Table of Contents

Exhibit 99.1

, 2016

Dear Hilton Worldwide Holdings Inc. Stockholder:

I am pleased to inform you that the board of directors of Hilton Worldwide Holdings Inc. (“Hilton Parent” and, together with its consolidated subsidiaries, “Hilton”) approved a plan to enhance long-term stockholder value by separating Hilton into three independent, publicly traded companies. Under the plan, Hilton Parent will execute tax-free spin-offs of Park Hotels & Resorts Inc. (“Park Parent” and, together with its consolidated subsidiaries, “Park Hotels & Resorts”), which will hold a portfolio of Hilton’s owned and leased hotels and resorts, and Hilton Grand Vacations Inc. (“HGV Parent” and, together with its consolidated subsidiaries, “Hilton Grand Vacations”), which will own and operate Hilton’s timeshare business. Upon completion of the spin-offs, Hilton Parent stockholders will own 100% of the outstanding shares of common stock of each of Park Parent and HGV Parent, and will continue to own 100% of the outstanding shares of common stock of Hilton Parent. Park Parent will be a leading lodging real estate investment trust with a diverse portfolio of iconic and market-leading hotels and resorts with significant underlying real estate value, and Hilton Grand Vacations will be a rapidly growing timeshare company that markets and sells vacation ownership intervals and manages resorts in top destinations. Hilton Parent will retain its core management and franchise business and continue to trade on the New York Stock Exchange as a leading global hospitality company.

We believe that this separation is in the best interests of Hilton Parent, its stockholders and other constituents, as it will result in three pure-play companies, enabling dedicated management teams to fully activate their respective businesses, take advantage of both organic and inorganic growth opportunities, and align their structures and capital allocation strategies with a dedicated investor base.

The spin-offs will be completed by way of a pro rata distribution of Park Parent and HGV Parent common stock to our stockholders of record as of 5:00 p.m., Eastern time, on December 15, 2016, the spin-off record date. Each Hilton Parent stockholder will receive one share of Park Parent common stock for every five shares of Hilton Parent common stock and one share of HGV Parent common stock for every ten shares of Hilton Parent common stock, in each case, held by such stockholder on the record date. The distribution of these shares will be made in book-entry form, which means that no physical share certificates will be issued. The transaction is subject to certain customary conditions. Stockholder approval of the distributions is not required, and you are not required to take any action to receive your shares of Park Parent and HGV Parent common stock. Immediately following the spin-offs, you will own common stock in Hilton Parent, Park Parent and HGV Parent. The common stock of Hilton Parent will continue to trade on the New York Stock Exchange under the symbol “HLT.” Both Park Parent and HGV Parent intend to have their common stock listed on the New York Stock Exchange under the symbols “PK” and “HGV,” respectively. We expect the spin-offs to be tax-free to the stockholders of Hilton Parent, except to the extent of cash received in lieu of fractional shares. The spin-offs are conditioned on, among other things, the ruling received by Hilton Parent from the Internal Revenue Service regarding certain U.S. federal income tax aspects of the spin-offs remaining in effect as of the distribution date, and the receipt of an opinion of our tax counsel confirming that the spin-offs will qualify as tax-free distributions under Section 355 of the Internal Revenue Code of 1986, as amended.

We have prepared the enclosed information statements, which describe the spin-offs in detail and contain important information about each of Park Hotels & Resorts and Hilton Grand Vacations, including historical financial statements. We are mailing to all Hilton Parent stockholders a notice with instructions informing holders how to access the information statements online. We urge you to read the information statements carefully.

We want to thank you for your continued support of Hilton, and we look forward to your support of all three companies in the future.

Sincerely,

Christopher J. Nassetta

President and Chief Executive Officer

Hilton Worldwide Holdings Inc.

Table of Contents

, 2016

Dear Hilton Grand Vacations Inc. Stockholder:

It is our pleasure to welcome you as a stockholder of our company, Hilton Grand Vacations Inc. (“HGV Parent” and, together with its consolidated subsidiaries, “Hilton Grand Vacations”). Following the distribution of all of the outstanding shares of HGV Parent common stock by Hilton Worldwide Holdings Inc. (“Hilton Parent”), Hilton Grand Vacations will be a rapidly growing timeshare company that markets and sells vacation ownership intervals and manages resorts in iconic leisure and urban destinations.

As an independent, publicly traded company, we will be better positioned to allocate capital and pursue a sales strategy that will maximize earnings growth, free cash flow production and returns on invested capital, all of which will drive overall value to our stockholders. In addition, we believe our management team will be able to respond more quickly and effectively to acquisition and market opportunities as well as execute our business and growth strategies.

We expect to have HGV Parent common stock listed on the New York Stock Exchange under the symbol “HGV” in connection with the distribution of HGV Parent common stock by Hilton Parent.

We invite you to learn more about HGV Parent by reviewing the enclosed information statement. We look forward to our future as an independent, publicly traded company and to your support as a holder of HGV Parent common stock.

Sincerely,

Mark D. Wang

President and Chief Executive Officer

Hilton Grand Vacations Inc.

Table of Contents

Information contained herein is subject to completion or amendment. A Registration Statement on Form 10 relating to these securities has been filed with the Securities and Exchange Commission under the Securities Exchange Act of 1934, as amended.

SUBJECT TO COMPLETION, DATED NOVEMBER 30, 2016

INFORMATION STATEMENT

Hilton Grand Vacations Inc.

Common Stock

(par value $0.01 per share)

This information statement is being sent to you in connection with the separation of Hilton Grand Vacations Inc. (“HGV Parent” and, together with its consolidated subsidiaries, “Hilton Grand Vacations” or “HGV”) from Hilton Worldwide Holdings Inc. (“Hilton Parent” and, together with its consolidated subsidiaries, “Hilton”), following which HGV Parent will be an independent, publicly traded company. As part of the separation, Hilton will undergo an internal reorganization, after which it will complete the separation by distributing all of the outstanding shares of HGV Parent common stock on a pro rata basis to the holders of Hilton Parent common stock. We refer to this pro rata distribution as the “distribution” and we refer to the separation, including the internal reorganization and distribution, as the “spin-off.” We expect that the spin-off will be tax-free to Hilton Parent stockholders for U.S. federal income tax purposes, except to the extent of cash received in lieu of fractional shares. Each Hilton Parent stockholder will receive one share of HGV Parent common stock for every ten shares of Hilton Parent common stock held by such stockholder on December 15, 2016, the record date. The distribution of shares will be made in book-entry form only. Hilton Parent will not distribute any fractional shares of HGV Parent common stock. Instead, the distribution agent will aggregate fractional shares into whole shares, sell the whole shares in the open market at prevailing market prices and distribute the aggregate net cash proceeds from the sales pro rata to each holder who would otherwise have been entitled to receive a fractional share in the spin-off. The distribution will be effective as of 5:00 p.m., Eastern time, on January 3, 2017. Immediately after the distribution becomes effective, we will be an independent, publicly traded company.

No vote or other action of Hilton Parent stockholders is required in connection with the spin-off. We are not asking you for a proxy and you should not send us a proxy. Hilton Parent stockholders will not be required to pay any consideration for the shares of HGV Parent common stock they receive in the spin-off, and they will not be required to surrender or exchange shares of their Hilton Parent common stock or take any other action in connection with the spin-off.

All of the outstanding shares of HGV Parent common stock are currently owned, directly or indirectly, by Hilton Parent. Accordingly, there is no current trading market for HGV Parent common stock. We expect, however, that a limited trading market for HGV Parent common stock, commonly known as a “when-issued” trading market, will develop at least two trading days prior to the record date for the distribution, and we expect “regular-way” trading of HGV Parent common stock will begin the first trading day after the distribution date. We intend to list HGV Parent common stock on the New York Stock Exchange (“NYSE”) under the ticker symbol “HGV.”

