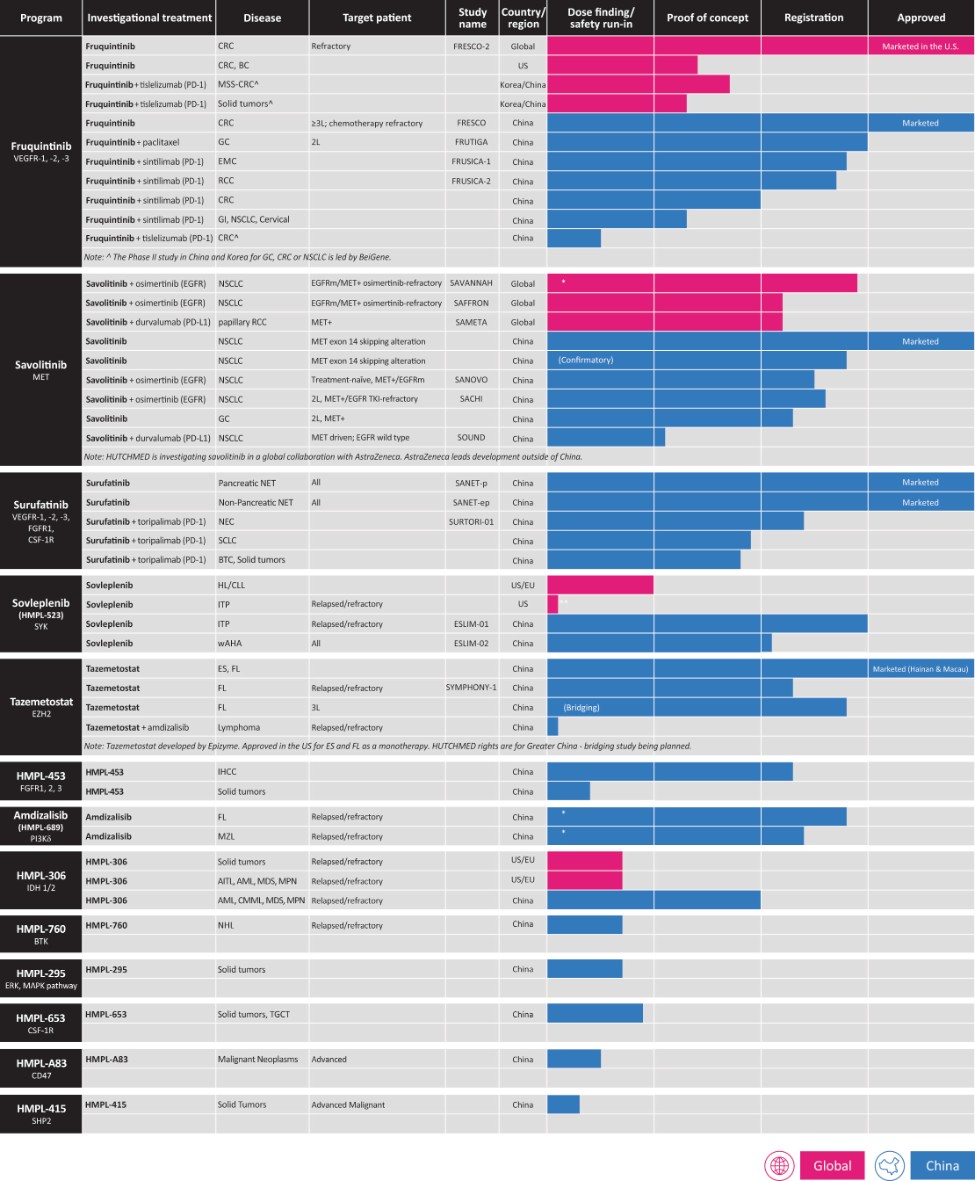

The following table summarizes the status of our clinical drug portfolio’s development as of the date of the filing of this annual report:

* Phase II registration-intent study subject to regulatory discussion.

73

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark one)

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended |

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to |

OR

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

Commission file number

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

+852 2121 8200

(Address of principal executive offices)

Chief Executive Officer and Chief Scientific Officer

Telephone: +

Facsimile: +

(Name, telephone, email and/or facsimile number and address of Company contact person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class |

| Trading Symbol(s) |

| Name of each exchange on which registered |

Nasdaq Global Select Market* |

*Not for trading, but only in connection with the listing of American depositary shares on the Nasdaq Global Select Market

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the Annual Report:

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

⌧

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

◻ Yes ⌧

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

⌧

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

⌧

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Accelerated filer ¨ | Non-accelerated filer ¨ | Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

†The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepare or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

International Financial Reporting Standards as issued | Other ◻ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

◻ Item 17 ◻ Item 18

If this is an Annual Report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

☐ Yes ☐ No

HUTCHMED (China) Limited

Table of Contents

3 | ||

5 | ||

7 | ||

7 | ||

7 | ||

7 | ||

67 | ||

158 | ||

158 | ||

181 | ||

199 | ||

203 | ||

203 | ||

204 | ||

214 | ||

214 | ||

217 | ||

217 | ||

Material Modifications to the Rights of Security Holders and Use of Proceeds | 217 | |

217 | ||

218 | ||

218 | ||

218 | ||

218 | ||

219 | ||

Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 219 | |

219 | ||

219 | ||

219 | ||

Disclosure Regarding Foreign Jurisdictions that Prevent Inspection | 219 | |

219 | ||

220 | ||

221 | ||

221 | ||

221 | ||

222 | ||

224 | ||

INTRODUCTION

This annual report on Form 20-F contains our audited consolidated statements of operations data for the years ended December 31, 2023, 2022 and 2021 and our audited consolidated balance sheet data as of December 31, 2023 and 2022. Our consolidated financial statements have been prepared in accordance with U.S. generally accepted accounting principles, or U.S. GAAP.

This annual report also includes audited consolidated income statement data for the years ended December 31, 2023, 2022 and 2021 and the audited consolidated statements of financial position data as of December 31, 2023 and 2022 for our non-consolidated joint venture, Shanghai Hutchison Pharmaceuticals. The financial statements of Shanghai Hutchison Pharmaceuticals have been prepared in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standard Board, or IASB.

