UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

Form 10-K

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended February 3, 2024

OR

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from __________ to __________

Commission file number: 001-37501

(Exact name of registrant as specified in its charter)

|

|

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(IRS Employer Identification No.)

|

|

|

|

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

(717 ) 657-2300

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

Trading Symbol

|

Name of each exchange on which registered

|

||

|

|

|

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934

during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of

Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or

an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

|

Accelerated filer ☐

|

Non-accelerated filer ☐

|

Smaller reporting company

|

Emerging growth company

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or

revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicated by check mark whether the registrant has filed a report on and

attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit

report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant

to § 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the voting stock held by non-affiliates of the registrant as of July 28, 2023 (the last business day of the registrant’s most

recently completed second fiscal quarter), based on the closing sale price per share as reported by the NASDAQ Stock Market LLC on such date, was approximately $4.4 billion. For purposes of this calculation only, the registrant has excluded all shares held in the treasury or that may be deemed to be beneficially owned by executive officers and directors of the registrant. By

doing so, the registrant does not concede that such persons are affiliates for purposes of federal securities laws.

The number of outstanding shares of the registrant’s common stock, $0.001 par value, as of March 22, 2024 was 61,366,747 .

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement for the 2024 Annual Meeting of Stockholders (the “Proxy Statement”), to be filed pursuant to

Regulation 14A within 120 days after the end of the 2023 fiscal year, are incorporated by reference into Part III of this Form 10-K.

| |

Page

|

|

|

PART I

|

||

|

Item 1.

|

1

|

|

|

Item 1A.

|

13

|

|

|

Item 1B.

|

32

|

|

|

Item 1C.

|

32

|

|

|

Item 2.

|

35

|

|

|

Item 3.

|

35

|

|

|

Item 4.

|

35

|

|

|

PART II

|

||

|

Item 5.

|

36

|

|

|

Item 6.

|

38

|

|

|

Item 7.

|

38

|

|

|

Item 7A.

|

51

|

|

|

Item 8.

|

52

|

|

|

Item 9.

|

78

|

|

|

Item 9A.

|

78

|

|

|

Item 9B.

|

80

|

|

|

Item 9C.

|

80

|

|

|

PART III

|

||

|

Item 10.

|

80

|

|

|

Item 11.

|

80

|

|

|

Item 12.

|

80

|

|

|

Item 13.

|

80

|

|

|

Item 14.

|

80

|

|

|

PART IV

|

||

|

Item 15.

|

81

|

|

|

Item 16.

|

84

|

|

Cautionary note regarding forward-looking statements

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified by words

such as “could,” “may,” “might,” “will,” “likely,” “anticipates,” “intends,” “plans,” “seeks,” “believes,” “estimates,” “expects,” “continues,” “projects” and similar references to future periods, prospects, financial performance and industry

outlook. Examples of forward-looking statements include, but are not limited to, statements we make regarding the outlook for our future business and financial performance, such as those contained in “Item 7. Management’s Discussion and Analysis of

Financial Condition and Results of Operations,” included elsewhere in this Annual Report on Form 10-K.

Forward-looking statements are based on our current expectations and assumptions regarding our business, capital market conditions, the economy, and other future conditions. Because forward-looking

statements relate to the future, by their nature, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict. As a result, our actual results may differ materially from those contemplated by the

forward-looking statements. Important factors that could cause actual results to differ materially from those in the forward-looking statements include regional, national or global political, economic, business, competitive, market and regulatory

conditions, including, but not limited to, supply chain developments, legislation, national trade policy, and the following:

| • |

our failure to adequately procure and manage our inventory, anticipate consumer demand, or achieve favorable product margins;

|

| • |

changes in consumer confidence and spending;

|

| • |

risks associated with our status as a “brick and mortar only” retailer;

|

| • |

risks associated with intense competition;

|

| • |

our failure to open new profitable stores, or successfully enter new markets, on a timely basis or at all;

|

| • |

fluctuations in comparable store sales and results of operations, including on a quarterly basis;

|

| • |

factors such as inflation, cost increases and energy prices;

|

| • |

the risks associated with doing business with international manufacturers and suppliers including, but not limited to, potential increases in tariffs on imported goods;

|

| • |

our inability to operate our stores due to civil unrest and related protests or disturbances;

|

| • |

our failure to properly hire and to retain key personnel and other qualified personnel;

|

| • |

changes in market levels of wages;

|

| • |

risks associated with cybersecurity events, and the timely and effective deployment, protection, and defense of computer networks and other electronic systems, including e-mail;

|

| • |

our inability to obtain favorable lease terms for our properties;

|

| • |

the failure to timely acquire, develop, open and operate, or the loss of, disruption or interruption in the operations of, any of our centralized distribution centers;

|

| • |

risks associated with our lack of operations in the growing online retail marketplace;

|

| • |

risks associated with litigation, the expense of defense, and potential for adverse outcomes;

|

| • |

our inability to successfully develop or implement our marketing, advertising and promotional efforts;

|

| • |

the seasonal nature of our business;

|

| • |

risks associated with natural disasters, whether or not caused by climate change;

|

| • |

outbreak of viruses, global health epidemics, pandemics, or widespread illness;

|

| • |

changes in government regulations, procedures and requirements; and

|

| • |

our ability to service indebtedness and to comply with our financial covenants.

|

See “Item 1A. Risk Factors” for a further description of these and other factors. For the reasons described above, we caution you against relying on any forward-looking statements, which should also be

read in conjunction with the other cautionary statements that are included elsewhere in this Annual Report on Form 10-K. Any forward-looking statement made by us in this annual report speaks only as of the date on which we make it. Factors or events

that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new

information, future developments or otherwise, except as may be required by law. You are advised, however, to consult any further disclosures we make on related subjects in our public announcements and Securities and Exchange Commission (“SEC”)

filings.

Ollie’s Bargain Outlet Holdings, Inc. operates on a fiscal year, consisting of the 52- or 53-week period ending on the Saturday nearer January 31 of the following calendar year. References to “2023,” “2022” and “2021”

represent the 2023 fiscal year ended February 3, 2024, the 2022 fiscal year ended January 28, 2023, and the 2021 fiscal year ended January 29, 2022, respectively. 2023 consisted of 53-weeks and each of 2022 and 2021 consisted of 52-weeks. References to “2024” refer to the 52-week fiscal year ending February 1, 2025.

In this report, the terms “Ollie’s,” the “Company,” “we,” “us” or “our” mean Ollie’s Bargain Outlet Holdings, Inc. and its wholly owned subsidiaries, unless the context indicates otherwise.

PART I

| Item 1. |

Business.

|

Our company

Ollie’s is America’s largest retailer of closeout merchandise and excess inventory. Our stores sell name brand household related items that consumers use in their everyday lives at prices that are

typically 20% to 70% below traditional retailers. Known for our assortment of products offered as “Good Stuff Cheap,” we offer customers a broad selection of brand name products, including housewares, bed and bath, food, floor coverings, health and

beauty aids, books and stationery, toys and electronics. Our differentiated go-to market strategy is characterized by a unique, fun and engaging treasure hunt shopping experience, compelling customer value proposition and witty, humorous in-store

signage, and advertising campaigns. These attributes have driven our rapid growth and strong and consistent store performance.

