UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________________________________________________________________

FORM 10-K

______________________________________________________________________________________________________

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2022

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

Commission File Number 001-37586

__________________________________________________________________________

(Exact name of registrant as specified in its charter)

_________________________________________________________________________

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||

| (Address of principal executive offices) | (Zip code) | ||||||||||

(Registrant’s telephone number)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class: | Trading Symbol(s) | Name of Each Exchange on Which Registered: | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

x | Accelerated filer | o | |||||||||

Non-accelerated filer | o | Smaller reporting company | |||||||||

Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark whether the Registrant is a shell company (as defined by Rule 12b-2 of the Exchange Act). Yes ☐ No x

At June 30, 2022, the aggregate market value of common stock held by non-affiliates of the Registrant was $2,401,433,359 . The market value held by non-affiliates excludes the value of those shares held by executive officers and directors of the Registrant.

The Registrant had 37,150,610 shares of common stock, $0.01 par value, outstanding at February 20, 2023.

| Documents Incorporated by Reference | |||||||||||

Ingevity Corporation

Form 10-K

INDEX

| Page No. | ||||||||||||||

2

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), and the Private Securities Litigation Reform Act of 1995 that reflect our current expectations, beliefs, plans, or forecasts with respect to, among other things, future events and financial performance. Forward-looking statements are often characterized by words or phrases such as “may,” “will,” “could,” “should,” “would,” “anticipate,” “estimate,” “expect,” “project,” “intend,” “plan,” “believe,” “target,” “prospects,” “potential,” “outlook,” “guidance,” and “forecast,” and other words, terms and phrases of similar meaning.

These statements, by their nature, involve certain estimates, expectations, projections, forecasts and assumptions, and are subject to various risks and uncertainties that are difficult to predict and often beyond our control. These risks and uncertainties may, and often do, cause actual results to differ materially from those contained in a forward-looking statement. Accordingly, readers are cautioned not to place undue reliance on any forward-looking statement. Any forward-looking statement is based on information currently available to us and speaks only as of the date that it is made. We have no duty, and undertake no obligation, to update any forward-looking statement to reflect developments occurring after the statement is made.

The risks and uncertainties that may cause actual results to differ materially from those indicated in any forward-looking may be included with the forward-looking statement itself. Other such risks and uncertainties include, but are not limited to, those discussed in Item 1A. Risk Factors in this report, as well as the following:

•we may be adversely affected by general global economic, geopolitical, and financial conditions beyond our control, including inflation and the war in Ukraine;

•we are exposed to risks related to our international sales and operations;

•adverse conditions in the automotive market have and may continue to negatively impact demand for our automotive carbon products;

•we face competition from substitute products, new technologies, and new or emerging competitors;

•if more stringent air quality standards worldwide are not adopted, our growth could be impacted;

•we may be adversely affected by a decrease in government infrastructure spending;

•adverse conditions in cyclical end markets may adversely affect demand for our products;

•our Performance Chemicals segment is highly dependent on crude tall oil ("CTO") which is limited in supply and subject to price increases that we may be unable to pass through;

•lack of access to sufficient CTO and other raw materials upon which we depend would impact our ability to produce our products;

•the inability to make or effectively integrate future acquisitions and other investments may negatively affect our results;

•we are dependent upon third parties for the provision of certain critical operating services at several of our facilities;

•adverse effects of the novel coronavirus ("COVID-19") pandemic;

•we may continue to be adversely affected by disruptions in our supply chain;

•the occurrence of natural disasters and extreme weather or other unanticipated problem such as labor difficulties (including work stoppages), equipment failure, or unscheduled maintenance and repair, which could result in operational disruptions of varied duration;

•we are dependent upon attracting and retaining key personnel;

•we are dependent on certain large customers;

•from time to time, we may be engaged in legal actions associated with our intellectual property rights;

•if we are unable to protect our intellectual property and other proprietary information, we may lose significant competitive advantage;

•information technology security breaches and other disruptions;

•complications with the design or implementation of our new enterprise resource planning system, including higher than anticipated associated costs;

•government policies and regulations, including, but not limited to, those affecting the environment, climate change, tax policies, tariffs, and the chemicals industry; and

•losses due to lawsuits arising out of environmental damage or personal injuries associated with chemical or other manufacturing processes.

3

PART I

ITEM 1. BUSINESS

General

Ingevity provides products and technologies that purify, protect, and enhance the world around us. Through a diverse team of talented and experienced people, we develop, manufacture, and bring to market solutions that are largely renewably sourced and help customers solve complex problems while making the world more sustainable. Our products are used in a variety of demanding applications, including automotive components that reduce gasoline vapor emissions, asphalt paving, road striping, oil exploration and production, agrochemicals, adhesives, lubricants, publication inks, coatings, elastomers, and bioplastics. We operate in two reporting segments: Performance Materials and Performance Chemicals.

Throughout this Annual Report on Form 10-K, except where otherwise stated or indicated by the context, "Ingevity," the "Company," "we," "us," or "our" means Ingevity Corporation and its consolidated subsidiaries and their predecessors.

Our business originated as part of the operations of our former parent company, Westvaco Corporation, in 1964, and we operated as a division of Westvaco Corporation and its corporate successors, including MeadWestvaco Corporation and WestRock Company (“WestRock”) until our separation from WestRock in May 2016. Our common stock began "regular-way" trading on the New York Stock Exchange in May 2016 under the symbol "NGVT."

Our principal executive offices are located at 4920 O'Hear Avenue, Suite 400, North Charleston, South Carolina 29405. Ingevity maintains a website at www.ingevity.com. We make available, free of charge through our website, our filings with the Securities and Exchange Commission (the “SEC”), including our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports, as soon as reasonably practicable after such items are filed with, or furnished to, the SEC. We also use our website to publish additional information that may be important to investors, such as presentations to analysts. Information contained in or connected to our website is not incorporated by reference into this Annual Report on Form 10-K. Reports we file with the SEC may also be viewed at www.sec.gov.

The table below illustrates our product lines and the primary end uses for our products by segment, as well as our revenue by segment for the fiscal year 2022. For more information on our U.S. and foreign operations, see Notes 4 and 19, to the Consolidated Financial Statements included within Part II. Item 8 of this Form 10-K.

| Performance Materials | Performance Chemicals | |||||||||||||

| Product Lines | Pavement Technologies | Industrial Specialties | Engineered Polymers | |||||||||||

| Primary End Uses | Gasoline vapor emissions control Purification of food, water, beverages, and chemicals | Warm mix asphalt Pavement preservation Pavement reconstruction and recycling Thermoplastic pavement markings | Adhesives Agrochemicals Lubricants Printing inks Industrial intermediates Oilfield | Coatings Resins Elastomers Adhesives Bioplastics Medical devices | ||||||||||

| 2022 Revenue | $548.5 million | $1,119.8 million | ||||||||||||

Governmental Regulations

Our manufacturing operations are subject to regulation by governmental and other regulatory authorities with jurisdiction over our operations. These regulations include the discharge of materials into the environment, the handling, storage, transportation, disposal, and clean-up of chemicals and waste materials, and otherwise relating to the protection of the environment, as well as other operational regulations, such as the Occupational Safety and Health Act ("OSHA") and the Toxic

4

Substances Control Act ("TSCA") in the U.S. and the Registration, Evaluation and Authorization of Chemicals ("REACH"), directives in the European Union, the United Kingdom ("UK"), and other countries. It is not possible to quantify with certainty the material effects that compliance with these regulations may have upon the capital expenditures, earnings, or competitive position of Ingevity, but we currently anticipate that such compliance will not have a material adverse effect on any of the foregoing. Environmental and other regulations and related legal proceedings have the potential to involve significant costs and liability for Ingevity.

