UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

____________________________

FORM 10-Q

_____________________________

(Mark One)

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended June 30, 2023

Or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission file number: 001-37524

_____________________________

(Exact name of registrant as specified in its charter)

_____________________________

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

| (Address of principal executive offices) | (Zip Code) | ||||

(336 ) 841-0300

(Registrant’s telephone number, including area code)

(Former name, former address and former fiscal year, if changed since last report)

_____________________________

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | Accelerated filer | o | |||||||||||

| o | Smaller reporting company | |||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

| Class of Stock | Shares Outstanding as of August 11, 2023 | |||||||

| Class A common stock, par value $0.01 per share | ||||||||

| Class B common stock, par value $0.01 per share | ||||||||

vTv THERAPEUTICS INC. AND SUBSIDIARIES

INDEX TO FORM 10-Q

FOR THE QUARTER ENDED JUNE 30, 2023

| PAGE NUMBER | ||||||||

2

PART I – FINANCIAL INFORMATION

The financial statements and other disclosures contained in this report include those of vTv Therapeutics Inc. (“we”, the “Company” or the “Registrant”), which is the registrant, and those of vTv Therapeutics LLC (“vTv LLC”), which is the principal operating subsidiary of the Registrant. Unless the context suggests otherwise, references in this Quarterly Report on Form 10-Q to the “Company”, “we”, “us” and “our” refer to vTv Therapeutics Inc. and its consolidated subsidiaries.

3

vTv Therapeutics Inc.

Condensed Consolidated Balance Sheets

(in thousands, except number of shares and per share data)

| June 30, 2023 | December 31, 2022 | ||||||||||

| (Unaudited) | |||||||||||

| Assets | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Accounts receivable | |||||||||||

| G42 Promissory Note receivable | |||||||||||

| Prepaid expenses and other current assets | |||||||||||

| Current deposits | |||||||||||

| Total current assets | |||||||||||

| Property and equipment, net | |||||||||||

| Operating lease right-of-use assets | |||||||||||

| Long-term investments | |||||||||||

| Total assets | $ | $ | |||||||||

| Liabilities, Redeemable Noncontrolling Interest and Stockholders’ Deficit | |||||||||||

| Current liabilities: | |||||||||||

| Accounts payable and accrued expenses | $ | $ | |||||||||

| Current portion of operating lease liabilities | |||||||||||

| Current portion of contract liabilities | |||||||||||

| Current portion of notes payable | |||||||||||

| Total current liabilities | |||||||||||

| Contract liabilities, net of current portion | |||||||||||

| Operating lease liabilities, net of current portion | |||||||||||

| Warrant liability, related party | |||||||||||

| Total liabilities | |||||||||||

| Commitments and contingencies | |||||||||||

| Redeemable noncontrolling interest | |||||||||||

| Stockholders’ deficit: | |||||||||||

Class A common stock, $ | |||||||||||

Class B common stock, $ | |||||||||||

| Additional paid-in capital | |||||||||||

| Accumulated deficit | ( | ( | |||||||||

| Total stockholders’ deficit attributable to vTv Therapeutics Inc. | ( | ( | |||||||||

| Total liabilities, redeemable noncontrolling interest and stockholders’ deficit | $ | $ | |||||||||

The accompanying notes are an integral part of the unaudited condensed consolidated financial statements.

4

vTv Therapeutics Inc.

Condensed Consolidated Statements of Operations - Unaudited

(in thousands, except number of shares and per share data)

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| Revenue | $ | $ | $ | $ | |||||||||||||||||||

| Operating expenses: | |||||||||||||||||||||||

| Research and development | |||||||||||||||||||||||

| General and administrative | |||||||||||||||||||||||

| Total operating expenses | |||||||||||||||||||||||

| Operating loss | ( | ( | ( | ( | |||||||||||||||||||

| Other income (expense), net | ( | ( | |||||||||||||||||||||

| Other income – related party | |||||||||||||||||||||||

| Interest income | |||||||||||||||||||||||

| Interest expense | ( | ( | ( | ||||||||||||||||||||

| Loss before income taxes and noncontrolling interest | ( | ( | ( | ( | |||||||||||||||||||

| Income tax provision | |||||||||||||||||||||||

| Net loss before noncontrolling interest | ( | ( | ( | ( | |||||||||||||||||||

| Less: net loss attributable to noncontrolling interest | ( | ( | ( | ( | |||||||||||||||||||

| Net loss attributable to vTv Therapeutics Inc. | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Net loss attributable to vTv Therapeutics Inc. common shareholders | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Net loss per share of vTv Therapeutics Inc. Class A common stock, basic and diluted | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Weighted average number of vTv Therapeutics Inc. Class A common stock, basic and diluted | |||||||||||||||||||||||

The accompanying notes are an integral part of the unaudited condensed consolidated financial statements.

5

vTv Therapeutics Inc.

Condensed Consolidated Statement of Changes in Redeemable Noncontrolling Interest and Stockholders’ Deficit - Unaudited

(in thousands, except number of shares)

| For the three months ended June 30, 2023 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Class A Common Stock | Class B Common Stock | |||||||||||||||||||||||||||||||||||||||||||||||||

| Redeemable Noncontrolling Interest | Shares | Amount | Shares | Amount | Additional Paid-in Capital | Accumulated Deficit | Total Stockholders' Deficit | |||||||||||||||||||||||||||||||||||||||||||

| Balances at March 31, 2023 | $ | $ | $ | $ | $ | ( | $ | ( | ||||||||||||||||||||||||||||||||||||||||||

| Net loss | ( | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||||||||||

| Share-based compensation | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||

| Change in redemption value of noncontrolling interest | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||||||

| Balances at June 30, 2023 | $ | $ | $ | $ | $ | ( | $ | ( | ||||||||||||||||||||||||||||||||||||||||||

| For the three months ended June 30, 2022 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Class A Common Stock | Class B Common Stock | |||||||||||||||||||||||||||||||||||||||||||||||||

| Redeemable Noncontrolling Interest | Shares | Amount | Shares | Amount | Additional Paid-in Capital | Accumulated Deficit | Total Stockholders' Deficit | |||||||||||||||||||||||||||||||||||||||||||

| Balances at March 31, 2022 | $ | $ | $ | $ | $ | ( | $ | ( | ||||||||||||||||||||||||||||||||||||||||||

| Net loss | ( | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||||||||||

| Share-based compensation | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||

| Issuance of Class A common stock to collaboration partner | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||

| Change in redemption value of noncontrolling interest | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||||||

| Balances at June 30, 2022 | $ | $ | $ | $ | $ | ( | $ | ( | ||||||||||||||||||||||||||||||||||||||||||

The accompanying notes are an integral part of the unaudited condensed consolidated financial statements.

6

vTv Therapeutics Inc.

Condensed Consolidated Statement of Changes in Redeemable Noncontrolling Interest and Stockholders’ Deficit - Unaudited

(in thousands, except number of shares)

| For the six months ended June 30, 2023 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Class A Common Stock | Class B Common Stock | |||||||||||||||||||||||||||||||||||||||||||||||||

| Redeemable Noncontrolling Interest | Shares | Amount | Shares | Amount | Additional Paid-in Capital | Accumulated Deficit | Total Stockholders' Deficit | |||||||||||||||||||||||||||||||||||||||||||

| Balances at December 31, 2022 | $ | $ | $ | $ | $ | ( | $ | ( | ||||||||||||||||||||||||||||||||||||||||||

| Net loss | ( | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||||||||||

| Share-based compensation | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||

| Change in redemption value of noncontrolling interest | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||||||

| Balances at June 30, 2023 | $ | $ | $ | $ | $ | ( | $ | ( | ||||||||||||||||||||||||||||||||||||||||||

| For the six months ended June 30, 2022 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Class A Common Stock | Class B Common Stock | |||||||||||||||||||||||||||||||||||||||||||||||||

| Redeemable Noncontrolling Interest | Shares | Amount | Shares | Amount | Additional Paid-in Capital | Accumulated Deficit | Total Stockholders' Deficit | |||||||||||||||||||||||||||||||||||||||||||

| Balances at December 31, 2021 | $ | $ | $ | $ | $ | ( | $ | ( | ||||||||||||||||||||||||||||||||||||||||||

| Net loss | ( | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||||||||||

| Share-based compensation | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||

| Issuance of Class A common stock to collaboration partner | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||

| Change in redemption value of noncontrolling interest | ( | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||

| Balances at June 30, 2022 | $ | $ | $ | $ | $ | ( | $ | ( | ||||||||||||||||||||||||||||||||||||||||||

The accompanying notes are an integral part of the unaudited condensed consolidated financial statements.

