UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

for the quarterly period ended

OR

for the transition period from _______ to _______.

Commission File Number:

(Exact Name of Registrant as Specified in Its Charter)

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

| | ||

| (Address of Principal Executive Offices) | (Zip Code) |

(Registrant’s Telephone Number, Including Area Code)

N/A

(Former Name, Former Address and Former Fiscal Year, if Changed Since Last Report)

Securities Registered Pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol(s) | Name Of Each Exchange On Which Registered | ||

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months

(or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days. ☒

Indicate by check mark whether the registrant

has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405

of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided in Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant

is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐

Yes

Securities Registered Pursuant to Section 12(b) of the Act:

The registrant

had

The registrant

had

AMPLIFY COMMODITY TRUST

Table of Contents

i

Part I.

INTERIM FINANCIAL INFORMATION

Item 1. Interim Financial Statements.

Item 1. Interim Financial Statements.

Index to Interim Financial Statements

1

AMPLIFY COMMODITY TRUST

Combined Statements of Assets and Liabilities

March 31, 2024 (Unaudited)

| BREAKWAVE | BREAKWAVE | |||||||||||

| DRY BULK SHIPPING | TANKER SHIPPING | |||||||||||

| ETF | ETF | COMBINED | ||||||||||

| Assets | ||||||||||||

| Investment in securities, at fair value (cost $ | $ | $ | $ | |||||||||

| Segregated cash held by broker | ||||||||||||

| Receivable on open futures contracts | ||||||||||||

| Interest receivable | ||||||||||||

| Receivable for capital shares sold | ||||||||||||

| Total assets | ||||||||||||

| Liabilities | ||||||||||||

| Due to Sponsor | ||||||||||||

| Payable on open futures contracts | ||||||||||||

| Other accrued expenses | ||||||||||||

| Payable for fund shares redeemed | ||||||||||||

| Total liabilities | ||||||||||||

| Net Assets | $ | $ | $ | |||||||||

| Shares outstanding (unlimited authorized) | ||||||||||||

| Net asset value per share | $ | |||||||||||

| Market value per share | $ | |||||||||||

See accompanying notes to unaudited interim financial statements.

2

AMPLIFY COMMODITY TRUST

Combined Statements of Assets and Liabilities

June 30, 2023

| BREAKWAVE DRY BULK SHIPPING | BREAKWAVE TANKER SHIPPING | |||||||||||

| ETF | ETF | COMBINED | ||||||||||

| Assets | ||||||||||||

| Investment in securities, at fair value (cost $ | $ | $ | $ | |||||||||

| Segregated cash held by broker | ||||||||||||

| Receivable on open futures contracts | ||||||||||||

| Interest receivable | ||||||||||||

| Total assets | ||||||||||||

| Liabilities | ||||||||||||

| Due to Sponsor | ||||||||||||

| Payable on open futures contracts | ||||||||||||

| Other accrued expenses | ||||||||||||

| Total liabilities | ||||||||||||

| Net Assets | $ | $ | $ | |||||||||

| Shares outstanding (unlimited authorized) | ||||||||||||

| Net asset value per share | $ | $ | ||||||||||

| Market value per share | $ | $ | ||||||||||

See accompanying notes to unaudited interim financial statements.

3

AMPLIFY COMMODITY TRUST

Schedules of Investments

March 31, 2024 (Unaudited)

| BREAKWAVE | BREAKWAVE | |||||||||||

| DRY BULK SHIPPING ETF | TANKER SHIPPING ETF | COMBINED | ||||||||||

| MONEY MARKET FUNDS - | ||||||||||||

| Invesco Government & Agency Portfolio - Institutional Class, | $ | $ | $ | |||||||||

| TOTAL MONEY MARKET FUNDS (Cost $ | ||||||||||||

| Total Investments (Cost $ | ||||||||||||

| Other Assets in Excess of Liabilities - | ||||||||||||

| TOTAL NET ASSETS - | $ | $ | $ | |||||||||

| (a) |

| (b) |

| BREAKWAVE DRY BULK SHIPPING ETF | Unrealized | AMPLIFY | ||||||

| Futures Contracts | Appreciation/ | COMMODITY | ||||||

| March 31, 2024 | (Depreciation) | TRUST | ||||||

| Baltic Capesize Time Charter Expiring | ||||||||

| April 30, 2024 (Underlying Face Amount at Market Value - $ | $ | ( | ) | $ | ( | ) | ||

| Baltic Capesize Time Charter Expiring | ||||||||

| May 31, 2024 (Underlying Face Amount at Market Value - $ | ||||||||

| Baltic Capesize Time Charter Expiring | ||||||||

| June 30, 2024 (Underlying Face Amount at Market Value - $ | ||||||||

| Baltic Exchange Panamax T/C Average Shipping Route Index Expiring | ||||||||

| April 30, 2024 (Underlying Face Amount at Market Value - $ | ( | ) | ( | ) | ||||

| Baltic Exchange Panamax T/C Average Shipping Route Index Expiring | ||||||||

| May 31, 2024 (Underlying Face Amount at Market Value - $ | ||||||||

| Baltic Exchange Panamax T/C Average Shipping Route Index Expiring | ||||||||

| June 30, 2024 (Underlying Face Amount at Market Value - $ | ||||||||

| Baltic Exchange Supramax T/C Average Shipping Route Expiring | ||||||||

| April 30, 2024 (Underlying Face Amount at Market Value - $ | ( | ) | ( | ) | ||||

| Baltic Exchange Supramax T/C Average Shipping Route Expiring | ||||||||

| May 31, 2024 (Underlying Face Amount at Market Value - $ | ( | ) | ( | ) | ||||

| Baltic Exchange Supramax T/C Average Shipping Route Expiring | ||||||||

| June 30, 2024 (Underlying Face Amount at Market Value - $ | ( | ) | ( | ) | ||||

| $ | $ | |||||||

| BREAKWAVE TANKER SHIPPING ETF | Unrealized | AMPLIFY | ||||||

| Futures Contracts | Appreciation/ | COMMODITY | ||||||

| March 31, 2024 | (Depreciation) | TRUST | ||||||

| Baltic Freight Route Middle East Gulf to China Expiring | ||||||||

| April 30, 2024 (Underlying Face Amount at Market Value - $ | $ | $ | ||||||

| Baltic Freight Route Middle East Gulf to China Expiring | ||||||||

| Baltic Freight Route Middle East Gulf to China Expiring | ||||||||

| June 30, 2024 (Underlying Face Amount at Market Value - $ | ( | ) | ( | ) | ||||

| Baltic Freight Route Middle East Gulf to China Expiring | ||||||||

| April 30, 2024 (Underlying Face Amount at Market Value - $ | ||||||||

| Baltic Freight Route Middle East Gulf to China Expiring | ||||||||

| May 31, 2024 (Underlying Face Amount at Market Value - $ | ||||||||

| Baltic Freight Route Middle East Gulf to China Expiring | ||||||||

| June 30, 2024 (Underlying Face Amount at Market Value - $ | ( | ) | ( | ) | ||||

| $ | ( | ) | $ | ( | ) | |||

See accompanying notes to unaudited interim financial statements.

4

AMPLIFY COMMODITY TRUST

Schedule of Investments

June 30, 2023

| BREAKWAVE DRY BULK SHIPPING | BREAKWAVE TANKER SHIPPING | |||||||||||

| ETF | ETF | COMBINED | ||||||||||

| MONEY MARKET FUNDS - | ||||||||||||

| First American US Treasury Obligations Fund, Class X, | $ | $ | $ | |||||||||

| TOTAL MONEY MARKET FUNDS (Cost $ | ||||||||||||

| Total Investments (Cost $ | ||||||||||||

| Other Assets in Excess of Liabilities - | ||||||||||||

| TOTAL NET ASSETS - | $ | $ | $ | |||||||||

| (a) | Annualized seven-day yield as of June 30, 2023. |

| (b) | $35,323,736 and $2,879,954, respectively, of cash is pledged as collateral for futures contracts. |

| BREAKWAVE DRY BULK SHIPPING ETF | Unrealized | AMPLIFY | ||||||

| Futures Contracts | Appreciation/ | COMMODITY | ||||||

| June 30, 2023 | (Depreciation) | TRUST | ||||||

| Baltic Exchange Panamax T/C Average Shipping Route Index Expiring | ||||||||

| July 28, 2023 (Underlying Face Amount at Market Value - $ | $ | ( | ) | $ | ( | ) | ||

| Baltic Exchange Panamax T/C Average Shipping Route Index Expiring | ||||||||

| August 25, 2023 (Underlying Face Amount at Market Value - $ | ( | ) | ( | ) | ||||

| Baltic Exchange Panamax T/C Average Shipping Route Index Expiring | ||||||||

| September 29, 2023 (Underlying Face Amount at Market Value - $ | ( | ) | ( | ) | ||||

| Baltic Exchange Supramax T/C Average Shipping Route Expiring | ||||||||

| July 28, 2023 (Underlying Face Amount at Market Value - $ | ( | ) | ( | ) | ||||

