 million in-place coal resource tons owned in fee or under long-term lease, as well as an estimated 43 million tons of coal from our recently acquired Amonate assets (the “Amonate Assets”). CORE’s coal royalties are currently generating royalty income from properties mined by Ramaco Resources (and third parties), including our Elk Creek mining complex (the “Elk Creek Complex”), our Berwind mining complex (the “Berwind Complex”) and minimum royalty payments on our currently non-producing RAM Mine, each as described below. |

2

| · | Coal Infrastructure Revenue: A non-cost bearing fee of $10 per ton on volumes attributable to coal preparation and $5 per ton attributable to rail-car loading facilities at the Elk Creek Complex, the Berwind Complex and our Knox Creek property (the “Knox Creek Complex”), which serve Ramaco Resources and other producers. Based on this fixed fee arrangement, revenue will increase or decrease depending on production volumes. |

| · | Ramaco Carbon: A vertically integrated platform of resource, research and future manufacturing assets consisting of (i) the non-producing, but permitted portion of the Brook Mine property located near Sheridan, Wyoming in the Powder River Basin of Wyoming containing an estimated 162 million tons of coal (“Carbon Ore”) and where rare earth elements (“REEs”) have been discovered, (ii) 53 patents and pending patents relating to the conversion of low-cost Carbon Ore at the Brook Mine property into higher value carbon products, which initial products consist of porous carbon (“PC”), graphene and carbon fibers developed in conjunction with partners such as the National Energy Technology Laboratory (“NETL”), the Oak Ridge National Laboratory (“ORNL”) and others, (iii) an 11,000 square foot carbon research and development facility (the “iCAM,” or the “Carbon Advanced Material Innovation Center”), which has facilities for conducting ongoing research on coal-to-advanced carbon products and materials manufacturing processes and (iv) a 120-acre industrial park (the “iPark”) where it is anticipated that future coal-to-advanced-carbon products and materials manufacturing will be conducted using Carbon Ore sourced from the adjacent Brook Mine property. |

| · | Rare Earth Elements: REEs, a critical input in numerous high-tech applications, including electric vehicle (“EV”) batteries, have been discovered in high concentrations in the Brook Mine coal seams and surrounding strata. Further core testing is underway to determine the areal extent of the quality and quantity of the REE exploration target and the commercial potential of the CORE deposit. |

CORE is not a separate legal entity and holders of our Class B common stock will not own a direct interest in the CORE Assets. Holders of the Class B common stock will be stockholders of Ramaco Resources and will be subject to all of the risks and liabilities of the Company as a whole. The Class B common stock will vote with the Class A common stock as a single class on all matters on which the Class A common stock is entitled to vote and will not have any specific voting rights or governance rights with respect to CORE. Subject to the requirements of Delaware law, all dividends will be reviewed quarterly and declared by our board of directors (our “Board”) at its discretion. It is anticipated that initially 20% of the revenue attributable to the CORE Assets will be paid as a dividend through December 31, 2023, with the percentage subject to change by our Board. Subject to the discretion of our Board and the requirements of Delaware law, we expect to pay an initial cash dividend of $2.84 million per quarter ($11.4 million annualized) on the Class B common stock for the balance of 2022 and $4.83 million per quarter ($19.3 million annualized) in 2023 based on the anticipated dividend of 20% of the revenue attributable to the CORE Assets. We will adjust the amount of our Class B common stock dividend for the period from the closing of the Distribution through December 31, 2022, based on the actual length of the period. See “Cash Dividend Policy and Restrictions on Dividends” and “Risk Factors–Risks Related to our Proposed Tracking Stock Structure.”

In the Distribution, shares of our Class B common stock will be issued to holders of record as of the close of business, New York City time, on , 2022, which will be the record date. Each holder will receive 0.2 shares of Class B common stock for every one share of existing common stock held on the record date (with cash in lieu of any fractional share interests). The Distribution should not be taxable to holders of our existing common stock, except with respect to the receipt of cash in lieu of fractional shares.

The following table illustrates the amount of cash attributable to the CORE Assets and the resulting cash available for dividends that we estimate that we will generate for the years ending December 31, 2022 and 2023, and the aggregate annual dividend we expect to pay to holders of our Class B common stock. We will adjust the amount of our Class B common stock dividend for the period from the closing of the Distribution through December 31, 2022, based on the actual length of the period. All of the amounts for the years ending December 31, 2022 and 2023 in the table below are estimates. See “Cash Dividend Policy and Restrictions on Dividends” for more information.

3

| Pro Forma Cash Available For Dividend For Year Ending December 31, | ||||||||

| (in thousands, except per share data) | 2022 | 2023 | ||||||

| (unaudited) | ||||||||

| Royalty Revenue | ||||||||

| Ramaco Coal | $ | 13,405 | $ | 25,781 | ||||

| Amonate Assets | 2,385 | 5,983 | ||||||

| Other | 60 | 180 | ||||||

| Total Royalty Revenue | $ | 15,850 | $ | 31,943 | ||||

| Infrastructure Revenue | ||||||||

| Preparation Plants (Processing) | $ | 27,259 | $ | 43,029 | ||||

| Rail Load-outs | 13,758 | 21,601 | ||||||

| Total Infrastructure Revenue | $ | 41,016 | $ | 64,631 | ||||

| Pro Forma Revenue | $ | 56,867 | $ | 96,574 | ||||

| Cash Available | $ | 56,867 | $ | 96,574 | ||||

| 20% Cash Available for Dividend | $ | 11,373 | $ | 19,315 | ||||

| Dividend Per Share of Class B Common Stock(1) | $ | 1.25 | $ | 2.12 | ||||

(1) Assumes 9,100,516 shares of Class B common stock.

Pro Forma Expected Annualized Dividends

| Year Ending December 31, | ||||||||

| (in millions) | 2022 | 2023 | ||||||

| Class A common stock(1) | $ | 20.0 | $ | 20.0 | ||||

| Class B common stock(2) | 11.4 | 19.3 | ||||||

| Total Dividends | $ | 31.4 | $ | 39.3 | ||||

(1) Assumes dividends for the Class A common stock are held constant in 2023. All dividend payments are subject to Board discretion.

(2) Dividends for the Class B common stock for the year ending December 31, 2022 are expected to be $2.84 million per quarter and will be paid in the quarter following the issuance of the Class B common stock. We will adjust the amount of our dividend for the period from the closing of the Distribution through December 31, 2022, based on the actual length of the period. Dividends for the Class B common stock will not be paid for quarters prior to such issuance in 2022.