7

vTv Therapeutics Inc.

Condensed Consolidated Statements of Cash Flows - Unaudited

(in thousands)

| Six Months Ended June 30, | |||||||||||

| 2023 | 2022 | ||||||||||

| Cash flows from operating activities: | |||||||||||

| Net loss before noncontrolling interest | $ | ( | $ | ( | |||||||

| Adjustments to reconcile net loss before noncontrolling interest to net cash used in operating activities: | |||||||||||

| Depreciation expense | |||||||||||

| Loss from G42 Promissory Note early redemption | |||||||||||

| Non-cash interest income | ( | ( | |||||||||

| Share-based compensation expense | |||||||||||

| Change in fair value of investments | ( | ||||||||||

| Change in fair value of warrants, related party | ( | ( | |||||||||

| Changes in assets and liabilities: | |||||||||||

| Accounts receivable | ( | ||||||||||

| Prepaid expenses and other assets | |||||||||||

| Accounts payable and accrued expenses | |||||||||||

| Contract liabilities | |||||||||||

| Net cash used in operating activities | ( | ( | |||||||||

| Cash flows from investing activities: | |||||||||||

| Purchases of property and equipment | ( | ||||||||||

| Net cash used in investing activities | ( | ||||||||||

| Cash flows from financing activities: | |||||||||||

| Proceeds from G42 Promissory Note early redemption related to sale of Class A common stock to collaboration partner | |||||||||||

| Proceeds from sale of Class A common stock to collaboration partner, net of offering costs | |||||||||||

| Repayment of notes payable | ( | ( | |||||||||

| Net cash provided by financing activities | |||||||||||

| Net increase in cash and cash equivalents | |||||||||||

| Total cash and cash equivalents, beginning of period | |||||||||||

| Total cash and cash equivalents, end of period | $ | $ | |||||||||

| Non-cash activities: | |||||||||||

| Change in redemption value of noncontrolling interest | $ | $ | ( | ||||||||

| Notes receivable recorded at fair value from collaboration partner | |||||||||||

The accompanying notes are an integral part of the unaudited condensed consolidated financial statements.

8

vTv Therapeutics Inc.

Notes to Condensed Consolidated Financial Statements – Unaudited

(dollar amounts are in thousands, unless otherwise noted)

Note 1: Description of Business, Basis of Presentation and Going Concern

Description of Business

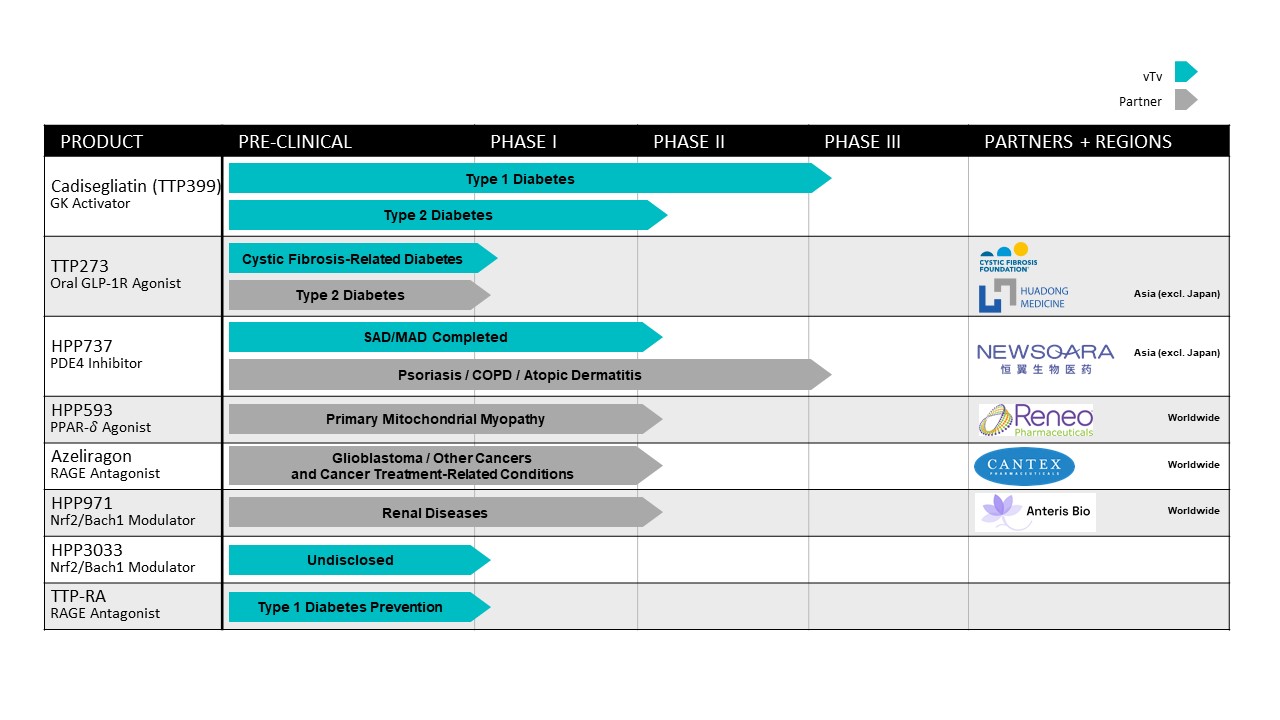

vTv Therapeutics Inc. (the “Company,” the “Registrant,” “we” or “us”) was incorporated in the state of Delaware in April 2015. The Company is a clinical stage pharmaceutical company focused on treating metabolic diseases to minimize their long-term complications through end-organ protection.

Principles of Consolidation

vTv Therapeutics Inc. is a holding company, and its principal asset is a controlling equity interest in vTv Therapeutics LLC (“vTv LLC”), the Company’s principal operating subsidiary, which is a clinical stage pharmaceutical company engaged in the discovery and development of orally administered small molecule drug candidates to fill significant unmet medical needs.

The Company has determined that vTv LLC is a variable-interest entity (“VIE”) for accounting purposes and that vTv Therapeutics Inc. is the primary beneficiary of vTv LLC because (through its managing member interest in vTv LLC and the fact that the senior management of vTv Therapeutics Inc. is also the senior management of vTv LLC) it has the power and benefits to direct all of the activities of vTv LLC, which include those that most significantly impact vTv LLC’s economic performance. vTv Therapeutics Inc. has therefore consolidated vTv LLC’s results pursuant to Accounting Standards Codification Topic 810, “Consolidation” in its Condensed Consolidated Financial Statements. Various holders own nonvoting interests in vTv LLC, representing a 22.1 % economic interest in vTv LLC, effectively restricting vTv Therapeutics Inc.’s interest to 77.9 % of vTv LLC’s economic results, subject to increase in the future, should vTv Therapeutics Inc. purchase additional nonvoting common units (“vTv Units”) of vTv LLC, or should the holders of vTv Units decide to exchange such units (together with shares of the Company’s Class B common stock, par value $0.01 (“Class B common stock”)) for shares of Class A common stock (or cash) pursuant to the Exchange Agreement (as defined in Note 9). vTv Therapeutics Inc. has provided financial and other support to vTv LLC in the form of its purchase of vTv Units with the net proceeds of the Company’s initial public offering (“IPO”) in 2015, its registered direct offering in March 2019, and its agreeing to be a co-borrower under the Venture Loan and Security Agreement (the “Loan Agreement”) with Horizon Technology Finance Corporation and Silicon Valley Bank (together, the “Lenders”) which was entered into in 2016. vTv Therapeutics Inc. entered into the letter agreements with MacAndrews and Forbes Group LLC (“M&F Group”), a related party and an affiliate of MacAndrews & Forbes Incorporated (together with its affiliates “MacAndrews”) in December 2017, July 2018, December 2018, March 2019, September 2019, and December 2019 (each a “Letter Agreement” and collectively, the “Letter Agreements”). In addition, vTv Therapeutics Inc. also entered into the Controlled Equity OfferingSM Sales Agreement (the “Sales Agreement”) with Cantor Fitzgerald & Co. (“Cantor Fitzgerald”) (the “ATM Offering”), the purchase agreement with Lincoln Park Capital Fund, LLC (“Lincoln Park”) (the “LPC Purchase Agreement”), the common stock purchase agreement with G42 Investments AI Holding RSC Ltd (“G42 Investments”) (the “G42 Purchase Agreement”) and the common stock and warrant purchase agreement with CinPax, LLC and CinRx, LLC, respectively (the “CinRx Purchase Agreement”). vTv Therapeutics Inc. will not be required to provide financial or other support for vTv LLC. However, vTv Therapeutics Inc. will control its business and other activities through its managing member interest in vTv LLC, and its management is the management of vTv LLC. Nevertheless, because vTv Therapeutics Inc. will have no material assets other than its interests in vTv LLC, any financial difficulties at vTv LLC could result in vTv Therapeutics Inc. recognizing a loss.

