UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________________________________________________________________

FORM 10-K

____________________________________________________________________

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2023

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from ________ to ________

Commission file number 001-38156

____________________________________

(Exact name of registrant as specified in its charter)

_______________________________________________________________________

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

(Address of principal executive offices) (Zip Code)

(212 ) 601-4700

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer | o | x | |||||||||

| Non-accelerated Filer | o | Smaller Reporting Company | |||||||||

| Emerging Growth Company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. x

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

As of June 30, 2023, the last business day of the Registrant’s most recently completed second fiscal quarter, the aggregate market value of the Registrant’s common stock held by non-affiliates of the Registrant was $521.8 million based on the closing sales price of the Registrant’s common stock as reported on the New York Stock Exchange. For purposes of this computation, all officers, directors and 10% beneficial owners of the Registrant’s common stock of which the Registrant is aware are deemed to be affiliates. Such determination should not be deemed to be an admission that such officers, directors or 10% beneficial owners are, in fact, affiliates of the Registrant.

As of February 16, 2024, there were 77,868,565 shares of the registrant’s common stock, $0.001 par value per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this Annual Report on Form 10-K incorporates information by reference from the Registrant’s definitive proxy statement with respect to its 2024 annual meeting of stockholders to be filed with the Securities and Exchange Commission within 120 days after the end of the Registrant’s fiscal year.

Table of Contents

| Page | ||||||||

| PART I | ||||||||

| Item 1C. | ||||||||

| PART II | ||||||||

| PART III | ||||||||

| PART IV | ||||||||

Certain Terms

In this annual report, except where the context requires otherwise:

•“Company,” “we,” “us,” and “our” refer to TPG RE Finance Trust, Inc., a Maryland corporation and, where applicable, its subsidiaries.

•“Manager” refers to our external manager, TPG RE Finance Trust Management, L.P., a Delaware limited partnership.

•“TPG” refers to TPG Inc., a Delaware corporation, and its affiliates.

•“TPG Fund” refers to any partnership or other pooled investment vehicle, separate account, fund-of-one or any similar arrangement or investment program sponsored, advised or managed (including on a subadvisory basis) by TPG, whether currently in existence or subsequently established (in each case, including any related alternative investment vehicle, parallel or feeder investment vehicle, co-investment vehicle and any entity formed in connection therewith, including any entity formed for investments by TPG and its affiliates in any such vehicle, whether invested as a limited partner or through general partner investments).

1

PART I

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), which reflect our current views with respect to, among other things, our operations and financial performance. You can identify these forward-looking statements by the use of words such as “outlook,” “believe,” “expect,” “potential,” “continue,” “may,” “should,” “seek,” “approximately,” “predict,” “intend,” “will,” “plan,” “estimate,” “anticipate,” the negative version of these words, other comparable words or other statements that do not relate strictly to historical or factual matters. By their nature, forward-looking statements speak only as of the date they are made, are not statements of historical fact or guarantees of future performance and are subject to risks, uncertainties, assumptions or changes in circumstances that are difficult to predict or quantify. Our expectations, beliefs and projections are expressed in good faith, and we believe there is a reasonable basis for them. However, there can be no assurance that management’s expectations, beliefs and projections will occur or be achieved, and actual results may vary materially from what is expressed in or indicated by the forward-looking statements.

There are a number of risks, uncertainties and other important factors that could cause our actual results to differ materially from the forward-looking statements contained in this Form 10-K. Such risks and uncertainties include, but are not limited to, the following:

•the general political, economic, regulatory, competitive and other conditions in the markets in which we invest;

•the level and volatility of prevailing interest rates and credit spreads;

•adverse changes in the real estate and real estate capital markets;

•general volatility of the securities markets in which we participate;

•changes in our business, investment strategies or target assets;

•difficulty in obtaining financing or raising capital;

•an inability to borrow incremental amounts or an obligation to repay amounts under our financing arrangements;

•reductions in the yield on our investments and increases in the cost of our financing;

•events giving rise to increases in our current expected credit loss reserve;

•adverse legislative or regulatory developments, including with respect to tax laws, securities laws and the laws governing financing and lending institutions;

•acts of God such as hurricanes, floods, earthquakes, wildfires, mudslides, volcanic eruptions, and other natural disasters, acts of war and/or terrorism and other events that may cause unanticipated and uninsured performance declines and/or losses to us or the owners and operators of the real estate securing our investments;

•global economic trends and economic conditions, including heightened inflation, slower growth or recession, changes to fiscal and monetary policy, higher interest rates, stress to the commercial banking systems of the U.S. and Western Europe, labor shortages, currency fluctuations and challenges in global supply chains;

•the failure of any banks with which we and/or our borrowers have a commercial relationship could adversely affect, among other things, our borrower's ability to access deposits or obtaining financing on favorable terms or at all;

•higher interest rates imposed by the Federal Reserve may lead to a decrease in prepayment speeds and an increase in the number of borrowers who exercise extension options, which could extend beyond the term of certain secured financing agreements we use to finance our loan investments;

•reduced demand for office space, including as a result of the COVID-19 pandemic and/or hybrid work schedules which allow work from remote locations other than the employer’s office premises;

•changes in the availability of attractive loan and other investment opportunities, whether they are due to competition, regulation or otherwise;

•deterioration in the performance of properties securing our investments that may cause deterioration in the performance of our investments, adversely impact certain of our financing arrangements and our liquidity, and potentially expose us to principal losses on our investments;

•defaults by borrowers in paying debt service or principal on outstanding indebtedness;

•the adequacy of collateral securing our investments and declines in the fair value of our investments;

•adverse developments in the availability of desirable investment opportunities, whether due to competition, regulation or otherwise;

2

•difficulty or delays in redeploying the proceeds from repayments of our existing investments;

•increased competition from entities engaged in mortgage lending and/or investing in our target assets;

•difficulty in successfully managing our growth, including integrating new assets into our existing systems;

•the cost of operating our platform, including, but not limited to, the cost of operating a real estate investment platform and the cost of operating as a publicly traded company;

•the availability of qualified personnel and our relationship with our Manager;

•conflicts with TPG and its affiliates, including our Manager, the personnel of TPG providing services to us, including our officers, and certain funds managed by TPG;

•our ability to maintain our qualification as a real estate investment trust (“REIT”) for U.S. federal income tax purposes;

•our ability to maintain our exemption or exclusion from registration under the Investment Company Act of 1940, as amended (the “Investment Company Act”); and

•authoritative U.S. generally accepted accounting principles (or “GAAP”) or policy changes from standard-setting bodies such as the Financial Accounting Standards Board (“FASB”), the Securities and Exchange Commission (“SEC”), the Internal Revenue Service (“IRS”), the New York Stock Exchange (“NYSE”) and other authorities that we are subject to, as well as their counterparts in any foreign jurisdictions where we might do business.

There may be other risks, uncertainties or factors that may cause our actual results to differ materially from the forward-looking statements contained in this Form 10-K, including risks, uncertainties, and factors disclosed in Item 1A – “Risk Factors” and in Item 7 – “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” You should evaluate all forward-looking statements made in this Form 10-K in the context of these risks, uncertainties and other factors.

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance, or achievements. We caution you that the risks, uncertainties and other factors referenced above may not contain all of the risks, uncertainties and other factors that are important to you. In addition, we cannot assure you that we will realize the results, benefits or developments that we expect or anticipate or, even if substantially realized, that they will result in the consequences or affect us or our business in the way expected. All forward-looking statements in this Form 10-K apply only as of the date made and are expressly qualified in their entirety by the cautionary statements included in this Form 10-K and in other filings we make with the SEC. We undertake no obligation to publicly update or revise any forward-looking statements to reflect subsequent events or circumstances, except as required by law.

3

Item 1. Business.

Company and Organization

TPG RE Finance Trust, Inc. is a commercial real estate finance company externally managed by TPG RE Finance Trust Management, L.P., an affiliate of TPG. Our principal executive offices are located at 888 Seventh Avenue, 35th Floor, New York, New York 10106. We are organized as a holding company and conduct our operations primarily through TPG RE Finance Trust Holdco, LLC (“Holdco”), a wholly owned Delaware limited liability company, and Holdco’s direct and indirect subsidiaries. We conduct our operations as a REIT for U.S. federal income tax purposes. We generally will not be subject to U.S. federal income taxes on our REIT taxable income to the extent that we annually distribute all of our REIT taxable income to stockholders and maintain our qualification as a REIT. We also operate our business in a manner that permits us to maintain an exclusion or exemption from registration under the Investment Company Act.

