[Net Lease]

LEASE AGREEMENT

THIS LEASE AGREEMENT is made this 18th day of June, 2015, between PROLOGIS CALIFORNIA I LLC (“Landlord”), and the Tenant named below.

| Tenant: | Throwdown Industries Holdings, LLC, a Delaware limited liability company | |

| Tenant’s Representative, | David E. Vautrin | |

| Address, and Telephone: | 18 Goodyear | |

| Suite 125 | ||

| Irvine, California 92618 | ||

| 949-916-9680 | ||

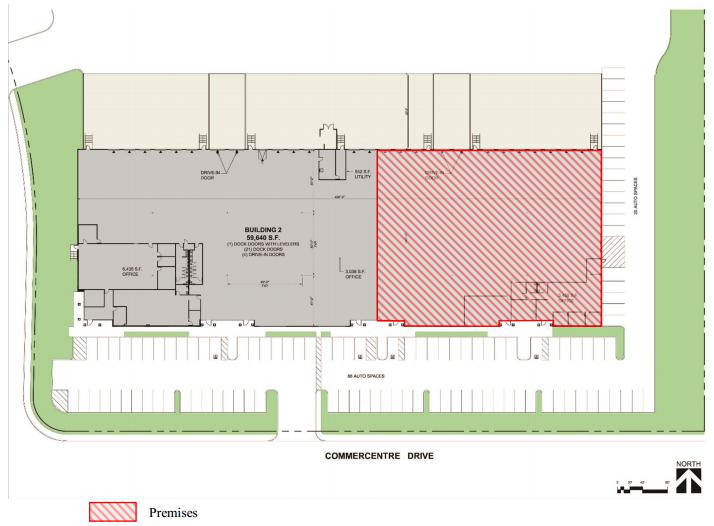

| Premises: | That portion of the Building, containing approximately 25,788 rentable square feet, as determined by Landlord, as shown on Exhibit A and more commonly known as 25731 Commercentre Drive, Lake Forest, California 92630. | |

| Project: | The project commonly known as Prologis Lake Forest Business Center | |

| Building: | Prologis Lake Forest Business Center 2 | |

| 25671 - 25731 Commercentre Drive | ||

| Lake Forest, California 92630 | ||

| Tenant’s Proportionate Share of Project: | 18.43 % of the 139,962 square foot Project | |

| Tenant’s Proportionate Share of Building: | 43.24 % of the 59,640 square foot Building | |

| Lease Term: | Beginning on the Commencement Date and ending on the last day of the thirty-eighth (38th) full month following the Commencement Date. | |

| Commencement Date: | September 1, 2015 | |

| Initial Monthly Base Rent: | See Addendum 1 |

| Initial Estimated Monthly Operating Expense Payments: (estimates only and subject to adjustment to actual costs and expenses according to the provisions of this Lease) | 1. | Utilities: included in Common Area Charges | |||

| 2. | Common Area Charges: | $1,959.88 | |||

| 3. | Taxes: | $2,965.62 | |||

| 4. | Insurance: | $386.82 | |||

| 5. | Others: | $644.70 | |||

| Prop. Mgmt. Fee | |||||

| Initial Estimated Monthly Operating Expense Payments: | $5,957.02 | |

| Initial Monthly Base Rent, and Estimated Operating Expense | $22,461.34 | |

| Security Deposit: | $23,466.45 | |

| Brokers: | Landlord: CBRE, Inc. - Gregg Haly and Matt Burgner Tenant: CBRE, Inc. - Cameron Lindee and Garrett Ellis | |

| Addenda: | 1. Base Rent Adjustments 2. HVAC Maintenance Contract 3. Move Out Conditions 4. One Renewal at Market 5. Construction Addendum | |

| Exhibits: | A. Site Plan | |

| B. Project Rules and Regulations | ||

| C. Commencement Date Certificate |

| - 1 - |

1. Granting Clause. In consideration of the obligation of Tenant to pay rent as herein provided and in consideration of the other terms, covenants, and conditions hereof, Landlord leases to Tenant, and Tenant takes from Landlord, the Premises, to have and to hold for the Lease Term, subject to the terms, covenants and conditions of this Lease.

2. Acceptance of Premises. Tenant shall accept the Premises in its condition as of the Commencement Date, subject to all applicable laws, ordinances, regulations, covenants and restrictions. Landlord has made no representation or warranty as to the suitability of the Premises for the conduct of Tenant’s business, and Tenant waives any implied warranty that the Premises are suitable for Tenant’s intended purposes. In no event shall Landlord have any obligation for any defects in the Premises or any limitation on its use. The taking of possession of the Premises shall be conclusive evidence that Tenant accepts the Premises and that the Premises were in good condition at the time possession was taken except for items that are Landlord’s responsibility under Paragraph 10 and any punchlist items agreed to in writing by Landlord and Tenant. No later than 10 days after written demand is made therefor by Landlord of Tenant, Tenant shall execute and deliver to Landlord a Commencement Date Certificate in the form of Exhibit C attached to and hereby made a part of this Lease.

Landlord represents and warrants, to its knowledge, that as of the Commencement Date the Building’s HVAC, electrical, plumbing and other mechanical systems are in good working order and Landlord warrants such systems for a period of ninety (90) days from the Commencement Date; provided, however, that such warranty shall not be effective for any maintenance, repairs or replacements necessitated due to the misuse of, or damages caused by, Tenant, its employees, contractors, agents, subtenants, or invitees.

3. Use. The Premises shall be used only for the purpose of receiving, storing, shipping, light manufacturing, and selling (but specifically excluding retail selling) products, materials and merchandise made and/or distributed by Tenant and its affiliate brands/companies and for and for such other lawful purposes as may be incidental.. Subject to Tenant’s compliance with all Legal Requirements, the Premises may also be used for an in-house fitness training show room for potential customers, employees, and affiliates and for one warehouse/holiday sale per year. Tenant shall not conduct or give notice of any auction, liquidation, or going out of business sale on the Premises. Tenant will use the Premises in a careful, safe and proper manner and will not commit waste, overload the floor or structure of the Premises or subject the Premises to use that would damage the Premises. Tenant shall not permit any objectionable or unpleasant odors, smoke, dust, gas, noise, or vibrations to emanate from the Premises, or take any other action that would constitute a nuisance or would disturb, unreasonably interfere with, or endanger Landlord or any tenants of the Project. With the exception of the designated truck loading docks connected to the Premises, outside storage, including without limitation, storage of trucks and other vehicles, is prohibited without Landlord’s prior written consent; provided, however, Tenant shall have the right to park operable vehicles and trailers overnight at the truck loading docks and designated truck and trailer parking areas for the Premises and operable automobiles in the designated automobile parking areas, and further provided there is no interference with the access of other tenants to the Building and Project parking lots and truck courts. Tenant, at its sole expense, shall use and occupy the Premises in compliance with all laws, including, without limitation, the Americans With Disabilities Act, orders, judgments, ordinances, regulations, codes, directives, permits, licenses, covenants and restrictions now or hereafter applicable to the Premises (collectively, “Legal Requirements”). The Premises shall not be used as a place of public accommodation under the Americans With Disabilities Act or similar state statutes or local ordinances or any regulations promulgated thereunder, all as may be amended from time to time. Tenant shall, at its expense, make any alterations or modifications, within or without the Premises, that are required by Legal Requirements related to Tenant’s use or occupation of the Premises. Tenant will not use or permit the Premises to be used for any purpose or in any manner that would void Tenant’s or Landlord’s insurance, increase the insurance risk, or cause the disallowance of any sprinkler credits. If any increase in the cost of any insurance on the Premises or the Project is caused by Tenant’s use or occupation of the Premises, or because Tenant vacates the Premises, then Tenant shall pay the amount of such increase to Landlord. Any occupation of the Premises by Tenant prior to the Commencement Date shall be subject to all obligations of Tenant under this Lease.

