1

1

2

2

3

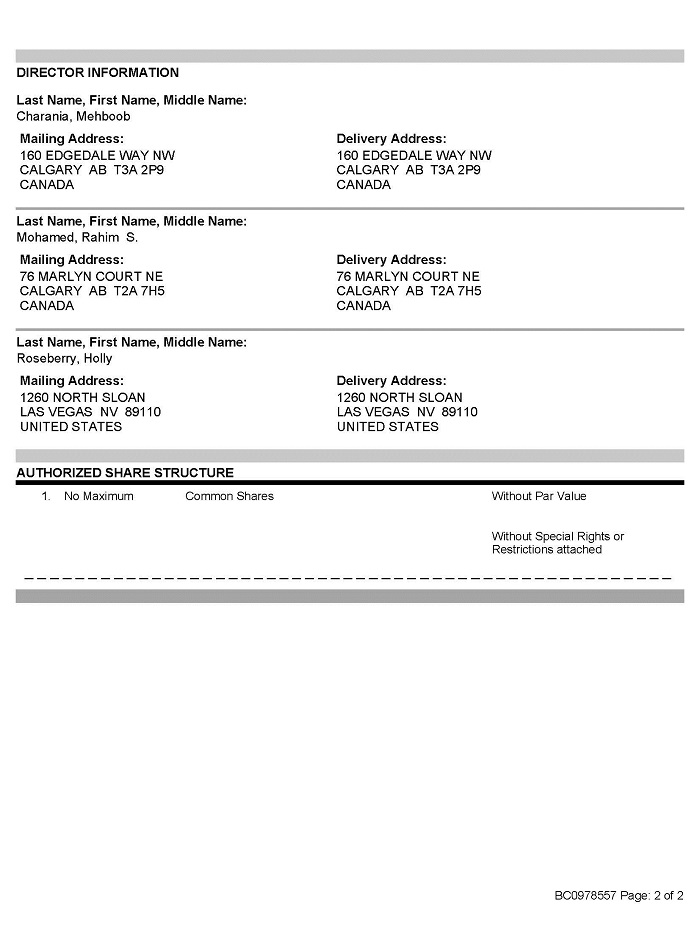

Incorporation Number: BC0978557

ARTICLES OF

ChitrChatr Communications Inc.

(The “Company”)

TABLE OF CONTENTS

| 1. Interpretation |

| 2. Shares and Share Certificates |

| 3. Issue of Shares |

| 4. Share Registers |

| 5. Share Transfers |

| 6. Transmission of Shares |

| 7. Purchase, Redeem or Otherwise Acquire Shares |

| 8. Borrowing Powers |

| 9. Alterations |

| 10. Meetings of Shareholders |

| 11. Proceedings at Meetings of Shareholders |

| 12. Votes of Shareholders |

| 13. Directors |

| 14. Election and Removal of Directors |

| 15. Alternate Directors |

| 16. Power and Duties of Directors |

| 17. Disclosure of Interest of Directors and Officers |

| 18. Proceedings of Directors |

| 19. Committees |

| 20. Officers |

| 21. Indemnification |

| 22. Dividends |

| 23. Accounting, Records and Reports |

| 24. Notices |

| 25. Seal |

| 26. Prohibitions |

| 27. Change of Registered and Records Office |

| 4 |

| 1. | INTERPRETATION |

| 1.1 | Definitions |

In these Articles, unless the context otherwise requires:

| (1) | "board of directors", "directors" and "board" mean the directors or sole director of the Company for the time being; |

| (2) | "Business Corporations Act" means the Business Corporations Act (British Columbia) from time to time in force and all amendments thereto and includes all regulations and amendments thereto made pursuant to that Act; |

| (3) | “Interpretation Act” means the Interpretation Act (British Columbia) from time to time in force and all amendments thereto and includes all regulations and amendments thereto made pursuant to that Act; |

| (4) | "legal personal representative" means the personal or other legal representative of the shareholder; |

| (5) | “public company” means a company that: |

| (a) | is a reporting issuer; |

| (b) | is a reporting issuer equivalent; |

| (c) | has registered its securities under the Securities Exchange Act of 1934 of the United States of America; |

| (d) | has any of its securities, within the meaning of the Securities Act, traded on or through the facilities of a securities exchange; or |

| (e) | has any of its securities, within the meaning of the Securities Act, reported through the facilities of a quotation and trade reporting system |

| (6) | “reporting issuer” has the same meaning as in the Securities Act; |

| (7) | “reporting issuer equivalent” means a corporation that, under the laws of any Canadian jurisdiction other than British Columbia, is a Reporting Issuer or an equivalent of a Reporting Issuer; |

| (8) | "registered address" of a shareholder means the shareholder's address as recorded in the central securities register of the Company; |

| (9) | "seal" means the seal of the Company, if any; |

| (10) | “Securities Act” means the Securities Act (British Columbia); |

| (11) | “Securities Exchange Act of 1934” means the United States Securities Exchange Act |

of 1934, as amended.

| 5 |

Business Corporations Act and Interpretation Act Definitions Applicable

The definitions in the Business Corporations Act and the definitions and rules of construction in the Interpretation Act, with the necessary changes, so far as applicable, and unless the context requires otherwise, apply to these Articles as if they were an enactment. If there is a conflict between a definition in the Business Corporations Act and a definition or rule in the Interpretation Act relating to a term used in these Articles, the definition in the Business Corporations Act will prevail in relation to the use of the term in these Articles. If there is a conflict between these Articles and the Business Corporations Act, the Business Corporations Act will prevail.

| 2. | SHARES AND SHARE CERTIFICATES |

| 2.1 | Authorized Share Structure |

The authorized share structure of the Company consists of shares of the class or classes and series, if any, described in the Notice of Articles of the Company.

| 2.2 | Form of Share Certificate |

Each share certificate issued by the Company must comply with, and be signed as required by the Business Corporations Act.

| 2.3 | Shareholder Entitled to Certificate or Acknowledgment |

Each shareholder is entitled, without charge, to (a) one share certificate representing the shares of each class or series of shares registered in the shareholder's name or (b) a non- transferable written acknowledgment of the shareholder's right to obtain such a share certificate, provided that in respect of a share held jointly by several persons, the Company is not bound to issue more than one share certificate and delivery of a share certificate for a share to one of several joint shareholders or to one of the shareholders' duly authorized agents will be sufficient delivery to all.

| 2.4 | Delivery by Mail |

Any share certificate or non-transferable written acknowledgment of a shareholder's right to obtain a share certificate may be sent to the shareholder by mail at the shareholder's registered address and neither the Company nor any director, officer or agent of the Company is liable for any loss to the shareholder because the share certificate or acknowledgement is lost in the mail or stolen.

| 2.5 | Replacement of Worn Out or Defaced Certificate or Acknowledgement |

If the directors are satisfied that a share certificate or a non-transferable written acknowledgment of the shareholder's right to obtain a share certificate is worn out or defaced, they must, on production to them of the share certificate or acknowledgment, as the case may be, and on such other terms, if any, as they think fit:

| (1) | order the share certificate or acknowledgement, as the case may be, to be cancelled; and |

| 6 |

| (2) | issue a replacement share certificate or acknowledgement, as the case may be. |

2.6 Replacement of Lost, Stolen or Destroyed Certificate or Acknowledgement

If a share certificate or a non-transferable written acknowledgement of a shareholder’s right to obtain a share certificate is lost, stolen or destroyed, a replacement share certificate or acknowledgement, as the case may be, must be issued to the person entitled to that share certificate or acknowledgement, as the case may be, if the directors receive:

| (1) | proof satisfactory to them that the share certificate or acknowledgment is lost, stolen or destroyed; and |

| (2) | any indemnity the directors consider adequate. |

2.7 Splitting Share Certificates

If a shareholder surrenders a share certificate to the Company with a written request that the Company issue in the shareholder's name two or more share certificates, each representing a specified number of shares and in the aggregate representing the same number of shares as the share certificate so surrendered, the Company must cancel the surrendered share certificate and issue replacement share certificates in accordance with that request.