| Baltic Exchange Supramax T/C Average Shipping Route Expiring | ||||||||

| August 25, 2023 (Underlying Face Amount at Market Value - $ | ( | ) | ( | ) | ||||

| Baltic Exchange Supramax T/C Average Shipping Route Expiring | ||||||||

| September 29, 2023 (Underlying Face Amount at Market Value - $ | ( | ) | ( | ) | ||||

| Baltic Capesize Time Charter Expiring July 29, 2022 | ||||||||

| July 28, 2023 (Underlying Face Amount at Market Value - $ | ( | ) | ( | ) | ||||

| Baltic Capesize Time Charter Expiring August 26, 2022 | ||||||||

| August 25, 2023 (Underlying Face Amount at Market Value - $ | ( | ) | ( | ) | ||||

| Baltic Capesize Time Charter Expiring September 23, 2022 | ||||||||

| September 29, 2023 (Underlying Face Amount at Market Value - $ | ( | ) | ( | ) | ||||

| $ | ( | ) | $ | ( | ) | |||

| BREAKWAVE TANKER SHIPPING ETF | Unrealized | AMPLIFY | ||||||

| Futures Contracts | Appreciation/ | COMMODITY | ||||||

| June 30, 2023 | (Depreciation) | TRUST | ||||||

| Baltic Freight Route Middle East Gulf to China | ||||||||

| July 28, 2023 (Underlying Face Amount at Market Value - $ |

$ | |

$ | |

||||

| Baltic Freight Route Middle East Gulf to China | ||||||||

| August 25, 2023 (Underlying Face Amount at Market Value - $ |

||||||||

| Baltic Freight Route Middle East Gulf to China | ||||||||

| September 29, 2023 (Underlying Face Amount at Market Value - $ |

|

|

||||||

| Baltic Freight RouteWest Africa to UK Continent | ||||||||

| July 28, 2023 (Underlying Face Amount at Market Value - $ |

|

|||||||

| Baltic Freight RouteWest Africa to UK Continent | ||||||||

| August 25, 2023 (Underlying Face Amount at Market Value - $ |

|

|

||||||

| Baltic Freight RouteWest Africa to UK Continent | ||||||||

| September 29, 2023 (Underlying Face Amount at Market Value - $ |

|

|

||||||

| $ | $ | |||||||

See accompanying notes to unaudited interim financial statements.

5

AMPLIFY COMMODITY TRUST

Combined Statements of Operations

Three Months Ended March 31, 2024 (Unaudited)

| BREAKWAVE DRY BULK | BREAKWAVE TANKER | |||||||||||

| SHIPPING ETF | SHIPPING ETF | COMBINED | ||||||||||

| Investment Income | ||||||||||||

| Interest | $ | $ | $ | |||||||||

| Expenses | ||||||||||||

| Sponsor fee | ||||||||||||

| CTA fee | ||||||||||||

| Audit fees | ||||||||||||

| Tax preparation fees | ||||||||||||

| Admin/accounting/custodian/transfer agent fees | ||||||||||||

| Legal fees | ||||||||||||

| Chief Compliance Officer fees | ||||||||||||

| Principal Financial Officer fees | ||||||||||||

| Regulatory reporting fees | ||||||||||||

| Brokerage commissions | ||||||||||||

| Distribution fees | ||||||||||||

| NJ Filing fees | ( | ) | ||||||||||

| Insurance expense | ||||||||||||

| Listing and calculation agent fees | ||||||||||||

| Marketing expenses | ||||||||||||

| Other expenses | ||||||||||||

| Wholesale support fees | ||||||||||||

| Total Expenses | ||||||||||||

| Less: Waiver of CTA fee | ( | ) | ( | ) | ||||||||

| Less: Expenses absorbed by Sponsor | ( | ) | ||||||||||

| Net Expenses | ||||||||||||

| Net Investment Income (Loss) | ( | ) | ( | ) | ( | ) | ||||||

| Net Realized and Unrealized Gain (Loss) on Investment Activity | ||||||||||||

| Net Realized Gain (Loss) on | ||||||||||||

| Investments and futures contracts | ||||||||||||

| Change in Unrealized Gain (Loss) on | ||||||||||||

| Investments and futures contracts | ( | ) | ( | ) | ||||||||

| Net realized and unrealized gain (loss) | ||||||||||||

| Net income (loss) | $ | $ | $ | |||||||||

See accompanying notes to unaudited interim financial statements.

6

AMPLIFY COMMODITY TRUST

Combined Statements of Operations

Three Months Ended March 31, 2023 (Unaudited)

| BREAKWAVE DRY BULK | BREAKWAVE TANKER | |||||||||||

| SHIPPING ETF | SHIPPING ETF | COMBINED | ||||||||||

| Investment Income | ||||||||||||

| Interest | $ | $ | $ | |||||||||

| Expenses | ||||||||||||

| Sponsor fee | ||||||||||||

| CTA fee | ||||||||||||

| Audit fees | ||||||||||||

| Tax preparation fees | ||||||||||||

| Admin/accounting/custodian/transfer agent fees | ||||||||||||

| Legal fees | ||||||||||||

| Chief Compliance Officer fees | ||||||||||||

| Principal Financial Officer fees | ||||||||||||

| Regulatory reporting fees | ||||||||||||

| Brokerage commissions | ||||||||||||

| Distribution fees | ||||||||||||

| NJ Filing fees | ||||||||||||

| Insurance expense | ||||||||||||

| Listing and calculation agent fees | ||||||||||||

| Marketing expenses | ||||||||||||

| Other expenses | ||||||||||||

| Website Support and Marketing Materials | ||||||||||||

| Printing and Postage | ||||||||||||

| Wholesale support fees | ||||||||||||

| Total Expenses | ||||||||||||

| Less: Waiver of CTA fee | ( | ) | ( | ) | ||||||||

| Less: Expenses absorbed by Sponsor | ||||||||||||

| Net Expenses | ||||||||||||

| Net Investment Income (Loss) | ( | ) | ( | ) | ||||||||

| Net Realized and Unrealized Gain (Loss) on Investment Activity | ||||||||||||

| Net Realized Gain (Loss) on | ||||||||||||

| Investments and futures contracts | ||||||||||||

| Change in Unrealized Gain (Loss) on | ||||||||||||

| Investments and futures contracts | ||||||||||||

| Net realized and unrealized gain (loss) | ||||||||||||

| Net income (loss) | $ | $ | $ | |||||||||

See accompanying notes to unaudited interim financial statements.

7

AMPLIFY COMMODITY TRUST

Combined Statements of Operations

Nine Months Ended March 31, 2024 (Unaudited)

| BREAKWAVE DRY BULK | BREAKWAVE TANKER | |||||||||||

| SHIPPING ETF | SHIPPING ETF | COMBINED | ||||||||||

| Investment Income | ||||||||||||

| Interest | $ | $ | $ | |||||||||

| Expenses | ||||||||||||

| Sponsor fee | ||||||||||||

| CTA fee | ||||||||||||

| Audit fees | ||||||||||||

| Tax preparation fees | ||||||||||||

| Admin/accounting/custodian/transfer agent fees | ||||||||||||

| Legal fees | ||||||||||||

| Chief Compliance Officer fees | ||||||||||||

| Principal Financial Officer fees | ||||||||||||

| Regulatory reporting fees | ||||||||||||

| Brokerage commissions | ||||||||||||

| Distribution fees | ||||||||||||

| NJ Filing fees | ||||||||||||

| Insurance expense | ||||||||||||

| Listing and calculation agent fees | ||||||||||||

| Marketing expenses | ||||||||||||

| Other expenses | ||||||||||||

| Website Support and Marketing Materials | ||||||||||||

| Printing and Postage | ||||||||||||

| Wholesale support fees | ||||||||||||

| Total Expenses | ||||||||||||

| Less: Waiver of CTA fee | ( | ) | ( | ) | ||||||||

| Less: Expenses absorbed by Sponsor | ( | ) | ||||||||||

| Net Expenses | ||||||||||||

| Net Investment Income (Loss) | ( | ) | ( | ) | ( | ) | ||||||

| Net Realized and Unrealized Gain (Loss) on Investment Activity | ||||||||||||

| Net Realized Gain (Loss) on | ||||||||||||

| Investments and futures contracts | ||||||||||||

| Change in Unrealized Gain (Loss) on | ||||||||||||

| Investments and futures contracts | ( | ) | ||||||||||

| Net realized and unrealized gain (loss) | ||||||||||||

| Net income (loss) | $ | $ | ( | ) | $ | |||||||

See accompanying notes to unaudited interim financial statements.

