UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22922

Aspiration Funds

(Exact name of registrant as specified in charter)

(Exact name of registrant as specified in charter)

4551 Glencoe Avenue, Marina Del Rey, California 90292

(Address of principal executive offices) (Zip code)

The Corporation Trust Company

1209 Orange Street, Wilmington, DE 19801

(Name and address of agent for service)

Registrant's telephone number, including area code: 252-972-9922

Date of fiscal year end: September 30

Date of reporting period: September 30, 2019

Annual Report 2019

As of September 30, 2019

Aspiration Flagship Fund

This report and the financial statements contained herein are submitted for the general information of the shareholders of the Aspiration Flagship Fund (the “Fund”). The Fund’s shares are not deposits or obligations

of, or guaranteed by, any depository institution. The Fund’s shares are not insured by the FDIC, Federal Reserve Board or any other agency, and are subject to investment risks, including possible loss of principal amount invested. Neither the Fund

nor the Fund’s distributor is a bank.

The Aspiration Flagship Fund is distributed by Capital Investment Group, Inc., Member FINRA/SIPC, 100 E. Six Forks Road, Suite 200, Raleigh, NC, 27609. There is no affiliation between the Aspiration Flagship Fund,

including its principals, and Capital Investment Group, Inc.

|

Statements in this Annual Report that reflect projections or expectations of future financial or economic performance of the Aspiration Flagship Fund (“Fund”) and of the market in general and statements

of the Fund’s plans and objectives for future operations are forward-looking statements. No assurance can be given that actual results or events will not differ materially from those projected, estimated, assumed or anticipated in any

such forward-looking statements. Important factors that could result in such differences, in addition to the other factors noted with such forward-looking statements, include, without limitation, general economic conditions such as

inflation, recession and interest rates. Past performance is not a guarantee of future results.

An investor should consider the investment objectives, risks, charges, and expenses of the Fund carefully

before investing. The prospectus contains this and other information about the Fund. A copy of the prospectus is available at funds.aspiration.com/flagship/

or by calling the Advisor at 800-683-8529. The prospectus should be read carefully before investing.

|

For More Information on the Aspiration Flagship Fund:

See Our Web site at aspiration.com

or

Call Our Shareholder Services Group at 800-683-8529.

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Fund’s shareholder reports will no longer be sent by mail, unless you specifically

request paper copies of the reports. Instead, the reports will be made available on the Fund’s website at https://www.nottinghamco.com/fundpages/Aspiration, and you will be notified by mail each time a report is posted and provided with a website

link to access the report.

If you have already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other

communications from a Fund electronically anytime by contacting your financial intermediary (such as a broker-dealer or bank) or, if you are a direct investor, by clicking Enroll at https://www.nottinghamco.com/fundpages/Aspiration.

You may, notwithstanding the availability of shareholder reports online, elect to receive all future shareholder reports in paper free of charge. If you invest through a financial intermediary, you can contact your

financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with a Fund, you can call 800-773-3863 to let the Fund know you wish to continue receiving paper copies of your

shareholder reports. Your election to receive reports in paper will apply to all funds held with the Fund complex.

Dear Aspiration Flagship Fund Shareholder,

Thank you for investing in the Aspiration Flagship Fund.

Our aim with the Aspiration Flagship Fund has been to make a low volatility strategy available to all investors. Such strategies are not designed to beat

the market. Rather, they historically have been used mainly by wealthier investors to complement other investments and smooth out the ups and downs of the market.

That said, if you’re looking for a mix of strategies that could help maximize long-term returns, consider combining Flagship with an investment strategy

that offers broad equity exposure, such as the 100% fossil fuel free Aspiration Redwood Fund. (To learn more, please visit our Aspiration Redwood Fund page.)

Over the past fiscal year, the Aspiration Flagship Fund performance was -.21% assuming no management fee. While the Fund fits within the

multialternative category, the Fund’s statutory benchmark, the S&P 500 Total Return Index had performance of 4.25% over the same period.

Concerns over weakening global growth and continuing battles between the U.S. and China over trade found investors in a quandary at the beginning of

the year. The U.S. economy was in the tenth year of an economic recovery – aiming to become the longest on record – yet data from the St. Louis Fed indicated the rate of growth to be the slowest on record ever seen during an expansionary period.

Even the Fed seemed to be taken a bit by surprise during its December 2018 assessment on the state of the economy, keeping in mind

there were four rate increases in 2018, which made it nine consecutive increases since the beginning of 2015 and the Fed had been forecasting three more increases in the coming year. At that meeting, less than one year ago, Chairman Jay Powell

commented on seeing a signaled “softening” in the economy and the forecast given at that time was reduced to two expected increases in 2019, down from that projected three - given just a short time before.

As they often do, things changed further shortly after this meeting. An ongoing weaker economy (though still positive) and

uncertainty surrounding the U.S. and China relationship resulted in the Fed to, at first, halt its plan for a rate increase and then reverse course and actually lower rates – which it did three times in 2019.

Still, through all of this, the U.S. stock market was positive and the Aspiration Flagship Fund – through the end of November –

found itself having its best calendar year on record.

There are two interesting characteristics of the Flagship Fund: lower volatility than the overall market, and low turnover. The

first is a function of the holdings as we tend to select a fund or ETF for inclusion in the portfolio based on its “risk-adjusted return.” In other words, if we have a choice of two holdings with similar return expectations, we would lean toward

selecting the one that is perceived to have lower risk.

It should be noted that lower volatility – mentioned above - does have two anticipated effects. During a market downturn, the

portion of a portfolio including the Aspiration Flagship Fund is anticipated to have a smaller decline. Likewise, the Fund on its own is expected to only have a degree of participation in a rising market. Liquid Alternative funds are typically

viewed as a complement to a stock and bond portfolio, expected to potentially diversify a portfolio’s overall risk.

We also tend not to make a lot of trades in the portfolio in the attempt to keep trading costs in check and with an eye on tax

efficiency (although this is not stated as a Fund objective). Further, we do not trade based on any type of market forecast and strive to keep our asset allocation somewhat close to the strategy put together when the Fund originated - making

adjustments to the holdings within each category.

This past year, there were some occasions where trades were made due to either an inflow or outflow of funds. These times were few

in number and the effect was slight.

Additionally, there were two adjustments of note with regard to the holdings in the portfolio.

Wisdom Tree Dynamic Long/Short U.S. Equity Fund is a fund that served us very well in 2017 and early 2018, but over the past year

the return has been negative (still showing a favorable long-term risk adjusted return). We have been actively reducing this holding throughout the year.

The Equinox family has a few mutual funds in the area of Managed Futures. With a low correlation (sometimes appearing negative) to

the overall market managed futures are seen as a hedging vehicle to complement a portion of a portfolio. We noticed that “risk” seemed to increase in the Equinox Chesapeake Strategy mutual fund, another position that served us well in 2017, so

we diluted the fund by replacing half with Equinox Mutual Hedge Futures Strategy – a fund from the same family with lower volatility.

Thanks again for investing in the Aspiration Flagship Fund. We take great pride in what we’ve been able to achieve. Know that we remain committed to

bringing you and all Americans accessible, high-quality investment services.

Best,

Andrei Cherny

CEO, Aspiration Partners, Inc.

