UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

Filed by the Registrant ☒

Filed by a Party other than the Registrant ☐

Check the appropriate box:

|

☐ |

Preliminary Proxy Statement |

|

☐ |

Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

|

☒ |

Definitive Proxy Statement |

|

☐ |

Definitive Additional Materials |

|

☐ |

Soliciting Material under § 240.14a-12 |

|

Cable One, Inc. |

|

(Name of Registrant as Specified in Its Charter) |

|

|

|

|

|

(Name of Person(s) Filing Proxy Statement, if Other than the Registrant) |

Payment of Filing Fee (Check the appropriate box):

|

☒ |

No fee required. |

|

☐ |

Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

|

|

(1) |

Title of each class of securities to which the transaction applies: |

|

|

(2) |

Aggregate number of securities to which the transaction applies: |

|

|

(3) |

Per unit price or other underlying value of the transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

|

|

(4) |

Proposed maximum aggregate value of the transaction: |

|

|

(5) |

Total fee paid: |

|

☐ |

Fee paid previously with preliminary materials. |

|

☐ |

Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

|

|

(1) |

Amount Previously Paid: |

|

|

(2) |

Form, Schedule or Registration Statement No.: |

|

|

(3) |

Filing Party: |

|

|

(4) |

Date Filed: |

|

|

210 E. Earll Drive Phoenix, AZ 85012 |

April 3, 2018

Dear Fellow Stockholders:

I am pleased to invite you to attend the 2018 Annual Meeting of Stockholders (the “Annual Meeting”) of Cable One, Inc. (the “Company”). The Annual Meeting will be held at the Company’s headquarters, 210 East Earll Drive, Phoenix, Arizona, 85012, on Tuesday, May 8, 2018, at 8:00 a.m., local time.

Included with this letter are a Notice of Annual Meeting of Stockholders and Proxy Statement, which describe the business to be conducted at the Annual Meeting.

Your vote is important. Whether or not you plan to attend the Annual Meeting, we hope you will vote as soon as possible. You may vote over the internet, as well as by telephone, or, if you requested to receive printed proxy materials, by returning a proxy card or voting instruction form in the envelope provided. If you plan to attend the Annual Meeting, kindly so indicate in the space provided on the proxy card or when prompted if voting over the internet or by telephone.

Sincerely,

/s/ Julia M. Laulis

Julia M. Laulis

Chair of the Board, President and

Chief Executive Officer

CABLE ONE, INC.

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

May 8, 2018

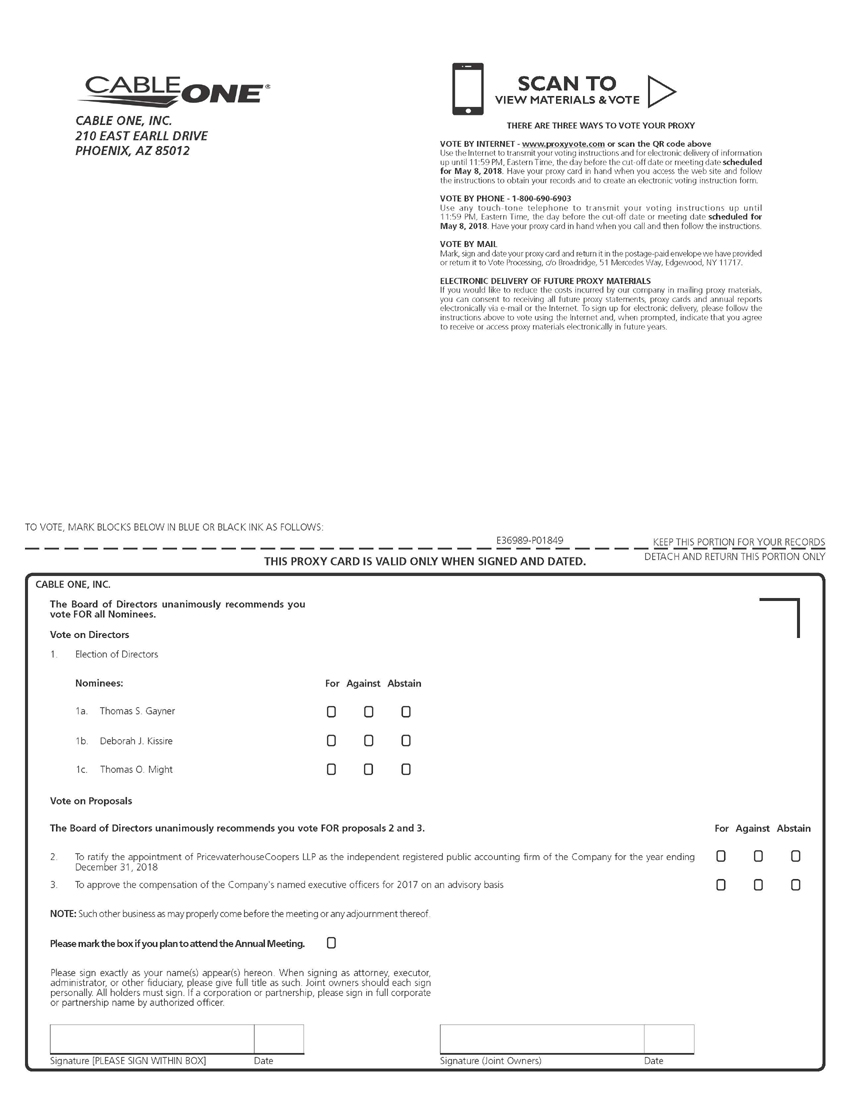

The 2018 Annual Meeting of Stockholders of Cable One, Inc. (the “Company”) will be held at the Company’s headquarters, 210 East Earll Drive, Phoenix, Arizona, 85012, on Tuesday, May 8, 2018, at 8:00 a.m., local time, for the following purposes:

|

1. |

To elect three Class III directors to hold office until the 2021 annual meeting of stockholders and until their respective successors are elected and qualified, as more fully described in the accompanying Proxy Statement. |

|

2. |

To ratify the appointment of PricewaterhouseCoopers LLP as the independent registered public accounting firm of the Company for the year ending December 31, 2018. |

|

3. |

To approve the compensation of the Company’s named executive officers for 2017 on an advisory basis. |

|

4. |

To transact such other business as may properly come before the meeting or any adjournment thereof. |

The Board of Directors of the Company has fixed the close of business on March 16, 2018, as the record date for the determination of stockholders entitled to notice of and to vote at the meeting.

It is important that your shares be represented and voted at the meeting. Please sign and return your proxy card at your earliest convenience. You may also vote your shares by telephone or over the internet. If you choose to vote your shares by telephone or over the internet, please follow the instructions in the enclosed Proxy Statement and proxy card. You may revoke your proxy at any time before it has been voted at the meeting. You may vote in person at the meeting even if you have previously given your proxy. For shares held through a broker, bank or other nominee, you may vote submitting voting instructions as provided by your broker, bank or other nominee; however, you may not vote such shares in person at the meeting unless you have a proxy executed in your favor by your broker, bank or other nominee.

By Order of the Board of Directors,

/s/ Peter N. Witty

Peter N. Witty

Secretary

Phoenix, Arizona

April 3, 2018

|

QUESTIONS AND ANSWERS |

|

|

PROPOSAL 1: ELECTION OF DIRECTORS |

|

|

CORPORATE GOVERNANCE |

|

|

PROPOSAL 2: RATIFICATION OF APPOINTMENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM |

|

|

EXECUTIVE COMPENSATION |

|

|

PROPOSAL 3: ADVISORY VOTE TO APPROVE EXECUTIVE COMPENSATION FOR 2017 |

|

|

DIRECTOR COMPENSATION |

|

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT |

|

|

SECTION 16(A) BENEFICIAL OWNERSHIP REPORTING COMPLIANCE |

|

|

EQUITY COMPENSATION PLAN INFORMATION |

|

|

REPORT OF THE AUDIT COMMITTEE |

|

|

CERTAIN RELATIONSHIPS AND RELATED PERSON TRANSACTIONS |

|

|

STOCKHOLDER PROPOSALS FOR THE 2019 ANNUAL MEETING OF STOCKHOLDERS |

|

|

HOUSEHOLDING OF PROXY MATERIALS |

|

|

OTHER MATTERS THAT MAY COME BEFORE THE ANNUAL MEETING |

|

|

ANNEX A: USE OF NON-GAAP FINANCIAL METRICS |

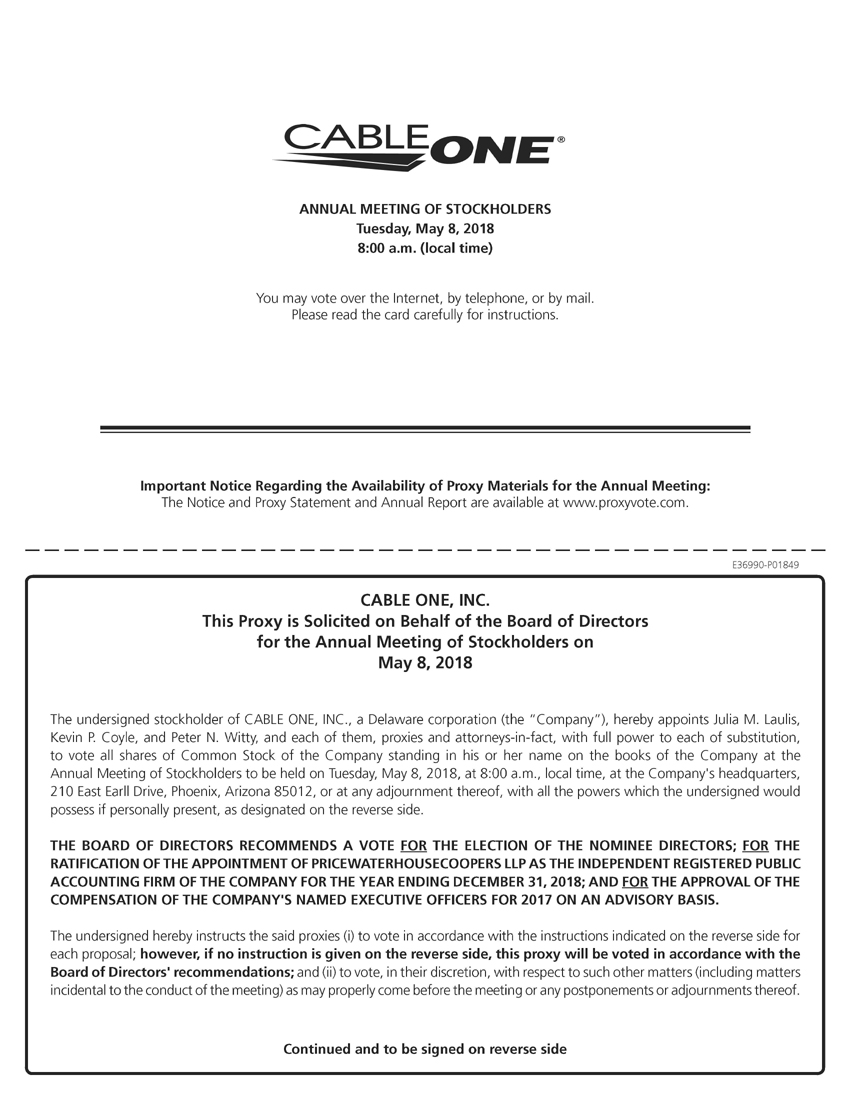

CABLE ONE, INC.

210 E. Earll Dr.

Phoenix, Arizona 85012

PROXY STATEMENT

FOR THE 2018 ANNUAL MEETING OF STOCKHOLDERS

May 8, 2018

This Proxy Statement contains information relating to the 2018 Annual Meeting of Stockholders (the “Annual Meeting”) of Cable One, Inc. (the “Company, “we,” “us,” “our,” or “Cable One”) to be held at the Company’s headquarters, 210 East Earll Drive, Phoenix, Arizona, 85012, on Tuesday, May 8, 2018, at 8:00 a.m., local time, or any adjournments thereof, for the purposes set forth in the accompanying Notice of Annual Meeting of Stockholders. The Board of Directors (the “Board”) of the Company is making this proxy solicitation.

Important Notice Regarding the Availability of Proxy Materials for the Annual Meeting of Stockholders

to Be Held on May 8, 2018

Our Proxy Statement and Annual Report to Stockholders are available at

www.proxyvote.com

These proxy solicitation materials, including this Proxy Statement and the accompanying proxy card or voting instruction form, were first distributed and made available on or about April 3, 2018 to all stockholders entitled to vote at the Annual Meeting.

|

Q: |

What am I voting on? |

|

A: |

There are three proposals scheduled to be voted on at the Annual Meeting: |

|

■ |

The election of three Class III directors to hold office until the 2021 annual meeting of stockholders and until their respective successors are elected and qualified or as otherwise provided in our Amended and Restated By-laws (“By-laws”); |

|

■ |

The ratification of the Audit Committee’s appointment of PricewaterhouseCoopers LLP as the independent registered public accounting firm of our Company for the year ending December 31, 2018; and |

|

■ |

The approval of the compensation of our named executive officers for 2017 on an advisory basis (also referred to as the “say-on-pay” vote). |

In the event that any nominee for election withdraws or for any reason is not able to serve as a director, Julia M. Laulis, Kevin P. Coyle and Peter N. Witty, acting as your proxies, may vote for such other person as the Board may nominate.

|

Q: |

What are the voting recommendations of the Board? |

|

A: |

The Board unanimously recommends you vote as follows: |

|

|

|

Board Vote Recommendation |

|

|

Page Reference for Additional Detail |

|

|

Election of Directors |

|

“FOR” each nominated director |

|

|

5 |

|

|

Ratification of PricewaterhouseCoopers LLP as our independent registered public accounting firm for 2018 |

|

“FOR” |

|

|

16 |

|

|

Advisory Vote on the Approval of Executive Compensation for 2017 |

|

“FOR” |

|

|

44 |

|

The Board knows of no reason that would cause any director nominee to be unable to act or to refuse to accept his or her nomination or election.

|

Q: |

Will any other matters be voted on? |

|

A: |

We are not aware of any matters to be voted on other than those referred to in this Proxy Statement. If any other matter is properly brought before the Annual Meeting, Julia M. Laulis, Kevin P. Coyle and Peter N. Witty, acting as your proxies, will vote for you at their discretion. |

|

Q: |

How do I vote? |

|

A: |

If you are a stockholder of record (that is, if your shares are registered in your name and not in “street name”), there are four ways to vote: |

|

■ |

Over the internet at www.proxyvote.com or scan the QR code on your proxy card with your mobile device. We encourage you to vote this way; |

|

■ |

By toll-free telephone at 1-800-690-6903; |

|

■ |

By completing and mailing your proxy card; or |

|

■ |

By attending the Annual Meeting and voting in person. |

If you hold shares in “street name” (that is, your shares are held in a brokerage account by a broker, bank or other nominee, also known as “beneficial owners”), you should follow the voting instructions provided by your broker, bank or other nominee.

If you wish to vote over the internet or by telephone, your vote must be received by 11:59 p.m., Eastern Time, on the day before the Annual Meeting. After that time, internet and telephone voting will not be permitted, and a stockholder of record wishing to vote who has not previously submitted a signed proxy card must vote in person at the Annual Meeting. Stockholders of record will be on a list held by the inspector of elections. Street name stockholders must obtain a proxy executed in their favor from the institution that holds their shares, whether it is their brokerage firm, bank or other nominee, and present it to the inspector of elections in order to vote at the Annual Meeting. Voting in person by a stockholder at the Annual Meeting will replace any previous votes submitted by proxy.

