UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended March 31, 2024 .

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the Transition Period from to .

Commission file number 001-36859

(Exact Name of Registrant as Specified in Its Charter)

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | ||||||||||

| (Address of Principal Executive Offices) | (Zip Code) | ||||||||||

(408 ) 967-1000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o | |||||||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

As of April 24, 2024, there were 1,046,046,041 shares of the registrant’s common stock, $0.0001 par value, outstanding, which is the only class of common or voting stock of the registrant issued.

PayPal Holdings, Inc.

TABLE OF CONTENTS

| Page Number | |||||||||||

PART I: FINANCIAL INFORMATION

ITEM 1: FINANCIAL STATEMENTS

PayPal Holdings, Inc.

CONDENSED CONSOLIDATED BALANCE SHEETS

| March 31, 2024 | December 31, 2023 | ||||||||||

| (In millions, except par value) | |||||||||||

| (Unaudited) | |||||||||||

| ASSETS | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Short-term investments | |||||||||||

| Accounts receivable, net | |||||||||||

| Loans and interest receivable, held for sale | |||||||||||

Loans and interest receivable, net of allowances of $ | |||||||||||

| Funds receivable and customer accounts | |||||||||||

| Prepaid expenses and other current assets | |||||||||||

| Total current assets | |||||||||||

| Long-term investments | |||||||||||

| Property and equipment, net | |||||||||||

| Goodwill | |||||||||||

| Intangible assets, net | |||||||||||

| Other assets | |||||||||||

| Total assets | $ | $ | |||||||||

| LIABILITIES AND EQUITY | |||||||||||

| Current liabilities: | |||||||||||

| Accounts payable | $ | $ | |||||||||

| Funds payable and amounts due to customers | |||||||||||

| Accrued expenses and other current liabilities | |||||||||||

| Total current liabilities | |||||||||||

| Other long-term liabilities | |||||||||||

| Long-term debt | |||||||||||

| Total liabilities | |||||||||||

| Commitments and contingencies (Note 13) | |||||||||||

| Equity: | |||||||||||

Common stock, $ | |||||||||||

Preferred stock, $ | |||||||||||

Treasury stock at cost, | ( | ( | |||||||||

| Additional paid-in-capital | |||||||||||

| Retained earnings | |||||||||||

| Accumulated other comprehensive income (loss) | ( | ( | |||||||||

| Total equity | |||||||||||

| Total liabilities and equity | $ | $ | |||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 4 | ||||||||||

PayPal Holdings, Inc.

CONDENSED CONSOLIDATED STATEMENTS OF INCOME (LOSS)

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (In millions, except per share data) | |||||||||||

| (Unaudited) | |||||||||||

| Net revenues | $ | $ | |||||||||

| Operating expenses: | |||||||||||

| Transaction expense | |||||||||||

| Transaction and credit losses | |||||||||||

| Customer support and operations | |||||||||||

| Sales and marketing | |||||||||||

| Technology and development | |||||||||||

| General and administrative | |||||||||||

| Restructuring and other | |||||||||||

| Total operating expenses | |||||||||||

| Operating income | |||||||||||

| Other income (expense), net | |||||||||||

| Income before income taxes | |||||||||||

| Income tax expense | |||||||||||

| Net income (loss) | $ | $ | |||||||||

| Net income (loss) per share: | |||||||||||

| Basic | $ | $ | |||||||||

| Diluted | $ | $ | |||||||||

| Weighted average shares: | |||||||||||

| Basic | |||||||||||

| Diluted | |||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 5 | ||||||||||

PayPal Holdings, Inc.

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (In millions) | |||||||||||

| (Unaudited) | |||||||||||

| Net income (loss) | $ | $ | |||||||||

| Other comprehensive income (loss), net of reclassification adjustments: | |||||||||||

| Foreign currency translation adjustments (“CTA”) | ( | ( | |||||||||

| Net investment hedges CTA gains, net | |||||||||||

| Tax expense on net investment hedges CTA gains, net | ( | ( | |||||||||

| Unrealized gains (losses) on cash flow hedges, net | ( | ||||||||||

| Tax (expense) benefit on unrealized gains (losses) on cash flow hedges, net | ( | ||||||||||

| Unrealized gains on available-for-sale debt securities, net | |||||||||||

| Tax expense on unrealized gains on available-for-sale debt securities, net | ( | ( | |||||||||

| Other comprehensive income (loss), net of tax | |||||||||||

| Comprehensive income (loss) | $ | $ | |||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 6 | ||||||||||

PayPal Holdings, Inc.

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

| Common Stock Shares | Treasury Stock | Additional Paid-In Capital | Accumulated Other Comprehensive Income (Loss) | Retained Earnings | Total Equity | ||||||||||||||||||||||||||||||

| (In millions) | |||||||||||||||||||||||||||||||||||

| (Unaudited) | |||||||||||||||||||||||||||||||||||

| Balances at December 31, 2023 | $ | ( | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||

| Net income | — | — | — | — | |||||||||||||||||||||||||||||||

| Foreign CTA | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Net investment hedges CTA gains, net | — | — | — | — | |||||||||||||||||||||||||||||||

| Tax expense on net investment hedges CTA gains, net | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Unrealized gains on cash flow hedges, net | — | — | — | — | |||||||||||||||||||||||||||||||

| Tax expense on unrealized gains on cash flow hedges, net | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Unrealized gains on available-for-sale debt securities, net | — | — | — | — | |||||||||||||||||||||||||||||||

| Tax expense on unrealized gains on available-for-sale debt securities, net | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Common stock and stock-based awards issued, net of shares withheld for employee taxes | — | ( | — | — | ( | ||||||||||||||||||||||||||||||

| Common stock repurchased | ( | ( | — | — | ( | ||||||||||||||||||||||||||||||

| Treasury stock reissuance | — | — | — | — | |||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

| Balances at March 31, 2024 | $ | ( | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||

| Common Stock Shares | Treasury Stock | Additional Paid-In Capital | Accumulated Other Comprehensive Income (Loss) | Retained Earnings | Total Equity | ||||||||||||||||||||||||||||||

| (In millions) | |||||||||||||||||||||||||||||||||||

| (Unaudited) | |||||||||||||||||||||||||||||||||||

| Balances at December 31, 2022 | $ | ( | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||

| Net income | — | — | — | — | |||||||||||||||||||||||||||||||

| Foreign CTA | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Net investment hedges CTA gains, net | — | — | — | — | |||||||||||||||||||||||||||||||

| Tax expense on net investment hedges CTA gains, net | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Unrealized losses on cash flow hedges, net | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Tax benefit on unrealized losses on cash flow hedges, net | — | — | — | — | |||||||||||||||||||||||||||||||

| Unrealized gains on available-for-sale debt securities, net | — | — | — | — | |||||||||||||||||||||||||||||||

| Tax expense on unrealized gains on available-for-sale debt securities, net | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Common stock and stock-based awards issued and assumed, net of shares withheld for employee taxes | — | ( | — | — | ( | ||||||||||||||||||||||||||||||

| Common stock repurchased | ( | ( | — | — | — | ( | |||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

| Balances at March 31, 2023 | $ | ( | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 7 | ||||||||||