In reviewing this information statement, you should carefully consider the matters described in “Risk Factors” beginning on page 28 of this information statement.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved these securities or determined if this information statement is truthful or complete. Any representation to the contrary is a criminal offense.

This information statement is not an offer to sell, or a solicitation of an offer to buy, any securities.

The date of this information statement is , 2016.

A Notice of Internet Availability of Information Statement Materials containing instructions describing how to access this Information Statement was first mailed to Hilton Parent stockholders on or about , 2016.

Table of Contents

| Page | ||||

| 1 | ||||

| 28 | ||||

| 54 | ||||

| 55 | ||||

| 67 | ||||

| 69 | ||||

| 70 | ||||

| 71 | ||||

| 72 | ||||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

79 | |||

| 104 | ||||

| 106 | ||||

| 123 | ||||

| 129 | ||||

| 159 | ||||

| 171 | ||||

| Security Ownership of Certain Beneficial Owners and Management |

177 | |||

| 180 | ||||

| 187 | ||||

| F-1 | ||||

Unless otherwise indicated or the context otherwise requires, references herein to:

| • | “Hilton Grand Vacations,” “HGV,” “we,” “our,” “us,” “the Company” and “our company” refer (1) prior to the consummation of our internal reorganization described under “The Spin-Off—Manner of Effecting the Spin-Off—Internal Reorganization,” to Hilton Resorts Corporation and its consolidated subsidiaries and (2) after such internal reorganization to Hilton Grand Vacations Inc. and its consolidated subsidiaries, which shall include HRC; |

| • | “HGV Parent” refer only to Hilton Grand Vacations Inc., exclusive of its subsidiaries; |

| • | “HRC” refer to Hilton Resorts Corporation and its consolidated subsidiaries; |

| • | “Hilton” refer to Hilton Worldwide Holdings Inc. and its consolidated subsidiaries, and references to “Hilton Parent” or “Parent” refer only to Hilton Worldwide Holdings Inc., exclusive of its subsidiaries; and |

| • | “Park Hotels & Resorts” refer to Park Hotels & Resorts Inc. and its consolidated subsidiaries, and references to “Park Parent” refer only to Park Hotels & Resorts Inc., exclusive of its subsidiaries; |

in each case giving effect to the spin-off, including the internal reorganization and distribution.

Additionally, unless otherwise indicated or the context otherwise requires, all information in this information statement gives effect to the effectiveness of our amended and restated certificate of incorporation and bylaws, the forms of which are filed as exhibits to the registration statement of which this information statement forms a part.

Table of Contents

FINANCIAL STATEMENT PRESENTATION

This information statement includes certain historical consolidated financial and other data for HRC. HRC will be considered our predecessor for financial reporting purposes. Hilton Grand Vacations Inc. is the registrant under the registration statement of which this information statement forms a part and will be the financial reporting entity following the consummation of the spin-off. The historical consolidated financial information of HRC as of December 31, 2015 and 2014 and for the years ended December 31, 2015, 2014 and 2013 has been derived from the audited consolidated financial statements of HRC included elsewhere in this information statement. The historical consolidated financial information of HRC as of December 31, 2013, 2012 and 2011 and for the years ended December 31, 2012 and 2011 has been derived from the unaudited consolidated financial statements of HRC that are not included in this information statement. The historical consolidated financial information of HRC as of September 30, 2016 and for the nine months ended September 30, 2016 and 2015 has been derived from the unaudited condensed consolidated financial statements of HRC that are included in this information statement. The unaudited consolidated financial statements of HRC have been prepared on the same basis as the audited consolidated financial statements of HRC and, in our opinion, have included all adjustments, which include only normal recurring adjustments, necessary to present fairly in all material respects our financial position and results of operations. The results for any interim period are not necessarily indicative of the results that may be expected for the full year. Our historical results are not necessarily indicative of the results expected for any future period.

This information statement also includes an unaudited pro forma consolidated balance sheet as of September 30, 2016 and unaudited pro forma consolidated statements of operations for the nine months ended September 30, 2016 and year ended December 31, 2015, which present our combined financial position and results of operations to give pro forma effect to the spin-off, including the internal reorganization and distribution and the other transactions described under “Unaudited Pro Forma Consolidated Financial Statements.” The unaudited pro forma consolidated financial statements are presented for illustrative purposes only and are not necessarily indicative of the operating results or financial position that would have occurred if the relevant transactions had been consummated on the date indicated, nor is it indicative of future operating results.

You should read our selected historical consolidated financial information and unaudited pro forma consolidated financial statements and the accompanying notes in conjunction with, and each is qualified in their entirety by reference to, the consolidated historical financial statements and related notes included elsewhere in this information statement and the financial and other information appearing elsewhere in this information statement, including information contained in “Risk Factors,” “Capitalization” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Other than the inception balance sheet, the financial statements of Hilton Grand Vacations Inc. have not been included in this information statement as it is a newly incorporated entity and has no business transactions or activities to date. In connection with the internal reorganization, Hilton Grand Vacations Inc. will become the parent of HRC.

INDUSTRY AND MARKET DATA

Certain industry and market data included in this information statement have been obtained from third-party sources that we believe to be reliable, including the American Resort Development Association (“ARDA”). Market estimates are calculated by using independent industry publications and other publicly available information in conjunction with our assumptions about our markets. While we are not aware of any misstatements regarding any industry, market or similar data presented herein and we have not independently verified such information, such data involves risks and uncertainties and are subject to change based on various factors, including those discussed under the headings “Special Note About Forward-Looking Statements” and “Risk Factors” in this information statement.

i

Table of Contents

CERTAIN DEFINED TERMS

Except where the context suggests otherwise, we define certain terms in this information statement as follows:

| • | “capital-efficient inventory” refers to our fee-for-service and just-in-time VOI inventory; |

| • | “Club” refers to Hilton Grand Vacations Club, our points-based vacation exchange program; |

| • | “contract sales” represents the total amount of VOI products under purchase agreements signed during the period where we have received a down payment of at least 10 percent of the contract price. Contract sales is not a recognized term under generally accepted accounting principles in the United States (“U.S. GAAP”), and should not be considered in isolation or as an alternative to timeshare sales, net, or any other comparable operating measure derived in accordance with U.S. GAAP. For a reconciliation of contract sales to sales of VOIs, net, which we believe is the most closely comparable U.S. GAAP financial measure, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations—Real Estate”; |

| • | “developed inventory” refers to VOI inventory sourced from projects developed by HGV; |

| • | “fee-for-service” refers to VOI inventory we sell and manage on behalf of third-party developers; |

| • | “just-in-time” refers to VOI inventory sourced in transactions that are designed to closely correlate the timing of the acquisition with our sale of that inventory to purchasers; |

| • | “owned inventory” refers to our developed and just-in-time VOI inventory; and |

| • | “VOIs” refers to vacation ownership intervals. |

ii

Table of Contents

This summary highlights information contained in this information statement and provides an overview of our company, our separation from Hilton and the distribution of HGV Parent common stock by Hilton Parent to its stockholders. For a more complete understanding of our business and the spin-off, you should read this entire information statement carefully, particularly the discussion set forth under “Risk Factors” and our audited historical consolidated financial statements, our unaudited pro forma consolidated financial statements and the respective notes to those statements included in this information statement.

Hilton Grand Vacations

Hilton Grand Vacations (“HGV”) is a rapidly growing timeshare company that markets and sells vacation ownership intervals (“VOIs”), manages resorts in top leisure and urban destinations, and operates a points-based vacation club. Our 46 resorts, representing 7,592 units, are located in iconic vacation destinations such as the Hawaiian Islands, New York City, Orlando and Las Vegas, and feature spacious, condominium-style accommodations with superior amenities and quality service. Through Hilton Grand Vacations Club (the “Club”), our approximately 265,000 members have the flexibility to exchange their VOIs for stays at any Hilton Grand Vacations resort or any property in the Hilton system of 12 industry-leading brands across more than 4,700 hotels, as well as numerous experiential vacation options, such as cruises and guided tours.