PS. Do you know anyone else you think we be a good fit to join Aspiration’s growing community of investors? Please put in a good word for us!

(RCASP1119001)

|

Aspiration Flagship Fund

|

|||||||||||||||||||

|

Performance Update (Unaudited)

|

|||||||||||||||||||

|

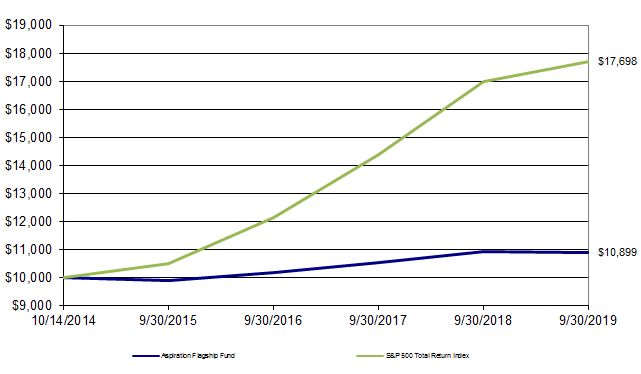

For the period from October 14, 2014 (Date of Initial Public Investment) through September 30, 2019

|

|||||||||||||||||||

|

Comparison of the Change in Value of a $10,000 Investment

|

|||||||||||||||||||

|

This graph assumes an initial investment of $10,000 at October 14, 2014 (Date of Initial Public Investment). All dividends and distributions

are reinvested. This graph depicts the performance of the Aspiration Flagship Fund versus the S&P 500 Total Return Index. It is important to note that the Fund is a professionally managed mutual fund while the index is not available

for investment and is unmanaged. The comparison is shown for illustrative purposes only.

|

|||||||||||||||||||

|

Average Annual Total Returns

|

|||||||||||||||||||

|

Gross

|

Net

|

||||||||||||||||||

|

As of

|

One

|

Since

|

Inception

|

Expense

|

Expense

|

||||||||||||||

|

September 30, 2019

|

Year

|

Inception

|

Date

|

Ratio*

|

Ratio*

|

||||||||||||||

|

Aspiration Flagship Fund - With maximum

|

|||||||||||||||||||

|

assumed contribution reduction**

|

-2.21%

|

-0.21%

|

10/14/14

|

4.13%

|

0.50%

|

||||||||||||||

|

Aspiration Flagship Fund - Without maximum

|

|||||||||||||||||||

|

assumed contribution reduction

|

-0.21%

|

1.75%

|

10/14/14

|

4.13%

|

0.50%

|

||||||||||||||

|

S&P 500 Total Return Index

|

4.25%

|

12.19%

|

N/A

|

N/A

|

N/A

|

||||||||||||||

|

*

|

The gross and net expense ratios shown are from the Fund's Financial Highlights as of September 30, 2019.

|

||||||||||||||||||

|

**

|

Investors in the Fund are clients of Aspiration Fund Adviser, LLC (the "Advisor") and may pay the Advisor a fee in the amount they believe is

fair ranging from 0% to 2% of the value of their investment in the Fund. The Average Annual Total Returns with a maximum assumed contributed reduction is calculated assuming a maximum advisory fee of 2% is paid by an investor to the

Advisor.

|

||||||||||||||||||

|

Performance quoted above represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate so that shares,

when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. An investor may obtain performance data, current to the most recent month-end, by visiting

aspiration.com.

|

|||||||||||||||||||

|

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the

redemption of Fund shares. Average annual total returns are historical in nature and measure net investment income and capital gain or loss from portfolio investments assuming reinvestments of distributions.

|

|||||||||||||||||||

|

Aspiration Flagship Fund

|

||||||||||

|

Schedule of Investments

|

||||||||||

|

As of September 30, 2019

|

||||||||||

|

Shares

|

Value (Note 1)

|

|||||||||

|

EXCHANGE-TRADED PRODUCTS - 39.19%

|

||||||||||

|

Event Driven - 10.89%

|

||||||||||

|

IndexIQ ETF Trust - IQ Hedge Multi-Strategy Tracker ETF

|

28,088

|

$

|

854,437

|

|||||||

|

*

|

IQ Merger Arbitrage ETF

|

23,688

|

759,200

|

|||||||

|

1,613,637

|

||||||||||

|

Global Macro - 14.93%

|

||||||||||

|

First Trust Senior Loan ETF

|

12,109

|

574,088

|

||||||||

|

Reality Shares DIVS ETF

|

38,467

|

1,004,373

|

||||||||

|

VanEck Vectors Investment Grade Floating Rate ETF

|

25,165

|

635,165

|

||||||||

|

2,213,626

|

||||||||||

|

Long/Short Equity - 6.41%

|

||||||||||

|

AGFiQ US Market Neutral Anti-Beta Fund

|

11,906

|

282,172

|

||||||||

|

First Trust Exchange-Traded Fund III-First Trust Long/Short Equity ETF

|

10,678

|

437,798

|

||||||||

|

WisdomTree Dynamic Long/Short U.S. Equity Fund

|

8,267

|

229,740

|

||||||||

|

949,710

|

||||||||||

|

Options Strategy - 4.30%

|

||||||||||

|

Global X S&P 500 Covered Call ETF

|

7,316

|

356,191

|

||||||||

|

Invesco S&P 500 BuyWrite ETF

|

12,951

|

280,389

|

||||||||

|

636,580

|

||||||||||

|

Unconstrained Bond - 2.66%

|

||||||||||

|

iShares TIPS Bond ETF

|

1,029

|

119,662

|

||||||||

|

Schwab US TIPS ETF

|

4,845

|

275,002

|

||||||||

|

394,664

|

||||||||||

|

Total Exchange-Traded Products (Cost $5,759,603)

|

5,808,217

|

|||||||||

|

OPEN-END FUNDS - 50.50%

|

||||||||||

|

Event Driven - 3.50%

|

||||||||||

|

Gabelli Enterprise Mergers and Acquisitions Fund

|

21,957

|

332,645

|

||||||||

|

The Merger Fund

|

10,931

|

186,153

|

||||||||

|

518,798

|

||||||||||

|

Global Macro - 18.28%

|

||||||||||

|

FPA New Income, Inc.