Reasons for Issuing the Class B Common Stock

We are issuing the Class B common stock because:

| 1. | We believe that CORE’s non-cost bearing royalty, infrastructure, carbon products and REE assets are forms of passive income that are fundamentally different than our coal mining operations, which may lead CORE to be valued based on the lower risk profile of the majority of such assets; |

| 2. | We believe that paying a separate dividend based on the financial performance of CORE in addition to the regular dividend on the Class A common stock can create additional value for holders of existing common stock; |

| 3. | Unlike other strategic alternatives to separate the CORE Assets, the Distribution should not be taxable to holders of our existing common stock (except with respect to the receipt of cash in lieu of fractional shares); and |

| 4. | The Class B common stock offers holders of existing common stock an opportunity to directly participate in the potential growth associated with the development of carbon products and REEs. |

Coal Royalties

CORE’s coal royalties primarily consist of coal properties owned in fee or under long-term leases that are leased or subleased to Ramaco Resources (approximately 95% of such leased properties) and various third parties. Such lessees pay a royalty based on the amount of coal mined and the realized price per ton. At present, CORE’s coal royalties do not include the Knox Creek Complex, which accounted for approximately 7% of Ramaco Resources’ production for the six months ended June 30, 2022.

CORE’s coal reserves are located in central and southern West Virginia, southwestern Virginia and southwestern Pennsylvania and present advantaged geologic characteristics such as relatively thick coal seams in the deep mines, a low effective mining ratio at the surface mines, and desirable metallurgical coal quality. As of December 31, 2021, the CORE Assets include approximately 38 million reserve tons and 473 million resource tons and an estimated 43 million tons of coal from the Amonate Assets, which excludes the Knox Creek Complex and other non-royalty producing properties. Because CORE leases properties to Ramaco Resources and third parties for development, CORE is able to benefit from production from our properties without investing capital or incurring operating expenses.

4

We anticipate that CORE’s coal royalties (which excludes production from the Knox Creek Complex) will be based on annual production of approximately 2.6 million tons of coal in 2022 and 4.0 million tons of coal in 2023. Based on existing commitments for 2022, we anticipate that CORE will receive royalty payments of approximately $16 million in 2022 and approximately $32 million in 2023 based on existing sale contracts and the current forward market prices for coal similar in quality to ours.

Going forward, we believe that we will be able to (i) take advantage of any future increases in U.S. and global benchmark coal prices, (ii) opportunistically increase the amount and prices of our projected production that is directed to both the domestic and the export markets, and (iii) capture favorable differentials between domestic and global benchmark prices. That is expected to, in turn, increase the amount of royalty revenue CORE receives from coal production at our properties. In the future, we may also choose to add certain additional coal reserves to CORE, increasing royalty income sources in the future.

Elk Creek Mining Complex

CORE’s Elk Creek Complex in southern West Virginia, our flagship complex, began production in late December 2016. The Elk Creek property consists of approximately 20,200 acres of controlled mineral and contains 16 coal bearing seams that we believe can be economically mined. Nearly all seams contain high-volatile coal accessible at or above drainage. Additionally, almost all of this coal is high-fluidity, which is an important quality for high-volatile coal. We currently market most of the coal produced from the Elk Creek Complex as a blended high-volatile A/B product. When segregated, a portion of the coal can be sold as a high-volatile A product for a premium. The market for Elk Creek production is principally North American coke and steel producers, but we also market coal to a geographically diverse group of international customers and occasionally to coal traders and brokers for use in filling orders for their blended products.

Ramaco Resources has leased from CORE enough reserves to mine the Elk Creek Complex for more than 20 years under its current mine plans. We estimate that the Elk Creek Complex contains approximately 29 million tons of coal reserves and 223 million tons of coal resources and expect the Elk Creek Complex to produce approximately 2.1 million tons of high volatile A/B coal in 2022 and 2.6 million tons in 2023. CORE currently has two lease arrangements with Ramaco Resources at the Elk Creek Complex, with initial terms of the leases of 10 years and secondary terms ranging from five to 10 years. Each lease continues to renew until the exhaustion of all mineable and merchantable coal. Our lease arrangements at the Elk Creek Complex currently require Ramaco Resources to pay royalties ranging from 0% to 10% of the realized price per ton of coal produced.

CORE also subleases certain controlled minerals at the Elk Creek Complex to third-party sublessees. This sublease is for an initial term of five years, one additional secondary term of five years (unless the sublessee gives notice of its intent not to renew) and evergreen extensions for additional one-year terms until exhaustion of all mineable and merchantable coal. The sublessee is required to pay both a minimum annual royalty per year and a per ton production royalty of approximately 10%.

In order to meet increased capacity anticipated from a throughput upgrade at the Elk Creek preparation plant (as described below), we began development work on additional low-cost, high-volatile underground and surface mines at the Elk Creek Complex, with production having begun during the second quarter of 2022 and with full levels of productivity expected by mid-2023. Additionally, as further described below, our Board has approved an upgrade at the Elk Creek preparation plant to take the plant’s annual capacity from roughly 2.1 million tons to roughly 3.0 million tons.

5

Berwind Mining Complex

CORE’s Berwind Complex is located on the border of southern West Virginia and southwest Virginia and is geographically well-positioned to fill the anticipated market for low-volatile coals. The Berwind Complex consists of approximately 47,200 acres of mineral, including the Amonate Assets described in more detail below.

Development of the Berwind Complex began in late-2017 in the Pocahontas No. 3 seam and has since sloped up to current mining in the thicker Pocahontas No. 4 seam. In 2020, we suspended development at the Berwind Complex due to lower pricing and demand largely caused by the economic effects of COVID-19. In early-2021, as pricing and demand improved, the Berwind Complex development resumed and Ramaco Resources successfully reached the Pocahontas No. 4 seam in late-2021.

During the ramping of production at the Berwind Complex, on July 10, 2022, Ramaco Resources experienced a material methane ignition at its Berwind mine, which is one of three active mines at the Berwind Complex. The other two mines have resumed production. Ramaco Resources, in conjunction with the appropriate state and federal regulatory authorities, will be conducting a full investigation into the incident. The mine was idle at the time of the incident, and there were no personnel in the mine nor any injuries or fatalities. At this time, Ramaco Resources is evaluating the extent of the damage. Production from the Berwind mine annualized to less than 0.3 million tons in the first half of 2022. Production at the Berwind mine is expected to be impacted for an indeterminant period of time. We assume that production will resume in the Berwind mine in January 2023 for our CORE projections.

At full production, including the Amonate Assets and the resumption of full production at the temporarily closed Berwind mine, we expect to produce approximately 1.1 million tons in 2023. We estimate that the Berwind Complex, excluding the Amonate Assets, contains approximately 9 million tons of coal reserves and 238 million tons in-place of coal resources with a mine life of over 20 years, and we estimate that the Amonate Assets contain an additional 43 million tons of coal.