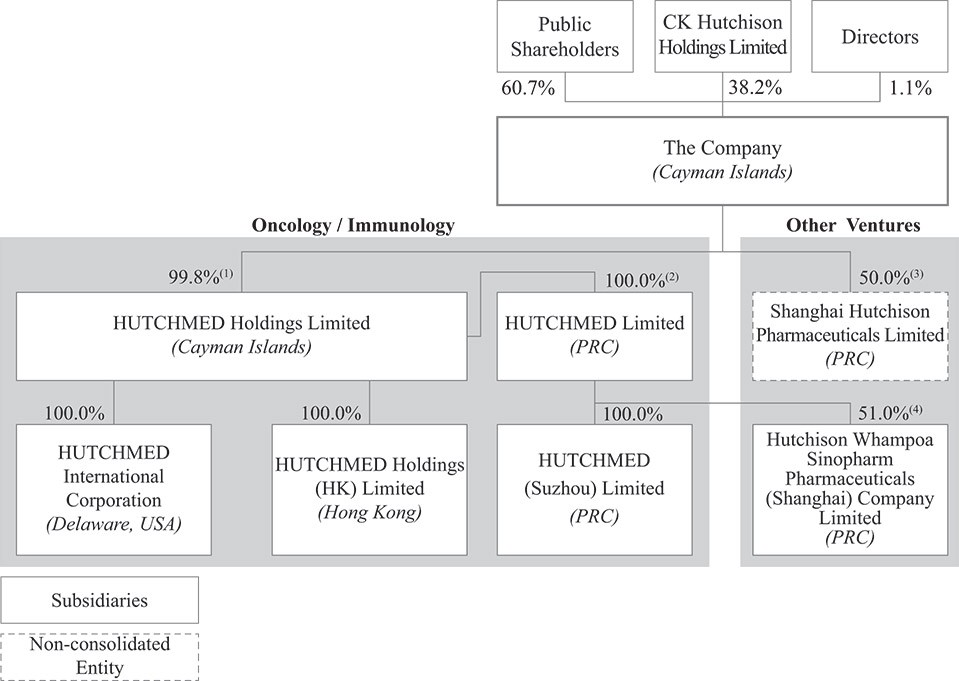

Unless the context requires otherwise, references herein to the “company,” “HUTCHMED,” “we,” “us” and “our” refer to HUTCHMED (China) Limited, a holding company incorporated in the Cayman Islands, and its consolidated subsidiaries and joint ventures, some of which, as noted below, are incorporated and operate in the PRC. “HUTCHMED Holdings” refers to HUTCHMED Holdings Limited, a subsidiary of the Company and a holding company incorporated in the Cayman Islands. “HUTCHMED Limited” refers to “HUTCHMED Limited”, a subsidiary of HUTCHMED Holdings which is incorporated in the PRC and through which we operate our Oncology/Immunology operations in China. Our other principal operating subsidiaries for our Oncology/Immunology operations are HUTCHMED International Corporation (incorporated in Delaware), HUTCHMED Holdings (HK) Limited (incorporated in Hong Kong) and HUTCHMED (Suzhou) Limited (incorporated and operates in the PRC). “Hutchison Sinopharm” refers to Hutchison Whampoa Sinopharm Pharmaceuticals (Shanghai) Company Limited, our PRC-incorporated joint venture with Sinopharm through which we operate our principal consolidated joint venture. See Item 4. “Information on the Company—C. Organizational Structure” for a diagram illustrating our corporate structure.

Conventions Used in this Annual Report

Unless otherwise indicated, references in this annual report to:

| ● | “ADRs” are to the American depositary receipts, which evidence our ADSs; |

| ● | “ADSs” are to our American depositary shares, each of which represents five ordinary shares; |

| ● | “AstraZeneca” are to AstraZeneca AB (publ); |

| ● | “China” or “PRC” refers to the People’s Republic of China including Hong Kong and Macau and, only for the purpose of this annual report, excluding Taiwan; and only in the context of describing PRC rules, laws, regulations, regulatory authority, and any PRC entities or citizens under such rules, laws and regulations and other legal or tax matters in this annual report, excludes Taiwan, Hong Kong, and Macau; the legal and operational risks associated with operating in China also apply to our operations in Hong Kong; |

| ● | “CK Hutchison” are to CK Hutchison Holdings Limited, a company incorporated in the Cayman Islands and listed on the Hong Kong Stock Exchange, and the ultimate parent company of our largest shareholder, Hutchison Healthcare Holdings Limited; |

| ● | “Eli Lilly” are to Lilly (Shanghai) Management Company Limited; |

| ● | “E.U.” are to the European Union; |

| ● | “Guangzhou Baiyunshan” are to Guangzhou Baiyunshan Pharmaceutical Holdings Company Limited, a leading China-based pharmaceutical company listed on the Shanghai Stock Exchange and the Hong Kong Stock Exchange; |

| ● | “Hain Celestial” are to The Hain Celestial Group, Inc., a Nasdaq-listed, natural and organic food and personal care products company; |

| ● | “HK$” or “HK dollar” are to the legal currency of the Hong Kong Special Administrative Region; |

3

| ● | “Hutchison Baiyunshan” are to Hutchison Whampoa Guangzhou Baiyunshan Chinese Medicine Company Limited, which was our non-consolidated joint venture with Guangzhou Baiyunshan in which we indirectly held a 50% interest through a holding company until our disposal of such interest on September 28, 2021 (this interest was previously held through a holding company in which we have a 80% interest); |

| ● | “HUTCHMED Science Nutrition” are to HUTCHMED Science Nutrition Limited, our previous wholly owned subsidiary which we divested in December 2023; |

| ● | “Hutchison Hain Organic” are to Hutchison Hain Organic Holdings Limited, our previous joint venture with Hain Celestial in which we had a 50% interest and divested in December 2023; |

| ● | “Hutchison Healthcare” are to Hutchison Healthcare Limited, our wholly owned subsidiary; |

| ● | “HUTCHMED Limited”, our PRC-incorporated subsidiary through which we operate our Oncology/Immunology operations in China and in which we have a 99.8% interest; |

| ● | “HUTCHMED Holdings” are to HUTCHMED Holdings Limited, our subsidiary incorporated in the Cayman Islands in which we have a 99.8% interest and which is the indirect holding company of HUTCHMED Limited; |

| ● | “Hutchison Sinopharm” are to Hutchison Whampoa Sinopharm Pharmaceuticals (Shanghai) Company Limited, our PRC-incorporated joint venture with Sinopharm in which we have a 50.9% interest and through which we operate our principal consolidated joint venture; |

| ● | “Inmagene” are to Inmagene Biopharmaceuticals; |

| ● | “ordinary shares” or “shares” are to our ordinary shares, par value $0.10 per share; |

| ● | “RMB” or “renminbi” are to the legal currency of the PRC; |

| ● | “SEHK” are to The Stock Exchange of Hong Kong Limited, or the Hong Kong Stock Exchange; |

| ● | “Shanghai Hutchison Pharmaceuticals” are to Shanghai Hutchison Pharmaceuticals Limited, our non-consolidated joint venture with Shanghai Pharmaceuticals in which we have a 50% interest; |

| ● | “Shanghai Pharmaceuticals” are to Shanghai Pharmaceuticals Holding Co., Ltd., a leading pharmaceutical company in China listed on the Shanghai Stock Exchange and the Hong Kong Stock Exchange; |

| ● | “Sinopharm” are to Sinopharm Group Co. Ltd., a leading distributor of pharmaceutical and healthcare products and a leading supply chain service provider in China listed on the Hong Kong Stock Exchange; |

| ● | “Takeda” are to Takeda Pharmaceuticals International AG |

| ● | “U.S.” or “United States” are to the United States of America; |

| ● | “$” or “U.S. dollars” are to the legal currency of the United States; and |

| ● | “£” or “pound sterling” are to the legal currency of the United Kingdom. |

References in this annual report to our “Oncology/Immunology” operations are to all activities related to oncology/immunology, including sales, marketing, manufacturing and research and development with respect to our drugs and drug candidates, and references to our “Other Ventures” are to all of our other businesses.

4

Our reporting currency is the U.S. dollar. In addition, this annual report also contains translations of certain foreign currency amounts into dollars for the convenience of the reader. Unless otherwise stated, all translations of pound sterling into U.S. dollars were made at £1.00 to $1.27, all translations of RMB into U.S. dollars were made at RMB7.16 to $1.00 and all translations of HK dollars into U.S. dollars were made at HK$7.8 to $1.00, which are the exchange rates used in our audited consolidated financial statements as of December 31, 2023. We make no representation that the pound sterling, HK dollar or U.S. dollar amounts referred to in this annual report could have been or could be converted into U.S. dollars, pounds sterling or HK dollars, as the case may be, at any particular rate or at all.

Trademarks and Service Marks

We own or have been licensed rights to trademarks, service marks and trade names for use in connection with the operation of our business, including, but not limited to, the trademarks “Hutchison”, “Chi-Med”, “Hutchison China MediTech”, “HUTCHMED”, “Elunate”, “Fruzaqla”, “Sulanda”, “Orpathys”, “Tazverik” and the logos used by HUTCHMED Limited. All other trademarks, service marks or trade names appearing in this annual report that are not identified as marks owned by us are the property of their respective owners.