4. Base Rent. Tenant shall pay Base Rent in the amount set forth on Page 1 of this Lease. The first month’s Base Rent, the Security Deposit, and the first monthly installment of estimated Operating Expenses (as hereafter defined) shall be due and payable on the date hereof, and Tenant promises to pay to Landlord without demand, deduction or set-off, monthly installments of Base Rent on or before the first day of each calendar month succeeding the Commencement Date. Payments of Base Rent for any fractional calendar month shall be prorated. All payments required to be made by Tenant to Landlord hereunder (or to such other party as Landlord may from time to time specify in writing) shall be made by check or by Electronic Fund Transfer (“EFT”) of immediately available federal funds before 11:00 a.m., Eastern Time at such place, within the continental United States, as Landlord may from time to time designate to Tenant in writing. The obligation of Tenant to pay Base Rent and other sums to Landlord and the obligations of Landlord under this Lease are independent obligations. Tenant shall have no right at any time to abate, reduce, or set-off any rent due hereunder except as may be expressly provided in this Lease. If Tenant is delinquent in any monthly installment of Base Rent or of estimated Operating Expenses for more than 5 business days, Tenant shall pay to Landlord on demand a late charge equal to 8 percent of such delinquent sum. The provision for such late charge shall be in addition to all of Landlord’s other rights and remedies hereunder or at law and shall not be construed as a penalty.

5. Security Deposit. The Security Deposit shall be held by Landlord as security for the performance of Tenant’s obligations under this Lease. The Security Deposit is not an advance rental deposit or a measure of Landlord’s damages in case of Tenant’s default. Upon each occurrence of an Event of Default (hereinafter defined), Landlord may use all or part of the Security Deposit to pay delinquent payments due under this Lease, and the cost of any damage, injury, expense or liability caused by such Event of Default, without prejudice to any other remedy provided herein or provided by law. Tenant shall pay Landlord on demand the amount that will restore the Security Deposit to its original amount. Landlord’s obligation respecting the Security Deposit is that of a debtor, not a trustee; no interest shall accrue thereon. The Security Deposit shall be the property of Landlord, but shall be paid to Tenant when Tenant’s obligations under this Lease have been completely fulfilled. Landlord shall not be required to keep all or any part of the Security Deposit separate from its general accounts. Tenant waives any limitations set forth in California Civil Code Section 1950.7 limiting the use to which a security deposit may be applied. Landlord shall be released from any obligation with respect to the Security Deposit upon transfer of this Lease and the Premises to a person or entity assuming Landlord’s obligations under this Paragraph 5.

| - 2 - |

6. Operating Expense Payments. During each month of the Lease Term, on the same date that Base Rent is due, Tenant shall pay Landlord an amount equal to 1/12 of the annual cost, as estimated by Landlord from time to time, of Tenant’s Proportionate Share (hereinafter defined) of Operating Expenses for the Project. Payments thereof for any fractional calendar month shall be prorated. The term “Operating Expenses” means all costs and expenses incurred by Landlord with respect to the ownership, maintenance, and operation of the Project including, but not limited to costs of: Taxes (hereinafter defined) and fees payable to tax consultants and attorneys for consultation and contesting taxes; insurance; utilities; maintenance, repair and replacement of all portions of the Project, including without limitation, paving and parking areas, roads, non-structural components of the roofs (including the roof membrane), alleys, and driveways, mowing, landscaping, snow removal, exterior painting, utility lines, heating, ventilation and air conditioning systems, lighting, electrical systems and other mechanical and building systems; amounts paid to contractors and subcontractors for work or services performed in connection with any of the foregoing; charges or assessments of any association to which the Project is subject; property management fees payable to a property manager, including any affiliate of Landlord, or if there is no property manager, an administration fee of 15 percent of Operating Expenses payable to Landlord; security services, if any; trash collection, sweeping and removal; and additions or alterations made by Landlord to the Project or the Building in order to comply with Legal Requirements (other than those expressly required herein to be made by Tenant) or that are appropriate to the continued operation of the Project or the Building as a bulk warehouse facility in the market area, provided that the cost of additions or alterations that are required to be capitalized for federal income tax purposes shall be amortized on a straight line basis over a period equal to the lesser of the useful life thereof for federal income tax purposes or 10 years. Operating Expenses do not include costs, expenses, depreciation or amortization for capital repairs and capital replacements required to be made by Landlord under Paragraph 10 of this Lease, debt service under mortgages or ground rent under ground leases, costs of restoration to the extent of net insurance proceeds received by Landlord with respect thereto, leasing commissions, or the costs of renovating space for tenants.

If Tenant’s total payments of Operating Expenses for any year are less than Tenant’s Proportionate Share of actual Operating Expenses for such year, then Tenant shall pay the difference to Landlord within 30 days after demand, and if more, then Landlord shall retain such excess and credit it against Tenant’s next payments except that during the last calendar year of the Lease Term or any extension terms thereof, Landlord shall refund any such excess within 60 days following the termination of the Lease Term or any extension terms thereof, provided that Tenant is not in default of its obligations under this Lease. For purposes of calculating Tenant’s Proportionate Share of Operating Expenses, a year shall mean a calendar year except the first year, which shall begin on the Commencement Date, and the last year, which shall end on the expiration of this Lease. With respect to Operating Expenses which Landlord allocates to the entire Project, Tenant’s “Proportionate Share” shall be the percentage set forth on the first page of this Lease as Tenant’s Proportionate Share of the Project as reasonably adjusted by Landlord in the future for changes in the physical size of the Premises or the Project; and, with respect to Operating Expenses which Landlord allocates only to the Building, Tenant’s “Proportionate Share” shall be the percentage set forth on the first page of this Lease as Tenant’s Proportionate Share of the Building as reasonably adjusted by Landlord in the future for changes in the physical size of the Premises or the Building. Landlord may equitably increase Tenant’s Proportionate Share for any item of expense or cost reimbursable by Tenant that relates to a repair, replacement, or service that benefits only the Premises or only a portion of the Project or Building that includes the Premises or that varies with occupancy or use. The estimated Operating Expenses for the Premises set forth on the first page of this Lease are only estimates, and Landlord makes no guaranty or warranty that such estimates will be accurate.

7. Utilities. Tenant shall pay for all water, gas, electricity, heat, light, power, telephone, sewer, sprinkler services, refuse and trash collection, and other utilities and services used on the Premises, all maintenance charges for utilities, and any storm sewer charges or other similar charges for utilities imposed by any governmental entity or utility provider, together with any taxes, penalties, surcharges or the like pertaining to Tenant’s use of the Premises. Landlord may cause at Tenant’s expense any utilities to be separately metered or charged directly to Tenant by the provider in the event Landlord reasonably determines that Tenant’s use of such jointly metered utility materially exceeds the use of such jointly metered utility by other tenants in the Building. Tenant shall pay its share of all charges for jointly metered utilities based upon consumption, as reasonably determined by Landlord. No interruption or failure of utilities shall result in the termination of this Lease or the abatement of rent. Tenant agrees to limit use of water and sewer for normal restroom use.

8. Taxes. Landlord shall pay all taxes, assessments and governmental charges (collectively referred to as “Taxes”) that accrue against the Project during the Lease Term, which shall be included as part of the Operating Expenses charged to Tenant. Landlord may contest by appropriate legal proceedings the amount, validity, or application of any Taxes or liens thereof. All capital levies or other taxes assessed or imposed on Landlord upon the rents payable to Landlord under this Lease and any franchise tax, any excise, use, margin, transaction, sales or privilege tax, assessment, levy or charge measured by or based, in whole or in part, upon such rents from the Premises and/or the Project or any portion thereof shall be paid by Tenant to Landlord monthly in estimated installments or upon demand, at the option of Landlord, as additional rent; provided, however, in no event shall Tenant be liable for any net income taxes imposed on Landlord unless such net income taxes are in substitution for any Taxes payable hereunder. If any such tax or excise is levied or assessed directly against Tenant or results from any Tenant-Made Alterations (defined below), then Tenant shall be responsible for and shall pay the same at such times and in such manner as the taxing authority shall require. Tenant shall be liable for all taxes levied or assessed against any personal property or fixtures placed in the Premises, whether levied or assessed against Landlord or Tenant.

| - 3 - |

9. Insurance. Landlord shall maintain all risk or special form property insurance covering the full replacement cost of the Building and commercial general liability insurance on the Project in forms and amounts customary for properties substantially similar to the Project, subject to customary deductibles. Landlord may, but is not obligated to, maintain such other insurance and additional coverages as it may deem necessary, including but not limited to, rent loss insurance. All such insurance shall be included as part of the Operating Expenses charged to Tenant. The Project or Building may be included in a blanket policy (in which case the cost of such insurance allocable to the Project or Building will be determined by Landlord based upon the total insurance cost calculations). Tenant shall also reimburse Landlord for any increased premiums or additional insurance which Landlord reasonably deems necessary as a result of Tenant’s use of the Premises.

