UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q |

ý | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2018

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 1-36313

TIMKENSTEEL CORPORATION (Exact name of registrant as specified in its charter) |

Ohio | 46-4024951 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

1835 Dueber Avenue SW, Canton, OH | 44706 | |

(Address of principal executive offices) | (Zip Code) | |

330.471.7000

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act

Large accelerated filer | ý | Accelerated filer | o | |||

Non-accelerated filer | o | (Do not check if smaller reporting company) | Smaller reporting company | o | ||

Emerging growth company | o | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial reporting accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ý

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

Class | Outstanding at July 16, 2018 | |||

Common Shares, without par value | 44,584,668 | |||

TimkenSteel Corporation

Table of Contents

PAGE | ||

2

PART I. FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENT

TimkenSteel Corporation

Consolidated Statements of Operations (Unaudited)

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||

(Dollars in millions, except per share data) | |||||||||||||

Net sales | $413.5 | $339.3 | $794.3 | $648.7 | |||||||||

Cost of products sold | 381.4 | 315.5 | 741.1 | 607.9 | |||||||||

Gross Profit | 32.1 | 23.8 | 53.2 | 40.8 | |||||||||

Selling, general and administrative expenses | 24.9 | 22.3 | 49.6 | 45.2 | |||||||||

Impairment charges and loss on sale or disposal of assets | 0.9 | — | 0.9 | — | |||||||||

Operating Income (Loss) | 6.3 | 1.5 | 2.7 | (4.4 | ) | ||||||||

Interest expense | 3.9 | 3.7 | 8.5 | 7.3 | |||||||||

Other income, net | 6.2 | 4.3 | 12.6 | 8.8 | |||||||||

Income (Loss) Before Income Taxes | 8.6 | 2.1 | 6.8 | (2.9 | ) | ||||||||

Provision for income taxes | 0.2 | 0.8 | 0.3 | 1.1 | |||||||||

Net Income (Loss) | $8.4 | $1.3 | $6.5 | ($4.0 | ) | ||||||||

Per Share Data: | |||||||||||||

Basic earnings (loss) per share | $0.19 | $0.03 | $0.15 | ($0.09 | ) | ||||||||

Diluted earnings (loss) per share | $0.19 | $0.03 | $0.14 | ($0.09 | ) | ||||||||

Dividends per share | $— | $— | $— | $— | |||||||||

See accompanying Notes to Unaudited Consolidated Financial Statements.

3

TimkenSteel Corporation

Consolidated Statements of Comprehensive Loss (Unaudited)

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||

2018 | 2017 | 2018 | 2017 | |||||||||||

(Dollars in millions) | ||||||||||||||

Net Income (Loss) | $8.4 | $1.3 | $6.5 | ($4.0 | ) | |||||||||

Other comprehensive income, net of tax: | ||||||||||||||

Foreign currency translation adjustments | (1.2 | ) | 0.6 | (0.4 | ) | 0.8 | ||||||||

Pension and postretirement liability adjustments | 0.2 | — | 0.3 | 0.3 | ||||||||||

Other comprehensive income (loss), net of tax | (1.0 | ) | 0.6 | (0.1 | ) | 1.1 | ||||||||

Comprehensive Income (Loss), net of tax | $7.4 | $1.9 | $6.4 | ($2.9 | ) | |||||||||

See accompanying Notes to Unaudited Consolidated Financial Statements.

4

TimkenSteel Corporation

Consolidated Balance Sheets (Unaudited)

June 30, 2018 | December 31, 2017 | ||||||

(Dollars in millions) | |||||||

ASSETS | |||||||

Current Assets | |||||||

Cash and cash equivalents | $39.0 | $24.5 | |||||

Accounts receivable, net of allowances (2018 - $1.8 million; 2017 - $1.4 million) | 173.6 | 149.8 | |||||

Inventories, net | 294.5 | 224.0 | |||||

Deferred charges and prepaid expenses | 2.3 | 3.9 | |||||

Other current assets | 10.9 | 8.0 | |||||

Total Current Assets | 520.3 | 410.2 | |||||

Property, Plant and Equipment, Net | 679.8 | 706.7 | |||||

Other Assets | |||||||

Pension assets | 17.4 | 14.6 | |||||

Intangible assets, net | 17.5 | 19.9 | |||||

Other non-current assets | 5.0 | 5.2 | |||||

Total Other Assets | 39.9 | 39.7 | |||||

Total Assets | $1,240.0 | $1,156.6 | |||||

LIABILITIES AND SHAREHOLDERS’ EQUITY | |||||||

Current Liabilities | |||||||

Accounts payable, trade | $177.8 | $135.3 | |||||

Salaries, wages and benefits | 29.4 | 32.4 | |||||

Accrued pension and postretirement costs | 11.5 | 11.5 | |||||

Other current liabilities | 18.8 | 27.6 | |||||

Total Current Liabilities | 237.5 | 206.8 | |||||

Non-Current Liabilities | |||||||

Convertible notes, net | 72.0 | 70.1 | |||||

Other long-term debt | 150.0 | 95.2 | |||||

Accrued pension and postretirement costs | 197.7 | 210.8 | |||||

Deferred income taxes | — | 0.3 | |||||

Other non-current liabilities | 11.8 | 12.7 | |||||

Total Non-Current Liabilities | 431.5 | 389.1 | |||||

Shareholders’ Equity | |||||||

Preferred shares, without par value; authorized 10.0 million shares; none issued | — | — | |||||

Common shares, without par value; authorized 200.0 million shares; issued 2018 and 2017- 45.7 million shares | — | — | |||||

Additional paid-in capital | 842.7 | 843.7 | |||||

Retained deficit | (231.0 | ) | (238.0 | ) | |||

Treasury shares - 2018 - 1.1 million; 2017 - 1.3 million | (33.0 | ) | (37.4 | ) | |||

Accumulated other comprehensive loss | (7.7 | ) | (7.6 | ) | |||

Total Shareholders’ Equity | 571.0 | 560.7 | |||||

Total Liabilities and Shareholders’ Equity | $1,240.0 | $1,156.6 | |||||

See accompanying Notes to Unaudited Consolidated Financial Statements.

5

TimkenSteel Corporation

Consolidated Statements of Cash Flows (Unaudited)

Six Months Ended June 30, | |||||||

2018 | 2017 | ||||||

(Dollars in millions) | |||||||

CASH PROVIDED (USED) | |||||||

Operating Activities | |||||||

Net Income (Loss) | $6.5 | ($4.0 | ) | ||||

Adjustments to reconcile net loss to net cash provided by operating activities: | |||||||

Depreciation and amortization | 36.9 | 37.8 | |||||

Amortization of deferred financing fees and debt discount | 3.0 | 2.1 | |||||

Impairment charges and loss on sale or disposal of assets | 0.9 | 0.4 | |||||

Deferred income taxes | (0.3 | ) | 0.2 | ||||

Stock-based compensation expense | 3.7 | 3.4 | |||||

Pension and postretirement expense (benefit), net | (2.9 | ) | 1.6 | ||||

Pension and postretirement contributions and payments | (12.9 | ) | (2.7 | ) | |||

Changes in operating assets and liabilities: | |||||||

Accounts receivable, net | (23.8 | ) | (61.9 | ) | |||

Inventories, net | (70.5 | ) | (35.1 | ) | |||

Accounts payable, trade | 42.5 | 43.8 | |||||

Other accrued expenses | (12.9 | ) | 1.5 | ||||

Deferred charges and prepaid expenses | 1.6 | 1.0 | |||||

Other, net | (1.9 | ) | 0.3 | ||||

Net Cash Used by Operating Activities | (30.1 | ) | (11.6 | ) | |||

Investing Activities | |||||||

Capital expenditures | (9.0 | ) | (6.8 | ) | |||

Proceeds from disposals of property, plant and equipment | 1.0 | — | |||||

Net Cash Used by Investing Activities | (8.0 | ) | (6.8 | ) | |||

Financing Activities | |||||||

Proceeds from exercise of stock options | 0.2 | 0.2 | |||||

Shares surrendered for employee taxes on stock compensation | (0.7 | ) | (1.2 | ) | |||

Revenue Refunding Bonds repayments | (30.2 | ) | — | ||||

Credit Agreement repayments | (65.0 | ) | — | ||||

Amended Credit Agreement borrowings | 155.0 | 30.0 | |||||

Amended Credit Agreement repayments | (5.0 | ) | — | ||||

Debt issuance costs related to Amended Credit Agreement | (1.7 | ) | — | ||||

Net Cash Provided by Financing Activities | 52.6 | 29.0 | |||||

Increase In Cash and Cash Equivalents | 14.5 | 10.6 | |||||

Cash and cash equivalents at beginning of period | 24.5 | 25.6 | |||||

Cash and Cash Equivalents at End of Period | $39.0 | $36.2 | |||||

See accompanying Notes to Unaudited Consolidated Financial Statements.

