Table of Contents

SUBMITTED CONFIDENTIALLY TO THE SECURITIES AND EXCHANGE COMMISSION ON JUNE 23, 2014

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM F-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

HÖEGH LNG PARTNERS LP

(Exact name of Registrant as specified in its charter)

| Republic of the Marshall Islands | 4400 | Not Applicable | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(IRS Employer Identification No.) |

2 Reid Street, Hamilton, HM 11, Bermuda +1 (441) 295-6815

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Watson, Farley & Williams LLP

1133 Avenue of the Americas

New York, New York 10036

(212) 922-2200

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Catherine S. Gallagher Adorys Velazquez Vinson & Elkins L.L.P. 2200 Pennsylvania Avenue NW, Suite 500W Washington, DC 20037 Telephone: (202) 639-6500 Facsimile: (202) 639-6604 |

Joshua Davidson Baker Botts L.L.P. 910 Louisiana Street Houston, Texas 77002 Telephone: (713) 229-1234 Facsimile: (713) 229-1522 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of each class of securities to be registered |

Proposed maximum aggregate offering price(1)(2) |

Amount of registration fee(3) | ||

| Common units representing limited partner interests |

$ | $ | ||

|

| ||||

|

| ||||

| (1) | Includes common units issuable upon exercise of the underwriters’ option to purchase additional common units. |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o). |

| (3) | To be paid in connection with the initial filing of the registration statement. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED , 2014

PRELIMINARY PROSPECTUS

Höegh LNG Partners LP

Common Units

Representing Limited Partner Interests

$ per common unit

This is the initial public offering of our common units. We are selling common units in this offering. Prior to this offering, there has been no public market for our common units. We anticipate that the initial public offering price will be between $ and $ per common unit. To the extent the underwriters sell more than common units in this offering, the underwriters have an option to purchase up to additional common units.

We are a Marshall Islands limited partnership formed to own, operate and acquire floating storage and regasification units (“FSRUs”), liquefied natural gas (“LNG”) carriers and other LNG infrastructure assets under long-term charters. At the closing of this offering, interests in our initial fleet of FSRUs will be contributed to us by Höegh LNG Holdings Ltd., a leading floating LNG service provider. Although we are organized as a limited partnership, we have elected to be treated as a corporation solely for U.S. federal income tax purposes. We have applied to list our common units on the New York Stock Exchange, under the symbol “HMLP.”

We are an “emerging growth company,” and we are eligible for reduced reporting requirements. See “Summary—Implications of Being an Emerging Growth Company.” Investing in our common units involves risks. Please read “Risk Factors” beginning on page 24.

These risks include the following:

| • | Our initial fleet consists of only three vessels. Any limitation on the availability or operation of those vessels could have a material adverse effect on our business, financial condition and results of operations. |

| • | We currently derive all of our revenue from two customers, and the loss of either of these customers would result in a significant loss of revenues and cash flow. |

| • | We may not have sufficient cash from operations following the establishment of cash reserves and payment of fees and expenses to enable us to pay the minimum quarterly distribution on our units. |

| • | We will be required to make substantial capital expenditures to maintain and expand our fleet, which will reduce our cash available for distribution. |

| • | We depend on Höegh LNG Holdings Ltd. and its subsidiaries for the management of our fleet and to assist us in operating and expanding our business. |

| • | Unitholders have limited voting rights, and our partnership agreement restricts the voting rights of unitholders who own more than 4.9% of our common units. |

| • | Our general partner and its affiliates own a significant interest in us and have conflicts of interest and limited duties to us and our unitholders, which may permit them to favor their own interests to your detriment. |

| • | Our general partner has a limited call right that may require you to sell your common units at an undesirable time or price. |

| • | U.S. tax authorities could treat us as a “passive foreign investment company,” which would have adverse U.S. federal income tax consequences to U.S. unitholders. |

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Common Unit | Total | |||||||

| Public Offering Price |

$ | $ | ||||||

| Underwriting Discount(1) |

$ | $ | ||||||

| Proceeds to Höegh LNG Partners LP (before expenses) |

$ | $ | ||||||

| (1) | Excludes an aggregate structuring fee of $ ( % of the offering proceeds) payable to Citigroup Global Markets Inc. See “Underwriting.” |

The underwriters expect to deliver the common units to purchasers on or about , 2014 through the book-entry facilities of The Depository Trust Company.

Citigroup

, 2014

Table of Contents

Table of Contents

We are responsible for the information contained in this prospectus and in any free writing prospectus we prepare or authorize. We have not authorized anyone to provide you with different information, and we take no responsibility for any other information others may give you. We are not, and the underwriters are not, making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date of this prospectus.

i

Table of Contents

| 96 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

101 | |||

| 101 | ||||

| 105 | ||||

| 106 | ||||

| 107 | ||||

| 109 | ||||

| 109 | ||||

| 109 | ||||

| 110 | ||||

| 124 | ||||

| 132 | ||||

| 132 | ||||

| 132 | ||||

| 134 | ||||

| 134 | ||||

| 135 | ||||

| 135 | ||||

| 136 | ||||

| 137 | ||||

| 139 | ||||

| 141 | ||||

| 143 | ||||

| 144 | ||||

| 145 | ||||

| 145 | ||||

| 146 | ||||

| 147 | ||||

| 148 | ||||

| 148 | ||||

| 149 | ||||

| 150 | ||||

| 152 | ||||

| 152 | ||||

| 153 | ||||

| 154 | ||||

| 154 | ||||

| 155 | ||||

| 156 | ||||

| 159 | ||||

| 159 | ||||

| 168 | ||||

| 168 | ||||

| 169 | ||||

| 170 | ||||

| 170 | ||||

| 171 | ||||

| 180 | ||||

| 180 | ||||

| 180 |

ii

Table of Contents

| 187 | ||||

| 187 | ||||

| 188 | ||||

| 190 | ||||

| 190 | ||||

| 190 | ||||

| 191 | ||||

| 191 | ||||

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT |

194 | |||

| 195 | ||||

| 195 | ||||

| 195 | ||||

| 196 | ||||

| 196 | ||||

| Restrictions on Transfer of Equity Interests; Purchase Rights |

196 | |||

| 197 | ||||

| 198 | ||||

| Distributions and Payments to our General Partner and Its Affiliates |

198 | |||

| 199 | ||||

| 210 | ||||

| 210 | ||||

| 210 | ||||

| 210 | ||||

| 211 | ||||

| 214 | ||||

| 214 | ||||

| 217 | ||||

| 221 | ||||

| 221 | ||||

| 221 | ||||

| 221 | ||||

| 223 | ||||

| 223 | ||||

| 223 | ||||

| 223 | ||||

| 223 | ||||

| 223 | ||||

| 225 | ||||

| 226 | ||||

| 226 | ||||

| 227 | ||||

| 227 | ||||

| 229 | ||||

| 230 | ||||

| 230 | ||||

| 230 | ||||

| 232 | ||||

| 232 | ||||

| 232 | ||||

| 232 | ||||

| 233 | ||||

| 233 | ||||

| 234 |

iii

Table of Contents

| 235 | ||||

| 235 | ||||

| 235 | ||||

| 235 | ||||

| 236 | ||||

| 236 | ||||

| 237 | ||||

| 238 | ||||

| 238 | ||||

| 238 | ||||

| 243 | ||||

| 243 | ||||

| 245 | ||||

| 245 | ||||

| 245 | ||||

| 246 | ||||

| 246 | ||||

| 248 | ||||

| Notice to Prospective Investors in the European Economic Area |

250 | |||

| 251 | ||||

| 252 | ||||

| 252 | ||||

| 252 | ||||

| 252 | ||||

| 253 | ||||

| 254 | ||||

| 254 | ||||

| 254 | ||||

| 255 | ||||

| 255 | ||||

| 256 | ||||

| FORM OF FIRST AMENDED AND RESTATED AGREEMENT OF LIMITED PARTNERSHIP OF HÖEGH LNG PARTNERS LP |

A-1 |

iv

Table of Contents

SERVICE OF PROCESS AND ENFORCEMENT OF CIVIL LIABILITIES

We are organized under the laws of the Marshall Islands as a limited partnership. Our general partner is organized under the laws of the Marshall Islands as a limited liability company. The Marshall Islands has a less developed body of securities laws as compared to the United States and provides protections for investors to a significantly lesser extent.