|

6,346

|

63,459

|

||||||||

|

Goldman Sachs Absolute Return Tracker Fund

|

61,641

|

604,695

|

||||||||

|

Guggenheim Macro Opportunities Fund

|

16,839

|

435,286

|

||||||||

|

Invesco Oppenheimer Fundamental Alternatives Fund

|

20,295

|

557,111

|

||||||||

|

Litman Gregory Masters Alternative Strategies Fund

|

90,753

|

1,049,101

|

||||||||

|

2,709,652

|

||||||||||

|

Long/Short Equity - 6.45%

|

||||||||||

|

Boston Partners Global Long/Short Fund

|

31,292

|

341,394

|

||||||||

|

Hancock Horizon Quantitative Long/Short Fund

|

34,058

|

614,752

|

||||||||

|

956,146

|

||||||||||

|

Managed Futures - 10.35%

|

||||||||||

|

*

|

361 Managed Futures Fund

|

52,615

|

614,547

|

|||||||

|

Equinox Chesapeake Strategy Fund

|

8,909

|

101,118

|

||||||||

|

*

|

Equinox MutualHedge Futures Strategy Fund

|

24,661

|

230,826

|

|||||||

|

Goldman Sachs Managed Futures Strategy Fund

|

54,119

|

587,737

|

||||||||

|

1,534,228

|

||||||||||

|

(Continued)

|

||||||||||

|

Aspiration Flagship Fund

|

||||||||||

|

Schedule of Investments - Continued

|

||||||||||

|

As of September 30, 2019

|

||||||||||

|

Shares

|

Value (Note 1)

|

|||||||||

|

OPEN-END FUNDS - CONTINUED

|

||||||||||

|

Options Strategy - 7.88%

|

||||||||||

|

AllianzGI Structured Return Fund

|

24,704

|

$

|

402,677

|

|||||||

|

Gateway Fund

|

13,806

|

463,337

|

||||||||

|

Glenmede Secured Options Portfolio

|

23,737

|

302,168

|

||||||||

|

1,168,182

|

||||||||||

|

Unconstrained Bond - 4.04%

|

||||||||||

|

Barings Active Short Duration Bond Fund

|

20,309

|

201,904

|

||||||||

|

BlackRock Strategic Income Opportunities Portfolio

|

40,083

|

397,221

|

||||||||

|

599,125

|

||||||||||

|

Total Open-End Funds (Cost $7,355,222)

|

7,486,131

|

|||||||||

|

COMMON STOCKS - 2.33%

|

||||||||||

|

Industrials - 1.95%

|

||||||||||

|

*

|

Trex Co., Inc.

|

3,176

|

288,794

|

|||||||

|

Materials - 0.39%

|

||||||||||

|

*

|

Livent Corp.

|

8,553

|

57,220

|

|||||||

|

Total Common Stocks (Cost $291,549)

|

346,014

|

|||||||||

|

LIMITED PARTNERSHIP - 2.92%

|

||||||||||

|

Energy - 2.92%

|

||||||||||

|

Enviva Partners LP

|

13,543

|

432,699

|

||||||||

|

Total Limited Partnership (Cost $344,129)

|

432,699

|

|||||||||

|

SHORT-TERM INVESTMENT - 1.13%

|

||||||||||

|

§

|

Fidelity Institutional Money Market Fund - Treasury Portfolio, 1.82%

|

167,840

|

167,840

|

|||||||

|

Total Short-Term Investment (Cost $167,840)

|

167,840

|

|||||||||

|

Total Value of Investments (Cost $13,918,343) - 96.07%

|

$

|

14,240,901

|

||||||||

|

Other Assets Less Liabilities - 3.93%

|

582,820

|

|||||||||

|

NET ASSETS - 100.00%

|

$

|

14,823,721

|

||||||||

|

*

|

Non-income producing investment

|

|||||||||

|

§

|

Represents 7 day effective yield as of September 30, 2019.

|

|||||||||

|

The following acronym or abbreviation is also used in this portfolio:

|

||||||||||

|

LP - Limited Partnership

|

||||||||||

|

ETF - Exchange-Traded Fund

|

||||||||||

|

(Continued)

|

||||||||||

|

Aspiration Flagship Fund

|

||||||||||

|

Schedule of Investments - Continued

|

||||||||||

|

As of September 30, 2019

|

||||||||||

|

|

||||||||||

|

Summary of Investments

|

||||||||||

|

% of Net

|

||||||||||

|

Assets

|

Value

|

|||||||||

|

Exchange-Traded Products

|

39.19%

|

$ 5,808,217

|

||||||||

|

Open-End Funds

|

50.50%

|

7,486,131

|

||||||||

|

Common Stocks

|

2.33%

|

346,014

|

||||||||

|

Limited Partnership

|

2.92%

|

432,699

|

||||||||

|

Short-Term Investment

|

1.13%

|

167,840

|

||||||||

|

Other Assets Less Liabilities

|

3.93%

|

582,820

|

||||||||

|

Total

|

100.00%

|

$ 14,823,721

|

||||||||

See Notes to Financial Statements

|

Aspiration Flagship Fund

|

|||

|

Statement of Assets and Liabilities

|

|||

|

As of September 30, 2019

|

|||

|

Assets:

|

|||

|

Investments, at value (cost $13,918,343)

|

$

|

14,240,901

|

|

|

Receivables:

|

|||

|

From Advisor

|

508,624

|

||

|

Fund shares sold

|

120,197

|

||

|

Dividends

|

15,245

|

||

|

Prepaid expenses:

|

|||

|

Registration and filing expenses

|

10,798

|

||

|

Fund accounting fees

|

2,249

|

||

|

Other operating expenses

|

876

|

||

|

Trustee fees and meeting expenses

|

286

|

||

|

Compliance fees

|

230

|

||

|

Transfer agent fees

|

182

|

||

|

Total Assets

|

14,899,588

|

||

|

Liabilities:

|

|||

|

Payables:

|

|||

|

Fund shares repurchased

|

15,628

|

||

|

Accrued expenses:

|

|||

|

Professional fees

|

41,797

|

||

|

Custody fees

|

8,177

|

||

|

Insurance fees

|

5,417

|

||

|

Distribution and service fees - Investor Class Shares

|

3,279

|

||

|

Shareholder fulfillment fees

|

1,498

|

||

|

Security pricing fees

|

65

|

||

|

Administration fees

|

6

|

||

|

Total Liabilities

|

75,867

|

||

|

Net Assets

|

$

|

14,823,721

|

|

|

Net Assets Consist of:

|

|||

|

Paid in capital

|

$

|

14,526,039

|

|

|

Distributable earnings

|

297,682

|

||

|

Total Net Assets

|

$

|

14,823,721

|

|

|

Shares Outstanding, no par value (unlimited authorized shares)

|

1,436,203

|

||

|

Net Asset Value, Maximum Offering Price and Redemption Price Per Share

|

$

|

10.32

|

|

|

See Notes to Financial Statements

|

|||

|

Aspiration Flagship Fund

|

|||

|

Statement of Operations

|

|||

|

For the fiscal year ended September 30, 2019

|

|||

|

Investment Income:

|

|||

|

Dividends

|

$

|

298,508

|

|

|

Total Investment Income

|

298,508

|

||

|

Expenses:

|

|||

|

Other operating expenses (Note 2)

|

231,447

|

||

|

Transfer Agent fees (Note 2)

|

180,993

|

||

|

Professional fees

|

139,310

|

||

|

Custody fees (Note 2)

|

62,647

|

||

|

Total Expenses

|

614,397

|

||

|

Expenses reimbursed by Advisor (Note 2)

|

(539,909)

|

||

|

Net Expenses

|

74,488

|

||

|

Net Investment Income

|

224,020

|

||

|

Realized and Unrealized Gain (Loss) on Investments:

|

|||

|

Net realized loss from:

|

|||

|

Sale of investments

|

(594,626)

|

||

|

Capital gain distributions from underlying funds

|

465,112

|

||

|

Total net realized loss

|

(129,514)

|

||

|

Net change in unrealized depreciation on investments

|

(145,837)

|

||

|

Net Realized and Unrealized Loss on Investments

|

(275,351)

|

||

|

Net Decrease in Net Assets Resulting from Operations

|

$

|

(51,331)