Your shares will be voted as you indicate. If you do not indicate your voting preferences, Julia M. Laulis, Kevin P. Coyle and Peter N. Witty, acting as your proxies, will vote your shares in accordance with the Board’s recommendations specified above under “What are the voting recommendations of the Board?”

|

Q: |

Who can vote? |

|

A: |

You can vote if you were a stockholder as of the close of business on March 16, 2018 (the “Record Date”). Each of your shares—whether held (i) directly in your name as stockholder of record or (ii) in street name—entitles you to one vote with respect to each proposal to be voted on at the Annual Meeting. However, street name stockholders generally cannot vote their shares directly and instead must instruct the broker, bank or nominee how to vote their shares. |

|

Q: |

Can I change my vote? |

|

A: |

Yes. If you are a stockholder of record, you can change your vote or revoke your proxy at any time before the Annual Meeting: |

|

■ |

By entering a new vote over the internet or by telephone by 11:59 p.m., Eastern Time, on the day before the Annual Meeting; |

|

■ |

By returning a properly signed proxy card with a later date that is received at or prior to the Annual Meeting; or |

|

■ |

By voting in person at the Annual Meeting. |

If you hold shares in street name, you may submit new voting instructions by contacting your bank, broker or other nominee. You may also change your vote or revoke your voting instructions in person at the Annual Meeting if you obtain a signed proxy from the record holder (bank, broker or other nominee) giving you the right to vote the shares. Only the latest validly executed proxy that you submit will be counted.

|

Q: |

What vote is required to approve a proposal? |

|

A: |

Each proposal requires the affirmative vote of majority of the votes cast at the Annual Meeting in order to be approved. “Abstentions” and “broker non-votes” will not be counted as votes cast with respect to that proposal, although they will have the practical effect of reducing the number of affirmative votes required to achieve a majority by reducing the total number of shares from which the majority is calculated. |

Regarding Proposal 1 (election of the Company’s directors), in accordance with our By-laws, any incumbent director who fails to receive a majority of the votes cast must submit an offer to resign from the Board no later than two weeks after the Company certifies the voting results. In that case, the remaining members of the Board would consider the resignation offer and may either (i) accept the offer or (ii) reject the offer and seek to address the underlying cause(s) of the majority-withheld vote. The Board must decide whether to accept or reject the resignation offer within 90 days following the certification of the stockholder vote, and, once the Board makes its decision, the Company must promptly make a public announcement of the Board’s decision (including a statement regarding the reasons for its decision in the event the Board rejects the offer of resignation).

|

Q: |

Who will count the vote? |

|

A: |

A representative of Broadridge Financial Solutions, Inc. will tabulate the votes and act as inspector of elections. |

|

Q: |

Who can attend the Annual Meeting? |

|

A: |

All stockholders of record as of the close of business on March 16, 2018 can attend. Street name stockholders must show proof of ownership in order to be admitted to the Annual Meeting. |

|

Q: |

What do I need to do to attend the Annual Meeting? |

|

A: |

In order to be admitted to the Annual Meeting, you must present proof of ownership of our common stock as of the Record Date. This can be a brokerage statement or letter from a broker, bank or other nominee indicating your ownership as of the Record Date, a proxy card, or a legal proxy or voting instruction card provided by your broker, bank or nominee. Any holder of a proxy from a stockholder must present the proxy card, properly executed, and a copy of the proof of ownership. Stockholders and proxyholders may also be asked to present a form of photo identification such as a driver’s license or passport. |

In addition, please follow these instructions:

|

■ |

If you vote by using the enclosed proxy card, check the appropriate box on the card to indicate that you plan to attend the Annual Meeting. |

|

■ |

If you vote over the internet or by telephone, follow the instructions provided to indicate that you plan to attend the Annual Meeting. |

Seating at the Annual Meeting will be on a first-come, first-served basis upon arrival at the Annual Meeting.

Backpacks, cameras, cell phones with cameras, recording equipment and other electronic recording devices will not be permitted inside the Annual Meeting. Failure to follow the Annual Meeting rules or permit inspection will be grounds for exclusion from the Annual Meeting.

|

Q: |

Can I bring a guest? |

|

A: |

No. The Annual Meeting is for stockholders only. |

|

Q: |

What is the quorum requirement of the Annual Meeting? |

|

A: |

A majority of the votes entitled to be cast by the outstanding shares of common stock entitled to vote generally on the business properly brought before the Annual Meeting must be present in person or by proxy to constitute a quorum for the Annual Meeting. If you vote, your shares will be part of the quorum. Abstentions and “broker non-votes” will be counted for purposes of determining whether a quorum is present at the Annual Meeting. As of the Record Date, there were 5,733,130 shares of our common stock outstanding and entitled to vote.

If you hold your shares in street name and do not provide voting instructions to your broker, New York Stock Exchange (“NYSE”) rules grant your broker discretionary authority to vote your shares on “routine matters” at the Annual Meeting, including for the ratification of PricewaterhouseCoopers LLP as our independent registered public accounting firm for 2018 in Proposal 2. However, the proposals regarding the election of directors and the say-on-pay vote are not considered “routine matters.” As a result, if you do not provide voting instructions to your broker, your shares will be voted on Proposal 2 but will not be voted on Proposals 1 and 3 (resulting in a “broker non-vote” with respect to each of Proposals 1 and 3). Although “broker non-votes” will be counted as present for purposes of determining a quorum, we urge you to promptly provide voting instructions to your broker or other nominee so that your shares are voted on all proposals. |

|

Q: |

Who is soliciting proxies? |

|

A: |

Solicitation of proxies is being made by our management through the mail, in person, over the internet or by telephone, without any additional compensation being paid to such members of management. The cost of such solicitation will be borne by us. In addition, we have requested brokers and other custodians, nominees and fiduciaries to forward proxy cards and proxy soliciting material to stockholders, and we will pay their fees and reimburse them for their expenses in so doing. |

|

Q: |

What other information about Cable One is available? |

|

A: |

The following information is available: |

|

■ |

We maintain on our website, http://ir.cableone.net, copies of our Annual Report on Form 10-K; Annual Report to Stockholders; Corporate Governance Guidelines; Statement of Ethical Principles; Code of Business Conduct; charters of the Audit, Compensation, Executive and Nominating and Governance Committees; Policy Statement Regarding Director Nominations and Stockholder Communications (the “Policy Statement”); and other information about the Company. |

|

■ |

In addition, printed copies of these documents will be furnished without charge (except exhibits) to any stockholder upon written request addressed to our Secretary at 210 E. Earll Drive, Phoenix, Arizona 85012. |

|

■ |

Amendments to, or waivers granted to our directors and executive officers under, the Code of Business Conduct, if any, will be posted on our website. |

|

Q: |

Can I receive materials relating to the Annual Meeting electronically? |

|

A: |

To assist us in reducing costs related to the Annual Meeting, stockholders who vote over the internet may consent to electronic delivery of mailings related to future annual stockholder meetings. We also make our Proxy Statements and Annual Reports available online and may eliminate mailing hard copies of these documents to those stockholders who consent in advance to electronic distribution. If you are voting over the internet, you may consent online at www.proxyvote.com when you vote. If you hold shares in street name, please also refer to information provided by the broker, bank or other nominee for instructions on how to consent to electronic distribution. |

PROPOSAL 1: ELECTION OF DIRECTORS

The Board is divided into three classes, designated Class I, Class II and Class III. Directors are elected by class for three-year terms, which continue until the third annual meeting of stockholders following the director’s election and until the director’s successor is elected and qualified. Our Amended and Restated Certificate of Incorporation (“Charter”) and By-laws provide that the number of the directors of the Company will be fixed from time to time by the Board.

There are three Class III directors whose term of office expires in 2018. The nominees for election as Class III directors, to serve for a three-year term until the 2021 annual meeting of stockholders and until his or her successor is elected and qualified, are Thomas S. Gayner, Deborah J. Kissire and Thomas O. Might. All nominees are currently directors of the Company. Messrs. Gayner and Might were previously elected by the then-sole stockholder of the Company, Graham Holdings Company (“GHC”), prior to the effective time of our spin-off from GHC (the “spin-off”). Ms. Kissire was recommended by representatives of GHC and elected by the Board in July 2015.

The candidates for election have been nominated by the Board based on the recommendation of the Nominating and Governance Committee. In choosing directors and nominees, the Company seeks individuals of the highest personal and professional ethics, integrity, business acumen and commitment to representing the long-term interests of our stockholders. In respect of its composition, the Board considers the diversity, skills and experience of prospective nominees in the context of the needs of the Board and seeks directors who are “independent” under applicable law and listing standards. Although our Corporate Governance Guidelines and the Policy Statement do not prescribe specific standards regarding Board diversity, the Board considers, as a matter of practice, the diversity of prospective nominees (including incumbent directors), both culturally and in terms of the variety of viewpoints on the Board, which may be enhanced by a mix of different professional and personal backgrounds and experiences.

Directors are elected by the affirmative vote of majority of the votes cast at the Annual Meeting. The Board knows of no reason that would cause any nominee to be unable to act or to refuse to accept his or her nomination or election. In the event that any nominee withdraws or for any reason is not able to serve as a director, the individuals acting as your proxies may vote for such other person as the Board may nominate.