Tenant, at its expense, shall maintain during the Lease Term the following insurance, at Tenant’s sole cost and expense: (1) commercial general liability insurance applicable to the Premises and its appurtenances providing, on an occurrence basis, a minimum combined single limit of $2,000,000; and in the event property of Tenant’s invitees or customers are kept in, or about the, Premises, Tenant shall maintain warehouser’s legal liability or bailee customers insurance for the full value of the property of such invitees or customers as determined by the warehouse contract between Tenant and its customer; (2) all risk or special form property insurance covering the full replacement cost of all property and improvements installed or placed in the Premises by Tenant; (3) workers’ compensation insurance as required by the state in which the Premises is located and in amounts as may be required by applicable statute and shall include a waiver of subrogation in favor of Landlord; (4) employers liability insurance of at least $1,000,000; (5) business automobile liability insurance having a combined single limit of not less than $1,000,000 per occurrence insuring Tenant against liability arising out of the ownership maintenance or use of any owned, hired or nonowned automobiles, and (6) business interruption insurance with a limit of liability representing loss of at least approximately 6 months of income. Any company writing any of Tenant’s insurance shall have an A.M. Best rating of not less than A-VIII and provide primary coverage to Landlord (any policy issued to Landlord providing duplicate or similar coverage shall be deemed excess over Tenant’s policies). All commercial general liability and, if applicable, warehouser’s legal liability or bailee customers insurance policies shall name Tenant as a named insured and Landlord, its property manager, and other designees of Landlord as the interest of such designees shall appear, as additional insureds. The limits and types of insurance maintained by Tenant shall not limit Tenant’s liability under this Lease. Tenant shall provide Landlord with certificates of such insurance as required under this Lease prior to the earlier to occur of the Commencement Date or the date Tenant is provided with possession of the Premises, and thereafter upon renewals at least 15 days prior to the expiration of the insurance coverage. Acceptance by Landlord of delivery of any certificates of insurance does not constitute approval or agreement by Landlord that the insurance requirements of this section have been met, and failure of Landlord to identify a deficiency from evidence provided will not be construed as a waiver of Tenant’s obligation to maintain such insurance. In the event any of the insurance policies required to be carried by Tenant under this Lease shall be cancelled prior to the expiration date of such policy, or if Tenant receives notice of any cancellation of such insurance policies from the insurer prior to the expiration date of such policy, Tenant shall: (a) immediately deliver notice to Landlord that such insurance has been, or is to be, cancelled, (b) shall promptly replace such insurance policy in order to assure no lapse of coverage shall occur, and (c) shall deliver to Landlord a certificate of insurance for such policy. The insurance required to be maintained by Tenant hereunder are only Landlord’s minimum insurance requirements and Tenant agrees and understands that such insurance requirements may not be sufficient to fully meet Tenant’s insurance needs.

The all risk or special form property insurance obtained by Landlord and Tenant shall include a waiver of subrogation by the insurers and all rights based upon an assignment from its insured, against Landlord or Tenant, their officers, directors, employees, managers, agents, invitees and contractors, in connection with any loss or damage thereby insured against. Neither party nor its officers, directors, employees, managers, agents, invitees or contractors shall be liable to the other for loss or damage caused by any risk coverable by all risk or special form property insurance, and each party waives any claims against the other party, and its officers, directors, employees, managers, agents, invitees and contractors for such loss or damage. The failure of a party to insure its property shall not void this waiver. Tenant and its agents, employees and contractors shall not be liable for, and Landlord hereby waives all claims against such parties for losses resulting from an interruption of Landlord’s business, or any person claiming through Landlord, resulting from any accident or occurrence in or upon the Premises or the Project from any cause whatsoever, including without limitation, damage caused in whole or in part, directly or indirectly, by the negligence of Tenant or its agents, employees or contractors. Landlord and its agents, employees and contractors shall not be liable for, and Tenant hereby waives all claims against such parties for losses resulting from an interruption of Tenant’s business, or any person claiming through Tenant, resulting from any accident or occurrence in or upon the Premises or the Project from any cause whatsoever, including without limitation, damage caused in whole or in part, directly or indirectly, by the negligence of Landlord or its agents, employees or contractors.

10. Landlord’s Repairs. Landlord shall repair, at its expense and without pass through as an Operating Expense, the structural soundness of the roof (which does not include the roof membrane), the structural soundness of the foundation, and the structural soundness of the exterior walls of the Building in good repair, reasonable wear and tear and uninsured losses and damages caused by Tenant, its agents and contractors excluded. The term “walls” as used in this Paragraph 10 shall not include windows, glass or plate glass, doors or overhead doors, special store fronts, dock bumpers, dock plates or levelers, or office entries. Tenant shall promptly give Landlord written notice of any repair required by Landlord pursuant to this Paragraph 10, after which Landlord shall have a reasonable opportunity to repair.

| - 4 - |

11. Tenant’s Repairs. Landlord, at Tenant’s expense as provided in Paragraph 6, shall maintain in good repair and condition the parking areas and other common areas of the Building, including, but not limited to driveways, alleys, landscape and grounds surrounding the Premises. Subject to Landlord’s obligation in Paragraph 10 and subject to Paragraphs 9 and 15, Tenant, at its expense, shall repair, replace and maintain in good condition all portions of the Premises and all areas, improvements and systems exclusively serving the Premises including, without limitation, dock and loading areas, truck doors, plumbing, water and sewer lines up to points of common connection, fire sprinklers and fire protection systems, entries, doors, ceilings, windows, interior walls, and the interior side of demising walls, and heating, ventilation and air conditioning systems. Such repair and replacements include capital expenditures and repairs whose benefit may extend beyond the Term. Heating, ventilation and air conditioning systems and other mechanical and building systems exclusively serving the Premises shall be maintained at Tenant’s expense pursuant to maintenance service contracts entered into by Tenant or, at Landlord’s election, by Landlord, in which case the costs of such contracts entered into by Landlord shall be included as an Operating Expense. The scope of services and contractors under such maintenance contracts shall be reasonably approved by Landlord. At Landlord’s request, Tenant shall enter into a joint maintenance agreement with any railroad that services the Premises. If Tenant fails to perform any repair or replacement for which it is responsible, Landlord may perform such work and be reimbursed by Tenant within 10 days after demand therefor. Subject to Paragraphs 9 and 15, Tenant shall bear the full cost of any repair or replacement to any part of the Building or Project that results from damage caused by Tenant, its agents, contractors, or invitees and any repair that benefits only the Premises.

