Table of Contents

As filed with the Securities and Exchange Commission on October 6, 2016

Registration No. 333-206017

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

POST–EFFECTIVE AMENDMENT NO. 2

TO

FORM S-11

FOR REGISTRATION UNDER

THE SECURITIES ACT OF 1933

OF SECURITIES OF CERTAIN REAL ESTATE COMPANIES

CNL HEALTHCARE PROPERTIES II, INC.

(Exact name of registrant as specified in its governing instruments)

CNL Center at City Commons

450 South Orange Avenue

Orlando, Florida 32801

Telephone: (407) 650-1000

(Address, including zip code, and telephone number, including area code, of the registrant’s principal executive offices)

Stephen H. Mauldin

Chief Executive Officer and President

CNL Healthcare Properties II, Inc.

CNL Center at City Commons

450 South Orange Avenue

Orlando, Florida 32801

Telephone: (407) 650-1000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Robert H. Bergdolt, Esq.

Christopher R. Stambaugh, Esq.

DLA Piper LLP (US)

4141 Parklake Avenue, Suite 300

Raleigh, North Carolina 27612-2350

Telephone: (919) 786-2000

Approximate date of commencement of proposed sale to public: As soon as practicable after the registration statement becomes effective.

If any of the securities being registered in this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box. ☒

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. ☐

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one)

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☐ (Do not check if a smaller reporting company) | Smaller reporting company | ☒ | |||

Explanatory Note

This Post-Effective Amendment No. 2 consists of the following:

| 1. | The Registrant’s final prospectus dated March 2, 2016. |

| 2. | Supplement no. 1 dated October 6, 2016 and Supplement no. 2 dated October 6, 2016 to the Registrant’s prospectus dated March 2, 2016, included herewith, which will be delivered as unattached documents along with the prospectus. |

| 3. | Part II, included herewith. |

| 4. | Signature, included herewith. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

Prospectus

CNL HEALTHCARE PROPERTIES II, INC.

|

Maximum Offering -- Up to $2,000,000,000 in shares of |

Minimum Offering $2,000,000 in shares of | |

| Class A, Class T or Class I Common Stock |

Class A, Class T or Class I Common Stock |

CNL Healthcare Properties II, Inc. is a newly formed Maryland corporation organized to acquire and manage a diversified portfolio of real estate properties, focusing primarily on the seniors housing, medical office building, acute care and post-acute care facility sectors, including stabilized, value add and development properties, as well as other income-producing real estate and real estate-related securities and loans. We also may invest in and originate mortgage, bridge or mezzanine loans or invest in entities that make investments in real estate. We are externally managed by CHP II Advisors, LLC, or our “advisor.” We intend to qualify and elect to be taxed as a real estate investment trust, or REIT, for federal income tax purposes beginning with our taxable year ending December 31, 2016, or our first year of material operations.

We are offering up to $1,750,000,000 of shares of our common stock on a “best efforts” basis, referred to herein as the “primary offering,” which means that CNL Securities Corp., or the “dealer manager,” will use its best efforts but is not required to sell any specific amount of shares. We are offering, in any combination, three classes of our common stock in our primary offering: Class A shares, Class T shares and Class I shares. We are also offering, in any combination, up to $250,000,000 of Class A, Class T and Class I shares to be issued pursuant to our distribution reinvestment plan. There are differing selling fees and commissions for each class. We will also pay annual distribution and stockholder servicing fees, subject to certain limits, on the Class T and Class I shares sold in the primary offering. We reserve the right to reallocate shares of common stock between our distribution reinvestment plan and our primary offering. This is a continuous offering that will end no later than two years from the date of this prospectus, unless extended in accordance with applicable securities laws. Subject to certain exceptions, you must initially invest at least $5,000 in shares of our common stock. Until we sell $2,000,000 in shares of common stock, your subscription funds will be held in escrow. If we do not sell $2,000,000 in shares of common stock, this offering will terminate and your funds will be returned promptly to you.

We are an “emerging growth company” under the federal securities laws and will be subject to reduced public company reporting requirements.

Investing in shares of our common stock involves a high degree of risk. You should purchase shares only if you can afford a complete loss of your investment. See “Risk Factors” beginning on page 26. Significant risks relating to your investment in shares of our common stock include, among others:

| • | We have no prior operating history and may not be able to achieve our investment objectives. If we are unable to raise substantial funds, we will be limited in the number and type of investments we may make. |

| • | There is no public trading market for our shares and we have no obligation to apply for listing on any securities market. You should consider our shares to be a long-term investment and be prepared to hold them for an indefinite period of time. There are also restrictions on the transferability of shares of our common stock. See “Description of Capital Stock—Restriction on Ownership of Shares of Capital Stock.” |

| • | This is a “blind pool” offering; other than as described herein or in a supplement to this prospectus, neither we nor our advisor has acquired or contracted to acquire any real property, debt or other investments. You will not have the opportunity to evaluate our future investments prior to purchasing shares of our common stock. |

| • | We may have difficulty funding our distributions with funds provided by cash flows from operating activities; therefore, until we generate sufficient operating cash flow, it is likely we will fund distributions to our stockholders with cash flows from financing activities, which may include borrowings and net proceeds from shares sold in this offering, cash resulting from a waiver or deferral of fees or expense reimbursements otherwise payable to our advisor or its affiliates, cash resulting from our advisor or its affiliates paying certain of our expenses, and proceeds from the sales of assets or from our cash balances (which may constitute a return of capital). The use of these sources to pay distributions could adversely impact the value of your shares. |

| • | Other real estate investment programs sponsored by the sponsor of this offering or its affiliates may have investment strategies that are similar to ours. Our advisor and our executive officers will face conflicts of interest relating to the purchase and management of our investments, and such conflicts may not be resolved in our favor. Our advisor will also face conflicts of interest as a result of their compensation arrangements with us, which could result in actions that are not in your best interests. |

Neither the Securities and Exchange Commission nor any state securities regulator has approved or disapproved of these securities or determined if this prospectus is truthful or complete. In addition, the Attorney General of the State of New York has not passed on or endorsed the merits of this offering. Any representation to the contrary is unlawful. The use of forecasts in this offering is prohibited. Any representation to the contrary and any predictions, written or oral, as to the amount or certainty of any present or future cash benefit or tax consequence which may flow from an investment in our common stock is not permitted.

|

|

||||||||||||||||

|

|

||||||||||||||||

| Maximum Aggregate Price to Public |

Maximum Selling Commissions |

Maximum Dealer Manager Fees |

Proceeds to Us Before Expenses (1) |

|||||||||||||

| Maximum Offering |

$ | 1,750,000,000 | $ | 37,625,000 (2) | $ | 45,718,750 (2) | $ | 1,666,656,250 | ||||||||