We operate our business as one segment. Our principal business activity is to directly originate and acquire a diversified portfolio of commercial real estate-related assets, consisting primarily of first mortgage loans and senior participation interests in first mortgage loans secured by institutional-quality properties in primary and select secondary markets in the United States.

Manager

We are externally managed by our Manager, TPG RE Finance Trust Management, L.P., an affiliate of TPG. TPG is a leading global, alternative asset management firm, founded in San Francisco in 1992, with $222 billion of assets under management (as of December 31, 2023) and investment and operational teams around the world. TPG invests across a broadly diversified set of strategies, including private equity, impact, credit, real estate, and market solutions. Our Manager manages our investments and our day-to-day business and affairs in conformity with our investment guidelines and other policies that are approved and monitored by our board of directors. Our Manager is responsible for, among other matters, the selection, origination or purchase and sale of our portfolio investments, our financing activities and providing us with investment advisory services. Our Manager is also responsible for our day-to-day operations and performs (or causes to be performed) such services and activities relating to our investments and business and affairs as may be appropriate. Our investment decisions are approved by an investment committee of our Manager that is comprised of senior investment professionals of TPG, including senior investment professionals of TPG’s real estate equity group and TPG’s executive committee.

TPG Real Estate, TPG’s real estate platform, includes TPG Real Estate Partners and TPG Thematic Advantage Core-Plus, TPG’s real estate equity investment vehicles, and us, TPG's public real estate debt investment platform. Collectively, TPG Real Estate managed more than $17.9 billion in real estate and real estate-related assets as of December 31, 2023. In the fourth quarter, TPG Real Estate held an initial closing of TPG Real Estate Credit Opportunities, and two associated funds-of-one (together the "TRECO Funds"). The TRECO Funds are private credit vehicles, with investment mandates focused on opportunistic real estate credit investing. TPG Real Estate’s teams work across TPG offices in New York, San Francisco and London, and representative offices in Atlanta and Chicago, and have 18 and 43 employees, respectively, between TPG’s real estate debt investment platform and TPG’s real estate equity platform.

Our chief executive officer, president and chief financial officer are senior TPG Real Estate professionals. None of our executive officers, our Manager, or other personnel supplied to us by our Manager is obligated to dedicate any specific amount of time to our business. Our Manager is subject to the supervision and oversight of our board of directors and has only such functions and authority as our board of directors delegates to it. Pursuant to a management agreement between our Manager and us (our “Management Agreement”), our Manager is entitled to receive a base management fee, an incentive fee, and certain expense reimbursements.

See Note 10 to our Consolidated Financial Statements included in this Form 10-K for more detail on the terms of the Management Agreement.

Investment Strategy

Our investment objective is to directly originate and acquire a diversified portfolio of commercial real estate-related credit assets, consisting primarily of first mortgage loans and senior participation interests in first mortgage loans secured by institutional-quality properties in primary and select secondary markets in the United States. We invest primarily in commercial mortgage loans and other commercial real estate-related debt instruments, including, but not limited to, the following:

•Commercial Mortgage Loans. We focus primarily on directly originating and selectively acquiring first mortgage loans. These loans are secured by high quality commercial real estate properties undergoing some form of transition and value creation, such as retenanting, refurbishment or other form of repositioning, may vary in duration, predominantly bear interest at a floating rate, may provide for regularly scheduled principal amortization and typically require a balloon payment of principal at maturity. These investments may encompass a whole commercial mortgage loan or may include a pari passu participation within a commercial mortgage loan.

4

•Other Commercial Real Estate-Related Debt Instruments. From time to time we may invest in other commercial real estate-related debt instruments, subject to maintaining our qualification as a REIT for U.S. federal income tax purposes and exclusion or exemption from regulation under the Investment Company Act, including, but not limited to, subordinate mortgage interests, mezzanine loans, secured real estate securities, note financing, preferred equity and miscellaneous debt instruments. We have in the past invested in short-term, primarily investment grade collateralized loan obligations (“CRE CLOs”) and commercial mortgage-backed securities (“CMBS”).

The commercial mortgage loans we target for origination or acquisition typically include, but are not limited to, the following characteristics:

•Unpaid principal balance greater than $35.0 million;

•As-is loan-to value (“LTV”) of less than 80% with respect to individual properties;

•Floating rate loans tied to the one-month U.S. dollar-denominated Secured Overnight Financing Rate (“Term SOFR”) and credit spreads of 300 to 600 basis points over the benchmark interest rate;

•Secured by properties that are: (1) primarily in the multifamily, life science, mixed-use, hospitality, self storage, and industrial real estate sectors; (2) expected to reach stabilization within 24 months of the origination or acquisition date; and (3) located in primary and select secondary markets in the U.S. that we believe have attractive economic conditions and commercial real estate fundamentals, such as growth in employment and household formation, medical infrastructure, universities and attractive cultural and lifestyle amenities; and

•Well-capitalized sponsors with experience in particular real estate sectors and geographic markets.

We believe that our current investment strategy provides significant opportunities to our stockholders for attractive risk-adjusted returns over time through cash distributions and capital appreciation. However, to capitalize on investment opportunities and returns at different points in the economic and real estate investment cycle, we may modify, expand or change our investment strategy by targeting other assets with debt characteristics, such as subordinate mortgage loans, mezzanine loans, preferred equity, real estate securities and note financings, in each case subject to any duties to offer or other contractual obligations to other funds managed by TPG. We may also target assets with equity-linked characteristics, or forms of direct equity ownership of commercial real estate properties, in either case subject to any duties to offer or other contractual obligations to other funds managed by TPG. We believe that the flexibility of our investment strategy, supported by our Manager’s significant commercial real estate experience and the extensive resources of TPG and TPG Real Estate, will allow us to take advantage of continued changing market conditions to maximize risk-adjusted returns to our stockholders.

We believe that the diversification of our investment portfolio, our ability to actively manage those investments, and the flexibility of our strategy positions us to generate attractive returns for our stockholders in a variety of market conditions over the long term.

Investment Portfolio

Our interest-earning assets are comprised almost entirely of a portfolio of floating rate, first mortgage loans and contiguous mezzanine loans. As of December 31, 2023, our balance sheet loan portfolio consisted of 53 loans held for investment totaling $3.7 billion of commitments and an unpaid principal balance of $3.5 billion, with a weighted average credit spread of 3.7%.

As of December 31, 2023, our balance sheet loan portfolio had a weighted average all-in yield of 9.3% and a weighted average term to extended maturity (assuming all extension options are exercised by our borrowers) of 2.6 years. As of December 31, 2023, 100.0% of our loan commitments were floating rate, of which 100.0% were first mortgage loans or, in one instance, a first mortgage loan and contiguous mezzanine loan both owned by us. As of December 31, 2023, our balance sheet loan portfolio had a weighted average LTV of 67.3% and, subject to the satisfaction of certain borrower milestones, $183.3 million of unfunded loan commitments.

We may hold real estate owned (“REO”) as a result of taking title to a loan's collateral. As of December 31, 2023, we owned four office properties and one multifamily property with an aggregate carrying value of $199.8 million.