Ollie’s was founded based on the idea that “everyone in America loves a bargain.” Since opening our first store in Mechanicsburg, PA in 1982, Ollie’s has been offering customers high quality brand name

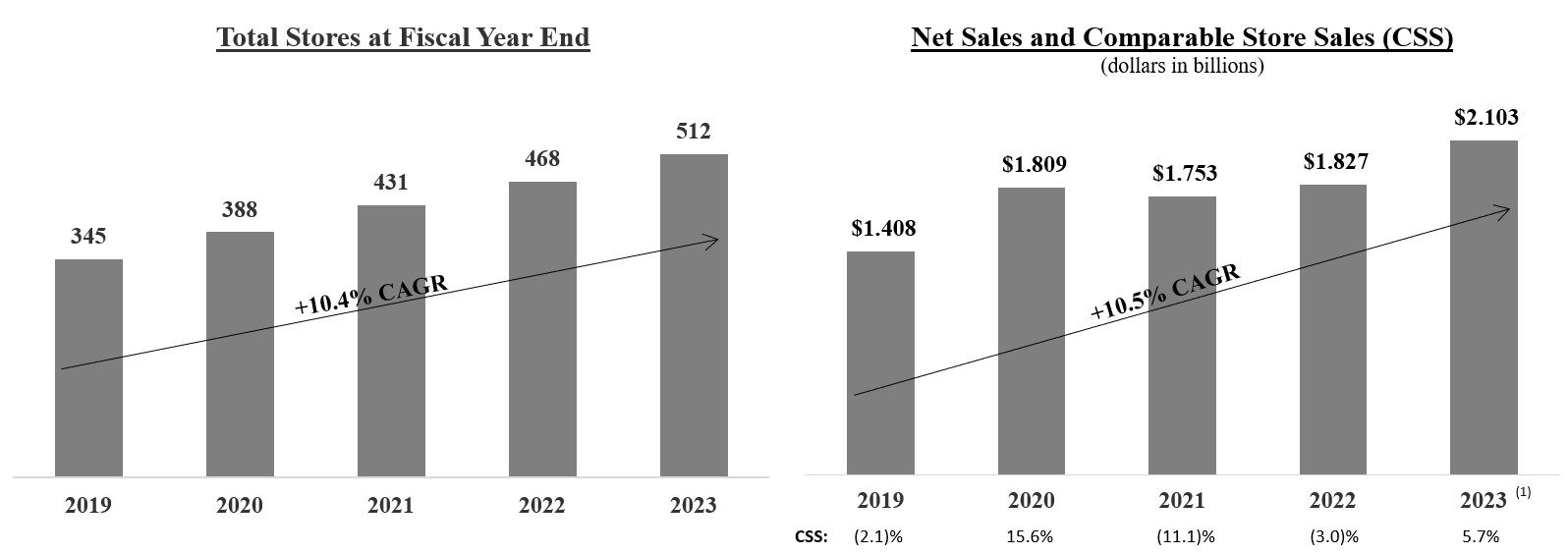

products at drastically reduced prices through the buying and selling of closeout merchandise and excess inventory. Our store base has grown organically by backfilling existing markets and leveraging our brand awareness, marketing, and infrastructure

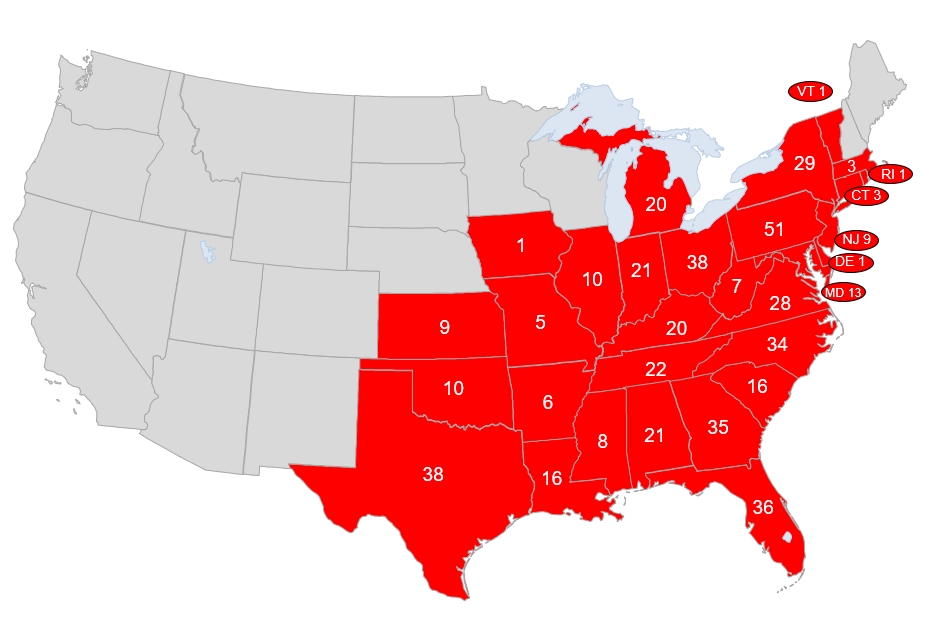

to expand into new markets in contiguous states. We have grown to 512 stores in 30 states as of February 3, 2024. Our no-frills, “semi-lovely” warehouse style stores average approximately 33,000 square feet and generate consistently strong financial

returns across all vintages, geographic regions, population densities, demographic groups, real estate formats and regardless of any co-tenant. Our business model has resulted in positive financial performance during strong and weak economic cycles.

We recently completed our latest Real Estate feasibility study, which utilizes population and demographic data to look at store count and density across a changing United States landscape. The migration trend out of larger metropolitan areas and into

rural suburban areas is a positive trend for Ollie’s and our latest analysis concludes that we could operate as many as 1,300 stores nationwide, up from a previous target of 1,050.

The closeout industry is large, highly fragmented, and growing. Fueling the growth is the consolidation of retailers and manufacturers around the globe. Larger retailers are being supplied by larger

manufacturers and this is leading to larger order and product flows. In addition, manufacturers are constantly developing and introducing new products, new packaging, and working around endless changes and disruptions in the marketplace and supply

chain. This is driving growth in the number of products being offered for sale by manufacturers at closeout type of prices. At the same time, the retail side of the closeout industry is highly fragmented, with many independent operators and small

format stores.

Our constantly changing merchandise assortment is procured by a highly experienced merchant team, who leverage deep, long-standing relationships with hundreds of major manufacturers, wholesalers,

distributors, brokers, and retailers. These relationships enable our merchant team to find and select only the best buys from a broad range of brand name closeout product offerings and to pass drastically reduced prices along to our customers. As we

grow, we believe our increased scale has provided and will continue to provide us with even greater access to brand name products as larger manufacturers seek larger buyers capable of acquiring an entire deal. Our merchant team augments these deals

with directly sourced products, including Ollie’s own private label brands and other products exclusive to Ollie’s.

Our business model has produced consistently strong growth and financial performance. From 2019 through 2023:

| • |

Our store base expanded from 345 stores to 512 stores, a compound annual growth rate, or CAGR, of 10.4% and we entered five new states;

|

| • |

Comparable store sales grew at an average rate of 1.0% per year; and

|

| • |

Net sales increased from $1.408 billion to $2.103 billion, a CAGR of 10.5%.

|

(1) 2023 consisted of 53 weeks compared with 52 weeks in the prior-year periods.

