UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

______________________

FORM 10-Q

(Mark one)

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended March 31, 2024

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from _________ to ___________

Commission file number 001-37884

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

(Address of principal executive offices) (Zip Code)

Telephone Number (859) 357-7777

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☑ | Accelerated filer | ☐ | |||||||||

Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No þ

At May 7, 2024, there were 128,854,818 shares of the registrant’s common stock outstanding.

TABLE OF CONTENTS

| Page | |||||

| PART I – FINANCIAL INFORMATION | |||||

| PART II – OTHER INFORMATION | |||||

2

PART I - FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

Valvoline Inc. and Consolidated Subsidiaries

Condensed Consolidated Statements of Comprehensive Income

| Three months ended March 31 | Six months ended March 31 | |||||||||||||||||||||||||

| (In millions, except per share amounts - unaudited) | 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||||

| Net revenues | $ | $ | $ | $ | ||||||||||||||||||||||

| Cost of sales | ||||||||||||||||||||||||||

| Gross profit | ||||||||||||||||||||||||||

| Selling, general and administrative expenses | ||||||||||||||||||||||||||

| Net legacy and separation-related expenses | ||||||||||||||||||||||||||

| Other income, net | ( | ( | ( | ( | ||||||||||||||||||||||

| Operating income | ||||||||||||||||||||||||||

| Net pension and other postretirement plan expenses | ||||||||||||||||||||||||||

| Net interest and other financing expenses | ||||||||||||||||||||||||||

| Income before income taxes | ||||||||||||||||||||||||||

| Income tax expense (benefit) | ( | |||||||||||||||||||||||||

| Income from continuing operations | ||||||||||||||||||||||||||

| (Loss) income from discontinued operations, net of tax | ( | ( | ||||||||||||||||||||||||

| Net income | $ | $ | $ | $ | ||||||||||||||||||||||

| Net earnings per share | ||||||||||||||||||||||||||

| Basic earnings (loss) per share | ||||||||||||||||||||||||||

| Continuing operations | $ | $ | $ | $ | ||||||||||||||||||||||

| Discontinued operations | ( | ( | ||||||||||||||||||||||||

| Basic earnings per share | $ | $ | $ | $ | ||||||||||||||||||||||

| Diluted earnings (loss) per share | ||||||||||||||||||||||||||

| Continuing operations | $ | $ | $ | $ | ||||||||||||||||||||||

| Discontinued operations | ( | ( | ||||||||||||||||||||||||

| Diluted earnings per share | $ | $ | $ | $ | ||||||||||||||||||||||

| Weighted average common shares outstanding | ||||||||||||||||||||||||||

| Basic | ||||||||||||||||||||||||||

| Diluted | ||||||||||||||||||||||||||

| Comprehensive income | ||||||||||||||||||||||||||

| Net income | $ | $ | $ | $ | ||||||||||||||||||||||

| Other comprehensive (loss) income, net of tax | ||||||||||||||||||||||||||

| Currency translation adjustments | ( | |||||||||||||||||||||||||

| Amortization of pension and other postretirement plan prior service credits | ( | ( | ( | ( | ||||||||||||||||||||||

| Unrealized loss on cash flow hedges | ( | ( | ( | ( | ||||||||||||||||||||||

| Other comprehensive (loss) income | ( | ( | ||||||||||||||||||||||||

| Comprehensive income | $ | $ | $ | $ | ||||||||||||||||||||||

The accompanying Notes to Condensed Consolidated Financial Statements are an integral part of these Condensed Consolidated Financial Statements.

3

Valvoline Inc. and Consolidated Subsidiaries

Condensed Consolidated Balance Sheets

| (In millions, except per share amounts - unaudited) | March 31 2024 | September 30 2023 | ||||||||||||

| Assets | ||||||||||||||

| Current assets | ||||||||||||||

| Cash and cash equivalents | $ | $ | ||||||||||||

| Receivables, net | ||||||||||||||

| Inventories, net | ||||||||||||||

| Prepaid expenses and other current assets | ||||||||||||||

| Short-term investments | ||||||||||||||

| Total current assets | ||||||||||||||

| Noncurrent assets | ||||||||||||||

| Property, plant and equipment, net | ||||||||||||||

| Operating lease assets | ||||||||||||||

| Goodwill and intangibles, net | ||||||||||||||

| Other noncurrent assets | ||||||||||||||

| Total noncurrent assets | ||||||||||||||

| Total assets | $ | $ | ||||||||||||

| Liabilities and Stockholders’ Equity | ||||||||||||||

| Current liabilities | ||||||||||||||

| Current portion of long-term debt | $ | $ | ||||||||||||

| Trade and other payables | ||||||||||||||

| Accrued expenses and other liabilities | ||||||||||||||

| Current liabilities held for sale | ||||||||||||||

| Total current liabilities | ||||||||||||||

| Noncurrent liabilities | ||||||||||||||

| Long-term debt | ||||||||||||||

| Employee benefit obligations | ||||||||||||||

| Operating lease liabilities | ||||||||||||||

| Other noncurrent liabilities | ||||||||||||||

| Total noncurrent liabilities | ||||||||||||||

| Commitments and contingencies | ||||||||||||||

| Stockholders' equity | ||||||||||||||

Preferred stock, | ||||||||||||||

Common stock, par value $ | ||||||||||||||

| Paid-in capital | ||||||||||||||

| Retained earnings | ||||||||||||||

| Accumulated other comprehensive income | ||||||||||||||

| Stockholders' equity | ||||||||||||||

Total liabilities and stockholders’ equity | $ | $ | ||||||||||||

The accompanying Notes to Condensed Consolidated Financial Statements are an integral part of these Condensed Consolidated Financial Statements.

4

Valvoline Inc. and Consolidated Subsidiaries

Condensed Consolidated Statements of Cash Flows

| Six months ended March 31 | ||||||||||||||

| (In millions - unaudited) | 2024 | 2023 | ||||||||||||

| Cash flows from operating activities | ||||||||||||||

| Net income | $ | $ | ||||||||||||

| Adjustments to reconcile net income to cash flows from operating activities: | ||||||||||||||

| Loss (income) from discontinued operations | ( | |||||||||||||

| Depreciation and amortization | ||||||||||||||

| Deferred income taxes | ( | |||||||||||||

| Stock-based compensation expense | ||||||||||||||

| Other, net | ||||||||||||||

| Change in operating assets and liabilities | ||||||||||||||

| Receivables | ( | |||||||||||||

| Inventories | ( | ( | ||||||||||||

| Payables and accrued liabilities | ||||||||||||||

| Other assets and liabilities | ( | |||||||||||||

| Operating cash flows from continuing operations | ||||||||||||||

| Operating cash flows from discontinued operations | ( | ( | ||||||||||||

| Total cash provided by operating activities | ||||||||||||||

| Cash flows from investing activities | ||||||||||||||

| Additions to property, plant and equipment | ( | ( | ||||||||||||

| Acquisitions of businesses | ( | ( | ||||||||||||

| Proceeds from maturities of short-term investments | ||||||||||||||

| Other investing activities, net | ( | |||||||||||||

| Investing cash flows from continuing operations | ( | |||||||||||||

| Investing cash flows from discontinued operations | ||||||||||||||

| Total cash provided by investing activities | ||||||||||||||

| Cash flows from financing activities | ||||||||||||||

| Proceeds from borrowings | ||||||||||||||

| Repayments on borrowings | ( | ( | ||||||||||||

| Repurchases of common stock | ( | ( | ||||||||||||

| Cash dividends paid | ( | |||||||||||||

| Other financing activities | ( | ( | ||||||||||||

| Financing cash flows from continuing operations | ( | ( | ||||||||||||

| Financing cash flows from discontinued operations | ( | |||||||||||||

| Total cash used in financing activities | ( | ( | ||||||||||||

| Effect of currency exchange rate changes on cash, cash equivalents and restricted cash | ||||||||||||||

| Increase in cash, cash equivalents and restricted cash | ||||||||||||||

| Cash, cash equivalents and restricted cash - beginning of period | ||||||||||||||

| Cash, cash equivalents and restricted cash - end of period | $ | $ | ||||||||||||

The accompanying Notes to Condensed Consolidated Financial Statements are an integral part of these Condensed Consolidated Financial Statements.