CORE has leased its property interests at the Berwind Complex other than the Amonate Assets from a third-party lessor until August 2030. Thereafter, the lease extends for one-year periods until the reserves are exhausted. CORE currently has two subleases to Ramaco Resources at the Berwind Complex, each with an initial term of five years. The subleases renew in evergreen periods of five years each until exhaustion of all mineable and merchantable coal. Ramaco Resources is required to pay both minimum annual royalties and per ton production royalties under the subleases and an override royalty on the underground lease.

As referenced above, in December 2021, Ramaco Resources acquired what were called the Amonate Assets from Coronado Global Resources Inc., which now operate as part of the overall Berwind Complex, commencing production in March 2022. The acquisition primarily consisted of low and mid-volatile coal reserves and resources. It also included several additional permitted mines and an idled 1.3-million ton per annum capacity coal preparation plant with a rail loading facility, all of which is now being refurbished and is expected to begin operation in the third quarter of 2022.

The Amonate Assets are currently both owned in fee as well as leased from third-party owners. The coal preparation and rail load out facilities acquired with the Amonate Assets will serve the entire Berwind Complex and will generate revenue for CORE on a percentage of the realized sales price.

Production from the Berwind Complex will generate revenue for CORE based on an aggregate effective royalty of ranging from approximately 1.5% to 7% per ton fee for coal produced and loaded.

Knox Creek Complex

The Knox Creek coal reserves and resources are currently leased from third-party owners and will not be included in the CORE Assets initially. However, as discussed below, the Knox Creek Complex will produce CORE infrastructure revenue based on a fee of $10 per ton of coal processed and a fee of $5 per ton of loaded coal using the Knox Creek coal preparation facilities, which will serve the entire Knox Creek Complex.

6

The Knox Creek Complex consists of approximately 62,100 acres of controlled mineral, a 650 tons per hour preparation plant and a coal-loading facility with a refuse impoundment. Rail service is provided by Norfolk Southern.

In the fourth quarter of 2019, Ramaco Resources acquired multiple permits for mining at the Knox Creek Complex. These permits are in close proximity to our Knox Creek preparation plant and loadout infrastructure and provide immediate access to two separate mining areas in Southwestern Virginia. We have spent approximately $4.4 million of capital to develop a high-volatile A coal mine in the Jawbone seam. The mine has been developed up to the coal face and may be placed into production in the future. The second mining area is a surface mining operation known as the Big Creek mine in the Tiller seam that began production in August 2021 and is currently being mined via surface and highwall mining methods. We added a highwall miner at this mine in the fourth quarter of 2021 and anticipate full-year production of approximately 300,000 tons of primarily mid-volatile coal. We estimate that the Knox Creek Complex contains approximately 1.1 million tons of coal reserves and 296 million tons of coal resources and we expect Big Creek to continue production at these levels for approximately three years.

RAM Mine

CORE’s RAM Mine is located in southwestern Pennsylvania and consists of approximately 1,570 acres of controlled coal resources. Subject to the issuance of a final mining permit and satisfactory market conditions, the RAM Mine is expected to go into operation within 12 to 18 months of final permit issuance.

Production of high-volatile coal from the Pittsburgh seam at the RAM Mine is planned from a single continuous-miner room-and-pillar underground operation. The mine is in close proximity to Pittsburgh area coke plants and in particular the U.S. Steel Clairton plant, the largest coking facility in the United States. The Pittsburgh seam coal has historically been a key feedstock for these coke plants.

Operation of our RAM Mine may require access to a newly constructed preparation plant and loading facility, third-party processing or direct shipment of raw coal product. We currently expect that coal from the RAM Mine will be transported to our customers by highway trucks, rail cars or by barge on nearby river systems. Upon commencement of mining, we estimate that the mine will produce at an annualized rate of between 300,000 and 500,000 tons with an estimated 10 years of mining life. The Ram Mine contains an estimated 11 million tons of coal resources.

CORE currently has one lease arrangement with Ramaco Resources at our RAM Mine, with an initial term of 10 years expiring in August 2025, and with the right to extend for an additional term of 10 years unless Ramaco Resources elects not to renew, and thereafter automatic one-year renewals until exhaustion of all mineable and merchantable coal. Ramaco Resources is required to pay both minimum annual royalties and per ton production royalties of approximately 5% of realized sale price.

Infrastructure Assets Revenue

CORE’s coal infrastructure assets currently consist of coal preparation plants at each of the Elk Creek Complex, the Berwind Complex and the Knox Creek Complex, as well as rail-car loading facilities at the Elk Creek Complex, the Berwind Complex and the Knox Creek Complex. CORE’s infrastructure revenue will be calculated based on a fee of $10 per ton of coal processed and a fee of $5 per ton of loaded coal using the CORE Assets. CORE’s per ton processing and loading fees will be subject to redetermination at the discretion of our Board. CORE will not be allocated any capital or operating costs. Through the year ending December 31, 2021, we estimate that CORE would have recognized pro forma $32 million of infrastructure assets revenue from our Elk Creek, Berwind and Knox Creek preparation plants and rail load-outs. The infrastructure assets revenue associated with the existing CORE infrastructure assets is projected to be $41 million in full-year 2022 and $65 in 2023 based on projected throughput.

7

Elk Creek Facilities

Elk Creek Complex coal production is processed through a 700 raw-ton-per-hour preparation plant operated by Ramaco Resources. The plant has a large-diameter (48”) heavy-media cyclone, dual-stage spiral concentrators, froth flotation, horizontal vibratory and screen bowl centrifuges.

The rail load-out facilities at the Elk Creek Complex are capable of loading 4,000 tons per hour and a full 150-car unit train in under four hours. The load-out facility is served by the CSX railroad. There are no third parties utilizing our rail facilities.

In 2021, Ramaco Resources shipped 2.0 million tons of Company produced coal from the Elk Creek Complex, 95% of which was processed at the Elk Creek preparation plant and 97% of which was shipped out via rail loadout. At a fee of $10 per ton of processed coal and $5 per ton of loaded coal, this would have equated to $29 million of revenue in 2021. Through the year ending December 31, 2022, we estimate that CORE would have recognized pro forma $30 million of revenue from our preparation plant and rail load-out.

During 2022, we plan to begin work on a throughput upgrade at the Elk Creek preparation plant. This upgrade, which has been approved by our Board, is expected to raise the nameplate processing capacity to approximately 1,150 raw tons per hour and annual processing capacity from this complex to approximately 3.0 million tons per year. We anticipate that this upgrade will be completed in the second quarter of 2023.

Berwind Facilities

Coal from the Berwind Complex is processed through a 650 raw-ton-per-hour preparation plant. We expect to utilize the facility to process coal from both the Berwind Complex and the recently acquired Amonate Assets. Production for 2023 is expected to be approximately 1.1 million tons of primarily low-volatile coal, up from 0.5 million tons in 2022. The Berwind Complex loads its coal utilizing a railcar-loading facility, which is served by the Norfolk Southern railroad.

