Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO FINANCIAL STATEMENTS

Confidential Draft No. 2 Submitted on March 27, 2015

As filed with the Securities and Exchange Commission on , 2015

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM S-11

REGISTRATION STATEMENT

FOR REGISTRATION UNDER THE SECURITIES ACT OF 1933

OF SECURITIES OF CERTAIN REAL ESTATE COMPANIES

COMMUNITY HEALTHCARE TRUST INCORPORATED

(Exact name of registrant as specified in its governing instruments)

354 Cool Springs Blvd.

Suite 106

Franklin, Tennessee 37067

(615) 771-3052

(Address, including zip code and telephone number, including area code, of registrant's principal executive offices)

Timothy G. Wallace

Community Healthcare Trust Incorporated

354 Cool Springs Blvd.

Suite 106

Franklin, Tennessee 37067

(615) 771-3052

(Name, address, including zip code and telephone number, including area code, of agent for service)

| Copies to: | ||

Tonya Mitchem Grindon J. Allen Roberts Baker, Donelson, Bearman, Caldwell & Berkowitz, PC Baker Donelson Center Suite 800 211 Commerce Street Nashville, Tennessee 37201 (615) 726-5600 (615) 744-5607 (fax) |

Justin R. Salon Morrison & Foerster LLP 2000 Pennsylvania Avenue, NW Suite 6000 Washington, District of Columbia 20006-1888 (202) 887-8785 (202) 887-0763 (fax) |

|

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box. o

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to Section 8(a), may determine.

The information in this prospectus is not complete and may be changed or supplemented. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities, and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS SUBJECT TO COMPLETION DATED MARCH 27, 2015

Community Healthcare Trust

Incorporated

Shares of Common Stock

Community Healthcare Trust Incorporated is a fully-integrated healthcare real estate company that was recently organized to acquire and own properties that are leased to hospitals, doctors, healthcare systems or other healthcare service providers located in geographic areas primarily outside of urban centers. As a result of favorable demographic trends affecting the healthcare industry, continuing increases in healthcare spending and the continuing shift in the delivery of healthcare services to community-based outpatient facilities, we believe our target properties are essential for healthcare providers to serve their local markets. Our management team has significant healthcare, real estate and public real estate investment trust, or REIT, experience and has long-established relationships with a wide range of healthcare providers, which we believe will provide us a competitive advantage in sourcing growth opportunities that produce attractive risk-adjusted returns.

This is our initial public offering, and no public market currently exists for our common stock. We are offering shares of our common stock to be sold in this offering. We currently expect the public offering price in this offering to be between $ and $ per share. We intend to apply to have our common stock listed on the New York Stock Exchange, or the NYSE, under the symbol "CHCT". Timothy G. Wallace, our Chairman, Chief Executive Officer and President, has committed to purchase $2,000,000 in shares of our common stock in a private placement at a price per share equal to the initial public offering price. This concurrent private placement is expected to close on the same day as this offering and is contingent upon completion of this offering. This offering is not contingent upon the closing of the concurrent private placement.

We intend to elect to be taxed and to operate in a manner that will allow us to qualify as REIT for U.S. federal income tax purposes commencing with our taxable year ending December 31, 2015. To assist us in qualifying and maintaining our qualification as a REIT, among other purposes, our charter generally limits any person from beneficially or constructively owning more than 9.8% in value of the outstanding shares of our capital stock and 9.8% in value or number of shares, whichever is more restrictive, of the outstanding shares of our common stock. See "Description of Capital Stock—Restrictions on Ownership and Transfer."

We are an "emerging growth company" under the federal securities laws and will be subject to reduced public company reporting requirements. Investing in our common stock involves a high degree of risk. See "Risk Factors" beginning on page 19 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

|

||||

| |

Per Share |

Total |

||

|---|---|---|---|---|

Public offering price |

$ | $ | ||

Underwriting discounts and commissions(1) |

$ | $ | ||

Proceeds, before expenses, to us |

$ | $ | ||

|

||||

- (1)

- See "Underwriting" for additional disclosure regarding the underwriting discounts and commissions and other expenses payable to the underwriters by us.

We have granted the underwriters the option to purchase up to an additional shares from us at the initial public offering price less the underwriting discount.

Delivery of the shares of common stock in book-entry form will be made on or about , 2015.

Sandler O'Neill + Partners, L.P.

Prospectus dated , 2015

You should rely only upon the information contained in this prospectus and any free writing prospectus provided or approved by us. We have not, and the underwriters have not, authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely upon it. We are not, and the underwriters are not, making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our common stock.

Industry and Market Data

We use industry forecasts and projections and market data throughout this prospectus, including data from publicly available sources and industry publications. Our forecasts and projections are based on industry surveys and the preparers' experience in the industry and there can be no assurance that any of our projections will be achieved. We believe that the surveys and market research others have performed are reliable, but we have not independently verified this information and the accuracy and completeness of the information are not guaranteed. Our estimates involve risks and uncertainties and are subject to change based on various factors, including those described under the heading "Risk Factors" in this prospectus.

i

This summary highlights key aspects of this offering which are contained elsewhere in this prospectus. This summary is not complete and does not contain all of the information that you should consider before making your investment decision. Before investing in our common stock, you should carefully read this entire prospectus, including the more detailed information set forth under the caption "Risk Factors," the historical and pro forma financial statements, including the related notes thereto, appearing elsewhere in this prospectus, and any free writing prospectus provided or approved by us.

Unless the context otherwise requires or indicates, references in this prospectus to "we," "us," "our," "the Company," "our company," and "Community Healthcare Trust" refer to Community Healthcare Trust Incorporated, a Maryland corporation recently organized to qualify as a REIT for U.S. federal income tax purposes, together with its consolidated subsidiaries, including Community Healthcare OP, LP, a Delaware limited partnership, or our operating partnership of which we are the sole general partner and own 100% of its interests. Additionally, references in this prospectus to the "Initial Properties" refer to the 35 properties in Non-Urban areas identified in this prospectus under the caption "Our Business—Initial Properties" that the Company has entered into written agreements to acquire with the net proceeds of this offering. We define "Non-Urban" areas as, collectively, suburban areas, exurban areas (areas adjoining metropolitan statistical areas) and micropolitan areas (areas with populations of 10,000 to 50,000 that do not directly border larger urban areas).

Unless the context otherwise requires or indicates, the information set forth in this prospectus assumes that (i) the acquisitions of the Initial Properties described in detail elsewhere in this prospectus have been completed, (ii) the underwriters' option to acquire additional shares of our common stock is not exercised, (iii) the concurrent private placement of $2,000,000 in shares of our common stock to Timothy G. Wallace, our Chairman, Chief Executive Officer and President, has closed and (iv) the shares of our common stock to be sold in this offering are sold at $ per share, which is the mid-point of the price range indicated on the cover page of this prospectus.

Overview

We are a fully-integrated healthcare real estate company that was recently organized as a Maryland corporation to acquire and own properties that are leased to hospitals, doctors, healthcare systems or other healthcare service providers in Non-Urban markets. Our strategic focus is to invest in real estate that is diversified across healthcare provider, geography, facility type and industry segment. We believe that favorable demographic trends, continuing increases in healthcare spending and the continuing shift in the delivery of healthcare services to community-based outpatient facilities create attractive opportunities for us. We intend to focus on Non-Urban healthcare facilities because we believe these properties are essential to healthcare providers in their local markets and can generate more attractive risk-adjusted returns than similar facilities in urban markets. In addition, we believe our management team's extensive relationships with healthcare providers and owners of healthcare facilities will provide us with the opportunity to acquire attractive Non-Urban healthcare facilities outside of a competitive bidding process. Furthermore, we believe there is significantly less competition from existing REITs and institutional buyers for these Non-Urban assets.

