UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2016

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 001-36638

Medley Management Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 47-1130638 |

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

280 Park Avenue, 6th Floor East

New York, New York 10017

(Address of principal executive offices)(Zip Code)

(212) 759-0777

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ |

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The number of shares of the registrant’s Class A common stock, par value $0.01 per share, outstanding as of November 14, 2016 was 5,809,130. The number of shares of the registrant’s Class B common stock, par value $0.01 per share, outstanding as of November 14, 2016 was 100.

TABLE OF CONTENTS

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q (“Form 10-Q”) contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) that reflect our current views with respect to, among other things, our operations and financial performance. Forward-looking statements include all statements that are not historical facts. In some cases, you can identify these forward-looking statements by the use of words such as “outlook,” “believes,” “expects,” “potential,” “may,” “should,” “could,” “seeks,” “approximately,” “predicts,” “intends,” “plans,” “estimates,” “anticipates” or the negative version of these words or other comparable words. Such forward-looking statements are subject to various risks and uncertainties. Accordingly, there are or will be important factors that could cause actual outcomes or results to differ materially from those indicated in these statements. We believe these factors include, but are not limited to, those described under Part I, Item 1A. “Risk Factors,” in our Annual Report on Form 10-K for the fiscal year ended December 31, 2015 (the “Annual Report on Form 10-K”) available on the SEC’s website at www.sec.gov, which include, but are not limited to, the following:

| · | difficult market and political conditions may adversely affect our business in many ways, including by reducing the value or hampering the performance of the investments made by our funds, each of which could materially and adversely affect our business, results of operations and financial condition; |

| · | we derive a substantial portion of our revenues from funds managed pursuant to advisory agreements that may be terminated or fund partnership agreements that permit fund investors to remove us as the general partner; |

| · | we may not be able to maintain our current fee structure as a result of industry pressure from fund investors to reduce fees, which could have an adverse effect on our profit margins and results of operations; |

| · | a change of control of us could result in termination of our investment advisory agreements; |

| · | the historical returns attributable to our funds should not be considered as indicative of the future results of our funds or of our future results or of any returns expected on an investment in our Class A common stock; |

| · | if we are unable to consummate or successfully integrate development opportunities, acquisitions or joint ventures, we may not be able to implement our growth strategy successfully; |

| · | we depend on third-party distribution sources to market our investment strategies; |

| · | an investment strategy focused primarily on privately held companies presents certain challenges, including the lack of available information about these companies; |

| · | our funds’ investments in investee companies may be risky, and our funds could lose all or part of their investments; |

| · | prepayments of debt investments by our investee companies could adversely impact our results of operations; |

| · | our funds’ investee companies may incur debt that ranks equally with, or senior to, our funds’ investments in such companies; |

| · | subordinated liens on collateral securing loans that our funds make to their investee companies may be subject to control by senior creditors with first priority liens and, if there is a default, the value of the collateral may not be sufficient to repay in full both the first priority creditors and our funds; |

| · | there may be circumstances where our funds’ debt investments could be subordinated to claims of other creditors or our funds could be subject to lender liability claims; |

| · | our funds may not have the resources or ability to make additional investments in our investee companies; |

| · | economic recessions or downturns could impair our investee companies and harm our operating results; |

| · | a covenant breach by our investee companies may harm our operating results; |

| · | the investment management business is competitive; |

i

| · | our funds operate in a competitive market for lending that has recently intensified, and competition may limit our funds’ ability to originate or acquire desirable loans and investments and could also affect the yields of these assets and have a material adverse effect on our business, results of operations and financial condition; |

| · | dependence on leverage by certain of our funds and by our funds’ investee companies subjects us to volatility and contractions in the debt financing markets and could adversely affect our ability to achieve attractive rates of return on those investments; |

| · | some of our funds may invest in companies that are highly leveraged, which may increase the risk of loss associated with those investments; |

| · | we generally do not control the business operations of our investee companies and, due to the illiquid nature of our investments, may not be able to dispose of such investments; |

| · | a substantial portion of our investments may be recorded at fair value as determined in good faith by or under the direction of our respective funds’ boards of directors or similar bodies and, as a result, there may be uncertainty regarding the value of our funds’ investments; |

| · | we may need to pay “clawback” obligations if and when they are triggered under the governing agreements with respect to certain of our funds and SMAs; |

| · | our funds may face risks relating to undiversified investments; |

| · | third-party investors in our private funds may not satisfy their contractual obligation to fund capital calls when requested, which could adversely affect a fund’s operations and performance; |

| · | our funds may be forced to dispose of investments at a disadvantageous time; |

| · | hedging strategies may adversely affect the returns on our funds’ investments; |

| · | our business depends in large part on our ability to raise capital from investors. If we were unable to raise such capital, we would be unable to collect management fees or deploy such capital into investments, which would materially and adversely affect our business, results of operations and financial condition; |

| · | we depend on our senior management team, senior investment professionals and other key personnel, and our ability to retain them and attract additional qualified personnel is critical to our success and our growth prospects; |

| · | our failure to appropriately address conflicts of interest could damage our reputation and adversely affect our business; |

| · | potential conflicts of interest may arise between our Class A common stockholders and our fund investors; |

| · | rapid growth of our business may be difficult to sustain and may place significant demands on our administrative, operational and financial resources; |

| · | we may enter into new lines of business and expand into new investment strategies, geographic markets and business, each of which may result in additional risks and uncertainties in our business; |

| · | extensive regulation affects our activities, increases the cost of doing business and creates the potential for significant liabilities and penalties that could adversely affect our business and results of operations; |

| · | failure to comply with “pay to play” regulations implemented by the SEC and certain states, and changes to the “pay to play” regulatory regimes, could adversely affect our business; |

| · | new or changed laws or regulations governing our funds’ operations and changes in the interpretation thereof could adversely affect our business; |

ii

| · | present and future business development companies for which we serve as investment adviser are subject to regulatory complexities that limit the way in which they do business and may subject them to a higher level of regulatory scrutiny; |

| · | we are subject to risks in using custodians, counterparties, administrators and other agents; |

| · | a portion of our revenue and cash flow is variable, which may impact our ability to achieve steady earnings growth on a quarterly basis and may cause the price of our Class A common stock to decline; |

| · | we may be subject to litigation risks and may face liabilities and damage to our professional reputation as a result; |

| · | employee misconduct could harm us by impairing our ability to attract and retain investors and subjecting us to significant legal liability, regulatory scrutiny and reputational harm, and fraud and other deceptive practices or other misconduct at our investee companies could similarly subject us to liability and reputational damage and also harm our business; |

| · | our substantial indebtedness could adversely affect our financial condition, our ability to pay our debts or raise additional capital to fund our operations, our ability to operate our business and our ability to react to changes in the economy or our industry and could divert our cash flow from operations for debt payments; |

| · | our Senior Secured Credit Facilities impose significant operating and financial restrictions on us and our subsidiaries, which may prevent us from capitalizing on business opportunities; |

| · | servicing our indebtedness will require a significant amount of cash. Our ability to generate sufficient cash depends on many factors, some of which are not within our control; |

| · | despite our current level of indebtedness, we may be able to incur substantially more debt and enter into other transactions, which could further exacerbate the risks to our financial condition; |

| · | operational risks may disrupt our business, result in losses or limit our growth; |

| · | Medley Management Inc.’s only material asset is its interest in Medley LLC, and it is accordingly dependent upon distributions from Medley LLC to pay taxes, make payments under the tax receivable agreement or pay dividends; |

| · | Medley Management Inc. is controlled by our pre-IPO owners, whose interests may differ from those of our public stockholders; |

| · | Medley Management Inc. will be required to pay exchanging holders of LLC Units for most of the benefits relating to any additional tax depreciation or amortization deductions that we may claim as a result of the tax basis step-up we receive in connection with sales or exchanges of LLC Units and related transactions; |

| · | in certain cases, payments under the tax receivable agreement may be accelerated and/or significantly exceed the actual benefits Medley Management Inc. realizes in respect of the tax attributes subject to the tax receivable agreement; and |

| · | anti-takeover provisions in our organizational documents and Delaware law might discourage or delay acquisition attempts for us that you might consider favorable. |

These factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included in this Form 10-Q. Forward-looking statements speak as of the date on which they are made, and we undertake no obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by law.

