| 0 Supplemental Financial Presentation August 2024 Offering everyone a piece of the American spirit—one handshake at a time. |

| 1 Important Information Forward-Looking Statements This presentation contains forward-looking statements that are subject to risks and uncertainties. All statements other than statements of historical fact included in this presentation are forward-looking statements. You can identify forward-looking statements by the fact that they generally include words such as "anticipate," "estimate," "expect," "project," "plan,“ "intend," "believe," “outlook” and other words of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events but not all forward-looking statements contain these identifying words. These forward-looking statements are based on assumptions that Boot Barn Holdings, Inc.’s (the “Company,” “we,” “us,” and “our”) management has made in light of their industry experience and on their perceptions of historical trends, current conditions, expected future developments and other factors that they believe are appropriate under the circumstances. As you consider this presentation, you should understand that these statements are not guarantees of performance or results. They involve risks, uncertainties (some of which are beyond the Company’s control) and assumptions. These risks, uncertainties and assumptions include, but are not limited to, the following: decreases in consumer spending due to declines in consumer confidence, local economic conditions or changes in consumer preferences; the Company’s ability to effectively execute on its growth strategy; and the Company’s failure to maintain and enhance its strong brand image, to compete effectively, to maintain good relationships with its key suppliers, and to improve and expand its exclusive product offerings. The Company discusses the foregoing risks and other risks in greater detail under the heading “Risk factors” in the periodic reports filed by the Company with the Securities and Exchange Commission. Although the Company believes that these forward-looking statements are based on reasonable assumptions, you should be aware that many factors could affect the Company’s actual financial results and cause them to differ materially from those anticipated in the forward-looking statements. Because of these factors, the Company cautions that you should not place undue reliance on any of these forward-looking statements. New risks and uncertainties arise from time to time, and it is impossible for the Company to predict those events or how they may affect the Company. Further, any forward-looking statement speaks only as of the date on which it is made. Except as required by law, the Company does not intend to update or revise the forward-looking statements in this presentation after the date of this presentation. Industry and Market Information Statements in this presentation concerning our industry and the markets in which we operate, including our general expectations and competitive position, business opportunity and market size, growth and share, are based on information from independent industry organizations and other third-party sources, data from our internal research and management estimates. Management estimates are derived from publicly available information and the information and data referred to above and are based on assumptions and calculations made by us based upon our interpretation of such information and data. The information and data referred to above are imprecise and may prove to be inaccurate because the information cannot always be verified with complete certainty due to the limitations on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties. As a result, please be aware that the data and statistical information in this presentation may differ from information provided by our competitors or from information found in current or future studies conducted by market research institutes, consultancy firms or independent sources. Recent Developments Our business and opportunities for growth depend on consumer discretionary spending, and as such, our results are particularly sensitive to economic conditions and consumer confidence. Inflation and other challenges affecting the global economy could impact our operations and will depend on future developments, which are uncertain. These and other effects make it more challenging for us to estimate the future performance of our business, particularly over the near-to-medium term. For further discussion of the uncertainties and business risks affecting the Company, see the sections captioned “Risk factors” in our periodic reports filed with the Securities and Exchange Commission. |

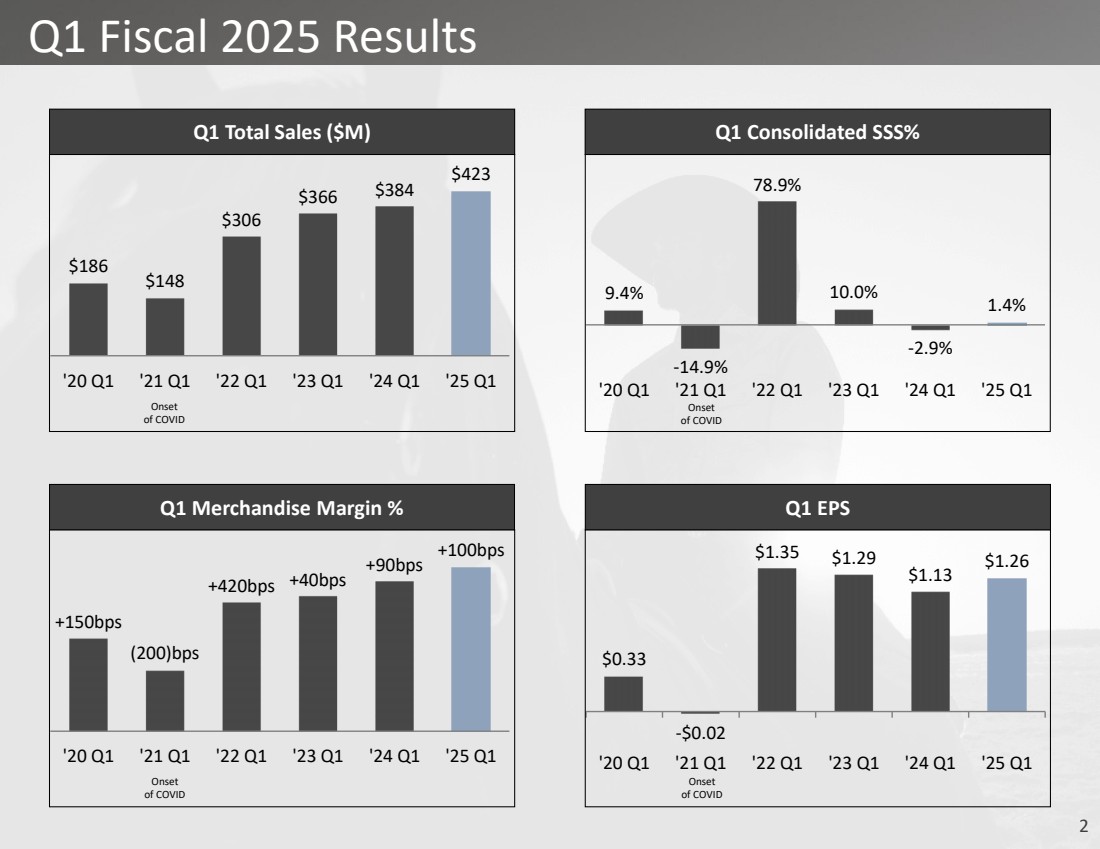

| 2 Q1 Fiscal 2025 Results $186 $148 $306 $366 $384 $423 '20 Q1 '21 Q1 '22 Q1 '23 Q1 '24 Q1 '25 Q1 Q1 Total Sales ($M) 9.4% -14.9% 78.9% 10.0% -2.9% 1.4% '20 Q1 '21 Q1 '22 Q1 '23 Q1 '24 Q1 '25 Q1 Q1 Consolidated SSS% +150bps (200)bps +420bps +40bps +90bps +100bps '20 Q1 '21 Q1 '22 Q1 '23 Q1 '24 Q1 '25 Q1 Q1 Merchandise Margin % $0.33 -$0.02 $1.35 $1.29 $1.13 $1.26 '20 Q1 '21 Q1 '22 Q1 '23 Q1 '24 Q1 '25 Q1 Q1 EPS Onset of COVID Onset of COVID Onset of COVID Onset of COVID |

| 3 Strategic Initiatives Update 1 2 3 4 New Stores Same Store Sales Omni-Channel Merchandise Margin & Exclusive Brands |

