As filed with the Securities and Exchange Commission on November 26, 2019

Registration No. 333-__________

UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM F-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

HUAHUI EDUCATION GROUP LIMITED

(Exact Name of Registrant as Specified in its Charter)

| Cayman Islands | 8299 | Not Applicable | ||

| (State

or Other Jurisdiction of Incorporation or Organization) |

(Primary

Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

13th Floor, Building B1, Wisdom Plaza,

Qiaoxiang Road, Nanshan District

Shenzhen, Guangdong Province, China 518000

Telephone: (86) 13728708818

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Copies to:

Henry F. Schlueter, Esq.

Celia Velletri, Esq.

Schlueter & Associates, P.C.

5290 DTC Parkway, Suite 150

Greenwood Village, CO 80111

Tel: 303-292-3883

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Approximate date of commencement of proposed sale to the public: From time to time after effectiveness of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. [X]

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act or Rule 12b-2 of the Securities Exchange Act of 1934.

Emerging growth company [X]

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. [ ]

CALCULATION OF REGISTRATION FEE

Title of Each Class of Securities to be Registered |

Amount to be Registered |

Proposed

Maximum Offering Price Per Share |

Proposed

Maximum Aggregate Offering Price(1) |

Amount

of Registration Fee |

||||||||||||

| Ordinary Shares, par value $0.0001 per share(2)(3) | 8,734,900 | $ | 0.10 |

$ | 873,490 | $ | 113.38 | |||||||||

| Total | 8,734,900 | $ | 0.10 | $ | 873,490 | $ | 113.38 | |||||||||

| (1) | Estimated solely for the purpose of determining the amount of registration fee in accordance with Rule 457(c) under the Securities Act of 1933, as amended. The registrant’s securities are not trading on any exchange or in any market, and our Ordinary Shares have a negative book value. The registration fee has been calculated based on an offering price of $0.10 per share, or $873,490. |

| (2) | In accordance with Rule 416(a), the Registrant is also registering an indeterminate number of additional Ordinary Shares that shall be issuable pursuant to Rule 416 to prevent dilution resulting from share splits, share dividends or similar transactions. |

| (3) | Reflects the resale by Selling Shareholders included herein of their Ordinary Shares. |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission acting pursuant to said Section 8(a) may determine.

The information in this prospectus is not complete and may be changed. Neither we nor the Selling Shareholders may sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION

DATED November 26, 2019

PRELIMINARY PROSPECTUS

HUAHUI EDUCATION GROUP LIMITED

This prospectus relates to the resale from time to time by the Selling Shareholders identified in this prospectus under the caption “Selling Shareholders” of up to 8,734,900 of our $0.0001 par value Ordinary Shares.

For the details about the Selling Shareholders, please see “Principal and Selling Shareholders – Selling Shareholders.” The Selling Shareholders may sell these shares from time to time in the principal market on which our Ordinary Shares are traded at the prevailing market price, in negotiated transactions or through any other means described in the section titled “Plan of Distribution.” The Selling Shareholders may be deemed underwriters within the meaning of the Securities Act of 1933, as amended, of the Ordinary Shares that they are offering. We will pay the expenses of registering these shares. We will not receive proceeds from the sale of our shares by the Selling Shareholders that are covered by this prospectus.

The shares are being registered to permit the Selling Shareholders, or their respective pledgees, donees, transferees or other successors-in-interest, to sell the shares from time to time in the public market. We do not know when or in what amount the Selling Shareholders may offer the securities for sale. The Selling Shareholders may sell some, all or none of the securities offered by this prospectus.

There is no market for the Ordinary Shares and there can be no assurance that a market for the shares will develop. However, management intends to seek to have the Ordinary Shares admitted to quotation on the appropriate market with OTC Markets subsequent to the SEC declaring the registration statement of which this prospectus is a part effective.

We are an emerging growth company, as defined in the U.S. Jumpstart Our Business Startups Act of 2012, or the JOBS Act, and, as such, have elected to comply with certain reduced public company reporting requirements.

Investing in the Ordinary Shares involves a high degree of risk. See “Risk Factors” beginning on page 8 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The Selling Shareholders may sell their Ordinary Shares described in this prospectus in a number of different ways, at prevailing market prices or privately negotiated prices and there is no termination date of the Selling Shareholders’ offering.

The date of this prospectus is ______________, 2019

TABLE OF CONTENTS

We have not authorized any person to provide you with information different from that contained in this prospectus or any related free-writing prospectus that we authorize to be distributed to you. This prospectus is not an offer to sell, nor is it seeking an offer to buy, these securities in any jurisdiction where the offer or sale is not permitted. The information in this prospectus speaks only as of the date of this prospectus unless the information specifically indicates that another date applies, regardless of the time of delivery of this prospectus or of any sale of the securities offered hereby.

For investors outside of the United States: We have not done anything that would permit this Offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than the United States. Persons outside of the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the Offering and the distribution of this prospectus outside of the United States.

This prospectus includes statistical and other industry and market data that we obtained from industry publications and research, surveys and studies conducted by third parties. Industry publications and third-party research, surveys and studies generally indicate that their information has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. While we believe these industry publications and third-party research, surveys and studies are reliable, you are cautioned not to give undue weight to this information.

All references in this prospectus to “$,” “U.S.$,” “U.S. dollars,” “dollars,” “US$” and “USD” mean United States dollars unless otherwise noted. All references to the “PRC” or “China” in this prospectus refer to the People’s Republic of China. All references to “Hong Kong” or “H.K.” in this prospectus refer to the Hong Kong Special Administrative Region of the People’s Republic of China. All references to the “United States,” “U.S.” or “US” refer to the United States of America.

| 2 |

| ● | “Ordinary Resolution” refers to a resolution passed by a simple majority of votes cast or approved in writing by a simple majority of votes entitled to be cast by the Members entitled to vote at a general or special meeting of the Company. | |

| ● | “Ordinary Shares” or “Shares” refers to the Company’s Ordinary Shares, par value $0.0001 per share. | |

| ● | “Exchange Act” refers to the U.S. Securities Exchange Act of 1934, as amended. | |

| ● | “Hong Kong” or “H.K.” refers to Hong Kong Special Administrative Region of the People’s Republic of China. | |

| ● | “Offering” refers to the resale of the Ordinary Shares offered by the Selling Shareholders included herein. | |

| ● | “PRC” and “China” refer to the People’s Republic of China. | |

| ● | “Securities and Exchange Commission,” “SEC,” “Commission” or similar terms refer to the United States Securities and Exchange Commission. | |

| ● | “Sarbanes-Oxley Act” refers to the Sarbanes-Oxley Act of 2002. | |

| ● | “Securities Act” refers to the U.S. Securities Act of 1933, as amended. | |

| ● | “Selling Shareholders” refers to our pre-existing shareholders who are selling their Ordinary Shares pursuant to the Registration Statement on Form F-1. | |

| ● | “United States,” “U.S.,” “USA” and “US” refer to the United States of America. | |

| ● | “$,” “U.S. $,” “U.S. dollars,” “dollars,” “US$” and “USD” refer to United States dollars. |

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements. A forward-looking statement is a projection about a future event or result, and whether the statement comes true is subject to many risks and uncertainties. These statements often can be identified by the use of terms such as “may,” “will,” “expect,” “believe,” “anticipate,” “estimate,” “approximate” or “continue,” or the negative thereof. The actual results, performance, achievements or activities of the Company, either express or implied, will likely differ from projected results or activities of the Company as described in this prospectus, and such differences could be material. You should review carefully all information included in this prospectus.

