UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| (Mark One) | |||||

| Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |||||

For the fiscal year ended December 31 , 2021

OR

| Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |||||

For the transition period from to

Commission file number: 001-36440

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation) | (I.R.S. Employer Identification No.) | |||||||||||||||||||

| (Address of principal executive offices) | (Zip code) | |||||||||||||||||||

Registrant’s telephone number, including area code: (844 ) 428-2667

Securities registered pursuant to Section 12(b) of the Act:

| (Title of each class) | (Trading Symbol) | (Name of each exchange on which registered) | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | ||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of common stock held by non-affiliates or registrant on June 30, 2021 was $1,747,564,461 .

As of February 15, 2022, there were 47,317,916 shares of Avanos Medical, Inc. common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

AVANOS MEDICAL, INC.

TABLE OF CONTENTS

| Part I | Page | |||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Part II | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| Part III | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| Part IV | ||||||||

| Item 15. | ||||||||

PART I

ITEM 1. BUSINESS

Overview

Avanos Medical, Inc. is a medical technology company focused on delivering clinically superior breakthrough medical device solutions to improve patients’ quality of life. Headquartered in Alpharetta, Georgia, Avanos is committed to addressing some of today’s most important healthcare needs, such as reducing the use of opioids while helping patients move from surgery to recovery. We develop, manufacture and market clinically superior solutions in more than 90 countries. Unless the context indicates otherwise, the terms “Avanos,” “Company,” “we,” “our” and “us” refer to Avanos Medical, Inc. and its consolidated subsidiaries. We were originally incorporated in Delaware in 2014. The address of our principal executive offices is 5405 Windward Parkway, Suite 100 South, Alpharetta, Georgia 30004, and our telephone number is (844) 428-2667.

We conduct our business in one operating and reportable segment that provides our medical device products to healthcare providers and patients. We have manufacturing facilities in the United States and Mexico. We provide a portfolio of innovative product offerings focused on chronic care and pain management to improve patient outcomes and reduce the cost of care.

Chronic care is a portfolio of products that include the following:

•Digestive health products such as our Mic-Key enteral feeding tubes, Corpak patient feeding solutions and NeoMed neonatal and pediatric feeding solutions. In the years ended December 31, 2021 and 2020, our legacy enteral feeding tubes, which includes our Mic-Key enteral feeding tubes, and our Corpak feeding solutions each accounted for more than 10% of our consolidated net sales. In the year ended December 31, 2019, only our legacy digestive health products accounted for more than 10% of our consolidated net sales.

•Respiratory health products such as our closed airway suction systems and other airway management devices under the Ballard, Microcuff and Endoclear brands. In the years ended December 31, 2021, 2020 and 2019, our closed airway suction systems accounted for more than 10% of our consolidated net sales.

Pain management is a portfolio of non-opioid pain solutions including:

•Acute pain products such as On-Q and ambIT surgical pain pumps and Game Ready cold and compression therapy systems. In the years ended December 31, 2021, 2020 and 2019, our surgical pain products, which includes both On-Q and ambIT pumps, accounted for more than 10% of our consolidated net sales.

•Interventional pain solutions, which provide minimally invasive pain relieving therapies, such as our Coolief pain therapy. In the years ended December 31, 2021, 2020 and 2019, products associated with our Coolief pain therapy accounted for more than 10% of our consolidated net sales.

Effects of the COVID-19 Pandemic

The COVID-19 global pandemic, which began in the first quarter of 2020, continues to disrupt global supply and distribution channels, and affect the way companies do business. We continue to monitor the developments associated with the COVID-19 pandemic and its effects on our employees, customers, supply chain and distribution channels. In addition, we will implement measures recommended by federal, state, local or relevant foreign authorities, or those that we determine are in the best interests of our employees, suppliers, shareholders and other stakeholders.

Our manufacturing sites are operational and have implemented new safety protocols and guidelines as recommended by federal, state, local and foreign governments. Employees at our administrative offices have been encouraged to work remotely; where offices have reopened, they have done so with strict safety and hygiene guidelines. The COVID-19 situation remains dynamic and is subject to rapid and possibly material changes due to variant strains or otherwise. It is not clear what the potential effects may be to our business going forward, including the impact on our revenues, results of operations or financial condition, particularly if pandemic conditions exacerbate over an extended period of time. Additional negative impacts may also arise from the COVID-19 pandemic that we are unable to foresee. The nature and extent of such impacts will depend on future developments, which are highly uncertain and cannot be predicted, including the availability and efficacy of COVID-19 vaccines, the willingness of the general public to get vaccinated and the impact of variant strains, such as the Omicron variant, on the health care market.

The risks the pandemic may continue to have on our operations and cash flows are described in “Risk Factors” in Item 1A of this report.

Business Acquisitions

On December 13, 2021, we entered into an agreement to acquire OrthogenRx, Inc. (“OrthogenRx”) for $130.0 million in cash at closing, subject to net working capital adjustments, plus up to an additional $30.0 million in contingent cash consideration based on OrthogenRx’s growth in net sales during 2022 and 2023. This acquisition closed on January 20, 2022.

1 | ||||||||

During 2019, we completed the acquisition of substantially all the assets of Endoclear, LLC (“Endoclear”) and Summit Medical Products, Inc. (“Summit), and we completed the acquisition of NeoMed, Inc. (“NeoMed”) (collectively, the “Acquisitions”). The aggregate purchase price for the Acquisitions was $57.5 million, net of cash acquired, plus future contingent payments of $7.2 million.

During 2018, we acquired Cool Systems, Inc. (“Game Ready”) for $65.7 million, net of cash acquired, which was based on a purchase price of $65.0 million plus certain adjustments as provided in the purchase agreement.

Divestiture

During 2018, we closed the sale of our Surgical and Infection Prevention (“S&IP”) business (the “Divestiture”) for $710.0 million plus certain adjustments as provided in the purchase agreement.

Sales and Marketing

We direct our primary sales and marketing efforts toward hospitals, ambulatory care centers, and other sites of care. We engage with physicians and other healthcare providers to highlight the unique benefits and competitive differentiation of our branded products. We work directly with physicians, nurses, professional societies, hospital administrators and healthcare group purchasing organizations (“GPOs”) to collaborate and educate on emerging practices and clinical techniques. These marketing programs are delivered directly to healthcare providers. Additionally, we provide marketing programs to our strategic distribution partners throughout the world.

Distribution

While our products are generally marketed directly to hospitals and other healthcare providers, they are generally sold through third-party wholesale distributors, with some sales directly to healthcare facilities and other end-user customers. In 2021, approximately 51% of our net sales in North America were made through distributors. In the year ended December 31, 2021, sales to Medline Industries, McKesson Corporation, and Owens & Minor, Inc. accounted for approximately 15%, 11%, and 10% of consolidated net sales, respectively. In the year ended December 31, 2020, sales to Medline Industries, McKesson Corporation, and Owens & Minor, Inc. accounted for approximately 12%, 12%, and 9% of consolidated net sales, respectively. In 2019, no single customer accounted for 10% or more of consolidated net sales.

Outside North America, sales are made either directly to end-user customers or through distributors, depending on the market served. In 2021, approximately 75% of our net sales outside North America were made through wholesalers or distributors.