Going Concern and Liquidity

To date, the Company has not generated any product revenue and has not achieved profitable operations. The continuing development of our drug candidates will require additional financing. From its inception through June 30, 2023, the Company has funded its operations primarily through a combination of private placements of common and preferred equity, research collaboration agreements, upfront and milestone payments for license agreements, debt and equity financings and the completion of its IPO in August 2015. As of June 30, 2023, the Company had an accumulated deficit of $280.8 million and has generated net losses in each year of its existence.

As of June 30, 2023, the Company’s liquidity sources included cash and cash equivalents of $12.6 million. Based on our current operating plan, we believe that our current cash and cash equivalents will allow us to meet our liquidity requirements into the third quarter of 2023. To meet our future funding requirements into the second quarter of 2024,

9

including funding the ongoing and future clinical trials of cadisegliatin (TTP399), we are evaluating several financing strategies, including direct equity investments and the potential licensing and monetization of other Company programs.

The Company may also use its remaining availability of $37.3 million under its Sales Agreement with Cantor Fitzgerald pursuant to which the Company may offer and sell, from time to time shares of the Company’s Class A common stock and the ability to sell an additional 9,437,376 shares of Class A common stock under the LPC Purchase Agreement based on the remaining number of registered shares. However, the ability to use these sources of capital is dependent on a number of factors, including the prevailing market price of and the volume of trading in the Company’s Class A common stock. See Note 9 for further details.

If we are unable to raise additional capital as and when needed, or upon acceptable terms, such failure would have a significant negative impact on our financial condition. As such, these conditions raise substantial doubt about the Company’s ability to continue as a going concern.

The Company’s financial statements have been prepared assuming the Company will continue as a going concern, which contemplates, among other things, the realization of assets and satisfaction of liabilities in the normal course of business. The Condensed Consolidated Financial Statements do not include adjustments to reflect the possible future effects on the recoverability and classification of recorded assets or the amounts of liabilities that might be necessary should the Company be unable to continue as a going concern.

Note 2: Summary of Significant Accounting Policies

Unaudited Interim Financial Information

The accompanying financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”). The accompanying Condensed Consolidated Balance Sheet as of June 30, 2023, Condensed Consolidated Statements of Operations for the three and six months ended June 30, 2023 and 2022, Condensed Consolidated Statement of Changes in Redeemable Noncontrolling Interest and Stockholders’ Deficit for the three and six months ended June 30, 2023 and 2022 and Condensed Consolidated Statements of Cash Flows for the six months ended June 30, 2023 and 2022 are unaudited. These unaudited financial statements have been prepared in accordance with the rules and regulations of the United States Securities and Exchange Commission (“SEC”) for interim financial information. Accordingly, they do not include all of the information and footnotes required by GAAP for complete financial statements. These financial statements should be read in conjunction with the audited financial statements and the accompanying notes for the year ended December 31, 2022, contained in the Company’s Annual Report on Form 10-K. The unaudited interim financial statements have been prepared on the same basis as the annual financial statements and, in the opinion of management, reflect all adjustments (consisting of normal recurring adjustments) necessary to state fairly the Company’s financial position as of June 30, 2023, the results of operations for the three and six months ended June 30, 2023 and 2022 and cash flows for the six months ended June 30, 2023 and 2022. The December 31, 2022 Condensed Consolidated Balance Sheet included herein was derived from the audited financial statements but does not include all disclosures or notes required by GAAP for complete financial statements.

The financial data and other information disclosed in these notes to the financial statements related to the three and six months ended June 30, 2023 and 2022 are unaudited. Interim results are not necessarily indicative of results for an entire year.

The Company does not have any components of other comprehensive income recorded within its Condensed Consolidated Financial Statements, and, therefore, does not separately present a statement of comprehensive income in its Condensed Consolidated Financial Statements.

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires the Company to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

On an ongoing basis, the Company evaluates its estimates, including those related to the grant date fair value of equity awards, the fair value of warrants to purchase shares of its Class A common stock, the fair value of its Class B common stock, the useful lives of property and equipment and the fair value of the Company’s debt, among others. The Company bases its estimates on historical experience and on various other assumptions that it believes to be reasonable, the results of which form the basis for making judgments about the carrying value of assets and liabilities.

10

Concentration of Credit Risk

Financial instruments that potentially expose the Company to concentrations of credit risk consist principally of cash on deposit with one financial institution. The balance of the cash account frequently exceed insured limits. The associated risk of concentration for cash and cash equivalents is mitigated by transferring a majority of our cash to a AAA rated money market account with a creditworthy institution.

One hundred percent (100

Cash and Cash Equivalents

The Company considers any highly liquid investments with an original maturity of three months or less to be cash and cash equivalents.

Investments

Investments in entities in which the Company has no control or significant influence, is not the primary beneficiary, and have a readily determinable fair value are classified as equity investments with readily determinable fair value. The investments are measured at fair value based on a quoted market price per unit in active markets multiplied by the number of units held without consideration of transaction costs (Level 1). Gains and losses are recorded in other income (expense), net on the Condensed Consolidated Statements of Operations.

Equity investments without readily determinable fair value include ownership rights that do not provide the Company with control or significant influence and these investments do not have readily determinable fair values. The Company has elected to measure its equity investments without readily determinable fair values at cost minus impairment, if any, plus or minus changes resulting from observable price changes in orderly transactions for the identical or similar investment.

Revenue Recognition

The Company uses the revenue recognition guidance established by ASC 606, Revenue From Contracts With Customers (“ASC 606”). When an agreement falls under the scope of other standards, such as ASC 808, Collaborative Arrangements (“ASC 808”), the Company will apply the recognition, measurement, presentation, and disclosure guidance in ASC 606 to the performance obligations in the agreements if those performance obligations are with a customer. Revenue recognized by analogizing to ASC 606, is recorded as collaboration revenue on the statements of operations.

The majority of the Company’s revenue results from its license and collaboration agreements associated with the development of investigational drug products. The Company accounts for a contract when it has approval and commitment from both parties, the rights of the parties are identified, payment terms are identified, the contract has commercial substance and collectability of consideration is probable. For each contract meeting these criteria, the Company identifies the performance obligations included within the contract. A performance obligation is a promise in a contract to transfer a distinct good or service to the customer. The Company then recognizes revenue under each contract as the related performance obligations are satisfied.

Research and Development

Major components of research and development costs include cash compensation, depreciation expense on research and development property and equipment, costs of preclinical studies, clinical trials and related clinical manufacturing, costs of drug development, costs of materials and supplies, facilities cost, overhead costs, regulatory and compliance costs, and

11

fees paid to consultants and other entities that conduct certain research and development activities on the Company’s behalf. Research and development costs are expensed as incurred.