| Class A Shares, Per Share |

$ | 11.08 | $ | 0.78 | $ | 0.30 | $ | 10.00 | ||||||||

| Class T Shares, Per Share (3) |

$ | 10.50 | $ | 0.21 | $ | 0.29 | $ | 10.00 | ||||||||

| Class I Shares, Per Share (3) |

$ | 10.00 | $ | — | — | $ | 10.00 | |||||||||

| Minimum Offering |

$ | 2,000,000 | $ | 43,000 (2) | $ | 52,250 (2) | $ | 1,904,750 | ||||||||

| Distribution Reinvestment Plan (4) |

$ | 250,000,000 | $ | — | $ | — | $ | 250,000,000 | ||||||||

| Class A Shares, Per Share |

$ | 10.00 | $ | — | $ | — | 10.00 | |||||||||

| Class T Shares, Per Share |

$ | 10.00 | $ | — | $ | — | $ | 10.00 | ||||||||

| Class I Shares, Per Share |

$ | 10.00 | $ | — | $ | — | $ | 10.00 | ||||||||

|

|

||||||||||||||||

|

|

||||||||||||||||

| (1) | The proceeds are calculated without deducting certain organization and offering expenses. The total of the other organization and offering expenses, excluding selling commissions, dealer manager fees and annual distribution and stockholder servicing fees, are estimated to be approximately $17,500,000 if the maximum primary offering amount is sold. Our advisor will pay these other organization and offering expenses on our behalf, without reimbursement by us. |

| (2) | The maximum and minimum selling commissions and dealer manager fee assume that 5%, 90% and 5% of the gross offering proceeds from the primary offering are from sales of Class A, Class T, and Class I, respectively. The selling commissions are equal to 7.00%, 2.00% and 0% of the sale price for Class A, Class T and Class I shares, respectively, with discounts available to some categories of investors, and the dealer manager fee is equal to 2.75%, 2.75% and 0% of the sale price for Class A, Class T and Class I shares, respectively, with discounts available to some categories of investors. |

| (3) | The Company will also pay an annual distribution and stockholder servicing fee, subject to certain limits, with respect to the Class T and Class I shares sold in the primary offering in an annual amount equal to 1.00% and 0.50%, respectively of the current primary gross offering price per Class T or Class I share, respectively, or, in certain cases, the estimated net asset value per Class T or Class I share, respectively, payable on a quarterly basis. See “Plan of Distribution.” |

| (4) | We will not pay selling commissions, dealer manager fees, annual distribution and stockholder servicing fees, or reimburse issuer costs, in connection with shares of common stock issued through our distribution reinvestment plan. For participants in the distribution reinvestment plan, distributions paid on Class A shares, Class T shares and Class I shares, as applicable, will be used to purchase Class A shares, Class T shares and Class I shares, respectively. |

The date of this prospectus is March 2, 2016

Table of Contents

We have established financial suitability standards for initial stockholders in this offering. These suitability standards require that a purchaser of shares have either:

| • | a net worth of at least $250,000; or |

| • | a gross annual income of at least $70,000 and a net worth of at least $70,000. |

In determining your net worth, do not include the value of your home, home furnishings or personal automobiles.

Our suitability standards also require that you:

| • | can reasonably benefit from an investment in our common stock based on your overall investment objectives and portfolio structure; |

| • | are able to bear the economic risk of the investment based on your overall financial situation; and |

| • | have an apparent understanding of: |

| • | the fundamental risks of your investment; |

| • | the risk that you may lose your entire investment; |

| • | the lack of liquidity of your shares; |

| • | the restrictions on transferability of your shares; |

| • | the background and qualifications of our advisor; and |

| • | the tax consequences of your investment. |

Our sponsor, CNL Financial Group, LLC, and each person selling shares on our behalf must make every reasonable effort to determine that the purchase of shares in this offering is a suitable and appropriate investment for each stockholder based on information provided by the stockholder regarding the stockholder’s financial situation and investment objectives. In the case of sales to fiduciary accounts, these minimum standards shall be met by the beneficiary, by the fiduciary account, or by the donor or grantor who directly or indirectly supplies the funds to purchase the shares if the donor or grantor is the fiduciary.

Certain states have established suitability requirements that are more stringent than the standards that we have established and described above. Shares will be sold to investors residing in these states only if those investors represent that they meet the additional suitability standards set forth below. In each case, these additional suitability standards exclude from the calculation of net worth the value of an investor’s home, home furnishings and personal automobiles.

| • | Alabama—In addition to meeting the applicable suitability standards set forth above, CNL Healthcare Properties II, Inc.’s securities will only be sold to Alabama residents who have a liquid net worth of at least 10 times their investment in this real estate program and its affiliates. |

| • | California—An investment in CNL Healthcare Properties II, Inc.’s securities is limited to California investors who have (i) a liquid net worth of not less than $100,000 and a gross annual income of not less than $75,000 or (ii) a net worth of $250,000, exclusive of his or her home, home furnishings, and automobile. In addition, a California resident may not invest more than 10% of his or her net worth in this offering. |

i

Table of Contents

| • | Idaho—An investment in CNL Healthcare Properties II, Inc.’s securities is limited to Idaho investors who have either (i) a liquid net worth of $85,000 and an annual gross income of $85,000 or (ii) a liquid net worth of $300,000. Additionally, an Idaho investor’s total investment in CNL Healthcare Properties II, Inc. shall not exceed 10% of such investor’s liquid net worth. For these purposes, “liquid net worth” is defined as that portion of net worth consisting of cash, cash equivalents and readily marketable securities. |

| • | Iowa—An investment in CNL Healthcare Properties II, Inc.’s securities is limited to Iowa investors who have either (a) a minimum net worth of $300,000 (exclusive of home, auto and furnishings) or (b) a minimum annual income of $70,000 and a net worth of $100,000 (exclusive of home, auto and furnishings). In addition, an Iowa resident may not invest more than 10% of his or her liquid net worth in this offering. For these purposes, “liquid net worth” shall consist of cash, cash equivalents and readily marketable securities. |

| • | Kentucky—A Kentucky resident who invests in the securities of CNL Healthcare Properties II, Inc. must have (i) a minimum gross annual income of $70,000 and a minimum net worth of $70,000, or (ii) a minimum net worth of $250,000. Moreover, no Kentucky resident shall invest more than 10% of his or her liquid net worth (cash, cash equivalents and readily marketable securities) in the securities of CNL Healthcare Properties II, Inc. or its affiliates’ non-publicly traded real estate investment trusts. |

| • | Missouri—In addition to meeting the applicable suitability standards set forth above, an investment in each class of CNL Healthcare Properties II, Inc.’s securities may not exceed 10% of a Missouri investor’s liquid net worth. |

| • | Nebraska—Investors who are not accredited investors as defined in Regulation D under the Securities Act of 1933, as amended, must limit their aggregate investment in this offering and in the securities of other non-publicly traded real estate investment trusts (REITs) to 10% of such investor’s net worth. |

| • | New Jersey—An investment in CNL Healthcare Properties II, Inc.’s securities is limited to New Jersey investors who have: (a) a minimum liquid net worth of at least $100,000 and a minimum annual gross income of not less than $85,000; or (b) a minimum liquid net worth of $350,000. For these purposes, ‘liquid net worth” is defined as that portion of net worth (total assets exclusive of home, home furnishings and automobiles, minus total liabilities) that consists of cash, cash equivalents and readily marketable securities. In addition, a New Jersey investor’s investment in us, our affiliates and other non-publicly traded direct investment programs (including real estate investment trusts, business development companies, oil and gas programs, equipment leasing programs and commodity pools, but excluding unregistered, federally and state exempt private offerings) may not exceed ten percent (10%) of his or her liquid net worth. |

| • | New Mexico—In addition to meeting the applicable suitability standards set forth above, your investment in CNL Healthcare Properties II, Inc., our affiliates and other non-traded real estate investment trusts may not exceed 10% of your liquid net worth. For these purposes, “liquid net worth” shall be defined as that portion of net worth which consists of cash, cash equivalents and readily marketable securities. |

