UNITED STATES SECURITIES AND

EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

|

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the quarterly period ended June 30, 2022

or

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from _________ to _____________

Commission file number: 001-38273

(Exact Name of Registrant as Specified in Its Charter)

|

|

|

|

|

(State or Other Jurisdiction of Incorporation or Organization)

|

|

(I.R.S. Employer Identification No.)

|

|

|

|

|

|

|

|

|

|

(Address of Principal Executive Offices)

|

|

(Zip Code)

|

Registrant’s telephone number, including area code: (510 ) 445-3700

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

|

Trading Symbol

|

|

Name of Each Exchange on which Registered

|

|

|

|

|

|

|

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act

of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data file required to be submitted pursuant to Rule 405

of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting

company or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

|

|

Accelerated filer

|

☐

|

|

|

Non-accelerated filer ☐

|

Smaller reporting company

|

|

|

|

|

Emerging growth company

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any

new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

|

Class

|

Number of Shares Outstanding

|

|

Class A Common Stock, $0.0001 par value

|

|

|

Class B Common Stock, $0.0001 par value

|

|

|

PART I.

|

5

|

||

|

Item 1.

|

5 | ||

| 5 | |||

| 6 | |||

| 7 | |||

| 9 | |||

| 10 | |||

|

Item 2.

|

35

|

||

|

Item 3.

|

63 | ||

|

Item 4.

|

63 | ||

|

PART II.

|

63 | ||

|

Item 1.

|

63 | ||

|

Item 1A.

|

64 | ||

|

Item 2.

|

71 | ||

|

Item 5.

|

Other Information

|

71 | |

|

Item 6.

|

72 | ||

| 73 | |||

ACM Research, Inc., or ACM Research, is a Delaware corporation founded in California in 1998 to supply capital equipment developed for the global semiconductor industry. Since 2005, ACM Research has conducted its business operations principally through its subsidiary ACM Research (Shanghai), Inc., or ACM Shanghai, a

limited liability corporation formed by ACM Research in the People’s Republic of China, or the PRC, in 2005. Unless the context requires otherwise, references in this report to “our company,” “our,” “us,” “we” and similar terms refer to ACM

Research, Inc. and its subsidiaries, including ACM Shanghai, collectively.

Our principal corporate office is located in Fremont, California. We conduct a substantial majority of our product development, manufacturing, support

and services in the PRC through ACM Shanghai. We perform, through a subsidiary of ACM Shanghai, additional product development and subsystem production in South Korea, and we conduct, through ACM Research, sales and marketing activities focused on

sales of ACM Shanghai products in North America, Europe and certain regions in Asia outside mainland China. ACM Research is not a PRC operating company, and we do not conduct our operations in the PRC through the use of a variable interest entity,

or VIE, or any other structure designed for the purpose of avoiding PRC legal restrictions on direct foreign investments in PRC-based companies. ACM Research has a direct ownership interest in ACM Shanghai as the result of its holding 82.5% of the

outstanding shares of ACM Shanghai. Stockholders of ACM Research may never directly own equity interests in ACM Shanghai. We do not believe that our corporate structure or any other matters relating to our business operations require that we obtain

any permissions or approvals from the China Securities Regulatory Commission, or the CSRC, or any other PRC central government authority in order to continue to list shares of Class A common stock of ACM Research on the Nasdaq Global Select Market.

We are subject to a number of legal and operational risks associated with our corporate structure, including as the result of a substantial portion

of our operations being conducted in the PRC. Consequences of any of those risks could result in a material adverse change in our operations or cause the value of ACM Research Class A common stock to significantly decline. Please carefully read

the information beginning on page 64 of this report and included in “Part II. Item 1A – Risk Factors,” in particular the risk factors addressing the following issues:

|

•

|

If any PRC central government authority were to determine that existing PRC laws or regulations require that ACM Shanghai obtain the

authority’s permission or approval to continue the listing of ACM Research’s Class A common stock in the United States or if those existing PRC laws and regulations, or interpretations thereof, were to change to require such

permission or approval, ACM Shanghai may be unable to obtain any such permission or approval or may only be able to obtain such permission or approval on terms and conditions that impose material new restrictions and limitations on

the operations of ACM Shanghai, either of which could have a material adverse effect on our business, financial condition, results of operations, reputation and prospects and on the trading price of ACM Research Class A common stock.

|

|

•

|

PRC central government authorities may intervene in, or influence, ACM Shanghai’s PRC-based operations at any time, and those

authorities’ rules and regulations can change quickly with little or no advance notice.

|

|

•

|

The PRC central government may determine to exert additional control over offerings conducted overseas or foreign investment in

PRC-based issuers, which could result in a material change in our operations and the value of ACM Research Class A common stock.

|

Recent statements and regulatory actions by PRC central government authorities with respect to the use of VIEs and to data security and

anti-monopoly concerns have not affected our ability to conduct our business operations in China. For further information, see “Part II. Item 1A – Risk Factors – Risks Related to International Aspects of Our Business.”

For purposes of this report, certain amounts in Renminbi, or RMB, have been translated into U.S. dollars solely for the

convenience of the reader. The translations have been made based on the conversion rates published by the State Administration of Foreign Exchange of the People’s Republic of China.

SAPS, TEBO, ULTRA C and ULTRA FURNACE are trademarks of ACM Research. For convenience, these trademarks appear in this report

without ™ symbols, but that practice does not mean that ACM Research will not assert, to the fullest extent under applicable law, ACM Research’s rights to the trademarks. This report also contains other companies’ trademarks, registered marks and

trade names, which are the property of those companies.

FORWARD-LOOKING STATEMENTS AND STATISTICAL DATA

This report contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. All statements, other

than statements of historical facts, included in this report regarding our strategy, future operations, future financial position, future revenue, projected costs, prospects, plans and objectives of management are forward-looking statements. In some

cases, you can identify forward-looking statements by terms such as “may,” “might,” “will,” “objective,” “intend,” “should,” “could,” “can,” “would,” “expect,” “believe,” “anticipate,” “project,” “target,” “design,” “estimate,” “predict,”

“potential,” “plan” or the negative of these terms, and similar expressions intended to identify forward-looking statements. These statements reflect our current views with respect to future events and are based on our management’s belief and

assumptions and on information currently available to our management. Although we believe that the expectations reflected in these forward-looking statements are reasonable, these statements relate to future events or our future operational or

financial performance, and involve known and unknown risks, uncertainties and other factors, including uncertainties surrounding the COVID‑19 pandemic (including effects of related PRC restrictions) and other factors described or incorporated by

reference in “Item 1A. Risk Factors” of Part II of this report, that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by these

forward-looking statements.

The information included under the heading “Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations –

Overview,” of Part I of this report contains statistical data and estimates, including forecasts, that are based on information provided by Gartner, Inc., or Gartner, in “Forecast: Semiconductor Wafer Fab Equipment, Worldwide, 4Q21 Update” (December

2021), or the Gartner Report. The Gartner Report represents research opinions or viewpoints that are published, as part of a syndicated subscription service, by Gartner and are not representations of fact. The Gartner Report speaks as of its original

publication date (and not as of the date of this report), and the opinions expressed in the Gartner Report are subject to change without notice. While we are not aware of any misstatements regarding any of the data presented from the Gartner Report,

estimates, and in particular forecasts, involve numerous assumptions and are subject to risks and uncertainties, as well as change based on various factors, that could cause results to differ materially from those expressed in the data presented

below.