8

AMPLIFY COMMODITY TRUST

Combined Statements of Operations

Nine Months Ended March 31, 2023 (Unaudited)

| BREAKWAVE DRY BULK | BREAKWAVE TANKER | |||||||||||

| SHIPPING ETF | SHIPPING ETF | COMBINED | ||||||||||

| Investment Income | ||||||||||||

| Interest | $ | $ | $ | |||||||||

| Expenses | ||||||||||||

| Sponsor fee | ||||||||||||

| CTA fee | ||||||||||||

| Audit fees | ||||||||||||

| Tax preparation fees | ||||||||||||

| Admin/accounting/custodian/transfer agent fees | ||||||||||||

| Legal fees | ||||||||||||

| Chief Compliance Officer fees | ||||||||||||

| Principal Financial Officer fees | ||||||||||||

| Regulatory reporting fees | ||||||||||||

| Brokerage commissions | ||||||||||||

| Distribution fees | ||||||||||||

| NJ Filing fees | ||||||||||||

| Insurance expense | ||||||||||||

| Listing and calculation agent fees | ||||||||||||

| Marketing expenses | ||||||||||||

| Other expenses | ||||||||||||

| Website Support and Marketing Materials | ||||||||||||

| Printing and Postage | ||||||||||||

| Wholesale support fees | ||||||||||||

| Interest expense | ||||||||||||

| Total Expenses | ||||||||||||

| Less: Waiver of CTA fee | ( | ) | ( | ) | ||||||||

| Less: Expenses absorbed by Sponsor | ||||||||||||

| Net Expenses | ||||||||||||

| Net Investment Income (Loss) | ( | ) | ( | ) | ||||||||

| Net Realized and Unrealized Gain (Loss) on Investment Activity | ||||||||||||

| Net Realized Gain (Loss) on | ||||||||||||

| Investments and futures contracts | ( | ) | ( | ) | ||||||||

| Change in Unrealized Gain (Loss) on | ||||||||||||

| Investments and futures contracts | ||||||||||||

| Net realized and unrealized gain (loss) | ||||||||||||

| Net income (loss) | $ | $ | $ | |||||||||

See accompanying notes to unaudited interim financial statements.

9

AMPLIFY COMMODITY TRUST

Combined Statements of Changes in Net Assets

Three Months Ended March 31, 2024 (Unaudited)

| BREAKWAVE DRY BULK | BREAKWAVE TANKER | |||||||||||

| SHIPPING ETF | SHIPPING ETF | COMBINED | ||||||||||

| Net Assets at Beginning of Period | $ | $ | $ | |||||||||

| Increase (decrease) in Net Assets from share transactions | ||||||||||||

| Addition of | ||||||||||||

| Redemption of | ( | ) | ( | ) | ( | ) | ||||||

| Net Increase (decrease) in Net Assets from share transactions | ( | ) | ( | ) | ||||||||

| Increase (decrease) in Net Assets from operations | ||||||||||||

| Net investment loss | ( | ) | ( | ) | ( | ) | ||||||

| Net realized gain (loss) | ||||||||||||

| Change in net unrealized gain (loss) | ( | ) | ( | ) | ||||||||

| Net Increase (decrease) in Net Assets from operations | ||||||||||||

| Net Assets at End of Period | $ | $ | $ | |||||||||

See accompanying notes to unaudited interim financial statements.

10

AMPLIFY COMMODITY TRUST

Statements of Changes in Net Assets

Three Months Ended March 31, 2023 (Unaudited)

| BREAKWAVE DRY BULK | BREAKWAVE TANKER | |||||||||||

| SHIPPING ETF | SHIPPING ETF | COMBINED | ||||||||||

| Net Assets at Beginning of Period | $ | $ | $ | |||||||||

| Increase (decrease) in Net Assets from share transactions | ||||||||||||

| Addition of | ||||||||||||

| Redemption of | ( | ) | ( | ) | ||||||||

| Net Increase (decrease) in Net Assets from share transactions | ||||||||||||

| Increase (decrease) in Net Assets from operations | ||||||||||||

| Net investment loss | ( | ) | ( | ) | ||||||||

| Net realized gain (loss) | ||||||||||||

| Change in net unrealized gain (loss) | ||||||||||||

| - | ||||||||||||

| Net Increase (decrease) in Net Assets from operations | ||||||||||||

| - | ||||||||||||

| Net Assets at End of Period | $ | $ | ||||||||||

See accompanying notes to unaudited interim financial statements.

11

AMPLIFY COMMODITY TRUST

Combined Statements of Changes in Net Assets

Nine Months Ended March 31, 2024 (Unaudited)

| BREAKWAVE DRY BULK | BREAKWAVE TANKER | |||||||||||

| SHIPPING ETF | SHIPPING ETF | COMBINED | ||||||||||

| Net Assets at Beginning of Period | $ | $ | $ | |||||||||

| Increase (decrease) in Net Assets from share transactions | ||||||||||||

| Addition of | ||||||||||||

| Redemption of | ( | ) | ( | ) | ( | ) | ||||||

| Net Increase (decrease) in Net Assets from share transactions | ( | ) | ( | ) | ( | ) | ||||||

| Increase (decrease) in Net Assets from operations | ||||||||||||

| Net investment loss | ( | ) | ( | ) | ( | ) | ||||||

| Net realized gain (loss) | ||||||||||||

| Change in net unrealized gain (loss) | ( | ) | ||||||||||

| Net Increase (decrease) in Net Assets from operations | ( | ) | ||||||||||

| Net Assets at End of Period | $ | $ | $ | |||||||||

See accompanying notes to unaudited interim financial statements.

12

AMPLIFY COMMODITY TRUST

Combined Statements of Changes in Net Assets

Nine Months Ended March 31, 2023 (Unaudited)

| BREAKWAVE DRY BULK | BREAKWAVE TANKER | |||||||||||

| SHIPPING ETF | SHIPPING ETF | COMBINED | ||||||||||

| Net Assets at Beginning of Period | $ | $ | $ | |||||||||

| Increase (decrease) in Net Assets from share transactions | ||||||||||||

| Addition of | ||||||||||||

| Redemption of | ( | ) | ( | ) | ||||||||

| Net Increase (decrease) in Net Assets from share transactions | ||||||||||||

| Increase (decrease) in Net Assets from operations | ||||||||||||

| Net investment loss | ( | ) | ( | ) | ||||||||

| Net realized gain (loss) | ( | ) | ( | ) | ||||||||

| Change in net unrealized gain (loss) | ||||||||||||

| - | ||||||||||||

| Net Increase (decrease) in Net Assets from operations | ||||||||||||

| - | ||||||||||||

| Net Assets at End of Period | $ | $ | ||||||||||

See accompanying notes to unaudited interim financial statements.

13

AMPLIFY COMMODITY TRUST

Combined Statements of Cash Flows

Nine Months Ended March 31, 2024 (Unaudited)

| BREAKWAVE DRY BULK | BREAKWAVE TANKER | |||||||||||

| SHIPPING ETF | SHIPPING ETF | COMBINED | ||||||||||

| Cash flows provided by (used in) operating activities | ||||||||||||

| Net income (loss) | $ | $ | ( | ) | $ | |||||||

| Adjustments to reconcile net income (loss) to net cash provided by (used in) operating activities: | ||||||||||||

| Net realized loss (gain) on investments | ( | ) | ( | ) | ( | ) | ||||||

| Change in net unrealized loss (gain) on investments | ( | ) | ( | ) | ||||||||

| Change in operating assets and liabilities: | ||||||||||||

| Sale (Purchase) of investments, net | ||||||||||||

| Increase in interest receivable | ( | ) | ||||||||||

| Increase in receivable on open futures contracts | ( | ) | ( | ) | ||||||||

| Decrease in payable on open futures contracts | ( | ) | ||||||||||

| Decrease in receivable for Fund shares sold | ( | ) | ( | ) | ||||||||

| Increase in due to sponsor | ( | ) | ||||||||||

| Decrease in other accrued expenses | ( | ) | ||||||||||

| Net cash provided by operating activities | ||||||||||||

| Cash flows from financing activities | ||||||||||||

| Proceeds from sale of shares | ||||||||||||

| Paid on redemption of shares | ( | ) | ( | ) | ( | ) | ||||||

| Net cash used in financing activities | ( | ) | ( | ) | ( | ) | ||||||

| Net increase (decrease) in cash and restricted cash | ||||||||||||

| Cash and restricted cash, beginning of period | ||||||||||||

| Cash and restricted cash, end of period | $ | $ | $ | |||||||||

| The following table provides a reconciliation of cash and restricted cash reported within the Statement of Assets and Liabilities that sum to the total of such amounts shown on the Statement of Cash Flows. | ||||||||||||

| Cash | $ | $ | $ | |||||||||

| Segregated cash held by broker | $ | $ | $ | |||||||||

| Total cash and restricted cash as shown on the statement of cash flows | $ | $ | $ | |||||||||

See accompanying notes to unaudited interim financial statements.

