UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark One)

o REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended

December 31, 2016 |

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

o SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report . . . . . . . . . . . . . . . . . . .

For the transition period from ___________________________ to ___________________________

Commission file number: 001-37877

The Bank of N.T. Butterfield & Son Limited

(Exact name of Registrant as specified in its charter)

Bermuda

(Jurisdiction of incorporation or organization)

65 Front Street, Hamilton, HM 12 Bermuda

(Address of principal executive offices)

Shaun Morris, 65 Front Street, Hamilton, HM 12 Bermuda

Telephone: (441) 295-1111; Fax: (441) 292-4365

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

Title of each class | Name of each exchange on which registered |

voting ordinary shares of par value BM$ 0.01 each | New York Stock Exchange Bermuda Stock Exchange |

Bermuda Stock Exchange | |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the

period covered by the annual report.

As of December 31, 2016, there were 53,284,872 shares of the registrant's common stock outstanding.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

oYes xNo

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

oYes xNo

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the

Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

xYes oNo

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

xYes oNo

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See

definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filero Accelerated filero Non-accelerated filerx

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAPx

International Financial Reporting Standards as issued by the International Accounting Standards Boardo

Othero

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the

registrant has elected to follow.

oItem 17 oItem 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the

Exchange Act).

oYes xNo

TABLE OF CONTENTS

Cross Reference Sheet | |

Explanatory Note | |

Implications of Being an Emerging Growth Company and a Foreign Private Issuer | |

Cautionary Note Regarding Forward-Looking Statements | |

Information on the Company | |

Selected Consolidated Financial and Other Data | |

Risk Factors | |

Market Information | |

Dividend Policy | |

Management’s Discussion and Analysis of Financial Condition and Results of Operations | |

Selected Statistical Data | |

Risk Management | |

Supervision and Regulation | |

Management | |

Major Shareholders and Related Party Transactions | |

Certain Taxation Considerations | |

Enforcement of Civil Liabilities | |

Material Modifications to the Rights of Security Holders and Use of Proceeds | |

Disclosure Control and Procedures | |

Principal Accountant Fees and Services | |

Issuer Purchases of Equity Securities | |

Where You Can Find More Information | |

Index to the Financial Statements | |

CROSS REFERENCE SHEET

Form 20-F

Item Caption | Location | Page | ||||

Part I | ||||||

Item 1 | Identity of Directors, Senior Management and Advisors | Not Applicable | N/A | |||

Item 2 | Offer Statistics and Expected Timetable | Not Applicable | N/A | |||

Item 3 | Key Information | Explanatory Note | ||||

Risk Factors | ||||||

Selected Consolidated Financial and Other Data | ||||||

Dividend Policy | ||||||

Item 4 | Information on the Company | Information on the Company | ||||

Supervision and Regulation | ||||||

Item 4A | Unresolved Staff Comments | Not Applicable | N/A | |||

Item 5 | Operating and Financial Review and Prospects | Management's Discussion and Analysis of Financial Condition and Results of Operations | ||||

Item 6 | Directors, Senior Management and Employees | Management | ||||

Major Shareholders and Related Party Transactions | ||||||

Item 7 | Major Shareholders and Related Party Transactions | Major Shareholders and Related Party Transactions | ||||

Item 8 | Financial Information | Reports of Independent Registered Public Accounting Firms | ||||

Consolidated Financial Statements and Notes to the Consolidated Financial Statements | ||||||

Item 9 | The Offer and Listing | Market Information | ||||

Item 10 | Additional Information | Management | ||||

Dividend Policy | ||||||

Supervision and Regulation | ||||||

Item 11 | Quantitative and Qualitative Disclosures about Market Risk | Risk Management | ||||

Item 12 | Description of Securities other than Equity Securities | Not Applicable | N/A | |||

Part II | ||||||

Item 13 | Defaults, Dividend Arrearages and Delinquencies | None | N/A | |||

Item 14 | Material Modifications to the Rights of Security Holders and Use of Proceeds | Material Modifications to the Rights of Security Holders and Use of Proceeds | ||||

Item 15 | Controls and Procedures | Disclosure Controls and Procedures | ||||

Item 16A | Audit Committee Financial Expert | Management - Audit Committee | ||||

Item 16B | Code of Ethics | Management - Code of Conduct and Ethics and Whistleblower Policy | ||||

Item 16C | Principal Accountant Fees and Services | Principal Accountant Fees and Services | ||||

Item 16D | Exemption from the Listing Standards for Audit Committees | Not Applicable | N/A | |||

Item 16E | Purchases of Equity Securities by the Issuer and Affiliated Purchasers | Issuer Purchases of Equity Securities | ||||

Item 16F | Changes in or Disagreements with Accountants | Not Applicable | N/A | |||

Item 16G | Significant Differences in Corporate Governance Practices | Management - Foreign Private Issuer Status | ||||

Item 16H | Mine Safety Disclosure | Not Applicable | N/A | |||

i

ii

EXPLANATORY NOTE

In this report, unless the context indicates otherwise, the term:

• | "Bank" or "Butterfield" refers to: |

• | The Bank of N.T. Butterfield & Son Limited; |

• | "BMA" refers to: |

• | The Bermuda Monetary Authority; |

• | "Board" refers to: |

• | The board of directors of the Bank; |

• | "IPO" refers to: |

• | Our initial public offering of 12,234,042 common shares completed on September 21, 2016; |

• | "common shares" refers to: |

• | The voting ordinary shares of par value BM$ 0.01 each in the Bank; |

• | "we", "our", "us", "the Company" and "the Group" refer to: |

• | The Bank and its consolidated subsidiaries. |

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

In this report, references to “BMD”, “BM$”, or “Bermuda Dollars” are to the lawful currency of Bermuda, and “USD”, “US$”, “$” and “US Dollars” are to the lawful currency of the United States of America. The Bermuda Dollar is pegged to the US Dollar on a one‑to‑one basis and therefore, for all periods presented, BM$1.00 = US$1.00.

Certain monetary amounts, percentages and other figures included in this report have been subject to rounding adjustments. Accordingly, figures shown as totals in certain tables may not be the arithmetic aggregation of the figures that precede them, and figures expressed as percentages in the text may not total 100% or, as applicable, when aggregated may not be the arithmetic aggregation of the percentages that precede them.

Our consolidated financial statements as of and for the years ended December 31, 2016, 2015 and 2014 have been audited, as stated in the report appearing herein, by PricewaterhouseCoopers Ltd., Bermuda, and are included in this report and are referred to as our audited consolidated financial statements. We have prepared these financial statements in accordance with generally accepted accounting principles in the United States of America (“US GAAP”).

We believe that the non‑GAAP measures included in this report provide valuable information to readers because they enable the reader to identify the financial measures we use to track the performance of our business and guide management. Furthermore, these measures provide readers with valuable information regarding our core activities, which allows for a more meaningful evaluation of relevant trends when considered in conjunction with measures calculated in accordance with US GAAP. Non‑GAAP measures used in this report are not a substitute for US GAAP measures and readers should consider the US GAAP measures as well. For more information on non‑GAAP measures, including a reconciliation to the most directly comparable US GAAP financial measures, see “Selected Consolidated Financial Data — Reconciliation of Non‑GAAP Financial Measures”.

INDUSTRY AND MARKET DATA

Some of the discussion contained in this report relies on certain market and industry data obtained from third‑party sources that we believe to be reliable. Market estimates are calculated by using independent industry publications and third‑party forecasts in conjunction with our assumptions about our markets. While we believe the industry and market data to be reliable as of the date of this report, this information is subject to change based on various factors, including those discussed under the headings “Cautionary Note Regarding Forward‑Looking Statements” and “Risk Factors” in this report.