The Company records accruals based on estimates of the services received, efforts expended and amounts owed pursuant to contracts with numerous contract research and manufacturing organizations. In the normal course of business, the Company contracts with third parties to perform various clinical study activities in the ongoing development of potential products. The financial terms of these agreements are subject to negotiation and variation from contract to contract and may result in uneven payment flows. Payments under the contracts depend on factors such as the achievement of certain events and the completion of portions of the clinical study or similar conditions. The objective of the Company’s accrual policy is to match the recording of expenses in its financial statements to the actual services received and efforts expended. As such, expense accruals related to clinical studies are recognized based on the Company’s estimate of the degree of completion of the event or events specified in the specific clinical study.

The Company records nonrefundable advance payments it makes for future research and development activities as prepaid expenses. Prepaid expenses are recognized as expenses in the Condensed Consolidated Statements of Operations as the Company receives the related goods or services.

Research and development costs that are reimbursed under a cost-sharing arrangement are reflected as a reduction of research and development expense.

Recently Issued Accounting Pronouncements

Fair Value Measurements: In June 2022, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2022-03 Fair Value Measurements (Topic 820): Fair Value Measurement of Equity Securities Subject to Contractual Sale Restrictions. These amendments clarify that a contractual restriction on the sale of an equity security is not considered part of the unit of account of the equity security and, therefore, is not considered in measuring fair value. This guidance is effective for public business entities for fiscal years, including interim periods within those fiscal years, beginning after December 15, 2023. Early adoption is permitted. The Company has assessed ASU 2022-03 and early adopted the guidance during the second quarter of 2022. The adoption did not have a material impact on the Company's Condensed Consolidated Financial Statements.

Note 3: Collaboration Agreements

G42 Purchase Agreement and Cogna Collaborative and License Agreement

The Company and G42 Investments AI Holding RSC Ltd, a private limited company (“G42 Investments”), entered into a Common Stock Purchase Agreement (the “G42 Purchase Agreement”), pursuant to which the Company sold to G42 Investments 10,386,274 shares of the Company’s Class A common stock at a price per share of approximately $2.41 , for an aggregate purchase price of $25.0 million, which was paid (i) $12.5 million in cash at the closing and (ii) $12.5 million in the form of a promissory note of G42 Investments to be paid at May 31, 2023 (the “G42 Promissory Note”). As part of the G42 Purchase Agreement, G42 Investments nominated a director as appointee and the Company’s board of directors approved appointing the new director to the Company’s board. On February 28, 2023, the Company and G42 Investments amended the G42 Purchase Agreement and modified the G42 Promissory Note to accelerate the payment due under the note. Pursuant to the amendment, on February 28, 2023, the Company received $12.0 million, which reflected the original amount due under the G42 Promissory Note less a 3.75 % discount, in full satisfaction of the note, resulting in a loss of $0.3 million and was recognized as a component of other income/(expense)in the Company’s Condensed Consolidated Statements of Operations.

G42 Investments has agreed to certain transfer restrictions (including restrictions on short sales or similar transactions) and restrictions on further acquisitions of shares, in each case subject to specified exceptions. Following the expiration of a lock up period, from the period May 31, 2022 until December 31, 2024, (or if earlier, the date of receipt of U.S. Food and Drug Administration (“FDA”) approval in the U.S. for cadisegliatin (TTP399), the Company has granted to G42 Investments certain shelf and piggyback registration rights with respect to those shares of Class A common stock issued to G42 Investments pursuant to the G42 Purchase Agreement, including the ability to conduct an underwritten offering to resell such shares under certain circumstances. The registration rights include customary cooperation, cut-back, expense reimbursement, and indemnification provisions.

Contemporaneously with the G42 Purchase Agreement, effective on May 31, 2022, the Company entered into a collaboration and license agreement (the “Cogna Agreement”) with Cogna Technology Solutions LLC, an affiliate of G42 Investments (“Cogna”), which requires Cogna to work with the Company in performing clinical trials for cadisegliatin (TTP399) as well as jointly creating a global development plan to develop, market, and commercialize cadisegliatin (TTP399) in certain countries in the Middle East, Africa, and Central Asia (the “Partner Territory”). Under the terms of the Cogna Agreement, Cogna will obtain a license under certain intellectual property controlled by the Company to enable it to

12

fulfill its obligations and exercise its rights under the Cogna agreement, including to develop and commercialize cadisegliatin (TTP399) in the Partner Territory, but will not have access to the various intellectual property (“IP”) related to the license and cadisegliatin (TTP399). Specifically, the Company will share various protocols with Cogna related to conducting the clinical trials and will provide the patient dosages and placebo of cadisegliatin (TTP399) needed to conduct the trials.

Under the Cogna Agreement, Cogna has the right to develop and commercialize cadisegliatin (TTP399) in the Partner Territory at its own cost once restrictions on the use of the IP have been lifted by the Company. The Cogna Agreement determined which specific countries in the Partner Territory that Cogna may pursue development and commercialization and provides the Company with the ability to determine when Cogna can benefit from this IP through the powers granted to the Company to approve the global development plan. Further, the Company may supply at cost, or Cogna may manufacture, cadisegliatin (TTP399) for commercial sale under terms to be agreed upon by the parties at a later date.

Separately, the Company will conduct its clinical trials for cadisegliatin (TTP399) outside of the Partner Territory at its own cost. The results of each party’s clinical trials will be combined by the Company to seek FDA approval in the United States for cadisegliatin (TTP399). On December 21, 2022, G42 Healthcare Technology Solutions LLC (formerly known as Cogna Technology Solutions LLC) novated its rights and obligation under the Cogna agreement to G42 Healthcare Research Technology Projects LLC (“G42 Healthcare”), an affiliate of G42 Investments. As a result of the novation, all reference to Cogna herein shall be deemed to refer to G42 Healthcare.

The G42 Purchase Agreement also provides for, following the receipt of FDA approval of cadisegliatin (TTP399), at the option of G42 Investments, either (a) the issuance of the Company’s Class A common stock (the “Milestone Shares”) having an aggregate value equal to $30.0 million or (b) the payment by the Company of $30.0 million in cash (the “Milestone Cash Payment”). The issuance of the Milestone Shares or the payment of the Milestone Cash Payment, as applicable, are conditioned upon receipt of the FDA approval and subject to certain limitations and conditions set forth in the G42 Purchase Agreement. There can be no assurance that the FDA approval will be granted or as to the timing thereof.

Once commercialization takes place in the Partner Territory, the Company will receive royalties in the single digits from Cogna on the net sales of cadisegliatin (TTP399) for a period of at least ten years after the first commercial sale of cadisegliatin (TTP399) in the Partner Territory.

Common stock is generally recorded at fair value at the date of issuance. In determining the fair value of the Class A common stock issued to G42 Investments, the Company considered the closing price of the common stock on the effective date. The Company did not make an adjustment to the fair value for sale restrictions on the stock in accordance with guidance recently adopted in ASU 2022-03. See the “Recently Issued Accounting Guidance” in this quarterly report on Form 10-Q for details of the ASU. Accordingly, the Company determined that cash consideration of $5.7 million should be recorded as fair value of the Class A common stock at the effective date, utilizing the Class A common stock closing price of $0.55 at the effective date.

A premium was paid on the Class A common stock by G42 Investments of $18.7 million, net of a note receivable discount of $0.6 million. This premium is determined to be the transaction price for all remaining obligations under the agreements, which will be accounted for under ASC 808 or ASC 606 based on determination of the unit of account.

The Company determined that certain commitments under the agreements are in the scope of ASC 808 as both the Company and Cogna are active participants in the clinical trials of cadisegliatin (TTP399), and both are exposed to significant risks and rewards based on the success of the clinical trials and subsequent FDA approval. Cogna is determined to be a vendor of the Company during the clinical trial phase, working on the Company’s behalf to complete R&D activities, and not in a customer capacity. The Company accounted for the commitments related to the clinical trials, which includes transfer of trial protocols, supply of clinical trial dosages, and collaboration on the joint development committee (“JDC”) as an ASC 808 unit of account, applying the recognition and measurement principles of ASC 606 by analogy. The Company will recognize collaboration revenue for its development activities under ASC 808 over time based on the estimated period of performance.

