UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10‑K

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended: December 31, 2020

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number 001-38118

DERMTECH, INC.

(Exact name of registrant as specified in its charter)

|

Delaware (State or other jurisdiction of incorporation or organization) |

84-2870849 (IRS Employer Identification No.) |

|

|

|

|

11099 N. Torrey Pines Road, Suite 100 La Jolla, CA |

92037 (Zip Code) |

Registrant’s telephone number, including area code: (858) 450‑4222

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

|

Common Stock, par value $0.0001 per share |

DMTK |

The Nasdaq Capital Market |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well‑known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such report(s), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S‑T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non‑accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b‑2 of the Exchange Acts.

|

Large accelerated filer |

|

☐ |

|

Accelerated filer |

|

☐ |

|

|

|

|

|

|

|

|

|

Non-accelerated filer |

|

☒ |

|

Smaller reporting company |

|

☒ |

|

|

|

|

|

|

|

|

|

|

|

|

|

Emerging growth company |

|

☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b‑2 of the Act). Yes ☐ No ☒

The aggregate market value of the registrant’s common stock, $0.0001 par value, held by non‑affiliates of the registrant as of the last business day of the registrant’s most recently completed second fiscal quarter was approximately $150,521,679 (based on the closing price of the registrant’s common stock on June 30, 2020 of $13.23 per share).

The number of shares outstanding of the registrant’s common stock, $0.0001 par value as of March 1, 2021 was 28,755,668.

DOCUMENTS INCORPORATED BY REFERENCE

The registrant intends to file a definitive proxy statement pursuant to Regulation 14A within 120 days after the end of the fiscal year ended December 31, 2020. Portions of such proxy statement are incorporated by reference into Part III of this Form 10‑K.

ANNUAL REPORT ON FORM 10‑K

YEAR ENDED DECEMBER 31, 2020

|

|

|

Page No. |

|

|

3 |

|

|

3 |

||

|

28 |

||

|

56 |

||

|

56 |

||

|

56 |

||

|

56 |

||

|

|

57 |

|

|

57 |

||

|

57 |

||

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

58 |

|

|

66 |

||

|

67 |

||

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

99 |

|

|

99 |

||

|

99 |

||

|

|

100 |

|

|

100 |

||

|

100 |

||

|

Security and Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

100 |

|

|

Certain Relationships and Related Transactions, and Director Independence |

100 |

|

|

100 |

||

|

|

101 |

|

|

101 |

||

|

104 |

||

|

105 |

||

i

Special Note Regarding Forward-Looking Statements

This report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. Forward-looking statements are statements other than historical facts and relate to future events or circumstances or our future performance, and they are based on our current assumptions, expectations and beliefs concerning future developments and their potential effect on our business. Words such as, but not limited to “anticipate,” “aim,” “believe,” “contemplate,” “continue,” “could,” “design,” “estimate,” “expect,” “intend,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “pro forma,” “project,” “seek,” “should,” “suggest,” “strategy,” “target,” “will,” “would,” and similar expressions or variations thereof are intended to identify forward-looking statements, but are not deemed to represent an all-inclusive means of identifying forward-looking statements as denoted in this report. These statements include, among other things, statements regarding:

|

|

• |

our ability to attain profitability; |

|

|

• |

our estimates regarding our future performance, including without limitation estimates of potential future revenues; |

|

|

• |

our ability to maintain commercial reimbursement for our tests; |

|

|

• |

our ability to efficiently bill for and collect revenue resulting from our tests; |

|

|

• |

our anticipated need to raise additional capital to fund our operations, commercialize our products, and expand our operations; |

|

|

• |

our ability to market and sell our tests to physicians and other clinical practitioners; |

|

|

• |

our ability to continue to develop our existing test and develop and commercialize additional novel tests; |

|

|

• |

our dependence on third parties for the manufacture of our products; |

|

|

• |

our ability to meet market demand for our current and planned future tests; |

|

|

• |

our reliance on our sole laboratory facility and the harm that may result if this facility became damaged or inoperable; |

|

|

• |

our ability to compete with our competitors and their competing products; |

|

|

• |

the importance of our executive management team; |

|

|

• |

our ability to retain and recruit key personnel; |

|

|

• |

our dependence on third parties for the supply of our laboratory substances, equipment and other materials; |

|

|

• |

the potential for us to incur substantial costs resulting from product liability lawsuits against us and the potential for these lawsuits to cause us to suspend sales of our products; |

|

|

• |

the possibility that a third party may claim we have infringed or misappropriated our intellectual property rights and that we may incur substantial costs and be required to devote substantial time defending against these claims; |

|

|

• |

the potential consequences of our expanding our operations internationally; |

|

|

• |

our ability to continue to comply with applicable privacy laws and protect confidential information from breaches; |

|

|

• |

how changes in federal health care policy could increase our costs, decrease our revenues and impact sales of and reimbursement for our tests; |

|

|

• |

our ability to continue to comply with federal and local laws concerning our business and operations and the consequences resulting from our failure to comply with such laws; |

|

|

• |

the possibility that we may be required to conduct additional clinical studies or trials for our tests and the consequences resulting from the delay in obtaining necessary regulatory approvals; |

|

|

• |

the harm resulting from the potential loss, suspension, or other restriction on one or more of our licenses, permits, certifications or accreditations, or the imposition of a fine or penalty on us under federal, state, or foreign laws; |

|

|

• |

our ability to maintain and our intellectual property protections; |

|

|

• |

how recent and potential future changes in tax policy could negatively impact our business and financial condition; |

|

|

• |

how recent and potential future changes in healthcare policy could negatively impact our business and financial condition; |

1

|

|

• |

our ability to manage the increased expenses and administrative burdens as a public company. |

Although forward-looking statements in this report reflect the good faith judgment of our management, such statements can only be based on facts and factors currently known by us. Consequently, forward-looking statements are inherently subject to risks and uncertainties and actual results and outcomes may differ materially from the results and outcomes discussed in or anticipated by the forward-looking statements. Factors that could cause or contribute to such differences in results and outcomes include, without limitation, those specifically addressed under the heading “Risk Factors” below, as well as those discussed elsewhere in this report. Readers are urged not to place undue reliance on these forward-looking statements, which speak only as of the date of this report. We file reports with the Securities and Exchange Commission, or the SEC, and our electronic filings with the SEC (including our quarterly reports on Form 10-Q and current reports on Form 8-K, and any amendments to these reports) are available free of charge on the SEC’s website at http://www.sec.gov.

We undertake no obligation to revise or update any forward-looking statements in order to reflect any event or circumstance that may arise after the date of this report, except as required by law. Readers are urged to carefully review and consider the various disclosures made throughout the entirety of this report, which are designed to advise interested parties of the risks and factors that may affect our business, financial condition and results of operations. We qualify all of our forward-looking statements by this special note.

2

Unless specifically noted otherwise, as used throughout this Business section, “we,” “our,” or “us” refers to the business, operations and financial results of DermTech Operations prior to, and the Company and its subsidiaries subsequent to, the completion of the Business Combination as the context requires. “Constellation” refers to the Company prior to the completion of the Business Combination.

Business Overview

We are an emerging growth molecular diagnostic company developing and marketing novel non-invasive genomics tests to aid in the diagnosis and management of various skin conditions, including skin cancer, inflammatory diseases, and aging-related conditions. Our technology provides a highly accurate alternative to surgical biopsy, minimizing patient discomfort, scarring, and risk of infection, while maximizing convenience. Our scalable genomics assays have been designed to work with a proprietary “adhesive patch skin sampling kit” utilizing “Smart StickersTM” that provide a tissue sample for analysis non-invasively.

