UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number (811-23226)

Listed Funds Trust

(Exact name of registrant as specified in charter)

615 East Michigan Street

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

Kent P. Barnes, Secretary

Listed Funds Trust

c/o U.S. Bancorp Fund Services, LLC

777 East Wisconsin Avenue, 10th Floor

Milwaukee, WI 53202

(Name and address of agent for service)

(414) 765-6511

Registrant's telephone number, including area code

Date of fiscal year end: July 31

Date of reporting period: July 31, 2022

Item 1. Reports to Stockholders.

(a)

AAF First Priority CLO Bond ETF

(AAA)

ANNUAL REPORT

July 31, 2022

AAF First Priority CLO Bond ETF

Table of Contents

Shareholder Letter (Unaudited) |

2 |

Performance Overview (Unaudited) |

3 |

Schedule of Investments |

4 |

Statement of Assets and Liabilities |

6 |

Statement of Operations |

7 |

Statements of Changes in Net Assets |

8 |

Financial Highlights |

9 |

Notes to Financial Statements |

10 |

Report of Independent Registered Public Accounting Firm |

17 |

Board Consideration and Approval of Continuation of Advisory Agreement (Unaudited) |

18 |

Trustees and Officers of the Trust (Unaudited) |

20 |

Shareholder Expense Example (Unaudited) |

22 |

Supplemental Information (Unaudited) |

23 |

Review of Liquidity Risk Management Program (Unaudited) |

24 |

Privacy Policy (Unaudited) |

25 |

1

AAF First Priority CLO Bond ETF

Shareholder Letter

July 31, 2022 (Unaudited)

Dear Shareholders,

On behalf of the entire team, we want to express our appreciation for the confidence you have placed in the AAF First Priority CLO Bond ETF (“AAA” or the “Fund”). The following information pertains to the fiscal year of August 1, 2021 through July 31, 2022 (the “current fiscal period”).

The Fund is an actively managed exchange-traded fund (“ETF”) that pursues its investment objective by investing in AAA rated first priority debt tranches of U.S. dollar-dominated collateralized loan obligations (“CLOs”). The Fund is actively managed and does not seek to track the performance of any particular index. The Fund seeks capital preservation and income.

The Fund had negative performance during the fiscal year ended on July 31, 2022. Total return at NAV for AAA was a negative 1.60% and the total return at market price was a negative 1.73%.

Positive impact to performance was derived from 3 sources; a) Income derived from interest paid on CLO bonds net of management fees (“Distributable Income”), b) principal appreciation, and c) the market price premium or discount to NAV. Income derived from interest paid on CLO bonds net of management fees contributed 1.31% to the Fund’s total return. Principal depreciation decreased the Fund’s NAV by 2.91%. The market price premium or discount to NAV decreased the Fund’s total return by 0.13%.

NAV Total Return (-1.60%) = Distributed Income (1.31%) + Principal Depreciation (-2.91%).

Market Price Total Return (-1.73%) = Distributed Income (1.31%) + Principal Depreciation (-2.91%) + the Market Price Premium or Discount (-0.13%).

Upon its launch, AAA was one of the first CLO ETFs on the market. The Fund commenced operations on September 8, 2020, with outstanding shares of 200,000. As of July 31, 2022, the Fund’s shares outstanding were 300,000.

We appreciate your investment in AAA.

Sincerely,

Peter Coppa,

Founder and Managing Partner

Alternative Access Funds, Adviser to the Fund

2

AAF First Priority CLO Bond ETF

Performance Overview

July 31, 2022 (Unaudited)

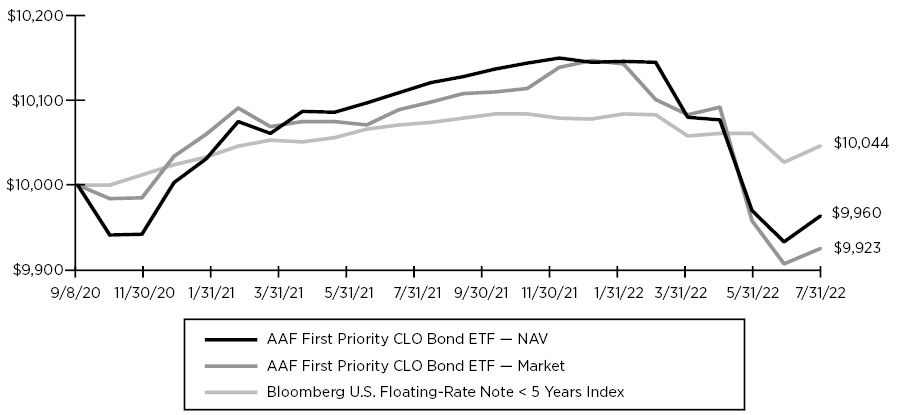

Hypothetical Growth of $10,000 Investment

(Since Commencement through 7/31/2022)

AVERAGE ANNUAL TOTAL RETURN FOR THE PERIODS ENDED JULY 31, 2022 |

||

Total Returns |

One Year Return |

Since |

AAF First Priority CLO Bond ETF —NAV |

-1.60% |

-0.21% |

AAF First Priority CLO Bond ETF —Market |

-1.73% |

-0.41% |

Bloomberg U.S. Floating-Rate Note < 5 Years Index |

-0.30% |

0.23% |

|

1 |

The Fund commenced operations on September 8, 2020. |

The performance data quoted represents past performance. Past performance does not guarantee future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. For the most recent month-end performance, please call (917) 535-5737. You cannot invest directly in an index. Shares are bought and sold at market price (closing price), not net asset value (“NAV”), and are not individually redeemed from the Fund. Market performance is determined using the bid/ask midpoint at 4:00 p.m. Eastern time when the NAV is typically calculated. Brokerage commissions will reduce returns. Returns shown include the reinvestment of all dividends and distribution. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Bloomberg U.S. Floating-Rate Note < 5 Years Index measures the performance of USD denominated, investment-grade, floating-rate notes across corporate and government-related sectors. It is not possible to invest directly in an index.

3

AAF First Priority CLO Bond ETF

Schedule of Investments

July 31, 2022

|

Principal |

Value |

||||||

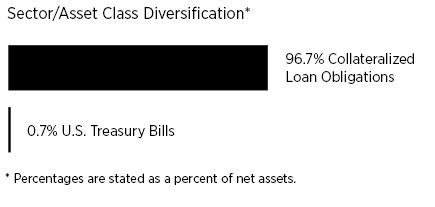

COLLATERALIZED LOAN OBLIGATIONS — 96.7% (a)(b)(c) |

||||||||

Cayman Islands — 96.7% (d) |

||||||||

AIMCO CLO |

||||||||

Series 2017-AA AR, 3.760% (3 Month LIBOR USD + 1.050%, 1.050% Floor), 4/20/2034 |

$ | 350,000 | $ | 335,782 | ||||

AMMC CLO 18, Ltd. |

||||||||

Series 2016-18A AR, 2.631% (3 Month LIBOR USD + 1.100%, 0.000% Floor), 5/27/2031 |

248,783 | 243,794 | ||||||

Atrium XII LLC |

||||||||

Series 12A AR, 3.589% (3 Month LIBOR USD + 0.830%, 0.000% Floor), 4/22/2027 |

210,509 | 206,115 | ||||||

Bain Capital Credit CLO |

||||||||

Series 2018-1A A1, 3.743% (3 Month LIBOR USD + 0.960%, 0.000% Floor), 4/23/2031 |

250,000 | 245,142 | ||||||

Barings CLO, Ltd. |

||||||||

Series 2015-2A AR, 3.900% (3 Month LIBOR USD + 1.190%, 0.000% Floor), 10/21/2030 |

300,000 | 296,252 | ||||||

Battalion CLO XX, Ltd. |

||||||||

Series 2021-20A A, 3.692% (3 Month LIBOR USD + 1.180%, 1.180% Floor), 7/17/2034 |

250,000 | 242,017 | ||||||

Burnham Park CLO, Ltd. |

||||||||

Series 2016-1A AR, 3.860% (3 Month LIBOR USD + 1.150%, 1.150% Floor), 10/22/2029 |

348,339 | 344,186 | ||||||

Cayuga Park CLO, Ltd. |

||||||||

Series 2020-1A AR, 3.860% (3 Month LIBOR USD + 1.120%, 1.120% Floor), 7/17/2034 |