By applying the principals in ASC 606 by analogy, the Company identified the performance obligation and considered the timing of satisfaction of the obligation to account for the pattern of revenue recognition. In order to recognize collaboration revenue, generally, the Company would begin satisfying its performance obligation and Cogna would need to be able to use and benefit from delivery of the assets or services. The performance obligation under the agreements that fall within the ASC 808 unit of account are concentrated in the clinical trials. As of June 30, 2023, the clinical trials had not commenced. Accordingly, no collaboration revenue was recognized for the ASC 808 unit of account during the three and six months ended June 30, 2023.

13

The Company identified certain commitments that are in the scope of ASC 606 as Cogna’s relationship is that of a customer for these commitments. The significant performance obligations that are in the scope of ASC 606 are (1) the development, commercialization and manufacturing license of the IP once restrictions on the use of the IP have been lifted by the Company and (2) a potential material right to a commercial supply agreement. The Company will recognize revenue from the development, commercial and manufacturing license at a point in time when the Company releases the restrictions on the use of the IP, which is expected to be after cadisegliatin (TTP399) is approved by the FDA. The Company will recognize revenue from the material right related to Cogna’s ability to purchase the commercial supply at cost as Cogna purchases the commercial supply from the Company, which will occur after the completion of the initial clinical trials (if Cogna decides to purchase the clinical supply from the Company). As a result, the Company has no t recognized any revenue under the ASC 606 unit of account during the three and six months ended June 30, 2023.

On February 28, 2023, the Company and G42 Investments amended the G42 Purchase Agreement and modified the G42 Promissory Note to accelerate the payment due under the note. Pursuant to the amendment, on February 28, 2023, the Company received $12.0 million, which reflected the original amount due under the G42 Promissory Note less a 3.75 % discount, in full satisfaction of the note, resulting in a loss of $0.3 million and was recognized as a component of other income/(expense) in the Company’s Condensed Consolidated Statements of Operations. The G42 Promissory Note receivable was classified and accounted for under ASC 310 Receivables (“ASC 310”) and was initially measured at its fair value of $11.9 million. The Company also recorded the $18.7 million as deferred revenue in the Condensed Consolidated Balance Sheets, as none of the underlying performance obligations had been satisfied as of and for the three and six months ended June 30, 2023.

Huadong License Agreement

The Company is party to a license agreement with Hangzhou Zhongmei Huadong Pharmaceutical Co., Ltd. (“Huadong”) (the “Huadong License Agreement”), under which Huadong obtained an exclusive and sublicensable license to develop and commercialize the Company’s glucagon-like peptide-1 receptor agonist (“GLP-1r”) program, including the compound TTP273, for therapeutic uses in humans or animals, in China and certain other Pacific Rim countries, including Australia and South Korea (collectively, the “Huadong License Territory”). Additionally, under the Huadong License Agreement, the Company obtained a nonexclusive, sublicensable, royalty-free license to develop and commercialize certain Huadong patent rights and know-how related to the Company’s GLP-1r program for therapeutic uses in humans or animals outside of the Huadong License Territory.

On January 14, 2021, the Company entered into the first amendment to the Huadong License Agreement ( the “First Huadong Amendment”) which eliminated the Company’s obligation to sponsor a multi-region clinical trial (the “Phase 2 MRCT”), and corresponding obligation to contribute up to $3.0 million in support of such trial. The amendment also reduced the total potential development and regulatory milestone payments by $3.0 million.

Prior to the First Amendment, the Company had allocated a portion of the transaction price to the obligation to sponsor and conduct a portion of the Phase 2 MRCT. Upon the removal of this performance obligation, the Company evaluated the impact of the modification under the provisions of ASC 606 and performed a reallocation of the transaction price among the remaining performance obligations. This resulted in the recognition of approximately $2.0 million of revenue on a cumulative catch-up basis during the six months ended June 30, 2022. The majority of the transaction price originally allocated to the Phase 2 MRCT performance obligation was reallocated to the license and technology transfer services combined performance obligation discussed below, which had already been completed. The reallocation of the purchase price in connection with the First Huadong Amendment was made based on the relative estimated selling prices of the remaining performance obligations.

The significant performance obligations under the Huadong License Agreement, as amended, were determined to be (i) the exclusive license to develop and commercialize the Company’s GLP-1r program, (ii) technology transfer services related to the chemistry and manufacturing know-how for a defined period after the effective date, (iii) the Company’s obligation to participate on a joint development committee (the “JDC”), and (iv) other obligations considered to be immaterial in nature.

The Company has determined that the license and technology transfer services related to the chemistry and manufacturing know-how represent a combined performance obligation because they were not capable of being distinct on their own. The Company also determined that there was no discernible pattern in which the technology transfer services would be provided during the transfer service period. As such, the Company recognized the revenue related to this combined performance obligation using the straight-line method over the transfer service period. This combined performance obligation was considered complete as of June 30, 2022. The Company recognized $2.0 million of revenue related to this combined performance obligation during the six months ended June 30, 2022. No revenue related to this combined performance obligation was recognized during the six months ended June 30, 2023.

14

A portion of the transaction price allocated to the obligation to participate in the JDC to oversee the development of products and the Phase 2 MRCT in accordance with the development plan remained deferred as of June 30, 2023, and revenue will be recognized using the proportional performance model over the period of the Company’s participation on the JDC. The unrecognized amount of the transaction price allocated to this performance obligation as of June 30, 2023 was immaterial. An immaterial amount of revenue for this performance obligation was recognized during the six months ended June 30, 2022. No

Contract Liabilities

Contract liabilities related to the Company’s collaboration agreements consisted of the following (in thousands):

| June 30, 2023 | December 31, 2022 | ||||||||||

| Current portion of contract liabilities | $ | $ | |||||||||

| Contract liabilities, net of current portion | |||||||||||

| Total contract liabilities | $ | $ | |||||||||

Note 4: Share-Based Compensation

The Company has issued nonqualified stock option awards to management, other key employees, consultants, and nonemployee directors. These option awards generally vest ratably over a three-year period and the option awards expire after a term of ten years from the date of grant. As of June 30, 2023, the Company had total unrecognized stock-based compensation expense for its outstanding stock option awards of approximately $2.0 million, which is expected to be recognized over a weighted average period of 2.3 years. The weighted average grant date fair value of options granted during the six months ended June 30, 2023 and 2022 was $0.76 and $0.65 per option, respectively. The aggregate intrinsic value of the in-the-money awards outstanding at June 30, 2023 was immaterial.

The following table summarizes the activity related to the stock option awards for the six months ended June 30, 2023:

| Number of Shares | Weighted Average Exercise Price | ||||||||||

| Awards outstanding at December 31, 2022 | $ | ||||||||||

| Granted | |||||||||||

| Forfeited | ( | ||||||||||

| Awards outstanding at June 30, 2023 | $ | ||||||||||

| Options exercisable at June 30, 2023 | $ | ||||||||||

| Weighted average remaining contractual term | |||||||||||

| Options vested and expected to vest at June 30, 2023 | $ | ||||||||||

| Weighted average remaining contractual term | |||||||||||

Compensation expense related to the grants of stock options is included in research and development and general and administrative expense as follows (in thousands):

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||||||

| Research and development | $ | $ | $ | $ | ||||||||||||||||||||||

| General and administrative | ||||||||||||||||||||||||||

| Total share-based compensation expense | $ | $ | $ | $ | ||||||||||||||||||||||

Note 5: Investments

15

Reneo completed its initial public offering in April 2021. Prior to Reneo becoming a publicly traded company, the Company’s investment in Reneo did not have a readily determinable fair value and was measured at cost less impairment, adjusted for any changes in observable prices, under the measurement alternative. Subsequent to Reneo’s initial public offering, the Company’s investment in Reneo is considered to have a readily determinable fair value and, as such, is adjusted to its fair value each period with changes in fair value recognized as a component of net loss.