12. Tenant-Made Alterations and Trade Fixtures. Any alterations, additions, or improvements made by or on behalf of Tenant to the Premises (“Tenant-Made Alterations”) shall be subject to Landlord’s prior written consent. Tenant shall cause, at its expense, all Tenant-Made Alterations to comply with insurance requirements and with Legal Requirements and shall construct at its expense any alteration or modification required by Legal Requirements as a result of any Tenant-Made Alterations. All Tenant-Made Alterations shall be constructed in a good and workmanlike manner by contractors reasonably acceptable to Landlord and only good grades of materials shall be used. All plans and specifications for any Tenant-Made Alterations shall be submitted to Landlord for its approval. Landlord may monitor construction of the Tenant-Made Alterations. Tenant shall reimburse Landlord for its costs in reviewing plans and specifications and in monitoring construction. Landlord’s right to review plans and specifications and to monitor construction shall be solely for its own benefit, and Landlord shall have no duty to see that such plans and specifications or construction comply with applicable laws, codes, rules and regulations. Tenant shall provide Landlord with the identities and mailing addresses of all persons performing work or supplying materials, prior to beginning such construction, and Landlord may post on and about the Premises notices of non-responsibility pursuant to applicable law. Tenant shall furnish security or make other arrangements satisfactory to Landlord to assure payment for the completion of all work free and clear of liens and shall provide certificates of insurance for worker’s compensation and other coverage in amounts and from an insurance company satisfactory to Landlord protecting Landlord against liability for personal injury or property damage during construction. Upon completion of any Tenant-Made Alterations, Tenant shall deliver to Landlord sworn statements setting forth the names of all contractors and subcontractors who did work on the Tenant-Made Alterations and final lien waivers from all such contractors and subcontractors. Upon surrender of the Premises, all Tenant-Made Alterations and any leasehold improvements constructed by Landlord or Tenant shall remain on the Premises as Landlord’s property, except to the extent Landlord requires removal at Tenant’s expense of any such items or Landlord and Tenant have otherwise agreed in writing in connection with Landlord’s consent to any Tenant-Made Alterations. Tenant shall repair any damage caused by the removal of such Tenant-Made Alterations upon surrender of the Premises.

Tenant, at its own cost and expense and without Landlord’s prior approval, may erect such shelves, racking, bins, machinery and trade fixtures (collectively “Trade Fixtures”) in the ordinary course of its business provided that such items do not alter the basic character of the Premises, do not overload or damage the Premises, and may be removed without injury to the Premises, and the construction, erection, and installation thereof complies with all Legal Requirements and with Landlord’s requirements set forth above. Tenant shall remove its Trade Fixtures and shall repair any damage caused by such removal upon surrender of the Premises.

13. Signs. Tenant shall not make any changes to the exterior of the Premises, install any exterior lights, decorations, balloons, flags, pennants, banners, or painting, or erect or install any signs, windows or door lettering, placards, decorations, or advertising media of any type which can be viewed from the exterior of the Premises, without Landlord’s prior written consent, which consent shall not be unreasonable withheld. Upon surrender or vacation of the Premises, Tenant shall have removed all signs and repair, paint, and/or replace the building facia surface to which its signs are attached. Tenant shall obtain all applicable governmental permits and approvals for sign and exterior treatments. All signs, decorations, advertising media, blinds, draperies and other window treatment or bars or other security installations visible from outside the Premises shall be subject to Landlord’s approval and conform in all respects to Landlord’s requirements.

14. Parking. Tenant shall be entitled to park in common with other tenants of the Project in those areas designated for nonreserved parking. Landlord may allocate parking spaces among Tenant and other tenants in the Project if Landlord reasonably determines that such parking facilities are becoming crowded. Landlord shall not be responsible for enforcing Tenant’s parking rights against any third parties.

15. Restoration. If at any time during the Lease Term the Premises are damaged by a fire or other casualty, Landlord shall notify Tenant within 60 days after such damage as to the amount of time Landlord reasonably estimates it will take to restore the Premises. If the restoration time is estimated to exceed 6 months, either Landlord or Tenant may elect to terminate this Lease upon notice to the other party given no later than 30 days after Landlord’s notice. If neither party elects to terminate this Lease or if Landlord estimates that restoration will take 6 months or less, then, subject to receipt of sufficient insurance proceeds, Landlord shall promptly restore the Premises excluding the improvements installed by Tenant or by Landlord and paid by Tenant, subject to delays arising from the collection of insurance proceeds or from Force Majeure events. Tenant at Tenant’s expense shall promptly perform, subject to delays arising from the collection of insurance proceeds, or from Force Majeure events (as defined in Paragraph 33), all repairs or restoration not required to be done by Landlord and shall promptly re-enter the Premises and commence doing business in accordance with this Lease. Notwithstanding the foregoing, either party may terminate this Lease if the Premises are damaged during the last year of the Lease Term and Landlord reasonably estimates that it will take more than one month to repair such damage. Base Rent and Operating Expenses shall be abated for the period of repair and restoration commencing on the date of such casualty event in the proportion which the area of the Premises, if any, which is not usable by Tenant bears to the total area of the Premises. Such abatement shall be the sole remedy of Tenant, and except as provided herein, Tenant waives any right to terminate the Lease by reason of damage or casualty loss.

| - 5 - |

Notwithstanding anything contained in the Lease to the contrary, to the extent the damage to the Project is attributable to Tenant, Tenant shall pay to Landlord with respect to any damage to the Project an amount of the commercially reasonable deductible under Landlord’s insurance policy, not to exceed $10,000.00, within 30 days after presentment of Landlord’s invoice.

16. Condemnation. If any part of the Premises or the Project should be taken for any public or quasi-public use under governmental law, ordinance, or regulation, or by right of eminent domain, or by private purchase in lieu thereof (a “Taking” or “Taken”), and the Taking would materially interfere with or impair Landlord’s ownership or operation of the Project, then upon written notice by Landlord this Lease shall terminate and Base Rent shall be apportioned as of said date. If part of the Premises shall be Taken, and this Lease is not terminated as provided above, the Base Rent payable hereunder during the unexpired Lease Term shall be reduced to such extent as may be fair and reasonable under the circumstances. In the event of any such Taking, Landlord shall be entitled to receive the entire price or award from any such Taking without any payment to Tenant, and Tenant hereby assigns to Landlord Tenant’s interest, if any, in such award. Tenant shall have the right, to the extent that same shall not diminish Landlord’s award, to make a separate claim against the condemning authority (but not Landlord) for such compensation as may be separately awarded or recoverable by Tenant for moving expenses and damage to Tenant’s Trade Fixtures, if a separate award for such items is made to Tenant.

17. Assignment and Subletting. Without Landlord’s prior written consent, which shall not be unreasonably withheld conditioned or delayed, and with the exception of Tenant Affiliates (defined below) and direct supply chain partners, Tenant shall not assign this Lease or sublease the Premises or any part thereof or mortgage, pledge, or hypothecate its leasehold interest or grant any concession or license within the Premises and any attempt to do any of the foregoing shall be void and of no effect. It shall be reasonable for the Landlord to withhold, delay or condition its consent, where required, to any assignment or sublease in any of the following instances: (i) the assignee or sublessee does not have a net worth calculated according to generally accepted accounting principles at least equal to the greater of the net worth of Tenant immediately prior to such assignment or sublease or the net worth of the Tenant at the time it executed the Lease; (ii) occupancy of the Premises by the assignee or sublessee would, in Landlord’s opinion, violate any agreement binding upon Landlord or the Project with regard to the identity of tenants, usage in the Project, or similar matters; (iii) the identity or business reputation of the assignee or sublessee will, in the good faith judgment of Landlord, tend to damage the goodwill or reputation of the Project; (iv) the assignment or sublease is to another tenant in the Project and is at rates which are below those charged by Landlord for comparable space in the Project; or (v) in the case of a sublease, the subtenant has not acknowledged that the Lease controls over any inconsistent provision in the sublease. The foregoing criteria shall not exclude any other reasonable basis for Landlord to refuse its consent to such assignment or sublease. Any approved assignment or sublease shall be expressly subject to the terms and conditions of this Lease. Tenant shall provide to Landlord all information concerning the assignee or sublessee as Landlord may reasonably request. Landlord may revoke its consent immediately and without notice if, as of the effective date of the assignment or sublease, there has occurred and is continuing any default under the Lease. For purposes of this paragraph, a transfer of the ownership interests controlling Tenant shall be deemed an assignment of this Lease unless such ownership interests are publicly traded. Notwithstanding the above, Tenant may assign or sublet the Premises, or any part thereof, to any entity controlling Tenant, controlled by Tenant or under common control with Tenant (a “Tenant Affiliate”), without the prior written consent of Landlord. Tenant shall reimburse Landlord for all of Landlord’s reasonable expenses in connection with any assignment or sublease not to exceed $1,500.00. This Lease shall be binding upon Tenant and its successors and permitted assigns. Upon Landlord’s receipt of Tenant’s written notice of a desire to assign or sublet the Premises, or any part thereof (other than to a Tenant Affiliate), Landlord may, by giving written notice to Tenant within 30 days after receipt of Tenant’s notice, terminate this Lease with respect to the space described in Tenant’s notice, as of the date specified in Tenant’s notice for the commencement of the proposed assignment or sublease.