2.8 Certificate Fee

There must be paid to the Company, in relation to the issue of any share certificate under Articles 2.5, 2.6 or 2.7, the amount, if any and which must not exceed the amount prescribed under the Business Corporations Act, determined by the directors.

2.9 Recognition of Trusts

Except as required by law or statute or these Articles, no person will be recognized by the Company as holding any share upon any trust, and the Company is not bound by or compelled in any way to recognize (even when having notice thereof) any equitable, contingent, future or partial interest in any share or fraction of a share or (except as by law or statute or these Articles provided or as ordered by a court of competent jurisdiction) any other rights in respect of any share except an absolute right to the entirety thereof in the shareholder.

3. ISSUE OF SHARES

| 3.1 | Directors Authorized |

Subject to the Business Corporations Act and the rights of the holders of issued shares of the Company, the Company may issue, allot, sell or otherwise dispose of the unissued shares, and issued shares held by the Company, at the times, to the persons, including directors, in the manner, on the terms and conditions and for the issue prices (including any premium at which shares with par value may be issued) that the directors may determine. The issue price for a share with par value must be equal to or greater than the par value of the share.

| 7 |

3.2 Commissions and Discounts

The Company may at any time, pay a reasonable commission or allow a reasonable discount to any person in consideration of that person purchasing or agreeing to purchase shares of the Company from the Company or any other person procuring or agreeing to procure purchasers for shares of the Company.

3.3 Brokerage

The Company may pay such brokerage fee or other consideration as may be lawful for or in connection with the sale or placement of its securities.

3.4 Conditions of Issue

Except as provided for by the Business Corporations Act, no share may be issued until it is fully paid. A share is fully paid when:

| (1) | consideration is provided to the Company for the issue of the share by one or more of the following: |

| (a) | past services performed for the Company; |

| (b) | property; or |

| (c) | money; |

| (2) | and the value of the consideration received by the Company equals or exceeds the issue price set for the share under Article 3.1. |

| 3.5 | Share Purchase Warrants, Options and Rights |

Subject to the Business Corporations Act, the Company may issue share purchase warrants, options and rights upon such terms and conditions as the directors determine, which share purchase warrants, options and rights may be issued alone or in conjunction with debentures, debenture stock, bonds, shares or any other securities issued or created by the Company from time to time.

4. SHARE REGISTERS

| 4.1 | Central Securities Register |

As required by and subject to the Business Corporations Act, the Company must maintain in British Columbia a central securities register. The directors may, subject to the Business Corporations Act, appoint an agent to maintain the central securities register. The directors may also appoint one or more agents, including the agent which keeps the central securities register, as transfer agent for its shares or any class or series of its shares, as the case may be, and the same or another agent as registrar for its shares or such class or series of its shares, as the case may be. The directors may terminate such appointment of any agent at any time and may appoint another agent in its place.

| 8 |

4.2 Closing Register

The Company must not at any time close its central securities register.

5. SHARE TRANSFERS

| 5.1 | Registering Transfers |

A transfer of a share of the Company must not be registered unless the Company or the transfer agent or registrar for the class or series of share to be transferred has received:

| (1) | a duly signed instrument of transfer in respect of the share; |

| (2) | if a share certificate has been issued by the Company in respect of the share to be transferred, that share certificate; |

| (3) | if a non-transferable written acknowledgement of the shareholder’s right to obtain a share certificate has been issued by the Company in respect of the share to be transferred, that acknowledgement; and |

| (4) | such other evidence, if any, as the Company or the transfer agent or registrar for the class or series of share to be transferred may require to prove the title of the transferor or the transferor’s right to transfer the share, the due signing of the instrument of transfer and the right of the transferee to have the transfer registered. |

5.2 Form of Instrument of Transfer

The instrument of transfer in respect of any share of the Company must be either in the form, if any, on the back of the Company's share certificates or in any other form that may be approved by the directors from time to time.

5.3 Transferor Remains Shareholder

Except to the extent that the Business Corporations Act otherwise provides, the transferor of shares is deemed to remain the holder of the shares until the name of the transferee is entered in a securities register of the Company in respect of the transfer.

5.4 Signing of Instrument of Transfer

If a shareholder, or his or her duly authorized attorney, signs an instrument of transfer in respect of shares registered in the name of the shareholder, the signed instrument of transfer constitutes a complete and sufficient authority to the Company and its directors, officers and agents to register the number of shares specified in the instrument of transfer or specified in any other manner, or, if no number is specified, all the shares represented by the share certificates or set out in the written acknowledgments deposited with the instrument of transfer:

| (1) | in the name of the person named as transferee in that instrument of transfer; or |

| (2) | if no person is named as transferee in that instrument of transfer, in the name of the person on whose behalf the instrument is deposited for the purpose of having the transfer registered. |

| 9 |

5.5 Enquiry as to Title Not Required

Neither the Company nor any director, officer or agent of the Company is bound to inquire into the title of the person named in the instrument of transfer as transferee or, if no person is named as transferee in the instrument of transfer, of the person on whose behalf the instrument is deposited for the purpose of having the transfer registered or is liable for any claim related to registering the transfer by the shareholder or by any intermediate owner or holder of the shares, of any interest in the shares, of any share certificate representing such shares or of any written acknowledgment of a right to obtain a share certificate for such shares.

5.6 Transfer Fee

There must be paid to the Company or the Company’s transfer agent, in relation to the registration of any transfer, the amount, if any, determined by the directors.

6. TRANSMISSION OF SHARES

| 6.1 | Legal Personal Representative Recognized on Death |

In case of the death of a shareholder, the legal personal representative, or if the shareholder was a joint holder, the surviving joint holder, will be the only person recognized by the Company as having any title to the shareholder's interest in the shares. Before recognizing a person as a legal personal representative, the directors may require proof of appointment by a court of competent jurisdiction, a grant of letters probate, letters of administration or such other evidence or documents as the directors consider appropriate.

6.2 Rights of Legal Personal Representative

The legal personal representative has the same rights, privileges and obligations that attach to the shares held by the shareholder, including the right to transfer the shares in accordance with these Articles, provided the documents required by the Business Corporations Act and the directors have been deposited with the Company. This Article 6.2 does not apply in the case of the death of a shareholder with respect to the shares registered in the shareholder’s name and the name of another person in joint tenancy.

7. PURCHASE, REDEEM OR OTHERWISE ACQUIRE SHARES

| 7.1 | Company Authorized to Purchase, Redeem or Otherwise Acquire Shares |

Subject to Article 7.2, the special rights or restrictions attached to the shares of any class or series, the Business Corporations Act, and securities laws and regulations of general application, the Company may, if authorized by the directors, purchase, redeem or otherwise acquire any of its shares at the price and upon the terms specified in such resolution.

