UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________________________________________________________________

FORM 10-K

______________________________________________________________________________________________________

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2020

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

Commission File Number 001-37586

__________________________________________________________________________

(Exact name of registrant as specified in its charter)

_________________________________________________________________________

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||

| (Address of principal executive offices) | (Zip code) | ||||||||||

(Registrant’s telephone number)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class: | Trading Symbol(s) | Name of Each Exchange on Which Registered: | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

x | Accelerated filer | o | |||||||||

Non-accelerated filer | o | Smaller reporting company | |||||||||

Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

o

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

Indicate by check mark whether the Registrant is a shell company (as defined by Rule 12b-2 of the Exchange Act). Yes ☐ No x

At June 30, 2020, the aggregate market value of common stock held by non-affiliates of the Registrant was $2,162,317,073 . The market value held by non-affiliates excludes the value of those shares held by executive officers and directors of the Registrant.

The Registrant had 40,468,010 shares of common stock, $0.01 par value, outstanding at February 15, 2021.

| Documents Incorporated by Reference | |||||||||||

Ingevity Corporation

Form 10-K

INDEX

| Page No. | ||||||||||||||

2

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), and the Private Securities Litigation Reform Act of 1995 that reflect our current expectations, beliefs, plans or forecasts with respect to, among other things, future events and financial performance. Forward-looking statements are often characterized by words or phrases such as “may,” “will,” “could,” “should,” “would,” “anticipate,” “estimate,” “expect,” “project,” “intend,” “plan,” “believe,” “target,” “prospects,” “potential” and “forecast,” and other words, terms and phrases of similar meaning.

These statements, by their nature, involve certain estimates, expectations, projections, forecasts and assumptions and are subject to various risks and uncertainties that are difficult to predict and often beyond our control. These risks and uncertainties may, and often do, cause actual results to differ materially from those contained in a forward-looking statement. Accordingly, readers are cautioned not to place undue reliance on any forward-looking statement. Any forward-looking statement is based on information currently available to us and speaks only as of the date that it is made. We have no duty, and undertake no obligation, to update any forward-looking statement to reflect developments occurring after the statement is made.

The risks and uncertainties that may cause actual results to differ materially from those indicated in any forward-looking may be included with the forward-looking statement itself. Other such risks and uncertainties include, but are not limited to, those discussed in Item 1A. Risk Factors in this report, as well as the following:

•adverse effects from the novel coronavirus ("COVID-19") pandemic;

•we may be adversely affected by general economic and financial conditions beyond our control;

•we are exposed to risks related to our international sales and operations;

•our reported results could be adversely affected by currency exchange rates and currency devaluation could impair our competitiveness;

•our operations outside the U.S. require us to comply with a number of U.S. and foreign regulations, violations of which could have a material adverse effect on our financial condition and results of operations;

•we may be adversely affected by changes in trade policy, including the imposition of tariffs and the resulting consequences;

•adverse conditions in the global automotive market or adoption of alternative and new technologies may adversely affect demand for our automotive carbon products;

•we face competition from producers of alternative products and new technologies, and new or emerging competitors;

•we face competition from infringing intellectual property activity;

•if increasingly more stringent air quality standards worldwide are not adopted, our growth could be impacted;

•we may be adversely affected by a decrease in government infrastructure spending;

•adverse conditions in cyclical end markets may adversely affect demand for our engineered polymers products;

•our printing inks business serves customers in a market that is facing declining volumes and downward pricing;

•our Performance Chemicals segment is highly dependent on crude tall oil ("CTO") which is limited in supply;

•lack of access to sufficient CTO would impact our ability to produce CTO-based products;

•a prolonged period of low energy prices may materially impact our results of operations;

•our engineered polymers product line may be adversely affected by the United Kingdom’s ("UK") withdrawal from the European Union;

•the acquisition (the "Caprolactone Acquisition") of Perstorp Holding AB's caprolactone division (the "Caprolactone Business") may expose us to unknown or understated liabilities;

•we are dependent upon third parties for the provision of certain critical operating services at several of our facilities;

•we may be adversely affected by disruptions in our supply chain;

•the occurrence of natural disasters, such as hurricanes, winter or tropical storms, earthquakes, tornadoes, floods, fires or other unanticipated problem such as labor difficulties (including work stoppages), equipment failure or unscheduled maintenance and repair, which could result in operational disruptions of varied duration;

3

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS (CONTINUED)

•we are dependent upon attracting and retaining key personnel;

•from time to time, we are called upon to protect our intellectual property rights and proprietary information though litigation and other means;

•if we are unable to protect our intellectual property and other proprietary information, we may lose significant competitive advantage;

•information technology security breaches and other disruptions;

•complications with the design or implementation of our new enterprise resource planning system;

•government policies and regulations, including, but not limited to, those affecting the environment, climate change, tax policies, tariffs and the chemicals industry; and

•losses due to lawsuits arising out of environmental damage or personal injuries associated with chemical or other manufacturing processes.

4

PART I

Item 1. Business

General

Ingevity provides products and technologies that purify, protect, and enhance the world around us. Through a diverse team of talented and experienced people, we develop, manufacture, and bring to market solutions that are both largely renewably sourced and help customers solve complex problems, while making the world more sustainable. We operate in two reporting segments: Performance Materials and Performance Chemicals. Our products are used in a variety of demanding applications, including automotive components that reduce gasoline vapor emissions, asphalt paving, oil exploration and production, agrochemicals, adhesives, lubricants, publication inks, coatings, elastomers, and bioplastics.

Throughout this Annual Report on Form 10-K, except where otherwise stated or indicated by the context, "Ingevity", the "Company", "we", "us", or "our" means Ingevity Corporation and its consolidated subsidiaries and their predecessors.

Our business originated as part of the operations of our former parent company, Westvaco Corporation, in 1964, and we operated as a division of Westvaco Corporation and its corporate successors, including MeadWestvaco Corporation and WestRock Company (“WestRock”) until our separation from WestRock in May 2016 (the “Separation”). Our common stock began "regular-way" trading on the New York Stock Exchange in May 2016 under the symbol "NGVT." Since the Separation, we acquired substantially all of the assets used in Georgia-Pacific Chemicals LLC’s pine chemical business (the “Pine Chemical Business”) in March 2018 and acquired Perstorp Holding AB’s entire caprolactone business (the “Caprolactone Business”) in February 2019. For additional information on these acquisitions, see Note 17 to the consolidated financial statements included within Part II. Item 8 of this Form 10-K.

Our principal executive offices are located at 4920 O'Hear Avenue, Suite 400, North Charleston, South Carolina 29405. Ingevity maintains a website at www.ingevity.com. We make available, free of charge through our website, our filings with the Securities and Exchange Commission (the “SEC”), including our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports, as soon as reasonably practicable after such items are filed with, or furnished to, the SEC. We also use our website to publish additional information that may be important to investors, such as presentations to analysts. Information contained in or connected to our website is not incorporated by reference into this Annual Report on Form 10-K. Reports we file with the SEC may also be viewed at www.sec.gov.