We utilize distribution centers in North America, Europe, Australia and Japan. No material portion of our business is subject to renegotiation of profits or termination of contracts at the election of the government.

Group Purchasing Organizations

We enter into agreements with GPOs which enables us to sell our products to their members, whether sold directly by us or through independent wholesale distributors. Agreements with GPOs are generally renewed every three years. GPOs negotiate pricing and volume purchasing discounts for hospitals, physician practices and other health care providers and institutions. Under our agreements with GPOs, we pay a fee based on sales of our products to GPO members, which is recorded as a reduction of net sales. Approximately 32% of our 2021 global net sales, including sales to wholesale distributors, were contracted through GPOs.

Competition

While no single company competes with us across the full breadth of our offerings, we face significant competition in U.S. and international markets.

There are a variety of treatment means and alternative clinical practices to address surgical and interventional pain management and respiratory and digestive health. We face competition from these alternative treatments, as well as improvements and innovations in products and technologies by our competitors. Major competitors include, among others:

•Digestive Health: Boston Scientific Corporation, Cook Medical and Applied Medical Technology, Inc.

•Respiratory Health: Becton, Dickinson and Company, Stryker Corporation, Medline Industries, Inc. and Smiths Medical

•Acute Pain: B. Braun Medical Inc., Pacira Pharmaceuticals, Inc., Teleflex Incorporated, Medtronic plc, Ambu A/S, Baxter International, Inc., Pajunk Medical Systems and Leventon

•Interventional Pain: Boston Scientific Corporation, Abbott Laboratories, Medtronic plc and Stryker Corporation

In developing and emerging markets, alternative clinical practices and different standards of care are our primary competition.

2 | ||||||||

While we believe that the number of procedures using our products will grow due, in part, to increasing global access to healthcare, we expect that our ability to compete with other providers of similar products will be impacted by rapid technological advances, pricing pressures and third-party reimbursement practices. We continue to defend our market positions and launched six new products in 2021. We believe that our key product characteristics, such as proven efficacy, reliability and safety, including our ability to launch innovative new products, our efficient manufacturing processes, and our established distribution network, field sales organization and customer service group, are important factors that distinguish us from our competitors.

Research and Development

We continuously engage in research and development to commercialize new products and enhance the effectiveness, reliability and safety of our existing products. We incurred research and development costs of $32.3 million in 2021, $34.9 million in 2020 and $37.7 million in 2019. These amounts consisted primarily of salaries and related expenses for personnel, product trial costs, outside laboratory and license fees, the costs of laboratory equipment and facilities and asset write-offs for equipment associated with unsuccessful product launches. We intend to continue our research and development efforts as a key strategy for growth.

We collaborate with physicians to develop solutions that seek to accelerate the global adoption of our therapies and procedures. We are investing to expand the indications for use of our pain products with clinical research and studies and associated new product developments. We are expanding our portfolio with customer-preferred product enhancements, such as next generation cooled radiofrequency generators and a full line of needles, kits and accessories for continuous peripheral nerve block procedures.

Intellectual Property

Patents, trademarks and other proprietary rights are very important to our business. We also rely upon trade secrets, manufacturing know-how, continuing technological innovations and licensing opportunities to maintain and improve our competitive position. We review third-party proprietary rights, including patents and patent applications, as they become available, in an effort to develop an effective intellectual property strategy, avoid infringement of third-party proprietary rights, identify licensing opportunities and monitor the intellectual property owned by others.

We hold numerous patents and have numerous patent applications pending in the United States and other countries that relate to the technology used in many of our products. We utilize patents in our acute pain management, interventional pain management, respiratory health and digestive health products. These patents generally expire between 2022 and 2038. None of the patents we license from third parties are material to our business.

Under our agreement with Owens & Minor, Inc., we may continue to distribute products bearing the “Halyard Health” or “Halyard” brands through February 2023. We continue rebranding efforts to ensure our customers’ transition from the Halyard brand.

We consider the patents and trademarks which we own and the trademarks under which we sell certain of our products, as a whole, to be material to our business. However, we do not consider our business to be materially dependent upon any individual patent or trademark.

Raw Materials

We use a wide variety of raw materials and other inputs in our production processes. We base our purchasing decisions on quality assurance, cost effectiveness and regulatory requirements, and we work closely with our suppliers to assure continuity of supply while maintaining high quality and reliability. We primarily purchase these materials from external suppliers, some of which are single-source suppliers.

Regulatory Matters

The development, manufacture, marketing, sale, promotion and distribution of our products are subject to comprehensive government regulation. Government regulation by various national, regional, federal, state and local agencies, both in the United States and other countries, addresses (among other matters) inspection of, and controls over, research and laboratory procedures, clinical investigations, product approvals and manufacturing, labeling, packaging, marketing and promotion, pricing and reimbursement, sampling, distribution, quality control, post-market surveillance, servicing, record keeping, storage and disposal practices. Our operations are also affected by trade regulations in many countries that limit the import of raw materials and finished products and by laws and regulations that seek to prevent corruption and bribery in the marketplace (including the U.S. Foreign Corrupt Practices Act and the United Kingdom Bribery Act, which provide guidance on corporate interactions with government officials) and require safeguards for the protection of personal data. In addition, we are subject to laws and regulations pertaining to healthcare fraud and abuse, including state and federal anti-kickback and false claims laws in the United States.

3 | ||||||||

Compliance with these laws and regulations is costly and materially affects our business. Among other effects, healthcare regulations substantially increase the time, difficulty and costs incurred in obtaining and maintaining approval to market newly developed and existing products. For example, in the United States, before we can market a new medical product, or market a new use for, claim for or significant modification to an existing product, we generally must first receive clearance under Section 510(k) of the Food, Drug and Cosmetic Act (“510(k) clearance”) from the United States Food and Drug Administration (“FDA”). In order for us to obtain 510(k) clearance, the FDA must determine that our proposed product is substantially equivalent to a device legally on the market, known as a predicate device, with respect to intended use, technology, safety and effectiveness. Similarly, most major markets for medical devices outside the United States also require clearance, approval or compliance with certain standards before a product can be commercially marketed. For instance, the European Union, or EU, harmonized national regulations for the control of medical devices through the European Medical Device Directive (“EU MDD”) with which manufacturers must comply. To sell medical devices in the EU, manufacturers must place a CE mark on their products, signifying to customers that the products meet EU requirements for safety and performance. For all but the lowest risk medical devices, manufacturers must have approval from a notified body prior to placing the CE mark on their devices. Medical devices without a CE mark may not be sold or distributed in the EU.

Effective May 26, 2021, the European Union adopted the EU Medical Device Regulation (“EU MDR”), replacing the EU MDD. The main goal of this regulation is to enhance product safety, quality and transparency for medical devices within the European Union. To achieve this, the EU MDR includes significant new requirements for medical devices, including enhanced requirements for clinical evidence and documentation, increased focus on device identification and traceability, and additional post-market surveillance and diligence. Compliance with the EU MDR will require re-certification of many of our products to the enhanced standards, during a transition period ending May 26, 2024. Complying with the EU MDR will require us to incur significant expenditures.

We also expect compliance with these regulations to continue to require significant technical expertise and capital investment to ensure compliance. Failure to comply will delay the release of a new product or result in regulatory and enforcement actions, the seizure or recall of a product, the suspension or revocation of the authority necessary for a product’s production and sale and other civil or criminal sanctions, including fines and penalties.