Solely for convenience, the trademarks, service marks and trade names referred to in this annual report are listed without the ®, ™ and (sm) symbols, but we will assert, to the fullest extent under applicable law, our applicable rights in these trademarks, service marks and trade names.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This annual report contains forward-looking statements made under the “safe harbor” provisions of the U.S. Private Securities Litigation Reform Act of 1995. These statements relate to future events or to our future financial performance and involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. The words “anticipate,” “assume,” “believe,” “contemplate,” “continue,” “could,” “estimate,” “expect,” “goal,” “intend,” “may,” “might,” “objective,” “plan,” “potential,” “predict,” “project,” “positioned,” “seek,” “should,” “target,” “will,” “would,” or the negative of these terms or other similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. These forward-looking statements are based on current expectations, estimates, forecasts and projections about our business and the industry in which we operate and management’s beliefs and assumptions, are not guarantees of future performance or development and involve known and unknown risks, uncertainties and other factors. These forward-looking statements include statements regarding:

| ● | the initiation, timing, progress and results of our or our collaboration partners’ pre-clinical and clinical studies, and our research and development programs; |

| ● | our or our collaboration partners’ ability to advance our drug candidates into, and/or successfully complete, clinical studies; |

| ● | the timing of regulatory filings and the likelihood of favorable regulatory outcomes and approvals; |

| ● | regulatory developments in China, the United States and other countries; |

| ● | the ability of our or our collaboration partners’ drug sales team to effectively develop and execute promotional and marketing activities to support the marketing and sales of our approved drug candidates; |

| ● | the timing, progress and results of our or our collaboration partners’ commercial launches, the rate and degree of market acceptance and potential market for any of our approved drug candidates; |

| ● | the pricing and reimbursement of our and our joint ventures’ products and our approved drug candidates; |

| ● | our ability to contract on commercially reasonable terms with contract research organizations, or CROs, third-party suppliers and manufacturers; |

5

| ● | the scope of protection we are able to establish and maintain for intellectual property rights covering our or our joint ventures’ products and our drug candidates; |

| ● | the ability of third parties with whom we contract to successfully conduct, supervise and monitor clinical studies for our drug candidates; |

| ● | estimates of our expenses, future revenue, capital requirements and our needs for additional financing; |

| ● | our ability to obtain additional funding for our operations; |

| ● | the potential benefits of our collaborations and our ability to enter into future collaboration arrangements; |

| ● | the ability and willingness of our collaborators to actively pursue development activities under our collaboration agreements; |

| ● | our receipt of milestone or royalty payments, service payments and manufacturing costs pursuant to our strategic alliances with AstraZeneca, Eli Lilly, Takeda and Inmagene; |

| ● | our financial performance; |

| ● | our ability to attract and retain key scientific and management personnel; |

| ● | our relationship with our joint venture and collaboration partners; |

| ● | developments relating to our competitors and our industry, including competing drug products; |

| ● | changes in our tax status or the tax laws in the jurisdictions that we operate; and |

| ● | developments in our business strategies and business plans. |

Actual results or events could differ materially from the plans, intentions and expectations disclosed in the forward-looking statements we make. As a result, any or all of our forward-looking statements in this annual report may turn out to be inaccurate. We have included important factors in the cautionary statements included in this annual report on Form 20-F, particularly in the section of this annual report on Form 20-F titled “Risk Factors,” that we believe could cause actual results or events to differ materially from the forward-looking statements that we make. We may not actually achieve the plans, intentions or expectations disclosed in our forward-looking statements, and you should not place undue reliance on our forward-looking statements. Moreover, we operate in a highly competitive and rapidly changing environment in which new risks often emerge. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make.

You should read this annual report and the documents that we reference herein and have filed as exhibits hereto completely and with the understanding that our actual future results may be materially different from what we expect. The forward-looking statements contained herein are made as of the date of the filing of this annual report, and we do not assume any obligation to update any forward-looking statements except as required by applicable law.

In addition, this annual report contains statistical data and estimates that we have obtained from industry publications and reports generated by third-party market research firms. Although we believe that the publications, reports and surveys are reliable, we have not independently verified the data and cannot guarantee the accuracy or completeness of such data. You are cautioned not to give undue weight to this data. Such data involves risks and uncertainties and are subject to change based on various factors, including those discussed above.

6

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

A. Reserved.

B. Capitalization and Indebtedness.

Not applicable.

C. Reasons for the Offer and Use of Proceeds.

Not applicable.

D. Risk Factors.

HUTCHMED (China) Limited is a Cayman Islands holding company which conducts its operations in China through its PRC subsidiaries (our corporate group does not utilize any variable interest entities). We face various legal and operational risks and uncertainties as a company with substantial operations in China. The PRC government has significant authority to exert influence on the ability of a company with substantial operations in China, like us, to conduct its business, accept foreign investments or be listed on a U.S. stock exchange. For example, we face risks associated with PRC regulatory approvals of offshore offerings, anti-monopoly regulatory actions, cybersecurity, data privacy and from U.S. regulators if there is a lack of inspection from the U.S. Public Company Accounting Oversight Board, or PCAOB, on our auditors, which is further discussed below under “—Holding Foreign Companies Accountable Act” and in various risk factors in this section. The PRC government may also intervene with or influence our operations as the government deems appropriate to further regulatory, political and societal goals. The PRC government publishes from time to time new policies that can significantly affect our industry and we cannot rule out the possibility that it will in the future further release regulations or policies regarding our industry that could adversely affect our business, financial condition and results of operations. Any such action, once taken by the PRC government, could cause the value of our ADSs and ordinary shares to significantly decline or in extreme cases, become worthless.

7

Holding Foreign Companies Accountable Act

Pursuant to the Holding Foreign Companies Accountable Act, or the HFCAA, if the SEC determines that we have filed audit reports issued by a registered public accounting firm that has not been subject to inspections by the PCAOB for two consecutive years, the SEC will prohibit our shares or the ADSs from being traded on a national securities exchange or in the over-the-counter trading market in the United States. On December 16, 2021, the PCAOB issued a report to notify the SEC of its determination that the PCAOB was unable to inspect or investigate completely registered public accounting firms headquartered in mainland China and Hong Kong, including our auditor. In March 2022, the SEC conclusively listed us as a Commission-Identified Issuer under the HFCAA following the filing of our annual report on Form 20-F for the fiscal year ended December 31, 2021. On December 15, 2022, the PCAOB issued a report that vacated its December 16, 2021 determination and removed mainland China and Hong Kong from the list of jurisdictions where it is unable to inspect or investigate completely registered public accounting firms. As a result, the SEC will not provisionally or conclusively identify an issuer as a Commission-Identified Issuer if it files an annual report with an audit report issued by a registered public accounting firm headquartered in mainland China or Hong Kong on or after December 15, 2022, until such time as the PCAOB issues a new determination. Whether the PCAOB will continue to be able to satisfactorily conduct inspections of PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong in the future is subject to uncertainty and depends on a number of factors out of our, and our auditor’s, control, including the uncertainties surrounding the relationship between China and the United States. If PCAOB determines in the future that it no longer has full access to inspect and investigate completely accounting firms in mainland China and Hong Kong and we continue to use an accounting firm headquartered in one of these jurisdictions to issue an audit report on our financial statements filed with the Securities and Exchange Commission, we would be identified as a Commission-Identified Issuer following the filing of the annual report on Form 20-F for the relevant fiscal year. There can be no assurance that we would not be identified as a Commission-Identified Issuer for any future fiscal year, and if we were so identified for two consecutive years, we would become subject to the prohibition on trading under the HFCAA. See Item 3.D. “Risk Factors—Risks Relating to our ADSs—The PCAOB had historically been unable to inspect our auditor in relation to their audit work performed for our financial statements and the inability of the PCAOB to conduct inspections of our auditor in the past has deprived our investors with the benefits of such inspections.” and Item 3.D. “ Risk Factors—Risks Relating to our ADSs—Our ADSs may be prohibited from trading in the United States under the HFCAA in the future if the PCAOB is unable to inspect or investigate completely auditors located in China. The delisting of the ADSs, or the threat of their being delisted, may materially and adversely affect the value of your investment.”

