UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANY

Investment Company Act file number 811-22940

The Endowment PMF Master Fund, L.P.

(Exact name of registrant as specified in charter)

4265 SAN FELIPE, 8TH FLOOR, HOUSTON, TX 77027

(Address of principal executive offices) (Zip code)

| With a copy to: | ||

| John A. Blaisdell | George J. Zornada | |

| The Endowment Master Fund, L.P. | K & L Gates LLP | |

| 4265 San Felipe, 8th Floor | State Street Financial Center | |

| Houston, TX 77027 | One Lincoln St. | |

| (Name and address of agent for service) | Boston, MA 02111-2950 | |

| (617) 261-3231 |

Registrant’s telephone number, including area code: 800-725-9456

Date of fiscal year end: 12/31/15

Date of reporting period: 12/31/15

Item 1. Reports to Stockholders.

the

ENDOWMENT FUND

The Endowment PMF Master Fund, L.P.

Shareholder Report

December 31, 2015

| The Endowment PMF Master Fund, L.P. |

||||

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 8 | ||||

| 9 | ||||

| 10 | ||||

| 11 | ||||

| 24 | ||||

| 29 |

Dear PMF Partners:

We would like to thank our investors for your patience and support as we continue pursuing the objectives of the PMF Fund, L.P. (the “Fund”)1. In this letter we will provide a review of the Fund’s performance for the year, briefly review the restructuring that was put in place in March of 2014, and lastly, provide a status on liquidation.

Private Equity Portfolio Performance since Inception

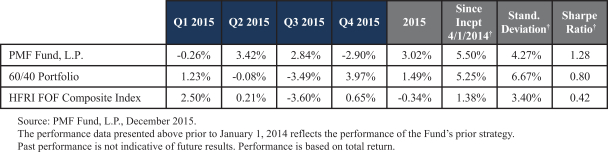

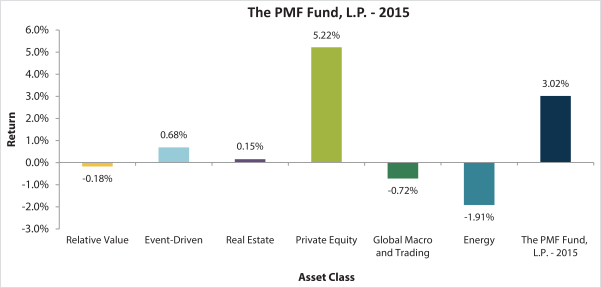

The Fund returned 3.02% in 2015, which outpaced the 60/40 Portfolio and HFRI FOF Composite Index by 1.53% and 3.36%, respectively. The year’s positive performance was driven by the second and third quarters with marks of 3.42% and 2.84%, respectively.

The Private Equity asset class was the primary driver of performance during the summer months, as well as for the year. The returns were a result of positive Initial Public Offering (“IPO”) activity as well as numerous markups from the venture capital, growth equity, and buyout sub asset classes. The Private Equity asset class added 5.22% to the overall portfolio in 2015 (as a reminder, performance contribution is calculated by multiplying the return of the asset class by its allocation within the portfolio). As investors might expect given the volatility across commodities and the energy sector, the Energy asset class was the largest detractor during the year at -1.91%.

1 The assets represented above were previously held by The Endowment Fund and were allocated to the PMF Fund on its inception date of April 1, 2014.

Source: Endowment Advisers, L.P., December 2015

Past performance is not indicative of future results. Performance is based on total return.

Fund Split and Liquidation Update

As you may recall, your interest in The Endowment Fund was moved to the PMF Fund effective as of April 1, 2014 after successful completion of the Investor Choice Plan (the “Plan”). As of the effective date of the split, the PMF Fund had over 6,000 investors and a total Net Asset Value (“NAV”) of approximately $1.72 billion. The Fund’s investment objective is to preserve portfolio value while prioritizing liquidity to investors over active management until the portfolio is fully liquidated. In doing so, the Fund has distributed more than $860 million to PMF investors since the split, which exceeds 50% of the 3/31/14 NAV. Distributions in 2015 totaled approximately $248 million or 14% of the original NAV.

The Fund will continue working to generate distributions for investors in 2016 under the terms of the Plan. The liquid hedge fund portfolio has been liquidated with the exception of a single fund. We anticipate receiving all remaining capital from this fund prior to year end 2016. In addition, we are happy to report that the Fund’s illiquid portfolio was cash flow positive in 2015 and since the execution of the Plan, meaning it generated distributions in excess of capital calls. It is important to note that we expect a tapering of future distributions to investors as the Fund becomes increasingly illiquid and relies more heavily on private equity investments for cash generation. We appreciate your patience as the Fund passes liquidity through to investors as soon as it becomes available and thank you for your continued support. If you have any questions, please do not hesitate to call our service desk at 1-800-725-9456.

Kindest Regards,

Endowment Advisers, L.P.2

2 This letter is provided solely for informational purposes and is exclusively intended for use by existing Fund investors and/or pre-qualified prospective Fund investors with whom the Fund or an authorized intermediary acting on behalf of the Fund has a pre-existing substantive relationship. No other distribution or use of this newsletter has been authorized. Neither this letter nor the information contained therein constitutes an offer to sell or a solicitation of any offer to buy any securities. Any offering or solicitation will be made only to eligible investors and pursuant to the current version of the applicable Private Placement Memorandum and other governing documents, all of which must be read in their entirety

Report of Independent Registered Public Accounting Firm

The Partners and Board of Directors

The Endowment PMF Master Fund, L.P.:

We have audited the accompanying statement of assets, liabilities and partners’ capital of The Endowment PMF Master Fund, L.P. (the “PMF Master Fund”), including the schedule of investments, as of December 31, 2015, and the related statements of operations and cash flows for the year then ended, and the statements of changes in partners’ capital and the financial highlights for the year then ended and the period from March 31, 2014 (commencement of operations) through December 31, 2014. These financial statements and financial highlights are the responsibility of the PMF Master Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audit.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of December 31, 2015, by correspondence with custodians and investees or other appropriate auditing procedures. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the PMF Master Fund as of December 31, 2015, and the results of its operations and cash flows for the year ended, and the changes in its partners’ capital and the financial highlights for the year then ended and the period from March 31, 2014 through December 31, 2014 in conformity with U.S. generally accepted accounting principles.

/s/ KPMG LLP

Columbus, Ohio

February 29, 2016

1

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Statement of Assets, Liabilities and Partners’ Capital

December 31, 2015

| Assets |

||||

| Investments in Investment Funds, at fair value (Cost $495,970,506) |

$ | 563,237,265 | ||

| Investments in affiliated Investment Funds, at fair value (Cost $391,808,760) |

390,701,263 | |||

|

|

|

|||

| Total investments |

953,938,528 | |||

| Cash and cash equivalents |

68,356,260 | |||

| Receivable from affiliate |

133,533 | |||

| Receivable from investments sold |

1,416,715 | |||

| Prepaids and other assets |

48,968 | |||

|

|

|

|||

| Total assets |

1,023,894,004 | |||

|

|

|

|||

| Liabilities and Partners’ Capital |

||||

| Withdrawals payable |

27,500,017 | |||

| Investment Management Fees payable |

1,036,659 | |||

| Offshore withholding tax payable |

13,432 | |||

| Administration fees payable |

267,750 | |||

| Accounts payable and accrued expenses |

397,316 | |||

|

|

|

|||

| Total liabilities |

29,215,174 | |||

|

|

|

|||

| Partners’ capital |

994,678,830 | |||

|

|

|

|||

| Total liabilities and partners’ capital |

$ | 1,023,894,004 | ||

|

|

|

See accompanying notes to financial statements.