In 2021, Ramaco Resources shipped 0.2 million tons of Company produced coal from the Berwind Complex, which was trucked to our Knox Creek preparation plant for processing. This tonnage did not include coal from the Amonate Assets, which we acquired in December 2021. Upon completion of the upgrade and rehabilitation of the preparation plant at the Berwind Complex that we acquired in the purchase of the Amonate Assets, most coal mined at the Berwind Complex will be processed in that preparation plant, which began refurbishment in December 2021 and is expected to commence initial operation in the third quarter of 2022. Once the refurbishment is complete, the Berwind preparation plant, at a fee of $10 per ton of processed coal and $5 per ton of loaded coal, this would have equated to $3 million in 2021 had the preparation plant and rail load-out been operational. Through the year ending December 31, 2022, we estimate that CORE would have recognized pro forma $8 million of revenue from the preparation plant and rail load-out, had these been operational at the time. Instead, the aforementioned revenue was recognized at our Knox Creek facilities, as our Berwind preparation plant and rail load-out was not yet up and running.

Knox Creek Facilities

The Knox Creek preparation plant has a capacity of processing 750 tons of raw coal per hour. In 2021, Ramaco Resources shipped 0.2 million tons of coal, the majority of which was produced at the Berwind Complex. All such coal was processed at our Knox Creek preparation plant and 68% of which was shipped via our rail load-out. At a fee of $10 per ton of processed coal and $5 per ton of loaded coal, this would have equated to $3 million of revenue in 2021. Through the year ending December 31, 2022, we estimate that CORE would have recognized pro forma $11 million of revenue from our Knox Creek preparation plant and rail load-out. This is inclusive of coal that was produced at the Berwind Complex and trucked to the Knox Creek Complex. We also process coal purchased from other independent producers at the Knox Creek preparation plant and load-out facilities.

Carbon Products

In 2011, Ramaco Carbon, LLC (“Ramaco Carbon”) acquired one of the largest fee owned private thermal coal deposits in the western United States from the Pittston Coal Company. The property was planned and permitted over several years and is now called the Brook Mine property. The Brook Mine property is located in the northern Powder River Basin near Sheridan, Wyoming and encompasses approximately 16,000 acres containing an in-place coal deposit of over 1.0 billion tons. The Ramaco Carbon permit is for a portion of the property containing an estimated 162 million tons of coal in addition to the REEs have been discovered in the Brook Mine coal seams and surrounding sub-surface strata. See “–Rare Earth Elements.”

8

In response to a fundamental shift in the U.S. coal-fired power generation market, which reduced demand for Powder River Basin coal, Ramaco Carbon, initiated a program to investigate alternative uses of its substantial coal resources. Over the past nine years, CORE has partnered with several research institutes, universities, strategic partners and, importantly, two Department of Energy National Laboratories spearheading U.S. national efforts to develop coal-to-carbon technology. CORE has secured exclusive licensing agreements from both the ORNL and the NETL for the research and development of a wide range of potential commercial applications of coal-to-carbon-based products and materials. As a result of its early initiative and research work to-date, CORE now has an industry leading position in the development of a coal-to-carbon products industry with 53 patented or patent pending processes to cost effectively convert coal to high value products.

Carbon Products Business Opportunity

Although we currently expect no carbon product revenue in 2022 and 2023, to commercialize the substantial Brook Mine coal deposits, we have developed a vertically integrated business plan that envisions the mining of coal that can be processed onsite into much higher value carbon products using our patented processes as well as the extraction and processing of high value REEs. The residual coal can then be sold into the thermal coal market with the proceeds being used to partially, or fully, fund the operating costs of mining, depending on the then prevailing price of Powder River Basin thermal coal. CORE could enter into an agreement with Ramaco Resources or a third party to develop the Brook Mine property and supply feedstock to carbon products manufacturing plants under long-term contracts, which could provide a royalty income stream to CORE in the future if successfully placed into production.

The scope of CORE’s research and development efforts is shown below by the different product examples that CORE has established as its material pillars. These coal-to-carbon product materials have strategic, wide-ranging relevancy in several essential market segments.

Market Segments

| Material | Building Products | Electric

Vehicles | Renewable

Energy | Life Sciences | Electronics | |||||||

| Activated Porous Carbons | ü | ü | ü | ü | ||||||||

| Graphene | ü | ü | ü | ü | ü | |||||||

| Graphite | ü | ü | ü | |||||||||

| Carbon Fiber | ü | ü | ü | ü | ||||||||

| Rare Earth Elements | ü | ü | ü | ü |

The first two carbon product materials that we believe can be commercialized over the next two years are porous carbon and graphene. Both of these materials have established markets that allow for both cost and quality substitution.

| · | Porous Carbon: PCs are any form of carbon made into high surface area absorbents that can be to attract and adsorb certain types of particles. PC is used as a primary material of construction for EV batteries and related fuel cell technologies. CORE’s research and development efforts with the NETL have helped produce a process for creating a high surface area carbon that constitutes an important component of an EV battery. This higher surface area from the PC hopefully will allow the battery to have a more efficient utilization of the cathode energy flow, which ultimately is expected to provide the EV a longer range and allow for a faster charge. |

9

| · | Graphene: Graphene is a two-dimensional single sheet of carbon atoms arranged in a hexagonal pattern that can exhibit stiffness, high thermal and electrical conductivity, strong chemical durability and high electron mobility. These properties may impart mechanical strength, corrosion resistance, durability, fracture toughness, thermal/electrical conductivity, and unique optical properties (emission and detection) to devices and composites. CORE has received three issued patents related to methods for producing and/or utilizing graphene from thermal carbon ore. The first form is suited for high volume bulk applications in the building products industry, where it can be used as a concrete additives admixture for cement and as an additive for paints and coatings. It also reduces permeability in paint/cement, which makes the product stronger, and allows it to last longer. The second form utilizes a high-quality form of graphene ideal for use in a wide range of electronic and life science applications. |

CORE has been in discussion with various parties, including Ramaco Resources, about licensing certain of its carbon products technologies for the manufacture of carbon products in facilities at the iPark property. If CORE is successful in negotiating agreements with third parties interested in manufacturing carbon products using Carbon Ore sourced from the Brook Mine property, CORE could receive future licensing fees from its patents and intellectual property, royalties on production at the Brook Mine property and lease income on the iPark property. We estimate that the commencement of carbon products commercial manufacturing could have a lead time of two to five years dependent on the product or material involved.