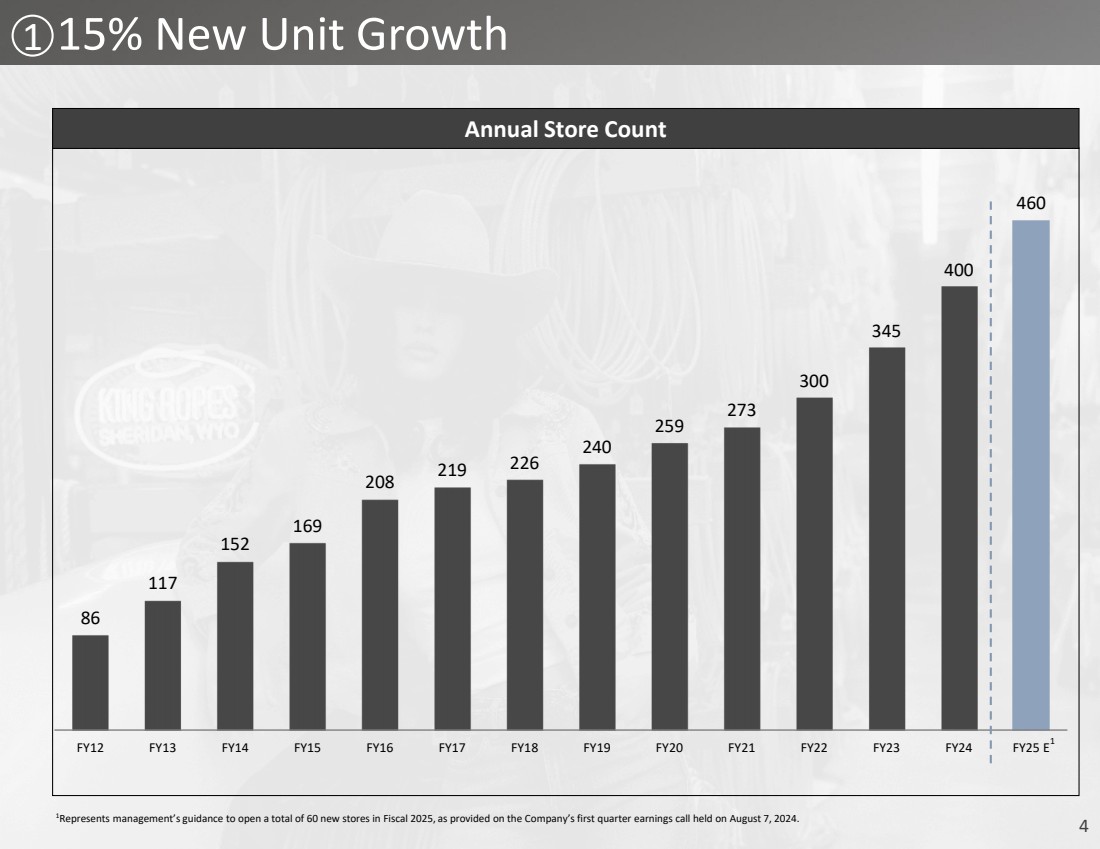

| 4 15% New Unit Growth 86 117 152 169 208 219 226 240 259 273 300 345 400 460 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25 E Annual Store Count 1 1Represents management’s guidance to open a total of 60 new stores in Fiscal 2025, as provided on the Company’s first quarter earnings call held on August 7, 2024. 1 |

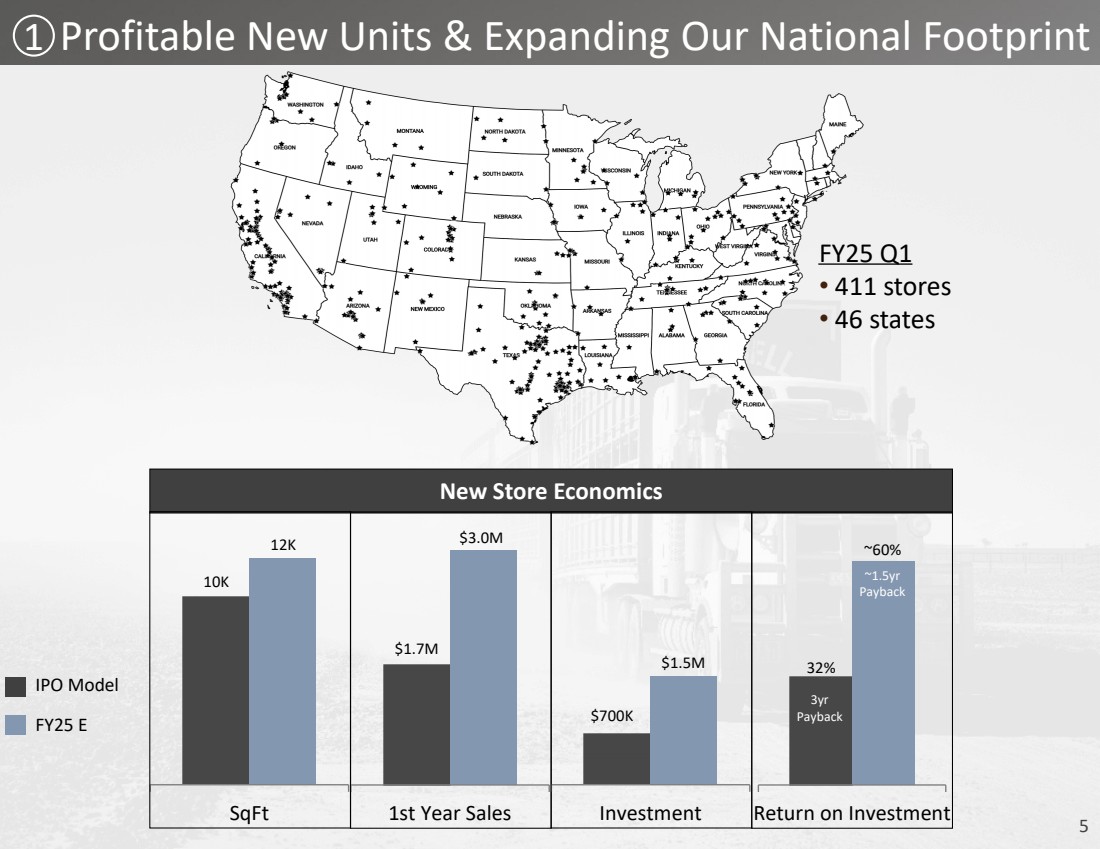

| 5 1 Profitable New Units & Expanding Our National Footprint FY25 Q1 • 411 stores • 46 states New Store Economics SqFt $1.7M $3.0M 1st Year Sales $700K Investment Return on Investment FY25 E 3yr Payback ~1.5yr Payback IPO Model $1.5M 32% 12K ~60% 10K |