You should rely only on the forward-looking statements that reflect management’s view as of the date of this prospectus. We undertake no obligation to publicly revise or update these forward-looking statements to reflect subsequent events or circumstances. You should also carefully review the risk factors described in other documents we file from time to time with the Securities and Exchange Commission (the “SEC”). The Private Securities Reform Act of 1995 contains a safe harbor for forward-looking statements on which the Company relies in making such disclosures. In connection with the “safe harbor,” we are hereby identifying important factors that could cause actual results to differ materially from those contained in any forward-looking statements made by us or on our behalf. Factors that might cause such a difference include, but are not limited to, those discussed in the section entitled “Risk Factors.”

| 3 |

This summary highlights information contained elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our Ordinary Shares, you should carefully read the entire prospectus, including our financial statements and the related notes included elsewhere in this prospectus. You should also consider, among other things, the matters described under “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in each case appearing elsewhere in this prospectus. Unless otherwise stated, all references to “us,” “our,” “we,” the “Company,” the “group” and similar designations refer to Huahui Education Group Limited, a Cayman Islands exempted company with limited liability,

History of the Company

The Company was originally incorporated in Nevada under the name “Duonas Corp.” on September 19, 2014. It maintains its principal executive offices at 13th Floor, Building B1, Wisdom Plaza, Qiaoxiang Road, Nanshan District, Shenzhen, Guangdong Province, China 518000. The Company was formed to produce and sell stylish decorative items made from concrete, such as a variety of sculptures, candleholders, lamps, tabletops, bookcases, vases of various shapes and forms and decorations for the garden.

The Company filed a registration statement on Form S-1 with the SEC on August 25, 2016, which was declared effective on October 12, 2016. In November 2017, subsequent to a change of control, the Company’s name was changed to Huahui Education Group Corporation, its ticker symbol was changed to “HHEG” and management of the Company abandoned its business plan and determined to seek a possible business combination. The business purpose of the Company changed to seeking the acquisition of, or merger with, an existing company.

As a result, the Company became a “shell company” (as such term is defined in Rule 12b-2 under the Exchange Act) with nominal assets and no business operations, and it sought to identify, evaluate and investigate various companies with the intent that, if such investigation warranted, a reverse merger transaction could be negotiated and completed pursuant to which the Company would acquire a target company with an operating business with the intent of continuing the acquired company’s business as a publicly held entity.

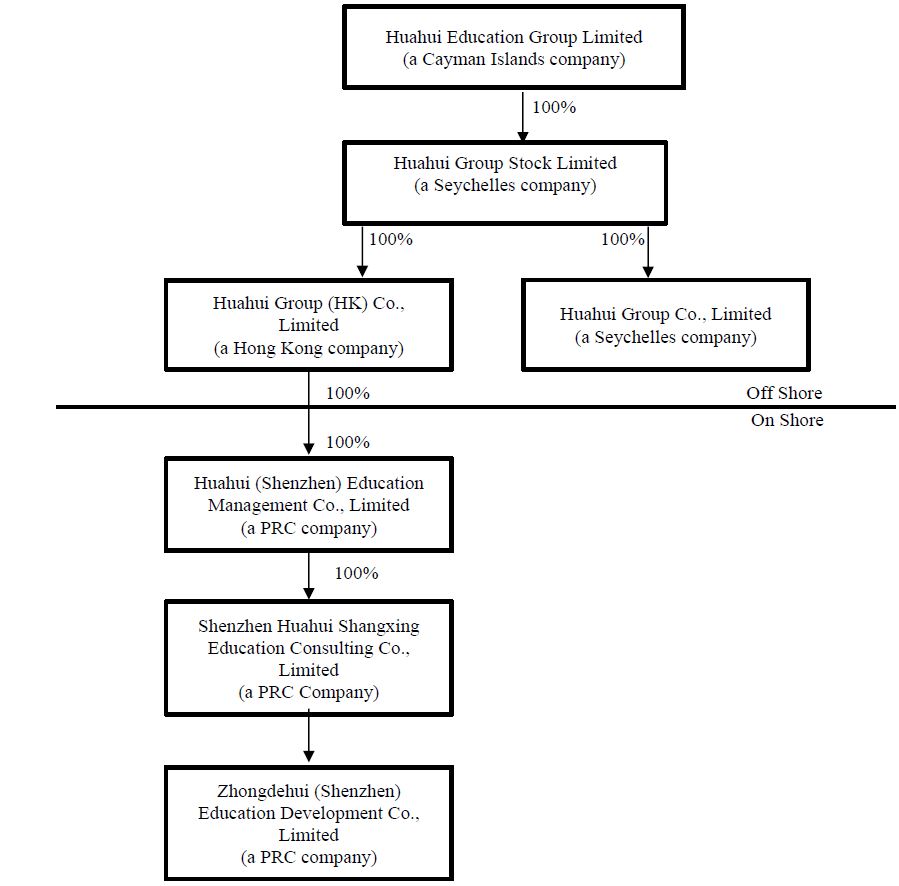

Effective February 22, 2019, the Company changed its domicile from Nevada to the Cayman Islands by merging into its wholly-owned Cayman Islands subsidiary, Huahui Education Group Limited (the “Redomicile Merger”). As a result of the Redomicile Merger, the Company’s name was changed to Huahui Education Group Limited.

On July 3, 2019 (the “Closing Date”), the Company closed on a share exchange (the “Share Exchange”) with Huahui Group Stock Limited, (“HGSL”), a Seychelles company limited by shares, and HGSL’s shareholders (the “HGSL Shareholders”). As a result, HGSL is now a wholly owned subsidiary of the Company. Under the Share Exchange Agreement, the HGSL Shareholders exchanged all of the shares that they held in HGSL for 300,000,000 Ordinary Shares of the Company.

As a result of the Share Exchange, management of the Company believes that the Company is no longer a shell company. The Company’s operations now consist of the operations of HGSL and its subsidiaries. When we refer in this prospectus to business and financial information for periods prior to the consummation of the Share Exchange, we are referring to the business and financial information of HGSL and its subsidiaries unless the context suggests otherwise; when we use phrases such as “we,” “our,” “company” and “us,” we are referring to the Company and all of its subsidiaries, as a combined entity.

| 4 |

The shares issued to the HGSL Shareholders in connection with the Share Exchange were not registered under the Securities Act. The purpose of the registration statement of which this prospectus is a part is to register a portion of those shares for resale together with all of the shares issued in the Redomicile Merger.