375,000 | 366,442 | ||||||

Cedar Funding VII CLO, Ltd. |

||||||||

Series 2018-7A A1, 3.710% (3 Month LIBOR USD + 1.000%, 1.000% Floor), 1/21/2031 |

375,000 | 368,712 | ||||||

CIFC Funding, Ltd. |

||||||||

Series 2014-4RA A1AR, 3.910% (3 Month LIBOR USD + 1.170%, 1.170% Floor), 1/17/2035 |

$ | 250,000 | $ | 242,217 | ||||

Series 2021-4A A, 3.562% (3 Month LIBOR USD + 1.050%, 1.050% Floor), 7/15/2033 |

290,000 | 281,896 | ||||||

Elmwood CLO IV, Ltd. |

||||||||

Series 2020-1A A, 3.752% (3 Month LIBOR USD + 1.240%, 1.240% Floor), 4/15/2033 |

250,000 | 245,144 | ||||||

Generate CLO, Ltd. |

||||||||

Series 4A A1R, 3.800% (3 Month LIBOR USD + 1.090%, 0.000% Floor), 4/20/2032 |

375,000 | 368,271 | ||||||

LCM XIX, Ltd. |

||||||||

Series 19A AR, 3.752% (3 Month LIBOR USD + 1.240%, 1.240% Floor), 7/15/2027 |

72,389 | 71,928 | ||||||

LCM XVIII, Ltd. |

||||||||

Series 18A A1R, 3.730% (3 Month LIBOR USD + 1.020%, 0.000% Floor), 7/21/2031 |

375,000 | 368,636 | ||||||

LCM XX, Ltd. |

||||||||

Series 20A AR, 3.750% (3 Month LIBOR USD + 1.040%, 0.000% Floor), 10/20/2027 |

137,575 | 136,103 | ||||||

Magnetite XII, Ltd. |

||||||||

Series 2015-12A ARR, 3.612% (3 Month LIBOR USD + 1.100%, 0.000% Floor), 10/15/2031 |

375,000 | 368,645 | ||||||

Palmer Square CLO, Ltd. |

||||||||

Series 2014-1A A1R2, 3.870% (3 Month LIBOR USD + 1.130%, 1.130% Floor), 1/17/2031 |

250,000 | 245,897 | ||||||

Recette CLO, Ltd. |

||||||||

Series 2015-1A ARR, 3.790% (3 Month LIBOR USD + 1.080%, 0.000% Floor), 4/20/2034 |

250,000 | 241,010 | ||||||

Rockford Tower CLO, Ltd. |

||||||||

Series 2021-1A A1, 3.880% (3 Month LIBOR USD + 1.170%, 1.170% Floor), 7/20/2034 |

300,000 | 289,510 | ||||||

Shackleton CLO, Ltd. |

||||||||

Series 2013-4RA A1A, 3.455% (3 Month LIBOR USD + 1.000%, 1.000% Floor), 4/14/2031 |

350,000 | 342,008 | ||||||

Symphony CLO XXII, Ltd. |

||||||||

Series 2020-22A A1A, 4.030% (3 Month LIBOR USD + 1.290%, 1.290% Floor), 4/18/2033 |

375,000 | 367,803 | ||||||

The accompanying notes are an integral part of the financial statements.

4

AAF First Priority CLO Bond ETF

Schedule of Investments

July 31, 2022 (Continued)

|

Principal |

Value |

||||||

Thompson Park CLO, Ltd. |

||||||||

Series 2021-1A A1, 3.512% (3 Month LIBOR USD + 1.000%, 1.000% Floor), 4/17/2034 |

$ | 250,000 | $ | 241,834 | ||||

TICP CLO IX, Ltd. |

||||||||

Series 2017-9A A, 3.850% (3 Month LIBOR USD + 1.140%, 1.140% Floor), 1/21/2031 |

250,000 | 245,178 | ||||||

Voya CLO, Ltd. |

||||||||

Series 2018-3A A1A, 3.662% (3 Month LIBOR USD + 1.150%, 1.150% Floor), 10/15/2031 |

375,000 | 368,945 | ||||||

TOTAL COLLATERALIZED LOAN OBLIGATIONS (Cost $7,205,201) |

7,073,467 | |||||||

SHORT-TERM INVESTMENTS — 0.7% |

||||||||

U.S. Treasury Bills — 0.7% |

||||||||

2.58%, 11/1/2022 (e) |

56,000 | 55,637 | ||||||

TOTAL SHORT-TERM INVESTMENTS (Cost $55,671) |

55,637 | |||||||

TOTAL INVESTMENTS (Cost $7,260,872) — 97.4% |

7,129,104 | |||||||

Other assets and liabilities, net — 2.6% |

187,604 | |||||||

NET ASSETS — 100.0% |

$ | 7,316,708 | ||||||

Percentages are stated as a percent of net assets.

LIBOR - London Interbank Offered Rate

|

(a) |

To the extent the Fund invests more heavily in particular sectors or asset classes, its performance will be especially sensitive to developments that significantly affect those sectors or asset classes. |

|

(b) |

Variable rate securities. The coupon is based on a reference index and spread. The rate reported is the rate in effect as of July 31, 2022. |

|

(c) |

Securities exempt from registration pursuant to Rule 144A under the Securities Act of 1933, as amended. These securities maybe resold in transactions exempt from registration to qualified institutional investors. The value of these securities total $7,073,467, which represents 96.7% of total net assets. |

|

(d) |

To the extent the Fund invests more heavily in particular countries, its performance will be especially sensitive to developments that significantly affect those countries. |

|

(e) |

The rate shown is the effective yield at period end. |

The accompanying notes are an integral part of the financial statements.

5

AAF First Priority CLO Bond ETF

Statement of Assets and Liabilities

July 31, 2022

Assets |

||||

Investments, at value (cost $7,260,872) |

$ | 7,129,104 | ||

Cash |

178,272 | |||

Interest receivable |

11,231 | |||

Total assets |

7,318,607 | |||

Liabilities |

||||

Payable to Adviser |

1,899 | |||

Total liabilities |

1,899 | |||

Net Assets |

$ | 7,316,708 | ||

Net Assets Consists of: |

||||

Paid-in capital |

$ | 7,565,048 | ||

Total distributable earnings (accumulated losses) |

(248,340 | ) | ||

Net Assets |

$ | 7,316,708 | ||

Shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) |

300,000 | |||

Net Asset Value, redemption price and offering price per share |

$ | 24.39 |

The accompanying notes are an integral part of the financial statements.

6

AAF First Priority CLO Bond ETF

Statement of Operations

For the Year Ended July 31, 2022

Investment Income |

||||

Interest income |

$ | 151,886 | ||

Total investment income |

151,886 | |||

Expenses |

||||

Advisory fees |

24,697 | |||

Total expenses |

24,697 | |||

Net investment income |

127,189 | |||

Realized and Unrealized Gain (Loss) on Investments |

||||

Net realized loss on investments |

(136,062 | ) | ||

Net change in unrealized appreciation/depreciation on investments |

(160,596 | ) | ||

Net realized and unrealized loss on investments |

(296,658 | ) | ||

Net decrease in net assets from operations |

$ | (169,469 | ) |

The accompanying notes are an integral part of the financial statements.

7

AAF First Priority CLO Bond ETF

Statements of Changes in Net Assets

Year Ended |

Period Ended |

|||||||

From Operations |

||||||||

Net investment income |

$ | 127,189 | $ | 96,472 | ||||

Net realized gain (loss) on investments |

(136,062 | ) | 643 | |||||

Net change in unrealized appreciation/depreciation on investments |

(160,596 | ) | 28,828 | |||||

Net increase (decrease) in net assets resulting from operations |

(169,469 | ) | 125,943 | |||||

From Distributions |

||||||||

Distributable earnings |

(118,047 | ) | (86,767 | ) | ||||

Total distributions |

(118,047 | ) | (86,767 | ) | ||||

From Capital Share Transactions |

||||||||

Proceeds from shares sold |

— | 9,980,905 | ||||||

Cost of shares redeemed |

(2,434,390 | ) | — | |||||

Transaction fees (Note 4) |

6,086 | 12,447 | ||||||

Net increase (decrease) in net assets resulting from capital share transactions |

(2,428,304 | ) | 9,993,352 | |||||

Total Increase (Decrease) in Net Assets |

(2,715,820 | ) | 10,032,528 | |||||

Net Assets |

||||||||

Beginning of period |

10,032,528 | — | ||||||

End of period |

$ | 7,316,708 | $ | 10,032,528 | ||||

Changes in Shares Outstanding |

||||||||

Shares outstanding, beginning of period |

400,000 | — | ||||||

Shares sold |

— | 400,000 | ||||||

Shares redeemed |

(100,000 | ) | — | |||||

Shares outstanding, end of period |

300,000 | 400,000 | ||||||

|

(1) |

The Fund commenced operations on September 8, 2020. |

The accompanying notes are an integral part of the financial statements.

