Summary of Significant Accounting Policies |

6 Months Ended | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Dec. 31, 2022 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Accounting Policies [Abstract] | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES | NOTE 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

GOING CONCERN

The accompanying consolidated financial statements (“CFS”) were prepared assuming the Company will continue as a going concern, which contemplates continuity of operations, realization of assets, and liquidation of liabilities in the normal course of business. For the six months ended December 31, 2022 and 2021, the Company had a net loss of approximately $2.63 million and $3.12 million. For the three months ended December 31, 2022 and 2021, the Company had a net loss of approximately $1.29 million and $1.68 million. The Company had an accumulated deficit of approximately $21.21 million as of December 31, 2022, and negative cash flow from operating activities of approximately $1.77 million and $3.82 million for the six months ended December 31, 2022 and 2021, respectively. The historical operating results including recurring losses from operations which raise doubt about the Company’s ability to continue as a going concern. Although the range of such recurring operating losses has narrowed in recent years, there can be no assurance the Company will become profitable or obtain necessary financing for its business or that it will be able to continue in business.

If deemed necessary, management could seek to raise additional funds by way of admitting strategic investors or. private or public offerings, or by seeking to obtain loans from banks or others, to support the Company’s research and development (“R&D”), procurement, marketing and daily operation. While management of the Company believes in the viability of its strategy to generate sufficient revenues and its ability to raise additional funds on reasonable terms and conditions, there can be no assurances to that effect. The ability of the Company to continue as a going concern depends upon the Company’s ability to further implement its business plan and generate sufficient revenue and its ability to raise additional funds by way of a public or private offering. There is no assurance that the Company will be able to obtain funds on commercially acceptable terms, if at all. There is also no assurance that the amount of funds the Company might raise will enable the Company to complete its initiatives or attain profitable operations. If the Company is unable to raise additional funding to meet its working capital needs in the future, it may be forced to delay, reduce or cease its operations.