The table below illustrates our product lines and the primary end uses for our products by segment, as well as our revenue by segment for fiscal year 2020. For more information on our U.S. and foreign operations, see Notes 5 and 20, to the consolidated financial statements included within Part II. Item 8 of this Form 10-K.

| Performance Materials | Performance Chemicals | |||||||||||||||||||

| Product Lines | Automotive Technologies | Process Purification | Pavement Technologies | Oilfield Technologies | Industrial Specialties | Engineered Polymers | ||||||||||||||

| Primary End Uses | Gasoline vapor emissions control | Purification of food, water, beverages and chemicals | Warm mix asphalt Pavement preservation Pavement reconstruction and recycling | Well service additives Production and downstream applications | Adhesives Agrochemicals Lubricants Printing inks Industrial intermediates | Coatings Resins Elastomers Adhesives Bioplastics Medical devices | ||||||||||||||

| 2020 Revenue | $510.0 million | $706.1 million | ||||||||||||||||||

5

Segments

Performance Materials

Our automotive technologies product line engineers, manufactures, and sells hardwood-based, chemically activated carbon products, produced through a highly technical and specialized process primarily for use in gasoline vapor emission control systems in cars, trucks, motorcycles, and boats. To maximize the productivity of our manufacturing assets, we also produce a number of other activated carbon products for food, water, beverage, and chemical purification applications, which are sold through our process purification product line.

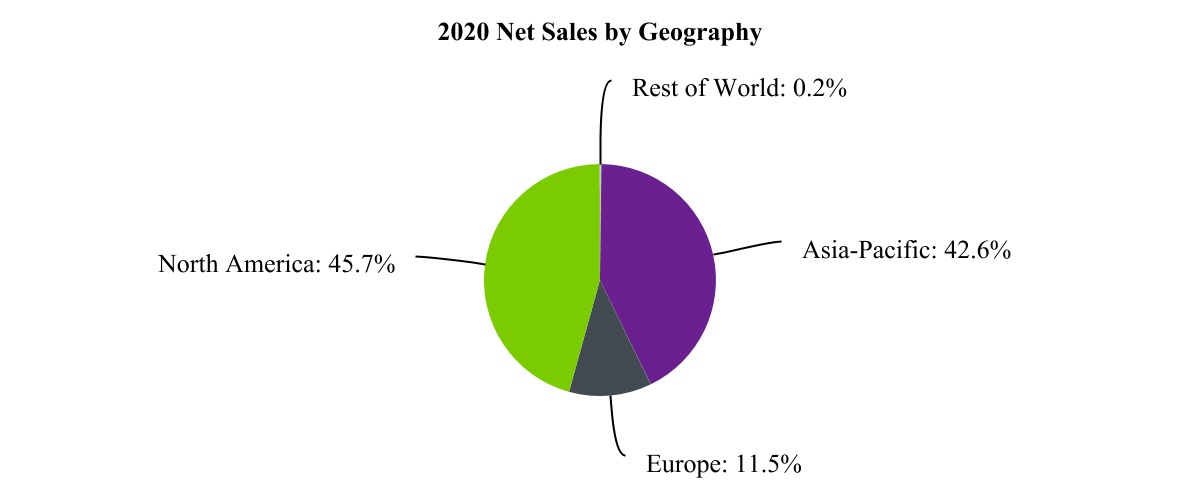

Our automotive activated carbon products primarily take the form of granular, pellets and honeycomb "scrubber", which are primarily utilized in vehicle-based gasoline vapor emission control systems that capture gasoline vapor emissions that would otherwise be released into the atmosphere as volatile organic compounds. The captured gasoline vapors are largely purged from the activated carbon and directed to the engine where they are used as supplemental power for the vehicle. In this way, our automotive activated carbon products are part of a system that provides for both environmental control and energy recovery. Performance Materials' net sales for 2020, 2019, and 2018 were $510.0 million, $490.6 million, and $400.4 million, respectively; the chart below allocates our 2020 Performance Materials' net sales by geography. Sales are assigned to geographic areas based on the location of the third party to which product was shipped.

Customers

We sell our automotive technologies products to over 60 customers around the globe. In 2020, our ten largest customers accounted for approximately 90 percent of the product line's sales. We are the trusted source of these products for many of the world’s largest automotive parts manufacturers, including BorgWarner Inc. (previously Delphi Technologies PLC), A. Kayser Automotive System GmbH, Korea Fuel-Tech Corporation, MAHLE GmbH, and many other large and small component manufacturers throughout the global automotive supply chain. Our process purification products are sold to approximately 70 customers globally. We sell our automotive technologies and process purification products primarily through our own direct sales force in North America, Europe, South America and Asia and also have a smaller, focused network of third-party distributors that have established a strong direct sales and marketing presence in North America and China.

Competition

Our automotive technologies competitors include Cabot Corp., Kuraray Co., Ltd., and several Chinese manufacturers. Ingevity has a decades-long track record of providing activated carbon that achieves life-of-vehicle emission standards. Given the imperative for automotive manufacturers to produce vehicles for the U.S., Canadian, and Chinese markets capable of meeting life-of-vehicle emission standards, or potentially face expensive recalls and unfavorable publicity, our automotive activated carbon products provide our customers the low-risk choice for this high performance application.

6

Competitors in our process purification product line include Cabot Corp., Kuraray Co., Ltd., Osaka Gas Chemicals Co., Ltd., and several domestic U.S. manufacturers and distributors of imported products.

Raw Materials and Production

Our Performance Materials segment serves customers globally from three manufacturing locations in the U.S. and two in China. The primary raw material (by volume) used in the manufacture of our activated carbon is hardwood sawdust. Sawdust is readily available and is sourced through multiple suppliers to protect against supply disruptions and to maintain competitive pricing.

We also utilize phosphoric acid, which is used to chemically activate the hardwood sawdust. This phosphoric acid is sourced through multiple suppliers to protect against supply disruptions and to maintain competitive pricing. The market price of phosphoric acid is affected by the global agriculture market as the majority of global phosphate rock production is used for fertilizer production and only a portion of that production is used to manufacture purified phosphoric acid.

Performance Chemicals

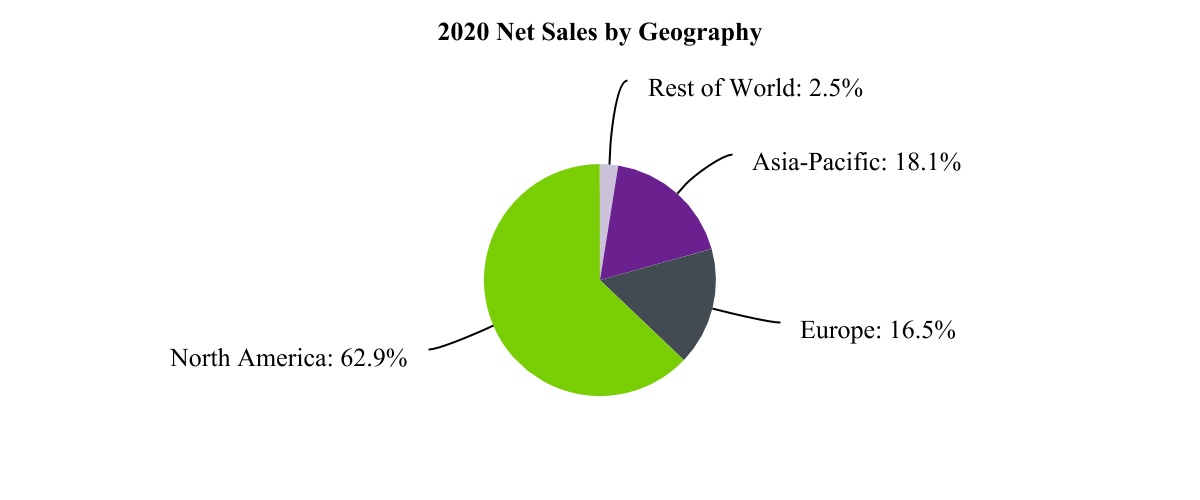

Ingevity’s Performance Chemicals segment is comprised of four product lines: pavement technologies, oilfield technologies, industrial specialties, and engineered polymers. Our products are utilized in warm mix paving, pavement preservation, pavement reconstruction and recycling, oil well service additives, oil production and downstream applications, adhesives, agrochemical dispersants, lubricants, printing inks, coatings, resins, elastomers, bioplastics, medical devices, and other diverse industrial uses. Our application expertise is often called upon by our customers to provide unique solutions that maximize resource efficiency. We have a broad and diverse customer base in this segment. In 2020, our top ten customers accounted for approximately 20 percent of our segment revenue, with the next 100 customers making up approximately 45 percent of our segment revenue. Performance Chemicals' net sales for 2020, 2019 and 2018 were $706.1 million, $802.3 million, and $733.2 million, respectively; the chart below allocates our 2020 Performance Chemicals' net sales by geography. Sales are assigned to geographic areas based on the location of the third party to which product was shipped.

