UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________________________________________________________

FORM 10-K

________________________________________________________________

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2021

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission file number: 001-36710

______________________________________________________________

(Exact name of registrant as specified in its charter)

________________________________________________________________

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (832 ) 337-2034

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

________________________________________________________________

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. x Yes ¨ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). x Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| x | Accelerated filer | ¨ | ||||||||||||

| Non-accelerated filer | ¨ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes x No

The aggregate market value of the registrant’s common units held by non-affiliates of the registrant as of June 30, 2021, was $1,828 million, based on the closing price of such units of $14.77 as reported on the New York Stock Exchange on such date. The registrant had 393,289,537 common units outstanding as of February 24, 2022.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This report includes forward-looking statements. You can identify our forward-looking statements by the words “anticipate,” “estimate,” “believe,” “budget,” “continue,” “could,” “intend,” “may,” “plan,” “potential,” “predict,” “seek,” “should,” “would,” “expect,” “objective,” “projection,” “forecast,” “goal,” “guidance,” “outlook,” “effort,” “target” and similar expressions.

We based the forward-looking statements on our current expectations, estimates and projections about us and the industries in which we operate in general. We caution you these statements are not guarantees of future performance as they involve assumptions that, while made in good faith, may prove to be incorrect, and involve risks and uncertainties we cannot predict. In addition, we based many of these forward-looking statements on assumptions about future events that may prove to be inaccurate. Accordingly, our actual outcomes and results may differ materially from what we have expressed in the forward-looking statements. Any differences could result from a variety of factors, including the following:

•The outcome of the non-binding, preliminary proposal made by SPLC to acquire all of our issued and outstanding common units not already owned by SPLC or its affiliates.

•The continued ability of Shell and our non-affiliate customers to satisfy their obligations under our commercial and other agreements.

•The volume of crude oil, refined petroleum products and refinery gas we transport or store and the prices that we can charge our customers.

•The tariff rates with respect to volumes that we transport through our regulated assets, which rates are subject to review and possible adjustment imposed by federal and state regulators.

•Changes in revenue we realize under the loss allowance provisions of our fees and tariffs resulting from changes in underlying commodity prices.

•Our ability to renew or replace our third-party contract portfolio on comparable terms.

•Fluctuations in the prices for crude oil, refined petroleum products and refinery gas, including fluctuations due to political or economic measures taken by various countries.

•The level of production of refinery gas by refineries and demand by chemical sites.

•The level of onshore and offshore (including deepwater) production and demand for crude oil by U.S. refiners.

•Changes in global economic conditions and the effects of a global economic downturn on the business of Shell and the business of its suppliers, customers, business partners and credit lenders.

•The ongoing COVID-19 pandemic and related governmental regulations and travel restrictions (including our vaccine mandate for offshore employees), and any resulting reduction in the global demand for oil and natural gas.

•Availability of acquisitions and financing for acquisitions on our expected timing and acceptable terms.

•Changes in, and availability to us of, the equity and debt capital markets.

•Liabilities associated with the risks and operational hazards inherent in transporting and/or storing crude oil, refined petroleum products and refinery gas.

•Curtailment of operations or expansion projects due to unexpected leaks, spills or severe weather disruption, including disruptions caused by hurricanes; riots, strikes, lockouts or other industrial disturbances; or failure of information technology systems due to various causes, including unauthorized access or attack.

•Costs or liabilities associated with federal, state and local laws and regulations, including those that may be implemented by the current U.S. presidential administration, relating to environmental protection and safety, including spills, releases and pipeline integrity.

•Costs associated with compliance with evolving environmental laws and regulations on climate change.

•Costs associated with compliance with safety regulations and system maintenance programs, including pipeline integrity management program testing and related repairs.

•Changes in tax status or applicable tax laws.

•Changes in the cost or availability of third-party vessels, pipelines, rail cars and other means of delivering and transporting crude oil, refined petroleum products and refinery gas.

•Direct or indirect effects on our business resulting from actual or threatened terrorist incidents or acts of war.

•The factors generally described in Part I, Item 1A. Risk Factors of this report.

GLOSSARY OF TERMS

Barrel: One stock tank barrel, or 42 U.S. gallons liquid volume, used in reference to crude oil or other liquid hydrocarbons.

BOEM: Bureau of Ocean Energy Management.

BSEE: Bureau of Safety and Environmental Enforcement.

Capacity: Nameplate capacity.

Common carrier pipeline: A pipeline engaged in the transportation of crude oil, refined products or natural gas liquids as a common carrier for hire.

Crude oil: A mixture of raw hydrocarbons that exists in liquid phase in underground reservoirs.

DOT: Department of Transportation.

EPAct: Energy Policy Act of 1992.

Expansion capital expenditures: Expansion capital expenditures are cash expenditures (including transaction expenses) for capital improvements. Expansion capital expenditures do not include maintenance capital expenditures or investment capital expenditures. Expansion capital expenditures do include interest payments (including periodic net payments under related interest rate swap agreements) and related fees paid during the construction period on construction debt. Where cash expenditures are made in part for expansion capital expenditures and in part for other purposes, our general partner determines the allocation between the amounts paid for each.

FERC: Federal Energy Regulatory Commission.

GAAP: U.S. generally accepted accounting principles.

HCAs: High Consequence Areas.

ICA: Interstate Commerce Act of 1887, as modified by the Elkins Act.

kbpd: Thousand barrels per day.

kbls: Thousand barrels.

klbs/d: Thousand pounds per day.

Life-of-lease transportation agreement: A contract in which the producer dedicates shipments of all current and future reserves pertaining to a specific lease or area to a specific carrier.

LNG: Liquefied natural gas.

LPSC: Louisiana Public Service Commission.

LTIP: Shell Midstream Partners, L.P. 2014 Incentive Compensation Plan.

Maintenance capital expenditures: Maintenance capital expenditures are cash expenditures (including expenditures for (a) the acquisition (through an asset acquisition, merger, stock acquisition, equity acquisition or other form of investment) by the Partnership or any of its subsidiaries of existing assets or assets under construction, (b) the construction or development of new capital assets by the Partnership or any of its subsidiaries, (c) the replacement, improvement or expansion of existing capital assets by the Partnership or any of its subsidiaries or (d) a capital contribution by the Partnership or any of its subsidiaries to a person that is not a subsidiary in which the Partnership or any of its subsidiaries has, or after such capital contribution will have, directly or indirectly, an equity interest, to fund the Partnership or such subsidiary’s share of the cost of the acquisition, construction or development of new, or the replacement, improvement or expansion of existing, capital assets by such person), in each case if and to the extent such acquisition, construction, development, replacement, improvement or expansion is made to maintain, over the long-term, the operating capacity or operating income of the Partnership and its subsidiaries, in the case of clauses (a), (b) and (c), or such person, in the case of clause (d), as the operating capacity or operating income of the Partnership and its subsidiaries or such person, as the case may be, existed immediately prior to such acquisition, construction, development, replacement, improvement, expansion or capital contribution. For purposes of this definition, “long-term” generally refers to a period of not less than twelve months.

mscf/d: Million standard cubic feet per day.

OPEC: The Organization of Petroleum Exporting Countries.

Partnership Agreement: Second Amended and Restated Agreement of Limited Partnership of Shell Midstream Partners, L.P., dated as of April 1, 2020.

PHMSA: Pipeline and Hazardous Materials Safety Administration.

Pipeline loss allowance or PLA: An allowance for volume losses due to measurement difference set forth in crude oil product transportation agreements, including long-term transportation agreements and tariffs for crude oil shipments.

Refined products: Hydrocarbon compounds, such as gasoline, diesel fuel, jet fuel and residual fuel that are produced by a refinery.

Refinery gas: Non-condensable gas obtained during distillation of crude oil or treatment of oil products in refineries.

