Exhibit 99.1

Unaudited Interim Report

for the

six-month

period ended 30 June 2023 4

| • | global, regional and local economic weakness and uncertainty, including the risks of an economic downturn, recession and/or inflationary pressures in one or more of our key markets, and the impact they may have on us, our customers and our suppliers and our assessment of that impact; |

| • | continued geopolitical instability (including as a result of the ongoing conflict between Russia and Ukraine), which may have a substantial impact on the economies of one or more of our key markets and may result in, among other things, disruptions to global supply chains, increases in commodity and energy prices with follow-on inflationary impacts, and economic and political sanctions; |

| • | financial risks, such as interest rate risk, foreign exchange rate risk (in particular as against the U.S. dollar, our reporting currency), commodity risk, asset price risk, equity market risk, counterparty risk, sovereign risk, liquidity risk, inflation or deflation, including inability to achieve our optimal net debt level; |

| • | changes in government policies and currency controls; |

| • | continued availability of financing and our ability to achieve our targeted coverage and debt levels and terms, including the risk of constraints on financing in the event of a credit rating downgrade; |

| • | the monetary and interest rate policies of central banks, in particular the European Central Bank, the Board of Governors of the U.S. Federal Reserve System, the Bank of England, Banco Central do Brasil, Banco Central de la República Argentina Banco de la República |

| • | changes in applicable laws, regulations and taxes in jurisdictions in which we operate, including the laws and regulations governing our operations and changes to tax benefit programs, as well as actions or decisions of courts and regulators; |

| • | limitations on our ability to contain costs and expenses or increase our prices to offset increased costs; |

| • | failure to meet our expectations with respect to expansion plans, premium growth, accretion to reported earnings, working capital improvements and investment income or cash flow projections; |

| • | our ability to continue to introduce competitive new products and services on a timely, cost-effective basis; |

| • | the effects of competition and consolidation in the markets in which we operate, which may be influenced by regulation, deregulation or enforcement policies; |

| • | changes in consumer spending; |

| • | changes in pricing environments; |

| • | volatility in the availability or prices of raw materials, commodities and energy; |

| • | difficulties in maintaining relationships with employees; |

| • | regional or general changes in asset valuations; |

| • | greater than expected costs (including taxes) and expenses; |

| • | damage to our reputation or brand image; |

| • | climate change and other environmental concerns; |

| • | the risk of unexpected consequences resulting from acquisitions, joint ventures, strategic alliances, corporate reorganizations or divestiture plans, and our ability to successfully and cost-effectively implement these transactions and integrate the operations of businesses or other assets we have acquired; |

| • | the outcome of pending and future litigation, investigations and governmental proceedings; |

| • | natural and other disasters, including widespread health emergencies such as the COVID-19 pandemic, cyberattacks and military conflict and political instability; |

| • | any inability to economically hedge certain risks; |

| • | inadequate impairment provisions and loss reserves; |

| • | technological disruptions, threats to cybersecurity and the risk of loss or misuse of personal data; |

| • | other statements included in this document that are not historical; and |

| • | our success in managing the risks involved in the foregoing. |

| • | Lead and grow the category : In the first six months of 2023, we invested approximately USD 3.5 billion in sales and marketing, an increase of 12.8% versus the same period in 2022, driving an increase of our portfolio brand power5 in approximately 60% of our key markets. We are executing on five proven and scalable levers to drive category expansion: |

○ |

Inclusive Category |

○ |

Core Superiority mid-single digit1 revenue increase, as double-digit growth in South Africa and Colombia was partially offset by the revenue decline of Bud Light in the US. Our mainstream brands gained or maintained share of segment in two thirds of our key markets, according to our estimates. |

○ |

Occasions Development no-alcohol beer portfolio delivered approximately 30%1 revenue growth in the second quarter of 2023, with our performance driven by Budweiser Zero in Brazil and the growth of Corona Cero in Canada and Europe. Leveraging our digital direct-to-consumer |

○ |

Premiumization : Our above core beer portfolio grew revenue by more than 10%1 in the second quarter of 2023, led by our global brands and double-digit1 growth of Modelo in Mexico and Spaten in Brazil. Our global brands grew revenue by 18.4%1,6 outside of their home markets in the second quarter of 2023, led by Corona, which was recently recognized by Kantar BrandZ as the #1 fastest growing global beer brand by value, which grew 23.7%1, 6 . Budweiser delivered a revenue increase of 16.9%1,6 with broad-based growth in 25 markets and supported by the return of consumer demand in China. Stella Artois grew by 14.5%1,6. |

○ |

Beyond Beer 1 as growth globally was partially offset by a soft malt-based seltzer industry in the US. Global growth was primarily driven by the expansion of Brutal Fruit in Africa and the Vicky portfolio in Mexico. |

| • | Digitize and monetize our ecosystem |

○ |

Digitizing our relationships with more than 6 million customers globally |

| 2023 captured through B2B digital platforms. In the second quarter of 2023, BEES had 3.3 million monthly active users and captured approximately USD 9.2 billion in gross merchandise value (GMV), growth of 15% and 30% versus the second quarter of 2022 respectively. BEES Marketplace is live in 15 markets with 63% of BEES customers also Marketplace buyers. Marketplace captured approximately USD 340 million in GMV from sales of third-party products in the second quarter of 2023, growth of 41% versus the same period last year. |

○ |

Leading the way in DTC solutions : Our omnichannel direct-to-consumer |

| • | Optimize our business : In the first six months of 2023, disciplined overhead management and efficient allocation of resources across our operations, enabled us to invest approximately USD 2.1 billion in capex and USD 3.5 billion in sales and marketing to drive the organic growth of our business, while managing the continued elevated cost environment. Underlying EPS4 for the first six months of 2023 was USD 1.37, an increase of USD 0.04 per same period of 2022, cycling a USD 0.05 per share net benefit from tax credits in Brazil year-over-year. |

Six-month period ended 30 June 2023 |

Six-month period ended 30 June 2022 |

Change |

||||||||||

(USD million, except volumes) |

(%) (1) |

|||||||||||

Volumes (thousand hectoliters) |

288,131 | 289,074 | (0.3 | ) | ||||||||

Revenue |

29,333 | 28,027 | 4.7 | |||||||||

Cost of sales |

(13,536 | ) | (12,784 | ) | (5.9 | ) | ||||||

Gross profit |

15,796 | 15,243 | 3.6 | |||||||||

Selling, General and Administrative expenses |

(9,051 | ) | (8,616 | ) | (5.0 | ) | ||||||

Other operating income/(expenses) |

327 | 478 | (31.6 | ) | ||||||||

Exceptional items |

(107 | ) | (105 | ) | (1.9 | ) | ||||||

Profit from operations |

6,965 | 7,000 | (0.5 | ) | ||||||||

Normalized EBITDA (²) |

9,668 | 9,583 | 0.9 | |||||||||

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

| (2) | Normalized EBITDA is a non-IFRS measure. For a discussion of how we use Normalized EBITDA and its limitations, and a table showing the calculation of our Normalized EBITDA, for the periods shown, see “—Normalized EBITDA” below. |

Six-month period ended 30 June 2023 |

Six-month period ended 30 June 2022 |

Change | ||||||||||

(thousand hectoliters) |

(%) (1) | |||||||||||

North America |

47,395 | 51,448 | (7.9 | ) | ||||||||

Middle Americas |

72,164 | 72,024 | 0.2 | |||||||||

South America |

76,023 | 76,815 | (1.0 | ) | ||||||||

EMEA |

42,842 | 42,962 | (0.3 | ) | ||||||||

Asia Pacific |

49,589 | 45,385 | 9.3 | |||||||||

Global Export and Holding Companies |

117 | 440 | (73.4 | ) | ||||||||

Total |

288,131 |

289,074 |

(0.3 |

) | ||||||||

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

Six-month period ended 30 June 2023 |

Six-month period ended 30 June 2022 |

Change | ||||||||||

(USD million) |

(%) (1) | |||||||||||

North America |

7,926 | 8,192 | (3.2 | ) | ||||||||

Middle Americas |

7,573 | 6,693 | 13.1 | |||||||||

South America |

5,849 | 5,333 | 9.7 | |||||||||

EMEA |

4,070 | 3,940 | 3.3 | |||||||||

Asia Pacific |

3,679 | 3,471 | 6.0 | |||||||||

Global Export & Holding Companies |

236 | 399 | (40.9 | ) | ||||||||

Total |

29,333 |

28,027 |

4.7 |

|||||||||

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

· |

The 2022 and 2023 acquisitions and disposals had no significant impact on our consolidated revenue for the six-month period ended 30 June 2023 compared to the six-month period ended 30 June 2022. |