Permissions, Approvals, Licenses and Permits Required from the PRC Authorities for Our Operations and for the Offering of Our Securities

We conduct our business primarily through our subsidiaries and joint ventures in China. Our operations in China are governed by PRC laws and regulations. As of the date of this annual report, we and our non-consolidated joint venture, Shanghai Hutchison Pharmaceuticals, have obtained the requisite permissions, approvals, licenses and permits from the PRC government authorities that are material for the business operations of our subsidiaries and our joint ventures in China, including, among others, pharmaceutical manufacturing permits, business licenses, drug registration certificates and pharmaceutical distribution permits and no such material permission or approval has been denied. For a detailed discussion on the licenses and permits we and our non-consolidated joint venture are required to obtain as a pharmaceutical company operating in China, see Item 4.B. “Business Overview—Certificates and Permits”, “Business Overview—Regulations—Government Regulation of Pharmaceutical Product Development and Approval,” “Business Overview—Regulations—Coverage and Reimbursement” and “Business Overview—Regulations—Other Healthcare Laws.” Given the uncertainties of interpretation and implementation of relevant laws and regulations and the enforcement practice by relevant government authorities, we may be required to obtain additional requisite permissions, approvals, licenses, permits and filings for the operation of our business in the future. See also “Risks Relating to Sales of Our Internally Developed Drugs and Other Drugs—Pharmaceutical companies in China are required to comply with extensive regulations and hold a number of permits and licenses to carry on their business. Our and our joint ventures’ ability to obtain and maintain these regulatory approvals is uncertain, and future government regulation may impose additional burdens on our operations.”

8

Furthermore, the PRC government has recently indicated an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers. For example, the CSRC published the Trial Measures and Listing Guidelines (defined below) on February 17, 2023 and became effective on March 31, 2023, designed to regulate overseas securities offerings by PRC domestic companies. Given the recent nature of the introduction of the Trial Measures and Listing Guidelines, there remains significant uncertainty as to the interpretation and implementation of regulatory requirements related to overseas securities offerings and other capital markets activities. As of the date of this annual report, in connection with our historical issuance of securities to foreign investors, we are not aware of any currently effective PRC laws, regulations and regulatory rules that would require us or our non-consolidated joint venture to obtain permissions from the China Securities Regulatory Commission (the “CSRC”), and we have not received any formal notice from any PRC authority indicating that we should apply for such permission or are subject to cybersecurity review or security assessment. If (i) we mistakenly conclude that certain regulatory filings, permissions and approvals are not required or (ii) applicable laws, regulations, or interpretations change and (iii) we are required to obtain such filings, permissions or approvals in the future, but fail to receive or maintain such filings, permissions or approvals, we may face sanctions by the CSRC, the Cyberspace Administration of China (the “CAC”) or other PRC regulatory agencies. In addition, rules and regulations in China can change with little advance notice. These regulatory agencies may impose fines and penalties on our operations in China, limit our operations in China, limit our ability to pay dividends outside of China, limit our ability to list on stock exchanges outside of China or offer our securities to foreign investors or take other actions that could have a material adverse effect on our business, financial condition, results of operations and prospects, as well as the trading price of our securities. Our non-consolidated joint venture faces the same risks as well. See also “Other Risks and Risks Relating to Doing Business in China—The PRC government exerts substantial influence over the manner in which we conduct our business activities. Its oversight and discretion over our business could result in a material adverse change in our operations and the value of our ordinary shares and ADSs. Changes in laws, regulations and policies in China and uncertainties with respect to the PRC legal system could materially and adversely affect us.” and “—The PRC government has increasingly strengthened oversight in offerings conducted overseas or on foreign investment in China-based issuers, which could result in a material change in our operations and our ordinary shares and ADSs could decline in value or become worthless.”

Cash Flows Through Our Organization

HUTCHMED (China) Limited is a Cayman Islands incorporated holding company with no material operations of its own. We conduct our operations primarily in China through our PRC subsidiaries and non-consolidated joint ventures, collectively referred to as the Onshore Entities below. HUTCHMED (China) Limited has an indirect equity ownership interest in all Onshore Entities through offshore Hong Kong-incorporated holding companies, and it has received funding through various capital markets transactions. We also fund our operations through cash flows generated and dividend payments from our Oncology/Immunology and Other Ventures operations (substantially all of which have been generated in China), service and milestone and upfront payments from our collaboration partners to our PRC subsidiaries, and bank loans to our subsidiaries.

We utilize a portion of our funds outside of China to support the operations of our subsidiaries in China through capital contributions and/or shareholder loans, which are the only methods by which we can fund our subsidiaries under PRC laws and regulations. Such capital contributions and shareholder loans are subject to the satisfaction of applicable government registration and approval requirements in China and limitations on the amount of shareholder loans relative to the amount of total capital contributions. If such subsidiaries generate sufficient income, they may repay shareholder loans or distribute retained earnings through cash dividends as determined by their respective board of directors. Our PRC subsidiaries are permitted to pay dividends only out of their retained earnings, if any, as determined in accordance with PRC accounting standards and regulations. Furthermore, our PRC subsidiaries are required to make appropriations to certain statutory reserve funds or may make appropriations to certain discretionary funds, which are not distributable as cash dividends except in the event of a solvent liquidation of the companies. The amount of any repayment of shareholder loans or dividend payments can be distributed to our various offshore subsidiaries through our offshore Hong Kong-incorporated holding companies. For more information, see Item 3.D. “Risk Factors—Other Risks and Risks Relating to Doing Business in China—Restrictions on currency exchange may limit our ability to receive and use our revenue effectively.” and Item 4.B. “Business Overview—Regulations—PRC Regulation of Foreign Currency Exchange, Offshore Investment and State-Owned Assets—Regulation on Investment in Foreign invested Enterprises.” Our joint ventures in China do not require intra-group funding as they have been profitable. Service and milestone and upfront payments from our collaboration partners are received directly by our PRC subsidiaries and reinvested into their operations.

9

For the years ended December 31, 2023, 2022 and 2021, HUTCHMED provided funds to its PRC subsidiaries of $20.0 million, $310.0 million and $230.0 million, respectively, of which $20.0 million, $100.0 million and $100.0 million, respectively, were in the form of capital contributions and nil, $210.0 million and $130.0 million, respectively, were in the form of shareholder loans. Additionally, during the years ended December 31, 2023 and 2022, shareholder loans of approximately $2.6 million and $3.4 million were repaid by a PRC subsidiary, respectively. There were no transfers of assets other than transfers of cash to/from PRC subsidiaries in 2023, 2022 and 2021.

For the years ended December 31, 2023, 2022 and 2021, the Hong Kong immediate holding company of our onshore non-consolidated joint venture, Shanghai Hutchison Pharmaceuticals, received dividends totaling approximately $42.3 million, $43.7 million and $49.9 million, respectively. These dividends were subject to a 5% withholding tax upon distribution from Shanghai Hutchison Pharmaceuticals to its Hong Kong immediate holding company.

HUTCHMED also conducts operations outside of China through subsidiaries in the U.S. and E.U. Such subsidiaries in the U.S. and E.U. have entered into service agreements with our PRC subsidiaries pursuant to which cash is transferred by our PRC subsidiaries to them to support their operations via the settlement of service invoices based on actual activities.

We have comprehensive cash management policies in place, including specific policies with respect to fund transfers through our organization. Our management regularly monitors the liquidity position and funding requirements of our subsidiaries and joint ventures. When funding is required by our operations in China, a thorough assessment is performed on the purpose of the funding (e.g., R&D investment, capital expenditures, etc.), the amount of funding and the form of injection (i.e., shareholder loans or capital contributions). Conversely, when a dividend distribution is to be made by an onshore joint venture, a similar assessment is performed on the cash flow forecast, sufficiency of funds and related factors. All necessary approvals are obtained at the chairman and chief executive officer levels and the board of directors for the relevant entities prior to any transfer. All such transfers and distributions are reviewed and approved by the relevant authorities where necessary, including the State Administration of Foreign Exchange, or SAFE, and the State Administration for Market Regulations, or SAMR. Our cash management policies and procedures also govern the management of any funds that are not yet required by our operations. Such funds are retained by our subsidiaries outside of China mainly in the form of short-term investments, such as time deposits with major banks in Hong Kong.