Markets Served

Pavement Technologies

Our pavement technologies product line produces a broad line of innovative additives and technologies utilized globally in road construction and pavement preservation, including pavement reconstruction and recycling.

Warm Mix Asphalt. Evotherm®, our premier road construction additive, is a warm mix asphalt technology that promotes adhesion by acting as both a liquid antistrip and a warm mix asphalt. Once Evotherm is mixed into the binder utilized for road layer construction, production temperatures can be significantly cooler than conventional hot mix asphalt. Lower production temperatures allow our customers to reduce emissions and fuel use during road construction as well as extend their paving seasons into colder months.

7

Pavement Preservation. We provide an array of pavement preservation products that eliminate many traditional asphalt heating, mixing and transportation demands – saving our customers time, energy and money. Our technical team matches the right emulsifier and design to our customers’ materials and conditions to create high-performing emulsions. We offer a full range of specialized cationic, anionic and amphoteric emulsifiers with additional, custom-formulated specialty additives.

Pavement Reconstruction and Recycling. We provide an array of pavement reconstruction and recycling additives that reduce the life cycle cost of pavement by enabling the milling and reuse of existing roadways. Our cold in-place recycling additives allow our customers to reopen existing roadways faster, while also lowering overall costs and jobsite emissions.

Customers

We supply our pavement technologies products to approximately 500 customers in 60 countries through our own direct sales force, primarily in North America and Asia, as well as a network of third-party distributors. In 2020, our ten largest customers accounted for 40 percent of the product line's sales. Our largest customers include: Colas SA, Ergon, Inc., Associated Asphalt Inc., and Idaho Asphalt Supply Inc.

Competition

Our primary competitors in pavement technologies are Nouryon Chemicals B.V., Arkema S.A., and Kao Specialties Americas LLC. We compete based on deep knowledge of our customers’ businesses and extensive insights into road building technologies and trends globally. We use these strengths to develop consulting relationships with government departments of transportation, facilitating new technology introduction into key markets around the world. Our combined expertise in the disciplines of chemistry and civil engineering provides us with a comprehensive understanding of the relationship between the molecular structure of our products and their impact on the performance of pavement systems. This allows us to develop products customized to local markets and to consistently deliver cost-effective solutions for our customers.

Oilfield Technologies

Our oilfield technologies product line produces and sells a wide range of innovative specialty chemical products for the global oilfield industry, including well service additives and chemical solutions for production and downstream applications.

Well Service Additives. Our well service additive products are formulated to increase emulsion stability and aid in fluid loss control for oil-based drilling fluids. Other additives include rheology modifiers, which are used to improve the viscosity properties of oil-based fluids and are typically used in deep water applications and wetting agents, which provide improved wetting of solids and aid in the efficiency of the drilling process. This family of products aids in accessing difficult to reach oil and gas reserves, both on and offshore around the globe.

Production and Downstream Applications. Our production and downstream products serve as corrosion inhibitors or their components. Crude oil and natural gas production are characterized by variable production rates and unpredictable changes due to the nature of the produced fluids including but not limited to water and salt content. Our corrosion inhibitors maximize production rates by reducing the downtime for key equipment and pipes due to corrosion.

Customers

We sell our oilfield technologies products to approximately 70 customers around the globe using our own sales representatives and third-party distributors. In 2020, our ten largest customers accounted for 70 percent of the product line's sales. Our largest customers include Ecolab, Inc., Halliburton Co., Schlumberger Ltd., and Newpark Resources, Inc.

Competition

Our primary oilfield technologies competitors include Lamberti S.p.A., Mobile Rosin Oil Company, Inc., and First Source Technologies, Inc. We compete based on our ability to understand our customers’ applications and deliver solutions that aid in their improvement of the exploration and production of oil and gas for end users. Our scale and manufacturing flexibility help us deliver the creativity, expedience, and confidence that customers in oilfield technologies require.

8

Industrial Specialties

Our industrial specialties product line produces and sells chemicals utilized in several industrial applications, including adhesive tackifiers, agrochemical dispersants, lubricant additives, printing ink resins, and industrial intermediates.

Adhesives. We are a global supplier of tackifier resins, which provide superior adhesion to difficult-to-bond materials, to the adhesives industry. Adhesive applications for our products include construction, product assembly, packaging, pressure sensitive labels and tapes, hygiene products, and road markings.

Agrochemicals. We produce dispersants for crop protection products as well as other naturally derived products for agrochemicals. Crop protection formulations are highly engineered, specifically formulated and cover a range of different formulation types, from liquids to solids. We deliver a wide range of dispersants that are high performing and consistent. In addition, our crop protection products are approved for use as inert ingredients in agrochemicals by regulatory agencies throughout the world.

Lubricants. We supply lubricant additives and corrosion inhibitors for the metalworking and fuel additives markets. Our lubricant products are multi-functional additives that contribute to lubricity, wetting, corrosion inhibition, emulsification, and general performance efficiency. Our products are valued because of their ease in handling, robust performance, and improved formulation stability.

Printing Inks. We are a leading supplier of ink resins from renewable resources to the global graphic arts industry for the preparation of printing inks. Our products improve gloss, drying speed, viscosity, adhesion, and rub resistance of the finished ink to the substrate. We produce a wide array of resins, typically specifically tailored to a customer’s use, which can vary by application, pigment type, end use, formulation, manufacturing, and printing process.

Industrial Intermediates. Our functional chemistries are sold across a diverse range of industrial markets including, among others, paper chemicals, textile dyes, rubber, cleaners, mining, and nutraceuticals.

Customers

We sell our industrial specialties products to approximately 500 customers around the globe in over 45 countries through our own direct sales representatives and third-party sales representatives and distributors. In 2020, our ten largest customers accounted for 40 percent of the product line's sales. Our largest customers include Ennis-Flint, Inc., H.B. Fuller Co., Syngenta Crop Protection AG, and Flint Group.

Competition

Our competitors, which differ depending on the product, application, and region, include Kraton Corp., Eastman Chemical Co., ExxonMobil Corp., Borregaard ASA, Lawter, Inc., Respol S.A., Firmenich SA, as well as several others. Specific to our industrial specialty products, our customers select the product that provides the best balance of performance, consistency, and price. Reputation and loyalty are also valued by our customers and allow us to win business when other factors are equal. In adhesives, our products compete against other tackifiers, including other tall oil resin ("TOR") based tackifiers as well as tackifiers produced from gum rosin and hydrocarbon starting materials. In addition, the choice of polymer used in an adhesive formulation drives the selection of tackifier. In agrochemicals, the selection of a dispersant is made early in the product development cycle and the formulator has a choice among our sulfonated lignin products, lower quality lignosulfonates and other surfactants such as naphthalene sulfonates. In lubricants, we compete against other producers of distilled tall oil and additives. In printing inks, our products compete against other resins that can be derived from TOR, gum rosin and, to a lesser extent, hydrocarbon sources. In our industrial intermediates business, our tall oil fatty acid ("TOFA") competes against widely available fats and oils derived from tallow, soy, rapeseed, palm, and cotton sources.

