UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

For

the quarterly period ended

OR

For the transition period _______________

Commission

File Number:

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification Number) |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s

telephone number, including area code:

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Date File required to be submitted pursuant to Rule

405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | ||

| Non-accelerated filer ☐ | Smaller reporting company | |

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| The |

As of August 6, 2024, there were shares of the Company’s common stock issued and outstanding.

Explanatory Note:

Although on January 1, 2024, we ceased to qualify as a smaller reporting company, as defined in Rule 12b-2 promulgated under the Exchange Act, we have requalified for such status commencing with this Quarterly Report on Form 10-Q, based on the aggregate market value of our common stock held by non-affiliates as of June 30, 2024. Our status as a smaller reporting company allows us to provide scaled disclosure in certain SEC filings, which may permit less disclosure than would apply to reporting companies that did not so qualify.

TABLE OF CONTENTS

| PART I. | FINANCIAL INFORMATION | 1 |

| ITEM 1. | FINANCIAL STATEMENTS (UNAUDITED) | 1 |

| Condensed Consolidated Balance Sheets | 1 | |

| Condensed Consolidated Statements of Operations and Comprehensive (Loss) Income | 2 | |

| Condensed Consolidated Statement of Stockholders’ Deficit | 3 | |

| Condensed Consolidated Statements of Cash Flows | 5 | |

| Notes to Condensed Consolidated Financial Statements | 6 | |

| ITEM 2. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 16 |

| ITEM 3. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 40 |

| ITEM 4. | CONTROLS AND PROCEDURES | 40 |

| PART II. | OTHER INFORMATION | 41 |

| ITEM 1. | LEGAL PROCEEDINGS | 41 |

| ITEM 1A. | RISK FACTORS | 41 |

| ITEM 2. | UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF PROCEEDS | 41 |

| ITEM 3. | DEFAULTS UPON SENIOR SECURITIES | 41 |

| ITEM 4. | MINE SAFETY DISCLOSURES | 41 |

| ITEM 5. | OTHER INFORMATION | 41 |

| ITEM 6. | EXHIBITS | 42 |

| SIGNATURES | 43 | |

| i |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

References in this report to “we,” “us,” “our,” the “Company” and “Inspired” refer to Inspired Entertainment, Inc. and its subsidiaries unless the context suggests otherwise.

Certain statements and other information set forth in this report, including in Item 2, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere herein, may relate to future events and expectations, and as such constitute “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and Section 27A of the Securities Act of 1933, as amended (the “Securities Act”). Our forward-looking statements include, but are not limited to, statements regarding our business strategy, plans and objectives and our expected or contemplated future operations, results, financial condition, beliefs and intentions. In addition, any statements that refer to projections, forecasts or other characterizations or predictions of future events or circumstances, including any underlying assumptions on which such statements are expressly or implicitly based, are forward-looking statements. The words “anticipate,” “believe,” “continue,” “can,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “scheduled,” “seek,” “should,” “would” and similar expressions, among others, and negatives expressions including such words, may identify forward-looking statements.

Our forward-looking statements reflect our current expectations about our future results, performance, liquidity, financial condition, prospects and opportunities, and are based upon information currently available to us, our interpretation of what we believe to be significant factors affecting our business and many assumptions regarding future events. Actual results, performance, liquidity, financial condition, prospects and opportunities could differ materially from those expressed in, or implied by, our forward-looking statements. This could occur as a result of various risks and uncertainties, including the following:

| ● | government regulation of our industries; | |

| ● | our ability to compete effectively in our industries; | |

| ● | the effect of evolving technology on our business; | |

| ● | our ability to renew long-term contracts and retain customers, and secure new contracts and customers; | |

| ● | our ability to maintain relationships with suppliers; | |

| ● | our ability to protect our intellectual property; | |

| ● | our ability to protect our business against cybersecurity threats; | |

| ● | our ability to successfully grow by acquisition as well as organically; | |

| ● | fluctuations due to seasonality; | |

| ● | our ability to attract and retain key members of our management team; | |

| ● | our need for working capital; | |

| ● | our ability to secure capital for growth and expansion; | |

| ● | changing consumer, technology and other trends in our industries; |

| ● | our ability to successfully operate across multiple jurisdictions and markets around the world; | |

| ● | changes in local, regional and global economic and political conditions; and | |

| ● | other factors described in the reports and documents we file from time to time with the U.S. Securities and Exchange Commission (the “SEC”). |

In light of these risks and uncertainties, and others discussed in this report, there can be no assurance that any matters covered by our forward-looking statements will develop as predicted, expected or implied. Readers should not place undue reliance on any forward-looking statements. Except as expressly required by the federal securities laws, we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events, changed circumstances or any other reason. We advise you to carefully review the reports and documents we file from time to time with the SEC.

| ii |

PART I - FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

INSPIRED ENTERTAINMENT, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(in millions, except share data)

June 30, 2024 | December 31, 2023 | |||||||

| (Unaudited) | ||||||||

| Assets | ||||||||

| Cash | $ | $ | ||||||

| Accounts receivable, net | ||||||||

| Inventory | ||||||||

| Prepaid expenses and other current assets | ||||||||

| Total current assets | ||||||||

| Property and equipment, net | ||||||||

| Software development costs, net | ||||||||

| Other acquired intangible assets subject to amortization, net | ||||||||

| Goodwill | ||||||||

| Operating lease right of use asset | ||||||||

| Costs of obtaining and fulfilling customer contracts, net | ||||||||

| Other assets | ||||||||

| Total assets | $ | $ | ||||||

| Liabilities and Stockholders’ Deficit | ||||||||

| Current liabilities | ||||||||

| Accounts payable and accrued expenses | $ | $ | ||||||

| Corporate tax and other current taxes payable | ||||||||

| Deferred revenue, current | ||||||||

| Operating lease liabilities | ||||||||

| Current portion of long-term debt | ||||||||

| Other current liabilities | ||||||||

| Total current liabilities | ||||||||

| Long-term debt | ||||||||

| Finance lease liabilities, net of current portion | ||||||||

| Deferred revenue, net of current portion | ||||||||

| Operating lease liabilities | ||||||||

| Other long-term liabilities | ||||||||

| Total liabilities | ||||||||

| Commitments and contingencies | ||||||||

| Stockholders’ deficit | ||||||||

| Preferred stock; $ par value; shares authorized, shares issued and outstanding at June 30, 2024 and December 31, 2023, respectively. | ||||||||

| Common stock; $ par value; shares authorized; shares and shares issued and outstanding at June 30, 2024 and December 31, 2023, respectively | ||||||||

| Additional paid in capital | ||||||||

| Accumulated other comprehensive income | ||||||||

| Accumulated deficit | ( | ) | ( | ) | ||||

| Total stockholders’ deficit | ( | ) | ( | ) | ||||

| Total liabilities and stockholders’ deficit | $ | $ | ||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 1 |

INSPIRED ENTERTAINMENT, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME (LOSS)

(in millions, except share and per share data)

(Unaudited)

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||

| Revenue: | ||||||||||||||||

| Service | $ | $ | $ | $ | ||||||||||||

| Product sales | ||||||||||||||||

| Total revenue | ||||||||||||||||

| Cost of sales: | ||||||||||||||||

| Cost of service (1) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Cost of product sales (1) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Selling, general and administrative expenses | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Depreciation and amortization | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Net operating income | ||||||||||||||||

| Other expense | ||||||||||||||||

| Interest expense, net | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Other finance income | ||||||||||||||||

| Total other expense, net | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Net income (loss) before income taxes | ( | ) | ||||||||||||||

| Income tax (expense) benefit | ( | ) | ( | ) | ( | ) | ||||||||||

| Net income (loss) | ( | ) | ||||||||||||||

| Other comprehensive income: | ||||||||||||||||

| Foreign currency translation (loss) gain | ( | ) | ( | ) | ( | ) | ||||||||||

| Reclassification of loss on hedging instrument to comprehensive income | ||||||||||||||||

| Actuarial gains on pension plan | ||||||||||||||||

| Other comprehensive income (loss) | ( | ) | ( | ) | ||||||||||||

| Comprehensive income (loss) | $ | $ | $ | ( | ) | $ | ( | ) | ||||||||

| Net income (loss) per common share – basic | $ | $ | $ | ( | ) | $ | ||||||||||

| Net income (loss) per common share - diluted | $ | $ | $ | ( | ) | $ | ||||||||||

| Weighted average number of shares outstanding during the period – basic | ||||||||||||||||

| Weighted average number of shares outstanding during the period – diluted | ||||||||||||||||

| Supplemental disclosure of stock-based compensation expense | ||||||||||||||||

| Stock-based compensation included in: | ||||||||||||||||

| Selling, general and administrative expenses | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

| (1) |

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 2 |

INSPIRED ENTERTAINMENT, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ DEFICIT

FOR THE PERIOD JANUARY 1, 2024 TO JUNE 30, 2024

(in millions, except share data)

(Unaudited)

| Common stock | Additional paid in | Accumulated other comprehensive | Accumulated | Total stockholders’ | ||||||||||||||||||||

| Shares | Amount | capital | income | deficit | deficit | |||||||||||||||||||

| Balance as of January 1, 2024 | $ | $ | $ | | $ | ( | ) | $ | ( | ) | ||||||||||||||

| Foreign currency translation adjustments | — | |||||||||||||||||||||||

| Reclassification of loss on pension plan to comprehensive income | — | |||||||||||||||||||||||

| Issuances under stock plans | ( | ) | ( | ) | ||||||||||||||||||||

| Stock-based compensation expense | — | |||||||||||||||||||||||

| Net loss | — | ( | ) | ( | ) | |||||||||||||||||||

| Balance as of March 31, 2024 | $ | $ | $ | $ | ( | ) | $ | ( | ) | |||||||||||||||

| Foreign currency translation adjustments | — | ( | ) | ( | ) | |||||||||||||||||||

| Reclassification of loss on pension plan to comprehensive income | — | |||||||||||||||||||||||

| Issuances under stock plans | ||||||||||||||||||||||||

| Stock-based compensation expense | — | |||||||||||||||||||||||

| Net income | — | |||||||||||||||||||||||

| Balance as of June 30, 2024 | $ | $ | $ | $ | ( | ) | $ | ( | ) | |||||||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 3 |

INSPIRED ENTERTAINMENT, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ DEFICIT

FOR THE PERIOD JANUARY 1, 2023 TO JUNE 30, 2023

(in millions, except share data)

(Unaudited)

| Common stock | Additional paid in | Accumulated other comprehensive | Accumulated | Total stockholders’ | ||||||||||||||||||||

| Shares | Amount | capital | income | deficit | deficit | |||||||||||||||||||

| Balance as of January 1, 2023 | $ | $ | $ | | $ | ( | ) | $ | ( | ) | ||||||||||||||

| Foreign currency translation adjustments | — | ( | ) | ( | ) | |||||||||||||||||||

| Reclassification of loss on pension plan to comprehensive income | — | |||||||||||||||||||||||

| Reclassification of loss on hedging instrument to comprehensive income | — | |||||||||||||||||||||||

| Issuances under stock plans | ||||||||||||||||||||||||

| Stock-based compensation expense | — | |||||||||||||||||||||||

| Net loss | — | ( | ) | ( | ) | |||||||||||||||||||

| Balance as of March 31, 2023 | $ | $ | $ | $ | ( | ) | $ | ( | ) | |||||||||||||||

| Foreign currency translation adjustments | — | ( | ) | ( | ) | |||||||||||||||||||

| Reclassification of loss on pension plan to comprehensive income | — | |||||||||||||||||||||||

| Reclassification of loss on hedging instrument to comprehensive income | — | |||||||||||||||||||||||

| Repurchase of common stock | ( | ) | ( | ) | ( | ) | ||||||||||||||||||

| Issuances under stock plans | ( | ) | ( | ) | ||||||||||||||||||||

| Stock-based compensation expense | — | |||||||||||||||||||||||

| Net income | — | |||||||||||||||||||||||

| Balance as of June 30, 2023 | $ | $ | $ | $ | ( | ) | $ | ( | ) | |||||||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 4 |

INSPIRED ENTERTAINMENT, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(in millions)

(Unaudited)

Six Months Ended June 30, | ||||||||

| 2024 | 2023 | |||||||

| Cash flows from operating activities: | ||||||||

| Net (loss) income | $ | ( | ) | $ | ||||

| Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||

| Depreciation and amortization | ||||||||

| Amortization of right of use asset | ||||||||

| Stock-based compensation expense | ||||||||

| Contract cost expense | ( | ) | ( | ) | ||||

| Reclassification of loss on hedging instrument to comprehensive income | ||||||||

| Non-cash interest expense relating to senior debt | ||||||||

| Changes in assets and liabilities: | ||||||||

| Accounts receivable | ( | ) | ||||||

| Inventory | ( | ) | ||||||

| Prepaid expenses and other assets | ||||||||

| Corporate tax and other current taxes payable | ( | ) | ( | ) | ||||

| Accounts payable and accrued expenses | ( | ) | ( | ) | ||||

| Deferred revenue and customer prepayment | ||||||||

| Operating lease liabilities | ( | ) | ( | ) | ||||

| Other long-term liabilities | ( | ) | ( | ) | ||||

| Net cash (used in) provided by operating activities | ( | ) | ||||||

| Cash flows from investing activities: | ||||||||

| Purchases of property and equipment | ( | ) | ( | ) | ||||

| Acquisition of third-party company trade and assets | ( | ) | ||||||

| Purchases of capital software and internally developed costs | ( | ) | ( | ) | ||||

| Net cash used in investing activities | ( | ) | ( | ) | ||||

| Cash flows from financing activities: | ||||||||

| Repurchase of common stock | ( | ) | ||||||

| Repayments of finance leases | ( | ) | ( | ) | ||||

| Net cash used in financing activities | ( | ) | ( | ) | ||||

| Effect of exchange rate changes on cash | ( | ) | ||||||

| Net (decrease) increase in cash | ( | ) | ||||||

| Cash, beginning of period | ||||||||

| Cash, end of period | $ | $ | ||||||

| Supplemental cash flow disclosures | ||||||||

| Cash paid during the period for interest | $ | $ | ||||||

| Cash paid during the period for income taxes | $ | $ | ||||||

| Cash paid during the period for operating leases | $ | $ | ||||||

| Supplemental disclosure of non-cash investing and financing activities | ||||||||

| Lease liabilities arising from obtaining right of use assets | $ | ( | ) | $ | ( | ) | ||

| Additional paid in capital from settlement of RSUs | $ | ( | ) | $ | ( | ) | ||

| Property and equipment acquired through finance lease | $ | $ | ||||||

| ARO assets arising during the period | $ | $ | ||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 5 |

1. Nature of Operations, Management’s Plans and Summary of Significant Accounting Policies, as restated

Company Description and Nature of Operations

We are a global gaming technology company, supplying content, platform, gaming terminals and other products and services to online and land-based regulated lottery, betting and gaming operators worldwide through a broad range of distribution channels, predominantly on a business-to-business basis. We provide end-to-end digital gaming solutions (i) on our own proprietary and secure network, which accommodates a wide range of devices, including land-based gaming machine terminals, mobile devices and online computer applications and (ii) through third party networks. Our content and other products can be found through the consumer-facing portals of our interactive customers and, through our land-based customers, in licensed betting offices, adult gaming centers, pubs, bingo halls, airports, motorway service areas and leisure parks.

Management Liquidity Plans

As

of June 30, 2024, the Company’s cash on hand was $

Management currently believes that the Company’s cash balances on hand, cash flows expected to be generated from operations, ability to control and defer capital projects and amounts available from the Company’s external borrowings will be sufficient to fund the Company’s net cash requirements through August 2025.

Basis of Presentation

The accompanying unaudited interim condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) for interim financial information and pursuant to the instructions to Form 10-Q and Article 8 of Regulation S-X of the United States Securities and Exchange Commission (“SEC”). Certain information or footnote disclosures normally included in financial statements prepared in accordance with U.S. GAAP have been condensed or omitted, pursuant to the rules and regulations of the SEC for interim financial reporting. Accordingly, they do not include all the information and footnotes necessary for a comprehensive presentation of financial position, results of operations, or cash flows. It is management’s opinion, however, that the accompanying unaudited interim condensed consolidated financial statements include all adjustments, consisting of a normal recurring nature, which are necessary for a fair presentation of the financial position, operating results and cash flows for the periods presented.

The accompanying unaudited interim condensed consolidated financial statements should be read in conjunction with the Company’s consolidated financial statements and notes thereto for the years ended December 31, 2023 and 2022. The financial information as of December 31, 2023 is derived from the audited consolidated financial statements presented in the Company’s Annual Report on Form 10-K for the year ended December 31, 2023 filed with the SEC on April 15, 2024. The financial information for the three and six months ended June 30, 2023 is derived from the unaudited consolidated financial statements presented in the Company’s Quarterly Report on Form 10-Q/A for the three and six months ended June 30, 2023 filed with the SEC on February 27, 2024. The interim results for the three and six months ended June 30, 2024 are not necessarily indicative of the results to be expected for the year ending December 31, 2024 or for any future interim periods.

| 6 |

2. Allowance for Credit Losses

Changes in the allowance for credit losses are as follows:

June 30, 2024 | December 31, 2023 | |||||||

| (in millions) | ||||||||

| Beginning balance | $ | ( | ) | $ | ( | ) | ||

| Additional allowance for credit losses | ( | ) | ( | ) | ||||

| Recoveries | ||||||||

| Write offs | ||||||||

| Foreign currency translation adjustments | ( | ) | ||||||

| Ending balance | $ | ( | ) | $ | ( | ) | ||

3. Inventory

Inventory consists of the following:

June 30, 2024 | December 31, 2023 | |||||||

| (in millions) | ||||||||

| Component parts | $ | $ | ||||||

| Work in progress | ||||||||

| Finished goods | ||||||||

| Total inventories | $ | $ | ||||||

Component parts include parts for gaming terminals. Our finished goods inventory primarily consists of gaming terminals which are ready for sale.

4. Accounts Payable and Accrued Expenses

Accounts payable and accrued expenses consist of the following:

June 30, 2024 | December 31, 2023 | |||||||

| (in millions) | ||||||||

| Accounts payable | $ | $ | ||||||

| Payroll and related costs | ||||||||

| Cost of sales including inventory | ||||||||

| Other | ||||||||

| Total accounts payable and accrued expenses | $ | $ | ||||||

| 7 |

5. Contract Related Disclosures

The following table summarizes contract related balances:

Accounts Receivable | Unbilled Accounts Receivable | Right to recover asset | Deferred Income | Customer Prepayments and Deposits | ||||||||||||||||

| (in millions) | ||||||||||||||||||||

| At June 30, 2024 | $ | $ | $ | $ | ( | ) | $ | ( | ) | |||||||||||

| At December 31, 2023 | $ | $ | $ | $ | ( | ) | $ | ( | ) | |||||||||||

Revenue

recognized that was included in the deferred income balance at the beginning of the period amounted to $

For the periods ended June 30, 2024 and 2023 respectively, there were no significant amounts of revenue recognized as a result of changes in contract transaction price related to performance obligations that were satisfied in the respective prior periods.

Transaction Price Allocated to Remaining Performance Obligations

At

June 30, 2024, the transaction price allocated to unsatisfied performance obligations for contracts expected to be greater than one year,

or performance obligations for which we do not have a right to consideration from the customer in the amount that corresponds to the

value to the customer for our performance completed to date, variable consideration which is not accounted for in accordance with the

sales-based or usage-based royalties guidance, or contracts which are not wholly unperformed, was approximately $

6. Long Term and Other Debt

Under our debt facilities in place as of June 30, 2024, we were not subject to covenant testing on our senior secured notes (the “Senior Secured Notes”). We are, however, subject to covenant testing at the level of Inspired Entertainment Inc., the ultimate holding company, on our Revolving Credit Facility Agreement (the “RCF Agreement”) which required the Company to maintain a maximum consolidated senior secured net leverage ratio of 6.0x on March 31, 2022, stepping down to 5.75x on March 31, 2023 and 5.50x from March 31, 2024 and thereafter (the “RCF Financial Covenant”). The RCF Financial Covenant is calculated as the ratio of consolidated senior secured net debt to consolidated pro forma EBITDA (defined as net loss excluding depreciation and amortization, interest expense, interest income and income tax expense) for the 12-month period preceding the relevant quarterly testing date and is tested quarterly on a rolling basis, subject to the Initial Facility (as defined in the RCF Agreement) being drawn on the relevant test date. The RCF Financial Covenant does not include a minimum interest coverage ratio or other financial covenants. Covenant testing at June 30, 2024 showed covenant compliance with a net leverage of 3.1x.

The Indenture governing the Senior Secured Notes contains covenants and certain reporting requirements including the requirement to provide the lender, within 60 days after the close of the quarter, unaudited quarterly financial statements with footnote disclosures.

There were no covenant violations in the periods ended June 30, 2024 or June 30, 2023.

Number of Shares | ||||

| Unvested Outstanding at January 1, 2024 (1) | ||||

| Granted (2) | ||||

| Forfeited | ( | ) | ||

| Vested | ( | ) | ||

| Unvested Outstanding at June 30, 2024 | ||||

| (1) |

|

| (2) |

The Company issued a total of shares during the six months ended June 30, 2024, in connection with the Company’s equity-based plans, which included an aggregate of shares issued in connection with the net settlement of RSUs that vested during the prior year (primarily on December 29, 2023).

8. Accumulated Other Comprehensive Loss (Income)

The accumulated balances for each classification of comprehensive loss (income) are presented below:

Foreign Currency Translation Adjustments | Change in Fair Value of Hedging Instrument | Unrecognized Pension Benefit Costs | Accumulated Other Comprehensive (Income) | |||||||||||||

| (in millions) | ||||||||||||||||

| Balance at January 1, 2024 | $ | ( | ) | $ | $ | $ | ( | ) | ||||||||

| Change during the period | ( | ) | ( | ) | ( | ) | ||||||||||

| Balance at March 31, 2024 | ( | ) | ( | ) | ||||||||||||

| Change during the period | ( | ) | ( | ) | ||||||||||||

| Balance at June 30, 2024 | $ | ( | ) | $ | $ | $ | ( | ) | ||||||||

Foreign Currency Translation Adjustments | Change in Fair Value of Hedging Instrument | Unrecognized Pension Benefit Costs | Accumulated Other Comprehensive (Income) | |||||||||||||

| (in millions) | ||||||||||||||||

| Balance at January 1, 2023 | $ | ( | ) | $ | $ | $ | ( | ) | ||||||||

| Change during the period | ( | ) | ( | ) | ||||||||||||

| Balance at March 31, 2023 | ( | ) | ( | ) | ||||||||||||

| Change during the period | ( | ) | ( | ) | ||||||||||||

| Balance at June 30, 2023 | $ | ( | ) | $ | $ | $ | ( | ) | ||||||||

In

connection with the issuance of the Senior Secured Notes, and the entry into the

“RCF Agreement on May 19, 2021, the Company terminated all of its interest rate swaps. Accordingly, hedge accounting is

no longer applicable. The amounts previously recorded in Accumulated Other Comprehensive Income were amortized into Interest expense

over the terms of the hedged forecasted interest payments. Losses reclassified from Accumulated Other Comprehensive Income into Interest

expense in the Consolidated Statements of Operations and Income for the six months ended June 30, 2024 and June 30, 2023 amounted to

$

| 8 |

Basic income/loss per share (“EPS”) is computed by dividing net income/loss attributable to common stockholders by the weighted-average number of common shares outstanding during the period, excluding the effects of any potentially dilutive securities. Diluted EPS gives effect to all dilutive potential shares of common stock outstanding during the period, including stock options and RSUs, unless the inclusion would be anti-dilutive.

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||

| RSUs | ||||||||||||||||

| Three months ended June 30, 2024 | Income (Numerator) (in millions) | Shares (Denominator) | Per-Share Amount | |||||||||

| Basic EPS | ||||||||||||

| Income available to common stockholders | $ | | $ | | ||||||||

| Effect of Dilutive Securities | ||||||||||||

| RSUs | $ | |||||||||||

| Diluted EPS | ||||||||||||

| Income available to common stockholders | $ | $ | ||||||||||

| Three months ended June 30, 2023 | Income (Numerator) (in millions) | Shares (Denominator) | Per-Share Amount | |||||||||

| Basic EPS | ||||||||||||

| Income available to common stockholders | $ | | $ | | ||||||||

| Effect of Dilutive Securities | ||||||||||||

| RSUs | $ | ( | ) | |||||||||

| Diluted EPS | ||||||||||||

| Income available to common stockholders | $ | $ | ||||||||||

| Six months ended June 30, 2023 | Income (Numerator) (in millions) | Shares (Denominator) | Per-Share Amount | |||||||||

| Basic EPS | ||||||||||||

| Income available to common stockholders | $ | | $ | | ||||||||

| Effect of Dilutive Securities | ||||||||||||

| RSUs | $ | ( | ) | |||||||||

| Diluted EPS | ||||||||||||

| Income available to common stockholders | $ | $ | ||||||||||

The calculation of Basic EPS includes the effects of and shares for the three and six months ended June 30, 2024 and 2023, respectively, with respect to RSU awards that have vested but have not yet been issued.

| 9 |

10. Other Finance Income

Other finance income consisted of the following:

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||

| (in millions) | (in millions) | |||||||||||||||

| Pension interest cost | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

| Expected return on pension plan assets | ||||||||||||||||

| $ | $ | $ | $ | |||||||||||||

11. Income Taxes

The

effective income tax rate for the three months ended June 30, 2024 and 2023 was

The effective tax rate reported in any given year will continue to be influenced by a variety of factors including the level of pre-tax income or loss, the income mix between jurisdictions, and any discrete items that may occur.

The Company recorded a valuation allowance against all of our deferred tax assets as of both June 30, 2024 and 2023. We intend to continue maintaining a full valuation allowance on our deferred tax assets until there is sufficient evidence to support the reversal of all or some portion of these allowances. However, given our current earnings and anticipated future earnings, we believe that there is a reasonable possibility that within the next twelve months, sufficient positive evidence may become available to allow us to reach a conclusion that a significant portion of the valuation allowance will no longer be needed. Release of the valuation allowance would result in the recognition of certain deferred tax assets and a decrease to income tax expense for the period the release is recorded. However, the exact timing and amount of the valuation allowance release are subject to change on the basis of the level of profitability that we are able to actually achieve.

12. Related Parties

Macquarie

Corporate Holdings Pty Limited (UK Branch) (“Macquarie UK”), (an arranger and lending party under our RCF Agreement) is an

affiliate of MIHI LLC, which beneficially owned approximately

Richard

Weil, the brother of A. Lorne Weil, our Executive Chairman, provides consulting services to the Company relating to our lottery operations

in the Dominican Republic under a consultancy agreement dated December 31, 2021, as amended. The aggregate amount incurred by the Company

in consulting fees was $

| 10 |

13. Leases

Certain of our arrangements include leases for equipment installed at customer locations. As the lessor, we combine lease and non-lease components for all classes of underlying assets in arrangements that involve operating leases. The single combined component is accounted for under ASC 606, Revenue from Contracts with Customers based on the consideration that the non-lease components are the predominant items in the arrangements. If a component cannot be combined, the consideration is allocated between the lease component and the non-lease component based on relative standalone selling price. The lease component is accounted for under ASC 842, Leases and the non-lease component is accounted for under ASC 606.

Lease income from operating leases is not material for any of the periods presented. Lease income from sales type leases is as follows:

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||

| (in millions) | (in millions) | |||||||||||||||

| Interest receivable | $ | $ | ||||||||||||||

| Profit recognized at commencement date of sales type leases | ||||||||||||||||

| $ | $ | $ | $ | |||||||||||||

14. Commitments and Contingencies

Employment Agreements

We are party to employment agreements with our executive officers and other employees of the Company and our subsidiaries which contain, among other terms, provisions relating to severance and notice requirements.

Legal Matters

From time to time, the Company may become involved in lawsuits and legal matters arising in the ordinary course of business. While the Company believes that, currently, it has no such matters that are material, there can be no assurance that existing or new matters arising in the ordinary course of business will not have a material adverse effect on the Company’s business, financial condition or results of operations.

| 11 |

15. Pension Plan

We operate a defined contribution plan in the US, and both defined benefit and defined contribution pension schemes in the UK. The defined contribution scheme assets are held separately from those of the Company in independently administered funds.

Defined Benefit Pension Scheme

The defined benefit scheme has been closed to new entrants since April 1, 1999 and closed to future accruals for services rendered to the Company for the entire financial statement periods presented. The latest actuarial valuation of the scheme (as at March 31, 2021), which was finalized in June 2022, determined that the statutory funding objective was not met, i.e., there were insufficient assets to cover the scheme’s technical provisions and there was a funding shortfall.

In June 2022, a recovery plan was put in place to eliminate the funding shortfall. The plan expects the shortfall to be eliminated by October 31, 2026.

The following table presents the components of our net periodic pension cost:

Six Months Ended June 30, | ||||||||

| 2024 | 2023 | |||||||

| (in millions) | ||||||||

| Components of net periodic pension cost: | ||||||||

| Interest cost | $ | $ | ||||||

| Expected return on plan assets | ( | ) | ( | ) | ||||

| Amortization of net loss | ||||||||

| Net periodic cost | $ | $ | ||||||

| 12 |

16. Segment Reporting and Geographic Information

The Company operates its business along four operating segments, which are segregated on the basis of revenue stream: Gaming, Virtual Sports, Interactive and Leisure. The Company believes this method of segment reporting reflects both the way its business segments are managed and the way the performance of each segment is evaluated.

The following tables present revenue, cost of sales, excluding depreciation and amortization, selling, general and administrative expenses, stock-based compensation expense and depreciation and amortization, operating income (loss) and total capital expenditures for the periods ended June 30, 2024 and June 30, 2023, respectively, by business segment. Certain unallocated corporate function costs have not been allocated to the Company’s reportable operating segments because these costs are not allocable and to do so would not be practical. Corporate function costs consist primarily of selling, general and administrative expenses, depreciation and amortization and capital expenditures relating to corporate/shared functions.

Segment Information

Three Months Ended June 30, 2024

| Gaming | Virtual Sports | Interactive | Leisure | Corporate Functions | Total | |||||||||||||||||||

| (in millions) | ||||||||||||||||||||||||

| Revenue: | ||||||||||||||||||||||||

| Service | $ | $ | $ | $ | $ | $ | ||||||||||||||||||

| Product sales | ||||||||||||||||||||||||

| Total revenue | ||||||||||||||||||||||||

| Cost of sales, excluding depreciation and amortization: | ||||||||||||||||||||||||

| Cost of service | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||||

| Cost of product sales | ( | ) | ( | ) | ( | ) | ||||||||||||||||||

| Selling, general and administrative expenses | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||

| Stock-based compensation expense | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||

| Depreciation and amortization | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||

| Segment operating income (loss) | ( | ) | ||||||||||||||||||||||

| Net operating income | $ | |||||||||||||||||||||||

| Total capital expenditures for the three months ended June 30, 2024 | $ | $ | $ | $ | $ | $ | ||||||||||||||||||

Three Months Ended June 30, 2023

| Gaming | Virtual Sports | Interactive | Leisure | Corporate Functions | Total | |||||||||||||||||||

| (in millions) | ||||||||||||||||||||||||

| Revenue: | ||||||||||||||||||||||||

| Service | $ | $ | $ | $ | $ | $ | ||||||||||||||||||

| Product sales | ||||||||||||||||||||||||

| Total revenue | ||||||||||||||||||||||||

| Cost of sales, excluding depreciation and amortization: | ||||||||||||||||||||||||

| Cost of service | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||||

| Cost of product sales | ( | ) | ( | ) | ||||||||||||||||||||

| Selling, general and administrative expenses | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||

| Stock-based compensation expense | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||

| Depreciation and amortization | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||

| Segment operating income (loss) | ( | ) | ||||||||||||||||||||||

| Net operating income | $ | |||||||||||||||||||||||

| Total capital expenditures for the three months ended June 30, 2023 | $ | $ | $ | $ | $ | $ | ||||||||||||||||||

| 13 |

Six Months Ended June 30, 2024

| Gaming | Virtual Sports | Interactive | Leisure | Corporate Functions | Total | |||||||||||||||||||

| (in millions) | ||||||||||||||||||||||||

| Revenue: | ||||||||||||||||||||||||

| Service | $ | $ | $ | $ | $ | $ | ||||||||||||||||||

| Product sales | ||||||||||||||||||||||||

| Total revenue | ||||||||||||||||||||||||

| Cost of sales, excluding depreciation and amortization: | ||||||||||||||||||||||||

| Cost of service | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||||

| Cost of product sales | ( | ) | ( | ) | ( | ) | ||||||||||||||||||

| Selling, general and administrative expenses | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||

| Stock-based compensation expense | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||

| Depreciation and amortization | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||

| Segment operating income (loss) | ( | ) | ||||||||||||||||||||||

| Net operating income | $ | |||||||||||||||||||||||

| Total capital expenditures for the six months ended June 30, 2024 | $ | $ | $ | $ | $ | $ | ||||||||||||||||||

Six Months Ended June 30, 2023

| Gaming | Virtual Sports | Interactive | Leisure | Corporate Functions | Total | |||||||||||||||||||

| (in millions) | ||||||||||||||||||||||||

| Revenue: | ||||||||||||||||||||||||

| Service | $ | $ | $ | $ | $ | $ | ||||||||||||||||||

| Product sales | ||||||||||||||||||||||||

| Total revenue | ||||||||||||||||||||||||

| Cost of sales, excluding depreciation and amortization: | ||||||||||||||||||||||||

| Cost of service | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||||

| Cost of product sales | ( | ) | ( | ) | ( | ) | ||||||||||||||||||

| Selling, general and administrative expenses | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||

| Stock-based compensation expense | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||

| Depreciation and amortization | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||

| Segment operating income (loss) | ( | ) | ||||||||||||||||||||||

| Net operating income | $ | |||||||||||||||||||||||

| Total capital expenditures for the six months ended June 30, 2023 | $ | $ | $ | $ | $ | $ | ||||||||||||||||||

| 14 |

Geographic Information

Geographic information for revenue is set forth below:

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||

| (in millions) | (in millions) | |||||||||||||||

| Total revenue | ||||||||||||||||

| UK | $ | $ | $ | $ | ||||||||||||

| Greece | ||||||||||||||||

| Rest of world | ||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||

UK revenue includes revenue from customers headquartered in the UK, but whose revenue is generated globally.

Geographic information of our non-current assets excluding goodwill is set forth below:

June 30, 2024 | December 31, 2023 | |||||||

| (in millions) | ||||||||

| UK | $ | $ | ||||||

| Greece | ||||||||

| Rest of world | ||||||||

| Total | $ | $ | ||||||

Software development costs are included as attributable to the market in which they are utilized.

17. Customer Concentration

During

the three months ended June 30, 2024, no customers represented at least 10% of the Company’s revenue. During the three months

ended June 30, 2023, one customer represented at least 10% of the Company’s revenue, accounting for

During

the six months ended June 30, 2024, one customer represented at least 10% of the Company’s revenue, accounting for

At

June 30, 2024, no customers represented at least 10% of the Company’s accounts receivable. At December 31, 2023, one customer

represented at least 10% of the Company’s accounts receivable, accounting for approximately

18. Subsequent Events

The Company evaluates subsequent events and transactions that occur after the balance sheet date up to the date that the financial statements were issued. Based upon this review, the Company did not identify subsequent events that would have required adjustment or disclosure in the consolidated financial statements.

| 15 |

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with the financial statements and related notes thereto included elsewhere in this report. This discussion contains forward-looking statements that involve risks and uncertainties. Our actual future results could differ materially from the historical results discussed below. Factors that could cause or contribute to such differences include, but are not limited to, those identified below and those referenced in the section titled “Risk Factors” included in our annual report on Form 10-K for our fiscal year ended December 31, 2023, filed with the SEC on April 15, 2024.

Forward-Looking Statements

We make forward-looking statements in this Management’s Discussion and Analysis of Financial Condition and Results of Operations. For definitions of the term Forward-Looking Statements, see the definitions provided in the Cautionary Note Regarding Forward-Looking Statements at the forepart of this report

Seasonality

Our results of operations can fluctuate due to seasonal trends and other factors. Sales of our gaming machines can vary quarter on quarter due to both supply and demand factors. Player activity for our holiday parks is generally higher in the second and third quarters of the year, particularly during the summer months and slower during the first and fourth quarters of the year.

Revenue

We generate revenue in four principal ways: i) on a participation basis, ii) on a fixed rental fee basis, iii) through product sales and iv) through software license fees. Participation revenue generally includes a right to receive a share of our customers’ gaming revenue, typically as a share of net win but sometimes as a share of the handle or “coin in” which represents the total amount wagered.

Geographic Range

Geographically, the majority of our revenue is derived from, and the majority of our non-current assets are attributable to, our UK operations. The remainder of our revenue is derived from, and non-current assets attributable to, Greece and the rest of the world (including North America).

For the three and six months ended June 30, 2024, we derived approximately 75% (in both periods) of our revenue from the UK (including customers headquartered in the UK but whose revenue is generated globally), respectively, 6% and 8% from Greece, respectively, and the remaining 19% and 17% across the rest of the world. During the three and six months ended June 30, 2023, we derived approximately 78% and 77% from the UK, 7% and 8% from Greece and 15% (in both periods) for the rest of world.

As of June 30, 2024, our non-current assets (excluding goodwill) were attributable as follows: 70% to the UK, 10% to Greece and 20% across the rest of the world. As of June 30, 2023, our non-current assets (excluding goodwill) were attributable as follows: 77% to the UK, 4% to Greece and 19% across the rest of the world.

| 16 |

Foreign Exchange

Our results are affected by changes in foreign currency exchange rates as a result of the translation of foreign functional currencies into our reporting currency and the re-measurement of foreign currency transactions and balances. The impact of foreign currency exchange rate fluctuations represents the difference between current rates and prior-period rates applied to current activity. The geographic region in which the largest portion of our business is operated is the UK and the British pound (“GBP”) is considered to be our functional currency. Our reporting currency is the U.S. dollar (“USD”). Our results are translated from our functional currency of GBP into the reporting currency of USD using average rates for profit and loss transactions and applicable spot rates for period-end balances. The effect of translating our functional currency into our reporting currency, as well as translating the results of foreign subsidiaries that have a different functional currency into our functional currency, is reported separately in Accumulated Other Comprehensive Income.

During the three and six months ended June 30, 2024, we derived approximately 25% (in both periods) of our revenue from sales to customers outside the UK (see caveat above), compared to 22% and 23% during the three and six months ended June 30, 2023, respectively.

In the section “Results of Operations” below, currency impacts shown have been calculated as the current-period average GBP:USD rate less the equivalent average rate in the prior year period, multiplied by the current period amount in our functional currency (GBP). The remaining difference, referred to as functional currency at constant rate, is calculated as the difference in our functional currency, multiplied by the prior-period average GBP:USD rate. This is not a U.S. GAAP measure, but is one which management believes gives a clearer indication of results. In the tables below, variances in particular line items from period to period exclude currency translation movements, and currency translation impacts are shown independently.

Non-GAAP Financial Measures

We use certain financial measures that are not compliant with U.S. GAAP (“Non-GAAP financial measures”), including EBITDA and Adjusted EBITDA, to analyze our operating performance. In this discussion and analysis, we present certain non-GAAP financial measures, define and explain these measures and provide reconciliations to the most comparable U.S. GAAP measures. See “Non-GAAP Financial Measures” below.

Results of Operations

Our results are affected by changes in foreign currency exchange rates, primarily between our functional currency (GBP) and our reporting currency (USD). During the three month periods ended June 30, 2024 and June 30, 2023, the average GBP:USD rates were 1.26 and 1.25, respectively, and for the six-month period were 1.27 and 1.24, respectively.

The following discussion and analysis of our results of operations has been organized in the following manner:

| ● | a discussion and analysis of the Company’s results of operations for the three and six-month periods ended June 30, 2024, compared to the same period in 2023; and | |

| ● | a discussion and analysis of the results of operations for each of the Company’s segments (Gaming, Virtual Sports, Interactive and Leisure) for the three and six-month periods ended June 30, 2024, compared to the same period in 2023, including key performance indicator (“KPI”) analysis. |

| 17 |

In the discussion and analysis below, certain data may vary from the amounts presented in our consolidated financial statements due to rounding.

For all reported variances, refer to the overall company and segment tables shown below. All variances discussed in the overall company and segment results are on a functional currency (at constant rate) basis, which excludes the impact of any changes in foreign currency exchange rates.

Key Events – Current Quarter

During the three-month period ended June 30, 2024 in the Gaming segment, Alberta Gaming, Liquor and Cannabis (“AGLC”) in Canada ordered 150 new Valor terminals which were deployed during the quarter following a successful six-month trial. In addition, William Hill has committed to lease 5,000 new Vantage® terminals. Deployment of the new terminals will begin in the fourth quarter of 2024, with expected completion in the first half of 2025.

During the three-month period ended June 30, 2024 we partnered with the NBA to provide a Virtual Sports offering, which went live in the Greek market during the period.

During the three-month period ended June 30, 2024 the Interactive segment went live with fourteen new operators. The total number of customers at the end of the period increased by nine due to changes with several smaller-scale customers. In addition, Inspired licensed its remote gaming server (“RGS”) to an operator customer, allowing the customer to host its own instance of the most recent version of our RGS.

Inspired also announced an engagement with Tunley Environmental to conduct a thorough business carbon assessment, with the goal of reducing the company’s carbon footprint aligning with the Company’s commitment to reduce its environmental footprint.

Key agreements made in the ordinary course of business in the three-month period ended June 30, 2024 include a contract with Meadow Bay Villages to run the family entertainment center at Billing Aquadrome, Northampton UK resulting in installations in May and July 2024.

Overall Company Results

Three and Six Months ended June 30, 2024, compared to Three and Six Months ended June 30, 2023

| For the Three-Month Period ended | Variance | For the Six-Month Period ended | Variance | |||||||||||||||||||||||||||||||||||||||||||||

| (In millions) | June 30, | June 30, | 2024 vs 2023 | June 30, | June 30, | 2024 vs 2023 | ||||||||||||||||||||||||||||||||||||||||||

| 2024 | 2023 | Variance Attributable to Currency Movement | Variance on a Functional currency basis | Total Functional Currency Variance % | Total Reported Variance % | 2024 | 2023 | Variance Attributable to Currency Movement | Variance on a Functional currency basis | Total Functional Currency Variance % | Total Reported Variance % | |||||||||||||||||||||||||||||||||||||

| Revenue: | ||||||||||||||||||||||||||||||||||||||||||||||||

| Service | $ | 65.8 | $ | 67.5 | $ | 0.6 | $ | (2.3 | ) | (3 | )% | (3 | )% | $ | 122.9 | $ | 125.0 | $ | 3.0 | $ | (5.1 | ) | (4 | )% | (2 | )% | ||||||||||||||||||||||

| Product | 9.8 | 11.9 | 0.2 | (2.3 | ) | (19 | )% | (18 | )% | 15.8 | 19.3 | 0.4 | (3.9 | ) | (20 | )% | (18 | )% | ||||||||||||||||||||||||||||||

| Total revenue | 75.6 | 79.4 | 0.8 | (4.6 | ) | (6 | )% | (5 | )% | 138.7 | 144.3 | 3.4 | (9.0 | ) | (6 | )% | (4 | )% | ||||||||||||||||||||||||||||||

| Cost of Sales, excluding depreciation and amortization: | ||||||||||||||||||||||||||||||||||||||||||||||||

| Cost of Service | (19.0 | ) | (20.5 | ) | (0.1 | ) | 1.6 | (8 | )% | (7 | )% | (34.9 | ) | (35.5 | ) | (0.7 | ) | 1.3 | (4 | )% | (2 | )% | ||||||||||||||||||||||||||

| Cost of Product | (5.8 | ) | (8.4 | ) | - | 2.6 | (31 | )% | (31 | )% | (10.3 | ) | (15.1 | ) | (0.3 | ) | 5.1 | (34 | )% | (32 | )% | |||||||||||||||||||||||||||

| Selling, general and administrative expenses | (29.2 | ) | (23.5 | ) | (0.3 | ) | (5.4 | ) | 23 | % | 24 | % | (61.1 | ) | (49.8 | ) | (1.7 | ) | (9.6 | ) | 19 | % | 23 | % | ||||||||||||||||||||||||

| Stock-based compensation | (1.6 | ) | (3.1 | ) | 0.2 | 1.3 | (42 | )% | (48 | )% | (3.9 | ) | (6.0 | ) | - | 2.1 | (35 | )% | (35 | )% | ||||||||||||||||||||||||||||

| Depreciation and amortization | (10.6 | ) | (10.1 | ) | (0.2 | ) | (0.3 | ) | 3 | % | 5 | % | (20.5 | ) | (19.5 | ) | (0.5 | ) | (0.5 | ) | 3 | % | 5 | % | ||||||||||||||||||||||||

| Net operating Income | 9.4 | 13.8 | 0.4 | (4.8 | ) | (35 | )% | (32 | )% | 8.0 | 18.4 | 0.2 | (10.6 | ) | (58 | )% | (57 | )% | ||||||||||||||||||||||||||||||

| Other income (expense) | ||||||||||||||||||||||||||||||||||||||||||||||||

| Interest expense, net | (6.7 | ) | (7.3 | ) | (0.1 | ) | 0.7 | (10 | )% | (8 | )% | (13.3 | ) | (13.6 | ) | (0.4 | ) | 0.7 | (5 | )% | (2 | )% | ||||||||||||||||||||||||||

| Other finance income (expense) | 0.1 | 0.1 | - | - | 0 | % | 0 | % | 0.2 | 0.2 | - | - | 0 | % | 0 | % | ||||||||||||||||||||||||||||||||

| Total other income (expense), net | (6.6 | ) | (7.2 | ) | (0.1 | ) | 0.7 | (10 | )% | (8 | )% | (13.1 | ) | (13.4 | ) | (0.4 | ) | 0.7 | (5 | )% | (2 | )% | ||||||||||||||||||||||||||

| Net Income (loss) from continuing operations before income taxes | 2.8 | 6.6 | 0.3 | (4.1 | ) | (62 | )% | (58 | )% | (5.1 | ) | 5.0 | (0.2 | ) | (9.9 | ) | (198 | )% | (202 | )% | ||||||||||||||||||||||||||||

| Income tax expense | (0.8 | ) | (1.0 | ) | (0.1 | ) | 0.3 | (30 | )% | (20 | )% | 1.4 | (0.8 | ) | - | 2.2 | (275 | )% | (275 | )% | ||||||||||||||||||||||||||||

| Net Income (Loss) | $ | 2.0 | $ | 5.6 | $ | 0.2 | $ | (3.8 | ) | (68 | )% | (64 | )% | $ | (3.7 | ) | $ | 4.2 | $ | (0.3 | ) | $ | (7.6 | ) | (181 | )% | (188 | )% | ||||||||||||||||||||

| Exchange Rate - $ to £ | 1.26 | 1.25 | 1.27 | 1.23 | ||||||||||||||||||||||||||||||||||||||||||||

See “Segments Results” below for a more detailed explanation of the significant changes in our components of revenue within the individual segment results of operations.

| 18 |

Revenue (for the three and six months ended June 30, 2024, compared to the three and six months ended June 30, 2023)

Consolidated Reported Revenue by Segment

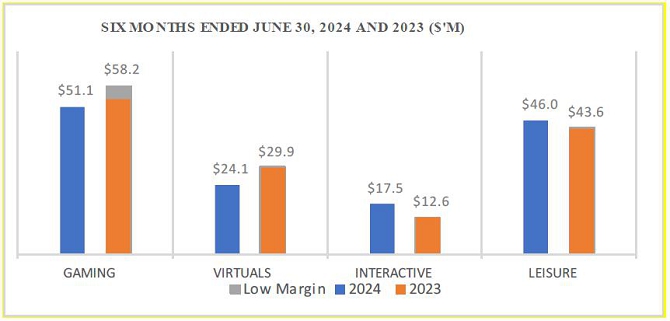

| ● | There were no Low Margin-related sales for the three and six-months ended June 30, 2024. For the three and six-months ended June 30, 2023 Low Margin-related sales were $4.4 million (in both periods) |

For the three and six months ended June 30, 2024, revenue on a functional currency (at constant rate) basis decreased by $4.6 million and $9.0 million, respectively, or 6% (in both periods)

For the three-month period ended June 30, 2024, Gaming revenue declined by $4.3 million. Gaming product sales declined $2.1 million due to a decrease in the UK market, partially offset by growth in North America, Gaming service revenue declined $2.2 million, due to a decrease in the UK and mainland European markets. Virtual Sports declined by $3.5 million due to reduced Online revenue. Interactive grew by $2.7 million, driven by revenue growth in the UK, North America and mainland Europe: and Leisure grew by $0.7 million predominately driven by the increased revenues in Holiday Parks due to the addition of a new site as well as growth in existing sites.

For the six-month period ended June 30, 2024, Gaming revenue declined by $8.2 million. Gaming product sales declined $3.7 million due to a decrease in the UK market for low margin sales in the prior year period not repeated in the current year, partially offset by growth in North America, Gaming service revenue decreased by $4.5 million predominately due to revenue decline in the UK and mainland European markets. Virtual Sports decreased by $6.4 million due to a decrease in Online revenue; Interactive grew by $4.6 million, driven by revenue growth in the UK, mainland Europe and Latin America; and Leisure revenue increased by $1.4 million due to increases in Holiday Parks and Pubs.

| 19 |

Cost of Sales, excluding depreciation and amortization

Cost of sales, excluding depreciation and amortization, for the three and six months ended June 30, 2024, decreased by $4.2 million and $6.4 million, or 15% and 13%, respectively. The decreases were driven by a $1.6 million and $1.3 million decrease in cost of service, respectively, predominately driven by the decrease in service revenues and by a $2.6 million and $5.1 million decrease in cost of product, predominantly driven by the decrease in product revenues, respectively.

Selling, general and administrative expenses

Selling, general and administrative (“SG&A”) expenses for the three and six months ended June 30, 2024 increased by $5.4 million and $9.6 million, or 23% and 19%, respectively.

The increase in the three-month period ended June 30, 2024, was primarily driven by an increase of $2.8 million due to cost of the restatement of our prior financial statements (excluded from adjusted EBITDA), $0.7 million due to cost of restructuring (excluded from adjusted EBITDA) and $0.9 million due to non-staff costs mainly for increased facility, travel, storage and distribution costs.

The increase in the six-month period ended June 30, 2024, was driven primarily by the $7.8 million costs of the restatement of our prior financial statements (removed from Adjusted EBITDA), an increase in non-staff costs of $2.9 million, of which the largest proportion was driven by increased facility, travel, external labor, IT, storage and distribution costs as well as an increase in staff cost of $0.5 million driven by support staff costs and an increase in national living wage and salary increases. This was partially offset by a reduction in the cost of group restructure of $2.1 million (removed from Adjusted EBITDA).

Stock-based compensation

During the three and six-month periods ended June 30, 2024, the Company recorded stock based compensation expenses of $1.6 million and $3.9 million, respectively, compared to stock based compensation expenses of $3.1 million and $6.0 million for the three and six months ended June 30, 2023. All expenses related to outstanding awards but the three and six months ended June 30, 2023, included $0.4 million related to award units that were fully vested on the date of grant and therefore were expensed immediately. The six months ended June 30, 2023 also included $0.7 million related to the group restructure.

Depreciation and amortization

Depreciation and amortization for the three-month period ended June 30, 2024, increased by $0.3 million. This increase was driven by increases in Virtual Sports of $1.6 million and Interactive of $0.2 million, partially offset by a reduction in Gaming of $1.2 million, due to assets being fully depreciated.

Depreciation and amortization for the six-month period ended June 30, 2024, increased by $0.5 million. This increase was driven by increases in Virtual Sports of $1.7 million and Interactive of $0.7 million, partially offset by a reduction in Gaming of $1.6 million and Leisure of $0.3 million due to assets being fully depreciated.

Net operating income / net income/(loss)

During the three and six-month periods ended June 30, 2024, net operating income was $9.4 million and $8.0 million, respectively, representing declines of $4.8 million and $10.6 million, respectively, compared to the prior year periods. The decreases were primarily due to the increases in SG&A expenses, (including the cost of restating our prior financial statements in the three and six-month periods).

For the three and six-months ended June 30, 2024 net income / (loss) was $2.0 million and net loss was $3.7 million, respectively, compared to a net income of $5.6 million and $4.2 million, respectively, in the prior periods.

For the three-month period ended June 30, 2024 the $3.8 million decline compared to the prior year period, was primarily due to the increase in SG&A expenses of $5.4 million. This was partially offset by a reduction in stock-based compensation of $1.3 million.

For the six-month period ended June 30. 2024 the $7.6 million decline compared to the prior year period, was primarily due to the increase in SG&A expenses of $9.6 million, primarily driven by the cost of the restatement of prior financial statements of $7.8 million. This was partially offset by a reduction in stock-based compensation of $2.1 million and in income tax expense of $2.2 million.

| 20 |

Deferred Tax

The Company recorded a valuation allowance against all of our deferred tax assets as of both June 30, 2024 and 2023. We intend to continue maintaining a full valuation allowance on our deferred tax assets until there is sufficient evidence to support the reversal of all or some portion of these allowances. However, given our current earnings and anticipated future earnings, we believe that there is a reasonable possibility that within the next six months, sufficient positive evidence may become available to allow us to reach a conclusion that a significant portion of the valuation allowance will no longer be needed. Release of the valuation allowance would result in the recognition of certain deferred tax assets and a decrease to income tax expense for the period the release is recorded. However, the exact timing and amount of the valuation allowance release are subject to change on the basis of the level of profitability that we are able to actually achieve.

Segment Results (for the three and six months ended June 30, 2024, compared to the three and six months ended June 30, 2023)

Gaming

We generate revenue from our Gaming segment through delivery of our gaming terminals preloaded with proprietary gaming software, server-based content, as well as services such as terminal repairs, maintenance, software upgrades and upgrades on a when and if available basis and content development. We receive rental fees for machines, typically in conjunction with long-term contracts, on both a participation and fixed fee basis. Our participation contracts are typically structured to pay us a percentage of net win (defined as net revenue to our operator customers, after deducting player winnings, free bets or plays and any relevant regulatory levies) from gaming terminals placed in our customers’ facilities. Typically, we recognize revenue from these arrangements on a daily basis over the term of the contract.

Revenue growth for our Gaming business is principally driven by changes in (i) the number of operator customers we have, (ii) the number of Gaming machines in operation, (iii) the net win performance of the machines and (iv) the net win percentage that we receive pursuant to our contracts with our customers.

Gaming, Key Performance Indicators

For the Three-Month Period ended | Variance | For the Six-Month Period ended | Variance | |||||||||||||||||||||||||||||

| June 30, | June 30, | 2024 vs 2023 | June 30, | June 30, | 2024 vs 2023 | |||||||||||||||||||||||||||

| Gaming | 2024 | 2023 | % | 2024 | 2023 | % | ||||||||||||||||||||||||||

| End of period installed base (# of terminals) (2) | 34,906 | 34,433 | 473 | 1.4 | % | 34,906 | 34,433 | 473 | 1.4 | % | ||||||||||||||||||||||

| Total Gaming - Average installed base (# of terminals) (2) | 34,878 | 34,715 | 163 | 0.5 | % | 34,831 | 34,746 | 85 | 0.2 | % | ||||||||||||||||||||||

| Participation - Average installed base (# of terminals) (2) | 29,917 | 30,522 | (605 | ) | (2.0 | )% | 29,875 | 30,658 | (783 | ) | (2.6 | )% | ||||||||||||||||||||

| Fixed Rental - Average installed base (# of terminals) | 4,962 | 4,193 | 769 | 18.3 | % | 4,955 | 4,089 | 866 | 21.2 | % | ||||||||||||||||||||||

| Service Only - Average installed base (# of terminals) | 5,308 | 12,898 | (7,590 | ) | (58.8 | )% | 6,578 | 13,529 | (6,951 | ) | (51.4 | )% | ||||||||||||||||||||

| Customer Gross Win per unit per day (1) (2) | £ | 96.0 | £ | 94.4 | £ | 1.6 | 1.7 | % | £ | 97.4 | £ | 96.3 | £ | 1.1 | 1.1 | % | ||||||||||||||||

| Customer Net Win per unit per day (1) (2) | £ | 70.8 | £ | 69.0 | £ | 1.8 | 2.6 | % | £ | 71.5 | £ | 70.3 | £ | 1.2 | 1.7 | % | ||||||||||||||||

| Inspired Blended Participation Rate | 5.3 | % | 5.7 | % | (0.4 | )% | (7.0 | )% | 5.4 | % | 5.7 | % | (0.3 | )% | (5.3 | )% | ||||||||||||||||

| Inspired Fixed Rental Revenue per Gaming Machine per week | £ | 39.6 | £ | 48.3 | £ | (8.7 | ) | (18.0 | )% | £ | 40.5 | £ | 49.0 | £ | (8.5 | ) | (17.3 | )% | ||||||||||||||

| Inspired Service Rental Revenue per Gaming Machine per week | £ | 5.3 | £ | 5.1 | £ | 0.2 | 3.9 | % | £ | 5.2 | £ | 5.1 | £ | 0.1 | 2.0 | % | ||||||||||||||||

| Gaming Long term license amortization (£’m) | £ | 0.6 | £ | 0.8 | £ | (0.2 | ) | (25.0 | )% | £ | 1.1 | £ | 1.6 | £ | (0.5 | ) | (31.3 | )% | ||||||||||||||

| Number of Machine sales | 705 | 1,523 | (818 | ) | (53.7 | )% | 1,294 | 2,211 | (917 | ) | (41.5 | )% | ||||||||||||||||||||

| Average selling price per terminal | £ | 8,971 | £ | 5,681 | £ | 3,290 | 57.9 | % | £ | 8,083 | £ | 6,365 | £ | 1,718 | 27.0 | % | ||||||||||||||||

| (1) | Includes all server-based gaming terminals in which the Company takes a participation revenue share across all territories. |

| (2) | Includes circa 2,500 of lottery terminals where the share is on handle instead of net win. |

In the table above:

“End of Period Installed Base” is equal to the number of deployed Gaming terminals at the end of each period that have been placed on a participation or fixed rental basis. Gaming participation revenue, which comprises the majority of Gaming Service revenue, is directly related to the participation terminal installed base. This is the medium by which our customers generate revenue and distribute a revenue share to the Company. To the extent all other key performance indicators (“KPIs”) and certain other factors remain constant, the larger the installed base, the higher the Company’s revenue would be for a given period. Management gives careful consideration to this KPI in terms of driving growth across the segment. This does not include Service Only terminals.

| 21 |

Revenue is derived from the performance of the installed base as described by the Gross and Net Win KPIs.

If the End of Period Installed Base is materially different from the Average Installed Base (described below), we believe this gives an indication as to potential future performance. We believe the End of Period Installed Base is particularly useful for assessing new customers or markets, to indicate the progress being made with respect to entering new territories or jurisdictions.

“Total Gaming - Average Installed Base” is the average number of deployed Gaming terminals during the period consisting of both participation terminals and fixed rental terminals. Therefore, it is more closely aligned to revenue in the period. We believe this measure is particularly useful for assessing existing customers or markets to provide comparisons of historical size and performance. This does not include Service Only terminals.

“Participation - Average Installed Base” is the average number of deployed Gaming terminals that generated revenue on a participation basis.

“Fixed Rental - Average Installed Base” is the average number of deployed Gaming terminals that generated revenue on a fixed rental basis.

“Service Only - Average Installed Base” is the average number of terminals that generated revenue on a service only basis.

“Customer Gross Win per unit per day” is a KPI used by our management to (i) assess impact on the Company’s revenue, (ii) determine changes in the performance of the overall market and (iii) evaluate the impacts of regulatory change and our new content releases on our customers. Customer Gross Win per unit per day is the average per unit cash generated across all Gaming terminals in which the Company takes a participation revenue share across all territories in the period, defined as the difference between the amounts staked less winnings to players divided by the Average Installed Base in the period, then divided by the number of days in the period.

Gaming revenue accrued in the period is derived from Customer Gross Win accrued in the period after deducting gaming taxes (defined as a regulatory levy paid by the Customer to government bodies) and applying the Company’s contractual revenue share percentage.

Our management believes Customer Gross Win measures are meaningful because they represent a view of customer operating performance that is unaffected by our revenue share percentage and allow management to (1) readily view operating trends, (2) perform analytical comparisons and benchmarking between customers and (3) identify strategies to improve operating performance in the different markets in which we operate.

“Customer Net Win per unit per day” is Customer Gross Win per unit per day after giving effect to the deduction of gaming taxes.

“Inspired Blended Participation Rate” is the Company’s average revenue share percentage across all participation terminals where revenue is earned on a participation basis, weighted by Customer Net Win per unit per day.

“Inspired Fixed Rental Revenue per Gaming Machine per week” is the Company’s average fixed rental amount across all fixed rental terminals where revenue is generated on a fixed fee basis, per unit per week.

“Inspired Service Rental Revenue per Gaming Machine per week” is the Company’s average service rental amount across all service only rental terminals where revenue is generated on a service only fixed fee basis, per unit per week.

“Gaming Long term license amortization” is the upfront license fee per terminal which is typically spread over the life of the terminal.

| 22 |

Our overall Gaming revenue from terminals placed on a participation basis can therefore be calculated as the product of the Participation - Average Installed Base, the Customer Net Win per unit per day, the number of days in the period, and the Inspired Blended Participation Rate, which is equal to “Participation Revenue”.

“Number of Machine sales” is the number of terminals sold during the period.

“Average selling price per terminal” is the total revenue in GBP of the Gaming terminals sold divided by the “number of Machine sales”.

Gaming, Recurring Revenue

Set forth below is a breakdown of our Gaming recurring revenue. Gaming recurring revenue principally consist of Gaming participation revenue and fixed rental revenue.

For the Three-Month Period ended | Variance | For the Six-Month Period ended | Variance | |||||||||||||||||||||||||||||

| June 30, | June 30, | 2024 vs 2023 | June 30, | June 30, | 2024 vs 2023 | |||||||||||||||||||||||||||

| (In £ millions) | 2024 | 2023 | % | 2024 | 2023 | % | ||||||||||||||||||||||||||

| Gaming Recurring Revenue | ||||||||||||||||||||||||||||||||

| Total Gaming Revenue | £ | 21.3 | £ | 24.8 | £ | (3.5 | ) | (14 | )% | £ | 40.4 | £ | 47.1 | £ | (6.7 | ) | (14 | )% | ||||||||||||||

| Gaming Participation Revenue | £ | 10.2 | £ | 10.9 | (0.7 | ) | (6 | )% | £ | 20.8 | £ | 22.4 | £ | (1.6 | ) | (7 | )% | |||||||||||||||

| Gaming Other Fixed Fee Recurring Revenue | £ | 3.0 | £ | 3.4 | £ | (0.4 | ) | (12 | )% | £ | 6.3 | £ | 7.0 | £ | (0.7 | ) | (10 | )% | ||||||||||||||

| Gaming Project Recurring Revenue | £ | 0.2 | £ | 0.2 | 0 | % | £ | 0.5 | £ | 0.4 | £ | 0.1 | 25 | % | ||||||||||||||||||

| Gaming Long-term license amortization | £ | 0.6 | £ | 0.8 | £ | (0.2 | ) | (25 | )% | £ | 1.2 | £ | 1.6 | £ | (0.4 | ) | (25 | )% | ||||||||||||||

| Total Gaming Recurring Revenue * | £ | 14.0 | £ | 15.3 | £ | (1.3 | ) | (8 | )% | £ | 28.8 | £ | 31.4 | £ | (2.6 | ) | (8 | )% | ||||||||||||||

| Gaming Recurring Revenue as a % of Total Gaming Revenue † | 65 | % | 62 | % | 3 | % | 71 | % | 67 | % | 4 | % | ||||||||||||||||||||

| Total Gaming excluding Low Margin Sales | £ | 21.3 | £ | 24.8 | £ | 40.4 | £ | 47.1 | ||||||||||||||||||||||||

| Gaming Recurring Revenue as a % of Total Gaming Revenue (excluding Low Margin Sales) | 65 | % | 72 | % | 71 | % | 72 | % | ||||||||||||||||||||||||

| * | Does not reflect Low Margin-related revenue |

| † | Total Gaming Revenue for the three and six-month period ended June 30, 2024 has no Low Margin sales and for the three and six-month period ended June 30, 2023 includes £3.5 million of Low Margin sales. Excluding Low Margin sales, Gaming Recurring Revenue was 65% and 71% of Total Gaming Revenue respectively. |

In the table above:

“Gaming Participation Revenue” includes our share of revenue generated from (i) our Gaming terminals placed in gaming and lottery venues; and (ii) licensing of our game content and intellectual property to third parties.

“Gaming Other Fixed Fee Recurring Revenue” includes service revenue in which the Company earns a periodic fixed fee on a contracted basis.

“Gaming Project Recurring Revenue” relates specifically to a single customer for machine upgrades and distribution.

“Gaming Long term license amortization” – see the set forth provided above.

| 23 |

“Total Gaming Recurring Revenue” is equal to Gaming Participation Revenue plus Gaming Other Fixed Fee Recurring Revenue.

Gaming, Service Revenue by Region

Set forth below is a breakdown of our Gaming service revenue by geographic region. Gaming Service revenue consists principally of Gaming participation revenue, Gaming other fixed fee revenue, Gaming long-term license amortization and Gaming other non-recurring revenue. See “Gaming Segment Revenue” below for a discussion of gaming service revenue between the periods under review.

| For the Three-Month Period ended | For the Six-Month Period ended | |||||||||||||||||||||||||||||||||||||||

| June 30, | June 30, | Variance | June 30, | June 30, | Variance | |||||||||||||||||||||||||||||||||||

| (In millions) | 2024 | 2023 | 2024 vs 2023 | Total Functional Currency % | 2024 | 2023 | 2024 vs 2023 | Total Functional Currency % | ||||||||||||||||||||||||||||||||

| Service Revenue: | ||||||||||||||||||||||||||||||||||||||||

| UK LBO | $ | 9.1 | $ | 9.9 | (0.8 | ) | (8 | )% | (9 | )% | $ | 18.2 | $ | 19.6 | $ | (1.4 | ) | (7 | )% | (9 | )% | |||||||||||||||||||

| UK Other | 3.3 | 3.4 | (0.1 | ) | (3 | )% | (3 | )% | 6.8 | 6.8 | - | 0 | % | 1 | % | |||||||||||||||||||||||||

| Italy | 0.4 | 0.7 | (0.3 | ) | (43 | )% | (57 | )% | 0.8 | 1.5 | (0.7 | ) | (47 | )% | (60 | )% | ||||||||||||||||||||||||