| • | North Dakota—In addition to meeting the applicable suitability standards set forth above, a North Dakota resident must have a net worth of at least ten times his or her investment in CNL Healthcare Properties II, Inc. |

| • | Oregon—In addition to the suitability standards set forth above, an Oregon investor’s maximum investment in CNL Healthcare Properties II, Inc. and its affiliates may not exceed 10% of the investor’s liquid net worth. For these purposes, “liquid net worth” is defined as that portion of an investor’s net worth consisting of cash, cash equivalents and readily marketable securities. |

| • | Pennsylvania—An investor’s investment in CNL Healthcare Properties II, Inc.’s securities may not exceed ten percent (10%) of his or her net worth (exclusive of home, furnishings and automobiles). |

| • | Vermont—In addition to meeting the applicable suitability standards set forth above, each investor who is not an “accredited investor” as defined in 17 C.F.R. § 230.501 may not purchase an amount of shares in this offering that exceeds 10% of the investor’s liquid net worth. For these purposes, “liquid net worth” is defined as an investor’s total assets (not including home, home furnishings, or automobiles) minus total liabilities. Vermont residents who are “accredited investors” as defined in 17 C.F.R. § 230.501 are not subject to the limitation described in this paragraph. |

In addition to the suitability standards established above, the following states have established recommendations for investors residing in those states. Shares will be sold to investors in these states only if those investors acknowledge the recommendations set forth below.

ii

Table of Contents

| • | Kansas—The Office of the Kansas Securities Commissioner recommends that an investor’s aggregate investment in our securities and other similar direct participation investments not exceed 10% of the investor’s liquid net worth. For this purpose, “liquid net worth” is defined as that portion of net worth that consists of cash, cash equivalents and readily marketable securities. |

| • | Maine—The Maine Office of Securities recommends that an investor’s aggregate investment in this offering and other similar direct participation investments not exceed 10% of the investor’s liquid net worth. For this purpose, “liquid net worth” is defined as that portion of net worth that consists of cash, cash equivalents and readily marketable securities. |

Since the minimum offering is less than $175 million, investors residing in Pennsylvania are cautioned to carefully evaluate the program’s ability to fully accomplish its stated objectives and to inquire as to the current dollar volume of program subscriptions. Pursuant to the requirements of the Pennsylvania Department of Banking and Securities, we will not solicit or accept subscriptions from Pennsylvania residents until after we have accepted subscriptions for shares totaling at least $87.5 million.

Before authorizing an investment in shares, fiduciaries of Plans (as defined below in the “Plan of Distribution” section) should consider, among other matters: (i) fiduciary standards imposed by the Employee Retirement Income Security Act of 1974, as amended or “ERISA” and governing state or other law, if applicable; (ii) whether the purchase of shares satisfies the prudence and diversification requirements of ERISA and governing state or other law, if applicable, taking into account any applicable Plan’s investment policy and the composition of the Plan’s portfolio, and the limitations on the marketability of shares; (iii) whether such fiduciaries have authority to hold shares under the applicable Plan investment policies and governing instruments; (iv) rules relating to the periodic valuation of Plan assets and the delegation of control over responsibility for “plan assets” under ERISA or governing state or other law, if applicable; (v) whether the investment will generate unrelated business taxable income to the Plan (see “Material U.S. Federal Income Tax Considerations—Taxation of U.S. Stockholders—Taxation of Tax-Exempt Stockholders”) and (vi) prohibitions under ERISA, the Internal Revenue Code of 1986, as amended, or the “Code” and/or governing state or other law relating to Plans engaging in certain transactions involving “plan assets” with persons who are “disqualified persons” under the Code or “parties in interest” under ERISA or governing state or other law, if applicable. See “Plan of Distribution—Certain Benefit Plan Considerations.”

Investors who meet the suitability standards described herein may subscribe for shares of our common stock as follows:

| • | Review this entire prospectus and any appendices and supplements accompanying this prospectus. |

| • | Complete the execution copy of the subscription agreement. A specimen copy of the subscription agreement is included in this prospectus as Appendix B. |

| • | Deliver your check for the full purchase price of the shares of our common stock being subscribed for, along with a completed, executed subscription agreement to your participating broker-dealer. |

| • | Make your check payable to “UMB Bank, N.A., Escrow Agent for CNL Healthcare Properties II, Inc.” until such time as we have raised the minimum offering ($2,000,000 in subscription proceeds, except $87,500,000 for Pennsylvania investors or $20,000,000 for Washington investors) and the funds are released from escrow. At that time, we will notify our dealer manager and participating brokers and ask that checks thereafter be made payable to “CNL Healthcare Properties II, Inc.” See “Plan of Distribution—The Offering” and “Plan of Distribution—Subscription Procedures.” |

By executing the subscription agreement and paying the total purchase price for the shares of our common stock subscribed for, each investor attests that he or she meets the minimum net worth or income standards as stated in the subscription agreement and agrees to be bound by all of its terms.

iii

Table of Contents

Subscriptions will be effective only upon our acceptance, and we reserve the right to reject any subscription, in whole or in part. An approved custodian/trustee must process and forward to us subscriptions made through individual retirement accounts, or “IRAs,” Keogh plans, 401(k) plans and other tax-deferred plans. See “Suitability Standards” and “Plan of Distribution—Subscription Procedures” for additional details on how you can purchase shares of our common stock.

iv

Table of Contents

| i | ||||

| iii | ||||

| 1 | ||||

| 1 | ||||

| 2 | ||||

| 26 | ||||

| 67 | ||||

| 71 | ||||

| 83 | ||||

| 91 | ||||

| 95 | ||||

| 113 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

118 | |||

| 123 | ||||

| 129 | ||||

| 130 | ||||

| 140 | ||||

| 143 | ||||

| 147 | ||||

| 149 | ||||

| 165 | ||||

| 168 | ||||

| 190 | ||||

| 191 | ||||

| 203 | ||||

| 204 | ||||

| 204 | ||||

| 204 | ||||

| F-1 | ||||

| Appendix A | ||||

| Appendix B | ||||

| Appendix C | ||||

| Appendix D | ||||

v

Table of Contents

Certain statements in this prospectus constitute “forward-looking statements.” Forward-looking statements are statements that do not relate strictly to historical or current facts, but reflect management’s current understandings, intentions, beliefs, plans, expectations, assumptions and/or predictions regarding the future of our business and its performance, the economy and other future conditions and forecasts of future events and circumstances. Forward-looking statements are typically identified by words such as “believes,” “expects,” “anticipates,” “intends,” “estimates,” “plans,” “continues,” “pro forma,” “may,” “will,” “seeks,” “should” and “could,” and words and terms of similar substance used in connection with discussions of future operating or financial performance, business strategy and portfolios, projected growth prospects, cash flows, costs and financing needs, legal proceedings, amount and timing of anticipated future distributions, estimated net asset value per share of our common stock and other matters.

Our forward-looking statements are not guarantees of our future performance and stockholders are cautioned not to place undue reliance on any forward-looking statements. While we believe our forward-looking statements are reasonable, such statements are inherently susceptible to uncertainty and changes in circumstances. As with any projection or forecast, forward-looking statements are necessarily dependent on assumptions, data and/or methods that may be incorrect or imprecise, and may not be realized. Our forward-looking statements are based on our current expectations and a variety of risks, uncertainties and other factors, many of which are beyond our ability to control or accurately predict.