8

AAF First Priority CLO Bond ETF

Financial Highlights

For a Share Outstanding Throughout Each Period

Year Ended |

Period Ended |

|||||||

Net Asset Value, Beginning of Period |

$ | 25.08 | $ | 25.00 | ||||

Income from investment operations: |

||||||||

Net investment income(2) |

0.32 | 0.25 | ||||||

Net realized and unrealized gain (loss) on investments |

(0.74 | ) | 0.02 | (7) | ||||

Total from investment operations |

(0.42 | ) | 0.27 | |||||

Less distributions paid: |

||||||||

From net investment income |

(0.29 | ) | (0.22 | ) | ||||

From net realized gains |

(0.00 | )(8) | — | |||||

Total distributions paid |

(0.29 | ) | (0.22 | ) | ||||

Capital share transactions: |

||||||||

Transaction fees (see Note 4) |

0.02 | 0.03 | ||||||

Total transaction fees |

0.02 | 0.03 | ||||||

Net Asset Value, End of Period |

$ | 24.39 | $ | 25.08 | ||||

Total return, at NAV(3)(4) |

(1.60 | )% | 1.21 | % | ||||

Total return, at Market(3)(4) |

(1.73 | )% | 0.98 | % | ||||

Supplemental Data and Ratios: |

||||||||

Net assets, end of period (000’s) |

$ | 7,317 | $ | 10,033 | ||||

Ratio of expenses to average net assets(5) |

0.25 | % | 0.25 | % | ||||

Ratio of net investment income to average net assets(5) |

1.29 | % | 1.11 | % | ||||

Portfolio turnover rate(4)(6) |

73 | % | 34 | % | ||||

|

(1) |

The Fund commenced investment operations on September 8, 2020. |

|

(2) |

Per share net investment income was calculated using average shares outstanding. |

|

(3) |

Total return in the table represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of distributions. |

|

(4) |

Not annualized for periods less than one year. |

|

(5) |

Annualized for periods less than one year. |

|

(6) |

Excludes in-kind transactions associated with creations and redemptions of the Fund. |

|

(7) |

Due to timing of capital share transactions, the per share amount of net realized and unrealized gain (loss) on investments varies from the amounts shown in the Statement of Operations. |

|

(8) |

Amount is less than $(0.005). |

The accompanying notes are an integral part of the financial statements.

9

AAF First Priority CLO Bond ETF

Notes to Financial Statements

July 31, 2022

|

1. |

ORGANIZATION |

AAF First Priority CLO Bond ETF (the “Fund”) is a diversified series of Listed Funds Trust (the “Trust”), formerly Active Weighting Funds ETF Trust. The Trust was organized as a Delaware statutory trust on August 26, 2016, under a Declaration of Trust amended on December 21, 2018, and is registered with the U.S. Securities and Exchange Commission (the “SEC”) as an open-end management investment company under the Investment Company Act of 1940, as amended (the “1940 Act”).

The Fund is an actively-managed exchange-traded fund (“ETF”). The Fund’s objective is to invest, under normal circumstances, at least 80% of its nets assets (plus any borrowings made for investment purposes) in AAA rated first priority debt tranches of U.S. dollar-dominated collateralized loan obligations (“CLOs”). CLOs are trusts that are typically collateralized by a pool of loans, which may include, among others, domestic and foreign senior secured loans, senior unsecured loans and subordinate corporate loans, including loans that may be rated below investment grade or equivalent unrated loans. The Fund may invest in CLOs of any maturity.

At a special meeting held on February 28, 2022, the Board approved an Agreement and Plan of Reorganization providing for the reorganization of the AAF First Priority CLO Bond ETF into AXS First Priority CLO Bond ETF, a newly created ETF series of Investment Managers Series Trust II.

|

2. |

SIGNIFICANT ACCOUNTING POLICIES |

The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, Financial Services — Investment Companies. The Fund prepares its financial statements in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) and follows the significant accounting policies described below.

New Accounting Pronouncements

In March 2020, FASB issued Accounting Standards Update (ASU) 2020-04, Reference Rate Reform (Topic 848) - Facilitation of the Effects of Reference Rate Reform on Financial Reporting. The amendments in ASU 2020-04 provides optional temporary financial reporting relief from the effect of certain types of contract modifications due to the planned discontinuation of LIBOR and other interbank-offered based reference rates as of the end of 2021. ASU 2020-04 is effective for certain reference rate-related contract modifications that occur during the period March 12, 2020 through December 31, 2022. Management is currently evaluating the impact, if any, of applying this ASU.

Use of Estimates

The preparation of the financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from these estimates.

Share Transactions

The net asset value (“NAV”) per share of the Fund will be equal to the Fund’s total assets minus the Fund’s total liabilities divided by the total number of shares outstanding. The NAV that is published will be rounded to the nearest cent. The NAV is determined as of the close of trading (generally, 4:00 p.m. Eastern Time) on each day the New York Stock Exchange (“NYSE”) is open for trading.

Fair Value Measurement

In calculating the NAV, the Fund’s debt securities, including collateralized loan obligations are generally valued using the last available bid prices or current market quotations provided by dealers or prices (including evaluated prices) supplied by approved independent third-party pricing services. Pricing services may use matrix pricing or valuation models that utilize

10

AAF First Priority CLO Bond ETF

Notes to Financial Statements

July 31, 2022 (Continued)

certain inputs and assumptions to derive values. Such valuations are typically categorized as Level 2 in the fair value hierarchy described below. Due to the inherent uncertainty of valuations, fair values may differ slightly from the values that would have been used had an active market existed.

Securities listed on the NASDAQ Stock Market, Inc. are generally valued at the NASDAQ official closing price. Foreign securities will be priced in their local currencies as of the close of their primary exchange or market or as of the time the Fund calculates its NAV on the valuation date, whichever is earlier.

If market quotations are not readily available, or if it is determined that a quotation of a security does not represent fair value, then the security is valued at fair value as determined in good faith by Alternative Access Funds, LLC (“AAF” or “Adviser”), the Fund’s Investment Adviser. using procedures adopted by the Board of Trustees of the Trust (the “Board”). The circumstances in which a security may be fair valued include, among others: the occurrence of events that are significant to a particular issuer, such as mergers, restructurings or defaults; the occurrence of events that are significant to an entire market, such as natural disasters in a particular region or government actions; trading restrictions on securities; thinly traded securities; and market events such as trading halts and early market closings. Due to the inherent uncertainty of valuations, fair values may differ significantly from the values that would have been used had an active market existed. Fair valuation could result in a different NAV than a NAV determined by using market quotations. Such valuations are typically categorized as Level 2 or Level 3 in the fair value hierarchy described below.

FASB ASC Topic 820, Fair Value Measurements and Disclosures (“ASC 820”) defines fair value, establishes a framework for measuring fair value in accordance with U.S. GAAP, and requires disclosure about fair value measurements. It also provides guidance on determining when there has been a significant decrease in the volume and level of activity for an asset or liability, when a transaction is not orderly, and how that information must be incorporated into fair value measurements. Under ASC 820, various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the following hierarchy:

|

● |

Level 1 — Unadjusted quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access. |

|

● |

Level 2 — Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar securities, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data. |

|

● |

Level 3 — Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available; representing the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available. |

The fair value hierarchy gives the highest priority to quoted prices (unadjusted) in active markets for identical assets or liabilities (Level 1) and the lowest priority to unobservable inputs (Level 3).