We have never declared or paid dividends on our ordinary shares. There have been no transfers, dividends or distributions made to U.S. investors to date. We currently expect to retain all future earnings for use in the operation and expansion of our business and do not have any present plan to pay any dividends. The declaration and payment of any dividends in the future will be determined by our board of directors in its discretion, and will depend on a number of factors, including our earnings, capital requirements, overall financial condition, and contractual restrictions. See Item 8. “Financial Information—A.8 Dividend Policy” and Item 3.D. “Risk Factors—Risks Relating to Our ADSs—We do not currently intend to pay dividends on our securities, and, consequently, your ability to achieve a return on your investment will depend on appreciation in the price of the ADSs.”

You should carefully consider all of the information in this annual report before making an investment in the ADSs. Below please find a summary of the principal risks and uncertainties we face, organized under relevant headings. In particular, as we are a China-based company incorporated in the Cayman Islands, you should pay special attention to subsections headed “Item 3. Key Information-3.D. Risk Factors-Other Risks and Risks Related to Doing Business in China.”

The following summarizes some, but not all, of the risks provided below. Please carefully consider all of the information discussed in this Item 3.D. “Risk Factors” in this annual report for a more thorough description of these and other risks.

Risks Relating to Our Financial Position and Need for Capital

| ● | Risks relating to our need for additional funding |

| ● | Risks relating to our existing and future indebtedness |

Risks Relating to Our Oncology/Immunology Operations and Development of Our Drug Candidates

| ● | Risks relating to our approach to the discovery and development of drug candidates and the lengthy, expensive and uncertain clinical development process |

10

| ● | Risks relating to expediting regulatory review, obtaining and maintaining regulatory approval and ongoing regulatory review for our drug candidates |

| ● | Risks relating to the commercialization of our drug candidates |

| ● | Risks relating to undesirable side effects of our drug candidates |

| ● | Risks relating to competition in discovering, developing and commercializing drugs |

| ● | Risks relating to our collaboration partners with respect to clinical trials, marketing and distribution |

| ● | Risks relating to our international operations |

Risks Relating to Sales of Our Internally Developed Drugs and Other Drugs

| ● | Risks relating to obtaining and maintaining permits and licenses for our and our joint ventures’ pharmaceutical operations in China |

| ● | Risks relating to leveraging our Other Ventures’ prescription drug business to commercialize our internally developed drug candidates |

| ● | Risks relating to competition in selling our approved, internally developed drugs and drugs of our Other Ventures |

| ● | Risks relating to maintaining and enhancing the brand recognition of our drugs |

| ● | Risks relating to the availability of reimbursement of our drugs, the lack of which could diminish our sales or profitability |

| ● | Risks relating to counterfeit products in China |

| ● | Risks relating to rapid changes in the pharmaceutical industry rendering our products obsolete |

| ● | Risks relating to cultivating or sourcing raw materials |

| ● | Risks relating to adverse publicity of us, our collaboration partners, our joint ventures or our products |

Risks Relating to Our Dependence on Third Parties

| ● | Risks relating to disagreements with current or future collaboration partners which we rely on for certain drug development activities including the conducting of clinical trials, manufacturing and commercialization of our medicines |

| ● | Risks relating to relying on third party suppliers for the active pharmaceutical ingredients in our drug candidate and drug products |

| ● | Risks relating to our collaboration partners or our CROs’ failure to comply with regulatory requirements pertaining to clinical trials |

| ● | Risks relating to our collaboration partners, principal investigators, CROs and other third-party contractors and consultants engaging in misconduct or other improper activities |

| ● | Risks relating to relying on distributors for logistics and distributions services |

| ● | Risks relating to the availability of benefits currently enjoyed by virtue of our association with CK Hutchison |

11

Other Risks and Risks Relating to Doing Business in China

| ● | Risks relating to compliance with privacy and cybersecurity laws, information security policies and contractual obligations related to data privacy and security and any information technology or data security failures |

| ● | Risks relating to product liability claims or lawsuits |

| ● | Risks relating to liabilities under anti-corruption laws, environmental, health and safety laws and laws relating to equity incentive plans |

| ● | Risks relating to changes in laws, regulations and policies in China and uncertainties with respect to the PRC legal system, China’s currency exchange limits and PRC government tax incentives or treatment |

Risks Relating to Intellectual Property

| ● | Risks relating to our, our joint ventures and our collaboration partners’ abilities to protect and enforce intellectual property rights and maintain confidentiality of trade secrets |

| ● | Risks relating to infringing upon third parties’ intellectual property rights |

Risks Relating to our ADSs

| ● | Risks relating to being delisted from the Nasdaq if the PCAOB is unable to inspect or investigate completely auditors located in China in the future |

| ● | Risks relating to our largest shareholder which may limit the ability of other shareholders to influence corporate matters |

You should carefully consider the following risk factors in addition to the other information set forth in this annual report. If any of the following risks were actually to occur, our company’s business, financial condition and results of operations prospects could be adversely affected and the value of our ADSs would likely suffer.

12

Risks Relating to Our Financial Position and Need for Capital

We may need substantial additional funding for our product development programs and commercialization efforts. If we are unable to raise capital on acceptable terms when needed, we could incur losses and be forced to delay, reduce or eliminate such efforts.

We expect to incur significant expenses in connection with our ongoing activities, particularly as we or our collaboration partners advance the clinical development of our clinical drug candidates which are currently in active or completed clinical studies in various countries. We will incur significant expenses as we continue research and development and initiate additional clinical trials of, and seek regulatory approval for, these and other future drug candidates. In addition, we have incurred and expect to continue to incur significant commercialization expenses related to product manufacturing, marketing, sales and distribution in China for surufatinib (marketed as Sulanda), our unpartnered drug product approved in China in December 2020, and any of our other unpartnered drug candidates that may be approved in the future. For example, the costs that may be required for the manufacture of any drug candidate that receives regulatory approval may be substantial as we may have to modify or increase the production capacity at our current manufacturing facilities or contract with third-party manufacturers. We may also incur expenses as we create additional infrastructure to support the research and development, commercialization and manufacturing of our drug products and candidates.

As a result, we have experienced negative cash flows from operations in the past. Our net cash used in operating activities was $204.2 million and $268.6 million for the years ended December 31, 2021 and 2022, respectively. Even though we generated significant amount of net cash of $219.3 million from our operating activities in 2023, this may not continue in the future as it depends on a variety of factors, including but not limited to:

| ● | the number and development requirements of the drug candidates we pursue; |

| ● | the scope, progress, timing, results and costs of researching and developing our drug candidates, and conducting pre-clinical and clinical trials; |

| ● | the cost, timing and outcome of regulatory review of our drug candidates; |

| ● | the cost and timing of commercialization activities, including product manufacturing, marketing, sales and distribution, for our drug candidates for which we have received regulatory approval; |

| ● | the amount and timing of any upfront milestone or royalty payments, service payments and reimbursement of manufacturing costs from our collaboration partners, with whom we cooperate with respect to the development and potential commercialization of certain of our drug candidates; |

| ● | the cash received from commercial sales of drug candidates for which we have received regulatory approval; |

| ● | our ability to establish and maintain strategic partnerships, collaboration, licensing or other arrangements and the financial terms of such agreements; and |

| ● | the cost, timing and outcome of preparing, filing and prosecuting patent applications, maintaining and enforcing our intellectual property rights and defending any intellectual property-related claims. |

Accordingly, we may need to obtain substantial funding in connection with our continuing operations through public or private equity offerings, debt financings, collaborations or licensing arrangements or other sources. If we are unable to raise capital when needed or on attractive terms to supplement the cash generated from operating activities to support our operations, we could incur losses and be forced to delay, reduce or eliminate our research and development programs or any future commercialization efforts.