Business of the Company

Through its indirect subsidiary, Zhongdehui (Shenzhen) Education Development Co., Limited (“ZDSE”) the Company is engaged in the business of professional management coaching, including researching, developing and applying methods for helping individuals to improve their personal and professional leadership skills and effectiveness. ZDSE’s clients consist of executive managers from large scale, small and medium-sized enterprises, as well as professionals and employees in various fields.

ZDSE has developed “The Way of Management” program with ten modules now, and more modules to be developed in the future. The current ten modules comprise the experiential course, which is comprised 60% of scenario exercises, 20% of group interactions and 20% of specified topics. ZDSE also monitors the performance and the changes and developments of clients in their workplaces, and ZDSE’s coaches provide guidance and support to the company’s clients both during completion of the modules and during the provision of post-completion services. The current ten modules are:

| ● | Exploration Management – helps clients recognize their behavioral patterns in corporate management and decision-making, identify their own deficiencies or human frailties, such as selfishness or greed, and discover the gap between themselves and the ideal manager. | |

| ● | Innovation Management - helps clients learn how to build an effective and productive team. | |

| ● | Practice Management – helps each client accomplish a personal business goal that the client has derived from the two previous modules. | |

| ● | Management Art – helps clients develop communication skills, including listening and questioning, as well as how to give constructive feedback. | |

| ● | Personality Management - helps clients learn how to deal with difficult personalities. | |

| ● | Foundations of Management – helps clients discover their core values and how they impact their decisions and their management style. | |

| ● | Relationship Management – helps clients understand and accept themselves – their strengths and their weaknesses – and helps them understand their own needs. | |

| ● | Positivity – helps clients achieve a positive mindset and approach work and life with a positive attitude. | |

| ● | Leadership Development for Women – helps female clients succeed within a masculine culture. | |

| ● | Fund Management – helps clients learn how to manage capital, use capital correctly and diversify their investments, as well as how to understand their relationship with money and to keep the acquisition of money in perspective. |

ZDSE believes that its team of coaches is crucial to the success of the company, and it has a team of professional and innovative coaches, most of have either master’s or doctoral degrees in their various professions as well as experience in the field of leadership development coaching. It also believes in the importance of innovation and continual improvement, and its four-member program development team analyzes the latest market trends and demand and regularly collects feedback from clients to improve the quality of the coaching experience offered by ZDSE.

ZDSE is headquartered in Shenzhen, and has established branches in Guangzhou, Shandong and Liaoning, China. Its management intends to establish additional branches in Jiangsu, Beijing, Shanghai, Chongqing and Xiamen within three to six years. By 2018, the company had coached 2,188 entrepreneurs, as well as personnel from more than 32 corporate training services and large listed companies. The types of companies served include real estate, high technology, medicine, health, schools, government agencies, auto industry, communications, logistics, robotics, property, construction, engineering, manufacturing, textile, rag trade, furniture and other fields.

| 5 |

Risk Factors

Investing in our Ordinary Shares involves risks. You should carefully consider the risks described in “Risk Factors” beginning on page 8 of this prospectus before making a decision to purchase Ordinary Shares. If any of these risks actually occurs, our business, financial condition or results of operations would likely be materially adversely affected. In such case, the trading price of our Ordinary Shares would likely decline, and you may lose all or part of your investment.

Our Securities

Our authorized capital is $50,000, consisting of 500,000,000 shares, $0.0001 par value per share. Holders of our Ordinary Shares are entitled to one vote for each whole share on all matters to be voted upon by shareholders, including the election of directors. Holders of our Ordinary Shares do not have cumulative voting rights in the election of directors. All of our fully paid Ordinary Shares are equal to each other with respect to dividend rights. Holders of our Ordinary Shares are entitled to receive dividends if and when declared by our Board of Directors out of funds legally available therefor under Cayman Islands law. In the event of our liquidation, the liquidator may, with the sanction of an Ordinary Resolution of the Company, divide among the shareholders in specie or in kind the whole or any part of the assets of the Company (whether they shall consist of property of the same kind or not) and may for such purpose set such value as he deems fair upon any property to be divided as aforesaid and may determine how such division shall be carried out as between the shareholders or different classes of shareholders. Holders of our Ordinary Shares have no preemptive rights to purchase any additional unissued Ordinary Shares. The Board of Directors has the ability to determine the rights, preferences and restrictions of preferred shares at their discretion.

As of October 31, 2019, there were 302,734,900 of our Ordinary Shares issued and outstanding. All shares were fully paid. We do not have any options to purchase shares or any preferred shares outstanding. (For a more complete description of our Ordinary Shares, see “Description of Share Capital,” below.)

Implications of Being an Emerging Growth Company and a Foreign Private Issuer

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). As an emerging growth company, we may take advantage of certain exemptions from specified disclosure and other requirements that are otherwise generally applicable to public companies. These exemptions include:

| ● | being permitted to provide only two years of audited financial statements, in addition to any required unaudited interim financial statements, with correspondingly reduced “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure; | |

| ● | not being required to comply with the auditor attestation requirements for the assessment of our internal control over financial reporting provided by Section 404 of the Sarbanes-Oxley Act of 2002; | |

| ● | reduced disclosure obligations regarding executive compensation; and | |

| ● | not being required to hold a nonbinding advisory vote on executive compensation or seek shareholder approval of any golden parachute payments not previously approved. |

We may take advantage of these provisions for up to five years or such earlier time that we are no longer an emerging growth company. We would cease to be an emerging growth company upon the earliest to occur of (i) the last day of the fiscal year in which we have more than $1.0 billion in annual revenue; (ii) the date we qualify as a “large accelerated filer,” with at least $700 million of equity securities held by non-affiliates; (iii) the issuance, in any three-year period, by our company of more than $1.0 billion in non-convertible debt securities; or (iv) the last day of the fiscal year ending after the fifth anniversary of the date of the first sale of common equity securities pursuant to an effective registration statement.

| 6 |

We are also considered a “foreign private issuer” and will report under the Exchange Act as a non-U.S. company with foreign private issuer status. This means that, even after we no longer qualify as an emerging growth company, as long as we qualify as a foreign private issuer under the Exchange Act, we will be exempt from certain provisions of the Exchange Act that are applicable to U.S. domestic public companies, including:

| ● | the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations in respect of a security registered under the Exchange Act; | |

| ● | the sections of the Exchange Act requiring insiders to file public reports of their stock ownership and trading activities and liability for insiders who profit from trades made in a short period of time; and | |

| ● | the rules under the Exchange Act requiring the filing with the Securities and Exchange Commission of quarterly reports on Form 10-Q containing unaudited financial and other specified information, or current reports on Form 8-K, upon the occurrence of specified significant events. |

We may take advantage of these exemptions until such time as we are no longer a foreign private issuer. We would cease to be a foreign private issuer at such time as more than 50% of our outstanding voting securities are held by U.S. residents and any of the following three circumstances applies: (i) the majority of our executive officers or directors are U.S. citizens or residents, (ii) more than 50% of our assets are located in the United States, or (iii) our business is administered principally in the United States.

We may choose to take advantage of some but not all of these reduced burdens. We have taken advantage of reduced reporting requirements in this prospectus. Accordingly, the information contained herein may be different from the information you receive from our competitors that are public companies, or other public companies in which you have made an investment.