BASIS OF PRESENTATION AND CONSOLIDATION

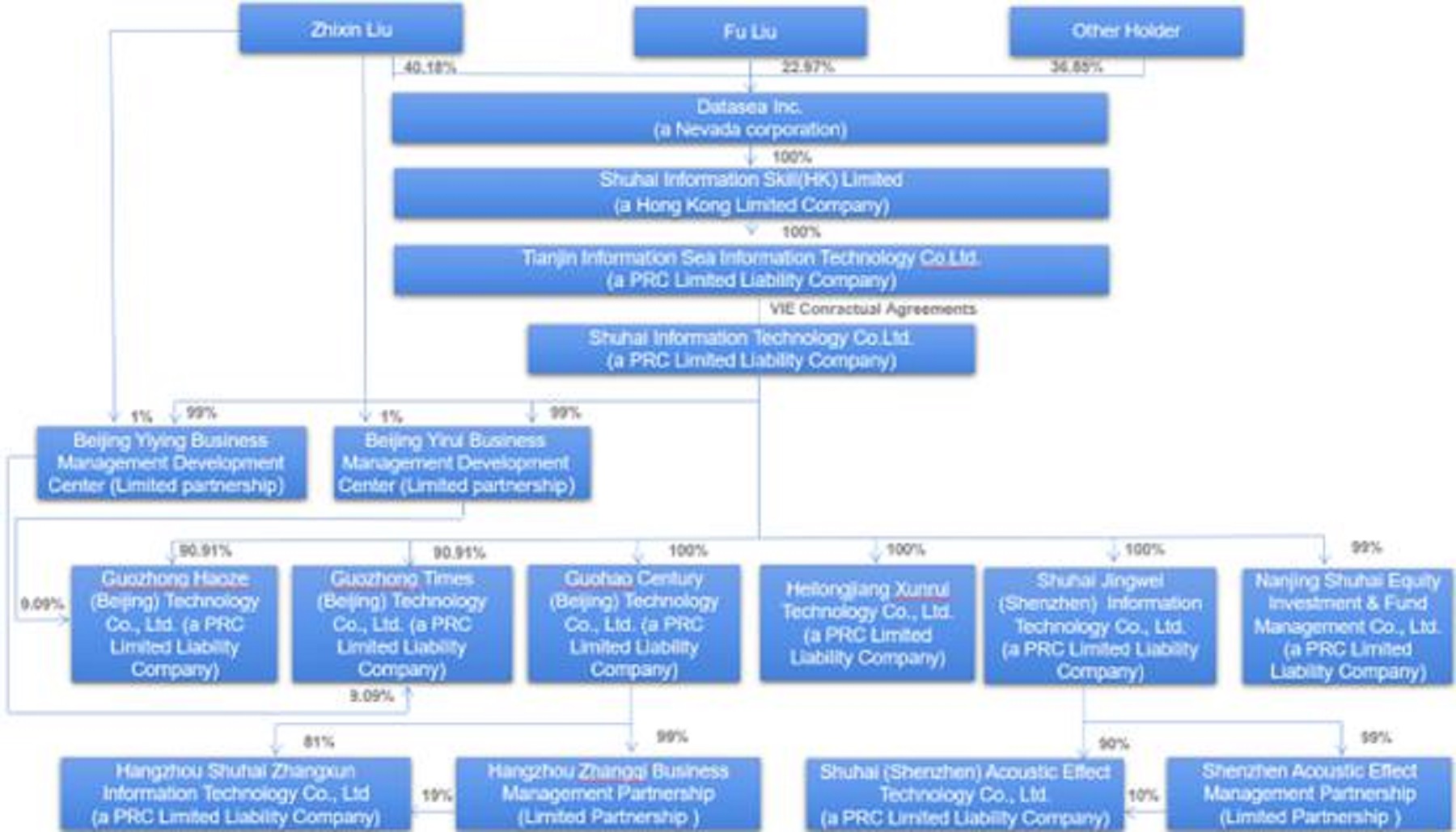

The CFS were prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) and applicable rules and regulations of the SEC regarding CFS. The accompanying CFS include the financial statements of the Company and its 100% owned subsidiaries Shuhai Information Skill (HK) Limited (“Shuhai Skill (HK)”), and Shuhai Information Technology Co., Ltd. (“Tianjin Information”), and its VIE, Shuhai Beijing, and Shuhai Beijing’s 100% owned subsidiaries – Heilongjiang Xunrui Technology Co. Ltd. (“Xunrui”), Guozhong Times (Beijing) Technology Ltd. (“Guozhong Times”), Guohao Century (Beijing) Technology Ltd. (“Guohao Century”), Guozhong Haoze, and Shuhai Jingwei (Shenzhen) Information Technology Co., Ltd. (“Jingwei”), and Guohao Century’s 99% owned subsidiary – Hangzhou Zhangqi Business Management Partnership (“Zhangqi”, a limited partnership) and 99.81% owned subsidiary – Hangzhou Shuhai Zhangxun Information Technology Co., Ltd. (“Zhangxun”) which consisted of 81% ownership from Guohao Century and 19% ownership from Zhangqi, and Shuhai Beijing’s 99% owned subsidiary - Nanjing Shuhai Equity Investment Fund Management Co. Ltd. (“Shuhai Nanjing”). During the year ended June 30, 2022, the Company incorporated two new subsidiaries Shuhai (Shenzhen) Acoustic Effect Technology Co., Ltd (“Shuhai Acoustic”) and Shenzhen Acoustic Effect Management Partnership (“Shenzhen Acoustic MP”). All significant inter-company transactions and balances were eliminated in consolidation. The chart below depicts the corporate structure of the Company as of the date of this report.

VARIABLE INTEREST ENTITY

Pursuant to Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Section 810, “Consolidation” (“ASC 810”), the Company is required to include in its CFS, the financial statements of Shuhai Beijing, its VIE. ASC 810 requires a VIE to be consolidated if the Company is subject to a majority of the risk of loss for the VIE or is entitled to receive a majority of the VIE’s residual returns. A VIE is an entity in which a company, through contractual arrangements, bears the risk of, and enjoys the rewards of such entity, and therefore the Company is the primary beneficiary of such entity.

Under ASC 810, a reporting entity has a controlling financial interest in a VIE, and must consolidate that VIE, if the reporting entity has both of the following characteristics: (a) the power to direct the activities of the VIE that most significantly affect the VIE’s economic performance; and (b) the obligation to absorb losses, or the right to receive benefits, that could potentially be significant to the VIE. The reporting entity’s determination of whether it has this power is not affected by the existence of kick-out rights or participating rights, unless a single enterprise, including its related parties and de - facto agents, have the unilateral ability to exercise those rights. Shuhai Beijing’s actual stockholders do not hold any kick-out rights that affect the consolidation determination.

Through the VIE agreements, Tianjin Information, an indirect subsidiary of Datasea is deemed the primary beneficiary of Shuhai Beijing and its subsidiaries. Accordingly, the results of Shuhai Beijing and its subsidiaries were included in the accompanying CFS. Shuhai Beijing has no assets that are collateral for or restricted solely to settle their obligations. The creditors of Shuhai Beijing do not have recourse to the Company’s general credit.