Ship-or-pay contract: A contract requiring payment for the transportation of crude oil or refined products even if the crude oil or refined products are not transported.

Throughput: The volume of crude oil, refined products or natural gas transported or passing through a refinery, pipeline, terminal or other facility during a particular period.

TRRC: Texas Railroad Commission.

SHELL MIDSTREAM PARTNERS, L.P.

TABLE OF CONTENTS

| Item | Page | ||||

PART I

Unless the context otherwise requires, references in this report to “Shell Midstream Partners,” “the Partnership,” “us,” “our,” “we,” “SHLX” or similar expressions refer to Shell Midstream Partners, L.P. and its subsidiaries. References to “our general partner” refer to Shell Midstream Partners GP LLC, a wholly owned subsidiary of Shell Pipeline Company LP (“SPLC”). References to “Shell” or “Parent” refer collectively to Shell plc and its controlled affiliates, other than us, our subsidiaries and our general partner.

Part I should be read in conjunction with Part II, Item 7 and with the consolidated financial statements and notes thereto included in Part II, Item 8 of this report.

Items 1 and 2. BUSINESS AND PROPERTIES

Overview

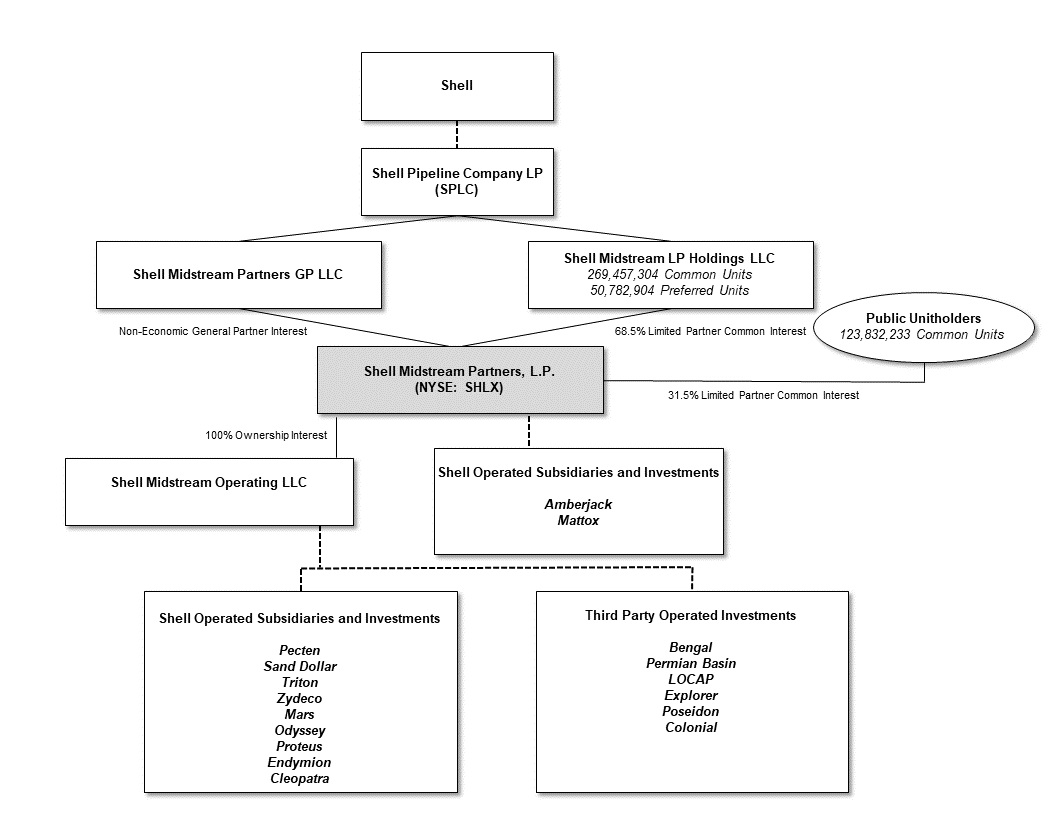

Shell Midstream Partners, L.P. is a Delaware limited partnership formed by Shell on March 19, 2014 to own and operate pipeline and other midstream assets, including certain assets acquired from SPLC and its affiliates. We conduct our operations either through our wholly owned subsidiary Shell Midstream Operating LLC (the “Operating Company”) or through direct ownership. Our general partner is Shell Midstream Partners GP LLC (our “general partner”).

As of December 31, 2021, our general partner holds a non-economic general partner interest in the Partnership, and affiliates of SPLC own a 68.5% limited partner interest (269,457,304 common units) and 50,782,904 Series A perpetual convertible preferred units (the “Series A Preferred Units”) in the Partnership. These common units and preferred units, on an as-converted basis, represent a 72% interest in the Partnership.

We own, operate, develop and acquire pipelines and other midstream and logistics assets. As of December 31, 2021, our assets include interests in entities that own (a) crude oil and refined products pipelines and terminals that serve as key infrastructure to transport onshore and offshore crude oil production to Gulf Coast and Midwest refining markets and deliver refined products from those markets to major demand centers and (b) storage tanks and financing receivables that are secured by pipelines, storage tanks, docks, truck and rail racks and other infrastructure used to stage and transport intermediate and finished products. The Partnership’s assets also include interests in entities that own natural gas and refinery gas pipelines that transport offshore natural gas to market hubs and deliver refinery gas from refineries and plants to chemical sites along the Gulf Coast.

We generate revenue from the transportation, terminaling and storage of crude oil, refined products, and intermediate and finished products through our pipelines, storage tanks, docks, truck and rail racks, generate income from our equity and other investments and generate interest income from financing receivables on certain logistics assets. Our operations consist of one reportable segment. See Note 1 — Description of the Business and Basis of Presentation in the Notes to Consolidated Financial Statements included in Part II, Item 8 of this report.

6

The following table reflects our ownership interests as of December 31, 2021:

| SHLX Ownership | |||||

| Pecten Midstream LLC (“Pecten”) | 100.0 | % | |||

| Sand Dollar Pipeline LLC (“Sand Dollar”) | 100.0 | % | |||

| Triton West LLC (“Triton”) | 100.0 | % | |||

Zydeco Pipeline Company LLC (“Zydeco”) (1) | 100.0 | % | |||

| Mattox Pipeline Company LLC (“Mattox”) | 79.0 | % | |||

| Amberjack Pipeline Company LLC (“Amberjack”) – Series A/Series B | 75.0% / 50.0% | ||||

| Mars Oil Pipeline Company LLC (“Mars”) | 71.5 | % | |||

| Odyssey Pipeline L.L.C. (“Odyssey”) | 71.0 | % | |||

| Bengal Pipeline Company LLC (“Bengal”) | 50.0 | % | |||

| Crestwood Permian Basin LLC (“Permian Basin”) | 50.0 | % | |||

| LOCAP LLC (“LOCAP”) | 41.48 | % | |||

| Explorer Pipeline Company (“Explorer”) | 38.59 | % | |||

| Poseidon Oil Pipeline Company, L.L.C. (“Poseidon”) | 36.0 | % | |||

| Colonial Enterprises, Inc. (“Colonial”) | 16.125 | % | |||

| Proteus Oil Pipeline Company, LLC (“Proteus”) | 10.0 | % | |||

| Endymion Oil Pipeline Company, LLC (“Endymion”) | 10.0 | % | |||

| Cleopatra Gas Gathering Company, LLC (“Cleopatra”) | 1.0 | % | |||

(1) Prior to May 1, 2021, we owned a 92.5% ownership interest in Zydeco and SPLC owned the remaining 7.5% ownership interest. Effective May 1, 2021, SPLC transferred its 7.5% ownership interest to us as part of the May 2021 Transaction. Refer to Note 3 —Acquisitions and Other Transactions in the Notes to Consolidated Financial Statements included in Part II, Item 8 of this report for additional information.