5

Valvoline Inc. and Consolidated Subsidiaries

Condensed Consolidated Statements of Stockholders' Equity

| Six months ended March 31, 2024 | ||||||||||||||||||||||||||||||||||||||

| (In millions, except per share amounts - unaudited) | Common stock | Paid-in capital | Retained earnings (deficit) | Accumulated other comprehensive income | Totals | |||||||||||||||||||||||||||||||||

| Shares | Amount | |||||||||||||||||||||||||||||||||||||

| Balance at September 30, 2023 | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | ||||||||||||||||||||||||||||||||||

| Stock-based compensation, net of issuances | — | ( | — | — | ( | |||||||||||||||||||||||||||||||||

| Repurchases of common stock | ( | — | ( | — | ( | |||||||||||||||||||||||||||||||||

| Other comprehensive income, net of tax | — | — | — | — | ||||||||||||||||||||||||||||||||||

| Balance at December 31, 2023 | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | ||||||||||||||||||||||||||||||||||

| Stock-based compensation, net of issuances | — | ( | — | — | ( | |||||||||||||||||||||||||||||||||

| Repurchases of common stock | ( | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||

| Other comprehensive loss, net of tax | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||

| Balance at March 31, 2024 | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||

| Six months ended March 31, 2023 | ||||||||||||||||||||||||||||||||||||||

| (In millions, except per share amounts - unaudited) | Common stock | Paid-in capital | Retained earnings | Accumulated other comprehensive (loss) income | Totals | |||||||||||||||||||||||||||||||||

| Shares | Amount | |||||||||||||||||||||||||||||||||||||

| Balance at September 30, 2022 | $ | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | ||||||||||||||||||||||||||||||||||

Dividends paid, $ | — | — | ( | — | ( | |||||||||||||||||||||||||||||||||

| Stock-based compensation, net of issuances | — | ( | — | — | ( | |||||||||||||||||||||||||||||||||

| Repurchases of common stock | ( | ( | — | ( | — | ( | ||||||||||||||||||||||||||||||||

| Other comprehensive income, net of tax | — | — | — | — | ||||||||||||||||||||||||||||||||||

| Balance at December 31, 2022 | $ | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | ||||||||||||||||||||||||||||||||||

| Stock-based compensation, net of issuances | — | — | — | |||||||||||||||||||||||||||||||||||

| Repurchases of common stock | ( | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||

| Other comprehensive income, net of tax | — | — | — | — | ||||||||||||||||||||||||||||||||||

| Balance at March 31, 2023 | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||

The accompanying Notes to Condensed Consolidated Financial Statements are an integral part of these Condensed Consolidated Financial Statements.

6

Index to Notes to Condensed Consolidated Financial Statements | Page | ||||

7

Valvoline Inc. and Consolidated Subsidiaries

Notes to Condensed Consolidated Financial Statements (Unaudited)

NOTE 1 – BASIS OF PRESENTATION AND SIGNIFICANT ACCOUNTING POLICIES

The accompanying unaudited condensed consolidated financial statements have been prepared by Valvoline Inc. (“Valvoline” or the “Company”) in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) and Securities and Exchange Commission regulations for interim financial reporting, which do not include all information and footnote disclosures normally included in annual financial statements. Therefore, these condensed consolidated financial statements should be read in conjunction with Valvoline’s Annual Report on Form 10-K for the fiscal year ended September 30, 2023.

Use of estimates, risks and uncertainties

The preparation of the condensed consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses, and the disclosures of contingent matters. Although management bases its estimates on historical experience and various other assumptions that are believed to be reasonable under the circumstances, actual results could differ significantly from the estimates under different assumptions or conditions.

Sale of Global Products business

On March 1, 2023, Valvoline completed the sale of its former Global Products reportable segment (“Global Products”) to Aramco Overseas Company B.V. (the “Transaction”). The operating results and cash flows associated with and directly attributed to the Global Products disposal group are reflected as discontinued operations within these condensed consolidated financial statements. Refer to Note 2 for additional information regarding the Global Products business, including income from discontinued operations. Unless otherwise noted, disclosures within these remaining Notes to Condensed Consolidated Financial Statements relate solely to the Company's continuing operations.

Recent accounting pronouncements

The following accounting guidance relevant to Valvoline was either issued or adopted in the current fiscal year or is expected to have a meaningful impact on Valvoline in future periods upon adoption.

Issued but not yet adopted

In November 2023, the Financial Accounting Standards Board (“FASB”) issued guidance that enhances reportable segment disclosures by requiring disclosure of significant reportable segment expenses and other items regularly provided to the Chief Operating Decision Maker (“CODM”) and included within measures of a segment’s profit or loss, inclusive of entities that operate in a single reportable segment. This guidance must be applied retrospectively to all prior periods presented and will become effective for Valvoline beginning with its fiscal 2025 annual financial statements and interim periods starting in fiscal 2026, with early adoption permitted. Valvoline is currently evaluating the impact this guidance will have on the Company and expects adoption will require enhanced disclosures regarding its CODM and the information used in assessing performance and allocating resources, including significant expenses.

In December 2023, the FASB issued guidance which enhances income tax disclosure requirements to include additional disaggregation within the effective tax rate reconciliation and income taxes paid. This guidance will be effective for Valvoline beginning with its fiscal 2026 annual financial statements, with early adoption permitted. The guidance must be applied prospectively, while retrospective application is permitted. The Company is currently assessing the impact of adoption, which is expected to result in enhanced income tax disclosures.

8

NOTE 2 - DISCONTINUED OPERATIONS

Sale of Global Products

Financial results

On March 1, 2023, Valvoline completed the sale of Global Products for a cash purchase price of $2.650 billion and recognized a pre-tax gain on the sale within Income from discontinued operations, net of tax, during the second quarter of fiscal 2023, coinciding with the completion of the sale. The Transaction was subject to customary closing settlements that were finalized in the third quarter of fiscal 2023 and resulted in the recognition of a pre-tax gain on sale of $1.572 billion during the fiscal year ended September 30, 2023.

The following table summarizes Income from discontinued operations within the Condensed Consolidated Statements of Comprehensive Income:

| Three months ended March 31 | Six months ended March 31 | |||||||||||||||||||||||||

| (In millions) | 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||||

| Net revenues | $ | $ | $ | $ | ||||||||||||||||||||||

| Cost of sales | ||||||||||||||||||||||||||

| Gross profit | ||||||||||||||||||||||||||

| Selling, general and administrative expenses | ||||||||||||||||||||||||||

| Net legacy and separation-related expenses | ||||||||||||||||||||||||||

| Equity and other income, net | ( | ( | ||||||||||||||||||||||||

| Operating (loss) income from discontinued operations | ( | ( | ||||||||||||||||||||||||

| Net pension and other postretirement plan expense | ||||||||||||||||||||||||||

| Net interest and other financing expenses | ||||||||||||||||||||||||||

Gain on sale of discontinued operations (a) | ( | ( | ||||||||||||||||||||||||

| (Loss) income before income taxes - discontinued operations | ( | ( | ||||||||||||||||||||||||

Income tax (benefit) expense (b) | ( | ( | ||||||||||||||||||||||||

| (Loss) income from discontinued operations, net of tax | $ | ( | $ | $ | ( | $ | ||||||||||||||||||||

(a)The gain on sale recorded in the three months ended March 31, 2023 includes the release of Accumulated other comprehensive income of $30.7 million associated with the realization of cumulative translation losses attributed to the Global Products business.

Post-closing arrangements

Valvoline sources substantially all lubricant and certain ancillary products for its stores through a long-term supply agreement with Global Products. Net revenues within the results of Global Products above include product sales to the Company's continuing operations prior to the closing of the Transaction, which were considered to be effectively settled and were not eliminated. These transactions totaled $34.6 million and $89.7 million for the three and six months ended March 31, 2023, respectively.

Valvoline also entered into a Transition Services Agreement with Global Products, effective March 1, 2023, to provide and receive services including information technology (“IT”), legal, finance, and human resources support. Transition services have lapsed periodically as business process transitions have occurred since the sale, and remaining services are generally expected to conclude within 18 months post-closing with limited IT transition services that may extend through early calendar year 2025. The income and costs associated with these services were not material during the three and six months ended March 31, 2024.

9

NOTE 3 - FAIR VALUE MEASUREMENTS

Recurring fair value measurements

The following tables set forth the Company’s financial assets and liabilities by level within the fair value hierarchy for those measured at fair value on a recurring basis:

As of March 31, 2024 | ||||||||||||||||||||||||||||||||

| (In millions) | Total | Level 1 | Level 2 | Level 3 | NAV (a) | |||||||||||||||||||||||||||

| Cash and cash equivalents | ||||||||||||||||||||||||||||||||

| Money market funds | $ | $ | $ | — | $ | — | $ | — | ||||||||||||||||||||||||

| Time deposits | — | — | — | |||||||||||||||||||||||||||||

| Prepaid expenses and other current assets | ||||||||||||||||||||||||||||||||

| Interest rate swap agreements | — | — | — | |||||||||||||||||||||||||||||

| Other noncurrent assets | ||||||||||||||||||||||||||||||||

| Non-qualified trust funds | — | — | ||||||||||||||||||||||||||||||

| Deferred compensation investments | — | — | — | |||||||||||||||||||||||||||||

| Total assets at fair value | $ | $ | $ | $ | — | $ | ||||||||||||||||||||||||||

| Other noncurrent liabilities | ||||||||||||||||||||||||||||||||

| Deferred compensation obligations | $ | $ | — | $ | — | $ | — | $ | ||||||||||||||||||||||||

| Total liabilities at fair value | $ | $ | $ | $ | — | $ | ||||||||||||||||||||||||||

As of September 30, 2023 | ||||||||||||||||||||||||||||||||

| (In millions) | Total | Level 1 | Level 2 | Level 3 | NAV (a) | |||||||||||||||||||||||||||

| Cash and cash equivalents | ||||||||||||||||||||||||||||||||

| Money market funds | $ | $ | $ | — | $ | — | $ | — | ||||||||||||||||||||||||

| Time deposits | — | — | — | |||||||||||||||||||||||||||||

| Prepaid expenses and other current assets | ||||||||||||||||||||||||||||||||

Currency derivatives (b) | — | — | — | |||||||||||||||||||||||||||||

| Interest rate swap agreements | — | — | — | |||||||||||||||||||||||||||||

| Other noncurrent assets | ||||||||||||||||||||||||||||||||

| Non-qualified trust funds | — | — | ||||||||||||||||||||||||||||||

| Deferred compensation investments | — | — | — | |||||||||||||||||||||||||||||

| Total assets at fair value | $ | $ | $ | $ | — | $ | ||||||||||||||||||||||||||

| Accrued expenses and other liabilities | ||||||||||||||||||||||||||||||||

Currency derivatives (b) | $ | $ | — | $ | $ | — | $ | — | ||||||||||||||||||||||||

| Other noncurrent liabilities | ||||||||||||||||||||||||||||||||

| Deferred compensation obligations | — | — | — | |||||||||||||||||||||||||||||

| Total liabilities at fair value | $ | $ | $ | $ | — | $ | ||||||||||||||||||||||||||

(a)Funds measured at fair value using the net asset value ("NAV") per share practical expedient have not been classified in the fair value hierarchy.