VIE Agreements

Operation and Intellectual Property Service Agreement – The Operation and Intellectual Property Service Agreement allows Tianjin Information Sea Information Technology Co., Ltd (“WFOE”) to manage and operate Shuhai Beijing and collect an operating fee equal to Shuhai Beijing’s pre-tax income, per month. If Shuhai Beijing suffers a loss and as a result does not have pre-tax income, such loss shall be carried forward to the following month to offset the operating fee to be paid to WFOE if there is pre-tax income of Shuhai Beijing the following month. Furthermore, if Shuhai Beijing cannot pay off its debts, WFOE shall pay off the debt on Shuhai Beijing’s behalf. If Shuhai Beijing’s net assets fall lower than its registered capital balance, WFOE shall provide capital for Shuhai Beijing to make up for the deficit.

Under the terms of the Operation and Intellectual Property Service Agreement, Shuhai Beijing entrusts Tianjin Information to manage its operations, manage and control its assets and financial matters, and provide intellectual property services, purchasing management services, marketing management services and inventory management services to Shuhai Beijing. Shuhai Beijing and its stockholders shall not make any decisions nor direct the activities of Shuhai Beijing without Tianjin Information’s consent.

Stockholders’ Voting Rights Entrustment Agreement – Tianjin Information has entered into a stockholders’ voting rights entrustment agreement (the “Entrustment Agreement”) under which Zhixin Liu and Fu Liu (collectively the “Shuhai Beijing Stockholders”) have vested their voting power in Shuhai Beijing to Tianjin Information or its designee(s). The Entrustment Agreement does not have an expiration date, but the parties can agree in writing to terminate the Entrustment Agreement. Zhixin Liu, is the Chairman of the Board, President, CEO of DataSea and Corporate Secretary, and Fu Liu, a Director of the DataSea (Fu Liu is the father of Zhixin Liu).

Equity Option Agreement – the Shuhai Beijing Stockholders and Tianjin Information entered into an equity option agreement (the “Option Agreement”), pursuant to which the Shuhai Beijing Stockholders have granted Tianjin Information or its designee(s) the irrevocable right and option to acquire all or a portion of Shuhai Beijing Stockholders’ equity interests in Shuhai Beijing for an option price of RMB0.001 for each capital contribution of RMB1.00. Pursuant to the terms of the Option Agreement, Tianjin Information and the Shuhai Beijing Stockholders have agreed to certain restrictive covenants to safeguard the rights of Tianjin Information under the Option Agreement. Tianjin Information agreed to pay RMB1.00 annually to Shuhai Beijing Stockholders to maintain the option rights. Tianjin Information may terminate the Option Agreement upon prior written notice. The Option Agreement is valid for a period of 10 years from the effective date and renewable at Tianjin Information’s option.

Equity Pledge Agreement – Tianjin Information and the Shuhai Beijing Stockholders entered into an equity pledge agreement on October 27, 2015 (the “Equity Pledge Agreement”). The Equity Pledge Agreement serves to guarantee the performance by Shuhai Beijing of its obligations under the Operation and Intellectual Property Service Agreement and the Option Agreement. Pursuant to the Equity Pledge Agreement, Shuhai Beijing Stockholders have agreed to pledge all of their equity interests in Shuhai Beijing to Tianjin Information. Tianjin Information has the right to collect any and all dividends, bonuses and other forms of investment returns paid on the pledged equity interests during the pledge period. Pursuant to the terms of the Equity Pledge Agreement, the Shuhai Beijing Stockholders have agreed to certain restrictive covenants to safeguard the rights of Tianjin Information. Upon an event of default or certain other agreed events under the Operation and Intellectual Property Service Agreement, the Option Agreement and the Equity Pledge Agreement, Tianjin Information may exercise the right to enforce the pledge.

As of this report date, there was no dividends paid from the VIE to the U.S. parent company or the shareholders of the Company. There has been no change in facts and circumstances to consolidate the VIE. The following financial statement amounts and balances of the VIE were included in the accompanying CFS as of December 31, 2022 and June 30, 2022, and for the six and three months ended December 31, 2022 and 2021, respectively.

USE OF ESTIMATES

The preparation of CFS in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting periods. Actual results could differ from those estimates. The significant areas requiring the use of management estimates include, but are not limited to, the estimated useful life and residual value of property, plant and equipment, provision for staff benefits, recognition and measurement of deferred income taxes and the valuation allowance for deferred tax assets. Although these estimates are based on management’s knowledge of current events and actions management may undertake in the future, actual results may ultimately differ from those estimates and such differences may be material to the CFS.