PayPal Holdings, Inc.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (In millions) | |||||||||||

| (Unaudited) | |||||||||||

| Cash flows from operating activities: | |||||||||||

| Net income (loss) | $ | $ | |||||||||

| Adjustments to reconcile net income (loss) to net cash provided by operating activities: | |||||||||||

| Transaction and credit losses | |||||||||||

| Depreciation and amortization | |||||||||||

| Stock-based compensation | |||||||||||

| Deferred income taxes | ( | ||||||||||

| Net (gains) losses on strategic investments | ( | ||||||||||

| Accretion of discounts on investments, net of amortization of premiums | ( | ( | |||||||||

| Adjustments to loans and interest receivable, held for sale | |||||||||||

| Other | ( | ||||||||||

| Originations of loans receivable, held for sale | ( | ||||||||||

| Proceeds from repayments and sales of loans receivable, originally classified as held for sale | |||||||||||

| Changes in assets and liabilities: | |||||||||||

| Accounts receivable | ( | ( | |||||||||

| Accounts payable | ( | ||||||||||

| Other assets and liabilities | ( | ||||||||||

| Net cash provided by operating activities | |||||||||||

| Cash flows from investing activities: | |||||||||||

| Purchases of property and equipment | ( | ( | |||||||||

| Proceeds from sales of property and equipment | |||||||||||

| Purchases and originations of loans receivable | ( | ( | |||||||||

| Proceeds from repayments and sales of loans receivable, originally classified as held for investment | |||||||||||

| Purchases of investments | ( | ( | |||||||||

| Maturities and sales of investments | |||||||||||

| Funds receivable | ( | ||||||||||

| Collateral posted related to derivative instruments, net | ( | ||||||||||

| Other investing activities | |||||||||||

| Net cash provided by investing activities | |||||||||||

| Cash flows from financing activities: | |||||||||||

| Proceeds from issuance of common stock | |||||||||||

| Purchases of treasury stock | ( | ( | |||||||||

| Tax withholdings related to net share settlements of equity awards | ( | ( | |||||||||

| Borrowings under financing arrangements | |||||||||||

| Repayments under financing arrangements | ( | ( | |||||||||

| Funds payable and amounts due to customers | ( | ( | |||||||||

| Collateral received related to derivative instruments, net | ( | ||||||||||

| Net cash used in financing activities | ( | ( | |||||||||

| 8 | ||||||||||

PayPal Holdings, Inc.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS—(continued)

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (In millions) | |||||||||||

| (Unaudited) | |||||||||||

| Effect of exchange rate changes on cash, cash equivalents, and restricted cash | ( | ( | |||||||||

| Net change in cash, cash equivalents, and restricted cash | ( | ||||||||||

| Cash, cash equivalents, and restricted cash at beginning of period | |||||||||||

| Cash, cash equivalents, and restricted cash at end of period | $ | $ | |||||||||

| Supplemental cash flow disclosures: | |||||||||||

| Cash paid for interest | $ | $ | |||||||||

| Cash paid for income taxes, net | $ | $ | |||||||||

| The table below reconciles cash, cash equivalents, and restricted cash as reported in the condensed consolidated balance sheets to the total of the same amounts shown in the condensed consolidated statements of cash flows: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Short-term investments | |||||||||||

| Funds receivable and customer accounts | |||||||||||

| Total cash, cash equivalents, and restricted cash shown in the condensed consolidated statements of cash flows | $ | $ | |||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 9 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

NOTE 1—OVERVIEW AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

OVERVIEW AND ORGANIZATION

PayPal Holdings, Inc. (“PayPal,” the “Company,” “we,” “us,” or “our”) was incorporated in Delaware in January 2015 and is a leading technology platform that enables digital payments and personalizes commerce experiences on behalf of merchants and consumers worldwide. PayPal’s mission is to revolutionize commerce globally by creating innovative experiences that are designed to make moving money, selling, and shopping simple, personalized, and secure.

We operate globally and in a rapidly evolving regulatory environment characterized by a heightened focus by regulators globally on all aspects of the payments industry, including countering terrorist financing, anti-money laundering, privacy, cybersecurity, and consumer protection. The laws and regulations applicable to us, including those enacted prior to the advent of digital payments, continue to evolve through legislative and regulatory action and judicial interpretation. New or changing laws and regulations, including changes to their interpretation and implementation, as well as increased penalties and enforcement actions related to non-compliance, could have a material adverse impact on our business, results of operations, and financial condition. We monitor these areas closely and are focused on designing compliant solutions for our customers.

SIGNIFICANT ACCOUNTING POLICIES

Basis of presentation and principles of consolidation

The accompanying condensed consolidated financial statements include the financial statements of PayPal and our wholly- and majority-owned subsidiaries. All intercompany balances and transactions have been eliminated in consolidation.

Investments in entities where we have the ability to exercise significant influence, but not control, over the investee are accounted for using the equity method of accounting. For such investments, our share of the investee’s results of operations is included in other income (expense), net on our condensed consolidated statements of income (loss). Investments in entities where we do not have the ability to exercise significant influence over the investee are accounted for at fair value or cost minus impairment, if any, adjusted for changes resulting from observable price changes, which are included in other income (expense), net on our condensed consolidated statements of income (loss). Our investment balance is included in long-term investments on our condensed consolidated balance sheets.

We determine at the inception of each investment, and re-evaluate if certain events occur, whether an entity in which we have made an investment is considered a variable interest entity (“VIE”). If we determine an investment is in a VIE, we then assess if we are the primary beneficiary, which would require consolidation. As of March 31, 2024 and December 31, 2023, no VIEs qualified for consolidation as the structures of these entities do not provide us with the ability to direct activities that would significantly impact their economic performance. As of March 31, 2024 and December 31, 2023, the carrying value of our investments in nonconsolidated VIEs was $178 million and $175 million, respectively, and is included as non-marketable equity securities applying the equity method of accounting in long-term investments on our condensed consolidated balance sheets. The investments in nonconsolidated VIEs are primarily investments in funds that are limited partnerships or similar structures which are focused on increasing access to capital for underserved communities. Our maximum exposure to loss related to our nonconsolidated VIEs, which represents funded commitments and any future funding commitments, was $246

These condensed consolidated financial statements and accompanying notes should be read in conjunction with the audited consolidated financial statements and accompanying notes included in our Annual Report on Form 10-K for the year ended December 31, 2023 (the “2023 Form 10-K”) filed with the United States (“U.S.”) Securities and Exchange Commission (“SEC”) on February 8, 2024.

In the opinion of management, these condensed consolidated financial statements reflect all adjustments, consisting only of normal recurring adjustments, which are necessary for a fair statement of the condensed consolidated financial statements for all interim periods presented. Certain amounts for prior periods have been reclassified to conform to the financial statement presentation as of and for the three months ended March 31, 2024.

| 10 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

Use of estimates

The preparation of condensed consolidated financial statements in conformity with U.S. generally accepted accounting principles (“GAAP”) requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the condensed consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. On an ongoing basis, we evaluate our estimates, including those related to provisions for transaction and credit losses, income taxes, loss contingencies, revenue recognition, and the evaluation of strategic investments for impairment. We base our estimates on historical experience and various other assumptions which we believe to be reasonable under the circumstances. Actual results could materially differ from these estimates.

Recent accounting guidance

In November 2023, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) 2023-07, Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures. The amended guidance requires incremental reportable segment disclosures, primarily about significant segment expenses. The amendments also require entities with a single reportable segment to provide all disclosures required by these amendments, and all existing segment disclosures. The amendments will be applied retrospectively to all prior periods presented in the financial statements and is effective for fiscal years beginning after December 15, 2023, and interim periods in fiscal years beginning after December 15, 2024, with early adoption permitted. We are evaluating the impact this amended guidance may have on the footnotes to our condensed consolidated financial statements.

In December 2023, the FASB issued ASU 2023-08, Intangibles – Goodwill and Other – Crypto Assets (Subtopic 350-60): Accounting for and Disclosure of Crypto Assets. This amended guidance requires fair value measurement of certain crypto assets each reporting period with the changes in fair value reflected in net income. The amendments also require disclosures of the name, fair value, units held, and cost bases for each significant crypto asset held and annual reconciliations of crypto asset holdings. The new guidance is effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2024, with early adoption permitted. We are required to apply these amendments as a cumulative-effect adjustment to retained earnings as of the beginning of the fiscal year in which the guidance is adopted. The adoption of this guidance is not expected to have a material impact on our condensed consolidated financial statements based on our current crypto asset holdings and fair value.