Our competitive strengths

We believe the following strengths differentiate us from our competitors and serve as the foundation for our current and future growth:

“Good Stuff Cheap”—Ever changing product assortment at drastically reduced prices. Our stores offer something for everyone across a diverse

range of merchandise categories at prices typically 20 to 70% off traditional retailers. Our product assortment frequently changes based on the wide variety of deals available from the hundreds of brand name suppliers we have relationships with. We

augment these opportunistic deals on brand name merchandise with directly-sourced unbranded products or those under our own private label brands and exclusively licensed recognizable brands and celebrity names. Brand name closeout merchandise

represented approximately 65% and non-closeout goods and private label products collectively represented approximately 35% of the retail value of our 2023 merchandise purchases. Our treasure hunt shopping environment and slogan “when it’s gone, it’s

gone” help to instill a “shop now” sense of urgency that encourages frequent customer visits.

Our growing scale and highly experienced and disciplined merchant team. Since our founding in 1982, Ollie’s has been offering customers

high quality brand name products at drastically reduced prices through the buying and selling of closeout merchandise and excess inventory. As we grow, we believe our increased scale provides us with even greater access to brand name closeout

products as larger manufacturers seek larger buyers. Our merchant team maintains strong, long-standing relationships with a diverse group of suppliers, allowing us to procure branded merchandise at compelling values for our customers. We have been

doing business with our top 15 suppliers for an average of over 15 years. Our well-established relationships with our suppliers, together with our scale, buying power, financial credibility and responsiveness, often make Ollie’s the first call for

available deals. Our direct relationships with our suppliers have increased as we have grown and we continuously strive to broaden our supplier network. These factors provide us with increased access to goods, which enable us to be more selective in

our deal-making and, we believe, help us provide compelling value and assortment of goods to our customers and fuel our continued profitable growth.

Distinctive brand and engaging shopping experience. Our distinctive and often self-deprecating humor and highly recognizable caricatures

are used in our stores, flyers, mailers, website and email campaigns. We attempt to make our customers laugh as we poke fun at ourselves and current events. We believe this approach creates a strong connection to our brand and sets us apart from

other, more traditional retailers. Our “semi-lovely” stores feature these same brand attributes together with witty signage in a warehouse format that creates a fun, relaxed and engaging shopping environment. We believe that by disarming our

customers by getting them to giggle a bit, they are more likely to look at and trust our products for what they are—extremely great bargains. We offer a “30-day no hard time guarantee” as a means to overcome any skepticism associated with our cheap

prices and to build trust and loyalty, because if our customers are not happy, we are not happy. We welcome customers to bring back their merchandise within that timeframe for a “no hard time” full refund. We also make it easy for our customers to

browse our stores by displaying our products on easily accessible fixtures and by keeping the stores clean and well-lit. We believe our humorous brand image, compelling values and welcoming stores resonate with our customers and define Ollie’s as a

unique and comfortable destination shopping location.

Extremely loyal “Ollie’s Army” customer base. Our best customers are members of our Ollie’s Army customer loyalty program, which stands at

14.0 million members as of February 3, 2024. For 2023, over 80% of our sales were from Ollie’s Army members, and we grew our base of loyal members by 5.9% in 2023. Ollie’s Army members spend approximately 40% more per shopping trip at Ollie’s than

non-members. We identify our target customer as “anyone age 25 or older with a wallet or a purse” seeking a great bargain.

Strong and consistent store model built for growth. We employ a proven new store model that generates strong cash flow, consistent

financial results and attractive returns on investment. Our highly flexible real estate approach has proven successful across all vintages, geographic regions, population densities, demographic groups, real estate formats and regardless of any

co-tenant. New stores have consistently opened strong, with higher net sales in their first 12 months of operations, than average existing stores due to the brand excitement surrounding grand openings and produced an average payback period of

approximately two years. We believe that our consistent store performance, strategically-located distribution centers, and disciplined approach to site selection support the portability and predictability of our new unit growth strategy.

Highly experienced and passionate management team. Our leadership team has guided our organization through its expansion and positioned us

for continued growth. We have assembled a talented and dedicated team of executives. Our senior executives possess extensive experience across a broad range of disciplines, including merchandising, marketing, real estate, finance, store operations,

supply chain management, and information technology. We believe by encouraging equity ownership and fostering a strong team culture, we have aligned the interests of our executives with those of our stockholders. We believe these factors result in a

cohesive team focused on sustainable long-term growth.

Our growth strategy

We plan to continue to drive growth in sales and profitability by executing on the following strategies:

Grow our store base. We believe our compelling value proposition and the success of our stores across a broad range of geographic regions,

population densities, and demographic groups create a significant opportunity to profitably increase our store count. Our internal estimates and third-party research conducted by Hoffman Strategy Group indicate the potential for more than 1,300

national locations. Our new store real estate model is flexible and focuses predominately on second generation sites ranging in size from 25,000 to 35,000 square feet. We believe there is an ample supply of suitable low-cost, second generation real

estate to allow us to infill within our existing markets as well as to expand into new, contiguous geographies. This approach leverages our distribution infrastructure, field management team, store management, marketing investments and brand

awareness. We expect our new store openings to be the primary driver of our continued, consistent growth in sales and profitability.

Increase our offerings of great bargains. We will continue to enhance our supplier relationships and develop additional sources to acquire

brand name closeout products for our customers. Our direct buying relationships with many major manufacturers, wholesalers, distributors, brokers, and retailers provide us with significant opportunities to expand our ever-changing assortment of brand

name closeout merchandise at extreme values. As we continue to grow, we believe our increased scale will provide us with even greater access to brand name closeout products as major manufacturers seek a single buyer to acquire an entire deal. We

plan to further invest in our merchandising team in order to expand and enhance our sourcing relationships and product categories, which we expect will drive shopping frequency and increase customer spending.

Leverage and expand Ollie’s Army. We intend to recruit new Ollie’s Army members and increase their frequency of store visits and spending

by enhancing our distinctive, fun and recognizable marketing programs, building brand awareness, further rewarding member loyalty and utilizing more sophisticated data-driven targeted marketing. We believe these strategies, coupled with a larger

store base, will enable us to increase the amount of sales driven by loyal Ollie’s Army customers seeking the next great deal.

Segments

We operate in one reporting segment. See Note 12, “Segment Reporting and Entity-Wide Information,” to our audited consolidated financial statements included elsewhere in this Annual Report on Form 10-K.

Our merchandise

Strategy

We offer a highly differentiated, constantly evolving assortment of brand name merchandise across a broad range of categories at drastically reduced prices. Our ever-changing assortment of “Good Stuff

Cheap” includes brand name closeout merchandise from leading manufacturers. We augment our brand name merchandise with opportunistic purchases of unbranded goods and our own domestic and direct-import private label brands in underpenetrated

categories to further enhance the assortment of products that we offer. Brand name closeout merchandise represented approximately 65% and non-closeout goods and private label products collectively represented approximately 35% of the retail value of

our 2023 merchandise purchases. We believe our compelling value proposition and the unique nature of our merchandise offerings have fostered our customer appeal across a variety of demographics and socioeconomic profiles.

Our warehouse format stores feature a broad number of categories including housewares, bed and bath, food, floor coverings, health and beauty aids, books and stationery, toys, and electronics as well as

other products including hardware, candy, clothing, sporting goods, pet and lawn and garden products. We focus on buying cheap to sell cheap and source products as unique buying opportunities present themselves. Our merchandise mix is designed to

combine unique and brand name bargains at extremely attractive price points. This approach results in frequently changing product assortments and localized offerings which encourage shopper frequency and a “shop now” sense of urgency as customers

hunt to discover the next deal.