CONTINGENCIES

Certain conditions may exist as of the date the CFS are issued, which may result in a loss to the Company but which will only be resolved when one or more future events occur or fail to occur. The Company’s management and legal counsel assess such contingent liabilities, and such assessment inherently involves an exercise of judgment. In assessing loss contingencies related to legal proceedings that are pending against the Company or unasserted claims that may result in such proceedings, the Company’s legal counsel evaluates the perceived merits of any legal proceedings or unasserted claims as well as the perceived merits of the amount of relief sought or expected to be sought. If the assessment of a contingency indicates that it is probable that a material loss has been incurred and the amount of the liability can be estimated, the estimated liability would be accrued in the Company’s CFS.

If the assessment indicates that a potential material loss contingency is not probable but is reasonably possible, or is probable but cannot be estimated, the nature of the contingent liability, together with an estimate of the range of possible loss if determinable and material, would be disclosed. As of December 31, 2022 and June 30, 2022, the Company has no such contingencies.

CASH AND EQUIVALENTS

Cash and equivalents include cash on hand, demand deposits and short-term cash investments that are highly liquid in nature and have original maturities when purchased of three months or less.

ACCOUNTS RECEIVABLE

The Company’s policy is to maintain an allowance for potential credit losses on accounts receivable. Management reviews the composition of accounts receivable and analyzes historical bad debts, customer concentrations, customer credit worthiness, current economic trends and changes in customer payment patterns to evaluate the adequacy of these reserves. As of December 31, 2022 and June 30, 2022, the Company had a $0 bad debt allowance for accounts receivable.

INVENTORY

Inventory is comprised principally of intelligent temperature measurement face recognition terminal and identity information recognition products, and is valued at the lower of cost or net realizable value. The value of inventory is determined using the first-in, first-out method. The Company periodically estimates an inventory allowance for estimated unmarketable inventories when necessary. Inventory amounts are reported net of such allowances. There were $54,900 and $56,971 allowances for slow-moving and obsolete inventory (mainly for Smart-Student Identification cards) as of December 31, 2022 and June 30, 2022, respectively.

PROPERTY AND EQUIPMENT

Property and equipment are stated at cost, less accumulated depreciation. Major repairs and improvements that significantly extend original useful lives or improve productivity are capitalized and depreciated over the period benefited. Maintenance and repairs are expensed as incurred. When property and equipment are retired or otherwise disposed of, the related cost and accumulated depreciation are removed from the respective accounts, and any gain or loss is included in operations. Depreciation of property and equipment is provided using the straight-line method over estimated useful lives as follows:

Leasehold improvements are depreciated utilizing the straight-line method over the shorter of their estimated useful lives or remaining lease term.

INTANGIBLE ASSETS

Intangible assets with finite lives are amortized using the straight-line method over their estimated period of benefit. Evaluation of the recoverability of intangible assets is made to take into account events or circumstances that warrant revised estimates of useful lives or that indicate that impairment exists. All of the Company’s intangible assets are subject to amortization. No impairment of intangible assets has been identified as of the balance sheet date.

Intangible assets include licenses, certificates, patents and other technology and are amortized over their useful life of three years.

FAIR VALUE (“FV”) OF FINANCIAL INSTRUMENTS

The carrying value of the Company’s short-term financial instruments, such as cash, accounts receivable, prepaid expenses, accounts payable, advance from customers, accrued expenses and other payables approximates their FV due to their short maturities. FASB ASC Topic 825, “Financial Instruments,” requires disclosure of the FV of financial instruments held by the Company. The carrying amounts reported in the balance sheets for current liabilities qualify as financial instruments and are a reasonable estimate of their FV because of the short period of time between the origination of such instruments and their expected realization and the current market rate of interest.

FAIR VALUE MEASUREMENTS AND DISCLOSURES

FASB ASC Topic 820, “Fair Value Measurements,” defines FV, and establishes a three-level valuation hierarchy for disclosures that enhances disclosure requirements for FV measures. The three levels are defined as follows:

As of December 31,2022 and June 30, 2022, the Company did not identify any assets or liabilities required to be presented on the balance sheet at FV on a recurring basis.