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

All other securities and investments for which market values are not readily available, including restricted securities, and those securities for which it is inappropriate to determine prices in accordance with the aforementioned procedures, are valued at fair value as determined in good faith under procedures adopted by the Board, although the actual calculations may be done by others. Factors considered in making this determination may include, but are not limited to, information obtained

11

AAF First Priority CLO Bond ETF

Notes to Financial Statements

July 31, 2022 (Continued)

by contacting the issuer, analysts, or the appropriate stock exchange (for exchange-traded securities), analysis of the issuer’s financial statements or other available documents and, if necessary, available information concerning other securities in similar circumstances.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. The hierarchy classification of inputs used to value the Fund’s investments at July 31, 2022, are as follows:

Level 1 |

Level 2 |

Level 3 |

Total |

|||||||||||||

Investments - Assets: |

||||||||||||||||

Collateralized Loan Obligations |

$ | — | $ | 7,073,467 | $ | — | $ | 7,073,467 | ||||||||

U.S. Treasury Bills |

— | 55,637 | — | 55,637 | ||||||||||||

Total Investments - Assets |

$ | — | $ | 7,129,104 | $ | — | $ | 7,129,104 | ||||||||

Security Transactions

Investment transactions are recorded as of the date that the securities are purchased or sold (trade date). Realized gains and losses from the sale or disposition of securities are calculated based on the specific identification basis.

Investment Income

Investments in CLOs may be subject to certain tax provisions that could result in the Fund incurring tax or recognizing income prior to receiving cash distributions related to such income. CLOs that fail to comply with certain U.S. tax disclosure requirements may be subject to withholding requirement that could adversely affect cash flows and investments results. Any unrealized losses the Fund experiences with respect to its CLO investments may be an indication of future realized losses. Investment transactions are recorded on a trade-date basis. Discounts and premiums on fixed income securities purchased are accreted or amortized using the effective interest method. Gain and losses on paydowns of CLOs are reflected in interest income on the Statement of Operations.

Tax Information, Dividends and Distributions to Shareholders and Uncertain Tax Positions

The Fund is treated as a separate entity for Federal income tax purposes. The Fund intends to qualify as a regulated investment company (“RIC”) under Subchapter M of the Internal Revenue Code of 1986, as amended (the “Internal Revenue Code”). To qualify and remain eligible for the special tax treatment accorded to RICs, the Fund must meet certain annual income and quarterly asset diversification requirements and must distribute annually at least 90% of the sum of (i) its investment company taxable income (which includes interest and net short-term capital gains) and (ii) certain net tax-exempt income, if any. If so qualified, the Fund will not be subject to Federal income tax.

Distributions to shareholders are recorded on the ex-dividend date. The Fund generally pays out dividends from net investment income, if any, monthly and distributes its net capital gains, if any, to shareholders at least annually. The Fund may also pay a special distribution at the end of the calendar year to comply with Federal tax requirements. The amount of dividends and distributions from net investment income and net realized capital gains are determined in accordance with Federal income tax regulations, which may differ from U.S. GAAP. These “book/tax” differences are either considered temporary or permanent in nature. To the extent these differences are permanent in nature, such amounts are reclassified within the components of net assets based on their Federal tax basis treatment; temporary differences do not require reclassification. Dividends and distributions which exceed earnings and profit for tax purposes are reported as a tax return of capital.

Management evaluates the Fund’s tax positions to determine if the tax positions taken meet the minimum recognition threshold in connection with accounting for uncertainties in income tax positions taken or expected to be taken for the purposes of measuring and recognizing tax liabilities in the financial statements. Recognition of tax benefits of an uncertain tax position is required only when the position is “more likely than not” to be sustained assuming examination by taxing authorities. Interest and penalties related to income taxes would be recorded as income tax expense. The Fund’s Federal income tax returns are subject to examination by the Internal Revenue Service (the “IRS”) for a period of three fiscal years after they are filed. State and

12

AAF First Priority CLO Bond ETF

Notes to Financial Statements

July 31, 2022 (Continued)

local tax returns may be subject to examination for an additional fiscal year depending on the jurisdiction. As of July 31, 2022, the Fund’s fiscal year end, the Fund had no material uncertain tax positions and did not have a liability for any unrecognized tax benefits. As of July 31, 2022, the Fund’s fiscal year end, the Fund had no examination in progress and management is not aware of any tax positions for which it is reasonably possible that the amounts of unrecognized tax benefits will significantly change in the next twelve months.

The Fund recognized no interest or penalties related to uncertain tax benefits in the 2022 fiscal period. At July 31, 2022, the Fund’s fiscal year end, the tax periods from commencement of operations remained open to examination in the Fund’s major tax jurisdiction.

Indemnification

In the normal course of business, the Fund expects to enter into contracts that contain a variety of representations and warranties and which provide general indemnifications. The Fund’s maximum exposure under these anticipated arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

|

3. |

INVESTMENT ADVISORY AND OTHER AGREEMENTS |

Investment Advisory Agreement

The Trust has entered into an Investment Advisory Agreement (the “Advisory Agreement”) with the Adviser. Under the Advisory Agreement, the Adviser provides a continuous investment program for the Fund’s assets in accordance with its investment objectives, policies and limitations, and oversees the day-to-day operations of the Fund subject to the supervision of the Board, including the Trustees who are not “interested persons” of the Trust as defined in the 1940 Act (the “Independent Trustees”).

Pursuant to the Advisory Agreement between the Trust, on behalf of the Fund, and AAF, the Fund pays a unified management fee to the Adviser, which is calculated daily and paid monthly, at an annual rate of 0.25% of the Fund’s average daily net assets. AAF has agreed to pay all expenses of the Fund except the fee paid to AAF under the Advisory Agreement, interest charges on any borrowings, dividends and other expenses on securities sold short, taxes, brokerage commissions and other expenses incurred in placing orders for the purchase and sale of securities and other investment instruments, acquired fund fees and expenses, accrued deferred tax liability, extraordinary expenses, and distribution (12b-1) fees and expenses (if any).

Distribution Agreement and 12b-1 Plan

Quasar Distributors, LLC (“Quasar” or the “Distributor”), a wholly owned subsidiary of Foreside Financial Group, LLC (“Foreside”), serves as the Fund’s distributor pursuant to a Distribution Agreement. The Distributor receives compensation from the Adviser for certain statutory underwriting services it provides to the Fund. The Distributor enters into agreements with certain broker-dealers and others that will allow those parties to be “Authorized Participants” and to subscribe for and redeem shares of the Fund. The Distributor will not distribute shares in less than whole Creation Units and does not maintain a secondary market in shares.

The Board has adopted a Distribution and Service Plan pursuant to Rule 12b-1 under the 1940 Act (“Rule 12b-1 Plan”). In accordance with the Rule 12b-1 Plan, the Fund is authorized to pay an amount up to 0.25% of the Fund’s average daily net assets each year for certain distribution-related activities. As authorized by the Board, no Rule 12b-1 fees are currently paid by the Fund and there are no plans to impose these fees. However, in the event Rule 12b-1 fees are charged in the future, they will be paid out of the Fund’s assets. The Adviser and its affiliates may, out of their own resources, pay amounts to third parties for distribution or marketing services on behalf of the Fund.

13

AAF First Priority CLO Bond ETF

Notes to Financial Statements

July 31, 2022 (Continued)

Administrator, Custodian and Transfer Agent

U.S. Bancorp Fund Services LLC, doing business as U.S. Bank Global Fund Services (“Fund Services” or “Administrator”) serves as administrator, transfer agent and fund accounting agent of the Fund pursuant to a Fund Servicing Agreement. U.S. Bank N.A. (the “Custodian”), an affiliate of Fund Services, serves as the Fund’s custodian pursuant to a Custody Agreement. Under the terms of these agreements, the Adviser pays the Fund’s administrative, custody and transfer agency fees.