5

Loan Portfolio

The following table details overall statistics for our loans held for investment portfolio as of December 31, 2023 (dollars in thousands):

| Balance sheet portfolio | Total loan exposure(1) | |||||||||||||

| Number of loans | 53 | 53 | ||||||||||||

| Floating rate loans | 100.0 | % | 100.0 | % | ||||||||||

Total loan commitment(1) | $ | 3,666,173 | $ | 3,666,173 | ||||||||||

Unpaid principal balance(2) | $ | 3,484,052 | $ | 3,484,052 | ||||||||||

Unfunded loan commitments(3) | $ | 183,293 | $ | 183,293 | ||||||||||

| Amortized cost | $ | 3,476,776 | $ | 3,476,776 | ||||||||||

Weighted average credit spread(4) | 3.7 | % | 3.7 | % | ||||||||||

Weighted average all-in yield(4) | 9.3 | % | 9.3 | % | ||||||||||

Weighted average term to extended maturity (in years)(5) | 2.6 | 2.6 | ||||||||||||

Weighted average LTV(6) | 67.3 | % | 67.3 | % | ||||||||||

_________________________________

(1)In certain instances, we create structural leverage through the co-origination or non-recourse syndication of a senior loan interest to a third-party. In either case, the senior mortgage loan (i.e., the non-consolidated senior interest) is not included on our balance sheet. When we create structural leverage through the co-origination or non-recourse syndication of a senior loan interest to a third-party, we retain on our balance sheet a mezzanine loan. Total loan exposure encompasses the entire loan portfolio we originated, acquired and financed. We did not have any non-consolidated senior interests as of December 31, 2023. See Item 7 – “Management’s Discussion and Analysis of Financial Condition and Results of Operations–Investment Portfolio Financing–Non-Consolidated Senior Interests” in this Form 10-K for additional information.

(2)Unpaid principal balance includes PIK interest of $1.2 million as of December 31, 2023.

(3)Unfunded loan commitments may be funded over the term of each loan, subject in certain cases to an expiration date or a force-funding date, primarily to finance property improvements or lease-related expenditures by our borrowers, and to finance operating deficits during renovation and lease-up.

(4)As of December 31, 2023, all of our loans were indexed to Term SOFR. In addition to credit spread, all-in yield includes the amortization of deferred origination fees, purchase price premium and discount, and accrual of both extension and exit fees. All-in yield for the total portfolio assumes Term SOFR as of December 31, 2023 for weighted average calculations.

(5)Extended maturity assumes all extension options are exercised by our borrowers; provided, however, that our loans may be repaid prior to such date. As of December 31, 2023, based on the unpaid principal balance of our total loan exposure, 8.4% of our loans were subject to yield maintenance or other prepayment restrictions and 91.6% were open to repayment by the borrower without penalty.

(6)Except for construction loans, LTV is calculated for loan originations and existing loans as the total outstanding principal balance of the loan or participation interest in a loan (plus any financing that is pari passu with or senior to such loan or participation interest) as of December 31, 2023, divided by the as-is appraised value of our collateral at the time of origination or acquisition of such loan or participation interest. For construction loans only, LTV is calculated as the total commitment amount of the loan divided by the as-stabilized value of the real estate securing the loan. The as-is or as-stabilized (as applicable) value reflects our Manager’s estimates, at the time of origination or acquisition of the loan or participation interest in a loan, of the real estate value underlying such loan or participation interest determined in accordance with our Manager’s underwriting standards and consistent with third-party appraisals obtained by our Manager.

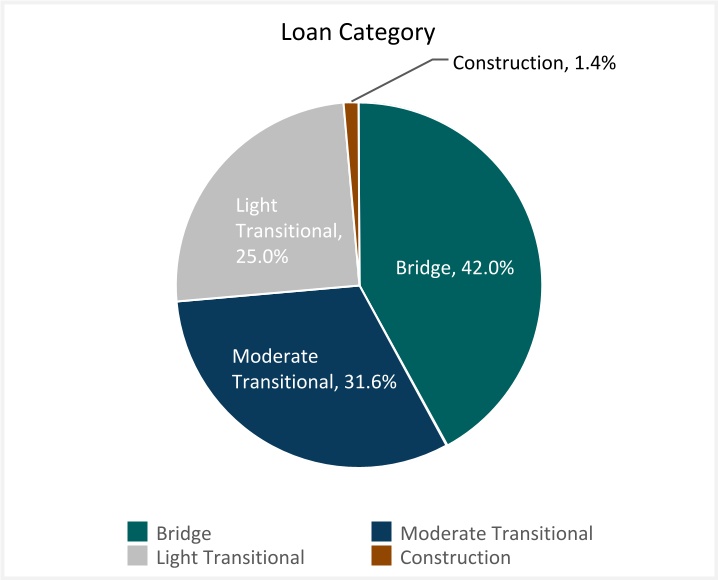

Our loans held for investment consist of Bridge, Light Transitional, Moderate Transitional and Construction floating rate loans that are secured by a diverse portfolio of properties located in primary and select secondary markets in the U.S. These loan categories are utilized by us to classify, define, and assess our loan investments. Generally, loan investments are classified based on a percentage of deferred fundings of the total loan commitment. Bridge loans limit deferred fundings to less than 10%, while Light and Moderate Transitional loans limit deferred fundings to 10% to 20%, and over 20%, respectively. Construction loans involve ground-up construction and deferred fundings often represent the majority of the loan commitment amount. Deferred fundings are commonly conditioned on the borrower’s satisfaction of certain collateral performance tests, the completion of specified property improvements, or both.

6

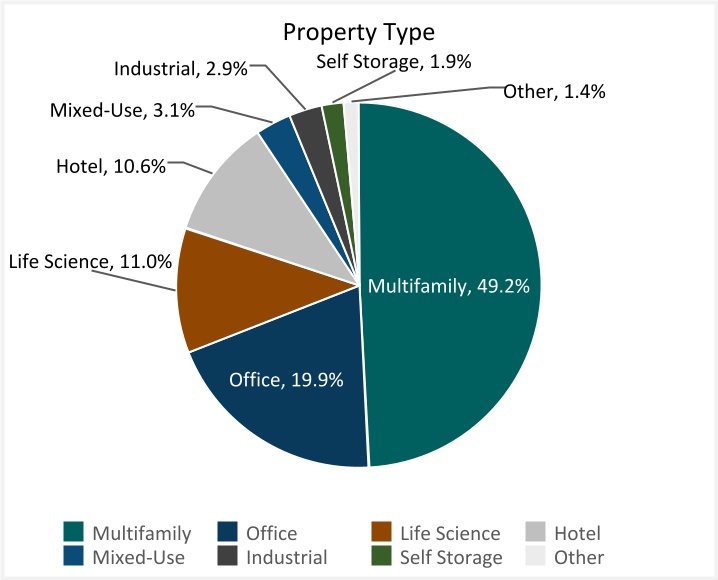

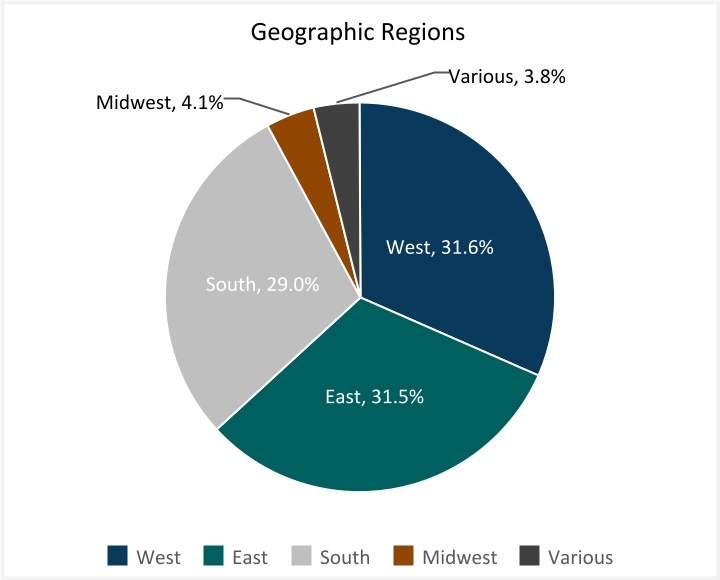

The following charts present, by total loan commitment, the property types securing our balance sheet loans held for investment portfolio and their geographic distribution within the U.S., as of December 31, 2023:

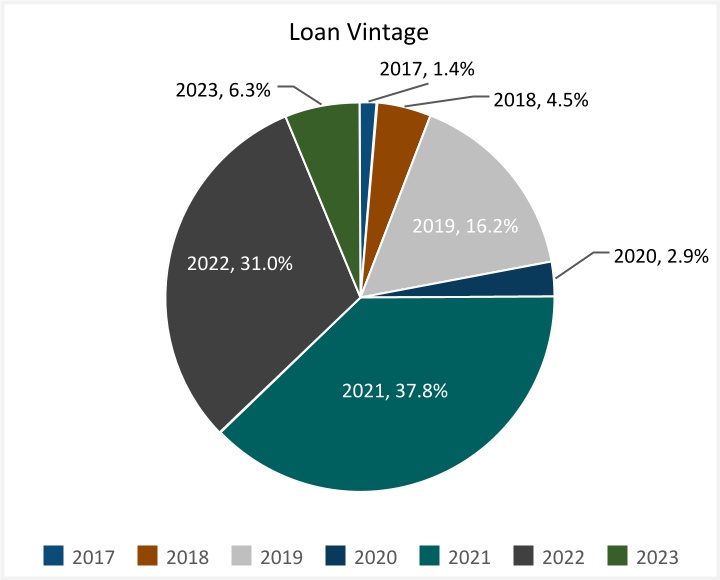

The following charts present, by total loan commitment, our loans held for investment portfolio by year of origination and loan category, as of December 31, 2023:

As of December 31, 2023, we did not have any loans on non-accrual status. As of December 31, 2023, our allowance for credit losses for loans held for investment was $69.8 million, or 190 basis points of total loan commitments, including an allowance for credit losses on unfunded loan commitments, compared to $214.6 million, or 395 basis points of total loan commitments, as of December 31, 2022, a decrease of $144.8 million from the prior year.

7

The following table details our total loan commitments and unpaid principal balance across the top 25 Metropolitan Statistical Areas (“MSA”), as of December 31, 2023 (dollars in thousands).

MSA(1) | MSA rank(1) | Number of loans | Loan commitment | Unpaid principal balance | ||||||||||||||||||||||

| New York City | 1 | 4 | $ | 604,133 | $ | 603,544 | ||||||||||||||||||||

| San Francisco | 11 | 3 | 392,900 | 363,728 | ||||||||||||||||||||||

| San Antonio | 24 | 4 | 184,370 | 178,438 | ||||||||||||||||||||||

| Los Angeles | 2 | 2 | 174,775 | 168,001 | ||||||||||||||||||||||

| Miami | 8 | 3 | 172,375 | 164,372 | ||||||||||||||||||||||

| Dallas | 4 | 2 | 124,000 | 100,093 | ||||||||||||||||||||||

| Baltimore | 21 | 1 | 122,500 | 121,133 | ||||||||||||||||||||||

| Phoenix | 12 | 2 | 78,100 | 69,511 | ||||||||||||||||||||||

| San Diego | 17 | 2 | 75,600 | 69,875 | ||||||||||||||||||||||

| Tampa | 18 | 1 | 69,000 | 64,570 | ||||||||||||||||||||||

| St. Louis | 20 | 1 | 65,600 | 57,000 | ||||||||||||||||||||||

| Atlanta | 9 | 1 | 44,500 | 35,072 | ||||||||||||||||||||||

| Chicago | 3 | 1 | 39,000 | 39,000 | ||||||||||||||||||||||

| Riverside (San Bernardino) | 13 | 1 | 36,440 | 33,915 | ||||||||||||||||||||||

| Other | 25 | 1,482,880 | 1,415,800 | |||||||||||||||||||||||

| Total | 53 | $ | 3,666,173 | $ | 3,484,052 | |||||||||||||||||||||

_________________________________

(1)Based on rankings of MSA for 2020 according to the United States Census Bureau.

Real Estate Owned

As of December 31, 2023, we owned four office properties and one multifamily property with an aggregate carrying value of $199.8 million.

For additional information regarding our investment portfolio as of December 31, 2023, see Item 7 – “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this Form 10-K.

8

Investment Portfolio Financing Strategy

We finance our investment portfolio using secured financing arrangements, including secured credit agreements, secured revolving credit facilities, mortgage loans, asset-specific financing arrangements, and collateralized loan obligations (“CLOs”). In certain instances, we may create structural leverage and obtain matched-term financing through the co-origination or non-recourse syndication of a senior loan interest to a third party (a “non-consolidated senior interest”). We may in the future use other forms of leverage, including structured financing other than CLOs, derivative instruments, and public and private secured and unsecured debt issuances by us or our subsidiaries.

We generally seek to match-fund and match-index our investments by minimizing the differences between the durations and indices of our investments and those of our liabilities, while minimizing our exposure to mark-to-market risk. This may be accomplished in certain instances using derivatives, although no such derivatives are currently used by us. Under certain circumstances, we may determine not to match-fund or match-index our investments, or we may otherwise be unable to do so.

Certain of our borrowing arrangements contain defined mark-to-market provisions that permit our lenders to issue margin calls to the Company only in the event that the collateral properties underlying the Company’s loans pledged to the Company’s lenders experience a non-temporary decline in value (“credit marks”) due to reasons other than capital markets events that result in changing credit spreads for similar borrowing obligations. As of December 31, 2023, 73.5% of our loan investment portfolio financing arrangements contained no mark-to-market provisions.

The following table details the principal balance amounts outstanding for our loan portfolio financing arrangements as of December 31, 2023 (dollars in thousands):

| Total indebtedness | Non-mark-to-market | Mark-to-market | ||||||||||||||||||

| Collateralized loan obligations | $ | 1,919,790 | $ | 1,919,790 | $ | — | ||||||||||||||

| Secured credit agreements | 799,518 | — | 799,518 | |||||||||||||||||

| Secured revolving credit facility | 23,782 | 23,782 | — | |||||||||||||||||

| Asset-specific financing | 274,158 | 274,158 | — | |||||||||||||||||

Total indebtedness(1) | $ | 3,017,248 | $ | 2,217,730 | $ | 799,518 | ||||||||||||||

| Percent of total indebtedness | 73.5 | % | 26.5 | % | ||||||||||||||||

_________________________________

(1)Excludes deferred financing costs of $8.4 million as of December 31, 2023.

The amount of leverage we employ for particular investments will depend upon our Manager’s assessment of the credit, liquidity, price volatility, and other risks of those assets and the financing counterparties, the availability of particular types of financing at the time, and the financial covenants under our financing arrangements. Our Manager’s decision to use leverage to finance our investments, including the amount of leverage we use, will be at its discretion and is not subject to the approval of our stockholders. We currently expect that our leverage, measured as the ratio of total debt to equity, will generally be less than 3.75:1, subject to compliance with our financial covenants under our secured financing agreements and other contractual obligations. We reserve the right to adjust this range without advance notice to satisfy our corporate finance and risk management objectives.

