UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For

the fiscal year ended

or

For the transition period from _________ to _________

Commission file number

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Not applicable. |

Securities registered under Section 12(b) of the Exchange Act: None

Securities registered under Section 12(g) of the Exchange Act: Common Stock, par value $0.0001

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate

by check mark whether the registrant (1) has filed all reports required by Section 13 or 15(d) of the Securities Exchange Act of 1934

during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject

to such filing requirements for the past 90 days. ☐ Yes ☒

Indicate

by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data

File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding

12 months (or for such shorter period that the registrant was required to submit and post such files). ☒

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report. Yes ☐ No

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

The

aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant was approximately $

State the number of shares outstanding of each of the issuer’s classes of common equity, as of the latest practicable date.

| Class | Outstanding April 7, 2023 | |

| Common Stock, $0.0001 par value per share |

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements that involve a number of risks and uncertainties. Although our forward-looking statements reflect the good faith judgment of our management, these statements can be based only on facts and factors of which we are currently aware. Consequently, forward-looking statements are inherently subject to risks and uncertainties. Actual results and outcomes may differ materially from results and outcomes discussed in the forward-looking statements.

Forward-looking statements can be identified by the use of forward-looking words such as “may,” “will,” “should,” “anticipate,” “believe,” “expect,” “plan,” “future,” “intend,” “could,” “estimate,” “predict,” “hope,” “potential,” “continue,” or the negative of these terms or other similar expressions. These statements include, but are not limited to, statements under the captions “Risk Factors,” “Management’s Discussion and Analysis or Plan of Operation” and “Description of Business,” as well as other sections in this report. Such forward-looking statements are based on our management’s current plans and expectations and are subject to risks, uncertainties and changes in plans that may cause actual results to differ materially from those anticipated in the forward-looking statements. You should be aware that, as a result of any of these factors materializing, the trading price of our common stock may decline. These factors include, but are not limited to, the following:

| ● | the availability and adequacy of capital to support and grow our business; | |

| ● | economic, competitive, business and other conditions in our local and regional markets; | |

| ● | actions taken or not taken by others, including competitors, as well as legislative, regulatory, judicial and other governmental authorities; | |

| ● | competition in our industry; | |

| ● | changes in our business and growth strategy, capital improvements or development plans; | |

| ● | the availability of additional capital to support development; and | |

| ● | other factors discussed elsewhere in this annual report. |

The cautionary statements made in this annual report are intended to be applicable to all related forward-looking statements wherever they may appear in this report.

We urge you not to place undue reliance on these forward-looking statements, which speak only as of the date of this report. We undertake no obligation to publicly update any forward looking-statements, whether as a result of new information, future events or otherwise.

All references in this Form 10-K that refer to the “Company”, “Nukkleus”, “we,” “us” or “our” refer to Nukkleus Inc. and its consolidated subsidiaries.

TABLE OF CONTENTS

i

PART I

Item 1. Business.

Nukkleus Inc. (formerly known as, Compliance & Risk Management Solutions Inc.) (the “Company” or “Nukkleus”) was formed on July 29, 2013 in the State of Delaware as a for-profit Company and established a fiscal year end of September 30.

Overview

We are a financial technology company with the aim of providing blockchain-enabled technology solutions.

Nukkleus Technology

Our Nukkleus Technology business unit offers a full-service transactions technology and advisory business providing end-to-end transactions technology solutions. We offer an advanced transactions platform for dealing and risk management with global liquidity and customizable leverage, where users have control over quote and liquidity strategies. Such technology and advisory services are currently offered through our General Services Agreement (“GSA”) with FXDD (for more information see the section captioned “FXDD Agreements” below).

Digital RFQ

Through our Digital RFQ subsidiary, we aim to provide cross-border payment and transactions solutions to institutional investors, and offer blockchain-enabled financial services solutions to institutional investors in a secure, compliant and globally accessible manner. The blockchain-enabled payment gateway we have developed has the capability to deliver global cross-border transfers of fiat currencies using blockchain rails. Digital RFQ currently offers payment and settlement services, including those utilizing blockchain networks, but does not provide custody or wallet services with respect to digital assets, and does not hold digital assets, reducing the risks and regulatory burden on its business. In future, Digital RFQ plans to offer a white-labelled digital bank with end-to-end digital banking solutions for international business. We expect to offer these products in the second or third calendar quarter of 2023. Our competitors in this product category are banks and other financial institutions, and we intend to compete by offering faster and more reliable products using more advanced technology. Products and services offered by Digital RFQ are distributed through our website.

Digital RFQ is regulated in the United Kingdom by the Financial Conduct Authority and is in good standing and is and has been in the past in material compliance with the applicable laws, rules and regulations promulgated thereby. Digital RFQ is subject to Anti Money Laundering (“AML”) and Counter Terrorist Finance (“CTF”) regulations consistent with our authorization by the Financial Conduct Authority as an Electronic Money Directive Agent, among others. For a discussion of the various laws and regulations Digital RFQ is subject.

The “blockchain technology” used by Digital RFQ in its payment processing business includes only advanced-stage and fully tested, well-established and fully collateralized stablecoins operated on the Bitcoin, Ethereum and Tron networks. However, in future, we will be free to use other blockchain networks if we determine that they offer more sophisticated or secure technology. Based on our risk assessments, we determine the appropriate network to use for a particular transaction or customer. We do not use stablecoins of an algorithmic nature, and in the event that we determine any particular stablecoin presents a threat or risk to the security of our business, customers or the transactions we process, we promptly move to another stablecoin network. We do not accept payment in digital assets and do not hold digital assets for investment or offer digital wallet services. For a description of the risks associated with the use of blockchain technology in financial services generally, and payment processing specifically.

DigiClear

Through DigiClear, we plan to develop technology that offers a custody and settlement utility operating system aiming to deliver value and a high-functioning automated post-trade solution. DigiClear aims to provide clients with the means to transfer underlying assets to alternative custodians at any time. We intend for DigiClear to use hardware security modules to offer technology that can secure client assets to block any unwanted modification of client settlement instructions or transfers. We expect that the transfer process that DigiClear’s technology will offer will be fully automated, monitored and can be processed within milliseconds. We expect to offer these products in the second or third calendar quarter of 2023. Our competitors in this product category are banks and other financial institutions and smaller financial technology companies, and we intend to compete by offering faster and more reliable products using more advanced technology. Products and services offered by DigiClear are distributed through our website.