Intellectual Property

Intellectual property, including patents, closely guarded trade secrets, and highly proprietary manufacturing know-how, as well as other proprietary rights, is a critical part of maintaining our technology leadership and competitive edge. Our business strategy includes filing patent and trademark applications where appropriate for proprietary developments, as well as protecting our trade secrets. We actively create, protect, and enforce our intellectual property rights. We are filing for and being granted patents for product and process developments for our Performance Materials business that we believe are both novel and consistent with trends in the technological development of engines. Our Evotherm® Warm Mix Asphalt technology is supported by numerous global patents. Additionally, our caprolactone and related technologies are supported by numerous global patents and trademarks, as well as proprietary manufacturing and technical know-how. The protection afforded by our patents and trademarks varies based on country, scope, and coverage, as well as the availability of legal remedies. Although our intellectual property taken as a whole is material to the business, there is no individual patent or trademark the loss of which could have a material adverse effect on the business.

On July 19, 2018, Ingevity filed suit against BASF Corporation (“BASF”) in the United States District Court for the District of Delaware (the “Delaware Proceeding”) alleging BASF infringed Ingevity’s patent covering canister systems used in the control of automotive gasoline vapor emissions (U.S. Patent No. RE38,844) (the “844 Patent”). On February 14, 2019, BASF asserted counterclaims against Ingevity in the Delaware Proceeding, alleging two claims for violations of U.S. antitrust law (one for exclusive dealing and the other for tying) as well as a claim for tortious interference with an alleged prospective business relationship between BASF and a BASF customer (the “BASF Counterclaims”). The BASF Counterclaims relate to Ingevity’s enforcement of the 844 Patent and Ingevity’s entry into several supply agreements with customers of its fuel vapor canister honeycombs. The U.S. District Court dismissed Ingevity’s patent infringement claims on November 18, 2020, and the case proceeded to trial on the BASF Counterclaims in September 2021.

On September 15, 2021, a jury in the Delaware Proceeding issued a verdict in favor of BASF on the BASF Counterclaims and awarded BASF damages of approximately $28.3 million, which will be trebled under U.S. antitrust law to approximately $85.0 million when the court enters judgment. In addition, BASF may seek pre- and post-judgment interest and attorneys’ fees and costs in amounts that they will have to support at a future date.

We disagree with the verdict, including the court’s application of the law, and we intend to seek judgment as a matter of law in the Delaware Proceeding post-trial briefing stage and on appeal, if necessary. In addition, we intend to challenge the U.S. District Court’s November 2020 dismissal of our patent infringement claims against BASF. Ingevity believes in the strength of its intellectual property and the merits of its position and intends to pursue all legal relief available to challenge these outcomes in the Delaware Proceeding. The final resolution of these matters could take up to eighteen months.

Seasonality

There are a variety of seasonal dynamics, including global climate and weather conditions, that impact our businesses, though none have currently materially affected our financial results, except in the case of the pavement technologies product line, where roughly 70 to 75 percent of revenue is generated between April and September. From a supply perspective, this seasonality is effectively managed through pre-season inventory build and active inventory management throughout the year.

Energy

Our manufacturing processes require a significant amount of energy. We are dependent on natural gas to fuel the processes in our chemical refineries and activated carbon plants. Although we believe that we currently have a stable natural gas supply and infrastructure for our operations, we are subject to volatility in the market price of natural gas. We enter into certain derivative financial instruments to mitigate expected fluctuations in market prices and the volatility of earnings and cash flow resulting from changes to the pricing of natural gas purchases. All of our manufacturing processes also consume a

5

significant amount of electricity. Each of these facilities are located in regulated service areas that have stable rate structures with reliable electricity supply.

Leveraging Sustainability

Throughout our Performance Chemicals and Performance Materials portfolios, we are a leader in adding value to products made from renewable materials and in derivatizing technologies that impart desirable environmental benefits in their use. To create a majority of our chemistries, we take crude tall oil from pine trees, hardwood sawdust (both co-products of the lumber, paper, and furniture-making industries), and vegetable oils and convert them into products that benefit customers, the environment, and society.

For the caprolactone-based products in our Performance Chemicals segment – although derived from traditional feedstocks – these solutions enable performance attributes in end-use markets that directly help customers and consumers meet sustainability goals. The superior durability of capa-based polyurethane technologies extends product life and the biodegradable performance of our thermoplastic polycaprolactones offers compostable end of-life solutions.

Put simply: Ingevity’s products help customers reduce their ecological impact. Our asphalt emulsifiers enable pavement recycling that reuses up to 100 percent of existing materials to create longer-lasting roads. Our automotive activated carbon products improve the air we breathe by recovering 8 million gallons of gasoline daily. Our lubricant technologies increase tool life and simplify formulations. And our alternative-fuel vehicle technology enables the use of renewable natural gas as fuel for pickup trucks and busses.

Our business is built on our ability to maximize the value and utility of materials over their lifecycle, and we will continue to enhance this value proposition through future acquisitions and new product development.

Human Capital Management

Talent

Our employees are critical to our success, and we strive to provide a safe, rewarding, and respectful workplace where our people are provided with opportunities to pursue career paths based on skills, performance, and potential. Our success depends, in part, on our ability to attract, retain and motivate critical resources across production, technical, engineering, sales, and various functional disciplines. If an ongoing failure to attract and retain individuals in key business roles and functions materialized, it could adversely affect our financial condition and operational results.

We currently employ approximately 2,050 employees, of whom approximately 77 percent are employed in the U.S. Approximately 19 percent of our employees are represented by domestic (i.e., U.S.) labor unions under various collective bargaining agreements ("CBA"). We engage in negotiations with labor unions for new CBAs from time to time based on expiration dates of agreements and statutory requirements. We consider our relationships with all salaried, union-hourly, and non-hourly employees to be positive and collaborative.

During the second quarter of 2022, at our Covington, Virginia Performance Materials' facility, the International Brotherhood of Electrical Workers (“IBEW”) AFL-CIO Local Union 464 ratified a four-year CBA, which expires January 15, 2025. In the third quarter of 2022, at our Covington Virginia Performance Materials' facility, the Covington Paper Workers Union, Local 675, affiliated with the Association of Western Pulp and Paper Workers ratified a four-year CBA which expires December 1, 2025. In the fourth quarter of 2022, at our Charleston South Carolina Performance Chemicals’ facility: (1) the United Steel, Paper, Forestry, Rubber, Manufacturing, Energy, Allied Industrial and Service Workers International Union (“USW”) on behalf of its Local Union 9-0508-02, ratified a four-year CBA, which expires June 30, 2026, and (2) the International Association of Machinists and Aerospace Workers (“IAM”) and its Charleston Lodge No. 183, ratified a four-year CBA, which expires June 30, 2026. In addition, the CBA at our Wickliffe, Kentucky Performance Materials facility with the USW, on behalf of its affiliated Local Union 0775, expired on February 1, 2023. The parties began contract renewal negotiations in January 2023.