|

|

See Notes to Financial Statements

|

Aspiration Flagship Fund

|

||||||||||

|

Statements of Changes in Net Assets

|

||||||||||

|

For the fiscal years ended September 30,

|

2019

|

2018

|

||||||||

|

Operations:

|

||||||||||

|

Net investment income

|

$

|

224,020 |

$

|

147,778 | ||||||

|

Net realized gain (loss) from investment transactions

|

(594,626)

|

18,980

|

||||||||

|

Capital gain distributions from underlying funds

|

465,112

|

42,340

|

||||||||

|

Net change in unrealized appreciation (depreciation) on investments

|

(145,837)

|

289,506

|

||||||||

|

Increase (Decrease) in Net Assets Resulting from Operations

|

(51,331)

|

498,604

|

||||||||

|

Distributions to Shareholders

|

(194,003)

|

(126,409)

|

||||||||

|

Decrease in Net Assets Resulting from Distributions

|

(194,003)

|

(126,409)

|

||||||||

|

Beneficial Interest Transactions:

|

||||||||||

|

Shares sold

|

4,716,220

|

9,301,430

|

||||||||

|

Reinvested dividends and distributions

|

193,823

|

126,059

|

||||||||

|

Shares repurchased

|

(5,301,397)

|

(4,391,075)

|

||||||||

|

Net Increase (Decrease) in Beneficial Interest Transactions

|

(391,354)

|

5,036,414

|

||||||||

|

Net Increase in Net Assets

|

(636,688)

|

5,408,609

|

||||||||

|

Net Assets:

|

||||||||||

|

Beginning of year

|

$

|

15,460,409 |

$

|

10,051,800 | ||||||

|

End of year

|

$

|

14,823,721 |

$

|

15,460,409 | ||||||

|

Share Information:

|

||||||||||

|

Shares sold

|

464,570

|

902,724

|

||||||||

|

Reinvested dividends and distributions

|

19,768

|

12,250

|

||||||||

|

Shares repurchased

|

(522,750)

|

(425,168)

|

||||||||

|

Net Increase in Shares of Beneficial Interest

|

(38,412)

|

489,806

|

||||||||

See Notes to Financial Statements

|

Aspiration Flagship Fund

|

|||||||||||||||

|

Financial Highlights

|

|||||||||||||||

|

For a share outstanding during the period

|

|||||||||||||||

|

or fiscal years ended September 30,

|

2019

|

2018

|

2017

|

2016

|

2015

|

(f)

|

|||||||||

|

Net Asset Value per Share, Beginning of Period

|

$

|

10.48

|

$

|

10.21

|

$

|

9.92

|

$

|

9.75

|

$

|

10.00

|

|||||

|

Income (Loss) from Investment Operations

|

|||||||||||||||

|

Net investment income

|

0.16

|

0.11

|

0.07

|

0.11

|

0.16

|

||||||||||

|

Net realized and unrealized gain (loss) on

|

|||||||||||||||

|

investments

|

(0.19)

|

0.27

|

0.28

|

0.17

|

(0.27)

|

||||||||||

|

Total from Investment Operations

|

(0.03)

|

0.38

|

0.35

|

0.28

|

(0.11)

|

||||||||||

|

Less Distributions to Shareholders:

|

|||||||||||||||

|

Net investment income

|

(0.11)

|

(0.11)

|

(0.06)

|

(0.11)

|

(0.14)

|

||||||||||

|

Net realized gains

|

(0.02)

|

-

|

-

|

-

|

-

|

||||||||||

|

Total Distributions

|

(0.13)

|

(0.11)

|

(0.06)

|

(0.11)

|

(0.14)

|

||||||||||

|

Net Asset Value per Share, End of Period

|

$

|

10.32

|

$

|

10.48

|

$

|

10.21

|

$

|

9.92

|

$

|

9.75

|

|||||

|

Total Return (e)

|

(0.21)%

|

3.74%

|

3.55%

|

2.87%

|

(1.21)%

|

(b)

|

|||||||||

|

Net Assets, End of Period (in thousands)

|

$

|

14,824

|

$

|

15,460

|

$

|

10,052

|

$

|

5,389

|

$

|

4,161

|

|||||

|

Ratios of:

|

|||||||||||||||

|

Gross Expenses to Average Net Assets (c)

|

4.13%

|

3.24%

|

5.40%

|

7.06%

|

19.23%

|

(a)

|

|||||||||

|

Net Expenses to Average Net Assets (c)

|

0.50%

|

0.50%

|

0.50%

|

0.50%

|

0.50%

|

(a)

|

|||||||||

|

Net Investment Income to Average Net Assets (c)(d)

|

1.52%

|

1.09%

|

0.72%

|

1.01%

|

0.95%

|

(a)

|

|||||||||

|

Portfolio turnover rate

|

14.90%

|

7.33%

|

13.99%

|

25.49%

|

67.24%

|

(b)

|

|||||||||

|

(a)

|

Annualized

|

||||||||||||||

|

(b)

|

Not annualized.

|

||||||||||||||

|

(c)

|

Does not include expenses of the investment companies in which the Fund invests.

|

||||||||||||||

|

(d)

|

Recognition of net investment income by the Fund is affected by the timing of the declaration of dividends by the underlying investment

companies in which the Fund invests.

|

||||||||||||||

|

(e)

|

Investors in the Fund are clients of Aspiration Fund Adviser, LLC (the "Advisor") and may pay the Advisor a fee in the amount they believe

is fair ranging from 0% to 2% of the value of their investment in the Fund. Assuming a maximum advisory fee of 2% is paid by an investor to the Advisor, the Total Return of an investment in the Fund would have been (2.21)%, 1.74%,

1.55%, 0.87%, and (3.21)% for the periods ended September 2019, 2018, 2017, 2016, and 2015, respectively.

|

||||||||||||||

|

(f)

|

For the fiscal period from October 14, 2014 (Date of Initial Public Investment) through September 30, 2015.

|

||||||||||||||

|

See Notes to Financial Statements

|

|||||||||||||||

Aspiration Flagship Fund

Notes to Financial Statements – Continued

As of September 30, 2019

1. Organization and Significant Accounting PoliciesThe Aspiration Flagship Fund (the “Fund”) is a series of the Aspiration Funds (the “Trust”). The Trust was organized as a Delaware statutory trust on October 16, 2013 and is registered under the Investment

Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company.

The Fund is a separate diversified series of the Trust and commenced operations on October 14, 2014. The investment objective of the Fund is to seek long-term capital appreciation by

providing risk-adjusted returns. The Fund seeks to achieve its investment objective by investing primarily in shares of registered investment companies, including open-end funds, exchange-traded funds (“ETFs”), and closed-end funds that

emphasize alternative strategies, such as funds that sell securities short; employ asset allocation, arbitrage, and/or option-hedged strategies; or that invest in distressed securities, the natural resources sector, and business development

companies (“BDCs”).