We are initially commercializing tests that will address unmet needs in the diagnostic pathway of pigmented skin lesions, such as moles or dark colored skin spots. Our current test facilitates the clinical assessment of pigmented skin lesions for melanoma. We have initially marketed this test directly to a concentrated group of dermatology clinicians. The simple application of the Smart Stickers to collect a sample may allow us to eventually market the test to primary care physicians and expand our efforts through telemedicine channels. We process our tests in a high complexity molecular laboratory that is certified under the Clinical Laboratory Improvement Amendments of 1988 (“CLIA”), College of American Pathologists (“CAP”) accredited and New York licensed. We also provide laboratory services to several pharmaceutical companies that access our technology on a contract basis within their clinical trials to better advance new drugs. We have a history of net losses since our inception.

Business Combination, Reverse Split and Domestication

On August 29, 2019, the Company, formerly known as Constellation Alpha Capital Corp., or Constellation, and DermTech Operations, Inc., formerly known as DermTech, Inc., or DermTech Operations, consummated the transactions contemplated by the Agreement and Plan of Merger, dated as of May 29, 2019, by and among the Company, DT Merger Sub, Inc., or Merger Sub, and DermTech Operations. We refer to this agreement, as amended by that certain First Amendment to Agreement and Plan of Merger dated as of August 1, 2019, as the Merger Agreement. Pursuant to the Merger Agreement, Merger Sub merged with and into DermTech Operations, with DermTech Operations surviving as our wholly owned subsidiary. We refer to this transaction as the Business Combination. In connection with and two days prior to the completion of the Business Combination, Constellation re-domiciled out of the British Virgin Islands and continued as a company incorporated in the State of Delaware.

On August 29, 2019, immediately following the completion of the Business Combination, we amended and restated our certificate of incorporation, or the Amended and Restated Certificate of Incorporation, to change the name of the Company to DermTech, Inc. Prior to the completion of the Business Combination, the Company was a shell company. Following the Business Combination, the business of DermTech Operations is the business of the Company.

On August 29, 2019, in connection with and immediately following the completion of the Business Combination, we filed a certificate of amendment, or the Certificate of Amendment, to the Amended and Restated Certificate of Incorporation to effect a one-for-two reverse stock split of our common stock on August 29, 2019, or the Reverse Stock Split. As a result of the Reverse Stock

3

Split, the number of issued and outstanding shares of our common stock immediately prior to the Reverse Stock Split was reduced into a smaller number of shares, such that every two shares of our common stock held by a stockholder immediately prior to the Reverse Stock Split were combined and reclassified into one share of our common stock.

Our Business

We are an emerging growth molecular diagnostic company developing and marketing novel non-invasive genomics tests that seek to transform the practice of dermatology and related fields. Our platform may change the diagnostic paradigm in dermatology from one that is subjective, invasive, less accurate and higher-cost, to one that is objective, non-invasive, more accurate and lower-cost. Our initial focus is skin cancer. We currently offer a test for the enhanced early detection of melanoma and are developing a product for non-melanoma skin cancer. We are also working on a product to assess skin cancer risk or UV damage. Our scalable genomics platform has been designed to work with a proprietary Smart Sticker adhesive patch sample collection kit that provides a skin sample collected easily and non-invasively, in contrast to the existing standard of care of using a scalpel to biopsy suspicious lesions. We also provide our services and technology platform on a contract basis to large pharmaceutical companies who use the technology in their clinical trials to test for the existence of genomic targets of various diseases and to measure the response of new drugs under development. We process our tests in a CLIA certified, CAP accredited and New York licensed commercial laboratory located in La Jolla, California that is licensed by the State of California and all states requiring out-of-state licensure. As described below, our technology platform is easy to use and integrates seamlessly into the current clinical diagnostic pathway by providing (i) simple and rapid tissue collection and shipping via standard express mail, (ii) sample processing via quantitative polymerase chain reaction, or qPCR, or other technologies and (iii) physician reporting within 48 to 72 hours. In addition, physicians can bill for their services using existing Evaluation and Management, or E&M, codes when our tests are ordered. Physicians can continue to bill for certain other procedures using existing Current Procedural Technology, or CPT, codes.

Dermatology is one of the largest medical markets in the United States. The skin cancer segment alone has over 15 million surgical diagnostic procedures performed each year in the United States, with an average annual spend of $8.1 billion from 2007 to 2011, according to the American Academy of Dermatology, or AAD. Current dermatologic diagnosis is primarily based on subjective visual assessments and subsequent surgical diagnostic procedures. This legacy paradigm is prone to error and results in a substantial number of unnecessary and invasive surgical procedures. Our platform provides a non-invasive alternative that minimizes patient discomfort, scarring, and risk of infection. Further, because our testing results utilize genomic analysis, we provide more accurate, objective diagnostic information than the currently prevailing diagnosis procedures. As described below, our first product, the Pigmented Lesion Assay (“PLA™”) has been demonstrated in a study published in JAMA Dermatology to lower the cost to diagnose melanoma while providing a more accurate and less invasive alternative to current methods based on assessing genomic atypia.

4

The general genomic testing market is highly saturated with other genomic diagnostic tests that are primarily marketed to pathology and oncology specialists. We are the first company to offer non-invasive genomic tests to the clinical dermatology market. We believe our technology platform will transform the practice of dermatology and will expand the base of clinicians that can practice high quality precision dermatology (e.g., primary care clinicians). As healthcare delivery diverges to more convenient delivery models, such as pharmacy-based/retail clinics and telemedicine, we believe our platform will facilitate the migration of dermatologic care to these alternative models. We believe our platform may allow for expanded consumer-based sample collection shipped directly to our laboratory, positively impacting the ease of use and convenience of providing dermatologic care.

Our PLA assesses pigmented skin lesions, moles or dark skin spots for melanoma and enhances early detection. Of the approximate 4.0 million surgical biopsies performed each year on pigmented skin lesions, over 90% are negative for melanoma and represent avoidable surgical procedures. The PLA improves the assessment of pigmented lesions by reducing the probability of missing melanoma to less than 1.0% (versus approximately 11-17% with the existing standard of care) and by reducing the number of surgical biopsies required to diagnose melanoma by tenfold (from about 25:1 to about 2.5:1). In addition, the PLA improves the positive predictive value (“PPV”) approximately five-fold (from 3-4% with the current surgical techniques to 18.7% with PLA). In March 2019, Medicare’s MolDX program, administered by Palmetto GBA, or MolDX, which performs technology assessments for genomic tests, issued a favorable draft Local Coverage Determination (“LCD”), or Draft LCD, for our PLA. In October 2019, the AMA provided us with a CPT Proprietary Laboratory Analysis code for our PLA of 0089U, or the PLA Code. Pricing of $760 for the PLA Code was published on December 24, 2019 as part of the CMS Clinical Laboratory Fee Schedule, or CLFS, for 2020, which has been confirmed for 2021. The Medicare final LCD, or Final LCD, first made available on December 26, 2019 expanded the coverage proposal in the Draft LCD from one test per date of service to two tests per date of service, and allows clinicians to order our PLA if they have sufficient skill and experience to decide whether a pigmented lesion should be biopsied or assessed by our PLA. Our PLA became eligible for Medicare reimbursement effective on February 10, 2020. Our local Medicare Administrative Contractor, Noridian Healthcare Solutions, LLC, or Noridian, relies upon MolDX for technology assessments of genomic-based tests and has adopted the Final LCD issued by MolDX. Noridian has issued its own LCD announcing coverage of our PLA. Even though the effective date of Noridian’s LCD is June 7, 2020, Noridian began reimbursing us for our PLA as of February 10, 2020.