A Trustee and all officers of the Trust are affiliated with the Administrator and Custodian.

|

4. |

CREATION AND REDEMPTION TRANSACTIONS |

Shares of the Fund are listed and traded on the NYSE Arca, Inc. (the “Exchange”). The Fund issues and redeems shares on a continuous basis at NAV only in large blocks of shares called “Creation Units.” Creation Units are issued and redeemed principally for cash, but may also be issued and redeemed in kind for securities held by or eligible to be held by the Fund. Shares generally will trade in the secondary market in amounts less than a Creation Unit at market prices that change throughout the day. Market prices for the shares may be different from their NAV. The NAV is determined as of the close of trading (generally, 4:00 p.m. Eastern Time) on each day the NYSE is open for trading. The NAV of the shares of the Fund will be equal to the Fund’s total assets minus the Fund’s total liabilities divided by the total number of shares outstanding. The NAV that is published will be rounded to the nearest cent; however, for purposes of determining the price of Creation Units, the NAV will be calculated to four decimal places.

Creation Unit Transaction Fee

Authorized Participants will be required to pay to the Custodian a fixed transaction fee (the “Creation Unit Transaction Fee”) in connection with the issuance or redemption of Creation Units. The standard Creation Unit Transaction Fee will be the same regardless of the number of Creation Units purchased or redeemed by an investor on the applicable business day. Effective May 2, 2022, the Creation Unit Transaction Fee charged by the Fund for each creation order is $300. Prior to this date, the Creation Unit Transaction Fee was $250.

An additional variable fee of up to a maximum of 2% of the value of the Creation Units subject to the transaction imposed for (i) creations effected outside the Clearing Process and (ii) creations made in an all cash amount (to offset the Trust’s brokerage and other transaction costs associated with using cash to purchase or redeem the requisite Deposit Securities). Investors are responsible for the costs of transferring the securities constituting the Deposit Securities to the account of the Trust. The Fund may determine to not charge a variable fee on certain orders when the Adviser has determined that doing so is in the best interests of Fund shareholders. Variable fees, if any, received by the Fund are displayed in the Capital Share Transactions section on the Statements of Changes in Net Assets.

Only “Authorized Participants” may purchase or redeem shares directly from the Fund. An Authorized Participant is either (i) a broker-dealer or other participant in the clearing process through the Continuous Net Settlement System of National Securities Clearing Corporation or (ii) a DTC participant and, in each case, must have executed a Participant Agreement with the Distributor. Most retail investors will not qualify as Authorized Participants or have the resources to buy and sell whole Creation Units. Therefore, they will be unable to purchase or redeem the shares directly from the Fund. Rather, most retail investors will purchase shares in the secondary market with the assistance of a broker and will be subject to customary brokerage commissions or fees. Securities received or delivered in connection with in-kind creates and redeems are valued as of the close of business on the effective date of the creation or redemption.

A creation unit will generally not be issued until the transfer of good title of the deposit securities to the Fund and the payment of any cash amounts have been completed. To the extent contemplated by the applicable participant agreement, Creation Units of the Fund will be issued to such authorized participant notwithstanding the fact that the Fund’s deposits have not been received in part or in whole, in reliance on the undertaking of the authorized participant to deliver the missing deposit securities as soon as possible. If the Fund or its agents do not receive all of the deposit securities, or the required cash amounts, by such time, then the order may be deemed rejected and the authorized participant shall be liable to the Fund for losses, if any.

14

AAF First Priority CLO Bond ETF

Notes to Financial Statements

July 31, 2022 (Continued)

|

5. |

FEDERAL INCOME TAX |

The tax character of distributions paid was as follows:

Ordinary |

Long-Term |

|||||||

Year ended July 31, 2022 |

$ | 118,047 | $ | — | ||||

Period ended July 31, 2021 |

86,767 | — | ||||||

|

(1) |

Ordinary income includes short-term capital gains. |

At July 31, 2022, the Fund’s fiscal year end, the components of distributable earnings (accumulated losses) and cost of investments on a tax basis, including the adjustments for financial reporting purposes as of the most recently completed Federal income tax reporting year, were as follows:

Federal Tax Cost of Investments |

$ | 7,260,872 | ||

Gross Tax Unrealized Appreciation |

$ | 77 | ||

Gross Tax Unrealized Depreciation |

(131,845 | ) | ||

Net Tax Unrealized Appreciation (Depreciation) |

(131,768 | ) | ||

Undistributed Ordinary Income |

19,490 | |||

Other Accumulated Gain/(Loss) |

(136,062 | ) | ||

Distributable Earnings / (Accumulated Losses) |

$ | (248,340 | ) |

Under current tax law, net capital losses realized after October 31 and net ordinary losses incurred after December 31 may be deferred and treated as occurring on the first day of the following fiscal year. The Fund’s carryforward losses and post-October losses are determined only at the end of each fiscal year. At July 31, 2022, the Fund’s fiscal year end, the Fund had short-term capital losses of $136,062 remaining which will be carried forward indefinitely to offset future realized capital gains.

|

6. |

INVESTMENT TRANSACTIONS |

Purchases and sales of investments (excluding short-term investments), creations in-kind and redemptions in-kind for the year ended July 31, 2022, were as follows:

Purchases |

Sales |

Creations In-Kind |

Redemptions |

||||||||||||

| $ | 6,708,605 | $ | 8,992,781 | $ | — | $ | — | ||||||||

During the year ended July 31, 2022, there were no realized gains and losses from in-kind redemptions.

|

7. |

PRINCIPAL RISKS |

As with all ETFs, shareholders of the Fund are subject to the risk that their investment could lose money. The Fund is subject to the principal risks, any of which may adversely affect the Fund’s NAV, trading price, yield, total return and ability to meet its investment objective.

A CLO is a trust collateralized by a pool of credit-related assets. Accordingly, CLO securities present risks similar to those of other types of credit investments, including default (credit), interest rate and prepayment risks. The extent of these risks depend largely on the type of securities used as collateral and the class of the CLOs in which the Fund invests. In addition, CLOs are often governed by a complex series of legal documents and contracts, which increases the risk of dispute over the interpretation and enforceability of such documents relative to other types of investments. There is also a risk that the trustee of a CLO does not properly carry out its duties to the CLO, potentially resulting in loss to the CLO.

15

AAF First Priority CLO Bond ETF

Notes to Financial Statements

July 31, 2022 (Continued)

LIBOR is used extensively in the U.S. and globally as a “benchmark” or “reference rate” for various commercial and financial contracts, including CLOs. Instruments in which the Fund invests may pay interest at floating rates based on LIBOR or may be subject to interest caps or floors based on LIBOR. The industry currently anticipates the conversion of all LIBOR based instruments to SOFR based instruments in June 2023 or sooner.

Since 2017, the United Kingdom’s Financial Conduct Authority has been working towards the cessation of LIBOR at the end of December 2021. In November 2020, though, the administrator of the U.S. Dollar LIBOR benchmarks, the ICE Benchmark Administration, extended the retirement date for most U.S. Dollar LIBOR rates until June 2023. Regulators and industry working groups have suggested numerous alternative reference rates to LIBOR. Leading alternatives include Sonia in the United Kingdom, €STR in the European Union, Tonar in Japan, and in the U.S., the New York Fed has been working to develop the Secured Overnight Financing Rate (SOFR). Global consensus is still coalescing around the transition to a new reference rate and the process for amending existing contracts. Abandonment of or modifications to LIBOR could have adverse impacts on newly issued financial instruments and existing financial instruments which reference LIBOR. There also remains uncertainty and risk regarding the willingness and ability of issuers to include enhanced provisions in new and existing contracts or instruments. The transition away from LIBOR may lead to increased volatility and illiquidity in markets that are tied to LIBOR, reduced values of LIBOR-related investments, and reduced effectiveness of hedging strategies, adversely affecting the Fund’s performance or NAV. In addition, the alternative reference rate may be an ineffective substitute resulting in prolonged adverse market conditions for the Fund.

The global outbreak of COVID-19 (commonly referred to as “coronavirus”) has disrupted economic markets and the prolonged economic impact is uncertain. The ultimate economic fallout from the pandemic, and the long-term impact on economies, markets, industries and individual issuers, are not known. The operational and financial performance of the issuers of securities in which the Fund invests depends on future developments, including the duration and spread of the outbreak, and such uncertainty may in turn adversely affect the value and liquidity of the Fund’s investments, impair the Fund’s ability to satisfy redemption requests, and negatively impact the Fund’s performance.