Notes on Prospectus Presentation

Numerical figures included in this prospectus have been subject to rounding adjustments. Accordingly, numerical figures shown as totals in various tables may not be arithmetic aggregations of the figures that precede them. Certain market data and other statistical information contained in this prospectus is based on information from independent industry organizations, publications, surveys and forecasts. Some market data and statistical information contained in this prospectus are also based on management’s estimates and calculations, which are derived from our review and interpretation of the independent sources listed above, our internal research and our knowledge of the executive coaching industry. While we believe such information is reliable, we have not independently verified any third-party information and our internal data has not been verified by any independent source.

Accordingly, actual events or circumstances may differ materially from events and circumstances that are assumed in this information and you are cautioned not to give undue weight to such data.

Securities Being Offered by Selling Shareholders

The Selling Shareholders are offering up to 8,734,900 Ordinary Shares. The Selling Shareholders may sell their Ordinary Shares at prevailing market prices or privately negotiated prices. We will not receive any proceeds from the sales by the Selling Shareholders.

Transfer Agent

The transfer agent for the Company’s Ordinary Shares is V Stock transfer, 18 Lafayette Place, Woodmere, New York 11598; telephone: 212-828-8436, toll-free: 855-9VSTOCK; facsimile: 646-536-3179.

| 7 |

Investing in our Ordinary Shares involves a high degree of risk. You should carefully consider the following risks and all other information contained in this prospectus, including our financial statements, consolidated financial statements and the related notes, before making an investment decision regarding our securities. The risks and uncertainties described below are those significant risk factors, currently known and specific to us that we believe are relevant to an investment in our securities. If any of these risks materialize, our business, financial condition or results of operations could suffer, the price of our Ordinary Shares could decline and you could lose part or all of your investment.

Risks Related to Our Business

Our limited operating history makes it difficult to evaluate our future prospects and results of operations.

The Company is in the process of developing its business and has a limited operating history. You should consider our future prospects in light of the risks and uncertainties experienced by early stage companies. Some of these risks and uncertainties relate to our ability to:

| ● | offer products of sufficient quality to attract and retain a larger client base; | |

| ● | attract additional clients and increase spending per client; | |

| ● | increase awareness of our products and continue to develop client loyalty; | |

| ● | respond to competitive market conditions; | |

| ● | respond to changes in our regulatory environment; | |

| ● | maintain effective control of our costs and expenses; | |

| ● | raise sufficient capital to sustain and expand our business; and | |

| ● | attract, retain and motivate qualified personnel. |

If we are unsuccessful in addressing any of these risks and uncertainties, our business may be materially and adversely affected.

We envision a period of rapid growth that may impose a significant burden on our administrative and operational resources which, if not effectively managed, could impair our growth.

Our strategy envisions a period of rapid growth that may impose a significant burden on our administrative and operational resources. The growth of our business will require significant investments of capital and management’s close attention. Our ability to effectively manage our growth will require us to substantially expand the capabilities of our administrative and operational resources and to attract, train, manage and retain qualified management, IT, sales and marketing, coaching and other personnel; we may be unable to do so. In addition, our failure to successfully manage our growth could result in our sales not increasing commensurately with capital investments. If we are unable to successfully manage our growth, we may be unable to achieve our goals.

We may not be able to raise the additional capital necessary to execute our business strategy, which could result in the curtailment of our operations.

We will need to raise additional funds to fully fund our existing operations and for development and expansion of our business. We have no current arrangements with respect to sources of additional financing and the needed additional financing may not be available on commercially reasonable terms, on a timely basis or at all. The inability to obtain additional financing when needed would have a negative effect on us, including possibly requiring us to curtail our operations. If any future financing involves the sale of equity securities, the shares held by our shareholders could be substantially diluted. If we borrow money or issue debt securities, the Company will be subject to the risks associated with indebtedness, including the risk that interest rates may fluctuate and the possibility that it may not be able to pay principal and interest on the indebtedness when due. Insufficient funds would prevent us from implementing our business plan and would require us to delay, scale back or eliminate certain of our operations.

| 8 |

We will be required to hire and retain skilled managerial personnel, IT and sales and marketing personnel.

Our continued success depends in large part on our ability to attract, train, motivate and retain qualified management, IT, sales and marketing and coaching personnel. Any failure to attract and retain the required managerial, technical and coaching personnel that are integral to our business may have a negative impact on our operations, which would have a negative impact on revenues. There can be no assurance that we will be able to attract and retain skilled persons and the loss of skilled coaches or technical personnel would adversely affect us.

We are dependent upon our officers and management for direction and the loss of any of these persons could adversely affect our operations and results.

We are dependent upon our officers for implementation of our proposed strategy and execution of our business plan. The loss of any of our officers could have a material adverse effect upon our results of operations and financial position. We do not maintain “key person” life insurance for any of our officers. The loss of any of our officers could delay or prevent the achievement of our business objectives.

We currently have only one operating subsidiary.

We are a holding company with a total of six subsidiaries; however, at the current time only one of those subsidiaries, Zhongdehui (Shenzhen) Education Development Co., Limited (“ZDSE”), is conducting operations. Therefore, we are totally dependent on ZDSE for our revenue. Although management intends that two more of the Company’s subsidiaries will commence operations in the near future, there can be no assurance that either of those subsidiaries will succeed in doing so or that, if started, either of those businesses will produce revenue. All of the operating subsidiaries would conduct their operations in the PRC.

We may be sued or become a party to litigation, which could require significant management time and attention and result in significant legal expenses and may result in an unfavorable outcome, which could have a material adverse effect on our business, financial condition, results of operations and cash flows.

We may be subject to a number of lawsuits from time to time arising in the ordinary course of our business. The expense of defending ourselves against such litigation may be significant. The amount of time to resolve these lawsuits is unpredictable and defending ourselves may divert management’s attention from the day-to-day operations of our business, which could adversely affect our business, results of operations and cash flows. In addition, an unfavorable outcome in such litigation could have a material adverse effect on our business, results of operations and cash flows.

Resales of our Ordinary Shares in the public market by the Selling Shareholders may cause the market price of our Ordinary Shares to decline.

Sales of Resale Shares could result in resales of our Ordinary Shares by our current shareholders concerned about the potential dilution of their holdings. In turn, these resales could have the effect of depressing the market price for our Ordinary Shares.

We are an emerging growth company within the meaning of the Securities Act and will take advantage of certain reduced reporting requirements.

We are an “emerging growth company,” as defined in the JOBS Act and take advantage of certain exemptions from various requirements applicable to other public companies that are not emerging growth companies including, most significantly, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act for so long as we are an emerging growth company. As a result, if we elect not to comply with such auditor attestation requirements, our investors may not have access to certain information they may deem important.

| 9 |

The JOBS Act also provides that an emerging growth company does not need to comply with any new or revised financial accounting standards until such date that a private company is otherwise required to comply with such new or revised accounting standards. The Company has elected to use the extended transition period for complying with new or revised accounting standard under Section 102(b)(2) of the Jobs Act, that allows the Company to delay the adoption of new or revised accounting standards that have different effective dates for public and private companies until those standards apply to private companies.