Carbon Products Facilities

CORE has also developed the Carbon Advanced Material Innovation Center. The iCAM is located contiguous to the Brook Mine property and has laboratory facilities to continue important research alongside national labs, other research institutes, and universities. We expect that the applied research will continue to develop new coal-to-carbon products applications. CORE has received five research grants from national labs to date, and its independent research efforts have resulted in six granted U.S. patents, one granted South African patent, two allowed U.S. patent applications, and approximately 44 more currently in process throughout various countries ranging from process to end product patents. CORE also has established research and development relationships with the NETL, the ORNL and several other leading research universities and private research organizations.

CORE also has the iPark, contiguous to the Brook Mine property and the iCAM, designed to house initial coal-to-carbon products manufacturing facilities. Future manufacturing operations can purchase or lease land at the iPark complex from CORE. To maximize logistical cost advantage, it is envisioned that these production facilities will purchase carbon feedstock from the Brook Mine property and convey the carbon ore to the processing plants at the iPark.

Rare Earth Elements

Although we currently expect no revenue from REEs in 2022 and 2023, the following is a discussion of developments pertaining to REEs that have been discovered in the Brook Mine coal seams and surrounding sub-surface strata, which is in addition to a large coal deposit at the Brook Mine property.

REEs are naturally occurring elements which are critical to a multitude of end markets including renewable energy, rechargeable batteries, consumer electronics, EVs, defense, medicine, agriculture, high-tech and chemical industries, many of which are experiencing rapidly increasing demand.

The United States has long been dependent on foreign sources, primarily China, to serve domestic markets requiring REE materials for manufacturing. Congress and the Department of Energy have earmarked millions of dollars to develop REEs.

10

Since 2014, the NETL, has been identifying high potential domestic sources of REEs as strategically critical to the United States economy and national security. The NETL has been engaged in research and development focused on the identification, extraction, separation and recovery of concentrated REE minerals from coal-based sources. Through a partnership within a Cooperative Research and Development Agreement, the NETL is working with CORE to assess REE occurrences in coal deposits and related sedimentary strata at CORE’s Brook Mine property.

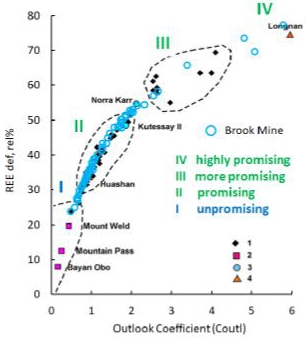

Based on early sampling and analysis, the results of the NETL’s initial analysis of the Brook Mine property and external analysis from Weir International, Inc. have shown REE concentrations characterized by the NETL as “very promising.” The initial NETL analysis revealed concentrations with a potentially world-class REE accumulation of middle REEs and heavy REEs shown in the graph below. The graph compares the relative concentration of REEs within the Brook Mine property (shown in blue) to known REE mines/deposits around the world:

Figure – Plot contrasting the Brook Mine samples versus other worldwide commercial REE ore bodies. This documents the significant promise of the Brook Mine REE deposits, which fall along the promising to highly promising spectrum for the full range of REEs, including the highly valued medium and heavy REEs. Based on this NETL data from 2020, the Brook Mine would rank as among the highest concentrations of REEs found in any deposits on a world-wide basis, including Chinese deposits.

Between November 2021 and February 2022, we completed a comprehensive drilling and coring exploration program consisting of 14 new drillholes targeting three coal seams within the Brook Mine property. Zones of elevated REEs were identified, with several intervals for REEs in two of the holes nearing 1,500 ppm.

We intend to continue to assess the REE development potential of the Brook Mine property through an ongoing 99-hole core drilling program, which we initiated in April 2022 with additional sampling analysis conducted by the NETL. This additional coring will also be used to assess the economic potential for REE recovery within the Brook Mine property. Through July 31, 2022, 29 cores have been drilled, 18 of which have been preliminarily analyzed using XRF scanners in the field with 100% showing the presence of REEs. More extensive testing and analysis is planned by the NETL to determine the size and areal extent of the REE deposit. It is estimated that the Ramaco Resources capital expenditure associated with the REE drilling program will total approximately $1.5 million in 2022.

11

This current drilling program will supplement an established 3,500 ft. sampling grid for the targeted coal seams within the Brook Mine property permit area. The drilling, core logging and XRF analysis is expected to be completed in late 2022. As a result of new drilling activity contemplated by the current drilling program, we expect the sampling grid to decrease to approximately 1,500 ft. Once completed, the additional drill core and analyses is expected to significantly enhance CORE’s understanding of both the deposit zones containing concentrations of REEs as well as the REE spatial distribution within the Brook Mine property.

Assuming that these efforts confirm the commercial viability of mining REEs, CORE could likely enter into a lease and royalty agreement with Ramaco Resources, or another party, to mine and commercially develop both the REEs and the coal.

Investment Highlights

| · | Experienced management team. CORE, through Ramaco Resources, has a highly experienced management team with a long history of evaluating, pursuing, consummating and leasing/developing acquisitions of coal reserve interests. They have previously held senior business development, financial and operations positions at large, publicly traded coal companies as well as successful private coal companies. |

| · | Significant revenue from coal royalties and infrastructure processing. CORE is expected to pay a quarterly dividend based on the financial performance of the CORE Assets. Based on Ramaco Resources’ projected coal production for the second half of 2022 and full year 2023 together with existing sales contracts and using the forward market prices for coal similar in grade to Ramaco Resources’, as well as the coal preparation and rail load-out fees in place, we project total revenue attributable to the CORE Assets to be $56.9 million and $96.6 million for the years ending December 31, 2022 and 2023, respectively. Based on these projections, we expect revenue available for payment as dividends to holders of our Class B common stock to be approximately $2.84 million per quarter ($11.4 million annualized) for the balance of 2022 and $4.83 million per quarter ($19.3 million annualized) in 2023 based on the anticipated dividend of 20% of the revenue attributable to the CORE Assets. We will adjust the amount of our Class B common stock dividend for the period from the closing of the Distribution through December 31, 2022, based on the actual length of the period. See “Cash Dividend Policy and Restrictions on Dividends.” |

| · | CORE’s royalty and infrastructure revenue will be less volatile. Because CORE’s revenue will be calculated on royalty income and infrastructure usage fees before the allocation of capital expenditures or operating expenses, CORE’s revenue is impacted less by changes in coal prices than Ramaco Resources. |

| · | Geologically advantaged metallurgical coal properties. CORE has advantaged geologic characteristics such as relatively thick coal seams at the underground mines, a low overburden mining ratio at the surface mines and desirable metallurgical coal quality which will foster continued mining activity and which we expect to generate royalty income over the next 20 years or more. Furthermore, a majority of the coal seams being developed on our properties are accessible above drainage, thereby reducing our up-front development costs as operator. These characteristics contribute to a production profile that we believe will contribute to a cash cost of production for our lessees that is substantially below most U.S. domestic metallurgical coal producers. As a result, we expect our lessees to operate our reserves profitably, which we believe will lead to relatively consistent production and royalty incomes from our properties. |