2021 Transactions

May 2021 Transaction

Effective May 1, 2021, Triton sold to Equilon Enterprises LLC d/b/a Shell Oil Products US (“SOPUS”), as designee of SPLC, substantially all of the assets associated with its clean products truck rack terminal and facility in Anacortes, Washington (the “Anacortes Assets”). In exchange for the Anacortes Assets, SPLC paid Triton $10 million in cash and transferred to the Operating Company, as designee of Triton, SPLC’s 7.5% interest in Zydeco (the “May 2021 Transaction”). Effective May 1, 2021, the Partnership owns a 100.0% ownership interest in Zydeco.

The May 2021 Transaction closed pursuant to a Sale and Purchase Agreement dated April 28, 2021 between Triton and SPLC, effective May 1, 2021 (the “May 2021 Sale and Purchase Agreement”). The May 2021 Sale and Purchase Agreement contains customary representations, warranties and covenants of Triton and SPLC. SPLC, on the one hand, and Triton, on the other hand, have agreed to indemnify each other and their respective affiliates, officers, directors and other representatives against certain losses resulting from any breach of their representations, warranties or covenants contained in the May 2021 Sale and Purchase Agreement, subject to certain limitations and survival periods.

In connection with the May 2021 Transaction, the Partnership and SPLC entered into a Termination of Voting Agreement dated April 28, 2021 and effective May 1, 2021, under which they agreed to terminate the Voting Agreement dated November 3, 2014 between the Partnership and SPLC, relating to certain governance matters for their respective direct and indirect ownership interests in Zydeco.

Auger Divestiture

On April 29, 2021, we executed an agreement to divest the 12” segment of the Auger pipeline, effective June 1, 2021. We received approximately $2 million in cash consideration for this sale. In anticipation of the intended divestment, we recorded an impairment charge of approximately $3 million during the first quarter of 2021. The remainder of the Auger pipeline continues to operate under the ownership of Pecten.

7

See Note 3 — Acquisitions and Other Transactions in the Notes to Consolidated Financial Statements in Part II, Item 8 of this report for additional information.

Organizational Structure

The following simplified diagram depicts our organizational structure as of December 31, 2021:

8

Our Assets and Operations

Our assets consist of the following systems:

Onshore Crude Pipelines

Our onshore crude pipelines transport various grades of crude oil across more than 500 miles. Our onshore crude pipelines serve varying purposes including transporting crude oil between major onshore demand centers, as well as aggregating volume from multiple offshore pipelines and connecting this offshore production to key onshore markets, including refineries and tankage space. These pipelines are regulated by PHMSA for safety and integrity, and the FERC, LPSC and TRRC for tariff regulations.

Our onshore crude pipelines transport volumes on a spot basis, as well as under transportation services and throughput and deficiency agreements (“T&D agreements”). In compliance with FERC indexing adjustments, our rates may be indexed annually.

Our FERC-approved transportation services agreements entitle the customer to a specified amount of guaranteed capacity on the pipeline. This capacity cannot be pro rated even if the pipeline is oversubscribed. In exchange, the customer makes a specified monthly payment regardless of the volume transported. If the customer does not ship its full guaranteed volume in a given month, it makes the full monthly cash payment, and it may ship the unused volume in a later month for no additional cash payment for up to 12 months, subject to availability on the pipeline. The cash payment received is recognized as deferred revenue, and therefore not included in revenue or net income until the earlier of the actual or estimated shipment of the unused volumes or the expiration of the 12-month period, as provided for in the applicable contract. If there is insufficient capacity on the pipeline to allow the unused volume to be shipped, the customer forfeits its right to ship such unused volume. We do not refund any cash payments relating to unused volumes.

T&D agreements, similar to transportation services agreements, require shippers to commit to a minimum volume for a fixed term. If the shipper falls below the minimum volume for the specified term, it is required to make a payment for the volume deficiency at the agreed transportation rate. Because this payment is due at the end of the specified payment term, the timing of cash flows may be affected. Unlike transportation services agreements, T&D agreements do not offer shippers firm space on the pipeline in question, and, if a segment of the pipeline system is oversubscribed, space is prorated in accordance with applicable regulations.

9

See “— Factors Affecting our Business and Outlook — Changes in Customer Contracting” for additional information on our transportation services and T&D agreements.

Offshore Crude Pipelines

The offshore crude pipelines in which we own interests span across approximately 1,500 miles, and are regulated primarily by PHMSA, BSEE or BOEM, and in some cases by the FERC or LPSC. Our offshore crude pipelines provide transportation for major oil producers and from multiple production fields in the Gulf of Mexico, offering delivery options into various pipelines, in which we may also own interests. Through the pipeline connectivity options, these pipelines provide access to desirable onshore destinations, including trading hubs and refinery complexes.

Our offshore crude pipelines generate revenue under several types of long-term transportation agreements: life-of-lease transportation agreements, life-of-lease transportation agreements with a guaranteed return, T&D agreements, debottleneck surcharge agreements and buy/sell agreements. Some crude oil also moves on our offshore pipelines under posted tariffs, which may be indexed annually. Inventory management fees are also charged in some cases.

Our life-of-lease transportation agreements have a term equal to the life of the applicable mineral lease and require producers to transport all production from the specified fields connected to the pipeline for the entire life of the lease. This means that the dedicated production cannot be transported by any other means, such as barges or another pipeline. Some of these agreements can also include provisions to guarantee a return to the pipeline, enabling the pipeline to recover its investment in the initial years despite the uncertainty in production volumes, by providing for an annual transportation rate adjustment over a fixed period of time to achieve a fixed rate of return. The calculation for the fixed rate of return is usually based on actual project costs and operating costs. At the end of the fixed period, some rates will be locked in at the last calculated rate and adjusted thereafter based on the FERC’s index.

Our offshore T&D agreements require shippers to dedicate production from specific fields for a fixed term, generally for life of the facility or lease. In addition, some T&D agreements require a minimum volume to be delivered for a fixed term. If the producer falls below the minimum volume for the specified term, they are required to make a payment for the volume deficiency at the agreed transportation rate. T&D agreements may, but typically do not, offer firm space on the pipeline in question. If a segment of the pipeline system is oversubscribed, space is prorated in accordance with the then-published rules and regulations of the pipeline.

Certain offshore systems provide for the transportation of crude oil through the use of buy/sell arrangements where crude is purchased at the receipt location into the pipeline and sold back to the counterparty at the destination at that price plus a transportation differential. Other systems provide for the transportation of crude oil via private Oil Transportation Agreements (“OTAs”). These OTAs are a mix of term and life-of-lease transportation agreements.

Refined Products Pipelines

We own interests in several refined products pipeline systems across approximately 7,400 miles spanning from the Gulf Coast to both the Midwest and the East Coast. These pipeline systems are regulated primarily by PHMSA and the FERC and transport refined products with many different specifications and for numerous shippers. The refined products pipelines connect refineries to both long-haul transportation pipelines and marketing terminals. These pipelines serve a diverse set of customers, including refiners, marketers, airports and airlines.

These refined products pipeline systems generate revenue under various types of rates and contracts, including ship-or-pay contracts that are renewable at the election of the shipper and may be indexed annually, joint tariff division agreements, FERC-approved rates subject to annual indexing and market-based rates. Additionally, there is an auction program on one system for certain excess capacity when the pipeline is fully subscribed.

Terminals and Storage

We own an interest in certain logistics assets in Louisiana, as well as interests in refined products and crude terminals located in Washington, Texas, Illinois and Oregon. Our logistics assets are comprised of crude, chemicals, intermediate and finished product pipelines, storage tanks, docks, truck and rail racks and supporting infrastructure. We generate revenue on these assets pursuant to terminaling services agreements with related parties, which are treated as a failed sale leaseback for accounting purposes.