We have identified material weaknesses in our internal control over financial reporting. If we fail to maintain an effective system of internal control over financial reporting, we may not be able to accurately report our financial results or prevent fraud. As a result, stockholders could lose confidence in our financial and other public reporting, which would harm our business and the trading price of our shares.

Effective internal control over financial reporting is necessary for us to provide reliable financial reports and, together with adequate disclosure controls and procedures, are designed to prevent fraud. Any failure to implement required new or improved controls, or difficulties encountered in their implementation, could cause us to fail to meet our reporting obligations. Ineffective internal control could also cause investors to lose confidence in our reported financial information, which could have a negative effect on the trading price of our shares.

We have identified material weaknesses in our internal control over financial reporting in the Company and in HGSL and its subsidiaries. As defined in Regulation 12b-2 under the Exchange Act, a “material weakness” is a deficiency, or combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of our annual or interim consolidated financial statements will not be prevented, or detected on a timely basis. Specifically, we determined that we had the following material weaknesses in our internal control over financial reporting: (i) we have limited controls over information processing; (ii) we have inadequate segregation of duties; (iii) we do not have a formal audit committee with a financial expert; and (iv) we do not have sufficient formal written policies and procedures for accounting and financial reporting with respect to the requirements and application of both generally accepted accounting principles in the United States of America, or GAAP, and SEC guidelines.

The Company intends to utilize a third-party independent contractor for the preparation of our financial statements in the future in an effort to remediate the deficiency. The implementation of this initiative will not fully address any material weakness or other deficiencies that we may have in our internal control over financial reporting. Although the financial statements and footnotes are reviewed by our management, we do not have a formal policy to review significant accounting transactions and the accounting treatment of such transactions. The third-party independent contractor is not involved in the day-to-day operations of the Company and may not be provided information from management on a timely basis to allow for adequate reporting/consideration of certain transactions.

Even if we develop effective internal controls over financial reporting, such controls may become inadequate due to changes in conditions, or the degree of compliance with such policies or procedures may deteriorate, which could result in the discovery of additional material weaknesses and deficiencies. In any event, the process of determining whether our existing internal control over financial reporting is compliant with Section 404 of the Sarbanes-Oxley Act (“Section 404”) and is sufficiently effective requires the investment of substantial time and resources by our senior management. As a result, this process may divert internal resources and take a significant amount of time and effort to complete. In addition, we cannot predict the outcome of this process and whether we will need to implement remedial actions in order to establish effective controls over financial reporting. The determination of whether or not our internal controls are sufficient, and any remedial actions required could result in us incurring additional costs that we did not anticipate, including the hiring of additional outside consultants. We may also fail to timely complete our evaluation, testing and any remediation required to comply with Section 404.

| 10 |

We are required, pursuant to Section 404, to furnish a report by management on, among other things, the effectiveness of our internal control over financial reporting. However, for as long as we are a “smaller reporting company,” our independent registered public accounting firm will not be required to attest to the effectiveness of our internal control over financial reporting pursuant to Section 404. While we could be a smaller reporting company for an indefinite amount of time, and thus relieved of the above-mentioned attestation requirement, an independent assessment of the effectiveness of our internal control over financial reporting could detect problems that our management’s assessment might not. Such undetected material weaknesses in our internal control over financial reporting could lead to financial statement restatements and require us to incur the expense of remediation.

Our independent auditors have issued an audit opinion for the Company, which includes a statement describing its going concern status. Our financial status creates a doubt as to whether the Company will continue as a going concern.

Our auditors have issued a going concern opinion regarding the Company. This means there is substantial doubt as to whether it can continue as an ongoing business for the next twelve months. The financial statements do not include any adjustments that might result from the uncertainty regarding the Company’s ability to continue in business. As such, we may have to cease operations and investors could lose part or all of their investment in the Company.

To the extent that our independent registered public accounting firm’s audit documentation related to their audit reports for the Company are, or will be, located in China, the PCAOB may not be able to inspect such audit documentation and, as a result, you may be deprived of the benefits of such inspection.

Our independent registered public accounting firm issued an audit opinion on the financial statements included in this prospectus and will issue audit reports related to the Company in the future. As the auditor of a company filing reports with the SEC and as a firm registered with the PCAOB, our auditor is required by the laws of the United States to undergo regular inspections by the PCAOB. However, to the extent that our auditor’s work papers are or become located in China, such work papers will not be subject to inspection by the PCAOB because the PCAOB is currently unable to conduct inspections without the approval of the Chinese authorities. Inspections of certain other firms that the PCAOB has conducted outside of China have identified deficiencies in those firms’ audit procedures and quality control procedures, which may be addressed as part of the inspection process to improve future audit quality. The inability of the PCAOB to conduct inspections of our auditors’ work papers in China would make it more difficult to evaluate the effectiveness of our auditor’s audit procedures or quality control procedures as compared to auditors outside of China that are subject to PCAOB inspections. Investors may consequently lose confidence in our reported financial information and procedures and the quality of our financial statements. As a result, our investors may be deprived of the benefits of the PCAOB’s oversight of our auditors through such inspections.

Risks Related to the Business of Our Sole Operating Subsidiary

Our business depends on the market recognition of our brand. If we are not able to maintain our reputation and enhance our brand recognition, our business and operating results may be materially and adversely affected.

Our track record in providing quality coaching services will determine whether our sole operating subsidiary, Zhongdehui (Shenzhen) Education Development Co., Limited (“ZDSE”) becomes recognized as a leading brand in the industry. We believe that market recognition of our brand is a key factor to ensuring our future success. As we continue to grow in size and broaden the scope of our program and services, however, it may become increasingly difficult to maintain the quality and consistency of the services we offer, which may negatively impact our brand and the popularity of our products and services offered thereunder.

| 11 |

Our brand value will also be affected by client perceptions. Those perceptions are affected by a number of factors; some of them are based on first-hand observation of our service quality while others may be based on indirect information from media or other sources. Incidents and any negative publicity related thereto, even if factually incorrect, may lead to significant deterioration of our brand image and reputation, and consequently negatively affect clients’ interest in our services and products, as well as top-notch executive coaches’ interest in being associated with our brand. Particularly in the age of digital media and social network, impacts of negative publicity associated with any single incident could be easily amplified and potentially cause impacts that go beyond our estimation or control.

In addition, scientific studies on education are constantly evolving and new or innovative conclusions on education methodologies or philosophies may affect clients’ perceptions of our services and products. If we are unable to maintain our reputation, enhance our brand recognition or increase positive awareness of our coaching products and services, it may be difficult to maintain and grow client enrollment or attract more business partners to join our network, and our business and growth prospects may be materially and adversely affected.

If we fail to maintain and increase client subscriptions for our services, our revenues may decline, and we may not be able to reach profitability.