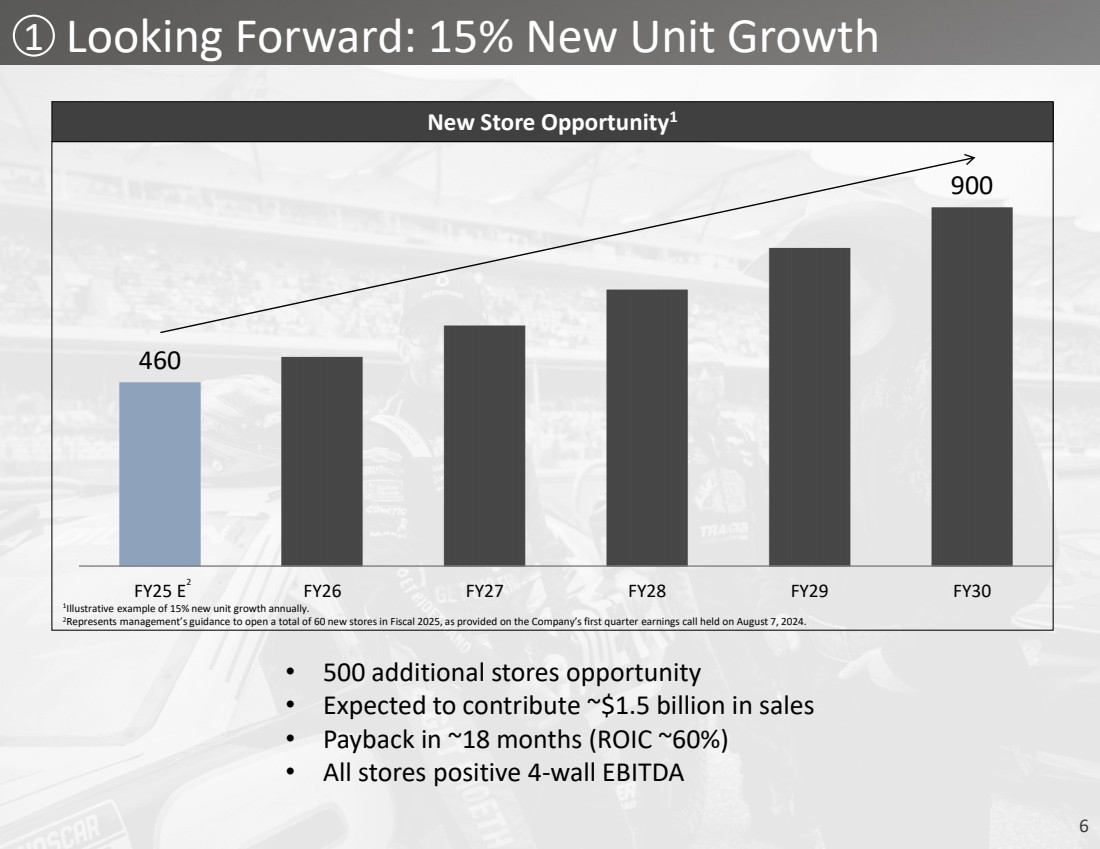

| 6 460 900 FY25 E FY26 FY27 FY28 FY29 FY30 1 Illustrative example of 15% new unit growth annually. 2Represents management’s guidance to open a total of 60 new stores in Fiscal 2025, as provided on the Company’s first quarter earnings call held on August 7, 2024. New Store Opportunity1 Looking Forward: 15% New Unit Growth • 500 additional stores opportunity • Expected to contribute ~$1.5 billion in sales • Payback in ~18 months (ROIC ~60%) • All stores positive 4-wall EBITDA 1 2 |

