UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2021

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO | |||||

Commission File Number 001-37534

(Exact name of Registrant as specified in its Charter)

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | ||||

(Address of Principal Executive Offices and Zip Code)

(603 ) 750-0001

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). Yes ☒ NO ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer a smaller reporting company or an emerging growth company. See the definitions of the “large accelerated filer,” “accelerated filer,” “non-accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

| ☒ | Accelerated filer | ☐ | ||||||||||||||||||

| Non-accelerated filer | ☐ | Small reporting company | ||||||||||||||||||

| Emerging Growth Company | ||||||||||||||||||||

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes ☒ No ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the Registrant’s Class A common stock held by non-affiliates, computed by reference to the last reported sale price of the Class A common stock as reported on the New York Stock Exchange on June 30, 2021 was approximately $6.3 billion.

The number of outstanding shares of the registrant’s Class A common stock, par value $0.0001 per share, and Class B common stock, par value $0.0001 per share, as of February 24, 2022 was 84,331,677 shares and 6,693,897 shares, respectively.

DOCUMENTS INCORPORATED BY REFERENCE

Table of Contents

| Page | ||||||||

| PART I | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| PART II | ||||||||

| Item 5. | ||||||||

| Item 6. | (Reserved) | |||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| Item 9C | Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | |||||||

| PART III | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| PART IV | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

2

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Such forward-looking statements reflect, among other things, our current expectations and anticipated results of operations, all of which are subject to known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements, market trends, or industry results to differ materially from those expressed or implied by such forward-looking statements. Therefore, any statements contained herein that are not statements of historical fact may be forward-looking statements and should be evaluated as such. Without limiting the foregoing, the words “anticipates,” “believes,” “estimates,” “expects,” “intends,” “may,” “plans,” “projects,” “should,” “targets,” “will” and the negative thereof and similar words and expressions are intended to identify forward-looking statements. These forward-looking statements are subject to a number of risks, uncertainties and assumptions, including those described in “Item 1A. – Risk Factors,” of this report. Unless legally required, we assume no obligation to update any such forward-looking information to reflect actual results or changes in the factors affecting such forward-looking information.

3

PART I

Item 1. Business.

Planet Fitness, Inc. is a Delaware corporation formed on March 16, 2015. Planet Fitness, Inc. Class A common stock trades on the New York Stock Exchange under the symbol “PLNT.”

Our Company

Fitness for everyone

We are one of the largest and fastest-growing franchisors and operators of fitness centers in the United States by number of members and locations, with a highly recognized national brand. Our mission is to enhance people’s lives by providing a high-quality fitness experience in a welcoming, non-intimidating environment, which we call the Judgement Free Zone. Our bright, clean stores are typically 20,000 square feet, with a large selection of high-quality, purple and yellow Planet Fitness-branded cardio, circuit- and weight-training equipment and friendly staff trainers who offer unlimited free fitness instruction to all our members in small groups through our PE@PF program. We offer this differentiated fitness experience at only $10 per month for our standard membership. This attractive value proposition is designed to appeal to a broad population, including occasional gym users and the approximately 80% of the U.S. and Canadian populations over age 14 who do not belong to a gym, particularly those who find the traditional fitness club setting intimidating and expensive. We and our franchisees fiercely protect Planet Fitness’s community atmosphere—a place where you do not need to be fit before joining and where progress toward achieving your fitness goals (big or small) is supported and applauded by our staff and fellow members.

In 2021, we recorded revenues of $587.0 million and system-wide sales of $3.4 billion (which we define as monthly dues and annual fees billed by us and our franchisees). We ended the year with approximately 15.2 million members and 2,254 stores in all 50 states, the District of Columbia, Puerto Rico, Canada, Panama, Mexico and Australia. System-wide sales for 2021 include $3.2 billion attributable to franchisee-owned stores, from which we generate royalty revenue, and $170.7 million attributable to our corporate-owned stores. Of our 2,254 stores, 2,142 are franchised and 112 are corporate-owned. Under signed area development agreements (“ADAs”) as of December 31, 2021, our franchisees have committed to open more than 1,000 additional stores.

In 2021, our corporate-owned stores had a segment EBITDA margin of 29.4% and had average unit volumes (“AUVs”) of approximately $1.6 million with four-wall EBITDA margins (an assessment of store-level profitability which includes local and national advertising expense) of approximately 34.0%, or approximately 26.9% after applying the current 7% royalty rate. Based on franchisee business reviews and management estimates since the onset of COVID-19, we believe that, on average, franchisee stores achieve four-wall EBITDA margins in line with, or higher than these corporate-owned store four-wall EBITDA margins. For a reconciliation of segment EBITDA margin to four-wall EBITDA margin for corporate-owned stores, see “Management’s Discussion and Analysis of Results of Operations and Financial Condition.”

Our growth is reflected in:

•2,254 stores as of December 31, 2021, compared to 1,518 as of December 31, 2017, reflecting a compound annual growth rate (“CAGR”) of 10.4%;

•15.2 million members as of December 31, 2021, compared to 10.6 million as of December 31, 2017, reflecting a CAGR of 9.4%;

•53 consecutive quarters of system-wide same store sales growth through the first quarter of 2020, with a return to system-wide same store sales growth in the third and fourth quarter of 2021 (which we define as year-over-year growth solely of monthly dues from stores that have been open and for which membership dues have been billed for longer than 12 months);

4

Planet Fitness – Home of the Judgement Free Zone

We bring fitness to a large, previously underserved segment of the population. Our differentiated member experience is driven by three key elements:

•Welcoming, non-intimidating environment: We believe fitness is essential to both physical and mental health, and every member should feel accepted and respected when they walk into a Planet Fitness regardless of their fitness level. Our stores provide a Judgement Free Zone where members can experience a non-intimidating and supportive environment. Our “come as you are” approach has fostered a strong sense of community among our members, allowing them not only to feel comfortable as they work toward their fitness goals but also to encourage others to do the same. By outfitting our stores with more cardiovascular and light strength equipment, and a limited offering of heavy free weights, we seek to reinforce our Judgement Free Zone philosophy by discouraging what we call “Lunk” behavior, such as dropping weights and grunting, that can be intimidating to new and occasional gym users.

•Distinct store experience: Because our stores are typically 20,000 square feet and we do not offer non-essential amenities such as group exercise classes, pools, day care centers and juice bars, we have more space for the equipment our members do use. We believe our tailored use of space is, at least in part, why we have not needed to impose time limits on our cardio machines. Part of our unique store experience is the diligence our members and employees have to maintain a clean and sanitized environment. Members’ etiquette typically includes wiping down the equipment before and after use with our sanitization spray, which is FDA-approved to kill the COVID-19 virus on surfaces.

•Exceptional value for members: In the U.S., for only $10 per month, our standard membership includes unlimited access to one Planet Fitness location and unlimited free fitness instruction to all members in small groups through our PE@PF program. And, for approximately $22.99 per month, our PF Black Card members have access to all of our stores system-wide and can bring a guest on each visit, which provides an additional opportunity to attract new members. Our PF Black Card members also have access to exclusive areas in our stores that provide amenities such as water massage beds, massage chairs, tanning equipment and more.