The success of our business depends largely on the number of clients. Therefore, our ability to continue to attract new clients and to retain existing clients is critical to our continued success and growth. Our client enrollment is affected by several factors, including our ability to develop new program materials and improve existing modules, expand our geographic reach, manage our growth while maintaining consistent and high coaching and service quality, effectively market and precisely target our services to a broader base of prospective clients and respond effectively to competition. If we are unable to continue to attract a sufficient number of new clients or to retain existing clients, our revenues may decline or we may not be able to reach profitability, either of which could have a material adverse effect on our business, financial condition and results of operations.

Our business relies on our ability to recruit, train and retain dedicated and qualified coaches and management personnel.

Our coaches are critical to the quality of our services and our reputation. We seek to recruit, train and retain qualified and dedicated coaches; however, there is a limited pool of executive coaches with the attributes we require. In addition, any foreign coaches we hire must hold valid working permits, which may not be obtained in a timely manner, or at all. Despite our various initiatives, investments to secure qualified personnel and competitive compensation, we still may not be able to recruit, train and retain sufficient qualified coaches to keep pace with our growth while maintaining consistent coaching quality in the different markets we serve. A shortage of qualified coaches or a deterioration in the quality of our coaches’ services, whether actual or perceived, or a significant increase in the average compensation paid by our competitors to their coaches would have a material adverse effect on our business, financial condition and results of operations.

Competition

The leadership and executive coaching market in China is rapidly evolving, highly fragmented and intensely competitive with relatively easy entry. Competition in this industry may persist and even intensify. As more competitors enter the market, we will have to compete based on brand image, program content and structure and service quality. New competitors may enter the market and one or more of our competitors may develop and implement training courses or methodologies that may adversely affect our ability to sell our services to new clients. Competitors continually introduce new programs and services that may compete directly with our services, or that may make our programs uncompetitive or obsolete. Larger competitors may have superior abilities to compete for clients and skilled professionals, reducing our ability to deliver quality work to our clients. Some of our competitors may have greater financial or other resources than we do. We cannot assure you that we will be able to compete successfully against existing or potential competitors, and if we fail to gain or maintain, or if we lose market share, our business, financial condition and results of operations may be materially and adversely affected.

| 12 |

We may not be successful in introducing new products or enhancing our existing products.

We currently offer only one module sequence - “The Way of Management.” We intend to continue developing new products, as well as further enhancing our existing products. This process is subject to risks and uncertainties, such as unexpected technical, operational, logistical or other problems that could delay the process temporarily or permanently. Moreover, we cannot assure you that any of these new products or enhancements of existing products will fulfill client needs, match the quality or popularity of those developed by our competitors, achieve widespread market acceptance or generate incremental revenues.

In addition, introducing new products or enhancing existing products requires us to make various investments in program and materials development and management, incur personnel expenses and potentially reallocate other resources. If we are unable to develop new products or cannot do so in a cost-effective manner or are otherwise unable to manage effectively the operations of those products, our financial condition and results of operations could be adversely affected.

Our success depends on the continuing efforts of our senior management team and other key personnel and our business may be harmed if we lose their services.

Our success depends in part on the continued application of services, efforts and motivation of our senior management team and key personnel. If one or more of our senior management members or key personnel are unable to continue in their present positions, we may not be able to find replacements successfully, and our business may be disrupted.

We will need to continue to hire additional personnel as our business grows. A shortage in the supply of personnel with the requisite skills could negatively impact our ability to manage our existing products and services, launch new products and expand our operations. There is competition for experienced personnel in the executive coaching industry and key personnel could leave us to join our competitors. Losing the services of our experienced personnel may be disruptive to and cause uncertainty for our business, which may have a material adverse effect on our business, financial condition and results of operations.

We could incur additional liabilities or our reputation could be damaged if we do not protect client data or if our information systems are breached.

We are dependent on information technology networks and systems to process, transmit and store electronic information and to communicate between our locations around China and with our clients. Security breaches of this infrastructure could lead to shutdowns or disruptions of our systems and potential unauthorized disclosure of confidential information. We are also required at times to manage, utilize and store sensitive or confidential client or employee data. As a result, we are subject to laws and regulations designed to protect this information. If any person, including any of our employees, mismanages or misappropriates such data, we could be subject to monetary damages, fines and/or criminal prosecution. Unauthorized disclosure of sensitive or confidential client or employee data, whether through systems failure, employee negligence, fraud or misappropriation could damage our reputation and cause us to lose clients.

Legal requirements relating to the collection, storage, handling, and transfer of personal data continue to evolve. China’s Cybersecurity Law (“CSL”), which came into effect in June 2017, regulates how organizations should protect digital information and outlines measures to safeguard Internet systems, products and services against cyberattacks. The CSL was supplemented in May 2018 with the Personal Information Security Specification, which was amended and strengthened in February 2019. Although these amendments attempt to ease the compliance burden placed on businesses, the laws could impose significant limitations, require changes to our business or restrict our use or storage of personal information, which may increase our compliance expenses and make our business more costly or less efficient to conduct.

| 13 |

Our business is sensitive to general economic conditions.

Our business may be negatively affected by a downturn in general economic conditions and rising labor and material costs in China. Furthermore, a serious and/or prolonged economic downturn combined with a negative or uncertain political climate could adversely affect our clients’ financial condition and the amount they are able to spend for our services. These conditions may reduce the demand for our services or depress the pricing of those services and have an adverse impact on our results of operations. Changes in global economic conditions may also shift demand to services for which we do not have competitive advantages, and this could negatively affect the amount of business that we are able to obtain. Such economic, political and client spending conditions are influenced by a wide range of factors that are beyond our control and that we have no comparative advantage in forecasting. If we are unable to successfully anticipate these changing conditions, we may be unable to effectively plan for and respond to those changes, and our business could be adversely affected.

Our business success also depends in part upon continued growth in the use of coaching. In challenging economic environments, our clients may reduce or defer their spending on new services and coaching solutions in order to focus on other priorities. At the same time, many companies have already invested substantial resources in their current means of conducting their business and they may be reluctant or slow to adopt new approaches that could disrupt existing personnel and/or processes. If growth in the general use of coaching services in business or our clients’ spending on these items declines, or if we cannot convince our clients or potential clients to embrace new services and solutions, our results of operations could be adversely affected.

In addition, our business tends to lag behind economic cycles and, consequently, the benefits of an economic recovery following a period of economic downturn may take longer for us to realize than other segments of the economy.

Risks Related to the People’s Republic of China

The Chinese government may exert substantial influence over the manner in which we conduct our business operations in China.

The Chinese government has exercised, and continues to exercise, substantial control over virtually every sector of the Chinese economy through regulation and state ownership. Our ability to conduct our coaching and consulting operations in China may be harmed by changes in its laws and regulations, including those relating to regulation of the coaching industry, taxation, import and export tariffs, environmental regulations, land use rights, property ownership and other matters. We believe that our operations in China are in material compliance with all applicable legal and regulatory requirements. However, the central or local governments of the jurisdictions in which we operate may impose new, stricter regulations or interpretations of existing regulations that would require additional expenditures and efforts on our part to ensure our compliance with such regulations or interpretations. Accordingly, government actions in the future could have a significant effect on us and our business.

China’s economic policies could affect our business.

All of our assets are located in China and all of our revenue is derived from our operations in China. Accordingly, our results of operations and prospects are subject, to a significant extent, to economic, political and legal developments in China.