· |

Our consolidated revenue for the six-month period ended 30 June 2023 also reflects a negative currency translation impact of USD 1,459 million mainly arising from currency translation effects in EMEA, South America and Asia Pacific. |

· |

In South America, the growth in the revenue per hectoliter in Argentina was driven primarily by revenue management initiatives in a highly inflationary environment. In Brazil, we reported double-digit revenue per hectoliter growth, driven by revenue management initiatives and continued premiumization. |

· |

In Middle Americas, the growth in the revenue per hectoliter was driven by pricing actions and other revenue management initiatives. |

· |

In EMEA, the growth in the revenue per hectoliter was driven by pricing actions. In Europe, there was also continued momentum of our premium and super premium brands. |

Six-month period ended 30 June 2023 |

Six-month period ended 30 June 2022 |

Change | ||||||||||

(USD million) |

(%) (1) | |||||||||||

North America |

(3,420 | ) | (3,349 | ) | (2.1 | ) | ||||||

Middle Americas |

(2,926 | ) | (2,625 | ) | (11.5 | ) | ||||||

South America |

(2,949 | ) | (2,792 | ) | (5.6 | ) | ||||||

EMEA |

(2,210 | ) | (2,000 | ) | (10.5 | ) | ||||||

Asia Pacific |

(1,750 | ) | (1,655 | ) | (5.7 | ) | ||||||

Global Export & Holding Companies |

(281 | ) | (362 | ) | 22.4 | |||||||

Total |

(13,536 |

) |

(12,784 |

) |

(5.9 |

) | ||||||

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

· |

The 2022 and 2023 acquisitions and disposals did not have a significant impact on our consolidated cost of sales for the six-month period ended 30 June 2023 compared to the six-month period ended 30 June 2022. |

· |

Our consolidated cost of sales for the six-month period ended 30 June 2023 also reflects a positive currency translation impact of USD 690 million mainly arising from currency translation effects in South America, EMEA and Asia Pacific. |

Six-month periodended 30 June 2023 |

Six-month periodended 30 June 2022 |

Change |

||||||||||

(USD million) |

(%) (1) |

|||||||||||

Selling, General and Administrative expenses |

(9,051 | ) | (8,616 | ) | (5.0 | ) | ||||||

Other operating income/(expenses) |

327 | 478 | (31.6 | ) | ||||||||

Total Operating Expenses |

(8,724 |

) |

(8,138 |

) |

(7.2 |

) | ||||||

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

Six-month periodended 30 June 2023 |

Six-month periodended 30 June 2022 |

Change |

||||||||||

(USD million) |

(%) (1) |

|||||||||||

North America |

(2,354 | ) | (2,279 | ) | (3.3 | ) | ||||||

Middle Americas |

(1,863 | ) | (1,631 | ) | (14.2 | ) | ||||||

South America |

(1,804 | ) | (1,609 | ) | (12.1 | ) | ||||||

EMEA |

(1,307 | ) | (1,341 | ) | 2.5 | |||||||

Asia Pacific |

(1,033 | ) | (999 | ) | (3.4 | ) | ||||||

Global Export & Holding Companies |

(692 | ) | (756 | ) | 8.5 | |||||||

Total |

(9,051 |

) |

(8,616 |

) |

(5.0 |

) | ||||||

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

| • | The 2022 and 2023 acquisitions and disposals had no significant impact on our consolidated selling, general and administrative expenses for the six-month period ended 30 June 2023 compared to the six-month period ended 30 June 2022. |

| • | Our consolidated selling, general and administrative expenses for the six-month period ended 30 June 2023 also reflects a positive currency translation impact of USD 426 million mainly arising from currency translation effects in South America, EMEA and Asia Pacific. |

Six-month period ended 30 June 2023 |

Six-month period ended 30 June 2022 |

Change |

||||||||||

(USD million) |

(%) (1) |

|||||||||||

North America |

18 | 28 | (35.7 | ) | ||||||||

Middle Americas |

8 | (12 | ) | - | ||||||||

South America |

171 | 312 | (45.2 | ) | ||||||||

EMEA |

83 | 88 | (5.7 | ) | ||||||||

Asia Pacific |

53 | 67 | (20.9 | ) | ||||||||

Global Export & Holding Companies |

(6 | ) | (5 | ) | (20.0 | ) | ||||||

Total |

327 |

478 |

(31.6 |

) | ||||||||

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

| • | The 2022 and 2023 acquisitions and disposals and the 2022 Brazilian tax credits negatively impacted our net consolidated other operating income and expenses by USD 204 million on a net basis for the six-month period ended 30 June 2023 compared to the six-month period ended 30 June 2022. |

| • | Our net consolidated other operating income and expenses for the six-month period ended 30 June 2023 had no significant currency translation impact. |

Six-month period ended 30 June 2023 |

Six-month period ended 30 June 2022 |

|||||||

(USD million) |

||||||||

COVID-19 costs |

- | (13 | ) | |||||

Restructuring |

(50 | ) | (51 | ) | ||||

Business and asset disposal (including impairment losses) |

(38 | ) | 6 | |||||

Legal costs |

(19 | ) | - | |||||

AB InBev Efes related costs |

- | (47 | ) | |||||

Total |

(107 |

) |

(105 |

) | ||||

Six-month periodended 30 June 2023 |

Six-month periodended 30 June 2022 |

Change |

||||||||||

(USD million) |

(%) (1) |

|||||||||||

North America |

2,131 | 2,570 | (17.1 | ) | ||||||||

Middle Americas |

2,781 | 2,416 | 15.1 | |||||||||

South America |

1,241 | 1,234 | 0.6 | |||||||||

EMEA |

618 | 667 | (7.4 | ) | ||||||||

Asia Pacific |

944 | 879 | 7.4 | |||||||||

Global Export & Holding Companies |

(749 | ) | (766 | ) | 2.2 | |||||||

Total |

6,965 |

7,000 |

(0.5 |

) | ||||||||

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

| • | The 2022 and 2023 acquisitions and disposals and the Brazilian tax credits negatively impacted our consolidated profit from operations by USD 239 million for the six-month period ended 30 June 2023 compared to the six-month period ended 30 June 2022. |

| • | Our consolidated profit from operations for the six-month period ended 30 June 2023 also reflects a negative currency translation impact of USD 358 million. |

| • | Our profit from operations for the six-month period ended 30 June 2023 was negatively impacted by USD 107 million of certain exceptional items, as compared to a negative impact of USD 105 million for the six-month period ended 30 June 2022. See “Exceptional Items” above for a description of exceptional items that impacted our profit from operations for the six-month period ended 30 June 2023 and 2022. |

Six-month period ended 30 June 2023 |

Six-month period ended 30 June 2022 |

Change |

||||||||||

(USD million) |

(%) (1) |

|||||||||||

Profit attributable to equity holders of AB InBev |

1,977 | 1,692 | 16.8 |

|||||||||

Profit attributable to non-controlling interests |

678 | 782 | (13.3 |

) | ||||||||

Profit of the period |

2,655 |

2,474 |

7.3 |

|||||||||

Net finance cost |

3,223 | 2,268 | (42.1 |

) | ||||||||

Income tax expense |

1,192 | 1,244 | 4.2 |

|||||||||

Share of result of associates |

(105 | ) | (129 | ) | (18.6 |

) | ||||||

Exceptional share of results of associates |

- |

1,143 | - |

|||||||||

Profit from operations |

6,965 |

7,000 |

(0.5 |

) | ||||||||

Exceptional items |

107 | 105 | (1.9 | ) | ||||||||

Profit from operations, before exceptional items (2) |

7,072 |

7,105 |

(0.5 |

) | ||||||||

Depreciation, amortization and impairment |

2,596 | 2,477 | (4.8 |

) | ||||||||

Normalized EBITDA (3) |

9,668 |

9,583 |

0.9 |

|||||||||

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

| (2) | Profit from operations, before exceptional items is a non-IFRS measure. See “Item 5. Operating and Financial Review and Results of Operations—Results of Operations—Year Ended 31 December 2022 Compared to Year Ended 31 December 2021—Normalized EBITDA” of our 2022 Annual Report for additional information on our definition and use of Profit from operations, before exceptional items. |

| (3) | Normalized EBITDA is a non-IFRS measure. See “Item 5. Operating and Financial Review and Results of Operations—Results of Operations—Year Ended 31 December 2022 Compared to Year Ended 31 December 2021—Normalized EBITDA” of our 2022 Annual Report for additional information on our definition and use of Normalized EBITDA. |