The Fund currently has an unlimited number of authorized shares, which are divided into two classes - Investor Class Shares and Class C Shares. Each class of shares has equal rights as to assets of the Fund, and

the classes are identical, except for differences in ongoing distribution and service fees and a contingent deferred sales charge on the Class C Shares. Both share classes are subject to distribution plan fees as described in Note 3. Income,

expenses (other than distribution and service fees), and realized and unrealized gains or losses on investments are allocated to each class of shares based upon its relative net assets. All classes have equal voting privileges, except where

otherwise required by law or when the Trustees determine that the matter to be voted on affects only the interests of the shareholders of a particular class. As of September 30, 2019, no Class C Shares have been issued.

The following is a summary of significant accounting policies consistently followed by the Fund. The policies are in conformity with accounting principles generally accepted in the United States of America

(“GAAP”). The Fund follows the accounting and reporting guidance in the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification 946 “Financial Services – Investment Companies.”

Principles of Accounting

The Fund uses the accrual method of accounting for financial reporting purposes.

Net Asset Value

The net asset value (“NAV”) per share of each class of a Fund is determined by dividing the Fund’s net assets attributable to each class by the number of shares issued and outstanding of that class on each day

the New York Stock Exchange (“NYSE”) is open for trading.

Investment Valuation

The Fund’s investments in securities, including ETFs, listed on an exchange or quoted on a national market system are valued at the last sales price as of 4:00 p.m. Eastern Time. Securities traded in the NASDAQ

over-the-counter market are generally valued at the NASDAQ Official Closing Price, which may not be the last sale price. Other securities traded in the over-the-counter market and listed securities for which no sale was reported on that date

are valued at the most recent bid price. Securities and assets for which representative market quotations are not readily available (e.g., if the exchange on which the portfolio security is principally traded closes early or if trading of the

particular portfolio security is halted during the day and does not resume prior to the Fund’s net asset value calculation) or which cannot be accurately valued using the Fund’s normal pricing procedures are valued at fair value as determined

in good faith under policies approved by the Trustees. A portfolio security’s “fair value” price may differ from the price next available for that portfolio security using the Fund’s normal pricing procedures. Instruments with maturities of

60 days or less are valued at amortized cost, which approximates fair value.

The Fund invests in portfolios of open-end investment companies (the “Underlying Funds”). The Underlying Funds value securities in their portfolios for which market quotations are readily available at their

market values (generally the last reported sale price) and all other securities and assets at their fair value to the methods established by the board of directors of the Underlying Funds. Open-ended funds are valued at their respective net

asset values as reported by such investment companies.

(Continued)

Aspiration Flagship Fund

Notes to Financial Statements – Continued

As of September 30, 2019

Fair Value Measurement

Various inputs are used in determining the fair value of the Fund's investments. These inputs are summarized in the three broad levels listed below:

Level 1: quoted prices in active markets for identical securities

Level 2: other significant observable inputs (including quoted prices for similar securities and identical securities in inactive markets, interest

rates, credit risk, etc.)

Level 3: significant unobservable inputs (including the Fund’s own assumptions in determining fair value of investments)

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet

established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination

of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value

measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. The following table summarizes the inputs as of September 30,

2019 for the Fund’s investments measured at fair value:

|

Aspiration Flagship Fund

|

||||||||

|

Investments in Securities (a)

|

Total

|

Level 1

|

Level 2

|

Level 3

|

||||

|

Investments

|

||||||||

|

Exchange-Traded Products*

|

$

|

5,808,217

|

$

|

5,808,217

|

$

|

-

|

$

|

-

|

|

Open-End Funds*

|

7,486,131

|

7,486,131

|

-

|

-

|

||||

|

Common Stocks*

|

346,014

|

346,014

|

-

|

-

|

||||

|

Limited Partnership*

|

432,699

|

432,699

|

-

|

-

|

||||

|

Short-Term Investment

|

167,840

|

167,840

|

-

|

-

|

||||

|

Total Investments

|

$

|

14,240,901

|

$

|

14,240,901

|

$

|

-

|

$

|

-

|

|

(a)

|

There were no Level 3 securities held during the fiscal year ended September 30, 2019.

|

*Refer to Schedule of Investments for breakdown based on investment strategy.

Investment Valuation Sectors

Global Macro. A global macro trading strategy involves investing in equity, fixed-income, foreign exchange, or commodity markets around the world. Macro Portfolio Managers

focus on underlying macroeconomic fundamentals in developing their investment theses. Monetary policy shifts, fiscal policy shifts, gross domestic product growth, or inflation all may be considered in developing a market view. Portfolio

Managers establish opportunistic long or short market positions to seek to benefit from anticipated market moves. Macro Portfolio Managers tend to make significant use of derivatives and leverage.

Long/Short Equity. Equity long/short strategies combine core long and short positions in stocks, stock indices, or derivatives related to the equity markets. Equity

long/short Portfolio Managers attempt to generate long term capital appreciation by developing and actively managing equity portfolios that include both long and short positions by purchasing perceived undervalued securities and selling

perceived overvalued securities to generate returns and to reduce a portion of general market risk. In generating non-market related returns, this investment approach emphasizes a Portfolio Manager’s discretionary approach based on fundamental

research.

(Continued)

Aspiration Flagship Fund

Notes to Financial Statements – Continued

As of September 30, 2019

Event Driven. Event-driven strategies involve the assessment of how, when, and if specific transactions will be completed and the effect on corporations and financial

assets. A common event-driven strategy is merger arbitrage (also called risk arbitrage). This involves the purchase of the stock of a target company involved in a potential merger and, in the case of a stock-for-stock offer, the short sale of

the stock of the acquiring company. The target company’s stock would typically trade at a discount to the offer price due to the uncertainty of the completion of the transaction. The positions may be reversed if the manager feels the

acquisition may not close. This strategy aims to capture the spread between the value of the security at the close of the transaction and its discounted value at the time of purchase. Other examples of event-driven strategies and

opportunities include corporate restructurings, spin-offs, operational turnarounds, activism, asset sales, and liquidations. Generally, investment funds within this strategy require a 60 to 90-day notice period to redeem at the next available

redemption date.

Managed Futures. Managed futures strategies refer to an investment where a portfolio of futures contracts is actively managed by the Portfolio Managers. Managed futures

are considered an alternative investment and are often used by funds and institutional investors to provide both portfolio and market diversification.

Options Strategy. Option strategies are the simultaneous, and often mixed buying or selling of one or more options that differ in one or more of the options' variables.

Options strategies allow traders to profit from movements in the underlying assets based on market sentiment.

Unconstrained Bond. Unconstrained bond strategies are an absolute return type approach that generally aim to reduce exposure to interest rates, among other risks, and give

investors flexibility in their fixed income portfolio. Unconstrained bond strategies allow managers to pursue returns across many asset classes and sectors.

Concentrations of Risk

The Fund seeks to achieve its investment objective by investing primarily in shares of registered investment companies, including open-end funds, ETFs, and closed-end funds that emphasize alternative strategies,

such as funds that sell securities short; employ asset allocation, arbitrage and/or option-hedged strategies; or that invest in distressed securities, the natural resources sector and BDCs. Underlying funds will be purchased and sold based

upon criteria which include, but are not limited to, correlation with other portfolio holdings and major indices, risk-adjusted returns believed to help the Fund achieve its goals, portfolio diversification, manager diligence, expense ratios,

and compliance with the Fund’s investment restrictions. The principal risks of investing in the Fund include: correlation risk, investment company risk, allocation risk, underlying fund concentration risk, leveraging risk, foreign investing

and emerging markets risk, convertible securities risk, BDC risk, high yield risk, liquidity risk, market risk, commodities risk, ETFs risk, distressed companies risk, alternative asset class risk, long/short selling risk, arbitrage risk,

futures risk, natural resources risk, equity securities risk, bonds and other fixed income securities risk, cybersecurity risk, and management risk.

