Filed Pursuant to Rule 424(b)(3)

Registration No. 333-268707

WHITE RIVER ENERGY CORP

PROSPECTUS

67,651,420 Shares of Common stock

16,931,266 Warrants to Purchase Shares of Common Stock

This Prospectus relates to the distribution (the “Spin-Off”) by Ecoark Holdings, Inc., now known as BitNile Metaverse, Inc. (“Ecoark”) of 42,253,521 shares of common stock, par value $0.0001 per share (the “Spin-Off Shares”) of White River Energy Corp (“White River,” the “Company,” “we,” “our,” or “us”), a Nevada corporation, to the holders of Ecoark common stock and convertible preferred stock (on an as-converted basis). We are also registering the issuance of up to an additional 1,000 shares of common stock to account for the rounding up of fractional shares that would otherwise be distributable to the Ecoark record holders as Spin-Off Shares (“Fractional Shares”), and unless expressly noted or the context clearly dictates otherwise, the up to 1,000 Fractional Shares are also included in references to “Spin-Off Shares” in this Prospectus. This Prospectus also relates to the offering and resale by the selling stockholders identified herein (the “Selling Stockholders”) of up to 25,396,899 shares of the common stock of White River (the “PIPE Shares”) and up to 16,931,266 warrants to purchase shares of common stock of White River (the “Warrants,” and together with the PIPE Shares, collectively, the “PIPE Securities”), which consists of shares of common stock issuable upon conversion of 263.1126308 outstanding shares of the Company’s Series C Convertible Preferred Stock (the “Series C”) and exercise of Warrants representing 200% warrant coverage issued in private placement transactions from October 2022 through April 2023 in a private investment in public equity offering by the Company (the “PIPE Offering”). The PIPE Shares and the Spin-Off Shares, are collectively referred to as the “Shares,” and together with the Warrants, the securities being offered hereby are collectively referred to as the “Securities.” The above number of PIPE Securities was determined based on the conversion price of approximately $0.777 per share, which is 80% of the 30-day VWAP (as defined in the Series C Certificate of Designation) of the Company’s common stock for the period ending 10 trading days prior to effectiveness of the Registration Statement of which this Prospectus is a part. See “The Private Placement” and “Selling Stockholders” for more information.

The Company is not selling any securities in this offering, and therefore will not receive any proceeds from the distribution of Spin-Off Shares by Ecoark and the sale of the PIPE Securities by the Selling Stockholders. However, we will receive gross proceeds upon the exercise of the Warrants if exercised for cash.

Spin-Off

The Spin-Off Shares of our common stock will be distributed to Ecoark holders of common stock and convertible preferred stock as of the record date of September 30, 2022 (the “Record Date”), on an as-converted basis for the preferred stock, meaning the holder of Ecoark’s outstanding convertible preferred stock as of the Record Date will also receive shares of White River common stock as if the shares of Ecoark common stock underlying their preferred stock were issued and outstanding (subject to beneficial ownership limitations) calculated as of the Record Date. As of the Record Date, there were 28,176,055 shares of Ecoark common stock outstanding and 4,438,096 shares of Ecoark common stock were issuable upon conversion of the convertible preferred stock, although the latter amount disregards the beneficial ownership limitations. No Fractional Shares of our common stock will be issued in the Spin-Off, and any Fractional Share of our common stock in the Spin-Off will be rounded up to the nearest whole share. We have agreed to issue Ecoark Fractional Shares to account for this rounding approach.

PIPE Securities

After the Spin-Off takes place, the Selling Stockholders may sell the PIPE Securities described in this Prospectus in a number of different ways and at varying prices. The prices at which the Selling Stockholders may sell the PIPE Securities in this offering will be determined by the prevailing market price for the shares of our common stock or in negotiated transactions. See “Plan of Distribution” for more information about how the Selling Stockholders may sell the Securities being registered pursuant to this Prospectus. Each Selling Stockholder may be deemed an “underwriter” within the meaning of Section 2(a)(11) of the Securities Act of 1933 (the “Securities Act”). The Selling Stockholders have informed us that they do not currently have any agreement or understanding, directly or indirectly, with any person to distribute the PIPE Securities. The Selling Stockholders will not receive their PIPE Securities until after the Spin-Off has taken place.

We have agreed to pay the expenses of the registration of the shares of our common stock offered and sold under the Registration Statement under the Spin-Off and by the Selling Stockholders. Each Selling Stockholder will pay any commissions and applicable to the Securities it sells.

Our common stock issued is traded on the OTCQB under the symbol “WTRV.” Our Warrants are expected to trade on the OTCQB under the symbol “WTRVW.” On September 29, 2023, the last reported sale price of our common stock on the OTCQB was $1.14.

Investing in our securities involves various risks. See “Risk Factors” beginning on page 4 of this Prospectus for a discussion of information that should be considered in connection with an investment in our securities.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this Prospectus is September 29, 2023

Table of Contents

You should rely only on information contained in this Prospectus. We have not authorized anyone to provide you with information that is different from that contained in this Prospectus. The Selling Stockholders are not offering to sell or seeking offers to buy securities in jurisdictions where offers and sales are not permitted. We are responsible for updating this Prospectus to ensure that all material information is included and will update this Prospectus to the extent required by law.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Prospectus contains, in addition to historical information, certain forward-looking statements, that includes information relating to future events, future financial performance, strategies, business opportunities, expectations including our goals and projections with respect to the planned Spin-Off by Ecoark of our common stock issuable upon conversion of its preferred stock, the expected results from and trends and developments in our oil and gas drilling and related activities, future plans for and anticipated transactions and relationships with respect to our oil and gas portfolio and operations and potential acquisition of a broker-dealer, our working capital needs and liquidity issues, expectations with respect to Ault Energy and the resale of working interests, and potential financings through the sale of our common stock or other securities, the subsequent use and sufficiency of the proceeds from any capital raising methods we may undertake to fund our operations. Such forward-looking statements include those that express plans, anticipation, intent, contingency, goals, targets or future development and/or otherwise are not statements of historical fact. These forward-looking statements are based on our current expectations and projections about future events and they are subject to risks and uncertainties known and unknown that could cause actual results and developments to differ materially from those expressed or implied in such statements.

In some cases, you can identify forward-looking statements by terminology, such as “may,” “should,” “would,” “expect,” “intend,” “anticipate,” “believe,” “estimate,” “continue,” “plan,” “potential” and similar expressions. Accordingly, these statements involve estimates, assumptions and uncertainties that could cause actual results to differ materially from those expressed in them. Any forward-looking statements are qualified in their entirety by reference to the factors discussed throughout this Prospectus or incorporated herein by reference.

You should read this Prospectus and the documents we have filed as exhibits to the Registration Statement, of which this Prospectus is a part, completely and with the understanding that our actual future results may be materially different from what we expect. You should not assume that the information contained in this Prospectus or any prospectus supplement is accurate as of any date other than the date on the front cover of those documents.

Risks, uncertainties and other factors that may cause our actual results, performance or achievements to be different from those expressed or implied in our written or oral forward-looking statements may be found in this Prospectus under the heading “Risk Factors.”