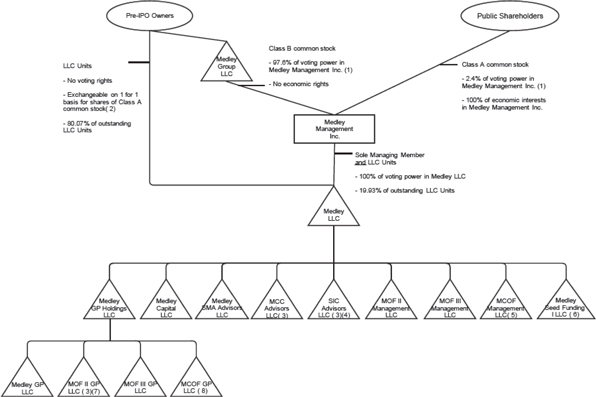

Medley Management Inc. was incorporated as a Delaware corporation on June 13, 2014, and its sole asset is a controlling equity interest in Medley LLC. Pursuant to a reorganization into a holding corporation structure (the “Reorganization”) consummated in connection with Medley Management Inc.’s initial public offering (“IPO”), Medley Management Inc. became a holding corporation and the sole managing member of Medley LLC, operating and controlling all of the business and affairs of Medley LLC and, through Medley LLC and its subsidiaries, conducts its business.

iii

Unless the context suggests otherwise, references herein to the “Company,” “Medley,” “we,” “us” and “our” refer to Medley Management Inc., Medley LLC and its consolidated subsidiaries.

The “pre-IPO owners” refers to the senior professionals who were the owners of Medley LLC immediately prior to the consummation of Medley Management Inc.’s IPO and subsequent purchase of 6,000,000 newly issued limited liability company units (the “LLC Units”) from Medley LLC, which correspondingly diluted the ownership interests of the pre-IPO owners in Medley LLC and resulted in Medley Management Inc.’s holding a number of LLC Units in Medley LLC equal to the number of shares of Class A common stock it issued in its IPO.

Unless the context suggests otherwise, references herein to:

| · | “AUM” refers to the assets of our funds, which represents the sum of the NAV of such funds, the drawn and undrawn debt (at the fund level, including amounts subject to restrictions) and uncalled committed capital (including commitments to funds that have yet to commence their investment periods); |

| · | “base management fees” refers to fees we earn for advisory services provided to our funds, which are generally based on a defined percentage of fee earning AUM or, in certain cases, a percentage of originated assets in the case of certain of our SMAs; |

| · | “BDC” refers to business development company; |

| · | “fee earning AUM” refers to the assets under management on which we directly earn base management fees; |

| · | “hurdle rates” refers to the rates above which we earn performance fees, as defined in the long-dated private funds’ and SMAs’ applicable investment management or partnership agreements. |

| · | “investee company” refers to a company to which one of our funds lends money or in which one of our funds otherwise makes an investment; |

| · | “long-dated private funds” refers to MOF II, MOF III and any other private funds we may manage in the future; |

| · | “management fees” refers to base management fees and Part I incentive fees; |

| · | “Medley LLC” refers to Medley LLC and its consolidated subsidiaries; |

| · | “MCOF” refers to Medley Credit Opportunity Fund LP; |

| · | “MOF II” refers to Medley Opportunity Fund II LP; |

| · | “MOF III” refers to Medley Opportunity Fund III LP; |

| · | “our funds” refers to the funds, alternative asset companies and other entities and accounts that are managed or co-managed by us and our affiliates; |

| · | “our investors” refers to the investors in our permanent capital vehicles, our private funds and our SMAs; |

| · | “Part I incentive fees” refers to fees that we receive from our permanent capital vehicles, which are paid in cash quarterly and are driven primarily by net interest income on senior secured loans subject to hurdle rates. With respect to periods subsequent to January 1, 2016, as it relates to Medley Capital Corporation (NYSE: MCC) (“MCC”), these fees are subject to netting against realized and unrealized losses; |

| · | “Part II incentive fees” refers to fees related to realized capital gains in our permanent capital vehicles; |

| · | “performance fees” refers to incentive allocations in our long-dated private funds and incentive fees from our SMAs, which are typically 15% or 20% of the total return after a hurdle rate, accrued quarterly, but paid after the return of all invested capital and in an amount sufficient to achieve the hurdle rate; | |

| · | “permanent capital” refers to capital of funds that do not have redemption provisions or a requirement to return capital to investors upon exiting the investments made with such capital, except as required by applicable law, which funds currently consist of MCC and Sierra Income Corporation (“SIC”). Such funds may be required, or elect, to return all or a portion of capital gains and investment income. In certain circumstances, the investment adviser of such a fund may be removed; and |

| · | “SMA” refers to a separately managed account; |

| · | “STRF” refers to Sierra Total Return Fund. |

iv

PART 1 – FINANCIAL INFORMATION

| Item 1. | Financial Statements |

Condensed Consolidated Balance Sheets

(Amounts in thousands, except share and per share amounts)

| As of | ||||||||

| September 30, | As of | |||||||

| 2016 | December 31, | |||||||

| (unaudited) | 2015 | |||||||

| Assets | ||||||||

| Cash and cash equivalents | $ | 57,331 | $ | 71,688 | ||||

| Investments, at fair value | 24,273 | 16,360 | ||||||

| Management fees receivable | 12,613 | 16,172 | ||||||

| Performance fees receivable | 4,245 | 2,518 | ||||||

| Other assets | 18,185 | 13,015 | ||||||

| Total assets | $ | 116,647 | $ | 119,753 | ||||

| Liabilities and Equity | ||||||||

| Loans payable | $ | 78,197 | $ | 100,871 | ||||

| Senior unsecured debt | 23,394 | - | ||||||

| Accounts payable, accrued expenses and other liabilities | 37,403 | 34,746 | ||||||

| Performance fee compensation payable | 1,066 | 1,823 | ||||||

| Total liabilities | 140,060 | 137,440 | ||||||

| Commitments and contingencies (Note 9) | ||||||||

| Redeemable Non-controlling Interests | 24,668 | - | ||||||

| Equity | ||||||||

| Class A common stock, $0.01 par value, 3,000,000,000 shares authorized; 6,042,050 and 6,010,646 issued as of September 30, 2016 and December 31, 2015, respectively; 5,809,130 and 5,993,941 outstanding as of September 30, 2016 and December 31, 2015, respectively | 58 | 60 | ||||||

| Class B common stock, $0.01 par value, 1,000,000 shares authorized; 100 shares issued and outstanding | - | - | ||||||

| Additional paid in capital (capital deficit) | 2,170 | 631 | ||||||

| Accumulated other comprehensive income (loss) | 47 | - | ||||||

| Retained earnings (accumulated deficit) | (4,473 | ) | (730 | ) | ||||

| Total stockholders' equity (deficit), Medley Management Inc. | (2,198 | ) | (39 | ) | ||||

| Non-controlling interests in consolidated subsidiaries | (1,863 | ) | (459 | ) | ||||

| Non-controlling interests in Medley LLC | (44,020 | ) | (17,189 | ) | ||||

| Total equity (deficit) | (48,081 | ) | (17,687 | ) | ||||

| Total liabilities, redeemable non-controlling interests and equity | $ | 116,647 | $ | 119,753 | ||||