6

TimkenSteel

Notes to Unaudited Consolidated Financial Statements

(dollars in millions, except per share data)

Note 1 - Company and Basis of Presentation

The accompanying Unaudited Consolidated Financial Statements have been prepared in accordance with generally accepted accounting principles in the United States (U.S. GAAP) for interim financial information. Accordingly, they do not include all of the information and footnotes required by U.S. GAAP for complete financial statements. In the opinion of management, all adjustments (consisting of normal recurring accruals) and disclosures considered necessary for a fair presentation have been included. For further information, refer to TimkenSteel’s Audited Consolidated Financial Statements and Notes included in its Annual Report on Form 10-K for the year ended December 31, 2017.

TimkenSteel Corporation (the Company or TimkenSteel) manufactures alloy steel, as well as carbon and micro-alloy steel, with an annual melt capacity of approximately 2 million tons and shipment capacity of 1.5 million tons. TimkenSteel’s portfolio includes special bar quality (SBQ) bars, seamless mechanical tubing (tubes), value-add solutions such as precision steel components, and billets. In addition, TimkenSteel manages machining, thermal treatment, and raw material recycling programs that are used as a feeder system for the Company’s melt operations. The Company’s products and services are used in a diverse range of demanding applications in the following market sectors: oil and gas; oil country tubular goods (OCTG); automotive; industrial equipment; mining; construction; rail; aerospace and defense; heavy truck; agriculture; and power generation.

The SBQ bars, tubes, and billets production processes take place at the Company’s Canton, Ohio manufacturing location. This location accounts for all of the SBQ bars, seamless mechanical tubes and billets the Company produces and includes three manufacturing facilities: the Faircrest, Harrison, and Gambrinus facilities. TimkenSteel’s value-add solutions production processes take place at three downstream manufacturing facilities: TimkenSteel Material Services (Houston, TX), Tryon Peak (Columbus, NC), and St. Clair (Eaton, OH). Many of the production processes are integrated, and the manufacturing facilities produce products that are sold in all of the Company’s market sectors. As a result, investments in the Company’s facilities and resource allocation decisions affecting the Company’s operations are designed to benefit the overall business of the Company, not any specific aspect of the business.

Note 2 - Recent Accounting Pronouncements

Adoption of New Accounting Standards

The Company adopted the following Accounting Standard Updates (ASU) in the first quarter of 2018, all of which were effective as of date January 1, 2018. The adoption of these standards did not have a material impact on the Unaudited Consolidated Financial Statements or the related Notes to the Unaudited Consolidated Financial Statements.

Standards Adopted | Description |

2014-09, Revenue from Contracts with Customers | The standard defines that a company will recognize revenue when it transfers control of goods or services to customers in an amount that reflects the consideration to which the company expects to be entitled in exchange for those goods or services. This standard also requires additional disclosures about the nature, amount, timing and uncertainty of revenues and cash flows from contracts with customers. |

2017-01, Clarifying the Definition of a Business | The standard clarifies the definition of a business when evaluating whether transactions should be accounted for as acquisitions, or disposals of assets or businesses. |

2017-09, Stock Compensation, Scope of Modification Accounting | The standard provides guidance intended to reduce diversity in practice when accounting for a modification to the terms and conditions of a share-based payment award. |

On January 1, 2018, TimkenSteel adopted the new revenue standard using the modified retrospective approach as applied to customer contracts that were not completed as of January 1, 2018. As a result, financial information for reporting periods beginning on or after January 1, 2018, are presented in accordance with the new revenue standard. Comparative financial information for reporting periods beginning prior to January 1, 2018, has not been adjusted and continues to be reported in accordance with the Company's revenue recognition policies prior to the adoption of the new revenue standard. The cumulative effect was an adjustment to the opening balance of retained earnings. Under the new revenue standard, the Company will continue

7

to recognize revenue at a point in time when it transfers promised goods or services to customers. Refer to Note 10 - Revenue Recognition in the Notes to Unaudited Consolidated Financial Statements for further discussion.

The following table outlines the cumulative effect of adopting the new revenue standard as of January 1, 2018.

Consolidated Balance Sheet caption | As of December 31, 2017 | ASU 2014-09 Adjustment | As of January 1, 2018 | |||||||||

Inventories, net | $224.0 | ($3.3 | ) | $220.7 | ||||||||

Other current liabilities | $27.6 | ($4.0 | ) | $23.6 | ||||||||

Retained deficit | ($238.0 | ) | $0.7 | ($237.3 | ) | |||||||

The ASU 2014-09 adoption adjustment is due to transactions in which the Company bills a customer for product but retains physical possession of the product until it is transferred to the customer at a point in time in the future. Prior to the adoption of the new revenue standard, TimkenSteel would recognize revenue when the product was physically transferred to the customer. Under the new revenue standard, the Company has satisfied its performance obligation and the customer obtains control when the goods are ready to be transferred to the customer and revenue is recorded at that time.

For the three and six months ended June 30, 2018, the adoption of the new revenue standard did not have a material impact on the Unaudited Consolidated Financial Statements.

Accounting Standards Issued But Not Yet Adopted

The Company has considered the recent ASUs issued by the FASB summarized below.

Standard Pending Adoption | Description | Effective Date | Anticipated Impact |

ASU 2018-07, Compensation - Stock Compensation (Topic 718): Improvements to Nonemployee Share-Based Payment Accounting | The standard provides an expanded scope of Topic 718, to include share-based payment transactions for acquiring goods and services from nonemployees. | January 1, 2019 | The Company is currently evaluating the impact of the adoption of this ASU on its results of operations and financial condition. |

ASU 2018-02, Reporting Comprehensive Income: Reclassification of Certain Tax Effects from Accumulated Other Comprehensive Income | The standard permits entities to reclassify tax effects stranded in accumulated other comprehensive income as a result of tax reform to retained earnings. | January 1, 2019 | The Company is currently evaluating the impact of the adoption of this ASU on its results of operations and financial condition. |

ASU 2018-01, Leases - Land Easement Practical Expedient for Transition to Topic 842 | The standard provides an optional transition practical expedient for land easements that allows an entity to continue applying its current accounting policy for certain land easements that exist or expire before the standard’s effective date. | January 1, 2019 | The Company is currently evaluating the impact of the adoption of this ASU on its results of operations and financial condition. |

ASU 2017-11, Distinguishing Liabilities from Equity; Derivatives and Hedging | The standard eliminates the requirement to consider “down round” features when determining whether certain equity-linked financial instruments or embedded features are indexed to an entity’s own stock. | January 1, 2019 | The Company is currently evaluating the impact of the adoption of this ASU on its results of operations and financial condition. |

ASU 2016-13, Measurement of Credit Losses on Financial Instruments | The standard changes how entities will measure credit losses for most financial assets, including trade and other receivables and replaces the current incurred loss approach with an expected loss model. | January 1, 2020 | The Company is currently evaluating the impact of the adoption of this ASU on its results of operations and financial condition. |

ASU 2016-02, Leases | The standard requires lessees to recognize lease liabilities and right-of-use assets on the balance sheet for operating leases, and requires additional quantitative and qualitative disclosures and must be adopted using a modified retrospective approach. | January 1, 2019 | The Company is currently reviewing its lease contracts, related systems and internal controls as it continues to evaluate the impact of the adoption of this ASU on its results of operations and financial condition. |

8

Note 3 - Inventories

The components of inventories, net as of June 30, 2018 and December 31, 2017 were as follows:

June 30, 2018 | December 31, 2017 | ||||||

Inventories: | |||||||

Manufacturing supplies | $40.3 | $36.3 | |||||

Raw materials | 45.8 | 31.9 | |||||

Work in process | 190.5 | 137.8 | |||||

Finished products | 90.1 | 82.9 | |||||

Gross inventory | 366.7 | 288.9 | |||||

Allowance for surplus and obsolete inventory | (7.5 | ) | (7.8 | ) | |||

LIFO reserve | (64.7 | ) | (57.1 | ) | |||

Total Inventories, net | $294.5 | $224.0 | |||||

Inventories are valued at the lower of cost or market, with approximately 65% valued by the LIFO method, and the remaining inventories, including manufacturing supplies inventory as well as international (outside the United States) inventories, valued by FIFO, average cost or specific identification methods.

An actual valuation of the inventory under the LIFO method can be made only at the end of each year based on the inventory levels and costs at that time. Accordingly, interim LIFO calculations must be based on management’s estimates of expected year-end inventory levels and costs. Because these calculations are subject to many factors beyond management’s control, annual results may differ from interim results as they are subject to the final year-end LIFO inventory valuation.

TimkenSteel projects that its LIFO reserve will increase for the year ending December 31, 2018, due primarily to higher anticipated scrap prices and inflation.

