Table of Contents

Filed pursuant to Rule 497

Registration File Number 333-209022

| PROSPECTUS |

NexPoint Real Estate Strategies Fund

Maximum Offering of 50,000,000 Class Z Shares

Shares of Beneficial Interest

The Fund. NexPoint Real Estate Strategies Fund (the “Fund”) is a newly-organized, continuously offered, non-diversified, closed-end management investment company that intends to operate as an interval fund.

This prospectus provides the information that a prospective investor should know about the Fund before investing. You are advised to read this prospectus carefully and to retain it for future reference. Additional information about the Fund, including a Statement of Additional Information (“SAI”) dated July 12, 2016, has been filed with the Securities and Exchange Commission (“SEC”). The SAI is available upon request and without charge by writing the Fund at NexPoint Real Estate Strategies Fund, c/o DST Systems, Inc., P.O. Box 219630, Kansas City, MO, 64121-9630, or by calling toll-free (844) 485-9167. The table of contents of the SAI appears on page 63 of this prospectus. You may request the Fund’s SAI, annual and semi-annual reports when available, and other information about the Fund or make shareholder inquiries by calling (844) 485-9167 or by visiting www.nexpointres.com. The SAI, which is incorporated by reference into (legally made a part of) this prospectus, is also available on the SEC’s website at http://www.sec.gov. The address of the SEC’s website is provided solely for the information of prospective shareholders and is not intended to be an active link.

Investment Objective. The Fund’s investment objective is to seek long-term total return, with an emphasis on current income, by primarily investing in a broad range of real estate-related debt, equity and preferred equity investments across multiple real estate sectors. There can be no assurance that the Fund will achieve this objective.

Investment Strategy. The Fund pursues its investment objective by investing, under normal circumstances, at least 80% of its assets (defined as net assets plus the amount of any borrowing for investment purposes) in real estate and real estate related securities, as further described in this prospectus.

Securities Offered. The Fund intends to engage in a continuous offering of shares of beneficial interest of the Fund. The Fund is authorized as a Delaware statutory trust to issue an unlimited number of shares. The Fund is offering to sell, through its principal underwriter, Highland Capital Funds Distributor, Inc. (the “Distributor”), under the terms of this prospectus, up to 50,000,000 shares of beneficial interest, at the net asset value (“NAV”) per share plus the applicable sales load. There is no sales load for Class Z shares. See “Fees and Fund Expenses” and “Plan of Distribution”. The initial NAV for Class Z shares is $20.00 per share. The minimum initial investment by a shareholder for Class Z shares is $100,000. The Distributor is not required to sell any specific number or dollar amount of the Fund’s shares, but will use reasonable efforts to sell the shares. The Fund is not required to raise a minimum amount of proceeds from this offering in order to commence operations. Funds received will be invested promptly and no arrangements have been made to place such funds in an escrow, trust or similar account. Assets that cannot be invested promptly in real estate or real estate related securities will be invested in cash or cash equivalents. The Fund’s continuous offering is expected to continue in reliance on Rule 415 under the Securities Act of 1933, until the earlier of the date the Fund has sold 50,000,000 shares or two years from the date the registration statement, of which this prospectus is a part, which may be extended by the Fund’s board of trustees (the “Board”).

Use of Leverage. The Fund anticipates incurring leverage as part of its investment strategy. The Fund will target overall leverage at 25% of the Fund’s total assets immediately after giving effect to such leverage but may use leverage up to 33.33% of the Fund’s total assets. The Fund may also invest in private and public real estate investment funds and real estate investment funds or trusts managed by affiliated or unaffiliated managers or entities wholly-owned by the Fund that may incur higher levels of leverage. Accordingly, the Fund, through these investments, may be exposed to higher levels of leverage than the Fund is permitted to, including a greater risk of loss with respect to such investments as a result of higher leverage employed by such entities.

Non-Traded REITs. The Fund may invest in publicly registered non-traded real estate investment trusts, which are illiquid and are not subject to the protections of the Investment Company Act of 1940. Some or all of these funds may be managed by NexPoint Advisors, L.P., the Fund’s investment adviser, or an affiliate.

Table of Contents

The Fund is newly organized, and its shares have no history of public trading. In addition, investors should understand that:

| • | the Fund does not currently intend to list its shares on any securities exchange; |

| • | there is no secondary market for the Fund’s shares, and the Fund does not expect that such a market will develop at this time; and |

| • | your investment in the Fund will be illiquid. |

Before investing, you should therefore consider the following factors:

| • | You may not have access to the money you invest for an extended period of time; |

| • | You may not be able to sell your shares at the time of your choosing regardless of how the Fund performs. |

| • | Because you may not be able to sell your shares at the time of your choosing, you may not be able to reduce your exposure in a market downturn. |

| • | An investment in the Fund may not be suitable for investors who may need the money they invested in a specified timeframe. |

| • | The amount of distributions that the Fund may pay, if any, is uncertain. |

| • | The Fund may pay distributions in significant part from sources that may not be available in the future and that are unrelated to the Fund’s performance, such as from offering proceeds, borrowings, and amounts from the Fund’s affiliates that are subject to repayment by investors. All or a portion of a distribution may consist of a return of capital. Because a return of capital may reduce a shareholder’s tax basis, it will increase the amount of gain or decrease the amount of loss on a subsequent disposition of the shareholder’s shares. |

The Fund has implemented a share repurchase program, but it is only required to repurchase up to 5% of its outstanding shares per quarter. The Fund intends to begin repurchasing shares at the end of the second full quarter following the effectiveness of this Registration Statement. In addition, the Fund may in the future determine to list its shares on a public securities exchange, but even if an active secondary market in the Fund’s shares were to develop as a result, closed-end fund shares frequently trade at a discount from their NAV. Investing in the Fund involves a considerable degree of risk. See “Risk Factors” on page 27 of this prospectus.

Neither the SEC nor any state securities commission has approved or disapproved these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Class Z Shares |

||||

| Public Offering Price Per Share |

$ | 20.00 | ||

| Maximum Sales Load as a Percentage of Purchase Amount1,2 |

None | |||

| Proceeds to the Fund3 |

$ | 20.00 | ||

| (1) | There is no sales load for Class Z shares. |

| (2) | The Adviser and/or its affiliates, in their discretion and from their own resources, may pay additional compensation to brokers or dealers in connection with the sale and distribution of Fund shares. There is no limit on the amount of additional compensation paid by the Adviser or its affiliates, subject to the limitations imposed by FINRA. See “Plan of Distribution.” |

| (3) | Assumes all shares currently registered are sold in the continuous offering. The Fund will also bear certain ongoing offering costs associated with the Fund’s continuous offering of shares. The Fund estimates that it will incur in connection with this offering approximately $5.2 million of offering and other expenses, or approximately $0.10 per Class Z share. The net proceeds to the Fund after payment of the maximum sales load and estimated offering expenses of $5.2 million will be approximately $995 million or approximately $19.90 per Class Z share, assuming the Fund raises $1,000,000,000 in this offering. See “Fees and Fund Expenses.” Offering costs incurred by the Fund will immediately reduce the Fund’s NAV and the value of the shares that you purchase in this offering. |

Highland Capital Funds Distributor, Inc.

The date of this prospectus is July 12, 2016.

Table of Contents

| 1 | ||||

| 13 | ||||

| 15 | ||||

| 15 | ||||

| 15 | ||||

| 16 | ||||

| 27 | ||||

| 43 | ||||

| 47 | ||||

| 48 | ||||

| 51 | ||||

| 53 | ||||

| 54 | ||||

| 55 | ||||

| 57 | ||||

| 58 | ||||

| 58 | ||||

| 61 | ||||

| 61 | ||||

| 62 | ||||

| 62 | ||||

| TABLE OF CONTENTS OF THE STATEMENT OF ADDITIONAL INFORMATION |

63 |

Table of Contents

This summary does not contain all of the information that you should consider before investing in the shares. You should review the more detailed information contained or incorporated by reference in this prospectus and in the SAI, particularly the information set forth under the heading “Risk Factors.”