See accompanying notes to unaudited condensed consolidated financial statements

F- 1

Condensed Consolidated Statements of Operations (unaudited)

(Amounts in thousands, except share and per share amounts)

| For the Three Months Ended | For the Nine Months Ended | |||||||||||||||

| September 30, | September 30, | |||||||||||||||

| 2016 | 2015 | 2016 | 2015 | |||||||||||||

| Revenues | ||||||||||||||||

| Management fees | $ | 15,262 | $ | 18,135 | $ | 50,220 | $ | 56,578 | ||||||||

| Performance fees | 1,446 | (14,595 | ) | 1,706 | (10,627 | ) | ||||||||||

| Other revenues and fees | 2,172 | 1,891 | 5,851 | 5,496 | ||||||||||||

| Total revenues | 18,880 | 5,431 | 57,777 | 51,447 | ||||||||||||

| Expenses | ||||||||||||||||

| Compensation and benefits | 6,964 | 5,914 | 21,396 | 19,532 | ||||||||||||

| Performance fee compensation | (212 | ) | (3,660 | ) | (238 | ) | (4,578 | ) | ||||||||

| General, administrative and other expenses | 8,801 | 1,626 | 25,679 | 10,756 | ||||||||||||

| Total expenses | 15,553 | 3,880 | 46,837 | 25,710 | ||||||||||||

| Other income (expense) | ||||||||||||||||

| Dividend income | 312 | 222 | 755 | 665 | ||||||||||||

| Interest expense | (2,403 | ) | (2,141 | ) | (6,593 | ) | (6,335 | ) | ||||||||

| Other income (expenses), net | 55 | (838 | ) | (1,559 | ) | (1,087 | ) | |||||||||

| Total other expense, net | (2,036 | ) | (2,757 | ) | (7,397 | ) | (6,757 | ) | ||||||||

| Income (loss) before income taxes | 1,291 | (1,206 | ) | 3,543 | 18,980 | |||||||||||

| Provision for (benefit from) income taxes | 77 | (113 | ) | 291 | 1,953 | |||||||||||

| Net income (loss) | 1,214 | (1,093 | ) | 3,252 | 17,027 | |||||||||||

| Net income (loss) attributable to redeemable non-controlling interests and non-controlling interests in consolidated subsidiaries | 438 | (2,150 | ) | 1,106 | (1,134 | ) | ||||||||||

| Net income attributable to non-controlling interests in Medley LLC | 556 | 785 | 1,774 | 15,576 | ||||||||||||

| Net income attributable to Medley Management Inc. | $ | 220 | $ | 272 | $ | 372 | $ | 2,585 | ||||||||

| Dividends declared per Class A common stock | $ | 0.20 | $ | 0.20 | $ | 0.60 | $ | 0.40 | ||||||||

| Net income (loss) per Class A common stock: | ||||||||||||||||

| Basic (Note 11) | $ | - | $ | 0.04 | $ | (0.05 | ) | $ | 0.38 | |||||||

| Diluted (Note 11) | $ | - | $ | 0.04 | $ | (0.05 | ) | $ | 0.38 | |||||||

| Weighted average shares outstanding - Basic and Diluted | 5,778,409 | 6,000,211 | 5,802,334 | 6,000,071 | ||||||||||||

See accompanying notes to unaudited condensed consolidated financial statements

F- 2

Condensed Consolidated Statements of Comprehensive Income (unaudited)

(Amounts in thousands)

| For the Three Months Ended | For the Nine Months Ended | |||||||||||||||

| September 30, | September 30, | |||||||||||||||

| 2016 | 2015 | 2016 | 2015 | |||||||||||||

| Net income (loss) | $ | 1,214 | $ | (1,093 | ) | $ | 3,252 | $ | 17,027 | |||||||

| Other comprehensive income (loss): | ||||||||||||||||

| Change in fair value on available-for-sale securities | 268 | - | 268 | - | ||||||||||||

| Total comprehensive income (loss) | 1,482 | (1,093 | ) | 3,520 | 17,027 | |||||||||||

| Comprehensive income (loss) attributable to redeemable non-controlling interests and non-controlling interests in consolidated subsidiaries | 469 | (2,150 | ) | 1,137 | (1,134 | ) | ||||||||||

| Comprehensive income (loss) attributable to Medley LLC | 746 | 785 | 1,964 | 15,576 | ||||||||||||

| Comprehensive income attributable to Medley Management Inc. | $ | 267 | $ | 272 | $ | 419 | $ | 2,585 | ||||||||

See accompanying notes to unaudited condensed consolidated financial statements

F- 3

Condensed Consolidated Statement of Changes in Equity and Redeemable Non-controlling Interests (unaudited)

(Amounts in thousands, except share and per share amounts)

| Additional | Non- | Non- | ||||||||||||||||||||||||||||||||||||||||||

| Paid in | Accumulated | Retained | controlling | controlling | Redeemable | |||||||||||||||||||||||||||||||||||||||

| Class A | Class B | Capital | Other | Earnings | Interests in | Interests in | Non- | |||||||||||||||||||||||||||||||||||||

| Common Stock | Common Stock | (Capital | Comprehensive | (Accumulated | Consolidated | Medley | Total | controlling | ||||||||||||||||||||||||||||||||||||

| Shares | Dollars | Shares | Dollars | Deficit) | Income (Loss) | Deficit) | Subsidiaries | LLC | Equity | Interests | ||||||||||||||||||||||||||||||||||

| Balance at December 31, 2015 | 5,993,941 | $ | 60 | 100 | $ | - | $ | 631 | $ | - | $ | (730 | ) | $ | (459 | ) | $ | (17,189 | ) | $ | (17,687 | ) | $ | - | ||||||||||||||||||||

| Net income (loss) | - | - | - | - | - | - | 372 | (10 | ) | 1,774 | 2,136 | 1,116 | ||||||||||||||||||||||||||||||||

| Change in fair value on available-for-sale securities | - | - | - | - | - | 47 | - | - | 190 | 237 | 31 | |||||||||||||||||||||||||||||||||

| Stock-based compensation | - | - | - | - | 2,735 | - | - | - | - | 2,735 | - | |||||||||||||||||||||||||||||||||

| Dividends on Class A common stock ($0.60 per share) | - | - | - | - | - | - | (4,115 | ) | - | - | (4,115 | ) | - | |||||||||||||||||||||||||||||||

| Issuance of Class A common stock related to vesting of restricted stock units | 31,404 | |||||||||||||||||||||||||||||||||||||||||||

| Repurchases of Class A common stock | (216,215 | ) | (2 | ) | - | - | (1,196 | ) | - | - | - | - | (1,198 | ) | - | |||||||||||||||||||||||||||||

| Contributions | - | - | - | - | - | - | - | 2 | - | 2 | 12,000 | |||||||||||||||||||||||||||||||||

| Distributions | - | - | - | - | - | - | - | (1,547 | ) | (16,448 | ) | (17,995 | ) | (675 | ) | |||||||||||||||||||||||||||||

| Reclassification of redeemable non-controlling interest | - | - | - | - | - | - | - | (41 | ) | (12,155 | ) | (12,196 | ) | 12,196 | ||||||||||||||||||||||||||||||

| Fair value of non-controlling interest | - | - | - | - | - | - | - | 192 | (192 | ) | - | - | ||||||||||||||||||||||||||||||||

| Balance at September 30, 2016 | $ | 5,809,130 | $ | 58 | 100 | $ | - | $ | 2,170 | $ | 47 | $ | (4,473 | ) | $ | (1,863 | ) | $ | (44,020 | ) | $ | (48,081 | ) | $ | 24,668 | |||||||||||||||||||