Any forward-looking statement made by us in this report speaks only as of the date on which it is made. Except as required by law, we assume no

obligation to update these statements publicly or to update the reasons actual results could differ materially from those anticipated in these statements, even if new information becomes available in the future.

You should read this report, and the documents that we reference in this report and have filed as exhibits to this report, completely and with the

understanding that our actual future results may be materially different from what we expect. We qualify all of our forward-looking statements by these cautionary statements.

| PART I. |

FINANCIAL INFORMATION

|

| Item 1. |

Financial Statements

|

ACM RESEARCH, INC.

(In thousands, except per share data)

(Unaudited)

|

June 30,

2022

|

December 31,

2021

|

|||||||

|

Assets

|

||||||||

|

Current assets:

|

||||||||

|

Cash and cash equivalents

|

$

|

|

$

|

|

||||

|

Restricted cash

|

||||||||

|

Short-term time deposits (note 2)

|

||||||||

|

Trading securities (note 15)

|

|

|

||||||

|

Accounts receivable (note 4)

|

|

|

||||||

|

Income tax receivable

|

||||||||

|

Other receivables

|

|

|

||||||

|

Inventories (note 5)

|

|

|

||||||

|

Advances to related party (note 16)

|

||||||||

|

Prepaid expenses

|

|

|

||||||

|

Total current assets

|

|

|

||||||

|

Property, plant and equipment, net (note 6)

|

|

|

||||||

|

Land use right, net (note 7)

|

|

|

||||||

|

Operating lease right-of-use assets, net (note 11)

|

|

|

||||||

|

Intangible assets, net

|

|

|

||||||

| Long-term time deposits (note 2) | ||||||||

|

Deferred tax assets (note 19)

|

|

|

||||||

|

Long-term investments (note 14)

|

|

|

||||||

|

Other long-term assets (note 8)

|

|

|

||||||

|

Total assets

|

|

|

||||||

|

Liabilities and Equity

|

||||||||

|

Current liabilities:

|

||||||||

|

Short-term borrowings (note 9)

|

|

|

||||||

|

Current portion of long-term borrowings (note 12)

|

|

|

||||||

|

Related party accounts payable (note 16)

|

||||||||

|

Accounts payable

|

|

|

||||||

|

Advances from customers

|

|

|

||||||

|

Deferred revenue

|

|

|

||||||

|

Income taxes payable (note 19)

|

|

|

||||||

|

FIN-48 payable (note 19)

|

|

|

||||||

|

Other payables and accrued expenses (note 10)

|

|

|

||||||

|

Current portion of operating lease liability (note 11)

|

|

|

||||||

|

Total current liabilities

|

|

|

||||||

|

Long-term borrowings (note 12)

|

|

|

||||||

|

Long-term operating lease liability (note 11)

|

|

|

||||||

|

Deferred tax liability (note19)

|

|

|

||||||

|

Other long-term liabilities (note 13)

|

|

|

||||||

|

Total liabilities

|

|

|

||||||

|

Commitments and contingencies (note 20)

|

||||||||

|

Equity:

|

||||||||

| Stockholders’ equity: |

||||||||

|

Common stock (1) (note 17)

|

|

|

||||||

|

Common stock (1) (note 17)

|

|

|

||||||

|

Additional paid-in capital

|

|

|

||||||

|

Retained earnings

|

|

|

||||||

|

Statutory surplus reserve (note 22)

|

||||||||

|

Accumulated other comprehensive income (loss)

|

(

|

)

|

|

|||||

|

Total ACM Research, Inc. stockholders’ equity

|

|

|

||||||

|

Non-controlling interests

|

|

|

||||||

|

Total equity

|

|

|

||||||

|

Total liabilities and equity

|

$

|

|

$

|

|

||||

|

(1)

|

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

ACM RESEARCH, INC.

(In thousands, except share and per share data)

(Unaudited)

|

Three Months Ended June 30,

|

Six

Months Ended June 30,

|

|||||||||||||||

|

2022

|

2021

|

2022

|

2021

|

|||||||||||||

|

Revenue (note 3)

|

$

|

|

$

|

|

$

|

|

$

|

|

||||||||

|

Cost of revenue

|

|

|

|

|

||||||||||||

|

Gross profit

|

|

|

|

|

||||||||||||

|

Operating expenses:

|

||||||||||||||||

|

Sales and marketing

|

|

|

|

|

||||||||||||

|

Research and development

|

|

|

|

|

||||||||||||

|

General and administrative

|

|

|

|

|

||||||||||||

|

Total operating expenses, net

|

|

|

|

|

||||||||||||

|

Income from operations

|

|

|

|

|

||||||||||||

|

Interest income

|

|

|

|

|

||||||||||||

|

Interest expense

|

(

|

)

|

(

|

)

|

(

|

)

|

(

|

)

|

||||||||

|

Unrealized gain (loss) on trading securities

|

(

|

)

|

|

(

|

)

|

|

||||||||||

|

Other income (expense), net

|

|

(

|

)

|

|

(

|

)

|

||||||||||

|

Equity income in net income of affiliates

|

|

|

|

|

||||||||||||

|

Income before income taxes

|

|

|

|

|

||||||||||||

|

Income tax benefit (expense) (note 19)

|

(

|

)

|

(

|

)

|

(

|

)

|

|

|||||||||

|

Net income

|

|

|

|

|

||||||||||||

|

Less: Net income attributable to non-controlling interests

|

|

|

|

|

||||||||||||

|

Net income attributable to ACM Research, Inc.

|

$

|

|

$

|

|

$

|

|

$

|

|

||||||||

|

Comprehensive income (loss):

|

||||||||||||||||

|

Net income

|

|

|

|

|

||||||||||||

|

Foreign currency translation adjustment, net of tax

|

(

|

)

|

|

(

|

)

|

|

||||||||||

|

Comprehensive income (loss)

|

(

|

)

|

|

(

|

)

|

|

||||||||||

|

Less: Comprehensive income (loss) attributable to non-controlling interests

|

(

|

)

|

|

(

|

)

|

|

||||||||||

|

Comprehensive income (loss) attributable to ACM Research, Inc.

|

$

|

(

|

)

|

$

|

|

$

|

(

|

)

|

$

|

|

||||||

|

Net income attributable to ACM Research, Inc. per common share (note 2):

|

||||||||||||||||

|

Basic

|

$

|

|

$

|

|

$

|

|

$

|

|

||||||||

|

Diluted

|

$

|

|

$

|

|

$

|

|

$

|

|

||||||||

|

Weighted average common shares outstanding used in computing per share amounts (note 2):

|

||||||||||||||||

|

Basic (1)

|

|

|

|

|

||||||||||||

|

Diluted (1)

|

|

|

|

|

||||||||||||

|

(1)

|

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

For the Six

Months Ended June 30, 2022

and 2021

(In thousands, except share and per share data)

