UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark one)

OR

For the fiscal year ended

OR

OR

for the transition period from ____________ to ____________

Commission file number

(Exact name of the Registrant as specified in its charter)

(Jurisdiction of incorporation or organization)

c/o Beijing Wenxin Co., Ltd.

People’s Republic of

Tel: +86-166-7863-6230

(Address of principal executive offices)

c/o Beijing Wenxin Co., Ltd.

People’s Republic of

Tel:

(Name, Telephone, E-mail and/or Facsimile Number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||

| The |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None.

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None.

As of the close of the period covered by this

annual report the issuer had

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☐ Large Accelerated filer | ☐ Accelerated filer | ☒ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant

has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial

reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or

issued its audit report.

If securities are registered pursuant to Section

12(b) of the Act, indicate by check mark whether the financial statement of the registrant included in the filing reflect the correction

of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| ☒ | ☐ International Financial Reporting Standards as issued by the International Accounting Standards Board | ☐ Other |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No

Table of Contents

i

CERTAIN INFORMATION

In this Annual Report on Form 20-F (the “Annual Report”), unless otherwise indicated, numerical figures included in this Annual Report have been subject to rounding adjustments. Accordingly, numerical figures shown as totals in various tables may not be arithmetic aggregations of the figures that precede them.

For the sake of clarity, this Annual Report follows the English naming convention of first name followed by last name, regardless of whether an individual’s name is Chinese or English.

Except where the context otherwise requires and for purposes of this Annual Report only:

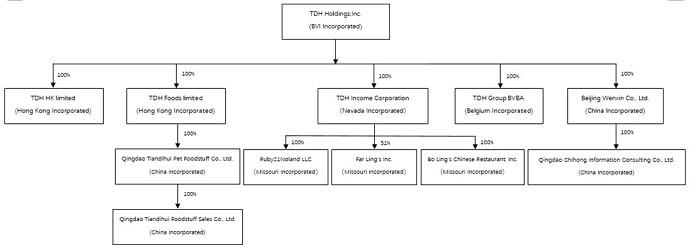

| ● | Depending on the context, the terms “we,” “us,” “our company,” and “our” refer to TDH Holdings, Inc., a British Virgin Islands company; |

| ● | TDH HK Limited, a Hong Kong company wholly-owned by TDH HOLDINGS, INC.; |

| ● | TDH Foods Limited, a Hong Kong company wholly-owned by TDH HOLDINGS, INC.; |

| ● | TDH Group BVA, a Belgium company wholly-owned by TDH Holdings, Inc; |

| ● | TDH Income Corporation, a Nevada corporation; |

| ● | Ruby21Noland LLC, a Missouri corporation; |

| ● | Far Ling’s Inc., a Missouri corporation; |

| ● | Bo Ling’s Chinese Restaurant, Inc., a Missouri corporation; |

| ● | Qingdao Tiandihui Foodstuffs Co., Ltd. (“Tiandihui”), a Chinese limited liability company, disposed in December 2023 as a result of the completion of bankruptcy proceedings; |

| ● | Qingdao Tiandihui Pet Foodstuffs Co., Ltd., a Chinese limited liability company; |

| ● | Qingdao Tiandihui Foodstuffs Sales Co., Ltd., a Chinese limited liability company; |

| ● | Beijing Chongai Jiujiu Cultural Communication Co., Ltd., a Chinese limited liability company, disposed in December 2023; |

| ● | Beijing Wenxin Company., Ltd., a Chinese limited liability company; |

| ● | Qingdao Chihong Information Consulting Co., Ltd., a Chinese limited liability company; |

| ● | “shares” and “common shares” refer to our shares, $0.02 par value per share; |

| ● | “China” and “PRC” refer to the People’s Republic of China, excluding, for the purposes of this Annual Report only, Macau, Taiwan and Hong Kong; and |

| ● | all references to “RMB,” and “Renminbi” are to the legal currency of China, all references to “USD,” and “U.S. Dollars” are to the legal currency of the United States., and all references to “Euro” and “€” are to the legal currency of Belgium. |

ii

FORWARD-LOOKING STATEMENTS

This Report contains “forward-looking statements” that represent our beliefs, projections and predictions about future events. All statements other than statements of historical fact are “forward-looking statements” including any projections of earnings, revenue or other financial items, any statements of the plans, strategies and objectives of management for future operations, any statements concerning proposed new projects or other developments, any statements regarding future economic conditions or performance, any statements of management’s beliefs, goals, strategies, intentions and objectives, and any statements of assumptions underlying any of the foregoing. Words such as “may”, “will”, “should”, “could”, “would”, “predicts”, “potential”, “continue”, “expects”, “anticipates”, “future”, “intends”, “plans”, “believes”, “estimates” and similar expressions, as well as statements in the future tense, identify forward-looking statements.

These statements are necessarily subjective and involve known and unknown risks, uncertainties and other important factors that could cause our actual results, performance or achievements, or industry results, to differ materially from any future results, performance or achievements described in or implied by such statements. Actual results may differ materially from expected results described in our forward-looking statements, including with respect to correct measurement and identification of factors affecting our business or the extent of their likely impact, the accuracy and completeness of the publicly available information with respect to the factors upon which our business strategy is based on the success of our business.

Forward-looking statements should not be read as a guarantee of future performance or results, and will not necessarily be accurate indications of whether, or the times by which, our performance or results may be achieved. Forward-looking statements are based on information available at the time those statements are made and management’s belief as of that time with respect to future events and are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the forward-looking statements. Important factors that could cause such differences include, but are not limited to, those factors discussed under the headings “Risk Factors”, “Operating and Financial Review and Prospects,” “Information on the Company” and elsewhere in this Annual Report.

This Annual Report should be read in conjunction with our audited financial statements and the accompanying notes thereto, which are included in Item 18 of this Annual Report.

Summary of Risk Factors

Investing in our Common Shares involves significant risks. You should carefully consider all of the information in this annual report before making an investment in our Common Shares. Below please find a summary of the principal risks we face, organized under the relevant headings. These risks are discussed more fully in the section titled “Risk Factors”

Risks related to our business. See “Risk Factors – Risks Related to Our Business”

Risk and uncertainties related to our business include, but are not limited to, the following:

| ● | We may be subject to claims that were not discharged in Tiandihui’s bankruptcy proceedings, which could have a material adverse effect on our operating results and profitability. |

| ● | The report of our independent registered public accounting firm on our financial statements includes an explanatory paragraph that expresses substantial doubt about our ability to continue as a going concern. |

| ● | We have historically incurred recurring losses and it is uncertain whether we may continue to incur losses in the future. |

| ● | We discontinued our petfood manufacturing segment and the turnaround of our business currently depends, in part, on our ability to successfully generate revenue in the restaurant segment. |

| ● | We depend on our key personnel, and our business and growth prospects may be severely disrupted if we lose their services. |

| ● | While we are not aware of any data breach in the past, cyber-attacks, computer viruses or any future failure to adequately maintain security and prevent unauthorized access to electronic and other confidential information could result in a data breach which could materially adversely affect our reputation, financial condition and operating results. |

iii

Risks related to our restaurant segment business. See “Risk Factors – Risks Related to the Restaurant Segment”