2

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Schedule of Investments

December 31, 2015

| Shares | Fair Value |

% of Partners’ Capital | ||||||

| Investments in Investment Funds |

||||||||

| Limited Partnerships, Exempted Limited Partnerships and Limited Liability Companies |

||||||||

| British Virgin Islands |

||||||||

| Private Equity (0.06% of Partners’ Capital) |

||||||||

| Penta Asia Domestic Partners, L.P. |

$ | 612,216 | ||||||

|

|

|

|||||||

| Total British Virgin Islands |

612,216 | |||||||

|

|

|

|||||||

| Cayman Islands |

||||||||

| Energy (2.65% of Partners’ Capital) |

||||||||

| Sentient Global Resources Fund III, L.P. |

18,436,954 | |||||||

| Sentient Global Resources Fund IV, L.P. |

7,998,270 | |||||||

| Private Equity (24.72% of Partners’ Capital) |

||||||||

| ABRY Advanced Securities Fund, L.P. |

191,918 | |||||||

| CX Partners Fund Ltd(1)(2) |

29,630,190 | |||||||

| Gavea Investment Fund II A, L.P. |

692,468 | |||||||

| Gavea Investment Fund III A, L.P.(1) |

7,712,669 | |||||||

| Hillcrest Fund, L.P.(2) |

7,464,271 | |||||||

| India Asset Recovery Fund L.P. |

191,033 | |||||||

| J.C. Flowers III LP(1) |

12,420,515 | |||||||

| LC Fund IV, L.P.(1)(2) |

22,285,659 | |||||||

| New Horizon Capital III, L.P.(1) |

25,404,198 | |||||||

| Northstar Equity Partners III(1) |

5,535,280 | |||||||

| Orchid Asia IV, L.P.(1) |

4,006,000 | |||||||

| Reservoir Capital Partners (Cayman), L.P. |

6,679,394 | |||||||

| Tiger Global Private Investment Partners IV, L.P.(1) |

8,712,701 | |||||||

| Tiger Global Private Investment Partners V, L.P.(1) |

19,941,138 | |||||||

| Tiger Global Private Investment Partners VI, L.P. |

12,246,684 | |||||||

| Trustbridge Partners II, L.P.(1) |

24,340,769 | |||||||

| Trustbridge Partners III, L.P.(1)(2) |

36,043,435 | |||||||

| Trustbridge Partners IV, L.P.(1) |

22,399,808 | |||||||

| Real Estate (1.40% of Partners’ Capital) |

||||||||

| Forum European Realty Income III, L.P.(1) |

9,493,111 | |||||||

| Phoenix Asia Real Estate Investments II, L.P.(1) |

4,460,741 | |||||||

|

|

|

|||||||

| Total Cayman Islands |

286,287,206 | |||||||

|

|

|

|||||||

| Guernsey |

||||||||

| Private Equity (0.47% of Partners’ Capital) |

||||||||

| Mid Europa Fund III LP(1) |

4,642,749 | |||||||

|

|

|

|||||||

| Total Guernsey |

4,642,749 | |||||||

|

|

|

|||||||

| United Kingdom |

||||||||

| Private Equity (0.43% of Partners’ Capital) |

||||||||

| Darwin Private Equity I L.P.(1) |

4,287,328 | |||||||

See accompanying notes to financial statements.

3

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Schedule of Investments, continued

December 31, 2015

| Shares | Fair Value |

% of Partners’ Capital | ||||||||

| Limited Partnerships, Exempted Limited Partnerships and Limited |

||||||||||

| United Kingdom (continued) |

||||||||||

| Real Estate (0.44% of Partners’ Capital) |

||||||||||

| Benson Elliott Real Estate Partners II, L.P.(1) |

$ | 867,925 | ||||||||

| Patron Capital, L.P. II(1) |

291,008 | |||||||||

| Patron Capital, L.P. III |

3,173,552 | |||||||||

|

|

|

|||||||||

| Total United Kingdom |

8,619,813 | |||||||||

|

|

|

|||||||||

| United States |

||||||||||

| Energy (13.79% of Partners’ Capital) |

||||||||||

| ArcLight Energy Partners Fund IV, L.P.(1) |

2,097,362 | |||||||||

| ArcLight Energy Partners Fund V, L.P.(1) |

3,604,729 | |||||||||

| CamCap Resources, L.P. |

13,024 | |||||||||

| EnCap Energy Capital Fund VII-B LP(1) |

2,182,895 | |||||||||

| EnCap Energy Infrastructure TE Feeder, L.P.(1)(2) |

2,564,049 | |||||||||

| Energy & Minerals Group Fund II, L.P.(1) |

16,858,460 | |||||||||

| Intervale Capital Fund, L.P.(1) |

4,383,465 | |||||||||

| Merit Energy Partners G, L.P.(1) |

16,294,380 | |||||||||

| Midstream & Resources Follow-On Fund, L.P.(1)(2) |

18,672,633 | |||||||||

| NGP Energy Technology Partners II, L.P.(1) |

5,267,138 | |||||||||

| NGP IX Offshore Fund, L.P.(1) |

8,281,244 | |||||||||

| NGP Midstream & Resources, L.P.(1) |

12,435,463 | |||||||||

| Quantum Parallel Partners V, L.P.(2) |

35,298,012 | |||||||||

| Tenaska Power Fund II-A, L.P.(1)(2) |

9,203,767 | |||||||||

| Event-Driven (6.25% of Partners’ Capital) |

||||||||||

| BDCM Partners I, L.P.(2) |

19,217,724 | |||||||||

| Credit Distressed Blue Line Fund, L.P.(3) |

11,778,713 | |||||||||

| Fortelus Special Situations Fund LP(2) |

3,041,847 | |||||||||

| Harbinger Capital Partners Fund I, L.P.(3) |

22,590,602 | |||||||||

| Harbinger Capital Partners Fund II, L.P. |

1,698,874 | |||||||||

| Harbinger Capital Partners Special Situations Fund, L.P. |

1,878,293 | |||||||||

| Harbinger Class L Holdings (U.S.), LLC |

59,759 | |||||||||

| Harbinger Class LS Holdings (U.S.) Trust |

3,225 | 594,027 | ||||||||

| Harbinger Class PE Holdings (U.S.) Trust |

4 | 812,763 | ||||||||

| Prospect Harbor Credit Partners LP |

463,588 | |||||||||

| Global Macro and Trading (1.16% of Partners’ Capital) |

||||||||||

| Blueshift Energy Fund, LP(1)(2) |

11,484,358 | |||||||||

| Passport Global Strategies III Ltd.(2) |

629 | 35,472 | ||||||||

| Private Equity (32.51% of Partners’ Capital) |

||||||||||

| Advent Latin American Private Equity Fund IV-F L.P. |

2,750,763 | |||||||||

| Advent Latin American Private Equity Fund V-F L.P. |

9,701,192 | |||||||||

See accompanying notes to financial statements.

4

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Schedule of Investments, continued

December 31, 2015

| Shares | Fair Value |

% of Partners’ Capital | ||||||||

| Limited Partnerships, Exempted Limited Partnerships and Limited |

||||||||||

| United States (continued) |

||||||||||

| Private Equity (32.51% of Partners’ Capital) (continued) |

||||||||||

| BDCM Opportunity Fund II, L.P.(1) |

$ | 8,850,602 | ||||||||

| Black River Commodity Multi-Strategy Fund LLC(1) |

112,219 | |||||||||

| Capital Royalty Partners LP(1) |

750,786 | |||||||||

| Catterton Growth Partners, L.P. |

14,990,173 | |||||||||

| CCM Small Cap Value Qualified Fund, L.P.(3) |

331,307 | |||||||||

| Chrysalis Ventures III, L.P. |

2,039,614 | |||||||||

| Crosslink Crossover Fund IV, L.P. |

397,248 | |||||||||

| Crosslink Crossover Fund V, L.P. |

2,793,526 | |||||||||

| Crosslink Crossover Fund VI, L.P. |

17,269,823 | |||||||||

| Dace Ventures I, LP(2) |

1,102,813 | |||||||||

| Fairhaven Capital Partners, L.P. |

9,251,816 | |||||||||

| Founders Fund III, LP |

22,599,468 | |||||||||

| Founders Fund IV, LP |

27,409,610 | |||||||||

| Garrison Opportunity Fund II A LLC |

9,955,000 | |||||||||

| Garrison Opportunity Fund LLC(2) |

9,320,237 | |||||||||

| HealthCor Partners Fund, L.P.(2) |

7,800,095 | |||||||||

| Highland Credit Strategies Liquidation Vehicle Onshore |

1,526,207 | |||||||||

| Ithan Creek Partners, L.P. |

6,690,050 | |||||||||

| L-R Global Partners, L.P. |

342,018 | |||||||||

| MatlinPatterson Global Opportunities Partners III L.P.(1) |

7,984,274 | |||||||||

| Middle East North Africa Opportunities Fund, L.P.(1)(3) |

3,969 | 361,769 | ||||||||

| Monomoy Capital Partners II, L.P. |

9,046,815 | |||||||||

| Monomoy Capital Partners, L.P. |

1,392,536 | |||||||||

| Pine Brook Capital Partners, L.P.(1) |

14,423,204 | |||||||||

| Pinto America Growth Fund, L.P.(1) |

2,130,248 | |||||||||

| Private Equity Investment Fund IV, L.P.(1)(2) |

4,537,416 | |||||||||

| Private Equity Investment Fund V. L.P.(1)(2) |

38,234,588 | |||||||||

| Saints Capital VI, L.P.(2) |

6,678,948 | |||||||||

| Sanderling Venture Partners VI Co-Investment Fund, L.P. |

952,234 | |||||||||

| Sanderling Venture Partners VI, L.P. |

1,002,082 | |||||||||

| Sterling Capital Partners II, L.P.(1) |

608,138 | |||||||||

| Sterling Group Partners II, L.P. |

82,806 | |||||||||

| Sterling Group Partners III, L.P. |

14,278,646 | |||||||||

| Strategic Value Global Opportunities Fund I-A, L.P. |

673,055 | |||||||||

| TAEF Fund, LLC |

1,743,896 | |||||||||

| Tenaya Capital V, LP |

3,837,000 | |||||||||

| Tenaya Capital VI, LP |

6,920,000 | |||||||||

| The Column Group, L.P. |

14,715,900 | |||||||||

| The Raptor Private Holdings L.P. |

1,209 | 619,076 | ||||||||

See accompanying notes to financial statements.

