1

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For The Fiscal Year Ended

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to ____________

Commission file number:

(Exact name of registrant as specified in its charter)

(State or other Jurisdiction of Incorporation or Organization)

(I.R.S. Employer Identification No.)

,

,

,

(Address of principal executive offices) (Zip Code)

(

)

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12 (b) of the Act:

Title of each class:

Trading Symbol(s)

Name of each exchange on which registered:

The Nasdaq Global Select Market

Securities registered pursuant to Section 12 (g) of the Act: NONE

Indicate by check mark if the registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act.

☑

No

☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes

☐

☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act

of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject

to such filing requirements for the past 90 days.

☑

No

☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to

submit such files).

☑

No

☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting

company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company”

and “emerging growth company” in Rule 12b-2 of the Exchange Act.

☑

Accelerated filer

☐

Non-accelerated filer

☐

Smaller reporting company

☐

Emerging growth company

☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for

complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act

☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its

internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting

firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included

in the filing reflect the correction of an error to previously issued financial statements.

☐

Indicate by a check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based

compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).

☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes

☐

No

☑

The aggregate market value, as reported by The NASDAQ Global Select Market, of the registrant’s Common Stock, $0.01 par value, held by

non-affiliates at December 2, 2023, which was the date of the last business day of the registrant’s most recently completed second fiscal quarter,

was $

.

As of July 23, 2024,

Common Stock, $0.01 par value, were outstanding.

2

DOCUMENTS INCORPORATED BY REFERENCE

The information called for by Part III of this Form 10-K is incorporated herein by reference from the registrant’s Definitive Proxy Statement

for its 2024 annual meeting of stockholders which will be filed pursuant to Regulation 14A not later than 120 days after the end of the fiscal

year covered by this report.

3

TABLE OF CONTENTS

Item

Page

Number

1.

1A.

1B.

1C.

2.

3.

4.

5.

6.

7.

7A.

8.

9.

9A.

9B.

9C.

10.

11.

12.

13.

14.

15.

16.

4

PART I.

FORWARD -LOOKING STATEMENTS

This report contains numerous forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 (the

“Securities Act”) and Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”) relating to our shell egg and egg

products business, including estimated future production data, expected construction schedules, projected construction costs,

potential future supply of and demand for our products, potential future corn and soybean price trends, potential future impact on

our business of the resurgence in United States (“U.S.”) commercial table egg layer flocks of highly pathogenic avian influenza

(“HPAI”), potential future impact on our business of inflation and changing interest rates, potential future impact on our business

of new legislation, rules or policies, potential outcomes of legal proceedings, including loss contingency accruals and factors that

may result in changes in the amounts recorded, and other projected operating data, including anticipated results of operations and

financial condition. Such forward-looking statements are identified by the use of words such as “believes,” “intends,” “expects,”

“hopes,” “may,” “should,” “plans,” “projected,” “contemplates,” “anticipates,” or similar words. Actual outcomes or results could

differ materially from those projected in the forward-looking statements. The forward-looking statements are based on

management’s current intent, belief, expectations, estimates, and projections regarding the Company and its industry. These

statements are not guarantees of future performance and involve risks, uncertainties, assumptions, and other factors that are

difficult to predict and may be beyond our control. The factors that could cause actual results to differ materially from those

projected in the forward-looking statements include, among others, (i) the risk factors set forth in Item 1A Risk Factors and

elsewhere in this report as well as those included in other reports we file from time to time with the Securities and Exchange

Commission (the “SEC”) (including our Quarterly Reports on Form 10-Q and Current Reports on Form 8-K), (ii) the risks and

hazards inherent in the shell egg business (including disease, pests, weather conditions, and potential for product recall), including

but not limited to the current outbreak of HPAI affecting poultry in the U.S., Canada and other countries that was first detected

in commercial flocks in the U.S. in February 2022 and that first impacted our flocks in December 2023, (iii) changes in the

demand for and market prices of shell eggs and feed costs, (iv) our ability to predict and meet demand for cage-free and other

specialty eggs, (v) risks, changes, or obligations that could result from our recent or future acquisition of new flocks or businesses

and risks or changes that may cause conditions to completing a pending acquisition not to be met, (vi) risks relating to changes

in inflation and interest rates, (vii) our ability to retain existing customers, acquire new customers and grow our product mix,

(viii) adverse results in pending litigation matters, and (ix) global instability, including as a result of the war in Ukraine, the Israel-

Hamas conflict and attacks on shipping in the Red Sea. Readers are cautioned not to place undue reliance on forward-looking

statements because, while we believe the assumptions on which the forward-looking statements are based are reasonable, there

can be no assurance that these forward-looking statements will prove to be accurate. Further, forward-looking statements included

herein are only made as of the respective dates thereof, or if no date is stated, as of the date hereof. Except as otherwise required

by law, we disclaim any intent or obligation to update publicly these forward-looking statements, whether because of new

information, future events, or otherwise.

ITEM 1. BUSINESS

Our Business

We are the largest producer and distributor of shell eggs in the United States. Our mission is to be the most sustainable producer

and reliable supplier of consistent, high quality fresh shell eggs and egg products in the country, demonstrating a "Culture of

Sustainability" in everything we do, and creating value for our shareholders, customers, team members and communities. We sell

most of our shell eggs throughout the majority of the U.S. and aim to maintain efficient, state-of-the-art operations located close

to our customers. We were founded in 1957 by the late Fred R. Adams, Jr. and are headquartered in Ridgeland, Mississippi.

The Company has one reportable operating segment, which is the production, grading, packaging, marketing and distribution of

shell eggs. Our integrated operations consist of hatching chicks, growing and maintaining flocks of pullets, layers and breeders,

manufacturing feed, and producing, processing, packaging, and distributing shell eggs. Layers are mature female chickens, pullets

are female chickens usually less than 18 weeks of age, and breeders are male and female chickens used to produce fertile eggs to

be hatched for egg production flocks. Our total flock as of June 1, 2024 consisted of approximately 39.9 million layers and 11.8

million pullets and breeders.

Many of our customers rely on us to provide most of their shell egg needs, including specialty and conventional eggs. Specialty

eggs encompass a broad range of products. We classify cage-free, organic, brown, free-range, pasture-raised and nutritionally

enhanced eggs as specialty eggs for accounting and reporting purposes. We classify all other shell eggs as conventional products.

While we report separate sales information for these egg types, there are many cost factors that are not specifically available for

conventional or specialty eggs due to the nature of egg production. We manage our operations and allocate resources to these

types of eggs on a consolidated basis based on the demands of our customers.

5

We believe that an important competitive advantage for Cal-Maine Foods is our ability to meet our customers’ evolving needs

with a favorable product mix of conventional and specialty eggs, including cage-free, organic, brown, free-range, pasture-raised

and nutritionally-enhanced eggs, as well as egg products. While a small part of our current business, the free-range and pasture-

raised eggs we produce and sell continues to grow and represents attractive offerings to a subset of consumers, and therefore our

customers, and help us continue to serve as the trusted provider of quality food choices.