The performance of the PLA is supported by numerous investigational studies, which enrolled an aggregate of over 7,000 patients and yielded a total of 21 peer-reviewed publications in top-rated medical dermatology journals. A publication in JAMA Dermatology demonstrated that the PLA significantly lowers the cost to diagnose melanoma while providing a more accurate and less invasive alternative to current methods. The current AAD melanoma guidelines indicate that non-invasive gene expression testing can be used as a part of the initial clinical assessment for pigmented lesions. In January 2021, the National Comprehensive Cancer Network® (“NCCN”) updated their NCCN Clinical Practice Guidelines in Oncology (“NCCN Guidelines®”) for cutaneous melanoma to recommend that the use of pre-diagnostic noninvasive genomic patch testing may be helpful to guide biopsy decisions for cutaneous melanoma. The NCCN’s recommendation indicated that there is uniform consensus that the intervention is appropriate. In addition, an independent panel of melanoma experts has produced consensus recommendations for use of our PLA product. We believe the PLA can be used as an alternative for the majority of these surgical biopsy procedures, which could create a total existing market opportunity for melanoma greater than $3.0 billion per year. We have also received Health Canada clearance for use of our platform and have established a non-exclusive licensing partnership with DermTech Canada. We are working with this partner to secure reimbursement coverage with various Canadian provinces.

We initiated the commercialization of our PLA product in the second quarter of 2016. We currently market these tests directly to dermatologists in the United States with a team of approximately 40 sales representatives throughout the United States and plan to expand our team into more regions throughout the United States during 2021. With our recent Medicare coverage and growth of testing volume and physician users, we believe our test is being reviewed for coverage by key United States commercial payors, including Aetna, Cigna Corporation, Humana, United Healthcare, CareCore National, eviCore healthcare, and others. We believe we will achieve successful coverage outcomes from these efforts over the next 24 to 36 months, although no assurances can be given that any reimbursement coverage approvals will be obtained.

In the second quarter of 2018, we introduced our Nevome product, an adjunctive reflex test for the PLA. The Nevome test was used with histopathology to identify additional risk factors for melanoma and to confirm the diagnosis of melanoma in PLA positive tests, which are subjected to surgical biopsy. The Nevome test analyzed early-stage melanoma driver mutations in the v-Raf murine sarcoma viral oncogene homolog B (“BRAF”), neuroblastoma RAS viral oncogene homolog (“NRAS”) and telomerase reverse transcriptase (“TERT”) genes. The Nevome test utilized the same genomic material collected from the initial adhesive patch sample used for the PLA and did not require additional sampling. We discontinued our Nevome product in November 2020, and we expect it to be replaced with the introduction of our second-generation PLA test, PLAplusTM, that we plan to launch in 2021. The PLAplus improves the sensitivity of the melanoma test to up to 97%. The launch of the PLAplus has been postponed due to supply chain related impacts from COVID-19. The timing of the launch of the PLAplus will depend on when we receive the required inventory required to run PCR tests, which is affected by COVID‑19 pandemic. The PLAplus test will add TERT promoter mutation analyses to the current PLA gene expression test further enhancing the test’s performance, and we will no longer test for BRAF or NRAS genes, which we tested for in our Nevome product.

5

We plan to expand our sales efforts as we obtain reimbursement coverage to provide sales coverage to a majority of over 13,000 healthcare professionals specializing in dermatology in the United States.

We believe the total annual United States market opportunity for our PLA and PLAplus tests exceeds $3.0 billion, and that the select annual worldwide market consisting of Australia, Europe, and Canada exceeds an additional $750 million.

Additional skin cancer product offerings, including for non-melanoma skin cancers (basal cell and squamous cell cancers), are currently under development. In the United States, approximately 12 million surgical biopsies are performed each year to diagnose approximately 5.0 million non-melanoma skin cancers. Many of the initial surgical procedures for these skin cancers are performed on cosmetically sensitive areas of the body, such as the face, neck and chest, creating significant demand for a non-invasive alternative. We believe the total market opportunity for our non-melanoma skin cancer products exceeds $3.0 billion in the United States and $1.0 billion in select world-wide markets.

We are also working on tests to facilitate the assessment of inflammatory skin diseases, such as atopic dermatitis and psoriasis, which will facilitate the appropriate diagnosis and treatment of these inflammatory diseases. The prevalence of atopic dermatitis in the United States is reported to be approximately 12% in children and 7.0% in adults with approximately 6.6 million patients having moderate-to-severe disease. The prevalence of psoriasis in the United States is approximately 2.2% with approximately 1.3 million patients having moderate to severe disease.

We also make our non-invasive molecular skin analysis platform available to pharmaceutical companies to facilitate the development of new targeted therapies in dermatology and cancer, including biologics. These partners use our platform and services to assess treatment response, monitor side effects and identify likely responders to the therapy under development. We have completed and have ongoing research collaborations with large pharmaceutical companies to facilitate their development of new targeted therapeutics in dermatology. We have initiated programs across the spectrum of pharmaceutical development stages from Phase 1 through Phase 3. We believe that some of these collaborations may lead to a complementary or companion diagnostic product for the pharmaceutical partner’s therapeutic candidate, if it reaches the commercial market. We have booked over $2.4 million of orders pursuant to research contracts in 2020, and many of these contracts are multi-year in length.

We offer our genomic tests through our CLIA certified and CAP accredited commercial laboratory located in La Jolla, California, which is licensed by the State of California and all states requiring out-of-state licensure. In the first quarter of 2018, we received our laboratory permit from the New York State Department of Health, the most rigorous licensing process for clinical diagnostic laboratories. We can scale our current facility to approximately 300,000 tests per year, with the ability to scale to over 1,000,000 tests per year with additional facility and capital investments.

Our sample collection technology maximizes collection of relevant tissue with minimal patient discomfort using adhesive patches. We have developed significant intellectual property and know-how around the use of adhesives for non-invasive biopsy and the transportation and handling of this type of sample. We have developed a proprietary process that allows us to extract genomic material from the patches with sufficient quality and quantity to perform gene expression, DNA mutation, transcriptomic analyses and other technologies. We believe our technology can be utilized to assess the microbiome of the skin with superior performance to existing methods that use swabs. The results of these efforts will allow us to introduce our sample collection technology to facilitate the diagnosis of a broad array of dermatologic conditions and other conditions where the skin serves as a surrogate target organ.

6

Enhancing early detection for superior patient care at a lower cost. The PLA is used to assess pigmented lesions that may harbor melanoma at the earliest stages (melanoma in situ or stage 1a), the most difficult lesions to diagnose. In our clinical studies, our PLA test has demonstrated a sensitivity of 91-95% and a specificity of 69-91% in differentiating these early-stage melanomas from non-melanoma using histopathology as the reference standard. This leads to a very high negative predictive value, or NPV, of greater than 99%, which is the probability our PLA test correctly ruled out melanoma. We completed a long-term follow-up study of the PLA that further confirmed the 99% NPV of the PLA by reevaluating and retesting lesions that were PLA negative 12 to 24 months prior to each subject’s enrollment in the study. We also completed a study that demonstrated that the PLA increases the positive predictive value, (“PPV”) for melanoma diagnosis by approximately fivefold, from 3-4% for the current pathway to 18.7% for the PLA. In addition, the PLA has demonstrated an approximate tenfold reduction in unnecessary surgical procedures, relative to the current visual assessment and histopathology standard of care. Such a reduction can result in significant cost savings for the health care system and reduces patient morbidity as compared to other diagnostic approaches. Table 1 below compares our PLA with other techniques and the existing standard of care for assessing early-stage melanoma in pigmented skin lesions.

