Confidentially submitted to the United States Securities and Exchange Commission on November 21, 2014.

This draft registration statement has not been publicly filed with the Securities and Exchange Commission

and all information herein remains strictly confidential.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1

ToFORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

CHECK-CAP LTD.

(Exact name of Registrant as specified in its charter)

|

Israel

(State or other jurisdiction of

incorporation or organization)

|

3844

(Primary Standard Industrial

Classification Code Number)

|

Not Applicable

(I.R.S. Employer

Identification Number)

|

Check-Cap Building

Abba Hushi Avenue

P.O. Box 1271

Isfiya, 30090

Mount Carmel, Israel

+972-4-8303400

(Address, including zip code, and telephone number,

including area code, of Registrant’s principal executive offices)

Puglisi & Associates

850 Library Avenue, Suite 204

Newark, Delaware 19711

302-738-6680

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

|

Mitchell S. Nussbaum, Esq.

Angela M. Dowd, Esq.

Loeb & Loeb LLP

345 Park Avenue

New York, New York 10154

(212) 407-4000 - Telephone

(212) 407-4990 - Facsimile

|

Eran Yaniv, Adv.

Sharon Rosen, Adv.

Fischer Behar Chen Well

Orion & Co.

3 Daniel Frisch Street

Tel Aviv, 6473104, Israel

+972 3 6944111 - Telephone

+972 3 6091116 - Facsimile

|

Yvan-Claude Pierre, Esq.

Daniel I. Goldberg, Esq.

Reed Smith LLP

599 Lexington Avenue

New York, New York 10022

(212) 521-5400 - Telephone

(212) 521-5450 - Facsimile

|

Shlomo Landress, Adv.

Amit, Pollak, Matalon & Co.

Nitsba Tower,

17 Yitzhak Sadeh St.,

Tel Aviv 67775, Israel

+972 3 568 9000

Telephone

+972 3 568 9001

Facsimile

|

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended, or the Securities Act, check the following box. T

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. £

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. £

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. £

__________________________

Calculation of Registration Fee

|

Title of Each Class of Securities to be Registered

|

Proposed Maximum Aggregate Offering

Price (1)

|

Amount of

Registration Fee (1)

|

||||||

|

Ordinary shares, par value NIS 0.01 (2)(3)

|

$ | $ | ||||||

|

Underwriter warrants(4)(6)

|

||||||||

|

Ordinary shares, par value NIS 0.01 underlying the underwriter warrants(3)(5)

|

$ | $ | ||||||

|

TOTAL

|

||||||||

|

|

(1)

|

Estimated solely for the purpose of calculating the amount of the registration fee pursuant to Rule 457(o) under the Securities Act.

|

|

|

(2)

|

Includes ordinary shares initially offered and sold outside the United States that may be resold from time to time in the United States either as part of their distribution or within 40 days after the later of the effective date of this registration statement and the date the ordinary shares are first bona fide offered to the public, and also includes ordinary shares that may be purchased by the underwriters pursuant to an option to purchase additional ordinary shares to cover over-allotments, if any. The ordinary shares are not being registered for the purpose of sales outside the United States.

|

|

|

(3)

|

Pursuant to Rule 416 of the Securities Act, the securities being registered hereunder include such additional securities as may be issued after the date hereof as a result of share splits, share dividends or similar transactions.

|

|

|

(4)

|

We have agreed to issue, upon closing of this offering, warrants exercisable for a period of four years following the effective date of this registration statement representing 5% of the aggregate number of ordinary shares issued in the offering, but not including the over-allotment option, or the “underwriter warrants,” to Chardan Capital Markets, LLC. Resales of the underwriter warrants on a delayed or continuous basis pursuant to Rule 415 under the Securities Act are registered hereby. Resales of ordinary shares issuable upon exercise of the underwriter warrants are also being similarly registered on a delayed or continuous basis hereby. See “Underwriting.”

|

|

|

(5) |

No fee required pursuant to Rule 457(g) under the Securities Act.

|

|

|

(6)

|

Estimated solely for purposes of calculating the registration fee pursuant to Rule 457(g) under the Securities Act. We have calculated the proposed maximum aggregate offering price of the ordinary shares underlying the underwriters’ warrants by assuming that such warrants are exercisable to purchase ordinary shares at a price per ordinary share equal to 100% of the price per ordinary share sold in this offering.

|

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall hereafter become effective in accordance with Section 8(a) of the Securities Act or until the registration statement shall become effective on such date as the Commission acting pursuant to said section 8(a), may determine.

The information contained herein is subject to completion or amendment. A registration statement relating to these securities has been filed with the U.S. Securities and Exchange Commission. These securities may not be sold until the registration statement becomes effective. This prospectus is not an offer to sell and is not a solicitation of an offer to buy in any jurisdiction in which an offer, solicitation, or sale is not permitted.

|

PRELIMINARY PROSPECTUS

|

SUBJECT TO COMPLETION, DATED NOVEMBER 21, 2014

|

Check-Cap Ltd.

Ordinary Shares

Check-Cap Ltd. is offering ordinary shares in its initial public offering. We currently expect the initial public offering price to be between $ and $ per ordinary share.

Prior to this offering, there has been no public market for our ordinary shares. We have applied for the listing of our ordinary shares on the NASDAQ Capital Market under the symbol “CHEK”. There is no assurance that this application will be approved.

Concurrently with this offering, we expect to complete a private placement of ordinary shares or the “Private Placement” at a purchase price per ordinary share equal to the public offering price in accordance with Regulation S under the Securities Act of 1933, as amended, or the “Securities Act” or Regulation D under the Securities Act, to certain investors including certain of our affiliates. The sale of such ordinary shares will not be registered under the Securities Act. We expect to receive $ in aggregate net proceeds from the Private Placement. See “Summary-Recent Developments—Credit Line Agreement; Private Placement”. The closing of the Private Placement is conditioned upon the completion of the offering to which this prospectus relates. However, the completion of the offering to which this prospectus relates is not conditioned upon the closing of the Private Placement.

We are an “emerging growth company” under applicable U.S. federal securities laws and may elect to comply with reduced public company reporting requirements. See “Implications of Being an Emerging Growth Company” on page 6 of this prospectus.

Investing in our ordinary shares involves a high degree of risk. You should read carefully the “Risk Factors” beginning on page 14 of this prospectus before investing in our ordinary shares that are the subject of this offering.

Neither the U.S. Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of the disclosures in this prospectus. Any representation to the contrary is a criminal offense.

|

Per Ordinary Share

|

Total

|

|||||||

|

Public offering price

|

$ | $ | ||||||

|

Underwriting discount and commissions (1)

|

$ | $ | ||||||

|

Proceeds, before expenses, to us

|

$ | $ | ||||||

|

|

(1)

|

We have also agreed to issue, upon closing of this offering, compensation warrants to Chardan Capital Markets, LLC as representative of the underwriters, entitling it to purchase up to ordinary shares. For a description of other terms of the compensation warrants and a description of the additional compensation to be received by the underwriters see “Underwriting.”

|

The underwriters have an option exercisable within 45 days from the date of this prospectus to purchase up to of additional ordinary shares from us at the public offering price, less the underwriting discount, solely to cover over-allotments. The ordinary shares issuable upon exercise of the underwriters’ over-allotment option have been registered under the registration statement of which this prospectus forms a part. In addition to the underwriting discount, we have agreed to pay certain of the expenses of underwriters incurred in connection with this offering, see “Underwriting” beginning on page 156 of this prospectus.