The following table presents certain information, as of March 16, 2018, concerning each nominee for election as a director and each director whose term of office will continue after the Annual Meeting.

|

Name |

|

Age |

|

Director Since |

|

Position |

|

Expiration of Term as Director |

|

Ms. Julia M. Laulis |

|

55 |

|

2017 |

|

Chair of the Board, President and Chief Executive Officer |

|

2019 |

|

Mr. Brad D. Brian* |

|

65 |

|

2015 |

|

Director |

|

2019 |

|

Mr. Thomas S. Gayner* |

|

56 |

|

2015 |

|

Lead Independent Director |

|

2018 |

|

Ms. Deborah J. Kissire* |

|

60 |

|

2015 |

|

Director |

|

2018 |

|

Mr. Thomas O. Might |

|

66 |

|

1995 |

|

Director |

|

2018 |

|

Mr. Alan G. Spoon* |

|

66 |

|

2015 |

|

Director |

|

2020 |

|

Mr. Wallace R. Weitz* |

|

68 |

|

2015 |

|

Director |

|

2020 |

|

Ms. Katharine B. Weymouth* |

|

51 |

|

2015 |

|

Director |

|

2019 |

* Independent Director

In addition to the information presented below regarding each nominee’s specific qualifications, skills, attributes and experience that led the Board to conclude that he or she should serve as a director, the Board believes that each nominee has demonstrated established records of accomplishment in areas relevant to our strategy and operations and share characteristics identified in our Corporate Governance Guidelines, Statement of Ethical Principles and the Policy Statement as essential to a well-functioning deliberative body, including honesty, integrity, judgment, acumen, ethics, financial literacy, independence, competence, diligence and commitment to the interests of all stockholders to build long-term stockholder value.

All of the directors and nominees have held senior positions as leaders of complex organizations and gained expertise in core management skills, such as strategy and business development, innovation, line operations, brand management, finance, compensation and leadership development, compliance and risk management. They have significant experience in corporate governance and oversight through their positions as senior executives and as directors of public companies and other institutions. These skills and experience are pertinent to our current and evolving business strategies, as well as to the Board’s oversight role, and enable the directors to provide diverse perspectives about the complex issues facing the Company.

The following matrix and biographies highlight specific qualifications, skills, attributes and experience of each of our directors who is a nominee for election as a director or whose term of office will continue after the Annual Meeting. The matrix is a summary only; therefore, it does not include all of the qualifications, skills, attributes and experience that each director offers, and the fact that a particular qualification, skill, attribute or experience is not listed does not mean that a director does not possess it.

|

|

|

Cable / Communications / Media Industry Experience |

|

Leadership Experience |

|

Governance / Board Experience |

|

Financial / Accounting Expertise |

|

Legal Expertise |

|

Diversity |

|

Brad D. Brian |

|

|

|

✓ |

|

|

|

|

|

✓ |

|

|

|

Thomas S. Gayner |

|

✓ |

|

✓ |

|

✓ |

|

✓ |

|

|

|

|

|

Deborah J. Kissire |

|

|

|

✓ |

|

✓ |

|

✓ |

|

|

|

✓ |

| Julia M. Laulis | ✓ | ✓ | ✓ | |||||||||

|

Thomas O. Might |

|

✓ |

|

✓ |

|

✓ |

|

|

|

|

|

|

|

Alan G. Spoon |

|

✓ |

|

✓ |

|

✓ |

|

✓ |

|

|

|

|

|

Wallace R. Weitz |

|

|

|

✓ |

|

✓ |

|

✓ |

|

|

|

|

|

Katharine B. Weymouth |

|

✓ |

|

✓ |

|

✓ |

|

|

|

✓ |

|

✓ |

Nominees for Election for a Term Expiring at the 2021 Annual Meeting of Stockholders

Thomas S. Gayner

Mr. Gayner has served as Co-Chief Executive Officer of Markel Corporation, a publicly traded financial holding company headquartered in Glen Allen, Virginia, since January 2016 and as a director since August 2016. He also served as President and Chief Investment Officer of Markel Corporation from May 2010 until December 2015 and as a director of Markel Corporation from 1998 to 2003. Since 1990, he has served as President of Markel-Gayner Asset Management Corporation. Previously, he was a certified public accountant at PricewaterhouseCoopers LLP and a Vice President of Davenport & Company LLC in Virginia. Mr. Gayner serves on the boards of GHC, Colfax Corporation and The Davis Series Mutual Funds. He also serves on the board of the Community Foundation of Richmond, a non-profit entity.

Mr. Gayner brings to the Board the leadership, management oversight and financial skills gained in his role as a senior manager and director of Markel Corporation as well as other public company boards.

In considering the nomination of Mr. Gayner to serve an additional term as a director, the other members of the Nominating and Governance Committee (on which Mr. Gayner serves as Chair) and the Board examined and purposefully evaluated Mr. Gayner’s roles with and obligations to entities other than the Company, including his position as an executive officer of Markel Corporation and his services as a board member of other public companies, including our former parent, GHC. His service as a director of GHC prior to the spin-off aligns with our long-term focus and offers stability as we have undertaken a strategic shift to become a residential high-speed data and business services-centric company. The Nominating and Governance Committee and the Board also took note of Mr. Gayner’s perfect attendance record in 2017 at meetings of the Board and of the Committees on which he served, as well as his exceptional attendance record in his nearly three years of service on our Board (Mr. Gayner has attended all but one of his Board and Committee meetings during that time). Furthermore, Mr. Gayner has vigorously discharged his leadership roles as our Lead Independent Director and as Chair of the Executive Committee and the Nominating and Governance Committee, both in preparedness and active participation, and he continues to be a valuable member of the Board with sufficient capacity to devote the necessary time and attention to matters concerning the Board. After a thorough evaluation of all of these considerations, as well as the leadership, management oversight and financial skills brought to the Board by Mr. Gayner, the Nominating and Corporate Governance Committee unanimously recommended and the Board unanimously re-nominated Mr. Gayner for election to the Board.

Deborah J. Kissire

Ms. Kissire retired as a partner of Ernst & Young LLP, an independent registered public accounting firm, in July 2015 after a 36-year career. At the time of her retirement, Ms. Kissire served as Ernst & Young’s Vice Chair and East Central Managing Partner as well as a member of the Americas Executive Board. Ms. Kissire serves on the boards of Axalta Coating Systems Ltd. and Omnicom Group Inc., and she has served on the boards of Goodwill Industries of Greater Washington and Junior Achievement USA.

Ms. Kissire brings to the Board her significant experience in public company financial reporting, accounting and financial control matters.

Thomas O. Might

Mr. Might retired as Executive Chairman of Cable One in December 2017. He has been a member of the Board of Cable One since 1995. Prior to his retirement from Cable One, Mr. Might served as Executive Chairman in 2017, as Chairman of the Board from 2015 to 2017, as Chief Executive Officer from 1994 to 2016 and as President from 1994 to 2014.

Mr. Might joined The Washington Post Company in 1978 as assistant to publisher Donald E. Graham after serving a summer internship at the newspaper in 1977. He was promoted to Vice President-Production in 1982 and served in that position until 1987, when he became Vice President-Production and Marketing. In 1991, Mr. Might was named Vice President-Advertising Sales.

In 1993, Mr. Might was promoted to President and Chief Operating Officer of Cable One. He became President and Chief Executive Officer of Cable One in 1994 and was elected to the Board in 1995.

Mr. Might was a Combat Engineer Officer in the U.S. Army from 1972 to 1976.

Mr. Might brings to the Board leadership and management oversight skills as well as intimate knowledge and perspective about the strategic and operational opportunities and challenges, economic and industry trends, and competitive and financial positioning of the Company based on his various executive roles at Cable One.

THE BOARD UNANIMOUSLY RECOMMENDS A VOTE “FOR” THE ELECTION OF EACH OF THE NOMINATED DIRECTORS.

Directors Continuing in Office

Brad D. Brian

Mr. Brian is a Co-Managing Partner at the California law firm Munger, Tolles & Olson LLP, having been with the firm for over 36 years. A complex civil and criminal litigator, Mr. Brian is a Fellow in the American College of Trial Lawyers and the International Academy of Trial Lawyers. Mr. Brian has represented numerous Fortune 500 corporations in lawsuits and government investigations. This work has included trials, regulatory investigations and internal corporate investigations. He also has defended companies against more than 40 lawsuits filed under the qui tam provisions of the False Claims Act. Mr. Brian is the co-editor of Internal Corporate Investigations (ABA 4th Ed. 2017). Mr. Brian was named a “Litigator of the Year” by The American Lawyer in 2016.

Mr. Brian brings to the Board his experience as a litigator and corporate advisor and his understanding of legal matters that may arise at Cable One.

Julia M. Laulis

Ms. Laulis has been Chair of the Board since January 2018, Chief Executive Officer and a member of the Board since January 2017 and President of Cable One since January 2015.