Note 4 - Property, Plant and Equipment

The components of property, plant and equipment, net as of June 30, 2018 and December 31, 2017, were as follows:

June 30, 2018 | December 31, 2017 | ||||||

Property, Plant and Equipment, net: | |||||||

Land | $13.4 | $13.4 | |||||

Buildings and improvements | 422.6 | 420.6 | |||||

Machinery and equipment | 1,403.0 | 1,387.4 | |||||

Construction in progress | 14.3 | 30.4 | |||||

Subtotal | 1,853.3 | 1,851.8 | |||||

Less allowances for depreciation | (1,173.5 | ) | (1,145.1 | ) | |||

Property, Plant and Equipment, net | $679.8 | $706.7 | |||||

Total depreciation expense was $34.0 million and $34.2 million for the six months ended June 30, 2018 and 2017, respectively. TimkenSteel recorded capitalized interest related to construction projects of $0.1 million and $0.3 million for the six months ended June 30, 2018 and 2017, respectively. During the six months ended June 30, 2018, TimkenSteel recorded approximately $0.5 million of impairment charges and loss on sale or disposals related to the discontinued use of certain assets.

9

Note 5 - Intangible Assets

The components of intangible assets, net as of June 30, 2018 and December 31, 2017 were as follows:

June 30, 2018 | December 31, 2017 | ||||||||||||||||||||||

Gross Carrying Amount | Accumulated Amortization | Net Carrying Amount | Gross Carrying Amount | Accumulated Amortization | Net Carrying Amount | ||||||||||||||||||

Intangible Assets Subject to Amortization: | |||||||||||||||||||||||

Customer relationships | $6.3 | $4.4 | $1.9 | $6.3 | $4.1 | $2.2 | |||||||||||||||||

Technology use | 9.0 | 6.1 | 2.9 | 9.0 | 5.9 | 3.1 | |||||||||||||||||

Capitalized software | 58.9 | 46.2 | 12.7 | 59.1 | 44.5 | 14.6 | |||||||||||||||||

Total Intangible Assets | $74.2 | $56.7 | $17.5 | $74.4 | $54.5 | $19.9 | |||||||||||||||||

Intangible assets subject to amortization are amortized on a straight-line method over their legal or estimated useful lives. Amortization expense for intangible assets for the six months ended June 30, 2018 and 2017 was $2.9 million and $3.6 million, respectively. During the six months ended June 30, 2018, TimkenSteel recorded approximately $0.4 million of impairment charges due to the discontinued use of certain capitalized software. There were no impairment charges recorded during the six months ended June 30, 2017.

Note 6 - Financing Arrangements

Convertible Notes

In May 2016, the Company issued $75.0 million aggregate principal amount of Convertible Senior Notes, and an additional $11.3 million principal amount to cover over-allotments (Convertible Notes). The Indenture for the Convertible Notes dated May 31, 2016, which was filed with the Securities and Exchange Commission as an exhibit to a Form 8-K filed on May 31, 2016, contains a complete description of the terms of the Convertible Notes. The key terms are as follows:

Maturity Date: June 1, 2021 unless repurchased or converted earlier

Interest Rate: 6.0% cash interest per year

Interest Payments Dates: June 1 and December 1 of each year, beginning on December 1, 2016

Initial Conversion Price: Approximately $12.58 per common share of the Company

Initial Conversion Rate: 79.5165 common shares per $1,000 principal amount of Notes

The net proceeds to the Company from the offering were $83.2 million, after deducting the initial underwriters’ discount and fees and the offering expenses payable by the Company. The Company used the net proceeds to repay a portion of the amounts outstanding under the Credit Agreement.

The components of the Convertible Notes as of June 30, 2018 and December 31, 2017 were as follows:

June 30, 2018 | December 31, 2017 | ||||||

Principal | $86.3 | $86.3 | |||||

Less: Debt issuance costs, net of amortization | (1.4 | ) | (1.6 | ) | |||

Less: Debt discount, net of amortization | (12.9 | ) | (14.6 | ) | |||

Convertible notes, net | $72.0 | $70.1 | |||||

The initial value of the principal amount recorded as a liability at the date of issuance was $66.9 million, using an effective interest rate of 12.0%. The remaining $19.4 million of principal amount was allocated to the conversion feature and recorded as a component of shareholders’ equity at the date of issuance. This amount represents a discount to the debt to be amortized through interest expense using the effective interest method through the maturity of the Convertible Notes.

10

Transaction costs were allocated to the liability and equity components based on their relative values. Transaction costs attributable to the liability component of $2.4 million are amortized to interest expense over the term of the Convertible Notes, and transaction costs attributable to the equity component of $0.7 million are included in shareholders’ equity.

The following table sets forth total interest expense recognized related to the Convertible Notes for the three and six months ended June 30, 2018 and 2017:

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||

2018 | 2017 | 2018 | 2017 | |||||||||

Contractual interest expense | $1.3 | $1.3 | $2.6 | $2.6 | ||||||||

Amortization of debt issuance costs | 0.1 | 0.1 | 0.2 | 0.2 | ||||||||

Amortization of debt discount | 0.8 | 0.8 | 1.7 | 1.6 | ||||||||

Total | $2.2 | $2.2 | $4.5 | $4.4 | ||||||||

The fair value of the Convertible Notes was approximately $157.0 million as of June 30, 2018. The fair value of the Convertible Notes, which falls within Level 1 of the fair value hierarchy, is based on the last price traded in June 2018.

Holders may convert all or any portion of their Convertible Notes, in multiples of $1,000 principal amount, at their option at any time prior to the close of business on the business day immediately preceding March 1, 2021 only under certain circumstances described in the Convertible Notes Indenture, based on the reported sale price of the Company’s common shares for specified trading days as a percentage of the conversion price of the Convertible Notes, and upon the occurrence of specified corporate events. On or after March 1, 2021 until the business day preceding the maturity date, holders may convert all or any portion of their Convertible Notes, in multiples of $1,000 principal amount, at their option.

Upon conversion, the Company will pay or deliver, as the case may be, cash, common shares or a combination of cash and common shares, at its election. If the Company satisfies its conversion obligation solely in cash or through payment and delivery, as the case may be, of a combination of cash and common shares, the amount of cash and number of common shares, if any, due upon conversion will be based on a daily conversion value calculated on a proportionate basis for each trading day in a 40-trading day period.

If the Company undergoes a fundamental change, subject to certain conditions, holders may require the Company to repurchase for cash all or part of their Convertible Notes at a repurchase price equal to 100% of the principal amount of the Convertible Notes to be repurchased, plus accrued and unpaid interest to the repurchase date.

Upon certain events of default occurring and continuing (including failure to pay principal or interest on the Convertible Notes when due and payable), the Trustee or the holders of at least 25% in principal amount may declare 100% of the principal and accrued and unpaid interest, if any, on all the Convertible Notes to be due and payable. In case of certain events of bankruptcy, insolvency or reorganization, involving the Company or a significant subsidiary, 100% of the principal and accrued and unpaid interest on the Convertible Notes will become due and payable immediately.

Other Long-Term Debt

The components of other long-term debt as of June 30, 2018 and December 31, 2017 were as follows:

June 30, 2018 | December 31, 2017 | ||||||

Variable-rate State of Ohio Water Development Revenue Refunding Bonds, maturing on November 1, 2025 (1.58% as of December 31, 2017) | $— | $12.2 | |||||

Variable-rate State of Ohio Air Quality Development Revenue Refunding Bonds, maturing on November 1, 2025 (1.60% as of December 31, 2017) | — | 9.5 | |||||

Variable-rate State of Ohio Pollution Control Revenue Refunding Bonds, maturing on June 1, 2033 (1.60% as of December 31, 2017) | — | 8.5 | |||||

Credit Agreement, due 2019 (LIBOR plus applicable spread) | — | 65.0 | |||||

Amended Credit Agreement, due 2023 (LIBOR plus applicable spread) | 150.0 | — | |||||

Total Other Long-Term Debt | $150.0 | $95.2 | |||||

Credit Agreement

11

On February 26, 2016, the Company, as a borrower, and certain domestic subsidiaries, as subsidiary guarantors, entered into the Amended and Restated Credit Agreement (the Credit Agreement), with JPMorgan Chase Bank, N.A., as administrative agent, and the other lenders party thereto. The Credit Agreement provided for a $265 million asset based revolving credit facility.

Amended Credit Agreement

On January 26, 2018, the Company as borrower, and certain domestic subsidiaries, as subsidiary guarantors, entered into the Second Amended and Restated Credit Agreement (Amended Credit Agreement), with JPMorgan Chase Bank, N.A., as administrative agent, Bank of America, N.A., as syndication agent, and the other lenders party thereto, which amended and restated the Company’s Credit Agreement.

The Amended Credit Agreement provides for a $300.0 million asset-based revolving credit facility, including a $15.0 million sublimit for the issuance of commercial and standby letters of credit and a $30.0 million sublimit for swingline loans. Pursuant to the terms of the Amended Credit Agreement, the Company is entitled, on up to two occasions and subject to the satisfaction of certain conditions, to request increases in the commitments under the Amended Credit Agreement in the aggregate principal amount of up to $50.0 million, to the extent that existing or new lenders agree to provide such additional commitments.