In December 2023, the FASB issued ASU 2023-09, Income Taxes (Topic 740): Improvements to Income Tax Disclosures. The amended guidance enhances income tax disclosures primarily related to the effective tax rate reconciliation and income taxes paid information. This guidance requires disclosure of specific categories in the effective tax rate reconciliation and further information on reconciling items meeting a quantitative threshold. In addition, the amended guidance requires disaggregating income taxes paid (net of refunds received) by federal, state, and foreign taxes. It also requires disaggregating individual jurisdictions in which income taxes paid (net of refunds received) is equal to or greater than 5 percent of total income taxes paid (net of refunds received). The amended guidance is effective for fiscal years beginning after December 15, 2024. The guidance can be applied either prospectively or retrospectively. We are evaluating the impact this amended guidance may have on the footnotes to our condensed consolidated financial statements.

There are other new accounting pronouncements issued by the FASB that we have adopted or will adopt, as applicable. We do not believe any of these new accounting pronouncements have had, or will have, a material impact on our condensed consolidated financial statements or disclosures.

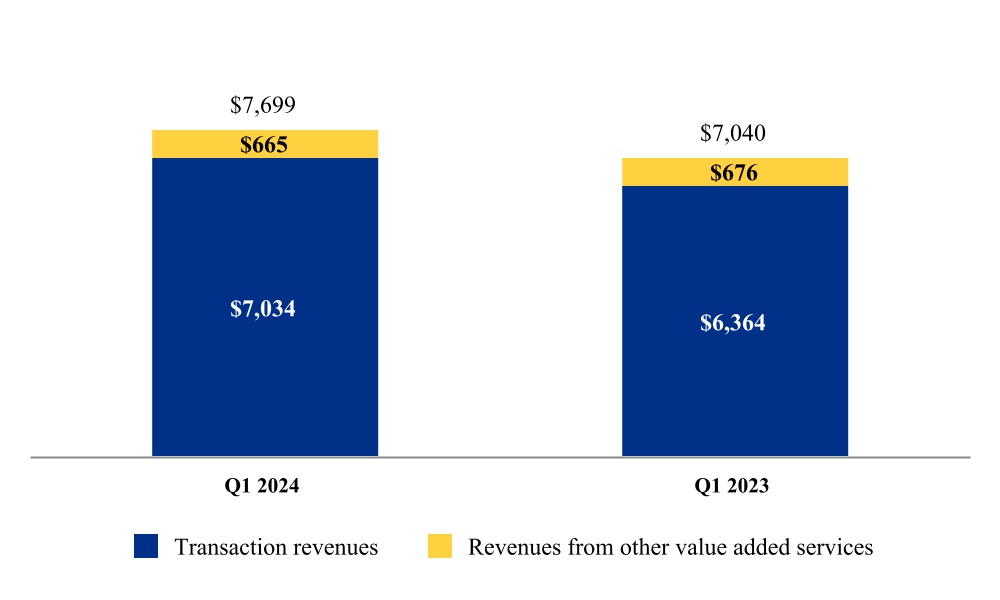

NOTE 2—REVENUE

We enable our customers to send and receive payments. We earn revenue primarily by completing payment transactions for our customers on our payments platform and from other value added services. Our revenues are classified into two categories: transaction revenues and revenues from other value added services.

| 11 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

DISAGGREGATION OF REVENUE

We determine operating segments based on how our chief operating decision maker (“CODM”) manages the business, makes operating decisions around the allocation of resources, and evaluates operating performance. Our CODM is our Chief Executive Officer, who regularly reviews our operating results on a consolidated basis. We operate as one segment and have one reportable segment. Based on the information provided to and reviewed by our CODM, we believe that the nature, amount, timing, and uncertainty of our revenue and cash flows and how they are affected by economic factors are most appropriately depicted through our primary geographical markets and types of revenue categories (transaction revenues and revenues from other value added services). Revenues recorded within these categories are earned from similar products and services for which the nature of associated fees and the related revenue recognition models are substantially similar.

The following table presents our revenue disaggregated by primary geographical market and category:

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (In millions) | |||||||||||

| Primary geographical markets | |||||||||||

| U.S. | $ | $ | |||||||||

Other countries(1) | |||||||||||

Total net revenues(2) | $ | $ | |||||||||

| Revenue category | |||||||||||

| Transaction revenues | $ | $ | |||||||||

| Revenues from other value added services | |||||||||||

Total net revenues(2) | $ | $ | |||||||||

(1) No single country included in the other countries category generated more than 10% of total net revenues.

(2) Total net revenues include $468 million and $451 million for the three months ended March 31, 2024 and 2023, respectively, which do not represent revenues recognized in the scope of Accounting Standards Codification Topic 606, Revenue from contracts with customers. Such revenues relate to interest and fees earned on loans and interest receivable, including loans and interest receivable, held for sale, as well as hedging gains or losses, and interest earned on certain assets underlying customer balances.

Net revenues are attributed to the country in which the party paying our fee is located.

NOTE 3—NET INCOME (LOSS) PER SHARE

Basic net income (loss) per share is computed by dividing net income (loss) for the period by the weighted average number of common shares outstanding during the period. Diluted net income (loss) per share is computed by dividing net income (loss) for the period by the weighted average number of shares of common stock and potentially dilutive common stock outstanding for the period. The dilutive effect of outstanding equity incentive awards is reflected in diluted net income (loss) per share by application of the treasury stock method. The calculation of diluted net income (loss) per share excludes all anti-dilutive common shares. During periods when we report net loss, diluted net loss per share is the same as basic net loss per share because the effects of potentially dilutive items would decrease the net loss per share.

| 12 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

The following table sets forth the computation of basic and diluted net income (loss) per share for the periods indicated:

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (In millions, except per share amounts) | |||||||||||

| Numerator: | |||||||||||

| Net income (loss) | $ | $ | |||||||||

| Denominator: | |||||||||||

| Weighted average shares of common stock - basic | |||||||||||

| Dilutive effect of equity incentive awards | |||||||||||

| Weighted average shares of common stock - diluted | |||||||||||

| Net income (loss) per share: | |||||||||||

| Basic | $ | $ | |||||||||

| Diluted | $ | $ | |||||||||

Common stock equivalents excluded from net income (loss) per diluted share because their effect would have been anti-dilutive or potentially dilutive | |||||||||||

NOTE 4—BUSINESS COMBINATIONS AND DIVESTITURES

NOTE 5—GOODWILL AND INTANGIBLE ASSETS

GOODWILL

The following table presents goodwill balances and adjustments to those balances during the three months ended March 31, 2024:

| December 31, 2023 | Goodwill Acquired | Adjustments | March 31, 2024 | ||||||||||||||||||||

| (In millions) | |||||||||||||||||||||||

| Total goodwill | $ | $ | $ | ( | $ | ||||||||||||||||||

The adjustments to goodwill during the three months ended March 31, 2024 pertained to foreign currency translation adjustments.

INTANGIBLE ASSETS

The components of identifiable intangible assets were as follows:

| March 31, 2024 | December 31, 2023 | ||||||||||||||||||||||||||||||||||||||||||||||

| Gross Carrying Amount | Accumulated Amortization | Net Carrying Amount | Weighted Average Useful Life (Years) | Gross Carrying Amount | Accumulated Amortization | Net Carrying Amount | Weighted Average Useful Life (Years) | ||||||||||||||||||||||||||||||||||||||||

| (In millions, except years) | |||||||||||||||||||||||||||||||||||||||||||||||

| Intangible assets: | |||||||||||||||||||||||||||||||||||||||||||||||

| Customer lists and user base | $ | $ | ( | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||||||||||||

| Marketing related | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||

| Developed technology | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||

| All other | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||

| Intangible assets, net | $ | $ | ( | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||||||||||||

| 13 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

Amortization expense for intangible assets was $56 million and $57 million for the three months ended March 31, 2024 and 2023, respectively. Additionally, in the three months ended March 31, 2023, we retired approximately $84 million of fully amortized intangible assets, of which $65 million and $19 million were included in customer lists and user base and developed technology, respectively.

Expected future intangible asset amortization as of March 31, 2024 was as follows (in millions):

| Fiscal years: | |||||

| Remaining 2024 | $ | ||||

| 2025 | |||||

| 2026 | |||||

| 2027 | |||||

| 2028 | |||||

| Total | $ | ||||

NOTE 6—LEASES

PayPal enters into various leases, which are primarily real estate operating leases. We use these properties for executive and administrative offices, data centers, product development offices, and customer services and operations centers. PayPal also enters into computer equipment finance leases.