| · | High quality and efficient coal infrastructure assets. CORE’s infrastructure assets are integral to Ramaco Resources’ mining operations and have been recently built or refurbished. As a result, these assets have relatively low operating costs. |

| · | Upside from potential carbon products. Ramaco Carbon’s research and development work over the past nine years has resulted in 53 issued, allowed and pending patents on processes to convert low-cost coal from Ramaco Resources’ Brook Mine property into high value carbon products such as porous carbon, graphene, carbon fiber, graphite and others. As a result, CORE is positioned to gain a first mover market position in the U.S. coal-to-carbon products industry by utilizing its leading-edge technology, proprietary intellectual property and low-cost carbon ore resource base. |

| · | Potential for the Brook Mine property to become an important U.S. source of REEs. Although in the early stage of determining the size and commercial potential of our REE deposit, initial analysis by the NETL and by the engineering consulting firm WEIR International, Inc. has found high concentration levels of a range of REEs, including the higher value medium and heavy REEs, within the Brook Mine seams. If these potentially world-class concentrations of REEs are commercially viable, such a development could provide CORE an additional royalty income stream. |

12

Dividend Policy

We currently pay a cash dividend of $5.0 million per quarter ($20.0 million annualized) on the existing common stock and expect to pay an initial cash dividend of $2.84 million per quarter ($11.4 million annualized) on the Class B common stock for the balance of 2022. We will adjust the amount of our Class B common stock dividend for the period from the closing of the Distribution through December 31, 2022, based on the actual length of the period. For illustration in 2023, if the Class A common stock cash dividend remained constant at $20.0 million and we additionally paid an estimated dividend of $19.3 million on the Class B common stock, the cash dividends from the shares of Class A common stock and Class B common stock would total $39.3 million. The dividend yield for these combined payments would be based upon the stock price at the time.

Both the 2022 and 2023 dividend payments on the Class B common stock would be made based on the performance of the CORE Assets and are estimated below based on an anticipated dividend distribution of 20% of the revenue attributable to the CORE Assets. The dividends for our Class A common stock and Class B common stock will be consistent with our publicly disclosed dividend policy, which may be modified by our Board from time to time.

Our ability to pay dividends is subject to the discretion of our Board and the requirements of applicable law. The timing and amount of dividends declared will depend on, among other things: (a) our earnings, earnings outlook, production, processing and shipping levels, financial condition, cash flow, cash requirements and our outlook on current and future market conditions, (b) our overall liquidity, (c) the restrictive covenants in our Credit and Security Agreement, dated November 2, 2018 (as amended or amended and restated, the “Credit Agreement”) with KeyBank National Association, as the administrative agent, and other lenders party thereto and any future debt instruments and (d) provisions of applicable law governing the payment of dividends.

The revenues attributable to CORE may be highly volatile, and we cannot predict with certainty the amount of cash, if any, that will be available for distribution as dividends in any period. Also, there may be a high degree of variability from period to period in the amount of cash, if any, that is available for the payment of dividends.

Treatment of Fractional Shares

You will not receive fractional shares in connection with the Distribution. Instead, the transfer and distribution agent will aggregate all fractional shares into whole shares and sell the whole shares at prevailing market prices on behalf of those holders who would have been entitled to receive a fractional share. The transfer and distribution agent will determine, in its sole discretion, when, how and through which broker-dealers such sales will be made without any influence by us. We anticipate that these sales will occur as soon as practicable after the Distribution is completed. Those holders will then receive a cash payment in the form of a check or wire transfer in an amount equal to their pro rata share of the total net proceeds of those sales. If you hold your stock through the transfer and distribution agent’s Direct Registration System, your check for any cash that you may be entitled to receive instead of fractional shares of Class B common stock will be mailed to you separately.

Neither we nor the transfer and distribution agent will guarantee any minimum sale price for any fractional shares. No interest will be paid on any cash you receive in lieu of a fractional share. The receipt of cash in lieu of fractional shares will generally be taxable to the recipient stockholders. See “Material U.S. Federal Income Tax Consequences—Tax Treatment of the Distribution.”

Recent Developments

Maben Acquisition

On August 8, 2022, the Company announced that Ramaco Development, LLC, a subsidiary of the Company, entered into an agreement to acquire 100% of the membership interests in Maben Coal LLC, a Delaware limited liability company (“Maben”), including its approximately 33 million tons of low volatile coal for an aggregate purchase price of $30 million. We anticipate initial highwall production will commence in late 2022, reaching full production of 250,000 tons of low volatile coal during the first half of 2023. The transaction also provides the future optionality to increase annual production to approximately 1 million tons annually.

13

Methane Ignition at Berwind Mine

On July 10, 2022, we experienced a material methane ignition at our Berwind mining complex. The cause of the ignition is unknown. We, in conjunction with the appropriate state and federal regulatory authorities, will be conducting a full investigation into the incident. The mine was idle at the time of the incident, and there were no personnel in the mine nor any injuries or fatalities. We are evaluating the extent of the damage. Production from the Berwind Complex is expected to be impacted for an indeterminant period of time. We will provide additional information regarding plans for both the rehabilitation and restarting of the mine as it becomes available.

Special Meeting and Stockholder Approval

At a special meeting on , 2022 (the “special meeting”), our stockholders approved the tracking stock proposal to (1) reclassify our existing common stock as shares of Class A common stock and (2) distribute tracking stock to be designated as Class B common stock to existing holders of the Class A common stock (the “tracking stock proposal”), and to amend our certificate of incorporation in connection with the tracking stock proposal. These amendments will become effective concurrent with the Distribution. As of August 26, 2022, we had 44,087,746 shares of existing common stock outstanding.

Corporate Information

Our headquarters are located at 250 West Main

Street, Suite 1800, Lexington, Kentucky 40507, and our telephone number is (859) 244-7455. Our investor relations website address is

ir.ramacoresources.com. Information contained on, or that can be accessed through, our website is not incorporated by reference into

this prospectus, and you should not consider information on our website to be part of this prospectus.