Important factors that could cause our actual results to vary materially from those expressed or implied in our forward-looking statements include, but are not limited to, the factors listed and described under “Risk Factors” in this prospectus, our Quarterly Reports on Form 10-Q and Annual Report on Form 10-K, as filed with the Commission and other documents we file from time to time with the Securities and Exchange Commission (the “Commission”).

All written and oral forward-looking statements attributable to us or persons acting on our behalf are qualified in their entirety by these cautionary statements. Forward-looking statements speak only as of the date on which they are made; we undertake no obligation to, and expressly disclaim any obligation to, update or revise forward-looking statements to reflect new information, changed assumptions, the occurrence of subsequent events, or changes to future operating results over time unless otherwise required by law.

This prospectus includes information with respect to market share and industry conditions from third-party sources or based upon our estimates using such sources when available. While we believe that such information and estimates are reasonable, we have not independently verified any of the data from third-party sources. Similarly, our internal research is based upon our understanding of industry conditions, and such information has not been independently verified.

1

Table of Contents

This prospectus summary highlights material information contained elsewhere in this prospectus. Because it is a summary, this section does not contain all of the information that is important to your decision whether to invest in our common stock. To understand this offering fully, you should read the entire prospectus carefully, including the “Risk Factors” section and the financial statements. As used herein, “the Company,” “we,” “our” and “us” refer to CNL Healthcare Properties II, Inc. and its operating partnership, CHP II Partners, LP and related subsidiaries, except where the context otherwise requires.

CNL Healthcare Properties II, Inc.

CNL Healthcare Properties II, Inc. was formed as a Maryland corporation on July 10, 2015 and is sponsored by CNL Financial Group, LLC, referred to herein as the “sponsor.” We intend to operate in a manner that will allow us to qualify as a real estate investment trust, or REIT, for U.S. federal income tax purposes, commencing with the taxable year in which we satisfy the minimum offering requirement or our first year of material operations, which is currently expected to be the year ending December 31, 2016.

We were formed to make investments in a portfolio of real estate properties that we believe will generate a steady current return and provide long-term value to our stockholders. In particular, we will focus on acquiring properties primarily located in the United States within the seniors housing, medical office building, acute care and post-acute care facility sectors, including stabilized, value add and development properties, as well as other types of real estate and real estate-related securities and loans. The types of medical office buildings that we may acquire include specialty medical and diagnostic service facilities, surgery centers, outpatient rehabilitation facilities and other facilities designed for clinical services. The types of acute care facilities that we may acquire include general acute care hospitals and specialty surgical hospitals. The types of post-acute care facilities that we may acquire include skilled nursing facilities, long-term acute care hospitals and inpatient rehabilitative facilities. We view, manage and evaluate our portfolio homogeneously as one collection of healthcare assets with a common goal of maximizing revenues and property income regardless of the asset class or asset type.

We generally expect to lease seniors housing properties to wholly-owned taxable REIT subsidiary entities (each a “TRS” and collectively “TRSs”) and engage independent third-party managers under management agreements to operate the properties as permitted under the REIT Investment Diversification and Empowerment Act of 2007 (“RIDEA”) structures; however, we may also lease our seniors housing properties to third-party tenants under triple net or similar lease structures, where the tenant bears all or substantially all of the costs (including cost increases, real estate taxes, utilities, insurance and ordinary repairs). Medical office, acute care and post-acute care properties will generally be leased on a triple net, net or modified gross basis to third-party tenants. In addition, we expect most investments will be wholly owned, although we may invest through partnerships with other entities where we believe it is appropriate and beneficial. We expect to invest in new property developments or properties which have not reached full stabilization. Finally, we also may invest in and originate mortgage, bridge or mezzanine loans or invest in entities that make investments similar to the foregoing investment types. We generally make loans to the owners of properties to enable them to acquire land or buildings or to develop property. In exchange, the owner generally grants us a first lien or collateralized interest in a participating mortgage collateralized by the property or by interests in the entity that owns the property.

Our office is located at 450 South Orange Avenue, Orlando, Florida 32801. Our telephone number is (407) 650-1000.

Our Sponsor and Our Advisor

CNL Financial Group, LLC is our sponsor and promoter and an affiliate of CNL Financial Group, Inc. (“CNL”), which is a leading private investment management firm providing alternative and global real estate investments. Since its inception in 1973, CNL and/or its affiliates have formed or acquired companies with more than $33 billion in assets. Based in Orlando, Florida, CNL was formed by and is currently indirectly owned and controlled by James M. Seneff, Jr. Services provided by CNL and its affiliates include advisory, acquisition, development, lease and loan servicing, asset and portfolio management, disposition, client services, capital raising, finance and administrative services.

2

Table of Contents

We are externally advised by our advisor, CHP II Advisors, LLC, a Delaware limited liability company, which is an affiliate of our sponsor. All of our executive officers are also executive officers of our advisor. Pursuant to the advisory agreement, our advisor is responsible for managing our affairs on a day-to-day basis, identifying and analyzing potential investment opportunities, presenting and making recommendations to our board of directors regarding such opportunities and making acquisitions and investments on our behalf.

Our management team has experience investing in, acquiring, developing and managing various types of real estate and real estate-related assets and we expect to benefit from this investment expertise and experience. Our advisor will provide advisory services relating to substantially all aspects of our investments and operations, including real estate acquisitions, asset management and other operational matters. We will pay our advisor certain fees for these services and will reimburse our advisor for expenses incurred on our behalf, subject to certain limitations.

Our advisor performs its duties and responsibilities to us under an advisory agreement and owes fiduciary duties to us and our stockholders. The term of the advisory agreement is for one year after the date of execution, subject to an unlimited number of successive one-year renewals upon the mutual consent of the parties. Our advisor has minimal assets with which to remedy any liabilities that may result under the advisory agreement. Our independent directors are required to review and approve the terms of our advisory agreement at least annually.

Our advisor may subcontract with affiliated or unaffiliated service providers for the performance of substantially all or a portion of its advisory services, but in such an event, our advisor will ultimately remain responsible for the completion and performance of all services and duties to be performed under our advisory agreement. The service providers our advisor may subcontract with may be insulated from liabilities to us for the services they perform, but they may have certain liabilities to our advisor.

Various affiliates of our sponsor and our advisor will provide services to us as described in the “Management,” “The Advisor and the Advisory Agreement” and “Conflicts of Interest” sections of this prospectus.

Terms of the Offering

We are offering up to $1,750,000,000 of shares of our common stock on a “best efforts” basis, referred to herein as the “primary offering,” which means that CNL Securities Corp., or the “dealer manager,” will use its best efforts but is not required to sell any specific amount of shares. We are offering, in any combination, three classes of our common stock in our primary offering: Class A shares, Class T shares and Class I shares. We are also offering, in any combination, up to $250,000,000 of Class A, Class T and Class I shares to be issued pursuant to our distribution reinvestment plan. There are differing selling fees and commissions for each class. The Company will also pay annual distribution and stockholder servicing fees, subject to certain limits, on the Class T and Class I shares sold in the primary offering. We reserve the right to reallocate shares of common stock between our distribution reinvestment plan and our primary offering.