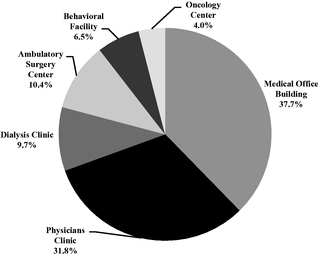

Upon completion of this offering and the acquisition of our Initial Properties, we will own 35 properties comprised of an aggregate of approximately 623,000 leasable square feet located in 18 states. Our Initial Properties are leased by healthcare providers across a diverse range of both facility types and healthcare industry segments, including ambulatory surgery centers, behavioral facilities, dialysis clinics, medical office buildings, oncology centers, and physician clinics. As of December 31, 2014, the Initial Properties were approximately 94% leased to 69 separate tenants. We believe our staggered lease maturity schedule and active asset management will optimize the value of our portfolio by consistently achieving market rental rates in new leases when the existing leases expire.

1

Substantially all of our revenues will be derived from net leases pursuant to which our tenants are generally responsible for substantially all of the operating expenses relating to the property, including real estate taxes, utilities, property insurance, routine maintenance and repairs and property management. We believe this net lease structure helps insulate us from increases in certain operating expenses and provides more predictable cash flow. The leases for our Initial Properties typically include rent escalation provisions designed to provide us with annual growth in our rental revenues. Tenants of our Initial Properties include many nationally recognized healthcare providers (or their affiliates), such as Adventist HealthCare, Inc., or Adventist, Hospital Corporation of America, or HCA, Fresenius Medical Care AG & Co., KGaA, or Fresenius, and AmSurg Corp., or AmSurg. Through these property investments and corresponding operating income, we seek to generate attractive risk-adjusted returns for our stockholders through a combination of stable and increasing dividends and potential long-term appreciation in the value of our properties and the value of our shares of common stock.

Our management team has between 22 and 33 years of healthcare, real estate and public REIT management experience and has long-established relationships with a wide range of healthcare providers. We believe these relationships provide us a competitive advantage in sourcing growth opportunities that produce attractive risk-adjusted returns.

During the initial terms of their respective employment agreements, all of our officers have elected to take 100% of their salary, bonus and long-term incentive compensation in the form of restricted stock, subject to an eight-year cliff-vesting period, which we believe creates a significant alignment of interest between management and our stockholders. In addition, Mr. Wallace, our Chairman, Chief Executive Officer and President, has committed to buy $2,000,000 in shares of our common stock in a concurrent private placement at the same price offered to the public pursuant to this prospectus, which we believe further aligns his interests with our stockholders. Finally, we have adopted stock ownership guidelines that require our officers and directors to continuously own an amount of our common stock based upon a multiple of such officer's annual base salary or such director's annual retainer, as applicable.

We intend to elect to be taxed and to operate in a manner to allow us to qualify as a REIT for U.S. federal income tax purposes commencing with our taxable year ending December 31, 2015.

Competitive Strengths

We believe our management team's significant healthcare, real estate and public REIT management experience distinguishes us from other REITs and real estate operators, both public and private. Specifically, our company's competitive strengths include, among others:

- •

- Strong, Diversified Initial Portfolio. Upon completion of

this offering and the acquisition of the Initial Properties, we will own 35 properties that are 94% leased, located in 18 states, leased by 69 separate tenants and comprised of six different

healthcare facility types. Our focus is on investing in properties where we can develop strategic alliances with financially sound healthcare providers that offer need-based healthcare services in our

target markets. Our tenant base includes many nationally recognized healthcare providers (or their affiliates), such as Adventist, HCA, Fresenius and AmSurg. We have structured, and intend to

maintain, our property portfolio with significant diversification with respect to healthcare provider, industry segment, facility type and geography.

- •

- Attractive and Disciplined Investment Focus. We intend to focus on acquiring Non-Urban healthcare facilities in off-market or lightly marketed transactions at purchase prices of approximately $10 million or less. We believe there is significantly less competition from existing REITs and institutional buyers for these Non-Urban assets than for comparable urban assets, thereby increasing the potential for more attractive risk-adjusted returns. In addition, we believe that healthcare-related real estate rents and valuations are less susceptible to changes in the

2

- •

- Extensive Relationships with Healthcare Providers, Intermediaries and Property

Owners. We believe that our management team has a strong reputation among, and a deep understanding of the real estate needs of,

healthcare providers in our target markets. For example, AmSurg, a nationally recognized leader in the development, management and operation of outpatient surgery centers, has designated us as one of

its two strategic partners to acquire real estate owned by physicians that are partners in surgery centers AmSurg operates. We believe that this strategic relationship demonstrates our ability to meet

the needs of healthcare providers by structuring transactions that are mutually advantageous to sellers, our tenants and us. We believe this ability will lead to strategic acquisition opportunities,

which will, in turn, produce attractive risk-adjusted returns. The Initial Properties were sourced through industry relationships and negotiated directly with the sellers. None of our Initial

Properties were acquired pursuant to "calls for offers" or other auction style bidding situations. We believe our relationships will provide us with additional off-market or lightly marketed

acquisition opportunities, thus providing us the opportunity to continue to purchase assets outside a competitive bidding process.

- •

- Experienced Management Team. Each of the members of our

management team has between 22 and 33 years of healthcare, real estate and/or public REIT management experience. Led by Timothy G. Wallace, our Chairman, Chief Executive Officer and President,

W. Page Barnes, our Executive Vice President and Chief Financial Officer, and Leigh Ann Stach, our Vice President—Financial Reporting and Chief Accounting Officer, our management team has

significant experience in acquiring, owning, operating and managing healthcare facilities and providing full service real estate solutions for the healthcare industry. Prior to founding our company,

Mr. Wallace was a co-founder and Executive Vice President of Healthcare Realty Trust (NYSE: HR). Between the initial public offering of HR in 1993 and his departure from HR in 2002,

Mr. Wallace was integral in helping to grow HR to over $2 billion in assets. Mr. Barnes has held executive positions with acute care and behavioral hospital companies and directed

healthcare lending for AmSouth Bank. Ms. Stach has experience in public healthcare REIT accounting and financial reporting.

- •

- Growth Oriented Capital Structure. We anticipate that,

upon completion of this offering and the acquisition of the Initial Properties, none of our properties will have mortgages and we will have no corporate debt outstanding. However, concurrently with or

shortly after the completion of this offering, we expect to obtain a credit facility, which we refer to as the anticipated credit facility, with a borrowing capacity of up to approximately

$75.0 million. We may also use limited partnership interests, or OP units, in Community Healthcare OP, LP, our operating partnership, as currency to acquire additional properties from

owners seeking to defer their potential taxable gain and diversify their holdings. We believe that the expected borrowing capacity under our anticipated credit facility, combined with our ability to

use OP units as acquisition currency, will provide us with significant financial flexibility to make opportunistic investments and fund future growth.

- •

- Significant Alignment of Interests. We have structured the compensation of our management team to closely align their interests with the interests of our stockholders. During the initial terms of their respective employment agreements, all of our officers have elected to take 100% of their salary, bonus and long-term incentive in the form of restricted stock that is subject to an eight-year cliff-vesting period. We believe that paying our management team solely with restricted stock that is subject to an eight-year cliff-vesting period effectively aligns the interests of our management team with those of our stockholders, creating significant incentives to maximize returns for our stockholders. In addition, concurrently with the completion of this offering, Mr. Wallace has committed to purchase $2,000,000 in shares of our common stock in a

general economy than many other types of commercial real estate due to favorable demographic trends and the need-based rise in healthcare expenditures, even during economic downturns.