The common element of our dynamic merchandise selection is the consistent delivery of great deals to our customers, with products offered at prices typically 20 to 70% off traditional retailers. Our

product price tags allow customers to compare our competitor’s price against Ollie’s price to further highlight the savings they can realize by shopping at our stores.

Product mix

Examples of our product offerings include:

| • |

Housewares: cooking utensils, dishes, appliances, plastic containers, cutlery, storage and garbage bags, detergents and cleaning supplies, cookware and

glassware, candles, hardware, frames, and giftware;

|

| • |

Bed and bath: household goods including bedding, towels, curtains, and associated hardware;

|

| • |

Food: packaged food including coffee, bottled non-carbonated beverages, salty snacks, candy, condiments, sauces, spices, dry pasta, canned goods, cereal,

and cookies;

|

| • |

Floor coverings: laminate flooring, commercial and residential carpeting, area rugs, and floor mats;

|

| • |

Books and stationery: novels, children’s, how-to, business, cooking, inspirational and coffee table books, greeting cards and various office supplies, and

party goods;

|

| • |

Electronics: home electronics, cellular accessories, and as seen on television;

|

| • |

Toys: dolls, action figures, puzzles, educational toys, board games, and other related items;

|

| • |

Health and beauty aids: personal care, hair care, oral care, health and wellness, over-the-counter medicine, first aid, sun

care, and personal grooming;

|

| • |

Seasonal: summer furniture, air conditioners, fans and space heaters, and lawn & garden; and

|

| • |

Other: clothing, sporting goods, pet products, luggage, and automotive.

|

The following table shows the breakdown of our product offerings as a percentage of net sales for each of the last three fiscal years:

|

|

Percentage of Net Sales

|

|||||||||||

|

|

2023

|

2022

|

2021

|

|||||||||

|

Consumables

|

23.8

|

%

|

21.6

|

%

|

19.8

|

%

|

||||||

|

Home

|

35.7

|

%

|

38.3

|

%

|

39.8

|

%

|

||||||

|

Seasonal

|

18.7

|

%

|

17.8

|

%

|

18.1

|

%

|

||||||

|

Other

|

21.8

|

%

|

22.3

|

%

|

22.3

|

%

|

||||||

|

Total

|

100.0

|

%

|

100.0

|

%

|

100.0

|

%

|

||||||

Consumables includes items such as health and beauty aids, food, candy, and pet food. Home includes items such as

housewares, domestics, floor coverings, and hardware. Seasonal includes items such as summer furniture, air conditioners, fans and space heaters, toys, and lawn & garden. Other includes items such as books and stationery, electronics, clothing, sporting goods, pet products, luggage, and automotive.

Product categories

We maintain consistent average margins across our primary product categories described below.

Brand name closeout merchandise

Brand name closeout merchandise represented approximately 65% of the retail value of our 2023 merchandise purchases. Our focus is to provide huge savings to our customers primarily through brand name

products across a broad range of merchandise. Our experienced merchant team purchases deeply discounted, branded or closeout merchandise primarily from manufacturers, retailers, distributors, and brokers. This merchandise includes overstocks,

discontinued merchandise, package changes, cancelled orders, excess inventory and buybacks from retailers, and major manufacturers.

Non-closeout goods/private label

Non-closeout and private label products collectively represented approximately 35% of the retail value of our 2023 merchandise purchases. We augment the breadth of our brand name merchandise with

non-closeout and private label merchandise. In categories where the consumer is not as brand conscious, such as food, home textiles, and furniture, or when we may not be offering a current brand name merchandise deal, we will buy deeply discounted

unbranded merchandise. These extreme value offerings are mixed in the stores with our brand name merchandise. We also have a variety of domestic and direct-import private label merchandise and exclusive products sold under numerous brands. These

high-quality products are developed in key categories such as housewares and are designed to create brand-like excitement and complement our brand name merchandise. We also have licenses for private label products that use recognizable celebrity

names or brand names. We routinely evaluate the quality and condition of these private label goods to ensure that we are delivering our customer a high-quality product at a great price.

Merchandise procurement and distribution

Our disciplined buying strategy and strict adherence to purchasing margins support our merchandising strategy of buying cheap to sell cheap.

Merchandising team

Our merchant team maintains strong, long-standing relationships with a diverse group of suppliers, allowing us to procure branded merchandise at compelling values for our customers. Our merchants

specialize by department in order to build category expertise, in-depth knowledge and sourcing relationships. We believe our buying approach, coupled with long-standing and newly formed relationships, enable us to find the best deals from major

manufacturers and pass drastically reduced prices along to our customers. We plan to further invest in and grow our merchandising team in order to expand and enhance our sourcing relationships and product categories, which we expect will drive

shopping frequency and increase customer spending.

Merchandise procurement

We believe that our strong sourcing capabilities are the result of our tenured merchant team’s ability to leverage deep, long-standing relationships with hundreds of manufacturers, wholesalers, brokers,

retailers, and other suppliers. Our merchants maintain direct relationships with brand manufacturers, regularly attend major tradeshows and travel the world to source extreme value offerings across a broad assortment of product categories. We are an

ideal partner to major manufacturers because our merchants are experienced and empowered to make quick decisions. Each opportunity is unique, and our merchants negotiate directly with the supplier to lock in a particular deal. Our ability to select

the most attractive opportunistic purchases from a growing number of available deals enables us to provide a wide assortment of goods to our customers at great bargain prices.

We source from over 1,100 suppliers. Our dedication to building strong relationships with suppliers is evidenced by an average relationship of over 15-years with our top 15 suppliers. As we continue to

grow, we believe our increased scale will provide us with even greater access to brand name products since many major manufacturers seek a single buyer to acquire the entire deal.

Distribution and logistics

We have made significant investments in our distribution network and personnel to support our store growth plan. Our stores generally receive shipments from our distribution centers one to two times a

week, depending on the season and specific store size and sales volume. We utilize independent third party freight carriers.

Currently, we distribute approximately 95% of our merchandise from our distribution centers in York, PA, which completed a 201,000 square feet expansion in the beginning of fiscal 2023 (804,000 square

feet), Commerce, GA (962,000 square feet), and Lancaster, TX (615,000 square feet).

During the first quarter of fiscal 2023, the Company purchased a parcel of land in Princeton, Illinois for its fourth distribution center and broke ground on construction of the 615,000 square feet

facility in April 2023, the distribution center is expected to be operational in the second half of fiscal 2024.

With the expansion of our York, PA distribution center and the addition of our fourth distribution center, we believe our distribution capabilities will support up to 750 stores.

Our stores

As of February 3, 2024, we operated 512 stores, averaging approximately 33,000 square feet, across 30 contiguous states in the eastern half of the United States. Our highly flexible real estate approach

has proven successful across all vintages, geographic regions, population densities, demographic groups, real estate formats and regardless of any co-tenant. Our business model has resulted in positive financial performance during strong and weak

economic cycles. We have successfully opened stores in five new states since 2019, highlighting the portability of our new store model.

In fiscal 2022, the Company implemented an ongoing store improvement initiative to provide our customers with an updated shopping experience, which showcases our tremendous value and the amazing deals

we offer in an organized and easy to navigate store format. We have remodeled 56 stores to date and 35 stores in fiscal 2023 and continue to see a sales uplift in newly remodeled locations. With a relatively low upfront investment, our remodels have

produced on average a payback period of approximately two years.