Forward-looking statements speak only as of the date they are made. You should not put undue reliance on any forward-looking statements. We assume no obligation to update forward-looking statements to reflect actual results, changes in assumptions or changes in other factors affecting forward-looking information, except to the extent required by applicable securities laws. If we do update one or more forward-looking statements, no inference should be drawn that we will make additional updates with respect to those or other forward-looking statements. New factors emerge from time to time, and it is not possible for us to predict which factors will arise. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. We qualify all of the information presented in this Prospectus particularly our forward-looking statements, by these cautionary statements.

| ii |

PROSPECTUS SUMMARY

Our Business

Overview

White River is a holding company which beginning in late July 2022 operates in the oil and gas exploration and drilling industry through White River Holdings Corp. (“White River Holdings”). Prior to the White River Holdings acquisition, the Company was formerly in the early stages of operations in the online sporting goods space, and was planning to operate as a retail distributor of cannabis products in California. In September 2022, the Company sold each of these entities to focus exclusively on its core business in the energy sector through its oil and gas operations.

White River also manages White River Energy Partners I LP, referred to elsewhere in this Prospectus as the “Fund” or “WR Fund,” which is consolidated for accounting purposes by the Company as the Company’s subsidiary is the only managing general partner of the Fund and has the power to deploy the investments from Fund into the Company for the various drilling projects they undertake. The Limited Partnership Agreement dated October 31, 2022 was amended by the Amended and Restated Limited Partnership Agreement effective on August 17, 2023 (dated August 15, 2023) (the “Partnership Agreement”). A subsidiary of the Company is the managing partner of the Fund. The Company’s subsidiary, the managing general partner contributed $100 as a capital contribution, and the remaining ownership held by the other partners are reflected as non-controlling interest. The Fund was formed to provide the Company with a non-dilutive source of capital to fund its oil and gas drilling ventures.

White River Acquisition

On July 25, 2022, the Company acquired White River Holdings from Ecoark in exchange for 1,200 shares of the Company’s newly designated Series A Convertible Preferred Stock (the “Series A”). Subject to certain terms and conditions set forth in the Certificate of Designation of the Series A, the Series A will become convertible into 42,253,521 shares of the Company’s common stock upon such time as (A) the Registration Statement on Form S-1, of which this Prospectus forms a part, has been declared effective, and (B) Ecoark elects to distribute the underlying shares of the Company’s common stock to Ecoark’s stockholders. The Series A has a stated value of $30 million and has a liquidation preference over the common stock and any subsequent series of junior preferred stock equal to the stated value, plus any accrued but unpaid dividends. Following the acquisition, the Company’s business focus has been on maintaining and growing its revenue generating capabilities in the oil and gas production space through White River.

PIPE Offering

From October 19, 2022 through April 30, 2023, the Company entered into a Securities Purchase Agreement (“SPA”) pursuant to which the Company sold 263.1126308 Units to 168 accredited investors, with each Unit consisting of one share of Series C and five-year Warrants to purchase up to 200% of the shares of common stock issuable upon conversion of the Series C, at a purchase price of $25,000 per Unit for a total purchase price of $6,577,816 in the PIPE Offering. The net proceeds from the PIPE Offering, after offering expenses and related costs, have been used for working capital and general corporate purposes including oil and gas drilling on the Company’s working interests in Louisiana and Mississippi. The shares of the Series C are expected to be converted upon the effective registration of the Registration Statement which includes this Prospectus.

The shares of the Company’s common stock underlying the securities issued to Ecoark in the White River Holdings acquisition and to the Selling Stockholders in the PIPE Offering are being registered under the Registration Statement of which this Prospectus forms a part.

Principal Operations

Following the White River acquisition described above, our principal operations consist of generating revenue through oil and gas exploration, drilling and production. Through White River the Company is now engaged in oil and gas exploration, drilling, production, and operations on approximately 34,000 cumulative acres of active mineral leases in Louisiana and Mississippi. We may also expand our energy asset portfolio or engage in other energy-related strategic transactions as they arise, provided we have sufficient capital and market and regulatory conditions otherwise enable favorable to such transactions. Such transactions may serve a number of business objectives, including by seeking to expand our product and service offerings and/or to increase our geographic footprint.

Planned Acquisition of a Broker-Dealer

We also plan to acquire a licensed broker-dealer for the purpose of enabling the Company to create and sell interests in oil and gas funds to assist the Company in continuing its oil and gas exploration and drilling activities. In the furtherance of this goal, we have entered into a Membership Interest Purchase Agreement (“MIPA”) to acquire Commenda Securities LLC, (“Commenda”) a licensed broker-dealer which is registered with the Securities and Exchange Commission (the “SEC”), for $70,000 plus certain other items not to exceed $50,000. We have applied to the Financial Industry Regulatory Authority (“FINRA”) which must approve the change of control of the broker-dealer. In March and April 2023 we sold additional Units to raise capital that will be required for regulatory purposes in order to close the acquisition. However, no assurance can be given that our change of control of the broker-dealer will be approved, or that any such acquisition will be successful. If we are unable to acquire a broker-dealer, our plans with respect to these oil and gas funds could be limited or restricted. In August 2023 we extended the deadline for the closing under the MIPA from July 2023 to October 31, 2023 (and possibly to December 31, 2023) in exchange for additional consideration to Commenda.

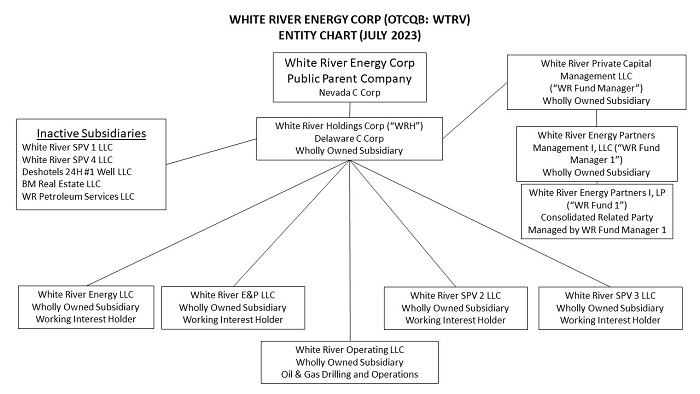

Organizational Chart

Set forth below is an organizational chart displaying the corporate structure of White River and our related subsidiaries, including the Fund:

| 1 |

THE OFFERINGS

| Issuer | White River Energy Corp, a Nevada corporation | |

| Spin-Off by Ecoark | 42,253,521 shares of White River common stock to be issued to Ecoark upon conversion of the Series A held by Ecoark and subsequently distributed by Ecoark to Ecoark’s stockholders on an as-converted basis as to the Ecoark convertible preferred stock, comprised of 36,503,711 Spin-Off Shares to be issued to holders of outstanding Ecoark common stock and up to 5,749,810 Spin-Off Shares to be issued to holders of outstanding Ecoark convertible preferred stock, which does not give effect to beneficial ownership limitations. These amounts are based on the total number of Spin-Off Shares divided by the 32,614,151 shares of Ecoark common stock outstanding and underlying the outstanding Ecoark convertible preferred stock (without taking into account the beneficial ownership limitations in the Ecoark preferred stock) as of the Record Date, which results in a Spin-Off ratio of 1.295557900618 White River Spin-Off Shares per Ecoark share of common stock. We may also issue up to 1,000 Fractional Shares as described elsewhere in this Prospectus. | |