Engineered Polymers

Our engineered polymers product line includes caprolactone and caprolactone based specialty chemicals for use in coatings, resins, elastomers, adhesives, bioplastics, and medical devices.

Coatings. We supply coating products that are used in automobile refinishing, sports floors, and marine applications. Our products enhance product performance by providing abrasion resistance, long durability, high quality finish, and enhanced performance in resin modification. Our products are often preferred because they provide a combination of traits that allows customers to displace several combinations of other products.

9

Resins. We supply resin products that are used in acrylic resins, polyurethane, and inks. Our products enhance product performance due to their protective properties, all weather performance and reduction or elimination of the need for solvents in formulations. Our products tend to be preferred where superior or particular performance levels are required.

Elastomers. We supply products that are used in wheel seals, mining screens, and polyurethane films. Our products enhance product performance due to their resistance to wear and tear, ability to maintain form and function under pressure and temperature and excellent UV resistance. Our products are often used in highly demanding applications where competing products do not reach required performance levels.

Adhesives. We supply products that are used in hot-melts, fabric lamination, and miscellaneous footwear components. Our products enhance product performance through their durability and substrate compatibility. Our products are often preferred because they are found to be easier to process and apply compared to competitive offerings.

Bioplastics. We supply products that are used in films, paper coatings, disposable cups, utensils, and packaging. Our products enhance product performance due to the combination of their biodegradability, improved mechanical properties, and wide processability when used in combination with other bioplastic solutions. Special grades are also available to help comply with food contact legislation in various regions and applications.

Medical Devices. We also supply products that are used in medical devices. Our products enhance end product performance due to their low melting point and ability to be thermoformed. Our products improve process conditions and provide patient comfort compared to competitive thermoplastic offerings.

Customers

We sell our engineered polymers chemicals to over 300 customers around the globe through our own direct sales representatives and third-party sales representatives and distributors. In 2020, our ten largest customers accounted for 40 percent of the product line's sales. Our largest customers include polyurethane, adhesive, coatings, and bioplastics manufacturers.

Competition

Our primary caprolactone competitors are Daicel, Corp. and BASF SE, but we also face competition from other competing materials. We compete based on performance as compared to the other competitive materials. We also compete by strengthening our technology-focused relationships with our customers.

Raw Materials and Production

Our Performance Chemicals segment serves customers globally from three manufacturing locations in the U.S. and one in the UK. Most of our pavement technologies, oilfield technologies, and industrial specialties products are derived from CTO, a co-product of the kraft pulping process, where pine is used as the source of the pulp. We also produce products derived from lignin, which is extracted from black liquor, another co-product of the kraft pulping process.

In 2016, we entered into a long-term supply agreement with WestRock pursuant to which we purchase all of the CTO and CTO equivalent tons of black liquor soap skimming ("BLSS"), the precursor to CTO, from WestRock's kraft mills as of such date, subject to certain exceptions. In 2018, we entered into a 20-year supply agreement with Georgia-Pacific LLC (“Georgia-Pacific”), pursuant to which we purchase the lesser of 125,000 tons of CTO and the aggregate output of CTO produced and originating at certain of Georgia-Pacific’s paper mills.

These relationships with WestRock and Georgia-Pacific are strategically important to our Performance Chemicals business due to the limited supply of CTO globally, of which we believe a significant portion is already under long-term supply agreements with other consumers of CTO. Under these agreements, we currently expect to source approximately 60 to 70 percent of our CTO requirements through 2025 based on the maximum operating rates of our three Performance Chemicals' pine chemicals facilities. The remainder of our CTO needs are sourced through short-term contracts in the open market.

We believe the supply from Georgia-Pacific, WestRock, and our other contracted sources of CTO will allow us to serve expected customer demand through 2021.

Our engineered polymers' products are caprolactone based, which is derived from cyclohexanone, a benzene derivative, and hydrogen peroxide, both of which are readily available in the market. We maintain multiple suppliers of

10

cyclohexanone to protect against supply disruptions and to maintain competitive pricing. Our hydrogen peroxide is currently supplied by Solvay Interox Limited, a co-located supplier at our Warrington, UK facility under a long-term supply agreement.

The other key raw materials used in the Performance Chemicals business are nonylphenol, pentaerythritol, and ethylene amines. These are sourced where possible through multiple suppliers to protect against supply disruptions and to maintain competitive pricing.

Energy

Our manufacturing processes require a significant amount of energy. We are dependent on natural gas to fuel the processes in our chemical refineries and activated carbon plants. Although we believe that we currently have a stable natural gas supply and infrastructure for our operations, we are subject to volatility in the market price of natural gas. We enter into certain derivative financial instruments in order to mitigate expected fluctuations in market prices and the volatility to earnings and cash flow resulting from changes to pricing of natural gas purchases. All of our manufacturing processes also consume a significant amount of electricity. Each of these facilities are located in regulated service areas that have stable rate structures with reliable electricity supply.

Governmental Regulations

Our manufacturing operations are subject to regulation by governmental and other regulatory authorities with jurisdiction over our operations. These regulations include regulations concerning the discharge of materials into the environment, the handling, storage, transportation, disposal, and clean-up of chemicals and waste materials, and otherwise relating to the protection of the environment, as well as other operational regulations, such as the Occupational Safety and Health Act and the Toxic Substances Control Act in the U.S. and the Registration, Evaluation and Authorization of Chemicals, or REACH, directive in Europe, the UK, and other countries. It is not possible to quantify with certainty the material effects that compliance with these regulations may have upon the capital expenditures, earnings or competitive position of Ingevity, but we currently anticipate that such compliance will not have a material adverse effect on any of the foregoing. Environmental and other regulations and related legal proceedings have the potential to involve significant costs and liability for Ingevity.

Intellectual Property

Intellectual property, including patents, closely guarded trade secrets and highly proprietary manufacturing know-how, as well as other proprietary rights, is a critical part of maintaining our technology leadership and competitive edge. Our business strategy includes filing patent and trademark applications where appropriate for proprietary developments, as well as protecting our trade secrets. We actively create, protect, and enforce our intellectual property rights. We are filing for and being granted patents for product and process developments for our Performance Materials business that we believe are both novel and consistent with trends in the technological development of engines. Our Evotherm Warm Mix Asphalt technology is supported by numerous global patents. Additionally, our Caprolactone Business and related technologies are supported by numerous global patents and trademarks, as well as proprietary manufacturing and technical know-how. The protection afforded by our patents and trademarks varies based on country, scope, and coverage, as well as the availability of legal remedies. Although our intellectual property taken as a whole is material to the business, there is no individual patent or trademark the loss of which could have a material adverse effect on the business.

In November 2020, we received an adverse decision finding some, but not all, of the claims in our “canister bleed emissions” patent invalid in our infringement action against BASF Corp in the U.S. District Court for the District of Delaware. We intend to challenge the decision, however in the meantime we anticipate the decision having limited impact on our commercial operations or financial results through the patent's expiration in March 2022.