We will not begin selling shares of our common stock in this offering until after the effective date of the registration statement of which this prospectus forms a part, and we will continue to offer shares of our common stock on a continuous basis until two years after the date of this prospectus, unless extended in accordance with applicable securities laws. However, in certain states the offering may continue for just one year unless we renew the offering period for up to one additional year. We reserve the right to terminate this offering at any time. Until we sell $2,000,000 in shares of common stock ($87,500,000 for Pennsylvania investors or $20,000,000 for Washington investors), your subscription funds will be held in escrow. If we do not sell $2,000,000 in shares of common stock, this offering will terminate and your funds will be returned promptly to you. The purchase of shares by our officers and directors and our advisor, our sponsor and their affiliates will count towards meeting the minimum offering requirement. There is no limit on the amount of shares that may be purchased by such persons and count towards meeting the minimum offering requirement. Any such purchases by our officers and our directors and our advisor, our sponsor and their affiliates will be for investment and not for resale. The offering proceeds will be held in an interest bearing escrow account at the escrow agent, UMB Bank, N.A., until we meet the minimum offering requirement. Thereafter, the offering proceeds will be released to us and will be available for investment or the payment of fees and expenses as soon as we accept your subscription agreement. We generally intend to admit stockholders on a daily basis. Subject to certain exceptions, you must initially invest at least $5,000 in shares of our common stock.

3

Table of Contents

We are offering three classes of our common stock in order to provide investors with more flexibility in making their investment in us. All investors can choose to purchase shares of Class A or Class T common stock in the offering, while Class I shares are only available to investors purchasing through certain registered investment advisors. Each share of our common stock, regardless of class, will be entitled to one vote per share on matters presented to the common stockholders for approval. The differences between the classes relate to the stockholder fees and selling commissions payable in respect of each class. The following summarizes the differences in fees and selling commissions among the classes of our common stock.

Class A Shares

| • | We will pay (i) a selling commission up to 7.00% and (ii) a dealer manager fee equal to 2.75% of the sale price for each Class A share sold in the primary offering. Subject to the 10% limit on underwriting compensation, Class A shares have higher front-end fees charged at the time of purchase of the shares than are charged on Class T shares due to the higher selling commission paid on Class A shares sold in the primary offering. Front-end fees are not paid on Class I shares. There are ways to reduce these charges. See “Plan of Distribution—Volume Discounts (Class A Shares Only)” for additional information. |

| • | No annual distribution and stockholder servicing fees are paid on Class A shares. |

Class T Shares

| • | We will pay (i) a selling commission equal to 2.00% and (ii) a dealer manager fee equal to 2.75% of the sale price for each Class T share sold in the primary offering. Subject to the 10% limit on underwriting compensation, Class T shares have lower front-end fees charged at the time of purchase of the shares than are charged on Class A shares due to the lower selling commission paid on Class T shares sold in the primary offering. Front-end fees are not paid on Class I shares. |

| • | Subject to, among other things, the 10% limit on underwriting compensation, the Company pays annual distribution and stockholder servicing fees in an annual amount equal to 1.00% of the then-current primary offering price per Class T share (or, in certain cases, the amount of our estimated net asset value per share), payable on a quarterly basis. This fee is not paid on Class A shares, is larger than the similar fee paid on Class I shares and, all things equal, will result in the per share distributions on Class T shares being less than the per share distributions on Class A shares or Class I shares. There is no assurance that we will pay distributions in any particular amount, if at all. |

Class I Shares

| • | Class I shares have no front-end fees. |

| • | Subject to, among other things, the 10% limit on underwriting compensation, the Company pays annual distribution and stockholder servicing fees in an annual amount equal to 0.50% of the then-current primary offering price per Class I share (or, in certain cases, the amount of our estimated net asset value per share), payable on a quarterly basis. This fee is not paid on Class A shares, is smaller than the similar fee paid on Class T shares and, all things equal, will result in the per share distributions on Class I shares being less than the per share distributions on Class A shares and more than the per share distributions on Class T shares. There is no assurance we will pay distributions in any particular amount, if at all. |

The annual distribution and stockholder servicing fees will be paid on each Class T share and Class I share that is purchased in the primary offering. We do not pay annual distribution and stockholder servicing fees with respect to shares sold under our distribution reinvestment plan or shares received as distributions, although the amount of the annual distribution and stockholder servicing fee payable with respect to Class T shares sold in our primary offering will be allocated among all Class T shares, including those sold under our distribution reinvestment plan and those received as distributions, and the amount of the annual distribution and stockholder servicing fee payable with respect to Class I shares sold in our primary offering will be allocated among all Class I shares, including those sold under our distribution reinvestment plan and those received as distributions.

4

Table of Contents

We will cease paying the annual distribution and stockholder servicing fee with respect to Class T shares held in any particular account, and those Class T shares will convert into a number of Class A shares determined by multiplying each Class T share to be converted by the applicable “Conversion Rate” described herein, on the earlier of (i) a listing of the Class A shares on a national securities exchange; (ii) a merger or consolidation of the Company with or into another entity, or the sale or other disposition of all or substantially all of the Company’s assets; (iii) after the termination of the primary offering in which the initial Class T shares in the account were sold, the end of the month in which total underwriting compensation paid in the primary offering is not less than 10% of the gross proceeds of the primary offering from the sale of Class A, Class T and Class I shares; and (iv) the end of the month in which the total underwriting compensation paid in a primary offering with respect to such Class T shares purchased in a primary offering, comprised of the dealer manager fees, selling commissions, and annual distribution and stockholder servicing fees, is not less than 9.75% of the gross offering price of those Class T shares purchased in such primary offering (excluding shares purchased through our distribution reinvestment plan and those received as stock dividends). If we redeem a portion, but not all of the Class T shares held in a stockholder’s account, the total underwriting compensation limit and amount of underwriting compensation previously paid will be prorated between the Class T shares that were redeemed and those Class T shares that were retained in the account. Likewise, if a portion of the Class T shares in a stockholder’s account is sold or otherwise transferred in a secondary transaction, the total underwriting compensation limit and amount of underwriting compensation previously paid will be prorated between the Class T shares that were transferred and the Class T shares that were retained in the account. Assuming a constant gross offering price or estimated net asset value per share of $10.50 and assuming none of the shares purchased were redeemed or otherwise disposed of or converted prior to the limits above being reached, we expect that with respect to a one-time $10,000 investment in Class T shares, approximately $100 in annual distribution and stockholder servicing fees will be paid to the dealer manager each year, until $500 in total annual distribution and stockholder servicing fees have been paid to the Dealer Manager with respect to such shares.

We will cease paying the annual distribution and stockholder servicing fee with respect to Class I shares held in any particular account, and those Class I shares will convert into a number of Class A shares determined by multiplying each Class I share to be converted by the applicable “Conversion Rate” described herein, on the earlier of (i) a listing of the Class A shares on a national securities exchange; (ii) a merger or consolidation of the Company with or into another entity, or the sale or other disposition of all or substantially all of the Company’s assets; (iii) after the termination of the primary offering in which the initial Class I shares in the account were sold, the end of the month in which total underwriting compensation paid in the primary offering is not less than 10% of the gross proceeds of the primary offering from the sale of Class A, Class T and Class I shares; and (iv) the end of the month in which the total underwriting compensation paid in a primary offering with respect to such Class I shares purchased in a primary offering, comprised of the dealer manager fees, selling commissions, and annual distribution and stockholder servicing fees, is not less than 9.75% of the gross offering price of those Class I shares purchased in such primary offering (excluding shares purchased through our distribution reinvestment plan and those received as stock dividends). If we redeem a portion, but not all of the Class I shares held in a stockholder’s account, the total underwriting compensation limit and amount of underwriting compensation previously paid will be prorated between the Class I shares that were redeemed and those Class I shares that were retained in the account. Likewise, if a portion of the Class I shares in a stockholder’s account is sold or otherwise transferred in a secondary transaction, the total underwriting compensation limit and amount of underwriting compensation previously paid will be prorated between the Class I shares that were transferred and the Class I shares that were retained in the account. Assuming a constant gross offering price or estimated net asset value per share of $10.00 and assuming none of the shares purchased were redeemed or otherwise disposed of or converted prior to the limits above being reached, we expect that with respect to a one-time $10,000 investment in Class I shares, approximately $50 in annual distribution and stockholder servicing fees will be paid to the dealer manager each year, until $975 in total annual distribution and stockholder servicing fees have been paid to the Dealer Manager with respect to such shares.