In addition to regulatory initiatives, our business can be affected by ongoing studies of the utilization, safety, efficacy and outcomes of healthcare products and their components that are regularly conducted by industry participants, government agencies and others. These studies can call into question the utilization, safety and efficacy of previously marketed products. In some cases, these studies have resulted, and may in the future result, in the discontinuance of, or limitations on, marketing of such products domestically or worldwide, and may give rise to claims for damages from persons who believe they have been injured as a result of their use.

Access to healthcare products continues to be a subject of investigation and action by governmental agencies, legislative bodies and private organizations in the United States and other countries. A major focus is cost containment. Efforts to reduce healthcare costs are also being made in the private sector, notably by healthcare payors and providers, which have instituted various cost reduction and containment measures. We expect insurers and providers to continue attempts to reduce the cost of healthcare products. Outside the United States, many countries control the price of healthcare products directly or indirectly, through reimbursement, payment, pricing, coverage limitations, or compulsory licensing. Budgetary pressures in the United States and in other countries may also heighten the scope and severity of pricing pressures on our products for the foreseeable future.

We expect debate to continue during the next several years at all government levels worldwide over the marketing, availability, method of delivery, and payment for healthcare products and services. We believe that future legislation and regulation in the markets we serve could affect access to healthcare products and services, increase rebates, reduce prices or the rate of price increases for healthcare products and services, change healthcare delivery systems, create new fees and obligations, or require additional reporting and disclosure. It is not possible to predict the extent to which we or the healthcare industry in general might be affected by the matters discussed above.

Since we market our products worldwide, certain products of a local nature and variations of product lines must also meet other local regulatory requirements. Certain additional risks are inherent in conducting business outside the United States, including price and currency exchange controls, changes in currency exchange rates, limitations on participation in local enterprises, expropriation, nationalization, and other governmental action.

Demand for many of our existing and new medical devices is, and will continue to be, affected by the extent to which government healthcare programs and private health insurers reimburse our customers for patients’ medical expenses in the countries where we do business. Statutory and regulatory requirements for Medicaid, Medicare, and other government healthcare programs govern provider reimbursement levels. From time to time, legislative changes are made to government healthcare programs that impact our business, and the federal and/or state governments may continue to enact measures in the future aimed at containing or reducing reimbursement levels for medical expenses paid for in whole or in part with government

4 | ||||||||

funds. We cannot predict the nature of such measures or their impact on our business, results of operations, financial condition and cash flows. Any reduction in the amount of reimbursements received by our customers could have a material adverse effect on our business by reducing their selection of our products and the prices they are willing to pay.

Environmental, Health and Safety Matters

Our operations are subject to federal, state, provincial and local laws, regulations and ordinances relating to various environmental, health and safety matters. Our operations are in compliance with, or we are taking actions designed to ensure compliance with, these laws, regulations and ordinances. However, the nature of our operations exposes us to the risk of claims concerning non-compliance with environmental, health and safety laws or standards, and there can be no assurance that material costs or liabilities will not be incurred in connection with those claims. We are not currently named as a party in any judicial or administrative proceeding relating to environmental, health or safety matters.

While we have incurred in the past several years, and will in the future continue to incur, capital and operating expenditures in order to comply with environmental, health and safety laws, regulations and ordinances, we believe that our future cost of compliance with such regulations and ordinances, and our exposure to liability for environmental, health and safety claims will not have a material adverse effect on our business, results of operations, financial condition or cash flows. However, future events, such as changes in existing laws and regulations, or contamination of sites owned, operated or used for waste disposal by us (including currently unknown contamination and contamination caused by prior owners and operators of such sites or other waste generators) may give rise to additional costs which could have a material adverse effect on our financial condition, results of operations or liquidity.

Employees and Human Capital Management

Employees are our most-valued resource and are at the center of everything we do. Their talent, diversity and commitment are crucial to our innovation and success. Our work environment fosters personal, professional and corporate growth and nurtures innovation through product development and customer solutions. Our global teams work together in a spirit of cooperation to improve health and healthcare every day.

Employee demographics presented in the table below represent the number of employees as of December 31, 2021:

| Global Employees | 2021 | % of Total | |||||||||

| United States | 962 | 21.1% | |||||||||

| Mexico | 3,356 | 73.7% | |||||||||

| Latin America | 9 | 0.2% | |||||||||

| Europe, Middle East and Africa | 110 | 2.4% | |||||||||

| Asia Pacific | 118 | 2.6% | |||||||||

| Total | 4,555 | ||||||||||

Compensation

We compensate employees competitively and fairly in markets throughout the world. Compensation for salaried employees is strongly tied to performance objectives. Salaried employees above a certain pay grade have a substantial portion of their total compensation subject to performance objectives. More about our executive officer compensation can be found in the proxy statement relating to our 2022 Annual Meeting of Stockholders (the “2022 Proxy Statement”).

Training and Educational Opportunities

Because we are a medical device manufacturer, our employees are regularly trained in key areas required by the FDA and other applicable regulatory authorities, including topics such as documentation, safety, complaint handling, anti-bribery and quality, among others. In addition to regulated training, employees are educated on the Avanos Code of Conduct, which aims to ensure all our employees understand and act in alignment with our cultural and behavioral expectations.

Employee Engagement

We believe that employees who are engaged in their roles, treated as partners in the business and recognized for their efforts, are more satisfied and productive. Our goal is to ensure that each of our more than 4,500 employees understands how he/she contributes to the company’s innovation and growth. This is accomplished through an employee recognition program and ongoing, two-way communications, including videos and podcasts, that allow employees to engage with and hear directly from members of the executive team.

5 | ||||||||

Employee Retention

In 2021, we implemented a multi-tiered employee retention strategy. The key elements of this strategy include: (i) enhanced compensation and rewards, including retention bonuses and equity grants for key employees, expanded benefits and more flexible work arrangements; (ii) fostering greater employee engagement through initiatives such as peer-to-peer coaching, internal promotions, a leadership development program and increased executive outreach through towns halls, podcast and videos; and (iii) recognizing employees for their efforts through a variety of awards, spotlights and appreciation events.

Health and Safety

We are committed to protecting our employees everywhere we operate. We identify potential risks associated with workplace activities in order to develop measures to mitigate possible hazards. In addition, we support employees with safety training and put specific programs in place for those working in potentially hazardous environments. We have taken additional measures during the COVID-19 pandemic, including implementing new safety protocols and guidelines as recommended by federal, state, local and foreign governments. Employees at our administrative offices have been encouraged to work remotely; where offices have reopened, they have done so with strict safety and hygiene guidelines.

Diversity and Inclusion

We are an equal opportunity employer committed to providing a workplace free of harassment or discrimination based on race, color, religion, sex, sexual orientation, gender identity, national origin, disability, veteran status or other legally protected characteristic. Our commitment to diversity and inclusion is aligned to foster the company’s success as we continue to grow our business and develop our workforce. Our employee profile below reflects the results on December 31, 2021.

| Employee Diversity | 2021 | |||||||

Women - global director and above(a) | 31.3% | |||||||

Ethnically diverse - U.S. director and above(a) | 15.9% | |||||||

| Women - global salaried employees | 42.9% | |||||||

| Ethnically diverse - U.S. salaried employees | 30.6% | |||||||

__________________________________________________

(a) Leaders in director-level position or higher.