|

|

|

Our PLA |

|

Visual Assessment & Pathology (Current Standard) |

|

Mechanism |

|

Tumor Biology |

|

Pattern Recognition |

|

Surgical Procedure Required |

|

No |

|

Yes |

|

Platform Technology |

|

Yes |

|

N/A |

|

Multiple Dermatologic Indications |

|

Yes |

|

Yes |

|

Physician Payment |

|

Yes |

|

Yes |

|

Simple Practice Integration |

|

Yes |

|

N/A |

|

Ease of Use |

|

Yes |

|

N/A |

|

Number Needed to Biopsy(1) |

|

2.7 |

|

>25 |

|

Number Needed to Excise(2) |

|

1.6 |

|

5.2 |

|

Better Performance |

|

|

|

|

|

NPV(3) |

|

>99% |

|

>81-89% |

|

PPV(4) |

|

18.7% |

|

4% |

|

Sensitivity(5) |

|

91-95% |

|

65-84% |

|

Cost |

|

$760(6) |

|

$947 |

|

Capital Equipment |

|

No |

|

No |

Table 1. The data summarized above compares our PLA with the existing standard of care for assessing early-stage melanoma in pigmented skin lesions.

Footnotes to Table 1:

|

|

(1) |

Number of surgical biopsies required to diagnose one melanoma. |

|

|

(2) |

Number of wide excision surgical procedures per melanoma diagnosed. |

|

|

(3) |

NPV measures the probability that a negative result is truly negative. |

|

|

(4) |

PPV measures the probability that a positive result is truly positive. |

|

|

(5) |

Sensitivity measures the proportion of actual positives that are correctly identified as such. |

|

|

(6) |

Figure represents a projected United States reimbursed price, though this price has not yet been negotiated with major United States payors. Pricing of $760 for the PLA Code was published on December 24, 2019 as part of the CMS Laboratory Fee Schedule for 2020 and confirmed for 2021. The Medicare Final Coverage Decision was made available on December 26, 2019 and the PLA became eligible for Medicare reimbursement on February 10, 2020. |

Our technology platform has the potential to transform dermatologic practice. We are the first and only company to offer non-invasive genomic testing to clinicians that practice dermatology. Current dermatologic practice is based on subjective visual assessments of cellular change that are prone to inaccuracy and lead to invasive surgical procedures that drive unnecessary costs. Our technology platform seeks to dramatically transform this paradigm by enhancing early detection at the genome level where cancer

7

begins providing non-invasive, objective, and more accurate information, thereby broadening the base of clinicians that can practice dermatology while also improving the performance of specialists.

Superior ease of use. Our non-invasive biopsy sample collection procedure can be performed in less than five minutes. All the necessary items, including adhesive patches, instructions, a marking pen for outlining, and a preaddressed and prepaid return shipping label, are contained in our kit. The collection procedure, when a clinician orders the test, can also be performed at the patient’s home with clinician guidance.

Simple integration into clinical practice. Our tests use an adhesive patch that replaces the scalpel traditionally used in the initial clinical assessment. Unlike other technologies, our platform does not require the installation and maintenance of capital equipment. The nursing support, documentation, specimen processing, and requisition post procedure are substantially similar to current practice. These issues are critical in a busy clinical practice where clinicians see patients every five to seven minutes.

Strong intellectual property protection. We have six issued United States patents, one of which is broadly directed to the use of an adhesive to collect samples containing RNA from the skin for analysis. In addition, we have been awarded patents on unique gene expression profiles and classifiers that differentiate melanoma from non-melanoma, one of which will not expire until 2029, and the other will not expire until 2030. Additional efforts to further expand our patent portfolio are ongoing and a number of provisional and non-provisional patent applications have been filed. We have also developed unique know-how and proprietary processes that allow us to extract sufficient quantities of low-quality genomic material from adhesive patch samples suitable for analysis.

Our Strategy

Our goal is to become the global leader in non-invasive genomics testing for dermatologic conditions. We believe our robust intellectual property portfolio, platform technology, first-to-market advantage, and groundbreaking research will facilitate the achievement of this goal. Specifically, we will focus on the following objectives:

Build a specialized sales force to introduce our products into the dermatology market. We intend to expand our existing direct specialty sales force as additional reimbursement coverage is achieved. Consistent with our current sales strategy, we will continue to recruit experienced sales representatives, primarily those from the dermatology sector who have existing physician relationships. We also plan to leverage this sales force by establishing distribution relationships with laboratory companies that do business with the clinical dermatologist or sell molecular tests.

Secure broad reimbursement coverage for our assays. We have targeted regional and national payors to secure favorable coverage decisions for the reimbursement of our tests. The PLA has completed the necessary analytical validity, clinical validity, and clinical utility studies that payors require molecular tests to undertake. We have also published a United States health economic impact study on the PLA in JAMA Dermatology, which shows that the PLA significantly reduces the relative cost to assess a pigmented lesion. The cost to fully adjudicate a pigmented lesion suspicious for melanoma is $947 in the United States. We believe the PLA could lead to cost savings of greater than $650 million per year in aggregate savings, based on approximately 4.0 million surgical biopsies performed per year to rule out melanoma, and assuming the PLA was to become the standard of care in the United States.

In March 2019, MolDX, which performs technology assessments for genomic tests, issued a favorable Draft LCD for the PLA. In late October 2019, the AMA provided us with the PLA Code. Pricing of $760 for the PLA Code was released on December 24, 2019 as part of the CLFS for 2020. The Final LCD, first made available on December 26, 2019, expanded the coverage proposal in the Draft LCD from one test per date of service to two tests per date of service, and allows clinicians to order our PLA if they have sufficient skill and experience to decide whether a pigmented lesion should be biopsied or assessed by our PLA. Our PLA became eligible for Medicare reimbursement on February 10, 2020. Our local Medicare Administrative Contractor, Noridian, relies upon MolDX for technology assessments of genomic-based tests and has adopted the Final LCD issued by MolDX. Noridian has issued its own LCD announcing coverage of our PLA. Even though the effective date of Noridian’s LCD is June 7, 2020, Noridian began reimbursing us for our PLA as of February 10, 2020.

In addition to our demonstrated clinical validity, clinical utility is the most important attribute of a test for establishing coverage policies with payors because it demonstrates how frequently physicians adhere to the recommendation of the test and the resulting improvement in clinical outcomes. In 2020, we completed and published our largest clinical utility study of the PLA based on real-world commercial usage. This most recent clinical utility study on 3,418 cases corroborates earlier utility studies and demonstrates that clinicians adhere to the recommendation of the PLA more than 98% of the time. Our test significantly reduces surgical procedures and improves the diagnostic pathway for pigmented lesion assessment. Lesions clinically suspicious for melanoma have negative PLA results in over 90% of cases, leading to an approximately 90% reduction in surgical biopsies in our 2020 study. In January of 2021, we published additional registry study data highlighting that PLA use enriches biopsied samples for melanoma almost 5-fold. We believe our body of clinical evidence and utility will lead to securing coverage policies from the major commercial payors over the next 24 to 36 months, although no assurances can be given that any reimbursement coverage approvals will be obtained.

8

We have secured several contracts with major preferred provider networks, including Blue Shield of California, Blue Cross and Blue Shield of Texas, Blue Cross and Blue Shield of Illinois, Carefirst - BCBS of Maryland and Priority Healthcare of Michigan. We have submitted clinical and technology assessment packages to eviCore healthcare, LLC, which provides consultative services for payors. We are in direct discussion with several national commercial payors, including Aetna, Cigna Corporation, UnitedHealthcare, Humana and several independent Blue plans, all of which have the PLA currently under review.