(b)The Company had outstanding contracts with notional values of $29.7 million as of September 30, 2023.

Fair value disclosures

The Company’s held-to-maturity U.S. treasury securities and long-term debt are reported in the Condensed Consolidated Balance Sheets at carrying value, rather than fair value, and are therefore excluded from the disclosure above of financial assets and liabilities measured at fair value within the condensed consolidated financial statements on a recurring basis. The following disclosures summarize the fair value of these assets and liabilities at each relevant balance sheet date.

10

U.S. treasury securities

The fair values of the Company’s U.S. treasury securities summarized below were determined utilizing quoted prices for identical securities from less active markets, which are considered Level 2 inputs within the fair value hierarchy. The U.S. treasury securities were fully matured as of March 31, 2024.

| September 30, 2023 | |||||||||||||||||

| (In millions) | Amortized cost | Gross unrealized losses | Fair value | ||||||||||||||

| Cash and cash equivalents | |||||||||||||||||

U.S. treasury securities (a) | $ | $ | — | $ | |||||||||||||

| Short-term investments | |||||||||||||||||

U.S. treasury securities (b) | $ | $ | ( | $ | |||||||||||||

(a)U.S. treasury securities with original maturity dates of three months or less.

(b)U.S. treasury securities with original maturities greater than three months and less than 12 months.

Debt

The fair values of the Company's outstanding fixed rate senior notes shown below are based on recent trading values, which are considered Level 2 inputs within the fair value hierarchy.

| March 31, 2024 | September 30, 2023 | |||||||||||||||||||||||||||||||||||||

| (In millions) | Fair value | Carrying value (a) | Unamortized discounts and issuance costs | Fair value | Carrying value (a) | Unamortized discounts and issuance costs | ||||||||||||||||||||||||||||||||

2030 Notes (b) | $ | $ | $ | ( | $ | $ | $ | ( | ||||||||||||||||||||||||||||||

| 2031 Notes | ( | ( | ||||||||||||||||||||||||||||||||||||

| Total | $ | $ | $ | ( | $ | $ | $ | ( | ||||||||||||||||||||||||||||||

(a)Carrying values shown are net of unamortized discounts and debt issuance costs.

(b)The 2030 Notes were reported in Current portion of long-term debt within the Condensed Consolidated Balance Sheet as of March 31, 2024 due to the execution of the Tender Offer in April 2024 as further described in Note 5.

Refer to Note 5 for details of these senior notes as well as Valvoline's other debt instruments that have variable interest rates with carrying amounts that approximate fair value.

NOTE 4 - BUSINESS COMBINATIONS

The Company acquired fifteen service center stores in single and multi-store transactions for an aggregate purchase price of $21.3 million during the six months ended March 31, 2024. These acquisitions expand Valvoline's retail presence in key North American markets, increase the number of company-operated service center stores, and contribute to growing the retail footprint to 1,928 system-wide service center stores.

During the six months ended March 31, 2023, the Company acquired 13 service center stores in single and multi-store transactions for an aggregate purchase price of $18.9 million.

11

The Company’s acquisitions are accounted for as business combinations. A summary follows of the aggregate cash consideration paid and the total assets acquired and liabilities assumed for the six months ended March 31:

| (In millions) | 2024 | 2023 | ||||||||||||

| Inventories | $ | $ | ||||||||||||

Property, plant and equipment (a) | ||||||||||||||

| Operating lease assets | ||||||||||||||

Goodwill (b) | ||||||||||||||

Intangible assets (c) | ||||||||||||||

Reacquired franchise rights (d) | ||||||||||||||

| Other | ||||||||||||||

Other current liabilities (a) | ( | ( | ||||||||||||

| Operating lease liabilities | ( | |||||||||||||

Other noncurrent liabilities (a) | ( | ( | ||||||||||||

| Total net assets acquired | $ | $ | ||||||||||||

(a)Includes finance lease assets in property, plant and equipment and finance lease liabilities in other current and noncurrent liabilities. During the six months ended March 31, 2024, acquired were $3.1 million and of $0.1 million and $3.0 million in other current and noncurrent liabilities, respectively. During the six months ended March 31, 2023, acquired were $2.4 million and of $0.1 million and $2.3 million in other current and noncurrent liabilities.

(b)Goodwill is generally expected to be deductible for income tax purposes and is primarily attributed to the operational synergies and potential growth expected to result in economic benefits in the respective markets of the acquisitions.

(c)Intangible assets acquired during the six months ended March 31, 2024 and 2023 have weighted average amortization periods of and nine years , respectively.

(d)Prior to the acquisition of former franchise service center stores, the Company licensed the right to operate franchised service centers, including the use of Valvoline's trademarks and trade name. In connection with these acquisitions, Valvoline reacquired those rights and recognized separate definite-lived reacquired franchise rights intangible assets, which are being amortized on a straight-line basis over the weighted average remaining term of approximately ten years for the rights reacquired in fiscal 2023. The effective settlement of these arrangements resulted in no settlement gain or loss as the contractual terms were at market. There have been no franchise rights reacquired during fiscal 2024.

The fair values above are preliminary for up to one year from the date of acquisition as they may be subject to measurement period adjustments if new information is obtained about facts and circumstances that existed as of the acquisition date. The Company does not currently expect any material changes to the preliminary purchase price allocations for acquisitions completed during the last twelve months.

NOTE 5 - DEBT

The following table summarizes Valvoline’s total debt as of:

| (In millions) | March 31 2024 | September 30 2023 | ||||||||||||

| 2031 Notes | $ | $ | ||||||||||||

| 2030 Notes | ||||||||||||||

| Term Loan | ||||||||||||||

Revolver (a) | ||||||||||||||

| Debt issuance costs and discounts | ( | ( | ||||||||||||

| Total debt | ||||||||||||||

| Current portion of long-term debt | ||||||||||||||

| Long-term debt | $ | $ | ||||||||||||

(a)As of March 31, 2024, the total borrowing capacity remaining under the $475.0 million revolving credit facility was $471.8 million due to a reduction of $3.2 million for letters of credit outstanding.

12

2030 Notes

On March 14, 2024, the Company commenced a tender offer (the “Tender Offer”) to purchase its outstanding 4.250 % senior unsecured notes due 2030 with an aggregate principal amount of $600.0 million (the “2030 Notes”). The Tender Offer was made to comply with the requirements of the asset sale covenant under the indenture governing the 2030 Notes in connection with the sale of Global Products.

On April 16, 2024, Valvoline completed the Tender Offer with 99.7 % of the outstanding principal amount tendered by the holders of the 2030 Notes. The Company used cash and cash equivalents on hand, in addition to borrowing $175.0 million on the Revolver to facilitate the $598.3 million purchase of the 2030 Notes at par, plus accrued and unpaid interest, and cancelled the 2030 Notes accepted for purchase. The Company elected to redeem the remaining balance outstanding of $1.7 million on April 29, 2024 pursuant to the terms and conditions of the indenture governing the 2030 Notes. Valvoline expects to recognize a loss on extinguishment of the 2030 Notes of $5.1 million during the third quarter of fiscal 2024 due to the write-off of unamortized debt issuance costs and discounts. The 2030 Notes are reported in Current portion of long-term debt within the Condensed Consolidated Balance Sheet as of March 31, 2024.

As of March 31, 2024, Valvoline was in compliance with all covenants under its long-term borrowings.