The Company’s investment in Anteris does not have a readily determinable fair value and is measured at cost less impairment, adjusted for any changes in observable prices.

The Company’s investments consist of the following:

| June 30, 2023 | December 31, 2022 | ||||||||||

| Equity investment with readily determinable fair value: | |||||||||||

| Reneo common stock | $ | $ | |||||||||

| Equity investment without readily determinable fair values assessed under the measurement alternative: | |||||||||||

| Anteris preferred stock | |||||||||||

| Total | $ | $ | |||||||||

No adjustments have been made to the value of the Company’s investment in Anteris since its initial measurement either due to impairment or based on observable price changes. The Company recognized an unrealized gain on its investment in Reneo of $0.3 million and $2.4 million for the three and six months ended June 30, 2023, respectively. The Company recognized an unrealized loss on its investment in Reneo of $0.2 million and $3.4 million for the three and six months ended June 30, 2022, respectively. These adjustments were recognized as a component of other income/(expense) in the Company’s Condensed Consolidated Statements of Operations.

Note 6: Commitments and Contingencies

Legal Matters

From time to time, the Company is involved in various legal proceedings arising in the normal course of business. If a specific contingent liability is determined to be probable and can be reasonably estimated, the Company accrues and discloses the amount. The Company is not currently a party to any material legal proceedings.

Novo Nordisk

In February 2007, the Company entered into an Agreement Concerning Glucokinase Activator Project with Novo Nordisk A/S (the “Novo License Agreement”) whereby the Company obtained an exclusive, worldwide, sublicensable license under certain Novo Nordisk intellectual property rights to discover, develop, manufacture, have manufactured, use and commercialize products for the prevention, treatment, control, mitigation or palliation of human or animal diseases or conditions. As part of this license grant, the Company obtained certain worldwide rights to Novo Nordisk’s GKA program, including rights to preclinical and clinical compounds such as cadisegliatin (TTP399). This agreement was amended in May 2019 to create milestone payments applicable to certain specific and nonspecific areas of therapeutic use. Under the terms of the amended Novo License Agreement, the Company has potential developmental and regulatory milestone payments totaling up to $9.0 million for approval of a product for the treatment of type 1 diabetes, $50.5 million for approval of a product for the treatment of type 2 diabetes, or $115.0 million for approval of a product in any other indication. The Company may also be obligated to pay an additional $75.0 million in potential sales-based milestones, as well as royalty payments, at mid-single digit royalty rates, based on tiered sales of commercialized licensed products. During the fourth quarter of 2021, the Company made a payment of $2.0 million related to the satisfaction of the milestone to complete the phase 2 trials for cadisegliatin (TTP399) under this agreement.

Note 7: Leases

16

term, which constituted a modification event under ASC 842 and, the lease classification for the asset remains as an operating lease. As a result of the remeasurement of the associated lease liabilities, the Company recognized additional right of use assets and corresponding lease liabilities of $0.1

At each of June 30, 2023 and December 31, 2022, the weighted average incremental borrowing rate for the operating leases held by the Company was 9.5 2.4 years and 2.9 years, respectively.

Maturities of lease liabilities for the Company’s operating leases as of June 30, 2023 were as follows (in thousands):

| 2023 (remaining six months) | $ | ||||

| 2024 | |||||

| 2025 | |||||

| 2026 | |||||

| 2027 | |||||

| Thereafter | |||||

| Total lease payments | |||||

| Less: imputed interest | ( | ||||

| Present value of lease liabilities | $ | ||||

Operating lease cost and the related operating cash flows for the six months ended June 30, 2023 and 2022 were immaterial amounts.

Note 8: Redeemable Noncontrolling Interest

The Company is subject to the Exchange Agreement with respect to the vTv Units representing the 22.1 % noncontrolling interest in vTv LLC outstanding as of June 30, 2023 (see Note 9). The Exchange Agreement requires the surrender of an equal number of vTv Units and Class B common stock for (i) shares of Class A common stock on a one -for-one basis or (ii) cash (based on the fair market value of the Class A common stock as determined pursuant to the Exchange Agreement), at the Company’s option (as the managing member of vTv LLC), subject to customary conversion rate adjustments for stock splits, stock dividends and reclassifications. The exchange value is determined based on a 20 -day volume weighted average price of the Class A common stock as defined in the Exchange Agreement, subject to customary conversion rate adjustments for stock splits, stock dividends and reclassifications.

The redeemable noncontrolling interest is recognized at the higher of (1) its initial fair value plus accumulated earnings/losses associated with the noncontrolling interest or (2) the redemption value as of the balance sheet date. At June 30, 2023 and December 31, 2022, the redeemable noncontrolling interest was recorded based on the redemption value as of the balance sheet date of $18.9 million and $16.6 million, respectively.

Changes in the Company’s ownership interest in vTv LLC while the Company retains its controlling interest in vTv LLC are accounted for as equity transactions, and the Company is required to adjust noncontrolling interest and equity for such changes. The following is a summary of net income attributable to vTv Therapeutics Inc. and transfers to noncontrolling interest:

| For the Three Months Ended June 30, | For the Six Months Ended June 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| Net loss attributable to vTv Therapeutics Inc. common shareholders | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Decrease/(Increase) in vTv Therapeutics Inc. accumulated deficit for purchase of LLC Units as a result of common stock issuances | ( | ||||||||||||||||||||||

| Change from net loss attributable to vTv Therapeutics Inc. common shareholders and transfers to noncontrolling interest | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

17

Note 9: Stockholders’ Deficit

Amendment to Certificate of Incorporation

On May 4, 2021, the Company filed an amendment to its Amended and Restated Certificate of Incorporation (the “Charter Amendment”) to increase the number of shares of Class A common stock that the Company is authorized to issue from 100,000,000 shares of Class A common stock to 200,000,000 shares of Class A common stock, representing an increase of 100,000,000 shares of authorized Class A common stock, with a corresponding increase in the total authorized common stock, which includes Class A common stock and Class B common stock, from 200,000,000 to 300,000,000 , and a corresponding increase in the total authorized capital stock, which includes common stock and preferred stock, from 250,000,000 shares to 350,000,000 shares.

G42 Investments Transaction

On May 31, 2022, the Company and G42 Investments entered in to the G42 Purchase Agreement (see Note 3), pursuant to which the Company agreed to sell to G42 Investments 10,386,274 shares of the Company's Class A common stock at a price per share of approximately $2.41 , for an aggregate purchase price of $25.0 million, consisting of (i) $12.5 million in cash at the closing of the transaction and (ii) $12.5 million in the form of a promissory note of G42 Investments to be paid at the one-year anniversary of the execution of the G42 Purchase Agreement (the “G42 Promissory Note”). On February 28, 2023, the Company and G42 Investments amended the G42 Purchase Agreement and modified the G42 Promissory Note to accelerate the payment due under the note. Pursuant to the amendment, on February 28, 2023, the Company received $12.0 million, which reflected the original amount due under the G42 Promissory Note less a 3.75 % discount, in full satisfaction of the note, resulting in a loss of $0.3 million and was recognized as a component of other income/(expense) in the Company’s Condensed Consolidated Statements of Operations.

CinPax and CinRx Transaction

On July 22, 2022 (the “Transaction Date”), the Company entered into the CinRx Purchase Agreement with CinPax and CinRx, pursuant to which the Company agreed to sell to CinPax 4,154,549 shares of the Company’s Class A common stock at a price per share of approximately $2.41 , for an aggregate purchase price of $10.0 million, which was paid (i) $6.0 million in cash at the closing of the transaction and (ii) $4.0 million in the form of a non-interest-bearing promissory note with CinPax and was paid to the Company on November 22, 2022. The CinRx Purchase Agreement provides CinPax the right to nominate a director to be approved to sit on the Company’s Board of Directors and a board observer, which was subsequently approved by the Company’s board.