Throughout the Company’s history, we have acquired other businesses in our industry. Since 1989, we have acquired and

integrated 24 businesses. Subsequent to the end of our 2024 fiscal year, we acquired our 25

th

substantially all the assets of ISE America, Inc. and certain of its affiliates, relating to their commercial shell egg production

and processing business. For information on our recent acquisitions, refer to

When we use “we,” “us,” “our,” or the “Company” in this report, we mean Cal-Maine Foods, Inc. and our consolidated

subsidiaries, unless otherwise indicated or the context otherwise requires. The Company’s fiscal year-end is on the Saturday

closest to May 31. Our fiscal year 2024 ended June 1, 2024, and the first three fiscal quarters of fiscal 2024 ended September 2,

2023, December 2, 2023, and March 2, 2024. All references herein to a fiscal year means our fiscal year and all references to a

year mean a calendar year.

Industry Background

According to the U.S. Department of Agriculture (“USDA”) Agricultural Marketing Service, in 2023 approximately 70% of table

eggs produced in the U.S. were sold as shell eggs, with 57% sold through food-at-home outlets such as grocery and convenience

stores, 11% sold to food-away-from home channels such as restaurants and 2% exported. The USDA estimated that in 2023

approximately 30% of eggs produced in the U.S. were sold as egg products (shell eggs broken and sold in liquid, frozen, or dried

form) to institutions (e.g. companies producing baked goods). For information about egg producers in the U.S., see “Competition”

below.

Our industry has been greatly impacted by the outbreaks of highly pathogenic avian influenza (“HPAI”) . For additional

information regarding HPAI and its impact on our industry and business, see

Given historical consumption trends, we believe that general demand for eggs in the U.S. increases basically in line with the

overall U.S. population growth; however, specific events can impact egg supply and consumption in a particular period, as

occurred with the 2015 HPAI outbreak, the COVID-19 pandemic (particularly during 2020), and the most recent HPAI outbreaks

starting in early 2022 and again in late 2023. For fiscal 2024, shell egg household penetration is approximately 97%. According

to the USDA’s Economic Research Service, estimated annual per capita consumption in the United States between 2019 and

2023 varied, ranging from 279 to 292 eggs which is directly impacted by available supply. The USDA calculates per capita

consumption by dividing total shell egg disappearance in the U.S. by the U.S. population.

The most significant shift in demand in recent years has been among specialty eggs, particularly cage-free eggs. For additional

information, see “Specialty Eggs.”

Prices for Shell Eggs

Wholesale shell egg sales prices are a critical component of revenue for the Company. We sell the majority of our conventional

shell eggs at prices based on formulas that take into account, in varying ways, independently quoted regional wholesale market

prices for shell eggs or formulas related to our costs of production, which include the cost of corn and soybean meal. We do not

sell eggs directly to consumers or set the prices at which eggs are sold to consumers.

Wholesale shell egg prices are volatile, cyclical, and impacted by a number of factors, including consumer demand, seasonal

fluctuations, the number and productivity of laying hens in the U.S. and outbreaks of agricultural diseases such as HPAI. We

believe the majority of conventional shell eggs sold in the U.S. in the retail and foodservice channels are sold at prices that take

into account, in varying ways, independently quoted wholesale market prices, such as those published by Urner Barry

Publications, Inc. (“UB”) or the USDA for shell eggs; however, grain-based or variations of cost plus arrangements are also

commonly utilized.

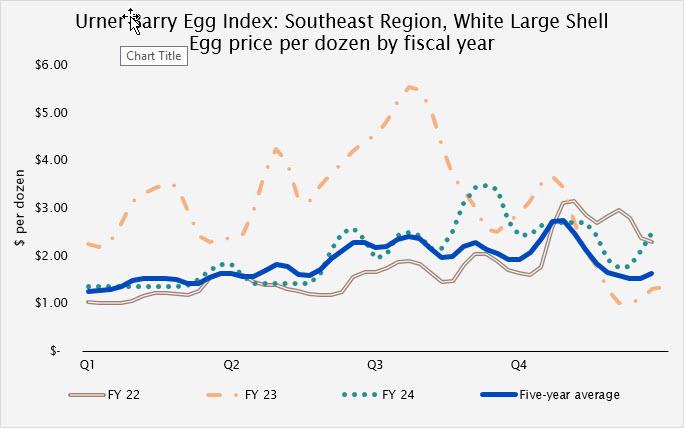

The weekly average price for the southeast region for large white conventional shell eggs as quoted by UB is shown below for

the past three fiscal years along with the five-year average price. The actual prices that we realize on any given transaction will

6

not necessarily equal quoted market prices because of the individualized terms that we negotiate with individual customers which

are influenced by many factors. As further discussed in

, egg prices in fiscal 2022 through fiscal 2024 were significantly impacted by HPAI.

Wholesale prices for cage-free eggs are quoted by independent sources such as UB and USDA. There is no independently quoted

wholesale market price for other specialty eggs such as nutritionally enhanced, organic, pasture-raise and free-range eggs.

Specialty eggs are typically sold at prices and terms negotiated directly with customers and in the case of cage-free eggs, can be

sold at prices that take into account independently quoted markets. Historically, prices for specialty eggs have generally been

higher due to customer and consumer willingness to pay more for specialty eggs. We utilize several different pricing mechanisms;

however, the majority of our specialty eggs are typically sold at prices and terms negotiated directly with customers. As a result,

specialty egg prices do not fluctuate as much as conventional pricing.

Depending on market conditions, input costs and individualized contract terms, the price we receive per dozen eggs in any given

transaction may be more than or less than our farm production and other costs per dozen.

Feed Costs for Shell Egg Production

Feed is a primary cost component in the production of shell eggs and represented 56.0% of our fiscal 2024 farm production costs.

We routinely fill our storage bins during harvest season when prices for feed ingredients, primarily corn and to a lesser extent

soybean meal, are generally lower. To ensure continued availability of feed ingredients, we may enter into contracts for future

purchases of corn and soybean meal, and as part of these contracts, we may lock-in the basis portion of our grain purchases

several months in advance. Basis is the difference between the local cash price for grain and the applicable futures price. The

difference can be due to transportation costs, storage costs, supply and demand, local conditions and other factors. A basis contract

is a common transaction in the grain market that allows us to lock-in a basis level for a specific delivery period and wait to set

the futures price at a later date. Furthermore, due to the more limited supply for organic ingredients, we may commit to purchase

organic ingredients in advance to help assure supply. Ordinarily, we do not enter into long-term contracts beyond a year to

purchase corn and soybean meal or hedge against increases in the prices of corn and soybean meal. As the quality and composition

of feed is a critical factor in the nutritional value of shell eggs and health of our chickens, we formulate and produce the vast

majority of our own feed at our feed mills located near our production plants. Our annual feed requirements for fiscal 2024 were

1.9 million tons of finished feed, of which we manufactured 1.8 million tons. We currently have the capacity to store 210 thousand

tons of corn and soybean meal, and we replenish these stores as needed throughout the year.