1

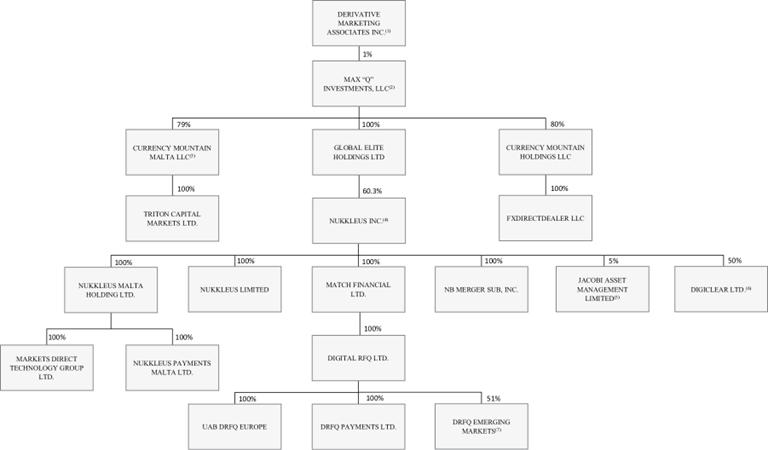

| (1) | Emil Assentato owns 100% of DMA. |

| (2) | Emil Assentato directly owns approximately 85% of Max Q, and indirectly owns an additional 1%. The remainder of Max Q is owned by various individuals and entities unaffiliated with Nukkleus’s officers and directors. |

| (3) | Emil Assentato owns 1% of Currency Mountain Malta LLC, and the remainder of Currency Mountain Malta LLC is owned by Rubens Investment Services, Inc., a wholly owned subsidiary of Compagnie Financière Tradition, a public company based in Switzerland, both of which are unaffiliated with Nukkleus’s officers and directors. |

| (4) | See section entitled “Security Ownership of Certain Beneficial Owners and Management” for director and officer beneficial ownership of Nukkleus shares. As Nukkleus’s common stock is quoted for trading on the OTC Pink Sheets, information on its other owners is not readily available. |

| (5) | Jamal Khurshid and Nicholas Gregory own, directly and indirectly, approximately 40% and 10% of Jacobi, respectively. The remainder of Jacobi is owned by various individuals and entities unaffiliated with Nukkleus’s officers and directors. |

| (6) | Navarock, Ltd., an entity unaffiliated with Nukkleus’s officers and directors, owns the remaining 50% of Digiclear. |

| (7) | Angel Holdings LLC, an entity unaffiliated with Nukkleus’s officers and directors, owns the remaining 49% of DRFQ Emerging Markets. |

Recent Developments

Merger Agreement – Brilliant Acquisition Corporation

On February 22, 2022, Nukkleus entered into an Agreement and Plan of Merger (as it may be amended, supplemented or otherwise modified from time to time, the “Merger Agreement”), by and among Nukkleus and Brilliant Acquisition Corporation, a British Virgin Islands company (“Brilliant”). Upon consummation of the transactions contemplated by the Merger Agreement, Nukkleus would become a Nasdaq-listed company (“PubCo”) and the parent company of Brilliant. The transactions contemplated by the Merger Agreement, are hereinafter referred to as the “Business Combination.

On September 21, 2022, parties to the Merger Agreement entered into an Amendment No. 1 to the Merger Agreement (the “Amendment”) solely to extend the Outside Closing Date (as defined in the Merger Agreement), to the later of (i) October 23, 2022, or, (ii) following the approval by Brilliant’s shareholders of the extension of the life of the SPAC pursuant to Brilliant’s organizational documents, to the date so approved, but not later than January 23, 2023.

On September 28, 2022, parties to the Merger Agreement entered into an Amendment No. 2 to the Merger Agreement (the “Second Amendment”) pursuant to which the parties agreed to increase the amount of the “Backstop Pool” (as defined in the Merger Agreement) of shares to be issued to Brilliant Public Shareholders in the Business Combination from the lower of (1) 506,000, and (2) 20% of the aggregate number of SPAC Shares and SPAC Rights issued and outstanding immediately prior to the Effective Time (each as defined in the Merger Agreement) prior to the Amendment to the lower of (1) 1,012,000, and (2) 40% of the aggregate number of SPAC Shares and SPAC Rights issued and outstanding immediately prior to the Effective Time pursuant to the Amendment.

2

On January 20, 2023, parties to the Merger Agreement entered into an Amendment No. 3 to the Merger Agreement (the “Third Amendment”) solely to extend the Outside Closing Date (as defined in the Merger Agreement), to the later of (i) April 23, 2023, or, (ii) following the approval by Brilliant’s shareholders of the extension of the life of the SPAC pursuant to Brilliant’s organizational documents, to the date so approved, but not later than June 23, 2023.

White Lion Stock Purchase Agreement

On May 17, 2022, Nukkleus entered into a Stock Purchase Agreement (the “White Lion Agreement”) with White Lion Capital Partners, LLC a California-based investment fund (“White Lion”). Under the terms of the White Lion Agreement, Nukkleus has the right, but not the obligation, to require White Lion to purchase shares of Nukkleus common stock up to a maximum amount of $75,000,000 or such lower amount as may be required pursuant to the rules of the market on which shares of Nukkleus common stock trades at such time. Pursuant to terms of the White Lion Agreement and the Registration Rights Agreement (as defined below), Nukkleus is required to use its commercially reasonable efforts to file with the SEC a registration statement covering the shares to be acquired by White Lion within sixty days following the closing of the previously announced business combination with Brilliant Acquisition Corporation described in Nukkleus’s Current Report on Form 8-K filed with the SEC on February 23, 2022 (the “Business Combination”).

The term of the White Lion Agreement commences on the effective date of the registration statement and shall end on December 31, 2024, or, if earlier, the date on which White Lion has purchased the maximum number of shares of Nukkleus Common Stock provided under the White Lion Agreement, in each case on the terms and subject to the conditions set forth in the White Lion Agreement. White Lion’s purchase price will be 96% of the dollar- volume weighted average price of Nukkleus common stock over the two consecutive trading days immediately following receipt of Nukkleus’s notice of its intent to make a draw.

During the term of the White Lion Agreement, on the terms and subject to the conditions set forth therein, Nukkleus may draw up to the lesser of (i) the number of shares of Nukkleus common stock which would result in beneficial ownership by White Lion of more than 4.99% of the outstanding shares of Nukkleus common stock, (ii) the number of shares of Nukkleus common stock equal to 30% of the average daily trading volume of Nukkleus common stock over the five consecutive trading days immediately following the notice date, or (iii) the number of Nukkleus common stock obtained by dividing $1,500,000 by the closing sale price of Nukkleus common stock on the notice date.

Nukkleus is not entitled to draw on the White Lion Agreement if the closing sale price of Nukkleus common stock on the trading day immediately preceding the notice date is less than $1.00 (following the reverse stock split proposed in connection with the closing of the Business Combination and described in Nukkleus’s Current Report on Form 8-K filed with the SEC on February 23, 2022, but adjusted for any other reorganization, recapitalization, non-cash dividend, stock split or other similar transaction). Nukkleus is not entitled to draw on the White Lion Agreement unless each of the following additional conditions is satisfied: (i) each of Nukkleus’s representations and warranties set forth in the White Lion Agreement is true and correct (subject to qualifications as to materiality set forth therein) in all respects as of such time; (ii) a registration statement is and remains effective for the resale of securities in connection with the White Lion Agreement; (iii) the trading of the Company’s common stock shall not have been suspended by the SEC, the applicable trading market or FINRA, or otherwise halted for any reason; (iv) the Company shall have complied with its obligations and shall not otherwise be in breach or default of any agreement set forth in the White Lion Agreement; (v) no statute, regulation, order, guidance, decree, writ, ruling or injunction shall have been enacted, entered, promulgated, threatened or endorsed by any federal, state, local or foreign court or governmental authority of competent jurisdiction, including, without limitation, the SEC, which prohibits the consummation of or which would materially modify or delay any of the transactions contemplated by the White Lion Agreement; (vi) all reports, schedules, registrations, forms, statements, information and other documents required to have been filed by us with the SEC pursuant to the reporting requirements of the Exchange Act of 1934 (other than Forms 8-K) shall have been filed with the SEC within the applicable time periods prescribed for such filings; (vii) to the extent the issuance of the put shares requires shareholder approval under the listing rules of the applicable national exchange or principal quotation system for the Nukkleus common stock, the Company has or will seek such approval; and (viii) certain other conditions as set forth in the White Lion Agreement.