(Unaudited)

|

|

Common

Stock Class A

|

Common

Stock Class B

|

||||||||||||||||||||||||||||||||||||||

|

|

Shares (1)

|

Amount

|

Shares (1)

|

Amount

|

Additional Paid-

in Capital

|

Retained earnings

|

Statutory Surplus

Reserve

|

Accumulated

Other

Comprehensive

Income

|

Non-controlling

interests

|

Total

Equity

|

||||||||||||||||||||||||||||||

|

Balance at December 31, 2020

|

|

$

|

|

|

$

|

|

$

|

|

$ |

$

|

|

$

|

|

$

|

|

$

|

|

|||||||||||||||||||||||

|

Net income

|

-

|

|

-

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

|

Foreign currency translation adjustment, net of tax

|

-

|

|

-

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

|

Exercise of stock options

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

|

Stock-based compensation

|

-

|

|

-

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

|

Exercise of stock warrants

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

|

Conversion of Class B common stock to Class A common stock

|

|

|

(

|

)

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||

|

Balance at June 30, 2021

|

|

$

|

|

|

$

|

|

$

|

|

$ |

$

|

|

$

|

|

$

|

|

$

|

|

|||||||||||||||||||||||

|

|

Common

Stock Class A

|

Common

Stock Class B

|

||||||||||||||||||||||||||||||||||||||

|

|

Shares (1)

|

Amount

|

Shares (1)

|

Amount

|

Additional Paid-

in Capital

|

Retained earnings

|

Statutory Surplus

Reserve

|

Accumulated

Other

Comprehensive

Income (Loss)

|

Non-controlling

interests

|

Total

Equity

|

||||||||||||||||||||||||||||||

|

Balance at December 31, 2021

|

|

$

|

|

|

$ |

$

|

|

$ |

$

|

|

$

|

|

$

|

|

$

|

|

||||||||||||||||||||||||

|

Net income

|

-

|

|

-

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

|

Foreign currency translation adjustment, net of tax

|

-

|

|

-

|

|

|

|

(

|

)

|

(

|

)

|

(

|

)

|

||||||||||||||||||||||||||||

|

Exercise of stock options

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

|

Stock-based compensation

|

-

|

|

-

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

|

Conversion of Class B common stock to Class

A common stock

|

|

|

(

|

)

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||

|

Balance at June 30, 2022

|

|

$

|

|

|

$

|

|

$

|

|

$ |

$

|

|

$

|

(

|

)

|

$

|

|

$

|

|

||||||||||||||||||||||

|

(1)

|

Prior period results have been adjusted to reflect the

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

ACM RESEARCH, INC.

For the Three Months Ended June 30,

2022 and 2021

(In thousands, except share and per share data)

(Unaudited)

|

Common

Stock Class A

|

Common

Stock Class B

|

|||||||||||||||||||||||||||||||||||||||

|

Shares (1)

|

Amount

|

Shares (1)

|

Amount

|

Additional Paid-

in Capital

|

Retained earnings |

Statutory Surplus

Reserve

|

Accumulated

Other

Comprehensive

Income

|

Non-controlling

interests

|

Total

Equity

|

|||||||||||||||||||||||||||||||

|

Balance at March 31, 2021

|

|

$

|

|

|

$

|

|

$

|

|

$ |

$

|

|

|

|

|

||||||||||||||||||||||||||

|

Net income

|

-

|

|

-

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

|

Foreign currency translation adjustment, net of tax

|

-

|

|

-

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

|

Exercise of stock options

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

|

Stock-based compensation

|

-

|

|

-

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

| Exercise

of warrants |

||||||||||||||||||||||||||||||||||||||||

| Conversion of class B common shares to Class A common shares | ( |

) | ||||||||||||||||||||||||||||||||||||||

|

Balance at June 30, 2021

|

|

$

|

|

|

$

|

|

$

|

|

$ |

$

|

|

$

|

|

$

|

|

$

|

|

|||||||||||||||||||||||

|

Common

Stock Class A

|

Common

Stock Class B

|

|||||||||||||||||||||||||||||||||||||||

|

Shares

|

Amount

|

Shares

|

Amount

|

Additional Paid-

in Capital

|

Retained earnings |

Statutory Surplus

Reserve

|

Accumulated

Other

Comprehensive

Income (Loss)

|

Non-controlling

interests

|

Total

Equity

|

|||||||||||||||||||||||||||||||

|

Balance at March 31, 2022

|

|

$

|

|

|

$

|

|

$

|

|

$ |

$

|

|

$

|

|

$

|

|

$

|

|

|||||||||||||||||||||||

|

Net Income

|

-

|

|

-

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

|

Foreign currency translation adjustment, net of tax

|

-

|

|

-

|

|

|

|

(

|

)

|

(

|

)

|

(

|

)

|

||||||||||||||||||||||||||||

|

Exercise of stock options

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

|

Stock-based compensation

|

-

|

|

-

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

|

Balance at June 30, 2022

|

|

$

|

|

|

$

|

|

$

|

|

$ |

$

|

|

$

|

(

|

)

|

$

|

|

$

|

|

||||||||||||||||||||||

|

(1)

|

|

ACM RESEARCH, INC.

(In thousands)

(Unaudited)

|

|

Three Months Ended June 30, |

Six

Months Ended June 30,

|

||||||||||||||

|

|

2022 |

2021 |

2022

|

2021

|

||||||||||||

|

Cash flows from operating activities:

|

||||||||||||||||

|

Net income

|

$ | $ |

$

|

|

$

|

|

||||||||||

|

Adjustments to reconcile net income from operations to net cash provided by (used in) operating activities

|

||||||||||||||||

|

Depreciation and amortization

|

|

|

||||||||||||||

|

Gain on disposals of property, plant and equipment

|

( |

) |

|

|

||||||||||||

|

Equity income in net income of affiliates

|

( |

) | ( |

) |

(

|

)

|

(

|

)

|

||||||||

|

Unrealized loss (gain) on trading securities

|

( |

) |

|

(

|

)

|

|||||||||||

|

Deferred income taxes

|

( |

) |

|

(

|

)

|

|||||||||||

|

Stock-based compensation

|

|

|

||||||||||||||

|

Net changes in operating assets and liabilities:

|

||||||||||||||||

|

Accounts receivable

|

( |

) | ( |

) |

(

|

)

|

(

|

)

|

||||||||

|

Other receivables

|

(

|

)

|

(

|

)

|

||||||||||||

|

Inventories

|

( |

) | ( |

) |

(

|

)

|

(

|

)

|

||||||||

| Advances to related party (note 16) |

( |

) | ( |

) | ||||||||||||

|

Prepaid expenses

|

( |

) | ( |

) |

(

|

)

|

(

|

)

|

||||||||

|

Other long-term assets

|

( |

) |

|

(

|

)