The underwriters expect to deliver the ordinary shares to purchasers on or about , 2015.

|

Chardan Capital Markets, LLC

|

Maxim Group LLC

|

, 2015

TABLE OF CONTENTS

Page

|

1

|

|

|

14

|

|

|

47

|

|

|

48

|

|

|

49

|

|

|

50

|

|

|

53

|

|

|

55

|

|

|

56

|

|

|

58

|

|

|

71

|

|

|

101

|

|

|

110

|

|

|

130

|

|

|

132

|

|

|

136

|

|

|

144

|

|

|

150

|

|

|

156

|

|

|

163

|

|

|

163

|

|

|

163

|

|

|

164

|

|

|

F-1

|

i

You should rely only on the information contained in this prospectus, any amendment or supplement to this prospectus or any free writing prospectus prepared by us or on our behalf. We have not, and the underwriters have not, authorized anyone to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not, and the underwriters are not, making an offer of these securities, or soliciting any offers to buy these securities, in any jurisdiction where the offer or solicitation is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our ordinary shares.

Neither we nor any of the underwriters has done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required other than the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of our ordinary shares set forth in, and the possession and distribution of, this prospectus outside of the United States.

We obtained statistical data, market data and other industry data and forecasts used throughout this prospectus from market research, publicly available information and industry publications. While we believe that the statistical data, industry data and forecasts and market research are reliable, we have not independently verified the data.

ii

|

PROSPECTUS SUMMARY

The following summary does not contain all of the information you should consider before investing in our ordinary shares. You should read the following summary together with the entire prospectus carefully, including the “Risk Factors” section beginning on page 14 and the financial statements and the accompanying notes to those financial statements beginning on page F-1 before making an investment decision. Unless otherwise indicated, all information in this prospectus assumes no exercise of the underwriters’ over-allotment option and no exercise of the underwriter warrants. Unless the context otherwise requires, references to “we,” “our,” “us,” “our company,” and “Check-Cap” refer to Check-Cap Ltd., an Israeli company. The terms “dollar,” “US$” or “$” refer to U.S. dollars, the lawful currency of the United States, and the term “NIS” refers to New Israeli Shekels, the lawful currency of the State of Israel. Unless otherwise indicated, U.S. dollar translation of NIS amounts presented in this prospectus are translated using the rate of $1.00 = NIS 3.4380, the exchange rate published by the Bank of Israel on June 30, 2014, and U.S. dollar translation of Euro amounts presented in this prospectus are translated using the rate of $1.00 = Euro 1.3693, the exchange rates published by the Wall Street Journal on June 30, 2014.

Our Company

We are a clinical stage medical diagnostics company engaged in the development of an ingestible imaging capsule that utilizes low-dose X-rays for the screening for colorectal cancer, or CRC. While CRC is the second leading cause of death from cancer in the United States and is largely preventable with early detection, about one-half of Americans over the age of 50 do not undergo any form of CRC screening due in large part to the pain, discomfort and embarrassment related to current screening methods. Unlike other structural screening methods that are designed to generate structural information of the colon for the detection of pre-cancerous polyps, such as optical colonoscopy, computed tomographic colonography, or CTC, and other capsule-based technology, our imaging capsule is designed to be ingested without any cleansing of the colon and to travel through the gastrointestinal tract naturally while the patient continues his or her normal daily routine. Furthermore, unlike all other CRC imaging devices currently on the market, which require the patient to fast for several hours prior to the procedure, the Check-Cap procedure enables patients to continue eating normally. We believe that this solution will be attractive to both physicians and patients, thereby increasing the number of people willing to undergo screening for CRC.

Our imaging capsule is being designed to create a reconstructed three-dimensional image of the colon and to detect clinically significant polyps with a high degree of sensitivity. Colon polyps are fleshy growths that occur on the lining of the colon. Polyps in the colon are extremely common, and when certain types of polyps grow large enough they can become cancerous.

Our imaging capsule will be swallowed by the patient and propelled by natural motility through the gastrointestinal tract and excreted naturally with no need for retrieval for data collection. Unlike other CRC screening methods, this process should not disrupt a patient’s normal activities or require fasting. Our imaging capsule employs X-rays which are considered low dose by the Radiation Safety Division of the Radiological Protection Branch of the Soreq Nuclear Research Center, which allows it to image the lining of the colon even when surrounded by intestinal content. As such, we believe that patients using our imaging capsule will not be required to undergo any prior bowel cleansing.

Our imaging capsule is being designed to transmit the data it collects to an external data recorder that will be worn by the patient. The external data recorder is being designed to transmit the data to physicians, who will then utilize our data viewer software application to analyze the data collected by our imaging capsule. We intend for physicians to be able to review the colon’s inner images at any location at any time, in less time than is required to perform an optical colonoscopy.

In order to enable a complete view of capsule positioning and motility, we have designed an external receiver and electromagnetic localization system, or RELS, which is mounted on the patient’s back throughout the entire screening procedure. The RELS is being designed to provide the physician with accurate localization data aligned with a reconstructed image.

A clinical proof-of-concept study, which was based on a 10-case study conducted at Tel Aviv Medical Center in Israel and used a prior version of our imaging capsule, did not identify any material safety or feasibility issues. The study demonstrated the applicability of our imaging technology to the human colon, generating images taken in the colon without any prior bowel-cleansing. All subjects ingested the capsule easily with smooth passage within the designated transit time, on average, within two to three days. There were no reported device-related adverse events. Mild effects on bowel movements were noted, which were determined to be related to the contrast agent.

In the event that polyps are identified by our imaging capsule, the patient would be required to undergo a subsequent traditional colonoscopy procedure to examine, remove and biopsy the polyps. For those patients who require a subsequent polypectomy, concerns regarding pain, discomfort and embarrassment may still remain with respect to the subsequent polypectomy. We do not, however, believe that these concerns will make the use of our imaging capsule any less attractive to doctors and patients. Although patients who are initially screened utilizing a traditional colonoscopy could avoid the need for a second procedure if polyps are discovered because they could undergo a polypectomy during the initial screening, if necessary, we believe that our imaging capsule will still be attractive to doctors and patients since a large majority of patients who are screened will not require a subsequent polypectomy. According to a review published by the Agency for Healthcare Research and Quality in October 2008, out of 100 adults aged 50-75, only 25-30 persons have one or more polyps and only 15 persons have significant (10+mm) polyps.

|

1

|

A clinical proof-of-concept study, which was based on a 10-case study conducted at Tel Aviv Medical Center in Israel and used a prior version of our imaging capsule, did not identify any material safety or feasibility issues. The study demonstrated the applicability of our imaging technology to the human colon, generating images taken in the colon without any prior bowel-cleansing. All subjects ingested the capsule easily with smooth passage within the designated transit time, on average, within two to three days. There were no reported device-related adverse events. Mild effects on bowel movements were noted, which were determined to be related to the contrast agent and passed within one to two days after the capsule was excreted.