Diversity, Equity & Inclusion

At Ingevity, we are committed to fostering a culture where we recognize, celebrate, and welcome the ways in which each other's unique backgrounds, experiences and perspectives help us reach the best solutions for our customers. To support us in developing practical and thoughtful ways to embed these principles into our everyday work, we created a dedicated team to advance diversity, equity, and inclusion ("DEI").

6

A strategic and intentional focus on DEI enhances the employee experience and satisfaction. It also supports more effective innovation, enhanced customer experience, and a deeper understanding of the communities Ingevity serves. Our diversity recruiting strategy is focused on ensuring everyone has an equitable experience by diversifying our talent pipeline through diverse candidate slates and interview teams as well as gender-neutral job descriptions. We are also enhancing our partnerships with organizations such as the National Society of Black Engineers (NSBE), National Black MBA Association, Society of Women Engineers (SWE), Society of Hispanic Engineers (SHPE), Society of Asian Scientist and Engineers (SASE), Corporate Gray, an organization that focuses on military recruiting, and historically black colleges and universities to broaden our candidate pool.

Our focus on advancing the diversity makeup of our leadership continues to positively impact our growth and success. Today, our board of directors is 30 percent women and 20 percent racially and ethnically diverse, and our executive team is 38 percent women-led and 13 percent racially and ethnically diverse. Our Women’s Network employee resource group ("ERG") has served many years as a catalyst for building community, supporting personal and professional development, and strengthening our business impact internally and externally. We also recently launched two new ERGs in support of our Black and Hispanic employees. ERGs aim to foster a richer and more diverse workplace by promoting a positive and inclusive employee experience.

Performance Management

We evaluate employee performance holistically, looking at the progress against goals, behaviors, feedback, and direct contributions of the employee and their level of impact on the business. Performance measurement includes accomplishments that supported the team, our company, internal and external customers, and our core values. In 2022, we modified our approach to create a more formalized record of employee performance at mid-year and year-end, including a new requirement for everyone at Ingevity to request feedback from colleagues who have insight into the respective employee's performance and contributions. We have a structured performance assessment review at least twice a year and continued to promote ongoing conversations between managers and employees to improve performance, drive business results, and increase employee engagement. Performance conversations often occur monthly or more frequently. The slight process enhancements allow Ingevity to cultivate a well-rounded view of each employee's strengths and identify opportunities for learning and growth.

Health & Safety

Ingevity has a world-class safety program and a strong safety culture. Personal, process, and public safety are core values at Ingevity. We work hard to protect employees, contractors, and the communities where we operate from injuries, illnesses and incidents through the design and delivery of safe operations, continuous improvement of personal and process safety performance, management systems, and programs, a strong culture of compliance, and a commitment to zero harm to people and the environment.

In 2022, we continued our efforts to increase reporting of and response to near miss incidents to prevent more serious injuries before they could occur. This included efforts to increase the number of near misses reported and an increase in reporting by a broader number of employees. We also continued to improve safety training, further expanded the use of leading indicators to ensure effective initiatives are proactively implemented, and improved incident investigation quality to ensure contributing factors are appropriately identified and addressed. Employees were trained on the importance of our Life-Saving Rules, put in place to prevent fatalities and serious injuries through leadership videos, monthly interactive training packages, and upgraded procedures, checklists, work permits, and audits. Additionally, in North America where the majority of our bulk shipments are executed, we abide by the American Chemistry Council’s Responsible Care practices of transporting our chemicals safely. We strategically utilize logistics providers that have committed to these higher standards of Safety, Security, Stewardship, and the Environment.

Segments

Performance Materials

We engineer, manufacture, and sell hardwood-based, chemically activated carbon products, which are produced through a highly technical and specialized process primarily for use in gasoline vapor emission control systems in cars, trucks, motorcycles, and boats. To maximize the productivity of our manufacturing assets, we also produce several other activated carbon products for food, water, beverage, and chemical purification applications.

Our automotive activated carbon products primarily take the form of granules, pellets, and honeycomb "scrubbers," which are primarily utilized in vehicle-based gasoline vapor emission control systems to capture gasoline vapors that would

7

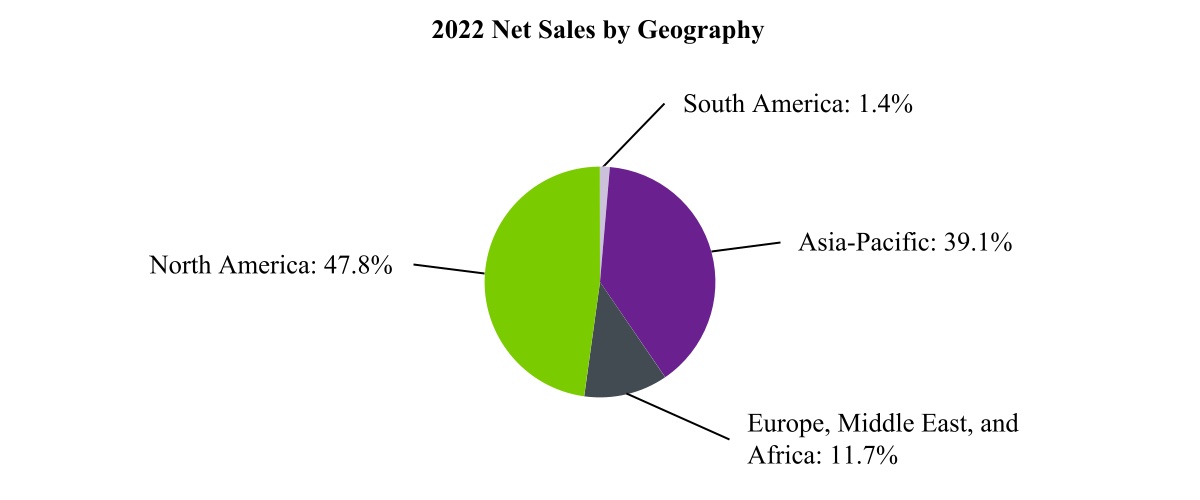

otherwise be released into the atmosphere as volatile organic compounds. The captured gasoline vapors are largely purged from the activated carbon and re-directed to the engine where they are used as supplemental power for the vehicle. In this way, our automotive activated carbon products are part of a system that improves the environment and fuel efficiency. Performance Materials' net sales for 2022, 2021, and 2020 were $548.5 million, $516.8 million, and $510.0 million, respectively. The chart below reflects our 2022 Performance Materials' net sales by geography. Sales are assigned to geographic areas based on the location of the party to which the product was shipped.

Raw Materials and Production

Our Performance Materials segment serves customers globally from three manufacturing locations in the U.S. and two in China. The primary raw material (by volume) used in the manufacture of our activated carbon is hardwood sawdust. Sawdust is readily available and is sourced through multiple suppliers to protect against supply disruptions and to maintain competitive pricing.

We also utilize phosphoric acid, which is used to chemically activate the hardwood sawdust. This phosphoric acid is sourced through multiple suppliers to protect against supply disruptions and to maintain competitive pricing. The market price of phosphoric acid is affected by the global agriculture market as the majority of global phosphate rock production is used for fertilizer production and only a portion of that production is used to manufacture purified phosphoric acid.