Available Information

We make financial information, news releases and other information available on our corporate website at www.avanos.com. Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are available free of charge on our corporate website as soon as reasonably practicable after we file these reports and amendments with, or furnish them to, the SEC. The information contained on or connected to our website is not incorporated by reference into this Annual Report on Form 10-K and should not be considered part of this or any other report filed with the SEC. Stockholders may also contact Stockholder Services, 5405 Windward Parkway, Suite 100 South, Alpharetta, Georgia 30004 or call (844) 428-2667 to obtain a hard copy of these reports without charge.

ITEM 1A. RISK FACTORS

Our business faces many risks and uncertainties. Any of the risks discussed below, as well as factors described in other places in this Annual Report on Form 10-K, or in our other filings with the SEC, could materially adversely affect our business, consolidated financial position, results of operations or cash flows. In addition, these items could cause our future results to differ from our recent results, from our anticipated future results and from those in any of our forward-looking statements. These risks are not the only ones we face. Other risks that we do not presently know about or that we presently believe are not material could also adversely affect us.

Risks Related to our Business and Industry

The ongoing COVID-19 pandemic could adversely impact our business operations, financial condition, results of operations and cash flows.

The COVID-19 pandemic has caused significant volatility in the global financial markets, caused disruption in global supply and distribution channels, dramatically changed the way companies do business and may adversely impact our financial position, results of operations and cash flows.

While we are closely monitoring the economic impact of the COVID-19 pandemic on our business, we currently cannot quantify the impact it will have on our future results of operations. The ongoing impact of the pandemic depends on a number

6 | ||||||||

of factors which are uncertain and unpredictable, including the severity, extent and duration of the pandemic and the potential severe adverse financial impact the pandemic could have on our customers. Our future results of operations and cash flows may suffer material adverse effects from delays in payments on outstanding accounts receivable, potential manufacturing, distribution and supply chain disruptions and uncertain demand, and the effects of any actions we may take to address the financial and operational challenges our customers may face. Other pandemic-related risks and uncertainties include, but are not limited to:

•postponement or cancellation of elective medical procedures and uncertainty as to whether or when they will resume;

•potential temporary or prolonged office, production facility or distribution center closures;

•the health of our employees and our ability to meet our staffing needs;

•potential new or continued governmental actions that may limit our employees’ ability to work;

•civil unrest relating to government, corporate and societal responses to the pandemic;

•volatility in economic conditions and the financial markets;

•risks associated with vaccine distribution; and

•other unanticipated effects that remain unknown.

If we experience any one of these risks or uncertainties, it may have a material adverse impact to our business, financial condition, results of operations and cash flows. The duration of any such impacts cannot be predicted because of the unprecedented nature of the COVID-19 pandemic. Additionally, our business could be severely impacted by widespread regional, national or global health epidemics unrelated to COVID-19 in the future.

We face strong competition. Our failure to compete effectively could have a material adverse effect on our business.

Our industry is highly competitive. We compete with many domestic and foreign companies ranging from small start-up enterprises that might sell only a single or limited number of competitive products or compete only in a specific market segment, to companies that are larger and more established than us, have a broad range of competitive products, participate in numerous markets and have access to significantly greater financial and marketing resources than we do. We are also subject to potential competition from new technologies or new market entrants. Competitive factors include price, alternative clinical practices, innovation, quality and reputation. Our failure to compete effectively could have a material adverse effect on our business, results of operations, financial condition and cash flows.

We may not be successful in developing, acquiring or marketing competitive products and technologies.

Our industry is characterized by extensive research and development and rapid technological advances. The future success of our business will depend, in part, on our ability to design, acquire and manufacture new competitive products and enhance existing products. Accordingly, we commit substantial time, funds and other resources to new product development, including research and development, acquisitions, licenses, clinical trials and physician education. We make these substantial expenditures without any assurance that our products will obtain regulatory clearance or reimbursement approval, acquire adequate intellectual property protection or receive market acceptance. Development by our competitors of improved products, technologies or enhancements may make our products, or those we develop, license or acquire in the future, obsolete or less competitive, which could negatively impact our net sales. Our failure to successfully develop, acquire or market competitive new products or enhance existing products could have a material adverse effect on our business, results of operations, financial condition and cash flows.

We cannot guarantee that any of our strategic acquisitions, investments or alliances will be successful.

We intend to supplement our growth through strategic acquisitions of, investments in and alliances with new medical technologies. The success of any acquisition, investment or alliance may be affected by a number of factors, including our ability to identify and then properly assess and value the potential business opportunity or to successfully integrate any business we may acquire into our existing business. These types of transactions may require more resources and investments than originally anticipated, may divert management’s attention from our existing business, may result in exposure to unexpected liabilities of the acquired business, and may not result in the expected benefits, savings or synergies. There can be no assurance that we will be able to identify and successfully make strategic acquisitions of, investments in and alliances with new medical technologies or that any past or future acquisition, investment or alliance will be cost-effective, profitable or successful.

We may be unable to attract and retain key employees necessary to be competitive.

Our ability to compete effectively depends upon our ability to attract and retain executives and other key employees, including people in technical, marketing, sales, and research and development positions. Competition for experienced employees, particularly for persons with specialized skills, can be intense. Our ability to recruit such talent will depend on a number of factors, including compensation and benefits, work location and work environment. If we cannot effectively recruit and retain qualified executives and employees, our business could be materially adversely affected.

7 | ||||||||

Breaches of our information technology systems could have a material adverse effect on our business.

We rely on information technology systems to process, transmit and store electronic information in our day-to-day operations. Our information technology systems may fail to perform as anticipated, and we may encounter difficulties in implementing new systems, adapting these systems to changing technologies or expanding them to meet the future needs and growth of our business. In addition, our information technology systems may be subjected to damage or interruption from power outages, computer and telecommunication failures, usage errors by our employees, security breaches, computer viruses or other malicious codes, unauthorized access attempts and cyber- or phishing-attacks. We also store certain information with third parties that could be subject to these types of attacks. These attacks could result in our intellectual property and other confidential information, including personal health information, being lost or stolen, disruption of our operations, loss of reputation and other negative consequences, such as increased costs for security measures or remediation costs and diversion of management attention. While we will continue to implement additional protective measures to reduce the risk of and detect future cyber incidents, cyber-attacks are becoming more sophisticated and frequent, and the techniques used in such attacks change rapidly. There can be no assurances that our protective measures will prevent future attacks that could have a material adverse effect on our business.

We may be unable to protect our intellectual property rights or may infringe the intellectual property rights of others.

We rely on patents, trademarks, trade secrets and other intellectual property assets in the operation of our business. Our efforts to protect our intellectual property and proprietary rights may not be sufficient. We cannot be sure that pending patent applications will result in the issuance of patents or that patents issued or licensed to us will remain valid or prevent competitors from introducing similar competing technologies. Our ability to enforce and protect our intellectual property rights may be limited in certain countries outside of the United States in which we operate, which could make it easier for our competitors to develop or distribute similar or superior competing technologies in those jurisdictions. In addition, our competitive position may be adversely affected by expirations of our significant patents, which would allow competitors to freely use our technology to compete with us.