The following map shows the number of stores in each of the states in which we operated as of February 3, 2024:

Store design and layout

All of our warehouse format stores incorporate the same philosophy: no-frills, bright, “semi-lovely” stores and a fun, treasure hunt shopping experience. We present our stores as “semi-lovely” to

differentiate our stores from other traditional retailers, and to minimize operating and build-out costs. Our stores also welcome our customers with vibrant and colorful caricatures together with witty signage. We attempt to make our customers laugh

as we poke fun at ourselves and current events. We believe that by disarming our customers by getting them to giggle a bit, they are able to look at and trust our products for what they are—extremely great bargains.

We believe the store layout and merchandising strategy help to encourage a “shop now” sense of urgency and increase frequency of customer visits as customers never know what they might come across in

our stores. We make it easy for our customers to browse our stores by displaying our frequently changing assortment of products on rolling tables, pallets and other display fixtures. Our store team leaders are responsible for maintaining our treasure

hunt shopping experience, keeping the stores clean and well-lit and ensuring our customers are engaged. We believe our humorous brand image, compelling values and welcoming stores resonate with our customers and define Ollie’s as a unique and

comfortable destination shopping location.

Expansion opportunities and site selection

We believe we can profitably expand our store count on a national scale to more than 1,300 locations based on internal estimates and third party research conducted by Hoffman Strategy Group. Our

disciplined real estate strategy focuses on infilling existing geographies as well as expanding into contiguous markets in order to leverage our distribution infrastructure, field management team, store management, marketing investments and brand

awareness.

We maintain a pipeline of real estate sites that have been approved by our real estate committee. Our recent store growth is summarized in the following table:

|

|

2023

|

2022

|

2021

|

|||||||||

|

Stores open at beginning of year

|

468

|

431

|

388

|

|||||||||

|

Stores opened

|

45

|

40

|

46

|

|||||||||

|

Stores closed

|

(1

|

)

|

(3

|

)

|

(3

|

)

|

||||||

|

Stores open at end of year

|

512

|

468

|

431

|

|||||||||

We utilize a rigorous site selection and real estate approval process in order to leverage our infrastructure, marketing investments and brand awareness. Members of our real estate team spend

considerable time evaluating prospective sites before bringing a new lease proposal to our real estate committee, which is comprised of senior management and executive officers. Our flexible store layout allows us to quickly take over a variety of

low-cost, second-generation sites, including former big box retail and grocery stores.

We believe there is an ample supply of suitable low-cost, second-generation real estate allowing us to infill within our existing markets as well as to expand into new, contiguous geographies. By

focusing on key characteristics such as proximity to the nearest Ollie’s store, ability to leverage distribution infrastructure, visibility, traffic counts, population densities of at least 40,000 people within ten miles and low rent per square foot,

we have developed a new store real estate model that has consistently delivered attractive returns on invested capital.

Our strong unit growth is supported by our predictable and compelling new store model. We target a store size between 25,000 to 35,000 square feet and an average initial cash investment of approximately

$1.0 million, which includes store fixtures and equipment, store-level and distribution center inventory (net of payables) and pre-opening expenses. With our

relatively low investment costs and strong new store opening performance, we target first-year annual new store sales of approximately $4.0 million. New stores have consistently opened strong, with higher net sales in their first 12 months of

operations, than average existing stores due to brand excitement surrounding grand openings and produced an average payback period of approximately two years. We believe that our consistent store performance, corporate infrastructure, including our

distribution centers, and disciplined approach to site selection support the portability and predictability of our new unit growth strategy.

Store-level management and training

Our Vice President of Store Operations oversees all store activities. Our stores are grouped into five regions, divided generally along geographic lines. We employ regional directors, who have

responsibility for the day-to-day operations of the stores in their region. Reporting to the regional directors are district team leaders and market team leaders who each manage a group of stores in their markets. At the store level, the leadership

team consists of a store team leader and potentially a co-team leader and/or an assistant team leader, who supervise the full and part-time associated within the store.

Each store team leader is responsible for the daily operations of the store, including the processing of merchandise to the sales floor and the presentation of goods throughout the store. Store team

leaders are trained to maintain a clean and appealing store environment for our customers. Store team leaders and co-team leaders are also responsible for the hiring, training, and development of associates.

We work tirelessly to hire talented people, to improve our ability to assess talent during the interview process and to regularly train those individuals at Ollie’s who are responsible for interviewing

candidates. We also devote substantial resources to training our new managers through our Team Leader Training Program. This program operates at designated training stores located across our footprint. It provides an in-depth review of our

operations, including merchandising, policies and procedures, asset protection and safety, and human resources. Part-time associates receive structured training as part of their onboarding.

For additional information on store-level management training and initiatives by the Company, see the discussion of Human Capital below.

Marketing and advertising

Our marketing and advertising campaigns feature colorful caricatures and witty sayings in order to make our customers laugh. We believe that by disarming our customers by getting them to giggle a bit,

they are able to look at and trust our products for what they are—extremely great bargains. Our distinctive and often self-deprecating humor and highly recognizable caricatures are used in all of our stores, flyers and advertising campaigns.

We tailor our marketing mix and strategy for each market, deal or promotion. We primarily use the following forms of marketing and advertising:

| • |

Print and direct mail: During 2023, we distributed over 650 million highly recognizable flyers. Our flyers are typically distributed

semi-monthly, for a total of 22 times per year, with increased frequency in peak shopping periods, and serve as the foundation of our marketing strategy to remain top of mind with our shoppers. They highlight

current deals to create shopping urgency and drive traffic and increase frequency of store visits;

|

| • |

Television and radio: We selectively utilize creative television/over the top television (“OTT”) and radio

advertising campaigns in targeted markets throughout the year, to create brand awareness and support new store openings;

|

| • |

Charity and community events: We are dedicated to maintaining a visible presence in the communities in which our stores are located through the sponsorship of charitable

organizations such as Feeding America, Toys for Tots, Children’s Miracle Network, and the Cal Ripken, Sr. Foundation. We believe supporting these organizations promotes our brand, underscores our values and builds a sense of community; and

|

| • |

Digital marketing and social media: We maintain an active online presence and promote our brand through our website, our mobile app, and digital and social media platforms,

including influencers across TikTok, Instagram, YouTube and Facebook. We also utilize targeted email marketing to highlight our latest brand name offerings and drive traffic to our stores.

|

Ollie’s Army

Our customer loyalty program, Ollie’s Army, stands at 14.0 million members as of February 3, 2024, an increase of 5.9% from 2022. In 2023, Ollie’s Army members accounted for over 82% of net sales and

spent approximately 40% more per shopping trip, on average, than non-members. Consistent with our marketing strategy, we engage new and existing Ollie’s Army members through the use of witty phrases and signage; examples include “Enlist in Ollie’s

Army today,” “become one of the few, the cheap, the proud” and “Ollie’s Army Boot Camp…all enlistees will receive 15% off their next purchase.” Throughout the year, for every $250 Ollie’s Army members spend, they receive a coupon for 10% off their

next entire purchase. Ollie’s Army ‘ranks’ are another savings opportunity for members. For the first $250 and $500 members spend in a calendar year, they receive a coupon for 20% and 30% off of one item, respectively. Historically, Ollie’s Army

members have demonstrated high redemption rates for promotional activities exclusive to Ollie’s Army members, such as our Valentine’s, Boot Camp, and 15% off holiday mailers. In addition, Ollie’s Army members have historically enthusiastically

responded to Ollie’s Army Night, an annual one-day after-hours sale in December exclusively for members. We expect to continue leveraging the data gathered from our proprietary database of Ollie’s Army members to better segment and target our

marketing initiatives and increase shopping frequency.