See accompanying notes to unaudited condensed consolidated financial statements

F- 4

Condensed Consolidated Statements of Cash

Flows (unaudited)

(Amounts in thousands)

| For the Nine Months Ended | ||||||||

| September 30, | ||||||||

| 2016 | 2015 | |||||||

| Cash flows from operating activities | ||||||||

| Net income (loss) | $ | 3,252 | $ | 17,027 | ||||

| Adjustments to reconcile net income to net cash provided by (used in) operating activities: | ||||||||

| Non-cash stock-based compensation | 2,735 | 2,376 | ||||||

| Net change in unrealized depreciation (appreciation) on investments | (8 | ) | 422 | |||||

| Loss on disposal of fixed assets | 27 | - | ||||||

| Loss (income) from equity method investments | 264 | 11,497 | ||||||

| Depreciation and amortization | 678 | 341 | ||||||

| Provision for (benefit from) deferred taxes | (576 | ) | 69 | |||||

| Amortization of debt issuance costs | 555 | 409 | ||||||

| Accretion of debt discount | 633 | 577 | ||||||

| Changes in operating assets and liabilities: | ||||||||

| Management fees receivable | 3,559 | (42 | ) | |||||

| Performance fees receivable | (1,727 | ) | (920 | ) | ||||

| Other assets | (1,006 | ) | (6,483 | ) | ||||

| Accounts payable, accrued expenses and other liabilities | 262 | (8,465 | ) | |||||

| Performance fee compensation payable | (757 | ) | (6,048 | ) | ||||

| Net cash provided by (used in) operating activities | 7,891 | 10,760 | ||||||

| Cash flows from investing activities | ||||||||

| Purchases of fixed assets | (1,924 | ) | (129 | ) | ||||

| Distributions received from equity method investments | 1,152 | 184 | ||||||

| Purchases of available-for-sale securities | (8,846 | ) | - | |||||

| Net cash provided by (used in) investing activities | (9,618 | ) | 55 | |||||

| Cash flows from financing activities | ||||||||

| Repayment of debt obligations | (23,812 | ) | (937 | ) | ||||

| Proceeds from issuance of debt obligations | 24,212 | - | ||||||

| Capital contributions from non-controlling interests in consolidated subsidiaries and redeemable non-controlling interests | 12,002 | - | ||||||

| Distributions to members and redeemable non-controlling interests | (18,670 | ) | (29,507 | ) | ||||

| Debt obligations issuance costs | (842 | ) | - | |||||

| Dividends paid | (4,115 | ) | (2,749 | ) | ||||

| Repurchases of Class A common stock | (1,198 | ) | - | |||||

| Capital contributions to equity method investments | (207 | ) | (1,074 | ) | ||||

| Net cash provided by (used in) financing activities | (12,630 | ) | (34,267 | ) | ||||

| Net increase (decrease) in cash and cash equivalents | (14,357 | ) | (23,452 | ) | ||||

| Cash and cash equivalents, beginning of period | 71,688 | 87,206 | ||||||

| Cash and cash equivalents, end of period | $ | 57,331 | $ | 63,754 | ||||

| Supplemental disclosure of non-cash investing and financing activities | ||||||||

| Reclassification of redeemable non-controlling interest | $ | 12,155 | $ | - | ||||

| Fixed assets | 2,293 | - | ||||||

| Fair value of non-controlling interest | 192 | - | ||||||

See accompanying notes to unaudited condensed consolidated financial statements

F- 5

Notes to Condensed Consolidated Financial Statements (unaudited)

1. ORGANIZATION AND BASIS OF PRESENTATION

Medley Management Inc. is an asset management firm offering yield solutions to retail and institutional investors. The corporation’s national direct origination franchise provides capital to the middle market in the U.S. Medley Management Inc., through its consolidated subsidiary, Medley LLC, provides investment management services to permanent capital vehicles, long-dated private funds and separately managed accounts and serves as the general partner to the private funds, which are generally organized as pass-through entities. Medley LLC is headquartered in New York City and has an office in San Francisco.

The Company’s business is currently comprised of only one reportable segment, the investment management segment, and substantially all Company operations are conducted through this segment. The investment management segment provides investment management services to permanent capital vehicles, long-dated private funds and separately managed accounts. The Company conducts its investment management business in the U.S., where substantially all its revenues are generated.

Initial Public Offering of Medley Management Inc.

Medley Management Inc. was incorporated on June 13, 2014 and commenced operations on September 29, 2014 upon the completion of its initial public offering (“IPO”) of its Class A common stock. Medley Management Inc. raised $100.4 million, net of underwriting discount, through the issuance of 6,000,000 shares of Class A common stock at an offering price to the public of $18.00 per share. Medley Management Inc. used the offering proceeds to purchase 6,000,000 newly issued LLC Units (defined below) from Medley LLC. Prior to the IPO, Medley Management Inc. had not engaged in any business or other activities except in connection with its formation and IPO.

In connection with the IPO, Medley Management Inc. issued 100 shares of Class B common stock to Medley Group LLC (“Medley Group”), an entity wholly owned by the pre-IPO members of Medley LLC. For as long as the pre-IPO members and then-current Medley personnel hold at least 10% of the aggregate number of shares of Class A common stock and LLC Units (defined below) (excluding those LLC Units held by Medley Management Inc.) then outstanding, the Class B common stock entitles Medley Group to a number of votes that is equal to 10 times the aggregate number of LLC Units held by all non-managing members of Medley LLC that do not themselves hold shares of Class B common stock and entitle each other holder of Class B common stock, without regard to the number of shares of Class B common stock held by such other holder, to a number of votes that is equal to 10 times the number of membership units held by such holder. The Class B common stock does not participate in dividends and does not have any liquidation rights.

Medley LLC Reorganization

In connection with the IPO, Medley LLC amended and restated its limited liability agreement to modify its capital structure by reclassifying the 23,333,333 interests held by the pre-IPO members into a single new class of units (“LLC Units”). The pre-IPO members also entered into an exchange agreement under which they (or certain permitted transferees thereof) have the right, subject to the terms of an exchange agreement, to exchange their LLC Units for shares of Medley Management Inc.’s Class A common stock on a one-for-one basis, subject to customary conversion rate adjustments for stock splits, stock dividends and reclassifications. In addition, pursuant to the amended and restated limited liability agreement, Medley Management Inc. became the sole managing member of Medley LLC.

The pre-IPO owners, are, subject to limited exceptions, prohibited from transferring any LLC Units held by them or any shares of Class A common stock received upon exchange of such LLC Units, until the third anniversary of the date of the closing of the IPO without the Company’s consent. Thereafter and prior to the fourth and fifth anniversaries of the closing of the IPO, such holders may not transfer more than 33 1/3% and 66 2/3%, respectively, of the number of LLC Units held by them, together with the number of any shares of Class A common stock received by them upon exchange therefor, without the Company’s consent.

F- 6

Medley Management Inc.

Notes to Condensed Consolidated Financial Statements (unaudited)

Basis of Presentation

The accompanying condensed consolidated financial statements have been prepared on the accrual basis of accounting in conformity with U.S. generally accepted accounting principles (“GAAP”) and include the accounts of Medley Management Inc., Medley LLC and its consolidated subsidiaries (collectively, “Medley” or the “Company”). Additionally, the accompanying condensed consolidated financial statements of the Company and related financial information have been prepared pursuant to the requirements for reporting on Form 10-Q and Article 10 of Regulation S-X. Accordingly, certain disclosures accompanying annual financial statements prepared in accordance with U.S. GAAP may be omitted. In the opinion of management, the unaudited condensed consolidated financial results included herein contain all adjustments, consisting solely of normal recurring accruals, considered necessary for the fair presentation of financial statements for the interim periods included herein. Therefore, this Form 10-Q should be read in conjunction with the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2015 (the “Annual Report on Form 10-K”). The current period’s results of operations will not necessarily be indicative of results that ultimately may be achieved for the full year ending December 31, 2016.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Principles of Consolidation

In accordance with Accounting Standards Codification (“ASC”) 810, Consolidation, the Company consolidates those entities where it has a direct and indirect controlling financial interest based on either a variable interest model or voting interest model. As such, the Company consolidates entities that the Company concludes are variable interest entities (“VIEs”), for which the Company is deemed to be the primary beneficiary and entities in which it holds a majority voting interest or has majority ownership and control over the operational, financial and investing decisions of that entity.