Most of our directors and officers and those of our subsidiaries are residents of countries other than the United States. Substantially all of our and our subsidiaries’ assets and a substantial portion of the assets of our directors and officers are located outside the United States. As a result, it may be difficult or impossible for U.S. investors to effect service of process within the United States upon us, our directors or officers, our general partner or our subsidiaries or to realize against us or them judgments obtained in U.S. courts, including judgments predicated upon the civil liability provisions of the securities laws of the United States or any state in the United States. However, we have expressly submitted to the jurisdiction of the U.S. federal and New York state courts sitting in the City of New York for the purpose of any suit, action or proceeding arising under the securities laws of the United States or any state in the United States, and we have appointed The Trust Company of the Marshall Islands, Inc., Trust Company Complex, Ajeltake Island, Ajeltake Road, Majuro, Marshall Islands MH96960, to accept service of process on our behalf in any such action.

Watson, Farley & Williams LLP, our counsel as to Marshall Islands law, has advised us that there is uncertainty as to whether the courts of the Marshall Islands would (i) recognize or enforce against us, our general partner or our directors or officers judgments of courts of the United States based on civil liability provisions of applicable U.S. federal and state securities laws or (ii) impose liabilities against us, our general partner or our directors and officers in original actions brought in the Marshall Islands, based on these laws.

PRESENTATION OF FINANCIAL INFORMATION

Predecessor and Rule 3-09 Financial Statements

The combined carve-out financial statements of our predecessor for accounting purposes, Höegh LNG Partners LP Predecessor (“our predecessor”), reflect interests in (i) Hoegh LNG Lampung Pte Ltd. and PT Hoegh LNG Lampung (the owner of the newbuilding FSRU, the PGN FSRU Lampung) and (ii) two joint ventures: SRV Joint Gas Ltd. (the owner of the FSRU, the GDF Suez Neptune) and SRV Joint Gas Two Ltd. (the owner of the FSRU, the GDF Suez Cape Ann). Our predecessor accounts for its equity interests in the two joint ventures as equity method investments in its combined carve-out financial statements. Rule 3-09 of Regulation S-X requires separate financial statements (“Rule 3-09 financial statements”) of 50% or less owned persons accounted for under the equity method by a registrant such as us if either the income or the investment test in Rule 1-02(w) of Regulation S-X exceeds 20%. Furthermore, Rule 3-09(c) of Regulation S-X provides for the combination of Rule 3-09 financial statements if the underlying investments are under common management. In such scenarios, the significance of investments under Rule 1-02(w) of Regulation S-X is to be measured on a combined basis. We have determined that common management exists among the joint ventures owning the GDF Suez Neptune and the GDF Suez Cape Ann, which exceed the 20% significance tests of Rule 3-09 of Regulation S-X. Accordingly, this prospectus includes audited combined financial statements as of and for the years ended December 31, 2013 and 2012 for the joint ventures owning the GDF Suez Neptune and the GDF Suez Cape Ann. Such financial statements, including related notes thereto, have been prepared in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”).

v

Table of Contents

This summary highlights information contained elsewhere in this prospectus. Unless we otherwise specify, all references to information and data in this prospectus about our business and fleet refer to our business and interests in our initial fleet of FSRUs that will be contributed to us upon the closing of this offering. Prior to the closing of this offering, we will not own interests in any vessels. You should read the entire prospectus carefully, including the historical combined carve-out financial statements of our predecessor and the notes to those financial statements. The information presented in this prospectus assumes, unless otherwise noted, (1) an initial public offering price of $ per common unit (the midpoint of the price range set forth on the cover page of this prospectus) and (2) that the underwriters do not exercise their option to purchase additional common units. You should read “Risk Factors” for more information about important risks that you should consider carefully before buying our common units. Unless otherwise indicated, all references to “dollars” and “$” in this prospectus are to, and amounts are presented in, U.S. Dollars.

References in this prospectus to “Höegh LNG Partners,” “we,” “our,” “us” and “the Partnership” or similar terms when used in a historical context refer to Höegh LNG Holdings Ltd. and its vessels and the subsidiaries that hold interests in the vessels in our initial fleet. When used in the present tense or prospectively, those terms refer to Höegh LNG Partners LP or any one or more of its subsidiaries, or to all such entities unless the context otherwise indicates. Unless the context requires otherwise, references in this prospectus to our or the “joint ventures” refer to the joint ventures that own two of the vessels in our initial fleet (the GDF Suez Neptune and the GDF Suez Cape Ann). Please read “—Summary Historical Financial and Operating Data” beginning on page 19 for an overview of our predecessor’s and our joint ventures’ operating results and financial position.

References in this prospectus to “our general partner” refer to Höegh LNG GP LLC, the general partner of Höegh LNG Partners. References in this prospectus to “our operating company” refer to Höegh LNG Partners Operating LLC, a wholly owned subsidiary of the Partnership. References in this prospectus to “Höegh UK” refer to Hoegh LNG Services Ltd, a wholly owned subsidiary of our operating company. References in this prospectus to “Höegh Lampung” refer to Hoegh LNG Lampung Pte Ltd., a wholly owned subsidiary of our operating company. References in this prospectus to “Höegh LNG” refer, depending on the context, to Höegh LNG Holdings Ltd. and to any one or more of its direct and indirect subsidiaries, other than us. References in this prospectus to “Höegh LNG Management” refer to Höegh LNG Fleet Management AS, a wholly owned subsidiary of Höegh LNG. References in this prospectus to “Höegh Maritime Management” refer to Hoegh LNG Maritime Management Pte. Ltd., a wholly owned subsidiary of Höegh LNG. References in this prospectus to “Höegh Norway” refer to Höegh LNG AS, a wholly owned subsidiary of Höegh LNG. References in this prospectus to “Höegh Asia” refer to Hoegh LNG Asia Pte. Ltd., a wholly owned subsidiary of Höegh LNG. References in this prospectus to “Höegh Shipping” refer to Hoegh LNG Shipping Services Pte Ltd, a wholly owned subsidiary of Höegh LNG. References in this prospectus to “Leif Höegh UK” refer to Leif Höegh (U.K.) Limited, a wholly owned subsidiary of Höegh LNG. References in this prospectus to “PT Hoegh” refer to PT Hoegh LNG Lampung, the owner of the PGN FSRU Lampung. References in this prospectus to “GDF Suez” refer to GDF Suez LNG Supply SA, a subsidiary of GDF Suez S.A. References in this prospectus to “PGN” refer to PT PGN LNG Indonesia, a subsidiary of PT Perusahaan Gas Negara (Persero) Tbk.

We are a growth-oriented limited partnership formed by Höegh LNG Holdings Ltd. (Oslo Børs symbol: HLNG), a leading floating LNG service provider, to own, operate and acquire floating storage and regasification units (“FSRUs”), LNG carriers and other LNG infrastructure assets under long-term charters, which we define as charters of five or more years. At the closing of this offering, interests in our initial fleet of FSRUs will be contributed to us by Höegh LNG.

1

Table of Contents

Our initial fleet will consist of modern FSRUs that operate under long-term charters with major energy companies or utilities. We intend to grow our business in the FSRU, LNG carrier and LNG infrastructure market through acquisitions from Höegh LNG and third parties. We also believe we can grow organically by continuing to provide reliable service to our customers and leveraging Höegh LNG’s relationships, expertise and reputation.