IMPAIRMENT OF LONG-LIVED ASSETS

In accordance with FASB ASC 360-10, “Accounting for the Impairment or Disposal of Long-Lived Assets”, long-lived assets such as property and equipment are reviewed for impairment whenever events or changes in circumstances indicate that the carrying value of an asset may not be recoverable, or it is reasonably possible that these assets could become impaired as a result of technological or other changes. The determination of recoverability of assets to be held and used is made by comparing the carrying amount of an asset to future undiscounted cash flows expected to be generated by the asset.

If such assets are considered impaired, the impairment to be recognized is measured as the amount by which the carrying amount of the asset exceeds its FV. FV generally is determined using the asset’s expected future undiscounted cash flows or market value, if readily determinable. Assets to be disposed of are reported at the lower of the carrying amount or FV less cost to sell. For the six and three months ended December 31, 2022 and 2021, there was no impairment loss recognized on long-lived assets.

UNEARNED REVENUE

The Company records payments received in advance from its customers or sales agents for the Company’s products as unearned revenue, mainly consisting of deposits or prepayment for 5G products from the Company’s sales agencies. These orders normally are delivered based upon contract terms and customer demand, and will recognize as revenue when the products are delivered to the end customers.

DEFERRED REVENUE

Deferred revenue consists primarily of local government’s financial support under “2020 Harbin Eyas Plan” to Xunrui for technology innovation of developing the Intelligent Campus Security Management Platform.

LEASES

The Company determines if an arrangement is a lease at inception under FASB ASC Topic 842. Right of Use Assets (“ROU”) and lease liabilities are recognized at commencement date based on the present value of remaining lease payments over the lease term. For this purpose, the Company considers only payments that are fixed and determinable at the time of commencement. As most of its leases do not provide an implicit rate, it uses its incremental borrowing rate based on the information available at commencement date in determining the present value of lease payments. The Company’s incremental borrowing rate is a hypothetical rate based on its understanding of what its credit rating would be. The ROU assets include adjustments for prepayments and accrued lease payments. The ROU asset also includes any lease payments made prior to commencement and is recorded net of any lease incentives received. The Company’s lease terms may include options to extend or terminate the lease when it is reasonably certain that it will exercise such options.

ROU assets are reviewed for impairment when indicators of impairment are present. ROU assets from operating and finance leases are subject to the impairment guidance in ASC 360, Property, Plant, and Equipment, as ROU assets are long-lived nonfinancial assets.

ROU assets are tested for impairment individually or as part of an asset group if the cash flows related to the ROU asset are not independent from the cash flows of other assets and liabilities. An asset group is the unit of accounting for long-lived assets to be held and used, which represents the lowest level for which identifiable cash flows are largely independent of the cash flows of other groups of assets and liabilities. The Company recognized no impairment of ROU assets as of December 31 2022 and June 30, 2022.

Operating leases are included in operating lease ROU and operating lease liabilities (current and non-current), on the consolidated balance sheets. As of December 31, 2022, the net ROU was $316,305 for the operating leases of the Company’s offices in various cities of China and senior officers’ dormitory in Beijing. As of December 31, 2022, total operating lease liabilities were $339,571, which was for the operating leases of the Company’s offices in various cities of China and senior officers’ dormitory in Beijing.

REVENUE RECOGNITION

The Company follows Accounting Standards Codification Topic 606, Revenue from Contracts with Customers (ASC 606).

The core principle underlying FASB ASC 606 is that the Company will recognize revenue to represent the transfer of goods and services to customers in an amount that reflects the consideration to which the Company expects to be entitled in such exchange. This will require the Company to identify contractual performance obligations and determine whether revenue should be recognized at a point in time or over time, based on when control of goods and services transfers to a customer. The Company’s revenue streams are identified when possession of goods and services is transferred to a customer.

FASB ASC Topic 606 requires the use of a new five-step model to recognize revenue from customer contracts. The five-step model requires the Company (i) identify the contract with the customer, (ii) identify the performance obligations in the contract, (iii) determine the transaction price, including variable consideration to the extent that it is probable that a significant future reversal will not occur, (iv) allocate the transaction price to the respective performance obligations in the contract, and (v) recognize revenue when (or as) the Company satisfies each performance obligation.

The Company derives its revenues from product sales and 5G messaging service contracts with its customers, with revenues recognized upon delivery of services and products. Persuasive evidence of an arrangement is demonstrated via product sale contracts and professional service contracts, with performance obligations identified. The transaction price, such as product selling price, and the service price to the customer with corresponding performance obligations are fixed upon acceptance of the agreement. The Company recognizes revenue when it satisfies each performance obligation, the customer receives the products and passes the inspection and when professional service is rendered to the customer, collectability of payment is probable. These revenues are recognized at a point in time after each performance obligations is satisfied. Revenue is recognized net of returns and value-added tax charged to customers.