Six-month period ended 30 June 2023 |

Six-month period ended 30 June 2022 |

Change |

||||||||||||||

(USD million) |

(%) (1) |

|||||||||||||||

Net interest expense |

(1,630) | (1,683) | 3.1 | |||||||||||||

Net interest on net defined benefit liabilities |

(42) | (37) | (13.5) | |||||||||||||

Accretion expense |

(385) | (336) | (14.6) | |||||||||||||

Net interest income on Brazilian tax credits |

78 | 113 | (31.0) | |||||||||||||

Other financial results |

(540) | (501) | (7.8) | |||||||||||||

Net finance cost before exceptional finance results (2) |

(2,520) |

(2,444) |

(3.1) |

|||||||||||||

Mark-to-market (2) |

(703) | 296 | - | |||||||||||||

Gain/(loss) on bond redemption and other |

- | (120) | - | |||||||||||||

Exceptional net finance income/(cost) (2) |

(703) |

176 |

- |

|||||||||||||

Net finance income/(cost) |

(3,223) |

(2,268) |

(42.1) |

|||||||||||||

| (1) | The percentage change reflects the improvement (or worsening) of results for the period as a result of the change in each item. |

| (2) | The financial information for the six-month period ended 30 June 2022 has been amended to conform to the basis of presentation for the six-month period ended 30 June 2023 to reflect the change in classification of mark-to-market |

Six-month period ended 30 June 2023 |

Six-month period ended 30 June 2022 |

|||||||||

Share price at the start of the six-month period (in euro) |

56.27 | 53.17 | ||||||||

Share price at the end of the six-month period (in euro) |

51.83 | 51.36 | ||||||||

Number of derivative equity instruments at the end of the period (in millions) |

100.5 | 100.5 | ||||||||

Six-month period ended 30 June 2023 |

Six-month period ended 30 June 2022 |

|||||||||

(USD million) |

||||||||||

Profit attributable to equity holders of AB InBev |

1,977 |

1,692 |

||||||||

Exceptional items, before taxes |

107 | 105 | ||||||||

Exceptional net finance cost, before taxes (1) |

703 | (176) | ||||||||

Exceptional share of results of associates |

- | 1,143 | ||||||||

Exceptional taxes |

(51) | (69) | ||||||||

Exceptional non-controlling interest |

(9) | 3 | ||||||||

Hyperinflation impacts |

35 | (26) | ||||||||

Underlying profit, attributable to equity holders of AB InBev (2) |

2,762 |

2,672 |

||||||||

| (1) | The financial information for the six-month period ended 30 June 2022 has been amended to conform to the basis of presentation for the six-month period ended 30 June 2023 to reflect the change in classification of mark-to-market |

| (2) | Underlying profit, attributable to equity holders of AB InBev is a non-IFRS measure. See “Item 5. Operating and Financial Review and Results of Operations—Results of Operations—Year Ended 31 December 2022 Compared to Year Ended 31 December 2021—Profit Attributable to Our Equity Holders” of our 2022 Annual Report for additional information on our definition and use of Underlying profit attributable to equity holders of AB InBev. |

Six-month period ended 30 June 2023 |

Six-month period ended 30 June 2022 |

|||||||||||

(USD per share) |

||||||||||||

Basic earnings per share |

0.98 |

0.84 |

||||||||||

Exceptional items, before taxes |

0.05 | 0.05 | ||||||||||

Exceptional net finance cost, before taxes (1) |

0.35 | (0.09) | ||||||||||

Exceptional share of results of associates |

- | 0.57 | ||||||||||

Exceptional taxes |

(0.03) | (0.03) | ||||||||||

Hyperinflation accounting impacts in EPS |

0.02 | (0.01) | ||||||||||

Underlying EPS (2) |

1.37 |

1.33 |

||||||||||

| (1) | The financial information for the six-month period ended 30 June 2022 has been amended to conform to the basis of presentation for the six-month period ended 30 June 2023 to reflect the change in classification of mark-to-market |

| (2) | Underlying EPS is a non-IFRS measure. See “Item 5. Operating and Financial Review—E. Results of Operations—Year Ended 31 December 2022 Compared to the Year Ended 31 December 2021—Profit Attributable to Our Equity Holders” of our 2022 Annual Report for additional information on our definition and use of Underlying EPS. |

Six-month period ended |

||||||||||||

30 June 2023 |

30 June 2022 |

|||||||||||

U.S. dollar |

27.3% | 29.3% | ||||||||||

Brazilian real |

14.5% | 13.7% | ||||||||||

Mexican peso |

12.3% | 10.3% | ||||||||||

Chinese yuan |

9.6% | 9.4% | ||||||||||

Euro |

5.5% | 5.5% | ||||||||||

Colombian peso |

3.6% | 4.1% | ||||||||||

South African rand |

3.6% | 3.9% | ||||||||||

Argentinean peso (1) |

3.4% | 3.3% | ||||||||||

Canadian dollar |

3.2% | 3.4% | ||||||||||

Peruvian nuevo sol |

3.1% | 2.8% | ||||||||||

Dominican peso |

2.1% | 2.0% | ||||||||||

Pound sterling |

1.9% | 2.1% | ||||||||||

South Korean won |

1.9% | 2.1% | ||||||||||

Other |

7.9% | 8.0% | ||||||||||

| (1) | Hyperinflation accounting was adopted starting from the September year-to-date |

Six-month period ended 30 June 2023 |

Six-month period ended 30 June 2022 |

|||||||||||

(USD million) |

||||||||||||

Cash flow from operating activities |

1,597 | 2,182 | ||||||||||

Cash flow from/(used in) investing activities |

(2,061) | (1,917) | ||||||||||

Cash flow from/(used in) financing activities |

(2,823) | (5,392) | ||||||||||

Net increase/(decrease) in cash and cash equivalents |

(3,287) |

(5,128) |

||||||||||

Six-month period ended 30 June 2023 |

Six-month period ended 30 June 2022 |

|||||||||||

(USD million) |

||||||||||||

Profit |

2,655 | 2,474 | ||||||||||

Interest, taxes and non-cash items included in profit |

7,512 | 7,015 | ||||||||||

Cash flow from operating activities before changes in working capital and provisions |

10,167 |

9,489 |

||||||||||

Change in working capital |

(4,615) | (3,339) | ||||||||||

Pension contributions and use of provisions |

(192) | (195) | ||||||||||

Interest and taxes (paid)/received |

(3,806) | (3,823) | ||||||||||

Dividends received |

43 | 50 | ||||||||||

Cash flow from operating activities |

1,597 |

2,182 |

||||||||||

Six-month period ended 30 June 2023 |

Six-month period ended 30 June 2022 |

|||||||||||

(USD million) |

||||||||||||

Net capital expenditure (1) |

(2,063) | (1,939) | ||||||||||

Sale/(acquisition) of subsidiaries, net of cash disposed/ acquired of |

(8) | (44) | ||||||||||

Proceeds from sale/(acquisition) of other assets |

10 | 66 | ||||||||||

Cash flow from / (used in) investing activities |

(2,061) |

(1,917) |

||||||||||

| (1) | Net capital expenditure consists of acquisitions of plant, property and equipment and of intangible assets, minus proceeds from sale. |

Six-month periodended 30 June 2023 |

Six-month periodended 30 June 2022 | |||||||||||

(USD million) | ||||||||||||

Dividends paid |

(1,923 | ) | (1,276 | ) | ||||||||

Net (payments on)/proceeds from borrowings |

155 | (3,452 | ) | |||||||||

Payments of lease liabilities |

(359 | ) | (286 | ) | ||||||||

Other (including purchase of non-controlling interests) |

(696 | ) | (378 | ) | ||||||||

Cash flow from / (used in) financing activities |

(2,823 |

) |

(5,392 |

) | ||||||||

Six-month periodended 30 June 2023¹ |

Year ended 31 December 2022² |

|||||||||||

USD million |

USD million |

|||||||||||

Income Statement Data |

||||||||||||

Revenue |

7,198 | 15,231 | ||||||||||

Gross profit |

3,675 | 8,183 | ||||||||||

Profit for the period |

66 | 975 | ||||||||||

Six-month periodended 30 June 2023 |

Year ended 31 December 2022 |

|||||||||||

USD million |

USD million |

|||||||||||

Statement of Financial Position Data |

||||||||||||

Due from non-guarantor subsidiaries |

95,048 | 99,031 | ||||||||||

Other non-current assets |

62,182 | 61,978 | ||||||||||

Non-current assets |

157,230 |

161,009 |

||||||||||

Due from non-guarantor subsidiaries |

10,064 | 3,595 | ||||||||||

Other current assets |

7,044 | 13,367 | ||||||||||

Current assets |

17,108 |

16,962 |

||||||||||

Due to non-guarantor subsidiaries |

23,547 | 24,657 | ||||||||||

Other non-current liabilities |

83,889 | 84,502 | ||||||||||

Non-current liabilities |

107,435 |

109,159 |

||||||||||

Due to non-guarantor subsidiaries |

10,824 | 12,894 | ||||||||||

Other current liabilities |

20,031 | 22,668 | ||||||||||

Current liabilities |

30,855 |

35,562 |

||||||||||

| (1) | For the six-month period ended 30 June 2023, revenue, gross profit and profit of the period includes USD 104 million, USD (225) million and USD 1,130 million of intercompany transactions with non-guarantor subsidiaries and related parties, respectively. |

| (2) | For the year ended 31 December 2022, revenue, gross profit and profit of the period includes USD 299 million, USD (439) million and USD 25 million of intercompany transactions with non-guarantor subsidiaries and related parties, respectively. |