14

Description of the Class B Common Stock

Please see “The Distribution” for a more detailed description of the matters described below.

| Issuer | Ramaco Resources, Inc. |

| Security to be Distributed | Class B common stock. |

| Distribution Ratio | Each holder of existing common stock will receive a distribution of 0.2 shares of Class B common stock for every one share of existing common stock held on the record date (with cash in lieu of any fractional share interests). |

| Fractional Shares | Fractional shares of our Class B common stock will not be distributed. Fractional shares of our Class B common stock will be aggregated and sold in the public market by the transfer and distribution agent, and stockholders will receive a cash payment in lieu of a fractional share. The aggregate net cash proceeds of these sales will be distributed ratably to those stockholders who would otherwise have received fractional interests. These proceeds generally will be taxable to those stockholders. |

| Distribution Agent, Transfer Agent and Registrar for the Shares | American Stock Transfer & Trust Company will be the distribution agent, transfer agent and registrar for the shares of our common stock. |

| Record Date | The record date is the close of business, New York City time, on , 2022. |

| Distribution Date | , New York City time, on , 2022. |

| Additional Issuances | Additional shares of the Class B common stock may be issued from time to time, including as consideration for acquisitions or for cash. |

| CORE Assets | The CORE Assets will initially consist of coal royalties, coal infrastructure revenue, Ramaco Carbon and REEs. Our Board retains full discretion to modify the CORE Assets from time to time. Holders of the Class B common stock will not have any specific rights with respect to CORE. See “Risk Factors—Holders of Class B common stock are common stockholders of the Company and, therefore, are subject to risks associated with an investment in the Company as a whole, even if a holder does not own shares of Class A common stock.” |

| Dividend Policy | Subject to the discretion of our Board and the requirements of Delaware law, we expect to pay an initial cash dividend of $2.84 million per quarter ($11.4 million annualized) on the Class B common stock for the balance of 2022 and $4.83 million per quarter ($19.3 million annualized) in 2023 based on the anticipated dividend of 20% of the revenue attributable to the CORE Assets. We will adjust the amount of our Class B common stock dividend for the period from the closing of the Distribution through December 31, 2022, based on the actual length of the period. Our Board may modify the dividend policy from time to time. See “Cash Dividend Policy and Restrictions on Dividends. |

| Voting and Governance | The Class B common stock will vote with the Class A common stock as a single class on all matters on which the Class A common stock is entitled to vote. The Class B common stock will not have any specific voting rights or governance with respect to CORE. |

| Exchange Right | Following the distribution of the Class B common stock, our Board may, in its sole discretion, elect to exchange all outstanding shares of the Class B common stock into shares of Class A common stock based on an exchange ratio determined by a 20-day trailing volume-weighted average price (“VWAP”) for each class of stock. |

15

| Use of Proceeds | We will not receive any proceeds from the distribution of our Class B common stock in the Distribution. |

| Material U.S. Federal Income Tax Consequences of the Distribution | Kirkland & Ellis LLP (“Kirkland & Ellis”) is providing an opinion as of the date hereof, which is being filed herewith as Exhibit 8.1 to the registration statement of which this prospectus is a part, to the effect that, under current U.S. federal income tax law:

· the Class B common stock should be treated as stock of the Company for U.S. federal income tax purposes;

· the Distribution should qualify as a distribution under Section 305(a) of the Internal Revenue Code of 1986, as amended (the “Code”), and therefore no income, gain or loss should be recognized by the holders of our existing common stock as a result of the Distribution (except with respect to the receipt of cash in lieu of fractional shares);

· no gain or loss should be recognized by us as a result of the Distribution; and

· the Class B common stock should not constitute “Section 306 stock,” within the meaning of Section 306(c) of the Code.

For a more complete summary of such opinion and the material U.S. federal income tax consequences of the Distribution and the ownership and disposition of the Class B common stock, see “Material U.S. Federal Income Tax Consequences.”

|

| Listing | There is not currently a public market for our Class B common stock. We intend to apply to list our Class B common stock on the NASDAQ under the symbol “METCB.” |

| Risk Factors | You should carefully read and consider the information set forth under the heading “Risk Factors” and all other information set forth in this prospectus before deciding to invest in our common stock. |

16

Summary Historical Financial Data

The following tables sets forth our historical financial data as of June 30, 2022 and 2021 and for each of the years in the three-year period ended December 31, 2021, 2020 and 2019. The following information is qualified in its entirety by, and should be read in conjunction with, our audited financial statements and notes thereto for the periods presented that are included in our Quarterly Report on Form 10-Q for the six months ended June 30, 2022 and our Annual Report on Form 10-K for the year ended December 31, 2021, both of which are incorporated by reference herein. See “Where You Can Find More Information.”

Summary Balance Sheet Data

| Six months ended June 30, | Years ended December 31, | |||||||||||||||||||

| (in thousands) | 2022 | 2021 | 2021 | 2020 | 2019 | |||||||||||||||

| (unaudited) | ||||||||||||||||||||

| Balance Sheet Data: | ||||||||||||||||||||

| Cash and cash equivalents | $ | 43,461 | $ | 19,394 | $ | 21,891 | $ | 5,300 | $ | 5,532 | ||||||||||

| Property, plant and equipment – net | 341,596 | 177,575 | 227,077 | 180,531 | 178,202 | |||||||||||||||

| Total assets | 489,706 | 247,082 | 329,033 | 228,623 | 226,813 | |||||||||||||||

| Current maturities of long-term debt | 40,531 | 6,679 | 11,135 | 4,872 | 3,333 | |||||||||||||||

| Long-term debt, less current portion | 58,972 | 6,709 | 40,301 | 12,578 | 9,614 | |||||||||||||||

| Other long-term obligations | 40,254 | 18,026 | 30,998 | 17,837 | 20,705 | |||||||||||||||

| Total stockholders’ equity | 279,682 | 185,430 | 211,074 | 169,095 | 170,083 | |||||||||||||||

Summary of Results of Operations Data

| Six months ended June 30, | Years ended December 31, | |||||||||||||||||||

| (in thousands, except per share data) | 2022 | 2021 | 2021 | 2020 | 2019 | |||||||||||||||

| (unaudited) | ||||||||||||||||||||

| Revenue | $ | 293,537 | $ | 119,511 | $ | 283,394 | $ | 168,915 | $ | 230,213 | ||||||||||

| Costs and expenses | ||||||||||||||||||||

| Cost of sales (exclusive of items shown separately below) | 157,897 | 88,958 | 195,412 | 145,503 | 162,470 | |||||||||||||||

| Asset retirement obligations accretion | 990 | 305 | 615 | 570 | 511 | |||||||||||||||

| Depreciation and amortization | 18,463 | 12,110 | 26,205 | 20,912 | 19,521 | |||||||||||||||

| Selling, general and administrative | 20,610 | 9,873 | 21,629 | 21,023 | 18,179 | |||||||||||||||

| Total costs and expenses | 197,960 | 111,246 | 243,861 | 188,008 | 200,681 | |||||||||||||||

| Operating income | 95,577 | 8,265 | 39,533 | (19,093 | ) | 29,532 | ||||||||||||||

| Other income | 2,714 | 6,367 | 7,429 | 11,926 | 1,758 | |||||||||||||||

| Interest expense, net | (3,068 | ) | (485 | ) | (2,556 | ) | (1,224 | ) | (1,193 | ) | ||||||||||

| Income before tax | 95,223 | 14,147 | 44,406 | (8,391 | ) | 30,097 | ||||||||||||||

| Income tax expense (benefit) | 20,472 | 62 | 4,647 | (3,484 | ) | 5,163 | ||||||||||||||

| Net income | $ | 74,751 | $ | 14,085 | $ | 39,759 | $ | (4,907 | ) | $ | 24,934 | |||||||||

| Earnings per common share | ||||||||||||||||||||

| Basic | $ | 1.69 | $ | 0.32 | $ | 0.90 | $ | (0.12 | ) | $ | 0.61 | |||||||||

| Diluted | $ | 1.66 | $ | 0.32 | $ | 0.90 | $ | (0.12 | ) | $ | 0.61 | |||||||||

| Adjusted EBITDA | $ | 121,917 | $ | 29,624 | $ | 79,042 | $ | 18,455 | $ | 55,382 | ||||||||||