The “Conversion Rate” with respect to Class T shares will be equal to the quotient, the numerator of which is the estimated value per Class T share (including any reduction for annual distribution and stockholder servicing fees as described herein) and the denominator of which is the estimated value per Class A share. The “Conversion Rate” with respect to Class I shares will be equal to the quotient, the numerator of which is the estimated value per Class I share (including any reduction for annual distribution and stockholder servicing fees as described herein) and the denominator of which is the estimated value per Class A share. See “Description of Capital Stock—Valuation Policy.”

5

Table of Contents

We will further cease paying the annual distribution and stockholder servicing fee on any Class T or Class I share that is redeemed or repurchased, as well as upon the Company’s dissolution, liquidation or the winding up of the Company’s affairs, or a merger or other extraordinary transaction in which the Company is a party and, with respect to Class T shares, in which the Class T shares as a class are exchanged for cash or other securities, or, with respect to Class I shares, in which the Class I shares as a class are exchanged for cash or other securities.

If we liquidate (voluntarily or otherwise), dissolve or wind up our affairs, then, immediately before such liquidation, dissolution or winding up, our Class T shares and Class I shares will automatically convert to Class A shares at the applicable Conversion Rate and our net assets, or the proceeds therefrom, will be distributed to the holders of Class A shares, which will include all converted Class T shares and Class I shares, in accordance with their proportionate interests.

With respect to the conversion of Class T shares or Class I shares into Class A shares described above, each Class T share or Class I share, as applicable, will convert into an equivalent amount of Class A shares based on the respective estimated net asset value per share for each class. We currently expect that the conversion will be on a one-for-one basis, as we expect the estimated net asset value per share of each Class A share, Class T share and Class I share to be effectively the same. Following the conversion of their Class T shares or Class I shares into Class A shares, those stockholders continuing to participate in our distribution reinvestment plan will receive Class A shares going forward at the then-current distribution reinvestment price per Class A share, which may be higher than the distribution reinvestment price that they were previously paying per Class T share or Class I share, as applicable.

The per share amount of distributions on Class A, Class T and Class I shares will differ because of different allocations of certain class-specific expenses. Specifically, distributions on Class T shares and Class I shares will be lower than distributions on Class A shares because the Company is required to pay ongoing annual distribution and stockholder servicing fees with respect to the Class T shares and Class I shares sold in the primary offering. There is no assurance we will pay distributions in any particular amount, if at all. If the annual distribution and stockholder servicing fee paid by the Company with respect to Class T shares exceeds the amount distributed to holders of Class A shares in a particular period (such excess amount is referred to herein as the “Excess Class T Fee”), the estimated value per Class T share would be permanently reduced by an amount equal to the Excess Class T Fee for the applicable period divided by the number of Class T shares outstanding at the end of the applicable period, reducing both the estimated value of the Class T shares used for conversion purposes and the applicable Conversion Rate described herein. Similarly, if the annual distribution and stockholder servicing fee paid by the Company with respect to Class I shares exceeds the amount distributed to holders of Class A shares in a particular period (such excess amount is referred to herein as the “Excess Class I Fee”), the estimated value per Class I share would be permanently reduced by an amount equal to the Excess Class I Fee for the applicable period divided by the number of Class I shares outstanding at the end of the applicable period, reducing both the estimated value of the Class I shares used for conversion purposes and the applicable Conversion Rate described herein.

If you are not eligible to purchase Class I shares, then in selecting between our Class A and Class T shares, you should consider whether you would prefer an investment with higher up-front fees and likely higher current distributions (Class A shares) versus an investment with lower up-front fees but likely lower current distributions (Class T shares). In addition, for the same investment amount, you will receive more Class T shares than you would if you purchased Class A shares, due to the differences in the purchase prices of the Class A and Class T shares, unless you are eligible for certain discounts on Class A shares. You should also consider whether you qualify for any discounts if you choose to purchase Class A shares. See the section of this prospectus entitled “Plan of Distribution” for a description of the circumstances under which selling commissions and dealer manager fees may be reduced in connection with certain purchases. Please also review the more detailed description of our classes of shares in the section entitled “Description of Capital Stock” in this prospectus, and consult with your financial advisor before making your investment decision.

In selecting between our Class A and Class I shares, you should consider whether you would prefer an investment with higher up-front fees and likely higher current distributions (Class A shares) versus an investment with lower up-front fees but likely lower current distributions (Class I shares). In addition, for the same investment amount, you will receive more Class I shares than you would if you purchased Class A shares, unless you are eligible for certain other discounts on Class A shares. You should also consider whether you qualify for any discounts if you choose to purchase Class A shares, which would improve your investment returns on Class A shares. See the

6

Table of Contents

section of this prospectus entitled “Plan of Distribution” for a description of the circumstances under which selling commissions and dealer manager fees may be reduced in connection with certain purchases. Please also review the more detailed description of our classes of shares in the section entitled “Description of Capital Stock” in this prospectus, and consult with your financial advisor before making your investment decision.

Estimated Use of Proceeds

Assuming that 5% of the primary offering gross proceeds come from sales of Class A shares, 90% of primary offering gross proceeds come from sales of Class T shares, and 5% of primary offering gross proceeds come from sales of Class I shares, our management team expects to invest approximately 95.24% of the primary offering gross offering proceeds to acquire real property, debt and other investments as described in this prospectus, and to pay the associated investment services fees and acquisition expenses. The actual percentage of offering proceeds used to make investments will depend on the number of primary shares sold and the number of shares sold pursuant to our distribution reinvestment plan as well as whether we sell more or less than we have assumed of either Class A shares, Class T shares or Class I shares. In addition, as noted below, until the net proceeds from this offering are fully invested and from time to time thereafter, we may not generate sufficient cash flow from operations to fully fund our distributions. Therefore, some or all of our distributions may be paid from other sources, which may include the net proceeds from this offering. We have not established a cap on the amount of our distributions that may be paid from any of these sources. The assumption that 5% of the primary offering gross proceeds will come from sales of Class A shares, 90% of the primary offering gross proceeds will come from sales of Class T shares, and 5% of the primary offering gross proceeds will come from sales of Class I shares is based upon the dealer manager’s expectations, taking into consideration the experiences of other multi-class blind pool initial public offerings of common stock by other REITs as well as future regulatory changes, and there can be no assurance that this assumption will prove to be accurate.

Our Investment Objectives

Our primary investment objectives are to invest in a diversified portfolio of assets that will allow us to:

| • | pay attractive and steady cash distributions; |

| • | preserve, protect and grow your invested capital; and |

| • | explore liquidity opportunities in the future, such as the sale of either the Company or our assets, potential mergers, or the listing of our common stock on a national exchange. |

There is no assurance that we will be able to achieve our investment objectives. While there is no order of priority intended in the listing of our objectives, stockholders should realize that our ability to meet these objectives may be severely handicapped by the performance of our properties.