Investment Transactions and Investment Income

Investment transactions are accounted for as of the date purchased or sold (trade date). Dividend income and distributions received from investment funds are recorded on the ex-dividend date. Realized gains and

losses are determined on the identified cost basis, which is the same basis used for Federal income tax purposes.

Expenses

The Fund bears expenses incurred specifically on its behalf as well as a portion of Trust level expenses, which are allocated according to methods reviewed by the Board of Trustees (“Trustees”).

Distributions

The Fund may declare and distribute dividends from net investment income (if any) annually. Distributions from capital gains (if any) are generally declared and distributed annually. Dividends and distributions

to shareholders are recorded on ex-date.

(Continued)

Aspiration Flagship Fund

Notes to Financial Statements – Continued

As of September 30, 2019

Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and

liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in the net assets from operations during the reporting period. Actual results could

differ from those estimates.

Federal Income Taxes

No provision for income taxes is included in the accompanying financial statements, as the Fund intends to distribute to shareholders all taxable investment income and realized gains and otherwise comply with

Subchapter M of the Internal Revenue Code applicable to regulated invest.

2. Transactions with Related Parties and Service Providers

Aspiration Fund Adviser, LLC (the “Advisor”) does not impose a set fee to manage individual shareholder accounts. Instead, the shareholders may pay the Advisor a fee to manage their individual accounts in the

amount they believe is fair, ranging from 0% to 2% of their net assets. Only clients of the Advisor may invest in the Fund. Those Advisor clients must establish an advisory relationship and open an individual account with the Advisor before

investing in the Fund. The Fund is responsible for its own operating expenses. Advisory fees will not be incurred by the Fund.

The Advisor has entered into a contractual agreement (the “Expense Limitation Agreement”) with the Trust, on behalf of the Fund, under which it has agreed to waive or reduce its fees and to assume other expenses

of the Fund, if necessary, in amounts that limit the Fund’s total operating expenses (exclusive of interest, taxes, dividends, litigation and indemnification expenses, brokerage commissions, borrowing costs, fees and expenses of other

investment companies in which the Fund invests, and other expenditures which are capitalized in accordance with GAAP, and other extraordinary expenses not incurred in the ordinary course of the Fund’s business) to not more than 0.50% of the

average daily net assets of the Fund for the current fiscal year. The current term of the Expense Limitation Agreement remains in effect until January 31, 2020. While there can be no assurance that the Expense Limitation Agreement will

continue after that date, it is expected to continue from year-to-year thereafter.

The Advisor paid the initial organizational costs of the Fund that were incurred prior to commencement of operations, which amounted to $123,370. During the initial period ended September 30, 2015, the Advisor

elected to bear $28,679 of those organizational costs and not make them subject to recoupment. As of September 30, 2019, no organizational costs are still subject to recoupment.

Reimbursements and waivers of expenses by the Advisor are subject to recoupment for a period not to exceed 3 years from the date on which the waiver or reimbursement was made by the Advisor, provided the annual

expense ratio does not exceed 0.50%. Please refer to the table below for a breakdown of the reimbursements and recoupment periods.

|

Fiscal Year/Period End

|

Reimbursement Amount

|

Recoupment Date Expiration

|

|

September 30, 2019

September 30, 2018

|

$539,909

$371,644

|

September 30, 2022

September 30, 2021

|

|

September 30, 2017

|

$365,065

|

September 30, 2020

|

Sub-Advisor

Emerald Separate Account Management, LLC (the “Sub-Advisor”) is responsible for management of the Fund’s investment portfolio according to the Fund’s investment objective, policies, and restrictions. The

Sub-Advisor is subject to the authority of the Board of Trustees and oversight by the Advisor. The Sub-Advisor is entitled to receive an annual sub-advisory fee, paid by the Advisor – not the Fund – for advisory services provided to the Fund,

according to a formula.

Administrator

The Nottingham Company serves as the Fund’s Administrator (the “Administrator”). The Fund pays a monthly fee to the Administrator based upon the average daily net assets of the Fund and subject to a minimum of

$2,000 per month. The Fund incurred $24,067 of fees by the Administrator for the fiscal year ended September 30, 2019.

(Continued)

Aspiration Flagship Fund

Notes to Financial Statements – Continued

As of September 30, 2019

Fund Accounting Services

The Nottingham Company serves as the Fund’s Fund Accounting Services Provider. Under the terms of the Fund Accounting and Administration Agreement, the Fund Accounting Service Provider calculates the daily net

asset value per share and maintains the financial books and records for the Fund. The Fund incurred $28,488 of fees by The Nottingham Company for the fiscal year ended September 30, 2019.

Compliance Services

Cipperman Compliance Services, LLC provides services as the Trust’s Chief Compliance Officer. Cipperman Compliance Services, LLC is entitled to receive customary fees from the Fund for their services pursuant to

the Compliance Services agreement with the Fund. The Fund incurred $28,812 in compliance fees for the fiscal year ended September 30, 2019.

Custodian

UMB Bank, N.A. provides services as the Fund’s custodian. For its services, the Custodian is entitled to receive compensation from the Fund pursuant to the Custodian’s fee arrangements with the Fund. The Fund

paid $62,647 in custody fees for the fiscal year ended September 30, 2019.

Transfer Agent

Nottingham Shareholder Services, LLC (“Transfer Agent”), an affiliate of The Nottingham Company, serves as transfer, dividend paying, and shareholder servicing agent for the Fund. For its services, the Transfer

Agent is entitled to receive compensation from the Fund pursuant to the Transfer Agent’s fee arrangements with the Fund. The Fund paid $180,993 to the Transfer Agent for the fiscal year ended September 30, 2019.

Distributor

Capital Investment Group, Inc. (the “Distributor”) serves as the Fund’s principal underwriter and distributor. The Distributor receives $5,000 per year paid in monthly installments for services provided and

expenses assumed. Additional expenses may be incurred for processing fees during the year. The Fund incurred $5,564 in distribution expenses for the fiscal year ended September 30, 2019. These fees are included in the Shareholder Fulfillment

Fees on the Statement of Operations.

Officers and Trustees of the Trust

As of September 30, 2019, certain officers of the Trust were also officers of the Administrator. Certain Trustees and an officer are also officers of the Advisor.

3. Distribution and Service Fees

The Trustees, including a majority of the Trustees who are not “interested persons” of the Trust as defined in the 1940 Act and who have no direct or indirect financial interest in such plan or in any agreement

related to such plan, adopted a distribution plan pursuant to Rule 12b-1 of the 1940 Act (the “Plan”). The 1940 Act regulates the manner in which a regulated investment company may assume expenses of distributing and promoting the sales of its

shares and servicing of its shareholder accounts. The Plan provides that the Fund may incur certain expenses, which may not exceed 0.25% per annum of the average daily net assets of the Investor Class Shares and 1.00% per annum of the average

daily net assets of the Class C Shares for each year elapsed subsequent to adoption of the Plan, for payment to the Distributor and others for items such as advertising expenses, selling expenses, commissions, travel or other expenses

reasonably intended to result in sales of shares of the Fund or support servicing of shareholder accounts. For the fiscal year ended September 30, 2019, $37,222 in distribution and service fees were incurred by the Investor Class Shares of the

Fund.