We operate in an industry characterized by extensive patent litigation and competitors may claim that our products infringe their intellectual property rights. Resolution of patent litigation or other intellectual property claims is inherently unpredictable, typically time consuming and costly and can result in significant damage awards and injunctions that could prevent the manufacture and sale of the affected products or require us to make significant royalty payments in order to continue selling the affected products. Any one of these could have a material adverse effect on our business, results of operations, financial condition and cash flows. At any given time we are involved as either a plaintiff or a defendant in a number of patent infringement actions, the outcomes of which may not be known for prolonged periods of time. We can expect to face additional claims of patent infringement in the future.

Our customers depend on third-party coverage and reimbursements. The failure of healthcare programs to provide coverage and reimbursement, or reductions in levels of reimbursement, could have a material adverse effect on our business.

The ability of our customers to obtain coverage and reimbursements for products they purchase from us is important to our business. Demand for many of our existing and new medical products is, and will continue to be, affected by the extent to which government healthcare programs and private health insurers reimburse our customers for patients’ medical expenses in the countries where we do business. Any reduction in the amount of reimbursements received by our customers could harm our business by reducing their selection of our products and the prices they are willing to pay.

In addition, as a result of their purchasing power, third-party payors are implementing cost-cutting measures such as seeking discounts, price reductions or other incentives from medical products suppliers and imposing limitations on coverage and reimbursements for medical technologies and procedures. These trends could compel us to reduce prices for our existing products and potential new products and could cause a decrease in the size of the market or a potential increase in competition that could have a material adverse effect on our business, results of operations, financial condition and cash flows.

An inability to obtain key components, raw materials or manufactured products from third parties may have a material adverse effect on our business.

We depend on the availability of various components, raw materials and manufactured products supplied by others for our operations. If the capabilities of our suppliers and third-party manufacturers are limited or stopped, due to quality, regulatory or other reasons, including natural disasters, pandemics or other health emergencies (such as the COVID-19 pandemic), political instability, government actions, prolonged power or equipment failures or labor dispute, it could negatively impact our ability to manufacture or deliver our products and could expose us to regulatory actions. Further, for quality assurance or cost effectiveness, we purchase from sole suppliers certain components and raw materials. Although there are other sources in the market place for these items, we may not be able to quickly establish additional or replacement sources for certain components or materials due to regulations and requirements of the FDA and other regulatory authorities regarding the manufacture of our products. The loss of any sole supplier or any sustained supply interruption that affects our ability to manufacture or deliver our

8 | ||||||||

products in a timely or cost effective manner could have a material adverse effect on our business, results of operations, financial condition and cash flows.

An interruption in our ability to manufacture products may have a material adverse effect on our business.

Many of our key products are manufactured at single locations, with limited alternate facilities. If one or more of these facilities experience damage, or if these manufacturing capabilities are otherwise limited or stopped due to quality, regulatory or other reasons, including natural disasters, pandemics or other health emergencies (such as the COVID-19 pandemic), political instability, government actions, prolonged power or equipment failures or labor dispute, it may not be possible to timely manufacture the relevant products at previous levels or at all. A reduction or interruption in any of these manufacturing processes could have a material adverse effect on our business, results of operations, financial condition and cash flows.

An interruption in distribution or transportation may have a material adverse effect on our business.

We rely on various transportation channels for global distribution of our products through shipping ports located throughout the world. Labor unrest, political instability, the outbreak of pandemics or other health emergencies (such as the COVID-19 pandemic), trade restrictions, transport capacity and costs, port security, weather conditions, natural disasters or other events could slow port activities and could adversely affect our business by interrupting product shipments and may increase our transportation costs if we are forced to use more expensive shipping alternatives.

The adoption and interpretation of tax laws may have a material adverse effect on our business.

The laws and rules and related interpretations dealing with income taxation are frequently reviewed and amended by governmental bodies, officials and regulatory agencies in the United States and other jurisdictions in which we do business. The governmental bodies may include the U.S. Internal Revenue Service, the U.S. Treasury Department, the U.S. Congress, taxing authorities in countries outside the U.S., and various state, provincial, local or municipal regulatory agencies. Our provision for income taxes and results of operations may be adversely affected by changes to our operating structure, changes in the mix of income and expenses in countries with differing tax rates, changes in the valuation of deferred tax assets and liabilities or changes in tax laws, regulations or administrative interpretations thereof. For example, the U.S. federal government could make changes to existing U.S. tax laws, including the Tax Cuts and Jobs Act of 2017 or the Coronavirus Aid, Relief and Economic Security (CARES) Act of 2020, which could include an increase in the corporate tax rate and the tax rate on foreign earnings. It cannot be predicted whether, when, in what form, or with what effective dates, tax laws, regulations and rulings may be enacted, promulgated, issued or amended that could result in a material adverse effect on our financial position, results of operations or cash flows.

We face significant uncertainty in the healthcare industry due to government healthcare reform in the United States and elsewhere.

The U.S. Congress, regulatory agencies and certain state legislatures, as well as international legislators and regulators, periodically review and assess alternative healthcare delivery systems and payment methods with an objective of ultimately reducing healthcare costs and expanding access. We cannot predict with certainty what healthcare initiatives, if any, will be implemented by states or foreign governments or what ultimate effect healthcare reform or any future legislation or regulation may have on our customers’ purchasing decisions regarding our products. However, the implementation of new legislation and regulation may lower reimbursements for our products, reduce medical procedure volumes and materially adversely affect our business, results of operations, financial condition and cash flows.

We are subject to extensive government regulation, which may require us to incur significant expenses to ensure compliance.

Many of our products are subject to extensive regulation in the United States by the FDA and other regulatory authorities and by comparable government agencies in other countries concerning the development, design, approval, manufacture, labeling, importing and exporting and sale and marketing of many of our products. Furthermore, our facilities are subject to periodic inspection by the FDA and other federal, state and foreign government authorities, which require manufacturers of medical devices to adhere to certain regulations, including the FDA’s Quality System Regulation, which requires periodic audits, design controls, quality control testing and documentation procedures, as well as complaint evaluations and investigation. Regulations regarding the development, manufacture and sale of medical products are evolving and subject to future change. We cannot predict what impact those regulatory changes may have on our business. Failure to comply with applicable regulations could lead to manufacturing shutdowns, product shortages, delays in product manufacturing, product seizures, recalls, operating restrictions, withdrawal or suspension of required licenses, and prohibitions against exporting of products to, or importing products from, countries outside the United States and may require significant resources to resolve. Any one or more of these events could have a material adverse effect on our business, results of operations, financial condition and cash flows.

We are subject to healthcare fraud and abuse laws and regulations that could result in significant liability, require us to change our business practices or restrict our operations in the future.

9 | ||||||||

We are subject to various U.S. federal, state and local laws targeting fraud and abuse in the healthcare industry, including the Food Drug and Cosmetic Act and anti-kickback and false claims laws. Violations of these laws are punishable by criminal or civil sanctions, including substantial fines, imprisonment and exclusion from participation in healthcare programs such as Medicare and Medicaid. These laws and regulations are wide ranging and subject to changing interpretation and application, which could restrict our sales or marketing practices. Furthermore, since many of our customers rely on reimbursement from Medicare, Medicaid and other governmental programs to cover a substantial portion of their expenditures, our exclusion from such programs as a result of a violation of these laws could have a material adverse effect on our business, results of operations, financial condition and cash flows.