In addition to the shares to be issued under the White Lion Agreement, Nukkleus will include in its registration statement additional shares of Nukkleus common stock in the amount of $750,000 being issued to White Lion in connection with the execution of the White Lion Agreement.

White Lion Registration Rights Agreement

In connection with the Company’s entry into the White Lion Agreement, Nukkleus entered into a Registration Rights Agreement with White Lion (the “Registration Rights Agreement”). Pursuant to the terms of the Registration Rights Agreement, Nukkleus has agreed to use its commercially reasonable efforts to file a registration statement under the Securities Act registering the resale of the shares sold under the White Lion Agreement within sixty days of the closing of the Business Combination. The Registration Rights Agreement also provides that Nukkleus is required to use its commercially reasonable efforts to keep the registration effective and to prepare and file with the SEC such amendments and supplements if the foregoing registration statement is not then in effect, and the Company proposes to file certain types of registration statements under as may be necessary to keep the registration statement effective.

3

FXDD Agreements

On May 24, 2016, Nukkleus Limited entered into a General Service Agreement to provide its software, technology, customer sales and marketing and risk management technology hardware and software solutions package to FML Malta Ltd. In December 2017, Nukkleus Limited, FML Malta Ltd. and Triton Capital Markets Ltd. (“TCM”) entered into a letter agreement providing that there was an error in drafting the General Service Agreement and acknowledging that the correct counter-party to Nukkleus Limited in the General Service Agreement is TCM. Accordingly, all references to FML Malta Ltd. have been replaced with TCM. TCM is a private limited liability company formed under the laws of Malta. The General Service Agreement entered with TCM provides that TCM will pay Nukkleus Limited at minimum $2,000,000 per month. On October 17, 2017, Nukkleus Limited entered into an amendment of the General Service Agreement with TCM. In accordance with the amendment, which was effective as of October 1, 2017, the minimum amount payable by TCM to Nukkleus Limited for services was reduced from $2,000,000 per month to $1,600,000 per month. Emil Assentato is also the majority member of Max Q Investments LLC (“Max Q”), which is managed by Derivative Marketing Associates Inc. (“DMA”). Mr. Assentato is the sole owner and manager of DMA. Max Q owns 79% of Currency Mountain Malta LLC, which in turn is the sole shareholder of TCM.

In addition, on May 24, 2016, in order to appropriately service TCM, Nukkleus Limited entered into a General Service Agreement with FXDIRECT, which provides that Nukkleus Limited will pay FXDIRECT a minimum of $1,975,000 per month in consideration of providing personnel engaged in operational and technical support, marketing, sales support, accounting, risk monitoring, documentation processing and customer care and support. FXDIRECT may terminate this agreement upon providing 90 days’ written notice. On October 17, 2017, Nukkleus Limited entered into an amendment of the General Service Agreement with FXDIRECT. Pursuant to the amendment, which was effective as of October 1, 2017, the minimum amount payable by Nukkleus Limited to FXDIRECT for services was reduced from $1,975,000 per month to $1,575,000 per month. Currency Mountain Holdings LLC is the sole shareholder of FXDIRECT. Max Q is the majority shareholder of Currency Mountain Holdings LLC.

The foregoing descriptions of the terms and conditions of the General Services Agreement with FML Malta Ltd, the amendment to such General Services Agreement, and the General Services Agreement with FXDIRECT are not complete and are qualified in their entirety by the full text of the applicable agreement, which are filed herewith as Exhibit 10.5, Exhibit 10.6 and Exhibit 10.7, respectively, and incorporated herein by reference.

The Market Opportunity

The FX market is a global, decentralized market for the trading of currencies. Nukkleus’s management believes that FX trading involves the simultaneous buying and selling of a currency pair for the purposes of hedging currency risk or to generate a profit. Nukkleus’s management believes that the FX market, once limited to large financial institutions, has expanded and matured over the past decade, and now captures a wide range of participants, including central banks, commercial banks, non-bank corporations, hedge funds, brokers and individual investors and traders. The market’s expansion has helped lead to a significant increase in trading activity. In addition to the increase in the breadth of market participants, management believes the key factors driving higher transaction volumes include the adoption of electronic and high frequency trading, tighter trading spreads, rising volatility among currencies and enhanced access to FX trading markets — primarily through online brokers, such as FXDD — for retail investors.

4

Management believes that FX trading, initially utilized primarily for hedging purposes, has evolved as investor sophistication levels have risen, trading costs have fallen, and as currencies have become increasingly viewed as a viable investment asset class. FX’s low, (or even negative) correlation among certain other portfolio assets, namely equities and fixed income, may help investors reduce overall portfolio volatility. As such, we believe that currencies are often viewed as an important portfolio diversification tool.

Fueled by the growing adoption of the internet, the retail segment of the FX market began to emerge in the late 1990s. Developing online brokerage firms provided individual investors with direct access to the global FX markets. Prior to the development of these trading platforms, we believe that individual retail investors were effectively locked out of the FX market as minimum trade sizes were typically too high for individual retail investors. Online FX brokers lowered the minimum volume barriers and transactions costs for retail trading, allowing individuals to establish trading accounts with much lower initial deposits. We believe the retail FX segment now represents the fastest growing portion of the overall FX market. We believe this growth will be driven by a handful of key market trends, including:

| ● | Increased investor demand for exposure to currencies; | |

| ● | Increasing internet adoption across the globe; | |

| ● | Growing engagement of the “offline” market; | |

| ● | Development of emerging markets and the emergence of an affluent middle class; and | |

| ● | Increasing regulation resulting in greater confidence. |

Participants in the retail FX market are geographically dispersed. Retail FX brokers, such as FXDD are seeking to expand their presence in projected high growth regional areas, such as Asia and the Middle East.

Systems and Services

Nukkleus provides its services in the following service categories, including pursuant to its General Services Agreement with TCM. Under the General Services Agreement, Nukkleus provides software technology and technical support to TCM in each of these service categories.

| ● | Category One: Introducing Broker Dealer Network and the Introducing Broker Interface | |

| ● | Category Two: Chinese and Middle East customer desk support | |

| ● | Category Three: Bridging software to the XWare (MT4 and MT5) platforms | |

| ● | Category Four: Forex Market Liquidity Access | |

| ● | Category Five: Turnkey risk management support software and Risk Management Team | |

| ● | Category Six: Front End Software Retail Trading Platforms and Customer Application Systems | |

| ● | Category Seven: Back Office Systems management |

5

Category One: Introducing Broker Dealer Network

Nukkleus, by arrangement pursuant to our services agreement with TCM and FXDIRECT, provides to TCM clients an introducing broker (IB) network spread across China, Japan and the Middle East. Our approach to the retail FX market is to focus on the development of relationships with independent local referring brokers who provide a recurring source of new customers. These referring brokers do not have an exclusive relationship with us, but are offered a competitive commission structure to deliver new customers to us. Our account managers primarily focus on building relationships with referring brokers, and master referring brokers (who refer other referring brokers to us), as well as with customers referred to us by referring brokers and acquired by us directly. We believe this approach, in contrast to retail FX brokers that focus solely or primarily on acquiring accounts through online marketing campaigns, has allowed us to provide services to TCM, which allows entities to achieve strong levels of net trading income, and accounts, as well as lower up front customer acquisition costs and greater customer satisfaction. Referring brokers are typically either individuals who are current or former FX traders or individuals or companies active in the area of FX trading and education and investment services advisory business.