Ms. Laulis joined Cable One in 1999 as Director of Marketing – Northwest Division. In 2001, she was named Vice President of Operations for the Southwest Division. In 2004, she accepted the additional responsibility for starting up Cable One’s Phoenix Customer Care Center. In 2008, she was named Chief Operations Officer, and in 2012, she was named Chief Operating Officer of Cable One. In January 2015, she was promoted to President and Chief Operating Officer of Cable One.

Prior to joining Cable One, Ms. Laulis served in various senior marketing positions with Jones Communications. Ms. Laulis began her 30-plus-year career in the cable industry with Hauser Communications.

Ms. Laulis serves on the boards of CableLabs and C-SPAN.

Ms. Laulis brings to the Board her significant operational and leadership experience as well as intimate knowledge and perspective about the strategic and operational opportunities and challenges, economic and industry trends, and competitive and financial positioning of the Company based on her various executive roles at Cable One.

Alan G. Spoon

Mr. Spoon is currently Partner Emeritus at Polaris Partners, a private investment firm that provides venture capital to development-stage companies. He has been with Polaris Partners since May 2000, previously serving as Managing General Partner and General Partner. Mr. Spoon was Chief Operating Officer and a director of The Washington Post Company from March 1991 through May 2000 and served as President of The Washington Post Company from September 1993 through May 2000. Prior to that, he held a wide variety of positions at The Washington Post Company, including President of Newsweek from September 1989 to May 1991. Mr. Spoon began his career at, and later became a partner of, The Boston Consulting Group.

Mr. Spoon serves on the boards of Danaher Corporation, Fortive Corporation, IAC/InterActiveCorp and Match Group, Inc. and previously served as a director of Cable One from 1991 to 2000. Additionally, he has served on the boards of Getty Images, TechTarget, Inc., Human Genome Sciences, Ticketmaster and American Management Systems. Previously, Mr. Spoon was a member of the Board of Regents at the Smithsonian Institution (formerly Vice Chairman). He is a member of the MIT Corporation (member of the Executive Committee), where he also serves on the board of edX (an online education platform).

Mr. Spoon’s public company leadership experience gives him insight into business strategy, leadership and executive compensation, and his public company and private equity experience give him insight into technology trends, acquisition strategy and financing. With more than 18 years of experience with The Washington Post Company, including nine years as a director of Cable One, he also has knowledge of Cable One’s business.

Wallace R. Weitz

Mr. Weitz founded the investment management firm Weitz Investment Management, Inc. in 1983 as Wallace R. Weitz & Company and has since served in various roles at Weitz Investment Management, including Chief Investment Officer, President and Portfolio Manager. Mr. Weitz manages the Partners III Opportunity Fund and co-manages the Partners Value Fund and Hickory Fund, each of which is managed by Weitz Investment Management. Mr. Weitz has served as a Trustee of the Weitz Funds since 1986. Mr. Weitz began his career in New York as a securities analyst before joining Chiles, Heider & Co. in Omaha, Nebraska in 1973. There, he spent 10 years as an analyst and portfolio manager. Mr. Weitz is on the Board of Trustees for Carleton College and serves on various other non-profit boards.

Mr. Weitz brings to the Board his substantial finance experience as an investor in public companies.

Katharine B. Weymouth

Ms. Weymouth was the Chief Executive Officer of Washington Post Media and Publisher of The Washington Post newspaper from February 2008 until October 2014. She joined The Washington Post Company in 1996 as Assistant General Counsel of The Washington Post newspaper and held various positions within that organization over the course of 18 years. Ms. Weymouth held several positions within The Washington Post’s advertising department, including Director of the department’s jobs unit, Director of Advertising Sales and Vice President of Advertising. She also served as Associate Counsel of Washingtonpost.Newsweek Interactive, then the online publishing subsidiary of The Washington Post Company. Ms. Weymouth has been a director of GHC, from which Cable One was spun-off in July 2015, since September 2010. She serves as a Trustee of the Philip L. Graham Fund and as a director of The Economic Club of Washington, D.C. and the Community Foundation for the Greater Capital Region.

Ms. Weymouth brings to the Board public company leadership, management oversight and operational expertise gained through her various senior roles with and directorship of GHC.

There are no family relationships among any of our directors and executive officers.

Board Committees and Meeting Attendance

The standing committees of the Board include the Audit Committee, Compensation Committee, Executive Committee, and Nominating and Governance Committee. As discussed in more detail below, each of the Audit, Compensation and Nominating and Governance Committees is comprised entirely of independent directors, consistent with the definition of “independent” under NYSE listing standards applicable to boards of directors generally and board committees in particular.

Each committee of the Board operates under a written charter that is maintained on our website, http://ir.cableone.net/govdocs, and has the authority to hire at the expense of the Company independent legal, accounting, financial or other advisors as it deems necessary or appropriate.

The following table summarizes the current membership of the Board and each of its committees, as well as the number of times the Board and each committee met during 2017.

|

Director |

|

Board |

|

Audit Committee |

|

Compensation Committee |

|

Executive Committee |

|

Nominating and Governance Committee |

|

Brad D. Brian* |

|

✓ |

|

|

|

✓ |

|

|

|

✓ |

|

Thomas S. Gayner* |

|

Lead Independent Director |

|

|

|

|

|

Chair |

|

Chair |

|

Deborah J. Kissire* |

|

✓ |

|

Chair |

|

|

|

|

|

|

|

Julia M. Laulis |

|

Chair |

|

|

|

|

|

✓ |

|

|

|

Thomas O. Might |

|

✓ |

|

|

|

|

|

|

|

|

|

Alan G. Spoon* |

|

✓ |

|

✓ |

|

|

✓ |

|

|

|

|

Wallace R. Weitz* |

|

✓ |

|

|

|

Chair |

|

|

|

✓ |

|

Katharine B. Weymouth* |

|

✓ |

|

✓ |

|

✓ |

|

|

|

|

|

Number of Meetings |

|

5 |

|

6 |

|

6 |

|

4 |

|

4 |

* Independent Director

Each director attended at least 75% of the meetings of the Board and the committees of the Board on which the director served in 2017.

Audit Committee

The functions of the Audit Committee include, among other duties, overseeing:

|

■ |

management’s conduct of our financial reporting process (including the development and maintenance of systems of internal accounting and financial controls); |

|

■ |

the integrity of our financial statements; |

|

■ |

our compliance with legal and regulatory requirements; |

|

■ |

the qualifications and independence of our outside auditor; |

|

■ |

the performance of our internal audit function; |

|

■ |

the outside auditor’s annual audit of our financial statements; and |

|

■ |

the preparation of certain reports required by the rules and regulations of the Securities and Exchange Commission (the “SEC”). |

The Board has determined that all members of the Audit Committee are non-employee, “financially literate,” “independent” directors within the meaning of the listing standards of the NYSE. None of the members of the Audit Committee has accepted, other than in such person’s capacity as a committee or Board member, any consulting, advisory or other compensatory fee from the Company or its affiliates.

The Board has determined that each of Ms. Kissire and Mr. Spoon has the requisite background and experience to be (and is) designated an “audit committee financial expert” within the meaning of Item 407(d)(5)(ii) of Regulation S-K due to his or her extensive experience, as discussed under “Proposal 1: Election of Directors.” In addition, the Board has determined that all of the members of the Audit Committee are well grounded in financial matters and are familiar with U.S. generally accepted accounting principles (“GAAP”). All of the members of the Audit Committee have a general understanding of internal controls and procedures for financial reporting, as well as an understanding of audit committee functions. To the extent that matters come before the Audit Committee that involve accounting issues, the members of the Audit Committee consult with and rely on management, in addition to consulting with external experts, such as the Company’s independent registered public accounting firm, PricewaterhouseCoopers LLP. In addition, the Audit Committee has authority to obtain advice from internal or external legal or other advisors.

Compensation Committee

The functions of the Compensation Committee include, among other duties:

|

■ |

determining and approving the compensation of our Chief Executive Officer; |

|

■ |

reviewing and approving the compensation of other members of our senior management; |

|

■ |

overseeing the administration and determination of awards under our compensation plans; and |

|

■ |

preparing any report on executive compensation required by the rules and regulations of the SEC. |

All members of the Compensation Committee are non-employee directors and have been determined to be “independent” within the meaning of the listing standards of the NYSE applicable to service on compensation committees.