Investment Strategy

We focus our investment activities on the acquisition, development and financing of properties primarily located within the United States that we believe have the potential for long-term growth and income generation based upon the demographic and market trends and other underwriting criteria and models that we have developed. We intend to focus on the acquisition of properties within the seniors housing, medical office building, acute care and post-acute care facility sectors, including stabilized, value add and development properties. We plan to invest in carefully selected, well-located real estate that will provide an income stream generally through the receipt of rental income. We generally expect to lease seniors housing properties to our TRSs and engage independent third-party managers to operate them. We may also lease seniors housing properties to third-party tenants under triple net or similar lease structures, where the tenant bears all or substantially all of the costs. These investment structures require us to pay all operating expenses and may result in greater variability in operating results, but allow us the opportunity to capture greater returns during periods of market recovery, inflation or strong performance. Medical office, acute care and certain post-acute care properties will be leased on a triple net, net or modified gross basis to third-party tenants.

7

Table of Contents

We may also invest in and originate mortgage, bridge and mezzanine loans, a portion of which may lead to an opportunity to purchase a real estate interest in the underlying property. In addition, we also may invest in other income-oriented real estate assets, securities and investment opportunities that are otherwise consistent with our investment objectives and policies.

We will supplement this prospectus to provide descriptions of additional material properties and other material real estate-related investments that we acquire or propose to acquire during the course of this offering.

Our Initial Capitalization

We sold 20,000 shares of our common stock to our advisor for an aggregate purchase price of $200,000 or $10.00 per share. We did not pay any selling commissions or dealer manager fees in connection with the sale. The 20,000 shares were converted into 20,000 Class A shares upon the filing of our Articles of Amendment and Restatement. Except for sales to its affiliates, our advisor may not sell its initial investment in us for so long as it serves as our advisor.

Borrowing Policies

We may borrow money to acquire real estate assets either at closing or sometime thereafter. These borrowings will take the form of interim or long-term financing primarily from banks or other lenders, and generally will be collateralized by a mortgage on one or more of our properties but also may require us to be directly or indirectly (through a guarantee) liable for the borrowings. We will borrow at either fixed or variable interest rates and on terms that will require us to repay the principal on a level schedule or at one time in a “balloon” payment. There is no limitation on the amount we may invest in any single property or other asset or on the amount we can borrow for the purchase of any individual property or other investment. Our charter limits the amount we may borrow, in the aggregate, to 300% of our net assets. Any borrowings over this limit must be approved by a majority of our independent directors and disclosed to our stockholders along with justification for exceeding this limit. See “Business—Financings and Borrowings” for further information.

Summary Risk Factors

An investment in our common stock is subject to significant risks that are described in more detail in the “Risk Factors” and “Conflicts of Interest” sections of this prospectus. If we are unable to effectively manage the impact of these risks, we may not meet our investment objectives and, therefore, you may lose some or all of your investment. We believe the following risks are most relevant to an investment in shares of our common stock:

| • | We have no prior operating history and there is no assurance that we will be able to achieve our investment objectives. The prior performance of other CNL-affiliated entities may not be an accurate barometer of our future results. |

| • | The offering price for each class of our shares was arbitrarily determined and will not accurately represent the current value of our assets at any particular time. The purchase price you pay for shares of our common stock may be higher than the value of our assets per share of our common stock at the time of your purchase. |

| • | This is a “best efforts” offering and if we are unable to raise substantial funds, we will be limited in the number and type of investments we may make. |

| • | This is a “blind pool” offering; neither we nor our advisor has presently acquired or contracted to acquire any real property, debt or other investments. You will not have the opportunity to evaluate our future investments prior to purchasing shares of our common stock. |

| • | There is no public trading market for shares of our common stock and we have no obligation or current plans to apply for listing on any public securities market. Therefore, you should consider our shares to be a long-term investment and be prepared to hold them for an indefinite period of time. |

8

Table of Contents

| • | We may have difficulty funding our distributions with funds provided by cash flows from operating activities; therefore, until we generate sufficient operating cash flow, it is likely we will fund distributions to our stockholders with cash flows from financing activities, which may include borrowings and net proceeds from primary shares sold in this offering, proceeds from the issuance of shares under our distribution reinvestment plan, cash resulting from a waiver or deferral of fees or expense reimbursements otherwise payable to our advisor or its affiliates, cash resulting from our advisor or its affiliates paying certain of our expenses, and proceeds from the sales of assets or from our cash balances (which may constitute a return of capital). The use of these sources to pay distributions and the ultimate repayment of any liabilities incurred could adversely impact our ability to pay distributions in future periods, decrease the amount of cash we have available for operations and new investments and/or potentially impact the value or result in dilution of your investment by creating future liabilities, reducing the return on your investment or otherwise. |

| • | We do not have control over market and business conditions that may affect our success, including changes in general or local economic or market conditions and changing demographics. Such external factors may reduce the value of properties that we acquire, the ability of our tenants to pay rent on a timely basis, or at all, the amount of the rent to be paid to us and the ability of borrowers to make loan payments on time, or at all, and may therefore negatively affect our cash flows and reduce the amount of cash available for distribution to our stockholders. |

| • | You are limited in your ability to sell your shares of common stock pursuant to our redemption plan. Our redemption plan limits the number of shares of our common stock that we can redeem at any time as well as the redemption price. Our board of directors may reject any redemption request for any reason or amend, suspend or terminate the redemption plan at any time. Therefore, you may not be able to sell any of your shares back to us under the redemption plan and, if you are able to sell your shares, you may not receive the same price you paid for such shares. |

| • | We do not own our advisor. None of our agreements with our advisor and its affiliates were negotiated at arm’s length. We pay substantial fees to our advisor and its affiliates, including the dealer manager, some of which are not based on the quality of the services rendered to us. The basis upon which such fees are calculated could influence their advice to us as well as their judgment in performing services for us. |

| • | Our board of directors determines our investment policies, including our policies regarding financing, growth, debt capitalization, REIT qualification and distributions. Our board of directors may amend or revise these and other policies without stockholder consent. |

| • | Thomas K. Sittema and Stephen H. Mauldin, two of our directors, are also officers and/or directors of our advisor and other affiliated entities. J. Chandler Martin, one of our independent directors, is also an independent director of CNL Healthcare Properties, Inc., an affiliate of our sponsor. Our officers also serve as officers of our advisor and may also serve as officers in one or more affiliated programs. These directors and officers share their management time and services among us and the affiliated companies and/or programs, which may own assets in asset classes in which we will invest, and could take actions that are more favorable to the other companies and/or programs than to us. |

| • | We are subject to risks as a result of the recent economic conditions in both the domestic and international credit markets. Volatility and uncertainty in debt markets could affect our ability to obtain financing for acquisitions or other activities related to real estate assets and the number, diversification or value of our real estate assets. |

| • | Our failure to qualify or remain qualified as a REIT would adversely affect our operations, the value of our common stock and our ability to make distributions to our stockholders. |

| • | Our use of leverage, such as mortgage indebtedness and other borrowings, increases the risk of loss on our investments. |

9

Table of Contents

| • | The continuation of a slow economy could adversely affect certain of the properties in which we invest, and the financial difficulties of our tenants and operators could adversely affect our revenues and results of operations. |

| • | We will not register as an investment company, and we will therefore not be subject to the substantive requirements imposed on registered investment companies by the Investment Company Act of 1940, or the “Investment Company Act.” If we are required to register as an investment company under the Investment Company Act, it could significantly impair the operation of our business. |

| • | If we internalize the management functions performed by our advisor and its affiliates, your interest in us could be diluted, we could incur other costs associated with being self-managed, we may not be able to retain or replace key personnel and we may have increased exposure to litigation as a result of such internalization. |

Our Operating Partnership

We expect to acquire properties through CHP II Partners, LP, referred to herein as “our operating partnership,” of which we own all of the limited partnership interests. We own a 1% general partnership interest through CHP II GP, LLC, a wholly-owned subsidiary. We believe that using an operating partnership structure gives us an advantage in acquiring properties from persons who may not otherwise sell such properties because of potentially unfavorable tax results.