The 10-case clinical proof-of-concept study focused on assessing the safety and feasibility of the Check-Cap imaging system. The 10-case study is the first part of a multi-center, prospective clinical feasibility study to establish the safety, functionality and preliminary efficacy of the Check-Cap imaging system in patients eligible for CRC screening, by comparing results from the clinical feasibility study with those from non-invasive, low-sensitivity fecal occult blood tests, or FOBTs, and fecal immunochemical tests, or FITs, as well as from optical colonoscopies. The feasibility study is designed to include a total of 60 subjects. The study is being conducted in Israel at the Tel Aviv Medical Center and Laniado Hospital and is planned to also be conducted at the Erasmus University Medical Center in the Netherlands. The clinical feasibility study will also evaluate the safety of the device in terms of total and segmental transit time and analyze the effects of the presence of polyps and variable colon dimensions on these parameters. The study will seek to create a clinical atlas of images that will enable comparisons between images acquired by different CRC screening modalities. During the feasibility study we will collect data about the overall imaging of the colon’s internal surfaces during the passage of the capsule to support the development of a correlation map of polyps identified by our imaging system with polyps imaged by optical colonoscopy and CTC. Additionally, the feasibility study will measure total radiation exposure and the distribution of contrast material within the colon.

Another objective of the 10-case study was to estimate total radiation exposure for each case study. This was calculated using standard established factors for calculating effective radiation exposure, such as the duration of the capsule inside the body, and was based on the activity of the radiation source inside the imaging capsule and radiation energy, both of which were measured for each case study. The average calculated exposure for the entire procedure in the 10-case study, from ingestion of the capsule to excretion, was 0.03 mSv (STD 0.007 mSv). This level of radiation exposure is similar to a single chest X-ray (approximately 0.06mSv) and two orders of magnitude less than a CTC.

Following the successful completion of the broader multi-center, prospective clinical feasibility study, we plan to submit a request for CE marking for the marketing and sale of our capsule in the European Union during 2015. We expect to perform post-marketing studies in Europe following CE marking. We anticipate launching our product commercially in Europe during 2016.

We plan to submit to the U.S. Food and Drug Administration, or FDA, a request to conduct a pivotal study in the United States in late 2015 to (i) demonstrate device safety as evidenced by a lack of device-related serious adverse events; and (ii) provide efficacy data concerning our imaging capsule’s sensitivity and specificity. We also intend to pursue clinical trials for regulatory approvals in Japan and China in parallel to the U.S. pivotal study. Pivotal studies are expected, among other things, to compare the images of polyps identified by our imaging system with the same polyps detected by traditional optical colonoscopy and CTC in instances where patients were referred after positive exam results. These clinical findings will be analyzed in comparison to results obtained from FOBTs and FITs. Subject to successful completion of our clinical trials, we anticipate launching our product commercially in the United States during 2017. We have submitted patent applications covering our technology in the United States, member states of the European Patent Organisation, Australia, Brazil, Canada, China, Hong Kong, India, Israel, Japan and South Korea. We have been granted patents for our core patent by the U.S. Patent and Trademark Office as well as from the European Patent Office, Australia, China, Hong Kong, Israel, India and Japan. We also filed patent applications describing the use of our imaging technology in several other medical applications.

|

2

|

Since our formation, we have not generated any revenues. We do not anticipate generating any revenues for the foreseeable future and we do not yet have any specific launch dates for our product. For the six months ended June 30, 2014, we had a total comprehensive loss of $2.2 million. For the year ended December 31, 2013, we had a total comprehensive loss of $4.0 million. As of June 30, 2014, we had an accumulated deficit of $24.7 million and a total shareholders’ deficit of $998,000.

Industry Background

According to the American Cancer Society, or the ACS, CRC is the third most common cancer diagnosed and the second leading cause of death from cancer in the United States. The ACS estimates that in 2014, in the United States approximately 136,830 people are expected to be diagnosed with CRC and approximately 50,310 people will die from CRC. According to the World Health Organization, or the WHO, in 2012, in Europe there were an estimated 471,000 cases of CRC and approximately 228,000 died from the disease, and in Japan there were an estimated 112,675 cases of CRC and approximately 49,345 died from the disease. According to the WHO, in 2020 the expected numbers of cases of CRC are estimated to be 159,972 in the United States, 528,481 in Europe, 128,346 in Japan and 1,678,127 worldwide.

CRC screening can reduce death rates from CRC by detecting polyps at an earlier, more treatable stage. CRC is one of the few cancers that can be prevented through screening because pre-cancerous polyps, from which colon cancers often develop, can be identified and removed. Moreover, the five-year survival rate is greater than 90% for CRC patients diagnosed at an early, localized stage. However, less than 40% of cases are currently diagnosed at that stage. According to the Centers for Disease Control and Prevention, or the CDC, at least 6 out of every 10 deaths from CRC could be prevented if every adult age 50 years or older was screened regularly and approximately 30,000 lives could be saved each year in the United States if the screening recommendations were followed. The ACS’ goal is to have 80% of those 50 years and older who are covered by the program screened by 2018.

Today, there is a range of options for CRC screening in the average risk population, with current technology falling into two general categories: (i) structural exams, such as optical colonoscopy, sigmoidoscopy, CTC and optical capsules (all of which require aggressive bowel preparation), which are invasive exams that enable physicians to visualize the colon for abnormalities, and (ii) stool tests, such as FOBTs, FITs and stool DNA tests, which test for blood and irregularities in DNA. Notwithstanding the many CRC screening alternatives, the fact that the tests are encouraged by clinicians and insurers and the clinical value of screening for CRC, a large portion of the population are still reticent to undergo CRC screening and are not satisfied with the currently available alternatives.

The ACS recommends that men and women over the age of 50 undergo an optical colonoscopy every 10 years or other structural tests, such as sigmoidoscopy or virtual colonoscopy, every five years or alternatively, a FOBT should be performed every year. According to the U.S. Census Bureau, as of mid-2014, there were projected to be approximately 91 million Americans aged 50-75 years. Assuming the longest screening interval of 10 years, the addressable annual U.S. patient population is at least 9.1 million.

Optical colonoscopy is currently considered the most reliable method for detecting disorders of the colon and is the standard screening tool for early detection of colon cancer. Optical colonoscopy demonstrates a high degree (approximately 95%) of sensitivity (i.e., detection of individuals with cancer) and specificity (i.e., avoiding false negative results). Optical colonoscopy involves the insertion of a flexible colonoscope, which is an approximately160 centimeters long endoscope, by a physician into a patient’s colon through the anus in order to visually inspect the interior of the colon. Air must be pumped in through the rectum in a process called “insufflation.” Sigmoidoscopy, or FSIG, is an endoscopic procedure that examines the lower part of the colon lumen. The exam may be performed with a variety of endoscopic instruments, including a standard 60 centimeter sigmoidoscope. FSIG is typically performed without sedation and with a more limited bowel preparation than a standard optical colonoscopy. An optical colonoscopy and sigmoidoscopy can perform both diagnostic and limited treatment functions, by allowing for the removal of polyps and adenomas during the course of the procedure; however, both of these procedures carry some risks of bowel perforations and bleeding and related limitations as they require prior cleansing of the bowel, insufflation and sedation, involve potential complications and may cause patient anxiety, discomfort and, in some cases, pain. In addition, a patient’s normal daily routine is disrupted for one or two days. |

3

|

CTC, or virtual colonoscopy, is an imaging procedure that results in cross-sectional, two- or three-dimensional views of the entire colon with the use of a special X-ray machine linked to a computer. Here, as well, a flexible tube is inserted into the rectum in order to allow air or carbon dioxide to open the colon. The patient then passes through the CT scanner, which creates multiple images of the colon interior. This method does not allow for treatment and the subject is exposed to a high dose of radiation. A full bowel cleansing is currently necessary for a successful examination by CTC.