The Fund

NexPoint Real Estate Strategies Fund (the “Fund”) is a newly-organized, continuously offered, non-diversified, closed-end management investment company that intends to operate as an interval fund. See “The Fund.” As an interval fund, the Fund will offer to make repurchases of no less than 5% of its outstanding shares at net asset value (“NAV”), on a quarterly basis, unless such offer is suspended or postponed in accordance with regulatory requirements. See “Quarterly Repurchases of Shares.”

Investment Objective and Policies

Investment Objective. The Fund’s investment objective is to seek long-term total return, with an emphasis on current income, by primarily investing in a broad range of private and public real estate-related debt, equity and preferred equity investments. There can be no assurance that the Fund will achieve this objective.

Investment Strategy. The Fund will pursue its investment objective by investing, under normal circumstances, at least 80% of its assets in “real estate and real estate related securities” (as defined below). In particular, the Fund will pursue its investment objective by investing the Fund’s assets primarily in (1) commercial mortgage backed securities (“CMBS”) and residential mortgage backed securities (“RMBS”), (2) direct preferred equity and mezzanine investments in real properties, (3) equity securities of public (both traded and non-traded) and private debt and equity real estate investment trusts (“REITs”) and/or real estate operating companies (“REOCs”) and (4) opportunistic and value added direct real estate strategies (through a wholly-owned REIT).

Preferred equity and mezzanine investments in real estate transactions come in various forms which may or may not be documented in the borrower’s organizational documents. Generally, real estate preferred equity and/or mezzanine investments are typically junior to first mortgage financing but senior to the borrower’s or sponsor’s equity contribution. The investments are typically structured as an investment by a third-party investor in the real estate owner or various affiliates in the chain of ownership in exchange for a direct or indirect ownership interest in the real estate owner entitling it to a preferred/priority return on its investment. Sometimes, the investment is structured much like a loan where (i) “interest” on the investment is required to be paid monthly by the “borrower” regardless of available property cash flow; (ii) the entire investment is required to be paid by a certain maturity date; (iii) default rate “interest” and penalties are assessed against the “borrower” in the event payments are not made timely; and (iv) a default in the repayment of investment potentially results in the loss of management and/or ownership control by the “borrower” in the company in favor of the investor or other third-party.

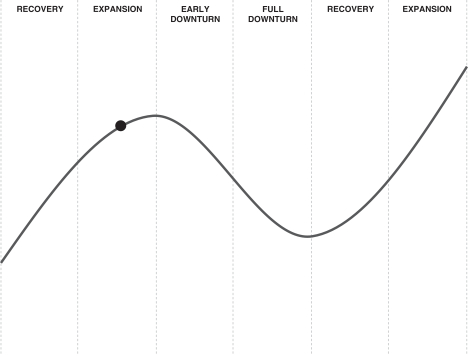

In addition, subject to the 15% Limitation and the 35% Limitation discussed in this Prospectus, the Fund may invest up to 20% of its total assets in equity or debt securities other than real estate and real estate related securities. NexPoint Advisors, L.P. (the “Adviser”), the Fund’s investment adviser, will evaluate each opportunity within the context of where the Adviser believes the various real estate subsectors are within the broader real estate cycle and tactically allocate among these opportunities. Also, the Adviser will select investments it believes offer the best potential outcomes and relative risk to assemble the most appropriate portfolio to meet the risk-adjusted return goals of the Fund. The Adviser has broad discretion to allocate the Fund’s assets among these investment categories and to change allocations as conditions warrant.

1

Table of Contents

This portfolio construction strategy is designed to (i) recognize and allocate capital based upon where the Adviser believes we are in the current real estate cycle, and as a result (ii) minimize drawdowns during market downturns and maximize risk adjusted returns during all market cycles, though there can be no assurance that this strategy will achieve this objective. The Fund will seek to utilize debt at the Fund level to leverage its returns when the Adviser believes doing so would be accretive to returns. The Fund will rely on the expertise of the Adviser and its affiliates to determine the appropriate structure for structured credit investments, which may include, bridge loans, common and preferred equity or other debt-like positions, as well as the acquisition of such instruments from banks, servicers or other third parties.

The Fund defines “real estate and real estate related securities” to consist of common stock, convertible or non-convertible preferred stock, warrants, convertible or non-convertible secured or unsecured debt, and partnership or membership interests issued by:

| • | CMBS, RMBS and other real estate credit investments, which include existing first and second mortgages on real estate, either originated or acquired in the secondary market, and secured, unsecured and/or convertible notes offered by REOCs and REITs; |

| • | publicly traded REITs managed by affiliated or unaffiliated asset managers and their foreign equivalents (“Public REITs”); |

| • | REOCs; |

| • | private real estate investment funds managed by affiliated or unaffiliated institutional asset managers (“Private Real Estate Investment Funds”); |

| • | registered closed-end funds that invest principally in real estate (collectively, “Public Investment Funds”); |

| • | real estate exchange traded funds (“ETFs”); and |

| • | publicly-registered non-traded REITs (“Non-Traded REITs”) and private REITs, generally wholly-owned by the Fund or wholly-owned or managed an affiliate. |

The Fund has not imposed limitations on the portion of its assets that may be invested in any of the other categories outlined above. The Fund, however, will limit its investments in Private Real Estate Investment Funds that are excluded from the definition of “investment company” under the 1940 Act by Section 3(c)(1) or Section 3(c)(7) of the 1940 Act to no more than 15% of its net assets. Such entities are typically private equity funds and hedge funds. The Fund will further limit its aggregate investments in issuers subject to the 15% Limitation as well as other private funds, private REITs and Private Real Estate Investment Funds to 35% of its net assets (the “35% Limitation”). For purposes of compliance with the 15% Limitation and the 35% Limitation, the Fund will not count its direct investments in wholly-owned subsidiaries but will look through such subsidiaries and count their underlying holdings. REITs are pooled investment vehicles that invest primarily in income-producing real estate or real estate-related loans or interests, and REOCs are companies that invest in real estate and whose shares trade on public exchanges. Foreign REIT equivalents are entities located in jurisdictions that have adopted legislation substantially similar to the REIT tax provisions in that they provide for flow-through tax treatment for the foreign REIT equivalent and require distributions of income to shareholders.

Leverage. The Fund anticipates incurring leverage as part of its investment strategy. The Fund will target overall leverage at 25% of the Fund’s total assets immediately after giving effect to such leverage, but may incur leverage up to 33.33% of the Fund’s total assets as permitted by the 1940 Act. There can be no assurance that any leveraging strategy the Fund employs will be successful during any period in which it is employed. The Fund may also invest in Private Real Estate Investment Funds, Public REITs, REOCs and Non-Traded REITs, which may incur higher levels of leverage. Accordingly, the Fund, through these investments, may be exposed to higher levels of leverage than the Fund is permitted to.

