As filed with the Securities and Exchange Commission on March 30, 2018

Registration No. 333-222208

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Amendment No. 3 to

FORM

S-1

REGISTRATION STATEMENT UNDER

THE SECURITIES ACT OF 1933

AERKOMM INC.

(Exact name of registrant as specified in its charter)

| Nevada | 4899 | 46-3424568 | ||

| (State

or other jurisdiction of incorporation or organization) |

(Primary

Standard Industrial Classification Code Number) |

(I.R.S.

Employer Identification No.) |

923 Incline Way #39

Incline Village, NV 89451

(877) 742-3094

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Jeffrey Wun

Chief Executive Officer

Aerkomm Inc.

923 Incline Way #39

Incline Village, NV 89451

(877) 742-3094

(Names, addresses and telephone numbers of agents for service)

Copy to:

Louis A. Bevilacqua, Esq. BEVILACQUA PLLC 1050 Connecticut Avenue NW Suite 500 Washington, DC 20036 (202) 869-0888 |

Fang Liu, Esq. Mei & Mark LLP 818 18th Street NW, Suite 410 Washington, DC 20006-3506 (888) 860-5678 |

Approximate date of commencement of proposed sale to public: From time to time after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | |

| Non-accelerated filer ☐ (Do not check if a smaller reporting company) | Smaller reporting company ☒ | |

| Emerging growth company ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered | Amount

to be Registered(1) |

Proposed maximum offering price per security(2) |

Proposed

maximum aggregate offering price(2)(3) |

Amount

of registration fee(4) |

||||||||||||

| Common Stock, par value $0.001 per share | 8,117,647 shares | $ | 8.50 |

$ | 69,000,000 | $ | 8,590.50 | |||||||||

| Underwriter Warrants (5) | - | |||||||||||||||

| Shares of Common Stock Underlying Underwriter Warrants (6) | 487,059 | $ | 5,175,000 |

$ | 644.29 |

|||||||||||

| (1) | Pursuant to Rule 416 under the Securities Act of 1933, as amended (the “Securities Act”), the shares being registered hereunder include such indeterminate number of shares of common stock as may be issuable with respect to the shares being registered hereunder as a result of stock splits, stock dividends or similar transactions. |

| (2) | Estimated solely for the purposes of calculating the registration fee pursuant to Rule 457 under the Securities Act of 1933, as amended. |

| (3) | Includes shares that may be sold pursuant to the exercise of a 45-day option granted to the underwriter to cover over-subscriptions, if any. |

| (4) | These fees have been paid in full. |

| (5) | In accordance with Rule 457(g) under the Securities Act, because the shares of the registrant’s shares of common stock underlying the Underwriter Warrants are being registered hereby, no separate registration fee is required with respect to the warrants registered hereby. |

| (6) | We have agreed to issue, on the closing date of this offering, warrants to our underwriter, exercisable at a rate of one warrant per share to purchase up to 6.0% of the securities sold by the Registrant in this offering (the “Underwriter Warrants”). Assuming an offering price of $8.50 per share and full exercise of the underwriter’s over-subscription option, on the closing date the underwriter would receive Underwriter Warrants to purchase 487,059 shares of our common stock at an aggregate purchase price of $5,175,000. The exercise price of the Underwriter Warrants is equal to 125% of the price of the common stock offered hereby. The Underwriter Warrants are exercisable within five years of the effective date of this registration statement. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MARCH 30, 2018

AERKOMM iNC.

UP TO $60,000,000 OF SHARES OF COMMON STOCK

We are offering up to $60,000,000 of shares of common stock on a best efforts basis as described in this prospectus, with a minimum offering amount of approximately $5,000,000, and a maximum offering amount of $60,000,000. We expect that the price to the public in this offering will be $8.50 per share.

Our common stock is quoted for trading on the OTC Markets Group Inc. OTCQX Best Market under the symbol “AKOM.” On March 28, 2018, the last reported sale price of our common stock on OTCQX was $7.5. After the effective date of the registration statement relating to this prospectus and following the filing of audited financial statements for our changed fiscal year end ending March 31, 2018 (as discussed in more detail below), we plan to file an application to the have the shares of common stock offered under this prospectus listed on either the New York Stock Exchange, or NYSE, or the Nasdaq Stock Market, or Nasdaq, under the symbol “AKOM.”

INVESTING IN OUR SECURITIES INVOLVES SIGNIFICANT RISKS. YOU SHOULD CAREFULLY READ “RISK FACTORS” BEGINNING ON PAGE 8 AND CONSIDER RISK FACTORS DESCRIBED HEREIN OR REFERRED TO IN ANY DOCUMENTS INCORPORATED BY REFERENCE IN THIS PROSPECTUS BEFORE INVESTING IN OUR SECURITIES.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Boustead Securities, LLC is the underwriter for this offering. The underwriter is selling our shares in this offering on a best efforts basis and is not required to sell any specific number or dollar amount of shares offered by this prospectus, but will use its best efforts to sell such shares. We have granted the underwriter the option for a period of 45 days to purchase up to an additional 15% of the total number of shares of common stock to be offered by us in this offering at the public offering price, less underwriting discounts and commissions, solely to cover over-subscriptions, if any. If the underwriter exercises the option in full, the total underwriting discounts and commissions payable by us will be $4,140,000, and the total proceeds to us, before expenses, will be $64,860,000. We do not intend to close this offering unless we sell at least $5,000,000 of shares, at the price per share set forth in the table below. This offering will terminate on July 9, 2018 (which we refer to as the “Initial Offering Termination Date”), which date may be extended to a date up to and including August 8, 2018 (which we refer to as the “Offering Termination Date”), unless we sell the maximum amount of shares set forth below before that date or we decide to terminate this offering prior to that date. In addition, in the event that the maximum amount has been met on or prior to the Offering Termination Date, the underwriter may exercise the over-subscription option on or prior to the Offering Termination Date to extend the offering for an additional 45 days. All subscription agreements and wire transfers should be sent to Signature Bank New York (“Signature Bank”), 905 Third Avenue, 9th Floor New York, NY 10022. The gross proceeds of this offering will be deposited at Signature Bank in an escrow account established by us until we have sold a minimum of $5,000,000 of shares. Once we satisfy the minimum offering amount, the funds will be released to us. In the event we do not sell a minimum of $5,000,000 of shares by the Offering Termination Date, all funds received will be promptly returned to investors without interest or offset.

| Per Share | Total Minimum | Total Maximum without Over-Subscription Option | Total Maximum with Over-Subscription Option | |||||||||||||

| Public offering price | $ | 8.50 | $ | 5,000,000 | $ | 60,000,000 | $ | 69,000,000 | ||||||||

| Underwriting discount(1) | $ | 0.51 | $ | 300,000 | $ | 3,600,000 | $ | 4,140,000 | ||||||||

| Proceeds, before expenses, to us(2) | $ | 7.99 | $ | 4,700,000 | $ | 56,400,000 | $ | 64,860,000 | ||||||||

| (1) | The underwriter will receive compensation in addition to the underwriting discount. See “Underwriting” beginning on page 76 of this prospectus for a description of compensation payable to the underwriter. |

| (2) | We estimate the total expenses of this offering, excluding the underwriting commissions, will be approximately $360,672 if the minimum number of shares being offered are sold, $360,672 if the maximum number of shares being offered are sold without exercise of the over-subscription option, or $360,672 if the maximum number of shares being offered are sold and the underwriter exercises the over-subscription option in full. Because this is a best efforts offering, the actual public offering amount, underwriting commissions and proceeds to us are not presently determinable and may be substantially less than the total maximum offering set forth above. |

On the closing date, we will issue the Underwriter Warrants to our underwriter exercisable at a rate of one warrant per share to purchase up to 6.0% of the securities sold in this offering, at an exercise price equal to 125% of the price at which we sell our common stock in this offering. We do not intend to list the Underwriter Warrants either on an exchange or an over the counter quotation system.