Our compelling VOI product allows customers to advance purchase a lifetime of vacations. Because our VOI owners generally purchase only the vacation time they intend to use each year, they are able to efficiently split the full cost of owning and maintaining a vacation residence with other owners. Our customers also benefit from the high-quality amenities and service at our Hilton-branded resorts. Furthermore, our points-based platform offers members tremendous flexibility, enabling us to more effectively adapt to their changing vacation needs over time. Building on the strength of that platform, we continuously seek new ways to add value to our Club membership, including enhanced product offerings, greater geographic distribution, broader exchange networks and further technological innovation, all of which drive better, more personalized vacation experiences and guest satisfaction.

As innovators in the timeshare business, we have successfully transformed from a highly capital-intensive business to a capital-efficient model by pursuing an inventory strategy focused on fee-for-service and just-in-time inventory acquisition.

1

Table of Contents

Inventory Sources as a Percentage of 2015 Contract Sales

|

• “Fee-for-service” refers to VOI inventory we sell and manage on behalf of third-party developers.

• “Just-in-time” refers to VOI inventory primarily sourced in transactions that are designed to closely correlate the timing of the acquisition with our sale of that inventory to purchasers.

• “Developed” refers to VOI inventory sourced from projects developed by HGV. |

Fee-for-service sales require virtually no capital investment on our part and provide us the flexibility to invest capital selectively. In 2015, our fee-for-service transactions represented 58% of contract sales, up from 0% in 2009. Based on our 2015 sales pace, we have access to more than six years of future inventory, with capital efficient arrangements representing approximately 85% of that supply. This visibility into our long-term supply allows us to efficiently manage inventory to meet predicted sales, reduce capital investments, minimize our exposure to the cyclicality of the real estate market and mitigate the risks of entering new markets.

The strength of our platform, coupled with what we believe is the industry’s most capital-efficient inventory sourcing model, has led to:

| • | Robust sales growth over the course of the cycle with contract sales increasing at a compound annual growth rate (“CAGR”) of 7.9% from 2007 to 2015, outperforming the industry, which experienced a decline of 2.6% over the same period; |

| • | Strong net owner growth with Club membership increasing at a 9% CAGR over the last four years to total approximately 265,000 members as of September 30, 2016; |

| • | Approximately 60% of our contract sales in the last five years coming from new owners; |

| • | Dramatically reduced capital requirements with inventory investment decreasing from an annual average of $405 million during 2007 and 2008 to $96 million during 2014 and 2015; |

| • | Significant cash flow from operations of over $1 billion from 2011 to 2015; |

| • | Strong segment Adjusted EBITDA margin of 35.5% in 2015, up 510 basis points since 2011; |

| • | Meaningfully improved return on invested capital from 2011 to 2015 by 28.8 percentage points to 41.3% in 2015; and |

| • | Total revenues of $1.5 billion, net income of $174 million and Adjusted EBITDA of $373 million for the year ended December 31, 2015, representing impressive growth of 46%, 139% and 75%, respectively since 2011. |

2

Table of Contents

After the spin-off, we expect to further capitalize on our competitive advantages as we fully activate our business, benefiting from a dedicated management team and independent capital resources. Over time, we plan to target a 50/50 mix between fee-for-service and owned sales as we believe this mix will optimize earnings growth, free cash flow production and returns on invested capital. We also will maintain an exclusive, long-term relationship with Hilton, through which our Club members will continue to have access to Hilton’s award-winning guest loyalty program and global portfolio of hotels, and we will continue to benefit from the strength and scale of Hilton’s robust commercial services platform. We expect to collaborate with Hilton and other third-parties on timeshare development opportunities in new and existing locations and across chain scale segments.

See “Summary—Summary Historical and Unaudited Pro Forma Consolidated Financial Data” for our definitions of contract sales, Adjusted EBITDA and return on invested capital and for reconciliations to measures calculated in accordance with GAAP.

The Timeshare Industry

The timeshare industry, also known as the vacation ownership industry, is one of the fastest-growing segments of the global travel and tourism sector. Annual timeshare sales in the United States increased over 800% between 1984 and 2015 to $8.6 billion. This growth was driven primarily by increased interest from established developers, owners and managers, particularly globally recognized lodging and entertainment companies, product evolution and geographic expansion. At inception, timeshare products were largely limited to a fixed or floating week, whereby a customer would purchase rights to use the same property each year, typically at the same time each year. The industry has since evolved to better meet consumer demands, offering more flexible products, such as membership in multi-property vacation networks. Additionally, product locations have expanded beyond traditional resort markets to include urban and international destinations.

The timeshare industry remains well-positioned for continued growth given favorable macroeconomic and secular trends. Economists forecast healthy consumer spending trends, while data released by the Commerce Department suggests a shift in spending patterns as consumers spend more on experiences and less on retail. Furthermore, timeshare sales in 2015 remained approximately 19% below the industry peak of $10.6 billion in 2007, suggesting continued growth potential during this stage of the current lodging cycle. We expect new product supply to attract new customers and stimulate incremental purchases from existing customers. Additionally, we expect an expanding middle class and rising growth in global tourism to bode well for the long-term health of the timeshare industry, while industry fragmentation should support continued consolidation activity.

Our Competitive Strengths

We believe the following competitive strengths position us as a leader and innovator in the timeshare industry.

| • | Exceptional Vacation Offerings. Our upscale resort collection features spacious, studio to three-bedroom condominium-style accommodations in high-demand destinations such as New York City, Orlando, the Hawaiian Islands and Las Vegas. We offer superior amenities such as full kitchens, in-unit washers and dryers, spas and kids’ clubs along with beach-front locations and the quality service that is synonymous with the Hilton name. We keep our properties modern through diligent use of reserves funded by homeowners’ associations (“HOAs”), which are deployed to update our properties on average every five years, resulting in consistent high property and service ratings. In addition, purchasers of our VOIs are enrolled in our flexible, points-based Hilton Grand Vacations Club exchange program, giving each member an annual allotment of Club points representing their owned interest and offering an attractive value proposition. Members have the ability to use their points for a |

3

Table of Contents

| variety of vacation options, including a priority reservation period at their home resort where their VOI is deeded, stays at any Hilton Grand Vacations resort, conversion to Hilton HHonors points, access to RCI’s vacation exchange network and exchanges for experiential travel alternatives. |

| • | Large and Growing Loyal Member Base. We have a loyal base of approximately 265,000 members, which has more than doubled since 2007, growing at a CAGR of nearly 9%. Yet, we continue to see tremendous growth opportunities across regions and demographics. Approximately 75% of our members were located in the United States, 20% in Japan and 5% in other international locations as of September 30, 2016. Based on information available to us, Millennials and Generation Xers made up nearly half of our first time buyers in the U.S. in 2015 and represent a growing and attractive demographic. Approximately 60% of our contract sales in the last five years were to new members, which benefits future sales given that for every dollar of initial VOI purchases by new members, we expect those members will on average purchase approximately another dollar of additional VOI product over the lifetime of their membership. We continuously strive to enhance Club value and our approximately 7,800 employees are committed to providing our members with exceptional service and cultivating member loyalty. |

| • | High-quality Customers. We consider our customer base to be among the highest quality in the industry, with our U.S. members having an average annual income level of greater than $100,000, meaningfully above the national average, a high percentage of home ownership and a frequent traveler profile. Additionally, our customers had a weighted average FICO score of 745 for new loan originations to U.S. and Canadian borrowers over the past three years, making them attractive purchasers. Our members’ creditworthiness is further demonstrated by low levels of HOA maintenance fee delinquencies, which averaged only 2.5% since 2011 compared to an annual range of 8% to 12% for the industry from 2011 to 2015. Additionally, our consumer loan portfolio has experienced low default rates of approximately 3% over the last several years. |