5

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Schedule of Investments, continued

December 31, 2015

| Shares | Fair Value |

% of Partners’ Capital |

||||||||

| Limited Partnerships, Exempted Limited Partnerships and Limited |

||||||||||

| United States (continued) |

||||||||||

| Private Equity (32.51% of Partners’ Capital) (continued) |

||||||||||

| Trivest Fund IV, L.P.(1)(2) |

$ | 11,968,255 | ||||||||

| Tuckerbrook SB Global Distressed Fund I, L.P.(2) |

3,488,413 | |||||||||

| Valiant Capital Partners LP |

3,573,808 | |||||||||

| VCFA Private Equity Partners IV, L.P.(1) |

588,073 | |||||||||

| VCFA Venture Partners V, L.P.(1) |

1,960,330 | |||||||||

| Voyager Capital Fund III, L.P. |

2,862,937 | |||||||||

| WestView Capital Partners II, L.P.(1)(2) |

12,678,050 | |||||||||

| Real Estate (8.07% of Partners’ Capital) |

||||||||||

| Aslan Realty Partners III, L.L.C.(1) |

111,370 | |||||||||

| Cypress Realty VI Limited Partnership |

4,187,820 | |||||||||

| Florida Real Estate Value Fund, L.P.(1)(2) |

4,821,321 | |||||||||

| GTIS Brazil Real Estate Fund (Brazilian Real) LP(1)(2) |

11,028,692 | |||||||||

| Lone Star Real Estate Fund II (U.S.), L.P. |

1,626,822 | |||||||||

| Monsoon Infrastructure & Realty Co-Invest, L.P.(1)(2) |

14,949,328 | |||||||||

| Northwood Real Estate Co-Investors LP(1) |

4,667,305 | |||||||||

| Northwood Real Estate Partners LP(1) |

9,569,048 | |||||||||

| Parmenter Realty Fund III, L.P.(1) |

928,280 | |||||||||

| Parmenter Realty Fund IV, L.P.(1) |

6,519,562 | |||||||||

| Pearlmark Mezzanine Realty Partners III, L.L.C.(1) |

4,562,800 | |||||||||

| Pennybacker II, LP(1)(2) |

3,473,638 | |||||||||

| SBC Latin America Housing US Fund, LP(2) |

9,093,736 | |||||||||

| Square Mile Partners III LP(1) |

4,751,031 | |||||||||

| Relative Value (2.69% of Partners’ Capital) |

||||||||||

| Eton Park Fund, L.P. |

1,825,625 | |||||||||

| King Street Capital, L.P. |

863,964 | |||||||||

| Magnetar Capital Fund LP(2) |

2,450,904 | |||||||||

| Magnetar SPV LLC(2) |

289,771 | |||||||||

| OZ Asia Domestic Partners, LP(1) |

1,502,558 | |||||||||

| PIPE Equity Partners LLC(3) |

4,474,749 | |||||||||

| PIPE Select Fund LLC(3) |

14,306,501 | |||||||||

| Stark Investments Ltd Partnership(1) |

42,740 | |||||||||

| Stark Select Asset Fund, LLC |

951,245 | |||||||||

|

|

|

|||||||||

| Total United States |

641,138,515 | |||||||||

|

|

|

|||||||||

| Total Limited Partnerships, Exempted Limited Partnerships and Limited Liability Companies |

941,300,499 | 94.64% | ||||||||

|

|

|

|||||||||

See accompanying notes to financial statements.

6

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Schedule of Investments, continued

December 31, 2015

| Shares | Fair Value |

% of Partners’ Capital |

||||||||||

| Passive Foreign Investment Companies |

||||||||||||

| Cayman Companies Limited by Shares, Exempted Companies and Limited Liability Companies |

||||||||||||

| Energy (0.11% of Partners’ Capital) |

||||||||||||

| Ospraie Special Opportunities (Offshore) Ltd. |

$ | 1,135,214 | ||||||||||

| Private Equity (0.04% of Partners’ Capital) |

||||||||||||

| Quorum Fund Ltd |

8,762 | 375,589 | ||||||||||

| Relative Value (0.44% of Partners’ Capital) |

||||||||||||

| CRC Credit Fund Ltd. |

47,458 | 4,375,664 | ||||||||||

|

|

|

|||||||||||

| Total Cayman Companies Limited by Shares, Exempted Companies and Limited Liability Companies |

5,886,467 | |||||||||||

|

|

|

|||||||||||

| Total Passive Foreign Investment Companies |

5,886,467 | 0.59% | ||||||||||

|

|

|

|||||||||||

| Private Corporations |

||||||||||||

| United States |

||||||||||||

| Real Estate (0.68% of Partners’ Capital) |

||||||||||||

| Legacy Partners Realty Fund II, Inc. |

1,014,661 | |||||||||||

| Legacy Partners Realty Fund III, Inc. |

4,940,441 | |||||||||||

| Net Lease Private REIT VI, Inc. |

189,365 | |||||||||||

| Net Lease Private REIT VII, Inc. |

303,549 | |||||||||||

| Net Lease Private REIT VII-A, Inc. |

303,546 | |||||||||||

|

|

|

|||||||||||

| Total Private Corporations |

6,751,562 | 0.68% | ||||||||||

|

|

|

|||||||||||

| Total Investments in Investment Funds |

953,938,528 | 95.91% | ||||||||||

|

|

|

|||||||||||

| Total Investments (Cost $887,779,266) |

$ | 953,938,528 | 95.91% | |||||||||

|

|

|

|||||||||||

The Master Fund’s total outstanding capital commitments to Investment Funds as of December 31, 2015 were $111,715,376. For certain Investment Funds for which the Master Fund has a capital commitment, the Master Fund may be allocated its pro-rata share of expenses prior to having to fund a capital call for such expenses.

| All | Investment Funds and securities are non-income producing unless noted otherwise. |

| (1) | Income producing investment |

| (2) | Affiliated investments (See Note 5b) |

| (3) | Affiliated investments for which ownership exceeds 25% of the Investment Fund’s Capital (See Note 5b) |

See accompanying notes to financial statements.

7

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Statement of Operations

Year Ended December 31, 2015

| Investment income: |

||||

| Dividend income (net of foreign tax withholding of $1,651) |

$ | 6,880,162 | ||

| Interest income |

453,045 | |||

| Dividend income from affiliated investments |

8,769,954 | |||

|

|

|

|||

| Total investment income |

16,103,161 | |||

|

|

|

|||

| Expenses: |

||||

| Investment Management Fees |

6,996,684 | |||

| Administration fees |

663,572 | |||

| Professional fees |

369,002 | |||

| Commitment fees |

252,360 | |||

| Custodian fees |

123,034 | |||

| Directors fees |

98,502 | |||

| Offshore withholding tax expense |

1,031,749 | |||

| Other expenses |

307,513 | |||

|

|

|

|||

| Total expenses |

9,842,416 | |||

|

|

|

|||

| Net investment income |

6,260,745 | |||

|

|

|

|||

| Net realized and unrealized gain (loss): |

||||

| Net realized gain from investments and foreign currency translations |

71,247,384 | |||

| Net realized gain from redemptions in-kind |

900,731 | |||

| Net realized gain from affiliated investments |

29,208,025 | |||

| Change in unrealized appreciation/depreciation |

(69,563,575 | ) | ||

|

|

|

|||

| Net realized and unrealized gain |

31,792,565 | |||

|

|

|

|||

| Net increase in partners’ capital resulting from operations |

$ | 38,053,310 | ||

|

|

|

See accompanying notes to financial statements.