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 4 | ||||

| 5 | ||||

| 6 |

For the six-month period ended 30 June |

||||||||||

Million US dollar, except earnings per shares in US dollar |

No tes |

20 23 |

2022¹ | |||||||

| Revenue |

||||||||||

| Cost of sales |

( |

( |

||||||||

| Gross profit |

||||||||||

| Distribution expenses |

( |

( |

||||||||

| Sales and marketing expenses |

( |

( |

||||||||

| Administrative expenses |

( |

( |

||||||||

| Other operating income/(expenses) |

||||||||||

| Exceptional costs above profit from operations |

7 | ( |

( |

|||||||

| Profit from operations |

||||||||||

| |

|

|

|

|

|

|

|

|

|

|

| Finance cost |

8 | ( |

( |

|||||||

| Finance income |

8 | |||||||||

| Net finance income/(cost) |

( |

( |

||||||||

| |

|

|

|

|

|

|

|

|

|

|

| Share of result of associates |

13 | |||||||||

| Exceptional share of results of associates |

7 / 13 | - | ( |

|||||||

| Profit before tax |

||||||||||

| |

|

|

|

|

|

|

|

|

|

|

| Income tax expense |

9 | ( |

( |

|||||||

| Profit of the period |

||||||||||

| Profit of the period attributable to: |

||||||||||

| Equity holders of AB InBev |

||||||||||

| Non-controlling interest |

||||||||||

| Basic earnings per share |

16 | |||||||||

| Diluted earnings per share |

16 | |||||||||

For the six-month period ended 30 June |

||||||||||

Million US dollar |

Notes |

2023 |

2022 |

|||||||

| Profit of the period |

||||||||||

| Other comprehensive income/(loss): items that will not be reclassified to profit or loss: |

||||||||||

| Re-measurements of post-employment benefits |

16 | |||||||||

| Other comprehensive income/(loss): items that may be reclassified subsequently to profit or loss: |

||||||||||

| Exchange differences on translation of foreign operations |

16 | |||||||||

| Effective portion of changes in fair value of net investment hedges |

( |

( |

||||||||

| Cash flow hedges recognized in equity |

( |

|||||||||

| Cash flow hedges reclassified from equity to profit or loss |

( |

( |

||||||||

| Other comprehensive income/(loss), net of tax |

||||||||||

| Total comprehensive income/(loss) |

||||||||||

| Attributable to: |

||||||||||

| Equity holders of AB InBev |

||||||||||

| Non-controlling interest |

||||||||||

Million US dollar |

Notes |

30 June 2023 |

31 December 2022 | |||||||

| ASSETS |

||||||||||

| Non-current assets |

||||||||||

| Property, plant and equipment |

10 | |||||||||

| Goodwill |

11 | |||||||||

| Intangible assets |

12 | |||||||||

| Investments in associates |

13 | |||||||||

| Investment securities |

15 | |||||||||

| Deferred tax assets |

||||||||||

| Employee benefits |

||||||||||

| Income tax receivables |

||||||||||

| Derivatives |

19 | |||||||||

| Trade and other receivables |

14 | |||||||||

| Total non-current assets |

||||||||||

| Current assets |

||||||||||

| Investment securities |

15 | |||||||||

| Inventories |

||||||||||

| Income tax receivables |

||||||||||

| Derivatives |

19 | |||||||||

| Trade and other receivables |

14 | |||||||||

| Cash and cash equivalents |

15 | |||||||||

| Assets classified as held for sale |

||||||||||

| Total current assets |

||||||||||

| Total assets |

||||||||||

| EQUITY AND LIABILITIES |

||||||||||

| Equity |

||||||||||

| Issued capital |

16 | |||||||||

| Share premium |

||||||||||

| Reserves |

||||||||||

| Retained earnings |

||||||||||

| Equity attributable to equity holders of AB InBev |

||||||||||

| Non-controlling interests |

||||||||||

| Total equity |

||||||||||

| Non-current liabilities |

||||||||||

| Interest-bearing loans and borrowings |

17 | |||||||||

| Employee benefits |

||||||||||

| Deferred tax liabilities |

||||||||||

| Income tax payables |

||||||||||

| Derivatives |

19 | |||||||||

| Trade and other payables |

||||||||||

| Provisions |

||||||||||

| Total non-current liabilities |

||||||||||

| Current liabilities |

||||||||||

| Bank overdrafts |

15 | |||||||||

| Interest-bearing loans and borrowings |

17 | |||||||||

| Income tax payables |

||||||||||

| Derivatives |

19 | |||||||||

| Trade and other payables |

||||||||||

| Provisions |

||||||||||

| Total current liabilities |

||||||||||

| Total equity and liabilities |

||||||||||

Attributable to equity holders of AB InBev |

||||||||||||||||||||||||||||||||||||||

Issued |

Share |

Treasury |

Other comprehensive income |

Retained |

Non- controlling |

Total | ||||||||||||||||||||||||||||||||

Million US dollar |

Notes |

Capital |

premium |

shares |

Reserves |

reserves |

earnings |

Total |

interest |

Equity | ||||||||||||||||||||||||||||

| As per 1 January 2022 |

( |

( |

||||||||||||||||||||||||||||||||||||

| Profit of the period |

- | - | - | - | - | |||||||||||||||||||||||||||||||||

| Other comprehensive income/(loss) |

16 | - | - | - | - | - | ( |

|||||||||||||||||||||||||||||||

| Total comprehensive income/(loss) |

- |

- |

- |

- |

||||||||||||||||||||||||||||||||||

| Dividends |

- | - | - | - | - | ( |

( |

( |

( |

|||||||||||||||||||||||||||||

| Treasury shares |

- | - | - | - | ( |

- | ||||||||||||||||||||||||||||||||

| Share-based payments |

18 | - | - | - | - | - | ||||||||||||||||||||||||||||||||

| Hyperinflation monetary adjustments |

- | - | - | - | - | |||||||||||||||||||||||||||||||||

| Scope and other changes |

- | - | - | - | - | ( |

( |

( |

( |

|||||||||||||||||||||||||||||

| As per 30 June 2022 |

( |

( |

||||||||||||||||||||||||||||||||||||

Attributable to equity holders of AB InBev |

||||||||||||||||||||||||||||||||||||||

Issued |

Share |

Treasury |

Other comprehensive income |

Retained |

Non- controlling |

Total | ||||||||||||||||||||||||||||||||

Million US dollar |

Notes |

Capital |

premium |

shares |

Reserves |

reserves |

earnings |

Total |

interest |

Equity | ||||||||||||||||||||||||||||

| As per 1 January 2023 |

( |

( |

||||||||||||||||||||||||||||||||||||

| Profit of the period |

- | - | - | - | - | |||||||||||||||||||||||||||||||||

| Other comprehensive income/(loss) |

16 | - | - | - | - | - | ( |

|||||||||||||||||||||||||||||||

| Total comprehensive income/(loss) |

- |

- |

- |

- |

||||||||||||||||||||||||||||||||||

| Dividends |

- | - | - | - | - | ( |

( |

( |

( |

|||||||||||||||||||||||||||||

| Treasury shares |

- | - | - | - | ( |

- | ||||||||||||||||||||||||||||||||

| Share-based payments |

18 | - | - | - | - | - | ||||||||||||||||||||||||||||||||

| Hyperinflation monetary adjustments |

- | - | - | - | - | |||||||||||||||||||||||||||||||||

| Scope and other changes |

- | - | - | - | - | ( |

( |

( |

||||||||||||||||||||||||||||||

| As per 30 June 2023 |

( |

( |

||||||||||||||||||||||||||||||||||||

For the six-month period ended 30 June |

||||||||||

Million US dollar |

Notes |

2023 |

2022¹ | |||||||

| OPERATING ACTIVITIES |

||||||||||

| Profit of the period |

||||||||||

| Depreciation, amortization and impairment |

||||||||||

| Net finance cost/(income) |

8 | |||||||||

| Equity-settled share-based payment expense |

18 | |||||||||

| Income tax expense |

9 | |||||||||

| Other non-cash items |

( |

|||||||||

| Share of result of associates |

13 | ( |

||||||||

| Cash flow from operating activities before changes in working capital and use of provisions |