14

AMPLIFY COMMODITY TRUST

Combined Statements of Cash Flows

Nine Months Ended March 31, 2023 (Unaudited)

| BREAKWAVE DRY BULK | BREAKWAVE TANKER | |||||||||||

| SHIPPING ETF | SHIPPING ETF | COMBINED | ||||||||||

| Cash flows provided by (used in) operating activities | ||||||||||||

| Net income (loss) | $ | $ | $ | |||||||||

| Adjustments to reconcile net income (loss) to net cash provided by (used in) operating activities: | ||||||||||||

| Net realized loss (gain) on investments | ||||||||||||

| Change in net unrealized loss (gain) on investments | ( | ) | ( | ) | ||||||||

| Change in operating assets and liabilities: | ||||||||||||

| Sale (Purchase) of investments, net | ( | ) | ( | ) | ||||||||

| Increase in interest receivable | ( | ) | ( | ) | ||||||||

| Increase in receivable on open futures contracts | ( | ) | ( | ) | ||||||||

| Decrease in payable on open futures contracts | ( | ) | ( | ) | ||||||||

| Decrease in receivable for Fund shares sold | ||||||||||||

| Increase in due to sponsor | ||||||||||||

| Decrease in other accrued expenses | ( | ) | ( | ) | ||||||||

| Net cash used in operating activities | ( | ) | ( | ) | ||||||||

| Cash flows from financing activities | ||||||||||||

| Proceeds from sale of shares | ||||||||||||

| Paid on redemption of shares | ( | ) | ( | ) | ||||||||

| Net cash provided by financing activities | ||||||||||||

| Net increase (decrease) in cash and restricted cash | ( | ) | ( | ) | ||||||||

| Cash and restricted cash, beginning of period | ||||||||||||

| Cash and restricted cash, end of period | $ | $ | $ | |||||||||

| The following table provides a reconciliation of cash and restricted cash reported within the Statement of Assets and Liabilities that sum to the total of such amounts shown on the Statement of Cash Flows. | ||||||||||||

| Cash | $ | $ | $ | |||||||||

| Segregated cash held by broker | ||||||||||||

| Total cash and restricted cash as shown on the statement of cash flows | $ | $ | $ | |||||||||

See accompanying notes to unaudited interim financial statements.

15

Amplify Commodity Trust

(Formerly, ETF Managers Group Commodity Trust I)

Notes to Interim Combined Financial Statements

March 31, 2024 (unaudited)

(1) Organization

Amplify Commodity Trust (formerly, ETF Managers Group Commodity Trust I) (the “Trust”) was organized as a Delaware statutory trust on July 23, 2014. Effective after the close of trading on February 14, 2024, ETF Managers Capital LLC, as the prior sponsor and commodity pool operator (the “Former Sponsor”) of the Trust, entered into an agreement (the “Transfer Agreement”) to resign as Sponsor to the Trust and transfer its role as the Trust’s sponsor to Amplify Investments LLC (“the Sponsor.”) Under the terms of the Transfer Agreement, the Former Sponsor no longer has any involvement in the operations, management or marketing of the Fund. In connection with this change of Sponsor, Trust changed its name from the ETF Managers Group Commodity Trust I to the Amplify Commodity Trust. The Trust is a series trust formed pursuant to the Delaware Statutory Trust Act and currently consists of two separate series. BREAKWAVE DRY BULK SHIPPING ETF (“BDRY”), is the first series of the Trust and is a commodity pool that continuously issues shares of beneficial interest that may be purchased and sold on the NYSE Arca. The second series of the Trust, BREAKWAVE TANKER SHIPPING ETF (“BWET”), each a “Fund” and together with BDRY, the “Funds”), is also a commodity pool that continuously issues shares of beneficial interest that may be purchased and sold on the NYSE Arca. The Funds are managed and controlled by the Sponsor, a Delaware limited liability company. The Sponsor is registered with the Commodity Futures Trading Commission (“CFTC”) as a “commodity pool operator” (“CPO”) and is a member of the National Futures Trading Association (“NFA”). Breakwave Advisors, LLC (“Breakwave”) is registered as a “commodity trading advisor” (“CTA”) with the CFTC and serves as the Funds commodity trading advisor.

BDRY commenced investment operations on March 22, 2018. BDRY commenced trading on the NYSE Arca on March 22, 2018 and trades under the symbol “BDRY.”

BDRY’s investment objective is to provide investors with exposure to the daily change in the price of dry bulk freight futures, before expenses and liabilities of BDRY, by tracking the performance of a portfolio (the “BDRY Benchmark Portfolio”) consisting of a three-month strip of the nearest calendar quarter of futures contracts on specified indexes (each a “Reference Index”) that measure rates for shipping dry bulk freight (“Freight Futures”). Each Reference Index is published each United Kingdom business day by the London-based Baltic Exchange Ltd. (the “Baltic Exchange”) and measures the charter rate for shipping dry bulk freight in a specific size category of cargo ship – Capesize, Panamax or Supramax. The three Reference Indexes are as follows:

| ● | Capesize: the Capesize 5TC Index; |

| ● | Panamax: the Panamax 4TC Index; and |

| ● | Supramax: the Supramax 6TC Index. |

The value of the Capesize 5TC Index is disseminated at 11:00 a.m., London Time and the value of the Panamax 4TC Index and the Supramax 6TC Index each is disseminated at 1:00 p.m., London Time. The Reference Index information disseminated by the Baltic Exchange also includes the components and value of each component in each Reference Index. Such Reference Index information also is widely disseminated by Reuters and/or other major market data vendors.

BDRY seeks to achieve its investment objective by investing substantially all of its assets in the Freight Futures currently constituting the BDRY Benchmark Portfolio. The BDRY Benchmark Portfolio includes all existing positions to maturity and settles them in cash. During any given calendar quarter, the BDRY Benchmark Portfolio progressively increases its positions to the next calendar quarter three-month strip, thus maintaining constant exposure to the Freight Futures market as positions mature.

16

Amplify Commodity Trust

(Formerly, ETF Managers Group Commodity Trust I)

Notes to Interim Combined Financial Statements

March 31, 2024 (unaudited)

(1) Organization - Continued

The BDRY Benchmark Portfolio maintains long-only

positions in Freight Futures. The BDRY Benchmark Portfolio includes a combination of Capesize, Panamax and Supramax Freight Futures. More

specifically, the BDRY Benchmark Portfolio includes

When establishing positions in Freight Futures,

BDRY will be required to deposit initial margin with a value of approximately

BDRY was created to provide investors with a cost-effective and convenient way to gain exposure to daily changes in the price of Freight Futures. BDRY is intended to be used as a diversification opportunity as part of a complete portfolio, not a complete investment program.

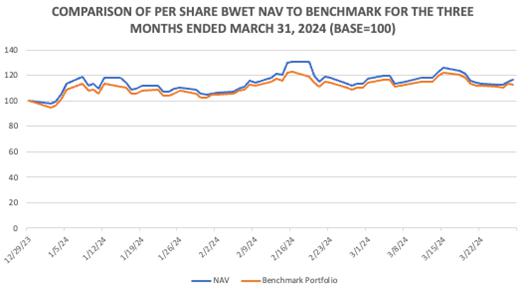

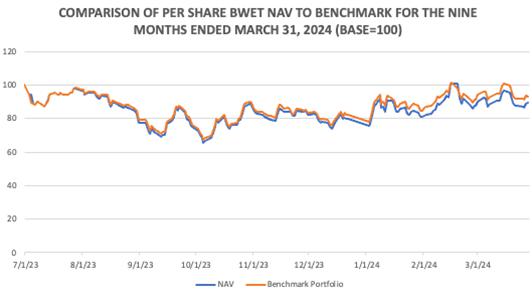

The Fund will incur certain expenses in connection with its operations. The Fund will hold cash or cash equivalents such as U.S. Treasuries or other high credit quality, short-term fixed-income or similar securities for direct investment or as collateral for the Freight futures and for other liquidity purposes and to meet redemptions that may be necessary on an ongoing basis. These expenses and income from the cash and cash equivalent holdings may cause imperfect correlation between changes in the Fund’s net asset value (“NAV”) and changes in the Benchmark Portfolio, because the Benchmark Portfolio does not reflect expenses or income.

The Fund seeks to trade its positions prior to maturity; accordingly, natural market forces may cost the Fund while rebalancing. Each time the Fund seeks to reconstitute its positions, barring movement in the underlying securities, the futures and option prices may be higher or lower. Such differences in price, barring a movement in the price of the underlying security, will constitute “roll yield” and may inhibit the Fund’s ability to achieve its investment objective.

Several factors determine the total return from investing in a futures contract position. One factor that impacts the total return that will result from investing in near month futures contracts and “rolling” those contracts forward each month is the price relationship between the current near month contract and the next month contract.

The CTA will close existing positions when it determines it would be appropriate to do so and reinvest the proceeds in other positions. Positions may also be closed out to meet orders for redemption baskets.

BWET commenced investment operations on May 3, 2023. BWET commenced trading on NYSE Arca on May 3, 2023 and trades under the symbol “BWET.”