The availability of borrowings under the Amended Credit Agreement is subject to a borrowing base calculation based upon a valuation of the eligible accounts receivable, inventory and machinery and equipment of the Company and the subsidiary guarantors, each multiplied by an applicable advance rate. The availability of borrowings may be further modified by reserves established from time to time by the administrative agent in its permitted discretion.

The interest rate per annum applicable to loans under the Amended Credit Agreement will be, at the Company’s option, equal to either (i) the alternate base rate plus the applicable margin or (ii) the relevant adjusted LIBO rate for an interest period of one, two, three or six months (as selected by the Company) plus the applicable margin. The base rate will be a fluctuating rate per annum equal to the greatest of (i) the prime rate of the administrative agent, (ii) the effective Federal Reserve Bank of New York rate plus 0.50% and (iii) the adjusted LIBO rate for a one-month interest period on the applicable date, plus 1.00%. The adjusted LIBO rate will be equal to the applicable London interbank offered rate for the selected interest period, as adjusted for statutory reserve requirements for eurocurrency liabilities. The applicable margin will be determined by a pricing grid based on the Company’s average quarterly availability. In addition, the Company will pay a commitment fee on the average daily unused amount of the credit facility in a percentage determined by the Company’s average daily availability for the most recently completed calendar month. The interest rate under the Amended Credit Agreement was 4.0% as of June 30, 2018. The amount available under the Amended Credit Agreement as of June 30, 2018 was $147.4 million.

The proceeds of the Amended Credit Agreement will be used to finance working capital, capital expenditures, certain permitted acquisitions and other general corporate purposes. In addition, $30.2 million of the proceeds were used to redeem the revenue refunding bonds (discussed below). All of the indebtedness under the Amended Credit Agreement is guaranteed by the Company’s material domestic subsidiaries, as well as any other domestic subsidiary the Company elects to make a party to the Amended Credit Agreement, and is secured by substantially all of the personal property of the Company and the subsidiary guarantors.

The Amended Credit Agreement matures on January 26, 2023. Prior to the maturity date, amounts outstanding are required to be repaid (without reduction of the commitments thereunder) from mandatory prepayment events from the proceeds of certain asset sales, equity or debt issuances or casualty events.

The Amended Credit Agreement contains certain customary covenants, including covenants that limit the ability of the Company and its subsidiaries to, among other things, (i) incur or suffer to exist certain liens, (ii) make investments, (iii) incur or guaranty additional indebtedness, (iv) enter into consolidations, mergers, acquisitions, sale-leaseback transactions and sales of assets, (v) make distributions and other restricted payments, (vi) change the nature of its business, (vii) engage in transactions with affiliates and (viii) enter into restrictive agreements, including agreements that restrict the ability to incur liens or make distributions.

In addition, the Amended Credit Agreement requires the Company to (i) unless certain conditions are met, maintain certain minimum liquidity as specified in the Amended Credit Agreement during the period commencing on March 1, 2021 and ending on June 1, 2021 and (ii) maintain a minimum specified fixed charge coverage ratio on a springing basis if minimum availability requirements as specified in the Amended Credit Agreement are not maintained.

The Amended Credit Agreement contains certain customary events of default. If any event of default occurs and is continuing, the Lenders would be entitled to take various actions, including the acceleration of amounts due under the Amended Credit Agreement, and exercise other rights and remedies.

12

Revenue Refunding Bonds

In connection with entering into the Amended Credit Agreement, on January 23, 2018, the Company redeemed in full $12.2 million of Ohio Water Development Revenue Refunding Bonds (originally due on November 1, 2025), $9.5 million of Ohio Air Quality Development Revenue Refunding Bonds (originally due on November 1, 2025) and $8.5 million of Ohio Pollution Control Revenue Refunding Bonds (originally due on June 1, 2033).

Note 7 - Accumulated Other Comprehensive Loss

Changes in accumulated other comprehensive loss for the six months ended June 30, 2018 and 2017 by component are as follows:

Foreign Currency Translation Adjustments | Pension and Postretirement Liability Adjustments | Total | |||||||||

Balance at December 31, 2017 | ($5.9 | ) | ($1.7 | ) | ($7.6 | ) | |||||

Other comprehensive income before reclassifications, before income tax | (0.4 | ) | — | (0.4 | ) | ||||||

Amounts reclassified from accumulated other comprehensive loss, before income tax | — | 0.3 | 0.3 | ||||||||

Income tax | — | — | — | ||||||||

Net current period other comprehensive (loss) income, net of income taxes | (0.4 | ) | 0.3 | (0.1 | ) | ||||||

Balance at June 30, 2018 | ($6.3 | ) | ($1.4 | ) | ($7.7 | ) | |||||

Foreign Currency Translation Adjustments | Pension and Postretirement Liability Adjustments | Total | |||||||||

Balance at December 31, 2016 | ($7.0 | ) | ($2.4 | ) | ($9.4 | ) | |||||

Other comprehensive income before reclassifications, before income tax | 0.8 | — | 0.8 | ||||||||

Amounts reclassified from accumulated other comprehensive loss, before income tax | — | 0.8 | 0.8 | ||||||||

Income tax | — | (0.5 | ) | (0.5 | ) | ||||||

Net current period other comprehensive income, net of income taxes | 0.8 | 0.3 | 1.1 | ||||||||

Balance at June 30, 2017 | ($6.2 | ) | ($2.1 | ) | ($8.3 | ) | |||||

The amount reclassified from accumulated other comprehensive loss for the pension and postretirement liability adjustment was included in other income, net in the Unaudited Consolidated Statements of Operations. These accumulated other comprehensive loss components are components of net periodic benefit cost. See Note 9 - Retirement and Postretirement Plans for additional information.

13

Note 8 - Changes in Shareholders' Equity

Changes in the components of shareholders’ equity for the six months ended June 30, 2018 were as follows:

Total | Additional Paid-in Capital | Retained Deficit | Treasury Shares | Accumulated Other Comprehensive Loss | |||||||||||||||

Balance at December 31, 2017 | $560.7 | $843.7 | ($238.0 | ) | ($37.4 | ) | ($7.6 | ) | |||||||||||

Net Income | 6.5 | — | 6.5 | — | — | ||||||||||||||

Pension and postretirement adjustment, net of tax | 0.3 | — | — | — | 0.3 | ||||||||||||||

Foreign currency translation adjustments | (0.4 | ) | — | — | — | (0.4 | ) | ||||||||||||

ASU 2014-09 adjustment | 0.7 | — | 0.7 | — | — | ||||||||||||||

Stock-based compensation expense | 3.7 | 3.7 | — | — | — | ||||||||||||||

Stock option activity | 0.2 | 0.2 | — | — | — | ||||||||||||||

Issuance of treasury shares | — | (4.9 | ) | (0.2 | ) | 5.1 | — | ||||||||||||

Shares surrendered for taxes | (0.7 | ) | — | — | (0.7 | ) | — | ||||||||||||

Balance at June 30, 2018 | $571.0 | $842.7 | ($231.0 | ) | ($33.0 | ) | ($7.7 | ) | |||||||||||

Note 9 - Retirement and Postretirement Plans

The components of net periodic benefit cost for the three and six months ended June 30, 2018 and 2017 were as follows:

Three Months Ended June 30, 2018 | Three Months Ended June 30, 2017 | ||||||||||||||

Components of net periodic benefit cost: | Pension | Postretirement | Pension | Postretirement | |||||||||||

Service cost | $4.3 | $0.5 | $4.6 | $0.4 | |||||||||||

Interest cost | 11.4 | 1.9 | 12.3 | 2.1 | |||||||||||

Expected return on plan assets | (18.5 | ) | (1.2 | ) | (17.7 | ) | (1.3 | ) | |||||||

Amortization of prior service cost | 0.1 | — | 0.1 | 0.3 | |||||||||||

Net Periodic Benefit Cost | ($2.7 | ) | $1.2 | ($0.7 | ) | $1.5 | |||||||||

Six Months Ended June 30, 2018 | Six Months Ended June 30, 2017 | ||||||||||||||

Components of net periodic benefit cost: | Pension | Postretirement | Pension | Postretirement | |||||||||||

Service cost | $8.6 | $0.9 | $9.2 | $0.8 | |||||||||||

Interest cost | 22.8 | 3.8 | 24.5 | 4.2 | |||||||||||

Expected return on plan assets | (36.9 | ) | (2.4 | ) | (35.2 | ) | (2.7 | ) | |||||||

Amortization of prior service cost | 0.2 | 0.1 | 0.2 | 0.6 | |||||||||||

Net Periodic Benefit Cost | ($5.3 | ) | $2.4 | ($1.3 | ) | $2.9 | |||||||||

14

Note 10 - Revenue Recognition

As discussed in Note 2 - Recent Accounting Pronouncements, on January 1, 2018 TimkenSteel adopted the new revenue recognition standard. Under this new standard, TimkenSteel recognizes revenue from contracts at a point in time when it has satisfied its performance obligation and the customer obtains control of the goods, at the amount that reflects the consideration the Company expects to receive for those goods. The Company receives and acknowledges purchase orders from its customers, which define the quantity, pricing, payment and other applicable terms and conditions. In some cases, the Company receives a blanket purchase order from its customer, which includes pricing, payment and other terms and conditions, with quantities defined at the time the customer issues periodic releases from the blanket purchase order. Certain contracts contain variable consideration, which primarily consists of rebates, that are accounted for in net sales and accrued based on the estimated probability of the requirements being met. Amounts billed to customers related to shipping and handling costs are included in net sales and related costs are included in costs of products sold in the Unaudited Consolidated Financial Statements.