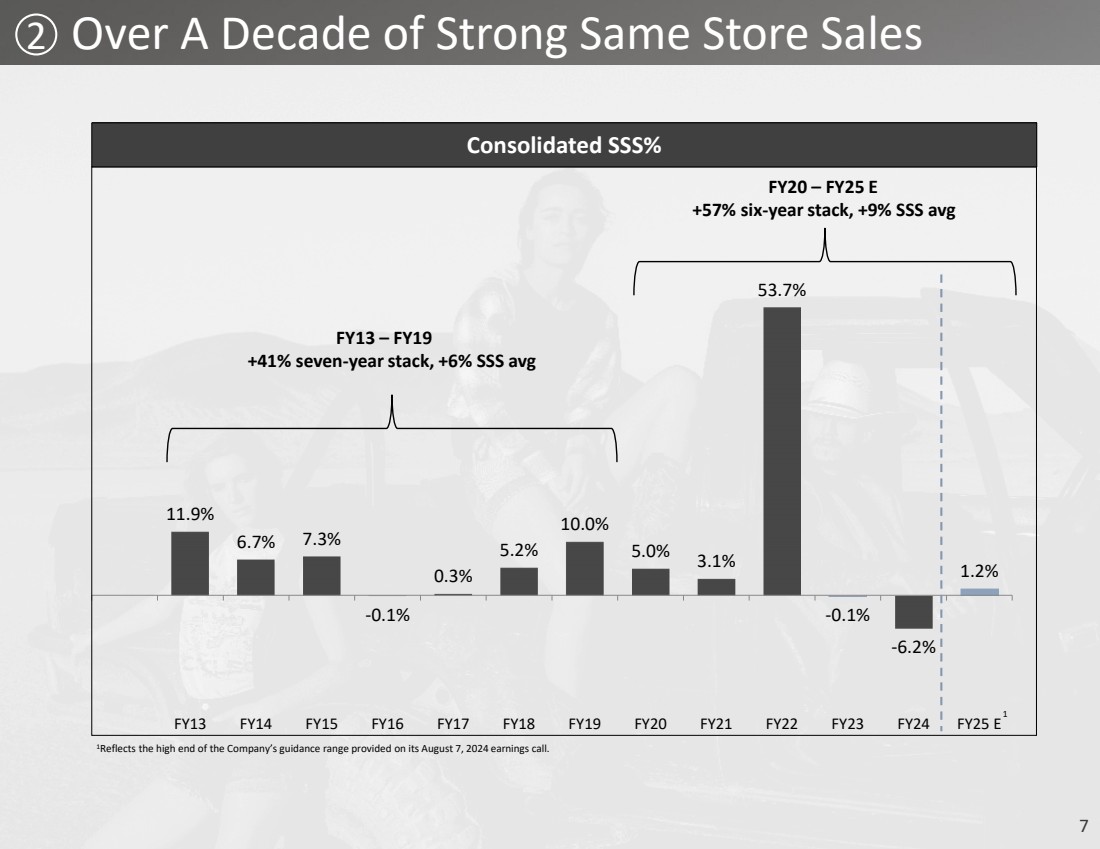

| 7 11.9% 6.7% 7.3% -0.1% 0.3% 5.2% 10.0% 5.0% 3.1% 53.7% -0.1% -6.2% 1.2% FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25 E Consolidated SSS% 2 Over A Decade of Strong Same Store Sales FY13 – FY19 +41% seven-year stack, +6% SSS avg FY20 – FY25 E +57% six-year stack, +9% SSS avg 1 1Reflects the high end of the Company’s guidance range provided on its August 7, 2024 earnings call. |

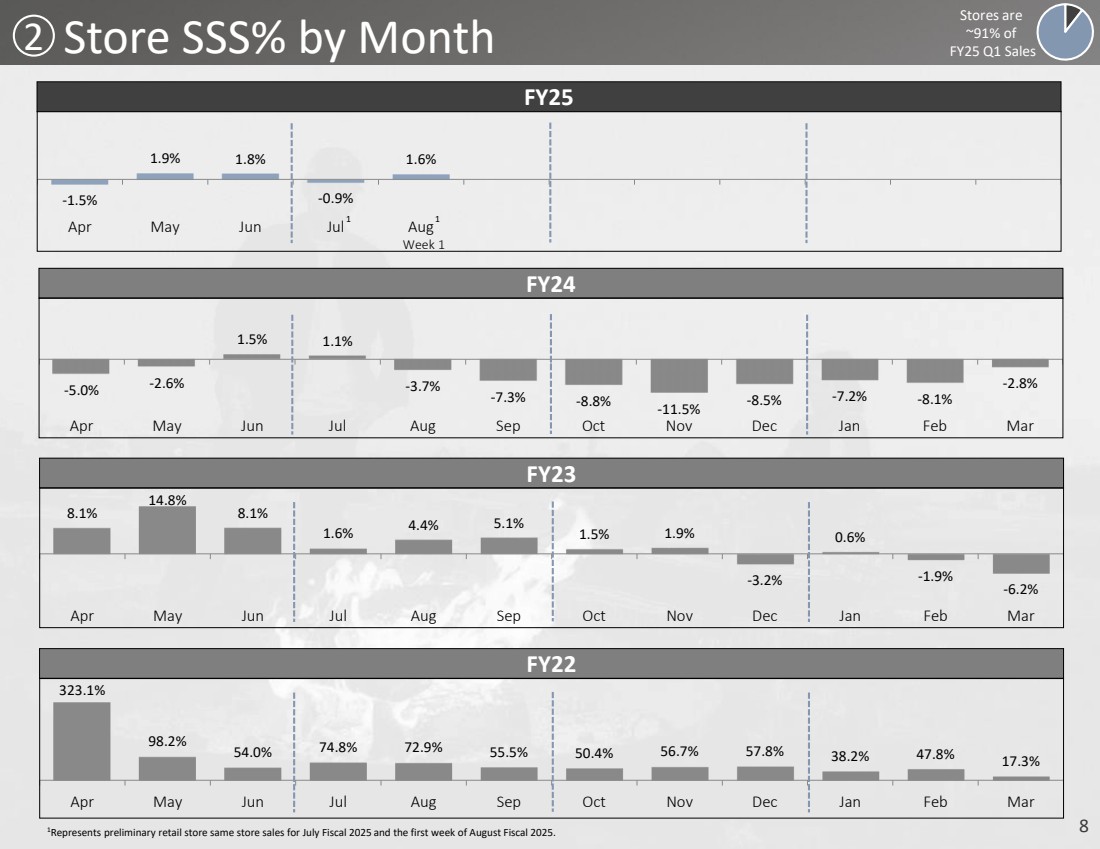

| 8 -1.5% 1.9% 1.8% -0.9% 1.6% Apr May Jun Jul Aug 2 Store SSS% by Month FY24 -5.0% -2.6% 1.5% 1.1% -3.7% -7.3% -8.8% -11.5% -8.5% -7.2% -8.1% -2.8% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar FY25 FY23 8.1% 14.8% 8.1% 1.6% 4.4% 5.1% 1.5% 1.9% -3.2% 0.6% -1.9% -6.2% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Stores are ~91% of FY25 Q1 Sales 1Represents preliminary retail store same store sales for July Fiscal 2025 and the first week of August Fiscal 2025. FY22 323.1% 98.2% 54.0% 74.8% 72.9% 55.5% 50.4% 56.7% 57.8% 38.2% 47.8% 17.3% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar 1 1 Week 1 |