7.2 Purchase When Insolvent

The Company must not make a payment or provide any other consideration to purchase, redeem or otherwise acquire any of its shares if there are reasonable grounds for believing that:

| 10 |

| (1) | the Company is insolvent; or |

| (2) | making the payment or providing the consideration would render the Company insolvent. |

7.3 Sale and Voting of Purchased, Redeemed or Otherwise Acquired Shares

If the Company retains a share redeemed, purchased or otherwise acquired by it, the Company may sell, gift or otherwise dispose of the share, but, while such share is held by the Company, it:

| (1) | is not entitled to vote the share at a meeting of its shareholders; |

| (2) | must not pay a dividend in respect of the share; and |

| (3) | must not make any other distribution in respect of the share. |

| 8. | BORROWING POWERS |

The Company, if authorized by the directors, may:

| (1) | borrow money in the manner and amount, on the security, from the sources and on the terms and conditions that they consider appropriate; |

| (2) | issue bonds, debentures and other debt obligations either outright or as security for any liability or obligation of the Company or any other person and at such discounts or premiums and on such other terms as they consider appropriate; |

| (3) | guarantee the repayment of money by any other person or the performance of any obligation of any other person; and |

| (4) | mortgage, charge, whether by way of specific or floating charge, grant a security interest in, or give other security on, the whole or any part of the present and future assets and undertaking of the Company. |

9. ALTERATIONS

| 9.1 | Alteration of Authorized Share Structure |

Subject to the Business Corporations Act, the Company may by directors resolution subdivide or consolidate all or any of its unissued, or fully paid issued, shares and if applicable, alter its Notice of Articles and, if applicable, Articles, accordingly; and subject to Article 9.2 and the Business Corporations Act, the Company may by ordinary resolution:

| (1) | create one or more classes or series of shares or, if none of the shares of a class or series of shares are allotted or issued, eliminate that class or series of shares; |

| (2) | increase, reduce or eliminate the maximum number of shares that the Company is authorized to issue out of any class or series of shares or establish a maximum number of shares that the Company is authorized to issue out of any class or series of shares for which no maximum is established; |

| 11 |

| (3) | if the Company is authorized to issue shares of a class of share with par value: |

| (a) | decrease the par value of those shares; or |

| (b) | if none of the shares of that class of shares are allotted or issued, increase the par value of those shares; |

| (4) | change all or any of its unissued, or fully paid issued, shares with par value into shares without par value or any of its unissued shares without par value into shares with par value; |

| (5) | alter the identifying name of any of its shares; or |

| (6) | otherwise alter its shares or authorized share structure when required or permitted to do so by the Business Corporations Act where it does not specify by a special resolution; |

and, if applicable, alter its Notice of Articles, and if applicable, its Articles, accordingly.

9.2 Special Rights or Restrictions

Subject to the Business Corporations Act and in particular those provisions of the Act relating to the rights of holders of outstanding shares to vote if their rights are prejudiced or interfered with, the Company may by ordinary resolution:

| (1) | create special rights or restrictions for, and attach those special rights or restrictions to, the shares of any class or series of shares, whether or not any or all of those shares have been issued; or |

| (2) | vary or delete any special rights or restrictions attached to the shares of any class or series of shares, whether or not any or all of those shares have been issued and alter its Notice of Articles and Articles accordingly. |

9.3 Change of Name

The Company may by directors resolution authorize an alteration of its Notice of Articles in order to change its name.

9.4 Other Alterations

If the Business Corporations Act does not specify the type of resolution and these Articles do not specify another type of resolution, the Company may by ordinary resolution alter these Articles.

10. MEETINGS OF SHAREHOLDERS

| 10.1 | Annual General Meetings |

Unless an annual general meeting is deferred or waived in accordance with the Business Corporations Act, the Company must hold its first annual general meeting within 18 months after the date on which it was incorporated or otherwise recognized, and after that must hold an annual general meeting at least once in each calendar year and not more than 15 months

| 12 |

after the last annual reference date at such time and place as may be determined by the directors.

10.2 Resolution Instead of Annual General Meeting

If all the shareholders who are entitled to vote at an annual general meeting consent in writing by unanimous resolution under the Business Corporations Act to all of the business that is required to be transacted at that annual general meeting, the annual general meeting is deemed to have been held on the date of the unanimous resolution. The shareholders must, in any unanimous resolution passed under this Article 10.2, select as the Company's annual reference date a date that would be appropriate for the holding of the applicable annual general meeting.

10.3 Calling of Meetings of Shareholders

The directors may, whenever they think fit, call a meeting of shareholders.

10.4 Notice for Meetings of Shareholders

The Company must send notice of the date, time and location of any meeting of shareholders (including, without limitation, any notice specifying the intention to propose a resolution as an exceptional resolution, a special resolution or a special separate resolution, and any notice to consider approving amalgamation into a foreign jurisdiction, an arrangement or the adoption of an amalgamation agreement, and any notice of a general meeting, class meeting or series meeting), in the manner provided in these Articles, or in such other manner, if any, as may be prescribed by ordinary resolution (whether previous notice of the resolution has been given or not), to each shareholder entitled to attend the meeting, to each director and to the auditor of the Company, unless these Articles otherwise provide, at least the following number of days before the meeting:

| (1) | if and for so long as the Company is a Public Company, 21 days; |

| (2) | otherwise, 10 days. |

10.5 Notice of Resolution to Which Shareholders May Dissent

The Company must send to each of its shareholders, whether or not their shares carry the right to vote, a notice of any meeting of shareholders at which a resolution entitling shareholders to dissent is to be considered specifying the date of the meeting and containing a statement advising of the right to send a notice of dissent together with a copy of the proposed resolution at least the following number of days before the meeting:

| (1) | if and for so long as the Company is a Public Company, 21 days; |

| (2) | otherwise, 10 days. |

10.6 Record Date for Notice

The directors may set a date as the record date for the purpose of determining shareholders entitled to notice of any meeting of shareholders. The record date must not precede the date on which the meeting is to be held by more than two months or, in the case of a general

| 13 |

meeting requisitioned by shareholders under the Business Corporations Act, by more than four months. The record date must not precede the date on which the meeting is held by fewer than:

| (1) | if and for so long as the Company is a Public Company, 21 days; |

| (2) | otherwise, 10 days. |

If no record date is set, the record date is 5 p.m. on the day immediately preceding the first date on which the notice is sent or, if no notice is sent, the beginning of the meeting.

10.7 Record Date for Voting

The directors may set a date as the record date for the purpose of determining shareholders entitled to vote at any meeting of shareholders. The record date must not precede the date on which the meeting is to be held by more than two months or, in the case of a general meeting requisitioned by shareholders under the Business Corporations Act, by more than four months. If no record date is set, the record date is 5 p.m. on the day immediately preceding the first date on which the notice is sent or, if no notice is sent, the beginning of the meeting.

10.8 Failure to Give Notice and Waiver of Notice

The accidental omission to send notice of any meeting to, or the non-receipt of any notice by, any of the persons entitled to notice does not invalidate any proceedings at that meeting. Any person entitled to notice of a meeting of shareholders may, in writing or otherwise, waive or reduce the period of notice of such meeting. Attendance of a person at a meeting of shareholders is a waiver of entitlement to notice of the meeting unless that person attends the meeting for the express purpose of objecting to the transaction of any business on the grounds that the meeting is not lawfully called.

10.9 Notice of Special Business at Meetings of Shareholders

If a meeting of shareholders is to consider special business within the meaning of Article 11.1, the notice of meeting must:

| (1) | state the general nature of the special business; and |

| (2) | if the special business includes considering, approving, ratifying, adopting or authorizing any document or the signing of or giving of effect to any document, have attached to it a copy of the document or state that a copy of the document will be available for inspection by shareholders: |

| (a) | at the Company's records office, or at such other reasonably accessible location in British Columbia as is specified in the notice; and |

| (b) | during statutory business hours on any one or more specified days before the day set for the holding of the meeting. |

| 14 |

11. PROCEEDINGS AT MEETINGS OF SHAREHOLDERS

| 11.1 | Special Business |

At a meeting of shareholders, the following business is special business:

| (1) | at a meeting of shareholders that is not an annual general meeting, all business is special business except business relating to the conduct of or voting at the meeting; |

| (2) | at an annual general meeting, all business is special business except for the following: |

| (a) | business relating to the conduct of or voting at the meeting; |

| (b) | consideration of any financial statements of the Company presented to the meeting; |

| (c) | consideration of any reports of the directors or auditor; |

| (d) | the setting or changing of the number of directors; |

| (e) | the election or appointment of directors; |

| (f) | the appointment of an auditor; |

| (g) | the setting of the remuneration of an auditor; |

| (h) | business arising out of a report of the directors not requiring the passing of a special resolution or an exceptional resolution; |

| (i) | any other business which, under these Articles or the Business Corporations Act, may be transacted at a meeting of shareholders without prior notice of the business being given to the shareholders. |

11.2 Special Majority

The majority of votes required for the Company to pass a special resolution at a meeting of shareholders is 2/3 of the votes cast on the resolution.