Our competitive strengths

We attribute our success to the following strengths:

•Market leader with differentiated member experience, nationally recognized brand and scale advantage. We are one of the largest and fastest-growing franchisors and operators of fitness centers in the United States by number of members and locations, with a highly recognized national brand.

•Differentiated member experience. Planet Fitness is the home of the Judgement Free Zone, a place where people of all fitness levels can feel comfortable working out at their own pace, feel supported in their efforts and not feel intimidated by pushy salespeople or other members who may ruin their fitness experience. Our philosophy is simple: Planet Fitness is an environment where members can relax, go at their own pace and be themselves without ever having to worry about being judged. No matter what size the goal, we believe that all of these accomplishments deserve to be celebrated.

•Nationally recognized brand. We have developed a highly relatable and recognizable brand focused on providing our members with a judgement-free environment. We do so through fun and memorable marketing campaigns and in-store signage. As a result, we have among the highest aided and unaided brand awareness scores in the U.S. fitness industry, according to our Brand Health research, a third-party consumer study that we have updated bi-annually.

•Scale advantage. Our scale provides several competitive advantages, including enhanced purchasing power and extended warranties with our fitness equipment and other suppliers and the ability to attract high-quality franchisee partners. In addition, we estimate that our large U.S. national advertising fund, funded by franchisees and us, together with our requirement that franchisees spend 7% of their monthly membership dues on local advertising, enabled us and our franchisees to spend over $225 million in 2021.

•Exceptional value proposition that appeals to a broad member demographic. Our low monthly membership dues combined with our non-intimidating and welcoming environment, enable us to attract a broad member demographic based on age, household income, gender and ethnicity. Our member base is over 50% female and our members come from both high- and low-income households. Approximately 20% of our stores are located in areas that the US government deems “low income,” providing access to improve health and wellness in underserved communities. Our broad appeal and ability to attract occasional and first-time gym users enable us to continue to target a large segment of the population in a variety of markets and geographies.

5

•Highly attractive franchise system built for growth. Our easy-to-operate model, strong store-level economics and brand strength have enabled us to attract a team of professional, successful franchisees from a variety of industries. We believe that our strategy to be predominantly franchisee-owned enables us to scale more rapidly than a predominantly company-owned strategy. Our streamlined model features relatively fixed labor costs, minimal inventory, automatic billing and limited cash transactions. The attractiveness of our franchise model is further evidenced by the fact that our franchisees re-invest their capital into the brand, with over 90% of our new stores in 2021 opened by our existing franchisee base. We view our franchisees as strategic partners in expanding the Planet Fitness store base and brand.

•Predictable and recurring revenue streams with high cash flow conversion. While 2020 brought an unprecedented disruption to the general economy, our industry and our business, when operating in a normal business environment, our model provides us with predictable and recurring revenue streams. In 2021, approximately 90% of both our corporate-owned store and franchise revenues consisted of recurring revenue streams, which include royalties, vendor commissions, monthly dues and annual fees. Generally our franchisees are obligated to purchase fitness equipment from us or our required vendor for their new stores and to replace this equipment approximately every five to seven years. As a result, these “equip” and “re-equip” requirements create a predictable and growing revenue stream as our franchisees open new stores under their ADAs.

Our growth strategies

We believe there are significant opportunities to grow our brand awareness, increase our revenues and profitability and deliver shareholder value by executing on the following strategies:

•Continue to grow our store base across a broad range of markets. We have grown our store count over the last five years, expanding from 1,518 stores as of December 31, 2017 to 2,254 stores as of December 31, 2021. As of December 31, 2021, our franchisees have signed ADAs to open more than 1,000 additional stores, including more than 500 over the next three years. Because our stores are successful across a wide range of geographies and demographics with varying population densities, we believe that our high level of brand awareness and low per capita penetration in certain markets create a significant opportunity to open new Planet Fitness stores. Based on our internal and third party analysis, we believe we have the potential to grow our store base to over 4,000 stores in the U.S. alone.

◦Drive revenue growth and system-wide same store sales. We have a significant history of positive system-wide same store sales growth, reaching 53 consecutive quarters through the first quarter of 2020, prior to the impact of the COVID-19 pandemic, with a return to system-wide same store sales growth in the third and fourth quarter of 2021. We expect to achieve system-wide same store sales growth primarily by:

•Attracting new members to existing Planet Fitness stores. As the population in the markets where we operate continue to focus on health and wellness, we believe we are well-positioned to capture a disproportionate share of these populations given our affordability and appeal to first-time and occasional gym users. We continue to evolve our offerings and enhance the PE@PF Program, our proprietary small group training program to appeal to our target member base. In addition to our in store experience, we also provide more than 500 workouts to both existing members and prospects via the free Planet Fitness mobile app, featuring differentiated content geared toward engaging with our community outside of our four walls and providing more ways to connect to our target audience – first time and casual gym users.

•Increasing mix of PF Black Card memberships by enhancing value and member experience. We expect to drive sales by attracting new members to join as a PF Black Card member as well as continuing to convert our existing members’ standard memberships to our premium PF Black Card membership. We encourage this upgrade by continuing to enhance the value of our PF Black Card benefits through the ability to use any Planet Fitness location, free guest privileges and additional in-store amenities, such as tanning equipment, hydro-massage beds, and affinity partnerships for discounts and promotions. Our PF Black Card members as a percentage of total membership has increased from 59.6% as of December 31, 2017 to 62.6% as of December 31, 2021, and our average monthly dues per member have increased from $16.10 to $17.63 over the same period.

•Increase brand investment to drive awareness and growth. We plan to continue to increase our strong brand awareness by leveraging significant marketing expenditures by our franchisees and us, which we believe will result in increased membership in new and existing stores and continue to attract high-quality franchisee partners. In 2021, we consolidated our national and local marketing agencies from 16 agency partners across our system to one agency of record in our ongoing efforts to drive greater efficiency, visibility, and national and local marketing coordination. Under our current franchise agreement, franchisees are required to contribute 2% of their monthly membership dues annually to our National Advertising Fund (“NAF”) and Canadian advertising fund, from which we spent $59.4 million in 2021 to support our national marketing campaigns, our social media platforms and the development of local advertising materials, and $2.8

6

million additional funding from our corporate-owned stores and included in store-operations expense on our consolidated statements of operations. Under our current franchise agreement, franchisees are also generally required to spend 7% of their monthly membership dues on local advertising. We expect both our NAF and local advertising spending to grow as our membership grows.

•Continue to expand royalties from increases in average royalty rate and new franchisees. While our current franchise agreement stipulates a monthly royalty rate of 7% of monthly dues and annual membership fees, as of December 31, 2021, only 39% of our stores are paying royalties at the current franchise agreement rate, primarily due to lower rates in historical agreements. As new franchisees enter our system and, generally, as current franchisees open new stores or renew their existing franchise agreements at the current royalty rate, our average system-wide royalty rate will increase. In 2021, our average royalty rate was 6.38% compared to 4.25% in 2017.