|

|||||||||||

| Related party accounts payable (note 16) |

||||||||||||||||

|

Accounts payable

|

( |

) |

|

|

||||||||||||

|

Advances from customers

|

|

|

||||||||||||||

|

Deferred revenue

|

||||||||||||||||

|

Income tax payable

|

|

|

||||||||||||||

|

FIN-48 payable

|

( |

) | ( |

) | ||||||||||||

|

Other payables and accrued expenses

|

( |

) |

|

|

||||||||||||

|

Other long-term liabilities

|

( |

) | ( |

) |

(

|

)

|

(

|

)

|

||||||||

|

Net cash flow (used in) provided by operating activities

|

( |

) | ( |

) |

(

|

)

|

|

|||||||||

|

|

||||||||||||||||

|

Cash flows from investing activities:

|

||||||||||||||||

|

Purchase of property, plant and equipment

|

( |

) | ( |

) |

(

|

)

|

(

|

)

|

||||||||

|

Purchase of intangible assets

|

( |

) | ( |

) |

(

|

)

|

(

|

)

|

||||||||

|

Decrease (increase) of short-term time deposits

|

( |

) | ||||||||||||||

| Decrease (increase) of long-term time deposits |

( |

) | ||||||||||||||

|

Net cash (used in) provided by investing activities

|

( |

) |

(

|

)

|

(

|

)

|

||||||||||

|

|

||||||||||||||||

|

Cash flows from financing activities:

|

||||||||||||||||

|

Proceeds from short-term borrowings

|

|

|

||||||||||||||

|

Repayments of short-term borrowings

|

( |

) | ( |

) |

(

|

)

|

(

|

)

|

||||||||

| Proceeds

from long-term borrowings |

||||||||||||||||

|

Repayments of long-term borrowings

|

( |

) | ( |

) |

(

|

)

|

(

|

)

|

||||||||

|

Proceeds from exercise of stock options

|

|

|

||||||||||||||

| Proceeds from warrant exercise to common stock |

||||||||||||||||

|

Net cash (used in) provided by financing activities

|

( |

) |

(

|

)

|

|

|||||||||||

|

|

||||||||||||||||

|

Effect of exchange rate changes on cash, cash equivalents and restricted cash

|

$ | ( |

) | $ |

$

|

(

|

)

|

$

|

|

|||||||

|

Net decrease in cash, cash equivalents and restricted cash

|

$ | ( |

) | $ | ( |

) |

$

|

(

|

)

|

$

|

(

|

)

|

||||

|

|

||||||||||||||||

|

Cash, cash equivalents and restricted cash at beginning of period

|

|

|

||||||||||||||

|

Cash, cash equivalents and restricted cash at end of period

|

$ | $ |

$

|

|

$

|

|

||||||||||

|

|

||||||||||||||||

|

Supplemental disclosure of cash flow information:

|

||||||||||||||||

|

Interest paid, net of capitalized interest

|

$ | $ |

$

|

|

$

|

|

||||||||||

|

Cash paid for income taxes

|

$ | $ |

$

|

|

$

|

|

||||||||||

|

|

||||||||||||||||

|

Non-cash financing activities:

|

||||||||||||||||

| Conversion of Class B common stock to Class A common stock |

$ |

$ |

$ |

$ |

||||||||||||

|

Cashless exercise of stock options

|

$ | $ |

$

|

|

$

|

|

||||||||||

| Non-cash investing activities: |

||||||||||||||||

| Transfer of prepayment for property to property, plant and equipment |

$ |

$ |

$ |

$ |

||||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

ACM RESEARCH, INC.

Notes to the Condensed Consolidated Financial Statements

(In thousands, except share, percentage and per share data)

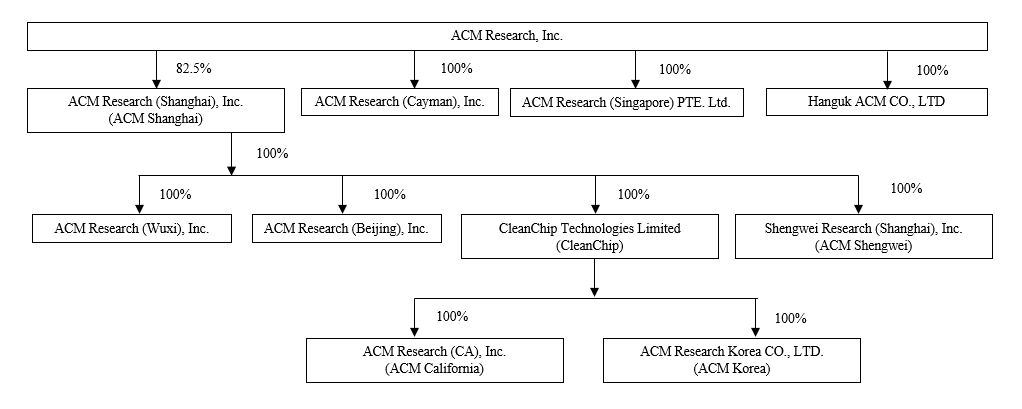

NOTE 1 – DESCRIPTION OF BUSINESS

ACM Research, Inc. (“ACM”) and its subsidiaries (collectively with ACM, the

“Company”) develop, manufacture and sell single-wafer wet cleaning equipment used to improve the manufacturing process and yield for advanced integrated chips. The Company markets and sells its single-wafer wet-cleaning equipment, which are based on the Company’s proprietary Space Alternated Phase Shift (“SAPS”) and Timely Energized Bubble Oscillation (“TEBO”) technologies, under the brand name “Ultra C.” These tools

are designed to remove random defects from a wafer surface efficiently, without damaging the wafer or its features, even at increasingly advanced process nodes.

ACM was incorporated in California in 1998, and it initially focused on developing tools for manufacturing process steps involving the integration

of ultra low-K materials and copper. The Company’s early efforts focused on stress-free copper-polishing technology, and it sold tools based on that technology in the early 2000s.

In 2006, the Company established its operational center in Shanghai in the People’s Republic of China (the “PRC”), where it operates through ACM’s

subsidiary, ACM Research (Shanghai), Inc. (“ACM Shanghai”). ACM Shanghai was formed to help establish and build relationships with integrated circuit manufacturers in the PRC, and the Company initially financed its Shanghai operations in part

through sales of non-controlling equity interests in ACM Shanghai.

In 2007, the Company began to focus its development efforts on single-wafer wet-cleaning solutions for the front-end chip fabrication process. The

Company introduced its SAPS megasonic technology, which can be applied in wet wafer cleaning at numerous steps during the chip fabrication process, in 2009. It introduced its TEBO technology, which can be applied at numerous steps during the

fabrication of small node two-dimensional conventional and three-dimensional patterned wafers, in March 2016. The Company has designed its equipment models for SAPS and TEBO solutions using a modular configuration that enables it to create a

wet-cleaning tool meeting the specific requirements of a customer, while using pre-existing designs for chamber, electrical, chemical delivery and other modules. In August 2018, the Company introduced its Ultra-C Tahoe wafer cleaning tool, which can

deliver high cleaning performance with significantly less sulfuric acid than typically consumed by conventional high-temperature single-wafer cleaning tools. Based on its electro-chemical plating (“ECP”) technology, the Company introduced in March

2019 its Ultra ECP AP, or “Advanced Packaging,” tool for bumping, or applying copper, tin and nickel to semiconductor wafers at the die-level, and its Ultra ECP MAP, or “Multi-Anode Partial Plating,” tool to deliver advanced electrochemical copper

plating for copper interconnect applications in front-end wafer fabrication processes. The Company also offers a range of custom-made equipment, including cleaners, coaters and developers, to back-end wafer assembly and packaging factories,

principally in the PRC.