| Securities offered by the Selling Stockholders | 25,396,899 shares of our common stock, which we refer to herein as “PIPE Shares,” comprised of (i) up to 8,465,633 shares of common stock issuable upon conversion of the Series C, and (ii) up to 16,931,266 shares of common stock issuable upon exercise of the Warrants. There are also up to 16,931,266 Warrants which may be separately sold by the Selling Stockholders rather than exercised, which together with the PIPE Shares are referred to herein as the “PIPE Securities.” As more particularly described under “The Private Placement,” the conversion price of the Series C, and in turn the number of PIPE Securities, is determined based on the lower of (i) $1.00 and (ii) 80% of the 30-day VWAP for the period ending on the 10th trading day preceding the effectiveness date (the “PIPE Securities Formula”). See also “Selling Stockholders.” | |

| Total common stock outstanding after these offerings | 78,485,220 shares of common stock; assuming all of the Shares offered in this offering are issued including the Spin-Off Shares and the PIPE Shares issuable upon conversion of the Series C and exercise of the Warrants. This amount does not include approximately 23,850,000 restricted stock units (“RSUs”) issued to the Company’s directors, officers, employees and advisors, which are subject to vesting conditions, as more particularly described under “Executive Compensation.” | |

| Use of Proceeds | We will not receive any proceeds from the sale of the Securities covered by this Prospectus. However, we will receive gross proceeds upon the exercise of the Warrants if exercised for cash. See “Use of Proceeds.” | |

| Risk Factors | Investing in our securities involves a high degree of risk. For a discussion of factors to consider before deciding to invest in our securities, you should carefully review and consider the “Risk Factors” beginning on page 4 of this Prospectus. |

| 2 |

Summary Risk Factors

Our business is subject to numerous risks and uncertainties that you should consider before investing in our common stock. Set forth below is a summary of the principal risks we face:

| ● | In our oil and gas operations, we have incurred losses since inception, we may continue to incur losses and negative cash flows in the future. | |

| ● | Conflicts of interest may arise, including rights granted to our executive officers under their Employment Agreements, the Company’s involvement in a new oil and gas drilling fund we sponsored, and other ventures our management and directors are or may become involved with separate from the Company. | |

| ● | We have a limited operating history, which makes it difficult to forecast our future results, making any investment in us highly speculative. | |

| ● | Potential impairment of intangible assets consisting of oil and gas reserves arising from our acquisition of White River Holdings in July 2022, which could adversely impact our stock price. | |

| ● | We may be required to record significant non-cash impairment charges related to a reduction in the carrying value of our proved oil and gas properties. | |

| ● | Our future cash flows and results of operations, are highly dependent on our ability to efficiently develop our current oil reserves and economically find or acquire additional recoverable reserves, as well as the prices of oil and gas which are subject to volatility. | |

| ● | Future approval by the SEC of its climate change rules and continued focus on environmental, social and governance (“ESG”) regulation and sustainability initiatives, which would have the effect of reducing demand for fossil fuels and negatively impact our operating results, stock price and ability to access capital markets. | |

| ● | We are focused exclusively on oil and gas operations with our initial portfolio located in only two states, and the lack of diversification exposes us and our investors to risk. | |

| ● | We face intense competition in the energy industry, much of which comes from larger competitors with longer operating histories, greater access to capital and human resources and vertically integrated operations, as well as smaller market participants which can more easily adjust to market conditions and trends. | |

| ● | We face risks related to our need for adequate insurance coverage and the possibility for uninsured or underinsured losses. | |

| ● | Because of the Russian invasion of Ukraine, high inflation and increased Federal Reserve interest rates in response as well as the banking crisis, we may have to deal with a recessionary economy which will reduce demand for our product. | |

| ● | Our future success depends on our ability to retain and attract high-quality personnel, and the efforts, abilities and continued service of our senior management. | |

| ● | We may struggle to manage our growth effectively, and as a result our business may be harmed. | |

| ● | Part of our business plan presently closing our acquisition of a broker-dealer to allow us to engage in fundraising efforts using multiple oil and gas funds over the next 10 years, and we may face challenges in this endeavor, including the high expenses and uncertainty in the acquisition process, exposure to liability through the acquired business, and regulatory burdens and related costs of compliance. | |

| ● | Certain of our activities or holdings, directly or through subsidiaries and other entities with which we do business, may subject us to federal or state regulation relating to investment companies and investment advisers. | |

| ● | Our common stock is currently a “penny stock” which trades on a limited basis on OTCQB, and due to factors beyond our control our stock price may be volatile. | |

| ● | Trading in our common stock is limited, and future sales of our common stock may depress our stock price. | |

| ● | Future issuances of our common stock, which we may effect to raise capital or for other reasons, would likely dilute the interests of our existing stockholders or have other adverse consequences. |

| 3 |

RISK FACTORS

Investing in our common stock involves a high degree of risk. Investors should carefully consider the following Risk Factors before deciding whether to invest in the Company. Additional risks and uncertainties not presently known to us, or that we currently deem immaterial, may also impair our business operations or our financial condition. If any of the events discussed in the Risk Factors below occur, our business, consolidated financial condition, results of operations or prospects could be materially and adversely affected. In such case, the value and marketability of the common stock could decline.

Risks Relating to Our Financial Condition

Because we have a limited operating history as a standalone oil and gas company, we cannot predict our future results.

White River’s oil and gas operations were operated under Ecoark as a portion of a larger public holding company with greater diversification and access to capital. Given our limited operating history as a standalone entity, it may be difficult to evaluate our future performance or prospects. You should consider the uncertainties that we may encounter as a company that should still be considered an early-stage oil and gas company. These uncertainties include:

| ● | the effect of the Biden Administration’s attempts to eliminate fossil fuels including the growth of the market for electric cars and trucks (and parallel state efforts); |

| ● | the impact from the SEC’s climate change rules; |

| ● | the price of oil; |

| ● | our ability to protect our oil and gas assets, including complying with mineral leases; |

| ● | our ability to locate and procure employees, contractors and third party service providers to assist us in our operations; |

| ● | our ability to adapt to changing market conditions and manage our planned growth effectively; and |

| ● | our evolving business model. |

If we are not able to address successfully some or all of these uncertainties, we may not be able to expand our business, compete effectively or achieve profitability.

| 4 |

We have incurred net losses since our inception and may continue to experience losses and negative cash flow in the future.

We have not been profitable since inception and have incurred significant operating losses and negative cash flow from operations particularly after our acquisition of White River Holdings. We recorded a net loss of approximately $43,089,977 and $6,922,753 for the fiscal year ended March 31, 2023 (“FY 2023”) and the fiscal year ended March 31, 2022 (“FY 2022”), respectively. For the three months ended June 30, 2023 (“FQ 23”), we incurred a net loss of $13,786,241 compared to a net loss of $1,986,544 for the three months ended June 30, 2022 (“FQ 22”). We may continue to incur losses and experience negative cash flows from operations for the foreseeable future. If we cannot achieve positive cash flow from operations or net income, we may need to raise additional capital on acceptable terms.

Because we require additional capital to fund our business objectives and support our growth, our inability to generate and obtain such capital could harm our business, operating results, financial condition and prospects.