While a majority of our lease agreements do not contain an explicit interest rate, certain of our lease agreements are subject to changes based on the Consumer Price Index or another referenced index. In the event of changes to the relevant index, lease liabilities are not remeasured and instead are treated as variable lease payments and recognized in the period in which the obligation for those payments is incurred.

The short-term lease exemption has been adopted for all leases with a duration of less than 12 months.

PayPal’s lease portfolio includes a small number of subleases. A sublease situation can arise when currently leased real estate space is available and is surplus to operational requirements.

The components of lease expense were as follows:

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (In millions) | |||||||||||

| Operating lease expense | $ | $ | |||||||||

| Sublease income | ( | ( | |||||||||

Total lease expense, net(1) | $ | $ | |||||||||

(1) During the three months ended March 31, 2024, finance lease expense was de minimis.

Supplemental cash flow information related to leases during the three months ended March 31, 2024 and 2023 were as follows:

| Three Months Ended March 31, 2024 | |||||

| (In millions) | |||||

| Cash paid for amounts included in the measurement of lease liabilities: | |||||

| Operating cash flows from operating leases | $ | ||||

Right-of-use (“ROU”) lease assets obtained in exchange for new operating lease liabilities | $ | ||||

| ROU lease assets obtained in exchange for new finance lease liabilities | $ | ||||

| 14 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

| Three Months Ended March 31, 2023 | |||||

| (In millions) | |||||

| Cash paid for amounts included in the measurement of lease liabilities: | |||||

| Operating cash flows from operating leases | $ | ||||

| ROU lease assets obtained in exchange for new operating lease liabilities | $ | ( | |||

Other non-cash ROU lease asset activity(1) | $ | ( | |||

(1) ROU lease asset impairment. Refer to “Note 17—Restructuring and Other” for further details.

Supplemental balance sheet information related to leases was as follows:

| March 31, 2024 | December 31, 2023 | ||||||||||||||||||||||

| (In millions, except weighted-average figures) | |||||||||||||||||||||||

Operating leases(1) | Finance leases(2) | Operating leases(1) | Finance leases(2) | ||||||||||||||||||||

| $ | $ | $ | $ | ||||||||||||||||||||

| Total lease liabilities | $ | $ | $ | $ | |||||||||||||||||||

| Weighted-average remaining lease term | — | ||||||||||||||||||||||

| Weighted-average discount rate | % | % | % | % | |||||||||||||||||||

(1) ROU assets for operating leases are included in “other assets” and lease liabilities for operating leases are included in “accrued expenses and other current liabilities” and “other long-term liabilities” on our condensed consolidated balance sheets.

(2) ROU assets for finance leases are included in “property and equipment, net” and lease liabilities for finance leases are included in “accrued expenses and other current liabilities” and “other long-term liabilities” on our condensed consolidated balance sheets.

Future minimum lease payments for our leases as of March 31, 2024 were as follows:

| Operating leases | Finance leases | ||||||||||

| Fiscal years: | (In millions) | ||||||||||

| Remaining 2024 | $ | $ | |||||||||

| 2025 | |||||||||||

| 2026 | |||||||||||

| 2027 | |||||||||||

| 2028 | |||||||||||

| Thereafter | |||||||||||

| Total | $ | $ | |||||||||

| Less: present value discount | ( | ||||||||||

| Lease liability | $ | $ | |||||||||

Operating lease amounts include minimum lease payments under our non-cancelable operating leases primarily for office and data center facilities. Finance lease amounts include minimum lease payments under our non-cancelable finance leases primarily for computer equipment. The amounts presented are consistent with contractual terms and are not expected to differ significantly from actual results under our existing leases.

As of March 31, 2024, we have additional operating leases, primarily for data centers, which will commence in the second quarter of 2024 or later with minimum lease payments aggregating to $102 million and lease terms ranging from to eight years . As of March 31, 2024, we have additional finance leases for computer equipment, which will commence in the second quarter of 2024 or later with minimum lease payments aggregating to $62 million and lease terms of five years .

| 15 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

NOTE 7—OTHER FINANCIAL STATEMENT DETAILS

CRYPTO ASSET SAFEGUARDING LIABILITY AND CORRESPONDING SAFEGUARDING ASSET

We allow our customers in certain markets to buy, hold, sell, convert, receive, and send certain cryptocurrencies as well as use the proceeds from sales of cryptocurrencies to pay for purchases at checkout. These cryptocurrencies consist of Bitcoin, Ethereum, Bitcoin Cash, Litecoin, and PayPal USD stablecoin (collectively, “our customers’ crypto assets”). We engage third parties, which are licensed trust companies, to provide certain custodial services, including holding our customers’ cryptographic key information, securing our customers’ crypto assets, and protecting them from loss or theft, including indemnification against certain types of losses such as theft. Our third-party custodians hold the crypto assets in a custodial account in PayPal’s name for the benefit of PayPal’s customers. We maintain the internal recordkeeping of our customers’ crypto assets, including the amount and type of crypto asset owned by each of our customers in that custodial account. As of March 31, 2024, we utilize two third-party custodians; as such, there is concentration risk in the event these custodians are not able to perform in accordance with our agreement.

The following table summarizes the significant crypto assets we hold for the benefit of our customers and the crypto asset safeguarding liability and corresponding safeguarding asset as of March 31, 2024 and December 31, 2023:

| March 31, 2024 | December 31, 2023 | ||||||||||

| (In millions) | |||||||||||

| Bitcoin | $ | $ | |||||||||

| Ethereum | |||||||||||

| Other | |||||||||||

| Crypto asset safeguarding liability | $ | $ | |||||||||

| Crypto asset safeguarding asset | $ | $ | |||||||||

| 16 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

ACCUMULATED OTHER COMPREHENSIVE INCOME (LOSS)

The following table summarizes the changes in accumulated balances of other comprehensive income (loss) for the three months ended March 31, 2024:

| Unrealized Gains (Losses) on Cash Flow Hedges | Unrealized Gains (Losses) on Available-for-sale Debt Securities | Foreign Currency Translation Adjustment (“CTA”) | Net Investment Hedges CTA Gains (Losses) | Estimated Tax (Expense) Benefit | Total | ||||||||||||||||||||||||||||||

| (In millions) | |||||||||||||||||||||||||||||||||||

| Beginning balance | $ | ( | $ | ( | $ | ( | $ | $ | ( | $ | ( | ||||||||||||||||||||||||

| Other comprehensive income (loss) before reclassifications | ( | ( | |||||||||||||||||||||||||||||||||

| Less: Amount of loss reclassified from accumulated other comprehensive income (loss) (“AOCI”) | ( | ( | |||||||||||||||||||||||||||||||||

| Net current period other comprehensive income (loss) | ( | ( | |||||||||||||||||||||||||||||||||

| Ending balance | $ | $ | ( | $ | ( | $ | $ | ( | $ | ( | |||||||||||||||||||||||||

The following table summarizes the changes in accumulated balances of other comprehensive income (loss) for the three months ended March 31, 2023:

| Unrealized Gains (Losses) on Cash Flow Hedges | Unrealized Gains (Losses) on Available-for-sale Debt Securities | Foreign CTA | Net Investment Hedges CTA Gains (Losses) | Estimated Tax (Expense) Benefit | Total | ||||||||||||||||||||||||||||||

| (In millions) | |||||||||||||||||||||||||||||||||||

| Beginning balance | $ | $ | ( | $ | ( | $ | ( | $ | $ | ( | |||||||||||||||||||||||||

| Other comprehensive income (loss) before reclassifications | ( | ( | ( | ||||||||||||||||||||||||||||||||

| Less: Amount of gain (loss) reclassified from AOCI | ( | ||||||||||||||||||||||||||||||||||

| Net current period other comprehensive income (loss) | ( | ( | ( | ||||||||||||||||||||||||||||||||

| Ending balance | $ | $ | ( | $ | ( | $ | $ | $ | ( | ||||||||||||||||||||||||||