In 2011, ACM Shanghai formed a wholly-owned subsidiary in the PRC, ACM Research (Wuxi), Inc. (“ACM Wuxi”), to manage sales and service operations.

In November 2016, ACM re-domesticated from California to Delaware pursuant to a merger in which ACM Research, Inc., a California corporation, was

merged into a newly formed, wholly-owned Delaware subsidiary, also named ACM Research, Inc.

In June 2017, ACM formed a wholly-owned subsidiary in Hong Kong, CleanChip Technologies Limited (“CleanChip”), to act on the Company’s behalf in

Asian markets outside the PRC by, for example, serving as a trading partner between ACM Shanghai and its customers, procuring raw materials and components, performing sales and marketing activities, and making strategic investments.

In August 2017, ACM purchased 18.77 % of ACM Shanghai’s equity interests held by Shanghai Science and Technology Venture Capital Co., Ltd. On

November 8, 2017, ACM purchased the remaining 18.36 % of ACM

Shanghai’s equity interests held by third parties, Shanghai Pudong High-Tech Investment Co., Ltd. and Shanghai Zhangjiang Science & Technology Venture Capital Co., Ltd. At December 31, 2017, ACM owned all of the outstanding equity interests of

ACM Shanghai, and indirectly through ACM Shanghai, owned all of the outstanding equity interests of ACM Wuxi.

10

On September 13, 2017, ACM effectuated a

reverse stock split of Class A and Class B common stock.

On November 2, 2017, the Registration Statement on Form S-1 for ACM’s initial public offering of Class A common stock was declared effective by the

U.S. Securities and Exchange Commission. Shares of Class A common stock began trading on the Nasdaq Global Market on November 3, 2017, and the closing for the offering was held on November 7, 2017.

In December 2017, ACM formed a wholly-owned subsidiary in the Republic of Korea, ACM Research Korea CO., LTD. (“ACM Korea”), to serve customers

based in Republic of Korea and perform sales and marketing and research and development (“R&D”) activities for new products and solutions.

In March 2019, ACM Shanghai formed a wholly-owned subsidiary in the PRC, Shengwei Research (Shanghai), Inc. (“ACM Shengwei”), to manage activities

related to addition of future long-term production capacity.

In June 2019, CleanChip formed a wholly-owned subsidiary in California, ACM Research (CA), Inc. (“ACM

California”), to provide procurement services on behalf of ACM Shanghai. In June 2019, ACM Korea was reorganized as a wholly-owned subsidiary of CleanChip.

In June 2019, ACM announced plans to complete a listing (the “STAR Listing”) of shares of ACM Shanghai on the Shanghai Stock Exchange’s Sci-Tech

innovAtion boaRd, known as the STAR Market, and a concurrent initial public offering (the “STAR IPO”) of ACM Shanghai shares in the PRC. ACM Shanghai is currently ACM’s primary operating subsidiary, and at the time of announcement, was wholly-owned

by ACM. To meet a STAR Listing requirement that it have multiple independent stockholders in the PRC, ACM Shanghai completed private placements of its shares in June and November 2019, following which, as of September 30, 2020, the private placement

investors held a total of 8.3 % of the outstanding shares of ACM Shanghai and ACM Research held the remaining 91.7 %. As part of the STAR Listing process, in June 2020 the ownership interests held by the private investors were reclassified from redeemable

non-controlling interests to non-controlling interests as the redemption feature was terminated.

In preparation for the STAR IPO, ACM completed a reorganization in December 2019 that

included the sale of all of the shares of CleanChip by ACM to ACM Shanghai for $3,500 . The reorganization and sale had no impact on ACM’s consolidated financial statements.

In August 2021, ACM formed a wholly-owned subsidiary in Singapore, ACM Research

(Singapore) PTE, Ltd. to perform sales, marketing, and other business development activities.

In November 2021, ACM Shanghai completed its STAR Listing and STAR IPO and its shares began trading on the STAR

Market. In the STAR IPO, ACM Shanghai issued 43,355,753 shares, representing 10 % of the total 433,557,100 shares outstanding after the issuance. The

shares were issued at a public offering price of RMB 85.00 per share, and the net proceeds of the STAR IPO, after issuance costs,

totaled $545,512 . Upon completion of the STAR IPO, ACM owned 82.5 % of the outstanding ACM Shanghai shares.

In February 2022, ACM Shanghai formed a wholly-owned subsidiary in China, ACM Research (Beijing), Inc. (“ACM Beijing”), to perform sales, marketing

and other business development activities.

In March 2022, ACM formed a wholly-owned subsidiary in South Korea, Hanguk ACM CO., LTD, to perform business development and other related

activities.

11

In March 2022, the Board of Directors of ACM declared a 3 two additional shares of Class A common stock for each then-held share of Class A common stock and two additional shares of Class B common stock for each then-held share of Class B common stock, which were distributed after the close of trading on March

23, 2022. Unless otherwise indicated, all share numbers, per share amount, share prices, exercise prices and conversion rates set forth in these notes and the accompanying condensed consolidated financial statements have been adjusted retrospectively

to reflect the Stock Split.

The Company has direct or indirect interests in the following subsidiaries:

|

|

|

Effective interest held as at

|

|||||||

|

Name of subsidiaries

|

Place and date of incorporation

|

June 30,

2022

|

December 31,

2021

|

||||||

|

|

|

|

%

|

|

%

|

||||

|

|

|

|

%

|

|

%

|

||||

|

|

|

|

%

|

|

%

|

||||

|

|

|

|

%

|

|

%

|

||||

|

|

|

|

%

|

|

%

|

||||

|

|

|

|

%

|

|

%

|

||||

|

|

|

|

%

|

|

%

|

||||

| % | % | ||||||||

| % | |||||||||

| % | |||||||||

NOTE 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation and Principles of Consolidation

The Company’s condensed consolidated financial statements include the accounts of ACM and its subsidiaries, including ACM Shanghai and its

subsidiaries, which include ACM Wuxi, ACM Shengwei, ACM Beijing, and CleanChip (the subsidiaries of which include ACM California and ACM Korea). ACM’s subsidiaries are those entities in which ACM, directly or indirectly, controls a majority of the

voting power. All significant intercompany transactions and balances have been eliminated upon consolidation.

The accompanying condensed consolidated financial statements of

the Company have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) for interim financial information and the rules and regulations of the Securities and Exchange Commission for

reporting on Form 10-Q. Accordingly, they do not include all the information and footnotes required by GAAP for complete financial statements. The accompanying condensed consolidated financial statements should be read in conjunction with the

historical consolidated financial statements of the Company for the year ended December 31, 2021 included in ACM’s Annual Report on Form 10-K for the year ended December 31, 2021.