Over the past two years, White River Holdings, increased its operating expenses in supporting its business of oil and gas exploration and drilling and consummating acquisitions of oil and gas properties. Included in our expenses is $150,000 per month in salary to two new officers of the management company for the Fund. We intend to continue to make substantial investments to fund our business and support our growth. Although we recently raised $6,577,816 in a Private Placement, we may desire to increase our drilling activity or acquire additional oil and gas properties. In addition, White River Energy Partners Management I LLC (the “Manager”), a subsidiary of the Company, is seeking to raise capital for the Fund in which the Manager is the managing general partner. In order to reduce dilution, our plan is to use investments into the Fund to support our drilling activities. However, through September 4, 2023, we have only raised $3,250,000 of the $50 million offering. See the Risk Factor on page 21 relating to issues with respect to capital raising for the Fund.

If we are unable to obtain adequate financing, our ability to continue to support our business growth and to respond to business challenges could be significantly impaired, and our business may be adversely impacted. In addition, our inability to generate or obtain the financial resources needed may require us to delay, scale back, or eliminate some or all of our operations and business objectives and sell some of our assets.

Further, if we (as contrasted to the drilling Fund discussed in this Prospectus) raise additional funds through future issuances of equity or convertible debt securities, our existing stockholders could suffer significant dilution, and any new equity or debt securities we issue could have rights, preferences and privileges superior to those of holders of our common stock.

| 5 |

Our ability to access capital markets could be limited.

From time-to-time, we may need to access capital markets to obtain long-term and short-term financing. However, our ability to access capital markets could be limited or adversely affected by, among other things, oil and gas prices, interest rates, our asset base, our track record in the industry, and the health or market perceptions of the drilling and overall oil and gas industry and the global economy. In addition, many of the factors that affect our ability to access capital markets, including the liquidity of the overall capital markets in general and the lack of liquidity for our common stock and the state of the economy and/or the oil and gas industry, among others, are outside of our control. There have also been efforts in recent years aimed at the investment community, including leading investment advisors, sovereign wealth funds, public pension funds, universities and other groups, promoting the divestment of fossil fuel equities as well as pressuring lenders and other financial services companies to limit or curtail activities with companies engaged in the extraction of fossil fuel reserves, which, if successful, could limit our ability to access capital markets. No assurance can be given that we will be able to access capital markets on terms acceptable to us when required to do so, which could adversely affect our business, financial condition and results of operations.

Since the Company’s executive officers are involved in other oil and gas ventures, and received certain interests and rights in our oil and gas drilling and production efforts pursuant to their Employment Agreements, conflicts of interest may arise.

Jay Puchir, the Company’s Chief Financial Officer, also serves as manager of the managing general partner of the Fund. The Company will act as the driller for the Fund and expects to receive management fees. While the Company’s management believes working with the Fund will benefit the Company, the Company and the Fund may compete with each other in drilling opportunities which creates a conflict of interest. To the extent that we have capital available to invest in drilling for our own account and the Fund participates either with us, or separately, to the extent that a well is successful, this conflict can adversely affect us. At the same time, we benefit if the well is not successful.

Additionally, pursuant to their respective Employment Agreements, each of Messrs. May and Puchir were granted a 5% overriding royalty interest or carried working interest (either, the “ORRI”) from the Company and its subsidiaries in any and all successfully drilled and completed oil and/or gas wells, as well as participation right of 15% and 10%, respectively, in the funding and ownership interest in any drilling or participation by the Company or any subsidiary in the drilling by a third party of an oil and gas well, which does not include the Fund but will include any other investment funds the Company sponsors. As of the date of this Prospectus, Messrs. May and Puchir have not exercised their participation rights in any of the Company’s drilling projects. The initial terms of their Employment Agreements are five years, subject in each case to renewal. While these arrangements are intended to directly align these officers’ incentives with the Company’s oil and gas exploration, drilling and production efforts by compensating them for the success of such ventures, they also directly divert any revenue generated by these ventures to these officers and away from the Company, which may be adverse to the Company and its stockholders. For example, a well that could have been profitable, or our operations as a whole, may not be profitable where it otherwise would have been as a result of the ORRI or the election of participation rights. Messrs. May and Puchir also have personal oil and gas investments which may also compete with the Company. These conflicts of interest may adversely affect our operations and financial condition, divert management’s time and attention away from running our primary business and result in our management to providing business opportunities to the Fund instead of the Company, any of which could materially adversely affect us.

Further, because each of Messrs. May and Puchir are also executive officers of Ecoark, they divert their limited time and attention to both entities and their respective businesses, and as a result conflicts of interest may arise that could be materially adverse to us.

Any of these or other endeavors that those involved in our operations chooses to pursue could materially harm our operations and ability to execute our business plan.

| 6 |

Because we have agreed with the Fund that we will subject to our cash availability and at the election of each partner redeem the investments of its partners, we may not have the capital to meet this obligation.

In order to attract investors to the Fund, subject to available cash we agreed to offer to redeem the investments of its partners (other than our subsidiary which is the managing general partner) within 90 days of the earlier of (i) 42 months after termination of the Fund’s offering, or (ii) June 30, 2027. As of the date of this Prospectus, the Fund has raised $3,250,000. The Company has extended the term of the Fund’s offering to December 31, 2023. The redemption price to be offered will be based upon the value of the units determined using a “PV20” industry formula conducted by an independent valuation firm selected by the Manager. See “Business-The Fund” at page 54.

We plan to launch a second limited partnership on or about January 1, 2024 and seek to raise up to $200 million with similar terms and conditions including redemption. We are hopeful that we receive approval to acquire the broker-dealer and that will assist us in raising substantially more money for the Fund and the second limited partnership. See the Risk Factors beginning at page 20.

We cannot predict what our financial condition or oil and drilling business will be on the redemption date(s), including whether we will have sufficient cash to meet our ongoing obligations and capital requirements. Because we have committed to offering to redeem partnership units, we are subject to the further risk that after making such payments, we will be unable to fund our ongoing operations or other capital commitments. While our redemption obligation is subject to our cash availability, if we have sufficient cash and use it to meet this obligation, our existing shareholders may be materially and adversely affected unless we can monetize the existing working interests held by the Fund through sale or borrowings. Usage of a substantial amount of cash could materially and adversely affect our ability to manage our business and carry on our oil and gas exploration activities. If we elect to borrow funds to redeem partners, we may incur substantial debt service obligations which will create additional expenses for us and may adversely affect our ability to buy drilling equipment, drill for new oil, and pay our obligations. In such an event, we would be forced to raise capital from one or more debt or equity financings to enable us to meet our working capital needs, which financings could be extremely dilutive, require us to pay high interest rates, dividends or other unfavorable financial terms, impose substantial restrictions on our operations or corporate governance, and contain other terms that are adverse to us and/or our other investors. If after redeeming partners, we encounter the events listed above, we may be required to cease operations. Further, if a dispute arises in connection with the Fund and its investors regarding the Company’s obligation to pay Fund investors and/or the amounts involved, the Company’s limited resources and personnel may need to be deployed towards such litigation, and we could be exposed to other adverse consequences as a result of such litigation, regardless of merit or outcome.

If we are unable to collect sums due to us for certain participation rights, we could experience material adverse consequences on our business and financial condition.