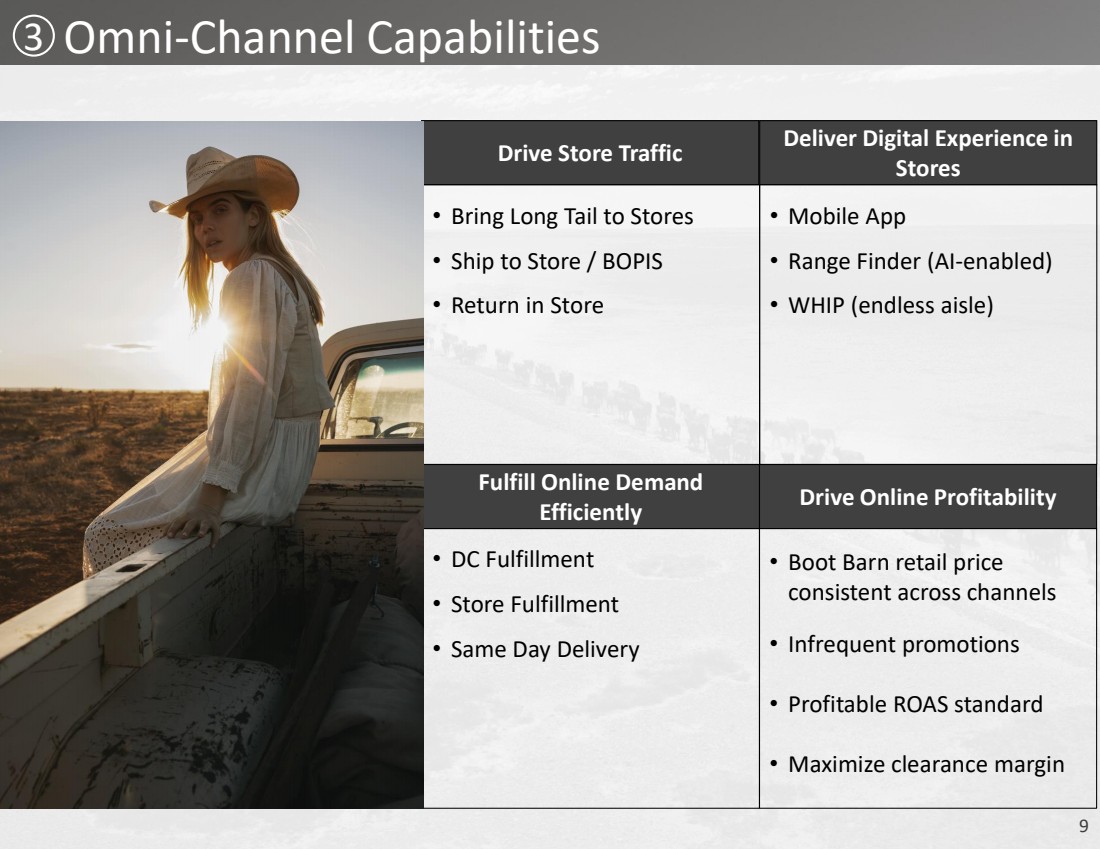

| 9 3 Omni-Channel Capabilities Drive Store Traffic • Bring Long Tail to Stores • Ship to Store / BOPIS • Return in Store Deliver Digital Experience in Stores • Mobile App • Range Finder (AI-enabled) • WHIP (endless aisle) Fulfill Online Demand Efficiently • DC Fulfillment • Store Fulfillment • Same Day Delivery Drive Online Profitability • Boot Barn retail price consistent across channels • Infrequent promotions • Profitable ROAS standard • Maximize clearance margin |

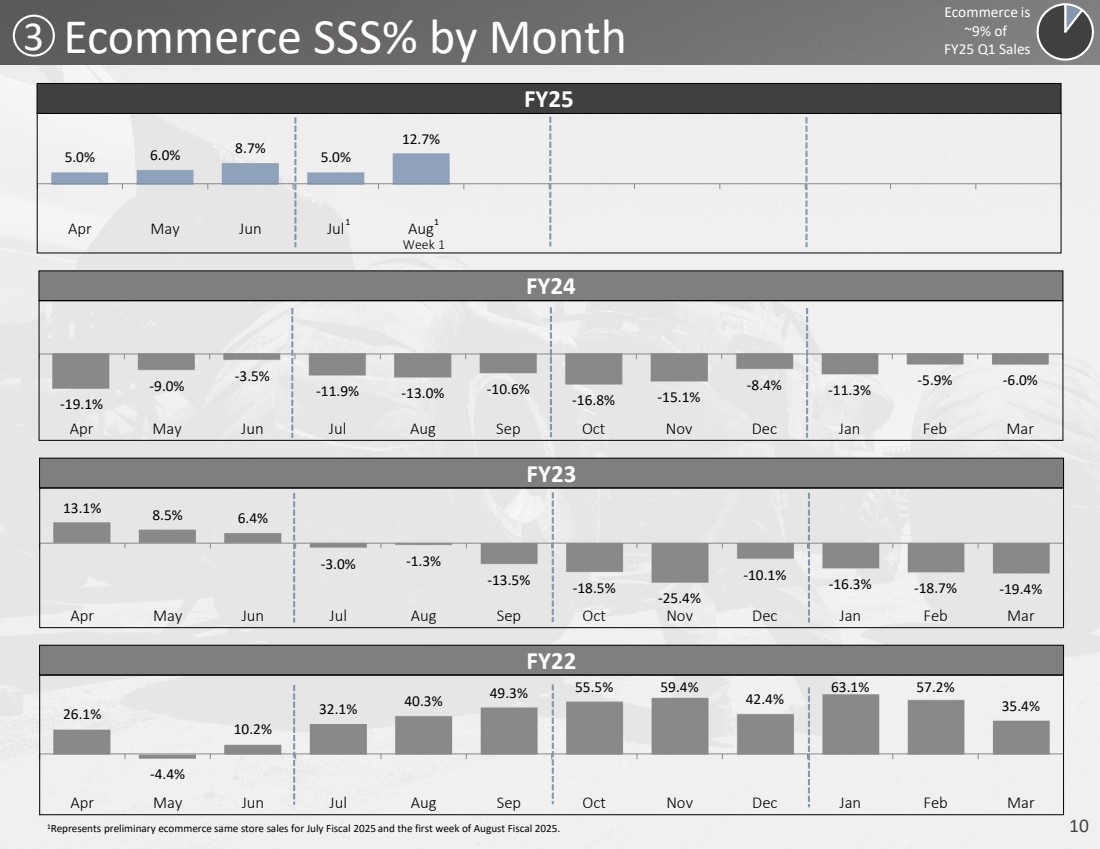

| 10 3 Ecommerce SSS% by Month 5.0% 6.0% 8.7% 5.0% 12.7% Apr May Jun Jul Aug FY24 -19.1% -9.0% -3.5% -11.9% -13.0% -10.6% -16.8% -15.1% -8.4% -11.3% -5.9% -6.0% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar FY25 FY23 13.1% 8.5% 6.4% -3.0% -1.3% -13.5% -18.5% -25.4% -10.1% -16.3% -18.7% -19.4% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Ecommerce is ~9% of FY25 Q1 Sales 1Represents preliminary ecommerce same store sales for July Fiscal 2025 and the first week of August Fiscal 2025. FY22 26.1% -4.4% 10.2% 32.1% 40.3% 49.3% 55.5% 59.4% 42.4% 63.1% 57.2% 35.4% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar 1 1 Week 1 |

| 11 WESTERN COUNTRY ARTIST INSPIRED WORK RANCH & RODEO 4 Exclusive Brands Portfolio PREMIUM VALUE |