Risk and uncertainties related to our restaurant segment business include, but are not limited to, the following:

| ● | Our restaurant base is geographically concentrated in Missouri, and we could be negatively affected by conditions specific to this state. |

| ● | Failure to preserve the value and relevance of our brand could have an adverse impact on our financial results. |

| ● | If we do not anticipate and address evolving consumer preferences and effectively execute our pricing, promotional and marketing plans, our business could suffer. |

| ● | We face intense competition in our market, which could hurt our business. |

| ● | Food safety and foodborne illness concerns may have an adverse effect on our reputation and business. |

Risks related to Doing Business in China. See “Risk Factors – Risks Related to Doing Business in China”

Risk and uncertainties related to doing business in China include, but are not limited to, the following:

| ● | Because of our corporate structure, we as well as the investors are subject to unique risks due to uncertainty of the interpretation and the application of the PRC laws and regulations. |

| ● | Uncertainties with respect to the PRC legal system could have a material adverse effect on us. |

| ● | The Chinese government exerts substantial influence over the manner in which we must conduct our business activities and may intervene or influence our operations at any time, which could result in a material change in our operations and the value of our Common Shares. |

| ● | Draft rules for China-based companies seeking for securities offerings in foreign stock markets was released by the CSRC for public consultation. While such rules have not yet come into effect, the Chinese government may exert more oversight and control over overseas public offerings conducted by China-based issuers, which could significantly limit or completely hinder our ability to offer or continue to offer our Common Shares to investors and could cause the value of our Common Shares to significantly decline or become worthless. |

| ● | CSRC and other Chinese government agencies may exert more oversight and control over offerings that are conducted overseas and foreign investment in China-based issuers. Additional compliance procedures may be required in connection offerings, and, if required, we cannot predict whether we will be able to obtain such approval. As a result, we face uncertainty about future actions by the PRC government that could significantly affect our ability to offer or continue to offer securities to investors and cause the value of our securities to significantly decline or be worthless. |

| ● | We may be liable for improper use or appropriation of personal information provided by our customers. |

| ● | Since our operations and some of our assets are located in the PRC, shareholders may find it difficult to enforce a U.S. judgment against the assets of our company, our directors and executive officers. |

| ● | We hold certain of our cash balances in RMB in uninsured bank accounts in China. |

iv

| ● | We may be subject to PRC regulatory limitations on merger and acquisition (M&A) activities. |

| ● | Fluctuation of the Renminbi may indirectly affect our financial condition by affecting the volume of cross-border money flow. |

| ● | We may become a passive foreign investment company, which could result in adverse U.S. tax consequences to U.S. investors. |

| ● | Introduction of new laws or changes to existing laws by the PRC government may adversely affect our business. |

| ● | Governmental control of currency conversion may affect the value of your investment. |

| ● | PRC’s labor law restricts our ability to reduce our workforce in the PRC in the event of an economic downturn and may increase our production costs. |

| ● | Changes in PRC’s political and economic policies could harm our business. |

| ● | If relations between the United States and China worsen, our share price may decrease and we may have difficulty accessing U.S. capital markets. |

| ● | Because our operations are located in the PRC, information about our operations is not readily available from independent third-party sources. | |

| ● | Failure to comply with PRC laws and regulations related to labor and employee benefits may subject us to penalties or additional cost. | |

| ● | We may be exposed to liabilities under the Foreign Corrupt Practices Act and Chinese anti-corruption law. | |

| ● | Our PRC subsidiaries are subject to restrictions on paying dividends or making other payments to us, which may restrict our ability to satisfy our liquidity requirements. |

Risks related to the Ownership of our Common Shares. See “Risk Factors – Risks Related to the Ownership of our Common Shares”

Risk and uncertainties related to ownership of our Commons Shares include, but are not limited to, the following:

| ● | We are a holding company incorporated in the British Virgin Islands. As a holding company with no material operations of our own, we conduct a substantial majority of our operations through our subsidiaries established in the PRC. |

| ● | Recent joint statement by the SEC and PCAOB, proposed rule changes submitted by Nasdaq, and an act passed by the U.S. Senate all call for additional and more stringent criteria to be applied to emerging market companies upon assessing the qualification of their auditors, especially the non-U.S. auditors who are not inspected by the PCAOB. These developments could add uncertainties to our listing. |

| ● | The Holding Foreign Companies Accountable Act all call for additional and more stringent criteria to be applied to emerging market companies upon assessing the qualification of their auditors, especially the non-U.S. auditors who are not inspected by the PCAOB. These developments could add uncertainties to our continued listing. |

| ● | If our financial condition deteriorates as a NASDAQ listed company, we may not meet continued listing standards on the NASDAQ Capital Market. |

| ● | We are a “foreign private issuer,” and our disclosure obligations differ from those of U.S. domestic reporting companies. As a result, we may not provide you the same information as U.S. domestic reporting companies or we may provide information at different times, which may make it more difficult for you to evaluate our performance and prospects. |

| ● | The market price of shares may be volatile, which could cause the value of your investment to decline. |

| ● | As the rights of shareholders under British Virgin Islands law differ from those under U.S. law, you may have fewer protections as a shareholder. |

v

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not required.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not required.

ITEM 3. KEY INFORMATION

| A. | [Reserved] |

| B. | Capitalization and Indebtedness |

Not required.

| C. | Reasons for the Offer and Use of Proceeds |

Not required.

| D. | Risk factors |

You should carefully consider the following risk factors, together with all of the other information included in this Annual Report.

Risks Related to Our Business

We may be subject to claims that were not discharged in Tiandihui’s bankruptcy proceedings, which could have a material adverse effect on our operating results and profitability.