TRADEMARKS AND SERVICE MARKS

We own or have rights to trademarks and service marks for use in connection with the operation of our business, including, but not limited to, the word Butterfield. All other trademarks or service marks appearing in this report that are not identified as marks owned by us are the property of their respective owners. Solely for convenience, the trademarks, service marks and trade names referred to in this report are listed without the ®, (TM) and (sm) symbols, but we will assert, to the fullest extent under applicable law, our applicable rights in these trademarks, service marks and trade names.

iii

IMPLICATIONS OF BEING AN EMERGING GROWTH COMPANY AND

A FOREIGN PRIVATE ISSUER

As a company with less than $1.0 billion in revenues during our last fiscal year, we are an “emerging growth company” as defined under the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). An emerging growth company may take advantage of reduced reporting requirements and is relieved of certain other significant requirements that are otherwise generally applicable to public companies.

As an emerging growth company:

• | we are exempt from the requirement to obtain an attestation and report from our auditors on management’s assessment of our internal control over financial reporting under the Sarbanes-Oxley Act of 2002; |

• | we may provide reduced disclosure regarding our executive compensation arrangements pursuant to the rules applicable to foreign private issuers and emerging growth companies, which means we do not have to include a compensation discussion and analysis and certain other disclosure regarding our executive compensation; and |

• | we are not required to seek a nonbinding advisory vote on executive compensation or golden parachute arrangements. |

We have elected to take advantage of the scaled disclosure requirements and other relief described above in this report and may take advantage of these exemptions for so long as we remain an emerging growth company. We will remain an emerging growth company until the earliest of (1) the end of the fiscal year during which we have total annual gross revenues of $1.0 billion or more, (2) the end of the fiscal year following the fifth anniversary of the completion of our IPO, (3) the date on which we have, during the previous three‑year period, issued more than $1.0 billion in nonconvertible debt and (4) the end of the fiscal year, after we have been subject to the requirements of Section 13(a) or 15(a) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), for a period of 12 calendar months and have filed at least one annual report pursuant to those sections, in which the market value of the Bank’s equity securities that are held by non‑affiliates exceeds $700 million as of June 30 of that year. We are expected to cease to qualify as an emerging growth company on December 31, 2017.

In addition to scaled disclosure and the other relief described above, the JOBS Act permits us an extended transition period for complying with new or revised accounting standards affecting public companies. We do not intend to take advantage of this extended transition period, which means that the financial statements included in this report, as well as any financial statements that we file in the future, will be subject to all new or revised accounting standards generally applicable to public companies.

We are a foreign private issuer, and so long as we qualify as a foreign private issuer under the Exchange Act, we will be exempt from certain provisions of the Exchange Act that are applicable to US domestic public companies, including:

• | the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations in respect of a security registered under the Exchange Act; |

• | the sections of the Exchange Act requiring insiders to file public reports of their share ownership and trading activities and liability for insiders who profit from trades made in a short period of time; |

• | the rules under the Exchange Act requiring the filing with the Securities and Exchange Commission of quarterly reports on Form 10‑Q containing unaudited financial and other specified information, or current reports on Form 8‑K, upon the occurrence of specified significant events; and |

• | Regulation Fair Disclosure, or Regulation FD, which regulates selective disclosures of material information by issuers. |

We are, however, required to file an annual report on Form 20‑F within four months of the end of each fiscal year. In addition, we have published and intend to continue to publish our results on a quarterly basis through press releases, distributed pursuant to the rules and regulations of the NYSE. Press releases related to financial results and material events have been and will continue to be furnished to the SEC on Form 6‑K. However, the information we are required to file with or furnish to the SEC is less extensive and less timely compared to that required to be filed with the SEC by US domestic issuers. As a result, you may not be afforded the same protections or information that would be made available to you, were you investing in a US domestic issuer. For additional discussion on our foreign private issuer status, see “Management — Foreign Private Issuer Status”.

iv

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This annual report contains forward-looking statements. Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based on our current beliefs, expectations or assumptions regarding the future of our business, future plans and strategies, our operational results and other future conditions. Forward-looking statements can be identified by words such as "anticipate," "believe," "estimate," "expect," "intend," "may," "plan," "predict," "project," "seek," "target," "potential," "will," "would," "could," "should," "continue," "contemplate" and other similar expressions, although not all forward-looking statements contain these identifying words. These forward-looking statements include all matters that are not historical facts. They appear in a number of places throughout this annual report and include statements regarding our intentions, beliefs or current expectation concerning, among other things, our results of operations, financial condition, capital and liquidity requirements, prospects, growth, strategies and the industry in which we operate.

There are important factors that could cause actual results to differ materially from those contemplated by such forward-looking statements. By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. We believe that these risks and uncertainties include, but are not limited to, those described in the "Risk Factors" section of this annual report, which include, but are not limited to, the following:

• | changes in economic and market conditions; |

• | changes in market interest rates; |

• | our access to sources of liquidity and capital to address our liquidity needs; |

• | our ability to attract and retain customer deposits; |

• | our ability to effectively compete with other financial services companies and the effects of competition in the financial services industry on our business; |

• | our ability to successfully execute our business plan and implement our growth strategy; |

• | our ability to successfully manage our credit risk and the sufficiency of our allowance for credit loss; |

• | our ability to successfully develop and commercialize new or enhanced products and services; |

• | our ability to transact business in EU countries in the aftermath of Brexit; |

• | damage to our reputation from any of the factors described in this section, in "Risk Factors" and in "Management's Discussion and Analysis of Financial Condition and Results of Operations"; |

• | our reliance on appraisals and valuation techniques; |

• | our ability to attract and maintain qualified employees and key executives; |

• | our reliance on third-party vendors; |

• | our reliance on the effective implementation and use of technology; |

• | our ability to identify and address cyber-security risks; |

• | the failure or interruption of our information and communications systems; |

• | the effectiveness of our risk management and internal disclosure controls and procedures; |

• | our ability to maintain effective internal control over financial reporting; |

• | the likelihood of success in, and the impact of, litigation or regulatory actions; |

• | the complex and changing regulatory environment in which we operate, including any changing regulatory requirements and restrictions placed on us by our principal regulator, the BMA, and other regulators, as well as our ability to comply with regulatory schemes in multiple jurisdictions; and |

• | the incremental costs of operating as a public company. |

These factors should not be construed as exhaustive and should be read with the other cautionary statements in this annual report.

Although we base these forward-looking statements on assumptions that we believe are reasonable when made, we caution you that forward-looking statements are not guarantees of future performance and that our actual results of operations, financial condition and liquidity, and the development of the industry in which we operate may differ materially from those made in or suggested by the forward-looking statements contained in this report. In addition, even if our results of operations, financial condition and liquidity, and the development of the industry in which we operate, are consistent with the forward-looking statements contained in this report, those results or developments may not be indicative of results or developments in subsequent periods.

Given these risks and uncertainties, you are cautioned not to place undue reliance on these forward-looking statements. Any forward-looking statement that we make in this report speaks only as of the date of such statement. Except to the extent required by applicable law, we undertake no obligation to update any forward-looking statements or to publicly announce the results of any revisions to any of those statements to reflect future events or developments. Comparisons of results for current and any prior periods are not intended to express any future trends or indications of future performance, unless specifically expressed as such, and should only be viewed as historical data.

v

INFORMATION ON THE COMPANY

Overview

We are a full service bank and wealth manager headquartered in Hamilton, Bermuda. We operate our business through six geographic segments: Bermuda, the Cayman Islands, and Guernsey, where our principal banking operations are located; and The Bahamas, Switzerland, and the United Kingdom, where we offer specialized financial services. We offer banking services, comprised of retail and corporate banking, and wealth management, which consists of trust, private banking, and asset management. In our Bermuda and Cayman Islands segments, we offer both banking and wealth management. In our Guernsey, Bahamas, and Switzerland segments, we offer wealth management. In our United Kingdom segment, we offer residential property lending.