Customers

We sell our automotive technologies products to approximately 80 customers around the globe. In 2022, our ten largest customers accounted for approximately 89 percent of sales. We are the trusted source of these products for many of the world’s largest automotive parts manufacturers, including BorgWarner Inc. (previously Delphi Technologies PLC), A. Kayser Automotive System GmbH, Korea Fuel-Tech Corporation, MAHLE GmbH, and many other large and small component manufacturers throughout the global automotive supply chain. Our process purification products are sold to approximately 60 customers globally. We sell our automotive technologies and process purification products primarily through our own direct sales force in North America, Europe, South America, Asia, and a smaller, focused network of third-party distributors that have established a strong direct sales and marketing presence in North America and China.

Competition

Our competitors include Norit, Kuraray Co., Ltd., and several domestic U.S. manufacturers and distributors of imported products and Chinese manufacturers. Ingevity has a decades-long track record of providing activated carbon that achieves life-of-vehicle emission standards. Given the imperative for automotive manufacturers to produce vehicles for the U.S., Canada, and China markets capable of meeting life-of-vehicle emission standards, or potentially face expensive recalls and unfavorable publicity, our automotive activated carbon products provide our customers the low-risk choice for this high-performance application. Additionally, we are well-positioned to meet increasing emissions standards around the world.

8

Performance Chemicals

Ingevity’s Performance Chemicals segment is comprised of three product lines: pavement technologies, industrial specialties, and engineered polymers. Our products are utilized in warm mix paving, pavement preservation, pavement reconstruction and recycling, road striping, adhesives, agrochemical dispersants, lubricants, printing inks, coatings, resins, elastomers, bioplastics, medical devices, oil well service additives, oil production and downstream applications, and other diverse industrial uses. Our application expertise is often called upon by our customers to provide unique solutions that maximize resource efficiency. We have a broad and diverse customer base in this segment. In 2022, our top ten customers accounted for approximately 23 percent of our segment revenue, with the next 100 customers making up approximately 49 percent of our segment revenue. Performance Chemicals' net sales for 2022, 2021, and 2020 were $1,119.8 million, $874.7 million, and $706.1 million, respectively. The chart below reflects our 2022 Performance Chemicals' net sales by geography. Sales are assigned to geographic areas based on the location of the party to which the product was shipped.

Raw Materials and Production

Our Performance Chemicals segment serves customers globally from seven manufacturing locations in the U.S. and one in the UK. Most of our industrial specialties and some of our pavement technologies products are derived from crude tall oil ("CTO"), a co-product of the kraft pulping process, where pine trees are used as the source of the pulp. We also produce products derived from lignin, which is extracted from black liquor, another co-product of the kraft pulping process.

We typically source over 80 percent of our CTO needs through long-term supply contracts. The remainder of our CTO needs is sourced through short-term contracts and spot purchases in the open market. Most of our long-term contracted volumes are sourced through two primary parties: WestRock and Georgia-Pacific LLC (“Georgia-Pacific”). During 2022, we sourced approximately 75 percent of our CTO and CTO equivalent volumes of black liquor soap skimming ("BLSS"), the precursor to CTO, from WestRock and Georgia-Pacific combined. These relationships with WestRock and Georgia-Pacific are strategically important to our Performance Chemicals business due to the limited supply of CTO globally, a significant portion of which we believe is already under long-term supply agreements with other consumers of CTO.

There are other pressures on the availability of CTO. Some pulp or paper mills may choose to consume their production of CTO to meet their energy needs or reduce their carbon footprint, rather than sell the CTO to third parties. Weather conditions have in the past and may in the future affect the availability and quality of pine trees used in the kraft pulping process and, therefore, the availability of CTO that meets Ingevity’s quality standards. Geopolitical risk factors could constrain CTO availability. For example, sanctions imposed on Russia in 2022 have constrained the global CTO supply by approximately 10 percent.

Also, there are regulatory pressures that may incentivize suppliers of CTO to sell CTO into alternative fuel markets (i.e., biofuels) rather than to historical end users such as Ingevity. CTO-based biofuel has been deemed to meet the EU’s Renewable Energy Directive, second phase (“RED II”) biofuel sustainability criteria. As a consequence of RED II, there has been a significant increase in demand for CTO and its derivatives, resulting in significantly increasing prices.

9

In addition to these developments in the EU, various pieces of legislation regarding the use of alternative fuels have been introduced in the U.S. at both the federal and state level. Currently, none of the U.S. legislation mandates or provides incentives for the use of CTO or its derivatives as a biofuel. Future legislation in the U.S. and elsewhere may promote the use of CTO or its derivatives as a feedstock for the production of biofuels, further constraining supply.

Because the supply of CTO is inherently constrained by the volume of kraft pulp processing as discussed above, as well as the recent diversion of CTO for the production of alternative fuels, the availability of CTO supply as a raw material for the pine-based chemicals industry is under pressure. This pressure has increased and we expect will continue to drive the cost of CTO to unprecedented levels. CTO accounted for approximately 14 percent of our consolidated cost of sales and 22 percent of our full company raw materials purchases in 2022.

As described above, the pricing and availability of CTO are impacted by the limited supply of the product and competing demands for its use, both of which drive pressure on its price. To diversify our raw material stream, we converted a portion of our Crossett, Arkansas CTO facility to run non-CTO-based alternative fatty acids ("AFA"). We currently sell AFA as well as AFA derivatives into end markets such as oilfield and industrial applications. We have invested and will continue to invest, in AFA production capacity at our Crossett, Arkansas facility as we expand the commercialization of our product offerings in existing and new markets, which may include the biofuels market.

Our engineered polymers' products are caprolactone based, which is derived from cyclohexanone, a benzene derivative, and hydrogen peroxide, both of which are readily available in the market. We maintain multiple suppliers of cyclohexanone to protect against supply disruptions and to maintain competitive pricing. Our hydrogen peroxide is currently supplied by Solvay Interox Limited, a co-located supplier at our Warrington, UK facility under a long-term supply agreement.

The other key raw materials used in the Performance Chemicals business are maleic anhydride, pentaerythritol, and ethylene amines. These are sourced where possible through multiple suppliers to protect against supply disruptions and to maintain competitive pricing.

Markets Served

Pavement Technologies

Our pavement technologies product line produces a broad line of innovative additives and technologies utilized globally in road construction and pavement preservation, including pavement reconstruction and recycling. With the acquisition of Ozark Materials, LLC and Ozark Logistics, LLC (collectively, “Ozark Materials”), we have added road striping technologies to the portfolio.

Warm Mix Asphalt. Evotherm®, our premier road construction additive, is a warm mix asphalt technology that promotes adhesion by acting as both a liquid antistrip and a warm mix asphalt. Once Evotherm® is mixed into the binder utilized for road layer construction, production temperatures can be significantly cooler than conventional hot mix asphalt. Lower production temperatures allow our customers to reduce emissions and fuel use during road construction as well as extend their paving seasons into colder months.

Pavement Preservation. We provide an array of pavement preservation products that eliminate many traditional asphalt heating, mixing, and transportation demands – saving our customers time, energy, and money. Our technical team matches the right emulsifier and design to our customers’ materials and conditions to create high-performing emulsions. We offer a full range of specialized cationic, anionic, and amphoteric emulsifiers with additional, custom-formulated specialty additives.