The Introducing Broker Interface: The Introducing Broker (“IB”) interface empowers our partners to view real time account data such as payouts, customer activity and reports.

Nukkleus delivers the software product in this category to TCM pursuant to the GSA with TCM and does not monitor or measure the number of end users of the software.

Category Two: Asia, including Chinese and Middle East Customer Desk Support

Nukkleus, by arrangement pursuant to our services agreement, provides to TCM customer desk support in multiple languages. A key element of the business strategy is the large, multi-lingual and multi-ethnic team of account managers at the headquarters in Jersey City, New Jersey, as well as in certain other locations such as Malta, Jakarta, Indonesia and Tokyo, Japan. We obtained the services of account managers by virtue of our services agreement with FXDIRECT. Account managers are compensated to a significant degree based on their performance, measured by net deposits inflows, new accounts funded and transaction volume generated by customers. We believe that this compensation structure motivates our account managers and leads to more active communication with our referring brokers and customers, an improved customer trading experience, improved referring broker and customer retention and increased deposits.

Nukkleus delivers the software product in this category to TCM pursuant to the GSA with TCM and does not monitor or measure the number of end users of the software.

Category Three: Bridging Software to the XWare (MT4 and MT5) platforms

XWare 4 Bridge: The MT4 Bridge is a middleware product that connects the XWare server with the XW Trading System. The Bridge passes both market data (i.e. quotes) and trading data (i.e. trade executions) between MT4 and the XW servers. By seamlessly integrating the two, the Bridge allows for real time trade execution, reduced slippage, and access to liquidity through the XW Liquidity Matrix.

Nukkleus delivers the software product in this category to TCM pursuant to the GSA with TCM and does not monitor or measure the number of end users of the software.

Category Four: Forex Market Liquidity Access

XWare Liquidity Matrix: Dealers need access to as much liquidity as possible. Forexware’s liquidity aggregation technology supports API from most of the world’s largest liquidity providers, including banks, hedge funds and electronic communication networks (ECN). Our aggregation technology integrates seamlessly with customers’ existing infrastructure, providing the power to optimize trading processes, manage accounts and revealing the most relevant information to make effective trading decisions.

The XWare Liquidity Bridge: With the XWare liquidity bridge, brokers can automatically submit trade requests to the liquidity provider of choice and receive confirmation prior to sending an “accept” or “reject” message to the broker’s client. The XWare Liquidity Bridge was developed to improve liquidity processes, risk and availability by providing a direct line of communication to vital backend processes. Brokers can create unique price streams from aggregated liquidity with sophisticated control over liquidity sources, pricing models, execution models and risk management.

XWare Live Rate Feed: The XWare Live Rate Feed provides customers with streaming liquidity and prices in real time that integrate seamlessly with existing trading platforms. The Quote Aggregator identifies outliers and bad ticks to ensure our clients capture accurate and reliable pricing to protect them from price fluctuations and anomalies that frequently occur with Liquidity Providers.

Nukkleus delivers the software product in this category to TCM pursuant to the GSA with TCM and does not monitor or measure the number of end users of the software.

6

Category Five: Turnkey Risk Management Support Software, and Risk Management Team

Nukkleus, by arrangement pursuant to our services agreement with FXDIRECT, fields a risk management team of seasoned professionals who constantly monitor liquidity flows and manage the hedging of transactions on a 24 / 7 basis, with three eight-hour shifts. This service is provided both to the TCM clients, as well as to third-party clients who request this service.

XWare Risk Monitor: The XWare Risk Manager is an essential component of the Forexware’s turnkey Xware suite, offered to new brokers entering the market, or existing brokers looking to replace their existing systems. Our management is of the belief that the Risk Manager software suite is the most vigorous and advanced risk management system available in the market today providing customers the power to customize risk management settings at their fingertips.

Nukkleus delivers the software product in this category to TCM pursuant to the GSA with TCM and does not monitor or measure the number of end users of the software.

Category Six: Front End Software Retail Trading Platforms and Customer Application Systems

XWare Trader: is a proprietary platform for retail and institutional traders. It offers fully customizable layouts including colors, layout manager and undocking of windows. Advanced charting, one-click trading, and automated execution for algo traders are all embedded in a modern interface.

Swordfish Trader: Swordfish Trader is a proprietary platform for retail and institutional traders. It offers fully customizable layouts including colors, layout manager, and undocking of windows. Advanced charting, one-click trading, and automated execution for algo traders are all embedded in a modern interface. Swordfish further offers risk management monitors unique from other trading platforms. Nukkleus has also acquired the right to apply for a US federal copyright in relation to Swordfish Trader.

Nukkleus delivers the software product in this category to TCM pursuant to the GSA with TCM and does not monitor or measure the number of end users of the software.

Category Seven: Back Office Systems Management:

XWare Apptracker: Xware Apptracker is a data workflow system designed to automate and manage new customer applications and account information in a centralized location. Xware App Tracker provides customers easy to use tools that save time, organize and track customer application information and manage new customer contract details for fast and efficient review and approval.

Reporting System: This complex and proprietary application generates customized reports, with numerous data queries pre-loaded to run in addition to those a client to choose to customize. It is designed to pull any number of named, defined data fields from both local databases and those from third party-run databases, such as Oracle Financials.

Nukkleus delivers the software product in this category to TCM pursuant to the GSA with TCM and does not monitor or measure the number of end users of the software.

In regard to its Digital RFQ business, Nukkleus currently quantifies and monitors certain metrics and indicators on a weekly, monthly, quarterly, semi-annual, and annual basis, including the following:

| ● | Total Trading Volume, | |

| ● | Total Trading Revenue, | |

| ● | Total Trading Loss, | |

| ● | Total Trading Margin, | |

| ● | Total Trading Clients, | |

| ● | Total Number of Trades, | |

| ● | Average Trading Volume, | |

| ● | Average Trading Loss, | |

| ● | Average Trading Margin. |

7

Intellectual Property

We have several registered trademarks and service marks (US and foreign) and software assets. We also intend to pursue additional foreign trademark registrations. Nukkleus has been assigned various registrations and trademarks relating to:

| ● | Forexware | |

| ● | MTXTREME | |

| ● | Total Broker Solution | |

| ● | Extreme Spreads | |

| ● | When the News Breaks, Be there to Trade it | |

| ● | Swordfish |

Nukkleus has further acquired Patent Number 8799142 in relation to Forexware Patent. This relates to a method of displaying information associated with currency exchange transactions in real time.

In addition to the revenues from our General Services Agreement with TCM, Nukkleus received revenue from financial services through Digital RFQ.