The following table provides the major sources of revenue by end market sector.

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Mobile | $141.6 | $135.6 | $284.1 | $272.2 | |||||||||||

Industrial | 166.9 | 120.2 | 314.6 | 230.8 | |||||||||||

Energy | 68.8 | 37.6 | 117.9 | 61.3 | |||||||||||

Other | 36.2 | 45.9 | 77.7 | 84.4 | |||||||||||

Total Net Sales | $413.5 | $339.3 | $794.3 | $648.7 | |||||||||||

The following table provides the major sources of revenue by product type.

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Bar | $262.4 | $219.8 | $496.8 | $418.0 | |||||||||||

Tube | 70.6 | 42.4 | 134.3 | 77.0 | |||||||||||

Value-add | 69.2 | 68.4 | 141.9 | 136.3 | |||||||||||

Other | 11.3 | 8.7 | 21.3 | 17.4 | |||||||||||

Total Net Sales | $413.5 | $339.3 | $794.3 | $648.7 | |||||||||||

15

Note 11 - Earnings Per Share

Basic income (loss) per share is computed based upon the weighted average number of common shares outstanding. Diluted earnings (loss) per share is computed based upon the weighted average number of common shares outstanding plus the dilutive effect of common share equivalents calculated using the treasury stock method or if-converted method. For the Convertible Notes, the Company utilizes the if-converted method to calculate diluted loss per share. Under the if-converted method, the Company adjusts net earnings to add back interest expense (including amortization of debt discount) recognized on the Convertible Notes and includes the number of shares potentially issuable related to the Convertible Notes in the weighted average shares outstanding. Treasury stock is excluded from the denominator in calculating both basic and diluted loss per share.

Common share equivalents for shares issuable for equity-based awards were excluded from the computation of diluted earnings (loss) per share for the six months ended June 30, 2017 because the effect of their inclusion would have been anti-dilutive. Common share equivalents for shares issuable upon the conversion of outstanding convertible notes, were excluded from the computation of diluted earnings (loss) per share for the three and six months ended June 30, 2018 and 2017 because the effect of their inclusion would have been anti-dilutive.

The following table sets forth the reconciliation of the numerator and the denominator of basic earnings (loss) per share and diluted earnings (loss) per share for the three and six months ended June 30, 2018 and 2017:

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Numerator: | |||||||||||||||

Net income (loss) for basic and diluted earnings per share | $8.4 | $1.3 | $6.5 | ($4.0 | ) | ||||||||||

Denominator: | |||||||||||||||

Weighted average shares outstanding, basic | 44.6 | 44.4 | 44.5 | 44.3 | |||||||||||

Dilutive effect of stock-based awards | 0.6 | 0.4 | 0.7 | — | |||||||||||

Weighted average shares outstanding, diluted | 45.2 | 44.8 | 45.2 | 44.3 | |||||||||||

Basic earnings (loss) per share | $0.19 | $0.03 | $0.15 | ($0.09 | ) | ||||||||||

Diluted earnings (loss) per share | $0.19 | $0.03 | $0.14 | ($0.09 | ) | ||||||||||

Note 12 - Income Tax Provision

TimkenSteel’s provision for income taxes in interim periods is computed by applying the appropriate estimated annual effective tax rates to income or loss before income taxes for the period. In addition, non-recurring or discrete items, including interest on prior-year tax liabilities, are recorded during the periods in which they occur.

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||

2018 | 2017 | 2018 | 2017 | |||||||||

Provision for incomes taxes | $0.2 | $0.8 | $0.3 | $1.1 | ||||||||

Effective tax rate | 1.9 | % | 39.6 | % | 4.1 | % | (39.1 | )% | ||||

Operating losses generated in the U.S. resulted in a decrease in the carrying value of the Company’s U.S. deferred tax liability to the point of a net U.S. deferred tax asset at December 31, 2016. At that time, the Company assessed, based upon operating performance in the U.S. and industry conditions that it was more likely than not it would not realize a portion of its U.S. deferred tax assets. The Company recorded a valuation allowance in 2016 and 2017 and remained in a valuation allowance position in the first half of 2018. Going forward, the need to maintain valuation allowances against deferred tax assets in the U.S. and other affected countries will cause variability in the Company’s effective tax rate. The Company will maintain a valuation allowance against its deferred tax assets in the U.S. and applicable foreign countries until sufficient positive evidence exists to eliminate them. The change in the effective tax rate for the three and six months ended June 30, 2018 compared to the

16

same periods in 2017 is primarily due to a discrete charge of approximately $1.0 million recorded in the second quarter of 2017.

Tax Cuts and Jobs Act Bill

On December 22, 2017, the Tax Cut and Jobs Act (the Act) was signed into law, which resulted in significant changes to U.S. tax and related laws. Some of the provisions of the Act affecting corporations include, but are not limited to reducing the federal corporate income tax rate from 35% to 21%, limiting the interest expense deduction, expensing of cost of acquired qualified property and eliminating the domestic production activities deduction. We are currently evaluating the impact of the Act, however we do not anticipate that the Act will have a material impact on our financial condition and results of operations. At this time, we do not anticipate a significant reduction in our effective income tax rate or our net deferred federal income tax assets as a result of the income tax rate reduction, as we expect to be in a valuation allowance in 2018.

Other provisions of the Act include a new minimum tax on certain foreign earnings, the Global Intangibles Low-taxed Income, a new tax on certain payments to foreign related parties, the Base Erosion Anti-avoidance Tax, a new incentive for Foreign-derived Intangibles Income, changes to the limitation on the deductibility of certain executive compensation, and new limitations on the deductibility of interest expense. Generally, these other provisions take effect for the Company in the year ending December 31, 2018. On December 22, 2017, the SEC issued Staff Accounting Bulletin No. 118 (SAB 118). This guidance allows registrants a “measurement period,” not to exceed one year from the date of enactment, to complete their accounting for the tax effects of the Act. SAB 118 further directs that, during the measurement period, registrants that are able to make reasonable estimates of the tax effects of the Act should include those amounts in their financial statements as “provisional” amounts. Registrants should reflect adjustments over subsequent periods as they are able to refine their estimates and complete their accounting for the tax effects of the Act. The tax effects related to the Act described in the paragraph above represent the Company’s reasonable estimates within the meaning of SAB 118. Also, it is expected that the U.S. Treasury will issue regulations and other guidance on the application of certain provisions of the Act. In subsequent periods, but within the measurement period, the Company will analyze that guidance and other necessary information.

Note 13 - Contingencies

TimkenSteel has a number of loss exposures incurred in the ordinary course of business, such as environmental claims, product warranty claims, and litigation. Establishing loss reserves for these matters requires management’s estimate and judgment regarding risk exposure and ultimate liability or realization. These loss reserves are reviewed periodically and adjustments are made to reflect the most recent facts and circumstances. As of June 30, 2018 and December 31, 2017, TimkenSteel had a $0.6 million and a $0.9 million contingency reserve, respectively, related to loss exposures incurred in the ordinary course of business.

Environmental Matters

From time to time, TimkenSteel may be a party to lawsuits, claims or other proceedings related to environmental matters and/or may receive notices of potential violations of environmental laws and regulations from the U.S. Environmental Protection Agency (EPA) and similar state or local authorities. TimkenSteel recorded reserves for such environmental matters as other current and non-current liabilities on the Consolidated Balance Sheets. Accruals related to such environmental matters represent management’s best estimate of the fees and costs associated with these matters. Although it is not possible to predict with certainty the outcome of such matters, management believes that their ultimate dispositions should not have a material adverse effect on TimkenSteel’s financial position, cash flows, or results of operations. As of June 30, 2018 and December 31, 2017, TimkenSteel had a $0.9 million and $0.5 million reserve for such environmental matters as other current and non-current liabilities on the Unaudited Consolidated Balance Sheets, respectively.

The following is a rollforward of the accrual related to environmental matters for the six months ended June 30, 2018 and 2017:

Six Months Ended June 30, | ||||||

2018 | 2017 | |||||

Beginning balance, January 1 | $0.5 | $0.6 | ||||

Expenses | 0.4 | 0.1 | ||||

Payments | — | (0.1 | ) | |||

Ending balance, June 30 | $0.9 | $0.6 | ||||

17

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

(dollars in millions, except per share data)

Business Overview

TimkenSteel Corporation (we, us, our, the Company or TimkenSteel) was incorporated in Ohio on October 24, 2013, and became an independent, publicly traded company as the result of a spinoff from The Timken Company on June 30, 2014.