FOBT is based on an analysis of stool samples and is currently the most widely used non-invasive screening test. It has a lower sensitivity in detecting polyps (measured by the percentage of polyps being found). According to the CDC, in 2012, only approximately 10.6% of men and 10.2% of women in the United States underwent the procedure due to its inconvenience and unreliable performance. FOBT is being replaced by a more sensitive blood stool technology FIT, but it is also not designed to detect the majority of non-bleeding polyps.

In 2009, optical capsule endoscopy became commercially available in Europe for CRC screening. In early 2014, the FDA granted approval for optical capsule endoscopy procedure to be used for CRC screening for use in patients who have had an incomplete optical colonoscopy. However, this technology requires bowel cleansing to a greater degree than is required for a regular optical colonoscopy, which can result in dehydration and in turn can lead to cancellation of the procedure in certain cases. Moreover, because this procedure must be completed within several hours in order to maintain a clean colon and to accommodate the capsule’s limited battery life, patients are required to drink large amounts of liquid so that the capsule can flow through the gastrointestinal tract during the time allotted. Furthermore, camera-based optical capsule endoscopy procedures generate a large number of images, often requiring more physician time to analyze the images than to conduct an optical colonoscopy.

Several companies are developing technologies based on molecular diagnostics (from blood and other bodily fluids), or MDx, tests that investigate the link between genes and the function of metabolic pathways, drug metabolism and disease development with a primary focus on the study of DNA, RNA and proteins. Genetic markers can be traced within stool samples in minute quantities. For example, a special collecting kit for stool samples and an analyzer to diagnose CRC based on these stool-based markers has been developed and recently approved by the FDA. While the method of screening for CRC using stool DNA testing has been endorsed by several societies, this test does not generate structural information on the colon and therefore, does not detect most pre-cancerous polyps.

Our Solution

We believe that our imaging capsule could represent a potential breakthrough in CRC screening by providing a structural exam without the pain, discomfort and embarrassment experienced by some patients undergoing a traditional optical colonoscopy and other currently available screening methods, by offering the following benefits:

|

|

·

|

eliminating the need for fasting and prior bowel cleansing, which would differentiate our imaging capsule from every other currently available structural screening exam;

|

|

|

·

|

providing patients with a procedure that requires them to swallow our capsule and small amounts of a contrast agent, thereby minimizing any disruption to their normal activities;

|

|

|

·

|

eliminating need to sedate patients;

|

|

|

·

|

obviating the requirement for the insufflation (the forcing of air into the gastrointestinal tract) of patients;

|

|

|

·

|

administering our technology on an outpatient basis;

|

|

|

·

|

providing digital reporting, storage and remote consulting capabilities; and

|

|

|

·

|

enabling a physician to analyze the results in approximately 10 minutes, which would be less time than is required to conduct an optical colonoscopy.

|

|

|

4

|

Although our imaging capsule utilizes radiation that is considered low dose, we believe that the risks associated with such radiation exposure are low compared to risks associated with other procedures such as perforation, bleeding or sedation related effects (optical colonoscopy and sigmoidoscopy) and dehydration and damage to kidneys (optical capsules). Furthermore, stool test methods (FOBTs, FITs and stool DNA) require a follow-up optical colonoscopy if abnormalities are detected. Unlike FOBTs, FITs and stool DNA tests, our capsule-based imaging modality generates structural information on the colon, which could assist in the detection of pre-cancerous polyps. We, therefore, do not believe that the low dose radiation in our imaging capsule will make our imaging capsule less attractive to physicians and patients than other less effective products that do not employ any radiation.

We believe that gastroenterologists will embrace our technology and encourage the use of our imaging capsule. This may increase the number of people undergoing CRC screening and may cause more people with polyps to obtain polypectomy – a therapeutic procedure during which polyps are removed and which currently receives different reimbursement coverage.

Our imaging capsule and RELS are intended to be prescribed to patients by physicians. One or two days prior to swallowing our capsule, a patient will begin drinking small amounts of a radio opaque contrast agent (such as barium sulfate or iodine) with his or her meals, which enhances the contrast of the colon surface. The capsule is propelled by natural motility through the gastrointestinal tract. As it makes its way through the gastrointestinal tract, information is transmitted to a receiving device worn by the patient that stores the information for offline analysis. After our imaging capsule is expelled from a patient’s body, the RELS will transmit the data to physicians, who will then utilize our data reviewer software application to analyze the data collected by our imaging capsule. Our proprietary software is being designed to process the data and produce a two and three-dimensional visualization of the colon. A physician will then analyze the visualization to determine whether any anatomical anomalies are present on the surface of the colon.

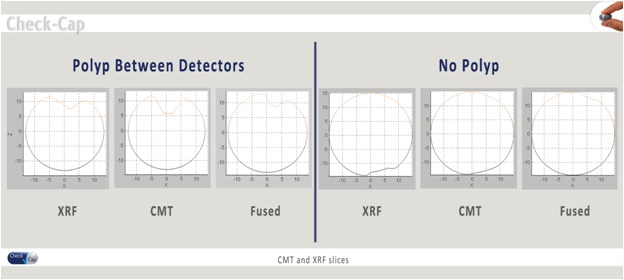

Our imaging capsule consists of an X-ray source and several X-ray detectors. The X-ray source is contained in a rotating radiation shield, enabling the generation of 360-degree angular scans. The collection of successive angular scans enables the virtual reconstruction of a portion of the colon. During movement of our imaging capsule longitudinally through the colon, successive images of portions of the colon are collected to enable the three-dimensional reconstruction of the colon. Our imaging capsule is also intended to identify polyps, which protrude inward into the colon, through the detection of irregularities in the topography of the colon.

Image for illustration purpose only

|

5

|

Our Strategy

Our goal is to become a leading supplier of CRC screening technology and, subject to the successful completion of the development of our technology and the receipt of the requisite regulatory approvals, to establish our technology as a leading CRC screening method. Key elements of our strategy include:

|

|

·

|

obtaining CE marking for the marketing and sale of our imaging capsule in the European Union, followed by obtaining regulatory approvals for the use of our imaging capsule initially in the United States and Japan. In Europe and Japan, we intend to offer our imaging capsule as an imaging and screening tool for the general population. In the United States, we will first seek to obtain regulatory approvals for our imaging capsule as an adjunct tool to FOBTs and FITs, and after we have conducted more extensive clinical studies, we anticipate applying to the FDA for the use of our imaging capsule as an initial screening tool;

|

|

|

·

|

obtaining third-party reimbursement for our technology;

|

|

|

·

|

enhancing our existing technology portfolio and developing new technologies; and

|

|

|

·

|

successfully marketing our product to establish a large customer base.

|

|

Our Challenges

Because we are still in the clinical and development stage, we are subject to certain challenges, including, among others, that:

|

|

·

|

our technology has been tested on a limited basis and therefore we cannot assure the product’s clinical value;

|

|

|

·

|

we need to CE mark the devices in the European Union and obtain the requisite regulatory approvals in the United States, Japan and other markets where we plan to focus our commercialization efforts;

|

|

·

|

we need to raise an amount of capital sufficient to complete the development of our technology, obtain the requisite regulatory approvals and commercialize our current and future products;

|

|

|

·

|

we need to obtain reimbursement coverage from third-party payors for procedures using our imaging capsule;

|

|

|

·

|

we need to increase our manufacturing capabilities; and

|

|

|

·

|

we need to establish and expand our customer base while competing against other sellers of capsule endoscopes as well as other current and future CRC screening technologies and methods.

|

|

Our ability to operate our business and achieve our goals and strategies is subject to numerous risks as described more fully in “Risk Factors.”