Corporate Office

Nukkleus’s principal executive office is 525 Washington Blvd, 14th Floor, Jersey City, New Jersey 07310. Our main telephone number is 212- 791-4663.

Employees

We have the equivalent to approximately 12 employees, of which 11 employees work for Digital RFQ and one employee works for Nukkleus. Through our relationship with FXDIRECT, we have access to approximately 30 account managers who speak over 10 different languages, and FXDIRECT has contractual relationships with hundreds of referring brokers in at least twenty different countries. It also has contracts with various independent contractors and consultants to fulfill additional needs, including investor relations, exploration, development, permitting, and other administrative functions, and may staff further with employees as it expands activities and brings new projects online.

8

Item 1A. Risk Factors.

Summary of Risk Factors The following summarizes the principal factors that make an investment in our company speculative or risky, all of which are more fully described in the Risk Factors section below. This summary should be read in conjunction with the Risk Factors section and should not be relied upon as an exhaustive summary of the material risks facing our business. The following factors could result in harm to our business, reputation, revenue, financial results, and prospects, among other impacts:

Risks Related to Nukkleus’s Business

| ● | We have a limited operating history in an evolving and highly volatile industry, which makes it difficult to evaluate our future prospects and may increase the risk that we will not be successful. |

| ● | If we do not effectively manage our growth and the associated demands on our operational, risk management, sales and marketing, technology, compliance and finance and accounting resources, our business may be adversely impacted. |

| ● | We face intense and increasing competition and, if we do not compete effectively, our competitive positioning and our operating results will be harmed. |

| ● | We currently compete at multiple levels with a variety of competitors. |

| ● | Cyberattacks and security breaches of our systems, or those impacting our customers or third parties, could adversely impact our brand and reputation and our business, operating results and financial condition. |

| ● | We may incur significant liability as a result of ongoing disputes. |

| ● | Any significant disruption in our technology could adversely impact our brand and reputation and our business, operating results, and financial condition. |

| ● | We rely on third parties in critical aspects of our business, which creates additional risk. Our ability to offer our services depends on relationships with other financial services institutions and entities, and our inability to maintain existing relationships or to enter into new such relationships could impact our ability to offer services to customers. |

| ● | Our banking relationships for transaction processing are concentrated in a small number of partners. |

| ● | Certain large customers provide a significant share of our revenue and the termination of such agreements or reduction in business with such customers could harm our business. If we lose or are unable to renew these and other marketplace and enterprise client contracts at favorable terms, our results of operations and financial condition may be adversely affected. |

| ● | Our products and services may be exploited to facilitate illegal activity such as fraud, money laundering, gambling, tax evasion, and scams. If any of our customers use our products or services to further such illegal activities, we could be subject to liability and our business could be adversely affected. Our efforts to detect and monitor such transactions for compliance with law may require significant costs, and our failure to effectively deal with bad, fraudulent or fictitious transactions and material internal or external fraud could negatively impact our business. |

| ● | Our compliance and risk management methods might not be effective and may result in outcomes that could adversely affect our reputation, operating results, and financial condition. We rely on third parties for some of our KYC and other compliance obligations. |

| ● | We rely on connectivity with blockchain networks for our Platforms. |

| ● | If we fail to develop, maintain, and enhance our brand and reputation, our business, operating results, and financial condition may be adversely affected. Moreover, unfavorable media coverage could negatively affect our business. |

9

| ● | Our future growth depends significantly on our marketing efforts, and if our marketing efforts are not successful, our business and results of operations will be harmed. |

| ● | Concerns about the environmental impacts of blockchain technology could adversely impact usage and perceptions of Nukkleus, its subsidiaries and our Platforms. |

| ● | The COVID-19 pandemic could have unpredictable, including adverse, effects on our business, operating results, and financial condition. |

| ● | As a remote-first company, we are subject to heightened operational and cybersecurity risks. |

Risks Related to Nukkleus’s Platforms

| ● | Our product offerings are centered on WebTrader, MetaTrader, XWare, Forexware and certain other platforms and product offerings (together, our “Platforms”). The regulatory landscape as it relates to processing payment transactions, including through our Platforms, continues to evolve. Such evolution may create additional regulatory burden and expense and could materially impact the use and adoption of our Platforms. |

| ● | The future development and growth of our Platforms is subject to a variety of factors that are difficult to predict and evaluate and may be in the hands of third parties to a substantial extent. If our Platforms do not grow as we expect, our business, operating results, and financial condition could be adversely affected. |

| ● | Due to unfamiliarity and some negative publicity associated with blockchain technology, our customer base may lose confidence in products and services that utilize blockchain technology. |

| ● | Our Platforms and blockchain-enabled payment processing services are innovative and are difficult to analyze vis-à-vis existing financial services laws and regulations around the world. Our platforms involve certain risks, including reliance on third parties, which could limit or restrict our ability to offer the product in certain jurisdictions. |

Risks Related to Nukkleus’s Financial Condition

| ● | There is no assurance that we will maintain profitability or that our revenue and business models will be successful. |

| ● | We may experience fluctuations in our quarterly operating results. |

| ● | Our financial forecasts, which were presented to Nukkleus’s Board and are included in this proxy statement/prospectus, may not prove to be accurate. |

| ● | Changes in U.S. and foreign tax laws, as well as the application of such laws, could adversely impact our financial position and operating results. |

| ● | If our estimates or judgment relating to our critical accounting policies prove to be incorrect, our operating results could be adversely affected. |

| ● | The nature of our business requires the application of complex financial accounting rules, and there is limited guidance from accounting standard setting bodies. If financial accounting standards undergo significant changes, our operating results could be adversely affected. |

10

| ● | Business metrics and other estimates are subject to inherent challenges in measurement, and our business, operating results, and financial condition could be adversely affected by real or perceived inaccuracies in those metrics. |

| ● | We are subject to changes in financial reporting standards or policies, including as a result of choices made by us, which could materially adversely affect our reported results of operations and financial condition and may have a corresponding material adverse impact on capital ratios. |

| ● | As a public company, we are required to develop and maintain proper and effective internal controls over financial reporting, and any failure to maintain the adequacy of these internal controls may adversely affect investor confidence in our company and, as a result, the value of our stock. |

| ● | We might require additional capital to support business growth, and this capital might not be available or may require stockholder approval to obtain. |

| ● | We may be affected by fluctuations in currency exchange rates |

Risks Related to Nukkleus’s Employees and Other Service Providers

| ● | In the event of employee or service provider misconduct or error, our business may be adversely impacted. |

| ● | The loss of one or more of our key personnel, or our failure to attract and retain other highly qualified personnel in the future, could adversely impact our business, operating results, and financial condition. |

| ● | Our culture emphasizes innovation, and if we cannot maintain this culture as we grow, our business and operating results could be adversely impacted. |

| ● | Our officers, directors, employees, and large stockholders may encounter potential conflicts of interests with respect to their positions or interests in certain entities, and other initiatives, which could adversely affect our business and reputation. |