From time to time, the Company is a party to various legal actions arising in the ordinary course of business. The Company accrues costs associated with these matters when they become probable and the amount can be reasonably estimated. Legal costs incurred in connection with loss contingencies are expensed as incurred. Since November 2019, the Company has been a subject of 57 lawsuits by its raw material supplies, printing and packaging supplies, transportation companies and other vendors. The claims raised in these lawsuits pertain to the Company’s non-payment of various invoices for supplier and vendor services rendered, with related interest and costs. In 44 cases, the creditors have reached civil conciliation letters with our company, and in 9 cases, the court has issued civil judgments. With respect to the remaining 4 cases, the plaintiffs withdrew the lawsuits because of lack of evidence. The settlement and judgments involved total claims of RMB13.86 million (USD $2.12 million). Such liabilities have been accrued and reflected in the consolidated financial statements for the year ended December 31, 2020. On March 13, 2021, a land use right and a factory building on the land owned by Tiandihui were auctioned by the court for $5,098,461 (RMB33.14 million). On March 16, 2022, the People’s Court of Huangdao District, Qingdao City, Shandong Province made a civil ruling and announced the acceptance of creditors’ application of bankruptcy liquidation of Tiandihui, and it entered into bankruptcy proceedings. On November 3, 2023, another land use right and a factory building on the land owned by Tiandihui were auctioned by the court for $875,321 (RMB 6.28 million). On December 27, 2023, the court announced that the bankruptcy property distribution plan of Tiandihui had been implemented and the bankruptcy proceedings were complete. As a result, Tiandihui has been fully disposed as of December 31, 2023, and substantially all the material claims against Tiandihui that arose prior to the date of the bankruptcy completion were addressed. However, we may be subject to claims that were not discharged in the bankruptcy proceedings, if any. To the extent any pre-bankruptcy liability still remains, the ultimate resolution of such claims and other obligations may have a material adverse effect on our future operating results, profitability and financial condition.

1

The report of our independent registered public accounting firm on our financial statements includes an explanatory paragraph that expresses substantial doubt about our ability to continue as a going concern, and if our business is unable to continue it is likely investors will lose all of their investment.

As discussed in Note 2 to the consolidated financial statements to this Annual Report, the Company fully discontinued its petfood business during 2023 because the Tiandihui bankruptcy process was concluded and all claims against Tiandihui were processed by December 27, 2023. Currently the Company’s revenue is substantially generated from the restaurant business segment. The Company’s business turnaround currently depends, in part, on its ability to successfully introduce, manage and acquire new restaurants. If the Company is not able to effectively manage and acquire new restaurants that successfully generate revenue, it may not be able to grow and maintain its business as anticipated, and its sales may decline and its future business, financial condition and results of operations may be materially adversely affected.

There can be no assurances that future revenue or capital infusion will be sufficient to enable the Company to develop its business to a level where it will be profitable or continuously to generate positive cash flows. Our auditor, YCM CPA Inc., has indicated in their report on the Company’s financial statements for the fiscal year ended December 31, 2023 that there is “substantial doubt about our ability to continue as a going concern”. A “going concern” opinion could impair our ability to finance our operations through the sale of equity, incurring debt, or other financing alternatives.

Management’s plan to alleviate the substantial doubt about our ability to continue as a going concern include working to improve the Company’s liquidity and capital sources mainly through cash flow from its operations and raise sufficient capital through equity or debt financing, strategic alliances or otherwise. If we are unable to achieve these goals, our business will be jeopardized and we may not be able to continue. If we ceased operations, it is likely that all of our investors will lose their investment.

In the absence of an additional liquidity, our ability to continue to operate will be impaired, and we may not be able to continue as a going concern. Additionally, even if we raise sufficient capital through equity or debt financing, strategic alliances or otherwise or generate additional revenue there can be no assurances that future revenue or capital infusion will be sufficient to enable us to develop our business to a level where it will be profitable or to generate positive cash flows.

We have historically incurred recurring losses and it is uncertain whether we may continue to incur losses in the future.

Due to the sharp rise in market price of raw materials, the lack of operational efficiency of our production facilities and our inability to make bank loan repayment to financial institutions upon maturity, we temporarily suspended our production and normal business operations and we were involved in certain legal proceedings beginning in November 2019. The COVID-19 outbreak and spread further disrupted our business activities during the period from the beginning of 2020 up to May 2020 when we resumed our business operations. Historically, we reported recurring losses of approximately $23.63 million and $0.86 million for the years ended December 31, 2023 and 2022, respectively. On October 31, 2021, we acquired 51% equity interests of Far Ling’s Inc. and 100% equity interests of Bo Ling’s Chinese Restaurant, Inc. This resulted in an increase of $3.1 million and $3.2 million in food service revenue for the years ended December 31, 2022 and 2023, respectively. However, we fully discontinued our petfood manufacturing segment in 2023 and currently our revenue is substantially generated from the restaurant business segment. Our business turnaround currently depends, in part, on our ability to successfully introduce, manage and acquire new restaurants. If we are not able to effectively manage and acquire new restaurants that successfully generate revenue, we may not be able to grow and maintain our business as anticipated. In order to achieve profitability, among other factors, management must successfully execute our growth and restaurant operations in the markets on which we are focused. If we are unable to successfully take necessary steps, we may be unable to sustain or increase our profitability in the future.

2

We discontinued our petfood manufacturing segment and the turnaround of our business depends, in part, on our ability to successfully generate revenue in the restaurant segment.

Due to the sharp rise in market price of raw materials, the lack of operational efficiency of our production facilities and our inability to make bank loan repayments upon maturity, we suspended our production and normal petfood business operations and we were involved in certain legal proceedings beginning in November 2019. The COVID-19 outbreak and spread further disrupted our business activities from the beginning of 2020 up to May 2020 when we resumed our petfood business operations. These factors led to significant decrease in our petfood sales. On October 31, 2021, we acquired 51% equity interests of Far Ling’s Inc and 100% equity interests of Bo Ling’s Chinese Restaurant, Inc. This resulted in an increase of $3.1 million and $3.2 million in food service revenue for the years ended December 31, 2022 and 2023, respectively.

We discontinued our petfood business during the first quarter of 2023 and we fully disposed of Tiandihui because its bankruptcy process concluded and all claims against it were processed by December 27, 2023. Our decision to discontinue our petfood business was driven largely by the following factors: the increase in cost of raw materials required for production; accepting less orders in an attempt to avoid unprofitable orders and customers; decreased demand for sales of petfood; its historical performance and expected business forecasts in the absence of further capital investments and opportunity costs; and lawsuits and the closing of our manufacturing facilities.

Our turnaround depends, in part, on our ability to successfully introduce manage and acquire new restaurants. This, in turn, depends on our ability to predict and respond to evolving consumer trends, demands and preferences. The management and acquisition of restaurants involves considerable costs. If we are not able to effectively manage and acquire new restaurants that successfully generate revenue, we may not be able to grow and maintain our business as anticipated, and our sales may decline and our business, financial condition and results of operations may be materially adversely affected.

We depend on our key personnel, and our business and growth prospects may be severely disrupted if we lose their services.

Our future success depends heavily upon the continued service of our key executives. We rely on their business, industry, financial and capital markets knowledge and experience. If our CEO or CFO became unable or unwilling to continue in their present positions, we may not be able to replace them easily, our business may be significantly disrupted and our financial condition and results of operations may be materially adversely affected.

We do not maintain key man life insurance on any of our senior management or key personnel.