BWET’s investment objective is to provide investors with exposure to the daily change in the price of crude oil tanker freight futures, before expenses and liabilities of the Fund, by tracking the performance of a portfolio (the “BWET Benchmark Portfolio”) mainly consisting of the nearest calendar quarter of futures contracts on specified indexes (each a “Reference Index”) that measure prices for shipping crude oil (“Freight Futures”). Freight Futures reflect market expectations for the future cost of transporting crude oil. Each Reference Index is published each United Kingdom business day by the London-based Baltic Exchange Ltd. (the “Baltic Exchange”) and measures the charter rate for crude oil in a specific size category of cargo ship and for a specific route. The two Reference Indexes are as follows:

| ● | The TD3C Index: Persian Gulf to China, 270,000mt cargo (Very Large Crude Carrier or VLCC tankers); |

| ● | The TD20 Index: West Africa to Europe, 130,000mt cargo (Suezmax Tankers) |

17

Amplify Commodity Trust

(Formerly, ETF Managers Group Commodity Trust I)

Notes to Interim Combined Financial Statements

March 31, 2024 (unaudited)

(1) Organization - Continued

The value of the TD3C Index and the TD20 Index is disseminated at 4:00 p.m. London Time by the Baltic Exchange. Such Reference Index information also is widely disseminated by Reuters, Bloomberg and/or other major market data vendors.

The Fund seeks to achieve its investment objective

by investing substantially all of its assets in the Freight Futures currently constituting the BWET Benchmark Portfolio. The BWET Benchmark

Portfolio includes a combination of TD3C and TD20 Freight Futures. More specifically, the Benchmark Portfolio includes

The BWET Benchmark Portfolio does not include and BWET does not invest in swaps, non-cleared freight forwards or other over-the-counter derivative instruments that are not cleared through exchanges or clearing houses. BWET may hold exchange-traded options on Freight Futures. The BWET Benchmark Portfolio is maintained by Breakwave and will be rebalanced annually. The Freight Futures currently constituting the BWET Benchmark Portfolio, as well as the daily holdings of BWET are available on BWET’s website at www.tankeretf.com.

When establishing positions in Freight Futures,

BWET will be required to deposit initial margin with a value of approximately

BWET was created to provide investors with a cost-effective and convenient way to gain exposure to daily changes in the price of Freight Futures. BWET is intended to be used as a diversification opportunity as part of a complete portfolio, not a complete investment program.

The Fund will incur certain expenses in connection with its operations. The Fund will hold cash or cash equivalents such as U.S. Treasuries or other high credit quality, short-term fixed-income or similar securities for direct investment or as collateral for the Treasury Instruments and for other liquidity purposes and to meet redemptions that may be necessary on an ongoing basis. The Fund may also realize interest income from its holdings in U.S. Treasuries or other market rate instruments. These expenses and income from the cash and cash equivalent holdings may cause imperfect correlation between changes in the Fund’s net asset value (“NAV”) and changes in the Benchmark Portfolio, because the Benchmark Portfolio does not reflect expenses or income.

The Fund seeks to trade its positions prior to maturity; accordingly, natural market forces may cost the Fund while rebalancing. Each time the Fund seeks to reconstitute its positions, barring movement in the underlying securities, the futures and option prices may be higher or lower. Such differences in price, barring a movement in the price of the underlying security, will constitute “roll yield” and may inhibit the Fund’s ability to achieve its investment objective.

Several factors determine the total return from investing in a futures contract position. One factor that impacts the total return that will result from investing in near month futures contracts and “rolling” those contracts forward each month is the price relationship between the current near month contract and the next month contract.

The CTA will close existing positions when it determines it would be appropriate to do so and reinvest the proceeds in other positions. Positions may also be closed out to meet orders for redemption baskets.

(2) Summary of Significant Accounting Policies

(a) Basis of Accounting

The accompanying combined interim financial statements of the Funds have been prepared in conformity with U.S. generally accepted accounting principles (“U.S. GAAP”). Each Fund qualifies as an investment company for financial reporting purposes under Topic 946 of the Accounting Standard Codification of U.S. GAAP.

18

Amplify Commodity Trust

(Formerly, ETF Managers Group Commodity Trust I)

Notes to Interim Combined Financial Statements

March 31, 2024 (unaudited)

(2) Summary of Significant Accounting Policies - Continued

(a) Basis of Accounting - Continued

The accompanying combined interim financial statements are unaudited, but in the opinion of management, contain all adjustments (which include normal recurring adjustments) considered necessary to present fairly the interim financial statements. These interim financial statements should be read in conjunction with the Fund’s annual report on Form 10-K for the year ended June 30, 2023, BDRY’s prospectus dated February 15, 2024 (the “BDRY Prospectus,”), and BWET’s prospectus dated February 15, 2024 (the “BWET” Prospectus”). Interim period results are not necessarily indicative of results for a full-year period.

(b) Use of Estimates

The preparation of the combined financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the combined financial statements and accompanying notes. Actual results could differ from those estimates. There were no significant estimates used in the preparation of the combined financial statements/

(c) Cash

Cash, when shown in the Combined Statements of Assets and Liabilities, represents non-segregated cash with the custodian and does not include short-term investments.

(d) Cash Held by Broker

Breakwave is registered as a “commodity trading advisor” and acts as such for the Funds. The Funds’ arrangement with its FCM requires the Funds to meet their variation margin requirement related to the price movements, both positive and negative, on futures contracts held by the Funds by keeping cash on deposit with the Commodity Broker (as defined below). These amounts are shown as segregated cash held by broker in the Combined Statements of Assets and Liabilities. Each Fund deposits cash or United States Treasury Obligations, as applicable, with the FCM subject to the CFTC regulations and various exchange and broker requirements. The combination of each Fund’s deposits with the FCM of cash and United States Treasury Obligations, as applicable, and the unrealized gain or loss on open futures contracts (variation margin) represents each Fund’s overall equity in its brokerage trading account. The Funds use their cash held by the FCM to satisfy individual variation margin requirements. The Funds earn interest on their cash deposited with the FCM and interest income is recorded on the accrual basis.

(e) Final Net Asset Value for Fiscal Period

The calculation time of the Fund’s final net asset value for creation and redemption of Fund shares for the three and nine months ended March 31, 2024 was at 4:00 p.m. Eastern Time on March 28, 2024 and March 31, 2023, respectively.

Although the Fund’s shares may continue to trade on secondary markets subsequent to the calculation of the final NAV, the 4:00 p.m. Eastern Time represented the final opportunity to transact in creation or redemption baskets for the three and nine months ended March 31, 2024 and March 31, 2023.

Fair value per share is determined at the close of the NYSE Arca.

For financial reporting purposes, each Fund values its investment positions based upon the final closing price in their primary markets. Accordingly, the investment valuations in these interim combined financial statements differ from those used in the calculations of the Fund’s final creation/redemption NAVs at March 29, 2024 and March 31, 2023.

(f) Investment Valuation

Short-term investments, excluding U.S. Treasury Bills, are carried at amortized cost, which approximates fair value. U.S. Treasury Bills, when held by the Funds, are valued as determined by an independent pricing service based on methods which include consideration of: yields or prices of securities of comparable quality, coupon, maturity and type; indications as to values from dealers; and general market conditions.

Futures and options contracts are valued at the last settled price on the applicable exchange on which that futures and/or options contract trades.

19

Amplify Commodity Trust

(Formerly, ETF Managers Group Commodity Trust I)

Notes to Interim Combined Financial Statements

March 31, 2024 (unaudited)

(2) Summary of Significant Accounting Policies - Continued

(g) Financial Instruments and Fair Value

Each Fund discloses the fair value of its investments in accordance with the Financial Accounting Standards Board (“FASB”) fair value measurement and disclosure guidance which requires a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The disclosure requirements establish a fair value hierarchy that distinguishes between: (1) market participant assumptions developed based on market data obtained from sources independent to the Fund (observable inputs); and (2) the Fund’s own assumptions about market participant assumptions developed based on the best information available under the circumstances (unobservable inputs). The three levels defined by the disclosure requirements hierarchy are as follows:

| Level I: | Quoted prices (unadjusted) in active markets for identical assets and liabilities that the reporting entity has the ability to access at the measurement date. |

| Level II: | Inputs other than quoted prices included within Level I that are observable for the asset or liability, either directly or indirectly. Level II inputs include the following: quoted prices for similar assets or liabilities in active markets, quoted prices for identical or similar assets or liabilities in markets that are not active, inputs other than quoted prices that are observable for the asset or liability, and inputs that are derived principally from or corroborated by observable market data by correlation or other means (market-corroborated inputs). |

| Level III: | Unobservable pricing input at the measurement date for the asset or liability. Unobservable inputs shall be used to measure fair value to the extent that observable inputs are not available. |

In some instances, the inputs used to measure fair value might fall in different levels of the fair value hierarchy. The level in the fair value hierarchy within which the fair value measurement in its entirety falls shall be determined based on the lowest input level that is significant to the fair value measurement in its entirety.