•Grow sales from fitness equipment and related services. Our franchisees are contractually obligated to purchase fitness equipment from us, and in certain international markets, from our required vendors. Due to our scale and negotiating power, we believe we offer competitive pricing for high-quality, purple and yellow Planet Fitness-branded fitness equipment. We expect our equipment sales to grow as our U.S. franchisees open new stores and replace used equipment as required every five to seven years. As the number of franchise stores continues to increase and existing franchise stores continue to mature, we anticipate incremental growth in revenue related to the sale of equipment to franchisees. In addition, we believe that regularly refreshing equipment helps our franchise stores maintain a consistent, high-quality fitness experience and is one of the contributing factors that drives new member growth. In certain international markets, we earn a commission on the sale of equipment by our required vendors to franchisee-owned stores.

Our industry

Due to our unique positioning to a broader demographic, we believe Planet Fitness has an addressable market that is significantly larger than the traditional health club industry. We view our addressable market as approximately 250 million people, representing the U.S. population over 14 years of age. We compete broadly for consumer discretionary spending related to leisure, sports, entertainment and other non-fitness activities in addition to the traditional health club market. Both our standard and PF Black Card memberships are priced significantly below the 2019 industry average of $52 per month, the latest available estimate from our industry’s trade association, the International Health, Racquet & Sportsclub Association’s (“IHRSA”).

According to IHRSA, from the start of the COVID-19 pandemic in March 2020 through January 1, 2022, 25% of all fitness facilities have permanently closed across the United States as a result of the pandemic. Over the same period of time, Planet Fitness has permanently closed none of its franchisee-owned or corporate-owned stores as a result of the pandemic.

Membership

We make it simple for members to join, whether online, through our mobile application or in-store—no pushy sales tactics, no pressure and no complicated rate structures. Our members generally pay the following amounts (or an equivalent amount in the store’s local currency):

•monthly membership dues of only $10 for our standard membership, or approximately $22.99 for PF Black Card members;

•current standard annual fees of approximately $39; and

•enrollment fees of approximately $0 to $59.

Belonging to a Planet Fitness store has perks whether members select the standard membership or the premium PF Black Card membership. Every member can take advantage of free pizza and bagels once a month (when stores are open and health regulations permit) and gets free, unlimited fitness instruction included in their monthly membership fee. Our PF Black Card members also have the right to reciprocal use of all Planet Fitness stores, can bring a friend with them each time they work out, and have access to massage beds and chairs and tanning, among other benefits. PF Black Card benefits extend beyond our store as well, with exclusive specials and discount offers from third-party retail partners. While some of our memberships require a cancellation fee, we offer, and require our franchisees to offer, a non-committal membership option.

As of December 31, 2021, we had approximately 15.2 million members. We utilize electronic funds transfer (“EFT”) as our primary method of collecting monthly dues and annual membership fees. Over 85% of membership fee payments to our corporate-owned and franchise stores are collected via Automated Clearing House (“ACH”) direct debit. We believe there are certain advantages to receiving a higher concentration of ACH payments, as compared to credit card payments, including less frequent expiration of billing information and reduced exposure to subjective chargeback or dispute claims and fees.

7

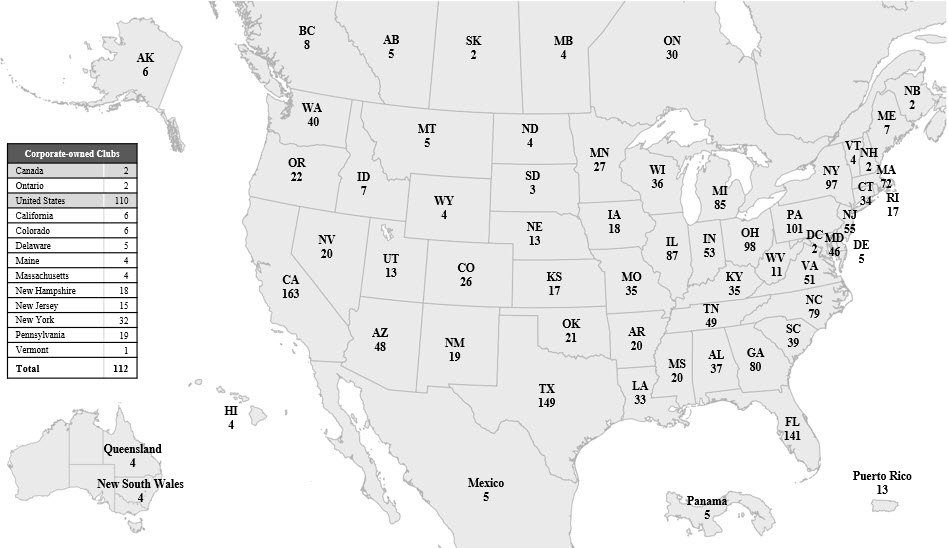

Our stores

We had 2,254 stores system-wide as of December 31, 2021, of which 2,142 were franchised and 112 were corporate-owned, located in 50 states, the District of Columbia, Puerto Rico, Canada, Panama, Mexico and Australia. The map below shows our franchisee-owned stores by location, and the accompanying table shows our corporate-owned stores by location.

Franchisee-owned store count by location | ||

Store model

Our store model is designed to generate attractive four-wall EBITDA margins, strong free cash flow and high returns on invested capital for both our corporate-owned and franchisee-owned stores. Based on franchisee business reviews and management estimates since the onset of COVID-19, we believe that, on average, franchisee stores achieve four-wall EBITDA margins in line with, or higher than these corporate-owned store four-wall EBITDA margins. The stores included in these business reviews represent those stores that voluntarily disclosed such information in response to our request, and we believe this information reflects a representative sample of franchisees based on the franchisee groups and geographic areas represented by these stores.

Fitness equipment

We provide our members with high-quality, Planet Fitness-branded fitness equipment from leading suppliers. In order to maintain a consistent experience across our store base, we stipulate specific pieces and quantities of cardio and strength-training equipment and work with franchisees to review and approve layouts and placement. Due to our scale, we are able to negotiate competitive pricing and secure extended warranties from our suppliers. As a result, we believe we offer equipment at more attractive pricing than franchisees could otherwise secure on their own.

Leases

We lease all but one of our corporate-owned stores and our corporate headquarters. Our store leases typically have initial terms of 10 years with two five-year renewal options, exercisable at our discretion. In October 2016, we executed a lease for our current corporate headquarters at 4 Liberty Lane West, Hampton, New Hampshire for an initial term of 15 years with one five-year renewal option, exercisable at our discretion. Our corporate headquarters serves as our base of operations for substantially all of our executive management and employees who provide our primary corporate support functions.

Franchisees own or directly lease from a third-party each Planet Fitness franchise location. We have not historically owned or entered into leases for Planet Fitness franchisee-owned stores and historically have generally not guaranteed franchisees’ lease

8

agreements, although we have done so in a few certain instances. In 2019, in connection with a real estate partnership, we began guaranteeing certain leases of our franchisees up to a maximum period of ten years, with earlier expiration dates if certain conditions are met.

Franchising

Franchising strategy

We rely heavily on our franchising strategy to develop new Planet Fitness stores, leveraging the ownership of entrepreneurs with specific local market expertise. As of December 31, 2021, there were 2,142 franchised Planet Fitness stores operated by approximately 120 franchisee groups. The majority of our existing franchise operators are multi-unit operators. As of December 31, 2021, 98% of all franchise stores were owned and operated by a franchisee group that owned at least three stores, and while our largest franchisee owned 175 stores, only 33% of our franchisee groups own more than ten stores. When considering a potential franchisee, we generally evaluate the potential franchisee’s prior experience in franchising or other multi-unit businesses, history in managing profit and loss operations, financial history and available capital and financing. We generally do not permit franchisees to borrow more than 80% of the initial investment for their Planet Fitness business.