| • | Long-term Recurring Revenue Streams. Our platform drives highly predictable, long-term recurring revenue streams through annual Club membership dues and exchange fees and from our management agreements with HOAs. Further, unlike traditional revenue-based hotel-management fees, our management fees are generally unaffected by changes in rental rate or occupancy, making them less susceptible to market downturns. Since our inception in 1992, no management agreement at any of our developed or fee-for-service properties has been terminated or lapsed. As a result of these recurring revenue streams, our resort operations and club management segment Adjusted EBITDA represented 43% of our total Adjusted EBITDA in 2015. |

| • | Highly Effective Marketing and Sales Model. Our data-driven, affinity-based marketing approach combined with our scaled and disciplined sales process has delivered consistent sales and new member growth over the past five years. By conducting our marketing and sales activities in large markets with high levels of inbound tourism, we are able to generate year-round tour flow, making it more cost effective to reach potential new members and therefore increasing margins. The efficiency of our sales and marketing is demonstrated by our real estate margin percentage of 27.5% in 2015. In addition, our targeted direct marketing enables us to reach customers who already have an affinity with Hilton and meet our high financial standards. As a result of our marketing expertise and our relationship with Hilton, our tour flow increased at a CAGR of 10.4% between 2007 and 2015. Importantly, we have the ability to scale our model by cross-marketing and cross-selling our resorts as well as employing effective hiring practices, proprietary training and advanced technology platforms. In Japan, for example, we have successfully sold our products in Hawaii using our off-site sales model, resulting in a Japanese member base of approximately 53,500 as of September 30, 2016. Our track record of contract sales growth even during the 2008 to 2010 market downturn demonstrates the effectiveness of our distribution model and sales execution. |

4

Table of Contents

| • | Capital-efficient Business Model. We are an industry leader in capital-efficient VOI sales, which represented 78% of our contract sales in 2015. Of these sales, fee-for-service represented 58% and just-in-time represented 20%. Since our first fee-for-service project in 2010, we have entered into 10 fee-for-service deals, which have contributed approximately 160,000 VOIs to our total supply. Our capital requirements have reduced dramatically as a result, producing strong cash flow and higher returns on invested capital. As we transitioned from capital-intensive real estate development to a more capital-efficient business model, our inventory investment decreased from an annual average of $405 million during 2007 and 2008 to $96 million during 2014 and 2015. In addition, we generated cash flow from operations of over $1 billion between 2011 and 2015. Further, our relationships with some of the largest and most sophisticated real estate investors in the world, including Blackstone, Goldman Sachs, Centerbridge and Strand Capital Group, have given us access to a wide range of capital partners and the credibility to execute deals in diverse markets. As a result of our efforts, all inventory sources are projected to supply us with access to more than six years of future inventory based on our 2015 sales pace, with capital efficient arrangements representing approximately 85% of that supply. |

| • | Exclusive, Long-term Relationship with Hilton. Our relationship with Hilton connects us with a portfolio of globally recognized, market-leading hospitality brands and a superior exchange network and gives us exclusive access to a large and growing base of loyal customers and a powerful network of commercial services. With a nearly 100-year pedigree in the hospitality industry, Hilton is one of the largest and fastest growing hospitality companies in the world, with over 4,700 properties in 104 countries and territories as of September 30, 2016. Our long-term license agreement with Hilton will give us the exclusive right to market, sell and lease VOI inventory and manage resorts under the Hilton Grand Vacations brand. In 2015, 93% of Club points redeemed were used within the Hilton system by members to stay at the home resort where their VOI is deeded, exchange within our Club or convert their Club points to HHonors points for hotel stays. We believe this loyalty to the Hilton system demonstrates high member satisfaction, attracts new Club members and rental guests, and lowers our customer acquisition costs. Furthermore, our products should command a higher price point given the strength of Hilton’s brand portfolio and reputation for exceptional service and quality. We believe our relationship with Hilton and access to its formidable platform are significant competitive advantages that position us for strong future growth. |

| • | Experienced and Execution-focused Management Team. Our experienced management team is headed by Mark D. Wang, our President and Chief Executive Officer, who has led Hilton’s global timeshare operations since 2008, including our successful transition to a capital-efficient business model. Mr. Wang has 35 years of experience in the timeshare industry, and our executive officers have an average of 29 years in the timeshare and hospitality industries. With this experience, our management team has created a lean and nimble organizational structure, which allows us to respond quickly and effectively to opportunities and dynamic market conditions. By fostering a culture with a strong focus on execution and operational effectiveness, management empowers our employees to respond to our members’ and guests’ needs and provide each of them with a unique and memorable experience. |

Our Business and Growth Strategies

Our goal is to create long-term value by delivering a lifetime of exceptional vacation experiences to our loyal and growing membership base and leveraging our capital-efficient business model to drive strong returns on invested capital, free cash flow and bottom-line growth. The following are key elements of our strategy to accomplish this goal:

| • | Grow Vacation Sales. We intend to continue growing contract sales by pursuing a balanced mix of sales to new and existing members. We expect to drive growth by enhancing the value of Club |

5

Table of Contents

| membership and expanding our highly effective sales distribution model within and outside of our existing markets. As part of this strategy, we will continue to pursue opportunities in large urban and resort markets with strong inherent demand such as Washington, D.C. and Maui, Hawaii. Over time, we intend to continue expanding our marketing and sales operations in Japan and explore opportunities for in-market product offerings to those customers. We already have experienced strong growth in Japan, with an increase of 130% in contract sales from 2007 to 2015, and believe we can leverage our success to further expand in Japan and across select Asian markets. We also will pursue growth opportunities by exploring additional development opportunities within the Hilton portfolio and expanding our marketing partnerships. |

| • | Grow Our Member Base. We have experienced 23 consecutive years of net owner growth. As part of our strategy to grow our member base, we will continue to use our relationship with Hilton to target new, brand-loyal members. The Hilton HHonors loyalty program represents a cost-effective source of member growth. We also will leverage new and existing marketing relationships and continue our successful local marketing programs. Our focus on enhancing Club value also will enable us to acquire new members by expanding the demographics of our member base. Our increased marketing efforts have resulted in member demographics shifting to younger generations, with an increase in Millennial and Generation X first time buyers in the U.S. to nearly half of our first time buyers in 2015, both of which represent a large and attractive future member base. Net owner growth supports strong future sales growth, as a significant portion of our member base buys additional VOI products, which expands our predictable, recurring fee-based resort and Club management business. |

| • | Continue to Enhance Member Experiences. We are continuously seeking new ways to add value to our Club membership, including expanding our vacation options and destinations, in-market and travel-related discounts, travel exchange partners and providing access to a growing network of new Hilton-branded hotels and resorts. We also intend to expand the technology options available to members, including our new website, mobile application and digital keys, which allow members and guests to skip the front desk and access their room via smartphone. Our employees also are an important part of the vacation experiences of our members and will continue to enhance these experiences by providing our signature high-quality customer service. We believe the dedicated service of our employees, vacation experiences and Club value we offer our members foster loyalty and generate significant repeat business through our most cost-effective marketing channel. |

| • | Optimize Our Sales Mix of Capital-efficient Inventory. We believe that optimizing our mix of capital-efficient and owned inventory sales will drive premium top line growth, cash flow generation and returns on invested capital. Over time, we will target a 50/50 sales mix of owned and fee-for-service inventory. We also intend to take advantage of our robust deal pipeline fueled by existing and new relationships with third-party developers for a full range of fee-for-service and just-in-time projects. We will maintain a disciplined approach to capital allocation, while strategically pursuing acquisitions and development of owned inventory in key markets. |

| • | Pursue Opportunistic Business Ventures. Despite recent consolidation, the timeshare industry remains fragmented. We will continue to evaluate market opportunities and consider strategic acquisitions that meet our high product and service standards. This could include corporate and property acquisitions to expand our inventory options and distribution capabilities. We also intend to use our relationship with Hilton and third-party developers as well as our innovative platform and industry experience to create new products and additional efficiencies. For example, we intend to continue collaborating with Hilton on timeshare development opportunities at new and existing hotel properties and explore growth opportunities along the Hilton brand spectrum. |

6

Table of Contents

Capital Allocation and Financial Policy

We plan to: pursue a disciplined capital allocation policy; invest capital selectively to source high-quality inventory in key, strategic markets; and finance the development and purchase of new VOI inventory through modest leverage and securitization of our timeshare financing receivables. We expect to target an investment grade credit rating and return capital to stockholders through dividends and stock buybacks over time.