In February 2015, the Financial Accounting Standards Board (“FASB”) issued ASU 2015-02, Consolidation (Topic 810) – Amendments to the Consolidation Analysis, which changes the consolidation analysis that a reporting entity must perform to determine whether it should consolidate certain types of legal entities. The Company elected to early adopt this new guidance using the modified retrospective method effective January 1, 2015. As a result of the adoption of ASU 2015-02, the Company determined that it is no longer the primary beneficiary of certain funds it manages. Therefore, the Company deconsolidated certain funds that had been consolidated under previous guidance effective January 1, 2015. As a result, amounts presented in the condensed consolidated financial statements herein for the three and nine months ended September 30, 2015 have been adjusted from amounts previously disclosed for the three and nine months ended September 30, 2015 to reflect the adoption of this guidance. Restatement of periods prior to January 1, 2015 was not required.

For legal entities evaluated for consolidation, the Company must determine whether the interests that it holds and fees paid to it qualify as a variable interest in an entity. This includes an evaluation of the management fees and performance fees paid to the Company when acting as a decision maker or service provider to the entity being evaluated. Under the new guidance, if (a) fees received by the Company are customary and commensurate with the level of services provided, and (b) the Company does not hold other economic interests in the entity that would absorb more than an insignificant amount of the expected losses or returns of the entity, the interest that the Company holds would not be considered a variable interest. The Company factors in all economic interests including proportionate interests through related parties, to determine if fees are considered a variable interest. Prior to the adoption of the new consolidation guidance, these fees were considered variable interests by the Company.

An entity in which the Company holds a variable interest is a VIE if any one of the following conditions exist: (a) the total equity investment at risk is not sufficient to permit the legal entity to finance its activities without additional subordinated financial support, (b) the holders of equity investment at risk have the right to direct the activities of the entity that most significantly impact the legal entity’s economic performance, (c) the voting rights of some investors are disproportionate to their obligation to absorb losses or rights to receive returns from a legal entity. Under the new guidance, for limited partnerships and other similar entities, non-controlling investors must have substantive rights to either dissolve the fund or remove the general partner (“kick-out rights”) in order to not qualify as a VIE.

For those entities that qualify as a VIE, the primary beneficiary is generally defined as the party who has a controlling financial interest in the VIE. The Company is generally deemed to have a controlling financial interest if it has (a) the power to direct the activities of a VIE that most significantly impact the VIE’s economic performance, and (b) the obligation to absorb losses or receive benefits from the VIE that could potentially be significant to the VIE. The Company determines whether it is the primary beneficiary of a VIE at the time it becomes initially involved with the VIE and reconsiders that conclusion continuously. The primary beneficiary evaluation is generally performed qualitatively on the basis of all facts and circumstances. However, quantitative information may also be considered in the analysis, as appropriate. These assessments require judgments. Each entity is assessed for consolidation on a case-by-case basis.

For those entities evaluated under the voting interest model, the Company consolidates the entity if it has a controlling financial interest. The Company has a controlling financial interest in a voting interest entity (“VOE”) if it owns a majority voting interest in the entity. Prior to the new guidance, the Company consolidated VOE’s where it was the general partner and as such, was presumed to have control.

F- 7

Medley Management Inc.

Notes to Condensed Consolidated Financial Statements (unaudited)

Consolidated Variable Interest Entities

Medley Management Inc. is the sole managing member of Medley LLC and, as such, it operates and controls all of the business and affairs of Medley LLC and, through Medley LLC, conducts its business. Under ASC 810, Medley LLC meets the definition of a VIE because the equity of Medley LLC is not sufficient to permit activities without additional subordinated financial support. Medley Management Inc. has the obligation to absorb expected losses that could be significant to Medley LLC and holds 100% of the voting power, therefore Medley Management Inc. is considered to be the primary beneficiary of Medley LLC.

As a result, Medley Management Inc. consolidates the financial results of Medley LLC and its subsidiaries and records a non-controlling interest for the economic interest in Medley LLC held by the non-managing members. Medley Management Inc.’s and the non-managing members’ economic interests in Medley LLC are 19.9% and 80.1%, respectively, as of September 30, 2016 and 20.4% and 79.6%, respectively, as of December 31, 2015. Net income attributable to the non-controlling interests in Medley LLC on the consolidated statements of operations represents the portion of earnings attributable to the economic interest in Medley LLC held by its non-managing members. Non-controlling interests in Medley LLC on the consolidated balance sheets represents the portion of net assets of Medley LLC attributable to the non-managing members based on total LLC Units of Medley LLC owned by such non-managing members.

As of September 30, 2016, Medley LLC has three majority owned subsidiaries, SIC Advisors LLC, Medley Seed Funding I LLC and STRF Advisors LLC, all of which are consolidated VIEs. Each of these entities was organized as a limited liability company and was legally formed to manage a designated fund and to isolate business risk. As of September 30, 2016, total assets and total liabilities, after eliminating entries, of these VIEs reflected in the consolidated balance sheets were an aggregate of $41.2 million and $24.8 million, respectively. As of December 31, 2015, Medley had only one majority owned subsidiary, SIC Advisors LLC, which was a consolidated VIE. As of December 31, 2015, total assets and total liabilities, after eliminating entries, of this VIE reflected in the consolidated balance sheets were $31.1 million and $21.2 million, respectively. Except to the extent of the assets of these VIEs that are consolidated, the holders of the consolidated VIEs’ liabilities generally do not have recourse to the Company.

Seed Investments

The Company accounts for seed investments through the application of the voting interest model under ASC 810-10-25-1 through 25-14 and consolidates a seed investment when the investment advisor holds a controlling interest, which is, in general, 50% or more of the equity in such investment. For seed investments for which the Company does not hold a controlling interest, the Company accounts for such seed investment under the equity method of accounting, at its ownership percentage of such seed investment’s net asset value.

Deconsolidated Funds

Prior to January 1, 2015, the Company had consolidated Medley Opportunity Fund II LP (“MOF II”) in its consolidated financial statements in accordance with ASC 810-20 as the Company was the general partner and the limited partners lacked kick out rights or participating rights. Under the guidance of ASU 2015-02, which the Company adopted effective as of January 1, 2015, the Company reconsidered the consolidation conclusion for MOF II and, as a result of the new guidance, determined that, although MOF II continues to be a VIE, the Company is no longer considered to be the primary beneficiary. Therefore, the Company deconsolidated MOF II at January 1, 2015 and records its investment in the entity under the equity method of accounting. See Note 3, “Investments.”

Non-Consolidated Variable Interest Entities

The Company holds interests in certain VIEs that are not consolidated because the Company is not deemed the primary beneficiary. The Company's interest in these entities is in the form of insignificant equity interests and fee arrangements. The maximum exposure to loss represents the potential loss of assets by the Company relating to these non-consolidated entities.

F- 8

Medley Management Inc.