NOTE 6 – INCOME TAXES

Income tax provisions for interim quarterly periods are based on an estimated annual effective income tax rate calculated separately from the effect of significant, infrequent or unusual discrete items related specifically to interim periods. The following summarizes income tax expense and the effective tax rate in each interim period:

| Three months ended March 31 | Six months ended March 31 | |||||||||||||||||||||||||

| (In millions) | 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||||

| Income tax expense (benefit) | $ | $ | $ | $ | ( | |||||||||||||||||||||

| Effective tax rate percentage | % | % | % | ( | % | |||||||||||||||||||||

13

NOTE 7 – EMPLOYEE BENEFIT PLANS

The following table summarizes the components of pension and other postretirement plan expense:

| Pension benefits | Other postretirement benefits | |||||||||||||||||||||||||

| (In millions) | 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||||

| Three months ended March 31 | ||||||||||||||||||||||||||

| Interest cost | $ | $ | $ | $ | ||||||||||||||||||||||

| Expected return on plan assets | ( | ( | ||||||||||||||||||||||||

| Amortization of prior service credits | ( | ( | ||||||||||||||||||||||||

| Net periodic benefit costs (income) | $ | $ | $ | ( | $ | ( | ||||||||||||||||||||

| Six months ended March 31 | ||||||||||||||||||||||||||

| Interest cost | $ | $ | $ | $ | ||||||||||||||||||||||

| Expected return on plan assets | ( | ( | ||||||||||||||||||||||||

| Amortization of prior service credit | ( | ( | ||||||||||||||||||||||||

| Actuarial gain | ||||||||||||||||||||||||||

| Net periodic benefit costs (income) | $ | $ | $ | ( | $ | ( | ||||||||||||||||||||

NOTE 8 – LITIGATION, CLAIMS AND CONTINGENCIES

From time to time, Valvoline is party to lawsuits, claims and other legal proceedings that arise in the ordinary course of business. The Company establishes liabilities for the outcome of such matters where losses are determined to be probable and reasonably estimable. Where appropriate, the Company has recorded liabilities with respect to these matters, which were not material for the periods presented as reflected in the condensed consolidated financial statements herein. There are certain claims and legal proceedings pending where loss is not determined to be probable or reasonably estimable, and therefore, accruals have not been made. In addition, Valvoline discloses matters when management believes a material loss is at least reasonably possible.

In all instances, management has assessed each matter based on current information available and made a judgment concerning its potential outcome, giving due consideration to the amount and nature of the claim and the probability of success. The Company believes it has established adequate accruals for liabilities that are probable and reasonably estimable.

Although the ultimate resolution of these matters cannot be predicted with certainty and there can be no assurances that the actual amounts required to satisfy liabilities from these matters will not exceed the amounts reflected in the condensed consolidated financial statements, based on information available at this time, it is the opinion of management that such pending claims or proceedings will not have a material adverse effect on its condensed consolidated financial statements.

14

NOTE 9 - EARNINGS PER SHARE

The following table summarizes basic and diluted earnings per share:

| Three months ended March 31 | Six months ended March 31 | |||||||||||||||||||||||||

| (In millions, except per share amounts) | 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||||

| Numerator | ||||||||||||||||||||||||||

| Income from continuing operations | $ | $ | $ | $ | ||||||||||||||||||||||

| (Loss) income from discontinued operations, net of tax | ( | ( | ||||||||||||||||||||||||

| Net income | $ | $ | $ | $ | ||||||||||||||||||||||

| Denominator | ||||||||||||||||||||||||||

| Weighted average common shares outstanding | ||||||||||||||||||||||||||

Effect of potentially dilutive securities (a) | ||||||||||||||||||||||||||

| Weighted average diluted shares outstanding | ||||||||||||||||||||||||||

| Basic earnings (loss) per share | ||||||||||||||||||||||||||

| Continuing operations | $ | $ | $ | $ | ||||||||||||||||||||||

| Discontinued operations | ( | ( | ||||||||||||||||||||||||

| Basic earnings per share | $ | $ | $ | $ | ||||||||||||||||||||||

| Diluted earnings (loss) per share | ||||||||||||||||||||||||||

| Continuing operations | $ | $ | $ | $ | ||||||||||||||||||||||

| Discontinued operations | ( | ( | ||||||||||||||||||||||||

| Diluted earnings per share | $ | $ | $ | $ | ||||||||||||||||||||||

NOTE 10 - SUPPLEMENTAL FINANCIAL INFORMATION

Cash, cash equivalents and restricted cash

The following provides a reconciliation of cash, cash equivalents and restricted cash reported within the Condensed Consolidated Statements of Cash Flows to the Condensed Consolidated Balance Sheets:

| (In millions) | March 31 2024 | September 30 2023 | March 31 2023 | |||||||||||||||||

| Cash and cash equivalents - continuing operations | $ | $ | $ | |||||||||||||||||

Cash and cash equivalents - held for sale (a) | ||||||||||||||||||||

| Total cash, cash equivalents and restricted cash | $ | $ | $ | |||||||||||||||||

(a)Former Global Products business whose operations were suspended during fiscal 2022, classified as held for sale and impaired as of September 30, 2023, and subsequently sold during the first quarter of fiscal 2024.

Accounts and other receivables

The following summarizes Valvoline’s accounts and other receivables in the Condensed Consolidated Balance Sheets as of:

| (In millions) | March 31 2024 | September 30 2023 | ||||||||||||

| Current | ||||||||||||||

| Trade | $ | $ | ||||||||||||

Notes receivable from franchisees | ||||||||||||||

| Other | ||||||||||||||

| Receivables, gross | ||||||||||||||

| Allowance for credit losses | ( | ( | ||||||||||||

| Receivables, net | $ | $ | ||||||||||||

Non-current (a) | ||||||||||||||

| Notes receivable | $ | $ | ||||||||||||

| Other | ||||||||||||||

| Noncurrent notes receivable, gross | ||||||||||||||

| Allowance for losses | ( | ( | ||||||||||||

| Noncurrent notes receivable, net | $ | $ | ||||||||||||

(a)Included in Other noncurrent assets within the Condensed Consolidated Balance Sheets.

Revenue recognition

The following disaggregates the Company’s net revenues by timing of revenue recognized:

| Three months ended March 31 | Six months ended March 31 | |||||||||||||||||||||||||

| (In millions) | 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||||

| Net revenues transferred at a point in time | $ | $ | $ | $ | ||||||||||||||||||||||

| Franchised revenues transferred over time | ||||||||||||||||||||||||||

| Net revenues | $ | $ | $ | $ | ||||||||||||||||||||||

The following table summarizes net revenues by category:

| Three months ended March 31 | Six months ended March 31 | |||||||||||||||||||||||||

| (In millions) | 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||||

| Oil changes and related fees | $ | $ | $ | $ | ||||||||||||||||||||||

| Non-oil changes and related fees | ||||||||||||||||||||||||||

Franchise fees and other (a) | ||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||||||||||||

(a)Includes $0.2 million of net revenues associated with suspended operations for the six months ended March 31, 2023.

15

FORWARD-LOOKING STATEMENTS

Certain statements in this Quarterly Report on Form 10-Q, other than statements of historical fact, are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements may include, without limitation, executing on its growth strategy to create shareholder value by driving the full potential in the Company’s core business, accelerating network growth and innovating to meet the needs of customers and the evolving car parc; realizing the benefits from the sale of Global Products; and future opportunities for the remaining stand-alone retail business; and any other statements regarding Valvoline's future operations, financial or operating results, capital allocation, debt leverage ratio, anticipated business levels, dividend policy, anticipated growth, market opportunities, strategies, competition, and other expectations and targets for future periods. Valvoline has identified some of these forward-looking statements with words such as “anticipates,” “believes,” “expects,” “estimates,” “is likely,” “predicts,” “projects,” “forecasts,” “may,” “will,” “should,” and “intends,” and the negative of these words or other comparable terminology. These forward-looking statements are based on Valvoline’s current expectations, estimates, projections, and assumptions as of the date such statements are made and are subject to risks and uncertainties that may cause results to differ materially from those expressed or implied in the forward-looking statements. Factors that might cause such differences include, but are not limited to, those discussed under the headings “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and “Quantitative and Qualitative Disclosures about Market Risk” in this Quarterly Report on Form 10-Q and Valvoline’s most recently filed Annual Report on Form 10-K. Valvoline assumes no obligation to update or revise these forward-looking statements for any reason, even if new information becomes available in the future, unless required by law.

| Index to Management’s Discussion and Analysis of Financial Condition and Results of Operations | Page | ||||

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis should be read in conjunction with the Annual Report on Form 10-K for the fiscal year ended September 30, 2023, as well as the condensed consolidated financial statements and the accompanying Notes to Condensed Consolidated Financial Statements included in Item 1 of Part I in this Quarterly Report on Form 10-Q. Unless otherwise noted, disclosures within Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations relate solely to the Company's continuing operations.

BUSINESS OVERVIEW AND PURPOSE

As the quick, easy, trusted leader in automotive preventive maintenance, Valvoline Inc. is creating shareholder value by driving the full potential in its core business, accelerating network growth and innovating to meet the needs of customers and the evolving car parc. With average customer ratings that indicate high levels of service satisfaction, Valvoline and the Company’s franchise partners keep customers moving with 15-minute stay-in-your-car oil changes; battery, bulb and wiper replacements; tire rotations; and other manufacturer recommended maintenance services. The Company operates and franchises more than 1,900 service center locations through its Valvoline Instant Oil ChangeSM and Great Canadian Oil Change retail locations and supports nearly 300 locations through its Express CareTM platform.