The loss of any one of them would have a material adverse effect on our business and operations. Competition for senior management and our other key personnel is intense and the pool of suitable candidates is limited. We may be unable to locate a suitable replacement for any senior management or key personnel that we lose. In addition, if any member of our senior management or key personnel joins a competitor or forms a competing company, they may compete with us for customers, business partners and other key professionals and staff members of our Company. In addition, we compete for qualified personnel with other companies, and we face competition in attracting skilled personnel and retaining the members of our senior management team. These personnel possess technical and business capabilities which are difficult to replace. There is intense competition for experienced senior management with technical and industry expertise in our industry, and we may not be able to retain our key personnel. Intense competition for these personnel could cause our compensation costs to increase, which could have a material adverse effect on our results of operations. Our future success and ability to grow our business will depend in part on the continued service of these individuals and our ability to identify, hire and retain additional qualified personnel. If we are unable to attract and retain qualified employees, we may be unable to meet our business and financial goals.

While we are not aware of any data breach in the past, cyber-attacks, computer viruses or any future failure to adequately maintain security and prevent unauthorized access to electronic and other confidential information could result in a data breach which could materially adversely affect our reputation, financial condition and operating results.

As part of business operations, we collect, process, store and transmit our employees, business partners and other third party data. Our customers, business partners and employees expect we adequately safeguard and protect their sensitive personal and business information. We may experience cyber-attacks and other security incidents of varying degrees from time to time, and we may incur significant costs in protecting against or remediating such incidents. In addition, we are subject to a variety of laws and regulations in the PRC and other countries relating to cybersecurity and data protection. Security breaches or unauthorized access to confidential information could also expose us to liability related to the loss of the information, time-consuming and expensive litigation and negative publicity. If security measures are breached because of third-party action, employee error, malfeasance or otherwise, or if design flaws in our technology infrastructure are exposed and exploited, our relationships with customers and cooperation partners could be severely damaged. Affected third parties or government authorities could initiate legal or regulatory actions against us in connection with any actual or perceived security breaches or improper access to or disclosure of data, which could cause us to incur significant expense and liability, and our business and operations could be materially and adversely affected.

3

Risks Related to the Restaurant Segment

Our restaurant base is geographically concentrated in Missouri, and we could be negatively affected by conditions specific to this state.

Bo Lings is located in Missouri. Adverse changes in demographic, unemployment, economic, regulatory or weather conditions in Missouri have had, and may continue to have, material adverse effects on our business, financial condition or results of operations. As a result of our concentration in this market, we have been, and in the future may be, disproportionately affected by adverse conditions in this market compared to other chain restaurants with a broader national footprint.

Failure to preserve the value and relevance of our brand could have an adverse impact on our financial results.

To be successful in the future, we believe we must preserve, enhance and leverage the value of our brand, including corporate purpose, mission and values. Brand value is based in part on consumer perceptions, which are affected by a variety of factors, including the nutritional content and preparation of our food, the ingredients we use, the manner in which we source commodities and our general business practices, including the people practices at Bo Lings. Consumer acceptance of our offerings is subject to change for a variety of reasons, and some changes can occur rapidly. For example, nutritional, health, environmental and other scientific studies and conclusions, which constantly evolve and may have contradictory implications, drive popular opinion, litigation and regulation (including initiatives intended to drive consumer behavior) in ways that affect the “informal eating out” (“IEO”) segment or perceptions of our brand, generally or relative to available alternatives. Our business could also be impacted by business incidents or practices, whether actual or perceived, particularly if they receive considerable publicity or result in litigation, as well as by our position or perceived lack of position on environmental, social responsibility, public policy, geopolitical and similar matters. Consumer perceptions may also be affected by adverse commentary from third parties, including through social media or conventional media outlets, regarding the IEO segment or our brand, culture, operations, suppliers or franchisees. If we are unsuccessful in addressing adverse commentary or perceptions, whether or not accurate, our brand and financial results may suffer.

If we do not anticipate and address evolving consumer preferences and effectively execute our pricing, promotional and marketing plans, our business could suffer.

Our continued success depends on our ability to build upon our historic strengths and competitive advantages. In order to do so, we need to anticipate and respond effectively to continuously shifting consumer demographics and trends in food sourcing, food preparation, food offerings, and consumer behavior and preferences, including with respect to environmental and social responsibility matters, in the IEO segment. If we are not able to predict, or quickly and effectively respond to, these changes, or if our competitors predict or respond more effectively, our financial results could be adversely impacted.

Our ability to build upon our strengths and advantages also depends on the impact of our pricing, promotional and marketing plans, and the ability to adjust these plans to respond quickly and effectively to evolving customer behavior and preferences, as well as shifting economic and competitive conditions. Existing or future pricing strategies and marketing plans, as well as the value proposition they represent, are expected to continue to be important components of our business strategy. However, they may not be successful, or may not be as successful as the efforts of our competitors, which could negatively impact sales, guest counts and market share.

We face intense competition in our market, which could hurt our business.

We compete primarily in the IEO segment, which is highly competitive. We also face sustained, intense competition from traditional, fast casual and other competitors, which may include many non-traditional market participants such as convenience stores, grocery stores, coffee shops and online retailers. We expect our environment to continue to be highly competitive, and our results in any particular reporting period may be impacted by a contracting IEO segment or by new or continuing actions, product offerings or consolidation of our competitors and third-party partners, which may have a short- or long-term impact on our results.

We compete on the basis of product choice, quality, affordability, service and location. In particular, we believe our ability to compete successfully in the current market environment depends on our ability to improve existing products, successfully develop and introduce new products, price our products appropriately, deliver a relevant customer experience, manage the complexity of our restaurant operations, manage our investments in technology and modernization, and respond effectively to our competitors’ actions or offerings or to unforeseen disruptive actions. There can be no assurance these strategies will be effective, and some strategies may be effective at improving some metrics while adversely affecting other metrics, which could have the overall effect of harming our business.

Food safety and foodborne illness concerns may have an adverse effect on our reputation and business.

Foodborne illnesses, such as E. coli, hepatitis A and salmonella, may occur within our system from time to time. In addition, food safety issues such as food tampering, contamination and adulteration occur or may occur within our system from time to time. Any report or publicity linking us, our competitors, our restaurant, to instances of foodborne illness or food safety issues could adversely affect our brand and reputation as well as our revenues and profits and possibly lead to product liability claims, litigation and damages. If a customer of our restaurant becomes ill from foodborne illnesses or as a result of food safety issues, it may be temporarily closed, which would decrease our revenues.

4

Risks Related to Doing Business in China

Because of our corporate structure, we as well as the investors are subject to unique risks due to uncertainty of the interpretation and the application of the PRC laws and regulations, including but not limited to limitation regulatory review of overseas listing of PRC companies through a special purpose vehicle. We are also subject to the risks of uncertainty about any future actions of the PRC government in this regard. We may also be subject to sanctions imposed by PRC regulatory agencies including Chinese Securities Regulatory Commission (“CSRC”) if we fail to comply with their rules and regulations. Adverse changes in political, economic and other policies of the Chinese government could have a material adverse effect on the overall economic growth of China, which could materially and adversely affect the growth of our business and our competitive position.