8

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Statement of Changes in Partners’ Capital

For the Period March 31, 2014 through December 31, 20141

and Year Ended December 31, 2015

| Partners’ capital at March 31, 2014 |

$ | — | ||

| Contributions |

539,387,194 | |||

| Transfer of Interests from The Endowment Master Fund, L.P. (Note 1) |

1,723,272,229 | |||

| Withdrawals |

(1,150,900,544 | ) | ||

| Net increase in partners’ capital resulting from operations: |

||||

| Net investment loss |

(11,275,595 | ) | ||

| Net realized gain from investments and foreign currency translations |

120,508,262 | |||

| Net realized gain from redemptions in-kind |

1,544,898 | |||

| Net realized gain from affiliated investments |

24,127,574 | |||

| Change in unrealized appreciation/depreciation |

(37,736,366 | ) | ||

|

|

|

|||

| Net increase in partners’ capital resulting from operations |

97,168,773 | |||

|

|

|

|||

| Partners’ capital at December 31, 2014 |

$ | 1,208,927,652 | ||

| Contributions |

65,889 | |||

| Withdrawals |

(252,368,021 | ) | ||

| Net increase in partners’ capital resulting from operations: |

||||

| Net investment income |

6,260,745 | |||

| Net realized gain from investments and foreign currency translations |

71,247,384 | |||

| Net realized gain from redemptions in-kind |

900,731 | |||

| Net realized gain from affiliated investments |

29,208,025 | |||

| Change in unrealized appreciation/depreciation |

(69,563,575 | ) | ||

|

|

|

|||

| Net increase in partners’ capital resulting from operations |

38,053,310 | |||

|

|

|

|||

| Partners’ capital at December 31, 2015 |

$ | 994,678,830 | ||

|

|

|

| 1 | The Endowment PMF Master Fund, L.P. commenced operations on March 31, 2014. |

See accompanying notes to financial statements.

9

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Statement of Cash Flows

For the year ended December 31, 2015

| Cash flows from operating activities: |

||||

| Net increase in partners’ capital resulting from operations |

$ | 38,053,310 | ||

| Adjustments to reconcile net increase in partners’ capital resulting from operations to net cash provided by operating activities: |

||||

| Purchases of investments |

(87,444,569 | ) | ||

| Proceeds from disposition of investments |

278,439,822 | |||

| Net realized gain from investments and foreign currency translations |

(71,247,384 | ) | ||

| Net realized gain from redemptions in-kind |

(900,731 | ) | ||

| Net realized gain from affiliated investments |

(29,208,025 | ) | ||

| Change in unrealized appreciation/depreciation from investments and foreign currency translations |

69,563,575 | |||

| Change in operating assets and liabilities: |

||||

| Foreign currency, at value |

3,449,077 | |||

| Receivable from affiliate |

325,258 | |||

| Receivable from investments sold |

35,140,948 | |||

| Receivable from affiliated investments sold |

36,602 | |||

| Prepaids and other assets |

35,958 | |||

| Investment Management Fees payable |

(1,198,007 | ) | ||

| Offshore withholding tax payable |

(334,300 | ) | ||

| Administration fees payable |

141,480 | |||

| Payable to Adviser |

(11,570 | ) | ||

| Accounts payable and accrued expenses |

(534,134 | ) | ||

|

|

|

|||

| Net cash provided by operating activities |

234,307,310 | |||

|

|

|

|||

| Cash flows from financing activities: |

||||

| Contributions |

65,889 | |||

| Withdrawals |

(277,532,809 | ) | ||

|

|

|

|||

| Net cash used in financing activities |

(277,466,920 | ) | ||

|

|

|

|||

| Effect of exchange rate changes in cash |

(633,667 | ) | ||

|

|

|

|||

| Net change in cash and cash equivalents |

(43,159,610 | ) | ||

| Cash and cash equivalents at beginning of year |

112,149,537 | |||

|

|

|

|||

| Cash and cash equivalents at end of year |

$ | 68,356,260 | ||

|

|

|

|||

| Supplemental schedule of cash activity: |

||||

| Cash paid for interest |

252,360 | |||

| Supplemental schedule of non-cash activity: |

||||

| Redemptions in-kind (cost $42,498,518) |

43,399,249 |

See accompanying notes to financial statements.

10

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Notes to Financial Statements

December 31, 2015

(1) ORGANIZATION

The Endowment PMF Master Fund, L.P. (the “Master Fund”), a Delaware limited partnership, commenced operations on March 31, 2014. The Master Fund is registered as a non-diversified, closed-end management investment company under the Investment Company Act of 1940, as amended (the “1940 Act”). The Master Fund is the master fund in a master-feeder structure in which there are currently three feeder funds.

On March 31, 2014 the Master Fund received in an in-kind transfer a portfolio of investment funds including, but not limited to, limited partnerships, limited liability companies, offshore corporations and other foreign investment vehicles (collectively, the “Investment Funds”) from The Endowment Master Fund, L.P. (the “Legacy Master Fund”), in exchange for limited partnership interests (the “Interests”) of the Master Fund totaling $1,723,272,229. The transfer was accounted for as a tax-free transaction resulting in Investment Funds transferring to the Master Fund with a total fair value of $1,490,836,309, consisting of total cost and accumulated appreciation of $1,317,376,887 and $173,459,422, respectively, and cash and other assets of $232,435,920.

The Master Fund’s investment objective is to manage a portfolio of Investment Funds and cash to preserve value while prioritizing liquidity to investors over active management, until such time as the Master Fund’s portfolio has been liquidated. The Master Fund holds a portfolio of Investment Funds, reflecting an approximate pro rata division of the portfolio of the Legacy Master Fund, managed in a broad range of investment strategies and asset categories. The Adviser, as hereinafter defined, manages the Master Fund portfolio primarily in a passive manner whereby the Master Fund holds to self-liquidating private equity and other similar illiquid interests in Investment Funds and oversees the liquidation of other Investment Funds that provide for redemption while managing the Master Fund’s cash to ensure the Master Fund has the ability to satisfy outstanding capital commitments relating to such portfolio holdings.

The Endowment Fund GP, L.P., a Delaware limited partnership, serves as the general partner of the Master Fund and the Legacy Master Fund (the “General Partner”). To the fullest extent permitted by applicable law, the General Partner has irrevocably delegated to a board of directors (the “Board” and each member a “Director”) its rights and powers to monitor and oversee the business affairs of the Master Fund, including the complete and exclusive authority to oversee and establish policies regarding the management, conduct, and operation of the Master Fund’s business. A majority of the members of the Board are independent of the General Partner and its management. To the extent permitted by applicable law, the Board may delegate any of its rights, powers and authority to, among others, the officers of the Master Fund, the Adviser, or any committee of the Board.

The Board is authorized to engage an investment adviser, and pursuant to an investment management agreement, (the “Investment Management Agreement”), it has selected Endowment Advisers, L.P. (the “Adviser”), to manage the Master Fund’s portfolio and operations. The Adviser is a Delaware limited partnership that is registered as an investment adviser under the Investment Advisers Act of 1940, as amended. Under the Investment Management Agreement, the Adviser is responsible for the establishment of an investment committee (the “Investment Committee”), which is responsible for developing, implementing, and supervising the Master Fund’s investment program subject to the ultimate supervision of the Board.

Under the Master Fund’s organizational documents, the Master Fund’s Directors and officers are indemnified against certain liabilities arising out of the performance of their duties to the Master Fund. In the normal course of business, the Master Fund enters into contracts with service providers, which also provide for indemnifications by the Master Fund. The Master Fund’s maximum exposure under these arrangements is

11

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Notes to Financial Statements, continued

December 31, 2015

unknown, as this would involve any future potential claims that may be made against the Master Fund. However, based on experience, the General Partner expects that risk of loss to be remote.

(2) SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES AND PRACTICES

(a) BASIS OF ACCOUNTING

The accounting and reporting policies of the Master Fund conform with U.S. generally accepted accounting principles (“U.S. GAAP”). The accompanying financial statements reflect the financial position of the Master Fund and the results of its operations. The Master Fund is an investment company and follows the investment company accounting and reporting guidance under Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, “Financial Services-Investment Companies”.

(b) CASH EQUIVALENTS

The Master Fund considers all unpledged temporary cash investments with a maturity date at the time of purchase of three months or less to be cash equivalents.

(c) INVESTMENT SECURITIES TRANSACTIONS

The Master Fund records investment transactions on a trade-date basis.

Investments that are held by the Master Fund, including those that have been sold short, are marked to fair value at the date of the financial statements, and the corresponding change in unrealized appreciation/ depreciation is included in the Statement of Operations.

Dividend income is recorded on the ex-dividend date. Other investment fund distributions are recorded based on the detail provided with the distribution notice, as applicable. Realized gains or losses on the disposition of investments are accounted for based on the first in first out method.