Area development agreements

An ADA specifies the number of Planet Fitness stores to be developed by the franchisee in a designated geographic area, and requires the franchisee to meet certain scheduled deadlines for the development and opening of each Planet Fitness store authorized by the ADA. If the franchisee meets those obligations and otherwise complies with the terms of the ADA, with a few limited exceptions we agree not to, during the term of the ADA, operate or franchise new Planet Fitness stores in the designated geographic area. The franchisee must sign a separate franchise agreement with us for each Planet Fitness store developed under an ADA and that franchise agreement governs the franchisee’s right to own and operate the Planet Fitness store.

Franchise agreements

For each franchised Planet Fitness store, we enter into a franchise agreement covering standard terms and conditions. Planet Fitness franchisees are not granted an exclusive area or territory under the franchise agreement. The franchise agreement requires that the franchisee operate the Planet Fitness store at a specific location and in compliance with our standard methods of operation, including providing the services, using the vendors and selling the merchandise that we require. The typical franchise agreement has a 10-year term. Additionally, franchisees must purchase equipment from us (or our required vendors in the case of our franchisees located in certain international markets) and generally replace the fitness equipment in their stores every five to seven years and periodically refurbish and remodel their stores.

Site selection and approval

Our stores are generally located in free-standing retail buildings or neighborhood shopping centers, and we consider locations in both high- and low-density markets. We seek out locations with (i) high visibility and accessibility, (ii) favorable traffic counts and patterns, (iii) availability of signage, (iv) ample parking or access to public transportation and (v) our targeted demographics. We use third-party site analytics tools that provide us with extensive demographic data and analysis that we use to review new and existing sites and markets for our corporate-owned stores and franchisee-owned stores. We assess population density and drive time, current tenant mix, layout, potential competition and impact on existing Planet Fitness stores and comparative data based upon existing stores. Our real estate team meets regularly to review sites for future development and follows a detailed review process to ensure each site aligns with our strategic growth objectives and critical success factors.

We help franchisees select sites and develop facilities in these stores that conform to the physical specifications for a Planet Fitness store. Each franchisee is responsible for selecting a site, but must obtain site approval from us.

Design and construction

Once we have approved a franchisee’s site selection, we assist in the design and layout of the store and track the franchisee’s progress from lease signing to grand opening. Franchisees are offered the assistance of our franchise support team to track key milestones, coordinate with vendors and make equipment purchases. Certain Planet Fitness brand elements are required to be incorporated into every new store, and we strive for a consistent appearance across all of our stores, emphasizing clean, attractive facilities, including full-size locker rooms, and modern equipment. Franchisees must abide by our standards related to fixtures, finishes and design elements, including distinctive touches such as our “Lunk” alarm. We believe these elements are critical to ensure brand consistency and member experience system-wide.

In 2021 and 2020, based on a sample of U.S. franchisee data, we believe construction of franchise stores averaged approximately 21 and 22 weeks, respectively, which is higher than our historical average before the COVID-19 pandemic of approximately 14 weeks. We sampled construction costs to build new stores from across a wide range of U.S. geographies, 35

9

and 43 new stores in 2021 and 2020, respectively. Based upon these samples, franchisees’ unlevered (i.e., not debt-financed) investment to open a new store ranged from approximately $1.6 million to $3.3 million and $1.6 million to $3.7 million, based upon our samples in 2021 and 2020, respectively. These amounts include fitness equipment purchased from us as well as costs for non-fitness equipment and leasehold improvements and is based in part upon data we received from four general contractors that oversaw the construction of the stores in the sample set. Additionally, these amounts include an estimate of other costs that are typically paid by the franchisee and not managed by the general contractor. These amounts can vary significantly depending on a number of factors, including landlord allowances for tenant improvements and construction costs from different geographies and does not necessarily represent the total construction costs on a cash basis.

Franchisee support

We live and breathe the motto One Team, One Planet in our daily interactions with franchisees. We designed our franchise model to be streamlined and easy-to-operate, with efficient staffing and minimal inventory, and is supported by an active, engaged franchise operations system. We provide our franchisees with operational support, marketing materials and training resources.

Training. We continue to update and expand Planet Fitness University, a comprehensive training resource to help franchisees operate successful stores. Courses are delivered online, and content focuses on customer service, operational policies, brand standards, cleanliness, security awareness, crisis management and vendor product information. The core online curriculum is offered in both English and Spanish to support our Spanish-speaking employees. We regularly add and improve the content available on Planet Fitness University as a no-cost service to help enhance training programs for franchisees. Additional training opportunities offered to our franchisees include new owner orientation, operations training and workshops held at Planet Fitness headquarters (when circumstances permit), in stores and through regularly held webinars and seminars.

Operational support and communication. We believe spending quality time with our franchisees in person is an important opportunity to further strengthen our relationships and share best practices. We have dedicated operations and marketing teams providing ongoing support to franchisees. We are hands on—we often attend franchisees’ presales and grand openings, and we host franchisee meetings each year, known as “PF Huddles.” We also communicate regularly with our franchisee base to keep them informed, and we host a franchise conference, generally every 18 months, that is geared toward franchisees and their operations teams.

We regularly communicate and collaborate with the Independent Franchise Counsel (“IFC”) and send a weekly email communication to all franchisees with timely information related to operations, marketing, financing and equipment. Every month, a franchisee newsletter is emailed to franchisees, which generally includes a personal note from our Chief Executive Officer.

Compliance with brand standards—Franchise Business Coach

Our corporate-owned stores provide incentive compensation for store staff to successfully drive key business metrics in the service, cleanliness, personnel and financial categories, and we encourage our franchisees to follow our lead. We have a dedicated field support team of franchise business coaches focused on ensuring that our franchisee-owned stores adhere to brand standards and providing ongoing assistance, training and coaching to all franchisees. We generally perform a site visit and operations review on each franchise store within 30 to 60 days of opening, and each franchisee ownership group is visited at least once per year in multiple locations for a business review with their franchise business coach thereafter.

We also use mystery shoppers to perform anonymous reviews of franchisee-owned stores. We generally select franchisee-owned stores for review randomly but also target underperforming stores and stores that have not performed well on previous visits from their franchise business coach.

Marketing

Marketing strategy

Our marketing strategy is anchored by our key brand differentiators—the Judgement Free Zone, our exceptional value and our high-quality experience. We employ memorable and creative advertising, which not only drives membership sales, but also showcases our brand philosophy, humor and innovation in the industry. We see Planet Fitness as a community gathering place, and the heart of our marketing strategy is to reinforce the “feel good” mental and physical benefits of exercise and create a welcoming in-store environment for our members.