We must obtain clearance or approval from the appropriate regulatory authorities prior to introducing a new product or a modification to an existing product. The regulatory clearance process may result in substantial costs, delays and limitations on the types and uses of products we can bring to market, any of which could have a material adverse effect on our business.

In the United States, before we can market a new product, or market a new use of, or claim for, or significant modification to, an existing product, we generally must first receive clearance or approval from the FDA and certain other regulatory authorities. Most major markets for medical devices outside the United States also require clearance, approval or compliance with certain standards before a product can be commercially marketed. The process of obtaining regulatory clearances and approvals to market a medical device can be costly and time consuming, involve rigorous pre-clinical and clinical testing, require changes in products or result in limitations on the indicated uses of products. There can be no assurance that these clearances and approvals will be granted on a timely basis, or at all. In addition, once a medical device has been cleared or approved, a new clearance or approval may be required before the medical device may be modified, its labeling changed or marketed for a different use. Medical devices are cleared or approved for one or more specific intended uses and promoting a device for an off-label use could result in government enforcement action. Furthermore, a product approval or clearance can be withdrawn or limited due to unforeseen problems with the medical device or issues relating to its application. The regulatory clearance and approval process may result in, among other things, delayed, if at all, realization of product net sales, substantial additional costs and limitations on the types of products we may bring to market or their indicated uses, any one of which could have a material adverse effect on our business, results of operations, financial condition and cash flows.

We may incur product liability losses, litigation liability, product recalls, safety alerts or regulatory action associated with our products which can be costly and disruptive to our business.

The risk of product liability claims is inherent in the design, manufacture and marketing of medical products of the type we produce and sell. A number of factors could result in an unsafe condition or injury to, or death of, a patient with respect to the products that we manufacture or sell, including the physician’s skill, technique and experience in performing the relevant surgical procedure, component failures, manufacturing flaws, design defects or inadequate disclosure of product-related risks or information.

In addition to product liability claims and litigation, an unsafe condition or injury to, or death of, a patient associated with our products could lead to a recall of, or issuance of a safety alert relating to, our products, or suspension or delay of regulatory product approvals or clearances, product seizures or detentions, governmental investigations, civil or criminal sanctions or injunctions to halt manufacturing and distribution of our products. Any one of these could result in significant costs and negative publicity resulting in reduced market acceptance and demand for our products and harm our reputation. In addition, a recall or injunction affecting our products could temporarily shut down production lines or place products on a shipping hold.

All of the foregoing types of legal proceedings and regulatory actions are inherently unpredictable and, regardless of the outcome, could disrupt our business, result in substantial costs or the diversion of management attention and could have a material adverse effect on our business, results of operations, financial condition and cash flows.

Economic conditions have affected and may continue to adversely affect our business, results of operations, financial condition and cash flows.

Disruptions in the financial markets and other macro-economic challenges affecting the economy and the economic outlook of the United States, Europe, Japan, China and other parts of the world may have an adverse impact on our results of operations, financial condition and cash flows. Economic conditions and depressed levels of consumer and commercial spending have caused and may continue to cause our customers to reduce, modify, delay or cancel plans to purchase our products, and we have observed certain hospitals delaying and prioritizing purchasing decisions, which has had and may continue to have a material adverse effect on our business, results of operations, financial condition and cash flows.

In addition, as a result of economic conditions, our customers inside and outside the United States, including foreign governmental entities or other entities that rely on government healthcare systems or government funding, may be unable to pay their obligations on a timely basis or to make payment in full. If our customers’ cash flow or operating and financial performance deteriorate or fail to improve, or if our customers are unable to make scheduled payments or obtain credit, they may not be able to pay, or may delay payment of accounts receivable owed to us. These conditions also may have an adverse

10 | ||||||||

effect on certain of our suppliers who may reduce output or change terms of sales, which could cause a disruption in our ability to produce our products. Any inability of current and/or potential customers to pay us for our products or any demands by our suppliers for different payment terms may have a material adverse effect on our business, results of operations, financial condition and cash flows.

Currency exchange rate fluctuations could have a material adverse effect on our business and results of operations.

Due to our international operations, we transact business in many foreign currencies and are subject to the effects of changes in foreign currency exchange rates, including the Mexican peso, Japanese yen, Australian dollar and the Euro. Our financial statements are reported in U.S. dollars with international transactions being translated into U.S. dollars. If the U.S. dollar strengthens in relation to the currencies of other countries where we sell our products, our U.S. dollar reported net sales and income will decrease. Additionally, we incur significant costs in foreign currencies and a fluctuation in those currencies’ value can negatively impact manufacturing and selling costs. While we have in the past engaged, and may in the future engage, in various hedging transactions in attempts to minimize the effects of foreign currency exchange rate fluctuations, there can be no assurance that these hedging transactions will be effective. Changes in the relative values of currencies occur regularly and could have an adverse effect on our business, results of operations, financial condition and cash flows.

We are exposed to price fluctuations of key commodities, which may negatively impact our results of operations.

We rely on product inputs in the manufacture of our products. Prices of oil and gas affect our distribution and transportation costs. Prices of these commodities are volatile and have fluctuated significantly in recent years, which has contributed to, and in the future may continue to contribute to, fluctuations in our results of operations. Our ability to hedge commodity price volatility is limited. Furthermore, due to competitive dynamics, the cost containment efforts of our customers and third-party payors, and contractual limitations, particularly with respect to products we sell under group purchasing agreements, which generally set pricing for a three-year term, we may be unable to pass along commodity-driven cost increases through higher prices. If we cannot fully offset cost increases through other cost reductions, or recover these costs through price increases or surcharges, we could experience lower margins and profitability which could have a material adverse effect on our business, results of operations, financial condition and cash flows.

Cost-containment efforts of our customers, healthcare purchasing groups, third-party payors and governmental organizations could adversely affect our sales and profitability.

Many of our customers are members of GPOs, or integrated delivery networks (“IDNs”). GPOs and IDNs negotiate pricing arrangements with healthcare product manufacturers and distributors and offer the negotiated prices to affiliated hospitals and other members. Although we are the sole contracted supplier to certain GPOs for certain product categories, members of the GPO are generally free to purchase from other suppliers, and such contract positions can offer no assurance that sales volumes of those products will be maintained. In addition, initiatives sponsored by government agencies and other third-party payors to limit healthcare costs, including price regulation and competitive bidding for the sale of our products, are ongoing in markets where we sell our products. Pricing pressure has also increased in our markets due to consolidation among healthcare providers, trends toward managed care, governments becoming payors of healthcare expenses and regulation relating to reimbursements. The increasing leverage of organized buying groups and consolidated customers and pricing pressure from third-party payors may reduce market prices for our products, thereby reducing our profitability and have a material adverse effect on our business, results of operations, financial condition and cash flows.

We are subject to political, economic and regulatory risks associated with doing business outside of the United States.