16

BUSINESS STRATEGY

As a pure play automotive retail services provider and the trusted leader in preventive automotive maintenance, Valvoline is well positioned to create long-term shareholder value through executing the Company’s strategic initiatives, which include:

•Driving the full potential of the core business through increasing market share and non-oil change revenue growth in existing stores by building on Valvoline’s strong foundation in marketing, technology, and data;

•Aggressively growing the retail footprint with company-operated store growth and an increased emphasis on franchisee store growth; and

•Developing capabilities to capture new customers through services expansion focused on fleet manager needs and needs of the evolving car parc.

SECOND FISCAL QUARTER 2024 OVERVIEW

The following were the significant events for the second fiscal quarter of 2024, each of which is discussed more fully in this Quarterly Report on Form 10-Q:

•Valvoline’s net revenues grew 13% over the prior year period driven by system-wide same-store sales ("SSS") growth of 7.7% and the addition of 147 net new stores to the system from the prior year.

•Income from continuing operations grew 32% to $43.3 million for the three months ended March 31, 2024 compared to the prior year. This growth is attributable to strong gross profit expansion which was partially offset by increased investments in selling, general and administrative expenses. Diluted earnings per share from the continuing operations increased 74% to $0.33 in the three months ended March 31, 2024 compared to the prior year period driven by earnings expansion from operating results and share count reductions from repurchases, including benefits from the prior year execution of the share repurchase tender offer.

•Adjusted EBITDA increased 21% over the prior year period due to strong top-line growth driven by higher average ticket price from pricing actions, non-oil change service penetration and premiumization. Additionally, benefits from improved labor cost efficiency were partially offset by growth investments in selling, general and administrative expenses.

•The Company returned $40.4 million to its shareholders during the quarter through repurchases of 1.0 million shares of Valvoline common stock completing the 2022 Share Repurchase Authorization for $1.6 billion and successfully returning a substantial portion of the net proceeds from the sale of Global Products to shareholders.

Use of Non-GAAP Measures

To aid in the understanding of Valvoline’s ongoing business performance, certain items within this document are presented on an adjusted, non-GAAP basis. These non-GAAP measures have limitations as analytical tools and should not be considered in isolation from, or as an alternative to, or more meaningful than, the financial statements presented in accordance with U.S. GAAP. The financial results presented in accordance with U.S. GAAP and reconciliations of non-GAAP measures included within this Quarterly Report on Form 10-Q should be carefully evaluated.

The following are the non-GAAP measures management has included and how management defines them:

•EBITDA - net income/loss, plus income tax expense/benefit, net interest and other financing expenses, and depreciation and amortization;

•Adjusted EBITDA - EBITDA adjusted for the impacts of certain unusual, infrequent or non-operational activity not directly attributable to the underlying business, which management believes impacts the comparability of operational results between periods ("key items," as further described below);

17

•Adjusted EBITDA margin - adjusted EBITDA divided by adjusted net revenues;

•Adjusted net revenues - reported net revenues adjusted for key items;

•Free cash flow - cash flows from operating activities less capital expenditures and certain other adjustments as applicable; and

•Discretionary free cash flow - cash flows from operating activities less maintenance capital expenditures and certain other adjustments as applicable.

Non-GAAP measures include adjustments from results based on U.S. GAAP that management believes enables comparison of certain financial trends and results between periods and provides a useful supplemental presentation of Valvoline's operating performance that allows for transparency with respect to key metrics used by management in operating the business and measuring performance. The manner used to compute non-GAAP information used by management may differ from the methods used by other companies, and may not be comparable. For a reconciliation of the most comparable U.S. GAAP measures to the non-GAAP measures, refer to the “Results of Operations” and “Financial Position, Liquidity and Capital Resources” sections below.

Management believes EBITDA measures provide a meaningful supplemental presentation of Valvoline’s operating performance between periods on a comparable basis due to the depreciable assets associated with the nature of the Company’s operations as well as income tax and interest costs related to Valvoline’s tax and capital structures, respectively. Adjusted EBITDA measures enable comparison of financial trends and results between periods where certain items may not be reflective of the Company’s underlying and ongoing operations performance or vary independent of business performance.

Management uses free cash flow and discretionary free cash flow as additional non-GAAP metrics of cash flow generation. By including capital expenditures and certain other adjustments, as applicable, management is able to provide an indication of the ongoing cash being generated that is ultimately available for both debt and equity holders as well as other investment opportunities. Free cash flow includes the impact of capital expenditures, providing a supplemental view of cash generation. Discretionary free cash flow includes maintenance capital expenditures, which are routine uses of cash that are necessary to maintain the Company's operations and provides a supplemental view of cash flow generation to maintain operations before discretionary investments in growth. Free cash flow and discretionary free cash flow have certain limitations, including that they do not reflect adjustments for certain non-discretionary cash flows, such as mandatory debt repayments.

The non-GAAP measures used by management exclude key items. Key items are often related to legacy matters or market-driven events considered by management to not be reflective of the ongoing operating performance. Key items may consist of adjustments related to: legacy businesses, including the separation from Valvoline's former parent company, the former Global Products reportable segment, and associated impacts of related activity and indemnities; non-service pension and other postretirement plan activity; restructuring-related matters, including organizational restructuring plans, the separation of Valvoline’s businesses, significant acquisitions or divestitures, debt extinguishment and modification, and tax reform legislation; in addition to other matters that management considers non-operational, infrequent or unusual in nature.

Details with respect to the description and composition of key items recognized during the respective periods presented herein are set forth below in the “EBITDA and Adjusted EBITDA” section of “Results of Operations” that follows.

Key Business Measures

Valvoline tracks its operating performance and manages its business using certain key measures, including system-wide, company-operated and franchised store counts and SSS; and system-wide store sales. Management believes these measures are useful to evaluating and understanding Valvoline's operating performance and should be considered as supplements to, not substitutes for, Valvoline's net revenues and operating income, as determined in accordance with U.S. GAAP.

18

Net revenues are influenced by the number of service center stores and the business performance of those stores. Stores are considered open upon acquisition or opening for business. Temporary store closings remain in the respective store counts with only permanent store closures reflected in the activity and end of period store counts. SSS is defined as net revenues by U.S. Valvoline Instant Oil Change (“VIOC”) stores (company-operated, franchised and the combination of these for system-wide SSS), with new stores, including franchised conversions, excluded from the metric until the completion of their first full fiscal year in operation as this period is generally required for new store sales levels to begin to normalize.

Net revenues are limited to sales at company-operated stores, in addition to royalties and other fees from independent franchised and Express Care stores. Although Valvoline does not recognize store-level sales from franchised stores as net revenues in its Statements of Condensed Consolidated Income, management believes system-wide and franchised SSS comparisons, store counts, and total system-wide store sales are useful to assess market position relative to competitors and overall store and operating performance.

RESULTS OF OPERATIONS

The following summarizes the results of the Company’s continuing operations for the periods ended March 31:

| Three months ended March 31 | Six months ended March 31 | |||||||||||||||||||||||||||||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||||||||||||||||||||||||||||||

| (In millions) | Amount | % of Net revenues | Amount | % of Net revenues | Amount | % of Net revenues | Amount | % of Net revenues | ||||||||||||||||||||||||||||||||||||||||||