2

Table of Contents

In addition to any indebtedness incurred by the Fund, any subsidiary of the Fund, including a REIT subsidiary, may also utilize leverage, including by mortgaging properties held by special purpose vehicles, or by acquiring property with existing debt. Any such borrowings will generally be the sole obligation of each respective special purpose vehicle, without any recourse to any other special purpose vehicle, a REIT subsidiary, the Fund or its assets, and the Fund will not treat such non-recourse borrowings as senior securities (as defined in the 1940 Act) for purposes of complying with the 1940 Act’s limitations on leverage unless the financial statements of the special purpose vehicle, or the subsidiary of the Fund that owns such special purpose vehicle, will be consolidated in accordance with Regulation S-X and other accounting rules. If cash flow is insufficient to pay principal and interest on a special purpose vehicle’s borrowings, a default could occur, ultimately resulting in foreclosure of any security instrument securing the debt and a complete loss of the investment, which could result in losses to the REIT subsidiary and, therefore, to the Fund. To the extent that any subsidiaries of the Fund, including a REIT subsidiary, directly incur leverage in the form of debt (as opposed to non-recourse borrowings made through special purpose vehicles), the amount of such recourse leverage used by the Fund and such subsidiaries, including a REIT subsidiary, will be consolidated and treated as senior securities for purposes of complying with the 1940 Act’s limitations on leverage by the Fund. See “Investment Objective, Policies and Strategies.”

Policies. The Fund’s 80% policy with respect to investment in real estate and real estate related securities is not fundamental and may be changed by the Board without shareholder approval. However, shareholders will be given at least 60 days’ notice prior to any change in the 80% Policy. The Fund’s SAI contains a list of all of the fundamental and non-fundamental investment policies of the Fund under the heading, “Investment Objective and Policies.” For purposes of the Fund’s 80% policy, the Fund will invest only in Public Investment Funds and Private Real Estate Investment Funds that either (1) have adopted a policy to invest, under normal circumstances, at least 80% of their net assets, plus borrowings for investment purposes, in real estate and real estate related securities, or (2) do not have a stated 80% policy, but do invest, under normal circumstances, at least 80% of their net assets, plus borrowings for investment purposes, in real estate and real estate related securities, as determined by the Adviser’s review of their portfolio holdings, investment objectives and strategies. Prior to investing in an underlying fund that does not have a stated 80% policy, the Adviser will review the underlying fund’s prospectus or offering memorandum, financial statements, and any available third party research, and may also meet with the underlying fund’s management team in order to determine whether the underlying fund follows an 80% policy under normal circumstances. Following the Fund’s investment in the underlying fund, the Adviser will continue to monitor the underlying fund on an ongoing basis, reviewing all relevant information as it becomes available. If at any point the Adviser has reason to believe that the underlying fund’s investment strategy has changed, or that the underlying asset mix has changed in a way that no longer satisfies the 80% policy, the Adviser will immediately reclassify the investment for purposes of testing the Fund’s compliance with its 80% policy. If the Fund were to temporarily fall out of compliance with its 80% Policy as a result of the reclassification of an underlying fund, the Fund would take one or more of the following actions in order to come back into compliance with its 80% Policy: (i) restricting additional investments that do not fall within the 80% Policy, (ii) selling one or more investments that are outside of the 80% Policy, (iii) deploying new capital raised in the Offering in investments that fall within the 80% Policy, or (iv) if available, utilizing borrowings from a credit facility to make investments that fall within the 80% Policy.

The Fund concentrates investments in the real estate and real estate related industry, meaning that, under normal circumstances, it invests 25% or more of its total assets in real estate and real estate related industry securities. This policy is fundamental and may not be changed by the Board without shareholder approval. The Fund’s SAI contains a list of all of the fundamental and non-fundamental investment policies of the Fund, under the heading “Investment Objective and Policies.”

Investment Adviser and Fees

NexPoint Advisors, L.P., which serves as the investment adviser of the Fund, is registered with the SEC as an investment adviser under the Investment Advisers Act of 1940, as amended (the “Advisers Act”) and is an

3

Table of Contents

affiliate of Highland Capital Management, L.P. (“Highland”). The Adviser will have access to Highland and its resources through a shared services agreement (the “Shared Services Agreement”). The Adviser also externally manages NexPoint Credit Strategies Fund (“NHF”), a registered closed-end fund whose shares trade on the New York Stock Exchange, and NexPoint Capital, Inc., a non-traded business development company and the following registered closed-end funds that intend to operate as interval funds but have not yet commenced operations: NexPoint Discount Yield Fund (“NDYF”), NexPoint Energy and Materials Opportunities Fund (“NEMO”), NexPoint Healthcare Opportunities Fund (“NHOF”), NexPoint Latin American Opportunities Fund (“NLAF”), NexPoint Distressed Strategies Fund (“NDSF”) and NexPoint Merger Arbitrage Fund (“NMAF”). A wholly-owned subsidiary of the Adviser, NexPoint Real Estate Advisors, L.P., manages a publicly traded REIT, NexPoint Residential Trust, Inc. (NYSE: NXRT). A wholly-owned subsidiary of the Adviser, NexPoint Real Estate Advisors II, L.P., manages NexPoint Multifamily Capital Trust, Inc. (“NMCT”), a real estate company that intends to elect to be taxed as a REIT that commenced operations on March 24, 2016. Our Adviser’s senior management team has experience across private lending, private equity, real estate investing and other investment strategies. Collectively, our Adviser’s affiliates manage approximately $17.1 billion in assets as of March 31, 2016, including approximately $1.9 billion of real estate related assets.

Pursuant to an investment advisory agreement with the Fund (the “Investment Advisory Agreement”), the Adviser will be entitled to receive a monthly fee at the annual rate of 1.25% of the Fund’s Daily Gross Assets. Daily Gross Assets is defined in the Investment Advisory Agreement as total assets, including assets resulting from leverage, less any liabilities. For purposes of calculating the Fund’s Daily Gross Assets, derivatives will be valued at their market value, not their notional value.

The Adviser and the Fund have entered into an expense limitation and reimbursement agreement (the “Expense Limitation Agreement”) under which the Adviser has agreed contractually to waive its fees and to pay or absorb the ordinary operating expenses of the Fund (including organizational and offering expenses, but excluding interest, dividend expenses on short sales, brokerage commissions, acquired fund fees and expenses, taxes and extraordinary expenses), to the extent that they exceed 1.75% per annum of the Fund’s average Daily Gross Assets for Class Z shares (the “Expense Limitation”). “Daily Gross Assets” is defined in the Expense Limitation Agreement as an amount equal to total assets, less any liabilities, but excluding liabilities evidencing leverage. If the Fund incurs expenses excluded from the Expense Limitation Agreement, the Fund’s expense ratio would be higher and could exceed the Expense Limitation. In consideration of the Adviser’s agreement to limit the Fund’s expenses, the Fund has agreed to repay the Adviser in the amount of any fees waived and Fund expenses paid or absorbed, subject to the limitations that: (1) the reimbursement for fees and expenses will be made only if payable not more than three years from the date of the reimbursement; and (2) the reimbursement may not be made if it would cause the Expense Limitation as of the time of waiver to be exceeded. The Expense Limitation Agreement will remain in effect at least until one year after the effective date of this registration statement, unless and until the Board approves its modification or termination. The Expense Limitation Agreement may be terminated only by the Board. After the expiration of the Expense Limitation Agreement, the agreement may be renewed at the discretion of the Adviser and the Board. See “Management of the Fund.”

REITs wholly-owned by the Fund will have separate investment advisory agreements with the Adviser. To the extent fees are paid to the Adviser by these entities, such fees will be offset against fees otherwise payable by the Fund to the Adviser, such that shareholders of the Fund will only be subject to one layer of fees to the Adviser. Notwithstanding this arrangement, the Fund and its shareholders will indirectly bear the expenses associated with forming such entities, non-advisory fees paid by such entities (if any) and operating expenses, including maintaining their REIT qualification. The Fund may invest in funds not managed by an affiliate of the Adviser (including closed-end funds, ETFs, private funds, externally managed traded and non-traded REITs, etc.), in which case two layers of fees will be paid by the Fund.

4

Table of Contents

In addition, certain of the mortgage REITs or Private Real Estate Investment Funds in which the Fund may invest may compensate their management through asset-based fees of up to 2.0% of total assets and incentive allocations or fees of as much as 20% of such underlying fund’s net assets. The Fund, through its investments in such entities, indirectly bears a portion of such expenses.