Upon the closing of this offering, our initial fleet will consist of interests in the following vessels:

| • | a 50% interest in the GDF Suez Neptune, an FSRU built in 2009 that is currently operating under a time charter with GDF Suez, a subsidiary of GDF Suez S.A., a French publicly listed, government-backed, electric utility company, and the leading LNG importer in Europe in 2012, that expires in 2029, with an option to extend for up to two additional periods of five years each; |

| • | a 50% interest in the GDF Suez Cape Ann, an FSRU built in 2010 that is currently operating under a time charter with GDF Suez that expires in 2030, with an option to extend for up to two additional periods of five years each; and |

| • | a 100% economic interest in the PGN FSRU Lampung, an FSRU built in 2014 that is expected to commence operations in July 2014 under a time charter with PGN, a subsidiary of an Indonesian publicly listed, government-controlled, gas and energy company that constructs gas pipelines and infrastructure and distributes and transmits natural gas to industrial, commercial and household users, that expires in 2034, with options to extend either for an additional 10 years or for up to two additional periods of five years each. |

For a description of our joint venture partners and the joint venture agreements related to the vessels in our initial fleet, please read “Our Joint Ventures and Joint Venture Agreements.”

We intend to leverage our relationship with Höegh LNG to make accretive acquisitions, which would be expected to increase our per unit cash available for distribution, of FSRUs, LNG carriers and other LNG infrastructure assets with long-term charters from Höegh LNG and third parties. Pursuant to the omnibus agreement we will enter into with Höegh LNG, our general partner, and our operating company at the closing of this offering, we will have a right to purchase from Höegh LNG any FSRU or LNG carrier operating under a charter of five or more years. Also pursuant to the omnibus agreement, we will have the right to purchase from Höegh LNG all or a portion of its interests in the FSRU, the Independence. In addition, we expect that Höegh LNG will secure a charter of five or more years for two additional newbuilding FSRUs, the Höegh Gallant and Hull no. 2551, at which point we will have the right to purchase them from Höegh LNG pursuant to the omnibus agreement. We cannot assure you that we will make any particular acquisition or that as a consequence we will successfully grow the amount of our per unit distributions. Among other things, our ability to acquire additional FSRUs, LNG carriers and other LNG infrastructure assets will be dependent upon our ability to raise additional equity and debt financing.

The Independence was constructed by Hyundai Heavy Industries Co., Ltd. (“HHI”) and was delivered to Höegh LNG from the shipyard in May 2014. Beginning no later than the fourth quarter of 2014, the Independence will operate under a time charter that expires in 2024 with AB Klaipèdos Nafta (“ABKN”), a Lithuanian publicly listed, government-controlled utility. We will have the right to purchase all or a portion of Höegh LNG’s interests in the Independence within 24 months after acceptance of such vessel by her charterer, subject to reaching an agreement with Höegh LNG regarding the purchase price and other terms in accordance with the provisions of the omnibus agreement and any rights ABKN has under the related time charter. We may exercise this option at one or more times during such 24-month period. Acceptance occurs after the vessel has been delivered and all inspections and testing of the vessel have been completed in accordance with the applicable charter requirements.

2

Table of Contents

The Höegh Gallant and Hull no. 2551 also are being constructed by HHI and are scheduled for delivery to Höegh LNG from the shipyard in July 2014 and March 2015, respectively. Although the Höegh Gallant and Hull no. 2551 have not yet been chartered, Höegh LNG is involved in several tender processes for FSRU projects globally, and we expect Höegh LNG to secure a charter of five or more years for both of them.

Our Relationship with Höegh LNG

We believe that one of our principal strengths is our relationship with Höegh LNG. With a track record dating back to the delivery of the world’s first Moss-type LNG carrier in 1973, we believe that Höegh LNG is one of the most experienced operators of LNG carriers and one of only three operators of FSRUs in the world. Our affiliation with Höegh LNG gives us access to Höegh LNG’s long-standing relationships with leading oil and gas companies, utility companies, shipbuilders, financing sources and suppliers, which we believe will allow us to compete more effectively when seeking additional long-term charters for FSRUs, LNG carriers and other LNG infrastructure assets. In addition, we believe Höegh LNG’s 40-year track record of providing LNG services and its technical, commercial and managerial expertise, including its leadership in the development of floating liquefaction solutions, will enable us to continue to maintain the high utilization of our fleet to preserve our stable cash flows. We cannot assure you that our relationship with Höegh LNG will lead to high fleet utilization rates or stable cash flows in the future.

We believe the following factors create opportunities for us to successfully execute our business strategy and plan and grow our business:

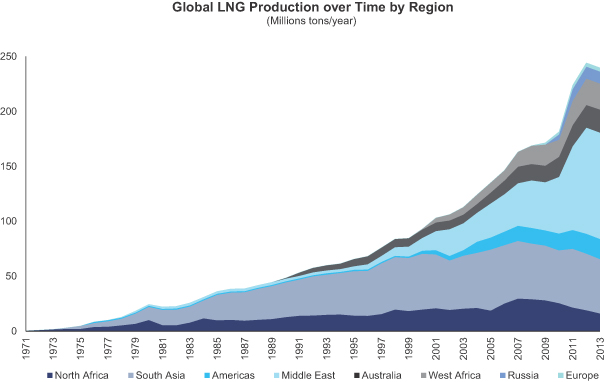

| • | Natural Gas and LNG Demand Growth. Natural gas is projected to be the fastest growing fossil fuel due to its low carbon intensity and clean burning characteristics, an abundance of reserves, market deregulation and global economic growth. According to Fearnley Consultants AS, a provider of maritime research and data compilation (“Fearnley Consultants”), LNG production capacity based on existing construction projects is projected to increase by nearly 40% by the end of 2020, and LNG exports transported by sea are projected to grow more than twice as fast as overall natural gas consumption through 2035. The number of countries importing LNG has more than doubled from 12 in 2000 to 29 in 2013. As increasing volumes of LNG are destination flexible (versus serving long-term, dedicated, point-to-point trade), and regional price differences in gas persist, more countries find LNG imports to be an important part of their energy strategy. We cannot assure you that growth rates comparable to historical growth rates or that projected growth rates for natural gas, LNG, LNG carriers or FSRUs will be achieved. Please read “Risk Factors” and “Industry.” |

| • | Advantages of Newbuilding FSRU Solutions. We believe that FSRUs have several advantages over traditional, onshore LNG terminals, including greater operational and market flexibility, accelerated project execution, reduced cost and more predictable capital investment requirements. The cost and flexibility of FSRU solutions have enabled certain markets to plan to import LNG to diversify supply and contribute to energy security. Newbuilding FSRUs are typically larger and more efficient than converted FSRU units. They can also compete as conventional LNG carriers when not operating as FSRUs. |

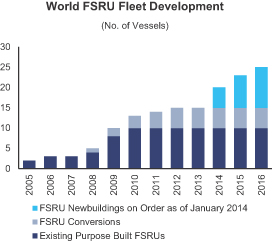

| • | Growing Demand for FSRUs. Demand for FSRUs is driven by importers’ desire for flexible and cost-effective import schemes to meet growing LNG requirements. FSRUs are able to quickly react to demand and evolving LNG price. They also offer a unique solution for small or highly seasonal markets. We believe that these factors will increasingly motivate customers to choose FSRUs for LNG importation needs. According to Fearnley Consultants, approximately 60 plans for FSRUs are being considered, compared to 19 FSRUs in operation as of May 2014. |

3

Table of Contents

| • | High Barriers to Entry. We believe the capital investment, regulatory and permitting and technical capabilities required to build and operate FSRUs and other LNG infrastructure act as substantial barriers to entry for potential competitors. Leading energy companies and utilities have increasingly strict pre-qualification and ongoing technical requirements for operators, and there are only three companies with experience of building and operating FSRUs. We believe that due to stringent requirements, customers will continue to look to experienced technical operators with proven track records for LNG infrastructure requirements. |

We can provide no assurance, however, that the industry dynamics described above will continue.