4. Purchases and Sales of Investment Securities

For the fiscal year ended September 30, 2019, the aggregate cost of purchases and proceeds from sales of investment securities (excluding short-term securities) were as follows:

|

Purchases of Securities

|

Proceeds from Sales of Securities

|

|

$2,149,776

|

$2,878,901

|

(Continued)

Aspiration Flagship Fund

Notes to Financial Statements – Continued

As of September 30, 2019

5. Federal Income Tax

Distributions are determined in accordance with Federal income tax regulations, which differ from GAAP, and, therefore, may differ significantly in amount or character from net investment income and realized

gains for financial reporting purposes. Financial reporting records are adjusted for permanent book/tax differences to reflect tax character but are not adjusted for temporary differences. There were no such reclassifications as of September

30, 2019.

Management reviewed the Fund’s tax positions taken on federal income tax returns for the open tax years/period from September 30, 2017 through September 30, 2019. As of and during the fiscal year ended September

30, 2019, the Fund does not have a liability for uncertain tax positions. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations. During the fiscal year

ended September 30, 2019, the Fund did not incur any interest or penalties.

The Fund identifies its major tax jurisdictions as U.S. Federal and the State of California where the Trust makes significant investments.

Distributions during the fiscal years ended September 30, 2019 and September 30, 2018 were characterized for tax purposes as follows:

|

|

September 30, 2019 |

September 30, 2018 | |

|

Ordinary Income

|

$ 167,494 |

$126,409 | |

|

Long-Term Capital Gains

|

26,509 | - | |

At September 30, 2019, the tax-basis cost of investments and components of distributable earnings were as follows:

|

Cost of Investments

|

$ |

13,919,073

|

||||

|

Gross Unrealized Appreciation

|

$ |

485,661

|

||||

|

Gross Unrealized Depreciation

|

(163,833)

|

|||||

|

Net Unrealized Appreciation

|

321,828

|

|||||

|

Undistributed Net Investment Income

|

105,368

|

|||||

|

Deferred Post-October Losses

|

(129,514)

|

|||||

|

Accumulated Distributable Earnings

|

$ |

297,682

|

||||

The difference between book-basis and tax-basis net unrealized appreciation (depreciation) is attributable to the deferral of losses from wash sales. In addition, realized losses reflected in the accompanying

financial statements include net capital losses realized between November 1 and the Funds’ fiscal year-end that have not been recognized for tax purposes (Deferred Post-October Losses).

6. Beneficial Ownership

The beneficial ownership, either directly or indirectly, of 25% or more of the voting securities of a fund creates a presumption of control of a fund, under Section 2(a)(9) of the Investment Company Act of 1940.

As of September 30, 2019, there were no control persons of the Fund.

7. Commitments and Contingencies

Under the Trust’s organizational documents, its officers and Trustees are indemnified against certain liabilities arising out of the performance of their duties to the Fund. In addition, in the normal course of

business, the Trust entered into contracts with its service providers, on behalf of the Fund, and others that provide for general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future

claims that may be made against the Fund. The Fund expects risk of loss to be remote.

(Continued)

Aspiration Flagship Fund

Notes to Financial Statements – Continued

As of September 30, 2019

8. New Accounting Pronouncements

In August 2018, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2018-13, Fair Value Measurement (Topic 820) – Disclosure

Framework–Changes to the Disclosure Requirements for Fair Value Measurement. The amendments eliminate certain disclosure requirements for fair value measurements for all entities, requires public entities to disclose certain new

information and modifies some disclosure requirements. The new guidance is effective for all entities for fiscal years beginning after December 15, 2019 and for interim periods within those fiscal years. An entity is permitted to early adopt

either the entire standard or only the provisions that eliminate or modify requirements. The Advisor is currently evaluating the impact of this new guidance on the Fund’s financial statements.

Management has evaluated the need for disclosures and/or adjustments resulting from subsequent events through the date of issuance of these financial statements.

Rescission Offer

Due to an administrative error, the Fund’s prospectus dated January 28, 2018 (the “2018 Prospectus”) incorrectly disclosed the performance of the S&P 500 Total Return Index. In connection with that error,

the Fund offered Fund shareholders the opportunity to rescind any purchases of shares of the Fund (“Eligible Shares”) that were made between January 28, 2018 and February 1, 2019 (the “Affected Period”).

The Fund offered to rescind all sales of Eligible Shares for the following amount: (1) the shareholder’s purchase price for the shares; (2) plus interest, calculated from the purchase date until the date the

rescission payment is made by the Fund using the greater of (i) the interest rate for Federal judgments, determined in accordance with the rate and method of calculation set forth in 28 U.S.C.ss.1961(a) and (b), or (ii) the applicable interest

rate designated by the state law of the state of the shareholder’s residence; (3) minus any dividends declared and paid or payable with respect to such shares. In addition, for shares redeemed prior to receiving this redemption offer, the

shareholder’s prior redemption proceeds would be subtracted from the amount payable under this rescission offer.

The actual cost of the rescission offer cannot be determined at this time because the number of shares purchased by the Fund pursuant to the rescission offer will depend upon a number of factors, including how

many shareholders accept the rescission offer. However, the Fund is not expected to bear any costs or expenses associated with this rescission offer. The Fund’s investment advisor, Aspiration Fund Adviser, LLC, has agreed to pay directly

and/or reimburse the Fund for the full cost of conducting this rescission offer.

This evaluation did not result in any subsequent events that necessitated disclosures and/or adjustments other than those previously noted.

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the shareholders and Board of Trustees

of Aspiration Flagship Fund

of Aspiration Flagship Fund

Opinion on the Financial Statements and Financial Highlights

We have audited the accompanying statement of asset and liabilities, including the schedule of investments of the Aspiration Flagship Fund, one of

the funds constituting the Aspiration Funds (the "Fund"), as of September 30, 2019, the related statements of operations, changes in net assets, and the financial highlights for the year then ended, and the related

notes. In our opinion, the financial statements and financial highlights present fairly, in all material respects, the financial position of the Aspiration Flagship Fund as of September 30, 2019, and the results of its operations, the changes

in its net assets, and the financial highlights for the year then ended in conformity with accounting principles generally accepted in the United States of America.

The statement of changes in net assets and the financial highlights for the year ended September 30, 2018 were audited by another independent registered public accounting firm

whose report, dated November 29, 2018, expressed an unqualified opinion on the statement of changes in net assets and those financial highlights. The financial highlights for the each of the two years in the period ended September 30, 2017

and the period from October 14, 2014 to September 30, 2015 were audited by another independent registered public accounting firm whose report, dated November 29, 2017, expressed an unqualified opinion on those financial highlights.

Basis for Opinion

These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial

statements and financial highlights based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Fund in

accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether

the financial statements and financial highlights are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting.

As part of our audits we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting.

Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements and financial highlights, whether due to error or fraud, and

performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements and financial highlights. Our audits also included evaluating

the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements and financial highlights. Our procedures included confirmation of securities owned as of

September 30, 2019, by correspondence with the custodian and brokers; when replies were not received from brokers, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinion.

Los Angeles, California

November 29, 2019

We have served as the auditor of one or more Aspiration Funds investment companies since 2019.

Aspiration Flagship Fund

Additional Information

(Unaudited)

1. Proxy Voting Policies and Voting Record

A copy of the Trust’s Proxy Voting and Disclosure Policy is included as Appendix B to the Fund’s Statement of Additional Information and are available, without charge, upon request, by calling 800-773-3863,

and on the website of the Securities and Exchange Commission (“SEC”) at sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available (1)

without charge, upon request, by calling the Fund at the number above and (2) on the SEC’s website at sec.gov.

2. Quarterly Portfolio Holdings

The Fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available on the SEC’s website at sec.gov.

You may also obtain copies without charge, upon request, by calling the Fund at 800-773-3863.

3. Tax Information

We are required to advise you within 60 days of the Fund’s fiscal year-end regarding federal tax status of certain distributions received by shareholders during each fiscal year. The following information is

provided for the Fund’s fiscal year ended September 30, 2019.

During the fiscal year ended September 30, 2019, the Fund paid $167,494 in ordinary income distributions and $26,509 in long-term capital gain distributions.

Dividend and distributions received by retirement plans such as IRAs, Keogh-type plans, and 403(b) plans need not be reported as taxable income. However, many retirement plans may need this information for

their annual information meeting.

4. Schedule of Shareholder Expenses

As a shareholder of the Fund, you incur ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses. This Example is intended to help you understand your

ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from April 1, 2019 through September 30, 2019.

Actual Expenses – The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line,

together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (e.g., an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the

first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes – The second line of the table below provides information about hypothetical account values and hypothetical expenses based

on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account

balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in

the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption

fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were

included, your costs would have been higher.

(Continued)

Aspiration Flagship Fund

Additional Information

(Unaudited)

|

Investor Class Shares

|

Beginning

Account Value

April 1, 2019

|

Ending

Account Value

September 30, 2019

|

Expenses Paid

During Period*

|

|

Actual

Hypothetical (5% annual return before expenses)

|

|||

|

$1,000.00

|

$1,020.80

|

$2.53

|

|

|

$1,000.00

|

$1,022.56

|

$2.54

|

*Expenses are equal to the average account value over the period multiplied by the Fund’s annualized expense ratio, multiplied by 183/365 (to reflect the six month period).

5. Information about Trustees and Officers

The business and affairs of the Fund and the Trust are managed under the direction of the Board of Trustees of the Trust. Information concerning the Trustees and officers of the Trust and Fund is set forth

below. Generally, each Trustee and officer serves an indefinite term or until certain circumstances such as their resignation, death, or otherwise as specified in the Trust’s organizational documents. Any Trustee may be removed at a

meeting of shareholders by a vote meeting the requirements of the Trust’s organizational documents. The Statement of Additional Information of the Fund includes additional information about the Trustees and officers and is available,

without charge, upon request by calling the Fund at 800-773-3863. The address of each Trustee and officer, unless otherwise indicated below, is 116 South Franklin Street, Rocky Mount, North Carolina 27804. The Independent Trustees each

received aggregate compensation of $11,280 during the fiscal year ended September 30, 2019 from the Fund for their services to the Fund and Trust.

|

Name, Age

and Address |

Position

held with Funds or Trust |

Length

of Time

Served

|

Principal Occupation

During Past 5 Years |

Number of

Portfolios

in Fund

Complex

Overseen

by Trustee

|

Other Directorships

Held by Trustee During Past 5 Years |

|

Independent Trustees

|

|||||

|

Chuck Daggs

(1947) 116 South Franklin Street Rocky Mount, NC 27804 |

Independent Trustee

|

Since 05/2018

|

Currently Retired; previously Executive Vice President of Wealth Management Group at Wells Fargo from 1998 – 2015.

|

2

|

None.

|

|

Coby A. King

(1960) 116 South Franklin Street Rocky Mount, NC 27804 |

Independent Trustee

|

Since 01/2016

|

President and Chief Executive Officer of High Point Strategies, LLC (Public Affairs Consulting) since 2013; Lobbyist for Ek & Ek, LLC (Public Affairs

Consulting) from 2012 – 2013; Senior Vice President at MWW Group, Inc. (Public Affairs Consulting) from 2008 – 2012.

|

2

|

None.

|

|

David L. Kingsdale

(1963) 116 South Franklin Street Rocky Mount, NC 27804 |

Independent Trustee

|

Since 10/2014

|

Chief Executive Officer of Millennium Dance Media, LLC since 2010; Owner of DLK, Inc. (media consulting agency) since 2005.

|

2

|

The Giving Back Fund; Prime Access Capital.

|

|

Interested Trustees

|

|||||

|

Andrei Cherny

(1975) 116 South Franklin Street Rocky Mount, NC 27804 |

Interested Trustee, Principal Executive Officer and President

|

Trustee Since 08/2017; President Since 2/2014

|

Chief Executive Officer of Aspiration Partners, LLC since 2013; Investor since 2009; previously, Managing Director and Senior Analyst for Burston-Marsteller (Public Relations

and Communications) from 2011 – 2013.

|

2

|

Board Member and President for Democracy: a Journal of Ideas.

|

(Continued)

Aspiration Flagship Fund

Additional Information

(Unaudited)

|

Name, Age

and Address |

Position

held with Funds or Trust |

Length

of Time

Served

|

Principal Occupation

During Past 5 Years |

Number of

Portfolios

in Fund

Complex

Overseen

by Trustee

|

Other Directorships

Held by Trustee During Past 5 Years |

|

Alexandra Horigan

(1983) 116 South Franklin Street Rocky Mount, NC 27804 |

Interested Trustee

|

Since 08/2017

|

Vice President of Operations of Aspiration Partners, Inc. since 2012.

|

2

|

None.

|

|

Other Officers

|

|||||

|

Ashley E. Harris

(1984) 116 South Franklin Street Rocky Mount, NC 27804 |

Treasurer, Principal Financial Officer and Assistant Secretary of the Trust

|

Since 12/2014

|

Fund Accounting Manager and Financial Reporting, The Nottingham Company since 2008.

|

n/a

|

n/a

|

|

Andrew P. Chica

(1975) 116 S. Franklin Street

Rocky Mount, NC 27804

|

Chief Compliance Officer

|

Since 07/2019

|

Compliance Director, Cipperman Compliance Services, LLC (01/2019-Present). Chief Compliance Officer of Hatteras Funds, LP and Hatteras Capital

Distributors, LLC (2007-Present)

|

n/a

|

n/a

|

6. Change of Independent Registered Public Accounting Firm

At a meeting held on September 19, 2019, based on the recommendation of the Audit Committee of the Aspiration Flagship Fund and Aspiration Redwood Fund, each a series of Aspiration Funds (hereinafter referred

to as the “Funds”) and the approval of the Board of Trustees, Ernst & Young, LLP was dismissed as the independent registered public accounting firm for the Funds. At the same meeting, based on the recommendation and approval of the