9

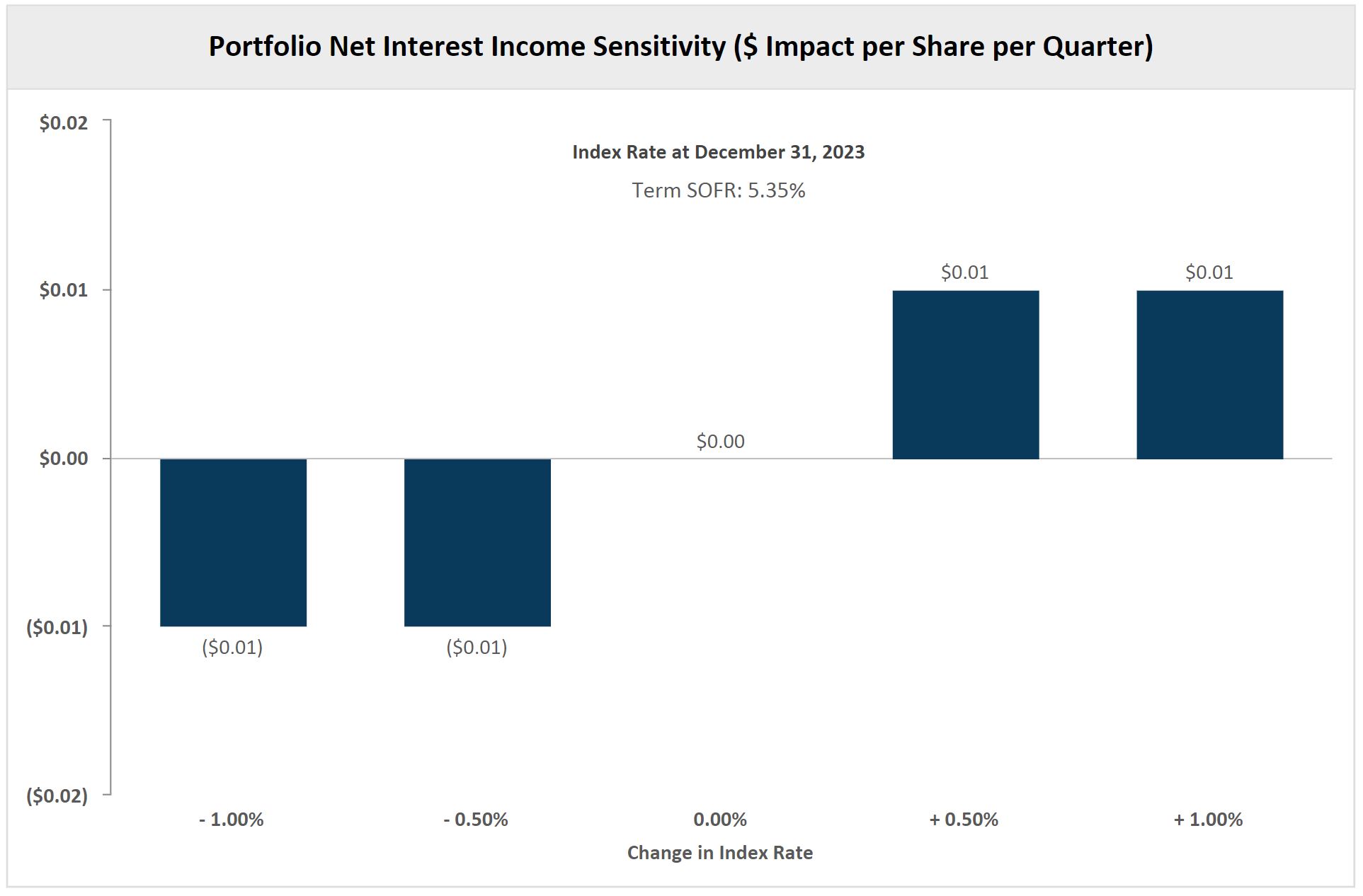

Floating Rate Portfolio

Our business model seeks to minimize our exposure to changing interest rates by match-indexing our assets and liabilities using the same benchmark index, which is Term SOFR. Accordingly, rising interest rates will generally increase our net interest income, while declining interest rates will generally decrease our net interest income, subject to the impact of interest rate floors in our mortgage loan investment portfolio. As of December 31, 2023, 100.0% of our loan investments by unpaid principal balance earned a floating rate of interest and were financed with liabilities that require interest payments based on floating rates, which resulted in approximately $0.5 billion of net floating rate exposure, subject to the impact of interest rate floors on all of our floating rate loans and less than 1.2% of our liabilities. Our liabilities are generally index-matched to each loan investment asset, resulting in a net exposure to movements in benchmark rates that varies based on the relative proportion of floating rate assets and liabilities.

The following table illustrates the quarterly impact to our net interest income of an immediate increase or decrease of 50 and 100 basis points in the Term SOFR benchmark rates underlying our existing floating rate loans held for investment portfolio and related liabilities as of December 31, 2023 (dollars in thousands).

Due to the floating rate and short-term nature of our loan investment portfolio, we have elected not to employ interest rate derivatives (e.g., interest rate swaps, caps, collars or swaptions) to limit our exposure to increasing interest rates, but we may do so in the future.

We had no fixed rate loans outstanding as of December 31, 2023.

10

Investment Guidelines

Our board of directors has approved the following investment guidelines:

•No investment will be made that would cause us to fail to maintain our qualification as a REIT under the Internal Revenue Code of 1986, as amended (the “Internal Revenue Code”);

•No investment will be made that would cause us or any of our subsidiaries to be required to be registered as an investment company under the Investment Company Act;

•Our Manager will seek to invest our capital in our target assets;

•Prior to the deployment of our capital into our target assets, our Manager may cause our capital to be invested in any short-term investments in money market funds, bank accounts, overnight repurchase agreements with primary Federal Reserve Bank dealers collateralized by direct U.S. government obligations and other instruments or investments determined by our Manager to be of high quality;

•Not more than 25% of our Equity (as defined in our Management Agreement) may be invested in any individual investment without the approval of a majority of our independent directors (it being understood, however, that for purposes of the foregoing concentration limit, in the case of any investment that is comprised (whether through a structured investment vehicle or other arrangement) of securities, instruments or assets of multiple portfolio issuers, such investment for purposes of the foregoing limitation will be deemed to be multiple investments in such underlying securities, instruments and assets and not the particular vehicle, product or other arrangement in which they are aggregated); and

•Any investment in excess of $300 million requires the approval of a majority of our independent directors.

These investment guidelines may be amended, supplemented or waived pursuant to the approval of our board of directors (which must include a majority of our independent directors) from time to time, without the approval of our stockholders.

Competition

We operate in a competitive market for the origination and acquisition of attractive investment opportunities. We compete with a variety of institutional investors, including other REITs, debt funds, specialty finance companies, savings and loan associations, banks, mortgage bankers, insurance companies, mutual funds, institutional investors, investment banking firms, financial institutions, private equity and hedge funds, governmental bodies and other entities and may compete with other TPG Funds (such as the TRECO Funds). Many of our competitors are substantially larger and have considerably greater financial, technical and marketing resources than we do. Several of our competitors, including other REITs, have recently raised, or are expected to raise, significant amounts of capital and may have investment objectives that overlap with our investment objectives, which may create additional competition for lending and other investment opportunities. Some of our competitors may have a lower cost of funds and access to funding sources that may not be available to us or are only available to us on substantially less attractive terms. Many of our competitors are not subject to the operating constraints associated with REIT tax compliance or maintenance of an exclusion or exemption from the Investment Company Act. In addition, some of our competitors may have higher risk tolerances or different risk assessments, which could allow them to consider a wider variety of investments and establish more lending relationships than we do. Competition may result in realizing fewer investments, higher prices, acceptance of greater risk, greater defaults, lower yields or a narrower spread of yields over our borrowing costs. In addition, competition for attractive investments could delay the investment of our capital.

In the face of this competition, we have access to our Manager’s professionals through TPG and TPG Real Estate, and their industry expertise, which provides us with an advantage in competing effectively for attractive investment opportunities, helps us assess risks and determine appropriate pricing for certain potential investments, and affords us access to capital with low costs and other attractive attributes. However, we may not be able to achieve our business goals or expectations due to the competitive risks that we face. For additional information concerning these competitive risks, see Item 1A – “Risk Factors—Risks Related to Our Lending and Investment Activities—We operate in a competitive market for the origination and acquisition of attractive investment opportunities and competition may limit our ability to originate or acquire attractive investments in our target assets, which could have a material adverse effect on us.”

Environmental, Social, and Governance

Because we are externally managed by our Manager, an affiliate of TPG, many of the Environmental, Social, and Governance (“ESG”) initiatives undertaken by them impact or apply to us. We risk damage to our reputation if we, affiliates of our Manager, or TPG fail to act responsibly in such areas as diversity and inclusion, environmental stewardship, support for local communities, corporate governance and transparency, and incorporating ESG factors in our investment processes. We strive to maintain an environment that fosters integrity, professionalism, and candor when conducting our day-to-day operations, during our investment decision making process, and while implementing and maintaining our ESG initiatives.

11

Employees

We do not have any employees, nor do we expect to have employees in the future. We are externally managed and are advised by our Manager pursuant to our Management Agreement between our Manager and us. All of our executive officers and certain of our directors are employees of our Manager or its affiliates.

Our success depends to a significant extent upon the ongoing efforts, experience, diligence, skill, and network of business contacts of our executive officers and the other key personnel of TPG provided to our Manager and its affiliates. These individuals evaluate, negotiate, execute, and monitor our loans, other investments and our capitalization, and advise us regarding maintenance of our REIT status and exclusion or exemption from regulation under the Investment Company Act. Our success depends on their skills and management expertise and continued service with our Manager and its affiliates.