Seasonality

There are a variety of seasonal dynamics, including global climate and weather conditions, that impact our businesses, though none materially affect financial results, except in the case of the pavement technologies product line, where roughly 70 to 75 percent of revenue is generated between April and September. From a supply perspective, this seasonality is effectively managed through pre-season inventory build and active inventory management throughout the year.

Human Capital Management

Our employees are critical to our success and we strive to provide a safe, rewarding and respectful workplace where our people are provided with opportunities to pursue career paths based on skills, performance and potential. Ingevity is

11

dependent upon our talented production workers who are key to ensuring safe and successful operations, as well as upon engineering, technical, sales and application specialists, together with experienced industry professionals, who are integral to our success. Additionally, we rely on senior management in order to establish and execute our business strategies. Our success depends, in part, on our ability to attract, retain and motivate these key performers. Our failure to attract and retain those making significant contributions could adversely affect our financial condition and results of operations.

We currently employ approximately 1,750 employees, of whom approximately 76 percent are employed in the U.S. Approximately 20 percent of our employees are represented by domestic (i.e. U.S.) labor unions under various collective bargaining agreements ("CBA"). We engage in negotiations with labor unions for new CBAs from time to time based upon expiration dates of agreements and statutory requirements. We consider our relationships with all salaried, union hourly and non-hourly employees to be positive and collaborative.

During the first quarter of 2020, at our Wickliffe, Kentucky Performance Materials' manufacturing facility, the United Steel, Paper and Forestry, Rubber, Manufacturing, Energy, Allied Industrial and Service Workers International Union, AFL-CIO-CLC ratified a three-year collective bargaining agreement ("CBA"), which expires February 1, 2023. Additionally, at our Crossett, Arkansas Performance Chemicals' manufacturing facility, the International Association of Machinists and Aerospace Workers Union ("IAM") agreed to extend the existing CBA by one year until January 15, 2021, in exchange for economic considerations. The Company and IAM resumed negotiations in Crossett in the first quarter of 2021, and the parties continue to operate under the expired CBA. In addition, at our Covington, Virginia Performance Materials' manufacturing facility, the CBA with Covington Local Union 464 of the International Brotherhood of Electrical Workers ("IBEW") agreement expired on January 15, 2021 and the CBA with Covington Local 675 affiliated with The Association of Western Pulp and Paper Workers ("AWPPW") will expire on December 1, 2021. The Company and Covington IBEW began negotiations in the first quarter of 2021, and the parties continue to operate under the expired CBA. Negotiations with the Covington AWPPW will begin in the fourth quarter of 2021.

Item 1A. Risk Factors

Based on the information currently known to us, we believe that the following information identifies the most significant risk factors affecting our company. However, the risks and uncertainties our company faces are not limited to those set forth in the risk factors described below. Additional risks and uncertainties not presently known to us or that we currently believe to be immaterial may also adversely affect our business. In addition, past financial performance may not be a reliable indicator of future performance, and historical trends should not be used to anticipate results or trends in future periods.

If any of the following risks and uncertainties develops into actual events, these events could have a material adverse effect on our business, financial condition or results of operations. In such case, the trading price of our common stock could decline.

Operational and Market Risks

The Novel Coronavirus (COVID-19) pandemic has and may continue to have an adverse effect our business, financial condition, results of operations, cash flows and stock price.

COVID-19 continues to spread in areas where we operate and transact business and the related pandemic continues to impact our operations and financial results. We have been classified as an essential business in the jurisdictions that have made this determination to date and have been allowed to continue our operations. However, our facilities - as well as the operations of our suppliers, customers and third-party sales representatives and distributors - have been, and will continue to be, disrupted by governmental and private sector responses to the COVID-19 pandemic. This includes business shutdowns, work-from-home orders and social distancing protocols, travel or health-related restrictions, as well as quarantines, self-isolations, and disruptions to transportation channels. Additional government shutdown orders or stay-at-home directives, or an outbreak among or quarantine of the employees in any of our facilities, could cause significant interruptions to, or temporary closures of our operations and could materially adversely affect our ability to adequately staff and maintain our operations. Furthermore, we may be unsuccessful at continuing to manage our business effectively due to the extended period of working from home by some of our employees. Working remotely may eventually lead to inefficiencies, as well as technology and security risks. Additionally, we are unsure if the extended period during which our employees are unable to travel to our facilities or those of our customers and suppliers may negatively impact our business.

12

Disruptions to the operations of our suppliers have at times, and may again, negatively impact our ability to purchase goods and services for our business at efficient prices and in sufficient amounts. Additionally, the operations of our customers have been, and could be further, disrupted, which can result in customers attempting to delay or cancel orders, reduce future orders or seek extended payment terms. Furthermore, the negative impact of the COVID-19 pandemic on the global economy, adverse changes in the industries that our products serve or adverse changes in the financial condition of our customers could further adversely impact demand for our products, particularly in the automotive industry and industrial and consumer applications. During 2020, many of our customers experienced extensive disruptions due to the COVID-19 pandemic, which directly impacted sales of our products, most particularly in the automotive industry during the second quarter of 2020. In addition, the significant decrease in energy prices resulting from the COVID-19 pandemic, including crude oil and gas prices, negatively impacted and could further impact the activities of our oilfield customers, resulting in a corresponding adverse effect on demand for our oilfield products. Furthermore, the markets for our engineered polymers products have also been negatively impacted due to reduced global industrial and consumer demand, and the markets for our industrial specialties products have also been negatively impacted due to reduced global industrial demand.

The extent of the impact that the COVID-19 pandemic will continue to have on our business and financial results will depend on various uncertainties and future developments, including the ultimate duration, severity and spread of the virus in the countries where we operate and transact business, additional actions taken by government authorities in their efforts to contain or treat the virus and to mitigate the economic disruptions and the global economic downturn resulting from the pandemic, the speed at which vaccines are deployed and their effectiveness against COVID-19 variants. These impacts, together with the other factors discussed, are highly uncertain and cannot be predicted, however they have and may continue to have an adverse effect on our business, financial condition, results of operations, cash flows and a negative impact on our stock price. There can be no assurance that any decrease in sales resulting from the COVID-19 pandemic will be offset by increased sales in subsequent periods.

If increasingly more stringent air quality standards worldwide are not adopted, our growth could be impacted.

Environmental standards drive the implementation of gasoline vapor emission control systems by automotive manufacturers. Given increasing societal concern over global warming and health hazards associated with poor air quality, there is growing pressure on regulators across the globe to take meaningful action. For those countries that have not significantly regulated gasoline vapor emissions, enacting more stringent regulations governing gasoline vapor emissions represents a significant upside to the Company’s automotive carbon business. However, regulators may react to a variety of considerations, including economic and political, that may mean that any such more stringent regulations are delayed or shelved entirely, in one or more countries or regions. As the adoption of more stringent regulations governing gasoline vapor emissions is expected to drive significant growth in our automotive carbon applications, the failure to enact such regulations will have a significant impact on the growth prospects for these products.

In order to compete successfully, we must develop new products and technologies meeting evolving market and customer needs; disruptive technologies could reduce the demand for the Company’s products.

Our industries and the end-use markets into which we sell our products experience periodic technological change and product improvement. Our future growth will depend on our ability to gauge the direction of commercial and technological progress in key end-use markets and on our ability to fund and successfully develop, manufacture and market products in such changing end-use markets. If we fail to keep pace with the evolving technological innovations in our end-use markets on a competitive basis, including with respect to innovation with regard to the development of alternative uses for, or application of, products developed that utilize such end-use products, our financial condition and results of operations could be adversely affected. Similarly, we face competition in our applications. Disruptive technology involving new or superior solutions could reduce the demand for the Company’s products.