Our refined products terminals receive refined products from pipelines and, in certain cases, barges, ships or railroads, and distribute them to third parties, who in turn deliver them to end-users and retail outlets. These terminals play a key role in

10

moving products to the end-user market by providing efficient product receipt, storage and distribution capabilities, inventory management, ethanol and biodiesel blending, and other ancillary services that include the injection of various additives. For each of these terminals, revenue, based on throughput, is generated via a single, long-term, terminaling services agreement with a related party, which is treated as an operating lease for accounting purposes. Each agreement provides for a guaranteed minimum throughput.

Our crude terminal feeds regional refineries and offers strategic trading opportunities by providing storage services for several customers and supplying refineries. Our storage tanks are 100% contracted via four terminal services agreements with expirations ranging from mid-2022 through 2024.

Other Midstream Assets

We have interests in certain other midstream assets. We own an interest in a network of refinery gas pipelines connecting multiple refineries and plants operated along the Gulf Coast to Shell chemical sites. The pipelines transport refinery gas, which is a mix of methane, natural gas liquids and olefins. This system generates revenue under transportation services agreements that include minimum revenue commitments and are treated as operating leases for accounting purposes. The contracts require a specified monthly payment regardless of volume shipped, and shippers do not receive a credit for unused volume in a given month to use in future months.

We also own interests in gas gathering systems that provide gathering and transportation for multiple gas producers and third-party gas shippers.

Additionally, our interest in a pipeline that connects the LOOP Clovelly Salt Dome storage facility to the active trading hub of St. James, Louisiana allows for crude oil arriving at the terminal to be dispatched to several local refineries or to other pipeline systems.

Pipeline and Terminal Systems Capacity

The following table sets forth certain information regarding our pipeline and terminal systems as of December 31, 2021:

| Pipeline System/Terminal System | Approximate Capacity (kbpd) (2) | Approximate Tank Storage Capacity (kbls) | ||||||||||||

| Onshore Crude Oil Pipelines | ||||||||||||||

| Zydeco crude oil system – Mainlines | ||||||||||||||

| Houston to Port Neches | 250 | — | ||||||||||||

| Port Neches to Houma | 375 | — | ||||||||||||

| Houma to Clovelly | 425 | — | ||||||||||||

| Houma to St James | 270 | — | ||||||||||||

| Delta crude oil system | 420 | — | ||||||||||||

| Offshore Crude Oil Pipelines | ||||||||||||||

| Amberjack crude oil system | ||||||||||||||

| Jack St. Malo | 200 | — | ||||||||||||

| Tahiti | 300 | — | ||||||||||||

| ADP 24” | 300 | — | ||||||||||||

| Jackalope | 200 | — | ||||||||||||

| Genesis | 50 | — | ||||||||||||

| Auger crude oil system | ||||||||||||||

| Enchilada Platform to Ship Shoal 28P | 200 | — | ||||||||||||

| 14/16” Auger export line | 150 | — | ||||||||||||

| Na Kika crude oil system | 160 | — | ||||||||||||

Mars crude oil system (1) | ||||||||||||||

| Mars TLP to West Delta 143 | 100 | — | ||||||||||||

| Olympus TLP to West Delta 143 | 100 | — | ||||||||||||

11

| West Delta 143 to Fourchon | 400 | — | ||||||||||||

| Fourchon to Clovelly | 600 | — | ||||||||||||

| Poseidon crude oil system | 350 | — | ||||||||||||

| Odyssey crude oil system | 220 | — | ||||||||||||

| Mattox crude oil system | 300 | — | ||||||||||||

| Proteus crude oil system | ||||||||||||||

| Thunder Horse TLP to South Pass 89E | 425 | — | ||||||||||||

| Endymion crude oil system | ||||||||||||||

| South Pass 89E to Clovelly | 425 | — | ||||||||||||

| Refined Products Pipelines | ||||||||||||||

| Bengal product system | ||||||||||||||

| Norco to Baton Rouge tank farm | 305 | — | ||||||||||||

| Colonial product system | 2,500 | — | ||||||||||||

| Explorer product system | 660 | — | ||||||||||||

| Terminals and Storage | ||||||||||||||

Triton refined products terminals (2) | ||||||||||||||

| Colex | — | 2,585 | ||||||||||||

| Des Plaines | — | 1,060 | ||||||||||||

| Portland | — | 405 | ||||||||||||

| Seattle | — | 520 | ||||||||||||

Norco Assets (3) | — | 10,800 | ||||||||||||

| Lockport terminal system | — | 2,000 | ||||||||||||

| Other Midstream Assets | ||||||||||||||

Refinery Gas Pipelines (4) | ||||||||||||||

| Houston Ship Channel | 3,960 | — | ||||||||||||

| Texas City | 5,280 | — | ||||||||||||

| Garyville – Norco | 3,720 | — | ||||||||||||

| Convent to Garyville | 3,840 | — | ||||||||||||

| Norco – Paraffinic | 3,720 | — | ||||||||||||

Permian Basin gas gathering system (4) | 240 | — | ||||||||||||

| LOCAP pipeline system and storage facility | 1,700 | 3,200 | ||||||||||||

Cleopatra gas gathering system (4) | ||||||||||||||

| Atlantis TLP to Ship Shoal 332A | 500 | — | ||||||||||||

(1) In addition to the pipeline capacity above, Mars also has storage capacity leases of storage caverns with a related party.

(2) The Des Plaines, Portland and Seattle refined products terminals have truck racks that are not included in the above table.

(3) The capacity for the Norco Assets shown above is comprised of 104 tanks. The Norco Assets also include associated pipelines, docks, trucks and rail racks that are not included in the above table.

(4) The approximate capacity information presented is in kbpd with the exception of the approximate capacity related to Cleopatra gas

gathering system and Permian Basin, which are presented in mscf/d, and Refinery Gas Pipeline, which is presented in klbs/d.

Our Relationship with Shell

Shell is an international energy company with expertise in the exploration, production, refining and marketing of oil and natural gas, and the manufacturing and marketing of chemicals. As one of the largest producers in the Gulf of Mexico, Shell is currently developing several deepwater prospects and associated infrastructure. In addition to its offshore production, Shell has onshore exploration and production interests and produces crude oil and natural gas throughout North America. Shell’s downstream portfolio includes interests in chemical processing plants throughout the United States, as well as a refinery on the

12

Gulf Coast. Shell’s portfolio of midstream assets provides key infrastructure required to transport and store crude oil and refined products for Shell and third parties. Shell’s ownership interests in transportation and midstream assets include crude oil and refined products pipelines, crude oil and refined products terminals, chemicals pipelines, natural gas pipelines and processing plants and LNG infrastructure assets. Shell or its affiliates are customers of most of our businesses.

SPLC is Shell’s principal midstream subsidiary in the United States. As of December 31, 2021, SPLC owned our general partner, a 68.5% limited partner interest in us and all of our Series A Preferred Units.

Customers

See Note 14 — Transactions with Major Customers and Concentration of Credit Risk in the Notes to Consolidated Financial Statements included in Part II, Item 8 of this report.

Competition

Our pipeline systems compete primarily with other interstate and intrastate pipelines and with marine and rail transportation. Some of our competitors may expand or construct transportation systems that would create additional competition for the services we provide to our customers. For example, newly constructed transportation systems in the onshore Gulf of Mexico region may increase competition in the markets where our pipelines operate. In addition, future pipeline transportation capacity could be constructed in excess of actual demand in the market areas we serve, which could reduce the demand for our services and could lead to the reduction of the rates that we receive for our services. While we do see some variation from quarter-to-quarter resulting from changes in our customers’ demand for transportation, this risk has historically been mitigated by the long-term, fixed-rate basis upon which we contracted our capacity.