Transfer Agent and Fund Administrator

DST Systems, Inc. (“DST”) serves as the transfer agent of the Fund. State Street Bank & Trust Company (“State Street”) serves as the Fund’s Administrator. See “Management of the Fund.”

Distribution Fees

Class Z shares are not subject to a distribution fee (“Distribution Fee”). See “Plan of Distribution.”

Shareholder Servicing Fee

The Fund will not pay a monthly shareholder servicing fee in connection with Class Z shares.

Closed-End Fund Structure

Closed-end funds differ from open end management investment companies (commonly referred to as mutual funds) in that closed-end funds do not typically redeem their shares at the option of the shareholder. Rather, closed-end fund shares typically trade in the secondary market via a stock exchange. Unlike many closed-end funds, however, the Fund’s shares will not be listed on a stock exchange. Instead, the Fund will operate as an interval fund, meaning that the Fund will provide limited liquidity to shareholders by offering to repurchase a limited amount of shares (at least 5%) on a quarterly basis, which is discussed in more detail below. An investment in the Fund is suitable only for investors who can bear the risks associated with the limited liquidity of the shares and should be viewed as a long-term investment. The Fund is subject to continuous asset in-flows, although not subject to continuous out-flows. The Board may, in the future, seek shareholder approval to list the Fund’s shares on a national securities exchange depending on market conditions and other factors.

Share Classes.

The Fund offers one share class by this prospectus: Class Z shares. The Fund has received exemptive relief from the SEC to issue multiple classes of shares and to impose asset-based distribution fees and early-withdrawal charges. The fund also offers Class A and Class C shares through separate prospectuses. An investment in any share class of the Fund represents an investment in the same assets of the Fund. However, the purchase restrictions and ongoing fees and expenses for each share class are different. The fees and expenses for the Class Z shares are set forth in “Fees and Fund Expenses.” If an investor has hired an intermediary and is eligible to invest in more than one class of shares, the intermediary may help determine which share class is appropriate for that investor. When selecting a share class, you should consider which share classes are available to you, how much you intend to invest, how long you expect to own shares, and the total costs and expenses associated with a particular share class.

Each investor’s financial considerations are different. You should speak with your financial advisor to help you decide which share class is best for you. Not all financial intermediaries offer all classes of shares. If your financial intermediary offers more than one class of shares, you should carefully consider which class of shares to purchase.

5

Table of Contents

Investor Suitability

An investment in the Fund involves a considerable amount of risk. It is possible that you may lose money. An investment in the Fund is suitable only for investors who can bear the risks associated with the limited liquidity of the shares and should be viewed as a long-term investment. Before making your investment decision, you should (i) consider the suitability of this investment with respect to your investment objectives and personal financial situation and (ii) consider factors such as your personal net worth, income, age, risk tolerance and liquidity needs.

Repurchases of Shares

The Fund is an interval fund and, as such, has adopted a fundamental policy to make quarterly repurchase offers, at NAV, of no less than 5% of the shares outstanding. There is no guarantee that shareholders will be able to sell all of the shares they desire in a quarterly repurchase offer because shareholders, in total, may wish to sell more than 5% of the Fund’s shares. If the amount of repurchase requests exceeds the number of shares the Fund offers to repurchase, the Fund will repurchase shares on a pro rata basis. Limited liquidity will be provided to shareholders only through the Fund’s quarterly repurchases. The Fund will maintain liquid securities or cash or, if available, will borrow in amounts sufficient to meet quarterly redemption requirements. See “Quarterly Repurchases of Shares.”

Summary of Risks

Investing in the Fund involves risks, including the risk that you may receive little or no return on your investment or that you may lose part or all of your investment. Consequently, you can lose money by investing in the Fund. No assurance can be given that the Fund will achieve its investment objective, and investment results may vary substantially over time and from period to period. An investment in the Fund is not appropriate for all investors.

An investment in the Fund is not a deposit of any bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency.

Substantial Conflicts of Interest. As a result of the Fund’s arrangements with Highland, there may be times when Highland, the Adviser or their affiliates have interests that differ from those of the Fund’s shareholders, giving rise to a conflict of interest. The Fund’s officers serve or may serve as officers, directors or principals of entities that operate in the same or a related line of business as the Fund does, or of investment funds managed by the Adviser or its affiliates. Similarly, the Adviser or its affiliates may have other clients with similar, different or competing investment objectives. In serving in these multiple capacities, they may have obligations to other clients or investors in those entities, the fulfillment of which may not be in the best interests of the Fund or its shareholders. For example, the Fund’s officers have, and will continue to have, management responsibilities for other investment funds, accounts or other investment vehicles managed or sponsored by the Adviser and its affiliates. The Fund’s investment objective may overlap, in part or in whole, with the investment objective of such affiliated investment funds, accounts or other investment vehicles, including, but not limited to, Freedom REIT, LLC (“Freedom REIT”) and NexPoint Real Estate Capital, Inc., which are subsidiaries of NHF, NexPoint Residential Trust, Inc. (“NXRT”), a REIT that has its shares listed on the NYSE, and NexPoint Multifamily Capital Trust, Inc. (“NMCT”), a real estate company that commenced operations on March 24, 2016. Freedom REIT is a Delaware limited liability company organized on September 17, 2012 to invest capital for NHF. As a result, those individuals may face conflicts in the allocation of investment opportunities among the Fund and other investment funds or accounts advised by or affiliated with the Adviser. The Adviser will seek to allocate investment opportunities among eligible accounts in a manner that is fair and equitable over time and consistent with its allocation policy. However, the Fund can offer no assurance that such opportunities will be allocated to it fairly or equitably in the short-term or over time.

6

Table of Contents

In addition, it is anticipated that at least some portion of the private and Non-Traded REITs in which the Fund will invest may include Non-Traded REITs sponsored, organized and managed by Highland and its affiliates and private REITs wholly-owned by the Fund and managed by an affiliate or not wholly-owned by the Fund but managed by an affiliate. Such investments are inherently subject to conflicts of interest as a result of the fact that James Dondero, who serves as President of and a portfolio manager for the Fund, Brian Mitts, who serves as Chief Financial Officer and Vice President of the Fund, and Matthew McGraner, who serves as a portfolio manager for the Fund, have ownership interests in entities advised by Highland or its affiliates. The Fund will seek to mitigate such conflicts by requiring that the independent trustees of the Fund periodically review the Fund’s investments in such Non-Traded REITs and private REITs and reaffirm that such investments remain in the Fund’s best interests and in the best interests of its shareholders. The Fund intends to limit its investments in such entities to the extent necessary to qualify as a regulated investment company (“RIC”) for tax purposes. In general, and subject to certain exceptions not applicable here, a RIC is not permitted to invest more than 25% of its total assets in any one issuer, or in any two or more issuers which the taxpayer controls and which are determined to be engaged in the same or similar trades or businesses or related trades or businesses. Please see “Risk Factors—Conflicts of Interest” for a description of risks associated with conflicts of interest.

Closed-End Fund (“CEF”) Risk. The Fund is a CEF. CEFs differ from open-end management investment companies (commonly referred to as mutual funds) in that CEFs generally list their shares for trading on a securities exchange and do not redeem their shares at the option of the shareholder. By comparison, mutual funds issue securities redeemable at net asset value at the option of the shareholder and typically engage in a continuous offering of their shares. Mutual funds are subject to continuous asset in-flows and out-flows that can complicate portfolio management, whereas CEFs generally can stay more fully invested in securities consistent with the CEF’s investment objective and policies. In addition, in comparison to open-end funds, CEFs have greater flexibility in their ability to make certain types of investments, including investments in illiquid securities.