Adverse conditions in the automotive market may adversely affect demand for our automotive carbon products.

Sales of our automotive activated carbon products are tied to global automobile production levels. Automotive production in the markets we serve can be affected by macro-economic factors such as interest rates, fuel prices, shifts in vehicle mix (including shifts toward alternative energy vehicles), consumer confidence, employment trends, regulatory and legislative oversight requirements and trade agreements. For example, the global economic downturn in 2008/2009, led to a drastic reduction in vehicle sales and an even greater reduction in vehicle production as OEMs right-sized their inventories to meet the lower sales volumes. Furthermore, primarily during the first half of 2020, the COVID-19 pandemic led to a significant reduction in vehicle production and vehicles sales were negatively impacted by government shutdown orders and stay-at-home directives. Regional disruptions due to localized natural disasters or multi-month strikes at suppliers or OEMs can also

13

significantly impact vehicle production and therefore demand for our automotive carbon products. Additionally, if the COVID-19 pandemic continues, it could negatively impact demand for automotive sales, which would adversely impact sales of our carbon products, as was the case in the second quarter of 2020. The extent to which COVID-19 pandemic impacts our results will depend on future developments, which are highly uncertain and cannot be predicted, including the severity of the COVD-19 pandemic, actions to contain COVID-19 or treat its impact, among others.

The Company’s pavement technologies product line is heavily dependent on government infrastructure spending.

A significant portion of our customers’ revenues in our pavement technologies business is derived from contracts with various foreign and U.S. governmental agencies, and therefore, when government spending is reduced, our customers’ need for our products is similarly reduced. While we do not do business directly with governmental agencies, our customers provide paving services to, for example, the governments of various jurisdictions within North America, South America, Europe, China, Brazil and India, and revenue either directly or indirectly attributable to such government spending continues to remain a significant portion of our revenues. Government business is, in general, subject to special risks and challenges, including: delays in funding and uncertainty regarding the allocation of funds to federal, state and local agencies, delays in the expenditures and delays or reductions in other state and local funding dedicated for transportation projects; other government budgetary constraints, cutbacks, delays or reallocation of government funding; long purchase cycles or approval processes; our customers’ competitive bidding and qualification requirements; changes in government policies and political agendas; and international conflicts or other military operations that could cause the temporary or permanent diversion of government funding from transportation or other infrastructure projects.

The Company’s engineered polymers product line is reliant on cyclical end-markets, such as the automotive market and the apparel market, which are impacted by changes in consumer and industrial demand.

Our engineered polymers product line end-markets are subject to constant and rapid technology changes, changes in consumer preferences, evolving standards, and changes in product supply and demand. For example, demand for our engineered polymers products in the automotive market, where our products are formulated into automotive resins and coatings and various components, may be affected by technological advances, changing automotive OEM specifications and global automobile production levels. In the footwear market, demand for our engineered polymers products, where our products are sold into footwear adhesives, may be affected by consumer discretionary spending and changes in consumer preferences. The impact of these changes may lead to increased competition from competing and substitute products and downward pricing pressures on our customers, and therefore, our engineered polymers product offerings. Additionally, if the COVID-19 pandemic continues, it could negatively impact demand for consumer and industrial demand, which would continue to adversely impact sales of our engineered polymers products.

The Company’s oilfield technologies business is significantly affected by trends in oil and natural gas prices that affect the level of exploration, development and production activity.

Demand for our oilfield technologies services and products is particularly sensitive to the level of exploration, development and production activity of, and the corresponding capital spending by, oil and natural gas companies, including national oil companies. The level of exploration, development and production activity is directly affected by trends in oil and natural gas prices, which historically have been volatile. Crude oil prices have declined significantly during 2020. Pricing moved from $58 per barrel in January to a low of $16 per barrel in April to $48 per barrel in December. Pricing is not currently forecasted to change significantly from these levels during 2021. While these pricing levels show recovery from the lows reached during the first half of 2020, they remain off their highs seen in the last decade.

Any prolonged low pricing environment for oil and natural gas is likely to result in reduced demand for our oilfield technology products, which may have a material adverse effect on our results of operations.

The Company’s printing inks business serves customers in a market that is facing declining volumes and downward pricing.

The use of inks in which our printing ink resins are used, such as those made for magazines and catalogs, has significantly decreased, as the printing industry has experienced a reduction in demand due to various factors including competition from alternative sources of communication, including email, the Web, electronic readers, interactive television and electronic retailing. The impacts of these changes have led to continued intense competition and downward pricing pressures on printing inks, and therefore, our ink products.

14

A prolonged period of low energy prices may materially impact our results of operations.

The price of energy may directly or indirectly impact demand, pricing or the profitability for certain Ingevity products. As petroleum oil prices fall or change rapidly, Ingevity products may be disadvantaged due to the fact that CTO and BLSS are thinly traded commodities with pricing commonly established for periods ranging from one quarter to one year periods of time. Due to this, alternative technologies which compete with product offerings provided by Ingevity may be advantaged from time to time in the marketplace. Protracted periods of high volatility or sustained oversupply of petroleum oil may also translate into increased competition from petroleum-based alternatives which would otherwise be consumed in petroleum transportation fuel blends. In addition, pricing for competing naturally derived oils such as palm or soybean is likely to provide further pressure on pricing of the Company’s products during periods of depressed petroleum prices.

We face competition from producers of substitute products and new technologies, and new or emerging competitors.

In the Performance Materials segment, there is competition from various other activated carbon manufacturers. These competitors are actively trying to develop more advanced and alternative activated carbon products that would more effectively compete with our products in the automotive applications. There is also competition in the automotive applications from non-activated carbon competitors or product offerings. For example, at least one OEM is using sealed tanks in certain subsets of its vehicles to comply with the Tier 3/LEV III regulations. While the sealed tank fuel systems generally require a similarly sized pelleted activated carbon canister to deal with refueling emissions, in most cases, they do not use an extruded honeycomb to meet current U.S. and California regulations. There is also emerging competition in the "honeycomb" space, which may impact sales of the Company's products. If a competitor were to succeed in developing products that are better suited for automotive evaporative emissions capture applications and/or a competitive technology, such as, but not limited to, sealed gas tanks, were to be implemented across a material number of vehicle platforms, our financial results could be negatively impacted.

In addition, growth in alternative vehicles, such as all-electric vehicles and hydrogen fuel cell vehicles, which do not use gasoline, may also adversely affect the demand for our products.

In the Performance Chemicals segment, hydrocarbon resins and gum rosin-based products compete with TOR-based resins in the adhesives and printing inks markets. The price of gum rosin has a significant impact on the market price for TOR and rosin derivatives and the price of gum rosin is driven by labor rates, land leasing costs and various other factors that are not within our control. Hydrocarbon resins, for example, C5 resins, are co-products from isoprene (synthetic rubber). Availability and pricing are determined by the supply and demand for synthetic rubber as well as crude oil prices as the feedstock for isoprene and various other factors that are not within our control. Animal and vegetable-based fatty acids compete with TOFA products in lubricant and industrial specialties. The market price for TOFA products is impacted by the prices of other fats and oils and the prices for other fats and oils is driven by actual and expected harvest rates, crude oil prices and the biofuel market. Other monomers, thermoplastics and polyols compete with our caprolactone based products. The price for our products is impacted by the prices of competitive substitutes which are influenced by petroleum prices as well as other supply and demand factors. Additionally, the Company faces competition from competitors that are actively developing new technologies and competing products across the segment. A significant investment by a competitor in a competitive technology or product line could negatively impact our financial results.