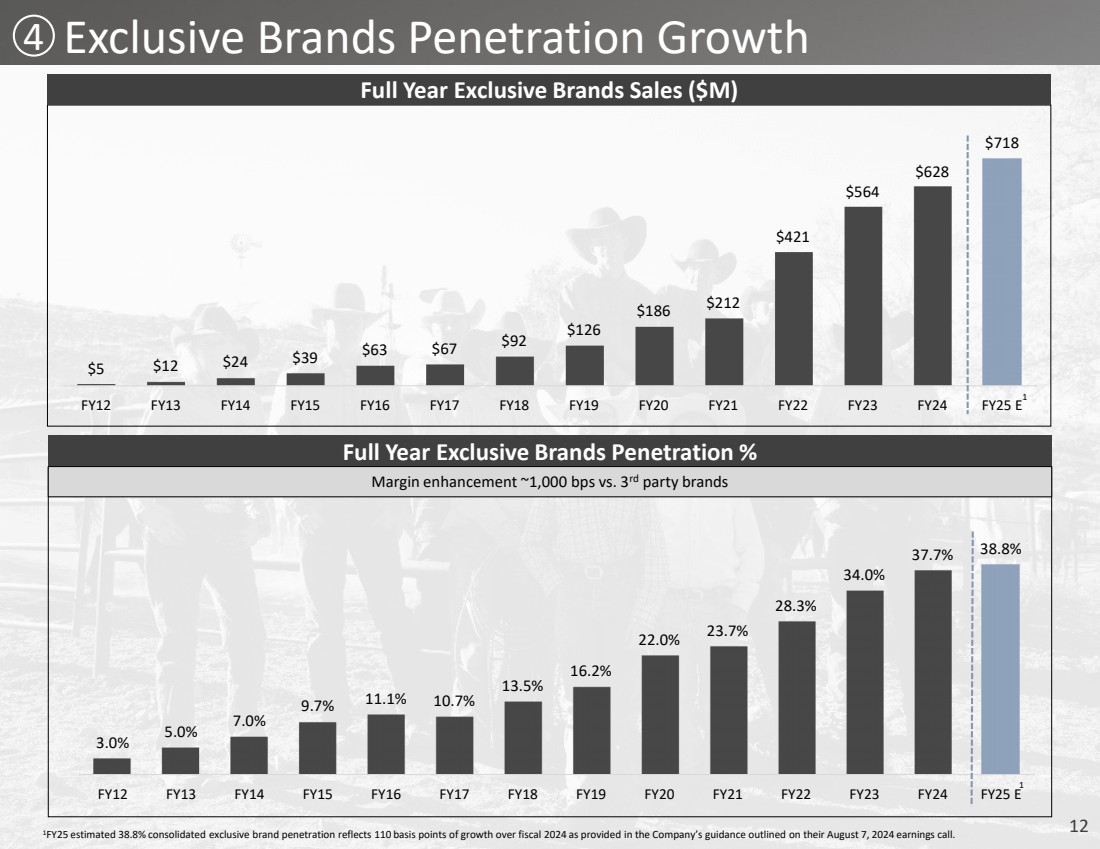

| 12 3.0% 5.0% 7.0% 9.7% 11.1% 10.7% 13.5% 16.2% 22.0% 23.7% 28.3% 34.0% 37.7% 38.8% FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25 E Full Year Exclusive Brands Penetration % Margin enhancement ~1,000 bps vs. 3rd party brands $5 $12 $24 $39 $63 $67 $92 $126 $186 $212 $421 $564 $628 $718 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25 E Full Year Exclusive Brands Sales ($M) 4 1FY25 estimated 38.8% consolidated exclusive brand penetration reflects 110 basis points of growth over fiscal 2024 as provided in the Company’s guidance outlined on their August 7, 2024 earnings call. 1 1 Exclusive Brands Penetration Growth |