For the year ended December 31, 2016 we generated $406.0 million in net revenue before provision for credit losses and other gains/losses ("Net Revenue"). Our total net revenue by each of our six geographic segments for the years ended December 31, 2016, 2015 and 2014 are as follows:

For the year ended | |||||||||||

In millions of $ | 2016 | 2015 | 2014 | ||||||||

Net Revenue | |||||||||||

Bermuda segment | $ | 231.4 | $ | 202.5 | $ | 201.0 | |||||

Cayman Islands segment | $ | 121.0 | $ | 105.8 | $ | 91.9 | |||||

Guernsey segment | $ | 39.0 | $ | 43.1 | $ | 46.1 | |||||

United Kingdom segment | $ | 6.0 | $ | 19.3 | $ | 26.4 | |||||

Bahamas segment | $ | 4.7 | $ | 5.3 | $ | 5.5 | |||||

Switzerland segment | $ | 3.8 | $ | 3.4 | $ | 2.5 | |||||

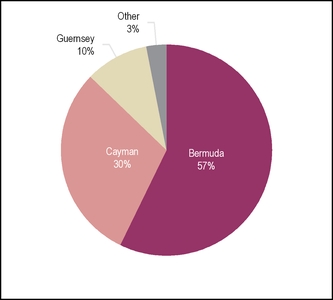

Our Net Revenue for the year ended December 31, 2016 consisted of 57% from our Bermuda segment, 30% from our Cayman Islands segment, 10% from our Guernsey segment, 1% from our United Kingdom segment, and 1% from each of our Bahamas and Switzerland segments. As of December 31, 2016, we had $11.1 billion in total assets, $3.6 billion in net loans, $10.0 billion in customer deposits (67% USD deposits, 18% USD-pegged deposits), $98.0 billion of trust assets under administration ("AUA"), and $4.7 billion of assets under management ("AUM").

In our Bermuda and Cayman Islands segments, our bank provides a full range of retail and corporate banking services to individuals, local businesses, captive insurers, reinsurance companies, trust companies, and hedge funds. The key products we offer include personal and business deposit services, residential and commercial mortgages, small and medium-sized enterprise and corporate loans, credit and debit card suite, merchant acquiring, mobile / online banking, and cash management. With seven branches and 51 ATMs as of December 31, 2016, we have a 39% Bermudian Dollar ("BMD") deposit market share in Bermuda and a 35% local deposit market share in the Cayman Islands as of December 31, 2015 based on data from the Bermuda Monetary Authority ("BMA") and the Cayman Islands Monetary Authority ("CIMA"), respectively.

In all of our segments except the United Kingdom, we offer wealth management to high net worth and ultra-high net worth individuals, family offices, and institutional and corporate clients. Our wealth management platform has three lines of business: trust, private banking, and asset management.

The trust business line, which utilizes specialists in each of our geographic areas, meets client needs in estate and succession planning, administration of complex asset holdings, and efficient coordination of family affairs. In addition, the business provides pension and employee benefits services for multinational corporations, as well as services that involve administration of and fiduciary responsibility for customized trust structures holding a wide range of asset types including financial assets, property, business assets, and art. As of December 31, 2016, trust AUA totaled $98.0 billion.

Our private banking business line offers access to a suite of services, targeted toward high net worth individuals, trusts, and family offices, that can be customized to each client's needs and preferences and delivered as part of a coordinated strategy by a dedicated private banker. We provide clients in our Bermuda, Cayman Islands, and Guernsey segments with an integrated model that combines traditional wealth management with banking, lending, cash management, foreign exchange services, custody and access to asset management and trust professionals within Butterfield. We also provide our clients with immediate access to their account information through the use of internet banking. As of December 31, 2016, total deposits and loans in our private banking business were $3.3 billion and $0.9 billion, respectively.

Our asset management business line provides a broad range of portfolio management services to institutional and private clients. Our target client base includes institutions such as pension funds and captive insurance companies with investable assets over $10 million and private clients such as high net worth individuals, families, and trusts with investable assets over $1 million. Our principal services include discretionary investment management, managed portfolio services, money market, and mutual fund offerings. We also offer advisory and self-directed brokerage options. Over 90% of the business's discretionary investment mandates call for balanced growth to conservative allocations. We focus on delivery of reasonable appreciation with an emphasis on capital preservation. The Bank relies on well-recognized and leading third parties to provide research and investment management expertise, while our own services are concentrated on portfolio construction and managing client relationships. We also provide customized reporting to meet specific needs of our major clients. As of December 31, 2016 our asset management AUM were $4.7 billion.

From 2012 to 2016, our GAAP net income to common shareholders and our core net income to common shareholders (‘‘Core Net Income to Common’’) had compound annual growth rates (‘‘CAGRs’’) of 67% and 35%, respectively(1). These results were achieved despite a low interest rate environment. We attribute this financial performance to the attractive markets in our segments, leading position in those markets, strong operating discipline, conservative balance sheet deployment, and ability to grow our award-winning wealth management business. Our earnings generation has allowed us to build capital to return to shareholders and invest strategically, both organically and through acquisitions, to further enhance the growth prospects of our Company. We aim to continue to build excess capital in the future, which we can redeploy into growing our business and return to shareholders.

1

The following charts show the trajectory of our performance from 2012 to 2016:

GAAP Net Income to Common ($ in millions) | GAAP Earnings per Common Share Fully Diluted | |

Core Net Income to Common ($ in millions)1 | Core Earnings per Common Share Fully Diluted2 | |

(1) | Core Net Income to Common is a non-GAAP financial measure that is calculated by adjusting net income for income or expense items which management considers not to be representative of the ongoing operations of our business and preference share dividends, guarantee fees and premiums paid on preference share buybacks and redemptions. For a reconciliation of Core Net Income to Common to GAAP net income to common, see "Selected Consolidated Financial and Other Data – Reconciliation of Non-GAAP Financial Measures". |

(2) | Core Earnings per Common Share Fully Diluted is a non-GAAP financial measure that is calculated by dividing Core Earnings to Common by the weighted average shares outstanding. For a reconciliation of Core Earnings per Common Share Fully Diluted to GAAP earnings per share, see "Selected Consolidated Financial and Other Data – Reconciliation of Non-GAAP Financial Measures". |

2

Our History

The origin of The Bank of N.T. Butterfield & Son Limited traces back to 1758, to the founding of the trading firm of Nathaniel Butterfield. In 1858, our company was established as a bank in Bermuda and has been instrumental to the local economy ever since. The Bank was later incorporated under a special act of the local Parliament in 1904. In the 1960s, as international businesses began contributing substantially to Bermuda's economy, we developed services to meet their needs. In 1967, we opened offices in the Cayman Islands and by the 1980s had expanded our operations to include retail banking, investment management, and fund administration. In 1973, we opened our Guernsey office in order to provide customers with access to the Pound Sterling after Bermuda's departure from the British Sterling zone. In addition to being Bermuda's first bank, we have a long history of innovating financial services on the island: we opened the first ATMs in Bermuda in the 1980s and launched Bermuda's first internet banking service in 2001. In 1971, we listed our common shares on the Bermuda Stock Exchange under the ticker symbol "NTB.BH".