The accompanying condensed consolidated balance sheet as of June 30, 2022, condensed consolidated statements of operations and comprehensive income (loss) for the

three and six months ended June 30, 2022 and 2021, condensed consolidated statements of changes in equity for the three and six months ended June 30, 2022 and 2021, and condensed consolidated statements of cash flows for the three and six months

ended June 30, 2022 and 2021 are unaudited. In the opinion of management, these unaudited condensed consolidated financial statements of the Company reflect all adjustments that are necessary for a fair presentation of the Company’s financial

position and results of operations. Such adjustments are of a normal recurring nature, unless otherwise noted. The balance sheet as of June 30, 2022 and the results of operations for the three and six months ended June 30, 2022 are not

necessarily indicative of the results to be expected for any future period.

12

Common Stock Split

Unless otherwise indicated, all prior period share and per share amounts, common stock, other capital, and retained earnings

information presented in the accompanying financial statements and these notes thereto has been retroactively adjusted to reflect the impact of the Stock Split (Note 1). Proportional adjustments were also made to outstanding awards under the

Company’s stock-based compensation plans.

Reclassification

Certain prior year amounts related to related party transactions have been reclassified to conform to current year presentation. Also, a portion

of the prior period balance for retained earnings on the Company’s consolidated balance sheet as of December 31, 2021 has been reclassified to Statutory surplus reserve to conform to the current period presentation. These reclassifications did not

have a material impact on the previously reported financial statements.

COVID-19 Assessment

The worldwide COVID-19 health pandemic and

related government and private sector responsive actions have adversely affected the economies and financial markets of many countries and specifically have negatively impacted the Company’s business operations, including in the PRC and the

United States. The continuation of the COVID-19 pandemic could continue to result in economic uncertainty and global economic policies that could reduce demand for the Company’s products and its customers’ chips and have a material adverse impact

on the Company’s business, operating results and financial condition.

The Company conducts substantially all of its product development, manufacturing, support and services in the PRC, and those activities have been directly

impacted by COVID-19 and related restrictions on transportation and public appearances.

|

•

|

In March 2022, several regions in China began to experience elevated levels of COVID-19 infections, and the PRC government instituted policies to restrict the spread of the virus. The

policies began with an increase of “spot quarantines,” under which a positive polymerase chain reaction (PCR) or other test would result in the quarantining of individual buildings, groups of buildings, or even full neighborhoods. The

policies were later expanded to full-city quarantines, including in the City of Shanghai, where substantially all of ACM Shanghai’s operations are located. COVID-19 related restrictions in Shanghai began to limit employee access to, and

logistics activities of, ACM Shanghai’s offices and production facilities in the Pudong district of Shanghai in March 2022, and therefore limited ACM Shanghai’s ability to ship finished products to customers and to produce new products.

Spot quarantines in mid-March 2022 began to impact a number of ACM Shanghai’s employees and led to a closure of ACM Shanghai’s administrative and R&D offices in Zhangjiang in the Pudong district. A subsequent quarantine of the

entire Pudong region of Shanghai was imposed in late March 2022 and impacted the operation of ACM Shanghai’s Chuansha production facility. Although the facility remained partially operational with a number of personnel staying on-site

for a prolonged period, the level of production declined significantly versus more normal levels. Furthermore, a number of the Company’s customers have substantial operations based in operations areas of the PRC, including in the City

of Shanghai, subject to a full-city restrictions, which began limiting the operations of those customers since the first quarter of 2022, including inhibiting their ability to receive, implement and operate new tools for their

manufacturing facilities. As a result, in some cases, ACM Shanghai was required to defer shipments of finished products to these customers because of operational and logistical limitations affecting customers other than, or in addition

to, ACM Shanghai.

|

|

•

|

In late April 2022, ACM Shanghai began to increase the level of its operations at the Chuansha manufacturing site using the “closed loop method,” in which a limited collection of

workers remain together as a group between a single hotel, the ACM Shanghai facility, and a dedicated bus transportation route, also referred to as “two spots and one line,” and had resumed substantially all of its Chuansha

manufacturing site operations by the end of the second quarter of 2022. On July 1, 2022, the Company transitioned operations at the Chuansha facility to a more normal production process, in which workers we able to return home

following their factory shifts.

|

|

•

|

In mid-June 2022, substantially all of ACM Shanghai’s R&D and administrative employees were allowed to return to work at the ZhangJiang facility following a 6-8 week period of

restricted access during which many employees had continued to work from home. ACM Shanghai has established several policies to help avoid or limit future outbreaks among employees and aimed at protecting employee safety and limiting

the possibility of a facility reclosing.

|

13

For the first six months of 2022, the Company experienced a negative impact to revenue and shipments as a result of restricted access and

logistics to its Shanghai-based production and administrative facilities. Thirteen tools amounting to $13 million in revenue and $24 million

in shipments that could not be shipped to customers in the three-months ended March 30, 2022 were subsequently shipped in the three months ended June 30, 2022. As a

result of the restrictions, the Company experienced a modest increase to operational costs due to increased logistics costs and inefficiencies that resulted from the restrictions, an increase in cash used in operations due in part to

an increase in accounts receivables that resulted from a shift of shipments towards the latter part of the period, and general administrative inefficiencies.

The Company anticipates that the effects of the PRC restrictions may continue for several months, with an expected increase of PRC operations, production

capacity and global logistics as Shanghai and other areas in the PRC begin to reopen. The Company cannot assure that closures or reductions of operations or production, whether of ACM Shanghai or of some of its key customers, may not be extended

or re-introduced in the second half of 2022 as the result of business interruptions arising from protective measures being taken by the PRC and other governmental agencies or of other consequences of COVID-19.

The Company’s corporate headquarters are located in San Mateo County in the San Francisco Bay Area. The effects of actions taken by local governmental agencies in

the future may negatively impact productivity, disrupt the business of the Company and delay timelines, the magnitude of which will depend, in part, on the length and severity of the restrictions and other limitations on the Company’s ability to

conduct its business in the ordinary course.

To date, the Company’s operations in South Korea, including the R&D center and production facilities of ACM Korea and the business development activities of

Hanguk ACM CO., LTD, have been largely unaffected directly by government restrictions relating to the COVID-19 pandemic.

The worldwide prolonged and broad-based shift to remote working environments resulting from COVID-19 continues to create inherent productivity, connectivity, and

oversight challenges and could affect the Company’s ability to enhance, develop and support existing products and services, detect and prevent spam and problematic content, hold product sales and marketing events, and generate new sales leads. In

addition, the changed environment under which the Company is operating could have an effect on its internal controls over financial reporting as well as its ability to comply with a number of timing and quality requirements. Additional or extended

governmental quarantines, restrictions or regulations could significantly impact the ability of the Company’s employees and vendors to work productively. Governmental restrictions have been inconsistent globally and it remains unclear when a return

to worksite locations or travel will be permitted or what restrictions will be in place in those environments. As the Company continues to return its workforce to the office in 2022, it may experience increased costs as it prepares and maintains

its facilities for a safe work environment and experiments with hybrid work models and it may suffer additional adverse effects on its ability to compete effectively and maintain its corporate culture.