Integrate our products into the standard of care. We conduct rigorous clinical research and basic science research and publish the results of this research in peer-reviewed journals. Overall, our research has yielded 21 publications in top peer-reviewed journals. The PLA’s performance is supported by over ten investigational studies, which enrolled an aggregate of over 7,000 patients. A study published in JAMA Dermatology demonstrated that the PLA significantly lowers the cost to diagnose melanoma while providing a more accurate and less invasive alternative to the current methods. Our research is frequently highlighted at clinical meetings and has several times been accepted for peer-reviewed late-breaking presentations at major medical society meetings.

The AAD melanoma guidelines updated every 5-7 years have indicated that non-invasive gene expression testing can be used as a part of the initial clinical assessment for pigmented lesions. In January 2021, NCCN recommended that there is uniform NCCN consensus to recognize the use of noninvasive genomic patch testing to help guide biopsy decisions for cutaneous melanoma, and it added the intervention to its NCCN Guidelines for cutaneous melanoma. In addition, an independent panel of melanoma experts produced consensus recommendations for use of our PLA product, which were published in 2019.

We have established an extensive board of over a dozen Key Opinion Leaders, or KOLs, in dermatology, including four former presidents of the AAD. These KOLs speak extensively about our technology platform and the PLA at various clinical and research meetings. In addition, these KOLs participate in our clinical studies and publish findings in peer-reviewed journals.

Establish alternate care delivery channels. We plan to expand our efforts in alternate care delivery channels including telemedicine, integrated primary care networks, and on-site and near-site employer health and retail clinics. These channels can help to democratize access to high quality dermatologic care, alleviate certain capacity limitations currently within dermatology and the related long lead times for dermatology specialist appointment availability, and improve the delivery of care to patients with ease of use, improved commute and wait times, and reduced patient fear that can accompany referrals to dermatology specialists.

Establish distribution partnerships for primary care. A substantial portion of dermatology is practiced in primary care. Based on the adoption progress we make within dermatology and integrated primary care networks, we plan to eventually access the primary care market more broadly by potentially establishing distribution relationships with companies that focus on this physician call point. An ideal partner would have several hundred sales professionals in the aggregate who access the primary care market, and ideally have experience selling genomic diagnostic products. Alternatively, we may plan to hire sales representatives to make direct calls to primary care offices.

Expand our product offerings. We have developed a platform that provides genomic analysis of the skin using a non-invasive adhesive patch platform as the sample collection method. This platform can be used to develop multiple products based on the same sample collection method, and it only requires different genomic markers to be assayed in our CLIA-certified laboratory. We are currently working to complete development of additional products, which will assess non-pigmented lesions for basal cell and squamous cell cancers. In addition, we are working to develop tests for inflammatory diseases of the skin.

Expand our marketing of research services to pharmaceutical companies. Our platform is used by several large pharmaceutical companies to facilitate their development of new targeted therapeutics in dermatology. Our PLA product helps identify biomarker treatment responses, track side effects, and identify patients that respond to the therapy. We plan to hire additional business development professionals to sell these services to the pharmaceutical industry. These efforts will include the participation in additional industry conferences and the presentation of our platform and data at additional medical conferences. Additionally, our collaborations with pharmaceutical partners may result in the introduction of complementary or companion diagnostic products for the partners’ therapeutic candidates that reach the commercial market.

Explore reference testing for large integrated dermatology networks and dermatopathology laboratories. Large dermatology practices with multiple clinics and generally more than 50 clinical professionals often have integrated dermatopathology and laboratory testing services for their clinics. For these situations and depending on federal and state regulations, we may plan to explore implementation of reference contracts, whereby the integrated laboratory will accession the PLA samples and bill for these samples, while paying us a contracted price. We estimate that 10-20% of our dermatology market opportunity may be accessed through this model.

9

Market Opportunity – Skin Cancer

Melanoma is currently one of the fastest growing cancers and the subject of significant attention in the medical community. The incidence of melanoma has doubled since 1973. While there has been a 20% decline in cancer deaths overall since 1991, melanoma is one of three cancers facing increasing death rates. According to a study from the Mayo Clinic, the incidence of melanoma increased eightfold among women under 40 and fourfold among men under 40 from 1970 to 2009.

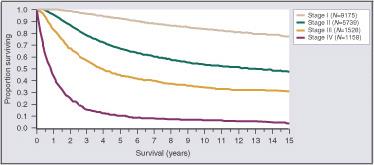

Melanoma is one of the deadliest forms of skin cancer. On average, melanoma causes more than one death every hour of every day of the year in the United States. The Skin Cancer Foundation projects that more than 7,000 people will die from melanoma in 2021. If diagnosed and removed early in its evolution, when confined to the outermost skin layer and deemed to be “in situ” (Stage 0), patients are expected to have a survival rate of almost 100%. Invasive melanomas that are thin and extend into the uppermost regions of the second skin layer (Stage 1) still have cure rates greater than 90%. However, once the cancer advances into the deeper layers of skin, the risk of it spreading to other parts of the body, or metastasis, and death increases. The table below depicts the survival rate of melanoma based on the stage of the cancer at initial diagnosis.

From Balch CM, Buzaid AC, Soong S-j et al: Final Version of the American Joint Committee on Cancer Staging Sysem for Cutaneous Melanoma. Journal of Clinical Oncology, August 2001.

An estimated 207,390 cases of melanoma will be diagnosed in the U.S. in 2021. Of those, it is estimated that 106,110 cases will be in situ (noninvasive), confined to the epidermis (the top layer of skin), and 101,280 cases will be invasive, penetrating the epidermis into the skin’s second layer (the dermis). On average, 25 surgical biopsies are performed per early-stage melanoma diagnosed, creating a total market opportunity of approximately 4.0 million surgical procedures per year. Outside the United States, the incidence of melanoma is highest in Western Europe, Australia, and Canada. We estimate that these select worldwide markets perform over 1.5 million surgical biopsies annually to diagnose approximately 75,000 melanomas, creating additional market opportunity that we believe exceeds $750 million per annum.

Over 5.4 million non-melanoma skin cancers (basal cell and squamous cell carcinomas) are diagnosed in the United States annually. The number of surgical biopsies needed to diagnose one non-melanoma skin cancer is approximately 2.5-3.0 among dermatologists and can be considerably higher when diagnosed by other clinicians such as nurse practitioners and primary care physicians. While these cancers are not as deadly as melanoma, they commonly occur on the face, head, neck, and other cosmetically sensitive areas, creating an important unmet medical need for a non-invasive alternative, and a potential market opportunity of approximately $3.0 billion in the United States per annum based on the approximately 10-12 million surgical biopsies performed to diagnosis of basal and squamous cell skin cancers.

Limitations of Current Melanoma Diagnostic Pathway

The estimated prevalence of pigmented lesions (moles) ranges from 2% to 8% in fair-skinned persons.

Pigmented lesions may be classified as clinically atypical by meeting one or more of the American Cancer Society’s ABCDE criteria, which includes Asymmetric, irregular Border, variegated or dark Color, Diameter greater than 6 mm, or Evolving mole. Atypical pigmented lesions are at risk for harboring melanoma. A meta-analysis of case-control studies found that the relative risk of melanoma is 1.45 in patients with one atypical mole vs. those with none, and this risk increases to 6.36 in those patients with five atypical moles. Management of atypical pigmented lesions involves ruling out melanoma via a visual assessment followed by surgical biopsy and histopathology. Ideally, when melanomas are identified, they are found at the earliest stages (melanoma in situ or stage 1a) when a high cure rate is possible by wide excision. Since a biopsy only partially removes a lesion for histopathologic analysis, early-stage melanomas diagnosed histopathologically from biopsy material are treated with follow-up wide excision procedures (generally with 0.5-1.0 cm margins).