Our History

Our history dates to 1992 with Hilton’s joint venture with Grand Vacations. In 1996, Hilton Grand Vacations became a wholly owned subsidiary of Hilton Parent. During the ensuing years we expanded our operations and established a track record of innovation in our industry. Unlike the broader timeshare industry, which experienced a contraction in 2008 and 2009 as a result of the overall economic recession, we were able to grow contract sales during the industry downturn and have continued to deliver contract sales growth in each period since, driven by our continued focus on marketing and sales activities, our strong development margins, large-market distribution model, synergies with Hilton, commitment to new owner transactions and lean organizational structure. Key events in our history are illustrated in the following timeline:

7

Table of Contents

HNA Group Strategic Investment and Secondary Offering

On October 24, 2016, Hilton Parent, The Blackstone Group L.P. and its affiliates (“Blackstone”) and HNA Tourism Group Co., Ltd. (“HNA”) announced that affiliates of Blackstone agreed to sell to HNA 247,500,000 shares of common stock of Hilton Parent, representing approximately 25% of the outstanding shares of common stock of Hilton Parent, pursuant to a stock purchase agreement between HNA and Blackstone (the “Sale”). The Sale is expected to close, subject to customary closing conditions (including receipt of regulatory approvals in the United States, China and certain other countries), in the first quarter of 2017. If the Sale closes after the spin-off record date, the Sale also will include the shares of common stock of HGV Parent and Park Parent received by Blackstone with respect to the shares of common stock of Hilton Parent being sold to HNA.

In connection with the Sale, HGV Parent entered into a stockholders agreement and a registration rights agreement with HNA, which will become effective upon the later to occur of (i) the closing of the Sale and (ii) the consummation of the spin-off. HGV Parent also entered into a registration rights agreement with Blackstone (which will become effective upon the consummation of the spin-off) and HGV Parent further intends to enter into a stockholders agreement with Blackstone at the consummation of the spin-off which will be substantially the same as Blackstone’s stockholders agreement with Hilton Parent. See “Certain Relationships and Related Party Transactions—Stockholders Agreements” and “Certain Relationships and Related Party Transactions—Registration Rights Agreements” for more detailed descriptions of these agreements.

On November 15, 2016, certain selling stockholders affiliated with Blackstone completed a secondary offering of 55,000,000 shares of common stock of Hilton Parent (the “Secondary Offering”). In this information statement, information with respect to the anticipated beneficial ownership of our common stock by Blackstone reflects the completion of the Secondary Offering.

Summary Risk Factors

There are a number of risks related to our business and the spin-off and related transactions, including:

| • | we are subject to the business, financial and operating risks inherent to the timeshare industry, any of which could reduce our revenues and limit opportunities for growth; |

| • | macroeconomic and other factors beyond our control can adversely affect and reduce demand for our products and services; |

| • | we do not own the Hilton brands and our business will be materially harmed if we breach our license agreement with Hilton or it is terminated; |

| • | our business depends on the quality and reputation of the Hilton brands and affiliation with the Hilton HHonors loyalty program; |

| • | our dependence on development activities exposes us to project cost and completion risks; |

| • | a decline in developed or acquired VOI inventory or our failure to enter into and maintain fee-for-service agreements may have an adverse effect on our business or results of operations; |

| • | we operate in a highly competitive industry; |

| • | we manage a concentration of properties in particular geographic areas, which exposes our business to the effects of regional events and occurrences; |

| • | if maintenance fees at our resorts are required to be increased, our product could become less attractive and our business could be harmed; |

8

Table of Contents

| • | the expiration, termination or renegotiation of our management agreements could adversely affect our cash flows, revenues and profits; |

| • | our indebtedness and other contractual obligations could adversely affect our financial condition, our ability to raise additional capital to fund our operations, our ability to operate our business, our ability to react to changes in the economy or our industry and our ability to pay our debts and could divert our cash flow from operations for debt payments; |

| • | we may be responsible for U.S. federal income tax liabilities that relate to the distribution; |

| • | we do not have a recent operating history as an independent company and our historical financial information does not predict our future results; |

| • | we may be unable to achieve some or all of the benefits that we expect to achieve from the spin-off; |

| • | we may have been able to receive better terms from unaffiliated third parties than the terms we receive in our agreements related to the spin-off; and |

| • | upon consummation of the spin-off, approximately 40% of the voting power in HGV Parent will be controlled by Blackstone and upon consummation of the Sale, 25% of the voting power in HGV Parent will be controlled by HNA and approximately 15% will be controlled by Blackstone, and their respective interests may conflict with ours or yours in the future. |

These and other risks related to our business and the spin-off are discussed in greater detail under the heading “Risk Factors” in this information statement. You should read and consider all of these risks carefully.

Hilton Grand Vacations Inc. was incorporated in the State of Delaware on May 2, 2016. Our headquarters are located at 6355 MetroWest Boulevard, Suite 180, Orlando, Florida 32835. Our telephone number is (407) 722-3100.

9

Table of Contents

The Spin-Off

Overview

On February 26, 2016, Hilton Parent announced its intention to implement the spin-off of HGV and Park Hotels & Resorts from Hilton, following which HGV Parent and Park Parent will be independent, publicly traded companies.

Before our spin-off from Hilton, we will enter into a Distribution Agreement and several other agreements with Hilton Parent and Park Parent related to the spin-off. These agreements will govern the relationship among us, Hilton and Park Hotels & Resorts after completion of the spin-off and provide for the allocation among us, Hilton and Park Hotels & Resorts of various assets, liabilities, rights and obligations (including employee benefits, intellectual property, insurance and tax-related assets and liabilities). These agreements also will include arrangements with respect to transitional services to be provided by Hilton to HGV and Park Hotels & Resorts. See “Certain Relationships and Related Party Transactions—Agreements with Hilton Parent and Park Parent Related to the Spin-Off.”

The distribution of HGV Parent common stock as described in this information statement is subject to the satisfaction or waiver of certain conditions. In addition, Hilton has the right not to complete the spin-off if, at any time prior to the distribution, the board of directors of Hilton Parent determines, in its sole discretion, that the spin-off is not then in the best interests of Hilton or its stockholders or other constituents, that a sale or other alternative is in the best interests of Hilton or its stockholders or other constituents, or that market conditions or other circumstances are such that it is not advisable at that time to separate HGV from Hilton. See “The Spin-Off—Conditions to the Spin-Off.”

10

Table of Contents

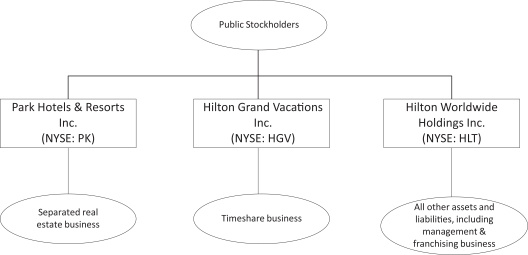

Organizational Structure

The simplified diagrams below (which omit certain wholly owned intermediate holding companies) depict the organizational structure of Hilton, Park Hotels & Resorts and Hilton Grand Vacations before and after giving effect to the spin-offs.