Competition among onshore common carrier crude oil pipelines is based primarily on posted tariffs, quality of customer service and connectivity to sources of supply and demand. We believe that our position along the Gulf Coast provides a unique level of service to our customers. Our pipelines and terminals face competition from a variety of alternative transportation methods including rail, water borne movements (including barging, shipping and imports) and other pipelines that service the same origins or destinations as our pipelines.

Our offshore crude oil pipelines are primarily supported by life-of-lease transportation agreements or direct connected production, which bears high switching costs in the form of capital investment or volume dedications. However, our offshore pipelines will compete for new production on the basis of geographic proximity to the production, cost of connection, available capacity, transportation rates and access to preferred onshore markets. The principal competition for our offshore pipelines include other crude oil pipeline systems, as well as producers who may elect to build or utilize their own production handling facilities. In addition, the ability of our offshore pipelines to access future oil and gas reserves will be subject to our ability, or the producers’ ability, to fund the capital expenditures required to connect to the new production. In general, our offshore pipelines are not subject to regulatory rate-making authority, and the rates our offshore pipeline charges for services are dependent on market conditions.

Competition for refined product transportation in any particular area is affected significantly by the end market demand for the volume of products produced by refineries in that area, the availability of products in that area and the cost of transportation to that area from distant refineries. In light of current market conditions, we expect greater competition in the markets in which we provide refined product transportation.

Our storage terminal competes with surrounding providers of storage tank services. Some of our competitors have expanded terminals and built new pipeline connections, and third parties may construct pipelines that bypass our location. These, or similar events, could have a material adverse impact on our operations.

Our refined products terminals generally compete with other terminals that serve the same markets. These terminals may be owned by major integrated oil and gas companies or by independent terminaling companies. While fees for terminal storage and throughput services are not regulated, they are subject to competition from other terminals serving the same markets. However, our contracts provide for stable, long-term revenue, which is not impacted by market competitive forces.

See “Management's Discussion and Analysis of Financial Condition and Results of Operations — Factors Affecting Our Business and Outlook” for additional information.

13

FERC and State Common Carrier Regulations

Our assets are subject to regulation by various federal, state and local agencies; for example, our interstate common carrier pipeline systems are subject to economic regulation by the FERC. Intrastate pipeline systems are regulated by the appropriate state agency.

The FERC regulates interstate transportation on our common carrier pipeline systems under the ICA, the EPAct and the rules and regulations promulgated under those laws. FERC regulations require that rates and terms and conditions of service for interstate service pipelines that transport crude oil and refined products (collectively referred to as “petroleum pipelines”) and certain other liquids be just and reasonable and must not be unduly discriminatory or confer any undue preference upon any shipper. The FERC’s regulations also require interstate common carrier petroleum pipelines to file with the FERC and publicly post tariffs stating their interstate transportation rates and terms and conditions of service.

Under the ICA, the FERC or interested persons may challenge existing or proposed new or changed rates, services or terms and conditions of service. The FERC is authorized to investigate such charges and may suspend the effectiveness of a new rate for up to seven months. A successful challenge could result in a common carrier pipeline paying refunds of revenue collected in excess of the just and reasonable rate, together with interest for the period the rate was in effect, if any. The FERC may also order a pipeline to reduce its rates prospectively, and may require a common carrier pipeline to pay shippers reparations retroactively for rate overages for a period of up to two years prior to the filing of a complaint. The FERC also has the authority to change terms and conditions of service if it determines that they are unjust or unreasonable or unduly discriminatory or preferential.

EPAct required the FERC to establish a simplified and generally applicable methodology to adjust tariff rates for inflation for interstate petroleum pipelines. As a result, the FERC adopted an indexing rate methodology which, as currently in effect, allows common carriers to change their rates within prescribed ceiling levels that are tied to changes in the U.S. Producer Price Index for Finished Goods (“PPI-FG”). The indexing methodology is applicable to existing rates, including grandfathered rates, with the exclusion of market-based rates. Rate increases made under the index methodology are presumed to be just and reasonable and require a protesting party to demonstrate that the portion of the rate increase resulting from application of the index is substantially in excess of the pipeline’s increase in costs. Despite these procedural limits on challenging the indexing of rates, the overall rates are not entitled to any specific protection against rate challenges. Under the indexing rate methodology, in any year in which the index is negative, pipelines must file to lower their rates if those rates would otherwise be above the rate ceiling. The FERC’s indexing methodology is subject to review every five years.

While common carrier pipelines often use the indexing methodology to change their rates, common carrier pipelines may elect to support proposed rates by using other methodologies such as cost-of-service rate making, market-based rates and settlement rates. Rates for a new service on a common carrier pipeline can be established through a negotiated rate with an unaffiliated shipper or via a cost-of-service approach. The rates shown in our FERC tariffs have been established using the indexing methodology, by settlement or by negotiation.

EPAct also deemed certain interstate petroleum pipeline rates then in effect to be just and reasonable under the ICA. These rates are commonly referred to as “grandfathered rates.” For example, Colonial’s rates in effect at the time of the passage of EPAct for interstate transportation service were deemed just and reasonable and therefore are grandfathered. New rates have since been established after EPAct for certain grandfathered pipeline systems such as Zydeco. The FERC may change grandfathered rates upon complaint only after it is shown that a substantial change has occurred since enactment in either the economic circumstances or the nature of the services that were a basis for the rate.

With respect to indexing, in 2020, the FERC commenced a proceeding to set the indexing formula for the five years commencing July 1, 2021. While the FERC initially adopted a formula of PPI-FG plus 0.78% on December 17, 2020, the FERC issued an order on rehearing on January 20, 2022 that revised the formula to PPI-FG minus 0.21%. The lower indexing adjustment resulted from the FERC adjusting the data set used to assess pipeline cost; taking into account the elimination of the income tax allowance and previously accrued accumulated deferred income tax (“ADIT”) balances for master limited partnership (“MLP”)-owned pipelines; and using updated cost data for 2014. The FERC’s order on rehearing is subject to potential judicial review. The rehearing order requires pipelines to recalculate their rate ceiling levels using the PPI-FG minus 0.21% formula for the period July 1, 2021 to June 30, 2022. For any rate that exceeds the recalculated ceiling level, the pipeline is required to file a rate reduction with the FERC to be effective March 1, 2022. We do not expect these rate recalculations to have a material effect on our financial position, operating results or cash flows.

We cannot predict whether or to what extent the index factor may change in the future.

14

In 2018, with respect to cost-of-service ratemaking, the FERC issued a policy statement and related orders that eliminated the recovery of an income tax allowance by MLP oil and gas pipelines in cost-of-service-based rates, although an MLP may claim in an individual proceeding that it is entitled to an income tax allowance based on a demonstration that its recovery of an income tax allowance does not result in a “double-recovery of investors’ income tax costs.” To the extent that we charge cost-of-service based rates, those rates could be affected by any changes in the FERC’s income tax allowance policy to the extent our rates are subject to complaint or challenge by the FERC acting on its own initiative, or to the extent that we propose new cost-of-service rates or changes to our existing rates.