Our PRC subsidiaries are located in China. Accordingly, our business, financial condition, results of operations and prospects are affected significantly by economic, political and legal developments in China. China’s economy differs from the economies of most developed countries in many respects, including with respect to the amount of government involvement, level of development, growth rate, control of foreign exchange, and allocation of resources. The PRC government exercises significant control over China’s economic growth through strategical allocation of resources, controlling the payment of foreign currency-denominated obligations, setting monetary policy, and providing preferential treatment to particular industries or companies. While the Chinese economy has experienced significant growth in the past decades, growth has been uneven, both geographically and among various sectors of the economy. The growth of the Chinese economy may not continue at a rate experienced in the past, and the impact of COVID-19 on the Chinese economy may continue. Any prolonged slowdown in the Chinese economy may reduce the demand for our services and materially and adversely affect our business and results of operations. Furthermore, any adverse change in the economic conditions in China, in policies of the PRC government or in laws and regulations in China could have a material adverse effect on the overall economic growth of China and market demand for our products and services. Such developments could adversely affect our businesses, lead to reduction in demand for our products and services and adversely affect our competitive position.

Uncertainties with respect to the PRC legal system could have a material adverse effect on us.

The PRC legal system is based on written statutes. Prior court decisions may be cited for reference but have limited precedential value. We conduct some of our business through our PRC Subsidiaries, and therefore these subsidiaries are generally subject to laws and regulations applicable to foreign investment in China. However, since these laws and regulations are relatively new and the PRC legal system continues to rapidly evolve, the interpretations of many laws, regulations and rules are not always uniform and enforcement of these laws, regulations and rules involves uncertainties, which may limit legal protections available to us. Recently, the General Office of the Central Committee of the Communist Party of China and the General Office of the State Council jointly issued the “Opinions on Severely Cracking Down on Illegal Securities Activities According to Law,” or the Opinions, which was made available to the public on July 6, 2021. The Opinions emphasized the need to strengthen the administration over illegal securities activities, and the need to strengthen the supervision over overseas listings by Chinese companies. Effective measures, such as promoting the construction of relevant regulatory systems will be taken to deal with the risks and incidents of China-concept overseas listed companies, and cybersecurity and data privacy protection requirements, etc. The Opinions and any related implementing rules to be enacted may subject us to compliance requirement in the future. In addition, some regulatory requirements issued by certain PRC government authorities may not be consistently applied by other government authorities (including local government authorities), thus making strict compliance with all regulatory requirements impractical, or in some circumstances impossible. For example, we may have to resort to administrative and court proceedings to enforce the legal protection that we enjoy either by law or contract. However, since PRC administrative and court authorities have discretion in interpreting and implementing statutory and contractual terms, it may be more difficult to predict the outcome of administrative and court proceedings and the level of legal protection we enjoy than in more developed legal systems. These uncertainties may impede our ability to enforce the contracts we have entered into with our business partners, customers and suppliers. In addition, such uncertainties, including any inability to enforce our contracts, together with any development or interpretation of PRC law that is adverse to us, could materially and adversely affect our business and operations. Furthermore, intellectual property rights and confidentiality protections in China may not be as effective as in the United States or other more developed countries. We cannot predict the effect of future developments in the PRC legal system, including the promulgation of new laws, changes to existing laws or the interpretation or enforcement thereof, or the preemption of local regulations by national laws. These uncertainties could limit the legal protections available to us and other foreign investors, including you. In addition, any litigation in China may be protracted and result in substantial costs and diversion of our resources and management attention.

5

The Chinese government exerts substantial influence over the manner in which we must conduct our business activities and may intervene or influence our operations at any time, which could result in a material change in our operations and the value of our Common Shares.

The Chinese government has exercised and continues to exercise substantial control over virtually every sector of the Chinese economy through regulation and state ownership. Our ability to operate in China may be harmed by changes in its laws and regulations, including those relating to securities regulation, data protection, cybersecurity and mergers and acquisitions and other matters. The central or local governments of these jurisdictions may impose new, stricter regulations or interpretations of existing regulations that would require additional expenditures and efforts on our part to ensure our compliance with such regulations or interpretations.

Government actions in the future could significantly affect economic conditions in China or particular regions thereof and could require us to materially change our operating activities or divest ourselves of any interests we hold in Chinese assets. Our business may be subject to various government and regulatory interference in the provinces in which we operate. We may incur increased costs necessary to comply with existing and newly adopted laws and regulations or penalties for any failure to comply. Our operations could be adversely affected, directly or indirectly, by existing or future laws and regulations relating to our business or industry.

Given recent statements by the Chinese government indicating an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers, any such action could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or become worthless.

Recently, the General Office of the Central Committee of the Communist Party of China and the General Office of the State Council jointly issued the Opinions on Severely Cracking Down on Illegal Securities Activities According to Law, or the Opinions, which was made available to the public on July 6, 2021. The Opinions emphasized the need to strengthen the administration over illegal securities activities, and the need to strengthen the supervision over overseas listings by Chinese companies. Effective measures, such as promoting the construction of relevant regulatory systems, will be taken to deal with the risks and incidents of China-concept overseas listed companies. As of the date of this annual report, we have not received any inquiry, notice, warning, or sanctions from PRC government authorities in connection with the Opinions.

On June 10, 2021, the Standing Committee of the National People’s Congress of China, or the SCNPC, promulgated the PRC Data Security Law, which took effect in September 2021. The PRC Data Security Law imposes data security and privacy obligations on entities and individuals carrying out data activities, and introduces a data classification and hierarchical protection system based on the importance of data in economic and social development, and the degree of harm it will cause to national security, public interests, or legitimate rights and interests of individuals or organizations when such data is tampered with, destroyed, leaked, illegally acquired or used. The PRC Data Security Law also provides for a national security review procedure for data activities that may affect national security and imposes export restrictions on certain data an information.

6

In early July 2021, regulatory authorities in China launched cybersecurity investigations with regard to several China-based companies that are listed in the United States. The Chinese cybersecurity regulator announced on July 2 that it had begun an investigation of Didi Global Inc. (NYSE: DIDI) and two days later ordered that the company’s app be removed from smartphone app stores. On July 5, 2021, the Chinese cybersecurity regulator launched the same investigation on two other Internet platforms, China’s Full Truck Alliance of Full Truck Alliance Co. Ltd. (NYSE: YMM) and Boss of KANZHUN LIMITED (Nasdaq: BZ). On July 24, 2021, the General Office of the Communist Party of China Central Committee and the General Office of the State Council jointly released the Guidelines for Further Easing the Burden of Excessive Homework and Off-campus Tutoring for Students at the Stage of Compulsory Education, pursuant to which foreign investment in such firms via mergers and acquisitions, franchise development, and variable interest entities are banned from this sector.