10

Marketing spending

National advertising. We support our franchisees both at a national and local level. We manage the NAF and Canadian advertising fund for franchisees and corporate-owned stores, with the goals of generating national awareness through national advertising and media partnerships, developing and maintaining creative assets to support local sale periods throughout the year, and building and supporting the Planet Fitness community via digital, social media and public relations. Our current U.S. and Canadian franchise agreements require franchisees to contribute approximately 2% of their monthly EFT annually to the NAF and Canadian advertising fund, respectively. In 2021 the NAF and Canadian advertising fund spent $62.2 million, $2.8 million of which is from our corporate-owned stores and included in store-operations expense on the consolidated statements of operations.

Local marketing. Our current franchise agreement requires franchisees to spend 7% of their monthly EFT on local marketing to support branding efforts and promotional sale periods throughout the year. In situations where multiple ownership groups exist in a geographic area, we have the right to require franchisees to form or join regional marketing cooperatives to maximize the impact of their marketing spending. Our corporate-owned stores contribute to, and participate in, regional marketing cooperatives with franchisees where practical. All franchisee-owned stores are supported by our dedicated franchisee marketing team, which provides guidance, tracking, measurement and advice on best practices. Franchisees spend their marketing dollars in a variety of ways to promote business at their stores on a local level. These methods may include direct mail, outdoor (including billboards), television, radio and digital advertisements and local partnerships and sponsorships.

Media partnerships

Given our scale and marketing resources through our NAF, we have aligned ourselves with high-profile media partners who have helped to extend the reach of our brand. For the past seven years, we have sponsored “Dick Clark’s New Year’s Rockin’ Eve with Ryan Seacrest,” and have been the sole presenting sponsor of the Times Square New Year’s Eve celebration through the Times Square Alliance, allowing the brand to be featured prominently in TV broadcasts covering Times Square during the celebration. This has allowed us to showcase the Planet Fitness brand and our judgement-free philosophy to an estimated over one billion TV viewers annually at a key time of year when health and wellness is top of mind for consumers.

Judgement Free Generation

The Judgement Free Generation is Planet Fitness’ philanthropic initiative designed to combat the judgement and bullying faced by today’s youth by creating a culture of kindness and encouragement. With our Judgement Free Zone principle as a solid foundation, The Judgement Free Generation aims to empower a generation to grow up contributing to a more judgement free planet— a place where everyone feels accepted and like they belong.

We have partnered with Boys & Girls Clubs of America to make a meaningful impact on the lives of today’s youth. Together with our franchisees, vendors and members, Planet Fitness has donated more than $7.0 million to support anti-bullying, pro-kindness initiatives since 2016.

Competition

In a broad sense, because many of our members are first-time or occasional gym users, we believe we compete with both fitness and non-fitness consumer discretionary spending alternatives for members’ and prospective members’ time and discretionary resources.

To a great extent, we also compete with other industry participants, including:

•other fitness centers;

•recreational facilities established by non-profit organizations such as YMCAs and by businesses for their employees;

•private studios and other boutique fitness offerings;

•racquet, tennis and other athletic clubs;

•amenity and condominium/apartment clubs;

•country clubs;

•online personal training and fitness coaching;

•the home-use fitness equipment industry;

•local tanning salons; and

•businesses offering similar services.

11

While the COVID-19 pandemic has had a significant impact on the health club industry, we expect that the industry will continue to be highly competitive and fragmented going forward. The number, size and strength of our competitors vary by region. Some of our competitors have an established presence in local markets or name recognition in their respective countries, and some are established in markets in which we have existing stores or intend to locate new stores. This competition is more significant internationally, where we have a limited number of stores and limited brand recognition.

Our objective is to compete primarily based upon the membership value proposition we are able to offer due to our significant economies of scale, high-quality fitness experience, judgement-free atmosphere and superior customer service, all at an attractive value, which we believe differentiates us from our competitors.

Our competition continues to increase as we continue to expand into new markets and add stores in existing markets. See also “Risk Factors—Risks related to our business and industry—The high level of competition in the health and fitness industry could materially and adversely affect our business.”

Suppliers

Franchisees are required to purchase fitness equipment from us (or our required vendors in the case of franchisees located in certain international markets) and are required to purchase various other items from vendors that we approve. We sell equipment purchased from third-party equipment manufacturers to franchisee-owned stores in the U.S. We also have one approved supplier of tanning beds, one approved supplier of massage beds and chairs, and various approved suppliers of non-fitness equipment and miscellaneous items. These vendors arrange for delivery of products and services directly to franchisee-owned stores. From time to time, we re-evaluate our supply relationships to ensure we obtain competitive pricing and high-quality equipment and other items.

Human Capital

Workforce

As of December 31, 2021, we employed 1,529 employees at our corporate-owned stores and 241 employees at our corporate headquarters located at 4 Liberty Lane West, Hampton, New Hampshire. None of our employees are represented by labor unions, and we believe we have an excellent relationship with our employees.

Planet Fitness franchises are independently owned and operated businesses. As such, employees of our franchisees are not employees of the Company.

Strategy

At Planet Fitness, we believe that an engaged, diverse, and inclusive culture is essential for the success of our business. To elevate our approach, in 2019 we hired a Chief People Officer to develop and implement an overarching human capital management strategy, programming and initiatives. Based on strategic analysis regarding the immediate and future needs of our business and our team members, we identified three critical areas of focus: Employee Engagement and Workplace Culture, Employee Health and Safety, and Diversity, Equity and Inclusion (“DE&I”). We believe that focus and investment in these three areas will, in turn, generate long-term value.

Employee Engagement and Workplace Culture

At Planet Fitness, we believe that culture is the core of our business. To ensure that our culture is rooted in ongoing engagement with our team members, our Chief People Officer hosts ongoing small informal meetings with team members across all departments. These conversations are designed to bring feedback about aspects of the business that are important to our workforce to the forefront of management’s attention, and to increase direct engagement and trust at every level of the company. Feedback is carefully reviewed by our human resources teams and shared with our executive leadership team, including our CEO.

We maintain numerous additional avenues for learning from our team members, ranging from anonymous surveys to town hall Q&A sessions and other ongoing opportunities to share thoughts and ideas. In 2020, we conducted a topic-specific survey to assess sentiment around a variety of topics such as workplace flexibility (i.e., remote/in-office), DE&I efforts, and improving our culture, and, in response, made several updates to our benefits package while ensuring existing programs were properly communicated to eligible team members (including, for instance, our enhanced parental leave and early release Fridays for increased flexibility). To promote employee satisfaction, we are continually seeking new ways to hear from our team members regarding their priorities and needs.

Training & Development

A critical component of maintaining our engaged and inclusive culture is making investments in our team members at all levels.

12

We offer 80+ courses through Planet Fitness University, our online training development program available to all team members. In response to the remote work environment, webinars and trainings on issues such as avoiding burnout and managing workload were developed in 2021. Ongoing programs at Planet Fitness include professional-level workshops led by our training department, in addition to our Leadership Academy for the accelerated development of our highest-potential team members. In 2021, there were over 30,000 active users of the PF University platform across our franchise community.

Health & Safety

Given our core mission is centered on improving people’s lives and keeping people healthy and the customer-facing nature of our business, the overall health and safety of our team members and our members has been a longstanding priority for the company and a core component of our broader environmental, social and corporate governance (“ESG”) objectives and strategy. In 2020, we were able to draw on our knowledge, experience and commitment to health and safety to act quickly to protect our Planet Fitness community during the COVID-19 pandemic. Our COVID-19 policies and protocols, which we developed in consultation with national and global health experts, include:

•Implementing policies to keep people safe, including adherence to local policies and regulations regarding capacity, mask wearing, and vaccination requirements;

•Equipping stores with disinfectant effective against COVID-19 on surfaces; and

•Adding a COVID-19 wellness questionnaire and touchless check-in via the Planet Fitness app.