(d) INVESTMENT VALUATION

The valuation of the Master Fund’s investments is determined as of the close of business at the end of each reporting period, generally monthly. The valuation of the Master Fund’s investments is calculated by UMB Fund Services, Inc., the Master Fund’s independent administrator (the “Administrator”).

The Board has formed a valuation committee (the “Board Valuation Committee”) that is responsible for overseeing the Master Fund’s valuation policies, making recommendations to the Board on valuation-related matters, and overseeing implementation by the Adviser of such valuation policies.

The Board has authorized the Adviser to establish a valuation committee of the Adviser (the “Adviser Valuation Committee”). The Adviser Valuation Committee’s function, subject to the oversight of the Board Valuation Committee and the Board, is generally to review valuation methodologies, valuation determinations, and any information provided to the Adviser Valuation Committee by the Adviser or the Administrator.

12

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Notes to Financial Statements, continued

December 31, 2015

The Master Fund is not able to obtain complete underlying investment holding details on each of the Investment Funds in order to determine if the Master Fund’s proportional, aggregated, indirect share of any investments held by the Investment Funds exceeds 5% of partners’ capital of the Master Fund as of December 31, 2015.

Investments held by the Master Fund are valued as follows:

| • | INVESTMENT FUNDS—Investments in Investment Funds are carried at fair value, using the net asset value (the “NAV”) as a practical expedient, as provided to the Administrator by the investment managers of such Investment Funds or the administrators of such Investment Funds. These Investment Funds value their underlying investments in accordance with policies established by such Investment Funds. Prior to investing in any Investment Fund, the Adviser Valuation Committee, as part of the due diligence process, conducts a review of the valuation methodologies employed by the Investment Fund to determine whether such methods are appropriate for the asset types. All of the Master Fund’s valuations utilize financial information supplied by each Investment Fund and are net of management and estimated performance incentive fees or allocations payable to the Investment Funds’ managers pursuant to the Investment Funds’ agreements. Generally, Investment Funds in which the Master Fund invests will use market value when available, and otherwise will use principles of fair value applied in good faith. The Adviser Valuation Committee will consider whether it is appropriate, in light of the relevant circumstances, to value shares at NAV as reported by an Investment Fund for valuation purposes, or whether to adjust such reported value to reflect an adjusted fair value. Because of the inherent uncertainty of valuation, fair value may differ significantly from the value that would have been used had readily available markets for the investments in Investment Funds existed. The Master Fund’s investments in Investment Funds are subject to the terms and conditions of the respective operating agreements and offering memoranda of such Investment Funds. |

| • | OTHER—Investments in open-end registered investment companies (“RICs”) that do not trade on an exchange are valued at the end of day NAV per share and are categorized as Level 1 in the fair value hierarchy. Where no value is readily available from a RIC or other security, or where a value supplied by a RIC is deemed not to be indicative of the RIC’s value, the Adviser Valuation Committee and/or the Board Valuation Committee, in consultation with the Administrator or the Adviser, will determine, in good faith, the fair value of the RIC or other security. Such fair valued investments are typically categorized as Level 1 or Level 2 in the fair value hierarchy, based upon the inputs used to value the investments. |

| • | SECURITIES NOT ACTIVELY TRADED—The value of securities, derivatives or synthetic securities that are not actively traded on an exchange shall be determined by obtaining quotes from brokers that normally deal in such securities or by an unaffiliated pricing service that may use actual trade data or procedures using market indices, matrices, yield curves, specific trading characteristics of certain groups of securities, pricing models or a combination of these procedures pursuant to the valuation procedures approved by the Board. In each of these situations, valuations are typically categorized as Level 2 or Level 3 in the fair value hierarchy, based upon the inputs used to value the investments. |

(e) FOREIGN CURRENCY

The accounting records of the Master Fund are maintained in U.S. dollars. Foreign currency amounts and investments denominated in a foreign currency, if any, are translated into U.S. dollar amounts at current exchange rates on the valuation date. Purchases and sales of investments denominated in foreign currencies are

13

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Notes to Financial Statements, continued

December 31, 2015

translated into U.S. dollar amounts at the exchange rate on the respective dates of such transactions. The Master Fund does not isolate the portion of the results of operations resulting from changes in foreign exchange rates on investments from fluctuations arising from changes in market prices of securities held. Such fluctuations are included with the net realized and unrealized gain or loss from investments and foreign currency translations.

(f) CFTC REGULATION

On August 13, 2013, the Commodity Futures Trading Commission (“CFTC”) adopted rules to harmonize conflicting Securities and Exchange Commission (the “SEC”) and CFTC disclosure, reporting and recordkeeping requirements for RICs that do not meet an exemption from the definition of commodity pool. The harmonization rules provide that the CFTC will accept the SEC’s disclosure, reporting, and recordkeeping regime as substituted compliance for substantially all of the otherwise applicable CFTC regulations as long as such investment companies meet the applicable SEC requirements.

Previously, in November 2012, the CFTC issued relief for fund of fund operators, including advisers to RIC’s, that may otherwise be required to register with the CFTC as commodity pool operators but do not have access to information from the investment funds in which they are invested in order to determine whether such registration is required. This relief delayed the registration date for such operators until the later of June 30, 2013 or six months from the date the CFTC issues revised guidance on the application of certain thresholds with respect to investments in commodities held by funds of funds. In December 2012, the Master Fund filed as required with the CFTC in order to claim this no-action relief, which was effective upon receipt of the filing. Although the CFTC now has adopted harmonization rules applicable to investment companies that are deemed to be commodity pools, the CFTC has not yet issued guidance on how funds of funds are to determine whether they are deemed to be commodity pools. As of December 31, 2015, the Master Fund is not considered a commodity pool and continues to rely on the fund of fund no-action relief.

(g) INVESTMENT INCOME

For investments in securities, dividend income is recorded on the ex-dividend date, net of withholding taxes. Interest income is recorded as earned on the accrual basis and includes amortization of premiums or accretion of discounts.

(h) FUND EXPENSES

Unless otherwise voluntarily or contractually assumed by the Adviser or another party, the Master Fund bears all expenses incurred in its business including, but not limited to, the following: all costs and expenses related to investment transactions and positions for the Master Fund’s account; legal fees; accounting, auditing and tax preparation fees; recordkeeping and custodial fees; costs of computing the Master Fund’s net asset value; fees for data and software providers; research expenses; costs of insurance; registration expenses; expenses of meetings of partners; directors fees; all costs with respect to communications to partners; transfer taxes; offshore withholding taxes; and other types of expenses as may be approved from time to time by the Board.

(i) INCOME TAXES

The Master Fund is organized and operates as a limited partnership and is not subject to income taxes as a separate entity. Such taxes are the responsibility of the individual partners. Accordingly, no provision for income

14

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Notes to Financial Statements, continued

December 31, 2015

taxes has been made in the Master Fund’s financial statements. Investments in foreign securities may result in foreign taxes being withheld by the issuer of such securities. For U.S. offshore withholding tax, the Master Fund may serve as withholding agent for its offshore feeder funds.

For the tax years ended December 31, 2014 and December 31, 2015, and for all major jurisdictions, management of the Master Fund has evaluated the tax positions taken or expected to be taken in the course of preparing the Master Fund’s tax returns to determine whether the tax positions will “more-likely-than-not” be sustained by the Master Fund upon challenge by the applicable tax authority. Tax positions not deemed to meet the more-likely-than-not threshold and that would result in a tax benefit or expense to the Master Fund would be recorded as a tax benefit or expense in the current period. For the year ended December 31, 2015, the Master Fund did not recognize any amounts for unrecognized tax benefit/expense. A reconciliation of unrecognized tax benefit/expense is not provided herein, as the beginning and ending amounts of unrecognized tax benefit/expense are zero, with no interim additions, reductions or settlements. Tax positions taken in tax years which remain open under the statute of limitations (generally three years for federal income tax purposes) are subject to examination by federal and state tax jurisdictions.

(j) USE OF ESTIMATES

The financial statements have been prepared in conformity with U.S. GAAP, which requires management to make estimates and assumptions relating to the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results may differ from those estimates and such differences may be significant.

(3) FAIR VALUE MEASUREMENTS

The Master Fund defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date under current market conditions.

The inputs used to determine the fair value of the Master Fund’s investments are summarized in the three broad levels listed below:

| • | Level 1—unadjusted quoted prices in active markets for identical investments and registered investment companies where the value per share (unit) is determined and published and is the basis for current transactions for identical assets or liabilities at the valuation date |

| • | Level 2—investments with other significant observable inputs |

| • | Level 3—investments with significant unobservable inputs (which may include the Master Fund’s own assumptions in determining the fair value of investments) |

Changes in valuation techniques may result in transfers in or out of an assigned level within the disclosure hierarchy. The Master Fund discloses transfers between levels based on valuations at the end of the reporting period. The inputs or methodology used for valuing investments are not necessarily an indication of the risk associated with investing in those investments.