Notes to Condensed Consolidated Financial Statements (unaudited)

As of September 30, 2016, the Company recorded investments, at fair value, attributed to these non-consolidated VIEs of $5.4 million, receivables of $1.8 million included as a component of other assets and a clawback obligation of $7.1 million included as a component of accounts payable, accrued expenses and other liabilities on the Company’s consolidated balance sheets. The clawback obligation assumes a hypothetical liquidation of a fund’s investments, at their then current fair values and a portion of tax distributions relating to performance fees which would need to be returned. As of December 31, 2015, the Company recorded investments, at fair value of $5.9 million, receivables of $0.9 million included as a component of other assets and a clawback obligation of $7.1 million included as a component of accounts payable, accrued expenses and other liabilities on the Company’s consolidated balance sheets. As of September 30, 2016, the Company’s maximum exposure to losses from these entities is $7.2 million.

Use of Estimates

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting period. Management’s estimates are based on historical experience and other factors, including expectations of future events that management believes to be reasonable under the circumstances. These assumptions and estimates also require management to exercise judgment in the process of applying the Company’s accounting policies. Significant estimates and assumptions by management affect the carrying value of investments, performance compensation payable and certain accrued liabilities. Actual results could differ from these estimates, and such differences could be material.

Indemnification

In the normal course of business, the Company enters into contractual agreements that provide general indemnifications against losses, costs, claims and liabilities arising from the performance of individual obligations under such agreements. The Company has not experienced any prior claims or payments pursuant to such agreements. The Company’s individual maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Company that have not yet occurred. However, based on management’s experience, the Company expects the risk of loss to be remote.

Non-Controlling Interests in Consolidated Subsidiaries

Non-controlling interests in consolidated subsidiaries represent the component of equity in such consolidated entities held by third-parties. These interests are adjusted for contributions to and distributions from Medley entities and are allocated income from Medley entities based on their ownership percentages.

Redeemable non-controlling interests represents interests of certain third parties that are not mandatorily redeemable but redeemable for cash or other assets at a fixed or determinable price or a fixed or determinable date, at the option of the holder or upon the occurrence of an event that is not solely within the control of the issuer. These interests are classified in temporary equity.

Investments

Investments include equity method investments that are not consolidated but over which the Company exerts significant influence. The Company measures the carrying value of its public non-traded equity method investment at NAV per share. The Company measures the carrying value of its privately-held equity method investments by recording its share of the underlying income or loss of these entities.

Unrealized appreciation (depreciation) resulting from changes in fair value of the equity method investments is reflected as a component of other income (expense) in the consolidated statements of operations. The Company evaluates its equity method investments for impairment whenever events or changes in circumstances indicate that the carrying amounts of such investments may not be recoverable.

The carrying amounts of equity method investments are reflected in investments in the consolidated statements of financial condition. As the underlying entities that the Company manages and invests in are, for U.S. GAAP purposes, primarily investment companies which reflect their investments at estimated fair value, the carrying value of the Company’s equity method investments in such entities approximates fair value. The Company evaluates its equity-method investments for impairment whenever events or changes in circumstances indicate that the carrying amounts of such investments may not be recoverable.

F- 9

Medley Management Inc.

Notes to Condensed Consolidated Financial Statements (unaudited)

Investments also include available-for-sale securities which consist of investments in publicly traded common stock. The Company measures the carrying value of its publicly traded investments in available-for-sale securities at the unadjusted closing price as of the valuation date on the primary market or exchange on which they trade. Unrealized appreciation (depreciation) resulting from changes in fair value of available-for-sale securities is recorded in accumulated other comprehensive income, redeemable non-controlling interests and non-controlling interests in Medley LLC. The cost of investments in available-for-sale securities is determined on a specific identification basis. Realized gains (losses) and declines in value judged to be other than temporary, if any, are reported in other income (expenses), net. The Company evaluates its investments in available-for-sale securities for impairment whenever events or changes in circumstances indicate that the carrying amounts of such investments may not be recoverable.

Debt Issuance Costs

Debt issuance costs represent direct costs incurred in conjunction with the establishment of credit facilities and debt refinancing. Debt issuance costs, and the related amortization expense, are adjusted when any prepayments of principal are made to the related outstanding debt. These costs are amortized as an adjustment to interest expense over the term of the related debt.

Adoption of ASU 2015-03

In April 2015, the FASB issued ASU 2015-03, Simplifying the Presentation of Debt Issuance Costs, which requires that debt issuance costs be presented in the balance sheet as a direct deduction from the carrying amount of the related debt liability, consistent with debt discounts. In August 2015, the FASB issued ASU 2015-15, Interest – Imputation of Interest, which updated ASU 2015-03 guidance to state that the SEC staff would not object to an entity deferring and presenting debt issuance costs relating to a line of credit arrangement as an asset and subsequently amortizing the deferred debt issuance costs ratably over the term of the line of credit arrangement, regardless of whether there are any outstanding borrowings on the line of credit agreement.

The Company adopted the new guidance and retrospectively presented debt issuance costs related to its long-term debt as a deduction from the carrying amount of the associated debt on its Consolidated Balance Sheets as of September 30, 2016 and December 31, 2015. The Company continues to present debt issuance costs related to its revolving credit facility as an asset on its Consolidated Balance Sheets as of September 30, 2016 and December 31, 2015. This change did not affect the Company’s consolidated statements of operations, cash flows or changes in equity.

Revenues

Management Fees

Medley provides investment management services to both public and private investment vehicles. Management fees include base management fees, other management fees, and Part I incentive fees, as described below.

Base management fees are calculated based on either (i) the average or ending gross assets balance for the relevant period, (ii) limited partners’ capital commitments to the funds, (iii) invested capital, (iv) NAV or (v) lower of cost or market value of a fund’s portfolio investments. For the private funds, Medley receives base management fees during a specified period of time, which is generally ten years from the initial closing date. However, such termination date may be earlier in certain limited circumstances or later if extended for successive one-year periods, typically up to a maximum of two years. Depending upon the contracted terms of the investment management agreement, management fees are paid either quarterly in advance or quarterly in arrears, and are recognized as earned over the period the services are provided.

Certain management agreements provide for Medley to receive other management fee revenue derived from up front origination fees paid by the portfolio companies of the funds, as well as separately managed accounts. These fees are recognized when Medley becomes entitled to such fees.

Certain management agreements also provide for Medley to receive Part I incentive fee revenue derived from net interest income (excluding gains and losses) above a hurdle rate. Effective January 1, 2016, as it relates to Medley Capital Corporation (“MCC”), these fees are subject to netting against realized and unrealized losses. Part I incentive fees are paid quarterly and are recognized as earned over the period the services are provided.

F- 10

Medley Management Inc.

Notes to Condensed Consolidated Financial Statements (unaudited)

Performance Fees

Performance fees consist principally of the allocation of profits from certain funds and separately managed accounts, to which Medley provides management services. Medley is generally entitled to an allocation of income as a performance fee after returning the invested capital plus a specified preferred return as set forth in each respective agreement. Medley recognizes revenues attributable to performance fees based upon the amount that would be due pursuant to the respective agreement at each period end as if the funds were terminated at that date. Accordingly, the amount recognized reflects Medley’s share of the gains and losses of the associated funds’ underlying investments measured at their current fair values. Performance fee revenue may include reversals of previously recognized performance fees due to a decrease in the net income of a particular fund that results in a decrease of cumulative performance fees earned to date. Since fund return hurdles are cumulative, previously recognized performance fees also may be reversed in a period of appreciation that is lower than the particular fund’s hurdle rate. For the three months ended September 30, 2016, there was no reversal of previously recognized performance fees. For the nine months ended September 30, 2016, the Company reversed $0.4 million of previously recognized performance fees. For the three and nine months ended September 30, 2015, the Company reversed $14.7 million and $18.7 million, respectively, of previously recognized performance fees. As of September 30, 2016, the Company recognized cumulative performance fees of $6.3 million.