11.3 Quorum

Subject to the special rights or restrictions attached to the shares of any class or series of shares, the quorum for the transaction of business at a meeting of shareholders is one shareholder present in person (or, being a corporation, partnership, trust or other non- individual legal entity represented in accordance with the provisions of the Business Corporations Act), or by proxy holding not less than one voting share of the Company entitled to be voted at the meeting.

11.4 One Shareholder May Constitute Quorum

If there is only one shareholder entitled to vote at a meeting of shareholders:

| (1) | the quorum is one person who is, or who represents by proxy, that shareholder, and |

| 15 |

| (2) | that shareholder, present in person or by proxy, may constitute the meeting. |

11.5 Other Persons May Attend

In addition to those persons who are entitled to vote at a meeting of shareholders, the only other persons entitled to be present at the meeting are the directors, the president (if any), the secretary (if any), the assistant secretary (if any), any lawyer for the Company, the auditor of the Company and any other persons invited by the directors are entitled to attend any meeting of shareholders, but if any of those persons does attend a meeting of shareholders, that person is not to be counted in the quorum and is not entitled to vote at the meeting unless that person is a shareholder or proxy holder entitled to vote at the meeting.

11.6 Requirement of Quorum

No business, other than the election of a chair of the meeting and the adjournment of the meeting, may be transacted at any meeting of shareholders unless a quorum of shareholders entitled to vote is present at the commencement of the meeting, but such quorum need not be present throughout the meeting.

11.7 Lack of Quorum

If, within one-half hour from the time set for the holding of a meeting of shareholders, a quorum is not present:

| (1) | in the case of a general meeting requisitioned by shareholders, the meeting is dissolved, and |

| (2) | in the case of any other meeting of shareholders, the meeting stands adjourned to the same day in the next week at the same time and place. |

11.8 Lack of Quorum at Succeeding Meeting

If, at the meeting to which the meeting referred to in Article 11.7(2) was adjourned, a quorum is not present within one-half hour from the time set for the holding of the meeting, the person or persons present and being, or representing by proxy, one or more shareholders entitled to attend and vote at the meeting shall be deemed to constitute a quorum.

11.9 Chair

The following individual is entitled to preside as chair at a meeting of shareholders:

| (1) | the chair of the board, if any; or |

| (2) | if the chair of the board is absent or unwilling to act as chair of the meeting, the president, if any. |

11.10 Election of Alternate Chair

If, at any meeting of shareholders, there is no chair of the board or president present within 15 minutes after the time set for holding the meeting, or if the chair of the board and the president are unwilling to act as chair of the meeting, or if the chair of the board and the president have

| 16 |

advised the secretary, if any, or any director present at the meeting, that they will not be present at the meeting, the directors present must choose one of their number or the lawyer for the Company to be chair of the meeting or if all of the directors present decline to take the chair or fail to so choose or if no director or lawyer for the Company is present, the shareholders entitled to vote at the meeting who are present in person or by proxy may choose any person present at the meeting to chair the meeting.

11.11 Adjournments

The chair of a meeting of shareholders may, and if so directed by the meeting must, adjourn the meeting from time to time and from place to place, but no business may be transacted at any adjourned meeting other than the business left unfinished at the meeting from which the adjournment took place.

11.12 Notice of Adjourned Meeting

It is not necessary to give any notice of an adjourned meeting of shareholders or of the business to be transacted at an adjourned meeting of shareholders except that, when a meeting is adjourned for 30 days or more, notice of the adjourned meeting must be given as in the case of the original meeting.

11.13 Decisions by Show of Hands or Poll

Subject to the Business Corporations Act, every motion put to a vote at a meeting of shareholders will be decided on a show of hands unless a poll, before or on the declaration of the result of the vote by show of hands, is directed by the chair or demanded by at least one shareholder entitled to vote who is present in person or by proxy.

| 11.14 | Declaration of Result |

The chair of a meeting of shareholders must declare to the meeting the decision on every question in accordance with the result of the show of hands or the poll, as the case may be, and that decision must be entered in the minutes of the meeting. A declaration of the chair that a resolution is carried by the necessary majority or is defeated is, unless a poll is directed by the chair or demanded under Article 11.13, conclusive evidence without proof of the number or proportion of the votes recorded in favour of or against the resolution.

| 11.15 | Motion Need Not be Seconded |

No motion proposed at a meeting of shareholders need be seconded unless the chair of the meeting rules otherwise, and the chair of any meeting of shareholders is entitled to propose or second a motion.

| 11.16 | Casting Vote |

In case of an equality of votes, the chair of a meeting of shareholders does not, either on a show of hands or on a poll, have a second or casting vote in addition to the vote or votes to which the chair may be entitled as a shareholder.

| 17 |

11.17 Manner of Taking Poll

Subject to Article 11.18, if a poll is duly demanded at a meeting of shareholders:

| (1) | the poll must be taken: |

| (a) | at the meeting, or within seven days after the date of the meeting, as the chair of the meeting directs; and |

| (b) | in the manner, at the time and at the place that the chair of the meeting directs; |

| (2) | the result of the poll is deemed to be the decision of the meeting at which the poll is demanded; and |

| (3) | the demand for the poll may be withdrawn by the person who demanded it. |

11.18 Demand for Poll on Adjournment

A poll demanded at a meeting of shareholders on a question of adjournment must be taken immediately at the meeting.

11.19 Chair Must Resolve Dispute

In the case of any dispute as to the admission or rejection of a vote given on a poll, the chair of the meeting must determine the dispute, and his or her determination made in good faith is final and conclusive.

11.20 Casting of Votes

On a poll, a shareholder entitled to more than one vote need not cast all the votes in the same way.

11.21 Demand for Poll

No poll may be demanded in respect of the vote by which a chair of a meeting of shareholders is elected.

11.22 Demand for Poll Not to Prevent Continuance of Meeting

The demand for a poll at a meeting of shareholders does not, unless the chair of the meeting so rules, prevent the continuation of a meeting for the transaction of any business other than the question on which a poll has been demanded.

11.23 Retention of Ballots and Proxies

The Company must, for at least three months after a meeting of shareholders, keep each ballot cast on a poll and each proxy voted at the meeting, and, during that period, make them available for inspection during normal business hours by any shareholder or proxyholder entitled to vote at the meeting. At the end of such three month period, the Company may destroy such ballots and proxies.

| 18 |

12. VOTES OF SHAREHOLDERS

| 12.1 | Number of Votes by Shareholder or by Shares |

Subject to any special rights or restrictions attached to any shares and to the restrictions imposed on joint shareholders under Article 12.3:

| (1) | on a vote by show of hands, every person present who is a shareholder or proxy holder and entitled to vote on the matter has one vote; and |

| (2) | on a poll, every shareholder entitled to vote on the matter has one vote in respect of each share entitled to be voted on the matter and held by that shareholder and may exercise that vote either in person or by proxy. |

12.2 Votes of Persons in Representative Capacity

A person who is not a shareholder may vote at a meeting of shareholders, whether on a show of hands or on a poll, and may appoint a proxy holder to act at the meeting, if, before doing so, the person satisfies the chair of the meeting, or the directors, that the person is a legal personal representative or a trustee in bankruptcy for a shareholder who is entitled to vote at the meeting.