15

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Notes to Financial Statements, continued

December 31, 2015

The Master Fund establishes valuation processes and procedures to ensure that the valuation techniques for investments categorized within Level 3 of the fair value hierarchy are fair, consistent, and appropriate. The Adviser is responsible for developing the Master Fund’s written valuation processes and procedures, conducting periodic reviews of the valuation policies, and evaluating the overall fairness and consistent application of the valuation policies. The Board Valuation Committee has authorized the Adviser to oversee the implementation of the Board approved valuation procedures by the Administrator. The Adviser Valuation Committee is comprised of various Master Fund personnel, which include members from the Master Fund’s portfolio management and operations groups. The Adviser Valuation Committee meets monthly or as needed, to determine the valuations of the Master Fund’s Level 3 investments. The valuations are supported by methodologies employed by the Investment Funds’ market data, industry accepted third party valuation models, or other methods the Adviser Valuation Committee deems to be appropriate, including the use of internal proprietary valuation models.

In April 2015, Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) 2015-07, Disclosures for Investments in Certain Entities That Calculate Net Asset Value per Share (or Its Equivalent), modifying Accounting Standards Codification (“ASC”) 820 Fair Value Measurement. The Master Fund has elected to early adopt and retrospectively apply ASU 2015-07. The impact of the early adoption of ASU 2015-07 has been reflected in the notes to the financial statements. Prior to this, investments valued using the practical expedient were categorized within the fair value hierarchy on the basis of whether the investment is redeemable with the investee at net asset value on the measurement date, never redeemable with the investee at net asset value, or redeemable with the investee at net asset value at a future date. The retroactive application of ASU 2015-07 results in the exclusion of any Investment Funds valued using NAV as practical expedient from the investment roll forward included in the December 31, 2014 audited financial statements. As a result of adopting ASU 2015-07, Investment Funds with a fair value of $953,938,528 are excluded from the fair value hierarchy as of December 31, 2015. As of December 31, 2015, the Fund does not hold any investments that have to be included in the Level 3 fair value hierarchy.

The Master Fund is permitted to invest in alternative investments that may not have a readily determinable fair value. For an investment that does not have a readily determinable fair value, the Master Fund uses the NAV reported by the Investment Fund as a practical expedient, without further adjustment, unless it is probable that the investment will be sold at a value significantly different than the reported NAV. If the practical expedient NAV is not as of the reporting entity’s measurement date, then the NAV is adjusted to reflect any significant events that would materially affect the value of the investment and the NAV of the Master Fund as of the valuation date.

16

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Notes to Financial Statements, continued

December 31, 2015

Certain Investment Funds in which the Master Fund invests have limitations on liquidity which may result in limitations on redemptions including, but not limited to, early redemption fees. Other than Investment Funds that are self-liquidating, such as Private Equity and some Energy, Natural Resources and Real Estate Funds, the Investment Funds in which the Master Fund invests have withdrawal rights ranging from monthly to annually, after a notice period, usually for a period of up to two years from the date of the initial investment or an additional investment. A listing of the investments held by the Master Fund and their attributes as of December 31, 2015, that qualify for this valuation approach is shown in the table below.

| Investment Category | Investment Strategy | Fair Value (in 000s) |

Unfunded Commitments (in 000s) |

Remaining Life* |

Redemption Frequency* |

Notice Period (in Days)* |

Redemption Restrictions and Terms* | |||||||||||

| Energy (a) | Private investments in securities issued by companies in the energy and natural resources sectors. | $ | 164,727 | $ | 26,159 | up to 15 years |

N/A | N/A | 0-15 years | |||||||||

| Event-Driven(b) | Strategies designed to profit from changes in the prices of securities of companies facing a major corporate event. | 62,136 | N/A | N/A | Quarterly | 45-90 | 0-5 years; up to 2.5% early withdrawal fee; possible 25% investor level gate; illiquid side pocket capital | |||||||||||

| Global Macro and Trading(c) | Investments across global markets and security types seeking to profit from macroeconomic opportunities. Strategies can be discretionary or systematic. Includes Commodity Trading Advisers. | 11,520 | N/A | N/A | Quarterly | 30-90 | 0-5

years; up to 6% | |||||||||||

| Private Equity(d) | Investments in nonpublic companies. | 579,143 | 62,335 | up to 10 years |

N/A | N/A | 0-10 years | |||||||||||

17

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Notes to Financial Statements, continued

December 31, 2015

| Investment Category | Investment Strategy | Fair Value (in 000s) |

Unfunded Commitments (in 000s) |

Remaining Life* |

Redemption Frequency* |

Notice Period (in Days)* |

Redemption Restrictions and Terms* | |||||||||||

| Real Estate(e) | Investments in REITs, private partnerships, and various real estate related mortgage securities. | 105,329 | 23,221 | up to 10 years |

N/A | N/A | 0-10 years | |||||||||||

| Relative Value(f) | Strategies seeking to profit from inefficiencies existing within capital structures, within markets, and across markets. | 31,084 | N/A | N/A | Quarterly | 30-120 | 0-5 years; up to 7% early redemption fee; possible 5% fund level gate; illiquid side pocket capital | |||||||||||

| $ | 953,939 | $ | 111,715 | |||||||||||||||

|

|

|

|

|

|||||||||||||||

| * | The information summarized in the table above represents the general terms for the specified asset class. Individual Investment Funds may have terms that are more or less restrictive than those terms indicated for the asset class as a whole. In addition, most Investment Funds have the flexibility, as provided for in their constituent documents, to modify and waive such terms. |

| (a) | This category includes Investment Funds that invest primarily in privately issued securities by companies in the energy and natural resources sectors and private investments in energy-related assets or companies. The Investment Funds include private funds and private partnerships with private investments in their portfolios. |

| (b) | This category includes Investment Funds that invest primarily in the following securities: common stock, preferred stock, and many types of debt. Events include mergers, acquisitions, restructurings, spin-offs, and litigation. |

| (c) | This category includes Investment Funds that invest in global markets and across all security types including equities, fixed income, derivatives, commodities, currencies, futures, and exchange-traded funds. Investment Funds in this category are typically private funds and may include global macro funds, and commodity trading advisors. |

| (d) | This category includes private equity funds that invest primarily in non-publicly traded companies in need of capital. These Investment Funds may vary widely as to sector, size, stage, duration, and liquidity. Certain of these Investment Funds may also focus on the secondary market, buying interests in existing private equity funds, often at a discount. |

| (e) | This category includes Investment Funds that invest in registered investment companies or managers that invest in real estate trusts (commonly known as “REITs”) and private partnerships that make investments in income producing properties, raw land held for development or appreciation, and various types of mortgage loans and common or preferred stock whose operations involve real estate. |

| (f) | This category includes Investment Funds with low net exposure to most financial markets. Underlying strategies include Equity Market Neutral or Statistical Arbitrage, Capital Structure Arbitrage, Convertible Arbitrage, Volatility Arbitrage, and Credit Arbitrage. |

18

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Notes to Financial Statements, continued

December 31, 2015

(4) PARTNERS’ CAPITAL ACCOUNTS

(a) ISSUANCE OF INTERESTS

Interests of the Master Fund are generally available only to those investors who received Interests as in-kind repurchase proceeds for their tendered interests in one of the feeder funds to the Legacy Master Fund. Interests of the Master Fund will generally not otherwise be offered or sold.

(b) ALLOCATION OF PROFITS AND LOSSES

For each fiscal period, generally monthly, net profits or net losses of the Master Fund are allocated among and credited to or debited against the capital accounts of all partners as of the last day of each fiscal period in accordance with the partners’ respective capital account ownership percentage for the fiscal period. Net profits or net losses are measured as the net change in the value of the partners’ capital of the Master Fund, including any change in unrealized appreciation or depreciation of investments and income, net of expenses, and realized gains or losses during a fiscal period.

(c) REPURCHASE OF INTERESTS

A partner will not be eligible to have the Master Fund repurchase all or any portion of an Interest at the partner’s discretion at any time. Interests are not redeemable nor are they exchangeable for Interests or shares of any other fund.

The Master Fund anticipates making quarterly distributions pro rata to all investors in an amount equal to the Master Fund’s excess cash (“Excess Cash”). Excess Cash is defined as the amount of cash on hand over and above the amount necessary or prudent for operational and regulatory purposes (“Required Cash”). The amount of Required Cash is determined by the Adviser with oversight by the Board. Excess Cash is generally distributed in the subsequent quarter or quarters where the aggregate of Excess Cash from such subsequent quarter(s) and prior quarters exceeds a threshold of $10 million. Intra-quarter distributions may also be made if Excess Cash exceeds a threshold of $25 million as of the forty fifth day after the end of any quarter. The Master Fund may make in-kind distributions of portfolio securities as deemed necessary.