In 2021 we adopted the recognized safety framework put forth by the International WELL Building Institute to ensure a safer and healthier environment for our employees and members across our global network. We aligned our franchised and corporate-owned stores, as well as our headquarters, within WELL’s evidence-based, third-party verified rating framework, and prioritized holistic aspects of health from improved air flow, hygienic hand washing practices, reduction in hand contact of high-touch surfaces, effective cleaning protocols and robust emergency preparedness and response. The work done in 2021 resulted in our achievement of the WELL Health-Safety Rating for Facility Operations and Management, making us the first fitness brand to accomplish this.

Diversity, Equity & Inclusion

We recognize that diversity of our workforce at all levels of our company is a business and social imperative. To assess and accelerate our efforts, in 2020 we formed a DE&I Task Force, with responsibility for developing a strategic roadmap to address short- and long-term priorities as well as a plan for ensuring that we continue to make progress. In 2021, we offered Cultural Competency & Unconscious Bias training to our executive leadership team, our headquarters team members, and our franchisees.

Planet Fitness measures diversity across ethnic/racial groups, gender and employee level to help inform human capital management strategies and ensure an engaged workforce. We will publicly disclose Equal Opportunity Employment Standard Form 100 data in our 2021 Impact Report.

Information technology and systems

All stores use a computerized, third-party hosted store management system to process new in-store memberships, bill members, update member information, check-in members, process point of sale transactions as well as track and analyze sales, membership statistics, cross-store utilization, member tenure, amenity usage, billing performance and demographic profiles by member. Our websites, mobile, and digital platforms are hosted by third parties, and we also rely on third-party vendors for related functions such as our system for processing and integrating new online memberships, updating member information and making online payments. We believe these systems are scalable to support our growth plans.

Our back-office computer systems are comprised of a variety of technologies designed to assist in the management and analysis of our revenues, costs and key operational metrics as well as support the daily operations of our headquarters. These computer systems include third-party hosted systems that support our real estate and construction processes, a third-party hosted financial system, third-party hosted data warehouses and business intelligence system to consolidate multiple data sources for reporting, advanced analysis, consumer insights and financial analysis and forecasting, a third-party hosted payroll system, on premise telephony systems and a third-party hosted call center software solution to manage and track member-related requests.

We also provide our franchisees access to a web-based, third-party hosted custom franchise management system to receive informational notices, operational resources and updates, training materials and other franchisee communications.

Beginning in 2018, we engaged with a third-party software development vendor to develop a new, custom digital platform, which, through the exchange of data and introduction of digital products and services, facilitates digital experiences across any digital channel, including mobile, online and in-store media. In 2020, we began introducing premium digital content, across multiple channels, but primarily through our mobile app. In 2021, we introduced content management services to the digital

13

platform allowing us to support the delivery of various types of content in multiple languages across the digital platform and connected channels. These solutions have facilitated our ability to continue providing differentiated and unique experiences to our customers, allow for various partnership types and are aligned with our ongoing business strategy.

We recognize the value of enhancing and extending the uses of information technology in virtually every area of our business. Our information technology strategy is aligned to support our business strategy and operating plans. We maintain an ongoing comprehensive multi-year program to introduce, replace, or upgrade key systems, enhance security and optimize their performance.

Intellectual property

We own many registered trademarks and service marks in the U.S. and in other countries, including “Planet Fitness,” “Judgement Free Zone,” “PE@PF,” “Lunk Alarm,” “Black Card,” “PF Black Card,” “No Gymtimidation,” “You Belong,” “The Judgement Free Generation,” “PF+” and various other trademarks and trade dress. We believe the Planet Fitness name and the many distinctive marks associated with it are of significant value and are very important to our business. Accordingly, as a general policy, we pursue registration of our marks in select international jurisdictions, monitor the use of our marks in the U.S. and internationally and challenge any unauthorized use of the marks.

We license the use of our marks to franchisees, third-party vendors and others through franchise agreements, vendor agreements and licensing agreements. These agreements typically restrict third parties’ activities with respect to use of the marks and impose brand standards requirements. We require licensees to inform us of any potential infringement of the marks.

We register some of our copyrighted material and otherwise rely on common law protection of our copyrighted works. Such copyrighted materials are not material to our business.

We also license some intellectual property from third parties for use in our stores but such licenses are not material to our business.

Government regulation

We and our franchisees are subject to various federal, international, state, provincial and local laws and regulations affecting our business.

We are subject to the FTC Franchise Rule promulgated by the FTC that regulates the offer and sale of franchises in the U.S. and its territories (including Puerto Rico) and requires us to provide to all prospective franchisees certain mandatory disclosure in a franchise disclosure document (“FDD”), unless otherwise exempt. In addition, we are subject to state franchise registration and disclosure laws in approximately 14 states and various business opportunity laws that regulate the offer and sale of franchises by requiring us, unless otherwise exempt, to register our franchise offering in those states prior to our making any offer or sale of a franchise in those states and to provide a FDD to prospective franchisees in accordance with such laws.

We are subject to franchise disclosure laws in six provinces in Canada that regulate the offer and sale of franchises by requiring us, unless otherwise exempt, to prepare and deliver a franchise disclosure document to disclose our franchise offering in those provinces in a prescribed format to prospective franchisees in accordance with such laws, and that regulate certain aspects of the franchise relationship. We are subject to similar franchise sales laws in Mexico and Australia, and may become subject to similar laws in other countries in which we may offer franchises in the future. We are also subject to franchise relationship laws in approximately 20 states and in various U.S. territories that regulate many aspects of the franchise relationship including, depending upon the jurisdiction, renewals and terminations of franchise agreements, franchise transfers, the applicable law and venue in which franchise disputes may be resolved, discrimination, and franchisees’ rights to associate, among others. In addition, we and our franchisees may also be subject to laws in other foreign countries where we or they do business.

We and our franchisees are also subject to the U.S. Fair Labor Standards Act of 1938, as amended, similar state laws in certain jurisdictions, and various other U.S. and international laws governing such matters as minimum-wage requirements, overtime and other working conditions. Based on our experience with hiring employees and operating stores, we believe a significant number of our and our franchisees’ employees are paid at rates related to the U.S. federal or state minimum wage, and past increases in the U.S. federal and/or state minimum wage have increased labor costs, as would future increases.

Our and our franchisees’ operations and properties are subject to extensive U.S. federal and state, as well as international, provincial and local laws and regulations, including those relating to environmental, building and zoning requirements. Our and our franchisees’ development of properties depends to a significant extent on the selection and acquisition of suitable sites, which are subject to zoning, land use, environmental, traffic and other regulations and requirements.