||||||||||

| Decrease/(increase) in trade and other receivables |

( |

( |

||||||||

| Decrease/(increase) in inventories |

( |

( |

||||||||

| Increase/(decrease) in trade and other payables |

( |

( |

||||||||

| Pension contributions and use of provisions |

( |

( |

||||||||

| Cash generated from operations |

||||||||||

| Interest paid |

( |

( |

||||||||

| Interest received |

||||||||||

| Dividends received |

||||||||||

| Income tax paid |

( |

( |

||||||||

| Cash flow from/(used in) operating activities |

||||||||||

| INVESTING ACTIVITIES |

||||||||||

| Acquisition of property, plant and equipment and of intangible assets |

10/12 | ( |

( |

|||||||

| Proceeds from sale of property, plant and equipment and of intangible assets |

||||||||||

| Sale/(acquisition) of subsidiaries, net of cash disposed/ acquired of |

( |

( |

||||||||

| Proceeds from sale/(acquisition) of other assets |

||||||||||

| Cash flow from/(used in) investing activities |

( |

( |

||||||||

| FINANCING ACTIVITIES |

||||||||||

| Sale/(purchase) of non-controlling interests |

( |

( |

||||||||

| Proceeds from borrowings |

17 | |||||||||

| Payments on borrowings |

17 | ( |

( |

|||||||

| Cash net finance (cost)/income other than interests |

( |

( |

||||||||

| Payment of lease liabilities |

( |

( |

||||||||

| Dividends paid |

( |

( |

||||||||

| Cash flow from/(used in) financing activities |

( |

( |

||||||||

| Net increase/(decrease) in cash and cash equivalents |

( |

( |

||||||||

| Cash and cash equivalents less bank overdrafts at beginning of year |

||||||||||

| Effect of exchange rate fluctuations |

( |

|||||||||

| Cash and cash equivalents less bank overdrafts at end of period |

15 |

|||||||||

Note |

||||

| Corporate information |

1 |

|||

| Statement of compliance |

2 |

|||

| Summary of significant accounting policies |

3 |

|||

| Use of estimates and judgments |

4 |

|||

| Segment reporting |

5 |

|||

| Acquisitions and disposals of subsidiaries |

6 |

|||

| Exceptional items |

7 |

|||

| Finance cost and income |

8 |

|||

| Income taxes |

9 |

|||

| Property, plant and equipment |

10 |

|||

| Goodwill |

11 |

|||

| Intangible Assets |

12 |

|||

| Investments in associates |

13 |

|||

| Trade and other receivables |

14 |

|||

| Cash and cash equivalents and investment securities |

15 |

|||

| Changes in equity and earnings per share |

16 |

|||

| Interest-bearing loans and borrowings |

17 |

|||

| Share-based payments |

18 |

|||

| Risks arising from financial instruments |

19 |

|||

| Collateral and contractual commitments for the acquisition of property, plant and equipment, loans to customers and other |

20 |

|||

| Contingencies |

21 |

|||

| Related parties |

22 |

|||

1. |

Corporate information |

2. |

Statement of compliance |

3. |

Summary of s ignificant accounting policies |

Closing rate |

Average rate |

|||||||||||||||

1 US dollar equals: |

30 June 2023 |

31 December 2022 |

30 June 2023 |

30 June 2022 |

||||||||||||

Argentinean peso |

- | - | ||||||||||||||

Brazilian real |

||||||||||||||||

Canadian dollar |

||||||||||||||||

Colombian peso |

||||||||||||||||

Chinese yuan |

||||||||||||||||

Euro |

||||||||||||||||

Mexican peso |

||||||||||||||||

Pound sterling |

||||||||||||||||

Peruvian nuevo sol |

||||||||||||||||

South Korean won |

||||||||||||||||

South African rand |

||||||||||||||||

4. |

Use of estimates and judgments |

5. |

Segment reporting |

North America |

Middle Americas |

South America |

EMEA |

Asia Pacific |

Global Export and Holding companies |

AB InBev Worldwide |

||||||||||||||||||||||||||||||||||||||||||||||||||

2023 |

2022 |

2023 |

2022 |

2023 |

2022 |

2023 |

2022 |

2023 |

2022 |

2023 |

2022 |

2023 |

2022 |

|||||||||||||||||||||||||||||||||||||||||||

Volume |

- |

- |

||||||||||||||||||||||||||||||||||||||||||||||||||||||

Revenue |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Profit from operations |

( |

( |

||||||||||||||||||||||||||||||||||||||||||||||||||||||

Net finance income/(cost) |

( |

( |

||||||||||||||||||||||||||||||||||||||||||||||||||||||

Share of results of associates |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Exceptional share of results of associates |

( |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||

Income tax expense |

( |

( |

||||||||||||||||||||||||||||||||||||||||||||||||||||||

Profit |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Segment assets (non-current) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Gross capex |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

6. |

Acquisi ti ons and disposals of subsidiaries |

7. |

Exceptional items |

For the six-month period ended 30 June Million US dollar |

2023 |

2022¹ | ||||||

COVID-19 costs |

( |

|||||||

Restructuring |

( |

( |

||||||

Business and asset disposal (including impairment losses) |

( |

|||||||

Legal costs |

( |

|||||||

AB InBev Efes related costs |

( |

|||||||

Impact on profit from operations |

( |

( |

||||||

Exceptional net finance income/(cost) |

( |

|||||||

Exceptional share of results of associates |

( |

|||||||

Exceptional taxes |

||||||||

Exceptional non-controlling interest |

( |

|||||||

Net impact on profit |

( |

( |

||||||

8. |

Finance cost and income |

2023 |

2022¹ |

|||||||||||||||||||||||||||

Million US dollar |

Finance cost |

Finance income |

Net |

Finance cost |

Finance income |

Net |

||||||||||||||||||||||

Interest income/(expense) |

( |

( |

) | ( |

( |

) | ||||||||||||||||||||||

Net interest on net defined benefit liabilities |

( |

- | ( |

) | ( |

- | ( |

) | ||||||||||||||||||||

Accretion expense |

( |

- | ( |

) | ( |

- | ( |

) | ||||||||||||||||||||

Net interest income on Brazilian tax credits |

- | - | ||||||||||||||||||||||||||

Other financial results |

( |

( |

) | ( |

( |

) | ||||||||||||||||||||||

Finance income/(cost) excluding exceptional items |

( |

( |

) |

( |

( |

) | ||||||||||||||||||||||

Exceptional finance income/(cost) |

( |

- | ( |

) | ( |

|||||||||||||||||||||||

Finance income/(cost) |

( |

( |

) |

( |

( |

) | ||||||||||||||||||||||

2023 |

2022¹ |

|||||||||||||||||||||||||||

Million US dollar |

Finance cost |

Finance income |

Net |

Finance cost |

Finance income |

Net |

||||||||||||||||||||||

Net foreign exchange gains/(losses) |

( |

- | ( |

) | ( |

- | ( |

) | ||||||||||||||||||||

Net gains/(losses) on hedging instruments |

( |

- | ( |

) | ( |

- | ( |

) | ||||||||||||||||||||

Hyperinflation monetary adjustments |

- | - | ||||||||||||||||||||||||||

Other financial income/(cost), including bank fees and taxes |

( |

( |

) | ( |

( |

) | ||||||||||||||||||||||

Other financial results |

( |

( |

) |

( |

( |

) | ||||||||||||||||||||||

| • | ( mark-to-market |

| • | In the six-month period ended 30 June 2022, ( |

9. |

Income taxes |

For the six-month period ended 30 June Million US dollar |

2023 |

2022 |

||||||

| Current tax expense |

( |

) | ( |

|||||

| Deferred tax (expense)/income |

||||||||

| Total income tax expense in the income statement |

( |

) |

( |

|||||

For the six-month period ended 30 June Million US dollar |

2023 |

2022 |

||||||

| Profit/(loss) before tax |

||||||||

| Deduct share of results of associates |

||||||||

| Deduct exceptional share of results of associates |

- | ( |

||||||

| Profit before tax and before share of results of associates |

||||||||

| Adjustments to the tax basis |

||||||||

| Government incentives |

( |

( |

||||||

| Non-deductible/(non-taxable) mark-to-market |

( |

|||||||

| Other expenses not deductible for tax purposes |

||||||||

| Other non-taxable income |

( |

( |

||||||

| Adjusted tax basis |

||||||||

| Aggregate weighted nominal tax rate |

||||||||

| Tax at aggregated nominal tax rate |

( |

( |

||||||

| Adjustments on tax expense |

||||||||

| Recognition/(de-recognition) of deferred tax assets on tax losses (carried forward) |