In 2016, we listed our common shares on the New York Stock Exchange under the ticker symbol "NTB". In 2008 and 2009, as a result of the global financial crisis, we realized losses attributable primarily to US non-agency mortgage backed securities in our investment portfolio, as well as write-downs on local market hospitality loans. To raise capital to offset these losses, the Bank executed a $200 million preference share offering in June 2009. In 2009 and 2010, we implemented a comprehensive restructuring plan for the Company: we hired a new management team, de-risked our balance sheet, and raised $550 million of common equity from a group of investors that included Carlyle Global Financial Services and related entities (collectively, "The Carlyle Group" or "Carlyle") and Canadian Imperial Bank of Commerce ("CIBC"), as well as existing shareholders. As part of the transaction, we launched a rights offering of $130 million on April 12, 2010, so as to allow the pre-transaction shareholders to participate in the recapitalization of the Company. The rights offering, which closed on May 12, 2010, was fully subscribed to, and the proceeds were used to repurchase shares from the recapitalization investors. As a result, the recapitalization investors' total investment was reduced to $420 million.

Since our restructuring, we have pursued a strategy to focus on our core strengths in banking and wealth management. We have executed upon our strategy by streamlining the Company's operations through exiting non-core markets, repositioning our balance sheet, investing in efficiency initiatives, and continuing to invest in our core business lines to grow both organically and through acquisitions. By following this strategy, we have significantly improved our financial results including growing Core Earnings to Common every year since 2011 and have been able to initiate a capital return policy for investors. The following items were key steps in executing our strategy:

• | In 2010, we sold our operations in Hong Kong and Malta, and in 2012, we sold our operations in Barbados as they were no longer consistent with our strategy. |

• | In 2010, we sold $820 million of asset-backed securities to cleanse our investment portfolio. |

• | In 2013, we implemented an annual cash dividend of $0.40 per year plus a $0.10 per year special dividend. |

• | In 2014, we completed two acquisitions, which allowed us to both expand and complement our existing business lines: Legis Group Holdings' Guernsey-based trust and corporate services business, as well as a significant portion of HSBC's corporate and retail banking business in the Cayman Islands. |

• | In April 2015, CIBC sold its 19% ownership stake. We repurchased and retired 8 million shares for a total of $120 million, and The Carlyle Group purchased CIBC's remaining 2.3 million shares and subsequently sold them to other existing investors. |

• | In December 2015, we repositioned our balance sheet to better match the duration of our assets and liabilities and to reclassify a portion of our Available for Sale ("AFS") portfolio as Held to Maturity ("HTM"). |

• | In February 2016, we commenced an orderly wind-down ("OWD") of our UK operations. We exited our private banking and asset management operations in our UK segment, but retain our UK high net worth mortgage lending business. The OWD was largely completed by the end of 2016 with the change in the business operations to mortgage lending services and the change of name from UK operations to Butterfield Mortgages Limited. The excess capital in the UK was released early in 2017, which we intend to invest in other areas of our business. |

• | In April 2016, we completed an acquisition of HSBC's Bermuda trust business and private banking investment management operations that added $1.6 billion of deposits to our balance sheet. As part of the transaction, HSBC also entered into an agreement to refer its existing private banking clients to Butterfield. |

• | In September 2016, we successfully completed a $288 million initial public offering and listing on the New York Stock Exchange, through which we raised approximately $126 million in net primary proceeds. |

• | In December 2016, we redeemed and canceled all of our issued and outstanding preference shares, which had a book value of $183 million, removing approximately $16 million of annual preference dividend and guarantee fees. We also repurchased for cancellation the outstanding warrant from the Government of Bermuda, removing a potentially dilutive instrument. |

Our Markets

Our two largest segments are Bermuda and the Cayman Islands. As of December 31, 2016, 59% of our total assets were held by our Bermuda segment and 29% by our Cayman Islands segment. Bermuda is our largest segment by number of employees, and we are the country's largest independent bank. As of December 31, 2016, our Bermuda segment had $6.8 billion of assets, $50.1 billion of trust AUA and $3.4 billion of AUM, and our Cayman Islands segment had $3.4 billion of assets, $4.0 billion of trust AUA and $0.8 billion of AUM.

3

The charts below provide the geographic distribution of our Net Revenue for the year ended December 31, 2016.

Segment Distribution of Net Revenue |

2016 Net Revenue: $406.0 million

Bermuda is a leading international financial center and a global hub for reinsurers, captive insurers, and other multi-national corporations. Foreign currency assets held by local banks totaled $18 billion in 2015, more than three times gross domestic product ("GDP") for the same period. According to a 2015 report from the Federal Insurance Office of the US Department of the Treasury, Bermuda is the domicile for 15 of the world's 40 largest reinsurance groups and accounts for 11% of global reinsurance premiums written and 15% of global property & casualty reinsurance premiums written. Bermuda's captive insurance market includes approximately 750 captive insurers according to a 2015 report by the BMA. Home to a population of approximately 66,000, the country had the second highest GDP per capita income in the world in 2015 at approximately $92,500 and a nominal GDP of $5.7 billion according to The Economist.

The Cayman Islands is also a leading international financial center, serving as the leading domicile for hedge funds globally and the second largest domicile (after Bermuda) for captive insurers globally. Total deposits held by banks equaled $12 billion as of 2015, or more than three times GDP for 2015. As of December 31, 2016, there were 10,586 regulated mutual funds registered in the Cayman Islands with 106 mutual fund administrators according to CIMA. We hold business relationships with approximately 650 funds, fund administrators, and related entities. Home to a population of approximately 60,000, the country had a 2015 GDP per capita of approximately $56,100 and a nominal GDP of $9.2 billion according to the Cayman Islands' Annual Economic Report.

The table below highlights the relative position of Bermuda and the Cayman Islands compared to the US and UK based on several macroeconomic factors:

Comparison of Selected 2015 Macroeconomic Indicators(1)

Bermuda | Cayman Islands | USA | UK | |||||||||||||

GDP per Capita (in thousands of $) | $ | 92.5 | $ | 56.1 | $ | 55.9 | $ | 44.2 | ||||||||

Unemployment | 7.0 | % | 4.2 | % | 5.3 | % | 5.4 | % | ||||||||

Consumer Price Inflation | 1.4 | % | (2.3 | )% | 0.1 | % | 0.1 | % | ||||||||

___________________

(1) | Source: The Economist, 2015 Bermuda Labour Force Survey Executive Report, and The Cayman Islands' Labour Force Survey Report Fall 2015 |

The international trust market is primarily concentrated in select jurisdictions, including Bermuda, the Cayman Islands, Guernsey, Hong Kong, Jersey, Singapore, and Switzerland. The leading international trust law firms serve as key introducers of clients to Butterfield and are the primary source of new business. Trust clients often hold assets that are international in nature, and as a result, performance of trust businesses is not generally linked to performance of the domestic economies where clients are served.

The private banking market in Bermuda, the Cayman Islands, and Guernsey is composed largely of resident high net worth individuals meeting minimum deposit and/or loan thresholds. Clients are introduced to the private bank through Butterfield's retail banking operation upon reaching the appropriate deposit or loan threshold, Butterfield's trust and asset management arms, as well as through external introducers. Although locally based, private banking clients often hold international assets, and as a result, business performance is not necessarily correlated to the domestic economies where clients are served.

Our asset management business line operates in Bermuda, the Cayman Islands, and Guernsey. As of December 31, 2016, 73% of our AUM was in Bermuda, 18% was in the Cayman Islands, 8% was in Guernsey. In Bermuda and the Cayman Islands, a majority of our institutional and private clients are domestic from a domicile perspective while a majority of our clients in Guernsey are tied to our trust business and are international in nature.

4

Our Competitive Strengths

Leading Bank in Attractive Markets

We are a leading bank in Bermuda with a 39% market share in BMD deposits and a 36% market share in BMD loans, respectively, as of December 31, 2015 (Source: BMA). In the Cayman Islands, we have a 35% market share in local deposits and a 25% market share in local mortgages as of December 31, 2015 (Source: CIMA). The Bermuda and Cayman Islands banking markets have historically been characterized by a limited number of participants and significant barriers to entry. In addition, these markets provide us with access to several attractive customer bases: in retail banking, we serve local residents and businesses; in corporate banking, we serve captive insurers, hedge funds, middle-market reinsurers, and other corporates; and in wealth management, we serve private trust clients and ultra-high net worth and high net worth individuals and families. Our market share, scale, history, and brand in our Bermuda and Cayman Islands segments have enabled us to achieve our strategic objectives, including lending at attractive margins, attracting low cost, sticky deposits, and growing our wealth management business, all of which have driven our earnings and capital generation.