Mortgage Backed Securities Risk. Mortgage backed securities are bonds which evidence interests in, or are secured by, commercial or residential mortgage loans, as the case may be. Accordingly, mortgage backed securities are subject to all of the risks of the underlying mortgage loans. In a rising interest rate environment, the value of mortgage backed securities may be adversely affected when payments on underlying mortgages do not occur as anticipated. The value of mortgage backed securities may also change due to shifts in the market’s perception of issuers and regulatory or tax changes adversely affecting the mortgage securities markets as a whole. In addition, mortgage backed securities are subject to the credit risk associated with the performance of the underlying commercial or residential mortgage properties. Mortgage backed securities are also subject to several risks created through the securitization process.

We may invest in the residual or equity tranches of CMBS, which we refer to as subordinate CMBS and interest-only CMBS. Subordinate CMBSs are paid interest only to the extent there are funds available to make payments. There are multiple tranches of CMBS, offering investors various maturity and credit risk characteristics. Tranches are categorized as senior, mezzanine, and subordinated/equity, according to their degree of risk. The most senior tranche of a CMBS has the greatest collateralization and pays the lowest interest rate. If there are defaults or the collateral otherwise underperforms, scheduled payments to senior tranches take precedence over those of mezzanine tranches, and scheduled payments to mezzanine tranches take precedence over those to subordinated/equity tranches. Lower tranches represent lower degrees of credit quality and pay higher interest rates intended to compensate for the attendant risks. The return on the lower tranches is especially sensitive to the rate of defaults in the collateral pool. The lowest tranche (i.e. the “equity” or “residual” tranche) specifically receives the residual interest payments (i.e., money that is left over after the higher tranches have been paid and expenses of the issuing entities have been paid) rather than a fixed interest rate. As a result, interest only CMBS possess the risk of total loss of investment in the event of prepayment of the underlying mortgages. We have not imposed a limit on the portion of our total assets that may be invested in interest-only multifamily CMBS.

7

Table of Contents

We also may invest in interest-only multifamily CMBS issued by multifamily mortgage loan securitizations. However, these interest-only multifamily CMBS typically only receive payments of interest to the extent that there are funds available in the securitization to make the payment and may introduce increased risks since these securities have no underlying principal cash flows.

Debt Securities Risk. When the Fund invests in debt securities, the value of your investment in the Fund will fluctuate with changes in interest rates. Typically, a rise in interest rates causes a decline in the value of debt securities. In general, the market price of debt securities with longer maturities will increase or decrease more in response to changes in interest rates than shorter-term securities. Other risk factors include credit risk (the debtor may default) and prepayment risk (the debtor may pay its obligation early, reducing the amount of interest payments). These risks could affect the value of a particular investment, possibly causing the Fund’s share price and total return to be reduced or fluctuate more than other types of investments. This kind of market risk is generally greater for funds investing in debt securities with longer maturities.

Non-Payment Risk. Debt securities are subject to the risk of non-payment of scheduled interest and/or principal. Nonpayment would result in a reduction of income to the Fund, a reduction in the value of the security experiencing nonpayment and a potential decrease in the NAV of the Fund. There can be no assurance that the liquidation of any collateral would satisfy the borrower’s obligation in the event of non-payment of scheduled interest or principal payments, or that such collateral could be readily liquidated.

Distribution Policy Risk. The Fund’s distribution policy may, under certain circumstances, have certain adverse consequences to the Fund and its shareholders because it may result in a return of capital resulting in less of a shareholder’s assets being invested in the Fund and, over time, increase the Fund’s expense ratio. The distribution policy also may cause the Fund to sell a security at a time it would not otherwise do so in order to manage the distribution of income and gain. Pending the investment of the net proceeds in accordance with the investment objective and policies, all or a portion of the Fund’s distributions may consist of a return of capital (i.e. from your original investment).

No Minimum Amount of Proceeds Required. The Fund is not required to raise a minimum amount of proceeds from this offering in order to commence operations. In order for the Fund to have viable operations, the Adviser believes the Fund will need to raise approximately $5 million in proceeds from this offering. To the extent that the Fund is unable to raise such amount in a timely manner or at all, it would have a negative impact on the ability of the Fund to diversify its portfolio and meet the asset diversification requirements to qualify as a RIC under the Code.

Public and Private Investment Funds Risk. For investments in Public Investment Funds and Private Real Estate Investment Funds not managed by the Adviser or its affiliates, Fund shareholders will bear two layers of fees and expenses: asset-based fees and expenses at the Fund level, and asset-based fees, incentive allocations or fees and expenses at the Public Investment Fund or Private Real Estate Investment Fund level. The Fund’s performance depends, in part, upon the performance of the Public Investment Fund and Private Real Estate Investment Fund managers and their selected strategies, the adherence by such managers to such selected strategies, the instruments used by such managers, and the Adviser’s ability to select managers and strategies and effectively allocate Fund assets among them.

Private Real Estate Investment Funds are not publicly traded and therefore are not liquid investments. To determine the value of the Fund’s investments in Private Real Estate Investment Funds, the Adviser considers, among other things, information provided by the Private Real Estate Investment Funds, including quarterly unaudited financial statements, which if inaccurate could adversely affect the Adviser’s ability to accurately value the Fund’s shares. In addition to valuation risk, shareholders of Private Real Estate Investment Funds are not entitled to the protections of the 1940 Act.

8

Table of Contents

To the extent the Fund invests in Private Real Estate Investment Funds managed by our Adviser or its affiliates, fees paid at the Private Real Estate Investment Fund level will be reimbursed to the Fund so that shareholders will only pay fees at the Fund level.

REIT Risk. REITs may be affected by changes in the real estate markets generally as well as changes in the values of the properties owned by the REIT or securing the mortgages owned by the REIT. REITs are dependent upon management skill and are not diversified. REITs are also subject to heavy cash flow dependency, defaults by borrowers, self-liquidation, and the possibility of failing to qualify for special tax treatment under the Internal Revenue Code of 1986, as amended (the “Code”), and to maintain an exemption under the 1940 Act. Finally, certain REITs may be self-liquidating at the end of a specified term, and run the risk of liquidating at an economically inopportune time.

Non-Traded REIT Risk. Non-traded REITs are subject to the following risks in addition to those described in “REIT Risk.” Non-Traded REITs are subject to significant commissions, expenses, and organizational and offering costs that reduce the value of an investor’s (including the Fund’s) investment. Non-Traded REITs are not liquid, and investments in Non-Traded REITs may not be accessible for an extended period of time. There is no guarantee of any specific return on the principal amount or the repayment of all or a portion of the principal amount invested in Non-Traded REITs. In addition, there is no guarantee that investors (including the Fund) will receive distributions. Distributions from Non-Traded REITs may be derived from sources other than cash flow from operations, including the proceeds of the offering, from borrowings, or from the sale of assets. Payments of distributions from sources other than cash flow from operations will decrease or diminish an investor’s interest.

Private REIT Risk. Private REITs are subject to the following risks in addition to those described in “Public and Private Real Estate Investment Funds Risk” and “REIT Risk.” Private REITS are unlisted, making them more difficult to value and trade. Moreover, private REITs generally are exempt from registration under the Securities Act of 1933, as amended (the “Securities Act”), and, as such, are not subject to the same disclosure requirements as Public REITs and Non-Traded REITs, which makes private REITs more difficult to evaluate from an investment perspective. In addition, Private REITs may not have audited financial statements.

ETF Risk. The value of ETFs can be expected to increase and decrease in value in proportion to increases and decreases in the indices that they are designed to track. The volatility of different index tracking stocks can be expected to vary in proportion to the volatility of the particular index they track. ETFs are traded similarly to stocks of individual companies. Although an ETF is designed to provide investment performance corresponding to its index, it may not be able to exactly replicate the performance of its index because of its operating expenses and other factors.