We believe that our future prospects for success are enhanced by the following aspects of our business:

| • | Relationship with a Leader in Floating Regasification Technology. We believe we will benefit from our relationship with Höegh LNG, a fully integrated provider of floating LNG infrastructure services, offering regasification and transportation services under long-term charters. Höegh LNG is one of only three operators of FSRUs in the world and has extensive experience in providing LNG transportation, having been operating since 1973, when it delivered the world’s first Moss-type LNG carrier. We believe that Höegh LNG’s expertise in the LNG sector, strong relationships with customers, shipyards and financial institutions, and newbuilding strategy will enable Höegh LNG to attract additional long-term charters for FSRUs, LNG carriers and other LNG infrastructure assets, which would in turn enhance our growth opportunities. |

| • | Secure Cash Flows from Long-Term Charters with Strong Counterparties. All three of our vessels operate under fixed-rate charters with an average remaining firm contract duration of 17 years as of March 31, 2014, excluding the exercise of any options. Both of our customers, GDF Suez (France) and PGN (Indonesia), are government-backed utility companies. Under our time charters, substantially all of our vessel operating expenses, including operating and maintenance expenses such as daily running costs and drydocking, are passed through to our customers. In addition, under these charters, we have no direct exposure to commodity prices and limited exposure to foreign exchange rates as all revenues are paid in U.S. Dollars. |

| • | Built-In Growth Opportunities. In addition to our initial fleet of three FSRUs, we will have the right to purchase from Höegh LNG additional assets on long-term charters, including the Independence. Commencing no later than the fourth quarter of 2014, the Independence will operate under a long-term, fixed-rate time charter of an initial duration of 10 years with ABKN, a Lithuanian publicly listed, government-controlled utility. We further expect Höegh LNG will secure long-term charters for two additional newbuilding FSRUs, which we would then have the right to purchase. We will also have the right to purchase any other additional FSRUs and LNG carriers in Höegh LNG’s fleet that are placed under a charter of five or more years. |

| • | Modern, Technologically Advanced Fleet. Both our initial fleet and the three newbuilding FSRUs that Höegh LNG has on order will be equipped with the latest floating, storage and regasification technology in terms of size, onboard regasification of LNG, thermal insulation, power generation and regas systems. These vessels have all been built by leading shipyards in South Korea that have constructed much of the world’s newbuilding FSRU fleet. We believe the significant investment needed to build FSRUs and our ability to customize specifications to customers’ requirements and to provide highly trained personnel for operations create significant barriers to entry for new competitors. As a result, we believe that we are positioned to become a preferred provider of FSRUs and other LNG infrastructure assets and to secure additional long-term charters. |

4

Table of Contents

| • | Höegh LNG’s Record of Efficiency, Safety and Operational Performance. Through its technical expertise in Höegh LNG Management, Höegh LNG has been safely and efficiently operating LNG vessels since 1973. With approximately 96 onshore employees and approximately 350 seafarers, Höegh LNG maintains global operations with in-house engineering expertise that allows us to offer our customers reliable and efficient performance, while maintaining close control over operating costs. This operational performance will also support our stable cash flow profile by maintaining high utilization of our fleet. |

We can provide no assurance, however, that we will be able to utilize our strengths described above. For further discussion of the risks that we face, please read “Risk Factors.”

Our primary business objective is to increase quarterly distributions per unit over time by executing the following strategies:

| • | Focus on FSRU Newbuilding Acquisitions. We intend to acquire newbuilding FSRUs on long-term charters, rather than FSRUs based on retrofitted, first-generation LNG carriers. We believe newbuilding vessels offer the greatest flexibility. Newbuilding FSRUs have superior fuel efficiency, improved storage performance and larger capacity than retrofitted, first-generation LNG carriers. Their larger capacity allows for a full cargo from a comparably sized, modern-day LNG carrier to be offloaded in a single transfer, and this streamlines logistics. In addition, Höegh LNG has strong customer relationships deriving from its ability to work alongside customers on their vessel design needs. Moreover, Höegh LNG pursues a strategy of maintaining one or more uncontracted newbuilding vessel on order so it can provide its customers an FSRU with minimum lead time. We believe that Höegh LNG’s ability to offer newbuild vessels promptly and its engineering expertise make it an operator of choice for projects that require rapid execution, complex engineering or unique specifications. This, in turn, enhances the growth opportunities available to us. |

| • | Pursue Strategic and Accretive Acquisitions of FSRUs, LNG Carriers and Other LNG Infrastructure Assets on Long-Term, Fixed-Rate Charters with Strong Counterparties. We will seek to leverage our relationship with Höegh LNG to make strategic and accretive acquisitions. Pursuant to the omnibus agreement that we will enter into with Höegh LNG, our general partner, and our operating company, we will have the right to purchase all or a portion of Höegh LNG’s interests in the Independence, as well as any newbuilding FSRU or LNG carrier under a charter of five or more years. We also intend to take advantage of business opportunities and market trends in the LNG transportation industry to grow our assets through third-party acquisitions of FSRUs, LNG carriers and other LNG infrastructure assets under long-term charters. |

| • | Expand Global Operations in High-Growth Regions. We will seek to capitalize on opportunities emerging from the global expansion of LNG production activity and the need to provide flexible regasification solutions in areas which require natural gas imports. According to Fearnley Consultants, growth in FSRU demand is expected to accelerate beyond 2015, and currently there are approximately 60 FSRU projects under consideration globally. We believe that Höegh LNG’s position as one of three FSRU operators in the world, 40-year operational track record and strong customer relationships will enable us to have early access to new projects worldwide. |

| • | Enhance and Diversify Customer Relationships Through Continued Operating Excellence and Technological Innovation. We intend to maintain and grow our cash flows by focusing on strong customer relationships and actively seeking the extension and renewal of existing charters, entering into new long-term charters with current customers, and identifying new business opportunities with other creditworthy charterers. We believe our customer relationships are enhanced by our ability to provide expert technical advice to our customers through Höegh LNG’s in-house engineering department, which |

5

Table of Contents

| in turn enables us to be directly involved in our customers’ project development processes. In addition, we will continue to incorporate safety, health, security and environmental stewardship into all aspects of vessel design and operation in order to satisfy our customers and comply with national and international rules and regulations. We believe that Höegh LNG’s operational expertise, recognized position, and track record in floating LNG infrastructure services will position us favorably to capture additional commercial opportunities in the FSRU and LNG sectors. |

We can provide no assurance, however, that we will be able to implement our business strategies described above or that the business strategies discussed above will increase our quarterly distributions. For further discussion of the risks that we face, please read “Risk Factors.”

An investment in our common units involves risks associated with our business, our partnership structure and the tax characteristics of our common units. Please read carefully the risks described under “Risk Factors” beginning on page 24 of this prospectus.

Implications of Being an Emerging Growth Company

Our predecessor had less than $1.0 billion in revenue during its last fiscal year, which means that we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act (the “JOBS Act”). An emerging growth company may take advantage of specified reduced reporting and other burdens that are otherwise applicable generally to public companies. These provisions include:

| • | the ability to present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations in the registration statement of its initial public offering; |

| • | exemption from the auditor attestation requirement in the assessment of the emerging growth company’s internal control over financial reporting; |

| • | exemption from new or revised financial accounting standards applicable to public companies until such standards are also applicable to private companies; and |

| • | exemption from compliance with any new requirements adopted by the Public Company Accounting Oversight Board requiring mandatory audit firm rotation or a supplement to the auditor’s report in which the auditor would be required to provide additional information about the audit and financial statements. |

We may take advantage of these provisions until the end of the fiscal year following the fifth anniversary of our initial public offering or such earlier time that we are no longer an emerging growth company. We will cease to be an emerging growth company if we have more than $1.0 billion in annual revenues, have more than $700 million in market value of our common units held by non-affiliates, or issue more than $1.0 billion of non-convertible debt over a three-year period. We may choose to take advantage of some, but not all, of these reduced burdens. For as long as we take advantage of the reduced reporting obligations, the information that we provide unitholders may be different than information provided by other public companies. We are choosing to “opt out” of the extended transition period relating to the exemption from new or revised financial accounting standards and, as a result, we will comply with new or revised financial accounting standards on the relevant dates on which adoption of such standards is required for non-emerging growth companies. Section 107 of the JOBS Act provides that our decision to opt out of the extended transition period for complying with new or revised financial accounting standards is irrevocable.