Disruptions at any of our manufacturing facilities could negatively impact our production, financial condition and results of operations.

An operational disruption in any of our facilities could negatively impact production and our financial results. The occurrence of a natural disaster, such as a hurricane, tropical storm, earthquake, tornado, severe weather, flood, fire, as well as risk that may result from climate change, could cause operational disruptions. Additionally, other unanticipated problems such as labor difficulties, health epidemics (including the COVID-19 pandemic), equipment failure, cyberattack or other cybersecurity incident, capacity expansion difficulties or unscheduled maintenance could also cause operational disruptions of varied duration. These types of disruptions could materially adversely affect our financial condition and results of operations to varying degrees dependent upon the facility, the duration of the disruption, our ability to shift business to another facility or find alternative sources of materials or energy. In certain cases, we have some products that are only made at one facility. For example, in the case of our Waynesboro, Georgia facility, while we have some redundancies within the facility, we only have one facility that makes our extruded honeycomb products. In the case of our Warrington, UK facility, while we have some redundancies within the facility, we only have one facility that makes our caprolactone products. As other examples, in our Charleston SC facility, we source black liquor from an adjacent paper mill to isolate and subsequently modify lignin to serve

15

our agriculture customers while we make the vast majority of our ink resin products in our DeRidder, Louisiana facility. While we have redundancies within these facilities, we have limited ability to make these products at other facilities. Finally, the COVID-19 pandemic is causing travel disruptions, quarantines and/or closures, which could result in disruptions to our manufacturing and production operations at our facilities, as well as those of our suppliers and customers. Any losses due to these events may not be covered by our existing insurance policies or may be subject to certain deductibles.

We are dependent upon third parties for the provision of certain critical operating services at several of our facilities.

We are dependent upon third parties for the provision of certain critical operating services at our Covington, Virginia Performance Materials facility and at the following Performance Chemicals facilities: Crossett, Arkansas; North Charleston, South Carolina; and Warrington, UK.

We are dependent on: (i) the WestRock Covington, Virginia paper mill (“WestRock VA Paper Mill”) for the provision of electricity, water, compressed air, steam and wastewater treatment to our Covington Performance Materials facility; (ii) the WestRock North Charleston, South Carolina paper mill (“WestRock SC Paper Mill”) for the provision of water, compressed air, steam and wastewater treatment at our North Charleston Performance Chemicals facility; (iii) the Georgia-Pacific Crossett, Arkansas paper mill and chemicals plant (collectively, “Georgia-Pacific Mill”) for the provision of natural gas, water, compressed air and wastewater treatment to our Crossett Performance Chemicals facility; and (iv) Solvay Plant for the provision of water, compressed air, nitrogen, natural gas, electricity, steam, and wastewater treatment and waste management at our Warrington Performance Chemicals facility. We have existing long-term contractual arrangements covering these services for our Covington, Crossett, North Charleston and Warrington facilities. The provision of these services would be at risk if any of the counterparties were to idle or permanently shut down the associated mill, or if operations at the associated mill were disrupted due to natural or other disaster, or by reason of strikes or other labor disruptions, or if there were a significant contractual dispute between the parties.

In the event that WestRock VA Paper Mill, WestRock SC Paper Mill, Georgia-Pacific Mill or Solvay Plant were to fail to provide the contracted services, we would be required to obtain these services from other third parties at an increased cost or to expend capital to provide these services ourselves. The expenses associated with obtaining or providing these services, as well as any interruption in our operations as a result of the failure of the counterparty to provide these services, may be significant and may adversely affect our financial condition and results of operations.

Furthermore, in the event that WestRock VA Paper Mill wastewater treatment operations do not comply with permits or applicable law and the WestRock VA Paper Mill is unable to determine the cause of such compliance, then we will be responsible for between 10 percent and 50 percent of the costs and expenses of such noncompliance (increasing in 10 percent increments per violation during each twelve month period) despite representing less than 3 percent of the total wastewater volume. These costs and expenses may be significant and may adversely affect our financial condition and results of operations.

Additionally, (i) our Covington Performance Materials facility is located on real property leased from WestRock pursuant to a long-term lease agreement, and is surrounded by the WestRock VA Paper Mill, (ii) a portion of our North Charleston Performance Chemicals facility is located on real property leased from WestRock and is adjacent to the WestRock SC Paper Mill; (iii) our Crossett Performance Chemicals facility is located on real property leased from Georgia-Pacific pursuant to a long-term lease agreement, and is surrounded by the Georgia-Pacific Paper Mill and (iv) our Warrington, UK Performance Chemicals facility is located on real property leased from Solvay pursuant to multiple long-term lease agreements, and is surrounded by the Solvay Plant. In the event we were to have a dispute with WestRock, Georgia-Pacific or Solvay regarding the terms of the relevant lease agreements, or we were otherwise unable to fully access or utilize the leased property, the associated business disruption may be significant and may adversely affect our financial condition and results of operations.

We are also dependent on third parties for the disposal of brine, which results from our own conversion of BLSS into CTO. If these service providers do not perform under their contracts, the costs of disposing of brine ourselves, including, for example, the transportation costs, could be significant.

We are dependent on certain customers.

We have certain large customers in particular businesses, the loss of which could have a material adverse effect on the applicable segment’s sales and, depending on the significance of the loss, our results of operations, financial condition or cash flows. Sales to the Company’s ten largest customers (across both segments) accounted for 36 percent of total sales for 2020. No customer accounted for more than 10 percent of total sales for 2020. With some exceptions, our business with those large

16

customers is based primarily upon individual purchase orders. As such, our customers could cease buying our products from us at any time, for any reason, with little or no recourse. If a major customer or multiple smaller customers elected not to purchase products from us, our financial condition and results of operations would be materially adversely affected.

We are dependent on attracting and retaining key personnel.

The Company is dependent upon its production workers, as well as upon engineering, technical, sales and application specialists, together with experienced industry professionals and senior management. Our success depends, in part, on our ability to attract, retain and motivate these key performers. Our failure to attract and retain those making significant contributions could adversely affect our financial condition and results of operations.

Work stoppages and other labor relations matters may have an adverse effect on our financial condition and results of operations.

Many of our production employees are governed by collective bargaining agreements (“CBAs”). From time to time the Company engages in negotiations to renew CBAs as those contracts are scheduled to expire. During the first quarter of 2020, at our Wickliffe, Kentucky Performance Materials' manufacturing facility, the United Steel, Paper and Forestry, Rubber, Manufacturing, Energy, Allied Industrial and Service Workers International Union, AFL-CIO-CLC ratified a three-year collective bargaining agreement ("CBA"), which expires February 1, 2023. Additionally, at our Crossett, Arkansas Performance Chemicals' manufacturing facility, the International Association of Machinists and Aerospace Workers Union ("IAM") agreed to extend the existing CBA by one year until January 15, 2021, in exchange for economic considerations. The Company and IAM resumed negotiations in Crossett in the first quarter of 2021, and the parties continue to operate under the expired CBA. In addition, at our Covington, Virginia Performance Materials' manufacturing facility, the CBA with Covington Local Union 464 of the International Brotherhood of Electrical Workers ("IBEW") agreement expired on January 15, 2021 and the CBA with Covington Local 675 affiliated with The Association of Western Pulp and Paper Workers ("AWPPW") will expire on December 1, 2021. The Company and Covington IBEW began negotiations in the first quarter of 2021, and the parties continue to operate under the expired CBA. Negotiations with the Covington AWPPW will begin in the fourth quarter of 2021.