Summary Attributed Historical Financial Data

The following tables sets forth selected historical attributed unaudited financial data for CORE as of June 30, 2022, and for each of the years in the three-year period ended December 31, 2021, 2020 and 2019. The following information is qualified in its entirety by, and should be read in conjunction with, our audited financial statements and notes thereto for the periods presented incorporated by reference herein.

17

Selected Summary of Results of Operations Data

| Six months ended June 30, | Years ended December 31, | |||||||||||||||

| (in thousands, except per share data) | 2022 | 2021 | 2021 | 2020 | ||||||||||||

| (unaudited) | ||||||||||||||||

| Royalty revenue | $ | 5,510 | $ | 2,244 | $ | 5,627 | $ | 3,265 | ||||||||

| Infrastructure revenue | 16,157 | 15,181 | 32,038 | 24,414 | ||||||||||||

| Proforma revenue | 21,667 | 17,425 | 37,665 | 27,679 | ||||||||||||

| Cash available | 21,667 | 17,425 | 37,665 | 27,679 | ||||||||||||

| 20% cash available for dividend | 4,333 | 3,485 | 7,533 | 5,536 | ||||||||||||

| Per share Class B common stock | $ | 0.48 | $ | 0.38 | $ | 0.83 | $ | 0.61 | ||||||||

18

Investment in our securities involves a high degree of risk. You should carefully consider the risks described in the section “Risk Factors” contained in our Annual Report on Form 10-K for the year ended December 31, 2021 and our subsequent quarterly reports on Form 10-Q, which are incorporated by reference in this prospectus in their entirety, as well as other information in this prospectus, any accompanying prospectus supplement and other documents that are incorporated by reference herein or therein, before purchasing any securities offered hereby. Each of the risks described could materially adversely affect our business, financial condition, results of operations, or ability to make distributions to our stockholders. In such case, you could lose all or a portion of your original investment. See “Where You Can Find Additional Information” beginning on page 53 of this prospectus.

Risks Related to our Proposed Tracking Stock Structure

Holders of Class B common stock are common stockholders of the Company and, therefore, are subject to risks associated with an investment in the Company as a whole, even if a holder does not own shares of Class A common stock.

Even though we have attributed, for financial reporting purposes, CORE to the Class B common stock in order to prepare the separate financial statement schedules included in this registration statement, we will retain legal title to all of our assets and our tracking stock capitalization will not limit our legal responsibility, or that of our subsidiaries, for the liabilities included in any set of financial statement schedules. Holders of Class B common stock will not have any legal rights related to specific assets attributed to CORE and, in any liquidation, holders of Class B common stock and Class A common stock will be entitled to receive a pro rata share of our available net assets based on their respective numbers of shares. See “Description of Common Stock—Class A and Class B Common Stock—Liquidation Rights.”

Our Board’s ability to reattribute businesses, assets and expenses between the Class A common stock and Class B common stock may make it difficult to assess the future prospects of a class of common stock based on past performance.

Our Board currently expects to attribute 100% of the costs associated with the CORE Assets to Ramaco Resources and zero such costs to CORE; however, our Board is vested with discretion to reattribute businesses, assets and liabilities that are attributed to one class of common stock to another class of common stock, without the approval of any of our stockholders. Any such reattribution made by our Board, as well as the existence, in and of itself, of the right to effect a reattribution may impact the ability of investors to assess the future prospects of the businesses and assets attributed to a class of common stock, including liquidity and capital resource needs to pay the projected dividend to holders of our Class B common stock, based on past performance. Stockholders may also have difficulty evaluating the liquidity and capital resources of the businesses and assets attributed to each class of common stock based on past performance, as our Board may use the liquidity of one class to fund the liquidity of another class and capital expenditure requirements through the use of loans and interests between classes. See “Cash Dividend Policy and Restrictions on Dividends” for additional information.

We could be required to use assets attributed to one class of common stock to pay liabilities attributed to another class.

The assets attributed to one class are potentially subject to the liabilities attributed to another class, even if those liabilities arise from lawsuits, contracts or indebtedness that are attributed to such other class. No provision of our Amended Charter prevents us from satisfying liabilities of one class with assets of another class, and our creditors will not in any way be limited by our tracking stock capitalization from proceeding against any assets they could have proceeded against if we did not have a tracking stock capitalization. See “Cash Dividend Policy and Restrictions on Dividends” for additional information.

19

The market price of the Class B common stock may not reflect the performance of CORE attributed to it, as we intend.

We cannot assure you that the market price of the Class B common stock related to CORE will, in fact, reflect the performance of CORE attributed to it. Holders of Class B common stock will be common stockholders of the Company as a whole and, as such, will be subject to all risks associated with an investment in the Company and all of our businesses, assets and liabilities. As a result, the market price of Class B common stock may, in part, reflect events that are intended to be reflected by the Class A common stock of the Company. In addition, investors may discount the value of Class B common stock because it is part of a common enterprise rather than a stand-alone entity.

The market price of the Class B common stock may be volatile, could fluctuate substantially and could be affected by factors that do not affect traditional common stock.

We do not know how the market will react to the Distribution. In addition, to the extent the market price of the Class B common stock tracks the performance of more focused classes of businesses, assets and liabilities than our existing common stock does, the market price of the Class B common stock may be more volatile than the market price of our existing common stock has been historically. The market price of the Class B common stock may be materially affected by, among other things:

| · | actual or anticipated fluctuations CORE’s operating results; |

| · | potential acquisition activity by the Company (regardless of the class to which it is attributed) or the companies in which we invest; |

| · | issuances of debt or equity securities to raise capital by the Company or the companies in which we invest and the manner in which that debt or the proceeds of an equity issuance are attributed to each of the classes; |

| · | changes in financial estimates by securities analysts regarding the Class B common stock, the Class A common stock or CORE attributable to the Class B common stock; |

| · | the complex nature and the potential difficulties investors may have in understanding the terms of our new tracking stock, as well as concerns regarding the possible effect of certain of those terms on an investment in our stocks; and |

| · | general market conditions. |