In May 2021, Zydeco, Mars and LOCAP filed with the FERC to decrease rates subject to the FERC’s indexing adjustment methodology that were previously at their ceiling levels by 0.5812% starting on July 1, 2021 and are required by the January 20, 2022 rehearing order to recalculate their ceiling levels and file a rate reduction for any rates that exceed the recalculated ceiling to be effective March 1, 2022. Rate complaints are currently pending at the FERC in Docket Nos. OR18-7-002, et al. challenging Colonial’s tariff rates, its market power, and its practices and charges related to transmix and product volume loss. A partial initial decision from the Administrative Law Judge was issued on December 1, 2021 finding that Colonial lacks the ability to exercise market power in the 90-county Gulf Coast geographic origin market, but no longer lacks the ability to exercise market power in the 16-county Tuscaloosa-Moundville geographic origin market. The partial initial decision also found that Colonial’s method of net recoveries of product loss is unjust and unreasonable and that Colonial should adopt a fixed allowance oil deduction for shortages in deliveries and determine the amount of reparations, if any, owed to shippers. The partial initial decision is a recommendation to the FERC based on the evidence received into the record by the Administrative Law Judge. The FERC may decide to adopt the recommendations made in full or part or make different determinations. If the FERC adopts the partial initial decision in whole, in addition to the changes in product loss charges described above, which may adversely affect Colonial, Colonial’s rates in respect of the 16-county Tuscaloosa-Moundville geographic origin market will no longer be market-based and could be reduced. The parties to the case will be filing briefs to argue for or against the recommendations, which will be considered by the FERC in its ruling. The timing of such ruling is unknown. For the issues not covered by the initial decision, the deadline for the Administrative Law Judge to issue a partial initial decision covering those issues is April 29, 2022.

Intrastate services provided by certain of our pipeline systems are subject to regulation by state regulatory authorities, such as the TRRC, which currently regulates Zydeco and Colonial pipeline rates, and the LPSC, which currently regulates the Zydeco, Mars, Delta and Colonial pipeline rates. State agencies typically require intrastate petroleum pipelines to file their rates with the agencies and permit shippers to challenge existing rates and proposed rate increases. State agencies may also investigate rates, services and terms and conditions of service on their own initiative. State regulatory commissions could limit our ability to increase our rates or to set rates based on our costs or could order us to reduce our rates and require the payment of refunds to shippers.

Certain pipelines, including Auger, Na Kika, Amberjack, Odyssey, Poseidon, Proteus, Endymion, Cleopatra and parts of Mars, are located offshore in the Outer Continental Shelf. As such, they are not subject to FERC or state rate regulation but are subject to the Outer Continental Shelf Lands Act (“OCSLA”). Under the OCSLA, we must provide open and nondiscriminatory access to both pipeline owner(s) and non-owner shippers and comply with other requirements.

Pipeline and Terminal Safety

Our assets are subject to strict safety laws and regulations. Our transportation and storage of crude oil, refined products and dry gas involve risks that hazardous liquids or gas may be released into the environment, potentially causing harm to the public or the environment. In turn, such incidents may result in substantial expenditures for response actions, significant government penalties, liability to government agencies for natural resources damages, liability and/or reparations to landowners and significant business interruption. PHMSA of the DOT has adopted safety regulations with respect to the design, construction, operation, maintenance, inspection and management of most of our assets. In addition, some states have adopted regulations, similar to existing PHMSA regulations, for intrastate gathering and transmission lines. The states in which most of our assets are located, Texas and Louisiana, are among the states that have developed regulatory programs that parallel the federal regulatory scheme and are applicable to intrastate pipelines transporting hazardous liquids and gases. The few assets not covered by PHMSA are regulated by the U.S. Environmental Protection Agency (“EPA”) and various state agencies and are designed and maintained to industry accepted codes and standards. PHMSA regulations contain requirements for the development and implementation of pipeline integrity management programs, which include the inspection and testing of pipelines and necessary maintenance or repairs. These regulations also require that pipeline operation and maintenance personnel meet certain qualifications and are included in a drug and alcohol testing program, and that pipeline operators develop comprehensive spill response plans.

15

We are subject to regulation by PHMSA under the Natural Gas Pipeline Safety Act of 1968 (“NGPSA”) and the Hazardous Liquid Pipeline Safety Act of 1979 (“HLPSA”). The NGPSA delegated to PHMSA through DOT the authority to regulate gas pipelines. The HLPSA delegated to PHMSA through DOT the authority to develop, prescribe, and enforce federal safety standards for the transportation of hazardous liquids by pipeline. Every four years PHMSA is up for reauthorization by Congress and with that reauthorization comes changes to the legislative requirements that Congress sets forth for the oversight of natural gas and hazardous liquid pipelines. In 2020, the Protecting our Infrastructure of Pipelines and Enhancing Safety Act of 2020 (the “Pipes Act”) was enacted. The Pipes Act reauthorized PHMSA through 2023 and imposed a few new mandates on the agency. The law establishes a PHMSA technology pilot, authorizes a new idled pipe operating status, contains process protections for operators during PHMSA enforcement proceedings and directs PHMSA to adopt regulations to address methane leaks from pipelines. There are no self-enacting portions of this act that impact our assets. We will be engaged in the regulatory process as PHMSA issues Reports and Notices of Proposed Rulemakings to meet the requirements set out in the Pipes Act. We will continue to work with industry groups to provide comments and recommendations to PHMSA on proposed regulations to help ensure improved safety without causing undue burden to operators.

PHMSA administers compliance with these statutes and has promulgated comprehensive safety standards and regulations for the transportation of hazardous liquids by pipeline, including regulations for the design and construction of new pipeline systems or those that have been relocated, replaced or otherwise changed (Subparts C and D of 49 CFR § 195); pressure testing (Subpart E of 49 CFR § 195); operation and maintenance of pipeline systems, including inspecting and reburying pipelines in the Gulf of Mexico and its inlets, establishing programs for public awareness and damage prevention, managing the integrity of pipelines in HCAs, and managing the operation of pipeline control rooms (Subpart F of 49 CFR § 195); protecting steel pipelines from the adverse effects of internal and external corrosion (Subpart H of 49 CFR § 195); and integrity management requirements for pipelines in HCAs (49 CFR § 195.452). Gas pipelines have similar requirements (49 CFR § 192).

In early 2021, PHMSA issued a revised map of the ecological High Consequence Areas (“HCAs”) in the Gulf of Mexico. This revised map expanded the ecological HCA of the Gulf of Mexico to include previously excluded dolphin and whale habitats. The HCA now encompasses most of the Gulf of Mexico. This places most liquid pipelines in the Gulf of Mexico in an HCA and subject to the assessment requirements of 49 CFR 195.452. This may impact certain operational activity such as the frequency at which certain inspections need to be performed and the types of inspections required at those intervals. The holistic impact to our business is uncertain at this time, but we expect that all companies with comparable Gulf of Mexico operations will be similarly impacted.

On June 14, 2021, as part of the self-executing provisions of the Protecting our Infrastructure of Pipelines and Enhancing Safety Act of 2020, the PHMSA published an advisory bulletin requiring operators to update inspection and maintenance plans to address eliminating hazardous leaks and minimizing releases of natural gas by December 27, 2021. This advisory bulletin is expected to have minimal impact on our operations but will require minor updates to our inspection and maintenance manuals.

We monitor the structural integrity of our pipelines through a program of periodic internal assessments using a variety of internal inspection tools, as well as hydrostatic testing that conforms to federal standards. We accompany these assessments with a comprehensive data integration effort and repair anomalies, as required, to ensure the integrity of the pipeline. We conduct a thorough review of risks to the pipelines and perform sophisticated calculations to establish an appropriate reassessment interval for each pipeline. We use external coatings and impressed current cathodic protection systems to protect against external corrosion. We conduct all cathodic protection work in accordance with National Association of Corrosion Engineers standards and continually monitor, test and record the effectiveness of these corrosion inhibiting systems. We have robust third-party damage prevention and public awareness programs to help protect our lines from the risk of excavation and other outside force damage threats. Our tanks are inspected on a routine basis in compliance with PHMSA and EPA regulations. Every tank periodically receives a full out of service, internal inspection per American Petroleum Institute standard 653 and is repaired as necessary.