Implications of Being an Emerging Growth Company

As a company with less than $1.0 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” pursuant to the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. An emerging growth company may take advantage of certain exemptions from specified disclosure and other requirements that are otherwise generally applicable to public companies. These exemptions include:

|

|

·

|

being permitted to provide only two years of audited financial statements, in addition to any required unaudited interim financial statements, with correspondingly reduced “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure;

|

|

|

·

|

not being required to comply with the auditor attestation requirements for the assessment of our internal control over financial reporting provided by Section 404 of the Sarbanes-Oxley Act of 2002;

|

|

|

·

|

not being required to comply with any requirements adopted by the Public Company Accounting Oversight Board requiring mandatory audit firm rotation or a supplement to the auditor’s report in which the auditor would be required to provide additional information about the audit and our financial statements;

|

|

|

·

|

reduced disclosure obligations regarding executive compensation; and

|

|

|

·

|

not being required to hold a nonbinding advisory vote on executive compensation or seek shareholder approval of any golden parachute payments not previously approved.

|

|

|

6

|

In addition, the JOBS Act provides that an emerging growth company can take advantage of an extended transition period for complying with new or revised accounting standards. However, we have elected to “opt out” of this provision and, as a result, we will comply with new or revised accounting standards as required when they are adopted for public companies. This decision to opt out of the extended transition period under the JOBS Act is irrevocable.

We will remain an emerging growth company until the earliest of (i) the last day of the fiscal year in which our total annual gross revenues exceed $1.0 billion; (ii) the last day of the fiscal year in which the fifth anniversary of the date of the first sale of ordinary shares under this registration statement occurs; (iii) the date on which we have, during the previous three-year period, issued more than $1.0 billion in non-convertible debt; or (iv) the date on which we are deemed to be a “large accelerated filer” under the Securities Exchange Act of 1934, as amended, or the Exchange Act. When we are no longer deemed to be an emerging growth company, we will not be entitled to rely on the exemptions provided in the JOBS Act discussed above. We may choose to take advantage of some, but not all, of the exemptions available to emerging growth companies. We have taken advantage of some of the reduced reporting exemptions in this prospectus. Accordingly, the information contained herein and in future filings with the U.S. Securities and Exchange Commission may be different from the information provided by other public companies in similar filings.

Concurrent Private Placement

Concurrently with this offering, we expect to complete a Private Placement of ordinary shares at a purchase price per ordinary share equal to the public offering price in accordance with Regulation S under the Securities Act or Regulation D under the Securities Act, to certain investors including certain of our affiliates. The sale of such ordinary shares will not be registered under the Securities Act. We expect to receive $ in aggregate net proceeds from the Private Placement. The closing of the Private Placement is conditioned upon the completion of the offering to which this prospectus relates. However, the completion of the offering to which this prospectus relates is not conditioned upon the closing of the Private Placement. Corporate Information

We were incorporated as a limited liability private company under the laws of the State of Israel on April 5, 2009, and on May 31, 2009, we acquired all of the business operations and substantially all of the assets of Check-Cap LLC, a Delaware limited liability company formed in December 2004. Our principal executive offices are located at Check-Cap Building, Abba Hushi Avenue, P.O. Box 1271, Isfiya, 30090, Mount Carmel, Israel. Our telephone number is +972-4-8303400. Our website address is www.check-cap.com. Information contained on, or accessible through, our website does not constitute part of this prospectus and is not incorporated by reference herein.

Throughout this prospectus we refer to the trademark “CHECK-CAP” that we use in our business. Furthermore, we received a notice of allowance for the “CHECK-CAP” mark and design logo in the United States and hold a registered trademark for the “CHECK-CAP” design logo in Europe. Other trademarks and service marks appearing in this prospectus are the property of their respective holders.

Recent Developments

Credit Line Agreement; Private Placement

On August 20, 2014, we entered into a certain credit line agreement, pursuant to which we obtained a credit line in an aggregate principal amount of $12 million from certain lenders and existing shareholders, or the Lenders. The credit line amount was deposited in an escrow account at the closing, which was consummated on October 14, 2014.

|

7

|

We issued to each Lender at closing a warrant, collectively referred to as the Credit Line Warrants, to purchase a number of our ordinary shares constituting 2% of our share capital on a fully diluted basis (assuming conversion of all of our convertible securities into ordinary shares at a 1:1 conversion rate) as of the closing for each $1 million (or portion thereof) extended by such Lender. The Credit Line Warrants are exercisable for a period of ten years at an exercise price of NIS 0.01 per share, and may be exercised on a net issuance basis.

Under the terms of the agreement, if we intend to consummate an initial public offering, or an IPO, and such IPO is expected to be consummated on or prior to February 18, 2015, or if we consummate an IPO on or prior to February 18, 2015, we will be entitled to call all or any part of the credit line amount and direct that such called amount be invested in ordinary shares in a private placement transaction that is exempt from the registration requirements of the Securities Act at a price per ordinary share equal to the public offering price per share in the IPO. In the event that we call less than the full credit line amount, we will call amounts on a pro rata basis among the Lenders based on their pro rata share of the total credit line amount. If we consummate an IPO on or prior to February 18, 2015, any part of the credit line amount not called by us will be released to the Lenders.

If we do not consummate an IPO on or prior to February 18, 2015, we may call the credit line amount at any time thereafter until April 14, 2016, subject to certain conditions. Any part of the credit line amount not called by us on or prior to such date will be released to the Lenders. If we call the credit line amount on or prior to April 14, 2016, the amount called will bear interest at the annual rate of 7%; provided that the aggregate interest rate will not be less than 5%. The called credit line amount will automatically convert into shares of our company upon the earlier of a qualified financing round (which includes a public offering, including an IPO), an M&A. Event (as defined in the agreement) and April 14, 2016, and the Lenders may elect to convert the entire called credit line upon a non-qualified financing round, all under the terms and conditions set forth in the credit line agreement. In the event that the qualified financing round is an IPO, in lieu of automatic conversion, we are entitled to deposit in trust an amount equal to 125% of the called credit line amount and irrevocably instruct the trustee to submit an offer, on behalf of each Lender, for the purchase of the IPO shares at the IPO price determined by our lead underwriters.

Israel-United States Binational Industrial Research and Development Foundation Grant

On July 13, 2014, we entered into a Cooperation and Project Funding Agreement with the Israel-United States Binational Industrial Research and Development Foundation, or the BIRD Foundation, and Synergy Research Inc., or Synergy, pursuant to which the BIRD Foundation has agreed to award a grant in the maximum amount of the lesser of (i) $900,000 and (ii) 50% of the actual expenditures for the funding of a project entitled “Collection & Analysis of Gastrointestinal Images for Diagnostic Adenomatic Polyps and Colorectal Cancer.” The development work is expected to be performed over a 24 month period by Synergy (or a subcontractor on its behalf) and us. Of the total grant amount, we are expected to receive an aggregate of $567,000 to fund our expenditures for the project, in five installments. We received our first advance payment from the BIRD Foundation of $68,000 in July 2014. Our research and development expenses, net is presented net of the differences between the fair value of the liability and the grant amount received from the BIRD Foundation.