Strong Capital Generation and Return

Since our recapitalization, we have streamlined our business by exiting non-core markets, executing on various operating efficiency initiatives, shifting the risk profile of our loan and securities portfolios, running off our legacy loan and securities portfolios, and deploying our excess capital in the form of dividends and share repurchases. Our return on equity for 2016 of approximately 9% and our Core ROATCE for 2016 of approximately 21% were driven by a number of factors, including: significant fee income with historically low capital requirements, low cost deposits, a high yielding loan portfolio, a conservative capital efficient securities portfolio, and our operations in corporate income tax neutral jurisdictions. As a result, our business generated core net income in 2016 well in excess of that needed to execute our organic balance sheet growth strategy.

Return on Equity | Core ROATCE1 | |

____________________________

(1) | Core ROATCE is a non-GAAP financial measure that is calculated by dividing core earnings to common shareholders by average tangible common equity. Average tangible common equity does not include the preference shareholders' equity or goodwill and intangible assets. For more information on the non-GAAP financial measures, see "Selected Consolidated Financial and Other Data — Reconciliation of Non-GAAP Financial Measures." |

Growth Opportunities

We expect that, all else being equal, a rising rate environment would increase our net interest income before provision for credit losses because an increase in our cost of deposits would lag an increase in yield of our securities and loans. In addition, a significant portion of our deposits are non-interest bearing (24% as of December 31, 2016), and as a result, a portion of our funding is insensitive to rising rates. Our non-interest bearing deposit balances have historically exhibited low correlation with interest rates, a behavior that we attribute in part to a sizeable client base that utilizes our bank for cash management purposes. Potential changes to our net interest income in hypothetical rising and declining rate scenarios, measured over a 12-month period, are presented in the chart below (these projections assume parallel shifts of the yield curves occurring immediately and no changes in other potential variables):

5

Net Interest Income Sensitivity |

A down 100 basis points interest rate shock shows a reduction in projected 12-month net interest income of 8.9% from the flat scenario. The loss of income is driven by lower loan and investment yields, which more than offset reduced rates paid on deposits. Mitigating against the loss of income is the potential to charge negative interest rates on deposits (which we currently do in some instances) and certain loans that have rate floors.

In addition, we are well-positioned as an acquirer of certain businesses, primarily in wealth management. Our acquisition strategy seeks to capitalize on opportunities created by international financial institutions that have faced operating issues requiring them to simplify their businesses. We consider a wide range of potential acquisition opportunities, and we have a well-defined, disciplined approach to identifying potential acquisition targets across numerous criteria including: geography, business alignment, size, timing, quality, buyer universe and financial hurdles. Our recent focus has been primarily on the private trust business where we have expertise, scale and a strong brand.

In 2014, we completed two acquisitions that allowed us to both expand and complement our existing businesses: In April 2014, we completed the acquisition of Legis Group’s Guernsey-based trust and corporate services business. The transaction enhanced the scale of our international trust capabilities and fortified our position as a leading player in Guernsey. In November 2014, we acquired select deposits and loans in the Cayman Islands from HSBC. At close, the transaction added approximately $0.5 billion of customer deposits with an average cost of 0.12%, and $144 million of loans.

In April 2016, we acquired HSBC’s Bermuda trust business and private banking investment management operations. HSBC also entered into an agreement to refer its existing private banking clients to Butterfield. This acquisition added over $18.9 billion of trust AUA, $1.3 billion of AUM, and $1.6 billion of deposits.

Efficient Balance Sheet and Visible Earnings

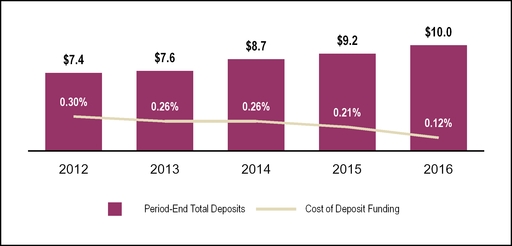

Our relationship-driven business model and international corporate clientele have allowed us to develop a sticky deposit base with historically low funding costs. We believe our customers’ deposit activity has historically been inelastic to deposit pricing given the nature of corporate activity and competition in retail deposit taking in our segments. From 2012 to 2016, customer deposits have grown at a compound annual growth rate (‘‘CAGR’’) of approximately 14% in Bermuda and 12% in the Cayman Islands, taking into account the HSBC Cayman acquisition in November 2014 that added $0.5 billion of new deposits, and the April 2016 acquisition of HSBC’s Bermuda trust business and private banking investment management operations that added $1.6 billion of new deposits. As of December 31, 2016, we had $10.0 billion in deposits at a cost of

0.12%, of which 24% were non-interest bearing demand deposits, 58% were interest bearing demand deposits with a weighted-average cost of 0.07%, and 18% were term deposits with a weighted-average cost of 0.47% and an average maturity of 80 days. We believe the market conditions in Bermuda and the Cayman Islands will allow us to continue to benefit from favorable deposit pricing.

6

The following chart shows customer deposit trends for 2012 to 2016:

Deposit Balance and Funding Costs ($ in billions) |

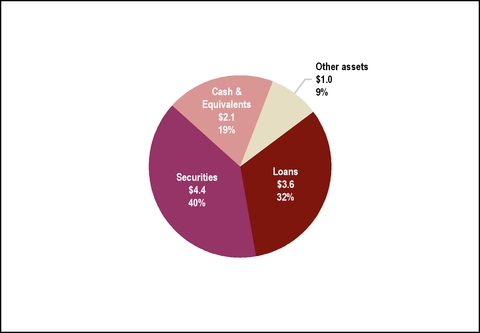

Historically, the markets in which we operate generate fewer loans than deposits, which has led us to take a conservative approach to managing our balance sheet. We accomplish this by maintaining a large cash balance and investing in high quality and liquid securities. The following chart illustrates our asset composition as of December 31, 2016:

Balance Sheet Composition - Total Assets ($ in billions) |

As of December 31, 2016, 19% of our balance sheet was cash and cash equivalents, which included cash and demand deposits with banks, unrestricted term deposits, certificates of deposits, and treasury bills with a maturity less than three months.

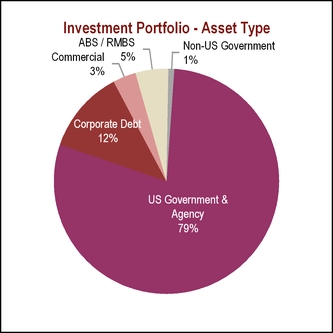

In addition to maintaining a large cash balance, we also have a large securities investment portfolio. We have a disciplined investment portfolio selection process and invest in highly rated securities. We also seek to ensure that our portfolio remains liquid across market cycles: 79% of our portfolio was invested in US government treasuries and mortgage-backed securities issued by US governmental agencies. Our investment strategy aims to align the interest rate risk profile of our assets and liabilities — as of December 31, 2016, the average duration of our AFS investment portfolio was 2.5 years, the average duration of our HTM investment portfolio was 6.3 years, and the average duration of our total investment portfolio was 3.4 years. As of December 31, 2016, the total value of our AFS investment portfolio was $3.3 billion, and the total value of our HTM investment portfolio was $1.1 billion.