While China’s economy has experienced significant growth over the past decades, growth has been irregular, both geographically and among various sectors of the economy, and the rate of growth has been slowing since 2012. Any adverse changes in economic conditions in China, in the policies of the Chinese government or in the laws and regulations in China could have a material adverse effect on the overall economic growth of China. Such developments could adversely affect our business and operating results, lead to reduction in demand for our services and adversely affect our competitive position. The Chinese government has implemented various measures to encourage economic growth and guide the allocation of resources. Some of these measures benefit the overall economy of China but may also have a negative effect on us. For example, our operating results and financial condition may be adversely affected by government control over capital investments or changes in tax regulations.

| 14 |

The economy of China has been transitioning from a planned economy to a more market-oriented economy. In recent years the Chinese government has implemented measures emphasizing the utilization of market forces for economic reform and the reduction of state ownership of productive assets and the establishment of improved corporate governance in business enterprises. In addition, the Chinese government continues to play a significant role in regulating industry development by imposing industrial policies. It also exercises significant control over China’s economic growth through the allocation of resources, controlling payment of foreign currency-denominated obligations, setting monetary policy and providing preferential treatment to particular industries or companies.

Fluctuation of the RMB may affect our financial condition by affecting the volume of cross-border money flow.

The value of the RMB is subject to changes in the PRC’s political and economic conditions. Since July 2005, the conversion of RMB into foreign currencies, including USD, has been based on rates set by the People’s Bank of China which are set based upon the interbank foreign exchange market rates and current exchange rates of a basket of currencies on the world financial markets.

We may face obstacles from the communist system in the PRC.

Foreign companies conducting operations in the PRC face significant political, economic and legal risks. The communist regime in the PRC may hinder Western investment.

We may have difficulty establishing adequate management, legal and financial controls in the PRC.

The PRC historically has been deficient in Western style management and financial reporting concepts and practices, as well as in modern banking, computer and other control systems. We may have difficulty in hiring and retaining a sufficient number of qualified employees to work in the PRC. As a result of these factors, we may experience difficulty in establishing management, legal and financial controls, collecting financial data and preparing financial statements, books of account and corporate records and instituting business practices that meet Western standards.

Because our assets and operations are located in China, you may have difficulty enforcing any civil liabilities against us under the securities and other laws of the United States or any state.

We are a holding company, and all of our assets are located in the PRC. In addition, our directors and officers are non-residents of the United States, and all or a substantial portion of the assets of these non-residents are located outside the United States. As a result, it may be difficult for investors to effect service of process within the United States upon these non-residents, or to enforce against them judgments obtained in United States courts, including judgments based upon the civil liability provisions of the securities laws of the United States or any state.

There is uncertainty as to whether courts of the PRC would enforce:

| ● | Judgments of United States courts obtained against us or these non-residents based on the civil liability provisions of the securities laws of the United States or any state; or | |

| ● | In original actions brought in the PRC, liabilities against us or non-residents predicated upon the securities laws of the United States or any state. |

Enforcement of a foreign judgment in the PRC also may be limited or otherwise affected by applicable bankruptcy, insolvency, liquidation, arrangement, moratorium or similar laws relating to or affecting creditors’ rights generally and will be subject to a statutory limitation of time within which proceedings may be brought.

| 15 |

The PRC legal system embodies uncertainties, which could limit law enforcement availability.

The PRC legal system is a civil law system based on written statutes. Unlike common law systems, decided legal cases have little precedence. In 1979, the PRC government began to promulgate a comprehensive system of laws and regulations governing economic matters in general. The overall effect of legislation over the past several decades has significantly enhanced the protections afforded to various forms of foreign investment in China. Our PRC subsidiaries are subject to PRC laws and regulations. However, these laws and regulations change frequently, and the interpretation and enforcement involve uncertainties. For instance, we may have to resort to administrative and court proceedings to enforce the legal protection that we are entitled to by law or contract. However, since PRC administrative and court authorities have significant discretion in interpreting statutory and contractual terms, it may be difficult to evaluate the outcome of administrative court proceedings and the level of law enforcement that we would receive in more developed legal systems. Such uncertainties, including the inability to enforce our contracts, could affect our business and operation. In addition, confidentiality protections in China may not be as effective as in the United States or other countries. Accordingly, we cannot predict the effect of future developments in the PRC legal system, particularly with regard to our business, including the promulgation of new laws. This may include changes to existing laws or the interpretation or enforcement thereof, or the preemption of local regulations by national laws. These uncertainties could limit the availability of law enforcement, including our ability to enforce our agreements.

Failure to make adequate contributions to various employee benefit plans as required by PRC regulations may subject us to penalties.

Companies operating in China are required to participate in various government sponsored employee benefit plans, including certain social insurance, housing funds and other welfare-oriented payment obligations, and contribute to the plans in amounts equal to certain percentages of salaries, including bonuses and allowances, of employees up to a maximum amount specified by the local government from time to time at locations where they operate their businesses. The requirement of employee benefit plans has not been implemented consistently by the local governments in China given the different levels of economic development in different locations. Our failure in making contributions to various employee benefit plans and in complying with applicable PRC labor-related laws may subject us to late payment penalties. We may be required to make up the contributions for these plans as well as to pay late fees and fines. If we are subject to late fees or fines in relation to the underpaid employee benefits, our financial condition and results of operations may be adversely affected.

We may rely on dividends and other distributions on equity paid by our PRC subsidiaries to fund any cash and financing requirements we may have, and any limitation on the ability of our PRC subsidiaries to make payments to us could have a material and adverse effect on our ability to conduct our business.

We are a Cayman Islands holding company and we rely principally on dividends and other distributions on equity from our PRC subsidiaries for our cash requirements, including for services of any debt we may incur. Our PRC subsidiaries’ ability to distribute dividends is based upon their distributable earnings. Current PRC regulations permit our PRC subsidiaries to pay dividends to their shareholders only out of their accumulated profits, if any, determined in accordance with PRC accounting standards and regulations. In addition, each of our PRC subsidiaries is required to set aside at least 10% of its after-tax profits each year, if any, to fund a statutory reserve until such reserve reaches 50% of its registered capital. Our PRC subsidiaries, as foreign invested enterprises, or FIEs, are also required to further set aside a portion of their after-tax profit to fund an employee welfare fund, although the amount to be set aside, if any, is determined at their discretion. These reserves are not distributable as cash dividends. If our PRC subsidiaries incur debt on their own behalf in the future, the instruments governing the debt may restrict their ability to pay dividends or make other payments to us. Any limitation on the ability of our PRC subsidiaries to distribute dividends or other payments to their shareholders could materially and adversely limit our ability to grow, make investments or acquisitions that could be beneficial to our business, pay dividends or otherwise fund and conduct our business.

| 16 |

Changes to PRC tax laws may subject us to greater taxes.

We base our tax position upon the anticipated nature and conduct of our business and upon our understanding of the tax laws of the various administrative regions and countries in which we have assets or conduct activities. However, our tax position is subject to review and possible challenge by taxing authorities and to possible changes in law, which may have retroactive effect. We cannot determine in advance the extent to which some jurisdictions may require us to pay taxes or make payments in lieu of taxes.