Under the terms of the grant agreement, we are required to repay the total grant in an amount equal to 5% of gross revenues derived from the product funded by the project, up to 100%, 113%, 125%, 138% and 150% of the grant amount, linked to the U.S. Consumer Price Index, if repaid within one year, two years, three years, four years and five or more years, respectively, of the original project completion date in accordance with the project proposal. Under the terms of the agreement, if any portion of the product funded by the project is sold outright to a third party prior to full repayment of the grant to the BIRD Foundation, one-half of the sale proceeds will be applied to the repayment of the grant. If the funded product is licensed to a third party, 30% of all payments received under the respective license agreement must be paid to the BIRD Foundation in repayment of the grant.

|

8

|

The Offering

|

|

|

Issuer

|

Check-Cap Ltd.

|

|

Ordinary shares offered by us in this offering

|

ordinary shares

|

|

Over-allotment option

|

The underwriters have an option for a period of 45 days to purchase up to additional ordinary shares to cover over-allotments, if any.

|

|

Ordinary shares outstanding immediately prior to the offering

|

ordinary shares

|

|

Ordinary shares to be issued in the concurrent Private Placement

|

|

|

Ordinary shares to be outstanding immediately after the offering and the concurrent Private Placement(1)

|

ordinary shares (or ordinary shares if the underwriters exercise in full their option to purchase additional shares).

|

|

Use of Proceeds

|

We estimate that the net proceeds from our issuance and sale of ordinary shares in this offering will be approximately $ million, based on the offering price of $ per share, and after deducting underwriting discounts and commissions and offering expenses payable by us. If the representative of the underwriters exercises the over-allotment option in full, we estimate that the net proceeds from this offering will be approximately $ million, based on the offering price of $ per share, and after deducting underwriting discounts and commissions and offering expenses payable by us. We will also expect to receive net proceeds of approximately $ million from the sale of ordinary shares in the concurrent Private Placement after deducting commissions payable by us. We currently expect to use the net proceeds from this offering and the concurrent Private Placement as follows:

· approximately $ million on research and development;

· approximately $ million on obtaining regulatory approvals of our product including approximately

$ million on clinical trials in Europe and the United States;

· approximately $ million to launch our product in selected countries in Europe;

· approximately $ million to build our manufacturing capabilities; and

· the balance, if any, for other general corporate purposes.

See “Use of Proceeds” beginning on page 48 of this prospectus.

|

| Private Placement |

Concurrently with this offering, we expect to complete a Private Placement of ordinary shares at a purchase price per ordinary share equal to the public offering price in accordance with Regulation S under the Securities Act or Regulation D under the Securities Act, to certain investors including certain of our affiliates. The sale of such ordinary shares will not be registered under the Securities Act. We expect to receive $ in aggregate net proceeds from the Private Placement. The closing of the Private Placement is conditioned upon the completion of the offering to which this prospectus relates. However, the completion of the offering to which this prospectus relates is not conditioned upon the closing of the Private Placement. See “Summary-Recent Developments—Credit Line Agreement; Private Placement”

|

9

|

Underwriter Compensation Warrants

|

We will issue to Chardan Capital Markets, LLC as representative of the underwriters, upon closing of this offering, compensation warrants entitling the underwriter to purchase 5% of the aggregate number of ordinary shares issued in this offering, but not including the over-allotment option. The underwriter warrants may be exercised for a period of four years following the date of effectiveness of the Registration Statement on Form F-1 of which this prospectus forms a part.

|

|

Dividend Policy

|

We do not anticipate declaring or paying any cash dividends on our ordinary shares following this offering.

|

|

Transfer Agent and the Registrar

|

|

|

Risk Factors

|

Investing in our securities involves a high degree of risk. See “Risk Factors” beginning on page 14 of this prospectus. See “Risk Factors” and other information included in this prospectus for a discussion of factors you should carefully consider before deciding to invest in our ordinary shares.

|

|

Proposed Symbol and Listing

|

We have applied for the listing our ordinary shares on the NASDAQ Capital Market under the symbol “CHEK.”

|

|

(1) The number of ordinary shares to be outstanding after our initial public offering and the concurrent Private Placement is based on ordinary shares issued and outstanding as of , 2014, and excludes:

|

|

·

|

19,498,426 ordinary shares issuable upon the exercise of outstanding warrants to purchase preferred shares (comprised of (i) warrants to purchase 836,412 Series C-1 preferred shares, (ii) warrants to purchase 1,546,996 Series C-2 preferred shares, (iii) warrants to purchase 503,872 Series D-1 preferred shares and (iv) warrants to purchase 16,611,146 Series D-2 preferred shares, following their conversion into warrants to purchase ordinary shares immediately prior to the closing of this offering) with a weighted average exercise price of $0.44 per ordinary share;

|

|

|

·

|

273,592 ordinary shares issuable upon the exercise of outstanding warrants, which will be automatically exercised, without consideration, if and when Guy Neev exercises any part of his options to purchase 1,995,475 ordinary shares, or the Neev Options, in proportion to (i) the portion of the Neev Options exercised by Guy Neev and (ii) the number of warrants held by the optionee with respect to which such warrants were granted that were exercised prior to the exercise of the Neev Options;

|

|

|

·

|

57,599,850 ordinary shares issuable upon the exercise of outstanding warrants with an exercise price of NIS 0.01 per ordinary share, of which (i) warrants to purchase 53,169,092 ordinary shares are fully vested; and (ii) warrants to purchase 4,430,758 ordinary shares will become fully vested upon the closing of this offering;

|

|

|

·

|

12,415,436 ordinary shares issuable upon the exercise of outstanding options with a weighted average exercise price of $0.17 per ordinary share, granted under our 2006 Unit Option Plan;

|

10

|

·

|

11,630,739 ordinary shares issuable upon the exercise of outstanding options with an exercise price of NIS 0.01 per ordinary share granted under our 2006 Unit Option Plan, which will become fully vested upon the closing of this offering;

|

|

| · | 769,453 ordinary shares issuable upon the exercise of options with an exercise price of $0.2478 per ordinary share, under our 2006 Unit Option Plan, which we have agreed that certain executive officers will be entitled to upon completion of an equity financing, which includes this offering;

|

|

| · | the ordinary shares issuable upon the exercise of warrants to be issued to certain finders in connection with the credit line agreement if either (i) the credit line amount extended to us is invested in ordinary shares in a private placement on or prior to February 18, 2015 or (ii) if we do not consummate an IPO on or prior to February 18, 2015 and we call the credit line amount, upon conversion of the credit line amount into ordinary shares in accordance with the terms of the credit line agreement; | |

|

·

|

150,000 ordinary shares issuable upon the exercise of warrants with an exercise price per ordinary shares equal to the initial public offering price to be issued to our U.S. legal counsel as partial compensation for services rendered in connection with the offering; and

|

|

|

·

|

the ordinary shares issuable upon exercise of the underwriter’s compensation warrants to be issued in connection with this offering.

|

|

|

Except as otherwise indicated, information in this prospectus reflects or assumes:

|

||

|

·

|

the adoption of our amended and restated articles of association prior to the closing of this offering, which will replace our articles of association currently in effect;.

|

|

|

·

|

a one-for- reverse split of our ordinary shares, which will occur prior to the pricing of this offering;

|

|

|

·

|

the conversion of all outstanding preferred shares into an aggregate of ordinary shares immediately prior to the closing of this offering;

|

|

|

·

|

the issuance of 1,995,475 ordinary shares to Mr. Guy Neev upon the exercise prior to the closing of this offering of the Neev Options;

|

|

|

·

|

the issuance of 7,503,521 ordinary shares issuable under warrants that will be automatically exercised, without consideration, upon the exercise by Guy Neev of the Neev Options;

|

|

| · |

the issuance of ordinary shares in the Private Placement at the initial public offering price per ordinary share;

|

|

|

·

|

an initial public offering price of $ , which is the mid-point of the range set forth of the front cover of this prospectus; and

|

|

|

·

|

that the underwriters do not exercise their over-allotment option.

|

|

11

|

Summary Financial Data

You should read the following summary financial information in conjunction with our financial statements and related notes, “Selected Financial Information” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in this prospectus.