12.3 Votes by Joint Holders

If there are joint shareholders registered in respect of any share:

| (1) | any one of the joint shareholders may vote at any meeting of shareholders, either personally or by proxy, in respect of the shares as if that joint shareholder were solely entitled to it; or |

| (2) | if more than one of the joint shareholders is present at any meeting of shareholders, personally or by proxy and more than one of them votes in respect of that share, then only the vote of the joint shareholder present whose name stands first on the central securities register in respect of the share will be counted. |

12.4 Legal Personal Representatives as Joint Shareholders

Two or more legal personal representatives of a shareholder in whose sole name any share is registered are, for the purposes of Article 12.3, deemed to be joint shareholders registered in respect of that share.

12.5 Representative of a Corporate Shareholder

If a corporation, that is not a subsidiary of the Company, is a shareholder, that corporation may appoint a person to act as its representative at any meeting of shareholders of the Company, and:

| (1) | for that purpose, the instrument appointing a representative must: |

| (a) | be received at the registered office of the Company or at any other place specified, in the notice calling the meeting, for the receipt of proxies, at least the number of business days specified in the notice for the receipt of proxies, |

| 19 |

or if no number of days is specified, two business days before the day set for the holding of the meeting or any adjourned meeting; or

| (b) | be provided, at the meeting or any adjourned meeting, to the chair of the meeting or any adjourned meeting to a person designated by the chair of the meeting or adjourned meeting; |

| (2) | if a representative is appointed under this Article 12.5: |

| (a) | the representative is entitled to exercise in respect of and at that meeting the same rights on behalf of the corporation as that corporation could exercise if it were a shareholder who is an individual, including, without limitation, the right to appoint a proxy holder; and |

| (b) | the representative, if present at the meeting, is to be counted for the purpose of forming a quorum and is deemed to be a shareholder present in person at the meeting. |

Evidence of the appointment of any such representative may be sent to the Company by written instrument, fax or any other method of transmitting legibly recorded messages.

12.6 Proxy Provisions Do Not Apply to All Companies

If and for so long as the Company is a Public Company or a pre-existing reporting company which has the Statutory Reporting Company Provisions as part of its Articles or to which the Statutory Reporting Company Provisions apply, Articles 12.7 to 12.15 apply only insofar as they are not inconsistent with any securities legislation in any province or territory of Canada or in the federal jurisdiction of the United States or in any state of the United States that is applicable to the Company insofar as they are not inconsistent with the regulations and rules made and promulgated under that legislation and all administrative policy statements, blanket order and rulings, notices and other administrative directions issued by securities commissions or similar authorities appointed under that legislation.

12.7 Appointment of Proxy Holders

Every shareholder of the Company, including a corporation that is a shareholder but not a subsidiary of the Company, entitled to vote at a meeting of shareholders of the Company may, by proxy, appoint one or more (but not more than five) proxy holders to attend and act at the meeting in the manner, to the extent and with the powers conferred by the proxy.

12.8 Alternate Proxy Holders

A shareholder may appoint one or more alternate proxy holders to act in the place of an absent proxy holder.

12.9 When Proxy Holder Need Not Be Shareholder

A person must not be appointed as a proxy holder unless the person is a shareholder, although a person who is not a shareholder may be appointed as a proxy holder if.

| (1) | the person appointing the proxy holder is a corporation or a representative of a |

| 20 |

corporation appointed under Article 12.5;

| (2) | the Company has at the time of the meeting for which the proxy holder is to be appointed only one shareholder entitled to vote at the meeting; |

| (3) | or the shareholders present in person or by proxy at and entitled to vote at the meeting for which the proxy holder is to be appointed, by a resolution on which the proxy holder is not entitled to vote but in respect of which the proxy holder is to be counted in the quorum, permit the proxy holder to attend and vote at the meeting; or |

| (4) | the Company is a Public Company. |

12.10 Deposit of Proxy

A proxy for a meeting of shareholders must:

| (1) | be received at the registered office of the Company or at any other place specified, in the notice calling the meeting, for the receipt of proxies, at least the number of business days specified in the notice, or if no number of days is specified, two business days before the day set for the holding of the meeting or any adjourned meeting; or |

| (2) | unless the notice provides otherwise, be provided, at the meeting or any adjourned meeting, to the chair of the meeting or adjourned meeting or to a person designated by the chair of the meeting or the adjourned meeting. |

A proxy may be sent to the Company by written instrument, fax or any other method of transmitting legibly recorded messages, including through Internet or telephone voting or by email, if permitted by the notice calling the meeting or the information circular for the meeting.

12.11 Validity of Proxy Vote

A vote given in accordance with the terms of a proxy is valid notwithstanding the death or incapacity of the shareholder giving the proxy and despite the revocation of the proxy or the revocation of the authority under which the proxy is given, unless notice in writing of that death, incapacity or revocation is received:

| (1) | at the registered office of the Company, at any time up to and including the last business day before the day set for the holding of the meeting or any adjourned meeting at which the proxy is to be used; or |

| (2) | at the meeting or any adjourned meeting by the chair of the meeting or adjourned meeting, before any vote in respect of which the proxy has been given, has been taken. |

| 21 |

12.12 Form of Proxy

A proxy, whether for a specified meeting or otherwise, must be either in the following form or in any other form approved by the directors or the chair of the meeting:

[name of company]

(the “Company”)

The undersigned, being a shareholder of the Company, hereby appoints [name] or, failing that person, [name], as proxy holder for the undersigned to attend, act and vote for and on behalf of the undersigned at the meeting of shareholders of the Company to be held on [month, day, year] and at any adjournment of that meeting.

Number of shares in respect of which this proxy is given (if no number is specified, then this proxy if given in respect of all shares registered in the name of the shareholder):

Signed [month, day, year]

[Signature of shareholder]

[Name of shareholder printed]

12.13 Revocation of Proxy

Subject to Article 12.14, every proxy may be revoked by an instrument in writing that is received:

| (1) | at the registered office of the Company at any time up to and including the last business day before the day set for the holding of the meeting or any adjourned meeting at which the proxy is to be used; or |

| (2) | at the meeting or any adjourned meeting, by the chair of the meeting or adjourned meeting, before any vote in respect of which the proxy has been given, has been taken. |

12.14 Revocation of Proxy Must Be Signed

An instrument referred to in Article 12.13 must be signed as follows:

| (1) | if the shareholder for whom the proxy holder is appointed is an individual, the instrument must be signed by the shareholder or his or her legal personal representative or trustee in bankruptcy; |

| (2) | if the shareholder for whom the proxy holder is appointed is a corporation, the instrument must be signed by the corporation or by a representative appointed for the corporation under Article 12.5. |

| 22 |

12.15 Production of Evidence of Authority to Vote

The chair of any meeting of shareholders may, but need not, inquire into the authority of any person to vote at the meeting and may, but need not, demand from that person production of evidence as to the existence of the authority to vote.

13. DIRECTORS

| 13.1 | First Directors, Number of Directors |

The first directors are the persons designated as directors of the Company in the Notice of Articles that applies to the Company when it is recognized under the Business Corporations Act. The number of directors, excluding additional directors appointed under Article 14.8, is set at:

| (1) | subject to paragraphs (2) and (3), the number of directors that is equal to the number of the Company's first directors; |

| (2) | if the Company is a Public Company, the greater of three and the most recently set of: |

| (a) | the number of directors set by ordinary resolution (whether or not previous notice of the resolution was given); and |

| (b) | the number of directors set under Article 14.4; |

| (3) | if the Company is not a Public Company, the most recently set of: |

| (a) | the number of directors set by ordinary resolution (whether or not previous notice of the resolution was given); and |

| (b) | the number of directors set under Article 14.4. |

13.2 Change in Number of Directors

If the number of directors is set under Articles 13.1(2)(a) or 13.1(3)(a):

| (1) | the shareholders by ordinary resolution may elect or appoint the directors needed to fill any vacancies in the board of directors up to that number; |

| (2) | if the shareholders do not elect or appoint the directors needed to fill any vacancies in the board of directors up to that number contemporaneously with the setting of that number, then the directors, subject to Article 14.8, may appoint, directors to fill those vacancies. |

13.3 Directors' Acts Valid Despite Vacancy

An act or proceeding of the directors is not invalid merely because fewer than the number of directors set or otherwise required under these Articles is in office.

| 23 |

13.4 Qualifications of Directors

A director is not required to hold a share in the capital of the Company as qualification for his or her office but must be qualified as required by the Business Corporations Act to become, act or continue to act as a director.