7

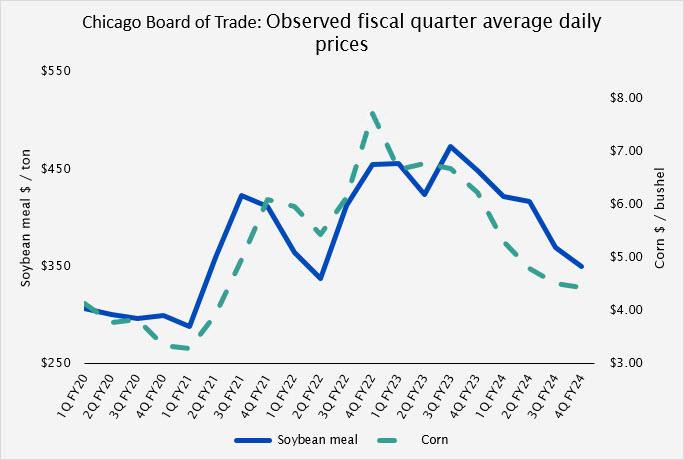

Our primary feed ingredients, corn and soybean meal, are commodities that are subject to volatile price changes due to weather,

various supply and demand factors, transportation and storage costs, speculators, agricultural, energy and trade policies in the

U.S. and internationally, and global instability that could disrupt the supply chain. We purchase the vast majority of our corn and

soybean meal from U.S sources but may be forced to purchase internationally when U.S. supplies are not readily available. Feed

grains are currently available from an adequate number of sources in the U.S. As a point of reference, a multi-year comparison

of the average of daily closing prices per Chicago Board of Trade for each quarter in our fiscal years 2020-2024 are shown below

for corn and soybean meal:

Shell Egg Production

Our percentage of dozens produced to sold was 88.8% of our total shell eggs sold in fiscal 2024. We supplement our production

through purchases of eggs from others when needed. The quantity of eggs purchased will vary based on many factors such as

our own production capabilities and current market conditions. In fiscal 2024, 91.2% of our production came from company-

owned facilities, and 8.8% from contract producers. The majority of our contract production is with family-owned farms for

organic, pasture-raised and free-range eggs. Under a typical arrangement with a contract producer, we own the flock, furnish all

feed and critical supplies, own the shell eggs produced and assume market risks. The contract producers own and operate their

facilities and are paid a fee based on production with incentives for performance.

The commercial production of shell eggs requires a source of baby chicks for laying flock replacement. We supply the majority

of our chicks from our breeder farms and hatch them in our hatcheries in a computer-controlled environment and obtain the

balance from commercial sources. The chicks are grown in our own pullet farms and are placed into the laying flock once they

reach maturity.

After eggs are produced, they are cleaned, graded and packaged. Substantially all our farms have modern “in-line” facilities which

mechanically gather, clean, grade and package the eggs at the location where they are laid. The in-line facilities generate

significant efficiencies and cost savings compared to the cost of eggs produced from non-in-line facilities, which process eggs

that have been laid at another location and transported to the processing facility. The in-line facilities also produce a higher

percentage of USDA Grade A eggs, which sell at higher prices. Eggs produced on farms owned by contractors are brought to our

8

processing plants to be graded and packaged. We maintain a Safe Quality Food (“SQF”) Management Program which is overseen

by our Food Safety Department and senior management team. As of June 1, 2024, every Company-owned processing plant is

SQF certified. Because shell eggs are perishable, we do not maintain large egg inventories. Our egg inventory averaged six days

of sales during fiscal 2024. We believe our constant focus on production efficiencies and automation throughout our vertical

integrated operations enable us to be a low-cost supplier in our markets.

We are proud to have created and upheld what we believe is a leading poultry Animal Welfare Program (“AWP”). We have

aligned our AWP with regulatory, veterinary and our third-party certifying bodies’ guidance to govern the welfare of animals in

our direct care, our contract farmers’ care. We continually review our program to monitor and evolve standards that guide how

we hatch chicks, rear pullets and nurture breeder and layer hens. At each stage of our animals’ lives, we are dedicated to providing

welfare conditions aligned to our commitment to the principles of the internationally recognized

Five Freedoms of Animal

Welfare

.

We do not use artificial hormones in the production of our eggs. Hormone use in the poultry and egg production industry has

been effectively banned in the U.S. since the 1950s. We have an extensive written protocol that allows the use of medically

important antibiotics only when animal health is at risk, consistent with guidance from the United States Food and Drug

Administration (“FDA”) and the Guidance for Judicious Therapeutic Use of Antimicrobials in Poultry, developed by the

American Association of Avian Pathologists. When antibiotics are medically necessary, a licensed veterinary doctor will approve

and administer approved doses for a restricted period. We do not use antibiotics for growth promotion or performance

enhancement.

Specialty Eggs

We are one of the largest producers and marketers of value-added specialty shell eggs in the U.S., which continues to be a

significant and growing segment of the market. We classify cage-free, organic, brown, free-range, pasture-raised and nutritionally

enhanced as specialty eggs for accounting and reporting purposes. Specialty eggs are intended to meet the demands of consumers

sensitive to environmental, health and/or animal welfare issues and to comply with state requirements for cage-free eggs.

Ten states have passed legislation or regulations mandating minimum space or cage-free requirements for egg production or

mandated the sale of only cage-free eggs and egg products in their states, with implementation of these laws ranging from January

2022 to January 2030. These states represent approximately 27% of the U.S. total population according to the 2020 U.S. Census.

California, Massachusetts, Colorado, Oregon, Washington, and Nevada, which collectively represent approximately 20% of the

total estimated U.S. population have cage-free legislation in effect currently.

A significant number of our customers have announced goals to either exclusively offer cage-free eggs or significantly increase

the volume of cage-free egg sales in the future, subject in most cases to availability of supply, affordability and consumer demand,

among other contingencies. Our customers typically do not commit to long-term purchases of specific quantities or types of eggs

with us, and as a result, it is difficult to accurately predict customer requirements for cage-free eggs. We are focused on adjusting

our cage-free production capacity with a goal of meeting the future needs of our customers in light of changing state requirements

and our customer’s goals. As always, we strive to offer a product mix that aligns with current and anticipated customer purchase

decisions. We are engaging with our customers to help them meet their announced goals and needs. We have invested significant

capital in recent years to acquire and construct cage-free facilities, and we expect our focus for future expansion will continue to

include cage-free facilities. Our volume of cage-free egg sales has continued to increase and account for a larger share of our

product mix. Cage-free egg revenue represented approximately 29.5% of our total net shell egg sales for fiscal year 2024. At the

same time, we understand the importance of our continued ability to provide affordable conventional eggs in order to provide our

customers with a variety of egg choices and to address hunger in our communities.

Branded Eggs

We are a member of the Eggland’s Best, Inc. cooperative (“EB”) and produce, market, distribute and sell

Egg-Land’s Best®

Land O’ Lakes®

and offerings include nutritionally enhanced, cage-free, organic, pasture -raised and free-range eggs.

Land O’ Lakes®

eggs are produced by hens that are fed a whole-grain vegetarian diet and include brown, organic and cage-free eggs.

In 2023, EB was the third best-selling dairy brand in the U.S. The top two best-selling branded specialty egg SKUs in 2023 were

EB branded eggs and seven out of 10 best-selling SKUs are EB branded eggs. In 2023, our sales (including sales through affiliates)

represented approximately 50% of EB branded eggs and 45% of

Land O’ Lakes®

branded eggs nationwide.

9

Our

Farmhouse Eggs

® brand eggs are produced at our facilities by hens that are provided with a vegetarian diet. Our offerings

of

Farmhouse Eggs

® include cage-free, organic and pasture raised eggs. We market organic, vegetarian and omega-3 eggs under

our

4-Grain®

Sunups®

Sunny Meadow®

brands are sold as

conventional eggs.

We also produce, market and distribute private label specialty and conventional shell eggs to several customers.

Egg Products

Egg products are shell eggs broken and sold in liquid, frozen, or dried form. We sell liquid and frozen egg products primarily to

the institutional, foodservice and food manufacturing sectors in the U.S. Our egg products are primarily sold through our wholly

owned subsidiaries American Egg Products, LLC located in Georgia and Texas Egg Products, LLC located in Texas. In fiscal

2024, egg product sales constituted approximately 3.8% of our revenue.