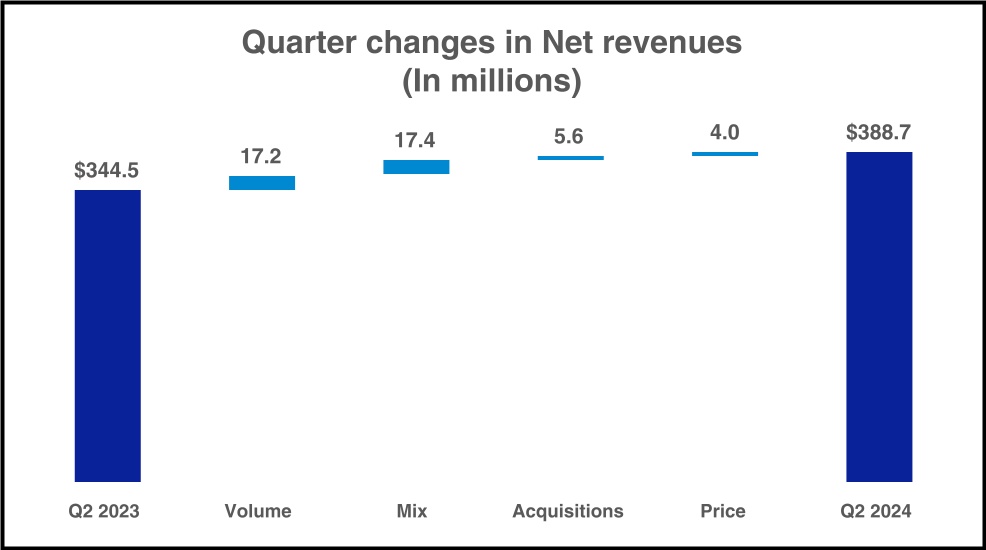

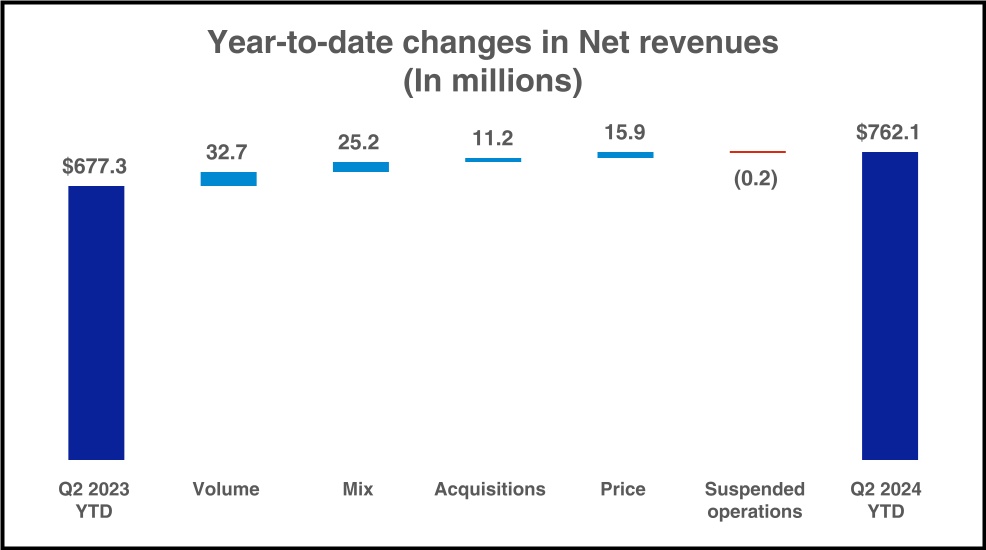

| Net revenues | $ | 388.7 | 100.0% | $ | 344.5 | 100.0% | $ | 762.1 | 100.0% | $ | 677.3 | 100.0% | ||||||||||||||||||||||||||||||||||||||

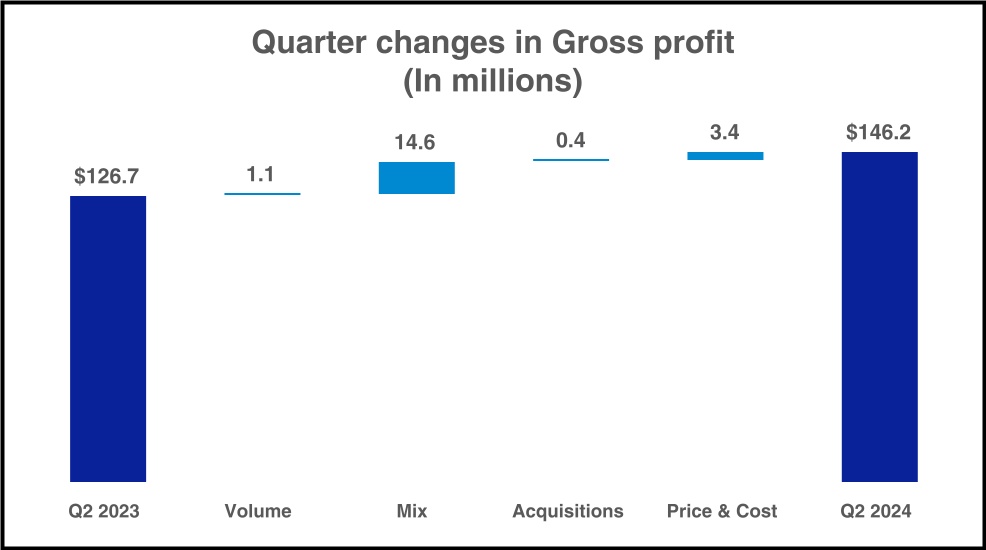

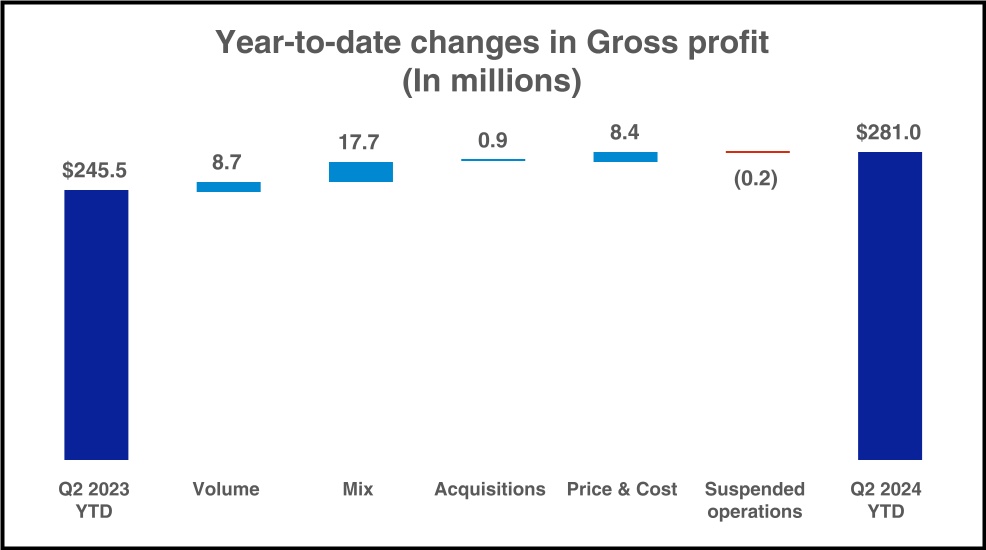

| Gross profit | $ | 146.2 | 37.6% | $ | 126.7 | 36.8% | $ | 281.0 | 36.9% | $ | 245.5 | 36.2% | ||||||||||||||||||||||||||||||||||||||

| Net operating expenses | $ | 69.8 | 18.0% | $ | 65.5 | 19.0% | $ | 141.8 | 18.6% | $ | 155.0 | 22.9% | ||||||||||||||||||||||||||||||||||||||

| Operating income | $ | 76.4 | 19.7% | $ | 61.2 | 17.8% | $ | 139.2 | 18.3% | $ | 90.5 | 13.4% | ||||||||||||||||||||||||||||||||||||||

| Income from continuing operations | $ | 43.3 | 11.1% | $ | 32.9 | 9.6% | $ | 77.2 | 10.1% | $ | 59.9 | 8.8% | ||||||||||||||||||||||||||||||||||||||

EBITDA (a) | $ | 98.4 | 25.3% | $ | 78.2 | 22.7% | $ | 182.4 | 23.9% | $ | 122.3 | 18.1% | ||||||||||||||||||||||||||||||||||||||

Adjusted EBITDA (a) | $ | 105.1 | 27.0% | $ | 87.1 | 25.3% | $ | 195.3 | 25.6% | $ | 160.4 | 23.7% | ||||||||||||||||||||||||||||||||||||||

(a)Refer to the “Use of Non-GAAP Measures” and Continuing operations EBITDA and Adjusted EBITDA for management’s definitions of the metrics presented above and reconciliation to the corresponding GAAP measures, where applicable.

19

| Three months ended March 31 | Six months ended March 31 | |||||||||||||||||||||||||

| 2024 | 2023 | 2023 | 2023 | |||||||||||||||||||||||

System-wide store sales - in millions (a) | $ | 746.1 | $ | 659.9 | $ | 1,469.0 | $ | 1,303.9 | ||||||||||||||||||

Year-over-year growth (a) | 13.1 | % | 18.5 | % | 12.7 | % | 17.7 | % | ||||||||||||||||||

Same-store sales growth (b) | ||||||||||||||||||||||||||

| Company-operated | 7.4 | % | 14.2 | % | 6.8 | % | 13.5 | % | ||||||||||||||||||

Franchised (a) | 8.0 | % | 12.9 | % | 8.0 | % | 12.0 | % | ||||||||||||||||||

System-wide (a) | 7.7 | % | 13.5 | % | 7.4 | % | 12.7 | % | ||||||||||||||||||

| Number of stores at end of period | |||||||||||||||||||||||||||||||||||

| Second Quarter 2024 | First Quarter 2024 | Fourth Quarter 2023 | Third Quarter 2023 | Second Quarter 2023 | |||||||||||||||||||||||||||||||

| Company-operated | 919 | 895 | 876 | 854 | 832 | ||||||||||||||||||||||||||||||

Franchised (a) | 1,009 | 995 | 976 | 950 | 949 | ||||||||||||||||||||||||||||||

Total system-wide stores (a) | 1,928 | 1,890 | 1,852 | 1,804 | 1,781 | ||||||||||||||||||||||||||||||

| (a) | Measures include Valvoline franchisees, which are independent legal entities. Valvoline does not consolidate the results of operations of its franchisees. | ||||||||||||||||||||||||||||||||||

| (b) | Valvoline determines SSS growth as sales by U.S. VIOC stores (company-operated, franchised, and the combination of these for system-wide SSS), with new stores, including franchised conversions, excluded from the metric until the completion of their first full fiscal year in operation. | ||||||||||||||||||||||||||||||||||