6

Table of Contents

We were formed on April 28, 2014 as a Marshall Islands limited partnership to own, operate and acquire FSRUs, LNG carriers and other LNG infrastructure assets under long-term charters. Prior to the closing of this offering, we will not own any vessels or other assets.

Prior to the closing of this offering, we and Höegh LNG will enter into transactions by which, among other things, Höegh LNG will contribute to us all of its equity interests and loans and promissory notes due to it and affiliates in each of the entities owning the GDF Suez Neptune, the GDF Suez Cape Ann and the PGN FSRU Lampung.

At or prior to the closing of this offering, the following transactions will occur:

| • | we will issue to Höegh LNG common units and all of our subordinated units, representing an aggregate % limited partner interest in us, and all of our incentive distribution rights, which will entitle Höegh LNG to increasing percentages of the cash we distribute in excess of $ per unit per quarter; |

| • | we will issue to Höegh LNG GP LLC, a wholly owned subsidiary of Höegh LNG, a non-economic general partner interest in us; |

| • | we will sell common units to the public in this offering, representing a % limited partner interest in us; and |

| • | we will apply the net proceeds of the offering as follows: (i) up to $140 million to make a loan to Höegh LNG in exchange for a note bearing interest at a rate of 5.88% per annum, which is repayable on demand or which we can elect to utilize as part of the purchase consideration in the event we purchase all or a portion of Höegh LNG’s interests in the Independence, (ii) $20 million for general partnership purposes and (iii) the remainder to make a cash distribution to Höegh LNG. |

In addition, at or prior to the closing of this offering:

| • | the shareholder loans made by Höegh LNG to each of our joint ventures, in part to finance the operations of such joint ventures, will be transferred to our operating company. As of March 31, 2014, our 50.0% share of the outstanding balance of the shareholder loans was $22.9 million. For a description of the shareholder loans, please read “Management’s Discussion and Analysis of Financial Condition and Results of Operation—Liquidity and Capital Resources—Borrowing Activities—Loans and Promissory Notes Due to Owners and Affiliates” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Borrowing Activities—Joint Ventures Debt—Loans Due to Owners (Shareholder Loans).” |

| • | the receivable for the $40 million promissory note due to Höegh LNG relating to Höegh Lampung will be transferred from Höegh LNG to our operating company. As of March 31, 2014, the outstanding balance including interest was $40.7 million. |

| • | we will enter into a new $85 million revolving credit facility with Höegh LNG, which we refer to as the sponsor credit facility and which will be undrawn at the closing of this offering; |

| • | we will enter into an omnibus agreement with Höegh LNG, our general partner, and our operating company governing, among other things: |

| • | to what extent we and Höegh LNG may compete with each other; |

| • | our right to purchase from Höegh LNG all or a portion of its interests in an additional newbuilding FSRU, the Independence, within 24 months after acceptance of such vessel by her charterer, subject to reaching an agreement with Höegh LNG regarding the purchase price and other terms in accordance with the provisions of the omnibus agreement and any rights ABKN has under the related time charter, which option we may exercise at one or more times during such 24-month period; |

7

Table of Contents

| • | certain rights of first offer on FSRUs and LNG carriers operating under charters of five or more years as described under “Certain Relationships and Related Party Transactions—Agreements Governing the Transactions—Omnibus Agreement;” and |

| • | Höegh LNG’s provision of certain indemnities to us; |

| • | we and our operating company will enter into an administrative services agreement with Höegh UK, pursuant to which Höegh UK will agree to provide us and our operating company certain administrative services (the “Höegh UK Administrative Services Agreement”); |

| • | Höegh UK will enter into an administrative services agreement with Höegh Norway, pursuant to which Höegh Norway will agree to provide Höegh UK certain administrative services (the “Höegh Norway Administrative Services Agreement,” and together with the Höegh UK Administrative Services Agreement, the “Administrative Services Agreements”); |

| • | our joint ventures will remain parties to ship management agreements with Höegh LNG Management pursuant to which Höegh LNG Management provides our joint ventures with technical and maritime management and crewing of the GDF Suez Neptune and the GDF Suez Cape Ann, and Höegh Norway will remain party to a sub-technical support agreement with Höegh LNG Management pursuant to which Höegh LNG Management provides technical support services with respect to the PGN FSRU Lampung; and |

| • | our joint ventures will remain parties to commercial and administration management agreements with Höegh Norway, and the owner of the PGN FSRU Lampung will remain party to a technical information and services agreement with Höegh Norway. |

For further details on our agreements with Höegh LNG and its affiliates, including amounts involved, please read “Certain Relationships and Related Party Transactions.”

We are a holding entity and will conduct our operations and business through subsidiaries, as is common with publicly traded limited partnerships, to maximize operational flexibility. We believe that conducting our operations through a publicly traded limited partnership will offer us the following advantages:

| • | access to the public equity and debt capital markets; |

| • | a lower cost of capital for expansion and acquisitions; and |

| • | an enhanced ability to use equity securities as consideration in future acquisitions. |

8

Table of Contents

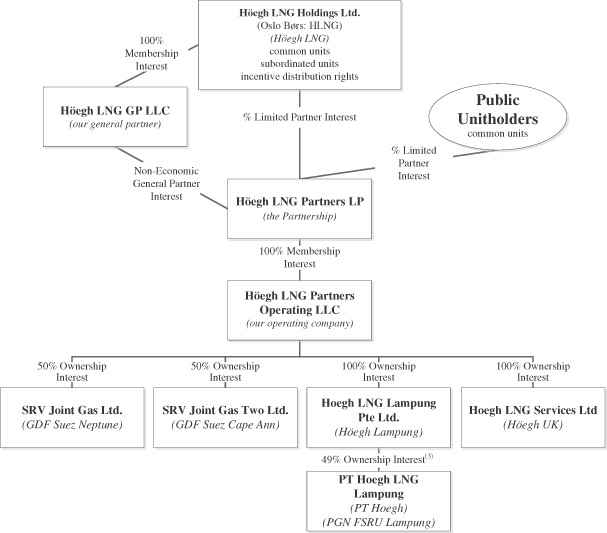

Simplified Organizational and Ownership Structure after This Offering

The following diagram depicts our simplified organizational and ownership structure after giving effect to the offering and related transactions described above, assuming no exercise of the underwriters’ option to purchase additional common units:

| Number of Units | Percentage Ownership | |||||

| Public Common Units(1)(2) |

% | |||||

| Höegh LNG Common Units(1) |

||||||

| Höegh LNG Subordinated Units |

||||||

|

|

|

|

||||

| 100.0 | % | |||||

|

|

|

|

||||

| (1) | If the underwriters exercise any part of their option to purchase additional common units, the number of common units shown to be owned by Höegh LNG will be reduced by the number of common units purchased in connection with any such exercise and will be sold to the public instead of being issued to |

9

Table of Contents

| Höegh LNG. Any such common units issued to Höegh LNG will be issued for no additional consideration. The exercise of the underwriters’ option will not affect the total number of units outstanding. If the underwriters’ option is exercised in full, then Höegh LNG would own % of the common units, and the public would own % of the common units. |

| (2) | Includes up to common units that may be purchased by certain of our directors, officers, employees and related persons pursuant to a directed unit program, as described in more detail in “Underwriting.” |

| (3) | Represents a 100% economic interest. Please read “Certain Relationships and Related Party Transactions—Agreements Governing the Transactions—PGN FSRU Lampung Agreements.” |

Our partnership agreement provides that our general partner will irrevocably delegate to our board of directors the authority to oversee and direct our operations, management and policies on an exclusive basis. Certain of our directors will also serve as directors of Höegh LNG or its affiliates. Our Chief Executive Officer and Chief Financial Officer, whose primary responsibility will be to our business, will be employed by one of our subsidiaries. Immediately prior to such employment, he was employed by a subsidiary of Höegh LNG, with his primary responsibility being preparation for this offering. In the future, he will work with Höegh LNG to develop opportunities for us. For example, our Chief Executive Officer and Chief Financial Officer may work to charter new vessels for Höegh LNG, which, pursuant to the omnibus agreement, we may have a right to purchase. For more information about these directors and officers, please read “Management—Directors and Executive Officers.”