Extended

periods of interruption to the Company’s corporate, development or manufacturing facilities due to the COVID-19 pandemic could cause the Company to lose revenue and market share, which would depress its financial performance and could be difficult

to recapture. The Company’s business may also be harmed if travel to or from the PRC or the United States continues to be restricted or inadvisable or if members of management and other employees are absent because they contract COVID-19, they

elect not to come to work due to the illness affecting others in the Company’s office or laboratory facilities, or they are subject to quarantines or other governmentally imposed restrictions.

14

Use of Estimates

The preparation of the condensed consolidated financial statements in conformity with GAAP requires management to make estimates and assumptions

that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the balance sheet date and the reported revenues and expenses during the reported period in the condensed consolidated financial

statements and accompanying notes. The Company’s significant accounting estimates and assumptions include, but are not limited to, those used for revenue recognition and deferred revenue, the valuation and recognition of fair value of trading

securities, stock-based compensation arrangements, realization of deferred tax assets, assessment for impairment of long-lived assets, allowance for doubtful accounts, inventory valuation, depreciable lives of property, plant and equipment and useful

life of intangible assets.

Management evaluates these estimates and assumptions on a regular basis. Actual results could differ from those estimates and assumptions.

Cash, Cash Equivalents and Restricted Cash

Cash and cash equivalents consist of cash on hand, bank deposits that are unrestricted as to withdrawal and use, and highly liquid investments with an original maturity date of three months or less at the date of purchase.

The following table presents cash, cash equivalents and restricted cash, according to jurisdiction as of June 30, 2022 and December 31, 2021:

|

June 30,

2022

|

December 31,

2021

|

|||||||

|

United States

|

$

|

|

$

|

|

||||

|

Mainland China

|

|

|

||||||

|

China Hong Kong

|

||||||||

|

South Korea

|

|

|

||||||

|

Total

|

$

|

|

$

|

|

||||

The amounts in mainland China do not include short-term and long-term time deposits which totaled $144,530 and $0 for the periods ending June 30, 2022 and

December 31, 2021, respectively.

Cash held in the U.S. exceeds the Federal Deposit Insurance Corporation (“FDIC”) insurance limits and is subject to risk of loss. No losses have

been experienced to date.

For amounts held in mainland China, PRC banks are subject to a series of risk control regulatory standards from PRC bank regulatory authorities.

The Company is required to obtain approval from the State Administration of Foreign Exchange (“SAFE”) to transfer funds in or out of the PRC. SAFE requires a valid agreement to approve the transfers, which are processed through a bank. Other than

PRC foreign exchange restrictions, the Company is not subject to any PRC restrictions and limitations on its ability to transfer funds among subsidiaries. Cash held in mainland China exceeds the insurance limits and is subject to risk of loss. No

losses have been experienced to date.

Amounts held in South Korea exceed the Korea Deposit Insurance Corporation (“KDIC”) insurance limits and is subject to risk of loss. No losses

have been experienced to date.

There is no additional restriction for the transfer of cash from bank accounts in the U.S., South Korea, and Hong Kong. For sales through CleanChip and ACM

Research, a certain amount of sales proceeds is repatriated back to ACM Shanghai in accordance with the transfer pricing arrangements in the ordinary course of business. For purchases made by ACM California on behalf of ACM Shanghai, cash payments

in accordance with the transfer pricing arrangements are delivered to ACM California from ACM Shanghai. ACM California borrows intercompany loans from CleanChip for working capital purposes.

For the six months ended June 30, 2022 and 2021, no transfers, dividends, or distributions have been made between ACM Research and its

subsidiaries, including ACM Shanghai, or to holders of ACM Research Class A common stock.

15

Time Deposits

Time deposits are deposited with banks in mainland China with

fixed periods and interest rates which can’t be withdrawn before maturity. They are also subject to risk control regulatory standards above upon maturity. Time deposits consisted of the following:

|

|

June 30,

2022

|

December 31,

2021

|

||||||

|

Deposit in China Merchant Bank which will mature on

|

$

|

|

$

|

|

||||

|

Deposit in China Everbright Bank which will mature on

|

|

|

||||||

|

Deposit in China Industrial Bank which will mature on

|

|

|

||||||

|

Deposit in China Merchant Bank which will mature on

|

|

|

||||||

|

Deposit in Bank of Ningbo which will mature on

|

|

|

||||||

|

|

$

|

|

$

|

|

||||

For the three and six months ended June 30, 2022, respectively, interest income related to time deposits was $951 and $1,539 , respectively.

Intangible Assets, Net

Intangible assets consist of software used for finance, manufacturing, and research and development purposes. Assets are valued at cost at the

time of acquisition and are amortized over their beneficial periods. If a contract specifies a beneficial period, then the intangible asset is amortized over a term not exceeding the beneficial period. For those intangible assets with contracts

that do not specify a beneficial period or for which local law does not specify a beneficial period, management estimates the beneficial period based on the period over which the asset is expected to contribute directly or indirectly to the cash

flows in accordance with ASC 350, Intangibles—Goodwill

and Other. The factors include, but are not limited to, the change of technology and the change of type of product. The company estimated these intangible assets with less than 10 years of beneficial period. Accordingly, they are amortized up to 10

years.

Revenue Recognition

The Company derives revenue principally from the sale of semiconductor capital equipment. Revenue from contracts with customers is recognized

using the following five steps pursuant ASC Topic 606, Revenue from Contracts with Customers:

|

1.

|

Identify the contract(s) with a customer;

|

|

2.

|

Identify the performance obligations in the contract;

|

|

3.

|

Determine the transaction price;

|

|

4.

|

Allocate the transaction price to the performance obligations in the contract; and

|

|

5.

|

Recognize revenue when (or as) the entity satisfies a performance obligation.

|

A contract contains a promise (or promises) to transfer goods or services to a customer. A performance obligation is a promise (or a group of

promises) that is distinct. The transaction price is the amount of consideration a company expects to be entitled from a customer in exchange for providing the goods or services.

The unit of account for revenue recognition is a performance obligation (a good or service). A contract may contain one or more performance

obligations. Performance obligations are accounted for separately if they are distinct. A good or service is distinct if the customer can benefit from the good or service either on its own or together with other resources that are readily

available to the customer, and the good or service is distinct in the context of the contract. Otherwise performance obligations are combined with other promised goods or services until the Company identifies a bundle of goods or services that is

distinct. Promises in contracts which do not result in the transfer of a good or service are not performance obligations, as well as those promises that are administrative in nature, or are immaterial in the context of the contract. The Company

has addressed whether various goods and services promised to the customer represent distinct performance obligations. The Company applied the guidance of ASC Topic 606 in order to verify which promises should be assessed for classification as

distinct performance obligations. The Company’s performance obligations in connection with a sale of equipment generally include production, delivery and installation, together with the provision of a warranty. Given that the Company’s products

are customized based on specifications of its customers, the Company determines that the promise to the customer is to provide a customized product solution. The product and customization services are inputs into the combined item for which

customer has contracted and, as a result, the product and installation services are not separately identifiable and are combined into a single performance obligation. Delivery of goods to a customer is not a separate performance obligation since

control of the goods normally does not transfer to the customer before shipment. The Company’s warranties provide assurance that its products will function as expected and in accordance with certain specifications. The Company’s warranties are

intended to safeguard the customer against existing defects and do not provide any incremental service to the customer. They are not separate performance obligations and accounted for under ASC 460, Guarantees. Production, delivery and installation of a product, together with provision of a warranty, are a single unit of accounting.