Competition

We compete with a diverse group of retailers, including discount, closeout, mass merchant, department, grocery, drug, convenience, hardware, variety, online, and other specialty stores.

The principal basis on which we compete against other retailers is by offering an ever-changing selection of brand name products at compelling price points in an exciting shopping environment.

Accordingly, we compete against a fragmented group of retailers, wholesalers, and jobbers to acquire merchandise for sale in our stores.

Our established relationships with our suppliers, coupled with our scale, associated buying power, financial credibility and responsiveness, often makes Ollie’s the first call for available deals. Our

direct relationships with suppliers have increased as we have grown, and we continuously strive to broaden our supplier network.

Trademarks and other intellectual property

We own multiple state and federally registered trademarks related to our brand, including “Ollie’s,” “Ollie’s Bargain Outlet,” “Good Stuff Cheap,” “Ollie’s Army,” “Real Brands Real Cheap!,” and “Real

Brands! Real Bargains!,” among others. In addition, we maintain a federal trademark for the image of Ollie, the face of our company. We also own registered trademarks for many of our private labels such as “Sarasota Breeze,” “Steelton Tools,”

“American Way,” and “Middleton Home,” among others. We routinely prosecute trademarks where appropriate, both for private label goods and to further identify our goods and services. We enter into trademark license agreements as necessary, which may

include our private label offerings, such as the Magnavox products available in our stores. Our trademark registrations have various expiration dates; however, assuming that the trademark registrations are properly renewed, they have a perpetual

duration. We also own several domain names, including www.ollies.us, www.ollies.com, www.olliesbargainoutlet.com, www.olliesarmy.com, www.ollies.cheap, www.sarasotabreeze.com and www.olliesmail.com, and

unregistered copyrights in our website content. We attempt to obtain registration of our trademarks and other intellectual property as practical and pursue infringement of those marks when appropriate.

Technology

Our management information systems provide a full range of business process assistance and timely information to support our merchandising team and strategy, management of multiple distribution centers,

stores and operations, and financial reporting. We believe our current systems provide us with operational efficiencies, scalability, management control, and timely reporting that allow us to identify and respond to merchandising and operating trends

in our business. We use a combination of internal and external resources to support store point-of-sale, merchandise acquisition and distribution, inventory management, financial reporting, real estate, and administrative functions. We continuously

assess ways to maximize productivity and efficiency, as well as evaluate opportunities to further enhance our existing systems. Our existing systems are scalable to support future growth.

Government regulation

We are subject to state and federal laws including labor and employment laws, including minimum wage requirements and wage and hour laws, laws governing advertising, privacy laws, safety regulations,

environmental laws and regulations, and other laws, including consumer protection regulations that regulate retailers and/or govern product standards, the promotion and sale of merchandise and the operation of stores and warehouse facilities. We

monitor changes in these laws and believe that we are in material compliance with all applicable laws.

We source a portion of our products from outside the United States. The U.S. Foreign Corrupt Practices Act and other similar anti-bribery and anti-kickback laws and regulations generally prohibit

companies and their intermediaries from making improper payments to non-U.S. officials for the purpose of obtaining or retaining business. Our policies and our vendor code of conduct mandate compliance with applicable law, including these laws and

regulations.

Human Capital

Attracting, developing, and retaining quality talent is key to our growth, and our success depends on cultivating an engaged and motivated workforce. We work hard to create an environment where Ollie’s team members can build fulfilling careers and we take pride in providing opportunities for growth and development.

We seek to build a diverse and inclusive workplace where we can leverage our collective talents, striving to ensure that all associates are treated with dignity and respect. We

believe that a workforce with a diversity of viewpoints, background, experience and industry knowledge, as well as more traditional characteristics of diversity, such as race and gender, are key to our culture and long-term success. We are committed

to providing equal employment opportunities and advancement consideration to all individuals based on job-related qualifications and ability to perform the job as well as maintaining an environment that is free of intimidation or harassment. We

value the talents and contributions of our associates and by focusing on our team members we know that the entire Ollie’s community will be well served.

Oversight and Management

Our Human Resources department manages all associate matters, including recruiting, hiring, compensation and benefits, performance management, and associate training. In addition, our management team works closely with

the Human Resources department to evaluate associate management issues such as retention and workplace safety. As we strive to retain and engage talent at all levels of our business, our Human Resources department also reviews our retention and

turnover rates and administers our talent and training programs and review process to support the development of our talent pipeline.

Associates

As of February 3, 2024, we employed over 11,500 associates, approximately 5,500 of whom were full-time and approximately 6,000 of whom were part-time. Of our total associate base, approximately 1,100 were based at our

store support center and distribution centers, and the remaining were store and field associates. The number of associates in a fiscal year fluctuates depending on the business needs at different times of the year. As

of February 3, 2024, approximately 60% of our workforce is self-identified female and approximately 40% is self-identified male. Over 40% of our workforce has self-identified as having a racial or ethnic minority background. None of our

associates belong to a union or are party to any collective bargaining or similar agreement.

Associate Training and Development Programs

We offer a compelling work environment with meaningful growth and career-development opportunities. This starts with the opportunity to do challenging work and learn on the job and is supplemented by

programs and continuous learning that help our team build skills to advance. We encourage a “promote-from-within” environment when internal resources permit. We also provide internal leadership development programs designed to prepare our

high-potential team members for greater responsibility. We believe internal promotions, coupled with the hiring of individuals with previous retail experience, will provide the management structure necessary to support our long-term strategic

growth initiatives.

Our Ollie’s Leadership Institute (“OLI”) is a program that is used to equip field associates with the ability to advance their career. Each OLI participant receives an individual development plan, designed to prepare

them for their next level position. Reflecting our belief in our “home grown” talent, OLI is our preferred source for new supervisors and team leaders. In 2023, over 45% of our current district team leaders were internally promoted to their

position. Company-wide, over 60% of our field positions were filled by internal promotions. We believe our training and development programs help create a positive work environment and result in stores that operate at a high level.

Compensation and Benefits

We are committed to providing market-competitive compensation for all positions. Eligible team members participate in one of our various bonus incentive programs, which provide the

opportunity to receive additional compensation based upon store and/or Company performance. In addition, we provide our eligible team members the opportunity to participate in a 401(k) retirement savings plan with a Company-sponsored match. We

also share in the cost of health insurance provided to eligible team members, and team members receive a discount on merchandise purchased from the Company. We additionally provide our team members with paid time off.

Workplace Health and Safety

Maintaining a safe and secure work environment is very important to us and we conduct our business in an environmentally sound manner based on customer needs and local requirements. To further promote a safe work

environment, we have established safety training programs. This includes administering an occupational injury- and illness-prevention program, together with an employee assistance program for team members.