Notwithstanding any assignment or subletting, Tenant and any guarantor or surety of Tenant’s obligations under this Lease shall at all times remain fully responsible and liable for the payment of the rent and for compliance with all of Tenant’s other obligations under this Lease (regardless of whether Landlord’s approval has been obtained for any such assignments or sublettings). In the event that the rent due and payable by a sublessee or assignee (or a combination of the rental payable under such sublease or assignment plus any bonus or other consideration therefor or incident thereto) exceeds the rental payable under this Lease, then Tenant shall be bound and obligated to pay Landlord as additional rent hereunder all such excess rental and other excess consideration within 10 days following receipt thereof by Tenant; provided in the event of a sublease which is less than 100% of the Premises such excess rental and other consideration shall be applied on a square foot basis.

If this Lease be assigned or if the Premises be subleased (whether in whole or in part) or in the event of the mortgage, pledge, or hypothecation of Tenant’s leasehold interest or grant of any concession or license within the Premises or if the Premises be occupied in whole or in part by anyone other than Tenant, then upon a default by Tenant hereunder Landlord may collect rent from the assignee, sublessee, mortgagee, pledgee, party to whom the leasehold interest was hypothecated, concessionee or licensee or other occupant and, except to the extent set forth in the preceding paragraph, apply the amount collected to the next rent payable hereunder; and all such rentals collected by Tenant shall be held in trust for Landlord and immediately forwarded to Landlord. No such transaction or collection of rent or application thereof by Landlord, however, shall be deemed a waiver of these provisions or a release of Tenant from the further performance by Tenant of its covenants, duties, or obligations hereunder.

| - 6 - |

18. Indemnification. Except for the negligence of Landlord, its agents, employees or contractors, and to the extent permitted by law, Tenant agrees to indemnify, defend and hold harmless Landlord, and Landlord’s agents, employees and contractors, from and against any and all losses, liabilities, damages, costs and expenses (including attorneys’ fees) resulting from claims by third parties for injuries to any person and damage to or theft or misappropriation or loss of property occurring in or about the Project and arising from the use and occupancy of the Premises or from any activity, work, or thing done, permitted or suffered by Tenant in or about the Premises or due to any other act or omission of Tenant, its subtenants, assignees, invitees, employees, contractors and agents. The furnishing of insurance required hereunder shall not be deemed to limit Tenant’s obligations under this Paragraph 18.

19. Inspection and Access. Upon providing 24 hours advance notice (except in the event of an emergency, in which case no advance notice is required), Landlord and its agents, representatives, and contractors may enter the Premises at any reasonable time to inspect the Premises and to make such repairs as may be required or permitted pursuant to this Lease and for any other business purpose. Upon providing 24 hours advance notice, Landlord and Landlord’s representatives may enter the Premises during business hours for the purpose of showing the Premises to prospective purchasers and, during the last year of the Lease Term, to prospective tenants. Landlord may erect a suitable sign on the Premises stating the Premises are available to let or that the Project is available for sale. Landlord may grant easements, make public dedications, designate and modify common areas and create restrictions on or about the Premises, provided that no such easement, dedication, designation, modification or restriction materially interferes with Tenant’s use or occupancy of the Premises. At Landlord’s request, Tenant shall execute such instruments as may be necessary for such easements, dedications or restrictions. Access, as used in this Paragraph 19, shall be granted to Landlord upon Landlord’s prior notice to Tenant and at such times so as to minimize, so far as may be reasonable under the circumstances, any material disturbance to Tenant’s operations.

20. Quiet Enjoyment. If Tenant shall perform all of the covenants and agreements herein required to be performed by Tenant, Tenant shall, subject to the terms of this Lease, at all times during the Lease Term, have peaceful and quiet enjoyment of the Premises against any person claiming by, through or under Landlord.

21. Surrender. Upon termination of the Lease Term or earlier termination of Tenant’s right of possession, Tenant shall surrender the Premises to Landlord in the same condition as received ordinary wear and tear, casualty loss and condemnation covered by Paragraphs 15 and 16 excepted and otherwise in accordance with the Move Out Conditions Addendum attached hereto. Without limiting the foregoing, Tenant shall remove any odor which may exist in the Premises resulting from Tenant’s occupancy of the Premises upon the termination of the Lease Term or earlier termination of Tenant’s right of possession. Any Trade Fixtures, Tenant-Made Alterations and property not so removed by Tenant as permitted or required herein shall be deemed abandoned and may be stored, removed, and disposed of by Landlord at Tenant’s expense, and Tenant waives all claims against Landlord for any damages resulting from Landlord’s retention and disposition of such property. All obligations of Tenant hereunder not fully performed as of the termination of the Lease Term shall survive the termination of the Lease Term, including without limitation, indemnity obligations, payment obligations with respect to Operating Expenses and obligations concerning the condition and repair of the Premises.

22. Holding Over. If Tenant retains possession of the Premises after the termination of the Lease Term, unless otherwise agreed in writing, such possession shall be subject to immediate termination by Landlord at any time, and all of the other terms and provisions of this Lease (excluding any expansion or renewal option or other similar right or option) shall be applicable during such holdover period, except that Tenant shall pay Landlord from time to time, upon demand, as Base Rent for the holdover period, an amount equal to 150% of the Base Rent in effect on the termination date, computed on a monthly basis for each month or part thereof during such holding over. All other payments shall continue under the terms of this Lease. In addition, Tenant shall be liable for all damages incurred by Landlord as a result of such holding over. No holding over by Tenant, whether with or without consent of Landlord, shall operate to extend this Lease except as otherwise expressly provided, and this Paragraph 22 shall not be construed as consent for Tenant to retain possession of the Premises. For purposes of this Paragraph 22, “possession of the Premises” shall continue until, among other things, Tenant has delivered all keys to the Premises to Landlord, Landlord has complete and total dominion and control over the Premises, and Tenant has completely fulfilled all obligations required of it upon termination of the Lease as set forth in this Lease, including, without limitation, those concerning the condition and repair of the Premises.

23. Events of Default. Each of the following events shall be an event of default (“Event of Default”) by Tenant under this Lease:

(i) Tenant shall fail to pay any installment of Base Rent or any other payment required herein when due, and such failure shall continue for a period of 5 days from the date such payment was due.

(ii) Tenant or any guarantor or surety of Tenant’s obligations hereunder shall (A) make a general assignment for the benefit of creditors; (B) commence any case, proceeding or other action seeking to have an order for relief entered on its behalf as a debtor or to adjudicate it as bankrupt or insolvent, or seeking reorganization, arrangement, adjustment, liquidation, dissolution or composition of it or its debts or seeking appointment of a receiver, trustee, custodian or other similar official for it or for all or of any substantial part of its property (collectively a “proceeding for relief”);; or”); (C) become the subject of any proceeding for relief which is not dismissed within 60 days of its filing or entry; or () die or suffer a legal disability (if Tenant, guarantor, or surety is an individual) or be dissolved or otherwise fail to maintain its legal existence (if Tenant, guarantor or surety is a corporation, partnership or other entity).

| - 7 - |

(iii) Any insurance required to be maintained by Tenant pursuant to this Lease shall be cancelled or terminated or shall expire or shall be reduced or materially changed, except, in each case, as permitted in this Lease.

(iv) Tenant shall not occupy or shall vacate the Premises whether or not Tenant is in monetary or other default under this Lease. Tenant’s vacating of the Premises shall not constitute an Event of Default if, prior to vacating the Premises, Tenant has made arrangements reasonably acceptable to Landlord to (a) ensure that Tenant’s insurance for the Premises will not be voided or cancelled with respect to the Premises as a result of such vacancy, (b) ensure that the Premises are secured and not subject to vandalism, and (c) ensure that the Premises will be properly maintained after such vacation, including, but not limited to, keeping the heating, ventilation and cooling systems maintenance contracts required by this Lease in full force and effect and maintaining the utility services. Tenant shall inspect the Premises at least once each month and report monthly in writing to Landlord on the condition of the Premises.