Underwriter

The date of this prospectus is March 29, 2018

Please read this prospectus carefully. It describes our business, financial condition and results of operations. We have prepared this prospectus so that you will have the information necessary to make an informed investment decision.

You should rely only on the information contained in this prospectus. We have not, and the underwriter has not, authorized anyone to provide you with any information other than that contained in this prospectus. We are offering to sell, and seeking offers to buy, the securities covered hereby only in jurisdictions where offers and sales are permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of the securities covered hereby. Our business, financial condition, results of operations and prospects may have changed since that date. We are not, and the underwriter are not, making an offer of these securities in any jurisdiction where the offer is not permitted.

For investors outside the United States: We have not, and the underwriter has not, taken any action that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the securities covered hereby or the distribution of this prospectus outside the United States.

This prospectus includes statistical and other industry and market data that we obtained from industry publications and research, surveys and studies conducted by third parties. Industry publications and third-party research, surveys and studies generally indicate that their information has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. We believe that the data obtained from these industry publications and third-party research, surveys and studies are reliable. We are ultimately responsible for all disclosure included in this prospectus.

We further note that the representations, warranties and covenants made by us in any agreement that is filed as an exhibit to the registration statement of which this prospectus is a part were made solely for the benefit of the parties to such agreement, including, in some cases, for the purpose of allocating risk among the parties to such agreements, and should not be deemed to be a representation, warranty or covenant to you. Moreover, such representations, warranties or covenants were accurate only as of the date when made. Accordingly, such representations, warranties and covenants should not be relied on as accurately representing the current state of our affairs.

WE HAVE NOT AUTHORIZED ANY DEALER, SALESPERSON OR OTHER PERSON TO GIVE ANY INFORMATION OR REPRESENT ANYTHING NOT CONTAINED IN THIS PROSPECTUS. YOU SHOULD NOT RELY ON ANY UNAUTHORIZED INFORMATION. THIS PROSPECTUS IS NOT AN OFFER TO SELL OR BUY ANY SHARES IN ANY STATE OR OTHER JURISDICTION IN WHICH IT IS UNLAWFUL. THE INFORMATION IN THIS PROSPECTUS IS CURRENT AS OF THE DATE ON THE COVER. YOU SHOULD RELY ONLY ON THE INFORMATION CONTAINED IN THIS PROSPECTUS.

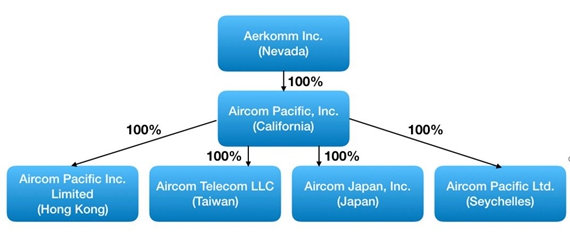

The following summary highlights selected information contained in greater detail elsewhere in this prospectus. This summary does not contain all the information you should consider before investing in our common stock. You should carefully read this prospectus in its entirety before investing in our common stock, including the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes beginning on page F-1 of this prospectus. Unless otherwise indicated, (i) the terms “Aerkomm,” “we,” “us” and “our” refer to Aerkomm Inc., a Nevada corporation, and our five wholly-owned subsidiaries Aircom Pacific, Inc., a California corporation, or Aircom, Aircom Pacific Inc. Limited (Hong Kong), or Aircom HK, Aircom Pacific Ltd. (Seychelles), or Aircom Seychelles, Aircom Japan, Inc. (Japan), or Aircom Japan, and Aircom Telecom LLC (Taiwan), or Aircom Taiwan, and (ii) the term “common stock” refers to the common stock, par value $0.001 per share, of Aerkomm Inc., a Nevada corporation. The financial information included herein is presented in United States dollars, or US Dollars, the functional currency of our company.

This prospectus assumes the over-subscription option of the underwriter has not been exercised, unless otherwise indicated.

Business Overview

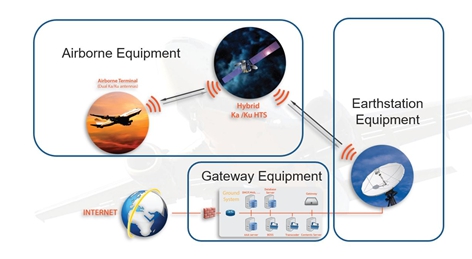

With advanced technologies and a unique business model, we, as a service provider of in-flight entertainment and connectivity, or IFEC, solutions, intend to provide airline passengers with a broadband in-flight experience that encompasses a wide range of service options. Such options include Wi-Fi, cellular, movies, gaming, live TV, and music. We plan to offer these core services, which we are currently still developing, through both built-in in-flight entertainment systems, such as a seat-back display, as well as on passengers’ personal devices. We also expect to provide content management services and e-commerce solutions related to our IFEC solutions.

We plan to partner with airlines and offer airline passengers free IFEC services. We plan to generate revenue through advertising and in-flight transactions. We believe that this is an innovative approach that differentiates us from existing market players.

To complement and facilitate our planned IFEC service offerings, we intend to build satellite ground stations and related data centers within the geographic regions where we expect to be providing IFEC airline services. Initially, we are planning to build our first ground station and data center in the Asia region, subject to the availability of sufficient capital and an appropriate ground location.

Competitive Strengths

Unique Business Model

We believe that our business model sets us apart from our competitors. We combine cutting-edge connectivity technology with a unique content-driven approach. Traditionally, providers of in-flight connectivity focus primarily on the profit margin derived from the sale of hardware to airlines and of bandwidth to passengers. Both airlines and passengers must “pay to play,” which results in low participation and usage rates. We break away from this model and set a new trend with our business model, under which neither airlines nor passengers need to pay for products or services. Furthermore, our business plan provides our airline partners with an opportunity to participate in our revenue sharing model. Taken together, this novel approach creates an incentive for airlines to work with us while driving up passenger usage rates.