On February 24, 2022, Russia commenced a military attack on Ukraine. The outbreak of hostilities between the two countries could result in more widespread conflict and could have a severe adverse effect on the region and the markets. In addition, sanctions imposed on Russia by the United States and other countries, and any sanctions imposed in the future could have a significant adverse impact on the Russian economy and related markets. The price and liquidity of investments may fluctuate widely as a result of the conflict and related events. How long such conflict and related events will last and whether it will escalate further cannot be predicted, nor its effect on the Fund.

A complete description of the principal risks is included in the Fund’s prospectus under the heading “Principal Investment Risks.”

|

8. |

BENEFICIAL OWNERSHIP |

The beneficial ownership, either directly or indirectly, of 25% or more of the voting securities of a fund creates a presumption of control of a fund, under section 2(a)(9) of the 1940 Act. At July 31, 2022, shareholders who are affiliated with the Adviser, as a beneficial shareholder, owned approximately 28% of the outstanding shares of the Fund.

|

9. |

SUBSEQUENT EVENTS |

The Fund paid distributions to shareholders as follows:

Record Date |

Ex-Date |

Reinvestment |

Ordinary |

Ordinary Income |

||||||

08/02/2022 |

08/01/2022 |

08/03/2022 |

$ | 0.0570 | $ | 17,100 | ||||

09/02/2022 |

09/01/2022 |

09/06/2022 |

$ | 0.0785 | $ | 23,550 | ||||

Other than as disclosed, there were no other subsequent events requiring recognition or disclosure through the date the financial statements were issued.

16

AAF First Priority CLO Bond ETF

Report of Independent Registered Public Accounting Firm

To the Shareholders of AAF First Priority CLO Bond ETF and

Board of Trustees of Listed Funds Trust

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of AAF First Priority CLO Bond ETF (the “Fund”), a series of Listed Funds Trust, as of July 31, 2022, the related statement of operations for the year then ended, the statements of changes in net assets and the financial highlights for each of the two periods in the period then ended, and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of July 31, 2022, the results of its operations for the year then ended, and the changes in net assets and the financial highlights for each of the two periods in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement whether due to error or fraud.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of July 31, 2022, by correspondence with the custodian. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

We have served as the Fund’s auditor since 2020.

COHEN & COMPANY, LTD.

Cleveland, Ohio

September 29, 2022

17

AAF First Priority CLO Bond ETF

Board Consideration and Approval of Continuation of Advisory Agreement

(Unaudited)

At a meeting held on August 16, 2022 (the “Meeting”), the Board of Trustees (the “Board”) of Listed Funds Trust (the “Trust”), including those trustees who are not “interested persons” of the Trust, as defined in the Investment Company Act of 1940 (the “1940 Act”) (the “Independent Trustees”), considered the approval of the continuation of the advisory agreement (the “Advisory Agreement”) between Alternative Access Funds, LLC (the “Adviser”) and the Trust, on behalf of the AAF First Priority CLO Bond ETF (the “Fund”).

Pursuant to Section 15 of the 1940 Act, the continuation of the Advisory Agreement after its initial two-year term must be approved annually by: (i) the vote of the Board or shareholders of the Fund and (ii) the vote of a majority of the Independent Trustees cast at a meeting called for the purpose of voting on such approval. As discussed in greater detail below, in preparation for the Meeting, the Board requested from and reviewed a wide variety of information provided by the Adviser.

The Board considered the materials it received in advance of the Meeting, including a memorandum from legal counsel to the Trust regarding the responsibilities of the Trustees in considering the approval of the Advisory Agreement under the 1940 Act, and information provided over the course of the prior year. The Board noted that on June 21, 2022, the Fund’s shareholders had approved a proposal to reorganize the Fund into the AXS First Priority CLO Bond ETF (the “Transaction”), a newly created series within a different trust with a different board of trustees, but that due to administrative delays, the Transaction had not yet been completed. As a result, it would be necessary for the Board to approve the renewal of the Advisory Agreement, which would otherwise expire as scheduled on September 8, 2022. In light of this information, the Board deliberated on the approval of the Advisory Agreement for the earlier of an additional one-year period or the completion of the Transaction. Throughout the process, the Trustees were afforded the opportunity to ask questions of, and request additional materials from, the Adviser. The Independent Trustees also met in executive session with counsel to the Trust to further discuss the advisory arrangement and the Independent Trustees’ responsibilities relating thereto.

At the Meeting, the Board and the Independent Trustees evaluated a number of factors, including, among other things: (i) the nature, extent, and quality of the services provided by the Adviser to the Fund; (ii) the Fund’s expenses and performance; (iii) the cost of the services provided and profits to be realized by the Adviser from the relationship with Fund; (iv) comparative fee and expense data for the Fund and other investment companies with similar investment objectives; (v) the extent to which the advisory fee for the Fund reflects economies of scale shared with its shareholders; (vi) any benefits derived by the Adviser from the relationship with the Fund, including any fall-out benefits enjoyed by the Adviser; and (vii) other factors the Board deemed relevant. In its deliberations, the Board considered the factors and reached the conclusions described below relating to the advisory arrangement and the renewal of the Advisory Agreement. In its deliberations, the Board did not identify any single piece of information that was paramount or controlling and the individual Trustees may have attributed different weights to various factors.

Nature, Extent, and Quality of Services Provided. The Board considered the scope of services provided under the Advisory Agreement, noting that the Adviser expected to continue to provide substantially similar investment management services to the Fund. In considering the nature, extent, and quality of the services provided by the Adviser, the Board considered the quality of the Adviser’s compliance infrastructure and past reports from the Trust’s Chief Compliance Officer. The Board also considered its previous experience with the Adviser and the investment management services it has provided to the Fund. The Board noted that it had received a copy of the Adviser’s registration form on Form ADV, as well as the response of the Adviser to a detailed series of questions which included, among other things, information about the background and experience of the firm’s key personnel, the firm’s cybersecurity policy, and the services provided by the Adviser.

In addition to the Adviser’s responsibilities with respect to implementing the Fund’s investment program, the Board also considered other services currently provided by the Adviser to the Fund, such as monitoring adherence to the Fund’s investment restrictions, monitoring compliance with various policies and procedures and with applicable securities regulations, and monitoring the extent to which the Fund achieved its investment objective as an actively managed fund.

Historical Performance. The Board noted that it had received information regarding the Fund’s performance for various time periods in the materials provided to the Board in advance of the Meeting. The Board noted that, for the one-year and since inception periods ended June 30, 2022, the Fund underperformed the Bloomberg U.S. Floating Rate Note <5 Years Index, before fees and expenses. The Board also noted that, for the one-year period ended July 31, 2022, the Fund underperformed the median for its peer funds in the universe of Ultrashort Bond and Bank Loan ETFs as reported by Morningstar (the “Category

18

AAF First Priority CLO Bond ETF

Board Consideration and Approval of Continuation of Advisory Agreement

Peer Group”). The Board, however, noted that because the Category Peer Group included ultrashort funds with average maturity durations of less than one year, which differs from that of the Fund, the Category Peer Group may not provide an apt performance comparison.

The Board also considered the Fund’s performance relative to certain funds identified by the Adviser as the Fund’s most similar peer funds (the “Selected Peer Group”). The Board noted the Fund underperformed the Selected Peer Group for the one-year period ended June 30, 2022.

Cost of Services Provided and Profitability. The Board reviewed the expense ratio for the Fund and compared the Fund’s expense ratio to its Category Peer Group and Selected Peer Group. The Board took into consideration that the Adviser charges a “unitary fee,” meaning the Fund pays no expenses except for the advisory fee paid to the Adviser pursuant to the Advisory Agreement and certain expenses excluded from the unitary fee arrangement, including interest charges on any borrowings, dividends and other expenses on securities sold short, taxes, brokerage commissions and other expenses incurred in placing orders for the purchase and sale of securities and other investment instruments, acquired fund fees and expenses, accrued deferred tax liability, extraordinary expenses, and distribution fees and expenses paid by the Trust under any distribution plan adopted pursuant to Rule 12b-1 under the 1940 Act. The Board noted that the Adviser continues to be responsible for compensating the Fund’s other service providers and paying the Fund’s other expenses out of its own fee and resources. The Board also evaluated the compensation and benefits received by the Adviser from its relationship with the Fund, taking into account analyses of the Adviser’s profitability with respect to the Fund.