As described elsewhere in this Prospectus under “Business-Key Developments,” in connection with its participation rights in various drilling wells, as of September 4, 2023 Ault Energy, LLC (“Ault Energy”), a subsidiary of Ault Alliance, Inc. [NYSE American: AULT] (“Ault”) owes us $1,745,569 in obligations related to various drilling wells. We entered into an agreement on April 4, 2023 with Ecoark and Ault (dated March 29, 2023) with the goal of permitting Ecoark to pay us the sums due on behalf of Ault. However, due to Ecoark’s lack of cash resources, we may not receive any further amounts. Further, the Company also has very limited cash resources as of the date of this Prospectus in part due to the failure of Ault Energy and Ecoark to pay these obligations. The Company has reserved the sums due from Ault Energy as of June 30, 2023, which means that there is not an account receivable reflected on the balance sheet as of that date. Nonetheless, the legal obligation of Ault and Ecoark remains. Based on the passage of a substantial amount of time without receiving the amounts owed to us and the limited capital resources of Ault and Ecoark according to publicly available information, our management has concluded that the risk of us being unable to collect these amounts from Ault or from Ecoark which agreed to make payments on Ault’s behalf is significant. As a result, the Company notified Ault Energy that it has terminated Ault’s rights to participate in future wells we drill due to Ault’s failure to make the payments, which rights were based on an oral understanding between the parties, and the Company will therefore need to either find other investors or if the well begins production use the production that Ault would have received to fund the Company’s operations. While we believe termination of Ault’s rights is warranted due to Ault’s failure to perform its payment obligation, we may become subject to litigation with Ault concerning Ault’s rights with respect to the wells, which among other adverse consequences would require us to incur costly expenses and divert limited time and resources towards such litigation and away from our operations. In addition, we may seek to enforce payment by instituting litigation against Ault in connection with the foregoing. Further, the failure to receive the sums due has exacerbated the Company’s liquidity problems. The failure to receive the payments could have a material adverse effect on our business and financial condition, and your investment in us, including based on the risks described above and in the Risk Factor titled “We have significant ongoing capital requirements that could affect our operations if we are unable to generate sufficient cash from operations or obtain financing on favorable terms.”

Because we have not entered into a Transition Services Agreement with Ecoark, we may encounter certain risks which could result in damages to us.

Often in spin-offs, the company distributing the dividend or the parent and the company being spun-off enter into a Transition Services Agreement outlining the rights and responsibilities between the parties and providing for payment to cover services usually rendered by the parent company. Because we operate independently of Ecoark and have control of all of our assets, we did not think we needed any agreement which would the parties’ respective rights and obligations following the spin-off. However, if we are incorrect in this conclusion, we could encounter difficulty in proving our ownership of any assets or face liabilities to third parties for acts committed by Ecoark prior to the distribution. Once control of Ecoark changes, we may not be able to prove our ownership or we may to defend an asserted liability. If incur legal fees in seeking to prove title or lose control of any assets or if we are found liable for actions that were predominately due to Ecoark’s actions, we may be required to sue Ecoark since we have no contractual indemnification rights. Any costs or damages may be material and we cannot assure you we will be able to collect from Ecoark even if we are successful.

Risks Relating to Our Oil and Gas Exploration and Production Operations

We have significant ongoing capital requirements that could affect our operations if we are unable to generate sufficient cash from operations or obtain financing on favorable terms.

The Company’s drilling plan entails extracting oil reserves across its approximately 34,000 acres of shallow and deep drilling rights. The Company has purchased a deep drilling rig to further vertically integrate its operations. However, with historically high oil prices, ancillary services related to drilling and producing oil wells have risen significantly. The Company is largely vertically integrated, since its exploration and drilling activities are primarily conducted in-house except for (i) wire line services to obtain exploratory data, (ii) concrete procurement and installation at well sites, and (iii) seismic and geophysical services.

We expect to pay for projected capital expenditures related to exploring and drilling additional oil wells with cash flows from operations or the proceeds from equity sales, including the Company’s recent financings. We also enter into Participation Agreements wherein we grant an interest in a well in exchange for capital deployed towards the well’s drilling and completion. We are presently owed $1,745,569 from Ault which sum we have been unable to collect. See the Risk Factor titled “If we are unable to collect sums due to us for certain participation rights, we could experience material adverse consequences on our business and financial condition.” If we were unable to generate sufficient cash from operations, we would need to seek alternative sources of capital to meet our capital requirements, which we may be unable to obtain on favorable terms, within the timeframes needed or desired, or at all. To the extent that our working capital is insufficient, we may have to scale back operations including our drilling activity.

Since analyzing a well’s potential is very risky, our management may make errors in assessing the potential of wells which could lead to limited revenue.

In our efforts to acquire, explore, and drill interests in oil and gas wells, management will assess reports about the recoverable reserves, future oil and gas prices, operating costs, potential liabilities, and other factors relating to the wells. These assessments are necessarily inexact, and their accuracy is inherently questionable and uncertain. The review of a subject property in connection with its acquisition assessment may not reveal all existing or potential problems or permit it to become sufficiently familiar with the property to fully assess its deficiencies and capabilities. Management and other personnel involved in the process may not inspect every well, and may not be able to observe structural and environmental problems even if it does inspect a well. If problems are identified, various affiliates, vendors, contractors, or third parties may be unwilling or unable to provide effective contractual protection against all or part of those problems. Any acquisition of property interests may not be economically successful, and unsuccessful acquisitions may have a material adverse effect on the Company’s financial condition, and future results of operations.

| 7 |

Unless we develop new reserves, reserves we acquire and subsequent production will decline, which would adversely affect our future cash flows and results of operations.

Producing oil reservoirs generally are characterized by declining production rates that vary depending upon reservoir characteristics and other factors. Unless we conduct successful ongoing exploration and development activities or continually acquire properties containing proven reserves, our proven reserves will decline as those reserves are produced. Our future reserves and production, and therefore our future cash flow and results of operations, are highly dependent on our success in efficiently and economically finding or acquiring recoverable reserves. We may not be able to develop, find or acquire sufficient reserves to replace our current and future production. Further, our projections about a well’s production prospects could prove to be incorrect. If we are unable to replace our current and future production, the value of our reserves will decrease, and our business, financial condition and results of operations would be materially and adversely affected. If our estimates provide to be incorrect now or in the future, for some or all of the wells we are exploring and producing from, it could materially adversely affect our operating results.

The loss of any of, or a material reduction in orders from, our largest customers would materially and adversely affect our results of operations and financial condition.

Our oil and gas business is and has been characterized by a high degree of customer concentration and reliance on a very limited number of customers for our revenue. The loss of any of these customers, particularly Plains Marketing, LP, a leading midstream energy company which we frequently rely on for our sales, or a material reduction in their purchases from us spending activities generally, would have a material adverse effect on our financial condition, liquidity and results of operations.

Since our exploration and production operations are subject to stringent environmental, oil and gas-related and occupational safety and health laws and regulations, noncompliance with such laws and regulations could expose us to material costs and liabilities.

Our exploration and production operations are subject to stringent federal, state and local laws and regulations governing, among other things, the drilling activities, production rates, the size and shape of drilling and spacing units or proration units, the transportation and sale of crude oil, gas, and the discharging of materials into the environment and environmental protection. These laws and regulations may limit the amount of oil and gas we can produce or limit the number of wells or the locations where we can drill.