Current Hilton Organizational Structure

Organizational Structure Following the Spin-Offs

11

Table of Contents

Financing Transactions

Subject to market conditions, we expect to complete one or more financing transactions on or prior to the completion of the spin-off. As a result of these financing transactions, upon consummation of the spin-off we expect to have total recourse indebtedness of approximately $500 million, excluding $450 million expected to be outstanding under our non-recourse financing receivables credit facility (the “Timeshare Facility”) and between $250 million and $300 million of our non-recourse notes backed by timeshare financing receivables (the “Securitized Debt”) expected to be outstanding. Included in our expected outstanding non-recourse Timeshare Facility balance is an intended borrowing of an additional $300 million, which proceeds will be used to distribute cash to Hilton Parent. After giving effect to the foregoing financing transactions, upon consummation of the spin-off, we expect to have $1.22 billion of total recourse and non-recourse indebtedness outstanding. There can be no assurances that any such financing transactions will be completed in the timeframe or size indicated or at all. See “The Spin-Off—Financing Transactions” and “Description of Certain Indebtedness.”

Questions and Answers About the Spin-Off

The following provides only a summary of the terms of the spin-off. For a more detailed description of the matters described below, see “The Spin-Off.”

| Q: | What is the spin-off? |

| A: | The spin-off is the series of transactions by which HGV will separate from Hilton. To complete the spin-off, Hilton Parent will distribute to its stockholders all of the outstanding shares of HGV Parent common stock. We refer to this as the distribution. Following the spin-off, HGV will be a separate company from Hilton, and Hilton will not retain any ownership interest in HGV. |

| Q: | What will I receive in the spin-off? |

| A: | As a holder of Hilton Parent common stock, you will retain your Hilton Parent shares and will receive one share of HGV Parent common stock for every ten shares of Hilton Parent common stock you own as of the record date. You also will receive one share of common stock of Park Parent for every five shares of Hilton Parent common stock you own as of the record date in connection with the spin-off of that company. The number of shares of Hilton Parent common stock you own and your proportionate interest in Hilton Parent will not change as a result of the spin-off. See “The Spin-Off.” |

| Q: | What is HGV Parent? |

| A: | HGV Parent is a rapidly growing timeshare company that markets and sells vacation ownership intervals and manages resorts in top destinations. HGV Parent is currently a subsidiary of Hilton Parent whose shares will be distributed to Hilton Parent stockholders when the spin-off is completed. After the spin-off is completed, HGV Parent will be an independent, publicly traded company. |

| Q: | Why is the separation of HGV Parent structured as a spin-off? |

| A: | Hilton Parent intends to implement the spin-off of (i) its timeshare business, which we refer to as Hilton’s “Timeshare business,” and (ii) a portfolio of 69 owned and leased hotel and resort properties, with nearly 36,000 rooms, comprising a substantial portion of Hilton’s ownership business, and certain related assets and operations, which we refer to collectively as the “Separated Real Estate business.” Hilton determined, and continues to believe, that a spin-off is the most efficient way to accomplish a separation of the Timeshare business from Hilton for various reasons, including: (i) a spin-off would be a tax-free distribution of HGV Parent common stock to Hilton Parent stockholders; (ii) a spin-off offers a higher degree of |

12

Table of Contents

| certainty of completion in a timely manner, lessening disruption to current business operations; and (iii) a spin-off provides greater assurance that decisions regarding HGV’s capital structure support future financial stability. After consideration of strategic alternatives, Hilton believes that a tax-free spin-off will enhance the long-term value of both Hilton and HGV. See “The Spin-Off—Reasons for the Spin-Off.” |

| Q: | Can Hilton decide to cancel the distribution of the HGV Parent common stock even if all the conditions have been met? |

| A: | Yes. The distribution of HGV Parent common stock is subject to the satisfaction or waiver of certain conditions. See “The Spin-Off—Conditions to the Spin-Off.” Hilton has the right not to complete the spin-off if, at any time prior to the distribution, the board of directors of Hilton Parent determines, in its sole discretion, that the spin-off is not then in the best interests of Hilton or its stockholders or other constituents, that a sale or other alternative is in the best interests of Hilton or its stockholders or other constituents, or that market conditions or other circumstances are such that it is not advisable at that time to separate HGV from Hilton. |

| Q: | What is being distributed in the spin-off? |

| A: | Approximately 99 million shares of HGV Parent common stock will be distributed in the spin-off, based on the number of shares of Hilton Parent common stock expected to be outstanding as of December 15, 2016 the record date, and assuming a distribution ratio of one-to-ten. The actual number of shares of HGV Parent common stock to be distributed will be calculated on the record date. The shares of HGV Parent common stock to be distributed by Hilton Parent will constitute all of the issued and outstanding shares of HGV Parent common stock immediately prior to the distribution. See “Description of Capital Stock—Common Stock.” |

| Q: | When is the record date for the distribution? |

| A: | The record date is December 15, 2016. |

| Q: | When will the distribution occur? |

| A: | The distribution date of the spin-off is January 3, 2017. We expect that it will take the distribution agent, acting on behalf of Hilton Parent, up to two weeks after the distribution date to fully distribute the shares of HGV Parent common stock to Hilton Parent stockholders. |

| Q: | What do I have to do to participate in the spin-off? |

| A: | Nothing. You are not required to take any action, although we urge you to read this entire document carefully. No stockholder approval of the distribution is required or sought. You are not being asked for a proxy. No action is required on your part to receive your shares of HGV Parent common stock. You will neither be required to pay anything for the new shares nor be required to surrender any shares of Hilton Parent common stock to participate in the spin-off. |

| Q: | How will stock options, time-vesting restricted stock units, and performance-vesting restricted stock units and restricted shares held by Hilton Grand Vacation employees be affected as a result of the spin-off? |

| A: | At the time of the distribution, subject to approval of the board of directors of Hilton Parent, in general, it is expected that all outstanding Hilton Parent equity-based compensation awards, whether vested or unvested, and which are held by any individual who is employed by us as of the separation will convert into awards |

13

Table of Contents

| that will settle in shares of Hilton Grand Vacations common stock following the spin-off, and performance-vesting awards will generally be converted into time-vesting awards based upon a performance level to be determined by the Hilton Parent Compensation Committee prior to the separation. For more information on the treatment of equity-based compensation awards in the spin-off, see “The Spin-Off—Treatment of Outstanding Equity Awards.” |

| Q: | How will fractional shares be treated in the spin-off? |

| A: | Fractional shares of HGV Parent common stock will not be distributed. Fractional shares of HGV Parent common stock to which Hilton Parent stockholders of record would otherwise be entitled will be aggregated and sold in the public market by the distribution agent at prevailing market prices. The distribution agent, in its sole discretion, will determine when, how and through which broker-dealers, provided that such broker-dealers are not affiliates of Hilton Parent or HGV Parent, and at what prices to sell these shares. The aggregate net cash proceeds of the sales will be distributed ratably to those stockholders who would otherwise have received fractional shares of HGV Parent common stock. See “The Spin-Off—Treatment of Fractional Shares” for a more detailed explanation. Receipt by a stockholder of proceeds from these sales in lieu of a fractional share generally will result in a taxable gain or loss to those stockholders for U.S. federal income tax purposes. Each stockholder entitled to receive cash proceeds from these shares should consult his, her or its own tax advisor as to such stockholder’s particular circumstances. We describe the material U.S. federal income tax consequences of the distribution in more detail under “The Spin-Off—Material U.S. Federal Income Tax Consequences of the Spin-Off.” |