Government Regulation

Our operations are subject, in certain instances, to supervision and regulation by U.S. and other governmental authorities, and may be subject to various laws and judicial and administrative decisions imposing various requirements and restrictions, which among other things: (i) regulate credit-granting activities; (ii) establish maximum interest rates, finance charges and other charges; (iii) require disclosures to customers; (iv) govern secured transactions; and (v) set collection, foreclosure, repossession and claims-handling procedures and other trade practices. We are also required to comply with certain provisions of the Equal Credit Opportunity Act that are applicable to commercial loans. We intend to conduct our business so that neither we nor any of our subsidiaries are required to register as an investment company under the Investment Company Act.

In our judgment, existing statutes and regulations have not had a material adverse effect on our business. In recent years, legislators in the United States and in other countries have said that greater regulation of financial services firms is needed, particularly in areas such as risk management, leverage, and disclosure. While we expect that additional new regulations in these areas may be adopted and existing ones may change in the future, it is not possible at this time to forecast the exact nature of any future legislation, regulations, judicial decisions, orders or interpretations, nor their impact upon our future business, financial condition, or results of operations or prospects.

Operating and Regulatory Structure

REIT Qualification

We made an election to be taxed as a REIT for U.S. federal income tax purposes, commencing with our initial taxable year ended December 31, 2014. We generally must distribute annually at least 90% of our net taxable income, subject to certain adjustments and excluding any net capital gain, in order for us to continue to qualify as a REIT for U.S. federal income tax purposes. To the extent that we satisfy this distribution requirement but distribute less than 100% of our net taxable income, we will be subject to U.S. federal income tax on our undistributed taxable income. In addition, we will be subject to a 4% nondeductible excise tax if the actual amount that we pay out to our stockholders in a calendar year is less than a minimum amount specified under U.S. federal tax laws. Our qualification as a REIT also depends on our ability to meet various other requirements imposed by the Internal Revenue Code, which relate to organizational structure, diversity of stock ownership, and certain restrictions with regard to the nature of our assets and the sources of our income. Even if we continue to qualify as a REIT, we may be subject to certain U.S. federal excise taxes and state and local taxes on our income and assets. If we fail to qualify as a REIT in any taxable year, we will be subject to U.S. federal income tax at regular corporate rates, and applicable state and local taxes, and will not be able to qualify as a REIT for the subsequent four years.

Furthermore, we have multiple taxable REIT subsidiaries (“TRSs”), which when active, pay U.S. federal, state, and local income tax on their net taxable income. See Item 1A – “Risk Factors – Risks Related to our REIT Status and Certain Other Tax Items” for additional tax status information.

Investment Company Act Exclusion or Exemption

We conduct, and intend to continue to conduct, our operations so that neither we nor any of our subsidiaries are required to register as an investment company under the Investment Company Act. Complying with provisions that allow us to avoid the consequences of registration under the Investment Company Act may at times require us to forego otherwise attractive opportunities and limit the manner in which we conduct our operations. We conduct our operations so that we are not an “investment company” as defined in Section 3(a)(1)(A) or Section 3(a)(1)(C) of the Investment Company Act. We believe we are not an investment company under Section 3(a)(1)(A) of the Investment Company Act because we do not engage primarily, or hold ourselves out as being engaged primarily, in the business of investing, reinvesting or trading in securities. Rather, through our wholly-owned or majority-owned subsidiaries, we are primarily engaged in non-investment company businesses related to real estate. In addition, we intend to conduct our operations so that we do not come within the definition of an investment company under Section 3(a)(1)(C) of the Investment Company Act because less than 40% of the value of our total assets (exclusive of U.S. government securities and cash items) on an unconsolidated basis will consist of “investment securities.” Excluded from the term “investment securities” (as that term is defined in the Investment Company Act) are securities issued by majority-owned subsidiaries that are themselves not investment companies and are not relying on the exclusions from the definition of investment company set forth in Section 3(c)(1) or Section 3(c)(7) of the

12

Investment Company Act. Our interests in wholly-owned or majority-owned subsidiaries that qualify for the exclusion pursuant to Section 3(c)(5)(C), as described below, Rule 3a-7, as described below, or another exclusion or exception under the Investment Company Act (other than Section 3(c)(1) or Section 3(c)(7) thereof), do not constitute “investment securities.”

We hold our assets primarily through direct or indirect wholly-owned or majority-owned subsidiaries, certain of which are excluded from the definition of investment company pursuant to Section 3(c)(5)(C) of the Investment Company Act. We classify the assets of our subsidiaries relying on the Section 3(c)(5)(C) exemption from the Investment Company Act based upon positions set forth by the SEC staff. Based on such positions, to qualify for the exclusion pursuant to Section 3(c)(5)(C), each such subsidiary generally is required to hold at least (i) 55% of its assets in “qualifying” real estate assets and (ii) at least 80% of its assets in “qualifying” real estate assets and real estate-related assets.

Certain of our subsidiaries rely on Rule 3a-7 under the Investment Company Act. We refer to these subsidiaries as our “CLO subsidiaries.” Rule 3a-7 under the Investment Company Act is available to certain structured financing vehicles that are engaged in the business of holding financial assets that, by their terms, convert into cash within a finite time period and that issue fixed income securities entitling holders to receive payments that depend primarily on the cash flows from these assets, provided that, among other things, the structured finance vehicle does not engage in certain portfolio management practices resembling those employed by management investment companies (e.g., mutual funds). Accordingly, each of these CLO subsidiaries is subject to legal and contractual restrictions regarding their structure and operation. As a result of these restrictions, our CLO subsidiaries may suffer losses on their assets and we may suffer losses on our investments in those CLO subsidiaries.

As a consequence of our seeking to avoid the need to register under the Investment Company Act on an ongoing basis, we and/or our subsidiaries may be restricted from making certain investments or may structure investments in a manner that would be less advantageous to us than would be the case in the absence of such requirements. In particular, a change in the value of any of our assets could negatively affect our ability to avoid the need to register under the Investment Company Act and cause the need for a restructuring of our investment portfolio. For example, these restrictions may limit our and our subsidiaries’ ability to invest directly in mortgage-backed securities that represent less than the entire ownership in a pool of senior mortgage loans, debt and equity tranches of securitizations and certain asset-backed securities, non-controlling equity interests in real estate companies or in assets not related to real estate; however, we and our subsidiaries may invest in such securities to a certain extent. In addition, seeking to avoid the need to register under the Investment Company Act may cause us and/or our subsidiaries to acquire or hold additional assets that we might not otherwise have acquired or held or dispose of investments that we and/or our subsidiaries might not have otherwise disposed of, which could result in higher costs or lower proceeds to us than we would have paid or received if we were not seeking to comply with such requirements. Thus, avoiding registration under the Investment Company Act may hinder our ability to operate solely on the basis of maximizing profits.

If we were required to register as an investment company under the Investment Company Act, we would become subject to substantial regulation with respect to our capital structure (including our ability to use borrowings), management, operations, transactions with affiliated persons (as defined in the Investment Company Act) and portfolio composition, including disclosure requirements and restrictions with respect to diversification and industry concentration and other matters. Compliance with the Investment Company Act would, accordingly, limit our ability to make certain investments and require us to significantly restructure our business plan, which could materially and adversely affect our ability to pay distributions to our stockholders.

Available Information

We maintain a website at www.tpgrefinance.com. We are providing the address to our website solely for the information of investors. The information on our website is not a part of, nor is it incorporated by reference into, this report. Through our website, we make available, free of charge, our annual proxy statement, annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after we electronically file such material with, or furnish them to, the SEC.

13

Item 1A. Risk Factors.

The following is a summary of the principal risks and uncertainties that could materially adversely affect our business, financial condition and results of operations. This summary should be read together with the more detailed risk factors contained below.

Risks Related to Our Lending and Investment Activities

•Our success depends on the availability of attractive investment opportunities and our Manager’s ability to identify, structure, consummate, leverage, manage and realize returns on our investments.

•Our commercial mortgage loans and other commercial real estate-related debt instruments expose us to risks associated with real estate investments generally.

•We operate in a competitive market for the origination and acquisition of attractive investment opportunities and competition may limit our ability to originate or acquire attractive investments in our target assets.

•The due diligence process undertaken by our Manager in regard to our investment opportunities may not reveal all facts relevant to an investment and, as a result, we may experience losses.