Executive Committee

The functions of the Executive Committee include, among other duties:

|

■ |

reviewing and providing guidance to the Board and to senior management of the Company regarding the Company’s strategy, operating plans and operating performance; and |

|

■ |

performing such other duties or responsibilities as may be delegated to the Committee from time to time by the Board. |

Nominating and Governance Committee

The functions of the Nominating and Governance Committee include, among other duties:

|

■ |

overseeing our corporate governance practices; |

|

■ |

reviewing and recommending to our Board amendments to our By-laws, Charter, committee charters and other governance policies; |

|

■ |

reviewing and making recommendations to our Board regarding the structure of our various board committees; |

|

■ |

identifying, reviewing and recommending to our Board individuals for election to the Board; |

|

■ |

adopting and reviewing policies regarding the consideration of candidates for our Board proposed by stockholders and other criteria for membership on our Board; |

|

■ |

overseeing the Chief Executive Officer succession planning process, including an emergency succession plan; |

|

■ |

reviewing the leadership structure for our Board; |

|

■ |

overseeing our Board’s annual self-evaluation; and |

|

■ |

overseeing and monitoring general governance matters, including communications with stockholders and regulatory developments relating to corporate governance. |

All members of the Nominating and Governance Committee are non-employee directors and have been determined to be “independent” within the meaning of the listing standards of the NYSE.

Corporate Governance Guidelines and Codes of Conduct

In order to help assure the highest levels of business ethics at Cable One, our Board has adopted the following Corporate Governance Guidelines and codes of conduct, which are maintained on our website, http://ir.cableone.net/govdocs.

Corporate Governance Guidelines

Our Corporate Governance Guidelines provide a framework for the governance of the Company. Among other things, our Corporate Governance Guidelines address director qualifications, Board operations, director compensation, management review and succession and director orientation and continuing education. The Corporate Governance Guidelines also provide for annual self-evaluations by the Board and its committees.

The Board has not established limits on the number of terms a director may serve prior to his or her 75th birthday; however, no director may be nominated to a new term if he or she would be age 75 or older at the time of the election.

Code of Business Conduct

Our Code of Business Conduct applies to our employees, including any employee directors. The Code of Business Conduct contains policies pertaining to, among other things, employee conduct in the workplace; electronic communications and information security; accuracy of books, records and financial statements; securities trading; confidentiality; conflicts of interest; fairness in business practices; anti-bribery and anti-corruption laws; antitrust laws; and political activities and solicitations.

Statement of Ethical Principles

Our Statement of Ethical Principles applies to our directors, officers and employees and is designed to deter wrongdoing and to promote, among other things:

|

■ |

honest and ethical conduct, including the ethical handling of actual or apparent conflicts of interest between personal and professional relationships; |

|

■ |

the protection of the confidentiality of our non-public information; |

|

■ |

the responsible use of and control over our assets and resources; |

|

■ |

full, fair, accurate, timely and understandable disclosure in reports and documents that we file with the SEC and other regulators and in our other public communications; |

|

■ |

compliance with applicable laws, rules and regulations; and |

|

■ |

accountability for adherence to the Statement of Ethical Principles and prompt internal reporting of any possible violation of the Statement of Ethical Principles. |

Director Nomination Process

Under our By-laws, stockholders of record are able to nominate persons for election to our Board only by providing proper notice to our Secretary. Proper notice must be timely, generally between 90 and 120 days prior to the relevant meeting (or, in the case of annual meetings, prior to the first anniversary of the prior year’s annual meeting), and must include, among other information, the name and address of the stockholder giving the notice, a representation that such stockholder is a holder of record of our common stock as of the date of the notice, certain information regarding such stockholder’s beneficial ownership of our securities and any derivative instruments based on or linked to the value of or return on our securities as of the date of the notice, certain information relating to each person whom such stockholder proposes to nominate for election as a director, a brief description of any other business such stockholder proposes to bring before the meeting and the reason for conducting such business and a representation as to whether such stockholder intends to solicit proxies.

The Nominating and Governance Committee will consider director candidates recommended by stockholders. Our By-laws provide that any stockholder of record entitled to vote for the election of directors at the applicable meeting of stockholders may nominate persons for election to our Board, if such stockholder complies with the applicable notice procedures.

Our Corporate Governance Guidelines and the Policy Statement contain information concerning the responsibilities of the Nominating and Governance Committee with respect to identifying and evaluating future director candidates. The Policy Statement sets forth our Nominating and Governance Committee’s general policy regarding the consideration of candidates proposed by stockholders; a description of the minimum criteria used by the Nominating and Governance Committee in evaluating candidates for the Board; a description of the Nominating and Governance Committee’s process for identifying and evaluating director nominees (including candidates recommended by stockholders); and the general process for communications between stockholders and the Board.

Majority Voting for Directors

Our By-laws provide for majority voting in uncontested director elections, and any incumbent director who fails to receive a majority of the votes cast must submit an offer to resign from the Board no later than two weeks after the Company certifies the voting results. In that case, the remaining members of the Board would consider the resignation offer and may either (i) accept the offer or (ii) reject the offer and seek to address the underlying cause(s) of the majority-withheld vote. The Board must decide whether to accept or reject the resignation offer within 90 days following the certification of the stockholder vote, and, once the Board makes its decision, the Company must promptly make a public announcement of the Board’s decision (including a statement regarding the reasons for its decision in the event the Board rejects the offer of resignation).

Director Independence

As set forth in our Corporate Governance Guidelines, the majority of directors must be “independent” according to the criteria for independence established by the NYSE. Our Corporate Governance Guidelines also require that all the members of each of the standing committees (other than the Executive Committee) must be independent and may not directly or indirectly accept any consulting, advisory or other compensatory fee (other than pension or other forms of deferred compensation for prior service which is not contingent in any way on continued service) from the Company or its subsidiaries and none of the members of the standing committees may have a material relationship with the Company. In order to determine that a director is independent, the Board must make an affirmative determination that the director satisfies applicable regulatory and NYSE listing requirements to be an independent director of the Company and that the director is free of any other relationship that would interfere with the exercise of independent judgment by such director. The Board has determined that the following directors are independent: Naomi M. Bergman (who did not stand for re-election at the conclusion of her term of office in 2017), Brad D. Brian, Thomas S. Gayner, Deborah J. Kissire, Alan G. Spoon, Wallace R. Weitz and Katharine B. Weymouth.

Executive Sessions of the Non-Management Directors

The listing standards of the NYSE call for the non-management directors of the Company to meet at regularly scheduled executive sessions without management. Mr. Gayner serves as Lead Independent Director of the Board, and he presides at the executive sessions of the Board. In 2017, the non-management directors regularly met in executive sessions outside the presence of any employee director or management, and the non-management directors expect to meet in executive session in 2018 as appropriate.

Board Leadership Structure

The Board supports flexibility in determining its leadership structure by not requiring the separation of the roles of Chairman of the Board and Chief Executive Officer. The Board believes that the Company and its stockholders are best served by maintaining this flexibility rather than mandating a particular leadership structure.

In 2017, Mr. Might served as Chairman of the Board as well as Executive Chairman of the Company, while Ms. Laulis served as President and Chief Executive Officer. Effective January 1, 2018, Ms. Laulis was appointed Chair of the Board upon Mr. Might’s retirement as an employee of the Company. During 2017, we maintained separate roles between Chairman of the Board and Chief Executive Officer in recognition of the differences between the two responsibilities and because we believed that, at that time and given Ms. Laulis’ recent promotion to the role of Chief Executive Officer, the separation of the roles was in the best interests of the Company.

We currently do not separate the roles of Chair of the Board and Chief Executive Officer. The Board believes that Ms. Laulis’ service as both Chair of the Board and Chief Executive Officer is in the best interests of the Company and that this structure is appropriate because Ms. Laulis possesses in-depth strategic and operational knowledge of the opportunities and challenges facing the Company and has played a critical role in the growth of the Company during her nearly 20-year career at Cable One through her experiences as an employee, executive and director of Cable One. Her dual role promotes decisive leadership, accountability and clarity in the overall direction of the Company’s business strategy as well as effective decision-making and strategic alignment between the Board and the Company’s senior management. The Board also believes that this approach facilitates clear and consistent communication of the Company’s strategy to all stakeholders and that, in consultation with our Lead Independent Director, Ms. Laulis is best positioned to develop agendas that focus on matters that merit Board attention.

To ensure the Board’s independence and proper functioning, the Board also appoints a Lead Independent Director. Mr. Gayner currently serves in this capacity. The Lead Independent Director typically chairs executive sessions of Board meetings and consults with Ms. Laulis and senior management regarding issues to be included in Board meeting agendas. The Lead Independent Director is also expected to collaborate with Ms. Laulis, along with the other members of the Executive Committee, in reviewing key operational and other matters and to act as a liaison between Ms. Laulis and the non-management directors. The role of the Lead Independent Director is able to provide strong leadership of the non-management directors and help the Board provide effective independent oversight of the Chair of the Board and Chief Executive Officer.