Dual-Band Satellite Technology

Most in-flight connectivity systems currently rely on the Ku-band satellite signals for communication, though many players in the market are working to provide higher bandwidth and faster transmitting rates using the Ka-band. However, there are few Ka-enabled satellites, which limits the coverage area in the Asia-Pacific region. Our dual band system architecture brings our airline partners and their passengers the benefits of both Ka- and Ku-band satellite technology. The Ka-band increases data throughput, while the Ku-band offers reliable service outside of the Ka-band coverage area or when Ka-band is not available due to weather or other interference.

| 1 |

Growth Strategy

We will strive to be a leading provider of IFEC solutions by pursuing the following growth strategies:

Increase Number of Connected Aircraft

As of the date of this report, we have not provided our services on any commercial aircraft. However, we plan to rollout installation and provide our services in 2018. We plan to leverage our unique ability to cost-effectively equip each commercial aircraft type in an airline’s fleet to increase the number of equipped aircraft, targeting full-fleet availability of our services for our current and future airline partners. We plan to pursue this significant global growth opportunity by leveraging our broad and innovative technology platform and technical expertise. Further, we will offer attractive business models to our prospective airline partners, giving them the flexibility to determine the connectivity solution that meets the unique demands of their business.

Increase Passenger Use of Connectivity

We believe that internet connectivity has become a necessary utility rather than a novelty because most passengers are trying to remain “connected” while travelling. This trend is manifestly evident from the increasing data usage on mobile phones. However, the traditional business model has been to charge as much money as possible for high-end in-flight connectivity services offered to a very small number of people. Such business logic has resulted in the in-flight connectivity option acquiring the reputation of being “pricey” and “only for business travelers whose employers will pay for it.” With a focus on catering to only a small number of people in a narrow market niche, our competitors are paying less attention to an innovative business model that can encourage a wider, broad-based usage of in-flight connectivity services. We believe that certain providers of existing in-flight connectivity services discourage in-flight usage since they believe such usage will increase their overhead expenses without generating additional profit. Due to such a business model and the small amounts of revenue generated from currently available connectivity services, airlines have considered in-flight connectivity as a “service” to passengers provided at their expense. Under this thinking, in-flight connectivity is a “cost center” from which airlines do not expect to generate profit.

We believe that the value of a networking system grows exponentially with its usage and it is a waste of resources to build a networking system to be utilized only by a narrow niche market. Therefore, our business model encourages usage of our in-flight connectivity services on a much broader basis. In order to encourage such broader usage, we plan to offer our in-flight connectivity services to passengers in all travel classes for free, while we generate revenue from add-on services that will tie together passengers’ connectivity and usage. Thus, with our business model, we plan to create connectivity friendly aircraft cabins to provide free on-board internet connectivity for the passengers, and to generate revenue through the sale of advertising commercials, banner advertising, in-app purchases, in-game purchases and other related in-flight transactions.

Expand Satellite Network

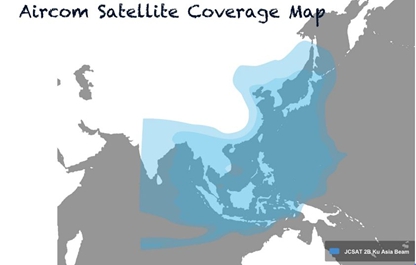

We will continue to expand our global satellite network coverage through the purchase of additional Ku-band and Ka-band capacity, and seek to install aircraft with our satellite solutions, while continuing to invest in research and development of satellite antenna and modem technologies. We are actively working with satellite providers in order to accommodate airlines’ global routes and growing fleets. We are monitoring the satellite industry for growth in coverage, with recent attention on China Satellite Communications Co. Ltd.’s, or China Satcom, plan to launch high-capacity Ka-band and Ka High Throughput Satellites, or HTS, multisport-beam satellites over the Asia-Pacific region.

Expand Satellite-Based Services to Other Markets

We anticipate broadening our satellite-based services to high-speed railways, maritime and cruise lines, 4G/5G backhauling, and converged triple-play services in remote communities, with the potential to expand internationally into new markets. Future business prospects will be evaluated on a case by case basis by weighing the projected revenue from advertising fees and e-commerce revenue shares against the operating and capital expenditures of satellite coverage, bandwidth and operations. Our existing business model could be applied to high-speed railways and cruise lines, both of which have a sufficient passenger base for the service to be viable. High-speed railways in China sit under existing, available Ka satellite coverage areas that are not served by 4G/LTE mobile networks, providing us with a unique opportunity to deliver our services. High-speed railways in other regions of Asia present similar opportunities. Remote communities in Asia lack a telecom infrastructure, partly due to geographical limitations such as the many islands of the Philippines or Indonesia. Satellite-based communications and mesh network technology make triple play services possible, delivering live TV broadcasting, videos, and telecom services to these regions.

| 2 |

Organization

We were incorporated in the State of Nevada on August 14, 2013 under the name Maple Tree Kids, Inc. On January 10, 2017, we changed our name to Aerkomm Inc. and on February 13, 2017, we consummated a reverse acquisition with Aircom Pacific, Inc., our wholly-owned subsidiary through which we conduct substantially all of our business transactions. Aerkomm’s principal executive offices are located at 923 Incline Way #39, Incline Village, NV 89451 and Aircom’s principal executive offices are located at 44043 Fremont Blvd., Fremont, CA 94538. Our telephone number is (877) 742-3094. We maintain a website at www.aerkomm.com. The information on our website or any other website is not incorporated by reference into this prospectus and does not constitute a part of this prospectus.

Risks Related to Our Business

Our business is subject to numerous risks, which are highlighted in the section entitled “Risk Factors” immediately following this prospectus summary. Some of these risks include:

| ● | we have a history of operating losses (after excluding non-recurring revenues) and we may not be able to reach or maintain profitability; |

| ● | difficulties in entering into and maintaining long-term business arrangements with airline partners, which agreements depends on numerous factors including the real or perceived availability, quality and price of our services and product offerings as compared to those offered by our competitors; |

| ● | difficulties in having airline partners and ultimately customers adopt our products and services; |

| ● | difficulties in implementing our technology and upgrades on a timely basis; |

| ● | difficulties in the execution of our expansion plans, including modification to our network to accommodate satellite technology, development and implementation of new satellite-based technologies, the availability of satellite capacity, costs of satellite capacity to which we may have to commit well in advance, and compliance with regulations; |

| ● | difficulties in managing a rapidly growing company; |

| ● | the number of aircraft in service in our markets, including consolidation of the airline industry or changes in fleet size by one or more of our commercial airline partners; |

| ● | the economic environment and other trends that affect both business and leisure travel; |

| ● | the continued demand for connectivity and proliferation of Wi-Fi enabled devices, including smartphones, tablets and laptops; |

| ● | our ability to obtain required telecommunications, aviation and other licenses and approvals necessary for our operations; |

| ● | changes in laws, regulations and interpretations affecting telecommunications services and aviation, including, in particular, changes that impact the design of our equipment and our ability to obtain required certifications for our equipment; |

| ● | our industry is subject to intense competition and rapid technological change, which may result in products or new solutions that are superior to our products under development or other future products we may bring to market from time to time and if we are unable to anticipate or keep pace with changes in the marketplace and the direction of technological innovation and customer demands, our products may become less useful or obsolete and our operating results will suffer; |

| ● | we may not be able to operate and grow our business effectively if we lose the services of any of our key personnel or are unable to attract qualified personnel in the future; and |

| ● | our growth strategy will require significant additional financial resources, which may not be available to us on acceptable terms. |

For further discussion of these and other risks you should consider before making an investment in our common stock, see the section titled “Risk Factors” immediately following this prospectus summary.

| 3 |

Emerging Growth Company

We qualify as an “emerging growth company” under the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. As a result, we are permitted to, and intend to, rely on exemptions from certain disclosure requirements. For so long as we are an emerging growth company, we will not be required to:

| ● | have an auditor report on our internal controls over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act; | |

| ● | comply with any requirement that may be adopted by the Public Company Accounting Oversight Board regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and the financial statements (i.e., an auditor discussion and analysis); | |

| ● | submit certain executive compensation matters to shareholder advisory votes, such as “say-on-pay” and “say-on-frequency;” and | |

| ● | disclose certain executive compensation related items such as the correlation between executive compensation and performance and comparisons of the CEO’s compensation to median employee compensation. |

In addition, Section 107 of the JOBS Act also provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards.