Seasonality

Our business is seasonal in nature and demand is generally the highest in our fourth fiscal quarter due to the holiday sales season. To prepare for the holiday sales season, we must order and keep in stock more

merchandise than we carry during other times of the year and generally engage in additional marketing efforts. We expect inventory levels, along with accounts payable and accrued expenses, to reach their highest levels in our third and fourth fiscal

quarters in anticipation of increased net sales during the holiday sales season. As a result of this seasonality, and generally because of variation in consumer spending habits, we experience fluctuations in net sales and working capital

requirements during the year. Because we offer a broad selection of merchandise at extreme values, we believe we are generally less impacted than other retailers by economic cycles, which correspond with declines in general consumer spending habits

and we believe we still benefit from periods of increased consumer spending.

Available Information

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities and Exchange Act are

available free of charge on our website, www.ollies.us, as soon as reasonably practicable after the electronic filing of such reports with the Securities and Exchange Commission (“SEC”). The SEC maintains a website (www.sec.gov) that contains

reports, proxy, and information statements and other information regarding issuers that file electronically with the SEC.

| ITEM 1A. |

RISK FACTORS

|

Investing in our common stock involves a high degree of risk. You should carefully consider the following risk factors, as well as other information in this Annual Report on Form

10-K, before deciding whether to invest in the shares of our common stock. The occurrence of any of the events described below could have a material adverse effect on our business, financial condition, or results of operations. In the case of such an

event, the trading price of our common stock may decline, and you may lose all or part of your investment.

RISK FACTOR SUMMARY

We are providing the following summary of the risk factors contained in our Form 10-K to enhance the readability and accessibility of our risk factor disclosures. We encourage our stockholders to

carefully review the full risk factors contained in this Form 10-K in their entirety for additional information regarding the risks and uncertainties that could cause our actual results to vary materially from recent results or from our anticipated

future results.

Risks Related to Business and Operations

| • |

We may not be able to execute our opportunistic buying strategy;

|

| • |

Fluctuations in comparable store sales and results of operations, including fluctuations on a quarterly basis, could cause our business performance to decline substantially, as comparable store sales

and results of operations have fluctuated in the past and may do so again in the future;

|

| • |

Consumer confidence and spending may be reduced in light of factors beyond our control and our results of operations and financial results may suffer;

|

| • |

Competition may increase in our segment of the retail market, which could put negative pressure on our results of operations and financial condition;

|

| • |

Identification of potential store locations and lease negotiations may not keep pace with our growth strategy;

|

| • |

We are a “brick and mortar only” retailer. Our lack of an online shopping option and an omnichannel customer experience may mean that we could face challenges to grow and retain customers. Our customers, including our Ollie’s Army

loyalty program members, may determine to shop at other stores or through web- and mobile-enabled services and therefore may not be as likely to shop at our stores;

|

| • |

We may not be able to develop and operate our distribution centers in an efficient or effective manner and that may result in not having sufficient inventory in our stores.

|

| • |

The loss or disruption of one or more of our distribution centers or disruption of our supply chain or third-party shipping carriers could also make it difficult for us to timely

receive or distribute merchandise to our stores;

|

| • |

External economic pressures over which we have no or limited control, including among other items inflation, a significant decline in economic activity across the economy, occupancy costs, and transportation costs may reduce our

profitability;

|

| • |

Shrinkage or the loss or theft of inventory and/or inventory management may result in material negative impacts on our results of operations;

|

| • |

We may not be able to hire and retain the right people to run our stores and our distribution centers. We also may not be able to hire and retain managerial personnel, the

appropriate merchant team for our retail segment, and the senior management team and executive officers sufficient to meet our goals. As a consequence, our results of operations and financial results may suffer; and

|

Risks Related to Legal and Regulatory Issues

| • |

We are subject to governmental laws, regulations, procedures, and requirements that can lead to substantial penalties if we fail to achieve and/or maintain compliance;

|

| • |

We are subject to risks associated with laws and regulations generally applicable to retailers and the risks associated with failing to comply with these laws and regulations;

|

| • |

From time to time, we are involved in legal proceedings from customers, suppliers, other vendors, employees, governments and governmental agencies, or competitors;

|

| • |

From time to time, we are involved in legal proceedings from stockholders; and

|

| • |

Legislative, regulatory and other actions resulting from the November 2024 elections for the U.S. President and the U.S. Congress are unpredictable and could have unforeseen consequences that could materially,

adversely affect our business, financial position, results of operations, and cash flows. Without limiting the generality of the foregoing statement, certain proposals regarding federal corporate tax reform and border-adjusted taxes, taxes

levied on imported goods, may result in a material adverse effect on our financial position, results of operations, and cash flows.

|

Risks Related to Technology and Cybersecurity

| • |

We may fail to maintain the security of information we hold relating to personal information or payment card data of our customers, employees, and suppliers;

|

| • |

We may not adequately prepare for, or respond to, existing and future privacy legislation; and

|

| • |

We may not be able to timely or adequately maintain or upgrade our technology systems needed for operations.

|

Risks Related to Accounting and Financial Matters

| • |

If our estimates or judgments relating to significant accounting policies prove to be incorrect, we could suffer negative financial results; and

|

| • |

Changes to the accounting rules or regulations could have material adverse effects on our results of operations.

|

Risks Related to Ownership of Our Common Stock and Corporate Governance

| • |

There is risk associated with our fluctuating quarterly operating results and we may fall short of prior periods, our projections, or the expectations of securities analysts or investors;

|

| • |

We may not declare dividends on our common stock in the foreseeable future; and

|

| • |

There are provisions in our organizational documents that could delay or prevent a change of control.

|

Risks Related to Our Indebtedness and Capitalization

| • |

Our credit facility can limit our ability to find other sources of financing;

|

| • |

There are covenants contained in our credit facility that we must meet in order to be able to use it;

|

| • |

If we are unable to generate sufficient cash flow to meet debt service, it could negatively impact our liquidity; and

|

| • |

We cannot guarantee that our share repurchase program will be fully consummated or that it will enhance long-term stockholder value.

|

For a more complete discussion of the material risks facing our business, see below.

BUSINESS AND OPERATIONS

We may not be able to execute our opportunistic buying strategy, adequately manage our supply of inventory, or anticipate customer demand, which could have a

material adverse effect on our business, financial condition, and results of operations.

Our business is dependent on our ability to strategically source a sufficient volume and variety of brand name merchandise at opportunistic pricing. We do not have significant control over the supply,

design, function, cost, or availability of much of the merchandise that we offer for sale in our stores. Additionally, because we source a substantial amount of our merchandise from suppliers on a closeout basis, or with significantly reduced prices

for various reasons, we are not always able to purchase specific merchandise on a recurring basis. We do not have long-term contracts with our suppliers and, therefore, we have no contractual assurances of pricing or access to merchandise, and any

supplier could discontinue sales to us at any time or offer us less favorable terms on future transactions. Our merchant team generally makes individual purchase decisions for merchandise that becomes available, and these purchases may be for large

quantities that we may not be able to sell on a timely or cost-effective basis. To the extent that certain of our suppliers are better able to manage their inventory levels and reduce the amount of their excess inventory, the amount of discount or

closeout merchandise available to us could also be materially reduced, potentially compromising our profit margin goals for procured merchandise. Due to economic uncertainties, governmental orders, or other challenges, one or more of our suppliers

could become unable to continue supplying discounted or closeout merchandise on terms or in quantities acceptable or desirable to us. We also compete with other retailers, wholesalers, and jobbers for discounted and closeout merchandise to sell in

our stores. Those businesses may be better able to anticipate customer demand or procure desirable merchandise. Shortages or disruptions in the availability of brand name or unbranded merchandise of a quality acceptable to our customers and to us

could have a material adverse effect on our business, financial condition, and results of operations and also may result in customer dissatisfaction. In addition, we may significantly overstock merchandise that proves to be undesirable and be forced

to take significant markdowns. We cannot ensure that our merchant team will continue to identify the appropriate customer demand and take advantage of appropriate buying opportunities, which could have a material adverse effect on our business,

financial condition, and results of operations.