Issuer Risk. The value of a specific security can perform differently from the market as a whole for reasons related to the issuer, such as management performance, financial leverage and reduced demand for the issuer’s goods and services.

Leverage Risk. The use of leverage, such as borrowing money to purchase securities, will cause the Fund or a Public Investment Fund or Private Real Estate Investment Fund in which the Fund has invested, to incur additional expenses and significantly magnify the Fund’s losses in the event of underperformance of the Fund’s (or Public Investment Fund’s or Private Real Estate Investment Fund’s) underlying investments. Interest payments and fees incurred in connection with such borrowings will reduce the amount of distributions available to the Fund’s shareholders. The Fund’s investments in Public Investment Funds and REITs managed by affiliated or unaffiliated institutional asset managers may incur higher levels of leverage. Accordingly, the Fund, through these investments, may be exposed to the higher levels of leverage than the Fund is permitted to, including a greater risk of loss with respect to such investments as a result of higher leverage employed by such entities.

9

Table of Contents

Liquidity Risk. There is currently no secondary market for the shares and the Fund expects that no secondary market will develop. Limited liquidity is provided to shareholders only through the Fund’s quarterly repurchase offers for no less than 5% of the shares outstanding at NAV. There is no guarantee that shareholders will be able to sell all of the shares they desire in a quarterly repurchase offer.

Management Risk. The Adviser’s judgments about the attractiveness, value and potential appreciation of particular asset classes and securities in which the Fund invests (directly or indirectly) may prove to be incorrect and may not produce the desired results.

Market Risk. An investment in the Fund’s shares is subject to investment risk, including the possible loss of the entire principal amount invested. An investment in the Fund’s shares represents an indirect investment in the securities owned by the Fund. The value of these securities, like other market investments, may move up or down, sometimes rapidly and unpredictably.

Medium and Small Capitalization Company Risk. Compared to investment companies that focus only on large capitalization companies, the Fund’s NAV may be more volatile because it also invests in medium and small capitalization companies. Compared to larger companies, medium and small capitalization companies are more likely to have (i) more limited product lines or markets and less mature businesses, (ii) fewer capital resources, (iii) more limited management depth and (iv) shorter operating histories. Further, compared to larger companies, the securities of small and medium capitalization companies are more likely to experience more significant changes in market values, be harder to sell at times and at prices that the Adviser believes appropriate, and offer greater potential for gains and losses.

New Offering with No Operating History. The Fund is a closed-end investment company with no history of operations. If the Fund commences operations under inopportune market or economic conditions, it may not be able to achieve its investment objective.

Concentration in Real Estate Securities Risk. The Fund will not invest in real estate directly, but, because the Fund will concentrate its investments in investment vehicles that invest principally in real estate and real estate related securities, its portfolio will be significantly impacted by the performance of the real estate market and may experience more volatility and be exposed to greater risk than a more diversified portfolio. The values of companies engaged in the real estate industry are affected by: (i) changes in general economic and market conditions; (ii) changes in the value of real estate properties; (iii) risks related to local economic conditions, overbuilding and increased competition; (iv) increases in property taxes and operating expenses; (v) changes in zoning laws; (vi) casualty and condemnation losses; (vii) variations in rental income, neighborhood values or the appeal of property to tenants; (viii) the availability of financing and (ix) changes in interest rates and leverage.

Non-Diversification Risk. While the Adviser intends to invest in a number of real estate and real estate-related securities issued by different issuers and employ multiple investment strategies with respect to the Fund’s investment portfolio, it is possible that a significant amount of the Fund’s investments could be invested in the instruments of only a few companies or other issuers or that at any particular point in time one investment strategy could be more heavily weighted than the others. The focus of the Fund’s investment portfolio in any one issuer would subject the Fund to a greater degree of risk with respect to defaults by such issuer or other adverse events affecting that issuer, and the focus of the portfolio in any one industry or group of industries would subject the Fund to a greater degree of risk with respect to economic downturns relating to such industry or industries.

Equity Securities Risk. The market prices of equity securities owned by the Fund may fall over short or long periods of time. In addition, equity securities represent a share of ownership in a company, and rank after bonds and preferred stock in their claim on the company’s assets in the event of bankruptcy.

10

Table of Contents

Preferred Securities Risk. Preferred securities are subject to credit risk and interest rate risk. Interest rate risk is, in general, that the price of a debt security falls when interest rates rise. Securities with longer maturities tend to be more sensitive to interest rate changes. Credit risk is the risk that an issuer of a security may not be able to make principal and interest or dividend payments on the security as they become due. Holders of preferred securities may not receive dividends, or the payment can be deferred for some period of time. In bankruptcy, creditors are generally paid before the holders of preferred securities.

Repurchase Policy Risks. Quarterly repurchases by the Fund of its shares typically will be funded from available cash or sales of portfolio securities. However, payment for repurchased shares may require the Fund to liquidate portfolio holdings earlier than the Adviser otherwise would liquidate such holdings, potentially resulting in losses, and may increase the Fund’s portfolio turnover. The Adviser may take measures to attempt to avoid or minimize such potential losses and turnover, and instead of liquidating portfolio holdings, may borrow money to finance repurchases of shares. If the Fund borrows to finance repurchases, interest on any such borrowings will negatively affect shareholders who do not tender their shares in a repurchase offer by increasing the Fund’s expenses and reducing net investment income. The Fund’s quarterly repurchase offers are a shareholder’s only means of liquidity with respect to his or her shares.

Risks Relating to Fund’s Tax Status. To remain eligible for the special tax treatment accorded to RICs and their shareholders under the Internal Revenue Code of 1986, as amended (the “Code”), the Fund must meet certain source of income, asset diversification and annual distribution requirements. If the Fund were to fail to comply with the income, diversification or distribution requirements, all of its taxable income regardless of whether timely distributed to shareholders would be subject to corporate-level tax and all of its distributions from earnings and profits (including from net long-term capital gains) would be taxable to shareholders as ordinary income. In any such event, the resulting corporate taxes could substantially reduce the Fund’s net assets, the amount of income available for distribution and the amount of its distributions. Any such failure would have a material adverse effect on the Fund and its shareholders.

RIC-Related Risks of Investments Generating Non-Cash Taxable Income. Certain of the Fund’s investments will require the Fund to recognize taxable income in a taxable year in excess of the cash generated on those investments during that year. In particular, the Fund expects that a portion of its investments in loans and other debt obligations will be treated as having “market discount” and/or “original issue discount” for U.S. federal income tax purposes, which, in some cases, could be significant. Because the Fund may be required to recognize income in respect of these investments before or without receiving cash representing such income, the Fund may have difficulty satisfying the annual distribution requirements applicable to RICs and avoiding Fund-level U.S. federal income or excise taxes. Accordingly, the Fund may be required to sell portfolio securities, including at potentially disadvantageous times or prices, raise additional debt or equity capital, or reduce new investments, to obtain the cash needed to make these income distributions. If the Fund liquidates portfolio securities to raise cash, the Fund may realize gain or loss on such liquidations; in the event the Fund realizes net long-term or short-term capital gains from such liquidation transactions, its shareholders may receive larger capital gain or ordinary dividends, respectively, than they would in the absence of such transactions.

REIT Tax Risk for REIT Subsidiaries. We intend to form one or more subsidiaries that will elect to be taxed as REITs beginning with the first year in which they commence material operations. In order for each subsidiary to qualify and maintain its qualification as a REIT, it must satisfy certain requirements set forth in the Code and Treasury Regulations that depend on various factual matters and circumstances. The Fund and the Adviser intend to structure each REIT subsidiary and its activities in a manner designed to satisfy all of these requirements. However, the application of such requirements is not entirely clear, and it is possible that the Internal Revenue Service (“IRS”) may interpret or apply those requirements in a manner that jeopardizes the ability of such REIT subsidiary to satisfy all of the requirements for qualification as a REIT.