Pavement Reconstruction and Recycling. We provide an array of pavement reconstruction and recycling additives that reduce the life cycle cost of pavement by enabling the milling and reuse of existing roadways. Our cold in-place recycling additives allow our customers to reopen existing roadways faster, while also lowering overall costs and jobsite emissions.

Thermoplastic Pavement Markings. We provide alkyd and hydrocarbon premium-based thermoplastic road striping technologies which provide long service life, excellent adhesion, superior color, and retro-reflectivity. Based on the customer and/or governmental agency requirements, the markings can be designed for varying levels of initial and retained performance properties.

10

Customers

We supply our pavement technologies products to approximately 650 customers in 65 countries through our own direct sales force, primarily in North America and Asia, as well as a network of third-party distributors. In 2022, our ten largest customers accounted for 42 percent of the product line's sales. Our largest customers include Colas SA, Ergon, Inc., Associated Asphalt Inc., and Idaho Asphalt Supply Inc.

Competition

Our primary competitors in pavement technologies are Nouryon Chemicals B.V., Arkema S.A., Kao Specialties Americas LLC, Sherwin-Williams Company, and PPG Industries Traffic Solutions. We compete based on deep knowledge of our customers’ businesses and extensive insights into road-building technologies and trends globally. We use these strengths to develop consulting relationships with government departments of transportation, facilitating new technology introduction into key markets around the world. Our combined expertise in the disciplines of chemistry and civil engineering provides us with a comprehensive understanding of the relationship between the molecular structure of our products and their impact on the performance of pavement systems. This allows us to develop products customized to local markets and to consistently deliver cost-effective solutions for our customers.

Industrial Specialties

Our industrial specialties product line produces and sells chemicals utilized in several industrial applications, including adhesive tackifiers, agrochemical dispersants, lubricant additives, printing ink resins, industrial intermediates, and oilfield.

Adhesives. We are a global supplier of tackifier resins, which provide superior adhesion to difficult-to-bond materials, to the adhesives industry. Adhesive applications for our products include construction, product assembly, packaging, pressure-sensitive labels and tapes, hygiene products, and road markings.

Agrochemicals. We produce dispersants for crop protection products as well as other naturally derived products for agrochemicals. Crop protection formulations are highly engineered, specifically formulated, and cover a range of different formulation types, from liquids to solids. We deliver a wide range of dispersants that are high performing and consistent. In addition, our crop protection products are approved for use as inert ingredients in agrochemicals by regulatory agencies throughout the world.

Lubricants. We supply lubricant additives and corrosion inhibitors for the metalworking and fuel additives markets. Our lubricant products are multi-functional additives that contribute to lubricity, wetting, corrosion inhibition, emulsification, and general performance efficiency. Our products are valued because of their ease in handling, robust performance, and improved formulation stability.

Printing Inks. We are a leading supplier of ink resins from renewable resources to the global graphic arts industry for the preparation of printing inks. Our products improve the gloss, drying speed, viscosity, adhesion, and rub resistance of the finished ink to the substrate. We produce a wide array of resins, typically specifically tailored to a customer’s use, which can vary by application, pigment type, end-use, formulation, manufacturing, and printing process.

Industrial Intermediates. Our functional chemistries are sold across a diverse range of industrial markets including, among others, paper chemicals, textile dyes, rubber, cleaners, mining, and nutraceuticals.

Oilfield. We supply oilfield well service additives to improve emulsion stability, aid in fluid loss control, for oil-based drilling muds. Other specialty additives, typically used in deep water applications, include rheology modifiers and wetting agents that improve viscosity properties and aid in the efficiency of the drilling process. We also supply corrosion inhibitors or their components for oil and gas production and downstream applications. Crude oil and natural gas production are characterized by variable production rates and unpredictable changes due to the nature of the produced fluids including but not limited to water and salt content, as well as supply and demand balance. Our corrosion inhibitors maximize production rates by reducing the downtime for key equipment and pipes due to corrosion.

Customers

We sell our industrial specialties products to approximately 500 customers around the globe in over 60 countries through our own direct sales representatives and third-party sales representatives and distributors. In 2022, our ten largest customers accounted for 36 percent of the product line's sales. Our largest customers include Haliburton, Solenis, Flint Group, H.B. Fuller Co., and Arboris.

11

Competition

Our competitors, which differ depending on the product, application, and region, include Kraton Corp., Eastman Chemical Co., ExxonMobil Corp., Borregaard ASA, Lawter, Inc., Repsol S.A., Firmenich SA, Lamberti S.p.A., Mobile Rosin Oil Company, Inc., as well as several others. Specific to our industrial specialty products, our customers select the product that provides the best balance of performance, consistency, and price. Reputation and loyalty are also valued by our customers and allow us to win business when other factors are equal. In adhesives, our products compete against other tackifiers, including other tall oil resin ("TOR") based tackifiers as well as tackifiers produced from gum rosin and hydrocarbon starting materials. In addition, the choice of polymer used in an adhesive formulation drives the selection of a tackifier. In agrochemicals, the selection of a dispersant is made early in the product development cycle and the formulator has a choice among our sulfonated lignin products, lower-quality lignosulfonates and other surfactants such as naphthalene sulfonates. In lubricants, we compete against other producers of distilled tall oil and additives. In printing inks, our products compete against other resins that can be derived from TOR, gum rosin and, to a lesser extent, hydrocarbon sources. In our industrial intermediates business, our tall oil fatty acid ("TOFA") competes against widely available fats and oils derived from tallow, soy, rapeseed, palm, and cotton sources. In oilfield, we compete against other tall oil specialty additives used for oil-based drilling fluids or corrosion inhibition formulations in the drilling, production and downstream applications of oilfield. We compete based on our ability to understand our customers’ applications and deliver solutions that aid in their improvement of the exploration drilling and production of oil and gas for end users. Our scale and manufacturing flexibility help us deliver the creativity, expedience, and confidence that customers in oilfield technologies require.

Engineered Polymers

Our engineered polymers product line includes caprolactone and caprolactone-based specialty polymers for use in coatings, resins, elastomers, adhesives, bioplastics, and medical devices.

Coatings. Our coating products are used in automobile refinishing, sports floors, windmill blade coatings, and marine applications. Our products enhance product performance by providing abrasion resistance, long durability, a high-quality finish, and enhanced performance in resin modification. Our products are often preferred because they provide a combination of traits that allows customers to displace several combinations of other products.

Resins. Our resin products are used in acrylic resins, polyurethane, and inks. Our products enhance product performance due to their protective properties, all-weather performance, and reduction or elimination of the need for solvents in formulations. Our products tend to be preferred where superior or particular performance levels are required.

Elastomers. Our products are used in wheels, seals, mining screens, and polyurethane films. Our products enhance product performance due to their resistance to wear and tear, ability to maintain form and function under pressure and temperature and excellent UV resistance. Our products are often used in highly demanding applications where competing products do not reach the required performance levels.

Adhesives. Our products are used in hot-melts, fabric lamination, and miscellaneous footwear components. Our products enhance product performance through their durability and substrate compatibility. Our products are often preferred because they are found to be easier to process and apply compared to competitive offerings.