The following table provides details about reclassifications out of AOCI for the periods presented below:

| Details about AOCI Components | Amount of Gains (Losses) Reclassified from AOCI | Affected Line Item in the Statements of Income (Loss) | ||||||||||||||||||

| Three Months Ended March 31, | ||||||||||||||||||||

| 2024 | 2023 | |||||||||||||||||||

| (In millions) | ||||||||||||||||||||

Gains on cash flow hedges—foreign currency exchange contracts | $ | $ | Net revenues | |||||||||||||||||

| Losses on investments | ( | ( | Net revenues | |||||||||||||||||

| Losses on investments | ( | Other income (expense), net | ||||||||||||||||||

| ( | Income before income taxes | |||||||||||||||||||

| Income tax expense | ||||||||||||||||||||

| Total reclassifications for the period | $ | ( | $ | Net income (loss) | ||||||||||||||||

| 17 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

OTHER INCOME (EXPENSE), NET

The following table reconciles the components of other income (expense), net for the periods presented below:

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (In millions) | |||||||||||

| Interest income | $ | $ | |||||||||

| Interest expense | ( | ( | |||||||||

| Net gains (losses) on strategic investments | ( | ||||||||||

| Other | |||||||||||

| Other income (expense), net | $ | $ | |||||||||

NOTE 8—CASH AND CASH EQUIVALENTS, FUNDS RECEIVABLE AND CUSTOMER ACCOUNTS, AND INVESTMENTS

The following table summarizes the assets underlying our cash and cash equivalents, funds receivable and customer accounts, short-term investments, and long-term investments as of March 31, 2024 and December 31, 2023:

| March 31, 2024 | December 31, 2023 | ||||||||||

| (In millions) | |||||||||||

Cash and cash equivalents(1) | $ | $ | |||||||||

| Funds receivable and customer accounts: | |||||||||||

Cash and cash equivalents(2) | $ | $ | |||||||||

| Time deposits | |||||||||||

| Available-for-sale debt securities | |||||||||||

| Funds receivable | |||||||||||

| Total funds receivable and customer accounts | $ | $ | |||||||||

| Short-term investments: | |||||||||||

| Time deposits | $ | $ | |||||||||

| Available-for-sale debt securities | |||||||||||

| Restricted cash | |||||||||||

| Total short-term investments | $ | $ | |||||||||

| Long-term investments: | |||||||||||

| Time deposits | $ | $ | |||||||||

| Available-for-sale debt securities | |||||||||||

| Strategic investments | |||||||||||

| Total long-term investments | $ | $ | |||||||||

(1) Includes $1.5 billion and $777 million of available-for-sale debt securities with original maturities of three months or less as of March 31, 2024 and December 31, 2023, respectively.

(2) Includes $931 million and $399 million of available-for-sale debt securities with original maturities of three months or less as of March 31, 2024 and December 31, 2023, respectively.

| 18 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

As of March 31, 2024 and December 31, 2023, the estimated fair value of our available-for-sale debt securities included within cash and cash equivalents, funds receivable and customer accounts, short-term investments, and long-term investments was as follows:

March 31, 2024(1) | |||||||||||||||||||||||

| Gross Amortized Cost | Gross Unrealized Gains | Gross Unrealized Losses | Estimated Fair Value | ||||||||||||||||||||

| (In millions) | |||||||||||||||||||||||

| Cash and cash equivalents: | |||||||||||||||||||||||

| U.S. government and agency securities | $ | $ | $ | $ | |||||||||||||||||||

| Commercial paper | |||||||||||||||||||||||

| Funds receivable and customer accounts: | |||||||||||||||||||||||

| U.S. government and agency securities | ( | ||||||||||||||||||||||

| Foreign government and agency securities | |||||||||||||||||||||||

| Corporate debt securities | ( | ||||||||||||||||||||||

| Asset-backed securities | ( | ||||||||||||||||||||||

| Municipal securities | ( | ||||||||||||||||||||||

| Commercial paper | ( | ||||||||||||||||||||||

| Short-term investments: | |||||||||||||||||||||||

| U.S. government and agency securities | ( | ||||||||||||||||||||||

| Foreign government and agency securities | ( | ||||||||||||||||||||||

| Corporate debt securities | ( | ||||||||||||||||||||||

| Asset-backed securities | ( | ||||||||||||||||||||||

| Commercial paper | ( | ||||||||||||||||||||||

| Long-term investments: | |||||||||||||||||||||||

| U.S. government and agency securities | ( | ||||||||||||||||||||||

| Foreign government and agency securities | ( | ||||||||||||||||||||||

| Corporate debt securities | ( | ||||||||||||||||||||||

| Asset-backed securities | |||||||||||||||||||||||

Total available-for-sale debt securities(2) | $ | $ | $ | ( | $ | ||||||||||||||||||

(1) “—” Denotes gross unrealized gain or unrealized loss of less than $1 million in a given position.

(2) Excludes foreign currency denominated available-for-sale debt securities accounted for under the fair value option. Refer to “Note 9—Fair Value Measurement of Assets and Liabilities.”

| 19 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

December 31, 2023(1) | |||||||||||||||||||||||

| Gross Amortized Cost | Gross Unrealized Gains | Gross Unrealized Losses | Estimated Fair Value | ||||||||||||||||||||

| (In millions) | |||||||||||||||||||||||

| Cash and cash equivalents: | |||||||||||||||||||||||

| U.S. government and agency securities | $ | $ | $ | $ | |||||||||||||||||||

| Commercial paper | |||||||||||||||||||||||

| Funds receivable and customer accounts: | |||||||||||||||||||||||

| U.S. government and agency securities | ( | ||||||||||||||||||||||

| Foreign government and agency securities | ( | ||||||||||||||||||||||

| Corporate debt securities | ( | ||||||||||||||||||||||

| Asset-backed securities | ( | ||||||||||||||||||||||

| Municipal securities | ( | ||||||||||||||||||||||

| Commercial paper | ( | ||||||||||||||||||||||

| Short-term investments: | |||||||||||||||||||||||

| U.S. government and agency securities | ( | ||||||||||||||||||||||

| Foreign government and agency securities | ( | ||||||||||||||||||||||

| Corporate debt securities | ( | ||||||||||||||||||||||

| Asset-backed securities | ( | ||||||||||||||||||||||

| Commercial paper | ( | ||||||||||||||||||||||

| Long-term investments: | |||||||||||||||||||||||

| U.S. government and agency securities | ( | ||||||||||||||||||||||

| Foreign government and agency securities | ( | ||||||||||||||||||||||

| Corporate debt securities | ( | ||||||||||||||||||||||

| Asset-backed securities | |||||||||||||||||||||||

Total available-for-sale debt securities(2) | $ | $ | $ | ( | $ | ||||||||||||||||||

(1) “—” Denotes gross unrealized gain or unrealized loss of less than $1 million in a given position.

(2) Excludes foreign currency denominated available-for-sale debt securities accounted for under the fair value option. Refer to “Note 9—Fair Value Measurement of Assets and Liabilities.”