Our wholly owned subsidiary, Höegh UK, will provide certain administrative services to us. Höegh UK will enter into the Höegh Norway Administrative Services Agreement, pursuant to which Höegh Norway, which is wholly owned by Höegh LNG, will agree to provide Höegh UK certain administrative services. Höegh UK will reimburse Höegh Norway for its reasonable costs and expenses incurred in connection with the provision of these services. We project that Höegh UK will reimburse Höegh Norway approximately $1.0 million in total under such administrative services agreement for the 12-month period ending September 30, 2015.

Our joint ventures are parties to ship management agreements with Höegh LNG Management, which is wholly owned by Höegh LNG, pursuant to which Höegh LNG Management provides technical and maritime management and crewing of the vessels. Furthermore, Höegh Norway is party to a sub-technical support agreement with Höegh LNG Management pursuant to which Höegh LNG Management provides technical support services with respect to the PGN FSRU Lampung. Pursuant to the ship management agreements and the sub-technical support agreement, our joint ventures and Höegh Norway, respectively, pay Höegh LNG Management fees for providing these services.

Our joint ventures are parties to commercial and administration management agreements with Höegh Norway pursuant to which Höegh Norway provides commercial and administrative services. The owner of the PGN FSRU Lampung is party to a technical information and services agreement with Höegh Norway, a master spare parts supply agreement with Höegh Asia and a master maintenance agreement with Höegh Shipping, pursuant to which Höegh Norway provides commercial, administration and support services.

Each of our joint ventures pays Höegh Norway an annual management fee equal to costs incurred plus 3% pursuant to their respective commercial and administration management agreement. In addition, each month, PT Hoegh pays Höegh Norway a fee for the provision of the technical information, including the intellectual property rights, and the services. The monthly fee includes a service fee, which consists of a pro rata payment of the estimated annual costs incurred by Höegh Norway under the technical information and services agreement plus a 5.0% fee on such payment, and a licensing fee. In addition, Höegh LNG Management is paid an annual management fee of approximately $672,000, $672,000 and $600,000 under the ship management agreements or sub-technical support agreement with each of SRV Joint Gas Ltd., SRV Joint Gas Two Ltd. and Höegh Norway,

10

Table of Contents

respectively. Pursuant to the master spare parts supply agreement, PT Hoegh will pay Höegh Asia for the actual cost of any supplied services plus a 5.0% fee on the cost of such supplied services. Pursuant to the master maintenance agreement, PT Hoegh will pay Höegh Shipping for the actual costs of any supplied services plus a 5.0% fee on the cost of such supplied services.

For a more detailed description of these agreements, please read “Certain Relationships and Related Party Transactions—Agreements Governing the Transactions—Joint Venture Commercial and Administration Management Agreements,” “Certain Relationships and Related Party Transactions—Agreements Governing the Transactions—PGN FSRU Lampung Agreements” and “Certain Relationships and Related Party Transactions—Agreements Governing the Transactions—Ship Management Agreements and Sub-Technical Agreement.”

Principal Executive Offices and Internet Address; SEC Filing Requirements

Our registered and principal executive offices are located at 2 Reid Street, Hamilton, HM 11, Bermuda, and our phone number is +1 (441) 295-6815. We expect to make our periodic reports and other information filed with or furnished to the United States Securities and Exchange Commission (the “SEC”) available, free of charge, through our website at www.hoeghlngpartners.com, which will be operational after this offering, as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. Please read “Where You Can Find More Information” for an explanation of our reporting requirements as a foreign private issuer.

Summary of Conflicts of Interest and Fiduciary Duties

Our general partner and our directors will have a legal duty to manage us in a manner beneficial to our unitholders, subject to the limitations described under “Conflicts of Interest and Fiduciary Duties.” This legal duty is commonly referred to as a “fiduciary duty.” Our directors also will have fiduciary duties to manage us in a manner beneficial to us, our general partner and our limited partners. As a result of these relationships, conflicts of interest may arise between us and our unaffiliated limited partners on the one hand, and Höegh LNG and its affiliates, including our general partner, on the other hand. The resolution of these conflicts may not be in the best interest of us or our unitholders. In particular:

| • | certain of our directors will also serve as directors or executive officers of Höegh LNG or its affiliates and as such will have fiduciary duties to Höegh LNG or its affiliates that may cause them to pursue business strategies that disproportionately benefit Höegh LNG or its affiliates or which otherwise are not in the best interests of us or our unitholders; |

| • | our partnership agreement permits our general partner to make a number of decisions in its individual capacity, as opposed to in its capacity as our general partner, which entitles our general partner to consider only the interests and factors that it desires, and it has no duty or obligations to give any consideration to any interest of or factors affecting us, our affiliates or any unitholder; when acting in its individual capacity, our general partner may act without any fiduciary obligation to us or the unitholders whatsoever; |

| • | Höegh LNG and its affiliates may compete with us, subject to the restrictions contained in the omnibus agreement, and could own and operate FSRUs and LNG carriers under charters of five or more years that may compete with our vessels if we do not purchase such vessels from Höegh LNG; |

| • | any agreement between us, on the one hand, and our general partner and its affiliates, on the other, will not grant to the unitholders, separate and apart from us, the right to enforce the obligations of our general partner and its affiliates in our favor; |

| • | borrowings by us and our affiliates will not constitute a breach of any duty owed by our general partner or our directors to our unitholders, including borrowings that have the purpose or effect of: (i) enabling our general partner or its affiliates to receive distributions on any subordinated units held by them or the incentive distribution rights or (ii) hastening the expiration of the subordination period; |

11

Table of Contents

| • | the holder or holders of our incentive distribution rights, which initially will be Höegh LNG, will have the right to reset the minimum quarterly distribution and the cash target distribution levels upon which the incentive distributions payable to such holder or holders are based without the approval of unitholders or the conflicts committee of our board of directors at any time when there are no subordinated units outstanding and we have made cash distributions to the holders of the incentive distribution rights at the highest level of incentive distribution for each of the prior four consecutive fiscal quarters; in connection with such resetting and the corresponding relinquishment by such holder or holders of incentive distribution payments based on the cash target distribution levels prior to the reset, such holder or holders will be entitled to receive a number of newly issued common units based on a predetermined formula described under “How We Make Cash Distributions—Höegh LNG’s Right to Reset Incentive Distribution Levels”; and |

| • | in connection with the offering, we will enter into agreements, and may enter into additional agreements, with Höegh LNG and certain of its subsidiaries, relating to the purchase of additional vessels, the provision of certain services to us by Höegh LNG and its affiliates and other matters. In the performance of their obligations under these agreements, Höegh LNG and its subsidiaries, other than our general partner, are not held to a fiduciary duty standard of care to us, our general partner or our limited partners, but rather to the standard of care specified in these agreements. |

For a more detailed description of our management structure, please read “Management—Directors and Executive Officers” and “Certain Relationships and Related Party Transactions.”