Further, we are required to obtain and maintain numerous environmental and oil and gas-related permits, approvals and certificates from various federal, state and local governmental agencies in connection with our exploration and production operations, and may incur substantial costs in doing so. If we acquire gas wells we may in the future be charged royalties on gas emissions or required to incur certain capital expenditures for air pollution control equipment or other air emissions-related issues. Additionally, our operations are subject to a number of federal and state laws and regulations, including the federal occupational safety and health and comparable state statutes, aimed at protecting the health and safety of employees.

| 8 |

Another significant risk inherent in drilling plans is the need to obtain drilling permits from local, state, federal and other governmental authorities, as appropriate. Delays in obtaining regulatory approvals and drilling permits, including delays which jeopardize our ability to realize the potential benefits from leased properties within the applicable lease periods, the failure to obtain a drilling permit for a well, or the receipt of a permit with unreasonable conditions or costs could have materially adverse effects on our ability to capitalize on proposed projects. As long as the Biden Administration or a successor Democratic Administration holds the Office of President, we expect the permitting process on federal lands will be marked by delays and refusals.

Although we will use third party contractors to handle delivery of crude oil and by-products, we may be subject to environmental liabilities for the acts of the contractors arising from the hauling and handling of hazardous materials, air emissions from our vehicles and facilities, and engine idling and discharge. Our operations involve the risks of environmental damage and hazardous waste disposal, among others. If we are involved in an accident involving hazardous substances, if there are releases of hazardous substances we transport, if soil or groundwater contamination is found at our facilities or results from our operations, or if we are found to be in violation of applicable environmental laws or regulations, we could owe clean-up costs and incur related liabilities, including substantial fines or penalties or civil and criminal liability, any of which could have a materially adverse effect on our business and operating results.

Failure to comply with these laws and regulations may subject us to sanctions, including administrative, civil or criminal penalties, remedial clean-ups or corrective actions, delays in permitting or performance of projects, natural resource damages and other liabilities. In addition, these laws and regulations may be amended and additional laws and regulations may be adopted in the future with more stringent legal requirements.

Our operations may generate waste that may be subject to the Federal Resource Conservation and Recovery Act (“RCRA”) and comparable state statutes. The EPA and various state agencies have limited the approved methods of disposal for certain hazardous and nonhazardous waste. Furthermore, certain waste generated by natural gas and oil operations that are currently exempt from treatment as hazardous waste may in the future be designated as hazardous waste and therefore become subject to more rigorous and costly operating and disposal requirements.

The Comprehensive Environmental Response, Compensation and Liability Act (“CERCLA”), RCRA and analogous state laws impose liability, without regard to fault or the legality of the original conduct, on specified classes of persons that are considered to have contributed to the release of a hazardous substance into the environment. These classes of persons include the owner or operator of the disposal site or sites where the release occurred and companies that disposed or arranged for the disposal of the hazardous substances found at the site. Persons who are or were responsible for releases of hazardous substances under CERCLA may be subject to joint and several liability for the costs of cleaning up the hazardous substances that have been released into the environment, for damages to natural resources, and for the costs of certain health studies. It is not uncommon for neighboring landowners and other third parties to file claims for personal injury and property damage allegedly caused by the hazardous substances released into the environment.

| 9 |

Our operations also may become subject to the Clean Air Act (“CAA”) and comparable state and local requirements. In 1990, Congress adopted amendments to the CAA containing provisions that have resulted in the gradual imposition of certain pollution control requirements with respect to air emissions. The EPA and states have developed and continue to develop regulations to implement these requirements. We are also subject to a variety of federal, state, local and international permitting and registration requirements relating to protection of the environment. While the Company believes it is in substantial compliance with current applicable environmental laws and regulations and that continued compliance with existing requirements will not have a material adverse effect on its operations, but it cannot be certain.

Legislation, regulations or government actions related to climate change, greenhouse gas emissions and sustainability initiatives and other “ESG” laws, regulations and government action, could result in increased compliance and operating costs and reduced demand for fossil fuels, and concern in financial and investment markets over greenhouse gasses and fossil fuel production could adversely affect demand for our products, limit our access to capital and materially and adversely affect our future operating results.

As described under “Business-Government Regulations”, our operations are regulated extensively at the federal, state and local levels, and lawmakers and government agencies continue to consider potential new laws and regulations that would regulate or otherwise affect our industry. Environmental and other governmental laws and regulations have increased the costs to plan, design, drill, install, operate and abandon oil and natural gas wells. The trend in recent years has been increased scrutiny and regulatory oversight of the oil and gas industry, including among other things increasingly the proposal of new laws and regulations aimed at reducing or restricting oil and gas production and use. For example, in a rulemaking notice in mid-November 2022, the EPA announced a new calculation that would raise the damage estimate referred to as the “Social Cost of Carbon” of from $51 per metric ton, which had been the rate for the last several years, to $190 per metric ton by 2022 and as much as $410 by the year 2080. This amount is expected to guide or influence numerous laws and regulations in the future that are designed to reduce carbon emissions and the harm they cause to the environment. Under these laws and regulations, we could also be liable for personal injuries, property damage and other damages. In addition, failure to comply with these laws and regulations may result in the suspension or termination of our operations and subject us to administrative, civil and criminal penalties and fines.

The adoption and implementation of these and other similar regulations could require us to incur material costs to monitor and report on greenhouse gas emissions or install new equipment to reduce emissions of greenhouse gases associated with our operations. In addition, these regulatory initiatives could drive down demand for our products and services in the oil and gas industry by stimulating demand for alternative forms of energy that do not rely on combustion of fossil fuels that serve as a major source of greenhouse gas emissions, which could have a material adverse effect on our business, financial condition, results of operations and cash flows. This could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

| 10 |

Because of the trend to use alternative energy technologies rather than oil and gas, it could have a material adverse effect on our results of operations.

Since our business depends on the level of activity in the oil and natural gas industry, any improvement in or new discoveries of alternative energy technologies that increase the use of alternative forms of energy and reduce the demand for oil and natural gas could have a material adverse effect on our business, financial condition and results of operations. As the United States and certain other countries transition to electric vehicles and as certain states in the United States are banning any usage of gas as a fuel, the oil and gas business is adversely affected. We will be further subject to state regulatory efforts such as California’s announced goal of eliminating the sale of vehicles which use gas by 2035. Automobile manufacturers are beginning to announce that they will only manufacture electric vehicles in the future. President Biden has also stated that the 2022 retail price rise in the price of gasoline was part of a plan to transition to electric vehicles.

As an example, in August 2022, the California Air Resources Board passed a rule banning the sale of gas vehicles by 2035, requiring 35% of new passenger vehicles sold by 2026 to be electric or otherwise not using gas with the number rising to 68% by 2030. It has been reported that more than a dozen states typically follow California which is the largest market for the sale of passenger vehicles. To date, New York, New Jersey, Massachusetts, Maryland, Washington and Oregon have followed California. The State of Washington has enacted a Rule similar to California. California also enacted a law effective July 1, 2022 banning the sale of gas powered lawn mowers and leaf blowers starting in 2024. Further in late September 2022 the California Air Resources Board banned natural gas heaters and furnaces by 2030. In May 2023 New York State passed a law banning gas stoves and furnaces, with limited exceptions, for all new buildings less than seven stories by 2026 and taller buildings by 2029. As this and the other trends outlined above are implemented, the Company could incur material and adverse effects on its results of operations.