(v) Tenant shall attempt or there shall occur any assignment, subleasing or other transfer of Tenant’s interest in or with respect to this Lease except as otherwise permitted in this Lease.

(vi) Tenant shall fail to discharge any lien placed upon the Premises in violation of this Lease within 20 days after any such lien or encumbrance is filed against the Premises.

(vii) Tenant shall fail to comply with any provision of this Lease other than those specifically referred to in this Paragraph 23, and except as otherwise expressly provided herein, such default shall continue for more than 30 days after Landlord shall have given Tenant written notice of such default (said notice being in lieu of, and not in addition to, any notice required as a prerequisite to a forcible entry and detainer or similar action for possession of the Premises).

(viii) Tenant agrees that any notice given by Landlord pursuant to this Paragraph of the Lease shall satisfy the requirements for notice under California Code of Civil Procedure Section 1161, and Landlord shall not be required to give any additional notice in order to be entitled to commence an unlawful detainer proceeding.

24. Landlord’s Remedies. Upon each occurrence of an Event of Default and so long as such Event of Default shall be continuing, Landlord may at any time thereafter at its election: terminate this Lease or Tenant’s right of possession, (but Tenant shall remain liable as hereinafter provided) and/or pursue any other remedies at law or in equity. Upon the termination of this Lease or termination of Tenant’s right of possession, it shall be lawful for Landlord, without formal demand or notice of any kind, to re-enter the Premises by summary dispossession proceedings or any other action or proceeding authorized by law and to remove Tenant and all persons and property therefrom. If Landlord re-enters the Premises, Landlord shall have the right to keep in place and use, or remove and store, all of the furniture, fixtures and equipment at the Premises.

Except as otherwise provided in the next paragraph, if Tenant breaches this Lease and abandoned the Premises prior to the end of the term hereof, or if Tenant’s right to possession is terminated by Landlord because of an Event of Default by Tenant under this Lease, this Lease shall terminate. Upon such termination, Landlord may recover from Tenant the following, as provided in Section 1951.2 of the Civil Code of California: (i) the worth at the time of award of the unpaid Base Rent and other charges under this Lease that had been earned at the time of termination; (ii) the worth at the time of award of the amount by which the reasonable value of the unpaid Base Rent and other charges under this Lease which would have been earned after termination until the time of award exceeds the amount of such rental loss that Tenant proves could have been reasonable avoided; (iii) the worth at the time of award by which the reasonable value of the unpaid Base Rent and other charges under this Lease for the balance of the term of this Lease after the time of award exceeds the amount of such rental loss that Tenant proves could have been reasonably avoided; and (iv) any other amount necessary to compensate Landlord for all the detriment proximately caused by Tenant’s failure to perform its obligations under this Lease or that in the ordinary course of things would be likely to result therefrom. As used herein, the following terms are defined: (a) The “worth at the time of award” of the amounts referred to in Sections (i) and (ii) is computed by allowing interest at the lesser of 18 percent per annum or the maximum lawful rate. The “worth at the time of award” of the amount referred to in Section (iii) is computed by discounting such amount at the discount rate of the Federal Reserve Bank of San Francisco at the time of award plus one percent; (b) The “time of award” as used in clauses (i), (ii), and (iii) above is the date on which judgment is entered by a court of competent jurisdiction; (c) The “reasonable value” of the amount referred to in clause (ii) above is computed by determining the mathematical product of (1) the “reasonable annual rental value” (as defined herein) and (2) the number of years, including fractional parts thereof, between the date of termination and the time of award. The “reasonable value” of the amount referred to in clause (iii) is computed by determining the mathematical product of (1) the annual Base Rent and other charges under this Lease and (2) the number of years including fractional parts thereof remaining in the balance of the term of this Lease after the time of award. Tenant acknowledges and agrees that the term “detriment proximately caused by Tenant’s failure to perform its obligations under this Lease” includes, without limitation, the value of any abated or free rent given to Tenant.

| - 8 - |

Even if Tenant has breached this Lease and abandoned the Premises, this Lease shall continue in effect for so long as Landlord does not terminate Tenant’s right to possession, and Landlord may enforce all its rights and remedies under this Lease, including the right to recover rent as it becomes due. This remedy is intended to be the remedy described in California Civil Code Section 1951.4, and the following provision from such Civil Code Section is hereby repeated: “The Lessor has the remedy described in California Civil Code Section 1951.4 (lessor may continue lease in effect after lessee’s breach and abandonment and recover rent as it becomes due, if lessee has right to sublet or assign subject only to reasonable limitations).” Any such payments due Landlord shall be made upon demand therefor from time to time and Tenant agrees that Landlord may file suit to recover any sums falling due from time to time. Notwithstanding any such reletting without termination, Landlord may at any time thereafter elect in writing to terminate this Lease for such previous breach.

Exercise by Landlord of any one or more remedies hereunder granted or otherwise available shall not be deemed to be an acceptance of surrender of the Premises and/or a termination of this Lease by Landlord, whether by agreement or by operation of law, it being understood that such surrender and/or termination can be effected only by the written agreement of Landlord and Tenant. Any law, usage, or custom to the contrary notwithstanding, Landlord shall have the right at all times to enforce the provisions of this Lease in strict accordance with the terms hereof; and the failure of Landlord at any time to enforce its rights under this Lease strictly in accordance with same shall not be construed as having created a custom in any way or manner contrary to the specific terms, provisions, and covenants of this Lease or as having modified the same. Tenant and Landlord further agree that forbearance or waiver by Landlord to enforce its rights pursuant to this Lease or at law or in equity, shall not be a waiver of Landlord’s right to enforce one or more of its rights in connection with any subsequent default. A receipt by Landlord of rent or other payment with knowledge of the breach of any covenant hereof shall not be deemed a waiver of such breach, and no waiver by Landlord of any provision of this Lease shall be deemed to have been made unless expressed in writing and signed by Landlord. To the greatest extent permitted by law, Tenant waives all right of redemption in case Tenant shall be dispossessed by a judgment or by warrant of any court or judge. The terms “enter,” “re-enter,” “entry” or “re-entry,” as used in this Lease, are not restricted to their technical legal meanings. Any reletting of the Premises shall be on such terms and conditions as Landlord in its sole discretion may determine (including without limitation a term different than the remaining Lease Term, rental concessions, alterations and repair of the Premises, lease of less than the entire Premises to any tenant and leasing any or all other portions of the Project before reletting the Premises). Landlord shall not be liable, nor shall Tenant’s obligations hereunder be diminished because of, Landlord’s failure to relet the Premises or collect rent due in respect of such reletting.

25. Tenant’s Remedies/Limitation of Liability. Landlord shall not be in default hereunder unless Landlord fails to perform any of its obligations hereunder within 30 days after written notice from Tenant specifying such failure (unless such performance will, due to the nature of the obligation, require a period of time in excess of 30 days, then after such period of time as is reasonably necessary). All obligations of Landlord hereunder shall be construed as covenants, not conditions; and, except as may be otherwise expressly provided in this Lease, Tenant may not terminate this Lease for breach of Landlord’s obligations hereunder. All obligations of Landlord under this Lease will be binding upon Landlord only during the period of its ownership of the Premises and not thereafter. The term “Landlord” in this Lease shall mean only the owner, for the time being of the Premises, and in the event of the transfer by such owner of its interest in the Premises, such owner shall thereupon be released and discharged from all obligations of Landlord thereafter accruing, but such obligations shall be binding during the Lease Term upon each new owner for the duration of such owner’s ownership. Any liability of Landlord under this Lease shall be limited solely to its interest in the Project, and in no event shall any personal liability be asserted against Landlord in connection with this Lease nor shall any recourse be had to any other property or assets of Landlord.

26. Landlord’s Lien/Security Interest. Landlord hereby waives any right of distraint or statutory lien for rent against Tenant’s property on the Premises that would permit Landlord to possess or sell Tenant’s property before obtaining a judgment. Landlord does not waive any right to obtain and enforce any judgment lien or any pre-judgment rights and remedies other than those described above.