In other words, an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We have elected to take advantage of the benefits of this extended transition period. Our financial statements may therefore not be comparable to those of companies that comply with such new or revised accounting standards.

We will remain an “emerging growth company” for up to five years, or until the earliest of (i) the last day of the first fiscal year in which our total annual gross revenues exceed $1 billion, (ii) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Exchange Act, which would occur if the market value of our shares of common stock that are held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter, or (iii) the date on which we have issued more than $1 billion in non-convertible debt during the preceding three year period.

Conventions Used in this Prospectus

Throughout this prospectus we use certain terms repeatedly. To assist you in reading and understanding the disclosure contained in this prospectus, please note the following frequently used terms, which, except as otherwise specified, have the meanings set forth below:

| ● | “we,” “us,” “our,” or “our company,” are to the combined business of Aerkomm Inc., a Nevada corporation, and its consolidated subsidiaries; |

| ● | “Aircom” are to Aircom Pacific, Inc., a California corporation and wholly-owned subsidiary of our company; |

| ● | “Aircom Seychelles” are to Aircom Pacific Ltd., a Republic of Seychelles company and wholly-owned subsidiary of Aircom; |

| ● | “Aircom HK” are to Aircom Pacific Inc. Limited, a Hong Kong company and wholly-owned subsidiary of Aircom; |

| ● | “Aircom Japan” are to Aircom Japan, Inc., a Japanese company and wholly-owned subsidiary of Aircom; | |

| ● | “Aircom Taiwan” are to Aircom Telecom LLC, a Taiwanese company and wholly-owned subsidiary of Aircom; |

| ● | “our shareholders” refers to holders of our shares of common stock; |

| ● | “offering” refers to the offering contemplated by this prospectus; |

| ● | “SEC” refers to the U.S. Securities and Exchange Commission; |

| ● | “Securities Act” refers to the Securities Act of 1933, as amended; and |

| ● | “Exchange Act” refers to the Securities Exchange Act of 1934, as amended. |

On January 10, 2017, we completed a 1-for-10 reverse split of our issued and outstanding common stock. All share and per share information in this report has been adjusted to give retroactive effect to such reverse split.

| 4 |

The Offering

| Securities being offered: | A minimum of 588,235 shares of our common stock and up to a maximum of 8,117,647 shares of common stock (assuming an offering price of $8.50 per share), or a minimum of approximately $5,000,000 and a maximum of $60,000,000. | |

| Best Efforts Offering | The underwriter is selling the shares offered in this prospectus on a “best efforts” basis and is not required to sell any specific number or dollar amount of the shares offered by this prospectus, but will use its best efforts to sell such shares. We will not close this offering unless we sell a minimum of $5,000,000 of shares. | |

| Securities issued and outstanding before this offering: | 41,460,097 shares of common stock as of March 28, 2018.(1) | |

| Securities issued and outstanding after this offering:(2) | 42,048,332 shares of our common stock if the minimum number of shares being offered is sold, 48,518,921 shares of our common stock if the maximum number of shares being offered are sold, 49,577,744 shares of our common stock if the underwriter exercises the over-subscription option in full. | |

| Underwriter’s over-subscription option: | The underwriting agreement with our underwriter provides that we will grant to the underwriter an option, exercisable within 45 days after the closing of this offering, to purchase up to an additional 15% of the total number of shares of common stock to be offered by us pursuant to this offering, solely for the purpose of covering over-subscriptions, if any. | |

| Use of proceeds: | We estimate our net proceeds from this offering will be approximately $4,339,328, if the minimum number of shares being offered are sold, approximately $56,039,328, if the maximum number of shares being offered are sold, or approximately $64,499,328 if the underwriter exercises their over-subscription option in full, based upon an assumed public offering price of $8.50 per share and after deducting the underwriting discounts and commissions and estimating offering expenses payable by us.

We expect to use the net proceeds of this offering for general corporate purposes, including working capital, product development, marketing activities, expending our internal organization and other capital expenditures including the purchase of land for the building of our first ground station and data center in the Asia region. For a more detailed discussion, see “Use of Proceeds” below. | |

| Escrow account | All subscription agreements and wire transfers should be sent to Signature Bank New York, 905 Third Avenue, 9th Floor New York, NY 10022. The gross proceeds of this offering will be deposited at Signature Bank in an escrow account established by us. The funds will be held in such escrow account until $5,000,000 of gross proceeds from the offering has been received, at which time the funds will be released to us. Any funds received in excess of $5,000,000 and up to $60,000,000 (or $69,000,000 if the underwriter exercises the over-subscription option in full) will immediately be available to us, after deducting the applicable underwriting commissions. If the minimum amount of $5,000,000 has not been received by July 9, 2018 (which we refer to as the “Initial Offering Termination Date”), which date may be extended to a date up to and including August 8, 2018 (which we refer to as the “Offering Termination Date”), all funds will be returned to purchasers in this offering on the next business day after the offering’s termination, without charge, deduction or interest. In the event that the maximum amount has been met on or prior to the Offering Termination Date, the underwriter may exercise the over-subscription option on or prior to the Offering Termination Date to extend the offering for an additional 45 days.