Fair value measurements also require additional disclosure when the volume and level of activity for the asset or liability have significantly decreased, as well as when circumstances indicate that a transaction is not orderly.

| March 31, 2024 (unaudited) | |||||||||||||||

| Short-Term Investments(a) |

Futures Contracts(b) |

Total | |||||||||||||

| Level I – Quoted Prices | $ | $ | $ | ||||||||||||

| a | – | Included in Investments in securities in the Combined Statements of Assets and Liabilities. |

| b | – | Included in Receivable on open futures contracts in the Combined Statements of Assets and Liabilities. |

| June 30, 2023 | |||||||||||||||

| Short-Term Investments(a) |

Futures Contracts(b) |

Total | |||||||||||||

| Level I – Quoted Prices | $ | $ | ( |

$ | |||||||||||

| a | – | Included in Investments in securities in the Combined Statements of Assets and Liabilities. |

| b | – | Included in Payable on open futures contracts in the Combined Statements of Assets and Liabilities. |

Transfers between levels are recognized at the end of the reporting period. During the nine months ended March 31, 2024 and the year ended June 30, 2023, BDRY recognized no transfers from Level I, Level II or Level III.

20

Amplify Commodity Trust

(Formerly, ETF Managers Group Commodity Trust I)

Notes to Interim Combined Financial Statements

March 31, 2024 (unaudited)

(2) Summary of Significant Accounting Policies - Continued

(g) Financial Instruments and Fair Value - Continued

The following tables summarize BWET’s valuation of investments at March 31, 2024 and at June 30, 2023 using the fair value hierarchy:

| March 31, 2024 (unaudited) | |||||||||||||||

| Short-Term Investments(a) |

Futures Contracts(b) |

Total | |||||||||||||

| Level I – Quoted Prices | $ | $ | $ | ||||||||||||

| a | – | Included in Investments in securities in the Combined Statements of Assets and Liabilities. |

| b | – | Included in Payable on open futures contracts in the Combined Statements of Assets and Liabilities |

| June 30, 2023 | |||||||||||||||

| Short-Term Investments(a) |

Futures Contracts(b) |

Total | |||||||||||||

| Level I – Quoted Prices | $ | $ | $ | ||||||||||||

| a | – | Included in Investments in securities in the Combined Statements of Assets and Liabilities. |

| b | – | Included in Receivable on open futures contracts in the Combined Statements of Assets and Liabilities. |

Transfers between levels are recognized at the end of the reporting period. During the nine months ended March 31, 2024 and the year ended June 30, 2023, BWET recognized no transfers from Level I, Level II or Level III.

The inputs or methodology used for valuing investments are not necessarily an indication of the risk associated with investing in those securities.

h) Investment Transactions and Related Income

Investment transactions are recorded on the trade date. All such transactions are recorded on the identified cost basis, and marked to market daily. Unrealized gain/loss on open futures contracts is reflected in Receivable/Payable on open futures contracts in the Combined Statements of Assets and Liabilities and the change in the unrealized gain/loss between periods is reflected in the Combined Statements of Operations. The Funds interest earned on short-term securities and on cash deposited with Marex Financial Ltd. is accrued daily and reflected as Interest Income, when applicable, in the Combined Statements of Operations.

(i) Federal Income Taxes

Each Fund is registered as a Delaware statutory trust and is treated as a partnership for U.S. federal income tax purposes. Accordingly, the Funds do not expect to incur U.S. federal income tax liability; rather, each beneficial owner is required to take into account their allocable share of the Funds’ income, gain, loss, deductions and other items for the Funds’ taxable year ending with or within the beneficial owner’s taxable year.

Management of the Funds has reviewed the open tax years and major jurisdictions and concluded that there is no tax liability resulting from unrecognized tax benefits relating to uncertain income tax positions taken or expected to be taken in future tax returns at March 31, 2024 and June 30, 2023. The Funds are also not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months. On an ongoing basis, management will monitor its tax positions taken to determine if adjustments to its conclusions are necessary based on factors including, but not limited to, further implementation of guidance expected from the FASB and on-going analysis of tax law, regulation, and interpretations thereof. The Funds’ federal tax returns are subject to examination by the Internal Revenue Service for a period of three years after they are filed.

21

Amplify Commodity Trust

(Formerly, ETF Managers Group Commodity Trust I)

Notes to Interim Combined Financial Statements

March 31, 2024 (unaudited)

(3) Investments

(a) Short -Term Investments

The Funds may purchase U.S. Treasury Bills, agency securities, and other high-credit quality short-term fixed income or similar securities with original maturities of one year or less. A portion of these investments may be used as margin for the Funds’ trading in futures contracts.

(b) Accounting for Derivative Instruments

In seeking to achieve each Fund’s investment objective, the commodity trading advisor uses a mathematical approach to investing. Using this approach, the commodity trading advisor determines the type, quantity and mix of investment positions that it believes in combination should produce returns consistent with the Fund’s objective.

All open derivative positions at March 31, 2024 and at June 30, 2023, as applicable, are disclosed in the Combined Schedules of Investments and the notional value of these open positions relative to the shareholders’ capital of the Funds is generally representative of the notional value of open positions to shareholders’ capital throughout the reporting periods for the Funds. The volume associated with derivative positions varies on a daily basis as the Funds transact in derivative contracts in order to achieve the appropriate exposure, as expressed in notional value, in comparison to shareholders’ capital consistent with the applicable Fund’s investment objective.

Following is a description of the derivative instruments used by the Funds during the reporting period, including the primary underlying risk exposures.

(c) Futures Contracts

The Funds enter into futures contracts to gain exposure to changes in the value of the Benchmark Portfolios. A futures contract obligates the seller to deliver (and the purchaser to accept) the future cash settlement of a specified quantity and type of a freight futures contract at a specified time and place. The contractual obligations of a buyer or seller of a freight futures contract may generally be satisfied by making an offsetting sale or purchase of an identical futures contract on the same or linked exchange before the designated date of delivery.

Upon entering into a futures contract, the Funds are required to deposit and maintain as collateral at least such initial margin as required by the exchange on which the transaction is affected. The initial margin is segregated as Cash held by broker, as disclosed in the Combined Statements of Assets and Liabilities, and is restricted as to its use. Pursuant to the futures contract, the Funds agree to receive from or pay to the broker an amount of cash equal to the daily fluctuation in value of the futures contract. Such receipts or payments are known as variation margin and are recorded by the Funds as unrealized gains or losses. The Funds will realize a gain or loss upon closing a futures transaction.

Futures contracts involve, to varying degrees, elements of market risk (specifically freight futures price risk) and exposure to loss in excess of the amount of variation margin. The face or contract amounts reflect the extent of the total exposure the Funds have in the particular classes of instruments. Additional risks associated with the use of futures contracts include imperfect correlation between movements in the price of the futures contracts and the market value of the underlying securities and the possibility of an illiquid market for a futures contract. With futures contracts, there is minimal counterparty risk to the Funds since futures contracts are exchange-traded and the exchange’s clearinghouse, as counterparty to all exchange-traded futures contracts, guarantees the futures contracts against default.

BREAKWAVE DRY BULK SHIPPING ETF

| Asset Derivatives | Liability Derivatives | |||||||||||||

| Derivatives | Combined Statements of Assets and Liabilities |

Fair Value(a) |

Combined Statements of Assets and Liabilities |

Fair Value |

||||||||||

| Dry Bulk Index Rates Market Risk | $ | |||||||||||||

| (a) |

22

Amplify Commodity Trust

(Formerly, ETF Managers Group Commodity Trust I)

Notes to Interim Combined Financial Statements

March 31, 2024 (unaudited)

(3) Investments - Continued

(c) Futures Contracts - Continued

BREAKWAVE DRY BULK SHIPPING ETF

| Asset Derivatives | Liability Derivatives | |||||||||||||

| Derivatives | Combined Statements of Assets and Liabilities |

Fair Value |

Combined Statements of Assets and Liabilities |

Fair Value(a) |

||||||||||

| Dry Bulk Index Rates Market Risk | $ | |||||||||||||

| (a) |

BREAKWAVE DRY BULK SHIPPING ETF

For the Three Months Ended March 31, 2024

| Derivatives | Location of Gain (Loss) on Derivatives | Realized Gain on Derivatives Recognized in Income |

Change in Unrealized Gain (Loss) on Derivatives Recognized in Income | ||||||||

| Dry Bulk Index Rates Market Risk | $ | $ | ( |

) | |||||||

The futures contracts open at March 31, 2024 are indicative of the activity for the three months ended March 31, 2024.

BREAKWAVE DRY BULK SHIPPING ETF

For the Three Months Ended March 31, 2023

| Derivatives | Location of Gain (Loss) on Derivatives | Realized Loss on Derivatives Recognized in Income |

Change in Unrealized Gain (Loss) on Derivatives Recognized in Income | ||||||||

| Dry Bulk Index Rates Market Risk | $ | $ | |||||||||

The futures contracts open at March 31, 2023 are indicative of the activity for the three months ended March 31, 2023.