Gross amortized cost and estimated fair value balances exclude accrued interest receivable on available-for-sale debt securities, which totaled $108 million and $101 million at March 31, 2024 and December 31, 2023, respectively, and were included in on our condensed consolidated balance sheets.

| 20 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

As of March 31, 2024 and December 31, 2023, the gross unrealized losses and estimated fair value of our available-for-sale debt securities included within cash and cash equivalents, funds receivable and customer accounts, short-term investments, and long-term investments for which an allowance for credit losses was not deemed necessary in the current period, aggregated by the length of time those individual securities have been in a continuous loss position, was as follows:

March 31, 2024(1) | |||||||||||||||||||||||||||||||||||

| Less than 12 months | 12 months or longer | Total | |||||||||||||||||||||||||||||||||

| Fair Value | Gross Unrealized Losses | Fair Value | Gross Unrealized Losses | Fair Value | Gross Unrealized Losses | ||||||||||||||||||||||||||||||

| (In millions) | |||||||||||||||||||||||||||||||||||

| Cash and cash equivalents: | |||||||||||||||||||||||||||||||||||

| U.S. government and agency securities | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| Commercial paper | |||||||||||||||||||||||||||||||||||

| Funds receivable and customer accounts: | |||||||||||||||||||||||||||||||||||

| U.S. government and agency securities | ( | ( | ( | ||||||||||||||||||||||||||||||||

| Foreign government and agency securities | |||||||||||||||||||||||||||||||||||

| Corporate debt securities | ( | ( | |||||||||||||||||||||||||||||||||

| Asset-backed securities | ( | ( | |||||||||||||||||||||||||||||||||

| Municipal securities | ( | ( | ( | ||||||||||||||||||||||||||||||||

| Commercial paper | ( | ( | |||||||||||||||||||||||||||||||||

| Short-term investments: | |||||||||||||||||||||||||||||||||||

| U.S. government and agency securities | ( | ( | |||||||||||||||||||||||||||||||||

| Foreign government and agency securities | ( | ( | |||||||||||||||||||||||||||||||||

| Corporate debt securities | ( | ( | ( | ||||||||||||||||||||||||||||||||

| Asset-backed securities | ( | ( | |||||||||||||||||||||||||||||||||

| Commercial paper | ( | ( | |||||||||||||||||||||||||||||||||

| Long-term investments: | |||||||||||||||||||||||||||||||||||

| U.S. government and agency securities | ( | ( | |||||||||||||||||||||||||||||||||

| Foreign government and agency securities | ( | ( | ( | ||||||||||||||||||||||||||||||||

| Corporate debt securities | ( | ( | |||||||||||||||||||||||||||||||||

| Asset-backed securities | |||||||||||||||||||||||||||||||||||

| Total available-for-sale debt securities | $ | $ | ( | $ | $ | ( | $ | $ | ( | ||||||||||||||||||||||||||

(1) “—” Denotes gross unrealized loss or fair value of less than $1 million in a given position.

| 21 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

December 31, 2023(1) | |||||||||||||||||||||||||||||||||||

| Less than 12 months | 12 months or longer | Total | |||||||||||||||||||||||||||||||||

| Fair Value | Gross Unrealized Losses | Fair Value | Gross Unrealized Losses | Fair Value | Gross Unrealized Losses | ||||||||||||||||||||||||||||||

| (In millions) | |||||||||||||||||||||||||||||||||||

| Cash and cash equivalents: | |||||||||||||||||||||||||||||||||||

| Commercial paper | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| Funds receivable and customer accounts: | |||||||||||||||||||||||||||||||||||

| U.S. government and agency securities | ( | ( | ( | ||||||||||||||||||||||||||||||||

| Foreign government and agency securities | ( | ( | |||||||||||||||||||||||||||||||||

| Corporate debt securities | ( | ( | |||||||||||||||||||||||||||||||||

| Asset-backed securities | ( | ( | |||||||||||||||||||||||||||||||||

| Municipal securities | ( | ( | ( | ||||||||||||||||||||||||||||||||

| Commercial paper | ( | ( | |||||||||||||||||||||||||||||||||

| Short-term investments: | |||||||||||||||||||||||||||||||||||

| U.S. government and agency securities | ( | ( | |||||||||||||||||||||||||||||||||

| Foreign government and agency securities | ( | ( | |||||||||||||||||||||||||||||||||

| Corporate debt securities | ( | ( | |||||||||||||||||||||||||||||||||

| Asset-backed securities | ( | ( | |||||||||||||||||||||||||||||||||

| Commercial paper | ( | ( | |||||||||||||||||||||||||||||||||

| Long-term investments: | |||||||||||||||||||||||||||||||||||

| U.S. government and agency securities | ( | ( | |||||||||||||||||||||||||||||||||

| Foreign government and agency securities | ( | ( | |||||||||||||||||||||||||||||||||

| Corporate debt securities | ( | ( | |||||||||||||||||||||||||||||||||

| Asset-backed securities | |||||||||||||||||||||||||||||||||||

| Total available-for-sale debt securities | $ | $ | ( | $ | $ | ( | $ | $ | ( | ||||||||||||||||||||||||||

(1) “—” Denotes gross unrealized loss or fair value of less than $1 million in a given position.

Unrealized losses have not been recognized into income as we neither intend to sell, nor anticipate that it is more likely than not that we will be required to sell, the securities before recovery of their amortized cost basis. The decline in fair value is due primarily to changes in market interest rates, rather than credit losses. We will continue to monitor the performance of the investment portfolio and assess whether impairment due to expected credit losses has occurred. During the three months ended March 31, 2024, we received $11.3 billion in proceeds from the sale and maturity of available-for-sale debt securities and incurred gross realized losses of $42 million. During the three months ended March 31, 2023, we received $6.4 billion in proceeds from the sale and maturity of available-for-sale debt securities and incurred gross realized losses of $25 million. Gross realized gains and losses were determined using the specific identification method.

Our available-for-sale debt securities included within cash and cash equivalents, funds receivable and customer accounts, short-term investments, and long-term investments classified by date of contractual maturity were as follows:

| March 31, 2024 | |||||||||||

| Amortized Cost | Fair Value | ||||||||||

| (In millions) | |||||||||||

| One year or less | $ | $ | |||||||||

| After one year through five years | |||||||||||

| After five years through ten years | |||||||||||

| After ten years | |||||||||||

| Total | $ | $ | |||||||||

Actual maturities may differ from contractual maturities as certain securities may be prepaid.

| 22 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

Supplemental cash flow information related to investments

Non-cash investing transactions that are not reflected in the condensed consolidated statement of cash flows for the three months ended March 31, 2024 include the purchase of investments not yet settled of $413 million.

STRATEGIC INVESTMENTS

Our strategic investments include marketable equity securities, which are publicly traded, and non-marketable equity securities, which are primarily investments in privately held companies. Our marketable equity securities have readily determinable fair values and are recorded as long-term investments on our condensed consolidated balance sheets at fair value with changes in fair value recorded in other income (expense), net on our condensed consolidated statements of income (loss). Marketable equity securities totaled $21 million and $24 million as of March 31, 2024 and December 31, 2023, respectively.

Our non-marketable equity securities are recorded in long-term investments on our condensed consolidated balance sheets. The carrying value of our non-marketable equity securities totaled $1.8 185 million and $182 million, respectively, for which we have the ability to exercise significant influence, but not control, over the investee. We account for these equity securities using the equity method of accounting. The remaining non-marketable equity securities do not have a readily determinable fair value and we measure these equity investments at cost minus impairment, if any, and adjust for changes resulting from observable price changes in orderly transactions for an identical or similar investment in the same issuer (the “Measurement Alternative”). All gains and losses on these investments, realized and unrealized, and our share of earnings or losses from investments accounted for using the equity method are recognized in other income (expense), net on our condensed consolidated statements of income (loss).

Measurement Alternative adjustments

The adjustments to the carrying value of our non-marketable equity securities accounted for under the Measurement Alternative in the three months ended March 31, 2024 and 2023 were as follows:

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (In millions) | |||||||||||

| Carrying amount, beginning of period | $ | $ | |||||||||

| Adjustments related to non-marketable equity securities: | |||||||||||

Net additions(1) | |||||||||||

| Gross unrealized gains | |||||||||||

| Gross unrealized losses and impairments | ( | ( | |||||||||

| Carrying amount, end of period | $ | $ | |||||||||

(1) Net additions include purchases, reductions due to sales of securities, and reclassifications when the Measurement Alternative is subsequently elected or no longer applies.