Prior to the Initial Offering Termination Date, in no event will funds be returned to you, unless we elect, at our option, to terminate the offering. In the event we decide to extend the offering period beyond the Initial Offering Termination Date, we will seek reconfirmations from investors who have deposited funds into the escrow account and all funds deposited by investors who do not reconfirm will be promptly returned without interest or offset. Except as described in the preceding sentence, you will only be entitled to receive a refund of your subscription if we do not raise a minimum of $5,000,000 by the Offering Termination Date, or if we terminate the offering before such date. |

| 5 |

| Current symbol: | OTCQX Best Market: AKOM. | |

Listing and proposed NYSE or Nasdaq symbol:

|

After the effective date of the registration statement relating to this prospectus and following the filing pf audited financial statements for our changed fiscal year end ending March 31, 2018 (discussed below), we plan to file an application to have the shares of common stock and warrants offered hereby listed on either the NYSE or the Nasdaq under the symbol “AKOM.” The Company expects to meet the NYSE and Nasdaq initial listing standards, including the market value of our publicly held shares, the market value of our listed securities, the number of our publicly held shares, the number of round lot shareholders, the number of market makers and the bid or closing price of our common stock, upon a successful completion of this offering, although no assurance can be given that we will successfully complete this offering or meet those standards and that our listing application to either the NYSE or the Nasdaq will be approved. To meet the exchanges’ financial statement seasoning requirements, on March 18, 2018, our board of directors voted to change our fiscal year to March 31 and prepare audited financial statements for the fiscal year ending March 31, 2018, giving us the exchange required audited financial statements for a full fiscal year following the completion of our reverse acquisition and the filing of our Form 10 information with the SEC on February 13, 2017. | |

| Dividend and distribution policy: | We have never declared or paid cash dividends on our common stock. We currently intend to retain all available funds and any future earnings for use in the operation of our business and do not anticipate paying any dividends on our common stock in the foreseeable future, if at all. Any future determination to declare dividends will be made at the discretion of our board of directors and will depend on our financial condition, operating results, capital requirements, general business conditions and other factors that our board of directors may deem relevant. | |

| Lock-up: | We and our directors, officers and any other 5% or greater holder of outstanding shares of common stock (and all holders of securities exercisable for or convertible into shares of common stock) have agreed with the underwriter not to offer for sale, issue, sell, contract to sell, encumber, grant any option for the sale of or otherwise dispose of any of our securities, including the issuance of shares of common stock upon currently outstanding option for a period of six (6) months after the date of this prospectus, without the prior written consent of the underwriter. See “Underwriting.” | |

| Risk factors: | Investing in our securities is highly speculative and involves a high degree of risk. You should carefully consider the information set forth in the “Risk Factors” section beginning on page 8 before deciding to invest in our securities. |

| (1) | The number of shares of our common stock outstanding after this offering is based on 41,460,097 shares of our common stock outstanding as of March 28, 2018, and excludes: |

| ● | 4,054,011 shares of our common stock reserved for future option grants pursuant to our 2017 Equity Incentive Plan; | |

| ● | 1,265,000 shares of our common stock have been approved by our board of directors for issuance upon the exercise of options granted to our officers, directors, employees and service providers; | |

| ● | 4,661,308 shares of our common stock issuable upon the exercise of options under our 2017 Equity Incentive Plan to be issued to holders of Aircom Pacific, Inc. options (“Aircom 2014 Plan”) assumed by us as a result of the closing of the reverse acquisition with Aircom Pacific, Inc.; and | |

| ● | Up to 487,059 shares of common stock underlying the Underwriter Warrants. |

| (2) | The total number of shares of common stock outstanding after this offering is based on 41,460,097 shares outstanding as of March 28, 2018 and an assumed public offering price of $8.50 per share. |

| 6 |

Summary Consolidated Financial Data

The following tables summarize our consolidated financial data. You should read this summary consolidated financial data together with the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes that are included elsewhere in this prospectus.

The consolidated statement of operations data for the years ended December 31, 2017, 2016 and 2015 are derived from our audited consolidated financial statements that are included elsewhere in this prospectus. Our historical results are not necessarily indicative of the results that may be expected in the future, and our interim results are not necessarily indicative of the results to be expected for the full year or any other period.

| Years Ended December 31, | ||||||||||||

| 2017 | 2016 | 2015 | ||||||||||

| Consolidated Statement of Operations Data: | ||||||||||||

| Revenue | $ | - | $ | - | $ | 6,128,900 | ||||||

| Cost of revenue | - | - | 1,337,905 | |||||||||

| Gross profit | - | - | 4,790,995 | |||||||||

| Operating expenses | 7,147,597 | 3,970,105 | 1,235,796 | |||||||||

| Income (loss) from continuing operations | (7,147,597 | ) | (3,176,464 | ) | 2,670,414 | |||||||

| Income (loss) from discontinued operations | - | - | - | |||||||||

| Net income (loss) | $ | (7,132,464 | ) | $ | (3,176,464 | ) | $ | 2,670,414 | ||||

| Net income (loss) per share: | ||||||||||||

| Basic | $ | (0.1748 | ) | $ | (0.0808 | ) | $ | 0.0841 | ||||

| Diluted | $ | (0.1748 | ) | $ | (0.0808 | ) | $ | 0.0759 | ||||

| Weighted average shares outstanding: | ||||||||||||

| Basic | 40,821,495 | 39,335,796 | 31,752,318 | |||||||||

| Diluted | 40,821,495 | 39,335,796 | 35,190,236 | |||||||||

| December 31, 2017 | ||||

| Consolidated Balance Sheet Data: | ||||

| Current assets | $ | 1,239,544 | ||

| Total assets | $ | 10,265,976 | ||

| Total liabilities | $ | 3,811,913 | ||

| Total stockholders’ equity | $ | 6,454,063 | ||

| 7 |

Investment in our common stock involves a high degree of risk. You should carefully consider each of the following risks, together with all other information set forth in this prospectus, including the financial statements and the related notes, before making a decision to buy our common stock. If any of the following risks actually occurs, our business could be harmed. In that case, the trading price of our common stock could decline, and you may lose all or part of your investment.

Risks Related to Our Business

Our company is in the development stage and has a limited operating history, which may make it difficult to evaluate our current business and predict our future performance.

Our company and our core business are in the development stage and faces all of the risks and uncertainties associated with a new and unproven business. We plan to launch our services in Asia in 2018, initially in China or Southeast Asia. The limited operating history of our business may make it difficult to accurately evaluate the business and predict its future performance. Any assessments of our current business and predictions that we or you make about our future success or viability may not be as accurate as they could be if we had a longer operating history. We have encountered and will continue to encounter risks and difficulties frequently experienced by growing companies in rapidly changing industries, and the size and nature of our market opportunity will change as we scale our business and increase deployment of our service. If we do not address any of the foregoing risks successfully, our business will be harmed.

Excluding non-recurring revenues in 2015 from affiliates, we have incurred operating losses in every quarter since we launched our business and may continue to incur quarterly operating losses, which could negatively affect the value of our company.

Excluding non-recurring revenues we earned from affiliates in 2015, we have incurred operating losses since our inception in 2014, and we may not be able to generate sufficient revenue in the future to generate operating income. We also expect our costs to increase materially in future periods, which could negatively affect our future operating results. We expect to continue to expend substantial financial and other resources on the continued launch and future expansion of our business. The amount and timing of these costs are subject to numerous variables and such initiatives may require additional funding. In addition, we may incur significant costs in connection with our pursuit of next generation air to ground technology or other new technologies. With respect to our expansion, such variables may include costs related to sales and marketing activities and administrative support functions, equipment subsidies to airlines and additional legal and regulatory expenses associated with operating in the international commercial aviation market. In addition, we expect to incur additional general and administrative expenses, including legal and accounting expenses, related to being a public company. These investments may not result in revenue or growth in our business. If we fail to grow our overall business and generate revenue, our financial condition and results of operations would be adversely affected.

There is substantial uncertainty that we will continue operations as a going concern in which case you could lose your entire investment.