The following tables set forth our summary financial data. You should read the following summary financial data in conjunction with, and it is qualified in its entirety by reference to, our historical financial information and other information provided in this prospectus, including “Selected Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and the related notes appearing elsewhere in this prospectus.

The summary statements of comprehensive loss data for the years ended December 31, 2012 and 2013, and the statements of financial position data as of December 31, 2013 are derived from our audited financial statements appearing elsewhere in this prospectus. The summary statements of comprehensive loss data for the six-month periods ended June 30, 2013 and 2014, and the statements of financial position data as of June 30, 2014 are derived from our unaudited financial statements appearing elsewhere in this prospectus. The unaudited financial statements have been prepared on the same basis as the audited financial statements and, in the opinion of management, reflect all adjustments necessary to present fairly our financial position as of June 30, 2014 and our results of operations for the six months ended June 30, 2013 and 2014. The historical results set forth below are not necessarily indicative of the results to be expected in future periods. Our financial statements have been prepared in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board. Statements of Comprehensive Loss Data

|

|

Year Ended December 31,

|

Six Months Ended June 30,

|

|||||||||||||||

|

2013

|

2012

|

2014

|

2013

|

|||||||||||||

|

(US$ in thousands, except per share data)

|

||||||||||||||||

|

(Unaudited)

|

||||||||||||||||

|

Research and development expenses, net(1)

|

2,662 | 2,692 | 1,640 | 1,364 | ||||||||||||

|

General and administrative expenses

|

1,090 | 1,203 | 564 | 520 | ||||||||||||

|

Other expenses (income)

|

(10 | ) | 13 | -- | -- | |||||||||||

|

Operating loss

|

3,742 | 3,908 | 2,204 | 1,884 | ||||||||||||

|

Finance income

|

(63 | ) | (416 | ) | (60 | ) | (45 | ) | ||||||||

|

Finance expenses

|

316 | 229 | 85 | 230 | ||||||||||||

|

Finance expenses (income), net

|

253 | (187 | ) | 25 | 185 | |||||||||||

|

Loss and total comprehensive loss for the period

|

3,995 | 3,721 | 2,229 | 2,069 | ||||||||||||

|

Loss per ordinary share of NIS 0.01 par value, basic and diluted(2)

|

0.18 | 0.17 | 0.10 | 0.09 | ||||||||||||

|

Weighted average number of ordinary shares outstanding – basic and diluted (in thousands)(2)

|

32,542 | 32,530 | 32,542 | 32,542 | ||||||||||||

|

Pro forma loss per ordinary share of NIS 0.01 par value(3)

|

||||||||||||||||

|

Basic and diluted (unaudited)(2)

|

||||||||||||||||

|

Pro forma weighted average number of ordinary shares outstanding - basic and diluted (in thousands) (unaudited)(2)

|

||||||||||||||||

12

| Statements of Financial Position Data |

As of December 31, 2013

|

As of June 30, 2014

|

|||||||||||

|

Actual

|

Pro forma(3)

|

Pro forma as

adjusted(4)

|

|||||||||||

|

(US$ in thousands)

Unaudited

|

|||||||||||||

|

Cash and cash equivalents

|

$ | 4,975 | $ | 2,794 | $ | ||||||||

|

Working capital(5)

|

4,131 | 1,990 | |||||||||||

|

Total assets

|

5,375 | 3,276 | |||||||||||

|

Capital stock

|

23,676 | 23,716 | |||||||||||

|

Total shareholders’ equity (deficit)

|

$ | 1,191 | $ | (998 | ) | ||||||||

|

|

(1)

|

Research and development expenses, net is presented net of the differences between the amount of grants received from the Office of the Chief Scientist of the Ministry of Economy (formerly named the Ministry of Industry, Trade and Labor), or the OCS, and the fair value of their financial liability. The effect of the participation by the OCS totaled $0.4 million and $0.2 million for the years ended December 31, 2013 and 2012, respectively. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Financial Operations Overview—Research and Development, Expenses, Net” for more information.

|

|

(2)

|

Basic and diluted loss per ordinary share is computed based on the basic and diluted weighted average number of ordinary shares outstanding during each period. For purposes of these calculations, the following ordinary shares are deemed to be outstanding: (i) the 1,995,475 ordinary shares issuable to Mr. Guy Neev upon exercise of the Neev Options; and (ii) the 7,503,521 ordinary shares issuable under warrants that will be automatically exercised without consideration upon the exercise by Mr. Guy Neev of the Neev Options. For additional information, see Note 17 to our financial statements for the year ended December 31, 2013 included elsewhere in this prospectus.

|

|

|

(3)

|

On a pro forma basis to give effect to the conversion immediately prior to the completion of this offering of all of our outstanding preferred shares into ordinary shares.

|

|

|

(4)

|

On a pro forma as adjusted basis to give further effect to (i) the issuance and sale of ordinary shares by us in this offering at an assumed initial public offering price of $ per share, the midpoint of the estimated initial public offering price range set forth on the cover of this prospectus, after deducting underwriting discounts and commissions and estimated offering expenses payable by us and (ii) the issuance and sale of ordinary shares by us in the concurrent Private Placement at an assumed price of $_______ per ordinary share, the estimated public offering price, after deducting commissions and estimated expenses payable by us in connection with the concurrent Private Placement.

|

|

|

(5)

|

Working capital is defined as total current assets minus total current liabilities.

|

13

Investing in our securities involves a high degree of risk. You should carefully consider the following risk factors and all other information contained in this prospectus, including the financial statements and the related notes appearing at the end of this prospectus, before purchasing our securities. If any of the following risks actually occur, they may materially harm our business and our financial condition and results of operations. In any such event, the market price of our securities could decline and you could lose all or part of your investment

Risks Related to Our Business

We have a history of losses, may incur future losses and may not achieve profitability.

We are a clinical and development-stage medical diagnostics company with a limited operating history. We have incurred net losses in each fiscal year since we commenced operations in 2009. We incurred net losses of $3.7 million in 2012, $4.0 million in 2013 and $2.2 million in the six months ended June 30, 2014. As of June 30, 2014, our accumulated deficit was $24.7 million. Our losses could continue for the foreseeable future as we continue our investment in research and development and clinical trials to complete the development of our technology and to attain regulatory approvals, begin the commercialization efforts for our imaging capsule, increase our marketing and selling expenses, and incur additional costs as a result of being a public company in the United States. The extent of our future operating losses and the timing of becoming profitable are highly uncertain, and we may never achieve or sustain profitability.