Bioplastics. Our products are used in films, paper coatings, disposable cups, utensils, and packaging. Our products enhance product performance due to the combination of their biodegradability, improved mechanical properties, and wide processability when used in combination with other bioplastic solutions. Special grades are also available to help comply with food contact legislation in various regions and applications.

Medical Devices. Our products are used in medical devices. Our products enhance end-product performance due to their low melting point and ability to be thermoformed. Our products improve process conditions and provide patient comfort compared to competitive thermoplastic offerings.

Customers

We sell our engineered polymers chemicals to over 300 customers around the globe through our own direct sales representatives and third-party sales representatives and distributors. In 2022, our ten largest customers accounted for approximately 45 percent of the product line's sales. Our largest customers include polyurethane, adhesive, coatings, and bioplastics manufacturers.

12

Competition

Our primary caprolactone competitors are Daicel, Corp., Juren, and BASF SE, but we also face competition from other competing materials. We compete based on performance as compared to the other competitive materials. We also compete by strengthening our technology-focused relationships with our customers.

ITEM 1A. RISK FACTORS

Based on the information currently known to us, we believe that the following information identifies the most significant risk factors affecting the Company. However, the risks and uncertainties we face are not limited to those set forth in the risk factors described below. Additional risks and uncertainties not presently known to us or that we currently believe to be immaterial may also adversely affect our business. In addition, past financial performance may not be a reliable indicator of future performance, and historical trends should not be used to anticipate results or trends in future periods.

If any of the following risks and uncertainties develop into actual events, these events could have a material adverse effect on our business, financial condition. or results of operations. In such a case, the trading price of our Common Stock could decline.

Operational and Market Risks

Adverse conditions in the automotive market have and may continue to negatively impact demand for our automotive carbon products.

Sales of our automotive activated carbon products are tied to global internal-combustion-engine ("ICE") and hybrid electric vehicle automobile ("HEV") production levels. ICE and HEV automotive production in the markets we serve can be affected by macro-economic factors such as interest rates, fuel prices, shifts in vehicle mix (including shifts toward alternative energy vehicles), consumer confidence, employment trends, regulatory and legislative oversight requirements, and trade agreements. For example, during the first half of 2020, the COVID-19 pandemic led to a significant reduction in vehicle production, and vehicle sales were negatively impacted by government shutdown orders and stay-at-home directives. Additionally, vehicle production inputs, such as the microchip shortages during 2021 and 2022, were further impacted by the complexity of the global automotive supply chain and have resulted in reduced vehicle production and, as a result, vehicle sales, and our operating results have been negatively impacted. We currently anticipate this negative impact to lessen during 2023.

The Company’s pavement technologies product line is heavily dependent on government infrastructure spending.

A significant portion of our customers’ and our revenues in our pavement technologies business is derived from contracts with various foreign and U.S. governmental agencies, and therefore, when government spending is reduced, our customers’ demand for our products is similarly reduced. Our customers provide paving services to, for example, the governments of various jurisdictions within North America, South America, Europe, China, Brazil, and India, and we sell pavement marking materials to the governments of various jurisdictions within North America, and revenue either directly or indirectly attributable to such government spending continues to remain a significant portion of our revenues. Government business is, in general, subject to special risks and challenges, including: delays in funding and uncertainty regarding the allocation of funds to federal, state, and local agencies; delays in spending or reductions in other state and local funding dedicated to transportation projects; other government budgetary constraints, cutbacks, delays or reallocation of government funding; long purchase cycles or approval processes; our customers’ and government agencies’ competitive bidding and qualification requirements; changes in government policies and political agendas; and international conflicts or other military operations that could cause the temporary or permanent diversion of government funding from transportation or other infrastructure projects.

Certain of the Company’s products are sold into cyclical end-markets, such as the automotive market and the apparel market, which are impacted by changes in consumer and industrial demand.

Certain of our products are sold into end-markets that are cyclical and subject to frequent and rapid technology changes, changes in consumer preferences, evolving standards, and changes in product supply and demand. For example, demand for our engineered polymers products in the automotive market, where our products are formulated into automotive resins and coatings and various components, may be affected by technological advances, changing automotive original equipment manufacturer ("OEM") specifications, and global automobile production levels. Demand for our engineered

13

polymers products, where our products are sold into footwear adhesives and structural support, may be affected by consumer discretionary spending and changes in consumer preferences. Additionally, sales of our industrial specialties products may be negatively impacted due to reduced global industrial demand. The impact of these changes may lead to increased competition from competing and substitute products and downward pricing pressures on our customers, and therefore, our engineered polymers and industrial specialties product offerings.

We face competition from new technologies and new or emerging competitors.

Our industries and the end-use markets into which we sell our products experience periodic technological change and product improvement. Our future growth depends on our ability to gauge the direction of commercial and technological progress in key end-use markets, to swiftly identify and respond to disruptive technologies, and to fund and successfully develop, manufacture, and market products in such changing end-use markets. If we fail to keep pace with the evolving or disruptive technological innovations in our end-use markets on a competitive basis, our financial condition and results of operations could be adversely affected.

In the Performance Materials segment, there is competition from other activated carbon manufacturers. These competitors are trying to develop more advanced and alternative activated carbon products that could more effectively compete with our products in automotive applications. There is also competition in automotive applications from non-activated carbon competitors and product offerings. For example, multiple OEMs are using sealed tanks in certain subsets of their vehicles to comply with the strict emission regulations (i.e., Tier 3/LEV III) in the U.S. While sealed tank fuel systems generally require an increased sized pelleted activated carbon canister to deal with refueling emissions, in most cases, they do not use an extruded honeycomb to meet current U.S. and California regulations. There is also emerging competition in the "honeycomb" space, which may impact sales of the Company's products. If a competitor were to succeed in developing products that are better suited than ours for automotive evaporative emissions capture applications and/or a competitive technology, such as, but not limited to, sealed gas tanks, our financial results could be negatively impacted.

In addition, the adoption of electric and hydrogen fuel cell vehicles is increasing in the U.S. and other parts of the world. Consumer demand for these alternative-fueled vehicles is expected to continue to increase significantly in future years as certain states and international governments implement limits on the sale of vehicles with ICE with targets to completely phase out sales of such vehicles by as early as 2030. A reduction in the sales of vehicles with internal combustion engines would reduce demand for our activated carbon automotive products. Our long-term strategy is to grow our sales of products for applications in all-electric and hydrogen fuel cell vehicles to off-set the expected decline in activated carbon sales for ICE. If we are unable to develop products for all-electric and hydrogen fuel cell vehicles or grow sales fast enough, our business and results of operations could be adversely impacted. The process of designing and developing new technology and related products is complex, costly, and uncertain and may require us to retain and recruit talent in areas of expertise outside of our current core competencies. There can be no assurance that such advances in technology will be feasible or will occur in a timely and efficient manner.

Certain of our products face competition from substitute products where the costs of different raw material inputs can impact the price competitiveness of our products and negatively impact our sales and/or profits as we respond to substitute product competition.