While the Company has generally positive relations with its labor unions, there is no guarantee the Company will be able to successfully negotiate new union contracts without work stoppages, labor difficulties or unfavorable terms. If we were to experience any extended interruption of operations at any of our facilities because of strikes or other work stoppages, our results of operations and financial condition could be materially and adversely affected. In addition, due to the co-location of our Covington, Crossett, North Charleston, and Warrington facilities within the WestRock VA Paper Mill, Georgia-Pacific Mill, WestRock SC Paper Mill and Solvay Plant facilities, a strike or work stoppage at any of these facilities could cause disruptions at our facilities, and our results of operations could be materially and adversely affected.

As we rely on information technologies to conduct our business, security breaches and other disruptions could compromise our information and expose us to liability, which could cause our business and reputation to suffer.

We rely on information technologies, some of which are managed by third parties, to manage the day-to-day operations and activities of our business, operate elements of our manufacturing facilities, manage our customer and vendor transactions, and maintain our financial, accounting and business records. In addition, we collect and store certain data, including proprietary business information, and may have access to confidential or personal information that is subject to privacy and security laws and regulations.

The secure processing, maintenance and transmission of sensitive, confidential and personal data is critical to our operations and business strategy. We follow industry best practices and have instituted a system of security policies, procedures, capabilities, and internal controls designed to protect this information. Additionally, we engage third-party threat detection and monitoring services which includes a global cyber security incident response team and our auditor conducts periodic ISO 27001 gap assessments on our information technology systems. Despite our security design and controls, and those of our third-party providers, we may be vulnerable to cyber- attacks, computer viruses, security breaches, inadvertent or intentional employee actions, system failures and other risks that could potentially lead to the compromising of sensitive, confidential or personal data, improper use of our, or our third-party provider systems, solutions or networks, unauthorized access, use, disclosure, modification or destruction of information, and operational disruptions. In addition, the global regulatory environment pertaining to information security and privacy is increasingly demanding, with new and changing requirements, such as the European Union’s General Data Protection Regulation (“GDPR”), California Consumer Privacy Act (“CCPA”), and the China Cybersecurity Law. GDPR, which applies to the collection, use, retention, security, processing, and

17

transfer of personally identifiable information of residents of European Union (“EU”) countries, mandates new compliance obligations, and imposes significant fines and sanctions for violations. CCPA requires companies to provide new data disclosure, access, deletion and opt-out rights to consumers in California. Implementing and complying with these laws and regulations may be more costly or take longer than we anticipate, or could otherwise affect our business operations. Such breaches, cyber incidents and disruptions, or failure to comply with laws and regulations related to information security or privacy, could result in legal claims or proceedings against us by governmental entities or individuals, significant fines, penalties or judgements, disruption of our operations, remediation requirements, changes to our business practices, and damage to our reputation, which could adversely affect our business, financial condition or results of operations.

Complications with the design or implementation of our new enterprise resource planning (“ERP”) system could adversely impact our business and operations.

We are in the process of a complex, multi-year implementation of a new ERP system necessary due to the finite life of the existing operating system. The ERP system implementation requires the integration of the new ERP system with multiple new and existing information systems and business processes in order to maintain the accuracy of our books and records and to provide our management team with information important to the operation of our business. Such an initiative is a major financial undertaking and will require substantial time and attention of management and key employees. The implementation of the ERP system may prove to be more difficult, costly, or time consuming than expected, and it is possible that the system will not yield the benefits anticipated. Failure to successfully design and implement the new ERP system as planned could harm our business, financial condition, and operating results. Additionally, if we do not effectively implement the ERP system as planned or the ERP system does not operate as intended, the effectiveness of our internal control over financial reporting could be negatively affected.

Supply Chain Risks

Disruptions within our supply chain could negatively impact our production, financial condition and results of operations.

We could be adversely affected by disruptions within our supply chain and transportation network. Our products are transported by truck, rail, barge or ship by third-party providers. The costs of transporting our products could be negatively affected by factors outside of our control, including rail service interruptions or rate increases, extreme weather events, tariffs, rising fuel costs and capacity constraints. Significant delays or increased costs affecting these transportation methods could materially affect our financial condition and results of operations. Disruptions at our suppliers could lead to short term or longer rises in raw material or energy costs and/or reduced availability of materials or energy, potentially affecting our financial condition and results of operations. For example, Solvay is our primary provider of hydrogen peroxide to our Warrington, UK Performance Chemicals facility, which is co-located with the Solvay Warrington, UK chemical plant (“Solvay Plant”). Disruptions at the Solvay Plant impacting Solvay’s ability to supply hydrogen peroxide could adversely affect our financial condition and results of operations. See also “—General Business and Economic Risks—Our engineered polymers product line may be adversely affected by the UK’s withdrawal from the European Union” and “Operational and Market Risks - We are dependent upon third parties for the provision of certain critical operating services at several of our facilities.”

Our Performance Chemicals segment is highly dependent on CTO, which is limited in supply; lack of access to sufficient CTO would impact our ability to produce CTO-based products.

The availability of CTO is essential to the Company’s Performance Chemicals segment. Availability of CTO is directly linked to the production output of kraft mills using pine as their source of pulp, which is the predominant fiber source for packaging grades of paper as well as fluff pulp for personal care products. As a result, there is a finite global supply of CTO-with global demand for softwood pulp driving the global supply of CTO, rather than demand for CTO itself. Most of the CTO made available for sale by its producers in North America is covered by long-term supply agreements, further constraining availability.

In 2016, we entered into a long-term supply agreement with WestRock pursuant to which we purchase all of the BLSS and CTO output from WestRock’s existing (at the time of separation) kraft mills, subject to certain exceptions. This agreement includes pricing terms based on market prices.

Pricing for the products in our agreement with WestRock is based on the prevailing market prices of products at the time of purchase. The pricing formulas are subject to certain pricing floors as set forth in the agreement with WestRock. Given

18

the take-or-pay requirements of the agreement with WestRock, in adverse market conditions we could be required to purchase BLSS and CTO from WestRock at prices where our results of operations could be materially and adversely affected.

In 2018, we entered into a 20-year CTO supply agreement with Georgia-Pacific, pursuant to which we purchase the lesser of 125,000 tons of CTO and the aggregate output of CTO produced and originating at certain of Georgia-Pacific’s paper mills.

Pricing for the CTO in our agreement with Georgia-Pacific is a market-based price, subject to ongoing adjustments. Given the take-or-pay requirements of the agreement with Georgia-Pacific, in adverse market conditions we could be required to purchase CTO from Georgia-Pacific at prices where our results of operations could be materially and adversely affected.

If any of our suppliers (including WestRock or Georgia-Pacific) fail to meet their respective obligations under our supply agreements or we are otherwise unable to procure an adequate supply of CTO, we would be unable to maintain our current level of production and our results of operations would be materially and adversely affected.

Beginning in 2025, either party to the WestRock agreement may provide a notice to the other party terminating the WestRock agreement five years from the date of such notice. Beginning one year after such notice, the quantity of products provided by WestRock under the agreement will be gradually reduced over a four-year period based on the schedule set forth in the agreement. In addition, from 2022 until 2025, either party may provide notice to remove a kraft mill as a supply source. The two largest kraft mills under the WestRock agreement currently supply approximately 17 to 19 percent and 18 to 20 percent, respectively, of the total amount of products supplied under our agreement with WestRock. If WestRock exercises its rights to terminate the agreement or remove a kraft mill as a supply source, and we are unable to arrange for a substitute supply of CTO, we would be unable to continue to produce the same quantity of products and our results of operations could be materially and adversely affected.