Although a majority of our directors will be elected by our common unitholders at our 2014 annual meeting, our general partner will have influence on decisions made by our board of directors. Our board of directors will have a conflicts committee composed solely of independent directors. Our board of directors may, but is not obligated to, seek approval of the conflicts committee for resolutions of conflicts of interest that may arise as a result of the relationships between Höegh LNG and its affiliates, on the one hand, and us and our unaffiliated limited partners, on the other. There can be no assurance that a conflict of interest will be resolved in favor of the Partnership.

For a more detailed description of the conflicts of interest and fiduciary duties of our general partner and its affiliates, please read “Conflicts of Interest and Fiduciary Duties.” For a description of our other relationships with our affiliates, please read “Certain Relationships and Related Party Transactions.”

In addition, our partnership agreement contains provisions that reduce the standards to which our general partner and our directors would otherwise be held under Marshall Islands law. For example, our partnership agreement limits the liability and reduces the fiduciary duties of our general partner and our directors to our unitholders. Our partnership agreement also restricts the remedies available to unitholders. By purchasing a common unit, you are treated as having agreed to the modified standard of fiduciary duties and to certain actions that may be taken by our general partner, its affiliates or our directors, all as set forth in our partnership agreement. Please read “Conflicts of Interest and Fiduciary Duties” for a description of the fiduciary duties that would otherwise be imposed on our general partner, its affiliates and our directors under Marshall Islands law, the material modifications of those duties contained in our partnership agreement and certain legal rights and remedies available to our unitholders under Marshall Islands law.

12

Table of Contents

| Common units offered to the public |

common units. |

| common units if the underwriters exercise in full their option to purchase additional common units. |

| Units outstanding after this offering |

common units and subordinated units, representing a % and % limited partner interest in us, respectively. If the underwriters do not exercise their option to purchase additional common units, we will issue common units to Höegh LNG upon the option’s expiration for no additional consideration. Accordingly, the exercise of the underwriters’ option will not affect the total number of common units outstanding. In addition, our general partner will own a non-economic general partner interest in us. |

| Use of proceeds |

We intend to use the net proceeds from this offering (approximately $ million, after deducting the underwriting discounts, structuring fees and estimated offering expenses payable by us) as follows: (i) up to $140 million to make a loan to Höegh LNG in exchange for a note bearing interest at a rate of 5.88% per annum, which is repayable on demand or which we can elect to utilize as part of the purchase consideration in the event we purchase all or a portion of Höegh LNG’s interests in the Independence, (ii) $20 million for general partnership purposes and (iii) the remainder to make a cash distribution to Höegh LNG. |

| The net proceeds from any exercise of the underwriters’ option to purchase additional common units (approximately $ million, if exercised in full, after deducting the underwriting discounts, structuring fees and estimated offering expenses payable by us) will be used to make an additional cash distribution to Höegh LNG. |

| Cash distributions |

We intend to make minimum quarterly distributions of $ per unit ($ per unit on an annualized basis) to the extent we have sufficient cash from operations after establishment of cash reserves and payment of fees and expenses, including payments to our general partner. In general, we will pay any cash distributions we make each quarter in the following manner: |

| • | first, 100.0% to the holders of common units, until each common unit has received a minimum quarterly distribution of $ plus any arrearages from prior quarters; |

| • | second, 100.0% to the holders of subordinated units, until each subordinated unit has received a minimum quarterly distribution of $ ; and |

| • | third, 100.0% to all unitholders, until each unit has received an aggregate distribution of $ . |

13

Table of Contents

| Within 45 days after the end of each fiscal quarter (beginning with the quarter ending , 2014), we will distribute all of our available cash to unitholders of record on the applicable record date. We will adjust the minimum quarterly distribution for the period from the closing of the offering through , 2014 based on the actual length of the period. Our ability to pay our minimum quarterly distribution is subject to various restrictions and other factors described in more detail under the caption “Our Cash Distribution Policy and Restrictions on Distributions.” |

| If cash distributions to our unitholders exceed $ per unit in a quarter, holders of our incentive distribution rights (initially, Höegh LNG) will receive increasing percentages, up to 50.0%, of the cash we distribute in excess of that amount. We refer to these distributions as “incentive distributions.” We must distribute all of our cash on hand at the end of each quarter, less reserves established by our board of directors to provide for the proper conduct of our business, to comply with any applicable debt instruments or to provide funds for future distributions. We refer to this cash as “available cash,” and we define its meaning in our partnership agreement. The amount of available cash may be greater than or less than the aggregate amount of the minimum quarterly distribution to be distributed on all units. |

| We believe, based on the estimates contained in and the assumptions listed under “Our Cash Distribution Policy and Restrictions on Distributions—Forecasted Cash Available for Distribution,” that we will have sufficient cash available for distribution to enable us to pay the minimum quarterly distribution of $ on all of our common and subordinated units for each quarter through September 30, 2015. However, we do not have a legal obligation to pay quarterly distributions at our minimum quarterly distribution rate or at any other rate. There is no guarantee that we will distribute quarterly cash distributions to our unitholders in any quarter. Unanticipated events may occur that could adversely affect the actual results we achieve during the forecast period. Consequently, our actual results of operations, cash flows and financial condition during the forecast period may vary from the forecast, and such variations may be material. Prospective investors are cautioned to not place undue reliance on the forecast and should make their own independent assessment of our future results of operations, cash flows and financial condition. |

| Please read “Our Cash Distribution Policy and Restrictions on Distributions—Forecasted Cash Available for Distribution.” |

| Subordinated units |

Höegh LNG will initially own all of our subordinated units. The principal difference between our common units and subordinated units is that in any quarter during the subordination period the subordinated units are entitled to receive the minimum quarterly distribution of $ per unit only after the common units have |

14

Table of Contents

| received the minimum quarterly distribution and arrearages in the payment of the minimum quarterly distribution from prior quarters. Subordinated units will not accrue arrearages. The subordination period generally will end if we have earned and paid at least $ on each outstanding common and subordinated unit for any three consecutive four-quarter periods ending on or after June 30, 2019. |

| For purposes of determining whether the subordination period will end, the three consecutive four-quarter periods for which the determination is being made may include one or more quarters with respect to which arrearages in the payment of the minimum quarterly distribution on the common units have accrued, provided that all such arrearages have been repaid prior to the end of each such four-quarter period. |

| The subordination period will also end upon the removal of our general partner other than for cause if units held by our general partner and its affiliates are not voted in favor of such removal. |

| When the subordination period ends, all subordinated units will convert into common units on a one-for-one basis, the common units will no longer be entitled to arrearages and the converted units will then participate pro rata with the other common units in distributions of available cash. |

| Please read “How We Make Cash Distributions—Subordination Period.” |

| Höegh LNG’s right to reset the target distribution levels |

Höegh LNG, as the initial holder of all of our incentive distribution rights, has the right, at a time when there are no subordinated units outstanding and it has received incentive distributions at the highest level to which it is entitled (50.0%) for each of the prior four consecutive fiscal quarters, to reset the initial cash target distribution levels at higher levels based on the distribution at the time of the exercise of the reset election. If Höegh LNG transfers all or a portion of the incentive distribution rights it holds in the future, then the holder or holders of a majority of our incentive distribution rights will be entitled to exercise this right. Following a reset election by Höegh LNG, the minimum quarterly distribution amount will be reset to an amount equal to the average cash distribution per common unit for the two fiscal quarters immediately preceding the reset election (we refer to such amount as the “reset minimum quarterly distribution amount”), and the target distribution levels will be reset to correspondingly higher levels based on the same percentage increases above the reset minimum quarterly distribution amount as our current target distribution levels. |

| In connection with resetting these target distribution levels, Höegh LNG will be entitled to receive a number of common units equal to |