Most of our manufacturing facilities are outside the United States in Mexico. We also may use contract manufacturers outside the United States from time to time and may source many of our raw materials and components from foreign suppliers. We distribute and sell our products in over 90 countries. In 2021, approximately 25% of our net sales were generated outside of North America and we expect this percentage will grow over time. Our operations outside of the United States are subject to risks that are inherent in conducting business internationally, including compliance with both United States and foreign laws and regulations that apply to our international operations. These laws and regulations include robust data privacy requirements, labor relations laws that may impede employer flexibility, tax laws, anti-competition regulations, import, customs and trade restrictions, export requirements, economic sanction laws, environmental, health and safety laws, anti-bribery laws such as the U.S. Foreign Corrupt Practices Act and similar anti-bribery laws in other jurisdictions. Given the high level of complexity of these laws, there is a risk that some provisions may be violated inadvertently or through fraudulent or negligent behavior of individual employees, our failure to comply with certain formal documentation requirements or otherwise. In addition, these laws are subject to changes, which may require additional resources or make it more difficult for us to comply with these laws. Violations of the laws and regulations governing our international operations could result in fines or criminal sanctions against us, our officers or our employees, and prohibitions on the conduct of our business. Any such violations could include prohibitions on our ability to manufacture or distribute our products in one or more countries and could have a material adverse effect on our reputation, our brand, our international expansion efforts, our ability to attract and retain employees, our business,

11 | ||||||||

results of operations, financial condition and cash flows. Our success depends, in part, on our ability to anticipate and prevent or mitigate these risks and manage difficulties as they arise.

We may be subject to trade protection measures that are being contemplated by the United States Government and other governments around the world, as well as potential disruptions in trade agreements, such as the exit of the United Kingdom from the EU. These measures and disruptions may result in new or higher tariffs, import-export restrictions and taxes. Changes in, or revised interpretations of import-export laws or international trade agreements, along with new or increased tariffs, trade restrictions or taxation on income earned or goods manufactured outside the United States may have a material adverse effect on our business, financial condition, results of operations and cash flows.

In addition to the foregoing, engaging in international business inherently involves a number of other difficulties and risks, including:

•different local medical practices, product preferences and product requirements,

•price and currency controls and exchange rate fluctuations,

•cost and availability of international shipping channels,

•longer payment cycles in certain countries other than the United States,

•minimal or diminished protection of intellectual property in certain countries,

•uncertainties regarding judicial systems, including difficulties in enforcing agreements through certain non-U.S. legal systems,

•political instability and actual or anticipated military or political conflicts, expropriation of assets, economic instability and the impact on interest rates, inflation and the credit worthiness of our customers, and

•difficulties and costs of staffing and managing non-U.S. operations.

These risks and difficulties, individually or in the aggregate, could have a material adverse effect on our business, results of operations, financial condition and cash flows.

We may need additional financing in the future to meet our capital needs or to make acquisitions and such financing may not be available on favorable terms, if at all.

We intend to continue our research and development activities and make acquisitions. Accordingly, we may need to seek additional debt or equity financing. We may be unable to obtain any desired additional financing on terms favorable to us, if at all. If adequate funds are not available on acceptable terms, we may be unable to fund our expansion, successfully develop or enhance products or respond to competitive pressures, any of which could negatively affect our business.

Risks Related to Ownership of Avanos Common Stock

We cannot guarantee that our stock price will not decline or fluctuate significantly.

The price at which Avanos common stock trades has and may continue to fluctuate significantly. The market price, or fluctuations in price, for Avanos common stock may be negatively influenced by many factors, including:

•actual or unanticipated fluctuations in our quarterly and annual operating results,

•our failure to achieve the quarterly financial results expected by the securities analysts who cover our stock,

•the outcome of litigation and enforcement actions,

•developments generally affecting the healthcare industry,

•changes in market valuations of comparable companies,

•the amount of our indebtedness,

•general economic, industry and market conditions,

•the depth and liquidity of the market for Avanos common stock,

•price fluctuations in key commodities,

•announcements by us or our competitors regarding performance, strategy, significant acquisitions, divestitures, strategic partnerships, joint ventures or capital commitments,

•fluctuations in interest and currency exchange rates,

•our dividend policy, and

•perceptions of or speculations by the press or investment community.

12 | ||||||||

These and other factors may lower the market price of Avanos common stock, regardless of our actual financial condition or operating performance.

We have no present intention to pay dividends on Avanos common stock.

We have no present intention to pay dividends on Avanos common stock. Any determination to pay dividends to holders of Avanos common stock will be at the discretion of our Board of Directors and will depend on many factors, including our financial condition, results of operations, projections, liquidity, earnings, legal requirements, restrictions in our debt agreements and other factors that our Board of Directors deems relevant.

The percentage of ownership of existing stockholders in Avanos may be diluted in the future.

In the future, a stockholder’s percentage ownership in Avanos may be diluted because of equity issuances for acquisitions, capital market transactions or otherwise, including equity awards that we may grant to our directors, officers and employees. In addition, our compensation committee has, and we anticipate that they will continue in the future to, grant stock options or other equity based awards to our employees. These awards will have a dilutive effect on existing stockholders and on our earnings per share, which could adversely affect the market price of shares of Avanos common stock.

In addition, our certificate of incorporation authorizes us to issue, without the approval of Avanos stockholders, one or more classes or series of preferred stock having such designation, powers, preferences and relative, participating, optional and other special rights, including preferences over Avanos common stock with respect to dividends and distributions, as our Board of Directors generally may determine. If our Board of Directors were to approve the issuance of preferred stock in the future, the terms of one or more classes or series of such preferred stock could dilute the voting power or reduce the value of Avanos common stock. Similarly, the repurchase or redemption rights or liquidation preferences we could assign to Avanos preferred stock could affect the residual value of Avanos common stock.

Certain provisions of our certificate of incorporation may make it difficult for stockholders to initiate litigation against us in a favorable forum for disputes with us or our directors or officers.

Our amended and restated certificate of incorporation designates the Court of Chancery of the State of Delaware (or if that court does not have jurisdiction, the U.S. District Court for the District of Delaware) as the exclusive forum for certain litigation that may be initiated by our stockholders, which could limit our stockholders’ ability to obtain a favorable judicial forum for disputes with us or our directors or officers.

Certain provisions of our certificate of incorporation and by-laws and of Delaware law may make it difficult for stockholders to change the composition of our Board of Directors and may discourage hostile takeover attempts which some of our stockholders may consider to be beneficial.

Certain provisions contained in our certificate of incorporation and by-laws and those contained in Delaware law may have the effect of delaying or preventing changes in control if our Board of Directors determines that such changes in control are not in the best interests of us and our stockholders. These provisions include, among other things, the following:

•the division of our Board of Directors into three classes, each with three-year staggered terms, although shareholders voted in 2020 to declassify our Board, and it will be fully declassified in 2023,

•the ability of our Board of Directors to issue shares of preferred stock and to determine the price and other terms, including preferences and voting rights, of those shares without stockholder approval,

•the inability of our stockholders to call a special meeting of stockholders,

•stockholder action may be taken only at a special or regular meeting of stockholders,

•advance notice procedures for nominating candidates to our Board of Directors or presenting matters at stockholder meetings,

•stockholder removal of directors only for cause and only by a supermajority vote,

•the ability of our Board of Directors, and not our stockholders, to fill vacancies on our Board of Directors, and

•supermajority voting requirements to amend our by-laws and certain provisions of our certificate of incorporation and to engage in certain types of business combinations.