23

Amplify Commodity Trust

(Formerly, ETF Managers Group Commodity Trust I)

Notes to Interim Combined Financial Statements

March 31, 2024 (unaudited)

(3) Investments - Continued

(c) Futures Contracts - Continued

BREAKWAVE DRY BULK SHIPPING ETF

The Effect of Derivative Instruments on the Combined Statements of Operations

For the Nine Months Ended March 31, 2024

| Derivatives | Location of Gain (Loss) on Derivatives | Realized Gain on Derivatives Recognized in Income |

Change in Unrealized Gain (Loss) on Derivatives Recognized in Income |

|||||||

| Dry Bulk Index Rates Market Risk | $ | $ | ||||||||

The futures contracts open at March 31, 2024 are indicative of the activity for the nine months ended March 31, 2024.

BREAKWAVE DRY BULK SHIPPING ETF

For the Nine Months Ended March, 31, 2023

| Derivatives | Location of Gain (Loss) on Derivatives | Realized Loss on Derivatives Recognized in Income |

Change in Unrealized Gain (Loss) on Derivatives Recognized in Income |

|||||||

| Dry Bulk Index Rates Market Risk | $ | ( |

$ | |||||||

The futures contracts open at March 31, 2023 are indicative of the activity for the nine months ended March 31, 2023.

BREAKWAVE TANKER SHIPPING ETF

| Asset Derivatives | Liability Derivatives | ||||||||||||

| Derivatives | Combined Statements of Assets and Liabilities |

Fair Value (a) |

Combined Statements of Assets and Liabilities |

Fair Value |

|||||||||

| Crude Oil Tanker Index Rates Market Risk | $ | $ | |||||||||||

| (a) | Represents cumulative depreciation of futures contracts as reported in the Combined Statements of Assets and Liabilities. |

24

Amplify Commodity Trust

(Formerly, ETF Managers Group Commodity Trust I)

Notes to Interim Combined Financial Statements

March 31, 2024 (unaudited)

(3) Investments - Continued

(c) Futures Contracts - Continued

BREAKWAVE TANKER SHIPPING ETF

| Asset Derivatives | Liability Derivatives | |||||||||||||

| Derivatives | Combined Statements of Assets and Liabilities |

Fair Value(a) |

Combined Statements of |

Fair Value |

||||||||||

| Crude Oil Tanker Index Rates Market Risk | $ | |||||||||||||

| (a) | Represents cumulative appreciation of futures contracts as reported in the Combined Statements of Assets and Liabilities. |

BREAKWAVE TANKER SHIPPING ETF

For the Three Months Ended March 31, 2024

| Derivatives | Location of Gain (Loss) on Derivatives | Realized Gain on Derivatives Recognized in Income |

Change in Unrealized Gain (Loss) on Derivatives Recognized in Income |

|||||||

| Crude Oil Tanker Index Rates Market Risk | $ | $ | ||||||||

The futures contracts open at March 31, 2024 are indicative of the activity for the three months ended March 31, 2024.

BREAKWAVE TANKER SHIPPING ETF

For the Nine Months Ended March 31, 2024

| Derivatives | Location of Gain (Loss) on Derivatives | Realized Gain on Derivatives Recognized in Income |

Change in Unrealized Gain (Loss) on Derivatives Recognized in Income |

|||||||

| Crude Oil Tanker Index Rates Market Risk | $ | $ | ( |

) | ||||||

The futures contracts open at March 31, 2024 are indicative of the activity for the nine months ended March 31, 2024.

25

Amplify Commodity Trust

(Formerly, ETF Managers Group Commodity Trust I)

Notes to Interim Combined Financial Statements

March 31, 2024 (unaudited)

(4) Agreements

(a) Management Fee

Each Fund pays the Sponsor a sponsor fee (the “Sponsor Fee”) in consideration of the Sponsor’s advisory services to the Funds. Additionally, each Fund pays the commodity trading advisor a license and service fee (the “CTA fee”).

BDRY pays the Sponsor an annual Sponsor Fee, monthly

in arrears, in an amount calculated as the greater of

The waiver of BDRY’s CTA fees, pursuant

to the undertaking, amounted to $

BWET pays the Sponsor an annual Sponsor Fee, monthly

in arrears, in an amount calculated as the greater of

The waiver of BWET’s CTA fees, pursuant

to the undertaking, amounted to $

The Funds currently accrue their daily expenses

up to the Expense Cap, or if less, at accrual estimates established by the Sponsor. At the end of each month, the accrued amount is remitted

to the Sponsor as the Sponsor has assumed, and is responsible for the payment of the routine operational, administrative and other ordinary

expenses of the Funds in excess of the Fund’s respective Expense Cap, which in the case of BDRY, aggregated $-

In the case of BWET, expenses absorbed by the

Sponsor aggregated $

(b) The Administrator, Custodian, Fund Accountant and Transfer Agent

Each Fund has appointed U.S. Bank, a national banking association, with its principal office in Milwaukee, Wisconsin, as the custodian (the “Custodian”). Its affiliate, U.S. Bancorp Fund Services, is the Fund accountant (“the Fund accountant”) of the Funds, transfer agent (the “Transfer Agent”) for Fund shares and administrator for the Funds (the “Administrator”). It performs certain administrative and accounting services for the Funds and prepares certain SEC, NFA and CFTC reports on behalf of the Funds. (U.S. Bank and U.S. Bancorp Fund Services are referred to collectively hereinafter as “U.S. Bank”).

26

Amplify Commodity Trust

(Formerly, ETF Managers Group Commodity Trust I)

Notes to Interim Combined Financial Statements

March 31, 2024 (unaudited)

(4) Agreements - Continued

(b) The Administrator, Custodian, Fund Accountant and Transfer Agent - Continued

Each Fund has agreed to pay U.S. Bank

(c) The Distributor

Through August 13, 2023, each Fund paid ETFMG

Financial LLC (the “former Distributor”), an affiliate of the Sponsor, an annual fee for statutory and wholesaling distribution

services and related administrative services equal to the greater of $

Effective August 14, 2023, the Sponsor entered

into a Marketing Agent Agreement (the “Marketing Agreement”) on behalf of the Trust and the Funds with Foreside Fund Services,

LLC (“Foreside”), pursuant to which Foreside provides certain marketing services to the Funds. Each Fund pays an annual fee

for such distribution services and related administrative services, with a minimum of approximately $

BDRY incurred $

BDRY pays the Sponsor an annual fee for wholesale

support services of $

BDRY incurred $

(d) The Commodity Broker

Marex Financial Ltd., registered in England, serves as each Fund’s clearing broker (the “Commodity Broker”). In its capacity as clearing 3broker, the Commodity Broker executes and clears the Fund’s futures transactions and performs certain administrative services for the Funds.

The Funds pay respective brokerage commissions, including applicable exchange fees, National Futures Association (“NFA”) fees, give–up fees, pit brokerage fees and other transaction related fees and expenses charged in connection with trading activities in CFTC regulated investments. Brokerage commissions on futures contracts are recognized on a half-turn basis.

The Sponsor does not expect annual brokerage commissions

and fees to exceed

27

Amplify Commodity Trust

(Formerly, ETF Managers Group Commodity Trust I)

Notes to Interim Combined Financial Statements

March 31, 2024 (unaudited)

(4) Agreements - Continued

(e) The Trustee

Under the Amended and Restated Declaration of

Trust and Trust Agreement (the “Trust Agreement”) for each Fund, Wilmington Trust Company, the Trustee of each of the Funds

(the “Trustee”) serves as the sole trustee of each Fund in the State of Delaware. The Trustee will accept service of legal

process on the Funds in the State of Delaware and will make certain filings under the Delaware Statutory Trust Act. Under the Trust Agreement

for each Fund, the Sponsor has the exclusive management and control of all aspects of the business of the Funds. The Trustee does not

owe any other duties to the Funds, the Sponsor or the Shareholders of the Funds. The Trustee has no duty or liability to supervise or

monitor the performance of the Sponsor, nor does the Trustee have any liability for the acts or omissions of the Sponsor. BDRY incurred

$

(f) Routine Offering, Operational, Administrative and Other Ordinary Expenses

The Sponsor, in accordance with the BDRY

Expense Cap limitation paid, after the waiver of the CTA fee for BDRY by Breakwave, if any, all of the routine offering,

operational, administrative and other ordinary expenses of BDRY in excess of

The CTA fee waiver for BDRY by Breakwave was $

In addition, the assumption of Fund expenses above

the BDRY Expense Cap by the Sponsor, pursuant to the undertaking (as discussed in Note 4a), amounted to $

The Sponsor, in accordance with the BWET Expense

Cap limitation paid, after the waiver of a portion of the CTA fee for BWET by Breakwave, all of the routine offering, operational, administrative

and other ordinary expenses of BWET in excess of

The CTA fee waiver for BWET by Breakwave was $

In addition, the assumption of Fund expenses above

the BWET Expense Cap by the Sponsor, pursuant to the undertaking (as discussed in Note 4a), amounted to $

28

Amplify Commodity Trust

(Formerly, ETF Managers Group Commodity Trust I)

Notes to Interim Combined Financial Statements

March 31, 2024 (unaudited)

(4) Agreements - Continued

(g) Organizational and Offering Costs

Expenses incurred in connection with organizing BDRY and BWET and up to the offering of their Shares upon commencement of their investment operations on March 22, 2018 and May 3, 2023, respectively, were paid by the Sponsor and Breakwave without reimbursement.