•Real estate valuation is inherently subjective and uncertain, and is subject to change, especially during periods of volatility. Our allowance for loan losses may prove inadequate.

•Interest rate, prepayment, concentration, liquidity, collateral and credit risk may adversely affect our financial performance. There are no assurances that the U.S. or global financial systems will remain stable.

•Any credit ratings assigned to our investments will be subject to ongoing evaluations and revisions, and we cannot assure you that those ratings will not be downgraded.

•The success of our investment strategy depends, in part, on our ability to successfully effectuate loan modifications and/or restructurings.

•We have in the past and may in the future acquire ownership of property securing our loans through foreclosure or deed-in-lieu of foreclosure. When we take title to the property securing one of our loans, and if we do not or cannot sell the property, we own and operate the property as “real estate owned.” Our real estate owned assets are subject to risks particular to real property. These risks may have resulted and may continue to result in a reduction or elimination of return from a loan secured by a particular property.

•Property insurance costs may continue to increase, and in some cases insurance may not be available.

Risks Related to Our Financing

•We have a significant amount of debt, which subjects us to increased risk of loss.

•Our financing arrangements may require us to provide additional collateral or repay debt.

•Certain of our current financing arrangements contain, and certain of our future financing arrangements may contain, various financial and operational covenants, and a default of any such covenants could materially and adversely affect us.

•There can be no assurance that we will be able to obtain or utilize additional financing arrangements in the future on similar or more favorable terms, or at all.

Risks Related to Our Relationship with Our Manager and its Affiliates

•We depend on our Manager and the personnel of TPG provided to our Manager for our success. We may not find a suitable replacement for our Manager if our Management Agreement is terminated, or if key personnel cease to be employed by TPG or otherwise become unavailable to us.

•Our Manager manages our portfolio pursuant to very broad investment guidelines and is not required to seek the approval of our board of directors for each investment, financing, asset allocation or hedging decision made by it, which may result in our making riskier loans and other investments.

Risks Related to Our Company

•Our investment, asset allocation and financing strategies may be changed without stockholder consent and we may not be able to operate our business successfully or implement our operating policies and investment strategy.

•TPG and our Manager may not be able to hire and retain qualified investment professionals or grow and maintain our relationships with key borrowers and loan brokers. We also depend on a third-party service provider for asset management services. We may not find a suitable replacement for this service provider if our agreement with them is terminated, or if key personnel of this service provider cease to be employed or otherwise become unavailable to us.

14

•Rapid changes in the market value or income potential of our assets may make it more difficult for us to maintain our qualification as a REIT or our exclusion or exemption from regulation under the Investment Company Act.

•Actions of the U.S. government and other governmental and regulatory bodies designed to stabilize or reform the financial markets may not achieve the intended effect.

•Operational risks, including the risks of cyberattacks, may disrupt our businesses, result in losses or limit our growth.

Risks Related to our REIT Status and Certain Other Tax Items

•Failure to comply with REIT requirements could subject us to higher taxes and liquidity issues and reduce the amount of cash available for distribution to our stockholders.

•Dividends payable by REITs do not qualify for the reduced tax rates available for some dividends.

•Compliance with the REIT requirements may hinder our ability to grow, which could materially and adversely affect us.

•We may choose to make distributions to our stockholders in shares of our common stock, in which case our stockholders could be required to pay income taxes in excess of the cash dividends they receive.

•Liquidation of assets may jeopardize our ability to maintain our REIT qualification or create additional tax liability for us.

Risks Related to Our Common Stock

•We have not established a minimum distribution payment level and we cannot assure you of our ability to pay distributions in the future.

•The authorized but unissued shares of our common stock and preferred stock may prevent a change in our control.

•Ownership limitations may delay, defer or prevent a transaction or a change in our control that might involve a premium price for our common stock or otherwise be in the best interest of our stockholders.

•Our charter contains provisions that make removal of our directors difficult, which makes it more difficult for our stockholders to effect changes to our management and may prevent a change in control of our company that is in the best interests of our stockholders.

General Risks

•A global economic slowdown, a recession or declines in real estate values could impair our investments and have a significant adverse effect on our business, financial condition and results of operations.

•Our obligations associated with being a public company, our failure to maintain an effective system of internal control and social, political, and economic instability, unrest, and other circumstances beyond our control could adversely affect our business operations.

15

Risks Related to Our Lending and Investment Activities

Our success depends on the availability of attractive investment opportunities and our Manager’s ability to identify, structure, consummate, leverage, manage and realize returns on our investments.

Our operating results are dependent upon the availability of, as well as our Manager’s ability to identify, structure, consummate, leverage, manage and realize returns on, our loans and other investments. In general, the availability of attractive investment opportunities and, consequently, our operating results, will be affected by the level and volatility of interest rates, conditions in the financial markets, general economic conditions, the demand for investment opportunities in our target assets and the supply of capital for such investment opportunities. We cannot assure you that our Manager will be successful in identifying and consummating attractive investments or that such investments, once made, will perform as anticipated.

Our commercial mortgage loans and other commercial real estate-related debt instruments expose us to risks associated with real estate investments generally.

We seek to originate and selectively acquire commercial mortgage loans and other commercial real estate-related debt instruments. Deterioration of real estate fundamentals generally, and in the United States in particular, has negatively impacted our performance by making it more difficult for borrowers to satisfy their debt payment obligations, increasing the default risk applicable to borrowers and made it relatively more difficult for us to generate attractive risk-adjusted returns. Real estate investments are subject to various risks, including:

•economic and market fluctuations;

•political instability or changes, terrorism and acts of war;

•changes in building, environmental, zoning and other laws;

•casualty or condemnation losses;

•regulatory limitations on rents or moratoriums against tenant evictions or foreclosures;

•decreases in property values;

•changes in the appeal of properties to tenants, including due to the impact of remote work on how tenants and workers can efficiently use commercial space;

•changes in supply (resulting from the recent growth in commercial real estate debt funds or otherwise) and demand;

•energy supply shortages;

•various uninsured or uninsurable risks;

•increasing costs relating to, or the unavailability of, various categories of property-related insurance;

•natural disasters and outbreaks of pandemic or contagious diseases;

•changes in government regulations (such as rent control or regulation of greenhouse gas emissions);

•changes in monetary policy;

•changes in capital expenditure costs;

•changes in the availability of debt financing and/or mortgage funds which may render the sale or refinancing of properties difficult or impracticable;

•increased mortgage defaults;

•declining interest rates which reduce asset yields, subject to the impact of interest rate floors on certain of our floating rate loans;

•increasing interest rates, which may make it more difficult for our borrowers to repay loans via a refinancing or sale of the collateral property;

•increases in borrowing rates;

•changes in consumer spending; and

•negative developments in the economy and/or adverse changes in real estate values generally and other risk factors that are beyond our control.

16

Recent concerns about the real estate market, rising interest rates, inflation, energy costs and geopolitical issues have contributed to increased volatility and diminished expectations for the economy and markets going forward. We cannot predict the degree to which economic conditions generally, and the conditions for commercial real estate debt investing in particular, will improve or decline. Any declines in the performance of the U.S. and global economies or in the real estate debt markets could have a material adverse effect on us.

Commercial real estate debt instruments that are secured or otherwise supported, directly or indirectly, by commercial property are subject to delinquency, foreclosure and loss, which could materially and adversely affect us.

Commercial real estate debt instruments, such as mortgage loans, that are secured or, in the case of certain assets (including participation interests, mezzanine loans and preferred equity), supported by commercial properties are subject to risks of delinquency and foreclosure and risks of loss that are greater than similar risks associated with loans made on the security of single-family residential property. The ability of a borrower to pay the principal of and interest on a loan secured by an income-producing property typically is dependent primarily upon the successful operation of such property rather than upon the existence of independent income or assets of the borrower. If the net operating income of the property is reduced, the borrower’s ability to pay the principal of and interest on the loan in a timely manner, or at all, may be impaired and therefore could reduce our return from an affected property or investment, which could materially and adversely affect us. Net operating income of an income-producing property may be adversely affected by the risks particular to commercial real property described above, as well as, among other things:

•tenant mix and tenant bankruptcies;

•success of tenant businesses;

•property management decisions, including with respect to capital improvements, particularly in older building structures;

•renovations or repositionings during which operations may be limited or halted completely;

•property location and condition, including, without limitation, any need to address environmental contamination or climate-related risks at a property;

•competition from comparable types of properties;

•changes in global, national, regional or local economic conditions or changes in specific industry segments;

•changes in interest rates, and in the state of the credit, securitization, debt and equity capital markets, including diminished availability or lack of debt financing for commercial real estate;

•global trade disruption, supply chain issues, significant introductions of trade barriers and bilateral trade frictions;

•declines in regional or local real estate values or rental or occupancy rates;

•responses of businesses, governments and individuals to pandemics or outbreaks of contagious disease;

•labor shortages and increases in the minimum wage and other forms of employee compensation and benefits;

•higher rates of inflation;

•changes in real estate tax rates, tax credits and other operating expenses;

•changes to tax laws and rates to which real estate lenders and investors are subject; and

•government regulations.