13

Raising capital may dilute our shareholders, restrict our operations or require us to relinquish rights to technologies or drug candidates.

We expect to finance our cash needs in part through cash flow from our operations, and we may also rely on raising capital through a combination of public or private equity offerings, debt financings and/or license and development agreements with collaboration partners. In addition, we may seek capital due to favorable market conditions or strategic considerations, even if we believe we have sufficient funds for our current or future operating plans. To the extent that we raise capital through the sale of equity or convertible debt securities (including potential further listings on other stock exchanges), the ownership interest of our shareholders may be materially diluted, and the terms of such securities could include liquidation or other preferences that adversely affect the rights of our existing shareholders. Debt financing and preferred equity financing, if available, may involve agreements that include restrictive covenants that limit our ability to take specified actions, such as incurring additional debt, making capital expenditures or declaring dividends. Additional debt financing would also result in increased fixed payment obligations.

In addition, if we raise funds through collaborations, strategic partnerships or marketing, distribution or licensing arrangements with third parties, we may have to relinquish valuable rights to our technologies, future revenue streams, research programs or drug candidates or grant licenses on terms that may not be favorable to us. We may also lose control of the development of drug candidates, such as the pace and scope of clinical trials, as a result of such third-party arrangements. If we are unable to raise funds through equity or debt financings when needed, we may be required to delay, limit, reduce or terminate our product development or future commercialization efforts or grant rights to develop and market drug candidates that we would otherwise prefer to develop and market ourselves.

Our existing and any future indebtedness could adversely affect our ability to operate our business.

Our outstanding indebtedness combined with current and future financial obligations and contractual commitments, including any additional indebtedness beyond our current loan facilities could have significant adverse consequences, including:

| ● | requiring us to dedicate a portion of our cash resources to the payment of interest and principal, and prepayment and repayment fees and penalties, thereby reducing money available to fund working capital, capital expenditures, product development and other general corporate purposes; |

| ● | increasing our vulnerability to adverse changes in general economic, industry and market conditions; |

| ● | subjecting us to restrictive covenants that may reduce our ability to take certain corporate actions or obtain further debt or equity financing; |

| ● | limiting our flexibility in planning for, or reacting to, changes in our business and the industry in which we compete; and |

| ● | placing us at a competitive disadvantage compared to our competitors that have less debt or better debt servicing options. |

We intend to satisfy our current and future debt service obligations with our existing cash and cash equivalents and short-term investments. Nevertheless, we may not have sufficient funds, and may be unable to arrange for financing, to pay the amounts due under our existing debt. Failure to make payments or comply with other covenants under our existing debt instruments could result in an event of default and acceleration of amounts due.

We have historically incurred significant net operating cash outflows, and may continue to experience net cash outflow from operating activities.

Investment in biopharmaceutical drug development is highly speculative. It entails substantial upfront expenditures and significant risk that a drug candidate might fail to gain regulatory approval or become commercially viable. Therefore, we expect to continue to incur significant expenses related to our ongoing operations, particularly research and development expenses, for the foreseeable future as we expand our development of, and seek regulatory approvals for, our drug candidates. We have historically generated net cash outflows from operations in 2021 and 2022. Although our net cash from operations turned positive in 2023, there is no guarantee that we will be able to continue to do so in the future as our operating cash flows depend on a number of variables that we may not be able to accurately predict or fully control, including the number and scope of our drug development programs and the associated cost of those programs, the cost of commercializing any approved products, our ability to generate revenue and the timing and amount of milestones and other payments we make or receive through arrangements with third parties. Our failure to generate positive cash flow from operations may adversely affect our ability to raise capital, maintain our research and development efforts, expand our business or continue our operations.

14

We face risks with our short-term investments and in collecting our accounts receivables.

Our short-term investments are bank deposits with maturities of more than three months but less than one year. Our short-term investments were $317.7 million and $602.7 million as of December 31, 2022 and 2023, respectively, and are placed with major financial institutions. These investments may earn yields substantially lower than expected. Failure to realize the benefits we expected from these investments may materially and adversely affect our business and financial results. To date, we have experienced no loss or lack of access to our invested cash or cash equivalents; however, we can provide no assurance that access to our invested cash and cash equivalents will not be impacted by adverse conditions in the financial and credit markets.

Our accounts receivable balance, net of allowance for credit losses, totaled $98.0 million and $116.9 million as of December 31, 2022 and 2023, respectively. We have policies and procedures in place to ensure that sales are made to customers with an appropriate credit history. We perform periodic credit evaluations of our customers and monitor risk factors and forward-looking information, such as country risk, when determining credit limits for customers. However, there can be no assurance such policies and procedures will effectively limit our credit risk and enable us to avoid losses, which could adversely affect our financial condition and results of operations. In addition, amounts due to us are not covered by collateral or credit insurance. If we fail to collect all or part of such accounts receivable in a timely manner, or at all, our financial condition may be materially and adversely affected.

Risks Relating to Our Oncology/Immunology Operations and Development of Our Drug Candidates

Our Oncology/Immunology operations historically operated at a net loss, and our future profitability is dependent on the performance of our Oncology/Immunology operations which rely on the successful commercialization of our drug candidates.

To date, savolitinib, fruquintinib and surufatinib (marketed as Orpathys, Elunate and Sulanda, respectively in China and in the U.S. for fruquintinib as Fruzaqla) are our only internally developed drug candidates that have been approved for sale. We do not expect our Oncology/Immunology operations to be significantly profitable unless and until we consistently generate substantial revenue from them and can successfully commercialize our other drug products.

Successful commercialization of our drug candidates is subject to many risks. Savolitinib is marketed as Orpathys in collaboration with our partner, AstraZeneca. We have partnered with Eli Lilly and Takeda on the commercialization of fruquintinib. Surufatinib is marketed by us as Sulanda without the support of a collaboration partner. Savolitinib, fruquintinib and surufatinib are the first innovative oncology drugs we, as an organization, have commercialized, and there is no guarantee that we or our collaboration partners will be able to successfully commercialize them or any of our other drug candidates for their approved indications. There are numerous examples of failures to meet expectations of market potential, including by pharmaceutical companies with more experience and resources than us. There are many factors that could cause the commercialization of savolitinib, fruquintinib and surufatinib or our other drug products to be unsuccessful, including a number of factors that are outside our control. In the case of fruquintinib, for example, the third-line metastatic colorectal cancer, or mCRC, patient population in China may be smaller than we estimate or physicians may be unwilling to prescribe, or patients may be unwilling to take, fruquintinib for a variety of reasons. Additionally, any negative development for fruquintinib, surufatinib or savolitinib in clinical development in additional indications, or in regulatory processes in other jurisdictions, may adversely impact the commercial results and potential of savolitinib, fruquintinib and surufatinib in China and globally. For example, in April 2022, the FDA issued a Complete Response Letter regarding the NDA for surufatinib for the treatment of non-pancreatic neuroendocrine tumors (NETs) and pancreatic NETs and determined that the data package submitted did not support an approval in the U.S. at the time. We subsequently withdrew our submissions to the FDA and the EMA for surufatinib. Thus, significant uncertainty remains regarding the commercial potential of savolitinib, fruquintinib and surufatinib.

Although our operations were profitable in 2023, we may not continue to achieve profitability based on the revenue to be generated from savolitinib, fruquintinib and surufatinib and/or our other drug candidates, if ever. If the commercialization of savolitinib, fruquintinib, surufatinib and/or our other drug candidates is unsuccessful or perceived as disappointing, our stock price could decline significantly and the long-term success of the product and our company could be harmed.