On November 14, 2021, the Cyberspace Administration of China (“CAC”) released the Regulations on the Network Data Security Management (Draft for Comments), or the Data Security Management Regulations Draft, to solicit public opinion and comments. Pursuant to the Data Security Management Regulations Draft, data processor holding more than one million users/users’ individual information shall be subject to cybersecurity review before listing abroad. Data processing activities refers to activities such as the collection, retention, use, processing, transmission, provision, disclosure, or deletion of data. According to the latest amended Cybersecurity Review Measures, which was promulgated on December 28, 2021, and became effective on February 15, 2022 and replace the Cybersecurity Review Measures promulgated on April 13, 2020, an online platform operator holding more than one million users/users’ individual information shall be subject to cybersecurity review before listing abroad. Since the Cybersecurity Review Measures is new, the implementation and interpretation thereof is not yet clear. As of the date of this annual report, we have not been informed by any PRC governmental authority of any requirement that we file for approval.

On August 17, 2021, the State Council promulgated the Regulations on the Protection of the Security of Critical Information Infrastructure, or the Regulations, which took effect on September 1, 2021. The Regulations supplement and specify the provisions on the security of critical information infrastructure as stated in the Cybersecurity Review Measures. The Regulations provide, among others, that protection department of certain industry or sector shall notify the operator of the critical information infrastructure in time after the identification of certain critical information infrastructure.

On August 20, 2021, the SCNPC promulgated the Personal Information Protection Law of the PRC, or the Personal Information Protection Law, which took effect in November 2021. As the first systematic and comprehensive law specifically for the protection of personal information in the PRC, the Personal Information Protection Law provides, among others, that (i) an individual’s consent shall be obtained to use sensitive personal information, such as biometric characteristics and individual location tracking, (ii) personal information operators using sensitive personal information shall notify individuals of the necessity of such use and impact on the individual’s rights, and (iii) where personal information operators reject an individual’s request to exercise his or her rights, the individual may file a lawsuit with a People’s Court. Given that the above mentioned newly promulgated laws, regulations and policies were recently promulgated or issued, and have not yet taken effect (as applicable), their interpretation, application and enforcement are subject to substantial uncertainties.

Draft rules for China-based companies seeking for securities offerings in foreign stock markets was released by the CSRC for public consultation. While such rules have not yet come into effect, the Chinese government may exert more oversight and control over overseas public offerings conducted by China-based issuers, which could significantly limit or completely hinder our ability to offer or continue to offer our Common Shares to investors and could cause the value of our Common Shares to significantly decline or become worthless.

On December 24, 2021, the CSRC and relevant departments of the State Council published the Draft Rules Regarding Overseas Listings, which aim to regulate overseas securities offerings and listings by China-based companies, are available for public consultation. The Draft Rules Regarding Overseas Listing aim to lay out the filing regulation arrangement for both direct and indirect overseas listing and clarify the determination criteria for indirect overseas listing in overseas markers.

7

The Draft Rules Regarding Overseas Listing, among other things, stipulate that, after making initial applications with overseas stock markets for initial public offerings or listings, all China-based companies shall file with the CSRC within three working days. The required filing materials with the CSRC include (without limitation): (i) record-filing reports and related undertakings, (ii) compliance certificates, filing or approval documents from the primary regulator of the applicants’ businesses (if applicable), (iii) security assessment opinions issued by related departments (if applicable), (iv) PRC legal opinions, and (v) prospectus. In addition, overseas offerings and listings may be prohibited for such China-based companies when any of the following applies: (1) if the intended securities offerings and listings are specifically prohibited by the laws, regulations or provision of the PRC; (2) if the intended securities offerings and listings may constitute a threat to, or endanger national security as reviewed and determined by competent authorities under the State Council in accordance with laws; (3) if there are material ownership disputes over applicants’ equity interests, major assets, core technologies, etc.; (4) if, in the past three years, applicants’ domestic enterprises, controlling shareholders or de facto controllers have committed corruption, bribery, embezzlement, misappropriation of property, or other criminal offenses disruptive to the order of the socialist market economy, or are currently under judicial investigation for suspicion of criminal offenses, or are under investigation for suspicion of major violations; (5) if, in the past three years, any directors, supervisors, or senior executives of applicants have been subject to administrative punishments for severe violations, or are currently under judicial investigation for suspicion of criminal offenses, or are under investigation for suspicion of major violations; (6) other circumstances as prescribed by the State Council. The Draft Administrative Provisions further stipulate that a fine between RMB 1 million and RMB 10 million may be imposed if an applicant fails to fulfill the filing requirements with the CSRC or conducts an overseas offering or listing in violation of the Draft Rules Regarding Overseas Listings, and in cases of severe violations, a parallel order to suspend relevant businesses or halt operations for rectification may be issued, and relevant business permits or operational license revoked.

The Draft Rules Regarding Overseas Listings, if enacted, may subject us to additional compliance requirements in the future, and though we believe that none of the situations that would clearly prohibit overseas listing and offering applies to us, we cannot assure you that we will be able to receive clearance of such filing requirements in a timely manner, or at all. There is also the possibility that we may not be able to obtain or maintain such approval or that we inadvertently concluded that such approval was not required. If prior CSRC approval was required while we inadvertently concluded that such approval was not required or if applicable laws and regulations or the interpretation of such were modified to require us to obtain the CSRC approval in the future, we may face regulatory actions or other sanctions from the CSRC or other Chinese regulatory authorities. These authorities may impose fines and penalties upon our operations in China, limit our operating privileges in China, delay or restrict the repatriation of the proceeds from offerings into China, or take other actions that could have a material adverse effect upon our business, financial condition, results of operations, reputation and prospects, as well as the trading price of our Common Shares. Any failure of us to fully comply with new regulatory requirements may significantly limit or completely hinder our ability to offer or continue to offer the Common Shares, cause significant disruption to our business operations, severely damage our reputation, materially and adversely affect our financial condition and results of operations, and cause the Common Shares to significantly decline in value or become worthless.

CSRC and other Chinese government agencies may exert more oversight and control over offerings that are conducted overseas and foreign investment in China-based issuers, especially those in the technology field. Additional compliance procedures may be required in connection offerings, and, if required, we cannot predict whether we will be able to obtain such approval. If we are required to obtain PRC governmental permissions to commence the sale of securities, we will not commence offerings until we obtain such permissions. As a result, we face uncertainty about future actions by the PRC government that could significantly affect our ability to offer or continue to offer securities to investors and cause the value of our securities to significantly decline or be worthless.