During the six and three months ended December 31, 2022, the Company’s revenue of $1.45 million and $0.41 million was mainly from 5G messaging services including 5G integrated message marketing cloud platform (“5G IMMCP”), 5G Short Message Services (“SMS”) and 5G value-added service. In addition, during the six months ended December 31, 2022, the Company’s revenue of $42,700 was from Smart Public Broadcasting project which was mainly for the auditory system design, music database management and update, and intelligent broadcasting system customization; and $85,161 from sale of Hailijia series air purification and sterilizers, which is the Company’s foundational acoustic intelligence product.

SEGMENT INFORMATION

FASB ASC Topic 280, “Segment Reporting,” requires use of the “management approach” model for segment reporting. The management approach model is based on the method a company’s management organizes segments within the company for making operating decisions and assessing performance. Reportable segments are based on products and services, geography, legal structure, management structure, or any other manners in which management disaggregates a company. Management determining the Company’s current operations constitutes a single reportable segment in accordance with ASC 280. The Company’s only business and industry segment is high technology and advanced information systems (“TAIS”). TAIS include smart city solutions that meet the security needs of residential communities, schools and commercial enterprises, and 5G messaging services including 5G SMS, 5G MMCP and 5G multi-media video messaging.

All of the Company’s customers are in the PRC and all revenues for the six and three months ended December 31, 2022 and 2021 were generated from the PRC. All identifiable assets of the Company are located in the PRC. Accordingly, no geographical segments are presented.

INCOME TAXES

The Company uses the asset and liability method of accounting for income taxes in accordance with FASB ASC Topic 740, “Income Taxes.” Under this method, income tax expense is recognized for the amount of: (i) taxes payable or refundable for the current period and (ii) deferred tax consequences of temporary differences resulting from matters that have been recognized in an entity’s financial statements or tax returns. Deferred tax assets also include the prior years’ net operating losses carried forward. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. The effect on deferred tax assets and liabilities of a change in tax rates is recognized in the results of operations in the period that includes the enactment date. A valuation allowance is provided to reduce the deferred tax assets reported if based on the weight of the available positive and negative evidence, it is more likely than not some portion or all of the deferred tax assets will not be realized.

The Company follows FASB ASC Topic 740, which prescribes a more-likely-than-not threshold for financial statement recognition and measurement of a tax position taken or expected to be taken in a tax return. FASB ASC Topic 740 also provides guidance on recognition of income tax assets and liabilities, classification of current and deferred income tax assets and liabilities, accounting for interest and penalties associated with tax positions, accounting for income taxes in interim periods, and income tax disclosures.

Under the provisions of FASB ASC Topic 740, when tax returns are filed, it is likely some positions taken would be sustained upon examination by the taxing authorities, while others are subject to uncertainty about the merits of the position taken or the amount of the position that would be ultimately sustained. The benefit of a tax position is recognized in the financial statements in the period during which, based on all available evidence, management believes it is more likely than not that the position will be sustained upon examination, including the resolution of appeals or litigation processes, if any. Tax positions taken are not offset or aggregated with other positions. Tax positions that meet the more-likely-than-not recognition threshold are measured as the largest amount of tax benefit that is more than 50 percent likely of being realized upon settlement with the applicable taxing authority. The portion of the benefits associated with tax positions taken that exceeds the amount measured as described above is reflected as a liability for unrecognized tax benefits in the accompanying balance sheets along with any associated interest and penalties that would be payable to the taxing authorities upon examination. Interest associated with unrecognized tax benefits is classified as interest expense and penalties are classified in selling, general and administrative expenses in the statement of income. As of December 31, 2022, the Company had no unrecognized tax benefits and no charges during the six and three months ended December 31, 2022, and accordingly, the Company did not recognize any interest or penalties related to unrecognized tax benefits. There was no accrual for uncertain tax positions as of December 31, 2022. The Company files a U.S. and PRC income tax return. With few exceptions, the Company’s U.S. income tax returns filed for the years ending on June 30, 2018 and thereafter are subject to examination by the relevant taxing authorities; the Company uses calendar year-end for its PRC income tax return filing, PRC income tax returns filed for the years ending on December 31, 2017 and thereafter are subject to examination by the relevant taxing authorities.

RESEARCH AND DEVELOPMENT EXPENSES

Research and development expenses are expensed in the period when incurred. These costs primarily consist of cost of materials used, salaries paid for the Company’s development department, and fees paid to third parties.