Common stock is generally recorded at fair value at the date of issuance. In determining the fair value of the Class A common stock issued to CinPax, the Company considered the closing price of the common stock on the Transaction Date. The Company did not make an adjustment to the fair value for sale restrictions on the stock in accordance with guidance recently adopted in ASU 2022-03. See the “Recently Issued Accounting Guidance” in this quarterly report on Form 10-Q for details of the ASU. Accordingly, the Company determined that cash consideration of $3.0 million should be recorded as fair value of the Class A common stock at the effective date, utilizing the Class A common stock closing price of $0.72 at the effective date.

The CinRx Purchase Agreement also provides CinRx warrants to purchase up to 1,200,000 shares of common stock at an initial exercise of price of approximately $0.72 per share (the “CinRx Warrants”). The CinRx Warrants were initially measured at fair value of $0.4 million using the Black-Scholes option model at the time of issuance and will be recorded in Warrant liability related party in the Condensed Consolidated Balance Sheets and will be subsequently remeasured at fair value through earnings on a recurring basis. (see Note 13)

The CinRx Warrants will become exercisable by CinRx only if (i) the Company receives approval from the U.S. Food and Drug Administration (“FDA Approval”) to market and distribute the pharmaceutical product containing the Company’s proprietary candidate, cadisegliatin (TTP399) (the “Product”), or (ii) the Company is acquired by a third party, sells all or substantially all of its assets related to the Product to a third party or grants a third party an exclusive license to develop, commercialize and manufacture the Product in the United States. If neither of these events happen within five years of the date of the issuance of the CinRx Warrants, the CinRx Warrants will expire and not be exercisable by CinRx. The exercise price of the CinRx Warrants and the number of shares issuable upon exercise of the CinRx Warrants are subject to adjustments in accordance with the terms of the CinRx Warrants.

Additionally, in conjunction with the CinRx Purchase Agreement the Company and CinRx entered into a Master Service Agreement (“CinRx MSA”) whereby CinRx provides the Company with consulting, preclinical and clinical trial services, as enumerated in project proposals negotiated between the Company and CinRx from time to time. (see Note 10)

18

The Company did not identify any other promises in the CinRx Purchase Agreement (aside from the issuance of common shares and the CinRx Warrants) and determined since there is no value ascribed to the CinRx MSA, the right to appoint a member and observer to the board of directors, that the remaining unallocated amount meets the definition of contributed equity and represents the amount in excess of par.

ATM Offering

In April 2020, the Company entered into the Sales Agreement with Cantor as the sales agent, pursuant to which the Company may offer and sell, from time to time, through Cantor, shares of its Class A common stock, par value $0.01 per share, having an aggregate offering price of up to $13.0 million by any method deemed to be an “at the market offering” as defined in Rule 415(a)(4) under the Securities Act (the “ATM Offering”). The shares are offered and sold pursuant to the Company’s shelf registration statement on Form S-3.

On January 14, 2021 and June 25, 2021, the Company filed a prospectus supplement in connection with the ATM Offering to increase the size of the at-the-market offering pursuant to which the Company may offer and sell, from time to time, through or to Cantor, as sales agent or principal, shares of the Company’s Class A common stock, by an aggregate offering price of $5.5 million and $50.0 million, respectively.

During the three and six months ended June 30, 2023 and 2022, the Company did not

Lincoln Park Capital Transaction

On November 24, 2020, the Company entered into the LPC Purchase Agreement and a registration rights agreement (the “Registration Rights Agreement”), pursuant to which the Company has the right to sell to Lincoln Park shares of the Company’s Class A common stock having an aggregate value of up to $47.0 million, subject to certain limitations and conditions set forth in the LPC Purchase Agreement. The Company will control the timing and amount of any sales of shares to Lincoln Park pursuant to the Purchase Agreement. During the three and six months ended June 30, 2023 and 2022, the Company did not

Note 10: Related-Party Transactions

MacAndrews & Forbes Incorporated

MacAndrews directly or indirectly controls 23,084,267 shares of Class B common stock. Further, as of June 30, 2023, MacAndrews directly or indirectly holds 36,519,212 shares of the Company’s Class A common stock. As a result, MacAndrews’ holdings represent approximately 57.0 % of the combined voting power of the Company’s outstanding common stock.

The Company has entered into several agreements with MacAndrews or its affiliates as further detailed below:

Letter Agreements

The Company had previously entered into the Letter Agreements with MacAndrews. Under the terms of the Letter Agreements, during the one year commitment period beginning on the date of each Letter Agreement, the Company had the right to sell to MacAndrews shares of its Class A common stock at a specified price per share, and MacAndrews had the right (exercisable up to three times) to require the Company to sell to it shares of Class A common stock at the same price. The commitment period of each of the Letter Agreements has now expired. In addition, in connection with and as a commitment fee for the entrance into certain of these Letter Agreements, the Company also issued MacAndrews warrants (the “Letter Agreement Warrants”) to purchase additional shares of the Company’s Class A common stock.

The Letter Agreement Warrants have been recorded as warrant liability, related party within the Company’s Condensed Consolidated Balance Sheets based on their fair value. The issuance of the Letter Agreement Warrants was considered to be a cost of equity recorded as a reduction to additional paid-in capital.

Exchange Agreement

Pursuant to the terms of the Exchange Agreement, but subject to the Amended and Restated LLC Agreement of vTv Therapeutics LLC, the vTv Units (along with a corresponding number of shares of the Class B common stock) are exchangeable for (i) shares of the Company’s Class A common stock on a one-for-one basis or (ii) cash (based on the fair market value of the Company’s Class A common stock as determined pursuant to the Exchange Agreement), at the Company’s option (as the managing member of vTv Therapeutics LLC), subject to customary conversion rate adjustments

19

for stock splits, stock dividends and reclassifications. Any decision to require an exchange for cash rather than shares of Class A common stock will ultimately be determined by the entire Board of Directors. As of June 30, 2023, MacAndrews had not exchanged any shares under the provisions of the Exchange Agreement.

Tax Receivable Agreement

The Company and MacAndrews are party to a tax receivable agreement (the “Tax Receivable Agreement”), which provides for the payment by the Company to M&F TTP Holdings Two LLC (“M&F”), as successor in interest to vTv Therapeutics Holdings, LLC (“vTv Therapeutics Holdings”), and M&F TTP Holdings LLC (or certain of its transferees or other assignees) of 85 % of the amount of cash savings, if any, in U.S. federal, state and local income tax or franchise tax that the Company actually realizes (or, in some circumstances, the Company is deemed to realize) as a result of (a) the exchange of Class B common stock, together with the corresponding number of vTv Units, for shares of the Company’s Class A common stock (or for cash), (b) tax benefits related to imputed interest deemed to be paid by the Company as a result of the Tax Receivable Agreement and (c) certain tax benefits attributable to payments under the Tax Receivable Agreement.

As no shares have been exchanged by MacAndrews pursuant to the Exchange Agreement (discussed above), the Company has not recognized any liability, nor has it made any payments pursuant to the Tax Receivable Agreement as of June 30, 2023.

Investor Rights Agreement

The Company is party to an investor rights agreement with M&F, as successor in interest to vTv Therapeutics Holdings (the “Investor Rights Agreement”). The Investor Rights Agreement provides M&F with certain demand, shelf, and piggyback registration rights with respect to its shares of Class A common stock and also provides M&F with certain governance rights, depending on the size of its holdings of Class A common stock. Under the Investor Rights Agreement, M&F was initially entitled to nominate a majority of the members of the Board of Directors and designate the members of the committees of the Board of Directors.

G42 Investments

On May 31, 2022, the Company entered into a common stock purchase agreement with G42 Investments pursuant to which the Company sold to G42 Investments 10,386,274 shares of the Company’s Class A common stock at a price per share of approximately $2.41 , for an aggregate purchase price of $25.0 million, which was paid (i) $12.5 million in cash at the closing and (ii) $12.5 million in the form of a promissory note of G42 Investments to be paid on May 31, 2023 (the “G42 Promissory Note”). As part of the G42 Purchase Agreement, G42 Investments put forward a director as appointee and the Company’s board of directors appointed the new director to the Company’s board on July 11, 2022. On February 28, 2023, the Company and G42 Investments entered into an amendment of the common stock purchase agreement pursuant to which G42 Investments agreed to accelerate payment of the amount due under the G42 Promissory Note. On February 28, 2023, the Company received $12.0 million from G42 Investments, which represented a 3.75 % discount to the full amount due under the G42 Promissory Note, in full and final satisfaction of the promissory note, resulting in a loss of $0.3 million and was recognized as a component of other income/(expense) in the Company’s Condensed Consolidated Statements of Operations.