Performance fees received in prior periods may be required to be returned by Medley in future periods if the funds’ investment performance declines below certain levels. Each fund is considered separately in this regard and, for a given fund, performance fees can never be negative over the life of a fund. If upon a hypothetical liquidation of a fund’s investments, at their then current fair values, previously recognized and distributed performance fees would be required to be returned, a liability is established for the potential clawback obligation. As of September 30, 2016, the Company had not received any performance fee distributions, except for tax distributions related to the Company’s allocation of net income, which included an allocation of performance fees. Pursuant to the organizational documents of each respective fund, a portion of these tax distributions is subject to clawback. As of September 30, 2016, the Company had accrued $7.1 million for clawback obligations that would need to be paid if the funds were liquidated at fair value as of the end of the reporting period. The Company’s actual obligation, however, would not become payable or realized until the end of a fund’s life.

Other Revenues and Fees

Medley provides administrative services to certain affiliated funds and is reimbursed for direct and allocated expenses incurred in providing such administrative services, as set forth in the respective agreement. These fees are recognized as revenue in the period administrative services are rendered.

Performance Fee Compensation

Medley has issued profit interests in certain subsidiaries to select employees. These profit-sharing arrangements are accounted for under ASC 710, Compensation — General, which requires compensation expense to be measured at fair value at the grant date and expensed over the vesting period, which is usually the period over which the service is provided. The fair value of the profit interests are re-measured at each balance sheet date and adjusted for changes in estimates of cash flows and vesting percentages. The impact of such changes is recorded in the consolidated statements of operations as an increase or decrease to performance fee compensation.

Stock-based Compensation

The Company accounts for stock-based compensation in accordance with ASC 718, Compensation – Stock Compensation. Under the fair value recognition provision of this guidance, stock-based compensation cost is measured at the grant date based on the fair value of the award and is recognized as expense over the requisite service period.

Stock-based compensation expense recognized for the periods presented is based on awards ultimately expected to vest and have been reduced for estimated forfeitures. ASC 718 requires forfeitures to be estimated at the time of grant and revised, if necessary, in subsequent periods if actual forfeitures differ from those estimates. The effect of such change in estimated forfeitures is recognized through a cumulative catch-up adjustment that is included in the period of the change in estimate.

The value of the portion of the award that is ultimately expected to vest on a straight-line basis over the requisite service period is included within compensation and benefits on the Company’s condensed consolidated statements of operations.

Income Taxes

The Company accounts for income taxes using the asset and liability approach, which requires the recognition of tax benefits or expenses for temporary differences between the financial reporting and tax basis of assets and liabilities. A valuation allowance is established when necessary to reduce deferred tax assets to the amounts expected to be realized. The Company also recognizes a tax benefit from uncertain tax positions only if it is “more likely than not” that the position is sustainable based on its technical merits. The Company’s policy is to recognize interest and penalties on uncertain tax positions and other tax matters as a component of income tax expense. For interim periods, the Company accounts for income taxes based on its estimate of the effective tax rate for the year. Discrete items and changes in its estimate of the annual effective tax rate are recorded in the period they occur.

F- 11

Medley Management Inc.

Notes to Condensed Consolidated Financial Statements (unaudited)

Medley Management Inc. is subject to U.S. federal, state and local corporate income taxes on its allocable portion of the income of Medley LLC at prevailing corporate tax rates, which are reflected in the Company’s condensed consolidated financial statements. Medley LLC and its subsidiaries are not subject to federal, state and local corporate income taxes since all income, gains and losses are passed through to its members. However, Medley LLC and its subsidiaries are subject to New York City’s unincorporated business tax, which is included in the Company’s provision for income taxes.

The Company analyzes its tax filing positions in all of the U.S. federal, state and local tax jurisdictions where it is required to file income tax returns, as well as for all open tax years in these jurisdictions. If, based on this analysis, the Company determines that uncertainties in tax positions exist, a liability is established.

Recent Accounting Pronouncements

In May 2014, the FASB issued ASU 2014-09, Revenue from Contracts with Customers (Topic 606), which provides that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for such goods or services. To achieve this core principle, an entity should apply the following steps: (1) identify the contracts with a customer, (2) identify the performance obligations in the contracts, (3) determine the transaction prices, (4) allocate the transaction prices to the performance obligations in the contracts, and (5) recognize revenue when, or as, the entity satisfies a performance obligation. The guidance also requires advanced disclosures regarding the nature, amount, timing and uncertainty of revenue and cash flows arising from an entity’s contracts with customers. In March 2016, the FASB issued ASU 2016-08, Revenue from Contracts with Customers (Topic 606): Principal versus Agent Considerations (Reporting Revenue Gross versus Net), which clarified the implementation guidance on principal versus agent considerations. In April 2016, the FASB issued ASU 2016-10, Revenue from Contracts with Customers (Topic 606): Identifying Performance Obligations and Licensing, which clarified the implementation guidance regarding performance obligations and licensing arrangements. The new standard will become effective for the Company on January 1, 2018, with early application permitted to the effective date of January 1, 2017. The Company is evaluating the effect that ASU 2014-09 will have on its consolidated financial statements and related disclosures. The Company has not yet selected a transition method nor has it determined the effect of the standard on its ongoing financial reporting.

In April 2015, the FASB issued ASU 2015-03, Simplifying the Presentation of Debt Issuance Costs, which requires that debt issuance costs be presented in the balance sheet as a direct deduction from the carrying amount of the related debt liability, consistent with debt discounts. Under previous accounting standards, such costs were reflected as an asset on the Company's consolidated balance sheets. Amortization of the costs continues to be reported as interest expense. The Company implemented the provisions of ASU 2015-03 as of January 1, 2016. As a result of the adoption, $1.7 million of debt issuance costs were reclassified from other assets to debt obligations as of December 31, 2015.

In January 2016, the FASB issued ASU 2016-01, Financial Instruments – Overall: Recognition and Measurement of Financial Assets and Financial Liabilities, which requires that all equity investments (except those accounted for under the equity method of accounting) be measured at fair value with changes in fair value recognized in net income. This guidance eliminates the available-for-sale classification for equity securities with readily determinable fair values. However, companies may elect to measure equity investments that do not have readily determinable fair values at cost minus impairment, if any, plus or minus changes resulting from observable price changes in orderly transactions for an identical or similar investment of the same issuer. This guidance is effective for fiscal years beginning after December 31, 2017. The Company is currently evaluating the impact of adopting this standard on its consolidated financial statements.

In February 2016, the FASB issued ASU 2016-02, Leases (Topic 842). This guidance requires an entity to recognize assets and liabilities arising from a lease for both financing and operating leases, along with additional qualitative and quantitative disclosures. This guidance is effective for fiscal years beginning after December 15, 2018, with early adoption permitted. The Company is currently evaluating the impact of adopting this standard on its consolidated financial statements.

In March 2016, the FASB issued ASU 2016-09, Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting. This guidance simplifies and improves several aspects of the accounting for share-based payment transactions, including the income tax consequences, classification of awards as either equity or liabilities and classification on the statement of cash flows. This guidance is effective for fiscal years beginning after December 31, 2016, with early adoption permitted. The Company is currently evaluating the impact of adopting this standard on its consolidated financial statements.

F- 12

Medley Management Inc.

Notes to Condensed Consolidated Financial Statements (unaudited)

In August 2016, the FASB issued ASU 2016-15, Statement of Cash Flows (Topic 230). This guidance intends to reduce the diversity in practice of how certain cash receipts and cash payments are classified on the statement of cash flows. This guidance is effective for fiscal years beginning after December 15, 2017, with early adoption permitted. The Company is currently evaluating the impact of adopting this standard on its consolidated financial statements.

The Company does not believe any other recently issued, but not yet effective, revisions to authoritative guidance will have a material effect on its consolidated balance sheets, results of operations or cash flows.