( |

( |

||||||

| (Underprovided)/overprovided in prior years |

( |

|||||||

| Deductions from interest on equity |

||||||||

| Deductions from goodwill and other tax deductions |

||||||||

| Change in tax rate |

- | |||||||

| Withholding taxes |

( |

( |

||||||

| Other tax adjustments |

( |

( |

||||||

| Total tax expense |

( |

( |

||||||

| Effective tax rate |

||||||||

10. |

Property, plant and equipment |

Million US dollar |

30 June 2023 |

31 December 2022 |

||||||

| Property, plant and equipment owned |

||||||||

| Property, plant and equipment leased (right-of-use |

||||||||

| Total property, plant and equipment |

||||||||

30 June 2023 |

31 December 2022 |

|||||||||||||||||||

Million US dollar |

Land and buildings |

Plant and equipment, fixtures and fittings |

Under construction |

Total |

Total |

|||||||||||||||

| Acquisition cost |

||||||||||||||||||||

| Balance at end of previous year |

||||||||||||||||||||

| Effect of movements in foreign exchange |

( |

|||||||||||||||||||

| Acquisitions |

||||||||||||||||||||

| Disposals through sale and derecognition |

( |

( |

( |

( |

||||||||||||||||

| Disposals through the sale of subsidiaries |

- |

( |

||||||||||||||||||

| Transfer (to)/from other asset categories and other movements¹ |

( |

|||||||||||||||||||

| Balance at end of the period |

||||||||||||||||||||

| Depreciation and impairment losses |

||||||||||||||||||||

| Balance at end of previous year |

( |

( |

- |

( |

( |

|||||||||||||||

| Effect of movements in foreign exchange |

( |

( |

- | ( |

||||||||||||||||

| Depreciation |

( |

( |

- | ( |

( |

|||||||||||||||

| Disposals through sale and derecognition |

- | |||||||||||||||||||

| Disposals through the sale of subsidiaries |

- | |||||||||||||||||||

| Impairment losses |

( |

( |

( |

( |

||||||||||||||||

| Transfer to/(from) other asset categories and other movements¹ |

( |

( |

( |

( |

||||||||||||||||

| Balance at end of the period |

( |

( |

- |

( |

( |

|||||||||||||||

| Carrying amount |

||||||||||||||||||||

| at 31 December 2022 |

||||||||||||||||||||

| at 30 June 2023 |

- |

|||||||||||||||||||

30 June 2023 |

||||||||||||

Million US dollar |

Land and buildings |

Machinery, equipment and other |

Total |

|||||||||

Net carrying amount at June 30 |

||||||||||||

Depreciation for the period ended June 30 |

( |

) | ( |

( |

||||||||

31 December 2022 |

||||||||||||

Million US dollar |

Land and buildings |

Machinery, equipment and other |

Total |

|||||||||

Net carrying amount at 31 December |

||||||||||||

Depreciation for the year ended 31 December |

( |

) | ( |

( |

||||||||

11. |

Goodwill |

Million US dollar |

30 June 2023 |

31 December 2022 |

||||||

Acquisition cost |

||||||||

Balance at end of previous year |

||||||||

Effect of movements in foreign exchange |

( |

|||||||

Disposals through the sale of subsidiaries |

- | ( |

||||||

Transfers (to)/from other asset categories |

( |

( |

||||||

Hyperinflation monetary adjustments |

||||||||

Balance at end of the period |

||||||||

Impairment losses |

||||||||

Balance at end of previous year |

( |

( |

||||||

Effect of movements in foreign exchange |

||||||||

Balance at end of the period |

( |

( |

||||||

Carrying amount |

||||||||

Balance at end of the period |

||||||||

Million US dollar |

30 June 2023 |

31 December 2022 |

||||||

United States |

||||||||

Rest of North America |

||||||||

Mexico |

||||||||

Colombia |

||||||||

Rest of Middle Americas |

||||||||

Brazil |

||||||||

Rest of South America |

||||||||

Europe |

||||||||

South Africa |

||||||||

Rest of Africa |

||||||||

China |

||||||||

Rest of Asia Pacific |

||||||||

Global Export and Holding Companies |

||||||||

Total carrying amount of goodwill |

||||||||

12. |

Intangible assets |

30 June 2023 |

31 December 2022 |

|||||||||||||||||||||||

Million US dollar |

Brands |

Commercial intangibles |

Software |

Other |

Total |

Total |

||||||||||||||||||

Acquisition cost |

||||||||||||||||||||||||

Balance at end of previous year |

||||||||||||||||||||||||

Effect of movements in foreign exchange |

( |

( |

||||||||||||||||||||||

Acquisitions and expenditures |

||||||||||||||||||||||||

Disposals through sale and derecognition |

( |

- | ( |

( |

( |

( |

||||||||||||||||||

Transfer (to)/from other asset categories and other movements¹ |

( |

|||||||||||||||||||||||

Balance at end of period |

||||||||||||||||||||||||

Amortization and impairment losses |

||||||||||||||||||||||||

Balance at end of previous year |

( |

( |

( |

( |

( |

( |

||||||||||||||||||

Effect of movements in foreign exchange |

- | ( |

( |

( |

( |

|||||||||||||||||||

Amortization |

- | ( |

( |

( |

( |

( |

||||||||||||||||||

Impairment |

- | - | ( |

- | ( |

( |

||||||||||||||||||

Disposals through sale and derecognition |

- | - | ||||||||||||||||||||||

Transfer to/(from) other asset categories and other movements¹ |

- | ( |

( |

( |

( |

( |

||||||||||||||||||

Balance at end of period |

( |

( |

( |

( |

( |

( |

||||||||||||||||||

Carrying value |

||||||||||||||||||||||||

at 31 December 2022 |

||||||||||||||||||||||||

at 30 June 2023 |

||||||||||||||||||||||||

13. |

Investments in associates |

2023 |

2022 |

|||||||||||||||||||||||

Million US dollar |

Castel |

Anadolu Efes |

AB InBev Efes |

Castel |

Anadolu Efes |

|||||||||||||||||||

Balance at 1 January |

||||||||||||||||||||||||

Effect of movements in foreign exchange |

( |

- | ( |

( |

||||||||||||||||||||

Dividends received |

- | ( |

- | - | ( |

|||||||||||||||||||

Share of results of associates |

- | ( |

||||||||||||||||||||||

Exceptional share of results of associates |

- | - | ( |

- | - | |||||||||||||||||||

Balance at 30 June |

- |

|||||||||||||||||||||||

14. |

Trade and other receivables |

Million US dollar |

30 June 2023 |

31 December 2022 | ||||||

Cash deposits for guarantees |

||||||||

Loans to customers |

||||||||

Tax receivable, other than income tax |

||||||||

Brazilian tax credits and interest receivables |

||||||||

Trade and other receivables |

||||||||

Non-current trade and other receivables |

||||||||