We may not succeed in completing the development of our product, commercializing our product and generating significant revenues.

Since commencing our operations, we have focused on the research and development and limited clinical trials of our imaging capsule. Our product is not approved for commercialization and has never generated any revenues. Our ability to generate revenues and achieve profitability depends on our ability to successfully complete the development of our product, obtain market approval and generate significant revenues. The future success of our business cannot be determined at this time, and we do not anticipate generating revenues from product sales for the foreseeable future. In addition, we have no experience in commercializing our imaging capsule and face a number of challenges with respect to our commercialization efforts, including, among others, that:

|

|

·

|

we may not have adequate financial or other resources to complete the development of our product;

|

|

|

·

|

we may not be able to manufacture our products in commercial quantities, at an adequate quality or at an acceptable cost;

|

|

|

·

|

we may not be able to establish adequate sales, marketing and distribution channels;

|

|

|

·

|

healthcare professionals and patients may not accept our imaging capsule;

|

|

|

·

|

we may not be aware of possible complications from the continued use of our imaging capsule since we have limited clinical experience with respect to the actual use of our imaging capsule;

|

|

|

·

|

technological breakthroughs in CRC screening, treatment and prevention may reduce the demand for our imaging capsule;

|

|

|

·

|

changes in the market for CRC screening, new alliances between existing market participants and the entrance of new market participants may interfere with our market penetration efforts;

|

|

|

·

|

third-party payors may not agree to reimburse patients for any or all of the purchase price of our imaging capsule, which may adversely affect patients’ willingness to purchase our imaging capsule;

|

|

|

·

|

uncertainty as to market demand may result in inefficient pricing of our imaging capsule;

|

|

|

·

|

we may face third-party claims of intellectual property infringement;

|

14

|

|

·

|

we may fail to obtain or maintain regulatory approvals for our imaging capsule in our target markets or may face adverse regulatory or legal actions relating to our imaging capsule even if regulatory approval is obtained; and

|

|

|

·

|

we are dependent upon the results of ongoing clinical studies relating to our imaging capsule and the products of our competitors.

|

If we are unable to meet any one or more of these challenges successfully, our ability to effectively commercialize our imaging capsule could be limited, which in turn could have a material adverse effect on our business, financial condition and results of operations.

Our early clinical experience to date may not have revealed certain potential limitations of the technology and potential complications from our imaging capsule.

To date, we have performed clinical studies with a prior version of our imaging capsule and with several versions of non-imaging capsules. The clinical trial that was conducted using the prior version of our imaging capsule was conducted under a different protocol and used a different group of patients. Therefore, we will have a limited ability to identify potential problems and/or inefficiencies concerning our imaging capsule in advance of its use in patients and we cannot assure you that its actual clinical performances will be satisfactory, or that its use will not result in unanticipated complications. Furthermore, the results from our first clinical studies and the previous pre-clinical studies may not be indicative of the clinical results obtained when we examine our final imaging capsule on real screening population. If our imaging capsule does not function as expected over time, we could be subject to liability claims, our reputation may be harmed and our imaging capsule would not be widely adopted.

We expect to derive most of our revenues from sales of one product or product line. Our inability to successfully commercialize this product, or any subsequent decline in demand for this product, could severely harm our ability to generate revenues.

We are currently dependent on the successful commercialization of our imaging capsule to generate revenues. As a result, factors adversely affecting our ability to successfully commercialize, or the pricing of or demand for, this product could have a material adverse effect on our financial condition and results of operations. If we are unable to successfully commercialize or create market demand for our imaging capsule, we will have limited ability to generate revenues.

Furthermore, and consequently, we are vulnerable to fluctuations in demand for our imaging capsule. Such fluctuations in demand may be due to many factors, including, among others:

|

|

·

|

market acceptance of a new product, including healthcare professionals’ and patients’ preferences;

|

|

|

·

|

development of similarly cost-effective products by our competitors;

|

|

|

·

|

development delays of our imaging capsule;

|

|

|

·

|

technological innovations in CRC screening, treatment and prevention;

|

|

|

·

|

adverse medical side effects suffered by patients using our imaging capsule, whether actually resulting from the use of our imaging capsule or not;

|

|

|

·

|

changes in regulatory policies toward CRC screening or imaging technologies;

|

|

|

·

|

changes in regulatory approval or clearance requirements for our product;

|

|

|

·

|

third-party claims of intellectual property infringement;

|

|

|

·

|

budget constraints and the availability of reimbursement or insurance coverage from third-party payors for our imaging capsule;

|

|

|

·

|

increases in market acceptance of other technologies; and

|

|

|

·

|

adverse responses from certain of our competitors to the offering of our imaging capsule.

|

15

If healthcare professionals do not recommend our product to their patients, our imaging capsule may not achieve market acceptance and we may not become profitable.

CRC screening candidates are generally referred by their healthcare professional to a specified device and screening technologies are purchased by prescription. If healthcare professionals, including physicians, do not recommend or prescribe our product to their patients, our imaging capsule may not achieve market acceptance and we may not become profitable. In addition, physicians have historically been slow to change their medical diagnostic and treatment practices because of perceived liability risks arising from the use of new products. Delayed adoption of our imaging capsule by healthcare professionals could lead to a delayed adoption by patients and third-party payors. Healthcare professionals may not recommend or prescribe our imaging capsule until certain conditions have been satisfied including, among others:

|

|

·

|

there is sufficient long-term clinical evidence to convince them to alter their existing screening methods and device recommendations;

|

|

|

·

|

there are recommendations from other prominent physicians, educators and/or associations that our imaging capsule is safe and effective;

|

|

|

·

|

we obtain favorable data from clinical studies for our imaging capsule;

|

|

|

·

|

reimbursement or insurance coverage from third-party payors is available; and

|

|

|

·

|

they become familiar with the complexities of our imaging capsule.

|

We cannot predict when, if ever, healthcare professionals and patients may adopt the use of our imaging capsule. Even if favorable data is obtained from clinical studies for our imaging capsule, there can be no assurance that prominent physicians would endorse it or that future clinical studies will continue to produce favorable data regarding our imaging capsule. In addition, prolonged market exposure may also be a pre-requisite to reimbursement or insurance coverage from third-party payors. If our imaging capsule does not achieve an adequate level of acceptance by patients, healthcare professionals and third-party payors, we may not generate significant product revenues and we may not become profitable.

If we are unable to market and sell our imaging capsule, we may not become profitable.

We have not had any sales of our imaging capsule to date. There can be no assurance that we will be able to receive regulatory clearance for our imaging capsule in the foreseeable future or ever or that our imaging capsule will be accepted as comparable or superior to existing technologies for the visualization, imaging or screening of the colon. Our ability to market and sell our imaging capsule successfully depends on one or more of the following:

|

|

·

|

the existence of clinical data sufficient to support the use of our imaging capsule for the visualization, imaging, or screening of the colon as compared to other colon visualization, imaging or screening methods (if clinical trials indicate that our imaging capsule is not as clinically effective as other current methods, or if our technology causes unexpected complications or other unforeseen negative effects, we may not obtain regulatory clearance or approval to market and sell our imaging capsule or physicians may be reluctant to use it);

|

|

|

·

|