7

The following charts show the composition of our investment portfolio by rating and asset type as of December 31, 2016:

Investment Portfolio - Rating | Investment Portfolio - Asset Type | |

The combination of our significant cash and securities portfolios helps drive our capital efficient balance sheet, with risk-weighted assets equal to 39% of our total assets and a Basel III total capital ratio of 17.6%, each as of December 31, 2016.

Our loan underwriting process requires that we complete a full credit assessment of every customer prior to committing to a loan, which we believe has resulted in a high quality loan portfolio. Our lending markets do not have secondary markets for loans and as such we hold all of our originated loans on our balance sheet. In 2015 and 2016, net charge-offs represented 0.2% and 0.3%, respectively, of average loans. As of December 31, 2016, our non-accrual loan balance was $48.5 million, or 1.3% of total loans, and 84% of our loans past due were full recourse residential mortgages. As of December 31, 2016, our loan portfolio consisted of 94% floating-rate loans and 6% fixed-rate loans.

The following chart shows the segment composition of our loan portfolio as of December 31, 2016:

Loan Portfolio Composition - Geography |

8

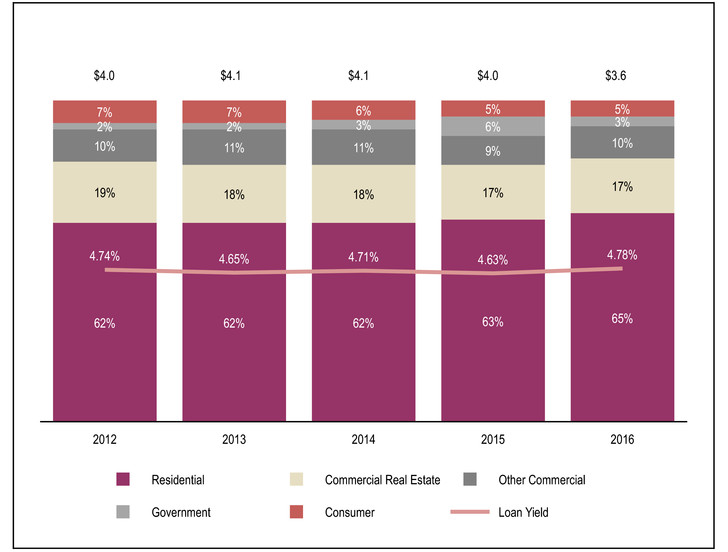

Our loan portfolio has exhibited stability over time. The following chart shows loan portfolio trends for 2012 to 2016:

Loan Balance and Yield ($ in bilions) |

The domestic lending markets in Bermuda and the Cayman Islands have a limited number of participants and significant barriers to entry. 65.2% of our loan balances were residential mortgages as of December 31, 2016. These loans are attractive for a number of reasons. The average yield on new retail residential mortgage originations in our Bermuda and Cayman segment in the fourth quarter of 2016 was 4.47%, which we believe is consistent with other firms that compete in our markets. In addition, our mortgages have exhibited predictable cash flows, with historically negligible refinancing activity due to high costs to refinance in Bermuda and the Cayman Islands. Finally, our mortgages have historically benefited from a manual underwriting process, low LTVs (68% of residential loans below 70% LTV as of December 31, 2015), and a full recourse system in Bermuda and the Cayman Islands.

We have also generated balanced sources of non-interest income from a well-diversified customer base. For the five year period ended December 31, 2016, our non-interest income is evenly split between banking which consists of banking and foreign exchange revenue, and wealth management, which consists of trust, asset management, and custody and other administration services. The wealth management non-interest income stream is not directly correlated with the performance of our banking business. For example, the typical trust we manage generates a relatively constant fee stream on an annual basis throughout its life. In addition, because fee revenue in our wealth management business lines is primarily driven by the size of our clients’ assets and holdings, which are generally diversified across multiple geographies, the performance of these businesses is not typically linked to the economies of our local markets. Non-interest income represented 36% of our total Net Revenue in 2016, and contributed materially to the Company’s high Core ROATCE and excess capital generation as limited capital is required for our fee income business.

9

The following charts show our various sources of non-interest income for the year ended December 31, 2016:

Non-Interest Income1 |

2016 Non-Interest Income: $147.5 million / 36.3% of Net Revenue

_____________

(1) Foreign exchange revenue represents income generated from client-driven transactions in the normal course of business. We do not engage in proprietary trading.

Strong Leadership with Deep Knowledge of Our Domestic and International Markets

Our management team has extensive and varied experience managing banking and financial services firms. We believe that our management team’s reputation and performance track record gives us an advantage in executing our organic growth and acquisition strategies.

Name | Title | Joined Butterfield | Prior Experience | Years of Experience | ||||

Michael Collins | Chief Executive Officer | 2009 | COO of HSBC Bermuda | 31 | ||||

Michael Schrum | Chief Financial Officer | 2015 | CFO of HSBC Bermuda | 21 | ||||

Daniel Frumkin | Chief Risk Officer | 2010 | CRO of Retail Banking at RBS | 30 | ||||

Robert Moore | Group Head of Trust | 1997 | Senior Manager of International Private Banking with Lloyds | 38 | ||||

Michael Neff | Group Head of Wealth Management | 2011 | Global Head of Wealth Management at RiskMetrics | 29 | ||||

In addition to his role as CEO, Michael Collins serves as a member of our Board. Barclay Simmons, our Non-Executive Chairman since 2015, joined our Board in 2011 and was named Vice Chairman in 2012. We have seven additional non-executive directors, who bring to the Bank a diverse array of experiences in the financial services industry from across the globe.

Our Strategy

Butterfield is both a leading banking business in Bermuda and the Cayman Islands and a growing, award-winning, and international wealth management business with operations in Bermuda, the Cayman Islands, Guernsey, The Bahamas, and Switzerland. Our strategy focuses on maintaining our leading banking position in Bermuda and the Cayman Islands while continuing to grow scale in our wealth management business across our core geographies. The key components of our strategic plan are:

Banking

Leverage Our Leading Market Position

We seek to remain a leading bank in Bermuda and the Cayman Islands in terms of local deposit and lending market share by continuing to provide excellent service, employ a high-quality work force, and offer a competitive product suite to our customers.

10

Improve Operating Efficiency

Our banking business operates in geographies with high operational costs. We carefully manage our cost structure to improve efficiency through the deployment of technology and continuous process improvement. We expect continued investments in core banking systems and expansion of electronic channels in Bermuda and the Cayman Islands, as well as upgrades in Guernsey, to result in improved operational efficiency.

Wealth Management

Leverage Relationships with Key Introducers

We have over 70 years of experience providing sophisticated trust services and an award-winning brand and we believe that our reputation and expertise are well-recognized by industry insiders, including the leading international trust law firms. These firms act as a key source of new business for trust services. We plan to leverage our relationships with key introducers to continue to grow our company and build our brand, as well as invest in the further development of our technical expertise and multi-jurisdictional offering. Our recent trust acquisitions have grown the size and reach of our business. As we continue to grow through organic and inorganic means, we believe that our business will increasingly benefit from referrals by key introducers.

Utilize Multi-Jurisdictional Offerings to Attract Client Base

We seek to take advantage of our presence, seasoned trust officers, and product offerings in key international financial centers in Bermuda, the Cayman Islands, Guernsey, The Bahamas, and Switzerland to attract our target client base. International trust law varies across different jurisdictions, and our multi-jurisdictional presence enables us to cater to a variety of client preferences from a geographical perspective. In recent years, we have experienced increased demand for trust services from our European, Asian, Latin American, and Middle Eastern clients. We view our trust business line as an opportunity for further growth.

Emphasize Strong Client Relationships

Our primary focus is to build strong client relationships using our knowledge of the local market and combining our banking and wealth management services to meet the financial needs of our customers. We believe our experience in building strong, long-term client relationships in our wealth management business will enable us to retain our existing clients and attract additional trust, private banking, and asset management business from them, as well as receive referrals to potential new clients. In addition, our wealth management business sources customers and benefits from the strong relationships we have in our banking business.