15

Table of Contents

| that number of common units whose aggregate quarterly cash distributions equaled the average of the distributions to it on the incentive distribution rights in the prior two quarters. For a more detailed description of Höegh LNG’s right to reset the target distribution levels upon which the incentive distribution payments are based and the concurrent right of Höegh LNG to receive common units in connection with this reset, please read “How We Make Cash Distributions—Höegh LNG’s Right to Reset Incentive Distribution Levels.” |

| Issuance of additional units |

Our partnership agreement authorizes us to issue an unlimited number of additional units, including units that are senior to the common units in rights of distribution, liquidation and voting, on the terms and conditions determined by our board of directors, without the consent of our unitholders. Please read “Units Eligible for Future Sale” and “Our Partnership Agreement—Issuance of Additional Interests.” |

| Board of directors |

We will hold a meeting of the limited partners every year to elect one or more members of our board of directors and to vote on any other matters that are properly brought before the meeting. Our general partner has the right to appoint three of the seven members of our board of directors who will serve as directors for terms determined by our general partner. At our 2014 annual meeting, the common unitholders will elect four of our directors. The four directors elected by our common unitholders at our 2014 annual meeting will be divided into four classes to be elected by our common unitholders annually on a staggered basis to serve for four-year terms. The majority of our directors will be non-United States citizens or residents. |

| Limited voting rights |

Except as otherwise described herein, each outstanding common unit is entitled to one vote on matters subject to a vote of common unitholders. However, to preserve our ability to claim an exemption from U.S. federal income tax under Section 883 of the U.S. Internal Revenue Code of 1986, as amended (the “Code”), if at any time, any person or group owns beneficially more than 4.9% of any class of units then outstanding, any such units owned by that person or group in excess of 4.9% may not be voted on any matter and will not be considered to be outstanding when sending notices of a meeting of unitholders, calculating required votes (except for purposes of nominating a person for election to our board of directors), determining the presence of a quorum or for other similar purposes under our partnership agreement, unless otherwise required by law. The voting rights of any such unitholders in excess of 4.9% will effectively be redistributed pro rata among the other common unitholders holding less than 4.9% of the voting power of all classes of units entitled to vote. Our general partner, its affiliates and persons who acquired common units with the prior approval of our board of directors will not be subject to this 4.9% limitation except with respect to voting their common units in the election of the elected directors. |

16

Table of Contents

| You will have no right to elect our general partner on an annual or other continuing basis. Our general partner may not be removed except by a vote of the holders of at least 75% of the outstanding units, including any units owned by our general partner and its affiliates, voting together as a single class. Upon consummation of this offering, Höegh LNG will own approximately % of our common units and all of our subordinated units, representing an aggregate % limited partner interest in us. If the underwriters’ option to purchase additional common units is exercised in full, Höegh LNG will own approximately % of our common units and will own all of our subordinated units, representing an aggregate % limited partner interest in us. As a result, you will initially be unable to remove our general partner without its or Höegh LNG’s consent, because Höegh LNG will own sufficient units upon completion of this offering to be able to prevent the general partner’s removal. Please read “Our Partnership Agreement—Voting Rights.” |

| Limited call right |

If at any time our general partner and its affiliates own more than 80.0% of the outstanding common units, our general partner has the right, but not the obligation, to purchase all, but not less than all, of the remaining common units at a price equal to the greater of (x) the average of the daily closing prices of the common units over the 20 trading days preceding the date three days before the notice of exercise of the call right is first mailed and (y) the highest price paid by our general partner or any of its affiliates for common units during the 90-day period preceding the date such notice is first mailed. Our general partner is not obligated to obtain a fairness opinion regarding the value of the common units to be repurchased by it upon the exercise of this limited call right. Please read “Our Partnership Agreement—Limited Call Right.” |

| U.S. federal income tax considerations |

Although we are organized as a limited partnership, we have elected to be treated as a corporation solely for U.S. federal income tax purposes. Consequently, all or a portion of the distributions you receive from us will constitute dividends for such purposes. The remaining portion of such distributions will be treated first as a non-taxable return of capital to the extent of your tax basis in your common units and, thereafter, as capital gain. We estimate that if you hold the common units that you purchase in this offering through the period ending December 31, 2016, the distributions you receive, on a cumulative basis, that will constitute dividends for U.S. federal income tax purposes will be approximately % of the total cash distributions you receive during that period. Please read “Material U.S. Federal Income Tax Considerations—U.S. Federal Income Taxation of U.S. Holders—Ratio of Dividend Income to Distributions” for the basis of this estimate. Please also read “Material U.S. Federal Income Tax Considerations—U.S. Federal Income Taxation of U.S. Holders—U.S. Federal Taxation of Distributions” for a discussion relating to the taxation of dividends. |

17

Table of Contents

| For a discussion of other material U.S. federal income tax consequences that may be relevant to prospective unitholders, please read “Material U.S. Federal Income Tax Considerations.” |

| Non-U.S. tax considerations |

For a discussion of material non-United States income tax considerations that may be relevant to prospective unitholders, please read “Non-United States Tax Consequences.” Please also read “Risk Factors— Tax Risks” for a discussion of the risk that unitholders may be attributed the activities we undertake in various jurisdictions for taxation purposes. |

| Exchange listing |

We have applied to list our common units on the New York Stock Exchange, under the symbol “HMLP.” |

18

Table of Contents

Summary Historical Financial and Operating Data

The following table presents summary historical financial and operating data of (i) Höegh Lampung, (ii) PT Hoegh (the owner of the PGN FSRU Lampung and the tower yoke mooring system (the “Mooring”)), (iii) interests in SRV Joint Gas Ltd. (the joint venture owning the GDF Suez Neptune) and (iv) interests in SRV Joint Gas Two Ltd. (the joint venture owning the GDF Suez Cape Ann). The transfer of the entities and the joint venture interests will be recorded at Höegh LNG’s consolidated book values. Höegh Lampung and PT Hoegh and our 50% interests in SRV Joint Gas Ltd. and SRV Joint Gas Two Ltd. are, collectively, referred to herein as our predecessor. Two of the vessels in our initial fleet (the GDF Suez Neptune and the GDF Suez Cape Ann) are owned by our joint ventures, each of which is owned 50% by us. Under applicable accounting rules, we do not consolidate the financial results of these two joint ventures into our predecessor’s financial results. Our predecessor accounts for its 50% equity interests in these two joint ventures as equity method investments in its combined carve-out financial statements. We derive cash flows from the operations of these two joint ventures from principal and interest payments on our shareholder loans to our joint ventures.

We have two segments, which are the “Majority Held FSRUs” and the “Joint Venture FSRUs.” As of March 31, 2014 and December 31, 2013 and 2012, Majority Held FSRUs included the PGN FSRU Lampung and construction contract revenue and expenses of the Mooring under construction. The Mooring will be sold to the charterer of the PGN FSRU Lampung. As of March 31, 2014 and December 31, 2013 and 2012, Joint Venture FSRUs included two 50%-owned FSRUs, the GDF Suez Neptune and the GDF Suez Cape Ann. We measure our segment profit based on segment EBITDA. Segment EBITDA is reconciled to operating income and net income for each segment in the segment table below. The accounting policies applied to the segments are the same as those applied in the historical combined carve-out financial statements, except that Joint Venture FSRUs are presented under the proportional consolidation method for the segment reporting and under the equity method in our predecessor’s historical combined carve-out financial statements. Under the proportional consolidation method, 50% of the Joint Venture FSRUs’ revenues, expenses and assets are reflected in the segment reporting. Management monitors the results of operations of our joint ventures under the proportional consolidation method and not the equity method.

You should read the following summary financial and operating data in conjunction with “Presentation of Financial Information,” “Selected Historical Financial and Operating Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operation,” as well as the historical combined carve-out financial statements of our predecessor, the historical combined financial statements of the two joint ventures that own the GDF Suez Neptune and the GDF Suez Cape Ann and the related notes thereto included elsewhere in this prospectus. The financial information included in this prospectus may not be indicative of our future results of operations, financial condition and cash flows.