11

Table of Contents

If a REIT subsidiary fails to qualify as a REIT for any taxable year and it does not qualify for certain statutory relief provisions, it will be subject to U.S. federal income tax on its taxable income at corporate rates. In addition, it will generally be disqualified from treatment as a REIT for the four taxable years following the year of losing its REIT status.

U.S. Federal Income Tax Matters

The Fund intends to elect to be taxed for U.S. federal income tax purposes, and intend to qualify annually thereafter, as a RIC under Subchapter M of the Code. As a RIC, the Fund generally will not have to pay corporate-level U.S. federal income taxes on any ordinary income or capital gain that it distributes to its shareholders from its taxable earnings and profits. Even if the Fund qualifies as a RIC, it generally will be subject to corporate-level U.S. federal income tax on its undistributed taxable income and could be subject to U.S. federal excise, state, local and foreign taxes. To obtain and maintain RIC tax treatment, the Fund must meet specified source-of-income and asset diversification requirements and distribute annually at least 90% of its ordinary income and net short-term capital gain in excess of net long-term capital loss, if any. See “U.S. Federal Income Tax Matters.”

Distribution Policy

The Fund’s distribution policy is to make monthly distributions to shareholders. The Board has the ultimate discretion as to whether such distributions will be in stock or in cash. However, this distribution policy is subject to change and there is no guarantee the target rate will be achieved. Unless a shareholder elects otherwise, the shareholder’s distributions will be reinvested in additional shares under the Fund’s distribution reinvestment policy. Shareholders who elect not to participate in the Fund’s distribution reinvestment policy will receive all distributions in cash paid to the shareholder of record (or, if the shares are held in street or other nominee name, then to such nominee). See “Distribution Policy” and “Distribution Reinvestment Policy.”

Custodian

State Street will serve as the Fund’s custodian. See “Management of the Fund.”

12

Table of Contents

The following table is intended to assist you in understanding the costs and expenses that an investor in this offering will bear directly or indirectly. We caution you that some of the percentages indicated in the table below are estimates and may vary. The information in the table below includes the fees and expenses expected to be incurred during the twelve months following effectiveness of the offering.

| Class Z Shares | ||

| Shareholder Transaction Expenses1 |

||

| Maximum Sales Load (as a percent of offering price) |

None | |

| Contingent Deferred Sales Charge2 |

None | |

| Exchange Fee |

None | |

| Annual Expenses (as a percentage of net assets attributable to shares) |

||

| Management Fees3 |

1.67% | |

| Interest Payments on Borrowed Funds4 |

0.51% | |

| Other Expenses5 |

2.18% | |

| Distribution Fee6 |

None | |

| Shareholder Servicing Fee |

None | |

| Acquired Fund Fees and Expenses7 |

None | |

|

| ||

| Total Annual Expenses |

4.36% | |

| Fee Waiver and Reimbursement8 |

(1.52)% | |

|

| ||

| Total Annual Expenses (after fee waiver and reimbursement)9 |

2.84% |

| 1. | The amounts shown in the table assume that the registration statement of which this prospectus forms a part is declared effective by the SEC and that the Fund sells $50.0 million worth of its shares of beneficial interest ratably during the twelve months following effectiveness of the registration statement, that the Fund’s net offering proceeds from such sales equal approximately $46.88 million, that the Fund’s average net assets during such period equal one-half of the net offering proceeds, or approximately $23.44 million, and that the Fund borrows funds equal to 25% of its average net assets during such period, or approximately $5.86 million. Actual expenses will depend on the number of shares the Fund sells in this offering and the amount of leverage it employs. If the Fund is unable to raise $50.0 million during the twelve months following effectiveness of the registration statement, its expenses as a percentage of the offering price would be significantly higher, to the extent applicable pursuant to the Expense Limitation Agreement. There can be no assurance that the Fund will sell $50.0 million worth of its common shares during the twelve months following effectiveness of the registration statement. |

| 2. | Class Z shares are not subject to a contingent deferred sales charge. |

| 3. | The SEC requires that the “management fees” percentage be shown as a percentage of net assets attributable to common shareholders, rather than total assets, including assets that have been funded with borrowed monies because common shareholders bear all of this cost. The management fee in the table above assumes borrowings to fund investments of approximately $5.86 million at the end of the first twelve months following effectiveness of the registration statement. |

| 4. | The Fund may borrow funds to make investments, including before it has fully invested the initial proceeds of this offering. The costs associated with any such outstanding borrowings, as well as issuing and servicing debt securities or issuing preferred stock, would be indirectly borne by its investors. The figure in the table assumes the Fund borrows for investment purposes an amount equal to 25% of its average net assets (including such borrowed funds) during such period and that the annual interest rate on the amount borrowed is 3.0%. The Fund’s ability to incur leverage during the twelve months following effectiveness of the registration statement depends, in large part, on the amount of money the Fund is able to raise through |

13

Table of Contents

| the sale of shares registered in this offering and capital markets conditions. The Fund does not plan to issue preferred stock during the twelve months following effectiveness of the registration statement. |

| 5. | Other expenses include accounting, legal and auditing fees, reimbursement of the compensation for administrative personnel, fees payable to the Fund’s independent trustees and expenses associated with the formation and qualification under the REIT rules of any REITs wholly-owned by the Fund, but does not include the operating expenses of the REITs wholly-owned by the Fund. The amount shown in the Fees and Fund Expenses table reflects the amount of all such other expenses expected to be incurred during the twelve months following effectiveness of the registration statement. |

| 6. | Class Z shares are not subject to a Distribution Fee. See “Plan of Distribution.” |

| 7. | Acquired Fund Fees and Expenses are the indirect costs of investing in other investment companies. These indirect costs may include performance fees paid to the Acquired Fund’s adviser or its affiliates. It does not include brokerage or transaction costs incurred by the Acquired Funds. The operating expenses in this fee table will not correlate to the expense ratio in the Fund’s financial highlights because the financial statements include only the direct operating expenses incurred by the Fund. We believe that the amounts under this line item will be less than 1 basis point. Therefore, any such estimated amounts are included in other expenses. |

| 8. | The Adviser and the Fund have entered into an Expense Limitation Agreement under which the Adviser has agreed contractually to waive its fees and to pay or absorb the ordinary annual operating expenses of the Fund (including organizational and offering expenses, but excluding interest, dividend expenses on short sales, brokerage commissions, acquired fund fees and expenses, taxes and extraordinary expenses), to the extent that they exceed 1.75% per annum of the Fund’s average Daily Gross Assets for Class Z shares (the “Expense Limitation”). If the Fund incurs expenses excluded from the Expense Limitation Agreement, the Fund’s expense ratio would be higher and could exceed the Expense Limitation. In consideration of the Adviser’s agreement to limit the Fund’s expenses, the Fund has agreed to repay the Adviser in the amount of any fees waived and Fund expenses paid or absorbed, subject to the limitations that: (1) the reimbursement for fees and expenses will be made only if payable not more than three years from the date of the reimbursement; and (2) the reimbursement may not be made if it would cause the Expense Limitation as of the time of waiver to be exceeded. The Expense Limitation Agreement will remain in effect at least until one year after the effective date of this registration statement unless and until the Board approves its modification or termination. The Expense Limitation Agreement may be terminated only by the Board. There can be no assurance that the Expense Limitation Agreement will be renewed. After the expiration of the Expense Limitation Agreement, the agreement may be renewed at the discretion of the Adviser and the Board. See “Management of the Fund.” |

| The Expense Limitation Agreement provides that the Fund will carry forward the amount of any foregone fees or “other expenses” paid, absorbed or reimbursed by the Adviser (the “Excess Expenses”), for a period not to exceed three years from the end of the fiscal quarter in which such fees are foregone or expense is incurred by the Adviser (the “Recoupment Period”) and that the Adviser is entitled to recoup from the Fund the amount of such Excess Expenses during the Recoupment Period to the extent that such recoupment does not cause the Fund’s “other expenses” plus recoupment to exceed the lesser of any operating expense limits in effect at the time of the original waiver or expense reimbursement and at the time of recoupment or reimbursement. The Adviser will not seek to recoup Excess Expenses if the then current distribution rate to shareholders is less than the distribution rate to shareholders in effect at the time the Excess Expenses were paid by the Adviser. |

| 9. | The value included in the “Total Annual Expenses” line item corresponds to the Expense Limitation pursuant to the Expense Limitation Agreement. The value in the “Fees and Fund Expenses” table is presented as a percentage of net assets, while the Expense Limitation, pursuant to the Expense Limitation Agreement, is calculated based on average Daily Gross Assets, but converted and expressed as a percentage of net assets for purposes of the fees and fund expenses table presentation. |