We manufacture alloy steel, as well as carbon and micro-alloy steel, with an annual melt capacity of approximately 2 million tons and shipment capacity of 1.5 million tons. Our portfolio includes special bar quality (SBQ) bars, seamless mechanical tubing (tubes), value-add solutions such as precision steel components, and billets. In addition, we manage machining, thermal treatment, and raw material recycling programs that are used as a feeder system for our melt operations. Our products and services are used in a diverse range of demanding applications in the following market sectors: oil and gas; OCTG; automotive; industrial equipment; mining; construction; rail; aerospace and defense; heavy truck; agriculture; and power generation.

Based on our knowledge of the steel industry, we believe we are the only focused SBQ steel producer in North America and have the largest SBQ steel large bar (6-inch diameter and greater) production capacity among North American steel producers. In addition, we are the only steel manufacturer able to produce rolled SBQ steel large bars up to 16-inches in diameter. SBQ steel is made to restrictive chemical compositions and high internal purity levels and is used in critical mechanical applications. We make these products from nearly 100% recycled steel, using our expertise in raw materials to create custom steel products. We focus on creating tailored products and services for our customers’ most demanding applications. Our engineers are experts in both materials and applications, so we can work closely with each customer to deliver flexible solutions related to our products as well as to their applications and supply chains. We believe our unique operating model and production assets give us a competitive advantage in our industry.

The SBQ bars, tubes, and billets production processes take place at our Canton, Ohio manufacturing location. This location accounts for all of the SBQ bars, seamless mechanical tubes and billets we produce and includes three manufacturing facilities: the Faircrest, Harrison, and Gambrinus facilities. Our value-add solutions production processes take place at three downstream manufacturing facilities: TimkenSteel Material Services (Houston, TX), Tryon Peak (Columbus, NC), and St. Clair (Eaton, OH). Many of the production processes are integrated, and the manufacturing facilities produce products that are sold in all of our market sectors. As a result, investments in our facilities and resource allocation decisions affecting our operations are designed to benefit the overall business, not any specific aspect of the business.

Capital Investments

Our recent capital investments are expected to significantly strengthen our position as a leader in providing differentiated solutions for the energy, industrial and automotive market sectors, while enhancing our operational performance and customer service capabilities.

In the fourth quarter of 2017, we launched our new advanced quench-and-temper heat-treat line. The approximately $40 million investment performs quench-and-temper heat-treat operations and has the capacity for up to 50,000 process-tons annually of 4-inch to 13-inch bars and tubes. This equipment is located in a separate facility in Perry Township, Ohio on the site of our Gambrinus Steel Plant, and is one of our larger thermal treatment facilities. This new equipment allows us to meet stringent industry requirements regardless of the order size, resulting in better service for our customers.

Impact of Raw Material Prices and LIFO

In the ordinary course of business, we are exposed to the volatility of the costs of our raw materials. Whenever possible, we manage our exposure to commodity risks primarily through the use of supplier pricing agreements that enable us to establish the purchase prices for certain inputs that are used in our manufacturing process. We also utilize a raw material surcharge mechanism that is designed to mitigate the impact of increases or decreases in raw material costs, although generally with a lag effect. This timing effect can result in raw material spread whereby costs can be over- or under-recovered in certain periods. While the surcharge generally protects gross profit, it has the effect of diluting gross margin as a percent of sales.

We value some of our inventory utilizing the LIFO inventory valuation method. Changes in the cost of raw materials and production activities are recognized in cost of products sold in the current period even though these materials and other costs may have been incurred in different periods at significantly different values due to the length of time of our production cycle. In a period of rising raw material prices, cost of products sold recognized under LIFO is generally higher than the cash costs incurred to acquire the inventory sold. Conversely, in a period of declining raw materials prices, cost of products sold recognized under LIFO is

18

generally lower than cash costs incurred to acquire the inventory sold. In periods of rising inventories and deflating raw material prices, the likely result will be a positive impact to net income. Conversely, in periods of rising inventories and increasing raw materials prices, the likely result will be a negative impact to net income.

Results of Operations

Net Sales

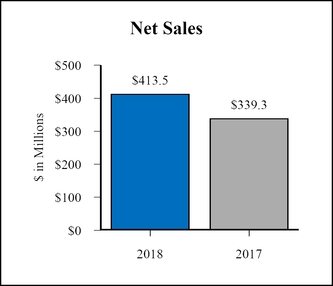

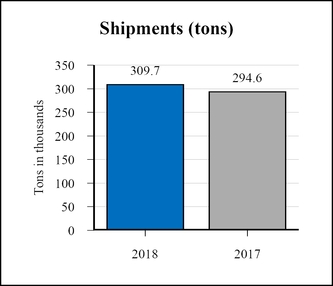

The charts below present net sales and shipments for the three months ended June 30, 2018 and 2017.

Net sales for the three months ended June 30, 2018 were $413.5 million, an increase of $74.2 million or 22% compared to the three months ended June 30, 2017. Excluding surcharges, net sales increased $48.0 million, or 18%. The increase was due to higher volumes of $20.0 million and price/mix of approximately $28.0 million. For the three months ended June 30, 2018, ship tons increased by 15.1 thousand tons, or 5%, compared to the three months ended June 30, 2017, due primarily to higher demand in industrial and energy end markets.

19

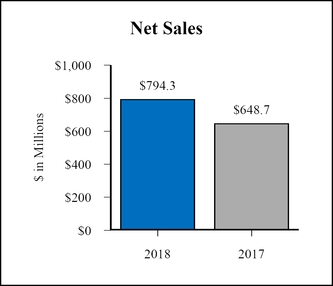

The charts below present net sales and shipments for the six months ended June 30, 2018 and 2017.

Net sales for the six months ended June 30, 2018 were $794.3 million, an increase of $145.6 million or 22% compared to the six months ended June 30, 2017. Excluding surcharges, net sales increased $87.0 million, or 17%. The increase was due to higher volumes of approximately $42 million and price/mix of approximately $46 million. For the six months ended June 30, 2018, ship tons increased by 34.9 thousand tons, or 6%, compared to the six months ended June 30, 2017, due primarily to higher demand in industrial and energy end markets.

20

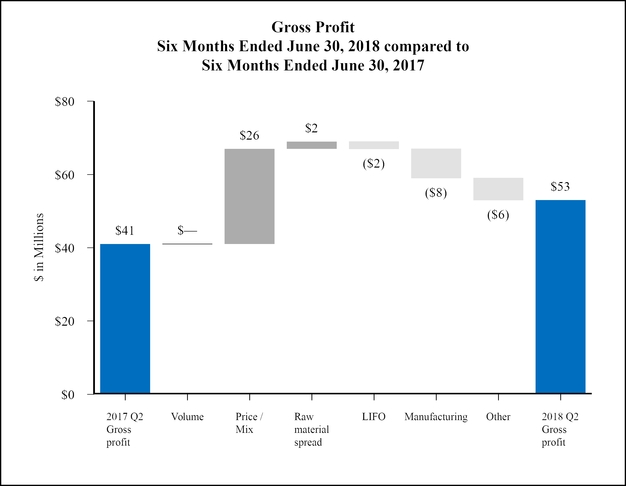

Gross Profit

Gross profit for the three months ended June 30, 2018 increased $8.3 million, or 35%, compared to the three months ended June 30, 2017. The increase was driven primarily by a favorable price/mix due to higher demand in the industrial and energy end markets. Partially offsetting the increase were unfavorable manufacturing costs and LIFO primarily due to higher inflation and higher raw material costs impacted by timing as well as higher costs of obsolete grades of scrap, and the absence of a supplier refund that occurred in the three months ended June 30, 2017.

21

Gross profit for the six months ended June 30, 2018 increased $12.4 million, or approximately 30%, compared to the six months ended June 30, 2017. The increase was driven primarily by a favorable price/mix due to higher demand in the industrial and energy end markets and favorable raw material spread. Partially offsetting the increase were unfavorable manufacturing costs due to higher inflation, non-recurring legal costs and employee benefit claims and the absence of a supplier refund that occurred in the six months ended June 30, 2017.

22

Selling, General and Administrative Expenses

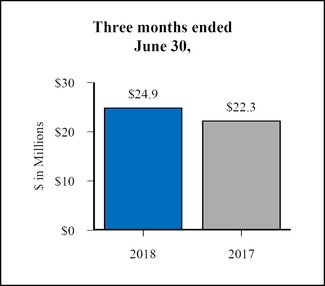

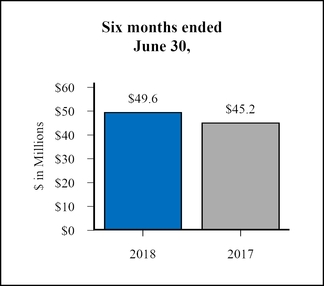

The charts below present selling, general and administrative (SG&A) expense for the three and six months ended June 30, 2018 and 2017.