13.5 Remuneration of Directors

The directors are entitled to the remuneration for acting as directors, if any, as the directors may from time to time determine. If the directors so decide, the remuneration of the directors, if any, will be determined by the shareholders. That remuneration may be in addition to any salary or other remuneration paid to any officer or employee of the Company as such, who is also a director.

13.6 Reimbursement of Expenses of Directors

The Company must reimburse each director for the reasonable expenses that he or she may incur in and about the business of the Company.

13.7 Special Remuneration for Directors

If any director performs any professional or other services for the Company that in the opinion of the directors are outside the ordinary duties of a director, or if any director is otherwise specially occupied in or about the Company's business, he or she may be paid remuneration fixed by the directors, or, at the option of that director, fixed by ordinary resolution, and such remuneration may be either in addition to, or in substitution for, any other remuneration that he or she may be entitled to receive.

13.8 Gratuity, Pension or Allowance on Retirement of Director

Unless otherwise determined by ordinary resolution, the directors on behalf of the Company may pay a gratuity or pension or allowance on retirement to any director who has held any salaried office or place of profit with the Company or to his or her spouse or dependants and may make contributions to any fund and pay premiums for the purchase or provision of any such gratuity, pension or allowance.

14. ELECTION AND REMOVAL OF DIRECTORS

| 14.1 | Election at Annual General Meeting |

At every annual general meeting and in every unanimous resolution contemplated by Article 10.2:

| (1) | the shareholders entitled to vote at the annual general meeting for the election of directors must elect, or in the unanimous resolution appoint, a board of directors consisting of the number of directors set by such resolution or for the time being set under these Articles; and |

| (2) | all directors cease to hold office immediately before the election or appointment of directors under paragraph (1), but are eligible for re-election or re-appointment. |

| 24 |

14.2 Consent to be a Director

No election, appointment or designation of an individual as a director is valid unless:

| (1) | that individual consents to be a director in the manner provided for in the Business Corporations Act; |

| (2) | that individual is elected or appointed at a meeting at which the individual is present and the individual does not refuse, at the meeting, to be a director; or |

| (3) | with respect to first directors, the designation is otherwise valid under the Business Corporations Act. |

14.3 Failure to Elect or Appoint Directors

If:

| (1) | the Company fails to hold an annual general meeting or all the shareholders who are entitled to vote at an annual general meeting fail to pass the unanimous resolution contemplated by Article 10.2, on or before the date by which the annual general meeting is required to be held under the Business Corporations Act; or |

| (2) | the shareholders fail, at the annual general meeting or in the unanimous resolution contemplated by Article 10.2, to elect or appoint any directors; |

then each director then in office continues to hold office until the earlier of:

| (3) | the date on which his or her successor is elected or appointed; and |

| (4) | the date on which he or she otherwise ceases to hold office under the Business Corporations Act or these Articles. |

14.4 Places of Retiring Directors Not Filled

If, at any meeting of shareholders at which there should be an election of directors, the places of any of the retiring directors are not filled by that election, those retiring directors who are not re-elected and who are asked by the newly elected directors to continue in office will, if willing to do so, continue in office to complete the number of directors for the time being set pursuant to these Articles until further new directors are elected at a meeting of shareholders convened for that purpose. If any such election or continuance of directors does not result in the election or continuance of the number of directors for the time being set pursuant to these Articles, the number of directors of the Company is deemed to be set at the number of directors actually elected or continued in office.

14.5 Directors May Fill Casual Vacancies

Any casual vacancy occurring in the board of directors may be filled by the directors.

14.6 Remaining Directors Power to Act

The directors may act notwithstanding any vacancy in the board of directors. If the Company has fewer directors in office than the number set pursuant to these Articles as the quorum of

| 25 |

directors, the directors may act for the purpose of appointing directors up to that number or of summoning a meeting of shareholders for the purpose of filling any vacancies on the board of directors or, subject to the Business Corporations Act, for any other purpose.

14.7 Shareholders May Fill Vacancies

The shareholders may elect or appoint additional directors to the board of directors by ordinary resolution.

14.8 Additional Directors

Notwithstanding Articles 13.1 and 13.2, between annual general meetings or unanimous resolutions contemplated by Article 10.2, the directors may appoint one or more additional directors, but the number of additional directors appointed under this Article 14.8 must not at any time exceed:

| (1) | one-third of the number of first directors, if, at the time of the appointments, one or more of the first directors have not yet completed their first term of office; or |

| (2) | in any other case, one-third of the number of the current directors who were elected or appointed as directors other than under this Article 14.8. |

Any director so appointed ceases to hold office immediately before the next election or appointment of directors under Article 14.1(1), but is eligible for re-election or re-appointment.

14.9 Ceasing to be a Director

A director ceases to be a director when:

| (1) | the term of office of the director expires; |

| (2) | the director dies; |

| (3) | the director resigns as a director by notice in writing provided to the Company or a lawyer for the Company; or |

| (4) | the director is removed from office pursuant to Articles 14.10 or 14.11. |

14.10 Removal of Director by Shareholders

The Company may remove any director before the expiration of his or her term of office by ordinary resolution. In that event, the shareholders may elect, or appoint by ordinary resolution, a director to fill the resulting vacancy. If the shareholders do not elect or appoint a director to fill the resulting vacancy contemporaneously with the removal, then the directors may appoint or the shareholders may elect, or appoint by ordinary resolution, a director to fill that vacancy.

| 26 |

14.11 Removal of Director by Directors

The directors may remove any director before the expiration of his or her term of office if the director is convicted of an indictable offence, or if the director ceases to be qualified to act as a director of a company and does not promptly resign, and the directors may appoint a director to fill the resulting vacancy.

15. ALTERNATE DIRECTORS

| 15.1 | Appointment of Alternate Director |

Any director (an “appointor”) may by notice in writing received by the Company appoint any person (an “appointee”) who is qualified to act as a director to be his or her alternate to act in his or her place at meetings of the directors or committees of the directors at which the appointor is not present unless (in the case of an appointee who is not a director) the directors have reasonably disapproved the appointment of such person as an alternate director and have given notice to that effect to his or her appointor within a reasonable time after the notice of appointment is received by the Company.

15.2 Notice of Meetings

Every alternate director so appointed is entitled to notice of meetings of the directors and of committees of the directors of which his or her appointor is a member and to attend and vote as a director at any such meetings at which his or her appointor is not present.

15.3 Alternate for More than One Director Attending Meetings

A person may be appointed as an alternate director by more than one director, and an alternate director:

| (1) | will be counted in determining the quorum for a meeting of directors once for each of his or her appointors and, in the case of an appointee who is also a director, once more in that capacity; |

| (2) | has a separate vote at a meeting of directors for each of his or her appointors and, in the case of an appointee who is also a director, an additional vote in that capacity; |

| (3) | will be counted in determining the quorum for a meeting of a committee of directors once for each of his or her appointors who is a member of that committee and, in the case of an appointee who is also a member of that committee as a director, once more in that capacity; and |

| (4) | has a separate vote at a meeting of a committee of directors for each of his or her appointors who is a member of that committee and, in the case of an appointee who is also a member of that committee as a director, an additional vote in that capacity. |

15.4 Consent Resolutions

Every alternate director, if authorized by the notice appointing him or her, may sign in place of his or her appointor any resolutions to be consented to in writing.

| 27 |

15.5 Alternate Director an Agent

Every alternate director is deemed to be the agent of his or her appointor.