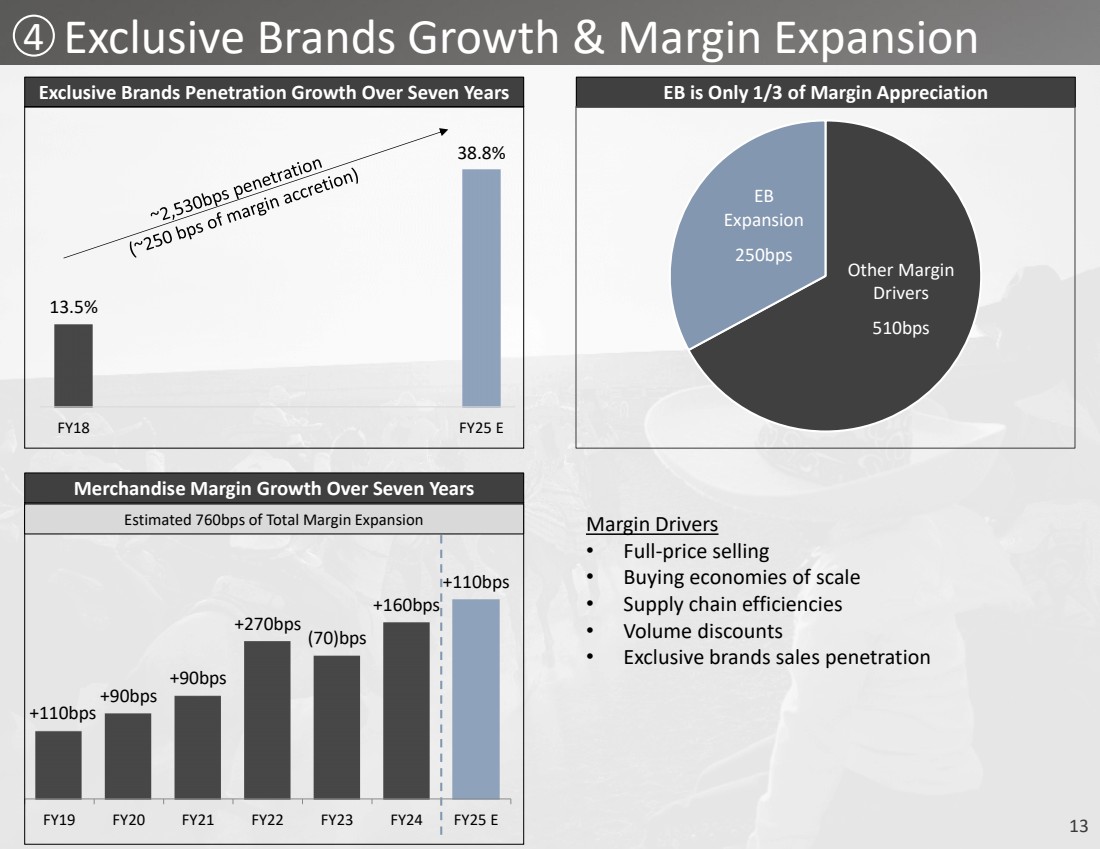

| 13 Margin Drivers • Full-price selling • Buying economies of scale • Supply chain efficiencies • Volume discounts • Exclusive brands sales penetration Exclusive Brands Penetration Growth Over Seven Years 13.5% 38.8% FY18 FY25 E EB is Only 1/3 of Margin Appreciation EB Expansion 250bps Other Margin Drivers 510bps +110bps +90bps +90bps +270bps (70)bps +160bps +110bps FY19 FY20 FY21 FY22 FY23 FY24 FY25 E Merchandise Margin Growth Over Seven Years 4 Estimated 760bps of Total Margin Expansion Exclusive Brands Growth & Margin Expansion |

| 14 FY25 Guidance |

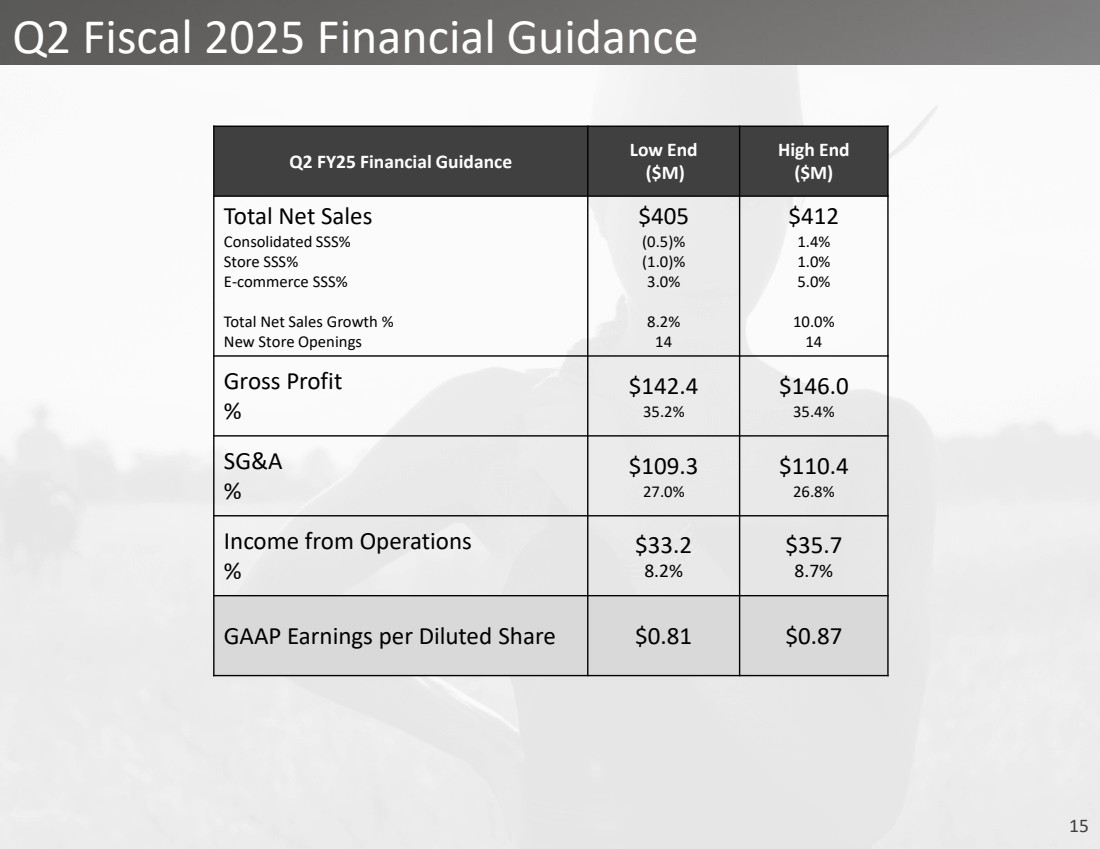

| 15 Q2 Fiscal 2025 Financial Guidance Q2 FY25 Financial Guidance Low End ($M) High End ($M) Total Net Sales Consolidated SSS% Store SSS% E-commerce SSS% Total Net Sales Growth % New Store Openings $405 (0.5)% (1.0)% 3.0% 8.2% 14 $412 1.4% 1.0% 5.0% 10.0% 14 Gross Profit % $142.4 35.2% $146.0 35.4% SG&A % $109.3 27.0% $110.4 26.8% Income from Operations % $33.2 8.2% $35.7 8.7% GAAP Earnings per Diluted Share $0.81 $0.87 |