Certain aspects of our offshore pipeline operations, such as new construction and modification, are also regulated by BOEM, BSEE and the U.S. Coast Guard. On January 27, 2021, President Biden issued an Executive Order on climate directing the Department of the Interior to pause on entering into new oil and natural gas leases on public lands or offshore waters “to the extent possible” and launch a review of all existing leasing and permitting practices related to fossil fuel development on public lands and waters. The review was completed in November 2021 and recommends changes to leasing and permitting practices that, if implemented, could result in increased costs in the form of higher royalties and other charges, as well as restrictions on lands available for leasing activities. Certain lease sales resumed thereafter as a result of legal challenges to the moratorium; however on January 27, 2022, a federal judge invalidated oil and gas lease sales relating to 80 million acres in the Gulf of Mexico, concluding that the Biden administration failed to account for the associated climate change impact in auctioning off the leases. If our customers are unable to secure leases or permits, sustained reductions in exploration or production activity in

16

our areas of operation could lead to reduced utilization of our pipeline and terminal systems or reduced rates under renegotiated transportation or storage agreements. We are still evaluating the effects of the judicial decision, the executive order and our customers’ potential inability to secure leases, which could adversely affect our long-term business, financial condition, results of operation or cash flows, including our ability to make cash distributions to our unitholders.

Product Quality Standards

Refined products that we transport are generally sold by our customers for consumption by the public. Various federal, state and local agencies have the authority to prescribe product quality specifications for refined products. Changes in product quality specifications or blending requirements could reduce our throughput volumes, require us to incur additional handling costs or require capital expenditures. For example, different product specifications for different markets affect the fungibility of the refined products in our system and could require the construction of additional storage. If we are unable to recover these costs through increased revenue, our cash flows and ability to pay cash distributions could be adversely affected. In addition, changes in the product quality of the refined products we receive on our refined product pipeline systems or at our tank farms could reduce or eliminate our ability to blend refined products.

Security

We are also subject to U.S. Department of Homeland Security Chemical Facility Anti-Terrorism Standards, which are designed to regulate the security of high-risk chemical facilities, and to Transportation Security Administration Pipeline Security Guidelines. We have an internal program of inspection designed to monitor and enforce compliance with all of these requirements. We believe that we are in material compliance with all applicable laws and regulations regarding the security of our facilities.

Cybersecurity and Data Privacy

Given our dependence on Information Technology (“IT”) and Operational Technology (“OT”) for our operations and the increasing role of digital technologies across our business, cyber-security attacks could cause significant harm to our business, e.g., in the form of loss of function, diminished productivity, loss of intellectual property, litigation, regulatory fines and/or reputational damage. Shell, like many other multinational company groups, is the target of attempts to gain unauthorized access to its systems and data through various channels, including by more sophisticated and coordinated actors, which are often referred to as advanced persistent threats. The intent of these attempted attacks range from data exfiltration, to extortion, to data manipulation, to destabilization and destruction.

We and/or our Parent protect our systems through our segmented architecture and with numerous technologies in line with industry best practices. We also maintain and regularly update cybersecurity plans, policies and procedures over our own IT and OT systems. In addition, we have strict protocols in place to better ensure the cybersecurity of any third parties who connect to our networks or process our data.

While the arrangements described above are in place, we cannot guarantee against compromise. A significant cyber-attack, should it be successful, could have a material effect on our operations. We maintain incident response and business continuity plans to mitigate any impact should such an attack occur.

For example, on May 7, 2021, the computerized equipment managing the Colonial pipeline was the target of a ransomware attack. We have a 16.125% ownership interest in Colonial, which owns and operates a pipeline that runs throughout the southern and eastern United States. Colonial proactively took certain systems offline to contain the threat and it paid a ransom in cryptocurrency to regain control of the equipment.

In the aftermath of this cyber intrusion, the Transportation Security Administration (“TSA”) issued two security directives. The first, issued in May 2021, requires owners and operators of TSA-designated critical pipelines to report confirmed and potential cybersecurity incidents to the Cybersecurity and Infrastructure Security Agency (“CISA”) within 12 hours of discovery, designate a cybersecurity coordinator to be available 24 hours a day, seven days a week, review current practices and identify any gaps and related remediation measures to address cyber-related risks and report the results to the TSA and CISA within 30 days.

The second security directive, issued in July 2021, imposes additional obligations on owners and operators of TSA-designated critical pipelines. This directive requires pipeline owners and operators to develop and implement specific mitigation measures to protect against ransomware attacks and other known threats to IT and OT systems, to develop a cybersecurity contingency and recovery plan and to conduct cybersecurity assessments. We have complied with the requirements of the first directive, and

17

our team continues to work in collaboration with the TSA to complete the requirements of the second directive in a timely manner. We remain committed to working with the TSA and other companies in our industry to increase the physical and cyber security posture of our industry.

We and our affiliates collect, process and maintain significant volumes of confidential data, including personal data, which is increasingly subject to specific U.S. and global regulations, including the California Consumer Privacy Act, the UK and EU General Data Protection Regulation, and a host of new or emerging legislation in other jurisdictions in which our Parent or its affiliates operate, such as Turkey, Brazil, China and India. Many of these laws require specific transparency and security obligations, and they require us to afford certain rights to individuals. They can restrict our ability to freely transfer personal data across borders, including within Shell, and they increasingly carry significant penalties for failing to comply. They can also provide for private rights of action, including via class action.

For additional information about cybersecurity and privacy risks and the cybersecurity and privacy programs and protocols we have in place to protect against those risks, see Item 1A. Risk Factors – IT/Cyber-security/Data Privacy/Terrorism Risks in this report.

Existing Guidance

The EU GDPR came into force in May 2018. The GDPR applies to personal data and activities that may be conducted by us, directly or indirectly through vendors and subcontractors, from an establishment in the EU. As interpretation and enforcement of the GDPR evolves, it creates a range of new compliance obligations, which could cause us to incur costs or require us to change our business practices in a manner adverse to our business. Failure to comply could result in significant penalties of up to a maximum of 4% of our global turnover, which could materially adversely affect our business, reputation, results of operations and cash flows. The GDPR also requires mandatory breach notification to the appropriate regulatory authority and impacted data owners.

The CCPA became effective on January 1, 2020 and gives California residents specific rights regarding their personal information, requires that companies take certain actions, including notifications of security incidents, and applies to activities regarding personal information that may be collected by us, directly or indirectly, from California residents. In addition, the CCPA grants California residents statutory private rights of action in the case of a data breach. As interpretation and enforcement of the CCPA evolves, it creates a range of new compliance obligations, which could cause us to change our business practices, with the possibility of significant financial penalties for noncompliance.

In 2010, Shell adopted its Binding Corporate Rules (“BCRs”), which require every Shell company to provide a minimum standard of data protection irrespective of its jurisdiction of formation or operations. The BCRs were revised in 2019 and formulated based on the requirements of the GDPR, which ensures that each Shell entity maintains a baseline of compliance with current, new or emerging legislation on top of which processes for compliance with any specific local legislation can be addressed. We cannot ensure that our current practices and policies in the area of personal data protection will be sufficient to comply with all new or emerging rules or regulations applicable to us nor that they mitigate all of the associated risks to our business.