10

While the purpose of the visual assessment or surgical biopsy is to rule out melanoma, the poor performance metrics of this diagnostic pathway leads to a low NPV for early-stage disease (Table 2 below). This is related to the low specificity of the visual assessment (3-10%), which results in a high number of biopsies on benign atypical nevi. During histopathologic assessment, a small number of melanomas must be identified from this large pool of biopsied atypical nevi. However, there is significant overlap in the histopathologic diagnostic criteria between atypical nevi and early-stage melanoma, invariably leading to false negative diagnoses and a relatively low sensitivity (65-84%). Elmore et al. BMJ (2017) 357:j2183, concluded that the diagnosis of early stage melanoma was not accurate after finding that 35% of slide interpretations for melanoma in situ or stage 1a melanomas by 187 pathologists received a false negative diagnosis as benign. With the prevalence of early-stage melanoma in biopsied lesions at approximately 5%, the negative predictive value ranges from 75-89%.

Welch and colleagues’ most recent N Engl J Med article (2021, 384:72-79) points out that melanoma diagnoses have increased more than 6-fold over the last 40 years. The authors attribute this increase to more frequent enhanced screening, lower pathological thresholds to label the morphologic changes as cancer, and importantly heightened clinical awareness to biopsy pigmented lesions. However, the article fails to address the main limitations of the current care standard for evaluating pigmented lesions relies primarily on visual atypia to guide biopsy decisions. About 4 million pigmented lesions are biopsied in the US alone to diagnose fewer than 200,000 cutaneous melanomas (about 25 biopsies to detect 1 melanoma based on Anderson et al. JAMA Dermatol. (2018) 154(5):569-573. Using non-invasive assessment of genomic atypia offered by the PLA rather than visual atypia alone to guide pigmented lesion biopsy decisions reduces avoidable biopsies while missing fewer melanomas. Precision genomics is currently used in other areas of oncology and has changed the paradigm of treatment. Integrating PLA use and precision genomics to enhance early detection non-invasively into standard practice rather than performing fewer skin examinations appears to be a superior solution to the conundrum highlighted by Welch and colleagues.

According to several published papers, the real NPV of the visual assessment or surgical biopsy pathway is likely 80% to 85%. In a study by Malvehy et al., BJD (2014) 171:1099, 206 in situ and stage 1a (thickness less than 0.75 mm) melanomas were diagnosed with a sensitivity of 81% and a specificity of 10%. The prevalence of early melanoma in the study was about 10%, yielding an NPV of 83%. In addition, the current pathway using visual atypia to guide biopsy decisions suffers from a low PPV of approximately 4% for melanoma diagnosis. The addition of the PLA to the visual assessment by clinicians increased the PPV for a melanoma diagnosis by approximately five-fold to 18.7%.

|

|

|

Current Pathway |

|

|

PLA |

|

||

|

Test Purpose |

|

Rule-out melanoma |

|

|

Rule-out melanoma |

|

||

|

Type |

|

Surgical biopsy/ histopathology |

|

|

Non-invasive gene expression |

|

||

|

NPV |

|

83% |

|

|

99% |

|

||

|

Probability of Missed Mel |

|

17% |

|

|

1% |

|

||

|

Probability of Mel Diagnosis |

|

4% |

|

|

18.7% |

|

||

|

Number Needed to Biopsy |

|

25 |

|

|

2.7 |

|

||

|

Number Needed to Excise |

|

5.2 |

|

|

1.6 |

|

||

|

Cost per Lesion Tested |

|

$ |

947 |

|

|

$ |

760 |

|

Table 2. Data summarized above compares the key performance metrics of the PLA versus the current pathway (visual assessment and surgical biopsy/histopathology) for managing pigmented skin lesions.

This low NPV for the current pathway is accompanied by a high number of unnecessary surgical procedures, again driven by the poor specificity of the visual assessment. The number of surgical biopsies needed to identify one melanoma averages 25 and ranges from eight to greater than 30 depending on the clinical setting. Further, the histopathologic review of biopsied lesions is extremely limited with 2% or less of the lesion sectioned and evaluated, leaving doubt as to what may be occurring in the rest of the lesion. Consequently, lesions that have cellular atypia and positive margins are often clinically managed conservatively and subjected to full excisions with margins. However, only 0.2% to less than 1.0% of lesions with atypia and positive margins that undergo excision are diagnostically upgraded, most commonly to a higher level of atypia and rarely to melanoma in situ, and such excisions can be considered unnecessary. Approximately 5.2 excisions with margins are performed per melanoma identified, emphasizing how the current pathway of surgical biopsy and limited histopathology assessment leads to more complex and invasive excisions.

11

The PLA

The PLA is a gene expression test that enhances early detection of genomic atypia and helps rule out melanoma and the need for a surgical biopsy of atypical pigmented lesions. The performance of the PLA is supported by over ten investigational studies, which enrolled over 7,000 patients and yielded 21 peer-reviewed publications in top rated medical dermatology journals. Key studies and manuscripts are summarized in Table 3 below. The PLA is based on a new platform technology for non-invasive genomic testing of the skin, which allows the molecular analysis of samples collected from adhesive patches. In contrast to the current pathway, the PLA has a very high NPV (greater than 99%) and high sensitivity (91-95%), ensuring a very low probability of missing melanoma. The PLA’s high specificity (69-91%) effectively reduces the number of false positive samples undergoing histopathologic review. This improves the overall sensitivity of the pathway and greatly increases the NPV.

The PLA’s NPV is supported by a 12-month follow-up study of 734 patients, which demonstrated that no melanomas were missed in the 12-month period following initial testing. In the third quarter of 2019 we initiated the TRUST study, which further examined long-term follow up of lesions previously tested negative by the PLA, and incorporated repeat testing of the previously tested lesion. This study more definitively confirmed the high NPV of the PLA test in a real-world setting, and we announced those topline results in December 2020. Of the lesions evaluated by means of repeat testing with the PLA (n=302), none were found to have clinically obvious melanoma upon the subject’s return to the clinic, confirming the results of the initial chart review. Eighty-nine percent of these lesions were negative on repeat testing with the PLA and 11.2% were positive. Positive lesions were biopsied and subjected to a single read histopathologic review. One percent of lesions (n=3) that tested positive on repeat testing were diagnosed as Stage 0, in situ. Photographic review of the three Stage 0 cases identified changes in clinical appearance since the initial test. The pathology reports from the remaining biopsied lesions indicated a variety of non-melanoma diagnoses, including compound nevi with mild to moderate atypia. Given the early stage (in situ) of the melanomas detected on repeat testing, and length of time from the initial test (an average of 15 months), it is difficult to determine whether these melanomas evolved after the initial test or were present at the time of the initial test. In any case, the finding of three melanomas in a cohort of 302 lesions subjected to repeat testing further confirms an NPV of the PLA of at least 99.0% and is consistent with the results from the full long-term follow‑up cohort. These results exemplify how PLA repeat testing of lesions that may have evolved over time after the initial negative PLA test have potential to identify early-stage melanoma and benefit patients. TRUST study findings corroborating the PLA’s high NPV were complemented by most recent registry data on the PLA’s high PPV (Brouha et al., SKIN, January 2021, 5(1):13-18). This data show that 316 lesions clinically suspicious for melanoma that were biopsied based on guidance offered by genomic atypia (positive PLA test results rather than visual atypia alone) were enriched approximately five-fold for histopathologic features of melanoma.