3

private placement at a price per share equal to the initial public offering price, which we believe further aligns his interests with our stockholders. Finally, we have adopted stock ownership guidelines that require our officers and directors to continuously own an amount of our common stock based on a multiple of such officer's annual base salary or such director's annual retainer, as applicable.

Our Business Objectives and Strategies

Our principal business objective is to provide attractive risk-adjusted returns to our stockholders through a combination of (i) sustainable and increasing rental income and cash flow that generates reliable, increasing dividends and (ii) potential long-term appreciation in the value of our properties and common stock. Our primary strategies to achieve our business objective are to invest in, own and proactively asset manage a diversified portfolio of healthcare properties, which we believe will drive reliable, increasing rental revenue and cash flow.

Growth Strategy

We anticipate being able to increase our current cash flow on the Initial Properties as leases mature. As of December 31, 2014, the Initial Properties were approximately 94% leased to 69 separate tenants with a weighted average remaining lease term for the portfolio of approximately 4.5 years. We believe our staggered lease maturity schedule and active asset management will optimize the value of our portfolio by consistently achieving market rental rates in new leases when the existing leases expire. Furthermore, in addition to having contractual rent escalation clauses in substantially all of our leases, our staggered lease maturity schedule increases the likelihood that we will consistently achieve market rental rates in new leases when the existing leases expire. In addition, we do not believe there is significant new supply growth or plans for the development of competitive facilities in our target markets. Thus, we believe this limited supply of competitive facilities in our target markets will increase the likelihood of significant tenant renewals.

We intend to grow our portfolio of healthcare properties primarily through acquisitions of Non-Urban healthcare facilities that provide stable revenue growth and predictable long-term cash flows. We generally expect to focus on individual acquisition opportunities of $10 million or less in off-market or lightly marketed transactions and do not intend to participate in competitive bidding or auctions of properties. We believe that there are abundant opportunities to acquire attractive healthcare properties in our target markets either from third-party owners of existing healthcare facilities or directly with healthcare providers through sale-leaseback transactions. We believe there is significantly less competition for these Non-Urban assets from existing REITs and institutional buyers than for comparable assets in urban areas, thereby increasing the potential for attractive risk-adjusted returns. Furthermore, we may acquire healthcare properties on a non-cash basis in a tax efficient manner through the issuance of OP units as consideration for the transaction.

We intend our investment portfolio to be diversified among healthcare facility type and segments such as ambulatory surgery centers, behavioral facilities, dialysis clinics, medical office buildings, oncology centers, and physician clinics, as well as being diverse both geographically and with respect to our tenant base. We seek to invest in properties where we can develop strategic alliances with financially sound healthcare providers that offer need-based healthcare services in our target markets.

Our primary acquisition focus will be on the following types of healthcare facilities:

- •

- Ambulatory surgery centers: Ambulatory surgery centers, also known as outpatient surgery centers, are freestanding healthcare facilities where surgical procedures not requiring an overnight hospital stay are performed. Procedures commonly performed include those related to dermatology, ear, nose and throat/audiology, pain, ophthalmology, orthopedics and sports health and urology.

4

- •

- Behavioral facilities: Behavioral facilities are healthcare facilities

that provide a range of clinical services for mental health and/or substance abuse diagnoses on an inpatient and/or outpatient basis. Behavioral health services provided may include assessment,

treatment, individual medical evaluation and management (including medication management), individual and group therapy, behavioral health counseling, family therapy and psychological testing for

recipients of all ages.

- •

- Dialysis clinics: Dialysis clinics are healthcare facilities that furnish

diagnostic, therapeutic and rehabilitative services required for the care of end stage renal disease dialysis patients.

- •

- Medical office buildings: Medical office buildings are buildings occupied

by healthcare providers and may be located near hospitals or other facilities where healthcare services are rendered or in close proximity to a population base. Medical office buildings can be leased

by physicians, physician practice groups, hospitals, healthcare systems or other healthcare providers.

- •

- Oncology centers: Oncology centers are healthcare facilities where one or

more of the three primary oncology disciplines are provided to ambulatory patients. These three disciplines are medical oncology (the treatment of cancer with medicine, including chemotherapy),

surgical oncology (the surgical aspects of cancer treatment, including biopsy, staging and surgical resection of tumors) and radiation oncology (the treatment of cancer with therapeutic radiation).

- •

- Physician clinics: Physician clinics are freestanding healthcare facilities that are primarily devoted to the care of ambulatory patients, can be privately operated or publicly managed and funded, and typically provide primary healthcare needs of populations in local communities utilizing physicians and other healthcare providers.

Our secondary acquisition focus will be on the following types of healthcare facilities:

- •

- Acute care hospitals: Acute care hospitals are traditional medical and

surgical hospitals providing both inpatient and outpatient medical services and are owned and/or operated either by a non-profit or for-profit hospital or hospital system. These facilities may act as

feeder facilities to dedicated regional medical centers.

- •

- Assisted living facilities: Assisted living facilities provide services

that include minimal nursing assistance and minimal assistance for activities of daily living. Assisted living facilities typically are comprised of one and two bedroom suites equipped with private

bathrooms and efficiency kitchens. Services bundled within one regular monthly fee usually include three meals per day in a central dining room, daily housekeeping, laundry, medical reminders and

24-hour availability of assistance with the activities of daily living, such as eating, dressing and bathing.

- •

- Post-acute care hospitals: Post-acute care hospitals are healthcare

facilities that offer restorative, rehabilitative and custodial care for people not requiring the more extensive and complex treatment available at acute care hospitals. Ancillary and sub-acute care

services that are provided may include occupational, physical, speech, respiratory and intravenous therapy, wound care, oncology treatment, brain injury care and orthopedic therapy.

- •

- Skilled nursing facilities: Skilled nursing facilities are inpatient

healthcare facilities with the staff and equipment to provide long-term skilled nursing care, rehabilitation and other related health services to patients, typically elderly, who need nursing care,

but do not require hospitalization.

- •

- Specialty hospitals: Specialty hospitals are hospitals that focus and specialize in providing care for certain conditions and performing certain procedures, such as cardiovascular and orthopedic surgery.

In connection with our review and consideration of healthcare real estate acquisition opportunities, we generally take into account a variety of considerations, including but not limited to:

- •

- whether the property will be leased to a financially-sound healthcare tenant;

5

- •

- the historical performance of the market and its future prospects;

- •

- property location, with an emphasis on proximity to a population base;

- •

- demand for healthcare related services and facilities;

- •

- current and future supply of competing properties;

- •

- occupancy and rental rates in the market;

- •

- population density and growth potential;

- •

- anticipated capital expenditures;

- •

- anticipated future acquisition opportunities; and

- •

- existing and potential competition from other healthcare real estate owners and tenants.

We currently have no intention to invest in companies that provide healthcare services structured to comply with the REIT Investment Diversification and Empowerment Act of 2007, or RIDEA.

Financing Strategy

Upon completion of this offering, none of the Initial Properties will be subject to any mortgage financing. Additionally, we expect to have no outstanding corporate-level indebtedness upon completion of this offering. However, in the future, we may incur fixed or floating rate indebtedness, including indebtedness secured by our properties. Concurrently with or shortly after the completion of this offering, we intend to obtain the anticipated credit facility in an amount up to approximately $75.0 million. We intend to use proceeds from the anticipated credit facility to finance additional property acquisitions and for general corporate purposes. As of the date of this prospectus, we have not received a commitment letter from any lenders for the anticipated credit facility, however, and there can be no assurance that we will enter into definitive documentation with regard to this facility on the terms we anticipate or at all. Our present financing policy prohibits incurring debt (secured or unsecured) in excess of 40% of our total book capitalization.