Net revenues

Net revenues increased $44.2 million, or 12.8% for the three months ended March 31, 2024 compared to the prior year period. Store operations fueled top-line expansion with system-wide SSS increasing by 7.7% largely due to increased ticket from non-oil change service penetration with the balance from net pricing and premiumization. Transaction growth contributed modestly to system-wide SSS growth driven primarily by benefits from day mix. Additionally, revenue growth was bolstered by the addition of 147 net new stores through openings and acquisitions. The following reconciles the year-over-year change in net revenues:

Net revenues increased $84.8 million, or 12.5% for the six months ended March 31, 2024 compared to the prior year period due to volume, mix and price improvements, as well as store expansion through net new openings and acquisitions. System-wide SSS grew 7.4% compared to the prior year with ticket contributing the majority of the

20

benefits from non-oil change service penetration, premiumization, and pricing actions, in addition to increased transactions. The following reconciles the year-over-year change in year-to-date net revenues:

Gross profit

Gross profit increased $19.5 million, or 15.4%, for the three months ended March 31, 2024 compared to the prior year period. Profitability increased primarily due to mix improvements from non-oil change service penetration and premiumization. Additionally, strategic pricing actions coupled with cost efficiencies, particularly in labor and modest benefits from materials increased profitability and were partially offset by increased store operating expenses, including higher depreciation. The following reconciles the year-over-year change in gross profit:

Gross profit margin improved in the three months ended March 31, 2024 compared to the prior year primarily due to labor efficiency resulting from strong schedule management.

Gross profit improved $35.5 million, or 14.5%, for the six months ended March 31, 2024 compared to the prior year period driven by increased average ticket from non-oil change service penetration and premiumization as well as pricing actions. Additionally, increased transactions and unit growth also provided benefits along with improved labor management. The following reconciles the year-over-year change in year-to-date gross profit:

21

The improvement in gross profit margin in the six months ended March 31, 2024 compared to the prior year was primarily due to pricing actions and labor efficiency which resulted in staff providing best-in-class customer experiences improving overall service mix. These benefits were partially offset by increased store operating expenses, including higher depreciation.

Net operating expenses

Details of the components of Net operating expenses are summarized below for the periods ended March 31:

| Three months ended March 31 | Six months ended March 31 | |||||||||||||||||||||||||||||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||||||||||||||||||||||||||||||

| (In millions) | Amount | % of Net revenues | Amount | % of Net revenues | Amount | % of Net revenues | Amount | % of Net revenues | ||||||||||||||||||||||||||||||||||||||||||

| Selling, general and administrative expenses | $ | 72.3 | 18.6 | % | $ | 62.6 | 18.2 | % | $ | 146.8 | 19.3 | % | $ | 128.6 | 19.0 | % | ||||||||||||||||||||||||||||||||||

| Net legacy and separation-related expenses | — | — | % | 3.8 | 1.1 | % | 0.1 | — | % | 29.2 | 4.3 | % | ||||||||||||||||||||||||||||||||||||||

| Other income, net | (2.5) | (0.6) | % | (0.9) | (0.3) | % | (5.1) | (0.7) | % | (2.8) | (0.4) | % | ||||||||||||||||||||||||||||||||||||||

| Net operating expenses | $ | 69.8 | 18.0 | % | $ | 65.5 | 19.0 | % | $ | 141.8 | 18.6 | % | $ | 155.0 | 22.9 | % | ||||||||||||||||||||||||||||||||||

Selling, general and administrative expenses (“SG&A”) increased $9.7 million and $18.2 million for the three and six months ended March 31, 2024, respectively, compared to the prior year periods. These increases were principally driven by costs from implementing stand-alone information technology platforms, and increased investments in advertising to attract and retain customers and talent to support future growth. Additionally, higher travel expenses related to the Company’s annual meeting and store growth contributed to the increase in the six months ended March 31, 2024.

Net legacy and separation-related expenses decreased $3.8 million and $29.1 million for the three and six months ended March 31, 2024, respectively, compared to the prior year periods attributable to activities that did not recur. In the three and six months ended March 31, 2023, the expense was primarily associated with the modification of certain performance-based unvested stock awards as a result of the sale of Global Products as well as expense of $24.4 million to increase the indemnity obligation and reflect the utilization of certain legacy tax attributes associated with the amendment of the tax matters agreement with its former parent company during the six months ended March 31, 2023.

22

Other income, net increased $1.6 million and $2.3 million in the three and six months ended March 31, 2024, respectively, compared to the prior year periods, primarily due to higher rental income from subleasing properties in connection with the sale of Global Products partially offset by expense associated with an investment impairment of $1.0 million in the prior year period which did not recur.

Net pension and other postretirement plan expenses

Net pension and other postretirement plan expenses were flat in the three months ended March 31, 2024 and decreased $0.3 million in the six months ended March 31, 2024 compared to the prior year periods. The decrease was generally attributable to higher recurring expected returns on plan assets partially offset by higher interest costs of the rate environment as a result of the most recent annual remeasurement of the plans.

Net interest and other financing expenses

Net interest and other financing expenses increased $2.2 million and decreased $2.9 million during the three and six months ended March 31, 2024, respectively, compared to the prior year periods. While higher rates on outstanding borrowings increased expense during the periods, interest income on invested remaining net proceeds from the sale of Global Products drove benefits. These benefits more than offset the increased expense in the year-to-date period and were lower to partially offset increased expense in the quarter as the investments matured prior to executing the Tender Offer in April 2024.

Income tax provision

The following table summarizes income tax provision and the effective tax rate for the current and prior year periods:

| Three months ended March 31 | Six months ended March 31 | |||||||||||||||||||||||||

| (In millions) | 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||||

| Income tax expense (benefit) | $ | 14.0 | $ | 11.4 | $ | 25.9 | $ | (8.7) | ||||||||||||||||||

| Effective tax rate percentage | 24.4 | % | 25.7 | % | 25.1 | % | (17.0) | % | ||||||||||||||||||

The increase in income tax expense for the three months ended March 31, 2024 was principally driven by higher pre-tax earnings, while the reduction in the effective tax rate was primarily attributed to the favorable impact of discrete tax benefits. The increases in income tax expense and the effective tax rate for the six months ended March 31, 2024 were driven by more normalized activity in the current year period as compared to the prior year period which included the recognition of a $26.5 million income tax benefit for the release of a valuation allowance due to the change in expectations regarding the utilization of certain legacy tax attributes as a result of the terms of the amended tax matters agreement with Valvoline’s former parent company. This amendment also resulted in higher Net legacy and separation-related expenses of $24.4 million for the related increased indemnity obligation for the six months ended March 31, 2023.

(Loss) income from discontinued operations, net of tax

The following summarizes (Loss) income from discontinued operations, net of tax for the current and prior year periods:

| Three months ended March 31 | Six months ended March 31 | |||||||||||||||||||||||||

| (In millions) | 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||||

| (Loss) income from discontinued operations, net of tax | $ | (1.9) | $ | 1,194.4 | $ | (3.9) | $ | 1,249.3 | ||||||||||||||||||

Earnings from discontinued operations declined $1.196 billion and $1.253 billion in the three and six months ended March 31, 2024, respectively, compared to the prior year periods primarily due to the recognition of a gain on the sale of the Global Products business in March 2023 resulting in costs associated with the separation of processes

23

and systems and no longer reflecting operational results from the underlying business for the three and six months ended March 31, 2024.

Continuing operations adjusted net revenues

The following table reconciles Net revenues to Adjusted net revenues for the current and prior year periods:

| Three months ended March 31 | Six months ended March 31 | |||||||||||||||||||||||||

| (In millions) | 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||||

| Reported net revenues | $ | 388.7 | $ | 344.5 | $ | 762.1 | $ | 677.3 | ||||||||||||||||||

| Key items: | ||||||||||||||||||||||||||

Suspended operations (a) | — | — | — | (0.2) | ||||||||||||||||||||||

Adjusted net revenues (b) (c) | $ | 388.7 | $ | 344.5 | $ | 762.1 | $ | 677.1 | ||||||||||||||||||

(a)Represents the results of a former Global Products business where operations were suspended during fiscal 2022 that were not included in the sale.

(b)Adjusted net revenues are reported net revenues adjusted for key items.

(c)Represents a non-GAAP measure. Refer to “Use of Non-GAAP Measures” for management’s definitions of the metrics presented above.