The following table summarizes the cumulative gross unrealized gains and cumulative gross unrealized losses and impairment related to non-marketable equity securities accounted for under the Measurement Alternative, held at March 31, 2024 and December 31, 2023, respectively:

| March 31, 2024 | December 31, 2023 | ||||||||||

| (In millions) | |||||||||||

| Cumulative gross unrealized gains | $ | $ | |||||||||

| Cumulative gross unrealized losses and impairments | $ | ( | $ | ( | |||||||

| 23 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

Unrealized gains (losses) on strategic investments, excluding those accounted for using the equity method

The following table summarizes the net unrealized gains (losses) on marketable and non-marketable equity securities, excluding those accounted for using the equity method, held at March 31, 2024 and 2023, respectively:

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (In millions) | |||||||||||

| Net unrealized gains (losses) | $ | ( | $ | ||||||||

| 24 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

NOTE 9—FAIR VALUE MEASUREMENT OF ASSETS AND LIABILITIES

FINANCIAL ASSETS AND LIABILITIES MEASURED AND RECORDED AT FAIR VALUE ON A RECURRING BASIS

The following tables summarize our financial assets and liabilities measured at fair value on a recurring basis as of March 31, 2024 and December 31, 2023:

| March 31, 2024 | Quoted Prices in Active Markets for Identical Assets (Level 1) | Significant Other Observable Inputs (Level 2) | ||||||||||||||||||

| (In millions) | ||||||||||||||||||||

| Assets: | ||||||||||||||||||||

Cash and cash equivalents(1) | ||||||||||||||||||||

| U.S. government and agency securities | $ | $ | $ | |||||||||||||||||

| Commercial paper | ||||||||||||||||||||

| Total cash and cash equivalents | ||||||||||||||||||||

Short-term investments(2): | ||||||||||||||||||||

| U.S. government and agency securities | ||||||||||||||||||||

| Foreign government and agency securities | ||||||||||||||||||||

| Corporate debt securities | ||||||||||||||||||||

| Asset-backed securities | ||||||||||||||||||||

| Commercial paper | ||||||||||||||||||||

| Total short-term investments | ||||||||||||||||||||

Funds receivable and customer accounts(3): | ||||||||||||||||||||

| U.S. government and agency securities | ||||||||||||||||||||

| Foreign government and agency securities | ||||||||||||||||||||

| Corporate debt securities | ||||||||||||||||||||

| Asset-backed securities | ||||||||||||||||||||

| Municipal securities | ||||||||||||||||||||

| Commercial paper | ||||||||||||||||||||

| Total funds receivable and customer accounts | ||||||||||||||||||||

Derivatives(4) | ||||||||||||||||||||

Crypto asset safeguarding asset(4) | ||||||||||||||||||||

Long-term investments(2),(5): | ||||||||||||||||||||

| U.S. government and agency securities | ||||||||||||||||||||

| Foreign government and agency securities | ||||||||||||||||||||

| Corporate debt securities | ||||||||||||||||||||

| Asset-backed securities | ||||||||||||||||||||

| Marketable equity securities | ||||||||||||||||||||

| Total long-term investments | ||||||||||||||||||||

| Total financial assets | $ | $ | $ | |||||||||||||||||

| Liabilities: | ||||||||||||||||||||

Derivatives(4) | $ | $ | $ | |||||||||||||||||

Crypto asset safeguarding liability(4) | ||||||||||||||||||||

| Total financial liabilities | $ | $ | $ | |||||||||||||||||

(1) Excludes cash of $8.2 billion not measured and recorded at fair value.

(2) Excludes restricted cash of $3 million and time deposits of $140 million not measured and recorded at fair value.

(3) Excludes cash, time deposits, and funds receivable of $23.3 billion underlying funds receivable and customer accounts not measured and recorded at fair value.

| 25 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

(4) Derivative assets and liabilities are included within “prepaid expenses and other current assets” and “other assets” and “accrued expenses and other current liabilities” and “other long-term liabilities,” respectively, on our condensed consolidated balance sheets. Crypto safeguarding asset and associated liability are recorded within “prepaid expenses and other current assets” and “accrued expenses and other current liabilities,” respectively, on our condensed consolidated balance sheets.

(5) Excludes non-marketable equity securities of $1.8 billion measured using the Measurement Alternative or equity method accounting.

| December 31, 2023 | Quoted Prices in Active Markets for Identical Assets (Level 1) | Significant Other Observable Inputs (Level 2) | ||||||||||||||||||

| (In millions) | ||||||||||||||||||||

| Assets: | ||||||||||||||||||||

Cash and cash equivalents(1) | ||||||||||||||||||||

| U.S. government and agency securities | $ | $ | $ | |||||||||||||||||

| Commercial paper | ||||||||||||||||||||

| Money market fund | ||||||||||||||||||||

| Total cash and cash equivalents | ||||||||||||||||||||

Short-term investments(2): | ||||||||||||||||||||

| U.S. government and agency securities | ||||||||||||||||||||

| Foreign government and agency securities | ||||||||||||||||||||

| Corporate debt securities | ||||||||||||||||||||

| Asset-backed securities | ||||||||||||||||||||

| Commercial paper | ||||||||||||||||||||

| Total short-term investments | ||||||||||||||||||||

Funds receivable and customer accounts(3): | ||||||||||||||||||||

| U.S. government and agency securities | ||||||||||||||||||||

| Foreign government and agency securities | ||||||||||||||||||||

| Corporate debt securities | ||||||||||||||||||||

| Asset-backed securities | ||||||||||||||||||||

| Municipal securities | ||||||||||||||||||||

| Commercial paper | ||||||||||||||||||||

| Total funds receivable and customer accounts | ||||||||||||||||||||

Derivatives(4) | ||||||||||||||||||||

Crypto asset safeguarding asset(4) | ||||||||||||||||||||

Long-term investments(2), (5): | ||||||||||||||||||||

| U.S. government and agency securities | ||||||||||||||||||||

| Foreign government and agency securities | ||||||||||||||||||||

| Corporate debt securities | ||||||||||||||||||||

| Asset-backed securities | ||||||||||||||||||||

| Marketable equity securities | ||||||||||||||||||||

| Total long-term investments | ||||||||||||||||||||

| Total financial assets | $ | $ | $ | |||||||||||||||||

| Liabilities: | ||||||||||||||||||||

Derivatives(4) | $ | $ | $ | |||||||||||||||||

Crypto asset safeguarding liability(4) | ||||||||||||||||||||

| Total financial liabilities | $ | $ | $ | |||||||||||||||||

(1) Excludes cash of $8.1 billion not measured and recorded at fair value.

(2) Excludes restricted cash of $3 million and time deposits of $173 million not measured and recorded at fair value.

(3) Excludes cash, time deposits, and funds receivable of $22.8 billion underlying funds receivable and customer accounts not measured and recorded at fair value.

| 26 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

(4) Derivative assets and liabilities are included within “prepaid expenses and other current assets” and “other assets” and “accrued expenses and other current liabilities” and “other long-term liabilities,” respectively, on our condensed consolidated balance sheets. Crypto safeguarding asset and associated liability are recorded within “prepaid expenses and other current assets” and “accrued expenses and other current liabilities,” respectively, on our condensed consolidated balance sheets.

(5) Excludes non-marketable equity securities of $1.8 billion measured using the Measurement Alternative or equity method accounting.

Our marketable equity securities are valued using quoted prices for identical assets in active markets (Level 1). There are no active markets for our crypto asset safeguarding liability or the corresponding safeguarding asset. Accordingly, we have valued the asset and liability using quoted prices on the active exchange that we have identified as the principal market for the underlying crypto assets (Level 2). All other financial assets and liabilities are valued using quoted prices for identical instruments in less active markets, readily available pricing sources for comparable instruments, or models using market observable inputs (Level 2).

A majority of our derivative instruments are valued using pricing models that take into account the contract terms as well as multiple observable inputs where applicable, such as currency rates, interest rate yield curves, option volatility, and equity prices (Level 2).

As of March 31, 2024 and December 31, 2023, we did not have any assets or liabilities requiring measurement at fair value on a recurring basis with significant unobservable inputs that would require a high level of judgment to determine fair value (Level 3).