Healthcare and Healthcare Real Estate Overview

We believe the U.S. healthcare industry is poised to continue to grow due to favorable demographic trends, increasing healthcare expenditures, new and proposed government initiatives and changing patient preferences. Furthermore, we believe these factors are contributing to the increased need for healthcare providers to enhance the delivery of healthcare by, among other things, integrating real estate solutions that focus on more efficient, cost-effective and conveniently located patient care. Specifically, we believe the factors and trends discussed below are creating an attractive environment in which to invest in healthcare properties.

Increases in U.S. Healthcare Spending

According to the United States Department of Health and Human Services, or HHS, healthcare spending accounted for approximately 17.4% of U.S. gross domestic product, or GDP, in 2013. As illustrated in the graph below, national healthcare expenditures continue to rise, and are projected to grow from an estimated $2.9 trillion in 2013 to an estimated $4.3 trillion by 2020, representing an average annual rate of growth of approximately 5.6%, reaching a projected 18.4% of GDP in 2020. The anticipated continuing increase in demand for healthcare services, together with an increasingly complex and costly regulatory environment, changes in medical technology and reductions in government reimbursements, are expected to put increased pressure on healthcare providers to find cost effective solutions for their real estate needs.

6

Annual U.S. Healthcare Expenditures

Source: U.S. Census Bureau, Population Projections; CMS, National Health Expenditures 1970-2021

Aging Population

The aging of the U.S. population has a direct effect on the demand for healthcare as older people, on average, utilize healthcare services at a rate well in excess of younger people. Thus, the aging population, driven by the baby boomer generation, and advances in medical technology and services that increase life expectancy are key drivers of the growth in healthcare expenditures.

Over the next 25 years the U.S. population is expected to grow by approximately 18.0%. The rapidly growing senior citizen population in the U.S. is expected to result in substantially increased demand for healthcare services as the baby boomer generation ages and life expectancies lengthen. The U.S. Census Bureau estimates the total number of Americans aged 65 and older is expected to increase from approximately 43 million in 2012 to approximately 74 million by 2030, with the number of citizens aged 65 and older expected to grow at approximately five times the rate of the overall population by 2030. In addition, the 65 and older age group was approximately 14.0% of the U.S. population in 2012 and is projected to grow to nearly 21.0% by 2030 as is shown in the graph below.

Source: Center for Medicare & Medicaid Services, U.S. Census Bureau, Population Division

7

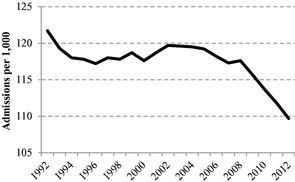

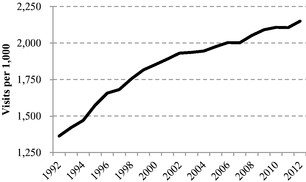

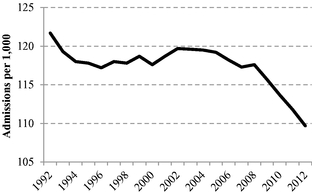

Clinical Care Continues to Shift to Outpatient Facilities

We believe the continued shift in the delivery of healthcare services to outpatient facilities will increase the need for smaller, more specialized and efficient hospitals and outpatient facilities that more effectively accommodate those services. As shown in the graph below, procedures traditionally performed in hospitals, such as certain types of surgery, are increasingly moving to outpatient facilities driven by advances in clinical science, shifting consumer preferences, limited or inefficient space in existing hospitals and lower costs in the outpatient environment. Additionally, studies by the American Hospital Association show that outpatient visits have grown approximately 94.0% from 1992 to 2012, whereas inpatient admissions have grown by just 11.0%. This continuing shift in the delivery of healthcare services to an outpatient environment increases the need for additional outpatient facilities and smaller, more specialized and efficient hospitals.

| Inpatient Admissions | Outpatient Visits | |

|

|

|

Source: American Hospital Association

We believe that healthcare is delivered more cost effectively and with higher patient satisfaction when it is provided on an outpatient basis. We believe the recently enacted Patient Protection and Affordable Care Act, or the Affordable Care Act, and healthcare market trends toward outpatient care will continue to push healthcare services out of larger, older, inefficient hospitals and into newer, more efficient and conveniently located outpatient facilities and smaller specialized hospitals. Increased specialization within the medical field is also driving demand for medical facilities that are purpose-built for particular specialties.

8

Increase in Insured Americans Through the Affordable Care Act

The recently enacted Affordable Care Act represents a significant overhaul of many aspects of healthcare regulations and health insurance and requires every American to have health insurance or be subjected to a tax. HHS predicts the Affordable Care Act will result in an additional 30 million Americans having health insurance by 2020, which we believe will increase the frequency of physician office visits. Accordingly, we believe the increased demand for healthcare services will result in the need for healthcare providers to invest in the expansion of medical, outpatient and smaller specialty hospital facilities.

Favorable Non-Urban Healthcare Outlook

We believe the factors discussed above will affect all markets within the healthcare space, but they will be most notable in Non-Urban areas where the growing aging population resides. Most Non-Urban residents live in counties bordering metropolitan areas, and only a small proportion live in remote communities. Over 61.0% of Non-Urban residents live in counties adjacent to urban areas. Another 29.0% of Non-Urban residents live in counties that contain regional population centers, or micropolitan areas, that do not directly border larger urban areas. Only a small portion of the population lives in geographically remote counties. Within these Non-Urban areas, residents tend to be older and poorer than their urban counterparts. We believe the majority of the newly-insured will enter the health system through Medicaid and state health exchanges. It has been estimated by United Health that, as a result of the implementation of the Affordable Care Act, an additional 8.0 million Non-Urban residents could be enrolled in Medicaid or state health exchanges by 2019. Therefore, we believe healthcare providers will need to make significant investments in these Non-Urban areas to ensure that these newly covered populations are able to get the care they need in manner that is cost-effective and conveniently located.

In conclusion, we believe the current market for quality healthcare facilities that satisfy our investment criteria and are located in Non-Urban markets is substantial. Furthermore, we believe that continued increases in healthcare spending, a growing aging population, the implementation of the Affordable Care Act and a continued shift to outpatient facilities, will result in even greater demand by healthcare providers to invest in new, specialized real estate assets in locations that are conveniently located for patients. Additionally, we believe that there are fewer competitors for this asset class because we believe that very few, if any, public REITs are focused on acquiring Non-Urban healthcare facilities in a price range of less than $10 million.

Our Initial Properties

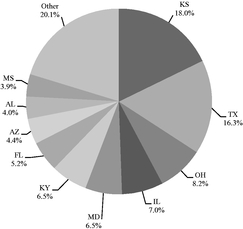

Upon completion of this offering and the acquisition of the Initial Properties, we will own a 100% fee simple interest in 35 properties comprised of an aggregate of approximately 623,000 leasable square feet located in 18 states. The Initial Properties are currently leased by 69 separate tenants and are subject to leases with a weighted average remaining lease term of approximately 4.5 years as of

9

December 31, 2014. The table below provides certain information regarding each of our Initial Properties as of December 31, 2014.