We and our franchisees are responsible at each of our respective locations for compliance with U.S. state laws, Canadian provincial laws and other international local laws that regulate the relationship between health clubs and their members. Nearly

14

all states and provinces have consumer protection regulations that limit the collection of monthly membership dues prior to opening, require certain disclosures of pricing information, mandate the maximum length of contracts and “cooling off” periods for members (after the purchase of a membership), set escrow and bond requirements for health clubs, govern member rights in the event of a member relocation or disability, provide for specific member rights when a health club closes or relocates or preclude automatic membership renewals.

We and our franchisees primarily accept payments for our memberships through EFTs from members’ bank accounts, and therefore, we and our franchisees are subject to federal, state and international laws legislation and certification requirements, including the Electronic Funds Transfer Act. Some states and provinces have passed or have considered legislation requiring gyms and health clubs to offer a prepaid membership option at all times and/or limit the duration for which memberships can auto-renew through EFT payments, if at all. Our business relies heavily on the fact that our memberships continue on a month-to-month basis after the completion of any initial term requirements, and compliance with these laws, regulations, and similar requirements may be onerous and expensive, and variances and inconsistencies from jurisdiction to jurisdiction may further increase the cost of compliance and doing business. States that have such health club statutes provide harsh penalties for violations, including membership contracts being void or voidable.

Additionally, the collection, maintenance, use, disclosure and disposal of personally identifiable data by our, or our franchisees’, businesses are regulated at the federal, state and international levels as well as by certain financial industry groups, such as the Payment Card Industry, Security Standards Council, the National Automated Clearing House Association (“NACHA”) and the Canadian Payments Association. Federal, state, international and financial industry groups may also consider from time to time new privacy and security requirements that may apply to our businesses and may impose further restrictions on our collection, disclosure, use, and disposal of personally identifiable information that is housed in one or more of our databases. These security requirements and further restrictions, including the General Data Protection Regulation (“GDPR”) and the California Consumer Privacy Act (“CCPA”), grant protections and causes of action related to consumer data privacy and the methods in which it is collected, stored, used, and disposed by us, our franchisees, and applicable third parties.

Many of the states and provinces where we and our franchisees operate stores have health and safety regulations that apply to health clubs and other facilities that offer indoor tanning services, including certain temporary regulations related to the COVID-19 pandemic. In addition, U.S. federal law imposes a 10% excise tax on indoor tanning services. Under the rule promulgated by the IRS imposing the tax, a portion of the cost of memberships that include access to our tanning services are subject to the tax.

Our organizational structure

Planet Fitness, Inc. is a holding company, and its principal asset is an equity interest in the membership units (“Holdings Units”) in Pla-Fit Holdings, LLC (“Pla-Fit Holdings”).

We are the sole managing member of Pla-Fit Holdings. We operate and control all of the business and affairs of Pla-Fit Holdings, and we hold 100% of the voting interest in Pla-Fit Holdings. As a result, we consolidate Pla-Fit Holdings’ financial results and report a non-controlling interest related to the Holdings Units not owned by us. See Note 1 to the consolidated financial statements included in Part II, Item 8 for more information.

Available information

Our website address is www.planetfitness.com, and our investor relations website is located at http://investor.planetfitness.com. Information on our website is not incorporated by reference herein. Copies of our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and our Proxy Statements for our annual meetings of shareholders, and any amendments to those reports, as well as Section 16 reports filed by our insiders, are available free of charge on our website as soon as reasonably practicable after we file the reports with, or furnish the reports to, the Securities and Exchange Commission (the “SEC”).The SEC maintains an Internet site (http://www.sec.gov) containing reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

15

Item 1A. Risk Factors.

We could be adversely impacted by various risks and uncertainties. If any of these risks actually occurs, our business, financial condition, operating results, cash flow and prospects may be materially and adversely affected. As a result, the trading price of our Class A common stock could decline.

Summary of Risk Factors

Risks related to our business and industry

•Our business and results of operations have been and may in the future be materially impacted by the ongoing COVID-19 pandemic, and could be impacted by similar events in the future.

•Our success depends substantially on the value of our brand, which could be materially and adversely affected by the high level of competition in the health and fitness industry, our ability to anticipate and satisfy consumer preferences, shifting views of health and fitness and our ability to obtain and retain high-profile strategic partnership arrangements.

•Our and our franchisees’ stores may be unable to attract and retain members, which would materially and adversely affect our business, results of operations and financial condition.

•Our intellectual property rights, including trademarks, trade names, copyrights and trade dress, may be infringed, misappropriated or challenged by others.

•We and our franchisees rely heavily on information systems, including the use of email marketing and social media, and any material failure, interruption or weakness may prevent us from effectively operating our business, damage our reputation or subject us to potential fines or other penalties.

•If we fail to properly maintain the confidentiality and integrity of our data, including member credit card, debit card, bank account information and other personally identifiable information, our reputation and business could be materially and adversely affected.

•The occurrence of cyber incidents, or a deficiency in cybersecurity, could negatively impact our business by causing a disruption to our operations, a compromise or corruption of confidential information, and/or damage to our employee and business relationships and reputation, all of which could harm our brand and our business.

•If we fail to successfully implement our growth strategy, which includes new store development by existing and new franchisees, our ability to increase our revenues and operating profits could be adversely affected.

•Our planned growth and changes in the industry could place strains on our management, employees, information systems and internal controls, which may adversely impact our business.

•If we cannot retain our key employees and hire additional highly qualified employees, we may not be able to successfully manage our businesses and pursue our strategic objectives.

•Economic, political and other risks associated with our international operations could adversely affect our profitability and international growth prospects.

•Our financial results are affected by the operating and financial results of, our relationships with and actions taken by our franchisees.

•We are subject to a variety of additional risks associated with our franchisees, such as potential franchisee bankruptcies, franchisee changes in control, franchisee turnover rising costs related to construction of new stores and maintenance of existing stores, which could adversely affect the attractiveness of our franchise model, and in turn our business, results of operations and financial condition.

•We and our franchisees could be subject to claims related to health and safety risks to members that arise while at both our corporate-owned and franchise stores.

•Our business is subject to various laws and regulations including, among others, those governing indoor tanning, electronic funds transfer, ACH, credit card, debit card, digital payment options auto-renewal contracts, and consumer protection more generally, and changes in such laws and regulations, failure to comply with existing or future laws and regulations or failure to adjust to consumer sentiment regarding these matters, could harm our reputation and adversely affect our business.

•We are subject to risks associated with leasing property subject to long-term non-cancelable leases.

•If we and our franchisees are unable to identify and secure suitable sites for new franchise stores, our revenue growth rate and profits may be negatively impacted.

•Opening new stores in close proximity may negatively impact our existing stores’ revenues and profitability.

•Our franchisees may incur rising costs related to construction of new stores and maintenance of existing stores, which could adversely affect the attractiveness of our franchise model, and in turn our business, results of operations and financial condition.

•Our dependence on a limited number of suppliers for equipment and certain products and services could result in disruptions to our business and could adversely affect our revenues and gross profit.

16

Risks related to the Sunshine Acquisition

•We may be unable to successfully realize the anticipated benefits of the Sunshine Acquisition.

•We may not have discovered undisclosed liabilities of the Sunshine Fitness stores during the due diligence process.

Risks related to our indebtedness

•Substantially all of the assets of certain of our subsidiaries are security, under the terms of securitization transactions that were completed on August 1, 2018, December 3, 2019 and February 10, 2022 and which impose certain restrictions on our activities and the activities of our subsidiaries.