On July 6, 2021, the General Office of the Communist Party of China Central Committee and the General Office of the State Council jointly issued a document to crack down on illegal activities in the securities market and promote the high-quality development of the capital market, which, among other things, requires the relevant governmental authorities to strengthen cross-border oversight of law-enforcement and judicial cooperation, to enhance supervision over China-based companies listed overseas, and to establish and improve the system of extraterritorial application of the PRC securities laws. Since this document is relatively new, uncertainties still exist in relation to how soon legislative or administrative regulation making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated, if any, and the potential impact such modified or new laws and regulations will have on our future business, results of operations, and the value of our securities.

8

Further, Chinese government continues to exert more oversight and control over Chinese technology firms. On July 2, 2021, Chinese cybersecurity regulator announced, that it had begun an investigation of Didi Global Inc. (NYSE: DIDI) and two days later ordered that the company’s application be removed from smartphone application stores. On July 5, 2021, the Chinese cybersecurity regulator launched the same investigation on two other Internet platforms, China’s Full Truck Alliance of Full Truck Alliance Co. Ltd. (NYSE: YMM) and Boss of KANZHUN LIMITED (Nasdaq: BZ).

Therefore, CSRC and other Chinese government agencies may exert more oversight and control over offerings that are conducted overseas and foreign investment in China-based issuers, especially those in the technology field. As of the date of this annual report, we have not received any requirement to obtain approval of CSRC to list on U.S. exchanges. Further, however, given the current regulatory environment in the PRC, we and our PRC subsidiaries are still subject to the uncertainty of interpretation and enforcement of the rules and regulations in the PRC, which can change quickly with little advance notice, and any future actions of the PRC authorities, additional compliance procedures may be required in connection with this offering and our business operations. As a result, we face uncertainty about future actions by the PRC government that could significantly affect our ability to offer or continue to offer securities to investors and cause the value of our Common Shares to significantly decline or be worthless.

We or our PRC subsidiaries may be subject to PRC laws relating to the use, sharing, retention, security and transfer of confidential and private information, such as personal information and other data. These laws continue to develop, and the PRC government may adopt other rules and restrictions in the future. Non-compliance could result in penalties or other significant legal liabilities.

The Cybersecurity Law, which was adopted by the National People’s Congress on November 7, 2016 and came into force on June 1, 2017, and the Cybersecurity Review Measures, or the “Review Measures,” which were promulgated on April 13, 2020, amended on December 28, 2021 and became effective on February 15, 2022, provide that personal information and important data collected and generated by a critical information infrastructure operator in the course of its operations in China must be stored in China, and if a critical information infrastructure operator purchases internet products and services that affect or may affect national security, it should be subject to cybersecurity review by the CAC. In addition, a cybersecurity review is required where critical information infrastructure operators, or the “CIIOs,” purchase network-related products and services, which products and services affect or may affect national security. Due to the lack of further interpretations, the exact scope of what constitute a “CIIO” remains unclear. Further, the PRC government authorities may have wide discretion in the interpretation and enforcement of these laws. In addition, Review Measures stipulates that an online platform operator holding more than one million users/users’ individual information shall be subject to cybersecurity review before listing abroad. Cybersecurity Review Measures does not provide a definition of “online platform operator”, therefore, we cannot assure you that we will not be deemed as an “online platform operator”. As of the date of this annual report, we or our PRC subsidiaries have not received any notice from any authorities identifying us as a CIIO or requiring us to undertake a cybersecurity review by the CAC. Further, as of the date of this annual report, we or our PRC subsidiaries have not been subject to any penalties, fines, suspensions, investigations from any competent authorities for violation of the regulations or policies that have been issued by the CAC. On June 10, 2021, the Standing Committee of the National People’s Congress promulgated the Data Security Law which took effect on September 1, 2021. The Data Security Law requires that data shall not be collected by theft or other illegal means, and it also provides that a data classification and hierarchical protection system shall be established. The data classification and hierarchical protection system protects data according to its importance in economic and social development, and the damages it may cause to national security, public interests, or the legitimate rights and interests of individuals and organizations if the data is falsified, damaged, disclosed, illegally obtained or illegally used, which protection system is expected to be built by the state for data security in the near future. On November 14, 2021, CAC published the Regulations on the Network Data Security Management (Draft for Comments), or the Data Security Management Regulations Draft to solicit public opinion and comments. Under the Data Security Management Regulations Draft, which provides that an overseas initial public offering to be conducted by a data processor processing the personal information of more than one million individuals shall apply for a cybersecurity review. Data processor means an individual or organization that independently makes decisions on the purpose and manner of processing in data processing activities, and data processing activities refers to activities such as the collection, retention, use, processing, transmission, provision, disclosure, or deletion of data. We may be deemed as a data processor under the Data Security Management Regulations Draft. However, the Data Security Management Regulations Draft has not been formally adopted. It is uncertain when the final regulation will be issued and take effect, how it will be enacted, interpreted or implemented, and whether it will affect us. There remains uncertainty as to how the Review Measures and the Data Security Management Regulations Draft will be interpreted or implemented and whether the PRC regulatory agencies, including the CAC, may adopt new laws, regulations, rules, or detailed implementation and interpretation related to the Review Measures and the Data Security Regulations Draft. If any such new laws, regulations, rules, or implementation and interpretation come into effect, we and our PRC subsidiaries expect to take all reasonable measures and actions to comply. We cannot assure you that PRC regulatory agencies, including the CAC, would take the same view as we do, and there is no assurance that we and our PRC subsidiaries can fully or timely comply with such laws should they be deemed applicable to our operations. Any cybersecurity review could also result in negative publicity with respect to our company and diversion of our managerial and financial resources. There is no certainty as to how such review or prescribed actions would impact our operations and we cannot guarantee that any clearance can be obtained or any actions that may be required for our continued listing on the Nasdaq capital market and the offering as well can be taken in a timely manner, or at all.

9

In addition, according to the Personal Information Protection Law, where the purpose of the activity is to provide a product or service to that natural person located within China, such activity shall comply with the Personal Information Protection Law. Further, the Data Security Law provides that where any data handling activity carried out outside of the territory of China harms the national security, public interests, or the legitimate rights and interests of citizens or organizations of China, legal liability shall be investigated in accordance with such law. However, the Personal Information Protection Law and the Data Security Law are relatively new, there remains uncertainty as to how the laws will be interpreted or implemented and whether the PRC regulatory agencies, including the CAC, may adopt new laws, regulations, rules, or detailed implementation and interpretation related to the two laws.

The regulatory requirements with respect to cybersecurity and data privacy are constantly evolving and can be subject to varying interpretations, and significant changes, resulting in uncertainties about the scope of our responsibilities in that regard. Failure to comply with the cybersecurity and data privacy requirements in a timely manner, or at all, may subject us to government enforcement actions and investigations, fines, penalties, suspension, or disruption of our PRC subsidiaries’ operations, among other things.

We may be liable for improper use or appropriation of personal information provided by our customers.