Trade receivables and accrued income |

||||||||

Interest receivables |

||||||||

Tax receivable, other than income tax |

||||||||

Loans to customers |

||||||||

Prepaid expenses |

||||||||

Other receivables |

||||||||

Current trade and other receivables |

||||||||

Of which: neither |

Of which not impaired as of the reporting date and past due |

|||||||||||||||||||||||

Net carrying amount as of 30 June 2023 |

impaired nor past due on the reporting date |

Less than 30 days |

Between 30 and 59 days |

Between 60 and 89 days |

More than 90 days |

|||||||||||||||||||

Trade receivables and accrued income |

||||||||||||||||||||||||

Loans to customers |

- | |||||||||||||||||||||||

Interest receivable |

- | - | - | - | ||||||||||||||||||||

Other receivables |

||||||||||||||||||||||||

Net carrying |

Of which: neither |

Of which not impaired as of the reporting date and past due |

||||||||||||||||||||||

amount as of 31 December 2022 |

impaired nor past due on the reporting date |

Less than 30 days |

Between 30 and 59 days |

Between 60 and 89 days |

More than 90 days |

|||||||||||||||||||

Trade receivables and accrued income |

||||||||||||||||||||||||

Loans to customers |

- | |||||||||||||||||||||||

Interest receivable |

- | - | - | - | ||||||||||||||||||||

Other receivables |

||||||||||||||||||||||||

15. |

Cash and cash equivalents and investment securities |

Million US dollar |

30 June 2023 |

31 December 2022 |

||||||

Short-term bank deposits |

||||||||

Cash and bank accounts |

||||||||

Cash and cash equivalents |

||||||||

Bank overdrafts |

( |

) |

( |

) | ||||

Cash and cash equivalents in the statement of cash flows |

||||||||

Million US dollar |

30 June 2023 |

31 December 2022 |

||||||

Investment in unquoted companies |

||||||||

Investment on debt securities |

||||||||

Non-current investments |

||||||||

Investment on debt securities |

||||||||

Current investments |

||||||||

16. |

Changes in equity and earnings per share |

Issued capital |

||||||||

Issued capital |

Million shares |

Million US dollar |

||||||

At the end of the previous year |

||||||||

Changes during the period |

||||||||

Of which: |

||||||||

Ordinary shares |

||||||||

Restricted shares |

||||||||

Treasury shares |

Result on the use of treasury shares |

|||||||||||

Treasury shares |

Million shares |

Million US dollar |

Million US dollar |

|||||||||

At the end of the previous year |

( |

) | ( |

) | ||||||||

Changes during the period |

( |

) | ( |

) | ||||||||

At the end of the current period |

( |

) |

( |

) | ||||||||

Million US dollar |

Translation Reserves |

Hedging reserves |

Post- employment benefits |

Total OCI Reserves |

||||||||||||

As per 1 January 2023 |

( |

( |

( |

|||||||||||||

Other comprehensive income/(loss) |

||||||||||||||||

Exchange differences on translation of foreign operations (gains/(losses)) |

- | - | ||||||||||||||

Cash flow hedges |

- | ( |

- | ( |

||||||||||||

Re-measurements of post-employment benefits |

- | - | ||||||||||||||

Other comprehensive income/(loss) |

( |

|||||||||||||||

As per 30 June 2023 |

( |

( |

( |

( |

||||||||||||

Million US dollar |

Translation Reserves |

Hedging reserves |

Post- employment benefits |

Total OCI Reserves |

||||||||||||

As per 1 January 2022 |

( |

( |

( |

|||||||||||||

Other comprehensive income/(loss) |

||||||||||||||||

Exchange differences on translation of foreign operations (gains/(losses)) |

- | - | ||||||||||||||

Cash flow hedges |

- | ( |

- | ( |

||||||||||||

Re-measurements of post-employment benefits |

- | - | - | - | ||||||||||||

Other comprehensive income/(loss) |

( |

- |

||||||||||||||

As per 30 June 2022 |

( |

( |

( |

|||||||||||||

Million shares |

2023 |

2022 |

||||||

Issued ordinary and restricted shares at 1 January, net of treasury shares |

||||||||

Effect of stock lending |

||||||||

Effect of delivery of treasury shares |

||||||||

Weighted average number of ordinary and restricted shares at 30 June |

||||||||

Million shares |

2023 |

2022 |

||||||

Weighted average number of ordinary and restricted shares at 30 June |

||||||||

Effect of share options, warrants and restricted stock units |

||||||||

Weighted average number of ordinary and restricted shares (diluted) at 30 June |

||||||||

For the six-month period ended 30 June |

||||||||

Million US dollar |

2023 |

2022¹ | ||||||

Profit attributable to equity holders of AB InBev |

||||||||

Net impact of exceptional items on profit (refer to Note 7) |

||||||||

Profit before exceptional items, attributable to equity holders of AB InBev |

||||||||

Hyperinflation impacts |

( |

|||||||

Underlying profit |

||||||||

For the six-month period ended 30 June |

||||||||

Million US dollar |

2023 |

2022 | ||||||

Profit attributable to equity holders of AB InBev |

||||||||

Weighted average number of ordinary and restricted shares |

||||||||

Basic EPS |

||||||||

Underlying profit |

||||||||

Weighted average number of ordinary and restricted shares |

||||||||

Underlying EPS |

||||||||

Profit attributable to equity holders of AB InBev |

||||||||

Weighted average number of ordinary and restricted shares (diluted) |

||||||||

Diluted EPS |

||||||||

17. |

Interest-bearing loans and borrowings |

Million US dollar |

30 June 2023 |

31 December 2022 | ||||||

Unsecured bond issues |

||||||||

Lease liabilities |

||||||||

Unsecured other loans |

||||||||

Secured bank loans |

||||||||

Non-current interest-bearing loans and borrowings |

||||||||

Unsecured bond issues |

||||||||

Lease liabilities |

||||||||

Secured bank loans |

||||||||

Unsecured bank loans |

||||||||

Unsecured other loans |

||||||||

Current interest-bearing loans and borrowings |

||||||||

Interest-bearing loans and borrowings |

||||||||

Million US dollar |

30 June 2023 |

31 December 2022 |

||||||

Non-current interest-bearing loans and borrowings |

||||||||

Current interest-bearing loans and borrowings |

||||||||

Interest-bearing loans and borrowings |

||||||||

Bank overdrafts |

||||||||

Cash and cash equivalents |

( |

( |

||||||

Interest bearing loans granted and other deposits (included within Trade and other receivables) |