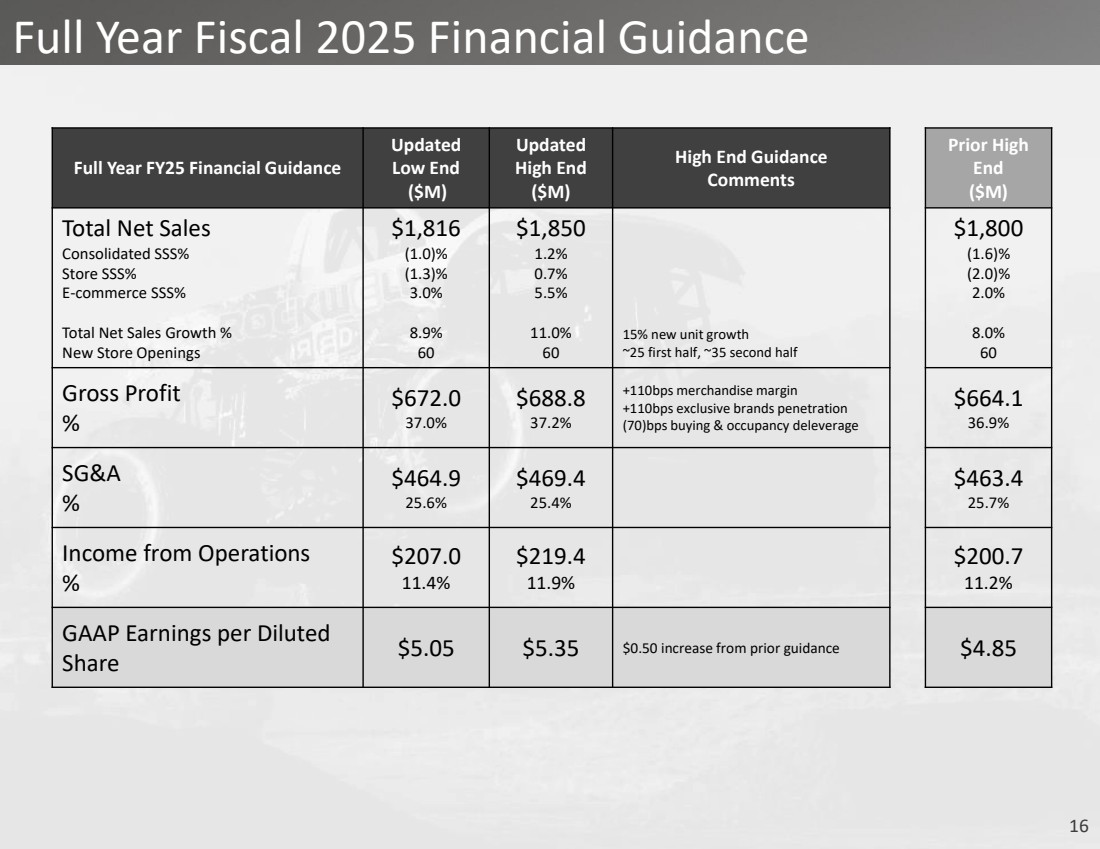

| 16 Full Year Fiscal 2025 Financial Guidance Full Year FY25 Financial Guidance Updated Low End ($M) Updated High End ($M) High End Guidance Comments Total Net Sales Consolidated SSS% Store SSS% E-commerce SSS% Total Net Sales Growth % New Store Openings $1,816 (1.0)% (1.3)% 3.0% 8.9% 60 $1,850 1.2% 0.7% 5.5% 11.0% 60 15% new unit growth ~25 first half, ~35 second half Gross Profit % $672.0 37.0% $688.8 37.2% +110bps merchandise margin +110bps exclusive brands penetration (70)bps buying & occupancy deleverage SG&A % $464.9 25.6% $469.4 25.4% Income from Operations % $207.0 11.4% $219.4 11.9% GAAP Earnings per Diluted Share $5.05 $5.35 $0.50 increase from prior guidance Prior High End ($M) $1,800 (1.6)% (2.0)% 2.0% 8.0% 60 $664.1 36.9% $463.4 25.7% $200.7 11.2% $4.85 |

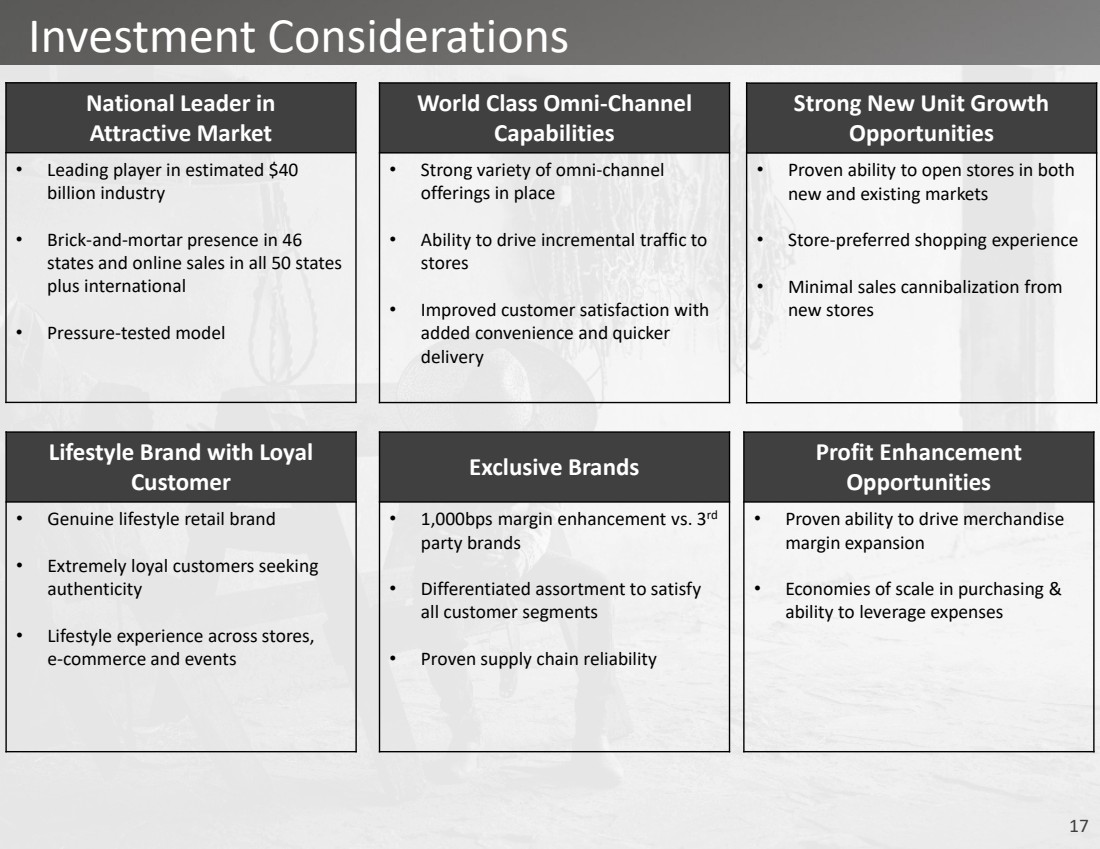

| 17 National Leader in Attractive Market • Leading player in estimated $40 billion industry • Brick-and-mortar presence in 46 states and online sales in all 50 states plus international • Pressure-tested model World Class Omni-Channel Capabilities • Strong variety of omni-channel offerings in place • Ability to drive incremental traffic to stores • Improved customer satisfaction with added convenience and quicker delivery Strong New Unit Growth Opportunities • Proven ability to open stores in both new and existing markets • Store-preferred shopping experience • Minimal sales cannibalization from new stores Lifestyle Brand with Loyal Customer • Genuine lifestyle retail brand • Extremely loyal customers seeking authenticity • Lifestyle experience across stores, e-commerce and events Profit Enhancement Opportunities • Proven ability to drive merchandise margin expansion • Economies of scale in purchasing & ability to leverage expenses Investment Considerations Exclusive Brands • 1,000bps margin enhancement vs. 3rd party brands • Differentiated assortment to satisfy all customer segments • Proven supply chain reliability |

| 18 investor.bootbarn.com |