Risks Related to Government Regulation

| ● | We are subject to various laws and regulations, and any adverse changes to, or our failure to comply with, any laws and regulations could adversely affect our brand, reputation, business, operating results, and financial condition. |

| ● | Legislative and regulatory actions taken now or in the future may increase our costs and impact our business, governance structure, financial condition or results of operations. |

| ● | The regulatory environment to which we are subject gives rise to various licensing requirements, legal and financial compliance costs and management time, and non-compliance could result in monetary and reputational damages, all of which could have a material adverse effect on our business, financial position and results of operations. |

| ● | The financial services industry is subject to intensive regulation. Major changes in laws and regulations, as well as enforcement actions, could adversely affect our business, financial position, results of operations and prospects. |

| ● | We are subject to laws, regulations, and executive orders regarding economic and trade sanctions, anti-bribery, anti-money laundering, and counter-terror financing that could impair our ability to compete in international markets or subject us to criminal or civil liability if we violate them. As we continue to expand and localize our international activities, our obligations to comply with the laws, rules, regulations, and policies of a variety of jurisdictions will increase and we may be subject to investigations and enforcement actions by U.S. and non-U.S. regulators and governmental authorities. |

11

| ● | Our consolidated balance sheets may not contain sufficient amounts or types of regulatory capital to meet the changing requirements of our various regulators worldwide, which could adversely affect our business, operating results, and financial condition. |

| ● | We obtain and process a large amount of sensitive customer data. Any real or perceived improper use of, disclosure of, or access to such data could harm our reputation, as well as have an adverse effect on our business. |

| ● | We are subject to complex and evolving laws, regulations, and industry requirements related to data privacy, data protection and information security across different markets where we conduct our business, including in the EEA, such laws, regulations, and industry requirements are constantly evolving and changing. Our actual or perceived failure to comply with such laws, regulations, and industry requirements, or our privacy policies/notices could harm our business by impairing customer trust and could subject us to fines and reputational harm. |

| ● | We are and may continue to be subject to litigation, including individual and class action lawsuits, as well as regulatory audits, disputes, inquiries, investigations and enforcement actions by regulators and governmental authorities. |

Risks Related to Nukkleus’s Intellectual Property

| ● | Our intellectual property rights are valuable, and any inability to protect them could adversely impact our business, operating results, and financial condition. |

| ● | In the future we may be sued by third parties for alleged infringement of their proprietary rights. |

General Risk Factors

| ● | The SEC has adopted amendments to Rule 15c2-11 under the Securities Exchange Act of 1934, which could adversely affect our common stock. |

| ● | Adverse economic conditions may adversely affect our business. |

| ● | We may be adversely affected by natural disasters, pandemics, and other catastrophic events, and by man-made problems such as war or terrorism, that could disrupt our business operations, and our business continuity and disaster recovery plans may not adequately protect us from a serious disaster. |

| ● | Acquisitions, joint ventures or other strategic transactions create certain risks and may adversely affect our business, financial condition or results of operations. |

| ● | Delaware law and our Certificate of Incorporation and Bylaws will contain certain provisions, including anti-takeover provisions that limit the ability of stockholders to take certain actions and could delay or discourage takeover attempts that stockholders may consider favorable. |

12

Risks Related to Nukkleus’s Business

We have a limited operating history in an evolving and highly volatile industry, which makes it difficult to evaluate our future prospects and may increase the risk that we will not be successful.

Nukkleus was formed in 2013 and since then our business model has continued to evolve. In 2021, we acquired a controlling interest in Match. In 2019, our Digital RFQ indirect subsidiary, and wholly owned subsidiary of Match, began to operate a payment processing business partly using blockchain technology. The comparability of our results in prior quarterly or annual periods should not be viewed as an indication of future performance. The “blockchain technology” used by Digital RFQ in its payment processing business and referred to throughout this proxy statement/prospectus is intended to refer to stablecoins operated on the Bitcoin, Ethereum and Tron networks, or such other blockchain networks as Digital RFQ may determine to be reliable and well established in the financial services industry, at an advanced stage and fully tested and collaterialized based on certain criteria summarized below. The blockchain networks used by Digital RFQ in its payment processing business are maintained and operated by third parties.

Because Digital RFQ makes use of blockchain technology only to process payments and does not hold digital assets, the criteria for the adoption and use of any blockchain network may differ from those of investors in stablecoins. Digital RFQ evaluates each blockchain and/or stablecoin on a daily and transaction-by-transaction basis, to minimize any risk associated with the blockchain or stablecoin and to ensure that Digital RFQ can reliably complete the transaction in and out of the stablecoin quickly to minimize such risk. Digital RFQ determines that a blockchain or stablecoin is suitable for use in its payment processing services by assessing the following criteria:

| ● | First, how widely supported is the blockchain stablecoin combination by Digital RFQ’s trading partners, including the banks and financial institutions Digital RFQ uses to support its business. Having sufficient trading partners that support the blockchain or stablecoin means there may be multiple choices of blockchain to use for any given trade. |

| ● | Second, whether there is sufficient liquidity in those partners’ holdings of the stablecoin to ensure Digital RFQ is able to trade in or out without exposure to volatility and price risk. |

To determine whether any blockchain technology meets Digital RFQ’s requirements and is a suitable candidate for use in Digital RFQ’s payment processing business, we assess the following criteria. We monitor these criteria for each blockchain or stablecoin we use regularly on an ongoing basis:

| ● | Market share. Digital RFQ assesses a blockchain or stablecoin’s share of the stablecoin market as a whole and market capitalization from publicly available information. Some stablecoins have been in existence longer than others and may have a larger market share and market capitalization. These factors also have an influence on the market perception of such stablecoins. For example, USDT ‘Tether’ is the most prominent stablecoin measured by market capitalization but has faced auditing issues, while newer products such as GBPT have had professional Big Four auditors from inception but do not have material market share to date and thus would not be perceived or assessed as at an advanced stage or well established. |

| ● | Auditing and Collateralization. Auditing is paramount to the security and stability of stablecoins and for this reason Digital RFQ will only work with firms that adhere to full collateralization that is independently verified by an outside auditor. Digital RFQ believes that collateralization is key in maturing stablecoins. For example, the UST Terra Luna ‘collapse’ showed that algorithmically-backed stability creates vulnerability to counterparty mismanagement and influence, driven by the difficulty and lack of auditing and intrinsic connection to the Terra network itself. In contrast, collateralized stablecoins such as USDT and USDC are fully backed by reserve fiat currency holdings and can be redeemed by holders for such fiat currency. Digital RFQ also views traditional markets, while much more established, as not completely free of risk since they rely substantially on fractional reserve banking to maintain the market. |

| ● | Counterparty Risk. Digital RFQ assesses counterparty risk in its stablecoin and blockchain selection in the issuer of the stablecoin and its governance and in the banks and financial institutions it uses to source liquidity. Digital RFQ assesses the degree of governance decentralization that may give direct control over funds (as backing, for example) or attack vectors to the governance architecture that could expose control over funds, and determines the degree of counterparty risk from the level of centralization. To assess the degree of centralization, Digital RFQ examines the number of parties controlling the blockchain protocol, the number of holders and the level of founder backing (demonstrated by founders holding a significant amount of the stablecoin). Digital RFQ is able to remain operationally stable throughout any given payment processing transaction due primarily to a robust counterparty infrastructure and minimal exposure to these ‘transit’ legs of the transaction (for more information on the third parties involved in Digital RFQ’s payment processing business, please refer to the section titled “We rely on connectivity to blockchain networks for our Platforms”. |

13

| ● | Smart Contract Risk. Smart contract risk relates to the technical security of a blockchain or stablecoin based on its underlying code. If one of the supported stablecoins or other digital currencies is compromised, collateral will be affected, thus threatening the solvency of the blockchain protocol. Projects must have undergone audits to be considered. We assess maturity based on the number of days and the number of transactions of the smart contract as a representation of use, community and development. These proxies show how strong the code is. |

However, because Digital RFQ makes use of blockchain technology only to process payments, and does not hold digital assets, we are able to constantly monitor the status of any blockchain network or stablecoin before, during and after a payment is processed, and determine which of the available blockchain networks is suitable for a particular transaction. We therefore do not believe we are exposed to material risks associated with holding stablecoins or other digital assets. Furthermore, we do not use stablecoins of an algorithmic nature, and in the event that we determine any particular stablecoin presents a threat or risk to the security of our business, customers or the transactions we process, we promptly move to another stablecoin network. We do not accept payment in digital assets and do not hold digital assets for investment or offer digital wallet services.