| Q: | Why has Hilton determined to undertake the spin-off? |

| A: | Hilton Parent’s board of directors has determined that the spin-off is in the best interests of Hilton Parent, its stockholders and other constituents because the spin-off will provide the following key benefits: |

| • | Direct and Differentiated Access to Capital Resources to Pursue Tailored Growth Strategies. Following the spin-off, HGV will be better positioned to target a 50/50 mix between fee-for-service and owned VOI inventory sales by opportunistically allocating capital toward owned inventory. We believe that optimizing our sales mix will enable us to maximize earnings growth, free cash flow production and returns on invested capital. As a company focused solely on the timeshare business with direct access to capital and independent financial resources, we believe we will be able to execute our business and growth strategies to drive overall value to our stockholders. Similarly, as a company focused on hotel management and franchising, Hilton Parent expects to benefit from alignment with a dedicated investor base, resulting in enhanced and more efficient access to capital to pursue a growth strategy best suited for its core, capital-light fee business. |

| • | Enhanced Investor Choices by Offering Investment Opportunities in Separate Entities. Hilton’s management and franchising and timeshare businesses exhibit different financial and operating characteristics and appeal to different types of investors with different investment goals and risk profiles. Finding investors who want to invest in the businesses together is more challenging than finding investors for each business individually. After the spin-off, investors should be better able to evaluate the financial performance of each company, as well as its strategy within the context of its particular market, thereby enhancing the likelihood that each company will achieve an appropriate market valuation. |

| • | Dedicated Management Team with Enhanced Strategic Focus. Following the spin-off, Hilton’s management and franchising and timeshare businesses will no longer compete for the attention and resources of a single management team and will benefit from dedicated management teams focused on designing and implementing tailored strategies to achieve the distinct goals and opportunities of each business. Moreover, free from constraints that arise from being part of a larger hospitality company, |

14

Table of Contents

| HGV’s dedicated management team will be able to respond more quickly and effectively to acquisition and market opportunities as well as execute its business and growth strategies. |

| • | Improved Management Incentive Tools. We expect to use equity-based and other incentive awards to compensate current and future employees. In multi-business companies such as Hilton, it is difficult to structure incentives that reward employees in a manner directly related to the performance of their respective business units. By granting awards linked to the performance of a pure-play business, the compensation arrangements of each company should provide enhanced incentives for employee performance and improve the ability of each company to attract, retain and motivate qualified personnel. |

| Q: | What are the U.S. federal income tax consequences of the spin-off? |

| A: | Hilton Parent has received a ruling (“IRS Ruling”) from the Internal Revenue Service (“IRS”) regarding certain U.S. federal income tax aspects of the spin-off. The spin-off is conditioned on the IRS Ruling remaining in effect as of the distribution date. In addition, the spin-off is conditioned on the receipt of an opinion of Simpson Thacher & Bartlett LLP, Hilton Parent’s tax counsel (“Spin-off Tax Counsel”), confirming tax-free treatment under Section 355 of the Code of the distributions. Although Hilton Parent has no current intention to do so, such conditions are solely for the benefit of Hilton Parent and its stockholders and may be waived by Hilton Parent in its sole discretion. The material U.S. federal income tax consequences of the distribution are described in more detail under “The Spin-Off—Material U.S. Federal Income Tax Consequences of the Spin-Off.” |

| Q: | Will the HGV Parent common stock be listed on a stock exchange? |

| A: | Yes. Although there is not currently a public market for HGV Parent common stock, before completion of the spin-off, HGV Parent will apply to list its common stock on the NYSE under the symbol “HGV.” It is anticipated that trading of HGV Parent common stock will commence on a “when-issued” basis at least two trading days prior to the record date. “When-issued” trading refers to a sale or purchase made conditionally because the security has been authorized but not yet issued. “When-issued” trades generally settle within four trading days after the distribution date. On the first trading day following the distribution date, any “when-issued” trading with respect to HGV Parent common stock will end, and “regular-way” trading will begin. “Regular-way” trading refers to trading after a security has been issued and typically involves a transaction that settles on the third full trading day following the date of the transaction. See “Trading Market.” |

| Q: | Will my shares of Hilton Parent common stock continue to trade? |

| A: | Yes. Hilton Parent common stock will continue to be listed and trade on the NYSE under the symbol “HLT.” |

| Q: | If I sell, on or before the distribution date, shares of Hilton Parent common stock that I held on the record date, am I still entitled to receive shares of HGV Parent common stock distributable with respect to the shares of Hilton Parent common stock I sold? |

| A: | Beginning on or shortly before the record date and continuing through the distribution date for the spin-off, Hilton Parent common stock will begin to trade in two markets on the New York Stock Exchange: a “regular-way” market and an “ex-distribution” market. If you hold shares of Hilton Parent common stock as of the record date for the distribution and choose to sell those shares in the “regular-way” market after the record date for the distribution and on or before the distribution date, you also will be selling the right to receive the shares of HGV Parent common stock in connection with the spin-off. However, if you hold |

15

Table of Contents

| shares of Hilton Parent common stock as of the record date for the distribution and choose to sell those shares in the “ex-distribution” market after the record date for the distribution and on or before the distribution date, you will still receive the shares of HGV Parent common stock in the spin-off. |

| Q: | Will the spin-off affect the trading price of my Hilton Parent stock? |

| A: | Yes. The trading price of shares of Hilton Parent common stock immediately following the distribution is expected to be lower than immediately prior to the distribution because its trading price will no longer reflect the value of the Timeshare business and Separated Real Estate business. However, we cannot predict the price at which the Hilton Parent shares will trade following the spin-off. |

| Q: | What financing transactions will be undertaken in connection with the spin-off? |

| A: | Subject to market conditions, we expect to complete one or more financing transactions on or prior to the completion of the spin-off. As a result of these financing transactions, upon consummation of the spin-off we expect to have total recourse indebtedness of approximately $500 million, excluding $450 million expected to be outstanding under the non-recourse Timeshare Facility and between $250 million and $300 million of non-recourse Securitized Debt expected to be outstanding. Included in our expected outstanding non-recourse Timeshare Facility balance is an intended borrowing of an additional $300 million, which proceeds will be used to distribute cash to Hilton Parent. After giving effect to the foregoing financing transactions, upon consummation of the spin-off, we expect to have $1.22 billion of total recourse and non-recourse indebtedness outstanding. We have not yet identified the specific sources of funds and there can be no assurances that any such financing transactions will be completed in the timeframe or size indicated or at all. The financing transactions will be described in greater detail in a subsequent amendment to the registration statement of which this information statement forms a part. See “The Spin-Off—Financing Transactions” and “Description of Certain Indebtedness.” |

| Q: | What is the estimated cash amount that Hilton Grand Vacations will contribute to Hilton Parent? |

| A: | Hilton Grand Vacations will contribute up to approximately $500 million in cash to Hilton Parent from proceeds of financing transactions expected to be completed on or prior to completion of the spin-off. |

| Q: | Who will comprise the senior management team and board of directors of HGV Parent after the spin-off? |

| A: | The executive officers following the spin-off will include Mark D. Wang, President and Chief Executive Officer, who will also serve as a director; James E. Mikolaichik, Chief Financial Officer; Michael D. Brown, Chief Operating Officer; Charles R. Corbin, Jr., General Counsel; and Stan R. Soroka, Chief Customer Officer. See “Management” for information on our executive officers and board of directors. |

| Q: | What will the relationship be between Hilton and HGV after the spin-off? |

| A: | Following the spin-off, HGV Parent will be an independent, publicly traded company, and Hilton Parent will have no continuing stock ownership interest in HGV Parent. HGV Parent will have entered into a Distribution Agreement with Hilton Parent and Park Parent and will enter into several other agreements for the purpose of allocating among Hilton Parent, HGV Parent and Park Parent various assets, liabilities, rights and obligations (including employee benefits, intellectual property, insurance and tax-related assets and liabilities). These agreements also will govern HGV’s relationship with Hilton and Park Hotels & Resorts |