Because we expect the SEC will adopt most, if not all of its proposed climate change rules, as a small producer, the compliance costs may adversely affect our future results of operating and financial condition, which effects may be material.

On March 21, 2022, the SEC released proposed rule changes that would require new climate-related disclosure in SEC filings, including certain climate-related metrics and greenhouse gas emissions, information about climate-related targets and goals, transition plans, if any, and extensive attestation requirements. In addition to requiring filers to quantify and disclose direct emissions data, the new rules would also require disclosure of climate impact arising from the operations and uses by the filer’s business partners and contractors and end-users of the filer’s products and/or services. If adopted as proposed, the rule changes would apply to the Company and result in us incurring material additional compliance and reporting costs, including monitoring, collecting, analyzing and reporting the new metrics and implementing systems and procuring additional internal and external personnel with the requisite skills and expertise to serve those functions. Such costs are likely to adversely affect our future results of operations and financial condition, which may be material. We expect the rule will be adopted in 2023 and be effective beginning at some point within a relatively short time period following adoption. We cannot predict the outcome of litigation which we expect will challenge any new climate change rules.

If Congress enacts the proposed price gouging bill, it could have a material adverse effect on our oil and gas operations and the Fund.

Senator Elizabeth Warren and others have introduced legislation aimed at rising gasoline and other prices and would empower the Federal Trade Commission (“FTC”) to investigate and penalize companies with “unconscionably excessive price increases.” The proposed legislation does not define what this phrase means so it will permit the FTC to define it. While we cannot predict whether the legislation will pass, the recent election and the apparent Republican control of the House of Representatives may mean the proposed bill will not be enacted. If it does pass, the FTC will enact Rules although it is possible it may enact an emergency Rule like other regulatory agencies have recently done. Any such legislation will likely affect gasoline prices. We believe price controls will have a material adverse effect on the Company and the Fund.

| 11 |

Because competition in the oil and natural gas industry is intense, we may be unable to effectively compete with larger companies with greater financial, technical and managerial resources.

We are a relatively small participant in the United States onshore oil and gas exploration and drilling industry and we face significant competition from major energy companies with substantial financial, technical, management, and other resources as well as large and other privately-held businesses which have competitive advantages. While we are mostly vertically integrated, our cost of operations is dependent in part on certain third-party services, and competition for these services can be significant, especially in times when commodity prices are high. Similarly, if and as we grow we will compete for trained, qualified personnel, and in times of lower prices for oil, we and other companies with similar production profiles may not be able to attract and retain this talent. Conversely, some of our competitors have a broader portfolio properties, assets and rights that in many cases enable them to both explore and drill wider geographic areas with a greater likelihood of success and/or complete the exploration, drilling, distribution and sale processes at lower costs while also offering related services to third parties.

Our ability to acquire and develop reserves in the future, and maintain and grow our customer base will depend on our ability to evaluate and select suitable properties and assets and to consummate transactions in a highly competitive environment for acquiring such properties and assets, marketing oil and gas, securing and compensating trained personnel and meeting demand for our products and services. Also, there is substantial competition for capital available for investment in the oil and gas industry. Our competitors may be able to pay more to acquire working interests in oil and gas leases as well as for personnel, property and services and to attract capital at lower rates. Because of our small size, we may be more affected than larger competitors. Further, the current inflation the United States is facing will affect us more that many well capitalized competitors.

The potential lack of availability of, or cost of, drilling rigs, equipment, supplies, personnel and crude oil field services could adversely affect our ability to execute on a timely basis our exploration and development plans within our budget.

We currently own three drilling rigs which can perform deep vertical and horizontal/directional drilling projects in depths of up to 34,000 feet, and three workover rigs. When the prices of crude oil increase, or the demand for equipment and services is greater than the supply in certain areas, we could encounter an increase in the cost of securing a deep drilling rig capable of performing lateral drilling projects in the Tuscaloosa Marine Shale. In addition, larger producers may be more likely to secure access to such equipment by offering more lucrative terms. If we are unable to acquire access to such resources, or can obtain access only at higher prices, our ability to convert our reserves into cash flow could be delayed and the cost of producing those reserves could increase significantly. In addition to increasing our costs, we may face the possibility of poorly rendered services or faulty or damaged equipment coupled with potential damage to downhole reservoirs and personnel injuries. Such issues can increase the actual cost of services, extend the time to secure such services and add costs for damages due to accidents sustained from the overuse of equipment and inexperienced personnel. All of these factors may adversely affect our results of operations and financial condition.

| 12 |

Drilling for and producing crude oil involves significant risks and uncertainties that could adversely affect our business, financial condition or results of operations.

Our drilling and production activities are subject to many risks, including the risk that we will not discover commercially productive reservoirs. Drilling for crude oil can be unprofitable, not only from dry holes, but from productive wells that do not produce sufficient revenues to return a profit. In addition, our drilling and producing operations may be curtailed, delayed or cancelled as a result of other factors, including but not limited to:

| ● | unusual or unexpected geological formations and miscalculations; |

| ● | fires; |

| ● | explosions and blowouts; |

| ● | pipe or cement failures; |

| ● | environmental hazards, such as natural gas leaks, oil spills, pipeline and tank ruptures, encountering naturally occurring radioactive materials, and unauthorized discharges of toxic gases, brine, well stimulation and completion fluids, or other pollutants into the surface and subsurface environment; |

| ● | loss of drilling fluid circulation; |

| ● | title problems for the properties on which we drill and resulting restrictions or termination of lease for oil drilling and production operations; |

| ● | facility or equipment malfunctions; |

| ● | unexpected operational events, especially the need to drill significantly deeper than originally contemplated or finding, despite an engineering study to the contrary; |

| ● | shortages of skilled personnel or unexpected loss of key drilling and production workers; |

| ● | shortages or delivery delays of equipment and services or of water used in hydraulic fracturing activities; |

| ● | compliance with environmental and other regulatory requirements and any unexpected remedial requirements for violations of environmental or other regulatory requirements; |

| ● | stockholder activism and activities by non-governmental organizations to restrict the exploration, development and production of oil and natural gas so as to minimize emissions of greenhouse gases; |

| ● | natural disasters; and |

| ● | adverse weather conditions. |

Some of the listed factors have occurred and adversely affected our business and reduced revenue. Any of these risks can cause substantial losses, including personal injury or loss of life, severe damage to or destruction of property, natural resources and equipment, pollution, environmental contamination, clean-up responsibilities, loss of wells, repairs to resume operations; and regulatory fines or penalties. Further, our exposure to operational risks may increase as our drilling activity expands.

| 13 |

We may not be insured or fully insured against certain of the above operational risks, either due to unavailability of such insurance or the high premiums and deductibles. The occurrence of an event that is not covered in full or in part by insurance could have a material adverse impact on our business, financial condition and results of operations.

Because of the speculative nature of drilling oil and gas wells, we cannot guarantee any return on your investment.

Oil and natural gas exploration is an inherently speculative activity. Before the drilling of a well, we cannot predict with absolute certainty the volume of oil and natural gas recoverable from the well; or the time it will take to recover the oil and gas.

In addition, oil and gas wells by their nature are depleting assets with respect to which production could last anywhere from a few months to more than 30 years. As a result, annual production will naturally decline over the life of a well, and so too will returns to investors.