Expand Revenues from Client Relationships Across Our Wealth Management Services

We believe that there is an opportunity to increase the revenues generated from client relationships across our wealth management business lines. For example, we seek to create personal banking and wealth management relationships with the professionals for whom we provide corporate banking services. In addition, trust relationships, which are very long lived, can present opportunities for use of other Butterfield services at different stages of a trust's lifecycle or to meet needs of family members outside the trust itself.

Client relationships from our recent acquisitions represent another area of opportunity to expand Butterfield services and products for high net worth customers and certain corporate and institutional clients. Through the acquisition of HSBC's Bermuda trust business and private banking investment management operations, we migrated 285 new relationships and $1.6 billion of deposits onto our platform.

Improve Operating Efficiency

We continue to identify areas where we can improve cost efficiency without impacting our quality of client service. Past initiatives have included implementation of one global Trust Administration system across segments, implementation of a new custody system, consolidation of our trading operations, and reduction in our fund administration expenses through consolidation.

Pursue Prudent Acquisitions to Increase Scale

We intend to continue pursuing acquisitions aligned with existing business operations, in particular to increase the scale of our trust business line. The fragmented nature of the market, with approximately 500 trust companies operating in key international financial centers, and recent sales of subsidiaries by several international financial institutions have created a favorable environment for companies with the resources and expertise to act as effective consolidators. We believe that our management team has developed a rigorous approach for conducting due diligence and efficiently integrating acquired businesses to meet our internal financial hurdles. In addition, we may pursue acquisitions of other wealth management businesses, including private banking businesses, and we plan to continue to opportunistically analyze potential acquisitions as a means of capital deployment.

Corporate Information

We are a local company incorporated under the laws of Bermuda, incorporated on October 22, 1904, pursuant to the Butterfield Act. We are registered with the Registrar of Companies in Bermuda under registration number 2106. Our registered office and principal executive offices are located at 65 Front Street, Hamilton, HM 12, Bermuda. Our agent for service of process in the United States is C T Corporation System, 111 Eighth Avenue, New York, New York 10011. Our telephone number is (441) 295-1111. We maintain a website at www.butterfieldgroup.com. Neither this website nor the information on or accessible through this website is included or incorporated in, or is a part of, this report.

Summary Risk Factors

Any of the factors set forth under "Risk Factors" may limit our ability to successfully execute our business strategy. Among these important risks are the following:

• | Adverse economic and market conditions, in particular in Bermuda and the Cayman Islands, have in the past resulted in and could in the future result in lower revenue, lower asset quality, increased provisions and lower earnings. |

• | Unlike geographically more diversified banks, our business is concentrated primarily in Bermuda and the Cayman Islands, and we may be more affected by a downturn in these markets than more diversified competitors. |

• | A decline in the residential real estate market, in particular in Bermuda, could increase the risk of loans being impaired and could have an adverse effect on our business, financial condition or results of operations. |

• | The value of the securities in our investment portfolio may decline in the future. |

11

• | Fluctuations in interest rates and inflation may negatively impact our net interest margin and our profitability. |

• | We depend primarily on deposits to fund our liquidity needs; if we are unable to effectively manage our liquidity across the jurisdictions in which we operate, our business, financial condition or results of operations could be adversely affected. |

• | We face competition in all aspects of our business, and may not be able to attract and retain wealth management, trust and banking clients at current levels. |

• | We could fail to attract, retain or motivate highly skilled and qualified personnel, including our senior management, other key employees or members of the Board, which could adversely affect our business; |

• | Our controls and procedures may fail or be circumvented, which could have an adverse impact on our business, financial condition or results of operations. |

• | Volatility levels and fluctuations in foreign currency exchange rates may affect our business, financial position and results of operations. |

• | Our international business model exposes us to different and possibly conflicting regulatory schemes across multiple jurisdictions. |

• | US withholding tax and information reporting requirements imposed under the Foreign Account Tax Compliance Act may apply. |

• | Fulfilling public company financial reporting and other regulatory obligations in the United States is expensive, time-consuming and may strain our resources. |

• | The uncertainty resulting from the recent vote by the UK electorate in favor of a UK exit from the European Union ("EU"), as well as changes in US legislation, regulation and government policy as a result of the 2016 US presidential and congressional elections, could adversely impact our business, financial condition and results of operations. |

• | We operate in a complex regulatory environment and legal and regulatory changes could have a negative impact on our business, financial condition or results of operations. |

• | Changes in US tax laws could cause the insurance and reinsurance industry to relocate from Bermuda, which could have an adverse effect on our business, financial condition and results of operations. |

• | Provisions of Bermuda law and our bye-laws could adversely affect the rights of our shareholders or prevent or delay a change in control. |

• | Bermuda law differs from the laws in effect in the United States and might afford less protection to shareholders. |

12

Our International Network and Group Structure

The following map presents the several geographic regions in which our business operates:

The following chart presents our corporate structure, indicating our principal subsidiaries as of December 31, 2016:

Bermuda

The Bank itself is licensed in Bermuda to provide banking services and wealth management services. Through its wholly owned Bermuda subsidiary Butterfield Asset Management Limited it provides asset management services and through its wholly owned Bermuda subsidiaries Butterfield Trust (Bermuda) Limited and Bermuda Trust Company Limited it provides corporate trustee, fiduciary and corporate administration services. Bermuda Securities (Bermuda) Limited provides investment advisory and listing sponsor services.

Cayman Islands

Butterfield Bank (Cayman) Limited, a wholly owned subsidiary of the Bank, provides banking services and its subsidiary Butterfield Trust (Cayman) Limited provides trustee, fiduciary and corporate administration services.

13

Guernsey

Butterfield Bank (Guernsey) Ltd. is a wholly owned subsidiary of the Bank and provides private banking, custody and administered banking services. Butterfield Trust (Guernsey) Ltd. is a subsidiary of Butterfield Bank (Guernsey) Limited. and provides trustee and fiduciary services.

Bahamas

Butterfield Trust (Bahamas) Limited is a wholly owned subsidiary of the Bank and provides trust and fiduciary services.

Switzerland

Butterfield Holdings (Switzerland) Limited is a wholly owned subsidiary of the Bank and provides investment services and through its subsidiary Butterfield Trust (Switzerland) Limited provides trust and fiduciary services.

United Kingdom

Butterfield Mortgages Limited is a wholly owned subsidiary of the Bank and provides residential property lending services.

Competition

The financial services industry and each of the markets in which we operate are competitive. We face strong competition in gathering deposits, making loans and obtaining client assets for management. We compete, both domestically and internationally, with globally oriented asset managers, retail and commercial banks, investment banking firms, brokerage firms and other investment service firms. Due to the trend toward consolidation in the global financial services industry, our larger competitors tend to have broader ranges of product and service offerings, increased access to capital, and greater efficiency. Larger financial institutions may also have greater ability to leverage increasing regulatory requirements and investment in expensive technology platforms. We also face competition from non-banking financial institutions. These institutions have the ability to offer services previously limited to commercial banks. In addition, non-banking financial institutions are not subject to the same regulatory restrictions as banks, and can often operate with greater flexibility and lower cost structures.

The Bermuda banking segment currently consists of four licensed banks and one licensed deposit-taking institution including one large subsidiary of an international bank, HSBC, and three domestic institutions, including Bermuda Commercial Bank and Clarien Bank. In the Cayman Islands, the Bank is one of six Class 'A' full service retail banks licensed to conduct business with domestic and international clients. There are also five non-retail Class 'A' banks and 148 limited service Class 'B' banks, including Cayman National and subsidiaries of international banks, such as RBC. In certain interest rate environments, additional significant competition for deposits may be expected to arise from corporate and government debt securities and money market mutual funds. We view HSBC in Bermuda and RBC in the Cayman Islands as our most significant competitors.