The Board noted the Fund’s expense ratio currently is equivalent to its unitary fee. The Board further noted that the Fund’s expense ratio was equal to the median expense ratio of its Category Peer Group and within the range of expense ratios of the Selected Peer Group.

Economies of Scale. The Board noted that it is not yet evident that the Fund has reached the size at which it has begun to realize economies of scale, but acknowledged that breakpoints might be warranted if the Fund’s assets continue to grow. However, the Board further determined that, based on the amount and structure of the Fund’s unitary fee, any such economies of scale would be shared with the Fund’s shareholders. The Board stated it would monitor fees as the Fund grows and consider whether fee breakpoints may be warranted in the future.

Conclusion. No single factor was determinative of the Board’s decision to approve the continuation of the Advisory Agreement; rather, the Board based its determination on the total mix of information available to it. Based on a consideration of all the factors in their totality, the Board, including a majority of the Independent Trustees, determined that the Advisory Agreement, including the compensation payable under the Advisory Agreement, was fair and reasonable to the Fund. The Board, including a majority of the Independent Trustees, therefore determined that the approval of the continuation of the Advisory Agreement was in the best interests of the Fund and its shareholders.

19

AAF First Priority CLO Bond ETF

Trustees and Officers of the Trust

July 31, 2022 (Unaudited)

The Fund’s Statement of Additional Information includes additional information about the Fund’s Trustees and Officers, and is available, without charge upon request by calling 1-800-617-0004, or by visiting the Fund’s website at www.aafetfs.com.

Name and Year of Birth |

Position Held |

Term of Office |

Principal Occupation(s) |

Number of |

Other |

Independent Trustees |

|||||

John L. Jacobs |

Trustee and Audit Committee Chair |

Indefinite term; since 2017 |

Chairman of Alerian, Inc. (since June 2018); Founder and CEO of Q3 Advisors, LLC (financial consulting firm) (since 2015); Executive Director of Center for Financial Markets and Policy (2016–2022); Distinguished Policy Fellow and Executive Director, Center for Financial Markets and Policy, Georgetown University (2015–2022); Senior Advisor, Nasdaq OMX Group (2015–2016); Executive Vice President, Nasdaq OMX Group (2013–2015) |

52 |

Independent Trustee, SHP ETF Trust (since 2021) (2 portfolios); Director, tZERO Group, Inc. (since 2020); Independent Trustee, Procure ETF Trust II (since 2018) (1 portfolio); Independent Trustee, Horizons ETF Trust I (2015-2019). |

Koji Felton |

Trustee |

Indefinite term; since 2019 |

Retired; formerly Counsel, Kohlberg Kravis Roberts & Co. L.P. (investment firm) (2013–2015); Counsel, Dechert LLP (law firm) (2011–2013) |

52 |

Independent Trustee, Series Portfolios Trust (since 2015) (10 portfolios). |

Pamela H. Conroy Year of birth: 1961 |

Trustee and Nominating and Governance Committee Chair |

Indefinite term; since 2019 |

Retired; formerly Executive Vice President, Chief Operating Officer & Chief Compliance Officer, Institutional Capital Corporation (investment firm) (1994–2008) |

52 |

Independent Trustee, Frontier Funds, Inc. (since 2020) (6 portfolios). |

Interested Trustee |

|||||

Paul R. Fearday, CPA* Year of birth: 1979 |

Trustee and Chairman |

Indefinite term; since 2019 |

Senior Vice President, U.S. Bancorp Fund Services, LLC (since 2008) |

52 |

None. |

|

* |

This Trustee is considered an “Interested Trustee” as defined in the 1940 Act because of his affiliation with U.S. Bancorp Fund Services, d/b/a U.S. Bank Global Fund Services and U.S. Bank N.A., which provide fund accounting, administration, transfer agency and custodian services to the Fund. |

20

AAF First Priority CLO Bond ETF

Trustees and Officers of the Trust

July 31, 2022 (Unaudited)

Name and Year of Birth |

Position(s) Held |

Term of Office |

Principal Occupation(s) During Past 5 Years |

Gregory Bakken |

President and Principal Executive Officer |

Indefinite term, February 2019 |

Vice President, U.S. Bancorp Fund Services, LLC (since 2006). |

Travis G. Babich |

Treasurer and Principal Financial Officer |

Indefinite term, September 2019 |

Vice President, U.S. Bancorp Fund Services, LLC (since 2005). |

Kacie G. Briody |

Assistant Treasurer |

Indefinite term, March 2019 |

Assistant Vice President, U.S. Bancorp Fund Services, LLC (since 2021); Officer, U.S. Bancorp Fund Services, LLC (2014 to 2021). |

Kent Barnes |

Secretary |

Indefinite term, February 2019 |

Vice President, U.S. Bancorp Fund Services, LLC (since 2018); Chief Compliance Officer, Rafferty Asset Management, LLC (2016 to 2018); Vice President, U.S. Bancorp Fund Services, LLC (2007 to 2016). |

Christi C. James |

Chief Compliance Officer and Anti-Money Laundering Officer |

Indefinite term, July 2022 |

Senior Vice President, U.S. Bancorp Fund Services, LLC (since 2022); Principal Consultant, ACA Group (2021 to 2022); Lead Manager, Communications Compliance, T. Rowe Price Investment Services, Inc. (2018 to 2021); Compliance & Legal Manager, CR Group LP (2017 to 2018). |

Joshua J. Hinderliter Year of birth: 1983 |

Assistant Secretary |

Indefinite term, May 2022 |

Assistant Vice President, U.S. Bancorp Fund Services, LLC (since 2022); Managing Associate, Thompson Hine LLP (2016 to 2022). |

21

AAF First Priority CLO Bond ETF

Shareholder Expense Example

(Unaudited)

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including brokerage commissions on purchases and sales of Fund shares; and (2) ongoing costs, including management fees and other fund expenses. The following example is intended to help you understand your ongoing costs (in dollars and cents) of investing in the Fund and to compare these costs with the ongoing costs of investing in other funds. The examples are based on an investment of $1,000 invested at the beginning of the period and held throughout the entire period (February 1, 2022 to July 31, 2022).

ACTUAL EXPENSES

The first line under the Fund in the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line for your Fund under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

HYPOTHETICAL EXAMPLE FOR COMPARISON PURPOSES

The second line in the table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as brokerage commissions paid on purchases and sales of Fund shares. Therefore, the second line in the table is useful in comparing ongoing Fund costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Beginning |

Ending |

Annualized |

Expenses |

|

AAF First Priority CLO Bond ETF |

||||

Actual |

$ 1,000.00 |

$ 981.60 |

0.25% |

$ 1.23 |

Hypothetical (5% return before expenses) |

$ 1,000.00 |

$ 1,023.55 |

0.25% |

$ 1.25 |

|

(1) |

Expenses are calculated using the Fund’s annualized expense ratio multiplied by the average account value during the period, multiplied by 181/365 days (to reflect the six-month period). |

22

AAF First Priority CLO Bond ETF

Supplemental Information

(Unaudited)

Investors should consider the investment objective and policies, risk considerations, charges and ongoing expenses of an investment carefully before investing. The prospectus contains this and other information relevant to an investment in the Fund. Please read the prospectus carefully before investing. A copy of the prospectus for the Fund may be obtained without charge by writing to the Fund, c/o U.S. Bank Global Fund Services, P.O. Box 701, Milwaukee, Wisconsin 53201-0701, by calling 1-800-617-0004, or by visiting the Fund’s website at www.aafetfs.com.

QUARTERLY PORTFOLIO HOLDING INFORMATION

The Fund files its complete schedule of portfolio holdings for its first and third fiscal quarters with the Securities and Exchange Commission (“SEC”) on Part F of Form N-PORT. The Fund’s Part F of Form N-PORT is available without charge, upon request, by calling toll-free at 1-800-617-0004. Furthermore, you may obtain the Part F of Form N-PORT on the SEC’s website at www.sec.gov.

PROXY VOTING INFORMATION

The Fund is required to file a Form N-PX, with the Fund’s complete proxy voting record for the 12 months ended June 30, no later than August 31 of each year. The Fund’s proxy voting record will be available without charge, upon request, by calling toll-free 1-800-617-0004 and on the SEC’s website at www.sec.gov.