During March 2023, MeadowCreek Food, LLC (“Meadowcreek”), a majority-owned subsidiary, began operations with a focus

on being a leading provider of hard -cooked eggs. We serve as the preferred supplier of specialty and conventional eggs that

MeadowCreek needs to manufacture egg products. MeadowCreek’s marketing plan is designed to extend our reach in the

foodservice and retail marketplace and bring new opportunities in the restaurant, institutional and industrial food products arenas.

Summary of Conventional and Specialty Shell Egg and Egg Product Sales

The following table sets forth the contribution as a percentage of revenue and volumes of dozens sold of conventional and

specialty shell egg and egg product sales for the following fiscal years:

2024

2023

2022

Revenue

Volume

Revenue

Volume

Revenue

Volume

Conventional Eggs

Branded

4.3

%

4.9

%

6.6

%

6.4

%

6.5

%

7.1

%

Private-label

46.8

54.4

52.9

52.6

48.3

54.9

Other

4.4

5.8

5.7

6.3

5.0

7.0

Total Conventional Eggs

55.5

%

65.1

%

65.2

%

65.3

%

59.8

%

69.0

%

Specialty Eggs

Branded

20.3

%

17.4

%

18.0

%

20.4

%

24.2

20.0

%

Private-label

18.5

16.3

11.3

12.9

11.3

9.5

Other

1.0

1.2

1.1

1.4

1.0

1.5

Total Specialty Eggs

39.8

%

34.9

%

30.4

%

34.7

%

36.5

%

31.0

%

Egg Products

3.8

%

3.9

%

3.4

%

Marketing and Distribution

In fiscal 2024, we sold our shell eggs and egg products in 39 states through the southwestern, southeastern, mid-western, mid-

Atlantic and northeastern regions of the U.S. as well as Puerto Rico through our extensive distribution network to a diverse group

of customers, including national and regional grocery store chains, club stores, companies servicing independent supermarkets in

the U.S., foodservice distributors and egg product consumers. Some of our sales are completed through co-pack agreements – a

common practice in the industry whereby production and processing of certain products are outsourced to another producer.

The majority of eggs sold are based on the daily or short-term needs of our customers. Most sales to established accounts are on

payment terms ranging from seven to 30 days. Although we have established long-term relationships with many of our customers,

most of them are free to acquire shell eggs from other sources.

The shell eggs we sell are either delivered to our customers’ warehouse or retail stores, by our own fleet or contracted refrigerated

delivery trucks, or are picked up by our customers at our processing facilities.

10

We are a member of the Eggland’s Best, Inc. cooperative and produce, market, distribute and sell

Egg-Land’s Best®

Land

O’ Lakes®

exclusive license agreements in Alabama, Arizona, Florida, Georgia, Louisiana, Mississippi and Texas, and in portions of

Arkansas, California, Nevada, North Carolina, Oklahoma and South Carolina. We also have an exclusive license in New York

City in addition to exclusivity in select New York metropolitan areas, including areas within New Jersey and Pennsylvania. As

discussed above under “Branded Eggs,” we also sell our own

Farmhouse Eggs

® and

4-Grain

® branded eggs.

In 2022, we joined as a member during the formation of ProEgg, Inc. (“ProEgg”), a new egg farmer cooperative in the western

United States. During 2024, after careful review and full analysis we decided to withdraw our membership in ProEgg. The

withdrawal from ProEgg did not affect any of our existing customer relationships.

Customers

Our top three customers accounted for an aggregate of 49.0%, 50.1% and 45.9% of net sales dollars for fiscal 2024, 2023, and

2022, respectively. Our largest customer, Walmart Inc. (including Sam's Club), accounted for 34.0%, 34.2% and 29.5% of net

sales dollars for fiscal 2024, 2023 and 2022, respectively.

For shell egg sales in fiscal 2024 , approximately 89% of our revenue related to sales to retail customers and 11% to sales to

foodservice providers. Retail customers include primarily national and regional grocery store chains, club stores, and companies

servicing independent supermarkets in the U.S. Foodservice customers include primarily companies that sell food products and

related items to restaurants, healthcare and education facilities and hotels.

Competition

The production, processing, and distribution of shell eggs is an intensely competitive business, which has traditionally attracted

large numbers of producers in the U.S. Shell egg competition is generally based on price, service and product quality. The shell

egg production industry remains highly fragmented. According to

Egg Industry Magazine

, the ten largest producers owned

approximately 54% and 53% of industry table egg layer hens at calendar year-end 2023 and 2022, respectively.

Seasonality

Retail sales of shell eggs historically have been highest during the fall and winter months and lowest during the summer months.

Prices for shell eggs fluctuate in response to seasonal demand factors and a natural increase in egg production during the spring

and early summer. Historically, shell egg prices tend to increase with the start of the school year and tend to be highest prior to

holiday periods, particularly Thanksgiving, Christmas and Easter. Consequently, and all other things being equal, we would

expect to experience lower selling prices, sales volumes and net income (and may incur net losses) in our first and fourth fiscal

quarters ending in August/September and May/June, respectively. Accordingly, we generally expect our need for working capital

to be highest during those quarters.

Growth Strategy

Our growth strategy is centered on growth through strategic acquisitions, organic growth, and expansion of our value-added

products business. We believe that we can continue to expand our market reach through strategic acquisitions and achieve

favorable returns through our proven operating model emphasizing synergies and efficient operations. Organic growth is

grounded in our culture of operational excellence to optimize everything we can control. We are committed to investing in our

existing operations to increase sales, profitability and customer service. We have continued to increase our production of cage-

free shell eggs and other higher value specialty eggs such as pasture-raised, free-range and organic shell eggs. We believe there

is long-term growth potential in value-added products such as hard-cooked eggs, which will enable us to leverage our existing

distribution channels, expand our reach in foodservice and retail marketplaces and bring new opportunities in the restaurant,

institutional and industrial food products arenas.

Trademarks and License Agreements

We own the trademarks

Farmhouse Eggs®

,

Sunups®

,

Sunny Meadow®

4Grain®

. We produce and market

Egg-Land's Best

®

and

Land O’ Lakes

® branded eggs under license agreements with EB. We believe these trademarks and license agreements are

important to our business.

11

Government Regulation

Our facilities and operations are subject to regulation by various federal, state, and local agencies, including, but not limited to,

the FDA, USDA, Environmental Protection Agency (“EPA ”), Occupational Safety and Health Administration ("OSHA") and

corresponding state agencies. The applicable regulations relate to grading, quality control, labeling, sanitary control and reuse or

disposal of waste. Our shell egg facilities are subject to periodic USDA, FDA, EPA and OSHA inspections. Our feed production

facilities are subject to FDA, EPA and OSHA regulation and inspections. We maintain inspection programs and in certain cases

utilize independent third-party certification bodies to monitor compliance with regulations, our own standards and customer

specifications. It is possible that we will be required to incur significant costs for compliance with such statutes and regulations.

In the future, additional rules could be proposed that, if adopted, could increase our costs.

A number of states have passed legislation or regulations mandating minimum space or cage-free requirements for egg production

or have mandated the sale of only cage-free eggs and egg products in their states. For further information refer to the heading

“Specialty Eggs” within this section.