Our future existence remains uncertain. We have generated no recurring revenues to date, our only non-recurring revenues were from sales to our affiliates in 2015 and we have suffered losses from our operations after excluding those non-recurring revenues. We also have outstanding accrued liabilities. Although we expect to raise capital from the sale of equity or debt securities, there is no assurance that we will be able to do so. This means that there is substantial doubt that we can continue as a going concern for the next twelve months unless we obtain additional capital to pay our bills and debts and execute our plan of operations.

We expect to rely on a few key customers for all of our initial revenue.

Our initial business will be substantially dependent on our relationship with a few key airline customers. There can be no assurance that we will be able to maintain our relationship with these airlines. If we are unable to maintain and renew our relationship with these airlines, or if our arrangement is modified so that the economic terms become less favorable to us, then our business would be materially adversely affected.

Our agreement with Hong Kong Airlines will have no legal effect until we receive approval of our VSTC by the HKCAD.

Until such time as we have received all required approvals from the Hong Kong Civil Aviation Department, or HKCAD, the agreement with Hong Kong Airlines only expresses the desires and understandings between us and Hong Kong Airlines and will not create any legal rights, liabilities or responsibilities whatsoever and will not be legally binding on us or Hong Kong Airlines. There can be no assurance as to when we will receive the required HKCAD approvals or if we will receive such approvals at all. If we do not receive the HKCAD approval of our Validation of Supplemental Type Certificate, or VSTC, our agreement with Hong Kong airlines will have no economic impact. Such an outcome would have a substantial adverse effect on our revenue prospect.

| 8 |

If the transactions contemplated by several memorandums of understanding (MOU) and our letter of intent (LOI) do not proceed, our results of operations and financial condition could be materially adversely affected.

On January 19, 2016, January 29, 2016, June 16, 2016, September 26, 2017, October 28, 2017 and March 7, 2018, we entered into the Yahoo MOU, the LeTV MOU, the India MOU, the Malta MOU, the LOI and the Airbus MOU, respectively. These MOUs and LOI are nonbinding and as a result, they only express the desires and understandings between the parties and do not create any legally binding rights, obligations or contracts except for certain customary provisions such as exclusivity, costs and expenses, confidentiality and governing law. For more information related to these MOUs, please refer to the section “MOUs and LOI with Our Business Partners.” Any binding obligation to proceed with the transactions contemplated by the MOUs and the LOI would need to be included in a definitive agreement that is subject to negotiations of the parties, approvals by the board of directors of respective parties and in certain instances, approvals from regulatory authorities. The Yahoo MOU and LeTV MOU expired in January 2018 and we are in the process of negotiating to extend those two MOUs. There can be no assurance that we will be able to extend the expired MOUs or enter into such definitive agreements or receive the required governmental approvals. If for whatever reason the transactions contemplated by the MOUs and the LOI do not proceed, our results of operations and financial condition could be materially adversely affected.

One of our suppliers has failed to deliver a key component of our IFEC system and we have terminated our satellite services agreement with another. We cannot be sure that we will be able to find alternative source for this component or for the required satellite services and, as a result, we may not be able to implement our business plan.

The implementation of the Hong Kong Airlines project is conditioned upon VSTC approval from the HKCAD. We and our equipment supplier have submitted the VSTC application to HKCAD but the application process is presently on hold due to the supplier’s failure to deliver a key component of the IFEC system. We do not expect this supplier to be able to delivery this key component and we are actively seeking alternative options to implement the Hong Kong Airline project, including developing necessary equipment or components thereof with other strategic partners. Because we cannot be sure when and if we will be able to obtain the IFEC component for the VSTC approval, we cannot be sure when we will receive approval for the Hong Kong Airlines project, if at all. If we are not able to source this necessary IFEC component, our current agreement with Hong Kong Airlines will not become executable and we will not be able to implement our business plan as currently envisioned.

Additionally, our satellite services agreement with Asia Satellite Telecommunications Company Limited, or AsiaSat, was recently terminated. If we are not able to find a replacement satellite services provider, we will not be able to deliver our service offerings to Hong Kong Airlines even once we receive the VSTC approval from HKCAD. Such a failure would have a negative impact on our business prospects.

If we cannot timely deliver our first order of onboard equipment to Klingon Aerospace Inc., our reseller and development partner, we may lose our agreement with Klingon.

Because of the delay in our receiving approval of the VSTC from the HKCAD, we have not been able to deliver to Klingon a ready for sale, certified onboard system equipment package. Klingon has the right to terminate our agreement with them upon 60 days’ prior notice, subject to a 60-day cure period, if we fail to timely deliver the certified product. If Klingon terminates its agreement with us, we may be responsible for refunding to Klingon the milestone payments that we have received.

We may not be able to grow our business with our current potential airline partner or successfully negotiate agreements with airlines to which we do not currently provide our service.

Currently, our only potential airline partner is Hong Kong Airlines, although we have not yet begun to sell our products and services to Hong Kong Airlines under our agreement with them. We are currently in negotiations or discussions with certain other airline partners to provide our IFEC services on additional aircraft in their fleets. We have no assurance that these efforts will be successful. Negotiations with prospective airline partners require substantial time, effort and resources. The time required to reach a final agreement with an airline is unpredictable and may lead to variances in our operating results from quarter to quarter. We may ultimately fail in our negotiations and any such failure could harm our results of operations due to, among other things, a diversion of our focus and resources, actual costs and opportunity costs of pursuing these opportunities. In addition, the terms of any future agreements could be materially different and less favorable to us than the terms included in our existing agreement with Hong Kong Airlines. To the extent that any negotiations with current or future potential airline partners are unsuccessful, or any new agreements contain terms that are less favorable to us, our growth prospects could be materially and adversely affected.

| 9 |

We will likely need additional financing to execute our business plan or new initiatives, which we may not be able to secure on acceptable terms, or at all.

We will require additional financing in the near and long term to fully execute our business plan. Our success may depend on our ability to raise such additional financing on reasonable terms and on a timely basis. Conditions in the economy and the financial markets may make it more difficult for us to obtain necessary additional capital or financing on acceptable terms, or at all. If we cannot secure sufficient additional financing, we may be forced to forego strategic opportunities or delay, scale back or eliminate additional service deployment, operations and investments or employ internal cost savings measures.

We are dependent on airline partners to be able to access our customers. We expect that future payments by these customers for our services to be provided to them will account for most, if not all, of our initial revenues.

Under our existing contract with Hong Kong Airlines, once our VSTC is approved by the HKCAD, we will provide our equipment for installation on, and provide our services to passengers on, a portion of the aircraft operated by this airline. We expect to enter into similar contracts with other airlines in the future but there is no assurance that we will be successful in signing up additional airlines partners. We expect that revenue from passengers using our service while flying on aircraft operated by our airline partners will account for the majority of our projected initial revenue once we begin our services. As of the date of this report, we do not yet have any revenue from equipment sales and installation. Our growth will be dependent on our ability to have our equipment installed on the aircraft of airline partners and increased use of our service on installed aircraft. Any delays in installations under these contracts may negatively affect our ability to grow our user base and revenue.