•We have a significant amount of debt outstanding, which will require a significant amount of cash to service and such indebtedness, along with the other contractual commitments of our subsidiaries, could adversely affect our business, financial condition and results of operations, as well as the ability of certain of our subsidiaries to meet their debt payment obligations.

•The ability to generate cash or refinance our indebtedness as it becomes due depends on many factors, some of which are beyond our control.

Risks related to our organizational structure

•We will be required to pay certain of our existing and previous owners for certain tax benefits we may claim. We expect that the payments we will be required to make will be substantial and may be accelerated and/or significantly exceed the actual benefits we realize in respect of the tax attributes subject to the tax receivable agreements and we will not be reimbursed for any payments made pursuant to the tax receivable agreements in the event that any tax benefits are disallowed.

•Unanticipated changes in effective tax rates or adverse outcomes resulting from examination of our income or other tax returns could adversely affect our financial condition and results of operations.

•Our ability to pay taxes and expenses, including payments under the tax receivable agreements, may be limited by our structure.

•In certain circumstances, Pla-Fit Holdings will be required to make distributions to us and the Continuing LLC Owners, and the distributions that Pla-Fit Holdings will be required to make may be substantial.

Risks related to our Class A common stock

•Provisions of our corporate governance documents could make an acquisition of our Company more difficult and may prevent attempts by our stockholders to replace or remove our current management, even if beneficial to our stockholders.

•Our organizational structure, including the tax receivable agreements, confers certain benefits upon the TRA Holders and the Continuing LLC Owners that do not benefit Class A common stockholders to the same extent as it will benefit the TRA Holders and the Continuing LLC Owners.

•If our internal control over financial reporting or our disclosure controls and procedures are not effective, we may not be able to accurately report our financial results, prevent fraud or file our periodic reports in a timely manner, which may cause investors to lose confidence in our reported financial information and may lead to a decline in our stock price.

•Our certificate of incorporation designates courts in the State of Delaware as the sole and exclusive forum for certain types of actions and proceedings that may be initiated by our stockholders, which could limit our stockholders’ ability to obtain a favorable judicial forum for disputes with us or our directors, officers or employees.

•Our stock price could be extremely volatile, and, as a result, stockholders may not be able to resell shares at or above their purchase price.

•Because we do not currently pay any cash dividends on our Class A common stock, you may not receive any return on investment unless you sell your Class A common stock for a price greater than that which you paid for it.

•Financial forecasting may differ materially from actual results.

Risks related to our business and industry

Our business and results of operations have been and may in the future be materially impacted by the ongoing COVID-19 pandemic, and could be impacted by similar events in the future.

The outbreak of the novel coronavirus COVID-19 (“COVID-19”) and the disease it causes, which was declared a pandemic by the World Health Organization in March 2020, continues to impact worldwide consumer behavior and economic activity. A public health pandemic such as COVID-19 poses the risk that we or our employees, franchisees, members, suppliers and other partners may be prevented from conducting business activities for an indefinite period of time, including due to shutdowns, travel restrictions, social distancing requirements, stay at home orders and advisories and other restrictions that may be suggested or mandated by governmental authorities. The COVID-19 pandemic may also have the effect of heightening many of

17

the other risks described elsewhere in this report, such as those relating to our growth strategy, international operations, our ability to attract and retain members, our supply chain, health and safety risks to our members, loss of key employees and changes in consumer preferences, as well as risks related to our significant indebtedness, including our ability to generate sufficient cash and comply with the terms of and restrictions under the agreements governing such indebtedness.

The duration of the COVID-19 pandemic and the extent of its impact remains highly uncertain and difficult to predict. However, the continued spread of the virus and the measures taken in response to it have disrupted our operations and have adversely impacted our business, financial condition and results of operations. For example, in response to the COVID-19 pandemic, we proactively closed all of our stores system-wide beginning in mid-March 2020, temporarily furloughed a majority of our corporate-owned store employees while corporate-owned stores remained closed, suspended billing membership and annual fees while stores were closed and temporarily suspended sales and placement of equipment. We and our franchisees took other actions, such as temporary rent deferrals and suspension of marketing activities, as additional measures to preserve cash and liquidity during closure periods. Temporary rent deferrals have often led to renegotiated rent payment schedules with landlords, some of which remain unresolved and may affect us or our franchisees in future periods. Our stores began reopening in early May 2020 as local guidelines allowed, and as of December 31, 2021, 2,246 of our 2,254 stores were open and operating, of which 2,134 were franchise stores and 112 were corporate-owned stores. As COVID-19 continues to impact areas in which our stores operate, certain of our stores have had to re-close, and additional stores may have to re-close, pursuant to local guidelines. Store members have not and will not be charged membership dues while our stores are temporarily closed and are credited for any membership dues paid for periods when their store is closed due to the COVID-19 pandemic. Compared to the periods prior to March 2020, we have experienced and may in the future experience decreased new store development and remodels, as well as decreased replacement equipment sales in 2021 and beyond as a result of the COVID-19 pandemic. In addition, as a result of COVID-19, we have experienced to date, and may in the future experience, a decrease in our net membership base compared to membership levels in March 2020, and the COVID-19 pandemic may have an ongoing impact on consumer behavior.

As our stores reopened, we have recognized franchise revenue and corporate-owned store revenue associated with any membership dues collected prior to temporary store closures. We may have to defer revenue in the future if stores are required to re-close.

Further, the constantly evolving nature of the COVID-19 pandemic and the emergence of new variants of coronavirus, such as “Omicron,” which the World Health Organization identified as a “variant of concern” in November 2021, may negatively impact our operating results in future periods. The significance of the ultimate operational and financial impact to us will depend on how long and widespread the disruptions caused by COVID-19, and the corresponding response to contain the virus and treat those affected by it, prove to be.

Our success depends substantially on the value of our brand.

Our success is dependent in large part upon our ability to maintain and enhance the value of our brand, our store members’ connection to our brand and a positive relationship with our franchisees. Brand value can be severely damaged even by isolated incidents, particularly if the incidents receive considerable negative publicity or result in litigation. Some of these incidents may relate to our policies, the way we manage our relationships with our franchisees, our growth strategies, our development efforts or the ordinary course of our, or our franchisees’, businesses. Other incidents that could be damaging to our brand may arise from events that are or may be beyond our ability to control, such as:

•actions taken (or not taken) by one or more franchisees or their employees relating to health, safety, welfare or otherwise;

•data security breaches or fraudulent activities associated with our and our franchisees’ electronic payment systems;

•regulatory, investigative or other actions relating to our and our franchisees’ data privacy practices;

•litigation and legal claims;

•third-party misappropriation, dilution or infringement or other violation of our intellectual property;

•regulatory, investigative or other actions relating to our and our franchisees’ provision of indoor tanning services;

•regulatory, investigative or other actions relating to pricing, billing and cancellation practices;

•illegal activity targeted at us or others; and

•conduct by individuals affiliated with us which could violate ethical standards or otherwise harm the reputation of our brand.

Consumer demand for our stores and our brand’s value could diminish significantly if any such incidents or other matters erode consumer confidence in us, our stores or our reputation as a health and fitness brand, which would likely result in fewer

18