Our business can potentially involve collecting and retaining certain internal and customer data. We also maintain information about various aspects of our operations as well as regarding our employees. The integrity and protection of our customer, employee and company data is critical to our business. Our customers and employees expect that we will adequately protect their personal information. We are required by applicable laws to keep strictly confidential the personal information that we collect, and to take adequate security measures to safeguard such information.

The PRC Criminal Law, as amended by its Amendment 7 (effective on February 28, 2009) and Amendment 9 (effective on November 1, 2015), prohibits institutions, companies, and their employees from selling or otherwise illegally disclosing a citizen’s personal information obtained in performing duties or providing services or obtaining such information through theft or other illegal ways. On November 7, 2016, the SCNPC issued the Cyber Security Law of the PRC, or Cyber Security Law, which became effective on June 1, 2017. Pursuant to the Cyber Security Law, network operators must not, without users’ consent, collect their personal information, and may only collect users’ personal information necessary to provide their services. Providers are also obliged to provide security maintenance for their products and services and shall comply with provisions regarding the protection of personal information as stipulated under the relevant laws and regulations.

The Civil Code of the PRC (issued by the PRC National People’s Congress on May 28, 2020 and effective from January 1, 2021) provides legal basis for privacy and personal information infringement claims under the Chinese civil laws. PRC regulators, including the CAC, the Ministry of Industry and Information Technology, or MIIT, and the Ministry of Public Security, have been increasingly focused on regulation in data security and data protection.

The PRC regulatory requirements regarding cybersecurity are evolving. For instance, various regulatory bodies in China, including the CAC, the Ministry of Public Security and the State Administration for Market Regulation, or the SAMR (formerly known as State Administration for Industry and Commerce, or the SAIC), have enforced data privacy and protection laws and regulations with varying and evolving standards and interpretations. In April 2020, the Chinese government promulgated Cybersecurity Review Measures, which came into effect on June 1, 2020, was amended on December 28, 2021, and became effective on February 15, 2022. According to the Cybersecurity Review Measures, (i) operators of critical information infrastructure must pass a cybersecurity review when purchasing network products and services which do or may affect national security; (ii) online platform operators who are engaged in data processing are also subject to the regulatory scope; (iii) the CSRC is included as one of the regulatory authorities for purposes of jointly establishing the state cybersecurity review working mechanism; (iv) online platform operators holding more than one million users/users’ individual information and seeking a listing outside China shall file for cybersecurity review; and (v) the risks of core data, material data or large amounts of personal information being stolen, leaked, destroyed, damaged, illegally used or illegally transmitted to overseas parties and the risks of critical information infrastructure, core data, material data or large amounts of personal information being influenced, controlled or used maliciously shall be collectively taken into consideration during the cybersecurity review process.

Certain internet platforms in China have been reportedly subject to heightened regulatory scrutiny in relation to cybersecurity matters. As of the date of this prospectus supplement, we and our PRC subsidiaries have not been informed by any PRC governmental authority of any requirement that we file for a cybersecurity review. However, if any of us is deemed to be a critical information infrastructure operator or a company that is engaged in data processing and holds personal information of more than one million users, we could be subject to PRC cybersecurity review.

10

As of the date hereof, we are of the view that we and our PRC subsidiaries are in compliance with the applicable PRC laws and regulations governing the data privacy and personal information in all material respects, including the data privacy and personal information requirements of the CAC, and we and our PRC subsidiaries have not received any complaints from any third party, or been investigated or punished by any PRC competent authority in relation to data privacy and personal information protection. However, as there remains significant uncertainty in the interpretation and enforcement of relevant PRC cybersecurity laws and regulations, we or our PRC subsidiaries could be subject to cybersecurity review, and if so, we may not be able to pass such review. In addition, we or our PRC subsidiaries could become subject to enhanced cybersecurity review or investigations launched by PRC regulators in the future. Any failure or delay in the completion of the cybersecurity review procedures or any other non-compliance with the related laws and regulations may result in fines or other penalties, including suspension of business, website closure, removal of our app from the relevant app stores, and revocation of prerequisite licenses, as well as reputational damage or legal proceedings or actions against us, which may have material adverse effect on our business, financial condition or results of operations.

On June 10, 2021, the SCNPC promulgated the PRC Data Security Law, which took effect in September 2021. The PRC Data Security Law imposes data security and privacy obligations on entities and individuals carrying out data activities, and introduces a data classification and hierarchical protection system based on the importance of data in economic and social development, and the degree of harm it will cause to national security, public interests, or legitimate rights and interests of individuals or organizations when such data is tampered with, destroyed, leaked, illegally acquired or used. The PRC Data Security Law also provides for a national security review procedure for data activities that may affect national security and imposes export restrictions on certain data an information.

As uncertainties remain regarding the interpretation and implementation of these laws and regulations, we cannot assure you that we and our PRC subsidiaries will comply with such regulations in all respects and we or our PRC subsidiaries may be ordered to rectify or terminate any actions that are deemed illegal by regulatory authorities. We or our PRC subsidiaries may also become subject to fines and/or other sanctions which may have material adverse effect on our business, operations and financial condition.

While we and our PRC subsidiaries take various measures to comply with all applicable data privacy and protection laws and regulations, the current security measures and those of our third-party service providers may not always be adequate for the protection of our customer, employee or company data. We or our PRC subsidiaries may be a target for computer hackers, foreign governments or cyber terrorists in the future.

Unauthorized access to our proprietary internal and customer data may be obtained through break-ins, sabotage, breach of our secure network by an unauthorized party, computer viruses, computer denial-of-service attacks, employee theft or misuse, breach of the security of the networks of our third-party service providers, or other misconduct. Because the techniques used by computer programmers who may attempt to penetrate and sabotage our proprietary internal and customer data change frequently and may not be recognized until launched against a target, we may be unable to anticipate these techniques.

Unauthorized access to our proprietary internal and customer data may also be obtained through inadequate use of security controls. Any of such incidents may harm our reputation and adversely affect our business and results of operations. In addition, we may be subject to negative publicity about our security and privacy policies, systems, or measurements. Any failure to prevent or mitigate security breaches, cyber-attacks or other unauthorized access to our systems or disclosure of our customers’ data, including their personal information, could result in loss or misuse of such data, interruptions to our service system, diminished customer experience, loss of customer confidence and trust, impairment of our technology infrastructure, and harm our reputation and business, resulting in significant legal and financial exposure and potential lawsuits.

Since our operations and some of our assets are located in the PRC, shareholders may find it difficult to enforce a U.S. judgment against the assets of our company, our directors and executive officers.

Our operations and some assets are located in the PRC. In addition, most of our executive officers and directors are non-residents of the U.S., and substantially all the assets of such persons are located outside the U.S. As a result, it could be difficult for investors to effect service of process in the U.S., or to enforce a judgment obtained in the U.S. against us or any of these persons.

11

We may be subject to PRC regulatory limitations on merger and acquisition (M&A) activities.