(5) INVESTMENTS IN PORTFOLIO SECURITIES

(a) INVESTMENT ACTIVITY

As of December 31, 2015 the Master Fund held investments in Investment Funds and securities. The agreements related to investments in Investment Funds provide for compensation to the Investment Funds’ managers/general partners or advisers in the form of management fees of up to 2.0% annually of monthly average net assets. In addition, many Investment Funds also provide for performance incentive fees/ allocations of up to 20% of an Investment Fund’s net profits, although it is possible that such ranges may be exceeded for certain investment managers. These management fees and incentive fees are in addition to the management fees charged by the Master Fund.

19

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Notes to Financial Statements, continued

December 31, 2015

During the year ended December 31, 2015, certain investments were received through a transfer-in-kind in connection with the redemption of certain investments. The fair value of these investments transferred-in-kind and related cost were as follows:

| Investments Redeemed |

Fair Value | Cost | Realized Gain (Loss) on Transfers In- Kind |

Unrealized Gain (Loss) on Transfers In- Kind |

Investments Received |

|||||||||||||||

| Tiger Global Private Investment Partners V, L.P. |

$ | 43,399,249 | $ | 42,498,518 | $ | 900,731 | $ | — | JD.com, Inc. | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||

| $ | 43,399,249 | $ | 42,498,518 | $ | 900,731 | $ | — | |||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||

For the year ended December 31, 2015, the aggregate cost of purchases and proceeds from sales of investments (excluding short-term investments) were $87,444,569 and $175,990,958, respectively.

The cost of the Master Fund’s underlying investments for Federal income tax purposes is adjusted for items of taxable income allocated to the Master Fund from such investments. The allocated taxable income is generally reported to the Master Fund by its underlying investments on Schedules K-1, Forms 1099 or PFIC statements, or a combination thereof.

The underlying investments generally do not provide the Master Fund with tax reporting information until well after year end, and as a result, the Master Fund is unable to calculate the year end tax cost of its investments until such time. The Master Fund’s book cost as of December 31, 2015, was $887,779,266, resulting in accumulated net unrealized appreciation of $66,159,262 consisting of $252,181,143 in gross unrealized appreciation and $186,021,881 in gross unrealized depreciation.

(b) AFFILIATED INVESTMENT FUNDS

At December 31, 2015, the Master Fund’s investments in certain Investment Funds were deemed to be investments in affiliated issuers under the 1940 Act, primarily because the Master Fund owns 5% or more of the Investment Funds’ total net assets. A listing of these affiliated Investment Funds (including activity during the year ended December 31, 2015) is shown below:

| Investment Funds |

Shares 12/31/2014 |

Shares 12/31/2015 |

Beginning Fair Value 12/31/2014 |

Cost of Purchases |

Cost of Sales* |

Realized Gain (Loss) on Investments |

Change in Unrealized Appreciation / Depreciation |

Ending Fair Value 12/31/2015 |

Interest/ Dividend Income |

|||||||||||||||||||||||

| BDCM Partners I, L.P. |

$ | 22,100,410 | $ | — | $ | (2,882,686 | ) | $ | 19,217,724 | $ | 497,302 | |||||||||||||||||||||

| Blueshift Energy Fund, LP |

31,172,637 | — | (11,735,506 | ) | 5,705 | (7,958,478 | ) | 11,484,358 | 961 | |||||||||||||||||||||||

| CCM Small Cap Value Qualified Fund, L.P. |

1,597,648 | — | (1,123,651 | ) | — | (142,690 | ) | 331,307 | — | |||||||||||||||||||||||

| Credit Distressed Blue Line Fund, L.P |

8,864,067 | — | — | — | 2,914,646 | 11,778,713 | — | |||||||||||||||||||||||||

| CX Partners Fund Ltd |

21,562,954 | 4,910,565 | (3,324,780 | ) | (43,683 | ) | 6,525,134 | 29,630,190 | 220,341 | |||||||||||||||||||||||

| Dace Ventures I, L.P. |

1,191,236 | 27,658 | — | 104,883 | (220,964 | ) | 1,102,813 | — | ||||||||||||||||||||||||

| EnCap Energy Infrastructure TE Feeder, L.P. |

3,765,890 | 326,630 | (104,327 | ) | 1,204,505 | (2,628,649 | ) | 2,564,049 | 45,072 | |||||||||||||||||||||||

| Florida Real Estate Value Fund, L.P. |

8,047,739 | — | (3,882,631 | ) | 506,047 | 150,166 | 4,821,321 | 821,499 | ||||||||||||||||||||||||

| Fortelus Special Situations Fund LP |

2,954,885 | — | (1,150,843 | ) | — | 1,237,805 | 3,041,847 | — | ||||||||||||||||||||||||

| Garrison Opportunity Fund LLC |

12,618,494 | 538,159 | (1,894,334 | ) | 1,492,378 | (3,434,460 | ) | 9,320,237 | — | |||||||||||||||||||||||

20

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Notes to Financial Statements, continued

December 31, 2015

| Investment Funds |

Shares 12/31/2014 |

Shares 12/31/2015 |

Beginning Fair Value 12/31/2014 |

Cost of Purchases |

Cost of Sales* |

Realized Gain (Loss) on Investments |

Change in Unrealized Appreciation / Depreciation |

Ending Fair Value 12/31/2015 |

Interest/ Dividend Income |

|||||||||||||||||||||||||||

| GTIS Brazil Real Estate Fund (Brazilian Real) LP |

$ | 16,718,472 | $ | — | $ | (34,234 | ) | $ | — | $ | (5,655,546 | ) | $ | 11,028,692 | $ | — | ||||||||||||||||||||

| Harbinger Capital Partners Fund I, L.P. |

14,495,648 | — | — | — | 8,094,954 | 22,590,602 | — | |||||||||||||||||||||||||||||

| HealthCor Partners Fund, L.P. |

8,050,383 | 126,564 | (51,740 | ) | — | (325,112 | ) | 7,800,095 | — | |||||||||||||||||||||||||||

| Hillcrest Fund, L.P. |

10,268,306 | 148,173 | (803,852 | ) | 790,142 | (2,938,498 | ) | 7,464,271 | — | |||||||||||||||||||||||||||

| LC Fund IV, L.P. |

19,930,273 | 307,951 | (97,694 | ) | 171,624 | 1,973,505 | 22,285,659 | 404,784 | ||||||||||||||||||||||||||||

| Magnetar Capital Fund LP |

3,094,731 | — | (891,173 | ) | — | 247,346 | 2,450,904 | — | ||||||||||||||||||||||||||||

| Magnetar SPV LLC |

1,447,232 | — | (1,151,987 | ) | — | (5,474 | ) | 289,771 | — | |||||||||||||||||||||||||||

| Middle East North Africa Opportunities Fund, L.P. |

3,969 | 3,969 | 675,206 | — | — | — | (313,437 | ) | 361,769 | — | ||||||||||||||||||||||||||

| Midstream & Resources Follow-On Fund, L.P. |

31,689,803 | 148,336 | (248,439 | ) | 209,680 | (13,126,747 | ) | 18,672,633 | 1,693,304 | |||||||||||||||||||||||||||

| Monsoon Infrastructure & Realty Co-Invest, L.P. |

14,464,134 | — | (1,035,107 | ) | — | 1,520,301 | 14,949,328 | — | ||||||||||||||||||||||||||||

| Passport Global Strategies III Ltd. |

1,896 | 629 | 188,708 | — | (93,462 | ) | — | (59,774 | ) | 35,472 | — | |||||||||||||||||||||||||

| Pennybacker II, LP |

5,150,000 | 149,581 | (2,222,717 | ) | 1,520,589 | (1,123,815 | ) | 3,473,638 | 108,659 | |||||||||||||||||||||||||||

| PIPE Equity Partners, LLC |

7,272,700 | — | (1,512,976 | ) | (725,664 | ) | (559,311 | ) | 4,474,749 | — | ||||||||||||||||||||||||||

| PIPE Select Fund LLC |

16,968,173 | — | (1,661,951 | ) | (140,111 | ) | (859,610 | ) | 14,306,501 | — | ||||||||||||||||||||||||||

| Private Equity Investment Fund IV, L.P. |

5,309,069 | 465,327 | (1,119,302 | ) | 256,825 | (374,503 | ) | 4,537,416 | — | |||||||||||||||||||||||||||