( |

( |

||||||

Debt securities (included within Investment securities) |

( |

( |

||||||

Net debt |

||||||||

Million US dollar |

Long-term debt, net of current portion |

Short-term debt and current portion of long- term debt |

||||||

Balance at 1 January 2023 |

||||||||

Proceeds from borrowings |

||||||||

Payments on borrowings |

( |

|||||||

Capitalization / (payment) of lease liabilities |

( |

|||||||

Amortized cost |

||||||||

Unrealized foreign exchange effects |

||||||||

Current portion of long-term debt |

( |

|||||||

(Gain)/Loss on bond redemption and other movements |

||||||||

Balance at 30 June 2023 |

||||||||

Million US dollar |

Long-term debt, net of current portion |

Short-term debt and current portion of long- term debt |

||||||

Balance at 1 January 2022 |

||||||||

Proceeds from borrowings |

||||||||

Payments on borrowings |

( |

( |

||||||

Capitalization / (payment) of lease liabilities |

( |

|||||||

Amortized cost |

||||||||

Unrealized foreign exchange effects |

( |

( |

||||||

Current portion of long-term debt |

( |

|||||||

(Gain)/Loss on bond redemption and other movements |

||||||||

Balance at 30 June 2022 |

||||||||

18. |

Share-based payments |

19. |

Risks arising from financial instruments |

30 June 2023 |

31 December 2022 |

|||||||||||||||||||||||||||||||

At fair |

At fair |

|||||||||||||||||||||||||||||||

value |

At fair |

value |

At fair |

|||||||||||||||||||||||||||||

At |

through |

value |

At |

through |

value |

|||||||||||||||||||||||||||

amortized |

profit or |

through |

amortized |

profit or |

through |

|||||||||||||||||||||||||||

Million US dollar |

cost |

loss |

OCI |

Total |

cost |

loss |

OCI |

Total |

||||||||||||||||||||||||

Cash and cash equivalents |

- | - | - | - | ||||||||||||||||||||||||||||

Trade and other receivables |

- | - | - | - | ||||||||||||||||||||||||||||

Investment securities |

||||||||||||||||||||||||||||||||

Interest rate swaps |

- | - | ||||||||||||||||||||||||||||||

Cross currency interest rate swaps |

- | - | ||||||||||||||||||||||||||||||

Foreign exchange forwards |

- | - | ||||||||||||||||||||||||||||||

Foreign currency futures |

- | - | - | - | ||||||||||||||||||||||||||||

Commodities |

- | - | - | - | ||||||||||||||||||||||||||||

Financial assets |

||||||||||||||||||||||||||||||||

Non-current |

||||||||||||||||||||||||||||||||

Current |

||||||||||||||||||||||||||||||||

Trade and other payables |

- | - | ||||||||||||||||||||||||||||||

Non-current interest-bearing loans and borrowings |

- | - | - | |||||||||||||||||||||||||||||

Current interest-bearing loans and borrowings |

- | - | - | - | ||||||||||||||||||||||||||||

Bank overdrafts |

- | - | - | - | ||||||||||||||||||||||||||||

Equity swaps |

- | - | - | - | ||||||||||||||||||||||||||||

Cross currency interest rate swaps |

- | - | ||||||||||||||||||||||||||||||

Foreign exchange forwards |

- | - | ||||||||||||||||||||||||||||||

Foreign currency futures |

- | - | - | - | ||||||||||||||||||||||||||||

Commodities |

- | - | - | - | ||||||||||||||||||||||||||||

Interest rate swaps |

- | - | ||||||||||||||||||||||||||||||

Financial liabilities |

||||||||||||||||||||||||||||||||

Non-current |

||||||||||||||||||||||||||||||||

Current |

||||||||||||||||||||||||||||||||

30 June 2023 |

Before hedging |

After hedging |

||||||||||||||

Interest-bearing financial liabilities |

Effective |

Amount |

Effective |

Amount |

||||||||||||

Million US dollar |

interest rate |

interest rate |

||||||||||||||

Floating rate |

||||||||||||||||

Canadian dollar |

- | - | ||||||||||||||

Euro |

||||||||||||||||

US dollar |

- | - | ||||||||||||||

Brazilian real |

||||||||||||||||

Other |

||||||||||||||||

Fixed rate |

||||||||||||||||

Canadian dollar |

||||||||||||||||

Chinese yuan |

||||||||||||||||

Euro |

||||||||||||||||

Pound sterling |

||||||||||||||||

South Korean won |

||||||||||||||||

US dollar |

||||||||||||||||

Other |

||||||||||||||||

31 December 2022 |

Before hedging |

After hedging |

||||||||||||||

Interest-bearing financial liabilities |

Effective |

Amount |

Effective |

Amount |

||||||||||||

Million US dollar |

interest rate |

interest rate |

||||||||||||||

Floating rate |

||||||||||||||||

Canadian dollar |

- | - | ||||||||||||||

Euro |

||||||||||||||||

Pound sterling |

- | - | ||||||||||||||

South Korean won |

- | |||||||||||||||

US dollar |

- | - | ||||||||||||||

Other |

||||||||||||||||

Fixed rate |

||||||||||||||||

Canadian dollar |

||||||||||||||||

Chinese yuan |

||||||||||||||||

Euro |

||||||||||||||||

Pound sterling |

||||||||||||||||

South Korean won |

||||||||||||||||

US dollar |

||||||||||||||||

Other |

||||||||||||||||

30 June 2023 |

31 December 2022 |

|||||||||||||||||||||||

Million US dollar |

Gross |

Impairment |

Net carrying amount |

Gross |

Impairment |

Net carrying amount |

||||||||||||||||||

Cash and cash equivalents |

- | - | ||||||||||||||||||||||

Trade receivables |

( |

( |

) | |||||||||||||||||||||

Other receivables |

( |

( |

) | |||||||||||||||||||||

Derivatives |

- | - | ||||||||||||||||||||||

Cash deposits for guarantees |

- | - | ||||||||||||||||||||||

Investment in unquoted companies |

( |

( |

) | |||||||||||||||||||||

Investment in debt securities |

- | - | ||||||||||||||||||||||

Loans to customers |

- | - | ||||||||||||||||||||||

( |

( |

) |

||||||||||||||||||||||

30 June 2023 |

31 December 2022 |

|||||||

Balance at end of previous year |

( |

( |

||||||

Impairment losses |

( |

( |

||||||

Derecognition |

||||||||

Currency translation and other |

( |

|||||||

Balance at end of period |

( |

( |

||||||

· |

Debt servicing; |

· |

Capital expenditures; |

· |

Investments in companies; |

· |

Increases in ownership of AB InBev’s subsidiaries or companies in which it holds equity investments; |

· |

Share buyback programs; and |

· |

Payments of dividends and interest on shareholders’ equity. |

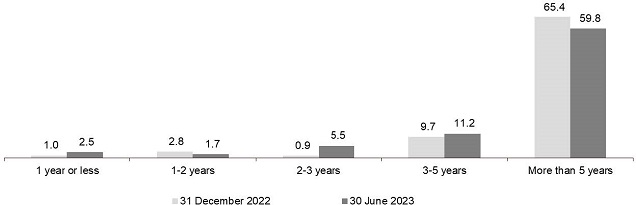

30 June 2023 |

||||||||||||||||||||||||||||

Million US dollar |

Carrying amount¹ |

Contractual cash flows |

Less than 1 year |

1-2 years |

2-3 years |

3-5 years |

More than 5 years |

|||||||||||||||||||||

Non-derivative financial liabilities |

||||||||||||||||||||||||||||

Unsecured bond issues |

( |

( |

( |

( |

( |

( |

( |

|||||||||||||||||||||

Trade and other payables |

( |

( |

( |

( |

( |

( |

( |

|||||||||||||||||||||

Lease liabilities |

( |

( |

( |

( |

( |

( |

( |

|||||||||||||||||||||

Secured bank loans |

( |

( |

( |

( |

( |

( |

( |

|||||||||||||||||||||

Unsecured bank loans |

( |

( |

( |

- | - | - | - | |||||||||||||||||||||

Unsecured other loans |

( |

( |

( |

( |

( |

( |

( |

|||||||||||||||||||||

Bank overdraft |

( |

( |

( |

- | - | - | - | |||||||||||||||||||||

( |

( |

( |

( |

( |

( |

( |

||||||||||||||||||||||

Derivative financial liabilities |

||||||||||||||||||||||||||||

Equity derivatives |

( |

( |

( |

- | - | - | ||||||||||||||||||||||

Foreign exchange derivatives |

( |

( |

( |

- | - | - | - | |||||||||||||||||||||

Cross currency interest rate swaps |

( |

( |

( |

( |

( |

( |

||||||||||||||||||||||

Commodity derivatives |

( |

( |

( |

- | - | - | ||||||||||||||||||||||

( |

( |

( |

( |

( |

( |

|||||||||||||||||||||||

Of which: related to cash flow hedges |

( |

( |

( |

( |

( |

|||||||||||||||||||||||

31 December 2022 |

||||||||||||||||||||||||||||

Million US dollar |

Carrying amount¹ |

Contractual cash flows |

Less than 1 year |

1-2 years |

2-3 years |

3-5 years |

More than 5 years |

|||||||||||||||||||||

Non-derivative financial liabilities |

||||||||||||||||||||||||||||

Unsecured bond issues |

( |

( |

( |

( |

( |

( |

( |

|||||||||||||||||||||

Trade and other payables |

( |

( |

( |

( |

( |

( |

( |

|||||||||||||||||||||

Lease liabilities |

( |

( |

( |

( |

( |

( |

( |

|||||||||||||||||||||

Secured bank loans |

( |

( |

( |

( |

( |

( |

( |

|||||||||||||||||||||

Unsecured bank loans |

( |

( |

( |

- | - | |||||||||||||||||||||||

Unsecured other loans |

( |

( |

( |

( |

( |

( |

( |

|||||||||||||||||||||

Bank overdraft |

( |

( |

( |

- | - | - | - | |||||||||||||||||||||

( |

( |

( |

( |

( |

( |

( |

||||||||||||||||||||||

Derivative financial liabilities |

||||||||||||||||||||||||||||

Equity derivatives |

( |

( |

( |

- | - | - | ||||||||||||||||||||||

Foreign exchange derivatives |

( |

( |

( |

- | - | - | - | |||||||||||||||||||||

Cross currency interest rate swaps |

( |

( |

( |

( |

( |

( |

( |

|||||||||||||||||||||

Commodity derivatives |

( |

( |

( |

( |

- | - | - | |||||||||||||||||||||

( |

( |

( |

( |

( |

( |

( |

||||||||||||||||||||||

Of which: related to cash flow hedges |

( |

( |

( |

( |

( |

- | ||||||||||||||||||||||

Assets |

Liabilities |

Net |

||||||||||||||||||||||

Million US dollar |

30 June 2023 |

31 December 2022 |

30 June 2023 |

31 December 2022 |

30 June 2023 |

31 December 2022 |

||||||||||||||||||

Foreign currency |

||||||||||||||||||||||||

Foreign exchange forwards |

( |

( |

( |

( |

||||||||||||||||||||

Foreign currency futures |

( |

|||||||||||||||||||||||

Interest rate |

||||||||||||||||||||||||

Interest rate swaps |

( |

( |

( |

|||||||||||||||||||||

Cross currency interest rate swaps |

( |

( |

( |

( |

||||||||||||||||||||

Commodities |

||||||||||||||||||||||||

Aluminum swaps |

( |