Because we have a limited history operating our business at its current scale and scope, it is difficult to evaluate our current business and future prospects, including our ability to plan for and model future growth. For example, recently launched services require substantial resources and there is no guarantee that such expenditures will result in profit or growth of our business. The rapidly evolving nature of the market in which we operate, substantial uncertainty concerning how these markets may develop, and other economic factors beyond our control, reduces our ability to accurately forecast quarterly or annual revenue. Failure to manage our current and future growth effectively could have an adverse effect on our business, operating results, and financial condition.

If we do not effectively manage our growth and the associated demands on our operational, risk management, sales and marketing, technology, compliance and finance and accounting resources, our business may be adversely impacted.

We have experienced recent significant growth through our acquisition of Match. In our recent acquisitions, including our acquisition of Match, our business has become increasingly complex by expanding the services we offer to include financial services and payment processing services. To effectively manage and capitalize on our growth, we must continue to expand our information technology and financial, operating, and administrative systems and controls, and continue to manage headcount, capital, and processes efficiently. Our continued growth could strain our existing resources, and we could experience ongoing operating difficulties in managing our business as it expands across numerous jurisdictions, including difficulties in hiring, training, and managing an employee base. Failure to scale and preserve our company culture with growth could harm our future success, including our ability to retain and recruit personnel and to effectively focus on and pursue our corporate objectives. If we do not adapt to meet these evolving challenges, or if our management team does not effectively scale with our growth, we may experience erosion to our brand, the quality of our products and services may suffer, and our company culture may be harmed. Moreover, the failure of our systems and processes could undermine our ability to provide accurate, timely, and reliable reports on our financial and operating results, including the financial statements provided herein, and could impact the effectiveness of our internal controls over financial reporting. In addition, our systems and processes may not prevent or detect all errors, omissions, or fraud, though we have experienced no such material errors, omissions or fraud in the past. For example, our employees may fail to identify transaction errors or fraudulent information provided by our customers. Any of the foregoing operational failures could lead to noncompliance with laws, loss of operating licenses or other authorizations, or loss of bank relationships that could substantially impair or even suspend company operations.

We intend to continue to develop our technology, in particular our blockchain-enabled payment processing offering. Successful implementation of this strategy may require significant expenditures before any substantial associated revenue is generated and we cannot guarantee that these increased investments will result in corresponding and offsetting revenue growth. Our growth may not be sustainable and depends on our ability to retain existing customers, attract new customers, expand product offerings, and increase processed volumes and revenue from both new and existing customers.

The future growth of our business depends on its ability to retain existing customers, attract new customers as well as getting existing customers and new customers to increase the volumes processed through our payments platform and therefore grow revenue. Our customers are not subject to any minimum volume commitments and they have no obligation to continue to use our services, and we cannot be sure that customers will continue to use our services or that we will be able to continue to attract new volumes at the same rate as we have in the past.

A customer’s use of our services may decrease for a variety of reasons, including the customer’s level of satisfaction with our products and services, the expansion of business to offer new products and services, the effectiveness of our support services, the pricing of our products and services, the pricing, range and quality of competing products or services, the effects of global economic conditions, regulatory or financial institution limitations, trust, perception and interest in foreign exchange and payment processing services and in our products and services, or reductions in the customer’s payment and transfer activity. Furthermore, the complexity and costs associated with switching to a competitor may not be significant enough to prevent a customer from switching service providers, especially for larger customers who commonly engage more than one payment service provider at any one time.

Any failure by us to retain existing customers, attract new customers, and increase revenue from both new and existing customers could materially and adversely affect our business, financial condition, results of operations and prospects. These efforts may require substantial financial expenditures, commitments of resources, developments of our processes, and other investments and innovations.

14

We face intense and increasing competition and, if we do not compete effectively, our competitive positioning and our operating results will be harmed.

We operate in a rapidly changing and highly competitive industry, and our results of operations and future prospects depend on, among other things:

| ● | the growth of our customer base, |

| ● | our ability to monetize our customer base, |

| ● | our ability to acquire customers at a lower cost, and |

| ● | our ability to increase the overall value to us of each of our customers while they use our products and services. |

Despite the regulatory barriers to enter the markets we serve, we expect our competition to continue to increase. In addition to established enterprises, we may also face competition from early-stage companies attempting to capitalize on the same, or similar, opportunities as we are. Some of our current and potential competitors have longer operating histories, particularly with respect to our digital financial services products, significantly greater financial, technical, marketing and other resources, and a larger customer base than we do. This allows them, among others, to potentially offer more competitive pricing or other terms or features, a broader range of digital financial products, or a more specialized set of specific products or services, as well as respond more quickly than we can to new or emerging technologies and changes in customer preferences.

Our existing or future competitors may develop products or services that are similar to our products and services or that achieve greater market acceptance than our products and services. This could attract new customers away from our services and reduce our market share in the future. Additionally, when new competitors seek to enter our markets, or when existing market participants seek to increase their market share, these competitors sometimes undercut, or otherwise exert pressure on, the pricing terms prevalent in that market, which could adversely affect our market share and/or ability to capitalize on new market opportunities.

We currently compete at multiple levels with a variety of competitors, including:

| ● | payment platforms; |

| ● | banks and non-bank financial institutions (including without limitation those using the Society for Worldwide Interbank Financial Telecommunication (SWIFT) payment system); and |

| ● | foreign exchange and derivative, including contract for difference (“CFD”), transfer processors. |

Because we do not currently control a bank or a bank holding company, we may be subject to regulation by a variety of state, federal and international regulators across our products and services and we rely on third-party banks to provide payment-processing services to our customers. This regulation by federal, state and international authorities increases our compliance costs, as we navigate multiple regimes with different examination schedules and processes and varying disclosure requirements.

We believe that our ability to compete depends upon many factors, both within and beyond our control, including the following:

| ● | the size, diversity and activity levels of our customer base; |

| ● | the timing and market acceptance of products and services, including developments and enhancements to those products and services offered by us and our competitors; |

| ● | customer service and support efforts; |

15

| ● | selling and marketing efforts; |

| ● | the ease of use, performance, price and reliability of solutions developed either by us or our competitors; |

| ● | changes in economic conditions, regulatory and policy developments; |

| ● | our ability to successfully execute on our business plans; |

| ● | our ability to enter new markets; |

| ● | general digital payments, capital markets, blockchain and stablecoin market conditions; |

| ● | the ongoing impact of the COVID-19 pandemic; and |

| ● | our brand strength relative to our competitors. |

Our current and future business prospects demand that we act to meet these competitive challenges but, in doing so, our revenue and results of operations could be adversely affected if we, for example, increase marketing expenditures or make other expenditures. All of the foregoing factors and events could adversely affect our business, financial condition, results of operations, cash flows and future prospects.