FREQUENCY DISTRIBUTION OF PREMIUMS AND DISCOUNTS

Information regarding how often shares of the Fund trade on an exchange at a price above (i.e., at a premium) or below (i.e., at a discount) the NAV of the Fund is available without charge, on the Fund’s website at www.aafetfs.com.

MATTERS SUBMITTED TO A SHAREHOLDER VOTE

A special meeting of shareholders of the Fund was held on June 21, 2022, and the following matters were approved:

Proposal to approve an Agreement and Plan of Reorganization pursuant to which all of the assets of the Fund will be transferred to AXS First Priority CLO Bond ETF (“Acquiring Fund”), newly formed series of Investment Managers Series Trust II, in exchange for shares of the Fund, distributed pro rata by the Fund to its shareholders, and the Acquiring Fund’s assumption of the Fund’s stated liabilities.

For: |

247,235 | |||

Against: |

2,000 | |||

Abstain: |

0 | |||

Total: |

247,235 |

23

AAF First Priority CLO Bond ETF

Review of Liquidity Risk Management Program

(Unaudited)

Pursuant to Rule 22e-4 under the Investment Company Act of 1940, the Trust, on behalf of the series of the Trust covered by this shareholder report (the “Series”), has adopted a liquidity risk management program to govern the Trust’s approach to managing liquidity risk. Rule 22e-4 seeks to promote effective liquidity risk management, thereby reducing the risk that a fund will be unable to meet its redemption obligations and mitigating dilution of the interests of fund shareholders. The Trust’s liquidity risk management program is tailored to reflect the Series’ particular risks, but not to eliminate all adverse impacts of liquidity risk, which would be incompatible with the nature of such Series.

The investment adviser to the Series has adopted and implemented its own written liquidity risk management program (the “Program”) tailored specifically to assess and manage the liquidity risk of the Series. At a recent meeting of the Board of Trustees of the Trust, the Trustees received a report pertaining to the operation, adequacy, and effectiveness of implementation of the Program for the period ended December 31, 2021. The report concluded that the Program is reasonably designed to assess and manage the Series’ liquidity risk and has operated adequately and effectively to manage such risk. The report reflected that there were no liquidity events that impacted the Series’ ability to timely meet redemptions without dilution to existing shareholders. The report further noted that no material changes have been made to the Program since its implementation.

There can be no assurance that the Program will achieve its objectives in the future. Please refer to the prospectus for more information regarding the Series’ exposure to liquidity risk and other principal risks to which an investment in the Series may be subject.

24

AAF First Priority CLO Bond ETF

Privacy Policy

July 31, 2022 (Unaudited)

We are committed to respecting the privacy of personal information you entrust to us in the course of doing business with us.

The Fund collects non-public information about you from the following sources:

|

● |

Information we receive about you on applications or other forms; |

|

● |

Information you give us orally; and/or |

|

● |

Information about your transactions with us or others. |

We do not disclose any non-public personal information about our customers or former customers without the customer’s authorization, except as permitted by law or in response to inquiries from governmental authorities. We may share information with affiliated and unaffiliated third parties with whom we have contracts for servicing the Fund. We will provide unaffiliated third parties with only the information necessary to carry out their assigned responsibilities. We maintain physical, electronic and procedural safeguards to guard your non-public personal information and require third parties to treat your personal information with the same high degree of confidentiality.

In the event that you hold shares of the Fund through a financial intermediary, including, but not limited to, a broker-dealer, bank, or trust company, the privacy policy of your financial intermediary would govern how your non-public personal information would be shared by those entities with unaffiliated third parties.

25

Investment Adviser:

Alternative Access Funds, LLC

840 Apollo Street, Suite 100

El Segundo, CA 90245

Legal Counsel:

Morgan, Lewis & Bockius LLP

1111 Pennsylvania Avenue, N.W.

Washington, D.C. 20004

Independent Registered Public Accounting Firm:

Cohen & Company, Ltd.

1350 Euclid Avenue, Suite 800

Cleveland, OH 44115

Distributor:

Quasar Distributors, LLC

111 East Kilbourn Avenue, Suite 2200

Milwaukee, WI 53202

Administrator, Fund Accountant & Transfer Agent:

U.S. Bancorp Fund Services, LLC

d/b/a U.S. Bank Global Fund Services

615 E. Michigan St.

Milwaukee, WI 53202

Custodian:

U.S. Bank N.A.

1555 North RiverCenter Drive, Suite 302

Milwaukee, WI 53212

This information must be preceded or accompanied by a current prospectus for the Fund.

(b) Not Applicable

Item 2. Code of Ethics.

The registrant has adopted a code of ethics that applies to the registrant’s principal executive officer and principal financial officer. The Registrant has not made any substantive amendments to its code of ethics during the period covered by this report. The registrant has not granted any waivers from any provisions of the code of ethics during the period covered by this report.

A copy of the registrant’s Code of Ethics is filed herewith.

Item 3. Audit Committee Financial Expert.

The registrant’s Board of Trustees has determined that there is at least one audit committee financial expert serving on its audit committee. Mr. John Jacobs is the “audit committee financial expert” and is considered to be “independent” as each term is defined in Item 3 of Form N-CSR.

Item 4. Principal Accountant Fees and Services.

The registrant has engaged its principal accountant to perform audit services, audit-related services, tax services and other services during the past fiscal year. “Audit services” refer to performing an audit of the registrant's annual financial statements or services that are normally provided by the accountant in connection with statutory and regulatory filings or engagements for the fiscal year. “Audit-related services” refer to the assurance and related services by the principal accountant that are reasonably related to the performance of the audit. “Tax services” refer to professional services rendered by the principal accountant for tax compliance, tax advice, and tax planning. There were no “Other services” provided by the principal accountant. The following table details the aggregate fees billed or expected to be billed for the last two fiscal years for audit fees, audit-related fees, tax fees and other fees by the principal accountant.

| FYE 07/31/2022 | FYE 07/31/2021 | |

| Audit Fees | $17,000 | $17,000 |

| Audit-Related Fees | $0 | N/A |

| Tax Fees | $4,500 | $4,500 |

| All Other Fees | $0 | N/A |

(e)(1) The audit committee has adopted pre-approval policies and procedures that require the audit committee to pre-approve all audit and non-audit services of the registrant, including services provided to any entity affiliated with the registrant.

(e)(2) The percentage of fees billed by Cohen & Company, Ltd. applicable to non-audit services pursuant to waiver of pre-approval requirement were as follows:

| FYE 07/31/2022 | FYE 07/31/2021 | |

| Audit-Related Fees | 0% | 0% |

| Tax Fees | 0% | 0% |

| All Other Fees | 0% | 0% |

(f) All of the principal accountant’s hours spent on auditing the registrant’s financial statements were attributed to work performed by full-time permanent employees of the principal accountant.

(g) The following table indicates the non-audit fees billed or expected to be billed by the registrant’s accountant for services to the registrant and to the registrant’s investment adviser (and any other controlling entity, etc.—not sub-adviser) for the last two years.

| Non-Audit Related Fees | FYE 07/31/2022 | FYE 07/31/2021 |

| Registrant | N/A | N/A |

| Registrant’s Investment Adviser | N/A | N/A |

(h) The audit committee of the board of trustees/directors has considered whether the provision of non-audit services that were rendered to the registrant's investment adviser is compatible with maintaining the principal accountant's independence and has concluded that the provision of such non-audit services by the accountant has not compromised the accountant’s independence.

The registrant has not been identified by the U.S. Securities and Exchange Commission as having filed an annual report issued by a registered public accounting firm branch or office that is located in a foreign jurisdiction where the Public Company Accounting Oversight Board is unable to inspect or completely investigate because of a position taken by an authority in that jurisdiction.

The registrant is not a foreign issuer.

Item 5. Audit Committee of Listed Registrants.

| (a) | The registrant is an issuer as defined in Rule 10A-3 under the Securities Exchange Act of 1934, (the “Act”) and has a separately-designated standing audit committee established in accordance with Section 3(a)(58)(A) of the Act. The entire Board of Trustees is acting as the registrant’s audit committee. |

(b) Not applicable.

Item 6. Investments.

| (a) | Schedule of Investments is included as part of the report to shareholders filed under Item 1 of this Form. |

| (b) | Not applicable. |