16

The transaction price is allocated to all the separate performance obligations in an arrangement. It reflects the amount of consideration to

which the Company expects to be entitled in exchange for transferring goods or services, which may include an estimate of variable consideration to the extent that it is probable of not being subject to significant reversals in the future based

on the Company’s experience with similar arrangements. The transaction price excludes amounts collected on behalf of third parties, such as sales taxes. This is done on a relative selling price basis using standalone selling prices (“SSP”). The

SSP represents the price at which the Company would sell that good or service on a standalone basis at the inception of the contract. Given the requirement for establishing SSP for all performance obligations, if the SSP is directly observable

through standalone sales, then such sales should be considered in the establishment of the SSP for the performance obligation.

For some sale contracts, in addition to the sale of semiconductor capital equipment, the Company also provides certain spare parts to the

customers. The Company defers revenue associated with spare parts sold together with its tool products, including production, delivery, installation and warranty which are accounted for as one

performance obligation, based on stand-alone observable selling prices for which it receives payments in advance and recognizes the revenue upon the subsequent shipment of the spare parts, which is expected within one year. The

deferred revenue was $2,950 and $3,180

at June 30, 2022 and December 31, 2021, respectively.

Revenue is recognized when the Company satisfies each performance obligation by transferring control of the promised goods or services to the

customer. Goods or services can transfer at a point in time (upon the acceptance of the products or upon the arrival at the destination as stipulated in the shipment terms) in a sale arrangement. In general, the Company recognizes revenue when a

tool has been demonstrated to meet the customer’s predetermined specifications and is accepted by the customer. If terms of the sale provide for a lapsing customer acceptance period, the Company recognizes revenue as of the earlier of the

expiration of the lapsing acceptance period and customer acceptance. In the following circumstances, however, the Company recognizes revenue upon shipment or delivery, when legal title to the tool is passed to a customer as follows:

|

●

|

When the customer has previously accepted the same tool with the same specifications and the Company can objectively demonstrate that the tool meets all of the required acceptance criteria;

|

|

●

|

When the sales contract or purchase order contains no acceptance agreement or lapsing acceptance provision and the Company can objectively demonstrate that the tool meets all of the required acceptance criteria;

|

|

●

|

When the customer withholds acceptance due to issues unrelated to product performance, in which case revenue is recognized when the system is performing as intended and meets predetermined specifications; or

|

|

●

|

When the Company’s sales arrangements do not include a general right of return.

|

The Company offers maintenance services, which consist principally of the installation and replacement of parts and small-scale modifications to

the equipment. The related revenue and costs of revenue are recognized when parts have been delivered and installed and the customers have obtained control of the parts.

The Company incurs costs related to the acquisition of its contracts with customers in the form of sales commissions. Sales commissions are paid

to third party representatives and distributors. Contractual agreements with these parties outline commission structures and rates to be paid. Generally speaking, the contracts are all individual procurement decisions by the customers and are not

for significant periods of time, nor do they include renewal provisions. As such, all contracts have an economic life of significantly less than a year. Accordingly, the Company expenses sales commissions when incurred. These costs are recorded

within sales and marketing expenses. The Company, therefore, does not have contract assets.

The Company does not incur any costs to fulfill the contracts with customers that are not already reported in compliance with another applicable

standard (for example, inventory or plant, property and equipment).

The Company receives payments from customers prior to the transfer of control either upon contract sign-off and/or the delivery of evaluation

tools, they are recorded as advances from customers.

17

Basic and Diluted Net Income per Common Share

Basic and diluted net income per common share are calculated as follows, as adjusted to give effect to the Stock Split:

|

|

Three Months Ended June 30,

|

Six

Months Ended June 30,

|

||||||||||||||

|

2022

|

2021

|

2022

|

2021

|

|||||||||||||

|

Numerator:

|

||||||||||||||||

|

Net income

|

$

|

|

$

|

|

$

|

|

$

|

|

||||||||

|

Less: Net income attributable to non-controlling interests

|

|

|

|

|

||||||||||||

|

Net income available to common stockholders, basic

|

$

|

|

$

|

|

$

|

|

$

|

|

||||||||

|

Less: Dilutive effect arising from stock-based awards by ACM Shanghai

|

||||||||||||||||

| Net income available to common stockholders, diluted | $ | $ | $ | $ | ||||||||||||

|

Weighted average shares outstanding, basic (1)

|

|

|

|

|

||||||||||||

|

Effect of dilutive securities

|

|

|

|

|

||||||||||||

|

Weighted average shares outstanding, diluted

|

|

|

|

|

||||||||||||

|

Net income per common share:

|

||||||||||||||||

|

Basic

|

|

|

|

|

||||||||||||

|

Diluted

|

$

|

|

$

|

|

$

|

|

$

|

|

||||||||

|

(1)

|

|

ACM has been authorized to issue Class A and Class B common stock since

redomesticating in Delaware in November 2016. The two classes of

common stock are substantially identical in all material respects, except for voting rights. Since ACM did not declare any cash dividends during the three

and six months ended June 30, 2022 or 2021, the net income per common share attributable to each class is the same under the “two-class” method. As such, the two classes of common stock have been presented on a combined basis in the condensed consolidated statements of

operations and comprehensive income and in the above computation of net income per common share.

Diluted net income per common share reflects the potential dilution from securities,

including stock options and issued warrants, that could share in ACM’s earnings. Certain potential dilutive securities were excluded from the net income per share calculation because the impact would be anti-dilutive. ACM’s potential dilutive

securities consist of stock options for the three and six months ended June 30, 2022 and 2021.

Concentration of Credit Risk

Financial instruments that potentially subject the Company to credit risk consist principally of cash and cash equivalents, time deposits, and

accounts receivable. The Company deposits and invests its cash with financial institutions that management believes are creditworthy.

The Company is potentially subject to concentrations of credit risks in its accounts receivable. For the three months ended June 30, 2022 and

2021, four customers accounted for 59.7 %

and two customers accounted for 73.3 %

of revenue, respectively. For the six months ended June 30, 2022 and 2021, four customers accounted for 55.0 % and two customers accounted for 57.3 % of revenue, respectively.

As of June 30, 2022 and December 31, 2021, four

customers accounted for 70.4 % and two

customers accounted for 53.8 %, respectively, of the Company’s accounts receivables. The Company believes that the receivable balances

from these largest customers do not represent a significant credit risk based on past collection experience.

Recent Accounting Pronouncements Not Yet Adopted

In June 2016 the Financial Accounting Standards Board, or FASB, issued Accounting Standards Update, or ASU, 2016-13, Financial Instruments-Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments. ASU 2016-13 replaced the pre-existing incurred loss impairment methodology with a