15

All of our drug candidates are still in development. If we are unable to obtain regulatory approval and ultimately commercialize our drug candidates, or if we experience significant delays in doing so, our business will be materially harmed.

All of our drug candidates are still in development, including those that have already received approval for the treatment of certain indications in China and United States. Although we may receive payments from our collaboration partners, including upfront payments and payments for achieving development, regulatory or commercial milestones, for certain of our drug candidates, our ability to generate significant revenue from our drug candidates is dependent on their receipt of additional regulatory approval and successful commercialization, which may never occur. Each of our drug candidates in development will require additional pre-clinical and/or clinical trials, regulatory approval in multiple jurisdictions, and substantial investment in manufacturing and significant efforts before we generate significant revenue from product sales. The success of our drug candidates will depend on several factors, including the following:

| ● | successful completion of additional pre-clinical and/or clinical trials; |

| ● | successful enrollment in, and completion of, additional clinical trials; |

| ● | receipt of additional regulatory approvals from applicable regulatory authorities for planned clinical trials, future clinical trials, drug registrations or post-approval trials; |

| ● | successful completion of all studies required to obtain regulatory approval and/or fulfillment of post-approval requirements in the United States, China, Europe, Japan and other jurisdictions for our drug candidates; |

| ● | adapting our commercial manufacturing capabilities to the specifications for our drug candidates for clinical supply and commercial manufacturing; |

| ● | obtaining and maintaining patent and trade secret protection or regulatory exclusivity for our drug candidates; |

| ● | launching commercial sales of our drug candidates, if and when approved, whether alone or in collaboration with others; |

| ● | acceptance of the drug candidates, if and when approved, by patients, the medical community and third-party payors; |

| ● | effectively competing with other therapies; |

| ● | obtaining and maintaining healthcare coverage and adequate reimbursement; |

| ● | enforcing and defending intellectual property rights and claims; and |

| ● | maintaining a continued acceptable safety profile of the drug candidates following approval. |

If we do not achieve one or more of these factors in a timely manner or at all, we could experience significant delays or an inability to successfully commercialize our drug candidates, which would materially harm our business.

Our primary approach to the discovery and development of drug candidates focuses on the inhibition of kinases, some of which are unproven.

A primary focus of our research and development efforts is on identifying kinase targets for which drug compounds previously developed by others affecting those targets have been unsuccessful due to limited selectivity, off-target toxicity and other problems. We then work to engineer drug candidates which have the potential to have superior efficacy, safety and other features as compared to such prior drug compounds. We also focus on developing drug compounds with the potential to be global best-in-class/next-generation therapies for validated kinase targets.

16

Even if we are able to develop compounds that successfully target the relevant kinases in pre-clinical studies, we may not succeed in demonstrating safety and efficacy of the drug candidates in clinical trials. Even if we are able to demonstrate safety and efficacy of compounds in certain indications in certain jurisdictions, we may not succeed in demonstrating the same in other indications or in the same indications in other jurisdictions. As a result, our efforts may not result in the discovery or development of drugs that are commercially viable or superior to existing drugs or other therapies on the market. While the results of pre-clinical studies, early-stage clinical trials as well as clinical trials in certain indications have suggested that certain of our drug candidates may successfully inhibit kinases and may have significant utility in several cancer indications, potentially in combination with other cancer drugs, chemotherapy and immunotherapies, we have not yet demonstrated efficacy and safety for many of our drug candidates in later stage clinical trials.

We may expend our limited resources to pursue a particular drug candidate or indication and fail to capitalize on drug candidates or indications that may be more profitable or for which there is a greater likelihood of success.

Because we have limited financial and managerial resources, we must limit our research programs to specific drug candidates that we identify for specific indications. As a result, we may forego or delay pursuit of opportunities with other drug candidates or for other indications that later prove to have greater commercial potential. Our resource allocation decisions may cause us to fail to capitalize on viable commercial drugs or profitable market opportunities. In addition, if we do not accurately evaluate the commercial potential or target market for a particular drug candidate, we may relinquish valuable rights to that drug candidate through collaboration, licensing or other royalty arrangements when it would have been more advantageous for us to retain sole development and commercialization rights to such drug candidate.

The regulatory approval processes of the U.S. Food and Drug Administration, or FDA, National Medical Products Administration of China, or NMPA, EMA, PDMA and comparable authorities in other countries are lengthy, time consuming and inherently unpredictable, and if we are ultimately unable to obtain regulatory approval for our drug candidates, our ability to generate revenue will be materially impaired.

Our drug candidates and the activities associated with their development and commercialization, including their design, testing, manufacture, safety, efficacy, recordkeeping, labeling, storage, approval, advertising, promotion, sale, distribution, import and export, are subject to comprehensive regulation by the FDA, NMPA, EMA, PDMA and other regulatory agencies in the United States, China, Europe, Japan and by comparable regulatory authorities in other countries. Securing regulatory approval requires the submission of extensive pre-clinical and clinical data and supporting information to the various regulatory authorities for each therapeutic indication to establish the drug candidate’s safety and efficacy. Securing regulatory approval also requires the submission of information about the drug manufacturing process to, and inspection of manufacturing facilities by, the relevant regulatory authority. Our drug candidates may not be effective, may be only moderately effective or may prove to have undesirable or unintended side effects, toxicities or other characteristics that may preclude our obtaining regulatory approval or prevent or limit commercial use.

The process of obtaining regulatory approvals in the United States, China, Europe, Japan and other countries is expensive, may take many years if additional clinical trials are required, if approval is obtained at all, and can vary substantially based upon a variety of factors, including the type, complexity and novelty of the drug candidates involved. Changes in regulatory approval policies during the development period, changes in or the enactment of additional statutes or regulations, or changes in regulatory review for each submitted New Drug Application, or NDA, pre-market approval or equivalent application types, may cause delays in the approval or rejection of an application. The FDA, NMPA, EMA, PDMA and comparable regulatory authorities in other countries have substantial discretion in the approval process and may refuse to accept any application or may decide that our data are insufficient for approval and require additional pre-clinical, clinical or other studies. Our drug candidates could be delayed in receiving, or fail to receive, regulatory approval for many reasons, including the following:

| ● | the FDA, NMPA, EMA, PDMA or comparable regulatory authorities may disagree with the number, design, size, conduct or implementation of our clinical trials; |

| ● | we may be unable to demonstrate to the satisfaction of the FDA, NMPA, EMA, PDMA or comparable regulatory authorities that a drug candidate is safe and effective for its proposed indication; |

| ● | the results of clinical trials may not meet the level of statistical significance required by the FDA, NMPA, EMA, PDMA or comparable regulatory authorities for approval; |

| ● | we may be unable to demonstrate that a drug candidate’s clinical and other benefits outweigh its safety risks; |

17

| ● | the FDA, NMPA, EMA, PDMA or comparable regulatory authorities may disagree with our interpretation of data from pre-clinical studies or clinical trials; |

| ● | the data collected from clinical trials of our drug candidates may not be sufficient to support the submission of an NDA or other submission or to obtain regulatory approval in the United States or elsewhere; |

| ● | the FDA, NMPA, EMA, PDMA or comparable regulatory authorities may fail to approve the manufacturing processes for our clinical and commercial supplies; |

| ● | the approval policies or regulations of the FDA, NMPA, EMA, PDMA or comparable regulatory authorities may significantly change in a manner rendering our clinical data insufficient for approval; |

| ● | the FDA, NMPA, EMA, PDMA or comparable regulatory authority may prioritize treatments for emerging health crises, such as COVID-19, resulting in delays for our drug candidates; |

| ● | the FDA, NMPA, EMA, PDMA or comparable regulatory authorities may restrict the use of our products to a narrow population; and |

| ● | our collaboration partners or CROs that are retained to conduct the clinical trials of our drug candidates may take actions that materially and adversely impact the clinical trials. |

In addition, even if we were to obtain approval, regulatory authorities may approve any of our drug candidates for fewer or more limited indications than we request, may not approve the price we intend to charge for our drugs, may grant approval contingent on the performance of costly post-marketing clinical trials, or may approve a drug candidate with a label that does not include the labeling claims necessary or desirable for the successful commercialization of that drug candidate. Any of the foregoing scenarios could materially harm the commercial prospects for our drug candidates.