Even if targeted wells are completed and produce oil and gas in commercial quantities, it may not produce enough oil and gas to pay for the costs of drilling and completing the well.

Because the oil and gas drilling business is very cyclical, we may face a downturn which in turn can adversely affect our business.

Between inflation, supply chain shortages and the war in Ukraine, among other factors, the price of oil has spiked in 2022 with peak oil prices over $122 per barrel of oil for WTI crude on June 8, 2022, which was the highest level in over 10 years. However, as the economy is seemingly worsening, the price of crude oil fell to early January levels with WTI crude at $78.74 on September 24, 2022, although the price increased to above $90 in early November 2022. As of September 4, 2023, WTI crude oil traded at approximately $85.55 per barrel. Changes in oil and natural gas prices (and specifically downwards trends or the lack of an increase) will have a significant adverse impact on our cash flow. Lower oil and gas prices may not only impact our revenues, but also may reduce the amount of oil and gas that we can produce economically. Historically, oil and gas prices have been volatile, and it is likely that they will continue to be volatile in the future. At some point, the regulatory factors facing fossil fuels and the drilling for oil as well as a recession may make oil drilling financially unattractive. In that event, our results of operations may be materially and adversely affected.

The volatility of oil and natural gas prices could also hamper our ability to produce oil and gas economically. Oil and natural gas prices are volatile, and a decline in prices could significantly, adversely affect both profitability and overall financial health of the Company. The oil and gas industry has experienced severe downturns characterized by oversupply and/or weak-to-zero demand.

Our future revenues from exploration and production operations, cash flows, and carrying value of our oil and gas properties will depend on oil prices. Commodity prices, including oil, are highly volatile and may fluctuate widely in response to relatively minor changes in supply and demand and market uncertainty. Additional factors which may affect oil prices and which are beyond our control include but are not limited to, the following factors:

| ● | worldwide and regional economic conditions impacting the global supply of and demand for oil, including the impact of the Russian invasion of Ukraine and inflation; |

| ● | the price and quantity of foreign imports of oil; |

| 14 |

| ● | consumer and business demand; |

| ● | geopolitical and economic conditions in or affecting other producing regions or countries, including the Middle East, Africa, South America and Russia; |

| ● | actions of the Organization of the Petroleum Exporting Countries, its members and other state-controlled oil companies relating to oil price and production controls; |

| ● | the level of global exploration, development and production; |

| ● | the level of global inventories; |

| ● | prevailing prices on local price indexes in the area in which we operate; |

| ● | the proximity, capacity, cost and availability of gathering and transportation facilities; |

| ● | localized and global supply and demand fundamentals and transportation availability; |

| ● | the cost of exploring for, developing, producing and transporting reserves; |

| ● | weather conditions and other natural disasters; |

| ● | technological advances affecting energy consumption; |

| ● | the price and availability of alternative fuels; |

| ● | government regulations, such as regulation of natural gas transportation and price controls; |

| ● | U.S. federal, state and local and non-U.S. governmental regulation and taxes; and |

| ● | market perceptions of future prices, whether due to the foregoing factors or others. |

Because oil prices have been volatile, there can be no certainty as to if, when and to what extent they may decline in the future. Further, while higher oil prices generally provide benefits to our drilling operations to the extent we have productive wells during the high price periods, they also pose increased costs in drilling additional wells.

Our operating results fluctuate due to the effect of seasonality, adverse weather or other natural occurrences that generally impact the oil and gas industry.

Operating levels of the oil industry have historically been lower in the winter months because of adverse weather conditions. More recently, we have experienced slowdowns from heavy rains and tornadoes. Accordingly, our revenue generally follows a seasonal pattern. Revenue can also be affected by other adverse weather conditions, holidays and the number of business days during a given period because revenue is directly related to the available working days. From time-to-time, we may suffer short-term impacts from severe weather and similar events, such as tornadoes, hurricanes, blizzards, ice storms, floods, fires, earthquakes, and explosions that could materially harm our results of operations or make our results of operations more volatile.

Because we may be subject to various claims and lawsuits in the ordinary course of business, increases in the amount or severity of these claims and lawsuits could adversely affect us.

In the ordinary course of our planned business, we may be exposed to various claims and litigation related to commercial disputes, personal injury, property damage, environmental liability and other matters. If we incur increases in litigation or serious claims, there are developments in legislative or regulatory trends, or our employees or contractors incur a catastrophic accident or series of accidents, involving property damage, personal injury, or environmental liability it could have a material adverse effect on our operating results and financial condition.

| 15 |

The extension of our active oil and gas mineral leases are in some cases subject to performing continuous drilling operations.

Our oil and gas mineral leases may contain acreage that is either held by production or not. In order to extend the leased acreage not held by production, the Company must maintain minimum continuous drilling operations in order to extend these leases to future periods. Further, at least one of our leases requires us to drill a new well every 270 days in order to maintain the rights, and our failure to do so would result in us losing the rights unless the owner agrees to a waiver or extension. The Company’s inability to perform operations during any given period could result in the Company’s losing the rights to future operations on that lease. The Company had until August 18, 2023 to begin drilling another well on this lease to maintain this lease, and commenced drilling a well by that deadline, thereby extending the aforementioned deadline under the lease for another 270 days.

We may be required to meet future drilling conditions and lack the capital to protect our interest in one or more wells.

In addition to the requirements under our current interests, we may acquire interests in wells that require continuous drilling in order to maintain our interest. In the past, White River Holdings a then subsidiary of Ecoark was unable to meet the drilling condition, which permitted our Chief Executive Officer (who is also Ecoark’s Chief Executive Officer) to personally acquire a portion of the working interest when he made the required investment. Because we may acquire oil and gas mineral leases that may require future drilling to maintain the leasehold interest, if we do the Company will be required to invest in future drilling in order to extend these leases to future periods or lose the interest in any such leases. If we lack the capital, our affiliates may acquire the leases by investing their own capital.

Our ability to spread the risks of drilling among many wells may be limited.

Our ability to spread risks through diversification will be related to our ability to obtain the necessary capital and other resources needed to evaluate a well’s prospects and deploy drilling equipment, as well as acquire and maintain drilling rights. Limited capital will force us to drill fewer wells, or forego opportunities management deems to be attractive, which decreases our ability to spread the risks of drilling and mitigate the possibility of deploying our limited resources towards a successful drilling venture. In addition, our revenue and ability to achieve or maintain profitability may decrease if management is unable to find enough suitable well locations to be drilled. While we have approximately 34,000 acres to select drilling locations from, there can be no assurance that we will be successful in drilling in a manner or pace that enables us to generate sufficient revenue at low enough costs to become profitable.

The Company may face issues with title defects, which could result in losses in leases which the Fund acquires.

There may be defects in the title to the leases on which the Company’s wells are drilled. In certain instances, the Company may elect not to obtain title opinions or take certain other due diligence related actions that could have otherwise unveiled problems, due to cost, timing or other constraints. Thus, the Company may experience losses from title defects which arose during drilling that would have been disclosed by such due diligence. Also, the Company may waive title requirements for the leases on which the Company’s wells are drilled. Any failure of title of working interest transferred to the Company could materially adversely affect our operating results and business.

| 16 |

We may be required to record significant non-cash impairment charges related to a reduction in the carrying value of our proved oil and gas properties, which could materially and adversely affect our results of operations.