Property

|

Location | Facility Type(1) |

Total Leasable Sq. Ft. |

In-Place Occupancy |

Annualized Lease Revenue(2) |

Percentage of Total Annualized Lease Revenue(3) |

Annualized Lease Revenue Per Leased Sq. Ft. ($)(4) |

Principal Tenant/Affiliate of | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Provena Medical Center |

Bourbonnais, IL | MOB | 54,000 | 91.60 | % | 834,611 | 7.00 | % | 16.87 | Presence Health | |||||||||||

Bayside Medical Center |

Pasadena, TX | MOB | 51,316 | 67.80 | % | 708,612 | 5.95 | % | 20.37 | HCA | |||||||||||

Cypress Medical Center |

Wichita, KS | MOB | 43,945 | 92.50 | % | 830,974 | 6.97 | % | 20.43 | HCA & Kansas Medical Center | |||||||||||

Los Alamos Professional Plaza |

Alamo, TX | MOB | 41,797 | 91.60 | % | 534,282 | 4.48 | % | 13.94 | CVS & Hidalgo County | |||||||||||

Adventist Behavioral Health |

Cambridge, MD | BF | 40,180 | 100.00 | % | 771,283 | 6.47 | % | 19.20 | Adventist Healthcare | |||||||||||

Cavalier Medical & Dialysis Center |

Florence, KY | MOB | 36,362 | 91.00 | % | 450,223 | 3.78 | % | 13.60 | Paradigm Pain & Spine Consultants | |||||||||||

Prairie Star Medical Facility II |

Shawnee, KS | MOB | 24,840 | 89.50 | % | 438,391 | 3.68 | % | 19.71 | Adventist Health System Sunbelt Healthcare Corporation | |||||||||||

Prairie Star Medical Facility I |

Shawnee, KS | PC | 24,557 | 100.00 | % | 460,464 | 3.86 | % | 18.75 | Adventist Health System Sunbelt Healthcare Corporation | |||||||||||

Williams Medical Clinic* |

Holly Spring, MS | PC | 24,024 | 100.00 | % | 462,000 | 3.88 | % | 19.23 | Williams Medical Clinic | |||||||||||

Dahlonega Medical Mall |

Dahlonega, GA | MOB | 20,621 | 97.70 | % | 328,333 | 2.75 | % | 16.30 | PCG Molecular | |||||||||||

Grandview Plaza |

Lancaster, PA | PC | 20,000 | 100.00 | % | 456,646 | 3.83 | % | 22.83 | Wellspan Health & Lancaster General Medical Group | |||||||||||

Brook Park Medical Building |

Brook Park, OH | MOB | 18,444 | 100.00 | % | 367,490 | 3.08 | % | 19.92 | Southwest Community Health System | |||||||||||

Fresenius Florence Dialysis Center |

Florence, KY | DC | 18,283 | 100.00 | % | 319,176 | 2.68 | % | 17.46 | Fresenius Medical Care | |||||||||||

Fresenius Corsicana Dialysis Center |

Corsicana, TX | DC | 17,699 | 82.60 | % | 236,329 | 1.98 | % | 16.17 | Fresenius Medical Care | |||||||||||

Columbia Gastroenterology Surgery Center |

Columbia, SC | ASC | 16,969 | 94.00 | % | 317,101 | 2.66 | % | 19.88 | Palmetto Health | |||||||||||

Family Medicine East |

Wichita, KS | PC | 16,581 | 100.00 | % | 410,838 | 3.45 | % | 24.78 | Family Medicine East Chartered | |||||||||||

Fresenius Gallipolis Dialysis Center |

Gallipolis, OH | DC | 15,110 | 100.00 | % | 137,805 | 1.16 | % | 9.12 | Fresenius Medical Care | |||||||||||

UW Health Clinic—Portage |

Portage, WI | PC | 14,000 | 100.00 | % | 284,462 | 2.39 | % | 20.32 | University of Wisconsin Health Clinics | |||||||||||

Desert Endoscopy Center |

Tempe, AZ | ASC | 13,000 | 100.00 | % | 270,367 | 2.27 | % | 20.80 | The Mesa AZ Endoscopy ASC | |||||||||||

Northwest Surgery Center |

Houston, TX | ASC | 11,200 | 100.00 | % | 466,356 | 3.91 | % | 41.64 | Northwest Surgery Associates | |||||||||||

Midwest Primary Care Clinic |

Cincinnati, OH | PC | 11,050 | 100.00 | % | 285,239 | 2.39 | % | 25.81 | Catholic Health Partners | |||||||||||

St. Alphonsus Medical Group Clinic |

Nampa, ID | PC | 10,751 | 100.00 | % | 221,826 | 1.86 | % | 26.53 | CHE Trinity Health | |||||||||||

UW Health Clinic—Fort Atkinson |

Fort Atkinson, WI | PC | 8,500 | 100.00 | % | 159,356 | 1.34 | % | 18.75 | University of Wisconsin Health Clinics | |||||||||||

Liberty Dialysis |

Castle Rock, CO | DC | 8,450 | 100.00 | % | 284,176 | 2.38 | % | 33.63 | Fresenius Medical Care | |||||||||||

Virginia Orthopaedic & Spine Specialists |

Portsmouth, VA | PC | 8,445 | 100.00 | % | 168,900 | 1.42 | % | 20.00 | Bon Secours Health System | |||||||||||

Continuum Wellness Center |

Gilbert, AZ | PC | 8,200 | 100.00 | % | 253,636 | 2.13 | % | 30.93 | Agility Health | |||||||||||

Court Street Surgery Center |

Circleville, OH | ASC | 7,787 | 88.80 | % | 183,154 | 1.54 | % | 26.50 | Surgery Partners | |||||||||||

Gulf Coast Cancer Centers |

Gulf Shores, AL | OC | 6,398 | 100.00 | % | 185,414 | 1.56 | % | 28.98 | Vantage Oncology | |||||||||||

Gulf Coast Cancer Centers |

Foley, AL | OC | 6,146 | 100.00 | % | 178,111 | 1.50 | % | 28.98 | Vantage Oncology | |||||||||||

Bassin Center For Plastic Surgery* |

Melbourne, FL | PC | 5,228 | 100.00 | % | 308,216 | 2.59 | % | 58.95 | Roger E. Bassin, M.D. | |||||||||||

Fresenius Fort Valley Dialysis Center |

Fort Valley, GA | DC | 4,920 | 100.00 | % | 110,068 | 0.92 | % | 22.37 | Fresenius Medical Care | |||||||||||

DaVita Etowah Dialysis Center |

Etowah, TN | DC | 4,720 | 100.00 | % | 64,731 | 0.54 | % | 13.68 | DaVita Health Partners | |||||||||||

Gulf Coast Cancer Centers |

Brewton, AL | OC | 3,971 | 100.00 | % | 115,080 | 0.97 | % | 28.98 | Vantage Oncology | |||||||||||

Bassin Center For Plastic Surgery* |

Lady Lake, FL | PC | 2,894 | 100.00 | % | 170,615 | 1.43 | % | 58.95 | Roger E. Bassin, M.D. | |||||||||||

Bassin Center For Plastic Surgery* |

Orlando, FL | PC | 2,420 | 100.00 | % | 142,672 | 1.20 | % | 58.95 | Roger E. Bassin, M.D. | |||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

Total/Average(5) |

622,808 | 93.72 | % | 11,916,937 | 100.00 | % | $ | 20.42 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

- *

- Denotes

that lease will be executed upon the acquisition of the property.

- (1)

- As

used in the table above, "OC" means oncology center, "ASC" means ambulatory surgery center, "PC" means physician clinic, "MOB" means

medical office building, "DC" means dialysis clinic and "BF" means behavioral facility.