Gum rosin-based products and hydrocarbon resins compete with our TOR-based resins in the adhesives and printing ink markets. The price of gum rosin has a significant impact on the market price for TOR and rosin derivatives and is driven by labor rates for harvesting, land leasing costs, and various other factors that are not within our control. Hydrocarbon resins, for example, C5 resins, are co-products from the manufacture of isoprene (synthetic rubber). Availability and pricing are determined by the supply/demand dynamics for synthetic rubber as well as the price of crude oil as the feedstock for isoprene and various other factors that are not within our control. Animal and vegetable-based fatty acids compete with TOFA products in lubricant and industrial specialties. The market price for TOFA products is impacted by the prices of other fats and oils, and the prices for other fats and oils are driven by actual and expected harvest rates, petroleum oil prices, and the biofuel market. Other monomers, thermoplastics, and polyols compete with our caprolactone-based products. The price for our products is impacted by the prices of competitive substitutes which are influenced by oil prices as well as other supply and demand factors. We may not be able to pass through raw material cost increases, or we may lose market share if we do not effectively manage our pricing, which in either case could negatively impact our financial results.

14

Additionally, the price of energy may directly or indirectly impact demand, pricing, or profitability for certain of our products. As petroleum oil prices can change rapidly, Ingevity products may be disadvantaged because CTO and BLSS are thinly traded commodities with pricing commonly established for periods ranging from one quarter to one-year periods. Due to this, alternative technologies which compete with product offerings provided by Ingevity may be advantaged from time to time in the marketplace. Protracted periods of high volatility or sustained oversupply of petroleum oil may also translate into increased competition from petroleum-based alternatives. In addition, pricing for competing naturally derived oils such as palm or soybean is likely to put further pressure on the pricing of the Company’s products during periods of depressed petroleum prices.

The COVID-19 pandemic has had and may continue to have, a negative impact on our business, financial condition, results of operations, and cash flows.

The COVID-19 pandemic continues to impact our operations and financial results. Our facilities, as well as the operations of our suppliers, customers, and third-party sales representatives and distributors, have been, and continue to be, disrupted by governmental and private sector responses to the COVID-19 pandemic, including, without limitation, government shutdown requirements, business shutdowns, work-from-home orders and social distancing protocols, travel or health-related restrictions, quarantines, self-isolations, and disruptions to transportation channels. These types of disruptions, or an outbreak among the employees in any of our facilities, could cause significant interruptions to, or temporary closures of, our operations and could materially adversely affect our ability to adequately staff and maintain our operations. Working remotely may eventually lead to inefficiencies, as well as technology and security risks. Additionally, we are uncertain if the extended period during which our employees are unable to travel to our facilities or those of our customers and suppliers may negatively impact our business.

Disruptions to the operations of our suppliers have at times, and may again, negatively impact our ability to purchase goods and services for our business at efficient prices and in sufficient amounts. Additionally, the operations of our customers have been and could be further, disrupted, which can result in customers attempting to delay or cancel orders, reduce future orders or seek extended payment terms. Furthermore, the negative impact of the COVID-19 pandemic on the global economy, adverse changes in the industries that our products serve or adverse changes in the financial condition of our customers could further adversely impact demand for our products, particularly in the automotive industry and industrial and consumer applications. The extent of the impact that the COVID-19 pandemic will continue to have on our business and financial results will depend on various uncertainties and future developments, including the ultimate duration, severity, and spread of the virus and any new variants in the countries where we operate and transact business, subsequent government actions, and the resulting economic impacts.

Disruptions at any of our facilities could negatively impact our production, financial condition, and results of operations.

Disruptions to any of our manufacturing operations or other facilities, due to natural disasters and extreme weather, such as a hurricane, tropical storm, earthquake, tornado, severe weather, flood, fire, or other unanticipated problems such as labor difficulties, pandemics (including the COVID-19 pandemic), equipment failure, cyberattacks or other cybersecurity incidents, capacity expansion difficulties or unscheduled maintenance, could cause operational disruptions of varied duration. Also, many of our production employees are governed by CBAs. The CBA at our North Charleston, South Carolina Performance Chemicals facility with the IBEW Local Union No. 1753 expired on June 30, 2022. The parties began contract negotiations in December 2022. In addition, the CBA at our Wickliffe, Kentucky Performance Materials facility with the USW, on behalf of its affiliated Local Union 0775, expired on February 1, 2023. The parties began contract renewal negotiations in January 2023. At both facilities, the parties continue to operate under the applicable expired CBA while negotiations are pending. While the Company has generally positive relations with its labor unions, there is no guarantee the Company will be able to successfully negotiate new union contracts without work stoppages, labor difficulties, or unfavorable terms. In addition, existing CBAs may not prevent a strike or work stoppage at the applicable plant.

These types of disruptions could materially adversely affect our financial condition and results of operations to varying degrees depending upon the facility, the duration of the disruption, and our ability to shift business to another facility or find alternative sources of manufacturing capacity. Any losses due to these events may not be covered by our existing insurance policies or may be subject to certain deductibles. In certain cases, we have products, such as our extruded honeycomb and caprolactone products, that are only made at one facility. While we have some redundancies within the facilities that are the sole manufacturer of certain products, we have limited ability to make these products at other facilities.

15

We are dependent upon third parties for the provision of certain critical operating services at several of our facilities.

We are dependent upon third parties for the provision of certain critical operating services, primarily utilities and related services (e.g., steam, compressed air, energy, water, wastewater treatment) at our Covington, Virginia Performance Materials facility and the following Performance Chemicals facilities: Crossett, Arkansas; North Charleston, South Carolina; and Warrington, UK. We have existing long-term contractual arrangements covering these services. The provision of these services would be at risk if any of the counterparties were to idle or permanently shut down their plant, or if operations were disrupted due to natural or other disaster, or by reason of strikes or other labor disruptions, or if there were a significant contractual dispute between the parties.

In the event that the applicable counterparty was to fail to provide the contracted services, we would be required to obtain these services from other third parties, most likely at an increased cost, or to expend capital to provide these services ourselves. The expenses associated with obtaining or providing these services, as well as any interruption in our operations as a result of the failure of the counterparty to provide these services, may be significant and may adversely affect our financial condition and results of operations.

Furthermore, in the event that WestRock’s Covington, VA paper mill’s wastewater treatment operations do not comply with permits or applicable law and WestRock is unable to determine the cause of such non-compliance, then we will be responsible for up to 50 percent of the costs and expenses of such noncompliance (increasing in 10 percent increments per violation during each twelve month period) despite representing less than 3 percent of the total wastewater volume. These costs and expenses may be significant and may adversely impact our financial condition and results of operations.

Additionally, several of our manufacturing facilities are leased. In the event we were to have a dispute with the landlord regarding the terms of the relevant lease agreements, or we were otherwise unable to fully access or utilize the leased property, the associated business disruption may be significant and may adversely affect our financial condition and results of operations.

We are also dependent on third parties for the disposal of brine, which results from our own conversion of BLSS into CTO. If these service providers do not perform under their contracts, the costs of disposing of brine ourselves, including, for example, the transportation costs, could be significant.

We are dependent on certain large customers.

We have certain large customers in particular businesses, the loss of which could have a material adverse effect on the applicable segment’s sales and, depending on the significance of the loss, our results of operations, financial condition, or cash flows. Sales to Ingevity’s ten largest customers (across both segments) accounted for 30 percent of total sales for 2022. No customer accounted for more than 10 percent of total sales for 2022. With some exceptions, our business with those large customers is based primarily upon individual purchase orders. As such, our customers could cease buying our products from us at any time, for any reason, with little or no recourse. If a major customer or multiple smaller customers elected not to purchase products from us, our financial condition and results of operations could be materially adversely affected.