SG&A expense for the three months and six months ended June 30, 2018 increased by $2.6 million and $4.4 million, respectively, compared to the same periods in 2017, due primarily to an increase in variable compensation and employee costs.

Interest Expense

Three Months Ended June 30, | |||||||||||

2018 | 2017 | $ Change | |||||||||

Cash interest paid | $4.3 | $4.1 | $0.2 | ||||||||

Accrued interest | (1.6 | ) | (1.3 | ) | (0.3 | ) | |||||

Amortization of convertible notes discount and deferred financing | 1.2 | 0.9 | 0.3 | ||||||||

Total Interest Expense | $3.9 | $3.7 | $0.2 | ||||||||

Six Months Ended June 30, | |||||||||||

2018 | 2017 | $ Change | |||||||||

Cash interest paid | $5.2 | $4.6 | $0.6 | ||||||||

Accrued interest | 0.3 | 0.6 | (0.3 | ) | |||||||

Amortization of convertible notes discount and deferred financing | 3.0 | 2.1 | 0.9 | ||||||||

Total Interest Expense | $8.5 | $7.3 | $1.2 | ||||||||

Interest expense for the three months ended June 30, 2018 was $3.9 million, an increase of $0.2 million compared to the three months ended June 30, 2017. Interest expense for the six months ended June 30, 2018 increased $1.2 million, compared to the same period in 2017. The increase is due to the write-off of deferred financing costs of $0.5 million associated with amending the Credit Agreement and $0.2 million associated with the redemption of the Revenue Refunding Bonds, which occurred in the first quarter of 2018, and higher average borrowings on the Amended Credit Agreement in the first half of 2018 as compared to average borrowings on the Credit Agreement in the same period in 2017, partially offset by lower interest rates. For additional details regarding the Credit Agreement, the Amended Credit Agreement and the Revenue Refunding Bonds, please refer to Note 6 - Financing Arrangements in the Notes to Unaudited Consolidated Financial Statements.

23

Provision for Income Taxes

Three Months Ended June 30, | ||||||||||||||

2018 | 2017 | $ Change | % Change | |||||||||||

Provision for income taxes | $0.2 | $0.8 | ($0.6 | ) | (75.0 | )% | ||||||||

Effective tax rate | 1.9 | % | 39.6 | % | NM | — | ||||||||

Six Months Ended June 30, | ||||||||||||||

2018 | 2017 | $ Change | % Change | |||||||||||

Provision for income taxes | $0.3 | $1.1 | ($0.8 | ) | (72.7 | )% | ||||||||

Effective tax rate | 4.1 | % | (39.1 | )% | NM | — | ||||||||

Operating losses generated in the U.S. resulted in a decrease in the carrying value of our U.S. deferred tax liability to the point of a net U.S. deferred tax asset at December 31, 2016. At that time, we assessed, based upon operating performance in the U.S. and industry conditions that it was more likely than not we would not realize a portion of our U.S. deferred tax assets. The Company recorded a valuation allowance in 2016 and 2017 and remained in a valuation allowance position in the first half of 2018. Going forward, the need to maintain valuation allowances against deferred tax assets in the U.S. and other affected countries will cause variability in our effective tax rate. We will maintain a valuation allowance against our deferred tax assets in the U.S. and applicable foreign countries until sufficient positive evidence exists to eliminate them. The change in the effective tax rate for the three and six months ended June 30, 2018 compared to the same periods in 2017 is primarily due to a discrete charge of approximately $1.0 million recorded in the second quarter of 2017.

On December 22, 2017, the Tax Cut and Jobs Act (the Act) was signed into law, which enacts significant changes to U.S. tax and related laws. We are currently evaluating the impact of the Act, however we do not anticipate that the Act will have a material impact on our financial condition and results of operations. At this time, we do not anticipate a significant reduction in our effective income tax rate or our net deferred federal income tax assets as a result of the income tax rate reduction, as we expect to be in a valuation allowance in 2018.

24

Net Sales, Excluding Surcharges

The table below presents net sales by end market sector, adjusted to exclude raw material surcharges, which represents a financial measure that has not been determined in accordance with U.S. GAAP. We believe presenting net sales by end market sector adjusted to exclude raw material surcharges provides additional insight into key drivers of net sales such as base price and product mix.

Net Sales adjusted to exclude surcharges | ||||||||||||||||||||||||||||||

(dollars in millions, tons in thousands) | ||||||||||||||||||||||||||||||

Three Months Ended June 30, | ||||||||||||||||||||||||||||||

2018 | 2017 | |||||||||||||||||||||||||||||

Mobile | Industrial | Energy | Other | Total | Mobile | Industrial | Energy | Other | Total | |||||||||||||||||||||

Tons | 111.9 | 123.0 | 40.5 | 34.3 | 309.7 | 108.7 | 102.8 | 25.7 | 57.4 | 294.6 | ||||||||||||||||||||

Net Sales | $141.6 | $166.9 | $68.8 | $36.2 | $413.5 | $135.6 | $120.2 | $37.6 | $45.9 | 339.3 | ||||||||||||||||||||

Less: Surcharges | 34.9 | 42.9 | 15.1 | 10.9 | 103.8 | 28.2 | 27.7 | 6.0 | 15.7 | 77.6 | ||||||||||||||||||||

Base Sales | $106.7 | $124.0 | $53.7 | $25.3 | $309.7 | $107.4 | $92.5 | $31.6 | $30.2 | $261.7 | ||||||||||||||||||||

Net Sales / Ton | $1,265.4 | $1,356.9 | $1,698.8 | $1,055.4 | $1,335.2 | $1,247.5 | $1,169.3 | $1,463.0 | $799.7 | $1,151.7 | ||||||||||||||||||||

Base Sales / Ton | $953.5 | $1,008.1 | $1,325.9 | $737.6 | $1,000.0 | $988.0 | $899.8 | $1,229.6 | $526.1 | $888.3 | ||||||||||||||||||||

Six Months Ended June 30, | ||||||||||||||||||||||||||||||

2018 | 2017 | |||||||||||||||||||||||||||||

Mobile | Industrial | Energy | Other | Total | Mobile | Industrial | Energy | Other | Total | |||||||||||||||||||||

Tons | 222.3 | 236.7 | 69.5 | 80.9 | 609.4 | 223.6 | 202.2 | 42.6 | 106.1 | 574.5 | ||||||||||||||||||||

Net Sales | $284.1 | $314.6 | $117.9 | $77.7 | $794.3 | $272.2 | $230.8 | $61.3 | $84.4 | $648.7 | ||||||||||||||||||||

Less: Surcharges | 66.2 | 78.1 | 26.1 | 24.1 | 194.5 | 51.1 | 48.1 | 8.9 | 27.8 | 135.9 | ||||||||||||||||||||

Base Sales | $217.9 | $236.5 | $91.8 | $53.6 | $599.8 | $221.1 | $182.7 | $52.4 | $56.6 | $512.8 | ||||||||||||||||||||

Net Sales / Ton | $1,278.0 | $1,329.1 | $1,696.4 | $960.4 | $1,303.4 | $1,217.4 | $1,141.4 | $1,439.0 | $795.5 | $1,129.2 | ||||||||||||||||||||

Base Sales / Ton | $980.2 | $999.2 | $1,320.9 | $662.5 | $984.2 | $988.8 | $903.6 | $1,230.0 | $533.5 | $892.6 | ||||||||||||||||||||

THE BALANCE SHEET

The following discussion is a comparison of the Consolidated Balance Sheets as of June 30, 2018 (Unaudited) and December 31, 2017:

Current Assets | June 30, 2018 | December 31, 2017 | |||||

Cash and cash equivalents | $39.0 | $24.5 | |||||

Accounts receivable, net | 173.6 | 149.8 | |||||

Inventories, net | 294.5 | 224.0 | |||||

Deferred charges and prepaid expenses | 2.3 | 3.9 | |||||

Other current assets | 10.9 | 8.0 | |||||

Total Current Assets | $520.3 | $410.2 | |||||

Refer to the Liquidity and Capital Resources section of this Management’s Discussion and Analysis of Financial Condition and Results of Operations for a discussion of the change in cash and cash equivalents. Accounts receivable, net increased $23.8 million as of June 30, 2018 compared to December 31, 2017, due to an increase in net sales of approximately $72.1 million in the second quarter 2018 compared to the fourth quarter of 2017. Inventories, net increased $70.5 million as of June 30, 2018 compared to December 31, 2017, primarily due to increased raw material costs and inventory build for increased sales demand in the industrial and energy end markets.

25

Property, Plant and Equipment | June 30, 2018 | December 31, 2017 | |||||

Property, plant and equipment, net | $679.8 | $706.7 | |||||

Property, plant and equipment, net decreased $26.9 million as of June 30, 2018 compared to December 31, 2017. The decrease was primarily due to $34.0 million of depreciation expense and approximately $0.5 million of impairment charges and loss on sale or disposals related to the discontinued use of certain assets, partially offset by capital expenditures of approximately $8.0 million during the six months ended June 30, 2018.