In addition, the non-invasive sampling leads to a dramatic reduction in surgical biopsies and subsequent excisions. Consequently, our studies have shown that the number of surgical biopsies needed to find one melanoma using the PLA is markedly reduced by almost tenfold to approximately 2.7 and the number of excisions needed is reduced to 1.6. Our studies have shown that the PLA can reduce unnecessary surgical biopsies of lesions clinically suspicious for melanoma by 90%, which is consistent with a 2017 review of 18,715 biopsied pigmented lesions that found that approximately 90% of surgical biopsies to rule out melanoma are performed on pigmented lesions that are not melanoma. Non-invasive gene expression testing has been added to the most recent AAD melanoma guidelines as part of the initial clinical assessment for clinically concerning lesions and recommended by the NCCN Guidelines as of January 2021. In addition, an independent expert committee has developed and published consensus use criteria for the PLA.

In the second quarter of 2021, we plan to make our second-generation PLA test, PLAplus, commercially available. The commercial launch of the PLAplus has been postponed due to supply chain related impacts from COVID-19. The timing of the commercial launch of the PLAplus will depend on when we receive the required inventory required to run PCR tests, which is affected by the COVID‑19 pandemic. This second-generation test will add a TERT promoter mutation analysis to the current PLA gene expression test. TERT promoter mutations are associated with early-stage melanoma and our validation testing against driver mutations showed in two publications that it can increase the sensitivity of the PLA to 97% with only a minor impact on specificity. Several other independent academic investigators have also shown that TERT promoter mutations have a high sensitivity and specificity for melanoma detection. With the upcoming addition of TERT to the PLA test (PLAplus) we discontinued our Nevome product in November 2020, which was a reflex confirmatory test offered for PLA positive tests.

12

|

Study |

|

Status |

|

Size (n) |

|

Publication |

|

Analytical Validation |

|

Complete |

|

125 |

|

Yao Z et al. Analytical characteristics of a noninvasive gene expression assay for pigmented skin lesions. Assay Drug Dev Technol. 2016;14(6):355-363. |

|

Clinical Validation-Pathology |

|

Complete |

|

555 |

|

Gerami P et al. Development and validation of a noninvasive 2-gene molecular assay for cutaneous melanoma. J Am Acad Dermatol. 2017;76(1):114-120.e2. |

|

Clinical Validation-Driver Mutations |

|

Complete |

|

626 |

|

Ferris L et al. Noninvasive analysis of high-risk driver mutations and gene expression profiles in primary cutaneous melanoma. J Invest Dermatol. 2019; 139(5):1127-1134. |

|

Clinical Utility |

|

Complete |

|

45 Derms |

|

Ferris L et al. Utility of a noninvasive 2-gene molecular assay for cutaneous melanoma and effect on the decision to biopsy. JAMA Dermatol. 2017;153(7):675-680. |

|

Real-World Clinical Utility |

|

Complete |

|

381 |

|

Ferris L et al. Real-world performance and utility of a noninvasive gene expression assay to evaluate melanoma risk in pigmented lesions. Melanoma Res. 2018; 28(5):478-482. |

|

1-Year Follow Up |

|

Complete |

|

734 |

|

Ferris L et al. Impact on clinical practice of a non-invasive gene expression melanoma rule-out test: 12-month follow-up of negative test results and utility data from a large US registry study. Dermatology Online Journal. 2019; 25(5). |

|

Real-World Utility Registry |

|

Complete |

|

1575 |

|

Ferris L et al. Impact on clinical practice of a non-invasive gene expression melanoma rule-out test: 12-month follow-up of negative test results and utility data from a large US registry study. Dermatology Online Journal. 2019; 25(5). |

|

Real-World Utility Registry |

|

Complete |

|

3418 |

|

Brouha B et al. Real-world utility of a non-invasive gene expression test to rule out primary cutaneous melanoma: a large US registry study. J Drugs Dermatol. 2020; 19(3).

Brouha B et al. Genomic atypia to enrich melanoma positivity in biopsied lesions: gene expression and pathology findings from a large U.S. registry study. SKIN 2021; 5(1):13-18. |

|

Adhesive Patch Validation |

|

Complete |

|

N/A |

|

Yao Z et al. An adhesive patch-based skin biopsy device for molecular diagnostics and skin microbiome studies. J Drugs Dermatol. 2017; 16(10):611-618. |

|

Association With Severe Atypia |

|

Complete |

|

103 |

|

Jackson S et al. Risk Stratification of Severely Dysplastic Nevi by Non-Invasively Obtained Gene Expression and Mutation Analyses. SKIN. 2020 March; 4(2). |

|

Recommendations for PLA Use |

|

Complete |

|

N/A |

|

Berman B et al. Appropriate use criteria for the integration of diagnostic and prognostic gene expression profile assays into the management of cutaneous malignant melanoma: an expert panel consensus-based modified Delphi process assessment. SKIN The Journal of Cutaneous Medicine. 2019; 3(5):291-306.

National Comprehensive Cancer Network (NCCN) Clinical Practice Guidelines in Oncology. Cutaneous Melanoma. Version 1.2021 at ME-11

Swetter SM et al. Melanoma: Clinical features and diagnosis. UpToDate. Waltham, MA. September 11 2020 |

|

Health Economics |

|

Complete |

|

319 |

|

Hornberger J, Siegel D. Clinical and economic implications of a noninvasive molecular pathology assay for early detection of melanoma. JAMA Dermatol. 2018;154(9):1-8. |

|

Genome Screen |

|

Complete |

|

202 |

|

Wachsman W et al., Noninvasive genomic detection of melanoma. British Journal of Dermatology. 2011; 164:797-806. |

Table 3. Summarizes key clinical studies and publications supporting the PLA.

13

Our Nevome test was an adjunctive reflex test for the PLA. It was used with histopathology to identify additional risk factors for melanoma and confirm the diagnosis. Approximately 13% of our PLA tests are positive. Lesions that test positively for the PLA are subjected to surgical biopsy and histopathologic review. Due to significant challenges in diagnosing early-stage melanoma by histopathology, additional information can be required to confirm the presence of melanoma and/or identify lesions with significant risk for melanoma that require wide excision. The Nevome test analyzed early-stage melanoma driver mutations in the BRAF, NRAS, and TERT genes, providing additional information and risk factors in the lesion being assessed. The Nevome test utilized the genomic material collected from the initial adhesive patch sample used for the PLA. In November 2020, we discontinued our Nevome test, which will be replaced with our PLAplus test in 2021.

Adhesive Skin Sample Collection Kit

We are the inventor and owner of the intellectual property for the Adhesive Skin Sample Collection Kit (pictured below). We have contracted with a Food and Drug Administration, or FDA, registered supplier to produce our kit under applicable quality systems requirements, and we control the exclusive distribution rights for the kit. Our kit’s adhesive patch allows for the collection of skin samples with minimal patient discomfort. A single kit contains all of the necessary components to complete the sample collection for our analysis, including the adhesive patches, instructions for use, a marking pen for lesion outlining, and a pre-addressed and prepaid return shipping pack. The unique properties of the adhesive maximize the collection of informative cellular material for our PLA. The entire procedure for the kit’s sample collection takes less than five minutes.

Telemedicine Option for the PLA

Telehealth is the provision of health-related services and information via electronic information and telecommunication technologies. Telemedicine is sometimes used interchangeably with telehealth, but some organizations define telemedicine in a more limited sense to describe remote clinical services, such as diagnosis and monitoring. Telemedicine enables patient and clinician interaction when rural settings, lack of transport, a lack of mobility, decreased funding, a lack of staff or other limitations such as social distancing guidelines related to the COVID-19 pandemic restrict or make difficult in-person access to healthcare.