| Private Equity Investment Fund V, L.P.** |

41,200,445 | 1,694,086 | (1,104,598 | ) | 1,293,584 | (4,848,929 | ) | 38,234,588 | 111,055 | |||||||||||||||||||||||||||

| Quantum Parallel Partners V, L.P. |

35,665,667 | 5,101,551 | (1,436,883 | ) | — | (4,032,323 | ) | 35,298,012 | — | |||||||||||||||||||||||||||

| Saints Capital VI, L.P. |

10,811,345 | — | (1,564,499 | ) | 2,561,526 | (5,129,424 | ) | 6,678,948 | — | |||||||||||||||||||||||||||

| SBC Latin America Housing US Fund, LP |

9,181,351 | 329,533 | (670,048 | ) | — | 252,900 | 9,093,736 | — | ||||||||||||||||||||||||||||

| Tenaska Power Fund II-A, L.P. |

8,319,874 | 208,251 | (17,970 | ) | — | 693,612 | 9,203,767 | — | ||||||||||||||||||||||||||||

| Trivest Fund IV, L.P. |

14,497,369 | 45,666 | (4,364,426 | ) | — | 1,789,646 | 11,968,255 | 181,486 | ||||||||||||||||||||||||||||

| Trustbridge Partners III, L.P. |

38,448,676 | 3,120,288 | (721,472 | ) | 6,128,461 | (10,932,518 | ) | 36,043,435 | 1,648,333 | |||||||||||||||||||||||||||

| Tuckerbrook SB Global Distressed Fund I, L.P. |

4,022,438 | — | (633,715 | ) | — | 99,690 | 3,488,413 | — | ||||||||||||||||||||||||||||

| Westview Capital Partners II, L.P. |

21,047,452 | 1,586,544 | (10,290,123 | ) | 16,133,793 | (15,799,616 | ) | 12,678,050 | 3,037,158 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

| $ | 452,793,415 | $ | 19,234,863 | $ | (54,944,440 | ) | $ | 31,470,284 | $ | (57,852,859 | ) | $ | 390,701,263 | $ | 8,769,954 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

| * | Sales include return of capital. |

| ** | Voting rights have been waived for this investment. |

21

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Notes to Financial Statements, continued

December 31, 2015

(6) FINANCIAL INSTRUMENTS WITH OFF-BALANCE SHEET RISK

In the normal course of business, the Investment Funds in which the Master Fund invests may trade various derivative securities and other financial instruments, and may enter into various investment activities with off- balance sheet risk both as an investor and as a principal. The Master Fund’s risk of loss in these Investment Funds is limited to the value of its investment in such Investment Funds.

(7) ADMINISTRATION AGREEMENT

In consideration for administrative, accounting, and recordkeeping services, the Master Fund pays the Administrator a monthly administration fee based on the month-end partners’ capital of the Master Fund. The Master Fund is charged, on an annual basis, 6 basis points on partners’ capital of up to $2 billion, 5 basis points on partners’ capital between the amounts of $2 billion and $5 billion, 2 basis points on partners’ capital between the amounts of $5 billion and $15 billion, and 1.25 basis points for amounts over $15 billion. The administration fee is payable monthly in arrears. The Administrator also provides the Master Fund with compliance, transfer agency, and other investor related services at an additional cost.

The administration fees are paid out of the Master Fund’s assets, which decreases the net profits or increases the net losses of the partners in the Master Fund. As of December 31, 2015, the Master Fund had $994,678,830 in partners’ capital. The total administration fees incurred for the year ended December 31, 2015, was $663,572.

(8) RELATED PARTY TRANSACTIONS

(a) INVESTMENT MANAGEMENT FEE

In consideration of the advisory and other services provided by the Adviser to the Master Fund, the Master Fund pays the Adviser an investment management fee (the “Investment Management Fee”) equal to 0.70% on an annualized basis of the Master Fund’s partners’ capital at the end of each month, payable monthly in arrears, for the six quarters following March 31, 2014, and 0.40% on an annualized basis for periods thereafter until the period ending March 31, 2024, when the Adviser will no longer receive the Investment Management Fee.

The Master Fund’s partners bear an indirect portion of the Investment Management Fee paid by the Master Fund. The Investment Management Fee decreases the net profits or increases the net losses of the Master Fund that are credited to or debited against the capital accounts of its partners. For the year ended December 31, 2015, $6,996,684 as incurred for Investment Management Fees.

(b) EXPENSE LIMITATION AGREEMENT

Through an expense limitation agreement (the “Expense Limitation Agreement”), the Adviser contractually agreed to limit total annualized expenses of the Master Fund, for the period April 1, 2014 through January 31, 2016, to the amount of 1.25%, exclusive of fees and expenses of underlying investment funds, borrowing and other investment-related costs and fees, taxes, litigation and other extraordinary expenses not incurred in the ordinary course of the Master Fund’s business.

Under the Expense Limitation Agreement, the Adviser is permitted to recover in later periods expenses it has borne to the extent that the Master Fund’s expenses fall below the rate in effect at the time of the waiver. The Master Fund, however, is not obligated to pay any such amounts beyond three years after the end of the fiscal year in which the Adviser reimbursed such expense. Any such recoupment by the Adviser shall not cause the

22

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

Notes to Financial Statements, continued

December 31, 2015

Master Fund to exceed the annual expense limitation rate that was in effect at the time of such waiver or reimbursement. For the year ended December 31, 2015, no such expense waiver has been incurred by the Master Fund.

(9) CREDIT FACILITY

The Master Fund entered into a line of credit agreement (the “Credit Agreement”) with Credit Suisse AG on July 17, 2014. The terms of the Credit Agreement provide a $50,000,000 credit facility. Borrowings under the Credit Agreement are secured by the Master Fund’s investments. The Credit Agreement provides for a commitment fee of 0.50% per annum plus interest accruing on any borrowed amounts at the three month London Interbank Offered Rate (LIBOR) plus a spread of 2.5% per annum during the commitment period and 3.00% per annum during the wind down period as defined in the Credit Agreement. There were no borrowings during the year ended December 31, 2015. The Credit Agreement expires on July 18, 2016.

(10) FINANCIAL HIGHLIGHTS

| Year Ended December 31, 2015 |

For the Period March 31, 2014 Through December 31, 20141 |

|||||||

| Net investment income (loss) to average partners’ capital2 |

0.58 | % | (1.04 | )% | ||||

| Expenses to average partners’ capital2,3 |

0.90 | % | 2.11 | % | ||||

| Portfolio Turnover4 |

8.38 | % | 5.28 | % | ||||

| Internal rate of return since inception5 |

5.05 | % | 8.89 | % | ||||

| Total return4,6 |

3.40 | % | 6.17 | % | ||||

| Partners’ capital, end of period (000’s) |

$ | 994,679 | $ | 1,208,928 | ||||

An investor’s return (and operating ratios) may vary from those reflected based on the timing of capital transactions.

| 1 | The Endowment PMF Master Fund, L.P. commenced operations on March 31, 2014. |

| 2 | Ratios are calculated by dividing the indicated amount by average partners’ capital measured at the end of each month during the period. These ratios have been annualized for periods less than twelve months. |

| 3 | Expense ratios do not include expenses of acquired funds that are paid indirectly by the Master Fund as a result of its ownership in the underlying funds. Expenses include U.S. offshore withholding tax, which is only allocable to investors investing through the offshore feeder funds. |

| 4 | Not annualized for periods less than twelve months. |

| 5 | The internal rate of return since inception (“IRR”) of the limited partners is net of all fees and profit allocations to the Adviser. The IRR reported is for the Master Fund as a whole. The IRR was computed based on the actual dates of the cash inflows (capital contributions), cash outflows (cash distributions) and the ending partners’ capital as of December 31, 2015 (the residual value). |

| 6 | The total return of the Master Fund is calculated as geometrically linked monthly returns for each month in the period. |

(11) SUBSEQUENT EVENTS

Management of the Master Fund has evaluated the need for additional disclosures and/or adjustments resulting from subsequent events through the date the financial statements were issued. Based on this evaluation, no adjustments were required to the financial statements as of December 31, 2015.

23

THE ENDOWMENT PMF MASTER FUND, L.P.

(A Limited Partnership)

December 31, 2015

(Unaudited)

Directors and Officers

The Master Fund’s operations are managed under the direction and oversight of the Board. Each Director serves for an indefinite term or until he or she reaches mandatory retirement, if any, as established by the Board. The Board appoints the officers of the Master Fund who are responsible for the Master Fund’s day-to-day business decisions based on policies set by the Board. The officers serve at the pleasure of the Board.

Compensation for Directors