15.6 Revocation or Amendment of Appointment of Alternate Director

An appointor may at any time, by notice in writing received by the Company, revoke or amend the terms of the appointment of an alternate director appointed by him or her.

15.7 Ceasing to be an Alternate Director

The appointment of an alternate director ceases when:

| (1) | his or her appointor ceases to be a director and is not promptly re-elected or re- appointed; |

| (2) | the alternate director dies; |

| (3) | the alternate director resigns as an alternate director by notice in writing provided to the Company or a lawyer for the Company; |

| (4) | the alternate director ceases to be qualified to act as a director; or |

| (5) | the term of his appointment expires, or his or her appointor revokes the appointment of the alternate director. |

15.8 Remuneration and Expenses of Alternate Director

The Company may reimburse an alternate director for the reasonable expenses that would be properly reimbursed if he or she were a director, and the alternate director is entitled to receive from the Company such proportion, if any, of the remuneration otherwise payable to the appointor as the appointor may from time to time direct.

| 16. | POWERS AND DUTIES OF DIRECTORS |

| 16.1 | Powers of Management |

The directors must, subject to the Business Corporations Act and these Articles, manage or supervise the management of the business and affairs of the Company and have the authority to exercise all such powers of the Company as are not, by the Business Corporations Act or by these Articles, required to be exercised by the shareholders of the Company.

16.2 Appointment of Attorney of Company

The directors may from time to time, by power of attorney or other instrument, under seal if so required by law, appoint any person to be the attorney of the Company for such purposes, and with such powers, authorities and discretions (not exceeding those vested in or exercisable by the directors under these Articles and excepting the power to fill vacancies in the board of directors, to remove a director, to change the membership of, or fill vacancies in, any committee of the directors, to appoint or remove officers appointed by the directors and to declare dividends) and for such period, and with such remuneration and subject to such conditions as the directors may think fit. Any such power of attorney may contain such

| 28 |

provisions for the protection or convenience of persons dealing with such attorney as the directors think fit. Any such attorney may be authorized by the directors to sub-delegate all or any of the powers, authorities and discretions for the time being vested in him or her.

16.3 Setting Remuneration of Auditor

The directors may set the remuneration of the Company's auditor from time to time without shareholder approval.

17. DISCLOSURE OF INTEREST OF DIRECTORS AND OFFICERS

| 17.1 | Obligation to Account for Profits |

A director or senior officer who holds a disclosable interest (as that term is used in the Business Corporations Act) in a contract or transaction into which the Company has entered or proposes to enter is liable to account to the Company for any profit that accrues to the director or senior officer under or as a result of the contract or transaction only if and to the extent provided in the Business Corporations Act.

17.2 Restrictions on Voting by Reason of Interest

A director who holds a disclosable interest in a contract or transaction into which the Company has entered or proposes to enter is not entitled to vote on any directors' resolution to approve that contract or transaction, unless all the directors have a disclosable interest in that contract or transaction, in which case any or all of those directors may vote on such resolution.

17.3 Interested Director Counted in Quorum

A director who holds a disclosable interest in a contract or transaction into which the Company has entered or proposes to enter and who is present at the meeting of directors at which the contract or transaction is considered for approval may be counted in the quorum at the meeting whether or not the director votes on any or all of the resolutions considered at the meeting.

17.4 Disclosure of Conflict of Interest or Property

A director or senior officer who holds any office or possesses any property, right or interest that could result, directly or indirectly, in the creation of a duty or interest that materially conflicts with that individual's duty or interest as a director or senior officer, must disclose the nature and extent of the conflict as required by the Business Corporations Act.

17.5 Director Holding Other Office in the Company

A director may hold any office or place of profit with the Company, other than the office of auditor of the Company, in addition to his or her office of director for the period and on the terms (as to remuneration or otherwise) that the directors may determine.

| 29 |

17.6 No Disqualification

No director or intended director is disqualified by his or her office from contracting with the Company either with regard to the holding of any office or place of profit the director holds with the Company or as vendor, purchaser or otherwise, and no contract or transaction entered into by or on behalf of the Company in which a director is in any way interested is liable to be voided for that reason.

17.7 Professional Services by Director or Officer

Subject to the Business Corporations Act, a director or officer, or any person in which a director or officer has an interest, may act in a professional capacity for the Company, except as auditor of the Company, and the director or officer or such person is entitled to remuneration for professional services as if that director or officer were not a director or officer.

17.8 Director or Officer in Other Corporations

A director or officer may be or become a director, officer or employee of, or otherwise interested in, any person in which the Company may be interested as a shareholder or otherwise, and, subject to the Business Corporations Act, the director or officer is not accountable to the Company for any remuneration or other benefits received by him or her as director, officer or employee of, or from his or her interest in, such other person.

18. PROCEEDINGS OF DIRECTORS

| 18.1 | Meetings of Directors |

The directors may meet together for the conduct of business, adjourn and otherwise regulate their meetings as they think fit, and meetings of the directors held at regular intervals may be held at the place, at the time and on the notice, if any, as the directors may from time to time determine.

18.2 Voting at Meetings

Questions arising at any meeting of directors are to be decided by a majority of votes and, in the case of an equality of votes, the chair of the meeting has a second or casting vote.

18.3 Chair of Meetings

The following individual is entitled to preside as chair at a meeting of directors:

| (1) | the chair of the board, if any; |

| (2) | in the absence of the chair of the board, the president, if any, if the president is a director; or |

| (3) | any other director chosen by the directors if: |

| (a) | neither the chair of the board nor the president, if a director, is present at the meeting within 15 minutes after the time set for holding the meeting; |

| 30 |

| (b) | neither the chair of the board nor the president, if a director, is willing to chair the meeting; or |

| (c) | the chair of the board and the president, if a director, have advised the secretary, if any, or any other director, that they will not be present at the meeting. |

18.4 Meetings by Telephone or Other Communications Medium

A director may participate in a meeting of the directors or of any committee of the directors in person or by telephone if all directors participating in the meeting, whether in person or by telephone or other communications medium, are able to communicate with each other. A director may participate in a meeting of the directors or of any committee of the directors by a communications medium other than telephone if all directors participating in the meeting, whether in person or by telephone or other communications medium, are able to communicate with each other and if all directors who wish to participate in the meeting agree to such participation. A director who participates in a meeting in a manner contemplated by this Article

18.4 is deemed for all purposes of the Business Corporations Act and these Articles to be present at the meeting and to have agreed to participate in that manner.

18.5 Calling of Meetings

A director may, and the secretary or an assistant secretary of the Company, if any, on the request of a director must, call a meeting of the directors at any time.

18.6 Notice of Meetings

Other than for meetings held at regular intervals as determined by the directors pursuant to Article 18.1, reasonable notice of each meeting of the directors, specifying the place, day and time of that meeting must be given to each of the directors and the alternate directors by any method set out in Article 24.1 or orally or by telephone.

18.7 When Notice Not Required

It is not necessary to give notice of a meeting of the directors to a director or an alternate director if:

| (1) | the meeting is to be held immediately following a meeting of shareholders at which that director was elected or appointed, or is the meeting of the directors at which that director is appointed; or |

| (2) | the director or alternate director, as the case may be, has waived notice of the meeting. |

18.8 Meeting Valid Despite Failure to Give Notice

The accidental omission to give notice of any meeting of directors to, or the non-receipt of any notice by, any director or alternate director, does not invalidate any proceedings at that meeting.

| 31 |

18.9 Waiver of Notice of Meetings

Any director or alternate director may send to the Company a document signed by him or her waiving notice of any past, present or future meeting or meetings of the directors and may at any time withdraw that waiver with respect to meetings held after that withdrawal. After sending a waiver with respect to all future meetings and until that waiver is withdrawn, no notice of any meeting of the directors need be given to that director and, unless the director otherwise requires by notice in writing to the Company, to his or her alternate director, and all meetings of the directors so held are deemed not to be improperly called or constituted by reason of notice not having been given to such director or alternate director. Attendance of a director or alternate director at a meeting of the directors is a waiver of notice of the meeting unless that director or alternate director attends the meeting for the express purpose of objecting to the transaction of any business on the grounds that the meeting is not lawfully called.