Classified Board Structure

We have a classified Board that we believe is important to and congruent with our philosophy of managing for the long term. While we are smaller than the nation’s biggest cable companies, we have a record of consistent, long-term financial and operational success driven by our differentiated operating philosophy. We emphasize focus as opposed to scale, and we have a multi-faceted strategy that builds upon our long track record of focusing on the right markets, the right products and the right customers, as well as controlling our operating and capital costs. Prior to 2012, we were focused on growing revenues through subscriber retention and growth in overall primary service units (“PSUs”). Since 2012, we have adapted our strategy to face the trend, which has affected the entire cable industry, of declining profitability of residential video and declining revenues from residential voice services. Beginning in 2013, we shifted our focus away from maximizing customer PSUs and towards growing and maintaining our higher margin businesses, namely residential data and business services. While this is a departure from more conventional strategies in the cable industry, we believe it is well suited to the markets in which we operate and enables us to take advantage of our strengths as a cable operator.

Because of the long-term nature of our strategy, it can take an extended period of time before financial and operational success fully manifest themselves. We are also a relatively new public company, with all of our directors having served less than three years since the spin-off and only Messrs. Might and Spoon having served as directors for more than three years (counting Mr. Spoon’s service as a director of our Company between 1991 and 2000 when we were a subsidiary of GHC where Mr. Spoon was an officer). We believe that standing for election every three years enables our directors to develop a robust understanding of our business and strategy while maintaining a long-term perspective that will enable us to drive continued growth and success of our business. In addition, as part of our stockholder outreach efforts, a number of our largest stockholders indicated that they have no concerns with our classified Board.

Board’s Role in Risk Oversight

The Board as a whole actively considers strategic decisions proposed by management, including matters affecting the business strategy and competitive and financial positions of the Company, and monitors the Company’s risk profile. Board meetings are focused on strategic matters affecting major areas of the Company’s business, including operational, execution and competitive risks and risk management initiatives. The Board fulfills certain risk oversight functions through its standing committees. For example, the Audit Committee plays a key role in risk oversight, particularly with respect to financial reporting, accounting and compliance matters; the Compensation Committee addresses the risk profile of the Company’s compensation program and arrangements; and the Nominating and Governance Committee oversees corporate governance-related risk associated with our governance practices and profile.

Risk oversight activities are supported by internal reporting structures that aim to surface directly to the Board key matters that can affect the Company’s risk exposures as well as by our leadership structure as described above. The Company has established a Disclosure Controls Committee that reports directly to the Audit Committee on certain matters relating to the Company’s public disclosures. The Board believes that its role in risk oversight does not affect the Board’s leadership structure.

Communicating with Directors

In accordance with the Policy Statement, stockholders and other interested persons seeking to communicate with the Board may submit any communications in writing to the Company’s Secretary, at the address of the Company’s headquarters: 210 E. Earll Drive, Phoenix, Arizona 85012. Any such communication must state the number of shares beneficially owned by the stockholder making the communication. The Secretary will review all incoming stockholder communications, except for solicitations, junk mail and obviously frivolous or inappropriate communications, and forward such communications, as appropriate, to the full Board or to any individual director or directors to whom the communication is directed.

Annual Meeting Attendance

The Board does not have a policy of requiring directors to attend annual meetings of stockholders; however, the Company generally schedules a Board meeting in conjunction with its annual meeting of stockholders and encourages directors and nominees for director to attend each annual meeting of stockholders. All of our current directors attended our 2017 annual meeting of stockholders.

Compensation Committee Interlocks and Insider Participation

Messrs. Brian, Spoon and Weitz and Ms. Weymouth served as members of the Compensation Committee in 2017. None of these individuals has ever been an employee of the Company. During 2017, none of our executive officers served on the board of directors or compensation committee of any other entity for which a member of our Board or Compensation Committee served as an executive officer.

Corporate Governance Policies Related to Compensation and Equity

Please refer to “Compensation Discussion and Analysis—Corporate Governance Policies” beginning on page 29 of this Proxy Statement for discussion of our stock ownership guidelines, and our policies with respect to prohibiting derivative trading, hedging and pledging; clawbacks; and the tax deductibility of compensation.

PROPOSAL 2: RATIFICATION OF APPOINTMENT OF

INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The firm of PricewaterhouseCoopers LLP, an independent registered public accounting firm, has audited the financial statements of our Company for the fiscal year ended December 31, 2017. Our Audit Committee has appointed PricewaterhouseCoopers LLP to serve as our independent registered public accounting firm for the fiscal year ending December 31, 2018 and recommends that stockholders vote in favor of the ratification of such appointment. Although ratification is not required by our By-laws or otherwise, the Board is submitting the selection of PricewaterhouseCoopers LLP to our stockholders for ratification as a matter of good corporate governance. If the appointment is not ratified, the Audit Committee will consider whether it is appropriate to select another independent registered public accounting firm. Even if the appointment is ratified, the Audit Committee, in its discretion, may select a different independent registered public accounting firm at any time during the year if it determines that such a change would be in the best interests of the Company and our stockholders.

We anticipate that representatives of PricewaterhouseCoopers LLP will be present at the Annual Meeting, will have the opportunity to make a statement if they desire to do so with respect to our financial statements for the fiscal year ended December 31, 2017 and the firm’s relationship with the Company and will be available to respond to appropriate questions from stockholders.

Audit Committee Pre-Approval Policies and Procedures

The Audit Committee’s charter provides that the duties and responsibilities of the Audit Committee include the pre-approval of audit and non-audit services performed by the independent registered public accounting firm in order to assure that the provision of such services does not impair our auditor’s independence. Any proposed services exceeding pre-approved cost levels will require specific pre-approval by the Audit Committee. The term of any pre-approval is 12 months from the date of pre-approval, unless the Audit Committee specifically provides for a different period. The Audit Committee will periodically review and pre-approve the services that may be provided by the independent registered public accounting firm as well as revise the list of pre-approved services from time to time, based on subsequent determinations.

The Audit Committee will not delegate to management responsibilities to pre-approve services performed by the independent registered public accounting firm. The Audit Committee may delegate pre-approval authority to one or more of its members. The annual audit services engagement terms and fees will be subject to the specific pre-approval of the Audit Committee. The Audit Committee will approve, if necessary, any changes in terms, conditions and fees resulting from changes in audit scope, Company structure or other matters. In addition to the annual audit services engagement specifically approved by the Audit Committee, the Audit Committee may grant pre-approval for other audit services, which are those services that only the independent auditor reasonably can provide. The Audit Committee will not approve any non-audit services prohibited by applicable SEC regulations or any services in connection with a transaction initially recommended by the independent registered public accounting firm, the purpose of which may be tax avoidance and the tax treatment of which may not be supported by the Internal Revenue Code of 1986, as amended (the “Code”), and related regulations.

Audit-related services are assurance and other services that are reasonably related to the performance of the audit or review of the Company’s financial statements or that are traditionally performed by the independent registered public accounting firm. The Audit Committee believes that the provision of audit-related services does not impair the independence of the independent registered public accounting firm.

The Audit Committee believes that the independent registered public accounting firm can provide tax services to the Company, such as tax compliance, tax planning and tax advice, without impairing such auditor’s independence. However, the Audit Committee will not permit the retention of the independent registered public accounting firm in connection with a transaction initially recommended by the independent auditor, the purpose of which may be tax avoidance and the tax treatment of which may not be supported in the Code and related regulations.

The Audit Committee may grant pre-approval of those permissible non-audit services classified as “All Other” services that it believes are routine and recurring services and would not impair the independence of the auditor.

Requests or applications to provide services that require specific approval by the Audit Committee will be submitted to the Audit Committee by the Chief Financial Officer (or other designated officer) and must include a statement from that individual as to whether, in his or her view, the request or application is consistent with the SEC’s rules on auditor independence.