- (2)

- Our

annualized lease revenue was calculated by multiplying (i) rental payments (defined as base rent payable by each tenant on a

monthly basis under the terms of a lease that was in place as of December 31, 2014) for the month ended December 31, 2014, by (ii) 12. During 2014, there were no material tenant

concessions or rent abatement periods on any of the Initial Properties. For a property that will be leased pursuant to a lease executed upon our acquisition of such property, annualized lease revenue

is the anticipated annual rental payments set forth in the applicable form of lease to be executed upon the acquisition of the property.

- (3)

- Percentage

of total annualized lease revenue was calculated by dividing annualized lease revenue for the relevant Initial Property by total

annualized lease revenue for the year ended December 31, 2014, expressed as a percentage.

- (4)

- Annualized

lease revenue per leased square foot was calculated by dividing annualized lease revenue for the relevant Initial Property by the

product of the total leasable square footage as of December 31, 2014 and the in-place occupancy as of December 31, 2014.

- (5)

- When we provide weighted-average figures, the amount is weighted by annualized lease revenue, except where otherwise noted.

10

Properties Under Evaluation

In addition to the Initial Properties, we are currently in discussions regarding a number of acquisition opportunities that we have identified through our management team's network of relationships and that we believe will enhance our growth and operating performance metrics. As of the date of this prospectus, we have identified and are in various stages of evaluating potential acquisitions of properties, all from unrelated third parties, for an aggregate purchase price of approximately $125.7 million, based upon our preliminary discussions with the sellers and our internal assessments of the value of these properties. As of the date of this prospectus, we have identified and performed an initial financial analysis of these properties to determine what we would be willing to pay for each property. However, none of the properties under evaluation by management are subject to binding purchase agreements, rights of first offer or rights of refusal and, as a result, none of the properties are deemed probable of acquisition as of the date of this prospectus. There can be no assurance that we will enter into definitive agreements with regard to any of these properties for the anticipated purchase price or at all.

Implications of Being an Emerging Growth Company

We qualify as an emerging growth company, as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act, because we had less than $1 billion annual revenues for the fiscal year ended December 31, 2014. An emerging growth company may take advantage of specified reduced reporting requirements and is relieved of certain other significant requirements that are otherwise generally applicable to public companies. As an emerging growth company, among other things:

- •

- we are exempt from the requirement to obtain an attestation and report from our auditors on the assessment of our internal control

over financial reporting pursuant to the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act;

- •

- we are permitted to provide less extensive disclosure about our executive compensation arrangements; and

- •

- we are not required to give our stockholders non-binding advisory votes on executive compensation or golden parachute arrangements.

The JOBS Act also permits us, as an emerging growth company, to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies and thereby allows us to delay the adoption of those standards until those standards would apply to private companies. We have irrevocably elected not to avail ourselves of this exemption from new or revised accounting standards, and, therefore, will be subject to the same new or revised accounting standards as other public companies that are not emerging growth companies.

We may take advantage of these provisions for up to five years or such earlier time that we are no longer an emerging growth company. Accordingly, the information contained in this prospectus and in other filings we will make with the Securities and Exchange Commission, or SEC, may be different than the information you receive from other public companies in which you hold stock. We would cease to be an emerging growth company upon the earliest to occur of: the last day of the first fiscal year in which we have more than $1 billion in annual revenues; the date we qualify as a "large accelerated filer," with at least $700 million in market value of our common stock held by non-affiliates; the issuance, in any three-year period, of more than $1 billion of non-convertible debt securities; and the last day of the fiscal year ending after the fifth anniversary of this offering.

11

Summary Risk Factors

An investment in our common stock involves a high degree of risk. You should carefully read and consider the risks discussed below and under the caption "Risk Factors" beginning on page 19 of this prospectus before investing in our common stock.

- •

- We are newly formed and have no operating history; therefore there is no assurance that we will be able to successfully operate our

business as a publicly traded company or generate sufficient cash flows to make or sustain distributions to our stockholders.

- •

- We may be unable to source off-market or lightly marketed deal flow in the future, which may have a material adverse effect on our

growth.

- •

- We may be unable to complete the acquisitions of our Initial Properties and/or any potential acquisitions, which would adversely

affect our results of operations and ability to make distributions to our stockholders.

- •

- We may be unable to successfully acquire properties and expand our operations into new or existing Non-Urban markets.

- •

- The value of the consideration for the Initial Properties may exceed the net proceeds from this offering and the concurrent private

placement and we may be unable to acquire certain of the Initial Properties immediately following completion of this offering or at all.

- •

- The healthcare industry is heavily regulated and new laws or regulations, changes to existing laws or regulations, changes to

reimbursement models or structure, loss of licensure or failure to obtain licensure could adversely impact our company and result in the inability of our tenants to make rent payments to us.

- •

- Adverse trends in healthcare provider operations may negatively affect our lease revenues and our ability to make distributions to our

stockholders.

- •

- Illiquidity of real estate investments could significantly impede our ability to respond to adverse changes in the performance of our

properties.

- •

- Uncertain market conditions could cause us to sell our healthcare properties at a loss in the future.

- •

- Conflicts of interest could arise in the future between the interests of our stockholders and the interests of holders of OP units,

which may impede business decisions that could benefit our stockholders.

- •

- Failure to qualify as a REIT, or failure to remain qualified as a REIT, would cause us to be taxed as a regular corporation, which

would adversely affect the value of our shares and substantially reduce funds available for distributions to our stockholders.

- •

- There has been no public market for our common stock prior to this offering and an active trading market for our common stock may not develop following this offering.

Concurrent Private Placement

Concurrently with the completion of this offering, Timothy G. Wallace, our Chairman, Chief Executive Officer and President, has committed to purchase $2,000,000 in shares of our common stock in a private placement at a price per share equal to the initial public offering price. This concurrent private placement is expected to close on the same day as this offering and is contingent upon completion of the offering. This offering is not contingent upon the closing of the concurrent private placement.

12

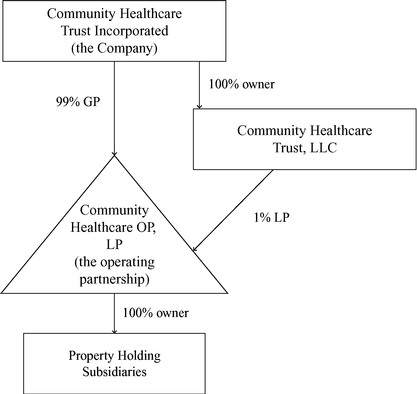

Structure and Formation of Our Company

Our Company

We are a fully-integrated healthcare real estate company that was recently organized as a Maryland corporation to acquire and own properties that are leased to hospitals, doctors, healthcare systems or other healthcare service providers in Non-Urban markets. We will conduct our business through a traditional umbrella partnership real estate investment trust, or UPREIT, structure in which our properties are owned by our operating partnership, directly or through subsidiaries, as described below under "Description of our Operating Partnership and our Partnership Agreement." We are the sole general partner of our operating partnership and, upon completion of this offering, we will own 100% of the OP units. Our board of directors will oversee our business and affairs.

Upon completion of this offering, we will issue shares of common stock ( shares of common stock if the underwriters exercise their option to purchase additional shares in full), including shares to be issued in the concurrent private placement, and, as soon as practicable thereafter and subject to customary closing conditions, we will acquire the Initial Properties. These transactions are described in more detail under the caption "Our Business—Initial Properties" in this prospectus.