CinRx Pharma, LLC

Master Services Agreement

On July 22, 2022, the Company entered into a Master Services Agreement with CinRx Pharma, LLC (“CinRx”) (the “CinRx MSA”). Under the CinRx MSA, CinRx provides the Company with consulting and clinical trial services, as enumerated in project proposals negotiated between the Company and CinRx from time to time. As of October 10, 2022, the Company agreed to pay CinRx fees of up to $0.2 million per month until approximately December 2024 in respect of ongoing agreed project proposals under the CinRx MSA, plus out-of-pocket expenses incurred by CinRx on the Company’s behalf. Dr. Jonathan Isaacsohn, who was appointed as chair of the Company’s board of directors on August 9, 2022, is the President and Chief Executive Officer of CinRx. CinPax, LLC, a subsidiary of CinRx, currently holds 4,154,549 shares of the Company’s Class A common stock.

Note 11: Income Taxes

20

license agreements with foreign entities. The Company did not record an income tax provision for the three months ended June 30, 2022.

Management has evaluated the positive and negative evidence surrounding the realization of its deferred tax assets, including the Company’s history of losses, and under the applicable accounting standards determined that it is more likely than not that the deferred tax assets will not be realized. The difference between the effective tax rate of the Company and the U.S. statutory tax rate of 21% on June 30, 2023 is due to the valuation allowance against the Company’s expected net operating losses.

As discussed in Note 10, the Company is party to a tax receivable agreement with a related party which provides for the payment by the Company to M&F (or certain of its transferees or other assignees) of 85 % of the amount of cash savings, if any, in U.S. federal, state and local income tax or franchise tax that the Company actually realizes (or, in some circumstances, the Company is deemed to realize) as a result of certain transactions. As no transactions have occurred which would trigger a liability under this agreement, the Company has not recognized any liability related to this agreement as of June 30, 2023.

Note 12: Net Loss per Share

Basic loss per share is computed by dividing net loss attributable to vTv Therapeutics Inc. by the weighted average number of shares of Class A common stock outstanding during the period. Diluted loss per share is computed giving effect to all potentially dilutive shares. Diluted loss per share for all periods presented is the same as basic loss per share as the inclusion of potentially issuable shares would be antidilutive.

A reconciliation of the numerator and denominator used in the calculation of basic and diluted net loss per share of Class A common stock is as follows (amounts in thousands, except per share amounts):

| For the Three Months Ended June 30, | For the Six Months Ended June 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| Numerator: | |||||||||||||||||||||||

| Net loss | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Less: Net loss attributable to noncontrolling interests | ( | ( | ( | ( | |||||||||||||||||||

| Net loss attributable to common shareholders of vTv Therapeutics Inc., basic and diluted | ( | ( | ( | ( | |||||||||||||||||||

| Denominator: | |||||||||||||||||||||||

| Weighted average vTv Therapeutics Inc. Class A common stock, basic and diluted | |||||||||||||||||||||||

| Net loss per share of vTv Therapeutics Inc. Class A common stock, basic and diluted | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

Potentially dilutive securities not included in the calculation of dilutive net loss per share are as follows:

| June 30, 2023 | June 30, 2022 | ||||||||||

Class B common stock (1) | |||||||||||

| Common stock options granted under the Plan | |||||||||||

| Common stock warrants | |||||||||||

| Total | |||||||||||

__________________________

| (1) | Shares of Class B common stock do not share in the Company’s earnings and are not participating securities. Accordingly, separate presentation of loss per share of Class B common stock under the two-class method has not been provided. Each share of Class B common stock (together with a corresponding vTv Unit) is exchangeable for one share of Class A common stock. | |||||||

21

Note 13: Fair Value of Financial Instruments

The carrying amount of certain of the Company’s financial instruments, including cash and cash equivalents, net accounts receivable, note receivable, accounts payable and other accrued liabilities approximate fair value due to their short-term nature.

The Company measures the value of its equity investments without readily determinable fair values at cost minus impairment, if any, plus or minus changes resulting from observable price changes in orderly transactions for the identical or similar investment. During the year ended December 31, 2021, Reneo completed its initial public offering. As a result, the fair value of the Company’s investment in Reneo’s common stock now has a readily determinable market value and is no longer eligible for the practical expedient for investments without readily determinable fair market values.

Assets and Liabilities Measured at Fair Value on a Recurring Basis

The Company evaluates its financial assets and liabilities subject to fair value measurements on a recurring basis to determine the appropriate level in which to classify them for each reporting period. This determination requires significant judgments. The Company determined that the G42 Promissory Note receivable was level 2 and the fair value measurement was based on the market yield curves. The following table summarizes the conclusions reached regarding fair value measurements as of June 30, 2023 and December 31, 2022 (in thousands):

| Balance at June 30, 2023 | Quoted Prices in Active Markets for Identical Assets (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | ||||||||||||||||||||

| Assets: | |||||||||||||||||||||||

| Equity securities with readily determinable fair value | $ | $ | $ | $ | |||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

| Liabilities: | |||||||||||||||||||||||

Warrant liability, related party (1) | $ | $ | $ | $ | |||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

| Balance at December 31, 2022 | Quoted Prices in Active Markets for Identical Assets (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | ||||||||||||||||||||

| Assets: | |||||||||||||||||||||||

| Equity securities with readily determinable fair value | $ | $ | $ | $ | |||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

| Liabilities: | |||||||||||||||||||||||

Warrant liability, related party (1) | $ | $ | $ | $ | |||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

_____________________________

| (1) | Fair value determined using the Black-Scholes option pricing model. Expected volatility is based on the historical volatility of the Company’s common stock over the most recent period. The risk-free rate is based on the U.S. Treasury yield curve in effect at the time of valuation. | ||||

22

| Changes in Level 3 instruments for the three months ended June 30, | |||||||||||||||||||||||||||||

| Balance at January 1 | Net Change in fair value included in earnings | Purchases / Issuance | Sales / Repurchases | Balance at June 30, | |||||||||||||||||||||||||

| 2023 | |||||||||||||||||||||||||||||

| Warrant liability, related party | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||

| Total | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||

| 2022 | |||||||||||||||||||||||||||||

| Warrant liability, related party | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||

| Total | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||

There were no transfers into or out of level 3 instruments and/or between level 1 and level 2 instruments during the three and six months ended June 30, 2023. Gains and losses recognized due to the change in fair value of the warrant liability, related party are recognized as a component of other income – related party in the Company’s Condensed Consolidated Statements of Operations.

The fair value of the Letter Agreement Warrants was determined using the Black-Scholes option pricing model or option pricing models based on the Company’s current capitalization. Expected volatility is based on the historical volatility of the Company’s common stock over the most recent period. The risk-free rate is based on the U.S. Treasury yield curve in effect at the time of valuation. Significant inputs utilized in the valuation of the Letter Agreement Warrants as of June 30, 2023 and December 31, 2022 were:

| June 30, 2023 | December 31, 2022 | ||||||||||||||||

| Range | Weighted Average | Range | Weighted Average | ||||||||||||||

| Expected volatility | |||||||||||||||||

| Risk-free interest rate | |||||||||||||||||

The fair value of the CinRx Warrants was determined using the Black-Scholes option pricing model. Expected volatility is based on the historical volatility of the Company’s common stock over the most recent period. The risk-free rate is based on the U.S. Treasury yield curve in effect at the time of valuation. Significant inputs utilized in the valuation of the CinRx Warrants as of June 30, 2023 were:

| Expected volatility | % | ||||

| Expected life of options in years | |||||

| Risk-free interest rate | % | ||||

| Expected dividend yield | % | ||||

The weighted average expected volatility and risk-free interest rate was based on the relative fair values of the warrants.

Note 14: Subsequent Events

23

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS