UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the Securities

Exchange Act of 1934

_________________

Filed by the Registrant x

Filed by a Party other than the Registrant ¨

Check the appropriate box:

|

¨ |

|

Preliminary Proxy Statement |

|

¨ |

|

Confidential, for Use of the Commission Only |

x Definitive Proxy Statement

¨ Definitive Additional Materials

¨ Soliciting Material Pursuant to Section 240.14a-12

HARMONY MERGER CORP.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

|

¨ |

|

No fee required. |

||

|

¨ |

|

Fee computed on table below per Exchange Act Rules 14a-6(i) (1) and 0-11. |

||

|

x |

|

Fee paid previously with preliminary materials. |

||

|

¨ |

|

Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

||

|

|

|

|

|

|

|

|

|

(1) |

|

Amount Previously Paid: |

|

|

|

|

|

|

|

|

|

|

|

Form, Schedule or Registration Statement No. |

|

|

|

|

|

|

|

|

|

|

|

Filing Party: |

|

|

|

|

|

|

|

|

|

|

|

Date Filed: |

|

|

|

|

|

|

HARMONY MERGER CORP.

777 Third Avenue, 37th Floor

New York, New York 10017

NOTICE OF SPECIAL

MEETING OF

STOCKHOLDERS

TO BE HELD ON JULY 24, 2017

To the Stockholders of Harmony Merger Corp.:

NOTICE IS HEREBY GIVEN that a special meeting of stockholders of Harmony Merger Corp. (“Harmony”), a Delaware corporation, will be held at 11:00 a.m. Eastern Time, on July 24, 2017, at the offices of Graubard Miller, Harmony’s counsel, at The Chrysler Building, 405 Lexington Avenue, 11th Floor, New York, New York 10174. You are cordially invited to attend the special meeting, which will be held for the following purposes:

(1) The Merger Proposal — To consider and vote upon a proposal to adopt the Agreement and Plan of Merger, dated as of April 17, 2017 (the “Agreement”), by and among Harmony, Harmony Merger Sub, LLC, a wholly-owned subsidiary of Harmony (“Merger Sub”), NextDecade, LLC (“NextDecade”), and certain members of NextDecade and entities affiliated with such members as more fully described elsewhere in this proxy statement. Following a series of simultaneous transactions to reorganize certain of these affiliates, Merger Sub will merge with and into NextDecade (the “Merger”) with NextDecade being the surviving entity of the Merger (the “Surviving Company”) and becoming a wholly-owned subsidiary of Harmony as described in more detail in this proxy statement, and to approve the transactions contemplated by such agreement, including the issuance of the merger consideration thereunder (collectively, the “business combination”). A copy of the Agreement is attached to the accompanying proxy statement as Annex A.

(2) The Charter Amendment Proposals — To consider and vote upon separate proposals to approve amendments to the amended and restated certificate of incorporation of Harmony, effective following the business combination, to (a) change the name of Harmony from “Harmony Merger Corp.” to “NextDecade Corporation”; (b) increase the number of authorized shares of Harmony Common Stock from 27,500,000 shares to 480,000,000 shares; (c) prohibit action of stockholders by written consent; (d) provide the Blocker Managers (as defined in the Agreement) and certain of their affiliates with certain rights including Harmony’s renunciation of its interest or any expectancy Harmony may have in certain corporate opportunities; (e) designate the Court of Chancery of the State of Delaware as the sole and exclusive forum for specified legal actions; and (f) remove provisions that will no longer be applicable to Harmony after the business combination. A copy of the amended and restated certificate of incorporation of Harmony is attached to the accompanying proxy statement as Annex C.

(3) The Director Election Proposal — To elect nine directors who, upon consummation of the business combination, will be the directors of Harmony.

(4) The Adjournment Proposal — To consider and vote upon a proposal to adjourn the special meeting to a later date or dates if it is determined by the officer presiding over the special meeting that more time is necessary or appropriate to consummate the business combination (the “Adjournment Proposal” together with the Merger Proposal, the Charter Proposals, and the Director Election Proposal, the “Proposals”).

These items of business are described in the attached proxy statement, which we encourage you to read in its entirety before voting. Only holders of record of Harmony Common Stock at the close of business on June 29, 2017 are entitled to notice of the special meeting and to vote and have their votes counted at the special meeting and any adjournments or postponements of the special meeting.

Harmony’s board of directors has determined that the Proposals are fair to and in the best interests of Harmony and its stockholders and recommends that you vote or give instruction to vote “FOR” the Merger Proposal, “FOR” each of the Charter Proposals, “FOR” the election of all of the persons nominated for election as directors and “FOR” the Adjournment Proposal, if presented.

Under the Agreement, the approval of the Merger Proposal and the Charter Proposals are conditions to the consummation of the business combination. Accordingly, if any of the Merger Proposal or the Charter Proposals is not approved, the other proposals will not be presented to the stockholders for a vote unless the parties waive this condition to closing.

All Harmony stockholders are cordially invited to attend the special meeting in person. To ensure your representation at the special meeting, however, you are urged to complete, sign, date and return the enclosed proxy card as soon as possible. If you are a stockholder of record of Harmony Common Stock, you may also cast your vote in person at the special meeting. If your shares are held in an account at a brokerage firm or bank, you must instruct your broker or bank on how to vote your shares or, if you wish to attend the special meeting and vote in person, obtain a proxy from your broker or bank.

A complete list of Harmony stockholders of record entitled to vote at the special meeting will be available for ten days before the special meeting at the principal executive offices of Harmony for inspection by stockholders during ordinary business hours for any purpose germane to the special meeting.

Your vote is important regardless of the number of shares you own. Whether you plan to attend the special meeting or not, please sign, date and return the enclosed proxy card as soon as possible in the envelope provided. If your shares are held in “street name” or are in a margin or similar account, you should contact your broker to ensure that votes related to the shares you beneficially own are properly counted.

Thank you for your participation. We look forward to your continued support.

By Order of the Board of Directors

/s/ Eric

S. Rosenfeld

Eric S. Rosenfeld

Chief Executive Officer

June 29, 2017

TO EXERCISE YOUR CONVERSION RIGHTS, YOU MUST AFFIRMATIVELY VOTE EITHER FOR OR AGAINST THE MERGER PROPOSAL AND DEMAND THAT HARMONY CONVERT YOUR SHARES INTO CASH NO LATER THAN THE CLOSE OF THE VOTE ON THE MERGER PROPOSAL BY TENDERING YOUR STOCK TO HARMONY’S TRANSFER AGENT PRIOR TO THE VOTE AT THE MEETING. YOU MAY TENDER YOUR STOCK BY EITHER DELIVERING YOUR STOCK CERTIFICATE TO THE TRANSFER AGENT OR BY DELIVERING YOUR SHARES ELECTRONICALLY USING CONTINENTAL STOCK TRANSFER & TRUST COMPANY’S DWAC (DEPOSIT WITHDRAWAL AT CUSTODIAN) SYSTEM. IF THE BUSINESS COMBINATION IS NOT COMPLETED, THEN THESE SHARES WILL NOT BE CONVERTED INTO CASH. IF YOU HOLD THE SHARES IN STREET NAME, YOU WILL NEED TO INSTRUCT THE ACCOUNT EXECUTIVE AT YOUR BANK OR BROKER TO WITHDRAW THE SHARES FROM YOUR ACCOUNT IN ORDER TO EXERCISE YOUR CONVERSION RIGHTS. SEE “SPECIAL MEETING OF HARMONY STOCKHOLDERS — CONVERSION RIGHTS” FOR MORE SPECIFIC INSTRUCTIONS.

This proxy statement is dated June 29, 2017 and is first being mailed to Harmony Merger Corp. stockholders on or about such date.

TABLE OF CONTENTS

|

SUMMARY OF THE MATERIAL TERMS OF THE TRANSACTIONS |

|

1 |

|

QUESTIONS AND ANSWERS ABOUT THE PROPOSALS |

|

4 |

|

SUMMARY OF THE PROXY STATEMENT |

|

10 |

|

SELECTED HISTORICAL FINANCIAL INFORMATION |

|

22 |

|

SELECTED HISTORICAL FINANCIAL INFORMATION — NEXTDECADE |

|

23 |

|

SELECTED UNAUDITED PRO FORMA CONDENSED CONSOLIDATED COMBINED FINANCIAL INFORMATION |

|

24 |

|

CAPITALIZATION |

|

29 |

|

RISK FACTORS |

|

30 |

|

FORWARD-LOOKING STATEMENTS |

|

48 |

|

SPECIAL MEETING OF HARMONY STOCKHOLDERS |

|

50 |

|

THE MERGER PROPOSAL |

|

55 |

|

THE AGREEMENT |

|

78 |

|

UNAUDITED PRO FORMA CONDENSED CONSOLIDATED COMBINED FINANCIAL STATEMENTS |

|

85 |

|

THE CHARTER PROPOSALS |

|

93 |

|

THE DIRECTOR ELECTION PROPOSAL |

|

95 |

|

EXECUTIVE COMPENSATION |

|

103 |

|

THE ADJOURNMENT PROPOSAL |

|

109 |

|

OTHER INFORMATION RELATED TO HARMONY |

|

110 |

|

BUSINESS OF NEXTDECADE |

|

117 |

|

NEXTDECADE’S MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

|

123 |

|

SOURCES AND USES OF FUNDS FOR THE BUSINESS COMBINATION |

|

131 |

|

TOTAL COMPANY SHARES TO BE ISSUED IN THE BUSINESS COMBINATION |

|

132 |

|

BENEFICIAL OWNERSHIP OF SECURITIES |

|

134 |

|

CERTAIN RELATIONSHIPS AND RELATED PERSON TRANSACTIONS |

|

137 |

|

PRICE RANGE OF HARMONY SECURITIES AND DIVIDENDS |

|

141 |

|

APPRAISAL RIGHTS |

|

141 |

|

STOCKHOLDER PROPOSALS |

|

142 |

|

OTHER STOCKHOLDER COMMUNICATIONS |

|

142 |

|

INDEPENDENT AUDITORS |

|

142 |

|

DELIVERY OF DOCUMENTS TO STOCKHOLDERS |

|

142 |

|

WHERE YOU CAN FIND MORE INFORMATION |

|

142 |

|

INDEX TO FINANCIAL STATEMENTS |

|

F-1 |

|

ANNEX A |

|

A-1 |

|

ANNEX B |

|

B-1 |

|

ANNEX C |

|

C-1 |

|

ANNEX D |

|

D-1 |

i

SUMMARY OF THE MATERIAL TERMS OF THE TRANSACTIONS

This summary, together with the sections entitled “Questions and Answers About the Proposals” and “Summary of the Proxy Statement,” summarizes certain information contained in this proxy statement, but does not contain all of the information that is important to you. You should read carefully this entire proxy statement, including the attached annexes, for a more complete understanding of the matters to be considered at the special meeting of Harmony stockholders.

• Harmony Merger Corp., a Delaware corporation (“Harmony,” “we,” “our” or “us”), is a blank check company formed for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses.

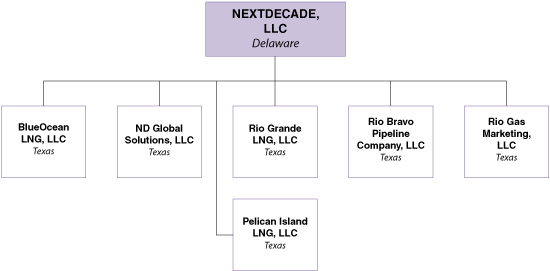

• NextDecade, LLC (“NextDecade”) is a liquefied natural gas (“LNG”) development company focused on LNG export projects and associated pipelines in the State of Texas. NextDecade’s first proposed LNG export facility, the Rio Grande LNG project located in Brownsville, Texas, along with the associated Rio Bravo pipeline originating in the Agua Dulce market area, is well-positioned among the second wave of U.S. LNG projects. For more detailed information regarding NextDecade’s business and the LNG Industry, please read the sections entitled “Business of NextDecade” and “Business of NextDecade —Global LNG Overview” included elsewhere in this proxy statement.

• Pursuant to the terms and subject to the conditions set forth in the Agreement, entities affiliated with certain of the members of NextDecade (the “Blocker Companies”) will merge with and into Harmony (each a “Blocker Merger” and, together, the “Blocker Mergers”), with Harmony being the surviving entity of the Blocker Mergers and, immediately thereafter Merger Sub will merge with and into NextDecade (the “Merger”) with NextDecade being the surviving entity of the Merger and becoming a wholly-owned subsidiary of Harmony. Please read the section entitled “The Merger Proposal — Structure of the Transaction.”

• As a result of the Blocker Mergers and the Merger, among other things, all outstanding limited liability company interests or limited partnership interests, as applicable, in each of the Blocker Companies, other than as provided for in the Agreement, (each such interest in a Blocker Company a “Blocker Membership Interest” and, collectively, the “Blocker Membership Interests”) and all existing membership interests of NextDecade (the “NextDecade Membership Interests”) will be canceled in exchange for the right to receive an aggregate of 97,866,510 shares of Harmony Common Stock plus the right to receive an additional 4,893,326 shares (up to 19,573,304 shares in the aggregate) of Harmony Common Stock upon the achievement by NextDecade of each of four milestones described herein and in the Agreement, subject to adjustment if additional equity investments are made in NextDecade prior to closing. Please read the section entitled “The Merger Proposal — Structure of the Transaction.”

• To provide a fund for payment to Harmony with respect to their post-closing rights to indemnification under the Agreement for breaches of representations and warranties and covenants by NextDecade (and in certain cases, the Blocker Companies), there will be placed in escrow (with Continental Stock Transfer & Trust Company as escrow agent) an aggregate of 3% of the shares of Harmony Common Stock issuable to the Members and the Blocker Owners (each as defined in the Agreement) at the closing of the business combination. Claims for indemnification will be reimbursable to the full extent of the damages in excess of a $5,000,000 deductible (but in no event in excess of the shares of Harmony Common Stock held in escrow). The shares of Harmony Common Stock in escrow shall be released to the Members and the Blocker Owners, subject to reduction for shares cancelled for claims ultimately resolved and those still pending resolution at the time of the release, on the first anniversary of the closing of the business combination. In addition, to the extent such indemnification is insufficient, the Blocker Owners of the Blocker Companies merged into Harmony have agreed to indemnify Harmony for damages arising out of or resulting from the breach of representations, warranties or covenants with respect to, or from pre-closing activities of, each Blocker Company of which it is a Blocker Owner in an amount not to exceed the value of the shares of Harmony Common Stock received by such Blocker Owner as merger consideration. Please read the section entitled “The Merger Proposal — Indemnification.”

• In connection with the signing of the Agreement, certain of the stockholders of Harmony prior to its initial public offering (“initial stockholders”) and certain Members entered into voting and support

1

agreements, respectively, whereby such initial stockholders agreed, among other matters, to vote in favor of the Agreement and the Merger Proposal, such Members agreed not to withdraw their approval for the Agreement and the Merger Proposal, and each of them agreed not to take any action to solicit, encourage, initiate, engage in or otherwise facilitate discussions or negotiations with, provide any information to, or enter into any agreement with any person (other than the parties to the Agreement) concerning any merger, sale of substantial assets or similar transaction involving Harmony or NextDecade prior to the closing of the business combination.

• The Agreement provides that both Harmony’s and NextDecade’s obligations to consummate the business combination are conditioned upon, among other things:

• the Merger Proposal and the Charter Proposals having been duly approved and adopted by the Harmony stockholders by the requisite vote under the laws of Delaware and Harmony’s amended and restated certificate of incorporation;

• Harmony having net tangible assets of at least $5,000,001 after taking into account holders of public shares that have exercised their right to convert their public shares into cash;

• all specified waiting periods under the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended (the “HSR Act”) having expired or been terminated and no governmental entity having enacted, issued, promulgated, enforced or entered any statute, rule, regulation, executive order, decree, injunction or other order which is in effect and which has the effect of making the Merger illegal or otherwise restraining, enjoining or prohibiting consummation of the Merger; and

• shares of Harmony Common Stock having been approved for listing upon the closing of the business combination on Nasdaq subject to the requirement to have a sufficient number of round lot holders.

The Agreement also provides for additional conditions specific to each of Harmony’s and NextDecade’s obligations to consummate the business combination. For more detailed information regarding the conditions to closing, please read the section entitled “The Agreement — Conditions to Closing of the Business Combination.”

• In addition to voting on the business combination, the stockholders of Harmony will vote on the following separate proposals to approve amendments to the amended and restated certificate of incorporation of Harmony, effective following the business combination, to (a) change the name of Harmony from “Harmony Merger Corp.” to “NextDecade Corporation”; (b) increase the number of authorized shares of Harmony Common Stock from 27,500,000 shares to 480,000,000 shares; (c) prohibit action of stockholders by written consent; (d) provide the Blocker Managers and certain of their affiliates with certain rights including Harmony’s renunciation of its interest or any expectancy Harmony may have in certain corporate opportunities; (e) designate the Court of Chancery of the State of Delaware as the sole and exclusive forum for specified legal actions; and (f) remove provisions that will no longer be applicable to Harmony after the business combination. The stockholders of Harmony will also vote on proposals to elect nine directors who, upon consummation of the business combination, will be the directors of Harmony and to approve, if necessary, an adjournment of the special meeting. Please read the sections entitled “The Charter Proposals,” “The Director Election Proposal,” and “The Adjournment Proposal.”

• The Agreement provides that either Harmony or NextDecade may terminate the Agreement in certain circumstances if the business combination is not consummated by July 27, 2017 or, with the prior consent of NextDecade, such later date as may be approved by the stockholders of Harmony. Additionally, the business combination shall not be consummated if Harmony’s public stockholders do not approve the business combination or if Harmony has less than $5,000,001 of net tangible assets following the exercise by the holders of Harmony Common Stock sold in its initial public offering (“public shares”) who validly exercise their conversion rights. Additionally, the Agreement may be terminated, among other reasons, by either Harmony or NextDecade upon material breach of the other party. NextDecade may also terminate the Agreement if less than $25,000,000 remains in the trust account established in connection with Harmony’s initial public offering following the exercise by the holders of public shares of their right to convert their public shares held by them into a pro rata share of

2

the trust account in accordance with Harmony’s charter documents. Please read the section entitled “The Agreement — Termination.”

• If elected by stockholders, after the consummation of the business combination, the following nine individuals will serve on the board of Harmony: Kathleen Eisbrenner, René van Vliet, Matthew Bonanno, David Magid, William Vrattos, Brian Belke, Avinash Kripalani, Eric S. Rosenfeld and David D. Sgro, Harmony’s Chief Executive Officer and Chief Operating Officer, respectively. Please read the section entitled “The Director Election Proposal.”

• Upon completion of the business combination, the executive officers of Harmony will be Kathleen Eisbrenner, Chief Executive Officer, René van Vliet, Chief Operating Officer, Ben Atkins, Chief Financial Officer, Alfonso Puga, Chief Commercial Officer, Shaun Davison, SVP Development and Regulatory Affairs, and Krysta De Lima, General Counsel. Please read the section entitled “The Director Election Proposal.”

• The Members and the Blocker Owners have agreed that they will not, subject to certain exceptions, transfer, sell, tender or otherwise dispose of the shares of Harmony Common Stock they will receive as a result of the business combination for a one hundred and eighty day period from the closing of the business combination. The Members and Blocker Owners will enter into lock-up agreements prior to the closing to evidence such restrictions. Please read the section entitled “The Merger Proposal — Sale Restriction.”

• On or prior to the closing of the business combination, the Members, the Blocker Owners and the initial stockholders will enter into a Registration Rights Agreement with Harmony providing such holders with certain demand and piggy-back registration rights with respect to registration statements filed by Harmony after the closing of the business combination. In connection with the execution of the Registration Rights Agreement, the prior registration rights agreement entered into between the initial stockholders and Harmony in connection with Harmony’s initial public offering relating to registration rights previously granted to such initial stockholders will be terminated. Please read the section entitled “Certain Relationships and Related Person Transactions — Harmony Related Person Transactions — Registration Rights.”

3

QUESTIONS AND ANSWERS ABOUT THE PROPOSALS

The following questions and answers briefly address some commonly asked questions about the proposals to be presented at the special meeting of stockholders of Harmony, including the proposed business combination. The following questions and answers do not include all the information that is important to Harmony stockholders. We urge Harmony stockholders to read carefully this entire proxy statement, including the annexes and other documents referred to herein.

|

Q. |

|

Why am I receiving this proxy statement? |

|

A. |

|

The parties have agreed to a business combination under the terms of the Agreement and Plan of Merger, dated as of April 17, 2017, that is described in this proxy statement. This agreement is referred to as the “Agreement.” A copy of the Agreement is attached to this proxy statement as Annex A, and Harmony encourages its stockholders to read it in its entirety. Harmony’s stockholders are being asked to consider and vote upon a proposal to adopt the Agreement, which, among other things, provides for the Blocker Mergers with Harmony being the surviving entity of the Blocker Mergers and, immediately thereafter, the Merger with NextDecade being the surviving entity of the Merger and becoming a wholly-owned subsidiary of Harmony. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

In addition to voting on the transactions contemplated by the Agreement, the stockholders of Harmony will vote on separate proposals to approve amendments to the amended and restated certificate of incorporation of Harmony, effective following the business combination, to (a) change the name of Harmony from “Harmony Merger Corp.” to “NextDecade Corporation”; (b) increase the number of authorized shares of Harmony Common Stock from 27,500,000 shares to 480,000,000 shares; (c) prohibit action of stockholders by written consent; (d) provide the Blocker Managers and certain of their affiliates with certain rights including Harmony’s renunciation of its interest or any expectancy Harmony may have in certain corporate opportunities; (e) designate the Court of Chancery of the State of Delaware as the sole and exclusive forum for specified legal actions; and (f) remove provisions that will no longer be applicable to Harmony after the business combination. The stockholders of Harmony will also vote on proposals to elect nine directors who, upon consummation of the business combination, will be the directors of Harmony and to approve, if necessary, an adjournment of the special meeting. Please read the sections entitled “The Charter Proposals,” “The Director Election Proposal,” and “The Adjournment Proposal.” |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Under the Agreement, the approval of the Merger Proposal and the Charter Proposals are conditions to the consummation of the business combination. Accordingly, if any of the Merger Proposal or Charter Proposals is not approved, the Director Election Proposal will not be presented to the stockholders for a vote. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Harmony will hold the special meeting of its stockholders to consider and vote upon these proposals. This proxy statement contains important information about the proposed transactions and the other matters to be acted upon at the special meeting. Stockholders should read it carefully. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The vote of stockholders is important. Stockholders are encouraged to vote as soon as possible after carefully reviewing this proxy statement. |

4

|

Q. |

|

Why is Harmony proposing the business combination? |

|

A. |

|

Harmony was organized to effect a merger, capital stock exchange, asset acquisition or other similar business combination with one or more businesses or entities. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Harmony completed its initial public offering of units, with each unit consisting of one share of its common stock and one redeemable warrant to purchase one share of common stock, on March 27, 2015, raising total gross proceeds of $115,000,000. Since the initial public offering, Harmony’s activity has been limited to the evaluation of business combination candidates. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NextDecade is a liquefied natural gas (“LNG”) development company focused on LNG export projects and associated pipelines in the State of Texas. NextDecade’s first proposed LNG export facility, the Rio Grande LNG project located in Brownsville, Texas, along with the associated Rio Bravo pipeline originating in the Agua Dulce market area, is well-positioned among the second wave of U.S. LNG projects. Based on its due diligence investigations of NextDecade and the industry in which it operates, including the financial and other information provided by NextDecade in the course of their negotiations, Harmony believes that a business combination with NextDecade will provide Harmony stockholders with an opportunity to participate in a company with significant growth potential. However, there is no assurance of this. Please read the section entitled “The Merger Proposal — Harmony’s Board of Directors’ and Special Advisor’s Reasons for Approval of the Transactions.” |

|

|

|

|

|

|

|

|

|

Q. |

|

Do I have conversion rights? |

|

A. |

|

If you are a holder of Harmony public shares as of the record date, you have the right to demand that Harmony convert such shares into cash provided that you vote either for or against the Merger Proposal. We sometimes refer to these rights to demand conversion of the public shares into a pro rata portion of the cash held in Harmony’s trust account as “conversion rights.” |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Notwithstanding the foregoing, a holder of public shares, together with any affiliate of his or any other person with whom he is acting in concert or as a “group” (as defined in Section 13(d)(3) of the Exchange Act) will be restricted from seeking conversion rights with respect to 20% or more of the public shares. Accordingly, all public shares in excess of 20% held by a public stockholder will not be converted to cash. Under Harmony’s amended and restated certificate of incorporation, the business combination may only be consummated if Harmony has net tangible assets of at least $5,000,001 following payment to all holders of public shares who properly demand conversion of their shares into cash. |

|

|

|

|

|

|

|

|

5

|

Q. |

|

How do I exercise my conversion rights? |

|

A. |

|

If you are a holder of public shares and wish to exercise your conversion rights, you must (i) affirmatively vote either for or against the Merger Proposal and (ii) demand that Harmony convert your shares into cash no later than the close of the vote on the Merger Proposal by delivering your stock to Harmony’s transfer agent physically or electronically using the DWAC (Deposit Withdrawal at Custodian) System prior to the vote at the meeting. Any holder of public shares voting for or against the Merger Proposal will be entitled to demand that his shares be converted for a full pro rata portion of the amount then in the trust account (which is anticipated to be approximately $113,866,204, or approximately $10.35 per share, as of two business days prior to the date of the special meeting). Such amount, less any owed but unpaid taxes on the funds in the trust account, will be paid promptly upon consummation of the business combination. There are currently no owed but unpaid income taxes on the funds in the trust account. However, under Delaware law, the proceeds held in the trust account could be subject to claims which could take priority over those of Harmony’s public stockholders exercising conversion rights, regardless of whether such holders vote for or against the Merger Proposal. Therefore, the per-share distribution from the trust account in such a situation may be less than originally anticipated due to such claims. Your vote on any proposal other than the Merger Proposal will have no impact on the amount you will receive upon exercise of your conversion rights. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If you are a holder of public shares, you may demand conversion rights either by checking the box on the proxy card or by submitting your request in writing to Harmony’s secretary, at the address listed at the end of this section and delivering your shares as indicated above. If you (i) initially do not vote with respect to the Merger Proposal but then wish to vote for or against it, or (ii) wish to exercise your conversion rights but initially do not check the box on the proxy card providing for the exercise of your conversion rights and do not send a written request to Harmony to exercise your conversion rights, you may request Harmony to send you another proxy card on which you may indicate your intended vote or your intention to exercise your conversion rights. You may make such request by contacting Harmony at the phone number or address listed at the end of this section. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Any request for conversion, once made by a holder of public shares, may be withdrawn at any time up to the time the vote is taken with respect to the Merger Proposal at the special meeting. If you deliver your shares for conversion to Harmony’s transfer agent and later decide prior to the special meeting not to elect conversion, you may request that Harmony’s transfer agent return the shares (physically or electronically). You may make such request by contacting Harmony’s transfer agent at the phone number or address listed at the end of this section. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Any corrected or changed proxy card or written demand of conversion rights must be received by Harmony’s secretary prior to the vote taken on the Merger Proposal at the special meeting. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If a holder of public shares votes for or against the Merger Proposal and demand is properly made as described above, then, if the business combination is consummated, Harmony will convert these shares into a pro rata portion of funds deposited in the trust account. If you exercise your conversion rights, then you will be exchanging your shares of Harmony Common Stock for cash and will no longer be a stockholder of Harmony upon consummation of the business combination. |

6

|

|

|

|

|

|

|

If you are a holder of public shares and you exercise your conversion rights, it will not result in the loss of any of your warrants of Harmony that you may hold. |

|

|

|

|

|

|

|

|

|

Q. |

|

Do I have appraisal rights if I object to the proposed business combination? |

|

A. |

|

No. Neither Harmony stockholders nor warrant holders have appraisal rights in connection with the business combination under the General Corporation Law of the State of Delaware (“DGCL”). |

|

|

|

|

|

|

|

|

|

Q. |

|

What happens to the funds deposited in the trust account after consummation of the business combination? |

|

A. |

|

Harmony shall cause the trust account to be disbursed upon the consummation of the business combination. All liabilities and obligations of Harmony due and owing or incurred shall be paid as and when due, including all amounts payable (i) to holders of public shares who elect to have their public shares converted to cash in accordance with the provisions of Harmony’s charter documents, (ii) for income tax or other tax obligations of Harmony prior to the closing, (iii) as repayment of loans and reimbursement of expenses to directors, officers and initial stockholders of Harmony and (iv) to third parties who have rendered services to Harmony in connection with its operations and efforts to effect a business combination. |

|

|

|

|

|

|

|

|

|

Q. |

|

What happens if a substantial number of public stockholders vote in favor of the Merger Proposal and exercise their conversion rights? |

|

A. |

|

Pursuant to Harmony’s amended and restated certificate of incorporation, all holders of public shares may vote in favor of the business combination and still exercise their conversion rights; provided that Harmony may not consummate the business combination if it has less than $5,000,001 of net tangible assets following consummation of the business combination. Accordingly, the business combination may be consummated even though the funds available from the trust account and the number of public stockholders are substantially reduced as a result of conversions of public shares. With fewer public shares and public stockholders, the trading market for Harmony’s shares following consummation of the business combination may be less liquid than the market for Harmony’s shares of common stock was prior to the business combination and Harmony may not be able to meet the listing standards for Nasdaq or another national securities exchange. Notwithstanding the foregoing, NextDecade is entitled to terminate the Agreement if less than $25,000,000 remains in the trust account following the exercise by the holders of public shares of their right to convert their public shares in accordance with Harmony’s charter documents. |

|

|

|

|

|

|

|

|

|

Q. |

|

What happens if the business combination is not consummated? |

|

A. |

|

If the business combination is not consummated by July 27, 2017 or, with NextDecade’s consent, such later date as approved by the stockholders of Harmony, either party may terminate the Agreement. If Harmony is unable to consummate a business combination within the permitted time period, Harmony must redeem 100% of the outstanding public shares, at a per-share price, payable in cash, equal to an amount then held in the trust account less taxes payable. |

|

|

|

|

|

|

|

|

|

Q. |

|

When do you expect the business combination to be completed? |

|

A. |

|

It is currently anticipated that the business combination will be consummated promptly following the Harmony special meeting which is set for July 24, 2017; however, such meeting could be adjourned, as described above. For a description of the conditions for the completion of the business combination, please read the section entitled “The Agreement — Conditions to Closing of the Business Combination.” |

|

|

|

|

|

|

|

|

|

Q. |

|

What do I need to do now? |

|

A. |

|

Harmony urges you to read carefully and consider the information contained in this proxy statement, including the annexes, and to consider how the business combination will affect you as a stockholder and/or warrant holder of Harmony. Stockholders should then vote as soon as possible in accordance with the instructions provided in this proxy statement and on the enclosed proxy card. |

7

|

Q. |

|

How do I vote? |

|

A. |

|

If you are a holder of record of Harmony Common Stock on the record date, you may vote in person at the special meeting or by submitting a proxy for the special meeting. You may submit your proxy by completing, signing, dating and returning the enclosed proxy card in the accompanying pre-addressed postage paid envelope. If you hold your shares in “street name,” which means your shares are held of record by a broker, bank or nominee, you should contact your broker to ensure that votes related to the shares you beneficially own are properly counted. In this regard, you must provide the broker, bank or nominee with instructions on how to vote your shares or, if you wish to attend the meeting and vote in person, obtain a proxy from your broker, bank or nominee. |

|

|

|

|

|

|

|

|

|

Q. |

|

What vote is required to approve the proposals being presented at the |

|

A. |

|

The approval of the Merger Proposal will require the affirmative vote of the holders of a majority of the outstanding shares of Harmony Common Stock on the record date. |

|

|

|

special meeting? |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The election of directors requires a plurality vote of the shares of common stock present in person or represented by proxy and entitled to vote at the special meeting. “Plurality” means that the individuals who receive the largest number of votes cast “FOR” are elected as directors. Consequently, any shares not voted “FOR” a particular nominee (whether as a result of an abstention, a direction to withhold authority or a broker non-vote) will not be counted in the nominee’s favor. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The approval of the Adjournment Proposal will require the affirmative vote of the holders of a majority of the then outstanding shares of common stock present and entitled to vote at the meeting. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Abstentions and broker non-votes will have the same effect as a vote “against” the Merger Proposal and the Charter Proposals. With respect to the Adjournment Proposal, if presented, abstentions will have the same effect as a vote “against” such proposal while broker non-votes will have no effect on such proposal. With respect to the Director Election Proposal, abstentions and broker non-votes will have no effect on such proposal. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For more information, please read the sections titled “Special Meeting of Harmony Stockholders — Abstentions and Broker Non-Votes” and “— Vote Required.” |

|

|

|

|

|

|

|

|

|

Q. |

|

If my shares are held in “street name,” will my broker, bank or nominee automatically vote my shares for me? |

|

A. |

|

No. Your broker, bank or nominee cannot vote your shares unless you provide instructions on how to vote in accordance with the information and procedures provided to you by your broker, bank or nominee. |

|

|

|

|

|

|

|

|

|

Q. |

|

May I change my vote after I have mailed my signed proxy card? |

|

A. |

|

Yes. Stockholders may send a later-dated, signed proxy card so that it is received by Harmony’s transfer agent prior to the vote at the special meeting or attend the special meeting in person and vote. Stockholders also may revoke their proxy by sending a notice of revocation to Harmony’s transfer agent, which must be received prior to the vote at the special meeting. |

8

|

Q. |

|

What happens if I fail to take any action with respect to the meeting? |

|

A. |

|

If you fail to take any action with respect to the meeting and the business combination is approved by stockholders and consummated, you will continue to be a stockholder and/or warrant holder of Harmony. As a corollary, failure to vote either for or against the Merger Proposal means you will not have any right in connection with the business combination to exchange your shares for a pro rata share of the funds held in Harmony’s trust account. If you fail to take any action with respect to the meeting and the business combination is not approved, you will continue to be a stockholder and/or warrant holder of Harmony. |

|

|

|

|

|

|

|

|

|

Q. |

|

What should I do with my stock and/or warrant certificates? |

|

A. |

|

Harmony warrant holders and those stockholders who do not elect to have their Harmony shares converted into the pro rata share of the trust account need not submit their certificates. Harmony stockholders who exercise their conversion rights must deliver their stock certificates to Harmony’s transfer agent (either physically or electronically) prior to the vote at the meeting in order to properly demand such conversion rights. |

|

|

|

|

|

|

|

|

|

Q. |

|

What should I do if I receive more than one set of voting materials? |

|

A. |

|

Stockholders may receive more than one set of voting materials, including multiple copies of this proxy statement and multiple proxy cards or voting instruction cards. For example, if you hold your shares in more than one brokerage account, you will receive a separate voting instruction card for each brokerage account in which you hold shares. If you are a holder of record and your shares are registered in more than one name, you will receive more than one proxy card. Please complete, sign, date and return each proxy card and voting instruction card that you receive in order to cast a vote with respect to all of your Harmony shares. |

|

|

|

|

|

|

|

|

|

Q. |

|

Who can help answer my questions? |

|

A. |

|

If you have questions about the business combination or if you need additional copies of the proxy statement or the enclosed proxy card you should contact: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mr. David D. Sgro |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Or |

|

|

|

|

|

|

|

MacKenzie Partners Inc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

You may also obtain additional information about Harmony from documents filed with the Securities and Exchange Commission (“SEC”) by following the instructions in the section entitled “Where You Can Find More Information.” If you are a holder of public shares and you intend to seek conversion of your shares, you will need to demand conversion of your shares by delivering your stock (either physically or electronically) to Harmony’s transfer agent at the address below prior to the vote at the special meeting. If you have questions regarding the certification of your position or delivery of your stock, please contact: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mr. Mark Zimkind |

9

SUMMARY OF THE PROXY STATEMENT

This summary highlights selected information from this proxy statement and does not contain all of the information that is important to you. To better understand the proposals to be submitted for a vote at the special meeting, including the business combination, you should read this entire document carefully, including the Agreement attached as Annex A to this proxy statement. The Agreement is the legal document that governs the business combination and the transactions that will be undertaken in connection with the business combination. It is also described in detail in this proxy statement in the section entitled “The Agreement.”

Parties to the Business Combination

Harmony Merger Corp.

Harmony Merger Corp. is a blank check company formed in order to effect a merger, capital stock exchange, asset acquisition or other similar business combination with one or more businesses or entities. Harmony was incorporated under the laws of Delaware on May 21, 2014.

The mailing address of Harmony’s principal executive office is 777 Third Avenue, 37th Floor, New York, New York 10017 and its telephone number at that address is (212) 319-7676. After the consummation of the transactions, Harmony’s principal executive office will be those of NextDecade located at 3 Waterway Square Place, The Woodlands, Texas 77380.

NextDecade, LLC

NextDecade, LLC is a LNG development company focused on LNG export projects and associated pipelines in the State of Texas. NextDecade’s first proposed LNG export facility, the Rio Grande LNG project located in Brownsville, Texas, along with the associated Rio Bravo pipeline originating in the Agua Dulce market area, is well-positioned among the second wave of U.S. LNG projects. NextDecade was formed under the laws of Delaware as a limited liability company on June 4, 2010.

The mailing address of NextDecade’s principal executive office is 3 Waterway Square Place, The Woodlands, Texas 77380.

The Business Combination

Pursuant to the terms and subject to the conditions of the Agreement, among other things, each of the Blocker Companies will merge with and into Harmony, with Harmony being the surviving entity of the Blocker Mergers, and immediately thereafter Merger Sub will merge with and into NextDecade with NextDecade being the surviving entity of the Merger and becoming a wholly-owned subsidiary of Harmony.

The Closing Consideration

Upon the consummation of the business combination, all of NextDecade’s outstanding membership interests will convert automatically into the right to receive an aggregate of 97,866,510 shares of Harmony Common Stock (subject to an increase in connection with certain potential pre-closing investments by investors as described in the Agreement). Additionally, all issued NextDecade Membership Interests under NextDecade’s Management Incentive Plan (“MIP”) that have not vested immediately prior to the closing of the business combination will convert automatically into the right to receive (A) at closing, an economically-equivalent number of shares of Harmony Common Stock and (B) following the closing and continuing for so long as any such shares remain subject to the transfer and forfeiture restrictions, in the event that any additional shares of Harmony Common Stock are issued, an additional number of shares of Harmony Common Stock (the “Restricted Shares”), in each case that are subject to transfer and forfeiture restrictions that are substantially similar to the transfer and forfeiture restrictions as were applicable to the unvested NextDecade Membership Interests.

10

The Contingent Consideration

In addition to the consideration described above, the holders of NextDecade Membership Interests and the owners of the Blocker Membership Interests shall, collectively, be entitled to receive four separate tranches of 4,893,326 shares of Harmony Common Stock each (up to 19,573,304 shares in the aggregate) upon the achievement of each of the following milestones:

Milestone 1 — NextDecade or one or more of its subsidiaries receiving a Final Environment Impact Statement issued by the Federal Energy Regulatory Commission by June 30, 2018.

Milestone 2 — The execution by NextDecade or one or more of its subsidiaries of a binding sale and purchase or tolling agreement (with customary conditions precedent) for the sale and purchase of, or the provision of tolling services with respect to, at least 1 million tons of LNG per annum by June 30, 2018.

Milestone 3 — The execution by NextDecade or one or more of its subsidiaries of an engineering procurement and construction contract (with customary conditions precedent) for the construction of the Rio Grande LNG export terminal by December 31, 2018.

Milestone 4 — An affirmative vote of the board of directors of Harmony to make a final investment decision for the Rio Grande LNG or Rio Bravo Pipeline projects by June 30, 2019.

Potential Carve-Out Investors in NextDecade

Prior to entering into negotiations with Harmony regarding the Merger, NextDecade was engaged in the process of identifying and securing additional development capital from strategic investors and financial investors. Strategic investors include LNG buyers seeking to secure offtake capacity at one or more of NextDecade’s proposed liquefaction facilities, or vendors involved in the construction of such facilities, or other third parties that NextDecade believes would add strategic value to its development projects. Financial investors include energy infrastructure funds, institutional investors, and others seeking to invest in developing LNG facilities.

Pursuant to the Merger Agreement, NextDecade and Harmony have agreed that, after April 17, 2017 (the date of the Merger Agreement) and prior to the closing, the following categories of investors may make an investment in NextDecade or its subsidiaries:

• one or more “strategic” investors in an aggregate amount of up to $75,000,000 in equity capital,

• one or more “financial” investors in an aggregate amount of up to $25,000,000 in equity capital; provided that any such financial investor agrees to purchase an equal dollar amount of Harmony Common Stock in the open market prior to the Closing at a price up to the per-share amount in Harmony’s trust account, and

• one or more members of the management of NextDecade or management of existing Members in an aggregate amount of up to $2,500,000,

in each case, at an implied pre-money valuation of NextDecade of no less than $800,000,000.

The potential strategic investors, financial investors, and management investors in NextDecade prior to the closing are referred to in the Merger Agreement and this proxy statement as “Carve-Out Investors.”

The number of “Additional Shares” issued by Harmony to Carve-Out Investors at the closing shall be calculated using the following formula: (i) the aggregate Carve-Out Investor Investment Amount made by all Carve-Out Investors, divided by (ii) the weighted average Implied Price Per Share of NextDecade for all such Carve-Out Investor Investment Amounts.

The “Carve-Out Investor Investment Amount” means the aggregate U.S. dollar value of any investment in NextDecade made by all Carve-Out Investors.

The “Implied Price Per Share” means the U.S. dollar amount calculated using the following formula: (i) $10.218, multiplied by (ii) the quotient of (A) the implied pre-money valuation of NextDecade in connection with such Carve-Out Investor’s investment in NextDecade and (B) $1,000,000,000.

11

Illustrative Calculation of Potential Additional Shares

For purposes of clarity only, an illustrative example follows:

Assuming (A) a “strategic” Carve-Out Investor invested $75,000,000 at an implied pre-money valuation of NextDecade of $900,000,000, and (B) a “financial” Carve-Out Investor invested $25,000,000 at an implied pre-money valuation of NextDecade of $800,000,000, then the Additional Shares would be calculated as:

1. 100,000,000, divided by (B) ((0.75 multiplied by ($10.218 multiplied by ($900,000,000 divided by $1,000,000,000))) plus (0.25 multiplied by ($10.218 multiplied by ($800,000,000 divided by $1,000,000,000)));

2. Which is equal to (A) $100,000,000, divided by (B) ((0.75 multiplied by ($10.218 multiplied by 0.9)) plus (0.25 multiplied by ($10.218 multiplied by 0.8)));

3. Which is equal to (A) $100,000,000, divided by (B) ((0.75 multiplied by 9.1962) plus (0.25 multiplied by 8.1744));

4. Which is equal to (A) $100,000,000, divided by (B) (6.89715 plus 2.0436);

5. Which is equal to (A) $100,000,000, divided by (B) 8.941;

6. Which is equal to 11,184,431 shares.

NextDecade has no obligation to issue additional shares to potential Carve-Out Investors prior to the closing, and NextDecade currently has no commitments from any Carve-Out Investors to purchase additional Next Decade shares prior to the closing. The closing of the Merger is not contingent on any Carve-Out Investors investing additional development capital in NextDecade prior to the closing. The information presented in this proxy statement assumes that no Additional Shares will be issued by Harmony at the closing. If any potential Carve-Out Investors execute definitive agreements to invest in NextDecade prior to the closing, NextDecade will promptly notify Harmony, and Harmony will issue a press release and file a Current Report on Form 8-K with the SEC, and Harmony will provide this information to its stockholders as additional proxy materials.

Lock-Up Agreements

Pursuant to the terms and subject to the conditions of the Agreement and certain lock-up agreements to be entered into at the closing, the Members and the Blocker Owners will not be able to sell any of the shares of Harmony Common Stock that they receive as a result of the business combination (subject to limited exceptions) until one hundred and eighty days after the consummation of the business combination. Please read the section entitled “The Merger Proposal — Sale Restriction” for more information.

Escrow Arrangement and Indemnification

To provide a fund for payment to Harmony with respect to its post-closing rights to indemnification under the Agreement for breaches of representations and warranties and covenants by NextDecade (and in certain cases, the Blocker Companies), there will be placed in escrow an aggregate of 3% of the shares of Harmony Common Stock issuable to the Members and the Blocker Owners at closing. Claims for indemnification will be reimbursable to the full extent of the damages in excess of a $5,000,000 deductible (but in no event in excess of the shares of Harmony Common Stock held in escrow).

The shares of Harmony Common Stock in escrow shall be released to the Members and the Blocker Owners, subject to reduction based on shares cancelled for claims ultimately resolved and those still pending resolution at the time of the release, on the first anniversary of the closing of the business combination. In addition, to the extent such indemnification is insufficient, the Blocker Owners of the Blocker Companies merged into Harmony have agreed to indemnify Harmony for damages arising out of or resulting from the breach of representations, warranties or covenants with respect to, or from pre-closing activities of, each Blocker Company of which it is a Blocker Owner in an amount not to exceed the value of the shares of Harmony Common Stock received by such Blocker Owner as merger consideration. Please read the section entitled “The Merger Proposal — Indemnification.”

12

Conditions to the Closing of the Business Combination

General Conditions

Both Harmony’s and NextDecade’s obligations to consummate the business combination contemplated by the Agreement are conditioned upon, among other things:

• the Merger Proposal and the Charter Proposals having been duly approved and adopted by the Harmony stockholders by the requisite vote under the laws of Delaware and Harmony’s amended and restated certificate of incorporation;

• Harmony having net tangible assets of at least $5,000,001 after taking into account holders of public shares that have exercised their right to convert their public shares into cash;

• all specified waiting periods under the HSR Act shall have expired or been terminated and no governmental entity shall have enacted, issued, promulgated, enforced or entered any statute, rule, regulation, executive order, decree, injunction or other order which is in effect and which has the effect of making the Merger illegal or otherwise restraining, enjoining or prohibiting consummation of the Merger; and

• Harmony’s shares shall be approved for listing upon the closing of the business combination on Nasdaq subject to the requirement to have a sufficient number of round lot holders.

In addition, each of Harmony’s and NextDecade’s obligations to consummate the business combination contemplated by the Agreement are conditioned upon, among other things:

• Except to the extent it does not cause a material adverse effect, the representations and warranties of the other party and of the Blocker Entities being true and correct (without regard to any materiality or material adverse effect qualifier contained therein) as of the date of the Agreement and on and as of the closing and the other party having performed or complied with all agreements and covenants required by the Agreement to be performed or complied with on or prior to the closing, and each of Harmony and NextDecade having received a certificate with respect to the foregoing from the other party; and

• all necessary consents, waivers and approvals required to be obtained by the other party in connection with the transactions having been received, other than consents, waivers and approvals the absence of which could not reasonably be expected to have a material adverse effect.

NextDecade’s Conditions to Closing

The obligations of NextDecade to consummate and effect the Merger are also subject to the satisfaction or waiver of various conditions, including, among other things:

• there being no material adverse change affecting Harmony;

• Harmony shall have been in compliance with the reporting requirements under the United States Securities Act of 1933, as amended, and the United States Securities Exchange Act of 1934, as amended;

• certain persons shall have resigned from all of their positions and offices with Harmony and Merger Sub;

• the Registration Rights Agreement (described below) shall have been executed and delivered and shall be in full force and effect;

• Harmony shall have arranged for funds remaining in the trust account to be dispersed to NextDecade and certain other parties upon the closing of the business combination;

• no less than $25,000,000 remains in the trust account following the exercise by the holders of public shares of their right to convert their public shares held by them into a pro rata share of the trust account in accordance with Harmony’s charter documents; and

• Harmony shall have terminated certain finder fee agreements.

13

Harmony’s Conditions to Closing

The obligations of Harmony and Merger Sub to consummate the business combination and transactions contemplated by the Agreement also are conditioned upon each of the following, among other things:

• there being no material adverse change affecting NextDecade;

• the lock-up agreements shall have been executed and delivered by the parties thereto; and

• (i) all outstanding indebtedness owned by any insider of NextDecade shall have been repaid in full; (ii) all guaranteed or similar arrangements pursuant to which NextDecade has guaranteed the payment or performance of any obligations of any NextDecade insider to a third party shall have been terminated; and (iii) no NextDecade insider shall own any direct equity interests in any subsidiary of NextDecade or in any other entity that is controlled, directly or indirectly, by NextDecade that utilizes in its name “NextDecade” or any derivative thereof.

Termination of the Agreement

The Agreement may be terminated at any time, but not later than the closing, as follows:

• by mutual written agreement of Harmony and NextDecade;

• by either Harmony or NextDecade if the transactions are not consummated on or before July 27, 2017 or, with NextDecade’s prior consent, such later date as approved by Harmony’s stockholders, provided that such termination is not available to a party whose action or failure to act has been a principal cause of or resulted in the failure of the transactions to be consummated before such date and such action or failure to act is a breach of the Agreement;

• by either Harmony or NextDecade if a governmental entity shall have issued an order, decree, judgment or ruling or taken any other action, in any case having the effect of permanently restraining, enjoining or otherwise prohibiting the transactions, which order, decree, ruling or other action is final and nonappealable;

• by either Harmony or NextDecade if the other party has breached any of its covenants or representations and warranties in any material respect and has not cured its breach within thirty days of the notice of an intent to terminate, provided that the terminating party is itself not in breach;

• by either Harmony or NextDecade if, at the Special Meeting (including any adjournments thereof), the Merger Proposal and the Charter Proposals are not duly approved and adopted by the stockholders of Harmony by the requisite vote under the DGCL and the Harmony charter documents;

• by either Harmony or NextDecade if the transactions shall fail to be approved by holders of Harmony’s public shares or Harmony has less than $5,000,001 of net tangible assets after taking into account holders of public shares seeking conversion rights;

• by NextDecade if less than $25,000,000 remains in Harmony’s trust account following the exercise by the holders of public shares of their right to convert their public shares into a pro rata share of the trust account in accordance with Harmony’s charter documents; or

• by NextDecade if the board of directors of Harmony or any committee or agent or representative thereof shall withdraw (or modify in a manner adverse to NextDecade), or propose to withdraw (or modify in a manner adverse to NextDecade), the Harmony board of director’s recommendation that the holders of Harmony Common Stock vote in favor of the adoption of the Agreement and the approval of the Merger.

If permitted under applicable law, either Harmony or NextDecade may waive any inaccuracies in the representations and warranties made to such party contained in the Agreement and waive compliance with any agreements or conditions for the benefit of itself or such party contained in the Agreement. However, the condition requiring that Harmony have at least $5,000,001 of net tangible assets may not be waived by Harmony, due to applicable laws.

14

The existence of the financial and personal interests of the Harmony directors may result in a conflict of interest on the part of one or more of them between what he may believe is best for Harmony and what he may believe is best for himself in determining whether or not to grant a waiver in a specific situation. Please read the section entitled “Risk Factors” for a fuller discussion of this and other risks.

Tax Consequences of the Transactions

Harmony has received an opinion from its counsel, Graubard Miller, that, for U.S. federal income tax purposes:

• No gain or loss will be recognized by stockholders of Harmony who do not elect conversion of their public shares; and

• A stockholder of Harmony who exercises conversion rights and effects a termination of the stockholder’s interest in Harmony will be required to recognize capital gain or loss upon the exchange of that stockholder’s shares of Harmony Common Stock for cash, if such shares were held as a capital asset on the date of the business combination. Such gain or loss will be measured by the difference between the amount of cash received and the tax basis of that stockholder’s shares of Harmony Common Stock.

The tax opinion is attached to this proxy statement as Annex D. Graubard Miller has consented to the use of its opinion in this proxy statement. For a description of the material U.S. federal income tax consequences of the merger, please read the information set forth in “The Merger Proposal — Material Federal Income Tax Consequences of the Transactions to Harmony and its Stockholders.”

Anticipated Accounting Treatment

The post-merger accounting will be determined by which entity is deemed the accounting acquirer. Harmony relied upon FASB ASC paragraphs 805-10-55-11 through 55-15 to make its determination of the acquirer for accounting purposes and believes NextDecade will be the accounting acquirer based on: (i) NextDecade owners’ preponderance of voting rights (at least 87%) in the combined entity after the business combination, (ii) the preponderance of representation of NextDecade board members on the combined entity’s board (7 of 9 total board members), (iii) the replacement of Harmony’s management team with NextDecade’s management team after the business combination, and (iv) NextDecade’s preponderance in relative size as evaluated by investment and valuation. Therefore, the mergers will be accounted for as a “reverse merger” and recapitalization at the date of the consummation of the transaction. Accordingly, the assets and liabilities and the historical operations that will be reflected in the combined company financial statements after the consummation of the mergers will be those of NextDecade and will be recorded at the historical cost basis of NextDecade. Harmony’s assets, liabilities and results of operations will be consolidated with those of NextDecade upon the consummation of the business combination.

Regulatory Matters

The transactions contemplated by the Agreement are not subject to any additional federal or state regulatory requirement or approval, except for the filing of required notifications and the expiration or termination of the required waiting periods under the HSR Act and filings with the applicable state offices necessary to effectuate the Blocker Mergers and the Merger. On May 8, 2017, the FTC granted early termination of the 30-day waiting period under the HSR Act, with respect to the business combination. The grant of early termination has the effect of satisfying the HSR Act condition under the Agreement.

Closing the Business Combination

The parties plan to complete the business combination promptly after the Harmony special meeting, provided that:

• Harmony’s stockholders have approved the Merger Proposal and the Charter Proposals;

• Harmony has net tangible assets of at least $5,000,001 after taking into account holders of public shares exercising their conversion rights; and

• the other conditions specified in the Agreement have been satisfied or waived.

15

Interests of Harmony’s Directors, Officers and Others in the Business Combination

When you consider the recommendation of Harmony’s board of directors in favor of approval of the Merger Proposal, you should keep in mind that Harmony’s initial stockholders, including its directors, executive officers and special advisor, have interests in such proposal that are different from, or in addition to, your interests as a stockholder or warrant holder. These interests include, among other things:

• If the business combination with NextDecade or another business combination is not consummated by July 27, 2017 or such later date as approved by Harmony’s stockholders, Harmony will cease all operations except for the purpose of winding up, redeeming 100% of the outstanding public shares for cash and, subject to the approval of its remaining stockholders and its board of directors, dissolving and liquidating. In such event, the 3,026,250 initial shares held by Harmony’s initial stockholders, including its directors and officers, which were acquired for an aggregate purchase price of $25,000 prior to Harmony’s initial public offering, would be worthless because Harmony’s initial stockholders are not entitled to participate in any redemption or distribution with respect to such shares. Such shares had an aggregate market value of $31,230,900 based upon the closing price of $10.32 per share on Nasdaq on June 29, 2017.

• The Harmony initial stockholders purchased an aggregate of 508,500 private units from Harmony for an aggregate purchase price of $5,085,000 (or $10.00 per unit). These purchases took place on a private placement basis simultaneously with the consummation of the initial public offering. All of the proceeds Harmony received from these purchases were placed in the trust account. Such units had an aggregate market value of $5,517,225 based upon the closing price of $10.85 per unit on Nasdaq on June 29, 2017. The purchasers waived the right to participate in any redemption or liquidation distribution with respect to such private units. Accordingly, the private units and underlying securities will become worthless if Harmony does not consummate a business combination within the required time period.

• The transactions contemplated by the Agreement provide that Eric S. Rosenfeld and David D. Sgro will be directors of Harmony following the business combination (assuming they are elected at this meeting). As such, in the future each may receive cash fees, stock options or stock awards that the Harmony board of directors determines to pay to its directors.

• If Harmony is unable to complete a business combination within the required time period, Mr. Rosenfeld will be personally liable to ensure that the proceeds in the trust account are not reduced by the claims of target businesses or claims of vendors or other entities that are owed money by Harmony for services rendered or contracted for or products sold to Harmony, but only if such a vendor or target business has not executed a trust account waiver agreement.

• Harmony’s officers, directors, initial stockholders and their affiliates are entitled to reimbursement of out-of-pocket expenses incurred by them in connection with certain activities on Harmony’s behalf, such as identifying and investigating possible business targets and business combinations. However, if Harmony fails to consummate a business combination within the required period, they will not have any claim against the trust account for reimbursement. Accordingly, Harmony may not be able to reimburse these expenses if the transactions, or another business combination, is not completed by the required date. As of June 29, 2017, Harmony’s officers, directors, initial stockholders and their affiliates had not incurred any unpaid reimbursable expenses but may do so prior to the special meeting.

• Since its inception, Harmony’s officers, directors and special advisor have made loans from time to time to Harmony to fund working capital requirements (excluding loans made to extend the time period Harmony has to complete a business combination). As of the date of this proxy statement, an aggregate of approximately $223,600 principal amount of these loans is outstanding. These loans are evidenced by non-interest bearing notes, all of which are convertible at the lenders’ election upon the consummation of an initial business combination into units of Harmony, at a price of $10.00 per unit. If Harmony’s officers and directors converted the full amount of the notes into units, it would result in them being issued an aggregate of 22,360 shares of common stock and 22,360 warrants of Harmony. If the business combination is not consummated, the notes will not be repaid or converted and will be forgiven.

16

• In connection with Harmony obtaining the extension of time to complete an initial business combination, the initial stockholders and NextDecade have loaned Harmony an aggregate of approximately $1,210,500 for the contributions necessary to secure such extension. These loans are evidenced by non-interest bearing notes. If the business combination is not consummated, the notes will not be repaid and will be forgiven.

• If Harmony is required to be liquidated and there are no funds remaining to pay the costs associated with the implementation and completion of such liquidation, Mr. Rosenfeld has agreed to advance Harmony the funds necessary to pay such costs and complete such liquidation (currently anticipated to be no more than approximately $15,000) and not to seek repayment for such expenses.

At any time prior to the special meeting, during a period when they are not then aware of any material nonpublic information regarding Harmony or its securities, the Harmony initial stockholders, NextDecade or the Members, the Blocker Owners and/or their respective affiliates may purchase shares from institutional and other investors who vote, or indicate an intention to vote, against the Merger Proposal, or execute agreements to purchase such shares from such investors in the future, or they may enter into transactions with such investors and others to provide them with incentives to acquire shares of Harmony’s common stock or vote their shares in favor of the Merger Proposal. The purpose of such share purchases and other transactions would be to increase the likelihood of satisfaction of the requirement that the holders of a majority of the outstanding shares of Harmony Common Stock on the record date vote in its favor or to decrease the number of public shares that were being converted to cash. While the exact nature of any such incentives has not been determined as of the date of this proxy statement, they might include, without limitation, arrangements to protect such investors or holders against potential loss in value of their shares, including the granting of put options and the transfer to such investors or holders of shares or warrants owned by the Harmony initial stockholders for nominal value.

Entering into any such arrangements may have a depressive effect on Harmony’s Common Stock. For example, as a result of these arrangements, an investor or holder may have the ability to effectively purchase shares at a price lower than market and may therefore be more likely to sell the shares he owns, either prior to or immediately after the special meeting.

If such transactions are effected, the consequence could be to cause the transactions to be approved in circumstances where such approval could not otherwise be obtained. Purchases of shares by the persons described above would allow them to exert more influence over the approval of the Merger Proposal and other proposals to be presented at the special meeting and would likely increase the chances that such proposals would be approved.