We elect to account for available-for-sale debt securities denominated in currencies other than the functional currency of our subsidiaries under the fair value option. Election of the fair value option allows us to recognize any gains and losses from fair value changes on such investments in other income (expense), net on the condensed consolidated statements of income (loss) to significantly reduce the accounting asymmetry that would otherwise arise when recognizing the corresponding foreign exchange gains and losses relating to customer liabilities. The following table summarizes the estimated fair value and amortized cost of our available-for-sale debt securities under the fair value option as of March 31, 2024 and December 31, 2023:

| March 31, 2024 | December 31, 2023 | ||||||||||||||||||||||

| Amortized Cost | Fair Value | Amortized Cost | Fair Value | ||||||||||||||||||||

| (In millions) | (In millions) | ||||||||||||||||||||||

| Funds receivable and customer accounts | $ | $ | $ | $ | |||||||||||||||||||

The following table summarizes the gains (losses) from fair value changes recognized in other income (expense), net related to the available-for-sale debt securities under the fair value option for the three months ended March 31, 2024 and 2023:

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (In millions) | |||||||||||

| Funds receivable and customer accounts | $ | ( | $ | ||||||||

| 27 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

ASSETS MEASURED AND RECORDED AT FAIR VALUE ON A NON-RECURRING BASIS

The following tables summarize our assets held as of March 31, 2024 and December 31, 2023 for which a non-recurring fair value measurement was recorded during the three months ended March 31, 2024 and the year ended December 31, 2023, respectively:

| March 31, 2024 | Significant Other Observable Inputs (Level 2) | Significant Other Unobservable Inputs (Level 3) | ||||||||||||||||||

| (In millions) | ||||||||||||||||||||

| Loans and interest receivable, held for sale | $ | $ | $ | |||||||||||||||||

Non-marketable equity securities measured using the Measurement Alternative(1) | ||||||||||||||||||||

| Total | $ | $ | $ | |||||||||||||||||

(1) Excludes non-marketable equity securities of $1.6 billion accounted for under the Measurement Alternative for which no observable price changes occurred during the three months ended March 31, 2024.

| December 31, 2023 | Significant Other Observable Inputs (Level 2) | Significant Other Unobservable Inputs (Level 3) | ||||||||||||||||||

| (In millions) | ||||||||||||||||||||

Loans and interest receivable, held for sale(1) | $ | $ | $ | |||||||||||||||||

Non-marketable equity investments measured using the Measurement Alternative(2) | ||||||||||||||||||||

Other assets(3) | ||||||||||||||||||||

| Total | $ | $ | $ | |||||||||||||||||

(1) As of December 31, 2023, loans and interest receivable, held for sale were valued using a price-based model. The price was the significant unobservable input and was determined based upon certain loan and risk classifications of the portfolio. Low, high and weighted average prices were all $0.99 1.00 par.

(2) Excludes non-marketable equity securities of $1.2 billion accounted for under the Measurement Alternative for which no observable price changes occurred during the year ended December 31, 2023.

(3) Consists of ROU lease assets recorded at fair value pursuant to impairment charges that occurred during the year ended December 31, 2023.

Beginning with the first quarter of 2024, we measure loans and interest receivable, held for sale using observable inputs, such as the most recent executed prices for comparable loans sold to the global investment firm. Accordingly, loans and interest receivable, held for sale are classified within Level 2 in the fair value hierarchy. Refer to “Note 11—Loans and interest receivable” for additional information on loans and interest receivable, held for sale.

We measure the non-marketable equity securities accounted for under the Measurement Alternative at cost minus impairment, if any, adjusted for observable price changes in orderly transactions for an identical or similar investment in the same issuer. Non-marketable equity securities that have been remeasured during the period based on observable price changes are classified within Level 2 in the fair value hierarchy because we estimate the fair value based on valuation methods which only include significant inputs that are observable, such as the observable transaction price at the transaction date. The fair value of non-marketable equity securities are classified within Level 3 when we estimate fair value using significant unobservable inputs such as when we remeasure due to impairment and use discount rates, forecasted cash flows, and market data of comparable companies, among others.

We evaluate ROU assets related to leases for indicators of impairment whenever events or changes in circumstances indicate that the carrying amount of an ROU asset may not be recoverable. Impairment losses on ROU lease assets related to office operating leases are calculated using estimated rental income per square foot derived from observable market data, and the impaired asset is classified within Level 2 in the fair value hierarchy.

| 28 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

FINANCIAL ASSETS AND LIABILITIES NOT MEASURED AND RECORDED AT FAIR VALUE

NOTE 10—DERIVATIVE INSTRUMENTS

SUMMARY OF DERIVATIVE INSTRUMENTS

Our primary objective in holding derivatives is to reduce the volatility of earnings and cash flows associated with changes in foreign currency exchange rates. Our derivatives expose us to credit risk to the extent that our counterparties may be unable to meet the terms of the arrangement. We seek to mitigate such risk by limiting our counterparties to, and by spreading the risk across, major financial institutions and by entering into collateral security arrangements. In addition, the potential risk of loss with any one counterparty resulting from this type of credit risk is monitored on an ongoing basis. We do not use any derivative instruments for trading or speculative purposes.

Cash flow hedges

We have significant international revenues and expenses denominated in foreign currencies, which subjects us to foreign currency exchange risk. We have a foreign currency exposure management program in which we designate certain foreign currency exchange contracts, generally with maturities of 12 months or less, to reduce the volatility of cash flows primarily related to forecasted revenues and expenses denominated in certain foreign currencies. The objective of these foreign currency exchange contracts is to help mitigate the risk that the U.S. dollar-equivalent cash flows are adversely affected by changes in the applicable U.S. dollar/foreign currency exchange rate. These derivative instruments are designated as cash flow hedges and accordingly, the derivative’s gain or loss is initially reported as a component of AOCI and subsequently reclassified into revenue or applicable expense line item in the condensed consolidated statements of income (loss) in the same period the forecasted transaction affects earnings. We evaluate the effectiveness of our foreign currency exchange contracts on a quarterly basis by comparing the critical terms of the derivative instruments with the critical terms of the forecasted cash flows of the hedged item; if the critical terms are the same, we conclude the hedge will be perfectly effective. We do not exclude any component of the changes in fair value of the derivative instruments from the assessment of hedge effectiveness. We report cash flows arising from derivative instruments consistent with the classification of cash flows from the underlying hedged items that these derivatives are hedging. Accordingly, the cash flows associated with derivatives designated as cash flow hedges are classified in cash flows from operating activities on our condensed consolidated statements of cash flows.

As of March 31, 2024, we estimated that $40 million of net derivative gains related to our cash flow hedges included in AOCI are expected to be reclassified into earnings within the next 12 months. During the three months ended March 31, 2024 and 2023, we did not discontinue any cash flow hedges because it was probable that the original forecasted transaction would not occur and as such, did not reclassify any gains or losses to earnings prior to the occurrence of the hedged transaction. If we elect to discontinue our cash flow hedges and it is probable that the original forecasted transaction will occur, we continue to report the derivative’s gain or loss in AOCI until the forecasted transaction affects earnings, at which point we also reclassify it into earnings. Gains and losses on derivatives held after we discontinue our cash flow hedges and on derivative instruments that are not designated as cash flow hedges are recorded in the same financial statement line item to which the derivative relates.

| 29 | ||||||||||

PayPal Holdings, Inc.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

(Unaudited)

Net investment hedges

We use forward foreign currency exchange contracts to reduce the foreign currency exchange risk related to our investment in certain foreign subsidiaries. These derivatives are designated as net investment hedges and accordingly, the gains and losses on the portion of the derivatives included in the assessment of hedge effectiveness is recorded in AOCI as part of foreign currency translation. We exclude forward points from the assessment of hedge effectiveness and recognize them in other income (expense), net on a straight-line basis over the life of the hedge. The accumulated gains and losses associated with these instruments will remain in AOCI until the foreign subsidiaries are sold or substantially liquidated, at which point they will be reclassified into earnings. The cash flows associated with derivatives designated as a net investment hedge are classified in cash flows from investing activities on our condensed consolidated statements of cash flows.

We have no

Foreign currency exchange contracts not designated as hedging instruments