3. INVESTMENTS

The components of investments are as follows:

| As of | ||||||||

| September 30, | As of | |||||||

| 2016 | December 31, | |||||||

| (unaudited) | 2015 | |||||||

| (Amounts in thousands) | ||||||||

| Equity method investments, at fair value | $ | 15,159 | $ | 16,360 | ||||

| Available-for-sale securities | 9,114 | - | ||||||

| Total investments, at fair value | $ | 24,273 | $ | 16,360 | ||||

Equity Method Investments

Medley measures the carrying value of its public non-traded equity method investments at NAV per share. Unrealized appreciation (depreciation) resulting from changes in NAV per share of the equity method investments is reflected as a component of other income (expense) in the consolidated statements of operations. The carrying value of the Company’s privately-held equity method investments is determined based on the amounts invested by the Company, adjusted for the equity in earnings or losses of the investee allocated based on the respective underlying agreements, less distributions received.

The Company evaluates its equity method investments for impairment whenever events or changes in circumstances indicate that the carrying amounts of such investments may not be recoverable. During the nine months ended September 30, 2016, the Company assessed that the liquidation value of its investment in CK Pearl Fund was below its carrying value and, that such decline led to an other than temporary impairment. As a result, the Company recorded a $0.5 million loss on its investment in CK Pearl Fund which is included as a component of other income (expenses), net on the condensed consolidated statements of operations. There were no impairment losses recorded during the three months ended September 30, 2016 or during the three and nine months ended September 30, 2015.

As of September 30, 2016 and December 31, 2015, the Company’s carrying value of its equity method investments was $15.2 million and $16.4 million, respectively. Included in this balance was $9.0 million as of September 30, 2016 and December 31, 2015 from the Company’s investment in publicly-held Sierra Income Corporation (“SIC”). The remaining balance as of September 30, 2016 and December 31, 2015 relates primarily to the Company’s investments in CK Pearl Fund, MOF II and Medley Opportunity Fund III LP (“MOF III”).

Available-For-Sale Securities

As of September 30, 2016, the Company’s carrying value of its available-for-sale securities was $9.1 million and consisted of 1,194,547 shares of publicly traded common stock. The Company measures the carrying value of its publicly traded investments in available-for-sale securities at the unadjusted closing price as of the valuation date on the primary market or exchange on which they trade. As of September 30, 2016, the Company recorded less than $0.1 million of cumulative unrealized gains in accumulated other comprehensive income and $0.2 million of cumulative unrealized gains in redeemable non-controlling interests and non-controlling interests in Medley LLC. There were no impairment charges recorded related to the Company’s investments in available-for-sale securities during three and nine months ended September 30, 2016.

F- 13

Medley Management Inc.

Notes to Condensed Consolidated Financial Statements (unaudited)

4. FAIR VALUE MEASUREMENTS

The Company follows ASC 820 for measuring the fair value of investments in available-for-sale securities. Fair value is the price that would be received from the sale of an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. Where available, fair value is based on observable market prices or parameters, or derived from such prices or parameters. Where observable prices or inputs are not available, valuation models are applied. These valuation models involve some level of management estimation and judgement, the degree of which is dependent on the price transparency for the instruments or market and the instruments’ complexity. Financial instruments recorded at fair value in the consolidated financial statements are categorized for disclosure purposes based upon the level of judgment associated with the inputs to the valuation of the investment as of the measurement date. The three levels are defined as follows:

| · | Level I – Valuations based on quoted prices in active markets for identical assets or liabilities at the measurement date. |

| · | Level II – Valuations based on inputs other than quoted prices in active markets included in Level I, which are either directly or indirectly observable at the measurement date. This category includes quoted prices for similar assets or liabilities in non-active markets including bids from third parties for privately held assets or liabilities, and observable inputs other than quoted prices such as yield curves and forward currency rates that are entered directly into valuation models to determine the value of derivatives or other assets or liabilities. |

| · | Level III – Valuations based on inputs that are unobservable and where there is little, if any, market activity at the measurement date. The inputs for the determination of fair value may require significant management judgment or estimation and is based upon management’s assessment of the assumptions that market participants would use in pricing the assets and liabilities. These investments include debt and equity investments in private companies or assets valued using the market or income approach and may involve pricing models whose inputs require significant judgment or estimation because of the absence of any meaningful current market data for identical or similar investments. The inputs in these valuations may include, but are not limited to, capitalization and discount rates, beta and EBITDA multiples. The information may also include pricing information or broker quotes that include a disclaimer that the broker would not be held to such a price in an actual transaction. The non-binding nature of consensus pricing and-or quotes accompanied by disclaimer would result in classification as Level III information, assuming no additional corroborating evidence. |

When determining the fair value of publicly traded equity securities, the Company uses the unadjusted closing price as of the valuation date on the primary market or exchange on which they trade. The Company’s investments in available-for-sale securities are categorized as Level I. As of September 30, 2016, there were no financial instruments classified as Level II or Level III.

A review of fair value hierarchy classifications is conducted on a quarterly basis. Changes in the observability of valuation inputs may result in a reclassification for certain financials assets or liabilities. Reclassifications impacting all levels of the fair value hierarchy are reported as transfers in or out of Level I, II or III category as of the beginning of the quarter in the reclassifications occur. There were no transfers between levels in the fair value hierarchy during the three and nine months ended September 30, 2016.

F- 14

Medley Management Inc.

Notes to Condensed Consolidated Financial Statements (unaudited)

5. OTHER ASSETS

The components of other assets are as follows:

| As of | ||||||||

| September 30, | As of | |||||||

| 2016 | December 31, | |||||||

| (unaudited) | 2015 | |||||||

| (Amounts in thousands) | ||||||||

| Fixed assets, net of accumulated depreciation of $1,716 and $1,667, respectively | $ | 5,221 | $ | 1,708 | ||||

| Security deposits | 1,975 | 3,034 | ||||||

| Administrative fees receivable (Note 10) | 2,019 | 1,654 | ||||||

| Deferred tax assets | 2,337 | 1,659 | ||||||

| Debt issuance costs, net of accumulated amortization of $74 and $48, respectively | 96 | 122 | ||||||

| Due from affiliates (Note 10) | 1,547 | 1,486 | ||||||

| Prepaid expenses and taxes | 3,349 | 2,293 | ||||||

| Other receivables | 1,641 | 1,059 | ||||||

| Total other assets | $ | 18,185 | $ | 13,015 | ||||

6. LOANS PAYABLE

The Company’s loans payable consist of the following:

| As of | ||||||||

| September 30, | As of | |||||||

| 2016 | December 31, | |||||||

| (unaudited) | 2015 | |||||||

| (Amounts in thousands) | ||||||||

| Term loans under the Credit Suisse Term Loan Facility, net of unamortized discount and debt issuance costs of $1,737 and $2,489, respectively | $ | 69,763 | $ | 92,511 | ||||

| Non-recourse promissory notes, net of unamortized discount of $1,566 and $1,953, respectively | 8,434 | 8,360 | ||||||

| Total loans payable | $ | 78,197 | $ | 100,871 | ||||

Credit Suisse Term Loan Facility

On August 14, 2014, the Company entered into a $110.0 million senior secured term loan credit facility (as amended, “Term Loan Facility”) with Credit Suisse AG, Cayman Islands Branch, as administrative agent and collateral agent thereunder, Credit Suisse Securities (USA) LLC, as bookrunner and lead arranger, and the lenders from time-to-time party thereto, which will mature on June 15, 2019.

On May 3, 2016, the Term Loan Facility was amended to permit the issuance of additional indebtedness by the Company with proceeds of such indebtedness to be used to prepay loans outstanding under the Term Loan Facility. The amendment also provided for the creation and funding of certain future funds, as well as for certain other technical changes to the Term Loan Facility.