The Fees and Fund Expenses Table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. You may qualify for sales charge discounts on purchases of shares if you and your family invest, or agree to invest in the future, at least $50,000 in the Fund. More information about these and other discounts is available from your financial professional and in “Plan of Distribution – Purchasing Shares” starting on page 59 of this prospectus. More information about management fees, fee waivers and other expenses is available in “Management of the Fund” starting on page 43 of this prospectus.

14

Table of Contents

EXAMPLE

The following example illustrates the hypothetical expenses that you would pay on a $1,000 investment assuming annual expenses attributable to shares remain unchanged and shares earn a 5% annual return. The example reflects total annual expenses after fee waivers and expense reimbursements for the one-year period and the first year of the three-, five-, and ten-year periods:

| Example |

1 Year |

3 Years |

5 Years |

10 Years |

||||||||||||

| Class Z Shares |

$ | 29 | $ | 118 | $ | 209 | $ | 442 | ||||||||

The example should not be considered a representation of actual future expenses. Actual expenses may be higher or lower than those shown.

If shareholders request repurchase proceeds be paid by wire transfer, such shareholders will be assessed an outgoing wire transfer fee at prevailing rates charged by DST, currently $10.00. The purpose of the above table is to help a holder of shares understand the fees and expenses that such holder would bear directly or indirectly. There can be no assurance that the Expense Limitation Agreement will be renewed. In the event the Expense Limitation Agreement is terminated by either party, investors will likely bear higher expenses.

Because the Fund is newly-formed and has no performance history as of the date of this prospectus, a financial highlights table for the Fund has not been included in this prospectus.

The Fund is a newly-organized, continuously offered, non-diversified, closed-end management investment company that intends to operate as an interval fund. The Fund was organized as a Delaware statutory trust on January 11, 2016 and has no operating history. The Fund’s principal office is located at 300 Crescent Court, Suite 700, Dallas, Texas 75201, and its telephone number is (972) 628-4100.

The net proceeds of the continuous offering of shares will be invested in accordance with the Fund’s investment objective and policies (as stated below) as soon as practicable after receipt. The Fund is not required to raise a minimum amount of proceeds from this offering in order to commence operations. The Fund will pay its organizational and offering expenses incurred with respect to its initial and continuous offering, less amounts advanced pursuant to the Expense Limitation Agreement. Pending investment of the net proceeds in accordance with the Fund’s investment objective and policies, the Fund will invest in money market or short-term, high quality fixed-income mutual funds. Investors should expect, therefore, that before the Fund has fully invested the proceeds of the offering in accordance with its investment objective and policies, the Fund’s assets would earn interest income at a modest rate which may be less than the Fund’s distribution rate. Our distributions may exceed our earnings and profits, especially during any period before we have invested substantially all of the proceeds from this offering. As a result, a portion of the distributions we make may represent a return of capital for tax purposes. A return of capital is a return of your investment rather than a return of earnings or gains derived from our investment activities. Any invested capital that is returned to shareholders will be reduced by the Fund’s fees and expenses, as well as the applicable sales load, which is non-refundable.

15

Table of Contents

INVESTMENT OBJECTIVE, POLICIES AND STRATEGIES

Investment Objective and Policies

Investment Objective. The Fund’s investment objective is to seek long-term total return, with an emphasis on current income, by primarily investing in a broad range of private and public real estate-related debt, equity and preferred equity investments. There can be no assurance that the Fund will achieve this objective. The Fund’s investment objective is non-fundamental and may be changed by the Board of Trustees without shareholder approval. Shareholders will, however, receive at least 60 days’ prior notice of any change in this investment objective.

Investment Strategy. The Fund will pursue its investment objective by investing, under normal circumstances, at least 80% of its assets in “real estate and real estate related securities” (as defined below). In particular, the Fund will pursue its investment objective by investing the Fund’s assets primarily in (1) CMBS and RMBS, (2) direct preferred equity and mezzanine investments in real properties (3) equity securities of public (both traded and non-traded) and private debt and equity REITs and/or REOCs and (4) opportunistic and value added direct real estate strategies (through a wholly-owned REIT).

Preferred equity and mezzanine investments in real estate transactions come in various forms which may or may not be documented in the borrower’s organizational documents. Generally, real estate preferred equity and/or mezzanine investments are typically junior to first mortgage financing but senior to the borrower’s or sponsor’s equity contribution. The investments are typically structured as an investment by a third-party investor in the real estate owner or various affiliates in the chain of ownership in exchange for a direct or indirect ownership interest in the real estate owner entitling it to a preferred/priority return on its investment. Sometimes, the investment is structured much like a loan where (i) “interest” on the investment is required to be paid monthly by the “borrower” regardless of available property cash flow; (ii) the entire investment is required to be paid by a certain maturity date; (iii) default rate “interest” and penalties are assessed against the “borrower” in the event payments are not made timely; and (iv) a default in the repayment of investment potentially results in the loss of management.

In addition, subject to the 15% Limitation and the 35% Limitation, the Fund may invest up to 20% of its total assets in equity or debt securities other than real estate and real estate related securities. The Adviser will evaluate each opportunity within the context of where the Adviser believes the various real estate subsectors are within the broader real estate cycle and tactically allocate among these opportunities. The Adviser has broad discretion to allocate the Fund’s assets among these investment categories and to change allocations as conditions warrant. Also, the Adviser will select investments it believes offer the best potential outcomes and relative risk to assemble the most appropriate portfolio to meet the risk-adjusted return goals of the Fund.

This portfolio construction strategy is designed to (i) recognize and allocate capital based upon where the Adviser believes we are in the current real estate cycle, and as a result (ii) minimize drawdowns during market downturns and maximize risk adjusted returns during all market cycles, though there can be no assurance that this strategy will achieve this objective. The Fund will seek to utilize debt at the Fund level to leverage its returns when the Adviser believes doing so would be accretive to returns. The Fund will rely on the expertise of the Adviser and its affiliates to determine the appropriate structure for structured credit investments, which may include, bridge loans, common and preferred equity or other debt-like positions, as well as the acquisition of such instruments from banks, servicers or other third parties.

The Fund defines “real estate and real estate related securities” to consist of common stock, convertible or non-convertible preferred stock, warrants, convertible or non-convertible secured or unsecured debt, and partnership or membership interests issued by:

| • | CMBS, RMBS and other real estate credit investments, which include existing first and second mortgages on real estate, either originated or acquired in the secondary market, and secured, unsecured and/or convertible notes offered by REOCs and REITs; |

| • | Public REITs; |

16

Table of Contents

| • | REOCs; |

| • | Private Real Estate Investment Funds; |

| • | Public Investment Funds; |

| • | Real estate ETFs; and |

| • | Non-Traded REITs and private REITs, generally wholly-owned by the Fund or wholly-owned or managed by an affiliate. |