We are dependent on attracting and retaining key personnel.

We are dependent upon our production workers, as well as upon engineering, technical, sales, and application specialists, together with experienced industry professionals and senior management. Our success depends, in part, on our ability to attract, retain and motivate key talent. Our failure to attract and retain individuals making significant contributions to our business could adversely affect our financial condition and results of operations.

The inability to make or effectively integrate future acquisitions and other investments may negatively affect our results.

As part of our growth strategy, we may pursue acquisitions of businesses and product lines or invest in joint ventures. The ability to grow through acquisitions or other investments depends upon our ability to identify, negotiate, finance, complete, and integrate suitable acquisitions or joint venture arrangements. There can be no assurances that we will be able to integrate these acquisitions in an efficient and cost-effective manner or that these acquisitions or joint ventures will generate the expected value.

16

Acquisitions and other investments may expose us to liability from the target company and/or joint venture partner. Acquisition and investment target companies may be or may become involved in disputes regarding intellectual property and other aspects of their businesses or may be subject to liabilities that are unknown at the time of the transaction, including liabilities under environmental or tax laws. Depending on the nature of our investment and/or structure of an acquisition, we may take on or be exposed to such liability, which could materially impact our business, financial condition, or results of operations.

As we rely on information technologies to conduct our business, cyber-attacks, data and privacy breaches, or a failure of information technology systems could disrupt our operations and expose us to liability, which could cause our business and reputation to suffer.

We rely on our information technology systems, some of which are managed by third parties, to support, manage and maintain the day-to-day operations and activities of our business, including our manufacturing facilities, customer and vendor transactions, and financial, accounting, and business records. In addition, we collect and store certain data, including proprietary business information, and may have access to confidential or personal information that is subject to privacy and security laws and regulations.

The secure processing, storage, and transmission of sensitive, confidential, and personal data is critical to our operations and business strategy. We have instituted a system of security policies, procedures, capabilities, internal controls and audits based on our pursuit of ISO 27001 certification, designed to protect this information. Additionally, we engage third-party threat detection, penetration testing, and monitoring services which includes a global cybersecurity incident response team. Despite our security architecture and controls, and those of our third-party providers, we may be vulnerable to cyber-attacks, computer viruses, security breaches, ransomware attacks, inadvertent or intentional employee actions, system failures, and other risks that could potentially lead to the compromising of sensitive, confidential or personal data, improper use of our, or our third-party provider systems, solutions or networks, unauthorized access, use, disclosure, modification or destruction of information, and operational disruptions. We also maintain an information security risk insurance policy to help mitigate the financial consequences of these risks, however, there is no guarantee that such a policy will be sufficient to address such costs. In addition, the global regulatory environment pertaining to information security and privacy is increasingly complex, with new and changing requirements, such as the European Union’s General Data Protection Regulation (“GDPR”), California Consumer Privacy Act (“CCPA”), and the China Cybersecurity Law and Personal Information Protection Law. GDPR, which applies to the collection, use, retention, security, processing, and transfer of personally identifiable information of residents of EU countries, mandates new compliance obligations and imposes significant fines and sanctions for violations. CCPA requires companies to provide new data disclosure, access, deletion, and opt-out rights to consumers in California. Implementing and complying with these laws and regulations may be more costly or take longer than we anticipate, or could otherwise affect our business operations. Information security breaches, cyber incidents, and disruptions, or failure to comply with laws and regulations related to information security or privacy, could result in legal claims or proceedings against us by governmental entities or individuals, significant fines, penalties or judgements, disruption of our operations, remediation requirements, changes to our business practices, and damage to our reputation, which could adversely affect our business, financial condition or results of operations.

Complications with the design or implementation of our new enterprise resource planning (“ERP”) system could adversely impact our business and operations.

We are in the process of a complex, multi-year implementation of a new ERP system that is necessary due to the finite life of the existing operating system. The ERP system implementation requires the integration of the new ERP system with multiple new and existing information systems and business processes in order to maintain the accuracy of our books and records and to provide our management team with information important to the operation of our business. Such an initiative is a major financial undertaking and requires substantial time and attention from management and key employees. The implementation of the ERP system may prove to be more difficult, costly, or time-consuming than expected, and it is possible that the system will not yield the benefits anticipated. Failure to successfully design and implement the new ERP system as planned could harm our business, financial condition, and operating results. Additionally, if we do not effectively implement the ERP system as planned or the ERP system does not operate as intended, the effectiveness of our internal control over financial reporting could be negatively impacted.

17

Supply Chain Risks

Disruptions within our supply chain have negatively impacted and could continue to negatively impact, our production, financial condition, and results of operations.

We have been, and could continue to be, adversely affected by disruptions within our supply chain and transportation network. Our products are transported by truck, rail, barge or ship primarily by third-party providers. The costs of transporting our products could be negatively affected by factors outside of our control, including rail service interruptions or rate increases, extreme weather events, tariffs, rising fuel costs, and capacity constraints. Recently, the unprecedented congestion in ocean shipping has, and could continue to, adversely impact the reliability of our export shipments to customers and imports of raw materials, and transport driver shortages experienced as a result of the COVID-19 pandemic have caused extended lead times for domestic shipments. Significant delays or increased costs relating to transportation could materially affect our financial condition and results of operations. Disruptions at our suppliers could lead to volatility or increases in raw material or energy costs and/or reduced availability of materials or energy, potentially affecting our financial condition and results of operations.

Our Performance Chemicals segment is highly dependent on CTO as a raw material, which is limited in supply, and may be subject to price increases; changing supply and demand economics for CTO could limit access to sufficient supply and/or cause price increases that we may be unable to pass through to customers.

CTO is essential to our industrial specialties and some of our pavement technologies product lines within our Performance Chemicals segment. Availability of CTO is directly linked to (as it is a co-product of) the production output of kraft mills using softwood, primarily pine trees, as their feedstock, (i.e., pulp). Softwood pulp is the predominant fiber source for packaging grades of paper as well as fluff pulp for personal care products. As a result, there is a finite global supply of CTO, with global demand for softwood pulp driving the global supply of CTO, rather than demand for CTO itself. Most of the CTO made available for sale by its producers in North America, where our manufacturing assets are located, is covered by long-term supply agreements, further constraining availability.

We typically source over 80 percent of our CTO needs through long-term supply contracts. The remainder of our CTO needs is sourced through short-term contracts and spot purchases in the open market. Most of our long-term contracted volumes are sourced through two primary parties: WestRock and Georgia-Pacific. During 2022, we sourced approximately 75 percent of our CTO and CTO equivalent volumes of BLSS, the precursor to CTO, from WestRock and Georgia-Pacific combined. These long-term CTO supply contracts permit periodic adjustment or negotiation of pricing and other terms. There can be no guarantee that pricing, CTO volume, and other terms will not be materially impacted as a result of these adjustments or negotiations. For example, effective January 1, 2022, WestRock removed a mill that had provided approximately 28,500 tons of CTO per year from our long-term supply agreement.

If any of our suppliers fail to meet their respective obligations under our supply agreements or we are otherwise unable to procure an adequate supply of CTO, we would be unable to maintain our current level of production and our results of operations could be materially and adversely affected.