Our Management

We operate under the direction of our board of directors, the members of which owe us fiduciary duties and are accountable to us and our stockholders in accordance with the Maryland General Corporation Law (the “MGCL”). Our board of directors is responsible for the management and control of our business and affairs and has responsibility for reviewing our advisor’s performance at least annually. Our board of directors has five members, three of whom are independent of our management, our advisor and our respective affiliates. Our directors are elected annually by our stockholders. Our board of directors has established an audit committee comprised of the independent directors.

All of our executive officers are also executive officers of our advisor and/or its affiliates. Our executive officers have extensive experience investing in real estate. Our chief executive officer and president has over 20 years of experience in the real estate and banking industries.

Conflicts of Interest

Substantial conflicts of interest exist between us and some of our affiliates. Our advisor and its executive officers will experience conflicts of interest in connection with the management of our business affairs. These conflicts arise principally from their involvement in other activities that may conflict with our business and interests. Conflicts of interest that exist between us and some of our affiliates include the following:

| • | Members of our board of directors, our executive officers and the executive officers of our advisor allocate their time between us, the other programs sponsored by CNL and our sponsor and other activities in which they are involved, which will limit the amount of time they spend on our business matters. In addition, CNL has two other public, non-traded real estate investment programs which have investment objectives similar to ours, CNL Healthcare Properties, Inc., which is closed to new investors, and CNL Lifestyle Properties, Inc., which is closed to new investors and evaluating liquidity events. Our sponsor also has one other public, non-traded real estate investment program, CNL Growth Properties, Inc., which is currently closed to new investors. Thomas K. Sittema, one of our directors, also serves on the board of directors of CNL Lifestyle Properties, Inc. and CNL Healthcare Properties, Inc. and we have some of the same executive officers as CNL Lifestyle Properties, Inc., CNL Healthcare Properties, Inc., and CNL Growth Properties, Inc. Additionally, our advisor and the advisors to CNL Lifestyle Properties, Inc. and CNL Healthcare Properties, Inc. have in common some of the same executive officers. All of these individuals devote only as much of their time to our business as they, in their judgment, determine is reasonably required, which could be substantially less than their full time. It is also intended that the managers of our advisor will devote the time necessary to fulfill their respective duties to us and our advisor. |

10

Table of Contents

| • | We compete with other existing and/or future real estate programs sponsored by CNL or its affiliates for the acquisition of properties and other investments, all of which may invest in commercial properties. In such event, we have adopted specialized procedures to determine which program sponsored by CNL, its affiliates or another entity should purchase any particular property, make any other investment or enter into a joint venture or co-ownership arrangement for the acquisition of specific investments. CNL and its affiliates are not required to offer any investment opportunity to us and we have no expectation that we will be offered any specific investment opportunity. |

| • | We may compete with other programs sponsored by CNL or its affiliates for the same tenants in negotiating and/or renegotiating, if applicable, leases or in selling similar properties in the same geographic region, and the executive officers of our advisor and its affiliates may face conflicts with respect to negotiating with such tenants and purchasers. |

| • | Our sponsor, advisor, directors or any of their affiliates may purchase or lease assets from us. Although a majority of our directors (including a majority of the independent directors) not otherwise interested in the transaction must determine that the transaction is fair and reasonable to us, there can be no assurance that the price for such purchase or lease of assets from us would be consistent with that obtained in an arm’s-length transaction. |

| • | We may purchase or lease assets from our sponsor, advisor, directors or any affiliate thereof. Although a majority of our directors (including a majority of the independent directors) not otherwise interested in the transaction must find that the transaction is fair and reasonable to us and at a price to us no greater than the cost of the asset to such advisor, sponsor, director or affiliate, unless substantial justification exists for the excess and our independent directors conclude the excess is reasonable, there can be no assurance that the price to us for such purchase or lease would be consistent with that obtained in an arm’s-length transaction. In no event may the purchase price to us of a property we purchase from our sponsor, advisor, a director or an affiliate thereof exceed its current appraised value as determined by an independent expert selected by our independent directors. |

| • | We may invest in joint ventures with our sponsor, our advisor, one or more of our directors or any of our affiliates. Although a majority of our directors (including a majority of the independent directors) not otherwise interested in the transaction must approve the investment as being fair and reasonable to us and on substantially the same terms and conditions as those that would be received by any other joint venturers, there can be no assurance that such terms and conditions would be as advantageous to us than if such terms and conditions were negotiated at arm’s length. |

| • | Our advisor and its affiliates receive fees in connection with transactions involving the purchase, management and sale of our investments, regardless of the quality of the services provided to us. There can be no assurance that such fees are as advantageous to us as if such fees were negotiated at arm’s length. |

| • | Our compensation arrangements with our advisor may provide an incentive to purchase assets using borrowings, because our advisor will receive an investment services fee and other fees based on the purchase price of the acquired asset which includes debt. |

| • | Agreements with our advisor and its affiliates were not, and will not be, negotiated at arm’s length and, accordingly, may be less advantageous to us than if similar agreements were negotiated with unaffiliated third parties. |

11

Table of Contents

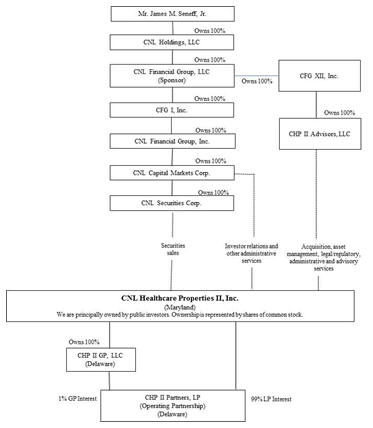

The following chart indicates the relationship between our advisor, our sponsor and certain other affiliates that will provide services to us.(1)

| (1) | Please see the disclosure below under “—Compensation of Our Advisor and Its Affiliates” for a description of the compensation, reimbursements and distributions we contemplate paying to our advisor, our dealer manager and other affiliates in exchange for services provided to us. |

James M. Seneff, Jr. wholly owns CNL Holdings, LLC. Mr. Seneff serves as a director and/or an officer of various CNL entities affiliated with our sponsor including our dealer manager, two other REITs sponsored by our sponsor, CNL Growth Properties, Inc. and CNL Healthcare Properties, Inc., and one other REIT, CNL Lifestyle Properties, Inc., sponsored by CNL.

See the “Risk Factors—Risks Related to Conflicts of Interest and our Relationships with our Advisor and its Affiliates” and “Conflicts of Interest” sections of this prospectus for a detailed discussion of the various conflicts of interest relating to your investment and the risks associated with such conflicts, as well as the policies that we have established to resolve or mitigate a number of these potential conflicts.

Compensation of Our Advisor and Its Affiliates