Furthermore, even though the NMPA has granted approval for fruquintinib and surufatinib for use in third-line mCRC and NET patients, respectively, and approval for savolitinib for lung cancer with MET exon 14 skipping alterations, we are still subject to substantial, ongoing regulatory requirements. See “—Even if we receive regulatory approval for our drug candidates, we are subject to ongoing obligations and continued regulatory review, which may result in significant additional expense.”

If the FDA, NMPA, EMA, PDMA or another regulatory agency revokes its approval of, or if safety, efficacy, manufacturing or supply issues arise with, any therapeutic that we use in combination with our drug candidates, we may be unable to market such drug candidate or may experience significant regulatory delays or supply shortages, and our business could be materially harmed.

We are currently developing combination therapies using our savolitinib, fruquintinib, surufatinib and other drug candidates with various immunotherapies, targeted therapies and/or other therapies. For example, we are currently developing savolitinib in combination with immunotherapy (Imfinzi) and targeted therapy (Tagrisso). However, we did not develop and we do not manufacture or sell Imfinzi, Tagrisso or any other therapeutic we use in combination with our drug candidates. We may also seek to develop our drug candidates in combination with other therapeutics in the future.

If the FDA, NMPA, EMA, PDMA or another regulatory agency revokes its approval, or does not grant approval, of any of these and other therapeutics we use in combination with our drug candidates, we will not be able to market our drug candidates in combination with such therapeutics. If safety or efficacy issues arise with these or other therapeutics that we seek to combine with our drug candidates in the future, we may experience significant regulatory delays, and we may be required to redesign or terminate the applicable clinical trials. In addition, if manufacturing or other issues result in a supply shortage of these or any other combination therapeutics, we may not be able to complete clinical development of savolitinib, fruquintinib, surufatinib and/or any other of our drug candidates on our current timeline or at all.

Even if one or more of our drug candidates were to receive regulatory approval for use in combination with a therapeutic, we would continue to be subject to the risk that the FDA, NMPA, EMA, PDMA or another regulatory agency could revoke its approval of the combination therapeutic, or that safety, efficacy, manufacturing or supply issues could arise with one of these combination therapeutics. This could result in savolitinib, fruquintinib, surufatinib or one of our other products being removed from the market or being less successful commercially.

18

We face substantial competition, and our competitors may discover, develop or commercialize drugs before or more successfully than we do.

The development and commercialization of new drugs is highly competitive. We face competition with respect to our current drug candidates, and will face competition with respect to any drug candidates that we may seek to develop or commercialize in the future, from major pharmaceutical companies, specialty pharmaceutical companies and biotechnology companies worldwide. There are a number of large pharmaceutical and biotechnology companies that currently market drugs or are pursuing the development of therapies in the field of kinase inhibition for cancer and other diseases. Some of these competitive drugs and therapies are based on scientific approaches that are the same as or similar to our approach, and others are based on entirely different approaches. Potential competitors also include academic institutions, government agencies and other public and private research organizations that conduct research, seek patent protection and establish collaborative arrangements for research, development, manufacturing and commercialization. Specifically, there are a large number of companies developing or marketing treatments for cancer and immunological diseases, including many major pharmaceutical and biotechnology companies.

Many of the companies against which we are competing or against which we may compete in the future have significantly greater financial resources and expertise in research and development, manufacturing, pre-clinical testing, conducting clinical trials, obtaining regulatory approvals and marketing approved drugs than we do. Mergers and acquisitions in the pharmaceutical, biotechnology and diagnostic industries may result in even more resources being concentrated among a smaller number of our competitors. Smaller or early-stage companies may also prove to be significant competitors, particularly through collaborative arrangements with large and established companies. These competitors also compete with us in recruiting and retaining qualified scientific and management personnel and establishing clinical trial sites and patient registration for clinical trials, as well as in acquiring technologies complementary to, or necessary for, our programs.

Our commercial opportunity could be reduced or eliminated if our competitors develop and commercialize drugs that are safer, more effective, have fewer or less severe side effects, are more convenient or are less expensive than any drugs that we or our collaborators may develop. Our competitors also may obtain FDA, NMPA, EMA, PDMA or other regulatory approval for their drugs more rapidly than we may obtain approval for ours, which could result in our competitors establishing a strong market position before we or our collaborators are able to enter the market. The key competitive factors affecting the success of all of our drug candidates, if approved, are likely to be their efficacy, safety, convenience, price, the level of generic competition and the availability of reimbursement from government and other third-party payors.

Clinical development involves a lengthy and expensive process with an uncertain outcome.

There is a risk of failure for each of our drug candidates. It is difficult to predict when or if any of our drug candidates will prove effective and safe in humans or will receive regulatory approval. Before obtaining regulatory approval from regulatory authorities for the sale of any drug candidate, we or our collaboration partners must complete pre-clinical studies and then conduct extensive clinical trials to demonstrate the safety and efficacy of our drug candidates in humans. Clinical testing is expensive, difficult to design and implement and can take many years to complete. The outcomes of pre-clinical development testing and early clinical trials may not be predictive of the success of later clinical trials, and interim results of a clinical trial do not necessarily predict final results. Moreover, pre-clinical and clinical data are often susceptible to varying interpretations and analyses, and many companies that have believed their drug candidates performed satisfactorily in pre-clinical studies and clinical trials have nonetheless failed to obtain regulatory approval of their drug candidates. Our current or future clinical trials may not be successful.

Commencing each of our clinical trials is subject to finalizing the trial design based on ongoing discussions with the FDA, NMPA, EMA, PDMA or other regulatory authorities. The FDA, NMPA, EMA, PDMA and other regulatory authorities could change their position on the acceptability of our trial designs or clinical endpoints, which could require us to complete additional clinical trials or impose approval conditions that we do not currently expect. Successful completion of our clinical trials is a prerequisite to submitting an NDA or analogous filing to the FDA, NMPA, EMA, PDMA or other regulatory authorities for each drug candidate and, consequently, the ultimate approval and commercial marketing of our drug candidates. We do not know whether any of our clinical trials will begin or be completed on schedule, if at all.

19

We and our collaboration partners may incur additional costs or experience delays in completing our pre-clinical or clinical trials, or ultimately be unable to complete the development and commercialization of our drug candidates.

We and our collaboration partners, including AstraZeneca, Eli Lilly, Takeda, BeiGene Ltd., or BeiGene, Inmagene, Innovent Biologics (Suzhou) Co., Inc., or Innovent, Genor Biopharma Co. Ltd., or Genor, Shanghai Junshi Biosciences Co. Ltd., or Junshi and Epizyme, Inc. (a subsidiary of Ipsen Pharma SAS), or Epizyme may experience delays in completing our pre-clinical or clinical trials, and numerous unforeseen events could arise during, or as a result of, future clinical trials, which could delay or prevent us from receiving regulatory approval, including:

| ● | regulators, institutional review boards, or IRBs, ethics committees or the China Human Genetic Resources Administration Office may not authorize us or our investigators to commence or conduct a clinical trial at a prospective trial site; |

| ● | we may experience delays in reaching, or we may fail to reach, agreement on acceptable terms with prospective trial sites and prospective CROs, who conduct clinical trials on behalf of us and our collaboration partners, the terms of which can be subject to extensive negotiation and may vary significantly among different CROs and trial sites; |

| ● | clinical trials may produce negative or inconclusive results, and we or our collaboration partners may decide, or regulators may require us or them, to conduct additional clinical trials or we may decide to abandon drug development programs; |