In the event of any default under a mortgage loan held directly by us, we will bear a risk of loss to the extent of any deficiency between the value of the collateral and the principal of and accrued interest on the mortgage loan. In the event of the bankruptcy of a mortgage loan borrower, the mortgage loan to that borrower will be deemed to be secured only to the extent of the value of the underlying collateral at the time of bankruptcy (as determined by the bankruptcy court), and the lien securing the mortgage loan will be subject to the avoidance powers of the bankruptcy trustee or debtor-in-possession to the extent the lien is unenforceable under state law. Foreclosure of a mortgage loan can be an expensive and lengthy process that could have a substantial negative effect on any anticipated return on the foreclosed mortgage loan.

17

We originate and acquire transitional loans, which involves greater risk of loss than stabilized commercial mortgage loans.

We originate and acquire transitional loans secured by first lien mortgages on commercial real estate, and in some instances pledges of equity in the property holder. These loans provide interim financing to borrowers seeking short-term capital for the acquisition, lease up or repositioning of commercial real estate and generally have an initial maturity of three years or less. A borrower under a transitional loan has usually identified an asset that the borrower views as undervalued, having been under-managed and/or is located in a recovering market. If the borrower's assessment of the asset as undervalued is inaccurate, or if the market in which the asset is located fails to recover according to the borrower’s projections, or if the borrower fails to improve the operating performance of the asset or the value of the asset, the borrower may not receive a sufficient return on the asset to satisfy the transitional loan, and we will bear the risk that we may not recover some or all of our investment. During periods in which there are decreases in demand for certain properties as a result of macroeconomic factors, reductions in the financial resources of tenants and defaults by borrowers or tenants, borrowers face additional challenges in transitioning properties. Market downturns or other adverse macroeconomic factors may affect transitional loans in our portfolio more adversely than loans secured by more stabilized assets. A portion of our loans are secured by office space and similar commercial real estate. This sector has recently been affected by certain macroeconomic factors, such as an increased prevalence of remote work.

In addition, borrowers often use the proceeds of a sale or refinancing to repay a loan, and both sales and refinancings are subject to the broader risk that the underlying collateral may not be liquid and that financing may not be available on acceptable terms or at all. In the event of any failure to repay under a transitional loan held by us, we will bear the risk of loss of principal and non-payment of interest and fees to the extent of any deficiency between the value of the underlying collateral and the principal amount and unpaid interest of the loan. To the extent we suffer such losses with respect to our loans, it could adversely affect our results of operations and financial condition.

There can be no assurances that the U.S. or global financial systems will remain stable, and the occurrence of another significant credit market disruption may negatively impact our ability to execute our investment strategy, which would materially and adversely affect us.

The U.S. and global financial markets experienced significant disruptions in the past, during which times global credit markets collapsed, borrowers defaulted on their loans at historically high levels, banks and other lending institutions suffered heavy losses and the value of real estate declined. During such periods, a significant number of borrowers became unable to pay principal and interest on outstanding loans as the value of their real estate declined. After the 2008 Global Financial Crisis, liquidity eventually returned to the market and property values recovered to levels that exceeded those observed prior to the Global Financial Crisis. However, declining real estate values due to changes in interest rates, economic conditions, or other factors, have in the past and could again in the future reduce the level of new mortgage and other real estate-related loan originations. Instability in the U.S. and global financial markets in the future could be caused by any number of factors beyond our control, including, without limitation, terrorist attacks or other acts of war and adverse changes in national or international economic, market and political conditions or another health pandemic. Any future sustained period of increased payment delinquencies, foreclosures or losses could adversely affect both our net interest income from loans in our portfolio as well as our ability to originate and acquire loans, which would materially and adversely affect us.

Difficulty in redeploying the proceeds from repayments of our existing loans and other investments could materially and adversely affect us.

As our loans and other investments are repaid, we attempt to redeploy the proceeds we receive into new loans and investments (which can include future fundings associated with our existing loans) and repay borrowings under our secured financing agreements and other financing arrangements. It is possible that we will fail to identify reinvestment options that would provide a yield and/or a risk profile that is comparable to the asset that was repaid. If we fail to redeploy the proceeds we receive from repayment of a loan or other investment in equivalent or better alternatives, we could be materially and adversely affected. If we cannot redeploy the proceeds we receive from repayments into funding loans in property types or geographic markets that our Manager has identified as priorities for us, such repayments may cause the composition of our loan portfolio to skew towards less favored property types or geographies and prevent us from achieving our portfolio construction objectives.

If we are unable to successfully integrate new assets and manage our growth, our results of operations and financial condition may suffer.

We have in the past and may in the future significantly increase the size and/or change the mix of our portfolio of assets. We may be unable to successfully and efficiently integrate newly-acquired assets into our existing portfolio or otherwise effectively manage our assets or our growth effectively. In addition, increases in our portfolio of assets and/or changes in the mix of our assets may place significant demands on our Manager’s administrative, operational, asset management, financial and other resources. Any failure to manage increases in size effectively could adversely affect our results of operations and financial condition.

18

We operate in a competitive market for the origination and acquisition of attractive investment opportunities and competition may limit our ability to originate or acquire attractive investments in our target assets, which could have a material adverse effect on us.

We operate in a competitive market for the origination and acquisition of attractive investment opportunities. We compete with a variety of institutional investors, including other REITs, debt funds, specialty finance companies, savings and loan associations, banks, mortgage bankers, insurance companies, mutual funds, institutional investors, investment banking firms, financial institutions, private equity and hedge funds, governmental bodies and other entities and may compete with TPG Funds (such as the TRECO Funds), subject to duties to offer, other contractual obligations and other internal rules. Many of our competitors are substantially larger and have considerably greater financial, technical and marketing resources than we do. Several of our competitors, including other REITs, have recently raised, or are expected to raise, significant amounts of capital, and may have investment objectives that overlap with our investment objectives, which may create additional competition for lending and other investment opportunities. Some of our competitors may have a lower cost of funds and access to funding sources that may not be available to us or are only available to us on substantially less attractive terms. Many of our competitors are not subject to the operating constraints associated with REIT tax compliance or maintenance of an exclusion or exemption from the Investment Company Act. In addition, some of our competitors may have higher risk tolerances or different risk assessments, which could allow them to consider a wider variety of investments and establish more lending relationships than we do. Competition may result in realizing fewer investments, higher prices, acceptance of greater risk, greater defaults, lower yields or a narrower spread of yields over our borrowing costs. In addition, competition for attractive investments could delay the investment of our capital. Furthermore, changes in the financial regulatory regime could decrease the restrictions on banks and other financial institutions and allow them to compete with us for investment opportunities that were previously not available to, or otherwise pursued by, them. See “—Risks Related to Our Company—Changes in laws or regulations governing our operations or those of our competitors, or changes in the interpretation thereof, or newly enacted laws or regulations, could result in increased competition for our target assets, required changes to our business practices and collectively could adversely impact our revenues and impose additional costs on us, which could materially and adversely affect us.”

As a result, competition may limit our ability to originate or acquire attractive investments in our target assets and could result in reduced returns. We can provide no assurance that we will be able to identify and originate or acquire attractive investments that are consistent with our investment strategy.

The due diligence process undertaken by our Manager in regard to our investment opportunities may not reveal all facts relevant to an investment and, as a result, we may experience losses, which could materially and adversely affect us.