27. Subordination. This Lease and Tenant’s interest and rights hereunder are and shall be subject and subordinate at all times to the lien of any first mortgage, now existing or hereafter created on or against the Project or the Premises, and all amendments, restatements, renewals, modifications, consolidations, refinancing, assignments and extensions thereof, without the necessity of any further instrument or act on the part of Tenant. Tenant agrees, at the election of the holder of any such mortgage, to attorn to any such holder. Tenant agrees upon demand to execute, acknowledge and deliver such instruments, confirming such subordination and such instruments of attornment as shall be requested by any such holder. Notwithstanding the foregoing, any such holder may at any time subordinate its mortgage to this Lease, without Tenant’s consent, by notice in writing to Tenant, and thereupon this Lease shall be deemed prior to such mortgage without regard to their respective dates of execution, delivery or recording and in that event such holder shall have the same rights with respect to this Lease as though this Lease had been executed prior to the execution, delivery and recording of such mortgage and had been assigned to such holder. The term “mortgage” whenever used in this Lease shall be deemed to include deeds of trust, security assignments and any other encumbrances, and any reference to the “holder” of a mortgage shall be deemed to include the beneficiary under a deed of trust.

28. Mechanic’s Liens. Tenant has no express or implied authority to create or place any lien or encumbrance of any kind upon, or in any manner to bind the interest of Landlord or Tenant in, the Premises or to charge the rentals payable hereunder for any claim in favor of any person dealing with Tenant, including those who may furnish materials or perform labor for any construction or repairs. Tenant covenants and agrees that it will pay or cause to be paid all sums legally due and payable by it on account of any labor performed or materials furnished in connection with any work performed on the Premises and that it will save and hold Landlord harmless from all loss, cost or expense based on or arising out of asserted claims or liens against the leasehold estate or against the interest of Landlord in the Premises or under this Lease. Tenant shall give Landlord immediate written notice of the placing of any lien or encumbrance against the Premises and cause such lien or encumbrance to be discharged within 20 days of the filing or recording thereof; provided, however, Tenant may contest such liens or encumbrances as long as such contest prevents foreclosure of the lien or encumbrance and Tenant causes such lien or encumbrance to be bonded or insured over in a manner satisfactory to Landlord within such 20 day period.

| - 9 - |

29. Estoppel Certificates. Tenant agrees, from time to time, within 10 days after request of Landlord, to execute and deliver to Landlord, or Landlord’s designee, any estoppel certificate requested by Landlord, stating that this Lease is in full force and effect, the date to which rent has been paid, that Landlord is not in default hereunder (or specifying in detail the nature of Landlord’s default), the termination date of this Lease and such other matters pertaining to this Lease as may be requested by Landlord. Tenant’s obligation to furnish each estoppel certificate in a timely fashion is a material inducement for Landlord’s execution of this Lease. No cure or grace period provided in this Lease shall apply to Tenant’s obligations to timely deliver an estoppel certificate.

30. Environmental Requirements. Except for Hazardous Material contained in products used by Tenant in de minimis quantities for ordinary cleaning and office purposes, and except for propane used in Tenant’s forklifts in the normal course of its business, and except for Hazardous Materials contained in products stored and/or distributed during Tenant’s normal course of business in their original, sealed, and unopened containers, Tenant shall not permit or cause any party to bring any Hazardous Material upon the Premises or transport, store, use, generate, manufacture or release any Hazardous Material in or about the Premises without Landlord’s prior written consent. Tenant, at its sole cost and expense, shall operate its business in the Premises in strict compliance with all Environmental Requirements and shall remediate in a manner satisfactory to Landlord any Hazardous Materials released on or from the Project by Tenant, its agents, employees, contractors, subtenants or invitees. Tenant shall complete and certify to disclosure statements as requested by Landlord from time to time relating to Tenant’s transportation, storage, use, generation, manufacture or release of Hazardous Materials on the Premises. The term “Environmental Requirements” means all applicable present and future statutes, regulations, ordinances, rules, codes, judgments, orders or other similar enactments of any governmental authority or agency regulating or relating to health, safety, or environmental conditions on, under, or about the Premises or the environment, including without limitation, the following: the Comprehensive Environmental Response, Compensation and Liability Act; the Resource Conservation and Recovery Act; and all state and local counterparts thereto, and any regulations or policies promulgated or issued thereunder. The term “Hazardous Materials” means and includes any substance, material, waste, pollutant, or contaminant listed or defined as hazardous or toxic, under any Environmental Requirements, asbestos and petroleum, including crude oil or any fraction thereof, natural gas liquids, liquefied natural gas, or synthetic gas usable for fuel (or mixtures of natural gas and such synthetic gas). As defined in Environmental Requirements, Tenant is and shall be deemed to be the “operator” of Tenant’s “facility” and the “owner” of all Hazardous Materials brought on the Premises by Tenant, its agents, employees, contractors or invitees, and the wastes, by-products, or residues generated, resulting, or produced therefrom. No cure or grace period provided in this Lease shall apply to Tenant’s obligations to comply with the terms and conditions of this Paragraph 30.

Notwithstanding anything to the contrary in this Paragraph 30, Tenant shall have no liability of any kind to Landlord as to Hazardous Materials on the Premises caused or permitted by (i) Landlord, its agents, employees, contractors or invitees; or (ii) any other tenants in the Project or their agents, employees, contractors, subtenants, assignees or invitees.

Tenant shall indemnify, defend, and hold Landlord harmless from and against any and all losses (including, without limitation, diminution in value of the Premises or the Project and loss of rental income from the Project), claims, demands, actions, suits, damages (including, without limitation, punitive damages), expenses (including, without limitation, remediation, removal, repair, corrective action, or cleanup expenses), and costs (including, without limitation, actual attorneys’ fees, consultant fees or expert fees and including, without limitation, removal or management of any asbestos brought into the property or disturbed in breach of the requirements of this Paragraph 30, regardless of whether such removal or management is required by law) which are brought or recoverable against, or suffered or incurred by Landlord as a result of any release of Hazardous Materials for which Tenant is obligated to remediate as provided above or any other breach of the requirements under this Paragraph 30 by Tenant, its agents, employees, contractors, subtenants, assignees or invitees, regardless of whether Tenant had knowledge of such noncompliance. The obligations of Tenant under this Paragraph 30 shall survive any termination of this Lease.

Landlord shall have access to, and a right to perform inspections and tests of, the Premises to determine Tenant’s compliance with Environmental Requirements, its obligations under this Paragraph 30, or the environmental condition of the Premises. Access shall be granted to Landlord upon Landlord’s prior notice to Tenant and at such times so as to minimize, so far as may be reasonable under the circumstances, any disturbance to Tenant’s operations. Such inspections and tests shall be conducted at Landlord’s expense, unless such inspections or tests reveal that Tenant has not complied with any Environmental Requirement, in which case Tenant shall reimburse Landlord for the reasonable cost of such inspection and tests. Landlord’s receipt of or satisfaction with any environmental assessment in no way waives any rights that Landlord holds against Tenant.

31. Rules and Regulations. Tenant shall, at all times during the Lease Term and any extension thereof, comply with all reasonable rules and regulations at any time or from time to time established by Landlord covering use of the Premises and the Project. The current Project rules and regulations are attached hereto as Exhibit B. In the event of any conflict between said rules and regulations and other provisions of this Lease, the other terms and provisions of this Lease shall control. Landlord shall not have any liability or obligation for the breach of any rules or regulations by other tenants in the Project.

| - 10 - |

32. Security Service. Tenant acknowledges and agrees that, while Landlord may patrol the Project, Landlord is not providing any security services with respect to the Premises and that Landlord shall not be liable to Tenant for, and Tenant waives any claim against Landlord with respect to, any loss by theft or any other damage suffered or incurred by Tenant in connection with any unauthorized entry into the Premises or any other breach of security with respect to the Premises.