Other Assets | June 30, 2018 | December 31, 2017 | |||||

Pension assets | $17.4 | $14.6 | |||||

Intangible assets, net | 17.5 | 19.9 | |||||

Other non-current assets | 5.0 | 5.2 | |||||

Total Other Assets | $39.9 | $39.7 | |||||

Pension assets increased $2.8 million as of June 30, 2018 compared to December 31, 2017, primarily driven by the annual pension contribution made in the first quarter of 2018 to the Company’s U.K. pension plan. Intangible assets, net decreased $2.4 million as of June 30, 2018 compared to December 31, 2017, primarily due to amortization expense of $2.9 million and approximately $0.4 million of impairment charges due to the discontinued use of certain capitalized software, partially offset by capitalized software expenditures of approximately $1.0 million during the six months ended June 30, 2018.

Liabilities and Shareholders’ Equity | June 30, 2018 | December 31, 2017 | |||||

Current liabilities | $237.5 | $206.8 | |||||

Convertible notes, net | 72.0 | 70.1 | |||||

Other long-term debt | 150.0 | 95.2 | |||||

Accrued pension and postretirement costs - long-term | 197.7 | 210.8 | |||||

Deferred income taxes | — | 0.3 | |||||

Other non-current liabilities | 11.8 | 12.7 | |||||

Total shareholders’ equity | 571.0 | 560.7 | |||||

Total Liabilities and Shareholders’ Equity | $1,240.0 | $1,156.6 | |||||

Current liabilities increased $30.7 million as of June 30, 2018 compared to December 31, 2017, primarily due to an increase in accounts payable of $42.5 million from higher production and scrap costs, partially offset by lower plant maintenance cost accruals related to our annual shutdown that occurred in the fourth quarter of 2017.

Other long-term debt increased due to net borrowings of $54.8 million on the Amended Credit Agreement primarily to fund working capital. See Note 6 - Financing Arrangements in the Notes to Unaudited Consolidated Financial Statements and the Liquidity and Capital Resources section of this Management’s Discussion and Analysis of Financial Condition and Results of Operations for additional discussion of our other long-term debt and the Convertible Notes.

Refer to Note 8 - Changes in Shareholders' Equity in the Notes to Unaudited Consolidated Financial Statements for details regarding the decrease in total shareholder’s equity.

26

LIQUIDITY AND CAPITAL RESOURCES

Convertible Notes

In May 2016, we issued $75.0 million aggregate principal amount of Convertible Notes, plus an additional $11.3 million principal amount to cover over-allotments. The Convertible Notes bear cash interest at a rate of 6.0% per year, payable semiannually on June 1 and December 1, beginning on December 1, 2016. The Convertible Notes will mature on June 1, 2021, unless earlier repurchased or converted. The net proceeds received from the offering were $83.2 million, after deducting the initial underwriters’ discount and fees and paying the offering expenses. We used the net proceeds to repay a portion of the amounts outstanding under the Credit Agreement.

Credit Agreement

On February 26, 2016, the Company, as borrower, and certain domestic subsidiaries, as subsidiary guarantors, entered into the Amended and Restated Credit Agreement (the Credit Agreement), with JPMorgan Chase Bank, N.A., as administrative agent, and the other lenders party thereto. The Credit Agreement provided for a $265 million asset based revolving credit facility.

Amended Credit Agreement

On January 26, 2018, we as borrower, and certain domestic subsidiaries, as subsidiary guarantors, entered into the Second Amended and Restated Credit Agreement (Amended Credit Agreement), with JPMorgan Chase Bank, N.A., as administrative agent, Bank of America, N.A., as syndication agent, and the other lenders party thereto, which amended and restated the Company’s existing Credit Agreement.

The Amended Credit Agreement provides for a $300 million asset-based revolving credit facility, including a $15 million sublimit for the issuance of commercial and standby letters of credit and a $30 million sublimit for swingline loans. Pursuant to the terms of the Amended Credit Agreement, we are entitled, on up to two occasions and subject to the satisfaction of certain conditions, to request increases in the commitments under the Amended Credit Agreement in the aggregate principal amount of up to $50 million, to the extent that existing or new lenders agree to provide such additional commitments.

The availability of borrowings under the Amended Credit Agreement is subject to a borrowing base calculation based upon a valuation of the eligible accounts receivable, inventory and machinery and equipment of us and our subsidiary guarantors, each multiplied by an applicable advance rate. The availability of borrowings may be further modified by reserves established from time to time by the administrative agent in its permitted discretion.

The interest rate per annum applicable to loans under the Amended Credit Agreement will be, at our option, equal to either (i) the alternate base rate plus the applicable margin or (ii) the relevant adjusted LIBO rate for an interest period of one, two, three or six months (as selected by the Company) plus the applicable margin. The base rate will be a fluctuating rate per annum equal to the greatest of (i) the prime rate of the administrative agent, (ii) the effective Federal Reserve Bank of New York rate plus 0.50% and (iii) the adjusted LIBO rate for a one-month interest period on the applicable date, plus 1.00%. The adjusted LIBO rate will be equal to the applicable London interbank offered rate for the selected interest period, as adjusted for statutory reserve requirements for eurocurrency liabilities. The applicable margin will be determined by a pricing grid based on our average quarterly availability. In addition, we will pay a commitment fee on the average daily unused amount of the credit facility in a percentage determined by our average daily availability for the most recently completed calendar month. The interest rate under the Amended Credit Agreement was 4.0% as of June 30, 2018. The amount available under the Amended Credit Agreement as of June 30, 2018 was approximately $147.4 million.

The Amended Credit Agreement matures on January 26, 2023. Prior to the maturity date, amounts outstanding are required to be repaid (without reduction of the commitments thereunder) from mandatory prepayment events from the proceeds of certain asset sales, equity or debt issuances or casualty events.

The Amended Credit Agreement contains certain customary covenants, including covenants that limit the ability of the Company and its subsidiaries to, among other things, (i) incur or suffer to exist certain liens, (ii) make investments, (iii) incur or guaranty additional indebtedness, (iv) enter into consolidations, mergers, acquisitions, sale-leaseback transactions and sales of assets, (v) make distributions and other restricted payments, (vi) change the nature of its business, (vii) engage in transactions with affiliates and (viii) enter into restrictive agreements, including agreements that restrict the ability to incur liens or make distributions.

In addition, the Amended Credit Agreement requires us to (i) unless certain conditions are met, maintain certain minimum liquidity as specified in the Amended Credit Agreement during the period commencing on March 1, 2021 and ending on June 1,

27

2021 and (ii) maintain a minimum specified fixed charge coverage ratio on a springing basis if minimum availability requirements as specified in the Amended Credit Agreement are not maintained.

The Amended Credit Agreement contains certain customary events of default. If any event of default occurs and is continuing, the Lenders would be entitled to take various actions, including the acceleration of amounts due under the Amended Credit Agreement, and exercise other rights and remedies.

Revenue Refunding Bonds

In connection with entering into the Amended Credit Agreement, on January 23, 2018, we redeemed in full $12.2 million of Ohio Water Development Revenue Refunding Bonds (originally due on November 1, 2025), $9.5 million of Ohio Air Quality Development Revenue Refunding Bonds (originally due on November 1, 2025) and $8.5 million of Ohio Pollution Control Revenue Refunding Bonds (originally due on June 1, 2033).

The following represents a summary of key liquidity measures under the Amended Credit Agreement as of June 30, 2018 and the Credit Agreement as of December 31, 2017:

June 30, 2018 | December 31, 2017 | |||||

Cash and cash equivalents | $39.0 | $24.5 | ||||

Maximum availability | $300.0 | $265.0 | ||||

Amount borrowed | 150.0 | 65.0 | ||||

Letter of credit obligations | 2.6 | 2.6 | ||||

Availability not borrowed | 147.4 | 197.4 | ||||

Availability block | — | 33.1 | ||||

Net availability | $147.4 | $164.3 | ||||

Total liquidity | $186.4 | $188.8 | ||||

Our principal sources of liquidity are cash and cash equivalents, cash flows from operations and available borrowing capacity under our Amended Credit Agreement. We currently expect that our cash and cash equivalents on hand, expected cash flows from operations and borrowings available under the Amended Credit Agreement will be sufficient to meet liquidity needs; however, these plans rely on certain underlying assumptions and estimates that may differ from actual results. Such assumptions include growing market demand, lowered operating costs and increased liquidity.

As of June 30, 2018, taking into account the foregoing, as well as our view of industrial, energy, and automotive market demands for our products, our 2018 operating plan and our long-range plan, we believe that our cash balance as of June 30, 2018 of $39.0 million, projected cash generated from operations, and borrowings available under the Amended Credit Agreement, will be sufficient to satisfy our working capital needs, capital expenditures and other liquidity requirements associated with our operations, including servicing our debt obligations, for at least the next twelve months and through January 26, 2023, the maturity date of our Amended Credit Agreement.