Audit and Other Fees

The following table provides information regarding the aggregate fees billed to the Company for professional services rendered by PricewaterhouseCoopers LLP for 2017 and 2016.

|

2017 |

2016 |

|||||||

|

Audit Fees (1) |

$ | 2,623,605 | $ | 1,858,000 | ||||

|

Audit-Related Fees (2) |

104,299 | 681,068 | ||||||

|

Tax Fees (3) |

72,000 | 36,504 | ||||||

|

All Other Fees (4) |

2,771 | 1,800 | ||||||

|

Total |

$ | 2,802,675 | $ | 2,577,372 | ||||

|

(1) |

Audit fees for 2017 and 2016 related to the annual audit and reviews of financial statements included in the Company’s quarterly filings, including reimbursable expenses. Audit fees for 2017 also related to the review of financial statements and other financial information of RBI Holding LLC (“NewWave”). Audit fees for 2016 also related to the initial annual audit of our internal control over financial reporting. |

|

(2) |

Audit-related fees for 2017 and 2016 related to assurance and other services reasonably related to the performance of the audit or reviews of financial statements and not included under “Audit Fees” above, including reimbursable expenses. Audit-related fees for 2016 also related to due diligence services related to mergers and acquisitions. |

|

(3) |

Tax fees for 2017 and 2016 related to tax compliance, tax advice and tax planning, including reimbursable expenses. These fees were primarily for mergers and acquisitions in 2017 and state and local tax consulting in 2016. |

|

|

|

|

|

|

(4) |

All other fees for 2017 and 2016 related to software licensing for finance and accounting research tools provided by PricewaterhouseCoopers LLP. |

THE BOARD UNANIMOUSLY RECOMMENDS A VOTE “FOR” THE RATIFICATION OF THE APPOINTMENT OF PRICEWATERHOUSECOOPERS LLP AS THE INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM OF OUR COMPANY FOR THE FISCAL YEAR ENDING DECEMBER 31, 2018.

Compensation Discussion and Analysis

Executive Summary

Named Executive Officers (“NEOs”)

This Compensation Discussion and Analysis describes the compensation of our NEOs named in the 2017 Summary Compensation Table:

|

Name |

|

Position |

|

Thomas O. Might (1) |

|

Executive Chairman (through December 31, 2017) |

|

Julia M. Laulis (2) |

|

Chair of the Board, President and Chief Executive Officer (“CEO”) |

|

Michael E. Bowker (3) |

|

Chief Operating Officer (“COO”) |

|

Kevin P. Coyle |

|

Senior Vice President and Chief Financial Officer (“CFO”) |

|

Charles B. McDonald |

|

Senior Vice President, Operations |

|

Alan H. Silverman (4) |

|

Former Senior Vice President, General Counsel and Secretary |

|

(1) |

Effective December 31, 2017, Mr. Might retired as Executive Chairman. He continues to serve as a non-employee director. |

|

|

(2) |

Effective January 1, 2018, Ms. Laulis was appointed Chair of the Board. |

|

|

(3) |

Effective May 2, 2017, Mr. Bowker was appointed COO. He previously served as Senior Vice President and Chief Sales and Marketing Officer. |

|

|

(4) |

Effective December 29, 2017, Mr. Silverman ceased serving as Senior Vice President, General Counsel and Secretary. |

2017 Highlights

In 2017, Cable One delivered strong results demonstrated by increased profitability, building stockholder value and completing key initiatives, including the acquisition of NewWave, which was the 19th largest cable operator in the United States. Since closing the NewWave acquisition in May 2017, we have been focused on integration not only from an operational and financial perspective, but on combining the culture and best practices of both organizations. Below are highlights of our performance in 2017, including Adjusted EBITDA, which was a performance metric used for our 2017 Annual Executive Bonus Plan (the “2017 Bonus Plan”):

|

■ |

Net income was $234.0 million in 2017, an increase of 131.5% compared to net income of $101.1 million in 2016. Net income included a $113.0 million income tax benefit as a result of the 2017 Federal tax reform legislation, commonly referred to as the Tax Cuts and Jobs Act of 2017 (the “2017 Tax Act”). Excluding both the contribution from NewWave operations and the change in accounting for capitalized labor costs effective since the first quarter of 2017, as previously disclosed beginning with our 2016 Annual Report on Form 10-K, filed on March 1, 2017, net income would have increased 113.8% to $216.2 million. |

|

■ |

Adjusted EBITDA was $443.1 million, an increase of 24.0% compared to Adjusted EBITDA of $357.4 million in 2016. See Annex A of this Proxy Statement, entitled “Use of Non-GAAP Financial Metrics,” for the definition of Adjusted EBITDA and a reconciliation of Adjusted EBITDA to net income, which is the most directly comparable measure under GAAP. Excluding both the contribution from NewWave operations and the capitalized labor change, Adjusted EBITDA would have increased 6.1% to $379.2 million. |

|

■ |

Net cash provided by operating activities was $324.5 million, an increase of 26.2% compared to net cash provided by operating activities of $257.1 million in 2016. |

|

■ |

Adjusted EBITDA less capital expenditures was $263.7 million, an increase of 16.4% compared to Adjusted EBITDA less capital expenditures of $226.5 million in 2016. See Annex A of this Proxy Statement, entitled “Use of Non-GAAP Financial Metrics,” for the definition of Adjusted EBITDA less capital expenditures and reconciliations to net income, which is the most directly comparable measure under GAAP when this metric is used as a performance measure, and to net cash provided by operating activities, which is the most directly comparable measure under GAAP when this metric is used as a liquidity measure. |

|

■ |

Total stockholder return as of December 31, 2017 grew 14.2% on a one-year basis and 26.8% on a compounded two-year basis. |

Noteworthy Changes to Our Compensation Program for 2017

|

■ |

Redesigned performance-based equity awards for 2017. The annual grant of performance-based restricted stock awards (“PSAs”) for 2017 was based on three-year cumulative Adjusted EBITDA less capital expenditures, which, as compared with the 2016 annual grant of PSAs, extended the performance period from one year to three years. For additional details, please see “2017 Compensation Actions” below. |

|

■ |

Management changes. Effective as of January 1, 2017, Mr. Might was appointed Executive Chairman and Ms. Laulis was appointed President and CEO. In connection with Mr. Might’s appointment, his annual base salary was reduced, he was not eligible to receive an annual bonus under our annual executive bonus plan for 2017 and he received a grant of PSAs. In connection with Ms. Laulis’ appointment, her annual base salary and target annual bonus were increased and she received a one-time promotional stock appreciation right (“SAR”) grant in addition to her annual PSA grant. Effective as of December 31, 2017, Mr. Might retired as Executive Chairman, although he continues to serve as a non-employee director of the Company. Effective May 2, 2017, Mr. Bowker was appointed COO. He previously served as Senior Vice President and Chief Sales and Marketing Officer. In addition, on December 29, 2017, Mr. Silverman ceased serving as Senior Vice President, General Counsel and Secretary. For additional details regarding the 2017 compensation terms for Mr. Might, Ms. Laulis, Mr. Bowker and Mr. Silverman, please see “Elements of our Compensation Program” below. |

|

■ |

Amended stock ownership guidelines in 2017. In 2017, the Board amended our stock ownership guidelines, which, among other things, increased the required stock ownership level for our CEO from a multiple of five times base salary to six times base salary and adopted the same six times base salary multiple for the position of Executive Chairman. The required stock ownership levels for the President and Senior Vice Presidents were also increased from multiples of 2.5 and 2.0 times base salary to 3.5 and 3.0 times base salary, respectively. The stock ownership guidelines were also clarified such that PSAs are not counted toward achievement of the applicable guideline multiple until all performance contingencies have been satisfied and require that if, following the initial five-year compliance period, an executive falls below the required ownership level, the executive retain net after-tax shares from SAR exercises or when PSAs or time-based restricted stock awards (“RSAs”) vest until the applicable guideline has been met. For additional details regarding the amended stock ownership guidelines, please see “Corporate Governance Policies—Stock Ownership Guidelines” below. |

Executive Compensation and Governance “Best Practices”

Below is a summary of best practices that we have implemented with respect to the compensation of our NEOs because we believe they support our compensation philosophy and are in the best interests of our Company and our stockholders.

|

✓ |

Our compensation is aligned with a pay-for-performance philosophy where a substantial portion of executive officer compensation is at-risk and tied to objective performance goals. |

|

✓ |

Both annual bonuses and, with limited exceptions, annual equity incentive awards are 100% based on financial operating performance against pre-defined objective goals with no discretion to increase payouts. |

|

✓ |

The Compensation Committee engages an independent compensation consultant. |

|

✓ |

We maintain robust executive and non-employee director stock ownership guidelines. |

|

✓ |

We maintain clawback provisions in our equity award agreements, and our long-term incentive plan permits recoupment of cash awards granted thereunder under various circumstances. |

|

✓ |

We prohibit all executives and directors from hedging and pledging our securities. |

|

✓ |

The Compensation Committee conducts an annual risk assessment of our compensation program. |

|

✓ |

We do not provide any “single trigger” acceleration of payments or benefits upon a change of control of the Company. |

|

✓ |