NONCONTROLLING INTERESTS

The Company follows FASB ASC Topic 810, “Consolidation,” governing the accounting for and reporting of noncontrolling interests (“NCIs”) in partially owned consolidated subsidiaries and the loss of control of subsidiaries. Certain provisions of this standard indicate, among other things, that NCI (previously referred to as minority interests) be treated as a separate component of equity, not as a liability, that increases and decreases in the parent’s ownership interest that leave control intact be treated as equity transactions rather than as step acquisitions or dilution gains or losses, and that losses of a partially-owned consolidated subsidiary be allocated to non-controlling interests even when such allocation might result in a deficit balance.

The net income (loss) attributed to NCI was separately designated in the accompanying statements of operations and comprehensive income (loss). Losses attributable to NCI in a subsidiary may exceed a non-controlling interest’s interests in the subsidiary’s equity. The excess attributable to NCIs is attributed to those interests. NCIs shall continue to be attributed their share of losses even if that attribution results in a deficit NCI balance.

As of December 31, 2022, Zhangxun was 0.19% owned by noncontrolling interest, Zhangqi was 1% owned by noncontrolling interest, and Shuhai Nanjing was 1% owned by noncontrolling interest, Shenzhen Acoustic MP was 1% owned by noncontrolling interest, Shuhai Shenzhen Acoustic was 30.1% owned by noncontrolling interest, Guozhong Times was 0.091% owned by noncontrolling interest, Guozhong Haoze was 0.091% owned by noncontrolling interest. During the six months ended December 31, 2022 and 2021, the Company had loss of $216,719 and $258,281 attributable to the noncontrolling interest, respectively. During the three months ended December 31, 2022 and 2021, the Company had loss of $120,095 and $146,181 attributable to the noncontrolling interest, respectively.

CONCENTRATION OF CREDIT RISK

The Company maintains cash in accounts with state-owned banks within the PRC. Cash in state-owned banks less than RMB500,000 ($76,000) is covered by insurance. Should any institution holding the Company’s cash become insolvent, or if the Company is unable to withdraw funds for any reason, the Company could lose the cash on deposit with that institution. The Company has not experienced any losses in such accounts and believes it is not exposed to any risks on its cash in these bank accounts. Cash denominated in RMB with a U.S. dollar equivalent of $37,413 and $153,607 as of December 31, 2022 and June 30, 2022, respectively, was held in accounts at financial institutions located in the PRC‚ which is not freely convertible into foreign currencies.

Cash held in accounts at U.S. financial institutions is insured by the Federal Deposit Insurance Corporation or other programs subject to certain limitations up to $250,000 per depositor. Cash was maintained at financial institutions in Hong Kong, and was insured by the Hong Kong Deposit Protection Board up to a limit of HK $500,000 ($64,000). As of December 31, 2022, the cash balance of $5,808 was maintained at financial institutions in Hong Kong. The Company, its subsidiaries and VIE have not experienced any losses in such accounts and do not believe the cash is exposed to any significant risk.

FOREIGN CURRENCY TRANSLATION AND COMPREHENSIVE INCOME (LOSS)

The accounts of the Company’s Chinese entities are maintained in RMB and the accounts of the U.S. parent company are maintained in United States dollar (“USD”). The accounts of the Chinese entities were translated into USD in accordance with FASB ASC Topic 830 “Foreign Currency Matters.” All assets and liabilities were translated at the exchange rate on the balance sheet date; stockholders’ equity is translated at historical rates and the statements of operations and cash flows are translated at the weighted average exchange rate for the period. The resulting translation adjustments are reported under other comprehensive income (loss) in accordance with FASB ASC Topic 220, “Comprehensive Income.” Gains and losses resulting from foreign currency transactions are reflected in the statements of operations.

The Company follows FASB ASC Topic 220-10, “Comprehensive Income (loss).” Comprehensive income (loss) comprises net income (loss) and all changes to the statements of changes in stockholders’ equity, except those due to investments by stockholders, changes in additional paid-in capital and distributions to stockholders.