In our wealth management business line, we face competition from local competitors as well as much larger financial institutions including financial institutions that are not based in the markets in which we operate. Revenues from the trust and wealth management business depend in large part on the level of assets under management, and larger international banks may have higher levels of assets under management.

In our trust business line, we face competition primarily from other specialized trust service providers. There are approximately 500 trust companies in the main international financial centers, and many of our competitors in this sector offer fund administration and corporate services work alongside private client fiduciary services.

Competition for deposits is also affected by the ease with which customers can transfer deposits from one institution to another. Our cost of funds fluctuates with market interest rates and may be affected by higher rates being offered by other financial institutions. Our management believes that our most direct competition for deposits comes from international and domestic financial services firms that target the same customers as the Bank.

Deposits

We are a deposit-led institution with leading market share in our primary segments: Bermuda and the Cayman Islands. We strive to maintain deposit growth and to maintain a strong liquidity profile through a significant excess of deposits over loans through market cycles.

Our deposits are generated principally by our banking business line, which offers retail and corporate checking, savings, and term deposits through our segments in Bermuda, the Cayman Islands and Guernsey. In addition, wealth management, through its private banking business line, also provides deposit services to high net worth and ultra-high net worth clients in those same geographic segments. As of December 31, 2016, our Bermuda, Cayman Islands and Guernsey segments contributed $5.9 billion, $3.0 billion and $1.0 billion, respectively, to our total customer deposit base. Deposits from all other segments totaled $0.1 billion as of December 31, 2016.

Total deposits as of December 31, 2016 were $10.0 billion, up 9.3% over total deposits as of December 31, 2015. Customer demand deposits, which include checking, savings and call accounts, totaled $8.2 billion, or 81.9% of customer deposits, as of December 31, 2016, compared to $7.7 billion, or 84%, as of December 31, 2015. Customer term deposits totaled $1.8 billion as of December 31, 2016. The cost of funds on total deposits improved from 21 basis points in 2015 to 12 basis points as of December 31, 2016 as a result of an increase in non-interest bearing deposits and small rate decreases in some jurisdictions, as well as the full repayment of the UK segment deposits, which carried a relatively higher cost than other jurisdictions.

Lending

We offer a broad set of lending offerings including residential mortgage lending, automobile lending, credit cards consumer financing, and overdraft facilities to our retail customers, and commercial real estate lending, commercial and industrial loans, and overdraft facilities to our commercial and corporate customers. These offerings are provided to our retail, commercial, and private banking clients in our key jurisdictions including Bermuda and the Cayman Islands. We also offer residential mortgage lending through our private banking business in Guernsey and to our high net worth and ultra-high net worth clients in the UK. Our loan portfolio, net of allowance for credit losses stood at $3.6 billion as of December 31, 2016. The loan portfolio represented 32.2% of total assets as of December 31, 2016, and loans, net of allowance for credit losses, as a percentage of customer deposits were 35.7%. The effective yield on total loans for the year ended December 31, 2016 was 4.78%, compared to 4.57% for the year ended December 31, 2015.

Residential Mortgage Lending

The residential mortgage portfolio comprises mortgages to clients with whom we are seeking to establish (or already have) a comprehensive financial services relationship. It includes mortgages to individuals and corporate loans secured by way of first ranking charges over the residential property to which each specific loan relates generally on terms which allow for the repossession and sale of the property if the borrower fails to comply with the terms of the loan. As of December 31, 2016, residential

14

mortgages (after specific allowance for credit losses) totaled $2.3 billion (a $197.5 million decrease from December 31, 2015), accounting for approximately 64.6% of the Group's total gross loan portfolio (after specific allowance for credit losses) and approximately 84.3% of total non-accrual loans in the Group's loan portfolio.

Consumer Lending

We provide loans, as part of our normal banking business, in respect of automobile financing, consumer financing, credit cards and overdraft facilities to retail and private banking clients in the jurisdictions in which we operate. As of December 31, 2016, non-residential loans to consumers (after specific allowance for credit losses) totaled $197.8 million, accounting for approximately 5.5% of the Group's total gross loan portfolio and approximately 2.1% of total non-accrual loans in the Group's loan portfolio.

Commercial Real Estate Lending

Commercial real estate loans are offered to real estate investors, developers and builders domiciled primarily in Bermuda and the United Kingdom. To manage the Group's credit exposure on such loans, the principal collateral is real estate held for commercial purposes and is supported by a registered mortgage. Cash flows from the properties, primarily from rental income, are generally supported by long-term leases.

As of December 31, 2016, our commercial real estate loan portfolio (after specific allowance for credit losses) totaled $609.8 million, accounting for approximately 16.9% of the Group's total gross loan portfolio and approximately 12.4% of total non-accrual loans in the Group's loan portfolio.

Our commercial real estate loan portfolio is broken down into two categories: commercial mortgage and construction. As of December 31, 2016, commercial mortgages totaled $580.9 million (after allowance for credit losses), and construction loans totaled $28.9 million, accounting for approximately 95.3% and 4.7% of our commercial real estate loan portfolio before allowance for credit losses, respectively.

Other Commercial Lending

The commercial and industrial loan portfolio includes loans and overdraft facilities advanced primarily to corporations and small and medium-sized entities, which are generally not collateralized by real estate and where loan repayments are expected to flow from the operation of the underlying businesses. As of December 31, 2016, the Group's other commercial loan portfolio totaled $469.0 million, accounting for approximately 13.0% of the Group's total gross loan portfolio. As of the same date, the Group's loans to governments totaled $112.4 million, accounting for approximately 3.1% of our loan portfolio. As of December 31, 2016, other commercial loans accounted for approximately 1.2% of our total non-accrual loans, and there were no loans to governments classified as non-accrual loans.

Investments

Given the large customer deposit base commanded in our Bermuda and Cayman Islands operations, and the relatively low volume of lending demand from our customer base, our investment strategy is more important than may be the case for most financial institutions. In recognition of this, we maintain what we believe to be a conservative approach to investments, requiring the purchase of mainly fixed-rate investments in order to manage interest rate risk. Our investment portfolio is comprised mainly of securities issued or guaranteed by the US Government or federal agencies. The securities in which we invest are generally limited to securities that are considered investment grade (i.e., "BBB" and higher by S&P's Financial Services LLC or an equivalent credit rating). Effective July 31, 2012, we entered into an agreement with Alumina Investment Management LLC ("Alumina") pursuant to which Alumina provides investment advisory services to us in respect of our US Treasury and agency portfolio.

As of December 31, 2016, the Group held $4.4 billion in investments, representing approximately 39.6% of total assets.

Cash and Liquidity Management

We operate across multiple currency jurisdictions with pervasive multi-currency products. In our deposit taking jurisdictions—Bermuda, the Cayman Islands and Guernsey—there are currently no dedicated central banks, and no deposit insurance scheme infrastructures (such as the Federal Deposit Insurance Corporation in the United States), with the exception of Bermuda, where a deposit insurance scheme has recently been implemented. In addition, we do not have access to borrowing or deposit facilities with the US Federal Reserve or the European Central Bank; therefore, we conservatively manage client deposit balances and the liquidity risk profile of our balance sheets. This involves the retention of significant cash or cash equivalent balances, management of intra-bank counterparty exposure and management of a significant short-dated US Treasury Bill portfolio. As of December 31, 2016, the cash due from banks of $2.1 billion was comprised primarily of $1.7 billion in interest earning cash equivalents, which are investments with a less than ninety day duration. The remaining amounts were comprised of non-interest earning and interest earning deposits of $0.1 billion and $0.3 billion, respectively.

Foreign Exchange Services