Accordingly, all such expenses are not reflected in the Combined Statements of Operations. The Funds will bear the costs of their continuous offering of Shares and ongoing offering expenses. Such ongoing offering costs will be included as a portion of the Routine Offering, Operational, Administrative and Other Ordinary Expenses. These costs will include registration fees for regulatory agencies and all legal, accounting, printing and other expenses associated therewith.

(h) Extraordinary Fees and Expenses

The Funds will pay all extraordinary fees and expenses, if any. Extraordinary fees and expenses are fees and expenses which are nonrecurring and unusual in nature, such as legal claims and liabilities, litigation costs or indemnification or other unanticipated expenses. Such extraordinary fees and expenses, by their nature, are unpredictable in terms of timing and amount. For the three and nine months ended March 31, 2024 and 2023, respectively, BDRY did not incur such expenses. For the three and nine months ended March 31, 2024, respectively, BWET did not incur such expenses.

(5) Creations and Redemptions

Each Fund issues and redeems Shares from time

to time, but only in one or more Creation Baskets. A Creation Basket is a block of

Except when aggregated in Creation Baskets, the Shares are not redeemable securities. Retail investors, therefore, generally will not be able to purchase or redeem Shares directly from or with the Fund. Rather, most retail investors will purchase or sell Shares in the secondary market with the assistance of a broker. Thus, some of the information contained in these Notes to Interim Combined Financial Statements – such as references to the Transaction Fee imposed on creations and redemptions – is not relevant to retail investors.

(a) Transaction Fees on Creation and Redemption Transactions

In connection with orders to create and redeem

one or more Creation Baskets, an Authorized Participant is required to pay a transaction fee, or AP Transaction Fee, of $

b) Share Transactions

BREAKWAVE DRY BULK SHIPPING ETF

| Summary of Share Transactions for the Three Months Ended March 31, 2024 | ||||||||

| Shares | Net Assets Decrease |

|||||||

| Shares Sold | $ | |||||||

| Shares Redeemed | ( |

( |

) | |||||

| Net Decrease | $ | ( |

) | |||||

BREAKWAVE DRY BULK SHIPPING ETF

| Summary of Share Transactions for the Three Months Ended March 31, 2023 | ||||||||

| Shares | Net Assets Decrease |

|||||||

| Shares Sold | $ | |||||||

| Shares Redeemed | ( |

) | ( |

) | ||||

| Net Decrease | $ | |||||||

29

Amplify Commodity Trust

(Formerly, ETF Managers Group Commodity Trust I)

Notes to Interim Combined Financial Statements

March 31, 2024 (unaudited)

(5) Creations and Redemptions - Continued

b) Share Transactions - Continued

BREAKWAVE DRY BULK SHIPPING ETF

| Summary of Share Transactions for the Nine Months Ended March 31, 2024 | ||||||||

| Shares | Net Assets Decrease |

|||||||

| Shares Sold | $ | |||||||

| Shares Redeemed | ( |

) | ( |

) | ||||

| Net Decrease | ( |

) | $ | ( |

) | |||

BREAKWAVE DRY BULK SHIPPING ETF

| Summary of Share Transactions for the Nine Months Ended March 31, 2023 | ||||||||

| Shares | Net Assets Increase |

|||||||

| Shares Sold | $ | |||||||

| Shares Redeemed | ( |

) | ( |

) | ||||

| Net Increase | $ | |||||||

BREAKWAVE TANKER SHIPPING ETF

| Summary of Share Transactions for the Three Months Ended March 31, 2024 | ||||||||

| Shares | Net Assets Increase |

|||||||

| Shares Sold | $ | |||||||

| Shares Redeemed | ( |

( |

||||||

| Net Increase | $ | |||||||

BREAKWAVE TANKER SHIPPING ETF

| Summary of Share Transactions for the Nine Months Ended March 31, 2024 | ||||||||

| Shares | Net Assets Decrease |

|||||||

| Shares Sold | $ | |||||||

| Shares Redeemed | ( |

) | ( |

) | ||||

| Net Decrease | ( |

) | $ | ( |

) | |||

30

Amplify Commodity Trust

(Formerly, ETF Managers Group Commodity Trust I)

Notes to Interim Combined Financial Statements

March 31, 2024 (unaudited)

(6) Risk

(a) Investment Related Risk

The NAV of BDRY and BWET shares relates directly to the value of the futures investments held by each Fund which are materially impacted by fluctuations in changes in spot charter rates. Charter rates for dry bulk vessels and crude oil tankers are volatile and have declined significantly since their historic highs and may remain at low levels or decrease further in the future.

Futures and options contracts have expiration dates. Before or upon the expiration of a contract, BDRY and/or BWET may be required to enter into replacement contracts that are priced higher or that have less favorable terms than the contracts being replaced (see “Negative Roll Risk,” below). The Freight Futures market settles in cash against published indices, so there is no physical delivery against the futures contracts.

Similar to other futures contracts, the Freight Futures curve shape could be either in “contango” (where the futures curve is upward sloping with the next futures price higher than the current one) or “backwardation” (where each of the next futures prices are lower than the current one). Contango curves are generally characterized by negative roll cost, as the expiring contract value is lower that the next prompt contract value, assuming the same lot size. That means there could be losses incurred when the contracts are rolled each period (“Negative Roll Risk”) and such losses are independent of the Freight Futures price level.

The Russia-Ukraine war poses an increasing risk for global economic growth. Major economic sanctions against Russia are having a considerable impact on oil and gas prices, given the dependence of the EU on oil and gas exports out of Russia combined with limited spare capacity of such commodities globally. Energy prices have increased significantly, leading to major inflationary pressures in the major developed countries that rely heavily on oil and gas exports out of Russia. In the case of BDRY, the combined Russia/Ukraine region account for approximately one-quarter of global grain production, one of the main cargoes transported by dry bulk vessels, while coal and iron ore exports out of the region have also been reduced. The above factors can have a material negative impact on demand for dry bulk transportation, while slower economic growth could also negatively affect demand for dry bulk commodities in the rest of the world, leading to lower dry bulk freight rates.

The conflict between Russia and Ukraine is having a profound impact on global commodities prices including grain and coal, two of the most important commodities for dry bulk shipping. Given the importance of the region in export volumes for both grains and coal, a prolonged stoppage could lead to significantly lower freight rates and thus a decline in freight futures prices and a decline in the value of BDRY. Although coal supplies could potentially be sourced from elsewhere partly mitigating the negative impact of the lost volumes, global grain production capacity is limited, and thus the impact of the lost volumes could not be easily mitigated. In addition, the recent geopolitical turmoil has led to an increase in government protectionism when it comes to commodities, and if such a trend continues, it could lead to lower bulk commodities trading globally over the long term. The impact of such a scenario on dry bulk shipping will be negative, leading to lower spot rates and as a result lower freight futures prices and a decline in the value of BDRY.

In the case of BWET, the conflict between Russia

and Ukraine has also had a profound impact on oil prices and as a result on tanker rates and might continue to impact the level of tanker

rates for years to come. Russia accounts for more than

Most recently, Hamas attacked Israel, with Israel then declaring war on Hamas in the Gaza Strip. This conflict has stoked fears of oil supply instability in the Middle East and globally. While not having an immediate impact on global oil production or tanker trade patterns, escalation or expansion of hostilities, interventions by other groups or nations, the imposition of economic sanctions on any of the oil producing nations, disruption of shipping transit in the Straits of Hormuz or other significant trade routes, or similar outcomes could lead to oil supply instability. The conflict is ongoing and, should it escalate and expand toother oil producing nations in the region, it may have a profound negative impact on oil prices and, as a result, the supply and demand for freight that could have a negative impact on spot freight rates for dry bulk and liquid freight and on Freight Futures.

In addition, The People’s Republic of China (“China”) accounts for a sizable part of oil demand, and changes in the economic and political environment in China and policies adopted by the government to regulate its economy may have a material adverse effect on tanker charter rates and as a result, Freight Futures.

31

Amplify Commodity Trust

(Formerly, ETF Managers Group Commodity Trust I)

Notes to Interim Combined Financial Statements

March 31, 2024 (unaudited)

(6) Risk - Continued

(b) Liquidity Risk

In certain circumstances, such as the disruption of the orderly markets for the futures contracts or Financial Instruments in which the Fund invest, the Funds might not be able to dispose of certain holdings quickly or at prices that represent what the market value may have been in an orderly market. Futures and option positions cannot always be liquidated at the desired price. It is difficult to execute a trade at a specific price when there is a relatively small volume of buy and sell orders in a market. A market disruption can also make it difficult to liquidate a position. The large size of the positions that the Funds may acquire increases the risk of illiquidity both by making its positions more difficult to liquidate and by potentially increasing losses while trying to do so. Such a situation may prevent the Funds from limiting losses, realizing gains or achieving a high correlation with the applicable Benchmark Portfolio.

(c) Natural Disaster/Epidemic Risk