Risks associated with or faced by our suppliers could adversely affect our results of operations and financial performance.

We source our merchandise from a variety of suppliers, and we depend on them to supply merchandise in a timely and efficient manner. If one or more of our current suppliers became unable to supply

merchandise, seeking alternative sources could increase our merchandise costs and supply chain lead time, potentially resulting in temporary reductions in store inventory levels, and could reduce the selection and quality of our merchandise. An

inability to obtain alternative sources could materially decrease our sales. Additionally, if a supplier fails to deliver on its commitments, we could experience merchandise out-of-stocks that could lead to lost sales and reputational harm.

Further, failure of suppliers to meet our compliance protocols could prolong our procurement lead time, resulting in lost sales and adverse margin impact. Changes to the prices and flow of certain merchandise is, at times, beyond our control for

reasons that include, among others: political or civil unrest, acts of war, currency fluctuations, disruptions in maritime lanes, port labor disputes, economic conditions and instability in countries in which foreign suppliers are located, the

financial instability of suppliers, failure to meet our terms and conditions or our standards, issues with our suppliers’ labor practices or labor disruptions they may experience (such as strikes, stoppages or slowdowns, which could also increase

labor costs during and following the disruption), the availability and cost of raw materials, pandemic outbreaks, merchandise quality or safety issues, transport availability and cost, increases in wage rates and taxes, transport security, inflation,

and other factors relating to suppliers. Any such circumstances could adversely affect our results of operations and profitability.

Fluctuations in comparable store sales and results of operations, including fluctuations on a quarterly basis, could cause our business performance to decline

substantially.

Our results of operations have fluctuated in the past, including on a quarterly basis, and can be expected to continue to fluctuate in the future.

Our comparable store sales and results of operations are affected by a variety of factors, including without limitation:

|

|

• |

national and regional economic trends in the United States;

|

|

|

• |

changes in gasoline prices;

|

|

|

• |

changes in shipping and transportation costs;

|

|

|

• |

changes in our merchandise mix;

|

|

|

• |

the weather;

|

|

|

• |

changes in pricing;

|

|

|

• |

changes in the timing of promotional and advertising efforts; and

|

|

|

• |

holidays or seasonal periods.

|

If our future comparable store sales fail to meet expectations, then our cash flow and profitability may decline substantially, which could have a material adverse effect on our business, financial condition, and

results of operations.

We rely on third parties to move merchandise through ports and transport them from ports to our centralized distribution centers.

Our ability to timely and effectively deliver merchandise to our stores relies in part on shipping and transportation partners to timely and safely move our merchandise from manufacturing facilities to

ports and then onto oceangoing carriers. The demand for space onboard oceangoing vessels can vary and costs to secure space can vary greatly. We may be subject to higher transportation costs or be unable to secure space for containers on

economically reasonable terms. In addition, there may be labor or other disputes at either ports of departure or at ports of entry that may delay or otherwise hinder the flow of merchandise. Additional factors, such as customs or border control

policies and unanticipated tariffs, such as additional or new import tariffs, may further delay or hinder transportation of merchandise or the costs to obtain them. There are multiple factors in the transportation of merchandise that are both

outside of our control and which may negatively impact the cost of the merchandise or the timeframes in which we receive the same.

Factors such as inflation, cost increases, and energy prices could have a material adverse effect on our business, financial condition, and results of operations.

Future increases in costs, such as the cost of labor, merchandise, shipping rates, freight and other transportation costs (including import costs), and store occupancy costs, may reduce our

profitability, given our pricing model. These cost increases may be the result of inflationary pressures, geopolitical factors, or public policies, which could further reduce our sales or profitability. Increases in other operating costs, including

changes in energy prices, wage rates, and lease and utility costs, may increase our cost of merchandise sold or selling, general, and administrative expenses. Our low-price model and competitive pressures in our industry may inhibit our ability to

reflect these increased costs in the prices of our merchandise and, therefore, reduce our profitability and have a material adverse effect on our business, financial condition, and results of operations.

Our ability to generate revenue is dependent on consumer confidence and spending, which may be subject to factors beyond our control, including changes in economic and political

conditions, as well as health concerns.

The success of our business depends, to a significant extent, on the level of consumer confidence and spending. A number of factors beyond our control affect the level of customer confidence and spending on the

merchandise that we sell, including, among other items:

|

|

• |

energy and gasoline prices;

|

|

|

• |

shipping and transportation costs;

|

|

|

• |

disposable income of our customers, which is impacted by unemployment levels, personal debt levels, and wages;

|

|

|

• |

interest rates and inflation;

|

|

|

• |

discounts, promotions, and merchandise offered by our competitors;

|

|

|

• |

negative reports and publicity about the discount retail industry;

|

|

|

• |

outbreak of viruses or widespread illness, and behavioral changes from a fear of contracting such viruses or illness;

|

|

|

• |

general economic and industry conditions;

|

|

|

• |

food prices;

|

|

|

• |

the state of the housing market;

|

|

|

• |

customer confidence in future economic conditions;

|

|

|

• |

fluctuations in the financial markets;

|

|

|

• |

government sponsored relief packages and governmental benefits, such as social security benefits, as affected by current cost of living adjustments, as well as any government stimulus payments and enhanced

unemployment benefits;

|

|

|

• |

tax rates and policies; and

|

|

|

• |

natural disasters, war, terrorism, and other hostilities.

|

Reduced customer confidence and spending may result in reduced demand for our merchandise, including discretionary items, and may force us to take inventory markdowns. Reduced demand also may require increased selling

and promotional expenses. Adverse economic conditions and any related decrease in customer demand for our merchandise could have a material adverse effect on our business, financial condition, and results of operations.

Many of the factors identified above also affect commodity rates, transportation costs, costs of labor, insurance, and healthcare, the strength of the U.S. dollar, lease costs, measures that create barriers to or

increase the costs associated with international trade, changes in other laws and regulations, and other economic factors, all of which may impact our cost of merchandise sold and our selling, general, and

administrative expenses, which could have a material adverse effect on our business, financial condition, and results of operations.

We do not compete in the growing online and omnichannel retail marketplace, which could have a material adverse effect on our business, financial condition, and

results of operations.

Our long-term business strategy does not presently include the development of online retailing capabilities or offering of an omnichannel shopping experience. To the extent that we implement online

operations, we would incur substantial expenses related to such activities and would be exposed to additional risks, including additional cybersecurity risk. Furthermore, the development of an online retail marketplace is a complex undertaking, and

there is no guarantee that the resources we apply to this effort will result in any material increased revenues or better overall operating performance. However, with the growing acceptance of online and omnichannel shopping, which may have

accelerated as a result of the COVID-19 pandemic, both among consumers who previously shopped online and consumers who did not previously do so, or did not do so as frequently, we may continue to face challenges related to customers shopping in

brick-and-mortar stores. In addition, the increased proliferation of mobile devices and enhanced and robust connections to mobile networks, competition from other retailers in the online and omnichannel retail marketplace is expected to continue to