The exchange rates used to translate amounts in RMB to USD for the purposes of preparing the CFS were as follows:

BASIC AND DILUTED EARNINGS (LOSS) PER SHARE (EPS)

Basic EPS is computed by dividing income available to common shareholders by the weighted average number of common shares outstanding for the period. Diluted EPS is computed similarly, except that the denominator is increased to include the number of additional common shares that would have been outstanding if the potential common shares had been issued and if the additional common shares were dilutive. Diluted EPS is based on the assumption that all dilutive convertible shares and stock options were converted or exercised. Dilution is computed by applying the treasury stock method. Under this method, options and warrants are assumed to have been exercised at the beginning of the period (or at the time of issuance, if later), and as if funds obtained thereby were used to purchase common stock at the average market price during the period. For the six and three months ended December 31, 2022 and 2021, the Company’s basic and diluted loss per share are the same as a result of the Company’s net loss. 1,319,953 warrants were anti-dilutive for each of the six and three months ended December 31, 2022 and 2021, respectively.

STATEMENT OF CASH FLOWS

In accordance with FASB ASC Topic 230, “Statement of Cash Flows,” cash flows from the Company’s operations are calculated based upon the local currencies. As a result, amounts shown on the statement of cash flows may not necessarily agree with changes in the corresponding asset and liability on the balance sheet.

RECENT ACCOUNTING PRONOUNCEMENTS

In June 2016, the FASB issued ASU No. 2016-13, Financial Instruments-Credit Losses (Topic 326), which requires entities to measure all expected credit losses for financial assets held at the reporting date based on historical experience, current conditions, and reasonable and supportable forecasts. This replaces the existing incurred loss model and is applicable to the measurement of credit losses on financial assets measured at amortized cost. This guidance is effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2022. Early application will be permitted for all entities for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2018. The Company is currently evaluating the impact that the standard will have on its CFS.

In August 2020, the FASB issued ASU 2020-06, Debt — Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging—Contracts in Entity’s Own Equity (Subtopic 815-40): Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity (“ASU 2020-06”). ASU 2020-06 simplifies the accounting for convertible debt by eliminating the beneficial conversion and cash conversion accounting models. Upon adoption of ASU 2020-06, convertible debt, unless issued with a substantial premium or an embedded conversion feature that is not clearly and closely related to the host contract, will no longer be allocated between debt and equity components. This modification will reduce the issue discount and result in less non-cash interest expense in financial statements. ASU 2020-06 also updates the earnings per share calculation and requires entities to assume share settlement when the convertible debt can be settled in cash or shares. For contracts in an entity’s own equity, the type of contracts primarily affected by ASU 2020-06 are freestanding and embedded features that are accounted for as derivatives under the current guidance due to a failure to meet the settlement assessment by removing the requirements to (i) consider whether the contract will be settled in registered shares, (ii) consider whether collateral is required to be posted, and (iii) assess shareholder rights. ASU 2020-06 is effective for fiscal years beginning after December 15, 2023. Early adoption is permitted, but no earlier than fiscal years beginning after December 15, 2020, and only if adopted as of the beginning of such fiscal year. The Company adopted ASU 2020-06 effective July 1, 2021. The adoption of ASU 2020-06 did not have any impact on the Company’s CFS presentation or disclosures.

In May 2021, the FASB issued ASU 2021-04, Earnings Per Share (Topic 260), Debt — Modifications and Extinguishments (Subtopic 470-50), Compensation — Stock Compensation (Topic 718), and Derivatives and Hedging — Contracts in Entity’s Own Equity (Subtopic 815-40): Issuer’s Accounting for Certain Modifications or Exchanges of Freestanding Equity-Classified Written Call Options (“ASU 2021-04”). ASU 2021-04 provides guidance as to how an issuer should account for a modification of the terms or conditions or an exchange of a freestanding equity-classified written call option (i.e., a warrant) that remains classified after modification or exchange as an exchange of the original instrument for a new instrument. An issuer should measure the effect of a modification or exchange as the difference between the fair value of the modified or exchanged warrant and the fair value of that warrant immediately before modification or exchange and then apply a recognition model that comprises four categories of transactions and the corresponding accounting treatment for each category (equity issuance, debt origination, debt modification, and modifications unrelated to equity issuance and debt origination or modification). ASU 2021-04 is effective for all entities for fiscal years beginning after December 15, 2021, including interim periods within those fiscal years. An entity should apply the guidance provided in ASU 2021-04 prospectively to modifications or exchanges occurring on or after the effective date. Early adoption is permitted for all entities, including adoption in an interim period. If an entity elects to early adopt ASU 2021-04 in an interim period, the guidance should be applied as of the beginning of the fiscal year that includes that interim period. The adoption of ASU 2021-04 is not expected to have any impact on the Company’s CFS presentation or disclosures.

The Company’s management does not believe that any other recently issued, but not yet effective, authoritative guidance, if currently adopted, would have a material impact on the Company’s financial statement presentation or disclosures. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||