Early detection of melanoma, the most deadly and aggressive form of skin cancer, is critical for best patient outcomes. DermTech’s PLA is the first non-invasive genomic diagnostic test for ruling out melanoma that, in addition to in-office sample collection, allows clinicians to supervise the patient’s sample collection via telemedicine. For patients who cannot easily have an in-office visit, this telemedicine solution enables dermatologists to maintain vigilance with their patients in detecting melanoma at the earliest stages.

Using our telemedicine option, a clinician can choose to assess the patient’s skin and suspicious lesion(s) via a teledermatology appointment and, if indicated, submit a patient-specific order to DermTech for the DermTech PLA. If requested by the clinician, the DermTech PLA Adhesive Skin Collection Kit will then be shipped directly to the patient with support from DermTech customer service. During a follow-up teledermatology appointment, a clinician will instruct and supervise the patient to collect their sample with the easy-to-use DermTech PLA adhesive patch. The patient will then return the collected sample(s) back to DermTech via the pre-labeled shipping envelope for analysis. Test results will be available to the ordering clinician within a few days.

In May 2020, SKIN, the official journal of the National Society for Cutaneous Medicine, published proof-of-concept data demonstrating that patients are able to reliably perform remote self-sampling of concerning moles using the PLA under physician supervision via telemedicine, enabling actionable molecular testing for accurate melanoma detection. As part of the Institutional Review Board (“IRB”) approved pilot study, 258 eligible melanoma survivors were contacted, and of the 211 who expressed interest in the PLA,

14

there were seven cases of self-identified concerning lesions, which were confirmed by a clinician to be suspicious of melanoma. These patients then conducted sample collections using DermTech’s non-invasive adhesive skin collection kit at home under the supervision of a clinician via telemedicine. Results from the study showed that skin samples collected by patients enabled successful PLA testing to objectively rule out melanoma in all (100%) of the cases evaluated. These findings are in line with sample collection results by licensed providers.

A clinician can assess the patient’s skin and suspicious lesion(s) via teledermatology where permitted by state law. Some state laws impose various restrictions on the practice of telemedicine and reimbursement may not be available under coverage and reimbursement policies governing telemedicine visits issued by third party payors.

Clinical Research Products

Research on the genomic basis of diseases has increased significantly over the last decade. Genomic analysis can facilitate drug development by identifying drug targets and stratifying patients into groups that will maximize drug response. Genomic analysis is part of the effort to personalize medical therapy to patients’ individual needs. Consequently, tools to facilitate this type of research are in high demand.

We offer a suite of products to facilitate clinical research using our technology platform. We have developed a proprietary process that allows us to extract genomic material from the adhesive patch with sufficient quality and quantity to perform gene expression, DNA mutation analysis, DNA methylation, and transcriptomic analyses. In addition, our platform can be utilized to assess the microbiome of the skin with superior performance to existing methods that use swabs. We have developed gene expression assays for the Th1, Th2, IFN-gamma, and Th17 inflammatory pathways. We market these assays to pharmaceutical companies developing drug products in dermatology. In addition, we develop custom gene assays to support development for these pharmaceutical partners. We have completed and have ongoing research collaborations with large pharmaceutical companies to facilitate their development of new targeted therapeutics in dermatology. Our technology platform has been deployed in Phase 1 through Phase 3 clinical programs. These efforts may also lead to the introduction of complementary and companion diagnostic products.

Leveraging Our Platform for Other Indications

We believe our adhesive patch genomic platform is applicable to numerous other indications in dermatology. While we are focused initially on skin cancer products, we believe there are significant business development opportunities in other areas. We have undertaken a number of pilot development activities in inflammatory diseases, and skin aging. This effort will also focus on potential licensing and partnering opportunities for the development of complementary and companion diagnostics for the pharmaceutical partners’ drug product candidates, should they reach the commercial market. In addition, because the processing of samples is the same regardless of the disease indication, our development activities will leverage our existing laboratory operations.

UV Damage DNA Risk Assessment Product (Luminate)

We are developing a UV Damage DNA risk assessment product. This product will assess DNA mutations associated with UV damage and non-melanoma skin cancer risk. Depending on the UV damage level of each individual, there are various treatment options to reduce the current level of DNA damage in their skin and the associated risk of future skin cancer including chemical peels, photodynamic therapy, laser therapy, topical pharmaceuticals, dietary supplements, and increased sunscreen use.

Based upon our market research, there are approximately 84 million Americans between the ages of 30 and 50, of which approximately 70% are concerned with UV damage. Of this population concerned with UV damage, approximately 30% have household incomes of at least $100,000 that would be most likely to consider using this product. We believe this age-group has significant aging anxiety due to the high prevalence of extrinsic signs of aging and are increasingly using anti-aging products to look younger. This UV Damage DNA mutation assessment product will allow individuals to proactively make data driven, fact-based decisions about their skin health.

Non-Melanoma Skin Cancer Diagnostic Products

To complement our melanoma rule-out product PLA, we are also utilizing our platform technology to develop products to rule out non-melanoma skin cancer including squamous cell and basal cell carcinoma. We identified differentially expressed genes that allow the identification of these cancers, and we are currently conducting analytical and clinical validation studies. Nearly 4.5 million basal and squamous cell carcinoma skin cancers are diagnosed each year making skin cancer the most common of all types of cancer. The majority of these cancers occur in cosmetically sensitive areas such as the head, neck and face. The number of skin cancer cases is increasing due to better skin cancer detection, people living longer, and increased sun exposure.

15

More than 80% of skin cancers are basal cell carcinomas. These cancers usually develop in sun-exposed areas, especially the head and neck, and tend to grow slowly. It is very rare for a basal cell cancer to spread to other parts of the body. If left untreated, basal cell cancers can grow into nearby areas and invade other tissues beneath the skin. If not removed completely, basal cell carcinoma can recur in the same place on the skin. People who have had basal cell skin cancers are also more likely to develop basal cell skin cancers in other places.

About 10% of skin cancers are squamous cell carcinomas. These cancers also commonly appear on sun-exposed areas of the body such as the face, ears, neck, lips, and backs of the hands. These cancers can also develop in scars or chronic skin sores elsewhere. Squamous cell cancers are more likely to grow into deeper layers of skin and spread to other parts of the body than basal cell cancers, although this is still uncommon.

Cutaneous T Cell Lymphoma

We are currently developing a Cutaneous T-cell lymphoma (“CTCL”) rule out test. CTCL is a rare type of skin cancer in which T-cells become immunologically active and attack the skin. CTCL results in rash-like skin redness, slightly raised or scaly round patches on the skin, and, sometimes, skin tumors. These features can resemble much more common inflammatory skin conditions.

Several types of cutaneous T-cell lymphoma exist including mycosis fungoides and Sezary syndrome. Mycosis fungoides is the most common form of CTCL while Sezary syndrome is less common but causes skin redness across larger areas of the body. The definitive diagnosis of CTCL is often challenging because of its nonspecific clinical and pathologic features, which requires integration of clinical, histopathologic, immunophenotyping, and molecular data by the treating physician.

Inflammatory Indications

Atopic dermatitis and psoriasis are chronic inflammatory skin diseases that affect millions of people and are characterized by both local and systemic inflammation. We have investigated gene expression profiles in the skin of atopic dermatitis and psoriasis. Responses to biologic therapy used in moderate to severe forms of these diseases can be variable and may wane over time. For example, only 30-40% of patients have a robust response to either anti-TNF alpha drugs used in psoriasis or the anti-IL-13 drugs used in atopic dermatitis. The low response rate of these drugs creates an unmet need for drug companion and complementary diagnostic products that identify responders to a specific therapy and that monitor responses over time.