Athena Funding Partners, LLC, or AFP, in which Timothy G. Wallace, our Chairman, Chief Executive Officer and President owns 99% of the interests, anticipates advancing or incurring an aggregate of approximately $ million in organizational, legal, accounting and other similar expenses in connection with this offering and the acquisition of the Initial Properties. We will reimburse AFP for these expenses upon completion of this offering and the acquisition of the Initial Properties. See "Certain Relationships and Related Transactions" for more detailed information relating to benefits to be received by our affiliates upon completion of the offering.

Our Operating Partnership

Our operating partnership was formed as a Delaware limited partnership on February 12, 2015 and will commence operations upon the completion of this offering and the acquisition of the Initial Properties. Following the completion of this offering, substantially all of our assets will be held by, and our operations will be conducted through, our operating partnership. We will contribute the net proceeds from this offering to our operating partnership in exchange for OP units. Our interest in our operating partnership will generally entitle us to share in cash distributions from, and in the profits and losses of, our operating partnership in proportion to our percentage ownership, which is currently 100%. As the sole general partner of our operating partnership, we generally will have the exclusive power under the partnership agreement to manage and conduct its business and affairs, subject to certain limited approval and voting rights of the limited partners, which are described in "Description of our Operating Partnership and our Partnership Agreement". In the future, we may issue OP units from time to time in connection with property acquisitions, as compensation or otherwise.

13

Corporate Structure

The chart below reflects our expected ownership structure immediately following completion of this offering and the acquisition of the Initial Properties. Following the completion of this offering, we will own directly or indirectly 100% of all subsidiaries, including our operating partnership.

Our Tax Status

We intend to elect and qualify to be taxed as a REIT for U.S. federal income tax purposes commencing with our taxable year ending December 31, 2015. Our qualification as a REIT will depend upon our ability to meet, on a continuing basis, through actual investment and operating results, various complex requirements relating to, among other things, the sources of our gross income, the composition and values of our assets, our distribution levels and the diversity of ownership of our capital stock. We believe that we will be organized in conformity with the requirements for qualification as a REIT under the Code and that our intended manner of operation will enable us to meet the requirements for qualification and taxation as a REIT for U.S. federal income tax purposes commencing with our taxable year ending December 31, 2015.

As a REIT, we generally will not be subject to U.S. federal income tax on our taxable income that we distribute currently to our stockholders. Under the Code, REITs are subject to numerous organizational and operational requirements, including a requirement that they distribute each year at least 90% of their REIT taxable income, determined without regard to the deduction for dividends paid and excluding any net capital gains. If we fail to qualify for taxation as a REIT in any taxable year and do not qualify for certain statutory relief provisions, our income for that year will be subject to tax at regular corporate rates, and we would be disqualified from taxation as a REIT for the four taxable years following the year during which we ceased to qualify as a REIT. Even if we qualify as a REIT for U.S. federal income tax purposes, we may still be subject to state and local taxes on our income and assets and to U.S. federal income and excise taxes on our undistributed income. See "Material U.S. Federal Income Tax Considerations."

14

Restrictions on Ownership of Our Shares

In order to help us qualify as a REIT, among other purposes, our charter, subject to certain exceptions, restricts the number of shares of our common stock that a person may beneficially or constructively own. Our charter provides that, subject to certain exceptions, no person may beneficially or constructively own more than 9.8% in value of the outstanding shares of our capital stock and 9.8%, in value or in number of shares, whichever is more restrictive, of the outstanding shares of our common stock. A more complete description of our shares of common stock, including restrictions upon the ownership and transfer thereof, is presented under the caption "Description of Capital Stock" in this prospectus.

Distribution Policy

We intend to pay cash dividends to holders of our common stock. We intend to pay a pro rata dividend with respect to the period commencing on the completion of this offering and ending , 2015 based on $ per share for a full quarter. On an annualized basis, this would be $ per share, or an annual dividend rate of approximately %, based on the mid-point of the price range indicated on the cover page of this prospectus. We intend to maintain our initial dividend rate for the 12-month period following completion of this offering unless actual results of operations, economic conditions or other factors differ materially from the assumptions used in our estimate. We intend to make dividend distributions that will enable us to meet the distribution requirements applicable to REITs and to eliminate or minimize our obligation to pay income and excise taxes. See "Material U.S. Federal Income Tax Considerations—Taxation of Taxable U.S. Stockholders" and "Risk Factors—Risks Related to Our Qualification and Operating as a REIT". We do not intend to reduce the expected dividend per share if the underwriters' option to purchase additional shares is exercised.

Any future distributions will be at the sole discretion of our board of directors, and their form, timing and amount, if any, will depend upon a number of factors, including the revenue we receive from our properties, our operating expenses, interest expense, the ability of our tenants to meet their obligations and unanticipated expenditures, our debt service requirements, our capital expenditures, prohibitions and other limitations under our financing arrangements, our REIT taxable income, the annual REIT distribution requirements, applicable law and such other factors as our board of directors deems relevant. To the extent that our cash available for distribution is less than 90% of our REIT taxable income, we may consider various means to cover any such shortfall, including borrowing under our anticipated credit facility or other loans, selling certain of our assets or using a portion of the net proceeds we receive from this offering or future offerings of equity, equity-related or debt securities or declaring taxable share dividends.

Corporate Information

We were formed as a Maryland corporation on March 28, 2014. Our corporate offices are located at 354 Cool Springs Blvd, Suite 106, Franklin, TN 37067. Our telephone number is 615-771-3052. Our internet website is www.communityhealthcaretrust.com. The information contained on, or accessible through, our website, or any other website, is not incorporated by reference into this prospectus and should not be considered a part of this prospectus.

15

Common stock offered by us |

shares | |

Common stock to be outstanding after this offering and the concurrent private placement |

shares(1) |

|

Use of proceeds |

We estimate that we will receive net proceeds from this offering and the concurrent private placement of approximately $ million (approximately $ million if the underwriters' option to purchase additional shares is exercised in full), after deducting the underwriting discount and estimated offering expenses payable by us. We will contribute the net proceeds from this offering and the concurrent private placement to our operating partnership. Our operating partnership intends to use the net proceeds from this offering and the concurrent private placement as follows: |

|

|

• approximately $114.5 million to acquire the Initial Properties; and |

|

|

• the balance, if any, for general corporate and working capital purposes, including payment of expenses associated with this offering and the acquisition of the Initial Properties and possible future acquisitions. |

|

Proposed NYSE symbol |

"CHCT" |

|

Restrictions on ownership |

Our charter provides that, subject to certain exceptions, no person may beneficially own or constructively own more than 9.8% in value of the outstanding shares of our capital stock and 9.8%, in value or in number of shares, whichever is more restrictive, of the outstanding shares of our common stock. |

|

|

In addition, our charter limits equity participation by "benefit plan investors" so that such participation in any class of our equity securities by such "benefit plan investors" will not be deemed "significant." For such purposes, the terms "benefit plan investors" and "significant" are determined by reference to certain regulations promulgated under the U.S. Department of Labor. See "ERISA Considerations." |

- (1)

- Includes (a) 200,000 shares of common stock that were previously sold to our stockholders in connection with our initial capitalization, (b) shares of common stock (based on the mid-point of the price range indicated on the cover page of this prospectus) to be issued in a $2,000,000 private placement to Mr. Wallace, our Chairman, Chief Executive Officer and President, concurrently with the completion of this offering and (c) an aggregate of shares of common stock to be issued under our 2014 Incentive Plan to members of our management for payment of salaries in stock in lieu of cash shortly after the completion of this offering. Excludes (a) shares of common stock that may be issued by us upon exercise of the underwriters' option to purchase additional shares in full and (b) shares of our common stock available for future issuance under our 2014 Incentive Plan.