A failure to maintain airline satisfaction with our equipment or our service could have a material adverse effect on our revenue and results of operations.

Our relationships with our current and future potential airline partners are critical to the growth and ongoing success of our business. If airline partners are not satisfied with our equipment or our service for any reason, including passenger dissatisfaction with the service as a result of capacity constraints, they may reduce efforts to co-market our service to their passengers, which could result in lower passenger usage and reduced revenue, which could in turn give airline partners the right to terminate their contracts with us. In addition, airline dissatisfaction with us for any reason, including delays in obtaining certification for or installing our equipment, could negatively affect our ability to expand our service to additional airline partners or aircraft or lead to claims for damages, which may be material, or termination rights under our existing or potential contracts with airline partners.

We are experiencing network capacity constraints in our operation region and expect capacity demands to increase, and we may in the future experience capacity constraints internationally. If we are unable to successfully implement planned or future technology enhancements to increase our network capacity, or our airline partners do not agree to such enhancements, our ability to maintain sufficient network capacity and our business could be materially and adversely affected.

All providers of wireless connectivity services, including all providers of in-flight connectivity services, face certain limits on their ability to provide connectivity service, including escalating capacity constraints due to expanding consumption of wireless services and the increasing prevalence of higher bandwidth uses such as file downloads and streaming media content. The success of our business depends on our ability to provide adequate bandwidth to meet customer demands while in-flight.

Competition from a number of companies, as well as other market forces, could result in price reduction, reduced revenue and loss of market share and could harm our results of operations.

We face strong competition from satellite-based providers of broadband services that include in-flight internet and live television services. Competition from such providers has had in the past and could have in the future an adverse effect on our ability to maintain or gain market share. Most of our competitors are larger, more diversified corporations and have greater financial, marketing, production, and research and development resources. As a result, they may be better able to withstand the effects of periodic economic downturns or may offer a broader product line to customers. In addition, to the extent that competing in-flight connectivity services offered by commercial airlines that are not our airline partners are available on more aircraft or offer improved quality or reliability as compared to our service, our business and results of operations could be adversely affected. Competition could increase our sales and marketing expenses and related customer acquisition costs. We may not have the financial resources, technical expertise or marketing and support capabilities to continue to compete successfully. A failure to effectively respond to established and new competitors could have a material adverse impact on our business and results of operations.

| 10 |

We may be unsuccessful in generating revenue from live television and other in-flight entertainment services.

We are currently developing a host of service offerings to deliver to our future commercial airline customers. We plan to offer live television and other service to our customers and no assurance can be given that we will ultimately be able to launch any channels or provide any service. Additionally, we plan to generate a revenue stream from our video on demand and other in-flight entertainment services. If we are unable to generate revenue from live television or if other entertainment services do not ultimately develop, our growth and financial prospects would be materially adversely impacted.

We are working to acquire a sufficient number of on-demand movies and television shows and a variety of other content on our system. The future growth prospects for our business depend, in part, on revenue from advertising fees and e-commerce revenue share arrangements on passenger purchases of goods and services, including video and media services. Our ability to generate revenue from these service offerings depends on:

| ● | growth of commercial airline customer base; |

| ● | the attractiveness of our customer base to media partners; |

| ● | rolling out live television and media on demand on more aircraft and with additional airline customers and increasing passenger adoption both in the U.S. and abroad; |

| ● | establishing and maintaining beneficial contractual relationships with media partners whose content, products and services are attractive to airline passengers; and |

| ● | our ability to customize and improve our service offerings in response to trends and customer interests. |

If we are unsuccessful in generating revenue from our service offerings, that failure could have a material adverse effect on our growth prospects.

We face limitations on our ability to grow our operations which could harm our operating results and financial condition.

We have not yet begun selling our products or services to our future customers. Our addressable market and our ability to expand in our operating region is inherently limited by various factors, including limitations on the number of commercial airlines with which we could partner, the number of planes in which our equipment can be installed, the passenger capacity within each plane and the ability of our network infrastructure or bandwidth to accommodate increasing capacity demands. Future expansion is also limited by our ability to develop new technologies on a timely and cost-effective basis, as well as our ability to mitigate network capacity constraints through, among other things, the expansion of our satellite coverage area. Our future growth may slow, or once we begin selling products and services to our customers, we may stop growing altogether, to the extent that we have exhausted all potential airline partners and as we approach installation on full fleets and maximum penetration rates on all flights. In order to grow our future revenue, we will have to rely on customer and airline partner adoption of currently available and new or developing services and additional offerings. We cannot assure you that we will be able to obtain a market presence or establish new markets and, if we fail to do so, our business and results of operations could be materially adversely affected.

We may be unsuccessful in expanding our operations internationally.

Our business will initially be international business. Our ability to grow our international business involves various risks, including the need to invest significant resources in unfamiliar markets and the possibility that we may not realize a return on our investments in the near future or at all. In addition, we have incurred and expect to continue to incur significant expenses before we generate any material revenue in these new markets. Under our agreements with providers of satellite capacity, we are obligated to purchase bandwidth for specified periods in advance. If we are unable to generate sufficient passenger demand or airline partners to which we provide satellite service to their aircraft terminate their agreements with us for any reason during these periods, we may be forced to incur satellite costs in excess of connectivity revenue generated through such satellites.

| 11 |

Any future international operations may fail to succeed due to risks inherent in foreign operations, including:

| ● | legal and regulatory restrictions, including different communications, privacy, censorship, aerospace and liability standards, intellectual property laws and enforcement practices; |

| ● | changes in international regulatory requirements and tariffs; |

| ● | restrictions on the ability of U.S. companies to do business in foreign countries, including restrictions on foreign ownership of telecommunications providers imposed by the U.S. Office of Foreign Assets Control, which we refer to as OFAC; |

| ● | inability to find content or service providers to partner with on commercially reasonable terms, or at all; |

| ● | compliance with the Foreign Corrupt Practices Act, the (U.K.) Bribery Act 2010 and other similar corruption laws and regulations in the jurisdictions in which we operate and related risks; |

| ● | difficulties in staffing and managing foreign operations; |

| ● | currency fluctuations; and |

| ● | potential adverse tax consequences. |

As a result of these obstacles, we may find it difficult or prohibitively expensive to grow our business internationally or we may be unsuccessful in our attempt to do so, which could harm our future operating results and financial condition.

We may not be successful in our efforts to develop and monetize new products and services that are currently in development, including our operations-oriented communications services.

In order to continue to meet the evolving needs of our future airline partners and customers, we must continue to develop new products and services that are responsive to those needs. Our ability to realize the benefits of enabling airlines, other aircraft operators and to use these applications, including monetizing our services at a profitable price point, depends, in part, on the adoption and utilization of such applications by airlines, other aircraft operators and other companies in the aviation industry such as aircraft equipment suppliers, and we cannot be certain that airlines, other aircraft operators and others in the aviation industry will adopt such offerings in the near term or at all. We also expect to continue to rely on third parties to develop and offer the operational applications to be used to gather and process data transmitted on our network between the aircraft and the ground, and we cannot be certain that such applications will be compatible with our network or onboard equipment or otherwise meet the needs of airlines or other aircraft operators. If we are not successful in our efforts to develop and monetize new products and services, including our operations-oriented communications services, our future business prospects, financial condition and results of operations would be materially adversely affected.