Environmental Regulation

Our operations and facilities are subject to various federal, state, and local environmental, health and safety laws and regulations

governing, among other things, the generation, storage, handling, use, transportation, disposal, and remediation of hazardous

materials. Under these laws and regulations, we must obtain permits from governmental authorities, including, but not limited to,

wastewater discharge permits. We have made, and will continue to make, capital and other expenditures relating to compliance

with existing environmental, health and safety laws and regulations and permits. We are not currently aware of any material

capital expenditures necessary to comply with such laws and regulations; however, as environmental, health and safety laws and

regulations are becoming increasingly more stringent, including those relating to animal wastes and wastewater discharges, it is

possible that we will have to incur significant costs for compliance with such laws and regulations in the future.

Human Capital Resources

As of June 1, 2024, we had 3,067 employees, of whom 2,370 worked in egg production, processing, and marketing, 204 worked

in feed mill operations and 493, including our executive officers, were administrative employees. Approximately 4.5% of our

personnel are part-time, and we utilize temporary employment agencies and independent contractors to augment our

staffing needs when necessary. For fiscal 2024, we had 1,962 average monthly contingent workers. As of June 1, 2024, none of

our employees were covered by a collective bargaining agreement. We consider our relations with employees to be good.

Culture and Values

We are proud to be contributing corporate citizens where we live and work and to help create healthy, prosperous

communities. Our colleagues help us continue to enhance our community contributions, which are driven by

our longstanding culture that strives to promote an environment that upholds integrity and respect and provides opportunities for

each colleague to realize full potential. These commitments are encapsulated in the

Cal-Maine Foods Code of Ethics and Business

Conduct

Human Rights Statement

.

Health and Safety

Our top priority is the health and safety of our employees, who continue to produce high-quality, affordable egg choices for our

customers and contribute to a stable food supply. Our enterprise safety committee is comprised of two corporate safety managers,

nine area compliance managers (three specifically for worker health and safety), and 55 local site compliance managers, feed mill

managers and general managers. The committee that oversees health and safety regularly reviews our written policies and

changes to OSHA regulation standards and shares information as it relates to outcomes from incidents in order to improve future

performance and our health and safety practices. The committee’s goals include working to help ensure that our engagements

with our consumers, customers, and regulators evidence our strong commitment to our workers’ health and safety.

Our commitment to our colleagues’ health includes a strong commitment to on-site worker safety, including a focus on accident

prevention and life safety. Our Safety and Health Program is designed to promote best practices that help prevent and minimize

workplace accidents and illnesses. The scope of our Safety and Health Program applies to all enterprise colleagues. Additionally,

to help protect the health and well-being of our colleagues and people in our value chain, we require that any contractors or

vendors acknowledge and agree to comply with the guidelines governed by our Safety and Health Program. At each of our

locations, our general managers are expected to uphold and implement our Safety and Health Program in alignment with OSHA

requirements. We believe that this program, which is reviewed annually by our senior management team, contributes to strong

12

safety outcomes. As part of our Safety and Health Program, we conduct multi-lingual training that covers topics such as slip-and-

fall avoidance, respiratory protection, prevention of hazardous communication of chemicals, the proper use of personal protective

equipment, hearing conservation, emergency response, lockout and tagout of equipment and forklift safety, among others. We

have also installed dry hydrogen peroxide biodefense systems in our processing facilities to help protect our colleagues’

respiratory health. To help drive our focus on colleague safety, we developed safety committees at each of our sites with employee

representation from each department.

We review the success of our safety programs on a monthly basis to monitor their effectiveness and the development of any

trends that need to be addressed. During fiscal year 2024 our recordable incident rates decreased by 20% compared to fiscal 2023.

People

Our strength as a company comes from our employees at all levels and we have a long-established culture that values each

individual’s contributions and encourages productivity and growth. This culture is driven by our board and executive

management team. Our board is comprised of seven members, four of whom are independent, two of whom are women, one of

whom is of a racial or ethnic minority. As of June 1, 2024, our total workforce was comprised of 31% women and 56% individuals

who identify as racial or ethnic minorities. Our Policy against Harassment, Discrimination, Unlawful or Unethical Conduct and

Retaliation; Reporting Procedure affirms our commitment to supporting our employees regardless of race, color, religion, sex,

national origin or any other basis protected by applicable law.

We are an Equal Opportunity Employer that prohibits any violation of applicable federal, state, or local law regarding

employment. Discrimination on any basis protected by applicable law is prohibited. We maintain strong protocols to help our

colleagues perform their jobs free from harassment and discrimination. We are committed to offering our colleagues opportunities

commensurate with our operational needs and their experiences, goals and contributions.

Recruitment, Development and Retention

We believe in compensating our colleagues with fair and competitive wages, in addition to offering

competitive benefits. Approximately 76% of our employees are paid at hourly rates, which are all paid at rates above the federal

minimum wage requirement. We offer our full-time eligible employees a range of benefits, including company-paid life

insurance. The Company provides a comprehensive self-insured health plan and pays approximately 82% of the costs of the plan

for participating employees and their families as of December 31, 2023. Recent benchmarking of our health plan

indicates comparable benefits, at lower employee contributions, when compared to an applicable Agriculture and

Food Manufacturing sector grouping, as well as peer group data. In addition, we offer employees the opportunity to purchase an

extensive range of other group plan benefits, such as dental, vision, accident, critical illness, disability and voluntary life. After

one year of employment, full-time employees who meet eligibility requirements may elect to participate in our

KSOP retirement plan, which offers a range of investment alternatives and includes many positive features, such as

automatic enrollment with scheduled automatic contribution increases and loan provisions. Regardless of the

employees’ elections to contribute to the KSOP, the Company contributes shares of Company stock or cash equivalent to 3%

of participants’ eligible compensation for each pay period that hours are worked.

We

provide extensive training and development related to safety, regulatory compliance, and task training.

We

invest in

developing our future leaders through our Management Intern, Management Trainee and informal mentoring programs.

Sustainability

We understand that climate, and the potential consequences of climate change, freshwater availability and preservation of global

biodiversity, in addition to responsible management of our flocks, are vital to the production of high-quality eggs and egg products

and to the success of our Company. We have engaged in agricultural production for more than 60 years. Our agricultural practices

continue to evolve as we continue to strive to meet the need for nutritious, affordable foods to feed a growing population even as

we exercise responsible natural resource stewardship and conservation. We published our most recent sustainability report for

our fiscal 2023 in July 2024, which is available on our website. Information contained on our website is not a part of this report

on Form 10-K.

Our Corporate Information

We maintain a website at www.calmainefoods.com where general information about our business and corporate governance

matters is available. The information contained in our website is not a part of this report. Our Annual Reports on Form 10-K,

Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, proxy statements, and all amendments to those reports filed or

13

furnished pursuant to Section 13(a) or 15(d) of the Exchange Act are available, free of charge, through our website as soon as

reasonably practicable after we file them with, or furnish them to, the SEC. In addition, the SEC maintains a website at

www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers that file

electronically with the SEC. Cal-Maine Foods, Inc. is a Delaware corporation, incorporated in 1969.

ITEM 1A. RISK FACTORS

Our business and results of operations are subject to numerous risks and uncertainties, many of which are beyond our

control. The following is a description of the known factors that may materially affect our business, financial condition or results

of operations. They should be considered carefully, in addition to the information set forth elsewhere in this Annual Report on

Form 10-K, including under Part II. Item 7. Management’s Discussion and Analysis of Financial Condition and Results of

Operations, in making any investment decisions with respect to our securities. Additional risks or uncertainties that are not

currently known to us, or that we are aware of but currently deem to be immaterial or that could apply to any company could

also materially adversely affect our business, financial condition or results of operations.

INDUSTRY RISK FACTORS

Market prices of wholesale shell eggs are volatile, and decreases in these prices can adversely impact our revenues and

profits.

Our operating results are significantly affected by wholesale shell egg market prices, which fluctuate widely and are outside our

control. As a result, our prior performance should not be presumed to be an accurate indication of future performance. Under

certain circumstances, small increases in production, or small decreases in demand, within the industry might have a large adverse

effect on shell egg prices. Low shell egg prices adversely affect our revenues and profits.

Market prices for wholesale shell eggs have been volatile and cyclical. Shell egg prices have risen in the past during periods of

high demand such as the initial outbreak of the COVID-19 pandemic and periods when high protein diets are popular. Shell egg

prices have also risen during periods of constrained supply, such as the latest highly pathogenic avian influenza (“HPAI”)

outbreak that was first detected in domestic commercial flocks in February 2022. During times when prices are high, the egg

industry has typically geared up to produce more eggs, primarily by increasing the number of layers, which historically has

ultimately resulted in an oversupply of eggs, leading to a period of lower prices.

As discussed above in

, seasonal fluctuations impact shell egg prices. Therefore, comparisons

of our sales and operating results between different quarters within a single fiscal year are not necessarily meaningful

comparisons.

A decline in consumer demand for shell eggs can negatively impact our business.

We believe high -protein diet trends, industry advertising campaigns, the improved nutritional reputation of eggs and an increase

in at-home consumption of eggs during the COVID-19 pandemic, have all contributed at one time or another to increased shell

egg demand. However, it is possible that the demand for shell eggs will decline in the future. Adverse publicity relating to health

or safety concerns and changes in the perception of the nutritional value of shell eggs, changes in consumer views regarding

consumption of animal-based products, as well as movement away from high protein diets, could adversely affect demand for

shell eggs, which could have a material adverse effect on our future results of operations and financial condition.

Feed costs are volatile and increases in these costs can adversely impact our results of operations.

Feed costs are the largest element of our shell egg (farm) production cost, ranging from 55% to 63% of total farm production cost

in the last five fiscal years.

Although feed ingredients, primarily corn and soybean meal, are available from a number of sources, we do not have control over

the prices of the ingredients we purchase, which are affected by weather, various global and U.S. supply and demand factors,

transportation and storage costs, speculators, and agricultural, energy and trade policies in the U.S. and internationally. For

example, while feed costs declined during fiscal 2024, we saw higher prices for corn and soybean meal in fiscal 2022 and 2023

as a result of weather-related shortfalls in production and yields, ongoing supply chain disruptions and the Russia-Ukraine War

and its impact on the export markets. Our costs for corn and soybean meal are also affected by local basis prices.

Increases in feed costs unaccompanied by increases in the selling price of eggs can have a material adverse effect on the results

of our operations and cash flow. Alternatively, low feed costs can encourage egg industry overproduction, possibly resulting in

lower egg prices and lower revenue.

14

Agricultural risks, including outbreaks of avian diseases such as HPAI, have harmed and in the future could harm our

business.

Our shell egg production activities are subject to a variety of agricultural risks. Unusual or extreme weather conditions, disease

and pests can materially and adversely affect the quality and quantity of shell eggs we produce and distribute. Outbreaks of avian

influenza among poultry occur periodically worldwide and have occurred sporadically in the U.S. Since the HPAI outbreaks in

2015, there were no reported significant outbreaks of HPAI in the commercial table egg layer flocks in the U.S. until the February

– December 2022 time period and then again beginning in November 2023. During the third and fourth quarters of our fiscal

2024, we experienced HPAI outbreaks within our facilities located in Kansas and Texas, resulting in total depopulation of 3.1

million laying hens and 577,000 pullets. Both locations have been cleared by the USDA to resume operations and repopulation

is expected to be completed before calendar year end. As of July 5, 2024, the U.S. Centers for Disease Control and Prevention

(“CDC”) reported outbreaks in 138 dairy herds in 12 states and five cases in the U.S. in persons who were exposed to infected

cows or poultry. The CDC has not reported any case of human-to-human transmission. The CDC considers that the overall risk

to the general U.S. public posed by the virus remains low; however, as a precautionary measure, the U.S. Department of Health

and Human Services has awarded funding to Moderna to develop a human vaccine against avian influenza. For additional

information, refer to

We maintain controls and procedures designed to reduce the risk of exposing our flocks and employees to harmful diseases;

however, despite these efforts, outbreaks of avian diseases can and do still occur and have adversely impacted, and may in the

future adversely impact, the health of our flocks and could in the future adversely impact the health of our employees. Continued

or intensified spread of HPAI could have a material adverse impact on our financial results by increasing government restrictions

on the sale and distribution of our products and requiring us to euthanize the affected layers. Negative publicity from outbreaks

within our industry can negatively impact customer perception. If a substantial portion of our layers or production facilities are

affected by any of these factors in any given quarter or year, our business, financial condition, and results of operations could be

materially and adversely affected.

Shell eggs and shell egg products are susceptible to microbial contamination, and we may be required to, or we may

voluntarily, recall contaminated products.

Shell eggs and shell egg products are vulnerable to contamination by pathogens such as Salmonella. The Company maintains

policies and procedures designed to comply with the complex rules and regulations governing egg production, such as The Final

Egg Rule issued by the FDA “Prevention of Salmonella Enteritidis in Shell Eggs During Production, Storage, and

Transportation,” and the FDA’s Food Safety Modernization Act. Shipment of contaminated products, even if inadvertent, could

result in a violation of law and lead to increased risk of exposure to product liability claims, product recalls and scrutiny by federal

and state regulatory agencies. We have little, if any, control over proper handling once the product has been shipped or

delivered. In addition, products purchased from other producers could contain contaminants that might be inadvertently

redistributed by us. As such, we might decide or be required to recall a product if we, our customers or regulators believe it poses

a potential health risk. Any product recall could result in a loss of consumer confidence in our products, adversely affect our

reputation with existing and potential customers and have a material adverse effect on our business, results of operations and

financial condition. We currently maintain insurance with respect to certain of these risks, including product liability insurance,

business interruption insurance, product recall insurance and general liability insurance, but in many cases such insurance is

expensive, difficult to obtain and no assurance can be given that such insurance can be maintained in the future on acceptable

terms, or in sufficient amounts to protect us against losses due to any such events, or at all.

Our profitability may be adversely impacted by increases in other input costs such as packaging materials and delivery

expenses, including as a result of inflation.

In addition to feed ingredient costs, other significant input costs include costs of packaging materials and delivery expenses. Our

costs of packing materials increased during the past three fiscal years due to inflation and higher labor costs, and during 2022

also as a result of supply chain constraints initially caused by the pandemic, and these costs may continue to increase. We also

experienced increases in delivery expenses during fiscal 2023 and 2022 due to increases in fuel and labor costs for both our fleet

and contract trucking, and these costs may continue to increase. Increases in these costs are largely outside of our control and

have an adverse effect on our profitability and cash flow.

15

BUSINESS AND OPERATIONAL RISK FACTORS

Our acquisition growth strategy subjects us to various risks.

As discussed in

, we plan to continue to pursue a growth strategy that includes, in part,

selective acquisitions of other businesses engaged in the production and sale of shell eggs, with a priority on those that will

facilitate our ability to expand our cage-free shell egg production capabilities in key locations and markets. We may over-estimate

or under-estimate the demand for cage-free eggs, which could cause our acquisition strategy to be less-than-optimal for our future

growth and profitability. The number of existing businesses with cage-free capacity that we may be able to purchase is limited,

as most production of shell eggs by other companies in our markets currently does not meet customer demands or legal

requirements to be designated as cage-free. Conversely, if we acquire cage-free production capacity, which is more expensive to

purchase and operate, and customer demands or legal requirements for cage-free eggs were to change, the resulting lack of

demand for cage-free eggs may result in higher costs and lower profitability .

Acquisitions require capital resources and can divert management’s attention from our existing business. Acquisitions also entail

an inherent risk that we could become subject to contingent or other liabilities, including liabilities arising from events or conduct

prior to our acquisition of a business that were unknown to us at the time of acquisition. We could incur significantly greater

expenditures in integrating an acquired business than we anticipated at the time of its purchase.

We cannot assure you that we:

●

will identify suitable acquisition candidates;

●

can consummate acquisitions on acceptable terms;

●

can successfully integrate an acquired business into our operations; or

●

can successfully manage the operations of an acquired business.

No assurance can be given that businesses we acquire in the future will contribute positively to our results of operations or

financial condition. In addition, federal antitrust laws require regulatory approval of acquisitions that exceed certain threshold

levels of significance, and we cannot guarantee that such approvals would be obtained.

The consideration we pay in connection with any acquisition affects our financial results. If we pay cash, we could be required

to use a portion of our available cash or credit facility to consummate the acquisition. To the extent we issue shares of our

Common Stock, existing stockholders may be diluted. In addition, acquisitions may result in additional debt. Our ability to access

any additional capital that may be needed for an acquisition may be adversely impacted by higher interest rates and economic

uncertainty.

Global or regional health crises including pandemics or epidemics could have an adverse impact on our business and

operations.

The effects of global or regional pandemics or epidemics can significantly impact our operations. Although demand for our

products could increase as a result of restrictions such as travel bans and restrictions, quarantines, shelter-in-place orders, and

business and government shutdowns, which can prompt more consumers to eat at home, these restrictions could also significantly

increase our cost of doing business due to labor shortages, supply-chain disruptions, increased costs and decreased availability of

packaging supplies or feed, and increased medical and other costs. We experienced these impacts as a result of the COVID-19

pandemic, primarily during our fiscal years 2020 and 2021. The pandemic recovery also contributed to higher inflation and

interest rates, which persist and may continue to persist. The impacts of health crises are difficult to predict and depend on

numerous factors including the severity, length and geographic scope of the outbreak, resurgences of the disease and variants,

availability and acceptance of vaccines, and governmental, business and individuals’ responses. A resurgence of COVID-19

and/or variants, or any future major public health crisis, would disrupt our business and could have a material adverse effect on

our financial results.

Our largest customers have accounted for a significant portion of our net sales volume. Accordingly, our business may be

adversely affected by the loss of, or reduced purchases by, one or more of our large customers.

Our customers, such as supermarkets, warehouse clubs and food distributors, have continued to consolidate and consolidation is

expected to continue. These consolidations have produced larger customers and potential customers with increased buying power

that are more capable of operating with reduced inventories, opposing price increases, and demanding lower pricing, increased

promotional programs and specifically tailored products. Because of these trends, our volume growth could slow or we may need

to lower prices or increase promotional spending for our products, any of which could adversely affect our financial results.

16

Our top three customers accounted for an aggregate of 49.0%, 50.1% and 45.9% of net sales dollars for fiscal 2024, 2023, and

2022, respectively. Our largest customer, Walmart Inc. (including Sam's Club), accounted for 33.8%, 34.2% and 29.5% of net

sales dollars for fiscal 2024, 2023 and 2022, respectively. Although we have established long-term relationships with most of our

customers who continue to purchase from us based on our ability to service their needs, they are generally free to acquire shell

eggs from other sources. If, for any reason, one or more of our large customers were to purchase significantly less of our shell

eggs in the future or terminate their purchases from us, and we were not able to sell our shell eggs to new customers at comparable

levels, it would have a material adverse effect on our business, financial condition, and results of operations.

Our business is highly competitive.

The production and sale of fresh shell eggs, which accounted for 96.1% to 96.6% of our net sales in our last three fiscal years, is

intensely competitive. We compete with a large number of competitors that may prove to be more successful than we are in

producing, marketing and selling shell eggs. We cannot provide assurance that we will be able to compete successfully with any

or all of these companies. Increased competition could result in price reductions, greater cyclicality, reduced margins and loss of

market share, which would negatively affect our business, results of operations, and financial condition.

We are dependent on our management team, and the loss of any key member of this team may adversely affect the

implementation of our business plan in a timely manner.

Our success depends largely upon the continued service of our senior management team. The loss or interruption of service of

one or more of our key executive officers could adversely affect our ability to manage our operations effectively and/or pursue

our growth strategy. We have not entered into any employment or non-compete agreements with any of our executive officers.

Competition could cause us to lose talented employees, and unplanned turnover could deplete institutional knowledge and result

in increased costs due to increased competition for employees.

Our business is dependent on our information technology systems and software, and failure to protect against or

effectively respond to cyber-attacks, security breaches, or other incidents involving those systems, could adversely affect

day-to-day operations and decision making processes and have an adverse effect on our performance and reputation.

The efficient operation of our business depends on our information technology systems, which we rely on to effectively manage

our business data, communications, logistics, accounting, regulatory and other business processes. If we do not allocate and

effectively manage the resources necessary to build and sustain an appropriate technology environment, our business, reputation,

or financial results could be negatively impacted. In addition, our information technology systems may be vulnerable to damage

or interruption from circumstances beyond our control, including systems failures, natural disasters, terrorist attacks,

viruses, ransomware, security breaches or cyber incidents. Cyber-attacks are becoming more sophisticated and are increasing in

the number of attempts and frequency by groups and individuals with a wide range of motives. We have experienced and expect

to continue to experience attempted cyber-attacks of our information technology systems or networks.

We regularly engage with third-party service providers as part of our operations to provide a high level of service to our customers.

We have implemented certain practices and policies to minimize the potential risks associated with the exchange of information

with contracted vendors. Despite these practices and policies, we cannot guarantee that information technology systems of our

third-party service providers will prevent and detect all cybersecurity breaches and incidents. Although we require third-party

service providers to notify us upon a potential breach or incident, there is a potential risk that our business, reputation, or financial

results could be negatively impacted by cybersecurity incidents at their businesses .

Additionally, future or past business transactions (such as acquisitions or integrations) could expose us to additional cybersecurity

risks and vulnerabilities, as our systems could be negatively affected by vulnerabilities present in acquired or integrated systems

and technologies. Furthermore, we may discover security issues that were not found during due diligence of such acquired or

integrated businesses, and it may be difficult to integrate businesses into our information technology environment and security

program.

Our information technology systems also subject us to numerous data privacy obligations. We may at times fail (or be perceived

to have failed) in our efforts to comply with our data privacy obligations. If we or the third parties on which we rely fail, or are

perceived to have failed, to address or comply with applicable data privacy obligations, we could face significant consequences,

including but not limited to government enforcement actions and litigation. A security breach of sensitive information could result

in damage to our reputation and our relations with our customers or employees. Any such damage or interruption could have a

material adverse effect on our business.

17

Technology and related business and regulatory requirements continue to change rapidly. Failure to update or replace legacy

systems to address these changes could result in increased costs, including remediation costs, system downtime, third party

litigation, regulatory actions or cyber security vulnerabilities which could have a material adverse effect on our business.

Labor shortages or increases in labor costs could adversely impact our business and results of operations.

Our success is dependent upon recruiting, motivating, and retaining staff to operate our farms. Approximately 76% of our

employees are paid at hourly rates, often in entry-level positions. While all our employees are paid at rates above the federal

minimum wage requirements, any significant increase in local, state or federal minimum wage requirements could increase our

labor costs. In addition, any regulatory changes requiring us to provide additional employee benefits or mandating increases in

other employee-related costs, such as unemployment insurance or workers compensation, would increase our costs. A shortage

in the labor pool, which may be caused by competition from other employers, the remote locations of many of our farms,

decreased labor participation rates or changes in government-provided support or immigration laws, particularly in times of lower

unemployment, could adversely affect our business and results of operations. A shortage of labor available to us could cause our

farms to operate with reduced staff, which could negatively impact our production capacity and efficiencies. In fiscal 2022, our

labor costs increased primarily due to the pandemic and its effects, which caused us to increase wages in response to labor

shortages. In fiscal 2023 and 2024, labor wages continued to rise due to inflation and low unemployment. Accordingly, any

significant labor shortages or increases in our labor costs could have a material adverse effect on our results of operations.

We are controlled by the family of our late founder, Fred R. Adams, Jr., and Adolphus B. Baker, Chairman of our Board

of Directors, controls the vote of 100% of our outstanding Class A Common Stock.

Fred R. Adams, Jr., our Founder and Chairman Emeritus died on March 29, 2020. A limited liability company (the “Daughters’

LLC”), owned by Mr. Adams’ son-in-law, Adolphus B. Baker, Chairman of our board of directors, Mr. Baker’s spouse and her

three sisters (Mr. Adams’ four daughters) (collectively, the “Family”), owns 100% of our outstanding Class A Common Stock

(which has 10 votes per share), controlling approximately 52.0% of our total voting power. As sole managing member of the

Daughters’ LLC, Mr. Baker controls the vote of 100% of our outstanding Class A Common Stock, except that certain

extraordinary matters requiring the vote of the Company’s stockholders such as a merger or amendment of the Company’s Second

Amended and Restated Certificate of Incorporation require joint approval of Mr. Baker and members of the Daughters’ LLC

holding a majority of its voting interests. Family members also have additional voting power due to beneficial ownership of our

Common Stock (which has one vote per share), directly or indirectly through the Daughter’s LLC and other entities, resulting in

family voting control of approximately 53.8% of our total voting power.

We understand that the Family intends to retain ownership of a sufficient amount of our Common Stock and our Class A Common

Stock to assure continued ownership of more than 50% of the voting power of our outstanding shares of capital stock. As a result

of this ownership, the Family has the ability to exert substantial influence over matters requiring action by our stockholders,

including amendments to our certificate of incorporation and by-laws, the election and removal of directors, and any merger,

consolidation, or sale of all or substantially all of our assets, or other corporate transactions. Delaware law provides that the

holders of a majority of the voting power of shares entitled to vote must approve certain fundamental corporate transactions such

as a merger, consolidation and sale of all or substantially all of a corporation’s assets; accordingly, such a transaction involving

us and requiring stockholder approval cannot be effected without the approval of the Family. Such ownership will make an

unsolicited acquisition of our Company more difficult and discourage certain types of transactions involving a change of control

of our Company, including transactions in which the holders of our Common Stock might otherwise receive a premium for their

shares over then current market prices. The Family’s controlling ownership of our capital stock may adversely affect the market

price of our Common Stock.

For additional information, refer to Exhibit 4.1 to this Annual Report on Form 10-K, “Description of Registrant’s Securities

Registered Under Section 12 of the Exchange Act.”

The price of our Common Stock may be affected by the availability of shares for sale in the market, and you may

experience significant dilution as a result of future issuances of our securities, which could materially and adversely affect

the market price of our Common Stock.

The sale or availability for sale of substantial amounts of our Common Stock could adversely impact its price. The Daughters’

LLC holds approximately 1.1 million shares of Common Stock (the “Subject Shares”) that are subject to an Agreement Regarding

Common Stock (the “Agreement”) filed as an exhibit to this report. The Subject Shares remain subject to potential sale under the

Agreement. The Agreement generally provides that if a holder of Subject Shares intends to sell any of the Subject Shares, such

party must give the Company a right of first refusal to purchase all or any of such shares. The price payable by the Company to

purchase shares pursuant to the exercise of the right of first refusal will reflect a 6% discount to the then-current market price

based on the 20 business-day volume-weighted average price. If the Company does not exercise its right of first refusal and

purchase the shares offered, such party will, subject to the approval of a special committee of independent directors of the Board

18

of Directors, be permitted to sell the shares not purchased by the Company pursuant to a Company registration statement, Rule

144 under the Securities Act of 1933, or another manner of sale agreed to by the Company. Although pursuant to the Agreement

the Company will have a right of first refusal to purchase all or any of those shares, the Company may elect not to exercise its

rights of first refusal, and if so such shares would be eligible for sale pursuant to the registration rights in the Agreement or

pursuant to Rule 144 under the Securities Act of 1933. Sales, or the availability for sale, of a large number of shares of our

Common Stock could result in a decline in the market price of our Common Stock.

In addition, our articles of incorporation authorize us to issue 120,000,000 shares of our Common Stock. As of June 1, 2024,

there were 44,238,766 shares of our Common Stock outstanding. Accordingly, a substantial number of shares of our Common

Stock are outstanding and are, or could become, available for sale in the market. In addition, we may be obligated to issue

additional shares of our Common Stock in connection with employee benefit plans (including equity incentive plans).

In the future, we may decide to raise capital through offerings of our Common Stock, additional securities convertible into or

exchangeable for Common Stock, or rights to acquire these securities or our Common Stock. We may also issue such securities

as consideration in an acquisition. The issuance of such securities could result in dilution of existing stockholders’ equity interests

in us. Issuances of substantial amounts of our Common Stock, or the perception that such issuances could occur, may adversely

affect prevailing market prices for our Common Stock, and we cannot predict the effect this dilution may have on the price of our

Common Stock.

LEGAL AND REGULATORY RISK FACTORS

Pressure from animal rights groups regarding the treatment of animals may subject us to additional costs to conform our

practices to comply with developing standards or subject us to marketing costs to defend challenges to our current

practices and protect our image with our customers. In particular, changes in customer preferences and state legislation

have accelerated an increase in demand for cage-free eggs, which increases uncertainty in our business and increases our

costs.

We and many of our customers face pressure from animal rights groups, such as People for the Ethical Treatment of Animals and

the Humane Society of the United States, to require companies that supply food products to operate their business in a manner

that treats animals in conformity with certain standards developed or approved by these groups. In general, we may incur

additional costs to conform our practices to address these standards or to defend our existing practices and protect our image with

our customers. The standards promoted by these groups change over time, but typically require minimum cage space for hens,