18.10 Quorum

The quorum necessary for the transaction of the business of the directors may be set by the directors and, if not so set, is deemed to be set at the two (2) directors in office or, if the number of directors is set at one, is deemed to be set at one director, and that director may constitute a meeting.

18.11 Validity of Acts Where Appointment Defective

Subject to the Business Corporations Act, an act of a director or officer is not invalid merely because of an irregularity in the election or appointment or a defect in the qualification of that director or officer.

18.12 Consent Resolutions in Writing

A resolution of the directors or of any committee of the directors may be passed without a meeting:

| (1) | in all cases, if each of the directors entitled to vote on the resolution consents to it in writing; or |

| (2) | in the case of a resolution to approve a contract or transaction in respect of which a director has disclosed that he or she has or may have a disclosable interest, if each of the directors who have not made such a disclosure consents in writing to the resolution. |

A consent in writing under this Article may be by signed document, fax, email or any other method of transmitting legibly recorded messages. A consent in writing may be in two or more counterparts which together are deemed to constitute one consent in writing. A resolution of the directors or of any committee of the directors passed in accordance with this Article 18.12 is effective on the date stated in the consent in writing or on the latest date stated on any counterpart and is deemed to be a proceeding at a meeting of directors or of the committee of the directors and to be as valid and effective as if it had been passed at a meeting of the directors or of the committee of the directors that satisfies all the requirements of the Business Corporations Act and all the requirements of these Articles relating to meetings of the directors or of a committee of the directors.

| 32 |

| 19. | COMMITTEES |

| 19.1 | Appointment and Powers of Executive Committee |

The directors may, by resolution, appoint an executive committee consisting of the director or directors that they consider appropriate, and this committee has, during the intervals between meetings of the board of directors, all of the directors’ powers, except:

| (1) | the power to fill vacancies in the board of directors; |

| (2) | the power to remove directors; |

| (3) | the power to change the membership of, or fill vacancies in, any committee of the directors; and |

| (4) | such other powers or restrictions, if any, as may be set out in the resolution or subsequent directors’ resolution. |

19.2 Appointment and Powers of Other Committee

The directors may, by resolution:

| (1) | appoint one or more committees (other than the executive committee) consisting of the director or directors that they consider appropriate; |

| (2) | delegate to a committee appointed under paragraph (1) any of the directors' powers, except: |

| (a) | the power to fill vacancies in the board of directors; |

| (b) | the power to remove a director; |

| (c) | the power to change the membership of, or fill vacancies in, any committee of the directors; and |

| (d) | the power to appoint or remove officers appointed by the directors; and |

| (3) | make any delegation referred to in paragraph (2) subject to the conditions set out in the resolution or any subsequent directors' resolution. |

19.3 Obligations of Committees

Any committee appointed under Article 19.1 or 19.2, in the exercise of the powers delegated to it, must:

| (1) | conform to any rules that may from time to time be imposed on it by the directors; and |

| (2) | report every act or thing done in exercise of those powers at such times as the directors may require. |

| 33 |

19.4 Powers of Board

The directors may, at any time, with respect to a committee appointed under Articles 19.1 or 19.2:

| (1) | revoke or alter the authority given to the committee, or override a decision made by the committee, except as to acts done before such revocation, alteration or overriding; |

| (2) | terminate the appointment of, or change the membership of, the committee; and |

| (3) | fill vacancies in the committee. |

19.5 Committee Meetings

Subject to Article 19.2(1) and unless the directors otherwise provide in the resolution appointing the committee or in any subsequent resolution, with respect to a committee appointed under Article 19.1 or 19.2:

| (1) | the committee may meet and adjourn as it thinks proper; |

| (2) | the committee may elect a chair of its meetings but, if no chair of a meeting is elected, or if at a meeting the chair of the meeting is not present within 15 minutes after the time set for holding the meeting, the directors present who are members of the committee may choose one of their number to chair the meeting; |

| (3) | a majority of the members of the committee constitutes a quorum of the committee; and |

| (4) | questions arising at any meeting of the committee are determined by a majority of votes of the members present, and in case of an equality of votes, the chair of the meeting does not have a second or casting vote. |

20. OFFICERS

| 20.1 | Directors May Appoint Officers |

The directors may, from time to time, appoint such officers, if any, as the directors determine and the directors may, at any time, terminate any such appointment.

20.2 Functions, Duties and Powers of Officers

The directors may, for each officer:

| (1) | determine the functions and duties of the officer; |

| (2) | entrust to and confer on the officer any of the powers exercisable by the directors on such terms and conditions and with such restrictions as the directors think fit; and |

| (3) | revoke, withdraw, alter or vary all or any of the functions, duties and powers of the officer. |

| 34 |

20.3 Qualifications

No officer may be appointed unless that officer is qualified in accordance with the Business Corporations Act. One person may hold more than one position as an officer of the Company. Any person appointed as the chair of the board or as the managing director must be a director. Any other officer need not be a director.

20.4 Remuneration and Terms of Appointment

All appointments of officers are to be made on the terms and conditions and at the remuneration (whether by way of salary, fee, commission, participation in profits or otherwise) that the directors thinks fit and are subject to termination at the pleasure of the directors, and an officer may in addition to such remuneration be entitled to receive, after he or she ceases to hold such office or leaves the employment of the Company, a pension or gratuity.

21. INDEMNIFICATION

| 21.1 | Definitions |

In this Article 21:

| (1) | “eligible party”, in relation to a company, means an individual who: |

| (a) | is or was a director, alternate director or officer of the Company; |

| (b) | is or was a director, alternate director or officer of another corporation |

| (i) | at a time when the corporation is or was an affiliate of the Company, or |

| (ii) | at the request of the Company; or |

| (c) | at the request of the Company, is or was, or holds or held a position equivalent to that of, a director, alternate director or officer of a partnership, trust, joint venture or other unincorporated entity; |

and includes, except in the definition of “eligible proceeding”, and s. 163(1)(c) and (d) and s. 165 of the Business Corporations Act, the heirs and personal or other legal representatives of that individual;

| (2) | “eligible penalty” means a judgment, penalty or fine awarded or imposed in, or an amount paid in settlement of, an eligible proceeding; |

| (3) | “eligible proceeding” means a legal proceeding or investigative action, whether current, threatened, pending or completed, in which an eligible party or any of the heirs and legal personal representatives of the eligible party, by reason of the eligible party being or having been a director or alternate director or officer of, or holding or having held a position equivalent to that of a director, alternative director or officer of, the Company or an affiliate of the Company: |

| (a) | is or may be joined as a party; or |

| (b) | is or may be liable for or in respect of a judgment, penalty or fine in, or expenses |

| 35 |

related to, the proceeding;

| (4) | “expenses” has the meaning set out in the Business Corporations Act. |

21.2 Mandatory Indemnification of Eligible Parties

Subject to the Business Corporations Act, the Company must indemnify each eligible party and his or her heirs and legal personal representatives against all eligible penalties to which such person is or may be liable, and the Company must, after the final disposition of an eligible proceeding, pay the expenses actually and reasonably incurred by such person in respect of that proceeding. Each eligible party is deemed to have contracted with the Company on the terms of the indemnity contained in this Article 21.2.

21.3 Indemnification of Other Persons

Subject to any restrictions in the Business Corporations Act, the Company may indemnify any person.

| 21.4 | Non-Compliance with Business Corporations Act |

The failure of an eligible party to comply with the Business Corporations Act or these Articles does not invalidate any indemnity to which he or she is entitled under this Part.