While these provisions have the effect of encouraging persons seeking to acquire control of our company to negotiate with our Board of Directors, they could enable the Board of Directors to hinder or frustrate a transaction that some, or a majority, of the stockholders might believe to be in their best interests and, in that case, may prevent or discourage attempts to remove and replace incumbent directors. We are also subject to Delaware laws that could have similar effects. One of these laws prohibits us from engaging in a business combination with a significant stockholder unless specific conditions are met.

13 | ||||||||

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

We own or lease operating facilities located throughout the world that handle manufacturing production, assembly, research, quality assurance testing, distribution and packaging of our products. We believe our facilities are suitable and adequate for our present operations. We lease our principal executive offices that are located in Alpharetta, Georgia. The locations of our principal medical device production facilities owned or leased by us around the world are as follows:

| Location | Country | Owned/Leased | ||||||||||||

| Nogales | Mexico | Owned | ||||||||||||

| Nogales | Mexico | Leased | ||||||||||||

| Tucson, Arizona | USA | Leased | ||||||||||||

| Magdalena | Mexico | Leased | ||||||||||||

| Tijuana | Mexico | Leased | ||||||||||||

ITEM 3. LEGAL PROCEEDINGS

See “Commitments and Contingencies” in Note 13 to the consolidated financial statements in Item 8 of this report for a description of current legal matters.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Avanos common stock is listed on the New York Stock Exchange (“NYSE”) under the ticker symbol “AVNS”. We did not pay any dividends on our common stock in the years ended December 31, 2021 and 2020 and we do not expect to pay any cash dividends on our common stock in the foreseeable future.

As of February 15, 2022, we had 10,767 holders of record of our common stock.

For information relating to securities authorized for issuance under equity compensation plans, see Part III, Item 12 of this Form 10-K.

Performance

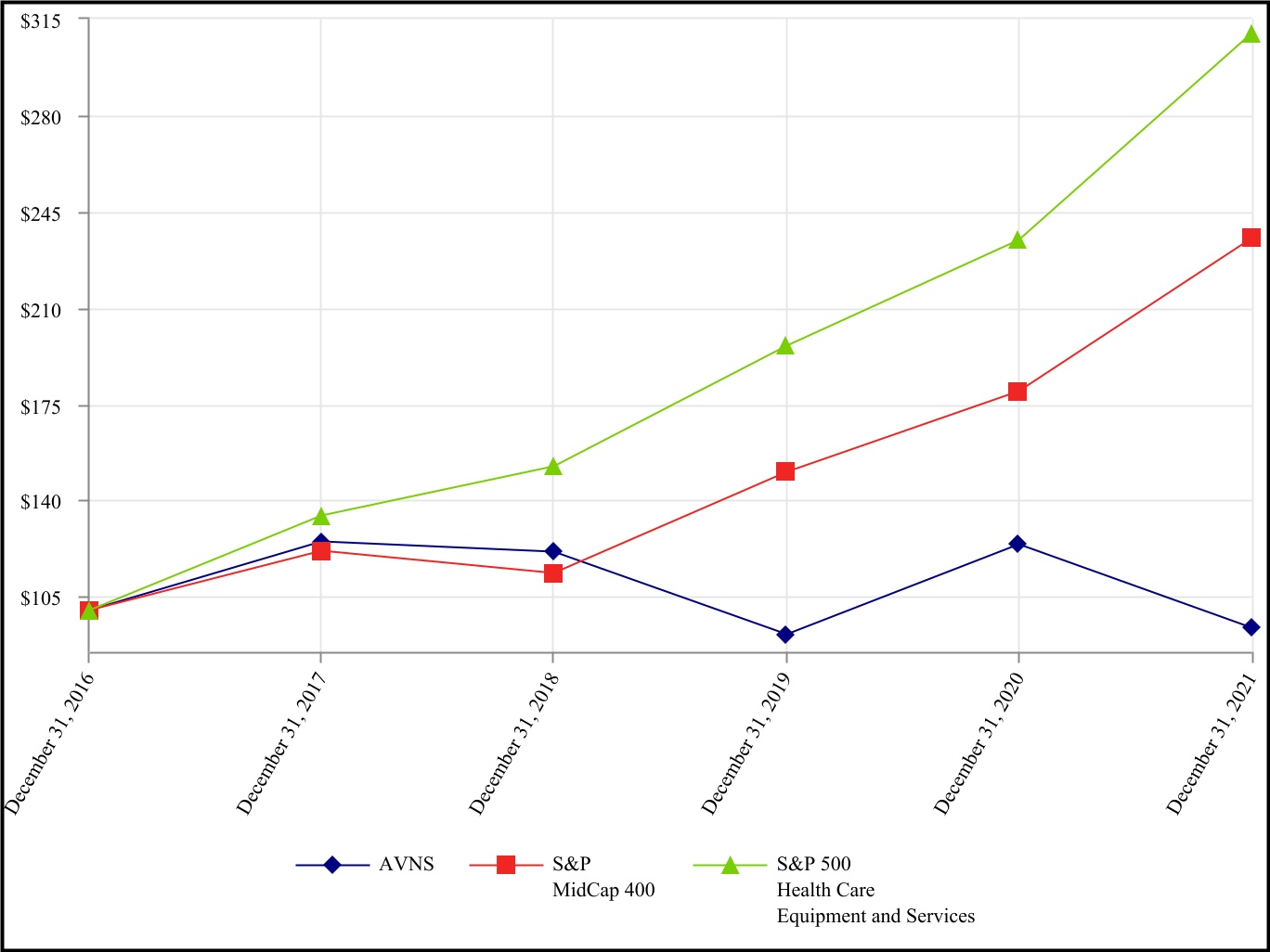

The following graph compares the cumulative total return of our common stock from December 31, 2016 through December 31, 2021 with the cumulative return of companies comprising the Standard and Poor’s S&P MidCap 400 Index and the S&P 500 Health Care Equipment and Services Index. The graph plots the change in value of an initial investment of $100 in each of our common stock, the S&P MidCap 400 Index and the S&P 500 Health Care Equipment and Services Index over the indicated time periods and assumes reinvestment of all dividends, if any, paid on the securities. We have not paid any cash dividends, and therefore, the cumulative total return calculation for us is based solely upon stock price appreciation and not upon reinvestment of cash dividends. The stock price performance shown on the graph is not necessarily indicative of future price performance.

14 | ||||||||

The preceding chart is based on the following data:

| AVNS | S&P MidCap 400 | S&P 500 Health Care Equipment and Services | |||||||||||||||

| December 31, 2016 | $ | 100.00 | $ | 100.00 | $ | 100.00 | |||||||||||

| December 31, 2017 | 124.88 | 121.58 | 134.39 | ||||||||||||||

| December 31, 2018 | 121.12 | 113.51 | 152.32 | ||||||||||||||

| December 31, 2019 | 91.13 | 150.24 | 196.19 | ||||||||||||||

| December 31, 2020 | 124.07 | 179.70 | 234.53 | ||||||||||||||

| December 31, 2021 | 93.75 | 235.27 | 309.83 | ||||||||||||||

ITEM 6. Reserved

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Introduction

Avanos is a medical technology company focused on delivering clinically superior breakthrough medical device solutions to improve patients’ quality of life. We are committed to addressing some of today’s most important healthcare needs, such as reducing the use of opioids while helping patients move from surgery to recovery. We develop, manufacture and market clinically superior solutions in more than 90 countries.

15 | ||||||||