Risks Related to the Company’s Shares

There is currently no trading market for our shares.

There currently is no trading market for our shares. Our outstanding shares cannot be offered, sold, pledged or otherwise transferred into or in the United States unless subsequently registered pursuant to, or exempt from registration under, the Securities Act and any other applicable federal or state securities laws or regulations in the United States. These restrictions will limit the ability of our shareholders to liquidate their investment.

The registration statement of which this prospectus is a part registered a portion of our outstanding shares for resale in the United States. We will seek to identify a market maker to apply for our shares to be admitted to quotation on the OTC Markets. We cannot assure you that we will be able to identify a market maker that will file such application or that, if the shares are admitted to quotation, a public market will ever develop. There is no guarantee that our shares will ever be quoted on the OTC Markets or any exchange. Furthermore, you will likely not be able to sell your securities if a regular trading market for our securities does not develop and we cannot predict the extent, if any, to which investor interest will lead to the development of a viable trading market in our shares. We expect the initial market for our shares to be limited, if a market develops at all. Even if a limited trading market does develop, there is a risk that the absence of potential buyers will prevent any potential sellers from selling their shares.

It is likely that there will be significant volatility in the trading price of our shares.

In the event that a public market for our Ordinary Shares is created or maintained in the future, market prices for the shares will be influenced by many factors and will be subject to significant fluctuations in response to variations in operating results of ZDSE and other factors. Our stock price will also be affected by the trading price of the stock of our competitors, investor perceptions of ZDSE, interest rates, general economic conditions and those specific to our industry, developments with regard to ZDSE’s operations and activities, our future financial condition and changes in our management.

Risks relating to low priced stocks

The Company’s Ordinary Shares are not quoted and traded on the OTC Markets, and the price at which the shares will trade in the future cannot currently be estimated. There can be no assurance that trading will be commenced or sustained, although management intends to take such actions as are necessary to initiate trading on the OTC Markets. The trading price of the shares will most likely be below $5.00. If our shares trade below $5.00 per share, trading in the shares may be subject to the requirements of certain rules promulgated under the Exchange Act, which require additional disclosure by broker-dealers in connection with any trades involving a stock defined as a penny stock (generally, any non-Nasdaq equity security that has a market price of less than $5.00 per share, subject to certain exceptions) and a two business day “cooling off period” before broker-dealers can effect transactions in penny stocks. For these types of transactions, the broker-dealer must make a special suitability determination for the purchaser and have received the purchaser’s written consent to the transaction prior to the sale. The broker-dealer also must disclose the commissions payable to the broker-dealer, current bid and offer quotations for the penny stock and, if the broker-dealer is the sole market-maker, the broker-dealer must disclose this fact and the broker-dealer’s presumed control over the market. These, and the other burdens imposed upon broker-dealers by the penny stock requirements, could discourage broker-dealers from effecting transactions in our shares which could severely limit the market liquidity of our shares and the ability of holders of our shares to sell them.

| 17 |

We do not intend to pay dividends.

We have not paid any cash dividends on any of our securities since inception and we do not anticipate paying any cash dividends on any of our securities in the foreseeable future.

Future sales of our securities, or the perception in the markets that these sales may occur, could depress our stock price.

We currently have issued and outstanding approximately 302,734,900 Ordinary Shares. Although only 8,734,900 of those shares have been registered for resale under the registration statement of which this prospectus is a part, the remaining 294,000,000 shares also may be sold in the future if registered under the Securities Act or if the shareholder qualifies for an exemption from registration under Rule 144, Rule 701, or other applicable exemption under the Securities Act. The market price of our capital stock could drop significantly if the holders of these restricted shares sell them or are perceived by the market as intending to sell them. These factors also could make it more difficult for us to raise capital or make acquisitions through the issuance of additional Ordinary Shares or other equity securities.

The ability of the Board of Directors of the Company to issue preferred shares and any anti-takeover provisions we adopt may depress the value of our Ordinary Shares.

Our Articles of Association authorize our Board of Directors to provide, out of unissued shares, for preferred shares in one or more classes or series within a class upon authority of the Board without further shareholder approval. Any preferred shares issued in the future may rank senior to the Ordinary Shares with respect to the payment of dividends or amounts upon liquidation, dissolution or winding up of the Company, or both, and any such preferred shares may have class or series voting rights. In addition, the Board of Directors may, in the future, adopt anti-takeover measures. The authority of the Board of Directors to issue preferred shares and any future anti-takeover measures it may adopt may, in certain circumstances, delay, deter or prevent takeover attempts and other changes in control of the Company not approved by its Board of Directors. As a result, the Company’s shareholders may lose opportunities to dispose of their shares at favorable prices generally available in takeover attempts or that may be available under a merger proposal and the market price of the Ordinary Shares and the voting and other rights of the Company’s shareholders may also be affected.

Our shareholders may face difficulties in protecting their interests, and their ability to protect their rights through the U.S. federal courts may be limited because we are incorporated under Cayman Islands law, we conduct substantially all of our operations in China and all of our directors and officers reside outside the United States.

We are incorporated in the Cayman Islands and conduct substantially all of our operations in China. All of our directors and officers reside outside the United States and their assets are located outside of the United States. As a result, it may be difficult or impossible for a shareholder to bring an action against us or against these individuals in the Cayman Islands or in China in the event that a shareholder believes that his rights have been infringed under the securities laws or otherwise. Even if a shareholder is successful in bringing an action of this kind, the laws of the Cayman Islands and of China may render the shareholder unable to enforce a judgment against our assets or the assets of our directors and officers. There is no statutory recognition in the Cayman Islands of judgments obtained in the United States, although the courts of the Cayman Islands will generally recognize and enforce a non-penal judgment of a foreign court of competent jurisdiction without retrial on the merits.

| 18 |

Our corporate affairs are governed by our memorandum and articles of association, as amended and restated from time to time, and by the Companies Law (2018 Revision) and common law of the Cayman Islands. The rights of shareholders to take legal action against us and our directors, actions by minority shareholders and the fiduciary responsibilities of our directors are to a large extent governed by the common law of the Cayman Islands. The common law of the Cayman Islands is derived in part from comparatively limited judicial precedent in the Cayman Islands as well as from English common law, which provides persuasive, but not binding, authority on a court in the Cayman Islands. The rights of our shareholders and the fiduciary responsibilities of our directors under Cayman Islands law are not as clearly established as they would be under statutes or judicial precedents in the United States. In particular, the Cayman Islands has a less developed body of securities laws than the United States and provides significantly less protection to investors. In addition, Cayman Islands companies may not have standing to initiate a shareholder derivative action in U.S. federal courts. As a result, our shareholders may have more difficulty in protecting their interests through actions against us, our management, our directors or our major shareholders than would shareholders of a corporation incorporated in a jurisdiction in the United States.

Our shareholders do not have the same protections or information generally available to shareholders of U.S. corporations because the reporting requirements for foreign private issuers are more limited than those applicable to public corporations organized in the United States.