33. Force Majeure. Landlord shall not be held responsible for delays in the performance of its obligations hereunder when caused by strikes, lockouts, labor disputes, acts of God, inability to obtain labor or materials or reasonable substitutes therefor, governmental restrictions, governmental regulations, governmental controls, delay in issuance of permits, enemy or hostile governmental action, civil commotion, fire or other casualty, and other causes beyond the reasonable control of Landlord (“Force Majeure”).

34. Entire Agreement. This Lease constitutes the complete agreement of Landlord and Tenant with respect to the subject matter hereof. No representations, inducements, promises or agreements, oral or written, have been made by Landlord or Tenant, or anyone acting on behalf of Landlord or Tenant, which are not contained herein, and any prior agreements, promises, negotiations, or representations are superseded by this Lease. This Lease may not be amended except by an instrument in writing signed by both parties hereto.

35. Severability. If any clause or provision of this Lease is illegal, invalid or unenforceable under present or future laws, then and in that event, it is the intention of the parties hereto that the remainder of this Lease shall not be affected thereby. It is also the intention of the parties to this Lease that in lieu of each clause or provision of this Lease that is illegal, invalid or unenforceable, there be added, as a part of this Lease, a clause or provision as similar in terms to such illegal, invalid or unenforceable clause or provision as may be possible and be legal, valid and enforceable.

36. Brokers. Tenant represents and warrants that it has dealt with no broker, agent or other person in connection with this transaction and that no broker, agent or other person brought about this transaction, other than the broker, if any, set forth on the first page of this Lease, and Tenant agrees to indemnify and hold Landlord harmless from and against any claims by any other broker, agent or other person claiming a commission or other form of compensation by virtue of having dealt with Tenant with regard to this leasing transaction.

37. Miscellaneous. (a) Any payments or charges due from Tenant to Landlord hereunder shall be considered rent for all purposes of this Lease.

(b) If and when included within the term “Tenant,” as used in this instrument, there is more than one person, firm or corporation, each shall be jointly and severally liable for the obligations of Tenant.

(c) All notices required or permitted to be given under this Lease shall be in writing and shall be sent by registered or certified mail, return receipt requested, or by a reputable national overnight courier service, postage prepaid, or by hand delivery addressed to Landlord at 17777 Center Court Drive North, Suite 100, Cerritos, California 90703, with a copy sent to Landlord at 4545 Airport Way, Denver, Colorado 80239, Attention: General Counsel, and to Tenant at 25731 Commercentre Drive, Lake Forest, California 92630 with copy sent to Jaime R. Quezon, Esq, 805 W Azeele Street, Tampa, FL 33606. Either party may by notice given aforesaid change its address for all subsequent notices or add an additional party to be copied on all subsequent notices. Except where otherwise expressly provided to the contrary, notice shall be deemed given upon delivery.

(d) Except as otherwise expressly provided in this Lease or as otherwise required by law, Landlord retains the absolute right to withhold any consent or approval.

(e) At Landlord’s request from time to time Tenant shall furnish Landlord with true and complete copies of its most recent annual and quarterly financial statements prepared by Tenant or Tenant’s accountants and any other financial information or summaries that Tenant typically provides to its lenders or shareholders. Any and all information provided by Tenant to Landlord pursuant to this Paragraph shall remain confidential and Landlord shall not disclose to any third party whatsoever other than prospective lenders or buyers of the Building bound by confidentiality agreement or as required by law.

(f) Neither this Lease nor a memorandum of lease shall be filed by or on behalf of Tenant in any public record. Landlord may prepare and file, and upon request by Landlord Tenant will execute, a memorandum of lease.

(g) The normal rule of construction to the effect that any ambiguities are to be resolved against the drafting party shall not be employed in the interpretation of this Lease or any exhibits or amendments hereto.

(h) The submission by Landlord to Tenant of this Lease shall have no binding force or effect, shall not constitute an option for the leasing of the Premises, nor confer any right or impose any obligations upon either party until execution of this Lease by both parties.

(i) Words of any gender used in this Lease shall be held and construed to include any other gender, and words in the singular number shall be held to include the plural, unless the context otherwise requires. The captions inserted in this Lease are for convenience only and in no way define, limit or otherwise describe the scope or intent of this Lease, or any provision hereof, or in any way affect the interpretation of this Lease.

(j) Any amount not paid by Tenant within 5 business days after its due date in accordance with the terms of this Lease shall bear interest from such due date until paid in full at the lesser of the highest rate permitted by applicable law or 15 percent per year. It is expressly the intent of Landlord and Tenant at all times to comply with applicable law governing the maximum rate or amount of any interest payable on or in connection with this Lease. If applicable law is ever judicially interpreted so as to render usurious any interest called for under this Lease, or contracted for, charged, taken, reserved, or received with respect to this Lease, then it is Landlord’s and Tenant’s express intent that all excess amounts theretofore collected by Landlord be credited on the applicable obligation (or, if the obligation has been or would thereby be paid in full, refunded to Tenant), and the provisions of this Lease immediately shall be deemed reformed and the amounts thereafter collectible hereunder reduced, without the necessity of the execution of any new document, so as to comply with the applicable law, but so as to permit the recovery of the fullest amount otherwise called for hereunder.

| - 11 - |

(k) Construction and interpretation of this Lease shall be governed by the laws of the state in which the Project is located, excluding any principles of conflicts of laws.

(l) Time is of the essence as to the performance of Tenant’s and Landlord’s obligations under this Lease.

(m) All exhibits and addenda attached hereto are hereby incorporated into this Lease and made a part hereof. In the event of any conflict between such exhibits or addenda and the terms of this Lease, such exhibits or addenda shall control.

(n) In the event either party hereto initiates litigation to enforce the terms and provisions of this Lease, the non-prevailing party in such action shall reimburse the prevailing party for its reasonable attorney’s fees, filing fees, and court costs.

(o) Tenant agrees and understands that Landlord shall have the right (provided that the exercise of Landlord’s rights does not adversely affect Tenant’s use and occupancy of the Premises or subject Tenant to additional costs), without Tenant’s consent, to place a solar electric generating system on the roof of the Building or enter into a lease for the roof of the Building whereby such roof tenant shall have the right to install a solar electric generating system on the roof of the Building. Upon receipt of written request from Landlord, Tenant, at Tenant’s sole cost and expense, shall deliver to Landlord data regarding the electricity consumed in the operation of the Premises (the “Energy Data”) for purposes of regulatory compliance, manual and automated benchmarking, energy management, building environmental performance labeling and other related purposes, including but not limited, to the Environmental Protection Agency’s Energy Star rating system and other energy benchmarking systems. Landlord shall use commercially reasonable efforts to utilize automated data transmittal services offered by utility companies to access the Energy Data. Landlord shall not publicly disclose Energy Data without Tenant’s prior written consent. Landlord may, however, disclose Energy Data that has been modified, combined or aggregated in a manner such that the resulting data is not exclusively attributable to Tenant.

(p) This Lease may be executed in any number of counterparts, each of which shall be deemed to be an original, and all of such counterparts shall constitute one Lease. Execution copies of this Lease may be delivered by facsimile or email, and the parties hereto agree to accept and be bound by facsimile signatures or scanned signatures transmitted via email hereto, which signatures shall be considered as original signatures with the transmitted Lease having the same binding effect as an original signature on an original Lease. At the request of either party, any facsimile document or scanned document transmitted via email is to be re-executed in original form by the party who executed the original facsimile document or scanned document. Neither party may raise the use of a facsimile machine or scanned document or the fact that any signature was transmitted through the use of a facsimile machine or email as a defense to the enforcement of this Lease.

(q) Within fifteen (15) days of Landlord’s written request, Tenant agrees to deliver to Landlord such information and/or documents as Landlord requires for Landlord to comply with California Public Resources Code Section 25402.10, or successor statute(s), and California Energy Commission adopted regulations set forth in California Code of Regulations, Title 20, Division 2, Chapter 4, Article 9, Sections 1680-1685, and successor and related California Code of Regulations, relating to commercial building energy ratings. Landlord makes the following statement based on Landlord’s actual knowledge in order to comply with California Civil Code Section 1938: The Building and Premises have not undergone an inspection by a Certified Access Specialist (CASp).