Environmental Matters

General. Our operations are subject to extensive and frequently changing federal, state and local laws, regulations and ordinances relating to the protection of the environment. Among other things, these laws and regulations govern the emission or discharge of pollutants into or onto the land, air and water, the handling and disposal of solid and hazardous wastes and the remediation of contamination. As with the industry in general, compliance with existing and anticipated environmental laws and regulations increases our overall cost of business, including our capital costs to construct, maintain, operate and upgrade equipment and facilities. While these laws and regulations affect our maintenance capital expenditures and net income, we do not believe they affect our competitive position, as the operations of our competitors are similarly affected. We believe our facilities are in substantial compliance with applicable environmental laws and regulations. However, these laws and regulations are subject to changes, or to changes in the interpretation of such laws and regulations, by regulatory authorities, and continued and future compliance with such laws and regulations may require us to incur significant expenditures. Additionally, violation of environmental laws, regulations and permits can result in the imposition of significant administrative, civil and criminal penalties, injunctions limiting our operations, investigatory or remedial liabilities or construction bans or delays in the construction of additional facilities or equipment. Moreover, a release of hydrocarbons or hazardous substances into the environment could, to the extent the event is not insured, subject us to substantial expenses, including costs to comply with applicable laws and regulations and to resolve claims by third parties for personal injury or property damage or claims by the U.S. federal government or state governments for natural resources damages. These impacts could directly and indirectly

18

affect our business and have an adverse impact on our financial position, results of operations and liquidity if we do not recover these expenditures through the rates and fees we receive for our services. We believe our competitors must comply with similar environmental laws and regulations. However, the specific impact on each competitor may vary depending on a number of factors, including, but not limited to, the type of competitor and location of its operating facilities.

We accrue for environmental remediation activities when the responsibility to remediate is probable and the amount of associated costs can be reasonably estimated. As environmental remediation matters proceed toward ultimate resolution or as additional remediation obligations arise, charges in excess of those previously accrued may be required. New or expanded environmental requirements, which could increase our environmental costs, may arise in the future. We believe we substantially comply with all legal requirements regarding the environment; however, as not all of the associated costs are fixed or presently determinable (even under existing legislation) and may be affected by future legislation or regulations, it is not possible to predict all of the ultimate costs of compliance, including remediation costs that may be incurred and penalties that may be imposed.

For additional information regarding environmental matters that impacted our business prior to 2021, refer to Part I, Items 1 and 2 — Business and Properties — Environmental Matters in our Annual Report on Form 10-K for the year ended December 31, 2020, filed with the SEC on February 23, 2021.

Air Emissions and Climate Change. Our operations are subject to the Clean Air Act and its regulations and comparable state and local statutes and regulations in connection with air emissions from our operations. Under these laws, permits may be required before construction can commence on a new source of potentially significant air emissions, and operating permits may be required for sources that are already constructed. These permits may require controls on our air emission sources, and we may become subject to more stringent regulations requiring the installation of additional emission control technologies.

Future expenditures may be required to comply with the Clean Air Act and other federal, state and local requirements for our various sites, including our pipeline and storage facilities. The impact of future legislative and regulatory developments, if enacted or adopted, could result in increased compliance costs and additional operating restrictions on our business, all of which could have an adverse impact on our financial position, results of operations and liquidity.

In December 2007, the U.S. Congress passed the Energy Independence and Security Act that created a second Renewable Fuels Standard. This standard requires the total volume of renewable transportation fuels (including ethanol and advanced biofuels) sold or introduced annually in the United States to rise to 36 billion gallons by the end of 2022. The requirements could reduce future demand for refined products and thereby have an indirect effect on certain aspects of our business.

Currently, several legislative and regulatory measures to address greenhouse gas (“GHG”) emissions (including carbon dioxide, methane and other gases) are in various phases of discussion or implementation in the United States. These measures include, but are not limited to, requirements effective in 2010 to report GHG emissions to the EPA on an annual basis and proposed federal legislation and regulation as well as state actions to develop statewide or regional programs, each of which require or could require reductions in our GHG emissions. President Biden has issued a series of Executive Orders seeking to adopt new regulations and policies to address climate change and suspend, revise or rescind prior agency actions that are identified as conflicting with the Biden Administration’s climate policies. Requiring reductions in GHG emissions could result in increased costs to (i) operate and maintain our facilities, (ii) install new emission controls at our facilities and (iii) administer and manage any GHG emissions programs, including acquiring emission credits or allotments. New requirements to address GHG emissions and climate change may also significantly affect the oil and gas production, processing, transmission and storage industry, as well as domestic refinery operations and may have an indirect effect on our business, financial condition and results of operations.

In addition, the EPA has proposed and may adopt further regulations under the Clean Air Act addressing GHGs, to which some of our facilities may become subject. For example, in November 2021, the EPA proposed new rules that would expand and strengthen emissions reduction requirements that are currently on the books for new, modified and reconstructed oil and natural gas sources, and would require states to reduce methane emissions from existing sources nationwide. Congress continues to consider legislation on GHG emissions, which may include proposals to monitor and limit emissions of GHGs, although the ultimate adoption and form of any federal legislation cannot presently be predicted. In addition, in 2016, the United States signed onto the United Nations Conference on Climate Change, which led to the creation of the Paris Agreement. The Paris Agreement requires countries to review and “represent a progression” in their intended nationally determined contributions, which set GHG emission reduction goals, every five years beginning in 2020.

19

The impact of future regulatory and legislative developments, if adopted or enacted, could result in increased compliance costs, increased utility costs, additional operating restrictions on our business and an increase in the cost of products generally. Like Shell, we actively monitor and assess these potential developments and believe we are best able to manage them when local policies provide a stable and predictable regulatory foundation for our future investments. Although such costs may impact our business directly or indirectly by impacting our facilities or operations, the extent and magnitude of that impact cannot be reliably or accurately estimated due to the present uncertainty regarding the additional measures and how they will be implemented.

In addition to the regulatory efforts described above, there have also been efforts in recent years aimed at the investment community, including investment advisors, sovereign wealth funds, public pension funds, universities and other groups, promoting the divestment of fossil fuel equities, as well as pressuring lenders and other financial services companies to limit or curtail activities with fossil fuel companies. If these efforts continue, they could have a material adverse effect on the price of our securities and our ability to access equity capital markets. Members of the investment community have begun to screen companies such as ours for sustainability performance, including practices related to GHGs and climate change, before investing in our common units. Our efforts to improve our sustainability practices, some of which are described below, may increase our costs, and we may be forced to implement uneconomic technologies in order to improve our sustainability performance and to meet specific requirements to perform services for certain customers.

Shell has publicly recognized that GHG emissions are contributing to the warming of the climate system and stated its support for the goals of the Paris Agreement. In 2017, Shell announced its “Net Carbon Footprint” ambition, and subsequently issued the Shell Energy Transition Report in 2018 and the Shell Sustainability Report in 2020, describing, among other things, Shell’s approach to the energy transition and its plans to lower its overall carbon footprint through various measures. Shell is seeking cost-effective ways to manage GHG emissions in line with its “Net Carbon Footprint” ambition and intends to enable customers to make lower-carbon-intensity choices by bringing lower-carbon-intensity products to the market aligned with demand. Shell also aims to reduce the GHG intensity of its portfolio while continuing to work on improving the energy efficiency of its existing operations. Moreover, Shell has a climate change risk management structure in place, which is supported by standards, policies and controls, and actively monitors the GHG emissions of all its assets, including us, as well as the lifecycle of its products, to quantify future regulatory costs related to GHG or other climate-related policies. As a member of the Shell group of companies, we participate in and support these various measures, policies and initiatives and, as such, are evaluating the appropriate integration of these practices and procedures into our own operating framework.

Waste Management and Related Liabilities. To a large extent, the environmental laws and regulations affecting our operations relate to the release of hazardous substances or solid wastes into soils, groundwater and surface water, and include measures to control pollution of the environment. These laws generally regulate the generation, storage, treatment, transportation and disposal of solid and hazardous waste. They also require corrective action, including investigation and remediation, at a facility where such waste may have been released or disposed.

CERCLA. The Comprehensive Environmental Response, Compensation, and Liability Act (“CERCLA”), which is also known as Superfund, and comparable state laws impose liability, without regard to fault or to the legality of the original conduct, on certain classes of persons that contributed to the release of a “hazardous substance” into the environment. These persons include the former and present owner or operator of the site where the release occurred and the transporters and generators of the hazardous substances found at the site.