Cyberattacks and security breaches of our systems, or those impacting our customers or third parties, could adversely impact our brand and reputation and our business, operating results and financial condition.

Our business involves the collection, storage, processing and transmission of confidential information, customer, employee, service provider and other personal data, as well as information required to access customer assets. We have built our reputation on the premise that our products and services offer customers a secure way to accept and make payments and store value. As a result, any actual or perceived security breach of us or our third-party partners may:

| ● | harm our reputation and brand; |

| ● | result in our systems or services being unavailable and interrupt our operations; |

| ● | result in improper disclosure of data and violations of applicable privacy and other laws; |

| ● | result in significant regulatory scrutiny, investigations, fines, penalties, and other legal, regulatory and financial exposure; |

| ● | cause us to incur significant remediation costs; |

| ● | lead to theft or irretrievable loss of our or our customers’ assets; |

| ● | reduce customer confidence in, or decreased use of, our products and services; |

| ● | divert the attention of management from the operation of our business; |

| ● | result in significant compensation or contractual penalties from us to our customers or third parties as a result of losses to them or claims by them; and |

| ● | adversely affect our business and operating results. |

Further, any actual or perceived breach or cybersecurity attack directed at other financial institutions or blockchain companies, whether or not we are directly impacted, could lead to a general loss of customer confidence in the use of technology to conduct financial transactions, which could negatively impact us including the market perception of the effectiveness of our security measures and technology infrastructure.

16

An increasing number of organizations, including large businesses, technology companies and financial institutions, as well as government institutions, have disclosed breaches of their information security systems, some of which have involved sophisticated and highly targeted attacks, including on their websites, mobile applications, and infrastructure. Attacks upon systems across a variety of industries, including the payment processing, forex and CFD industry, are increasing in their frequency, persistence, and sophistication, and, in many cases, are being conducted by sophisticated, well-funded, and organized groups and individuals, including state actors. The techniques used to obtain unauthorized, improper, or illegal access to systems and information (including customers’ personal data and digital assets), disable or degrade services, or sabotage systems are constantly evolving, may be difficult to detect quickly, and often are not recognized or detected until after they have been launched against a target. These attacks may occur on our systems or those of our third-party service providers or partners. Certain types of cyberattacks could harm us even if our systems are left undisturbed. For example, attacks may be designed to deceive employees and service providers into releasing control of our systems to a hacker, while others may aim to introduce computer viruses or malware into our systems with a view to stealing confidential or proprietary data. Additionally, certain threats are designed to remain dormant or undetectable until launched against a target and we may not be able to implement adequate preventative measures.

Although we do not have a past history of material security breaches or cyberattacks, and do not believe we are a target of such breaches or attacks, we have developed systems and processes designed to protect the data we manage, prevent data loss and other security breaches, effectively respond to known and potential risks. We expect to continue to expend significant resources to bolster these protections, but there can be no assurance that these security measures will provide absolute security or prevent breaches or attacks. Threats can come from a variety of sources, including criminal hackers, hacktivists, state-sponsored intrusions, industrial espionage, and insiders. Certain threat actors may be supported by significant financial and technological resources, making them even more sophisticated and difficult to detect. As a result, our costs and the resources we devote to protecting against these advanced threats and their consequences may increase over time.

Although we maintain insurance coverage that we believe is adequate for our business, it may be insufficient to protect us against all losses and costs stemming from security breaches, cyberattacks, and other types of unlawful activity, or any resulting disruptions from such events. Outages and disruptions of our systems, including any caused by cyberattacks, may harm our reputation and our business, operating results, and financial condition.

We may incur significant liability as a result of ongoing disputes.

We were party to the BT Prime Litigation, and the case against us has now been dismissed with prejudice with no material liability to us. We may be subject to various other legal proceedings, consumer arbitrations, and regulatory investigation matters. If any of these matters are resolved unfavorably to us, our business and results of operations may be adversely affected.

17

Any significant disruption in our technology could adversely impact our brand and reputation and our business, operating results, and financial condition.

Our reputation and ability to grow our business depends on our ability to operate our service at high levels of reliability, scalability, and performance, including the ability to process and monitor, on a daily basis, a large number of transactions that occur at high volume and frequencies across multiple systems. The proper functioning of our products and services, the ability of our customers to make and receive payments, and our ability to operate at a high level, are dependent on our ability to access the blockchain networks underlying our Platforms and other supported blockchain-based products and technology, for which access is dependent on our systems’ ability to access the internet. Further, the successful and continued operations of such blockchain networks will depend on a network of computers, miners, or validators, and their continued operations, all of which may be impacted by service interruptions.

Our systems, the systems of our third-party service providers and partners, and certain blockchain networks, have experienced from time to time and may experience in the future service interruptions or degradation because of hardware and software defects or malfunctions, distributed denial-of-service and other cyberattacks, insider threats, break-ins, sabotage, human error, vandalism, earthquakes, hurricanes, floods, fires, and other natural disasters, power losses, disruptions in telecommunications services, fraud, military or political conflicts, terrorist attacks, computer viruses or other malware, or other events. In addition, extraordinary site usage could cause our computer systems to operate at an unacceptably slow speed or even fail. Some of our systems, including systems of companies we have acquired, or the systems of our third-party service providers and partners are not fully redundant, and our or their disaster recovery planning may not be sufficient for all possible outcomes or events.

If any of our systems, or those of our third-party service providers, are disrupted for any reason, our products and services may fail, resulting in unanticipated disruptions, slower response times and delays in our services, including our customers’ payments through our Platforms. This could lead to failed or unauthorized payments, incomplete or inaccurate accounting, loss of customer information, increased demand on limited customer support resources, customer claims, and complaints with regulatory organizations, lawsuits, or enforcement actions.

A prolonged interruption in the availability or reduction in the availability, speed, or functionality of our products and services could harm our business. Frequent or persistent interruptions in our services could cause current or potential customers or partners to believe that our systems are unreliable, leading them to switch to our competitors or to avoid or reduce the use of our products and services, and could permanently harm our reputation and brands.

Moreover, to the extent that any system failure or similar event results in damages to our customers or their business partners, these customers or partners could seek significant compensation or contractual penalties from us for their losses, and those claims, even if unsuccessful, are likely to be time-consuming and costly for us to address. Problems with the reliability or security of our systems would harm our reputation, and damage to our reputation and the cost of remedying these problems could negatively affect our business, operating results, and financial condition.

In addition, we are continually improving and upgrading our information systems and technologies. Implementation of new systems and technologies is complex, expensive, time-consuming, and may not be successful. If we fail to timely and successfully implement new information systems and technologies, or improvements or upgrades to existing information systems and technologies, or if such systems and technologies do not operate as intended, it could have an adverse impact on our business, internal controls (including internal controls over financial reporting), operating results, and financial condition.