16

Table of Contents

| following the spin-off and will provide arrangements for employee matters, tax matters, intellectual property matters, insurance matters and other specified liabilities, rights and obligations attributable to periods before and, in some cases, after the spin-off. These agreements also will include arrangements with respect to transitional services to be provided by Hilton to HGV and Park Hotels & Resorts. The Distribution Agreement will provide, in general, that HGV will indemnify Hilton against any and all liabilities arising out of HGV’s business as constituted in connection with the spin-off and any other liabilities and obligations assumed by HGV, and that Hilton will indemnify HGV against any and all liabilities arising out of the businesses of Hilton as constituted in connection with the spin-off and any other liabilities and obligations assumed by Hilton. In addition, HGV Parent and Hilton will enter into a long-term license agreement with Hilton will give HGV the exclusive right to market, sell and rent VOI inventory and manage resorts under the Hilton Grand Vacations brand. |

| Q: | What will HGV Parent’s dividend policy be after the spin-off? |

| A: | Although we expect to return capital to stockholders through dividends or otherwise in the future, we have no current plans to pay dividends on our common stock. Any decision to declare and pay dividends in the future will be made at the sole discretion of our board of directors and will depend on, among other things, our results of operations, cash requirements, financial condition, contractual restrictions and other factors that our board of directors may deem relevant. See “Dividend Policy.” |

| Q: | What are the anti-takeover effects of the spin-off? |

| A: | Some provisions of the amended and restated certificate of incorporation and bylaws of HGV Parent, Delaware law and possibly the agreements governing HGV Parent’s new debt, as each will be in effect immediately following the spin-off, may have the effect of making more difficult an acquisition of control of HGV in a transaction not approved by HGV’s board of directors. See “Description of Capital Stock—Anti-Takeover Effects of Our Certificate of Incorporation and Bylaws and Certain Provisions of Delaware Law.” In addition, under the Tax Matters Agreement, HGV Parent will agree, subject to certain terms, conditions and exceptions, not to enter into any transaction for a period of two years following the distribution involving an acquisition (including issuance) of HGV Parent common stock or certain other transactions that could cause the distribution to be taxable to Hilton Parent. The parties also will agree to indemnify each other for any tax resulting from any transaction to the extent a party’s actions caused such tax liability, whether or not the indemnified party consented to such transaction or the indemnifying party was otherwise permitted to enter into such transaction under the Tax Matters Agreement, and for all or a portion of any tax liabilities resulting from the distribution under certain other circumstances. Generally, Hilton Parent will recognize a taxable gain on the distribution if there are (or have been) one or more acquisitions (including issuances) of HGV Parent capital stock representing 50 percent or more of HGV Parent’s stock, measured by vote or value, and the acquisitions are deemed to be part of a plan or series of related transactions that include the distribution. Any such acquisition of HGV Parent common stock within two years before or after the distribution (with exceptions, including public trading by less-than-5% stockholders and certain compensatory stock issuances) generally will be presumed to be part of such a plan unless that presumption is rebutted. Moreover, under the Stockholders Agreement, HGV Parent will agree to restrict certain issuances and repurchases of its stock to manage the aggregate shift in ownership of HGV Parent’s stock as a result of such acquisitions. As a result, HGV’s obligations may discourage, delay or prevent a change of control of HGV. |

| Q: | What are the risks associated with the spin-off? |

| A: | There are a number of risks associated with the spin-off and ownership of HGV Parent common stock. These risks are discussed under “Risk Factors.” |

17

Table of Contents

| Q: | Where can I get more information? |

| A. | If you have any questions relating to the mechanics of the distribution, you should contact the distribution agent at: |

Wells Fargo Shareowner Services

P.O. Box 64874

St. Paul, MN 55164-0874

Toll Free Number: 800-468-9716

Before completion of the spin-off, if you have any questions relating to the spin-off, you should contact Hilton Parent at:

Hilton Worldwide Holdings Inc.

Investor Relations

Phone: 703-883-5476

Email: ir@hilton.com

www.hiltonworldwide.com

After completion of the spin-off, if you have any questions relating to HGV, you should contact HGV Parent at:

Hilton Grand Vacations Inc.

Investor Relations

Phone: 407-722-3327

Email: rlafleur@hgvc.com

www.hiltongrandvacations.com

18

Table of Contents

Summary of the Spin-Off

| Distributing Company |

Hilton Worldwide Holdings Inc., a Delaware corporation. After the distribution, Hilton Parent will not own any shares of HGV Parent common stock. |

| Distributed Company |

Hilton Grand Vacations Inc., a Delaware corporation and a wholly owned subsidiary of Hilton Parent. After the spin-off, HGV Parent will be an independent, publicly traded company. |

| Distributed Securities |

All of the outstanding shares of HGV Parent common stock owned by Hilton Parent, which will be 100 percent of the HGV Parent common stock issued and outstanding immediately prior to the distribution. |

| Record Date |

The record date for the distribution is December 15, 2016. |

| Distribution Date |

The distribution date is January 3, 2017. |

| Internal Reorganization |

As part of the spin-off, Hilton will undergo an internal reorganization, which we refer to as the “internal reorganization,” pursuant to which, among other things and subject to limited exceptions: |

| • | all of the assets and liabilities (including whether accrued, contingent or otherwise, and subject to certain exceptions) associated with the Timeshare business will be retained by or transferred to us or our subsidiaries; |

| • | all of the assets and liabilities (including whether accrued, contingent or otherwise, and subject to certain exceptions) associated with the Separated Real Estate business will be retained by or transferred to Park Parent or its subsidiaries; and |

| • | all other assets and liabilities (including whether accrued, contingent or otherwise, and subject to certain exceptions) of Hilton will be retained by or transferred to Hilton Parent or its subsidiaries (other than us, Park Parent or our respective subsidiaries). |

| In particular, following the internal reorganization, Hilton Grand Vacations will own HRC, the legal entity that currently owns and operates the entirety of Hilton Parent’s Timeshare business, which has historically operated as a distinct operating segment. See the financial statements of HRC included in this information statement for additional details on the historical assets, liabilities and obligations of the Timeshare business. |

| After completion of the spin-off: |

| • | we will be an independent, publicly traded company (NYSE : HGV), and will own and operate Hilton’s timeshare business; |

19

Table of Contents

| • | Park Parent will be an independent, self-administered, publicly traded company (NYSE : PK), and will hold a portfolio of Hilton’s real estate assets and certain other assets and operations as described herein; and |

| • | Hilton will continue to be an independent, publicly traded company (NYSE: HLT) and continue to own and operate its management and franchising business and will continue to hold certain real estate assets not transferred to Park Hotels & Resorts as part of the spin-off. |

| See “The Spin-Off—Manner of Effecting the Spin-Off—Internal Reorganization.” |

| Distribution Ratio |

Each holder of Hilton Parent common stock will receive one share of HGV Parent common stock for every ten shares of Hilton Parent common stock held at 5:00 p.m., Eastern time, on December 15, 2016. |

| Immediately following the spin-off, HGV Parent expects to have 27 record holders of shares of common stock and approximately 99 million shares of common stock outstanding, based on the number of stockholders and outstanding shares of Hilton Parent common stock on November 8, 2016 and the distribution ratio. The figures exclude shares of Hilton Parent common stock held directly or indirectly by Hilton Parent, if any. The actual number of shares to be distributed will be determined on the record date and will reflect any repurchases of shares of Hilton Parent common stock and issuances of shares of Hilton Parent common stock in respect of awards under Hilton Parent equity-based incentive plans between the date the Hilton Parent board of directors declares the dividend for the distribution and the record date for the distribution. |

| The Distribution |