16

Summary Historical and Pro Forma Financial and Other Information

The following table sets forth financial information for the Company which is derived from the audited consolidated financial statements included elsewhere in this prospectus. Except for the historical information as and for the year ended December 31, 2014, the information provided below is unaudited. The pro forma information provided in the table below is presented as of and for the year ended December 31, 2014 after giving effect to (a) the sale of the shares of common stock offered hereby (after deducting underwriting discounts and offering expenses payable by us and assuming the underwriters' option to purchase additional shares of common stock is not exercised), (b) the concurrent private placement of $2,000,000 in shares of common stock to Timothy G. Wallace, our Chairman, Chief Executive Officer and President, and (c) the acquisition of the Initial Properties and the entry into the related leases as if such transactions had occurred on January 1, 2014.

The pro forma information incorporates certain assumptions that are included in the Notes to the Unaudited Pro Forma Financial Statements included elsewhere in this prospectus. See "Selected Historical and Pro Forma Financial and Other Data." The pro forma information is for informational purposes and does not purport to represent what the actual financial position or results of operations of the Company would have been as of or for the periods indicated had the transactions been completed as of the date indicated, nor does it purport to represent any future financial position or results of operations.

You should read the following summary historical and pro forma financial information together with the discussion under the caption "Management's Discussion and Analysis of Financial Condition and Results of Operations," and the consolidated financial statements and related notes thereto included elsewhere in this prospectus.

17

| |

At or for the Year Ended December 31, 2014 |

||||||

|---|---|---|---|---|---|---|---|

| |

Historical | As Adjusted for the Offering and Acquisition of Initial Properties |

|||||

Pro forma statement of income data: |

|||||||

Revenues: |

|||||||

Rental income |

$ | — | $ | ||||

Costs and Expenses: |

|||||||

Property operating expenses |

— | ||||||

Depreciation and amortization |

— | ||||||

General and administrative expenses |

— | ||||||

| | | | | | | | |

Total expenses |

— | ||||||

| | | | | | | | |

Net income |

$ | — | $ | ||||

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Net income per share |

$ | — | |||||

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Shares outstanding |

200,000 | ||||||

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Pro forma balance sheet data: |

|||||||

Assets: |

|||||||

Cash and cash equivalents |

$ | 2,000 | $ | ||||

Real estate investments |

— | ||||||

Intangible assets |

— | ||||||

| | | | | | | | |

Total Assets |

$ | 2,000 | $ | ||||

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Liabilities and Stockholders' equity Liabilities: |

|||||||

Other liabilities |

$ | — | $ | ||||

| | | | | | | | |

Total Liabilities |

$ | — | $ | ||||

| | | | | | | | |

Stockholders' equity: |

|||||||

Preferred stock, $0.01 par value 50,000,000 shares authorized; none outstanding |

— | ||||||

Common stock, $0.01 par value 450,000,000 shares authorized; 200,000 issued and outstanding; issued and outstanding, as adjusted |

2,000 | ||||||

Additional paid-in capital |

— | ||||||

| | | | | | | | |

Total stockholders' equity |

2,000 | ||||||

| | | | | | | | |

Total liabilities and stockholders' equity |

$ | 2,000 | $ | ||||

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Other data: |

|||||||

Funds from operations(1) |

$ | — | $ | ||||

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Funds from operations per share(1) |

$ | — | $ | ||||

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

Net operating income(1) |

$ | — | $ | ||||

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

- (1)

- Funds from operations, or FFO, and net operating income, or NOI, are not measures calculated under generally accepted accounting principles, or GAAP, in the U.S. The GAAP measure that we believe to be most directly comparable to FFO and NOI is net income (loss). See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Financial Measures" for the definitions of FFO and NOI and a reconciliation of each measure to net income (loss).

18

An investment in our common stock involves a high degree of risk. In addition to all other information contained in this prospectus, you should carefully consider the following risk factors before purchasing our common stock. The occurrence of any of the following risks could materially and adversely affect our business, prospects, financial condition, results of operations and our ability to make cash distributions to our stockholders, which could cause you to lose all or part of your investment. The risks set forth below represent those risks and uncertainties that we believe are material to our business, financial condition and results of operations, our ability to make distributions to our stockholders and the trading price of our common stock. Some statements in this prospectus, including statements in the following risk factors, constitute forward-looking statements. Please refer to the section captioned "Cautionary Statement Regarding Forward-Looking Statements."

Risks Related to Our Business

We are newly formed and have no operating history; therefore there is no assurance that we will be able to successfully operate our business as a publicly traded company or generate sufficient cash flows to make or sustain distributions to our stockholders.

We are newly formed and have no operating history. In addition, we currently have nominal assets and will commence operations only upon completion of this offering. Further, we will initially only have eight employees, including our executive officers. We are subject to all of the business risks and uncertainties associated with any new business, including the risk that we will not achieve our investment objectives as described in this prospectus and that the value of your investment could decline substantially. Our financial condition and results of operations will depend on many factors, including the availability of acquisition opportunities, readily accessible short and long-term financing, conditions in the financial markets and economic conditions generally. There can be no assurance that we will be able to generate sufficient cash flow over time to pay our operating expenses and make distributions to stockholders. Our limited resources may also materially and adversely impact our ability to successfully operate our Initial Properties or implement our business plan successfully. As a result of our failure to successfully operate our business, implement our investment strategy or generate sufficient revenue to make or sustain distributions to stockholders, the value of your investment could decline significantly or you could lose all or a portion of your investment.

Additionally, we cannot assure you that the past experience of our executive officers will be sufficient to successfully operate our company as a REIT or a listed public company, including the requirements to timely meet disclosure requirements of the SEC. We may be required to revise our control systems and procedures in order to qualify and maintain our qualification as a REIT, to satisfy our periodic and current reporting requirements under applicable regulations of the SEC and to comply with the NYSE listing standards, and this transition could place a significant strain on our management systems, infrastructure and other resources. Failure to operate successfully as a listed public company or maintain our qualification as a REIT would have an adverse effect on our financial condition, results of operations, cash flow and per share trading price of our common stock.

We may be unable to source off-market or lightly marketed deal flow in the future, which may have a material adverse effect on our growth.

A key component of our investment strategy is to acquire additional Non-Urban healthcare properties in off-market or lightly marketed transactions, relying on our officers' relationships with healthcare providers and real estate brokers. All of our Initial Properties were sourced in off-market or lightly marketed transactions based upon the relationship developed by our management team's relationships with healthcare providers. We seek to acquire properties before they are widely marketed by real estate brokers. As we expect to compete with many national, regional and local acquirers of

19

healthcare properties, properties that are acquired in off-market or lightly marketed transactions are typically more attractive to us as a purchaser because of the absence of a formal sales process, which could lead to higher prices. In the formal sales process, our potential acquisition targets may find our competitors to be more attractive because they may have greater resources, may be willing to pay more for the properties or may have a more compatible operating philosophy. In particular, larger REITs, including publicly traded and privately held REITs, private equity investors or institutions investment funds who are targeting healthcare properties may enjoy significant competitive advantages that result from, among other things, a lower cost of capital, enhanced operating efficiencies, more risk tolerance, more personnel and market penetration and familiarity with markets. As such, if we do not have access to off-market or lightly marketed deal flow in the future, our ability to locate and acquire additional properties in Non-Urban markets at attractive prices could be materially and adversely affected which could materially impede our growth, and, as a result, adversely affect our operating results.

Our business could be harmed if key personnel terminate their employment with us or if we are unsuccessful in integrating new personnel into our operations.