A future act or threat of terrorism or other events could result in a prohibition on the use of Wi-Fi enabled devices on aircraft.

A future act of terrorism, the threat of such acts or other airline accidents could have an adverse effect on the airline industry. In the event of a terrorist attack, terrorist threats or unrelated airline accidents, the industry would likely experience significantly reduced passenger demand. The U.S. federal government or foreign governments could respond to such events by prohibiting the use of Wi-Fi enabled devices on aircraft, which would eliminate demand for our equipment and service. In addition, any association or perceived association between our equipment or service and accidents involving aircraft on which our equipment or service operates would likely have an adverse effect on demand for our equipment and service. Reduced demand for our products and services would adversely affect our business prospects, financial condition and results of operations.

| 12 |

If our efforts to retain and attract customers are not successful, our revenue will be adversely affected.

We expect to generate substantially all of our revenue from sales of services, some of which will be on a subscription basis. We must be able to retain subscribers and attract new and repeat customers. If we are unable to effectively retain subscribers and attract new and repeat customers, our business, financial condition and results of operations would be adversely affected.

Unreliable service levels, lack of sufficient capacity, uncompetitive pricing, lack of availability, security risk and lack of related features of our equipment and services are some of the factors that may adversely impact our ability to retain customers and partners and attract new and repeat customers. If our customers are able to satisfy their in-flight entertainment needs through activities other than broadband internet access, at no or lower cost, they may not perceive value in our products and services. If our efforts to satisfy and retain customers and subscribers are not successful, we may not be able to attract new customers through word-of-mouth referrals. Any of these factors could cause our customer growth rate to fall, which would adversely impact our business, financial condition and results of operations.

The demand for in-flight broadband internet access service may decrease or develop more slowly than we expect. We cannot predict with certainty the development of the U.S. or international in-flight broadband internet access market or the market acceptance for our products and services.

Our future success depends upon growing demand for in-flight broadband internet access services, which is inherently uncertain. We have invested significant resources towards the roll-out of new service offerings, which represent a substantial part of our growth strategy. We face the risk that the U.S. and international markets for in-flight broadband internet access services may decrease or develop more slowly or differently than we currently expect, or that our services, including our new offerings, may not achieve widespread market acceptance. We may be unable to market and sell our services successfully and cost-effectively to a sufficiently large number of customers.

Our business depends on the continued proliferation of Wi-Fi as a standard feature in mobile devices. The growth in demand for in-flight broadband internet access services also depends in part on the continued and increased use of laptops, smartphones, tablet computers, and other Wi-Fi enabled devices and the rate of evolution of data-intensive applications on the mobile internet. If Wi-Fi ceases to be a standard feature in mobile devices, if the rate of integration of Wi-Fi on mobile devices decreases or is slower than expected, or if the use of Wi-Fi enabled devices or development of related applications decreases or grows more slowly than anticipated, the market for our services may be substantially diminished.

Increased costs and other demands associated with our growth could impact our ability to achieve profitability over the long term and could strain our personnel, technology and infrastructure resources.

We expect our costs to increase in future periods, which could negatively affect our future operating results. We expect to experience growth in our headcount and operations, which will place significant demands on our management, administrative, technological, operational and financial infrastructure. Anticipated future growth will require the outlay of significant operating and capital expenditures and will continue to place strains on our personnel, technology and infrastructure. Our success will depend in part upon our ability to contain costs with respect to growth opportunities. To successfully manage the expected growth of our operations, on a timely and cost-effective basis we will need to continue to improve our operational, financial, technological and management controls and our reporting systems and procedures. In addition, as we continue to grow, we must effectively integrate, develop and motivate a large number of new employees, and we must maintain the beneficial aspects of our corporate culture. If we fail to successfully manage our growth, it could adversely affect our business, financial condition and results of operations.

Adverse economic conditions may have a material adverse effect on our business.

Macro-economic challenges are capable of creating volatile and unpredictable environments for doing business. We cannot predict the nature, extent, timing or likelihood of any economic slowdown or the strength or sustainability of any economic recovery, worldwide, in the United States or in the airline industry. For many travelers, air travel and spending on in-flight internet access are discretionary purchases that they can eliminate in difficult economic times. Additionally, a weaker business environment may lead to a decrease in overall business travel, which is an important contributor to our service revenue. These conditions may make it more difficult or less likely for customers to purchase our equipment and services. If economic conditions in the United States or globally deteriorate further or do not show improvement, we may experience material adverse effects to our business, cash flow and results of operations.

| 13 |

Our operating results may fluctuate unpredictably and may cause us to fail to meet the expectations of investors, adversely affecting our stock price.

We operate in a highly dynamic industry and our future quarterly operating results may fluctuate significantly. Our future revenue and operating results may vary from quarter to quarter due to many factors, many of which are not within our control. As a result, comparing our operating results on a period-to-period basis may not be meaningful. Further, it is difficult to accurately forecast our revenue, margin and operating results, and if we fail to match our expected results or the results expected by financial analysts or investors, the future trading price of our common stock may be adversely affected.

In addition, due to generally lower demand for business travel during the summer months and holiday periods, and leisure and other travel at other times during the year, our quarterly results may not be indicative of results for the full year. Due to these and other factors, quarter-to-quarter comparisons of our historical operating results should not be relied upon as accurate indicators of our future performance.

If our marketing and advertising efforts fail to generate revenue on a cost-effective basis, or if we are unable to manage our marketing and advertising expenses, it could harm our results of operations and growth.

Our future growth and profitability, as well as the maintenance and enhancement of our brands, will depend in large part on the effectiveness and efficiency of our future marketing and advertising expenditures. We plan to use a diverse mix of television, print, trade show and online marketing and advertising programs to promote our business. Significant increases in the pricing of one or more of our marketing and advertising channels could increase our expenses or cause us to choose less expensive, but potentially less effective, marketing and advertising channels. In addition, to the extent we implement new marketing and advertising strategies, we may in the future have significantly higher expenses. We may in the future incur, marketing and advertising expenses significantly in advance of the time we anticipate recognizing revenue associated with such expenses, and our marketing and advertising expenditures may not result in increased revenue or generate sufficient levels of brand awareness. If we are unable to maintain our marketing and advertising channels on cost-effective terms, our marketing and advertising expenses could increase substantially, our customer levels could be affected adversely, and our business, financial condition and results of operations may suffer.

Regulation by United States and foreign government agencies, including the Federal Aviation Administration and the Federal Communications Commission, may increase our costs of providing service or require us to change our services.

We are subject to various regulations, including those regulations promulgated by various federal, state and local regulatory agencies and legislative bodies and comparable agencies outside the United States where we may do business. The two U.S. government agencies that have primary regulatory authority over our operations are the Federal Aviation Administration, or FAA, and the Federal Communications Commission, or FCC.