Continuing operations EBITDA and Adjusted EBITDA

The following table reconciles Income from continuing operations to EBITDA and Adjusted EBITDA for the current and prior year periods:

| Three months ended March 31 | Six months ended March 31 | |||||||||||||||||||||||||

| (In millions) | 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||||

| Income from continuing operations | $ | 43.3 | $ | 32.9 | $ | 77.2 | $ | 59.9 | ||||||||||||||||||

| Income tax expense (benefit) | 14.0 | 11.4 | 25.9 | (8.7) | ||||||||||||||||||||||

| Net interest and other financing expenses | 15.5 | 13.3 | 29.1 | 32.0 | ||||||||||||||||||||||

| Depreciation and amortization | 25.6 | 20.6 | 50.2 | 39.1 | ||||||||||||||||||||||

EBITDA from continuing operations (a) | 98.4 | 78.2 | 182.4 | 122.3 | ||||||||||||||||||||||

Net pension and other postretirement plan expenses (b) | 3.6 | 3.6 | 7.0 | 7.3 | ||||||||||||||||||||||

Net legacy and separation-related expenses (c) | — | 3.8 | 0.1 | 29.2 | ||||||||||||||||||||||

Information technology transition costs (d) | 3.1 | 0.4 | 5.8 | 0.7 | ||||||||||||||||||||||

Investment and divestiture-related costs (e) | — | 1.0 | — | 1.0 | ||||||||||||||||||||||

Suspended operations (f) | — | 0.1 | — | (0.1) | ||||||||||||||||||||||

Adjusted EBITDA from continuing operations (a) | $ | 105.1 | $ | 87.1 | $ | 195.3 | $ | 160.4 | ||||||||||||||||||

| (a) | EBITDA from continuing operations is defined as income from continuing operations, plus income tax expense (benefit), net interest and other financing expenses, and depreciation and amortization attributable to continuing operations. Adjusted EBITDA from continuing operations is EBITDA adjusted for key items attributable to continuing operations. | ||||

| (b) | Includes several elements impacted by changes in plan assets and obligations that are primarily driven by the debt and equity markets, including remeasurement gains and losses, when applicable; and recurring non-service pension and other postretirement net periodic activity, which consists of interest cost, expected return on plan assets and amortization of prior service credits. Management considers these elements are more reflective of changes in current conditions in global markets (in particular, interest rates), outside the operational performance of the business, and are also legacy amounts that are not directly related to the underlying business and do not have an impact on the compensation and benefits provided to eligible employees for current service. Refer to Note 7 in the Notes to Condensed Consolidated Financial Statements in Item 1 of Part I in this Quarterly Report on Form 10-Q for further details. | ||||

24

| (c) | Activity associated with legacy businesses, including the separation from Valvoline’s former parent company and its former Global Products reportable segment. This activity includes the recognition of and adjustments to indemnity obligations to its former parent company; certain legal, financial, professional advisory and consulting fees; and other expenses incurred by the continuing operations in connection with and directly related to these separation transactions and legacy matters. This incremental activity directly attributable to legacy matters and separation transactions is not considered reflective of the underlying operating performance of the Company’s continuing operations. During the six months ended March 31, 2023, the Company recognized $24.4 million of pre-tax expense to reflect its increased estimated indemnity obligation which also resulted in an income tax benefit of $26.5 million to reflect the release of valuations allowances in connection with the amendment of the Tax Matters Agreement with Valvoline’s former parent company. | ||||

| (d) | Consists of expenses incurred related to the Company’s transition to a stand-alone enterprise resource planning software system during fiscal years 2023 and 2024, including data conversion, temporary support, training, and redundant expenses incurred from duplicative technology platforms during implementation. These expenses are reflective of incremental costs directly associated with technology transitions and data migration that are not considered to be reflective of the ongoing expenses of operating the Company’s technology platforms. | ||||

| (e) | Expense recognized to reduce the carrying value of an investment interest determined to be impaired. This cost is not considered to be reflective of the underlying performance of the Company’s ongoing continuing operations. | ||||

| (f) | Represents the results of a former Global Products business where operations were suspended during fiscal 2022. This business was not included in the sale of the Global Products business in March 2023. It was classified as held for sale and impaired as of September 30, 2023, and subsequently sold during the first fiscal quarter of 2024. These results are not indicative of the operating performance of the Company’s ongoing continuing operations. | ||||

Adjusted EBITDA from continuing operations increased $18.0 million for the three months ended March 31, 2024 and increased $34.9 million in the six months ended March 31, 2024 compared to the prior year periods driven by strong revenue growth primarily due to higher average ticket from pricing actions, non-oil change service penetration, and premiumization. In addition, improved labor cost efficiency was partially offset by SG&A investments to support future growth.

FINANCIAL POSITION, LIQUIDITY AND CAPITAL RESOURCES

Overview

The Company closely manages its liquidity and capital resources. Valvoline’s liquidity requirements depend on key variables, including the level of investment needed to support business strategies, the performance of the business, capital expenditures, borrowing arrangements, and working capital management. Capital expenditures, acquisitions, share repurchases, and dividend payments are components of the Company’s cash flow and capital management strategy, which to a large extent, can be adjusted in response to economic and other changes in the business environment. The Company has a disciplined approach to capital allocation, which focuses on investing in key priorities that support Valvoline’s business and growth strategies and returning capital to shareholders, while funding ongoing operations.

Continuing operations cash flows

Valvoline’s continuing operations cash flows as reflected in the Condensed Consolidated Statements of Cash Flows are summarized as follows for the six months ended March 31:

| (In millions) | 2024 | 2023 | ||||||||||||

| Cash provided (used by): | ||||||||||||||

| Operating activities | $ | 92.1 | $ | 173.5 | ||||||||||

| Investing activities | $ | 230.6 | $ | (96.3) | ||||||||||

| Financing activities | $ | (237.6) | $ | (279.4) | ||||||||||

Operating activities

The decrease in cash flows provided by operating activities of $81.4 million from the prior year was primarily driven by changes in net working capital. Unfavorable changes in payables and accruals of approximately $60 million were due to the establishment of the supply agreement and other separation-related matters with Global Products in the prior year. Additionally, a lengthened collection cycle during the current year due to billing delays in connection with the implementation of a new enterprise resource planning (“ERP”) system contributed approximately $25 million to the growth in working capital.

25

Investing activities

The decrease in cash flows used in investing activities of $326.9 million from the prior year was substantially driven by proceeds from the maturities of short-term investments of $350.0 million. This cash inflow was partially offset by a net outflow of $3.7 million for cash transferred in connection with selling a former Global Products business during the current year, in addition to loans extended to franchisees, net of repayments of $5.2 million, an increase in acquisition activity of $2.4 million, and increased capital expenditures of $7.8 million to support investments in store growth.

Financing activities

The decrease in cash flows used in financing activities of $41.8 million from the prior year was primarily due to returning $45.2 million less in cash to shareholders through share repurchases from utilizing the remaining authorization under the 2022 Share Repurchase Authorization during the second quarter of fiscal 2024 in addition to a $23.7 million decrease in cash inflows from net borrowing activity. This decreased use of cash from the prior year was partially offset by lower dividends paid of $21.8 million as the Company discontinued its dividend during the second quarter of fiscal 2023 following the sale of Global Products.

Continuing operations free cash flow

The following sets forth free cash flow and discretionary free cash flow and reconciles cash flows from operating activities to both measures. These free cash flow measures have certain limitations, including that they do not reflect adjustments for certain non-discretionary cash flows, such as mandatory debt repayments. Refer to the “Use of Non-GAAP Measures” section included above in this Item 2 for additional information regarding these non-GAAP measures.

| Six months ended March 31 | ||||||||||||||

| (In millions) | 2024 | 2023 | ||||||||||||

| Cash flows provided by operating activities | $ | 92.1 | $ | 173.5 | ||||||||||

| Less: Maintenance capital expenditures | (13.6) | (9.7) | ||||||||||||

| Discretionary free cash flow | 78.5 | 163.8 | ||||||||||||

| Less: Growth capital expenditures | (73.6) | (69.7) | ||||||||||||

| Free cash flow | $ | 4.9 | $ | 94.1 | ||||||||||

The decrease in free cash flow from continuing operations over the prior year was driven by lower cash flow provided by operating activities in addition to increased capital expenditures during the current period. The increase in maintenance capital expenditures over the prior year period was driven by facility and equipment expenditures due to the growing store count. In addition, the higher growth capital expenditures over the prior year period primarily relate to new store construction. The Company continues to focus the majority of its capital spend toward growth, which is expected to drive a high return on invested capital.

Discontinued operations cash flows

The cash flows of the discontinued operation are reflected in the Condensed Consolidated Statements of Cash Flows and are summarized below for the six months ended March 31:

| (In millions) | 2024 | 2023 | ||||||||||||

| Cash (used in) provided by: | ||||||||||||||

| Operating activities | $ | (3.9) | $ | (63.4) | ||||||||||

| Investing activities | $ | — | $ | 2,623.2 | ||||||||||

| Financing activities | $ | — | $ | (108.1) | ||||||||||

26

The declines in cash flows used in operating and financing activities and those provided from investing activities of the discontinued operation were due to the completion of the sale of Global Products in March 2023, where prior year cash flows were from conducting business within the former Global Products segment and the current year cash flows generally relate to the completion of the separation of the business processes and systems. During the prior year period, cash flows used in operating activities of the discontinued operation were largely driven by trade and other payables activity operating in an unfavorable working capital environment, in addition to transaction costs to support the sale of the Global Products business. Prior year discontinued operations cash flows provided by investing activities were due to the cash consideration received, net of cash transferred to Global Products entities, at the close of the sale of Global Products of $2.6 billion. The decrease in cash flows used in financing activities of discontinued operations was due to net repayments on borrowings during the prior year period, driven by the extinguishment of the $175 million Trade Receivables Facility.

Debt