This draft registration statement has not been publicly filed with the Securities and Exchange Commission and all information herein remains strictly confidential.

As confidentially submitted with the Securities and Exchange Commission on June 25, 2021

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

PROCEPT BIOROBOTICS CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware | 3841 | 26-0199180 | ||||||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) | ||||||

900 Island Drive

Redwood City, CA, 94065

(650) 232-7200

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Reza Zadno, Ph.D.

Chief Executive Officer

900 Island Drive

Redwood City, CA, 94065

(650) 232-7200

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

B. Shayne Kennedy Drew Capurro Latham & Watkins LLP 650 Town Center Drive, 20th Floor Costa Mesa, CA 92626 (714) 540-1235 | Alaleh Nouri General Counsel Jonathan Stone Senior Corporate Counsel 900 Island Drive Redwood City, CA, 94065 (650) 232-7200 | Charles S. Kim Kristin VanderPas Dave Peinsipp Denny Won Cooley LLP 4401 Eastgate Mall San Diego, CA 92121 (858) 550-6000 | ||||||

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | Accelerated filer | o | ||||||||

| Non-accelerated filer | x | Smaller reporting company | x | ||||||||

| Emerging growth company | x | ||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

Title of each class of securities to be registered | Proposed maximum aggregate offering price(1)(2) | Amount of registration fee(3) | ||||||

| Common stock, par value $0.00001 per share | $ | $ | ||||||

(1)Estimated solely for the purpose of calculating the registration fee in accordance with Rule 457(o) under the Securities Act of 1933, as amended.

(2)Includes the offering price of shares of common stock that may be sold if the underwriters fully exercise their option to purchase additional shares of common stock.

(3)To be paid in connection with the initial filing of the registration statement.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

EXPLANATORY NOTE

Pursuant to the applicable provisions of the Fixing America’s Surface Transportation Act, we are omitting our unaudited financial statements as of and for the three months ended March 31, 2020 and 2021 because they relate to historical periods that we believe will not be required to be included in the prospectus at the time of the first public filing of the registration statement. We intend to include all financial information required by Regulation S-X at the date of such public filing of the registration statement.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state or other jurisdiction where the offer or sale is not permitted.

Subject to Completion

Preliminary Prospectus dated , 2021

Shares

Common Stock

This is an initial public offering of shares of common stock of PROCEPT BioRobotics Corporation. We are selling shares of our common stock.

Prior to this offering, there has been no public market for our common stock. It is currently estimated that the initial public offering price will be between $ and $ per share. We intend to apply to list our common stock on the Nasdaq Global Market under the symbol “PRCT.”

We are an “emerging growth company” and a “smaller reporting company” as defined under the federal securities laws and, as such, we have elected to comply with certain reduced public company reporting requirements for this prospectus and may elect to do so in future filings.

Investing in our common stock involves risks that are described in the “Risk Factors” section beginning on page 13 of this prospectus.

| Per Share | Total | ||||||||||

Initial public offering price | $ | $ | |||||||||

Underwriting discounts and commissions(1) | $ | $ | |||||||||

Proceeds, before expenses, to us | $ | $ | |||||||||

__________

(1)See the section titled “Underwriting” for additional information regarding compensation payable to the underwriters.

To the extent that the underwriters sell more than shares of common stock, the underwriters have the option to purchase up to an additional shares of common stock from us at the initial public offering price less the underwriting discounts and commissions.

Neither the Securities and Exchange Commission nor any other state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of common stock to purchasers on or about , 2021.

| BofA Securities | Goldman Sachs & Co. LLC | ||||||||||

| Cowen | Guggenheim Securities | SVB Leerink | |||||||||

The date of this prospectus is , 2021

TABLE OF CONTENTS

| Page | |||||

CERTAIN TRADEMARKS, TRADE NAMES AND SERVICE MARKS | |||||

__________________

We have not, and the underwriters have not, authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses prepared by or on behalf of us or to which we have referred you. We and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares of common stock offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus or in any applicable free writing prospectus is current only as of its date, regardless of its time of delivery or any sale of shares of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

For investors outside the United States: We have not, and the underwriters have not, done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of common stock and the distribution of this prospectus outside the United States.

i

MARKET AND INDUSTRY DATA

This prospectus includes estimates regarding market and industry data that we prepared based on our management’s knowledge and experience in the markets in which we operate, together with information obtained from various sources, including publicly available information, industry reports and publications, surveys, our customers, distributors, suppliers, trade and business organizations and other contacts in the markets in which we operate. In some cases, we do not expressly refer to the sources from which this data is derived. Management estimates are derived from publicly available information released by independent industry analysts and third-party sources, as well as data from our internal research, and are based on assumptions made by us upon reviewing such data and our knowledge of such industry and markets which we believe to be reasonable.

In presenting this information, we have made certain assumptions that we believe to be reasonable based on such data and other similar sources and on our knowledge of, and our experience to date in, the markets for the products we distribute. Market share data is subject to change and may be limited by the availability of raw data, the voluntary nature of the data gathering process and other limitations inherent in any statistical survey of market shares. In addition, customer preferences are subject to change. Accordingly, you are cautioned not to place undue reliance on such market share data.

CERTAIN TRADEMARKS, TRADE NAMES AND SERVICE MARKS

This prospectus includes trademarks and service marks owned by us, including, without limitation, PROCEPT BioRobotics®, AquaBeam®, Aquablation®, and our logo, which are our property and are protected under applicable intellectual property laws. This prospectus also contains trademarks, trade names and service marks of other companies, which are the property of their respective owners. Solely for convenience, trademarks, trade names and service marks referred to in this prospectus may appear without the ®, ™ or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks, trade names and service marks. We do not intend our use or display of other parties’ trademarks, trade names or service marks to imply, and such use or display should not be construed to imply, a relationship with, or endorsement or sponsorship of us by, these other parties.

ii

PROSPECTUS SUMMARY

This summary highlights selected information contained elsewhere in this prospectus. Because this is only a summary, it does not contain all the information that may be important to you. You should read the entire prospectus carefully, especially the sections titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” as well as our consolidated financial statements and related notes included elsewhere in this prospectus, before deciding to invest in our common stock. In this prospectus, unless the context requires otherwise, references to “PROCEPT,” the “Company,” “we,” “us,” and “our,” refer to PROCEPT BioRobotics Corporation.

Our Company

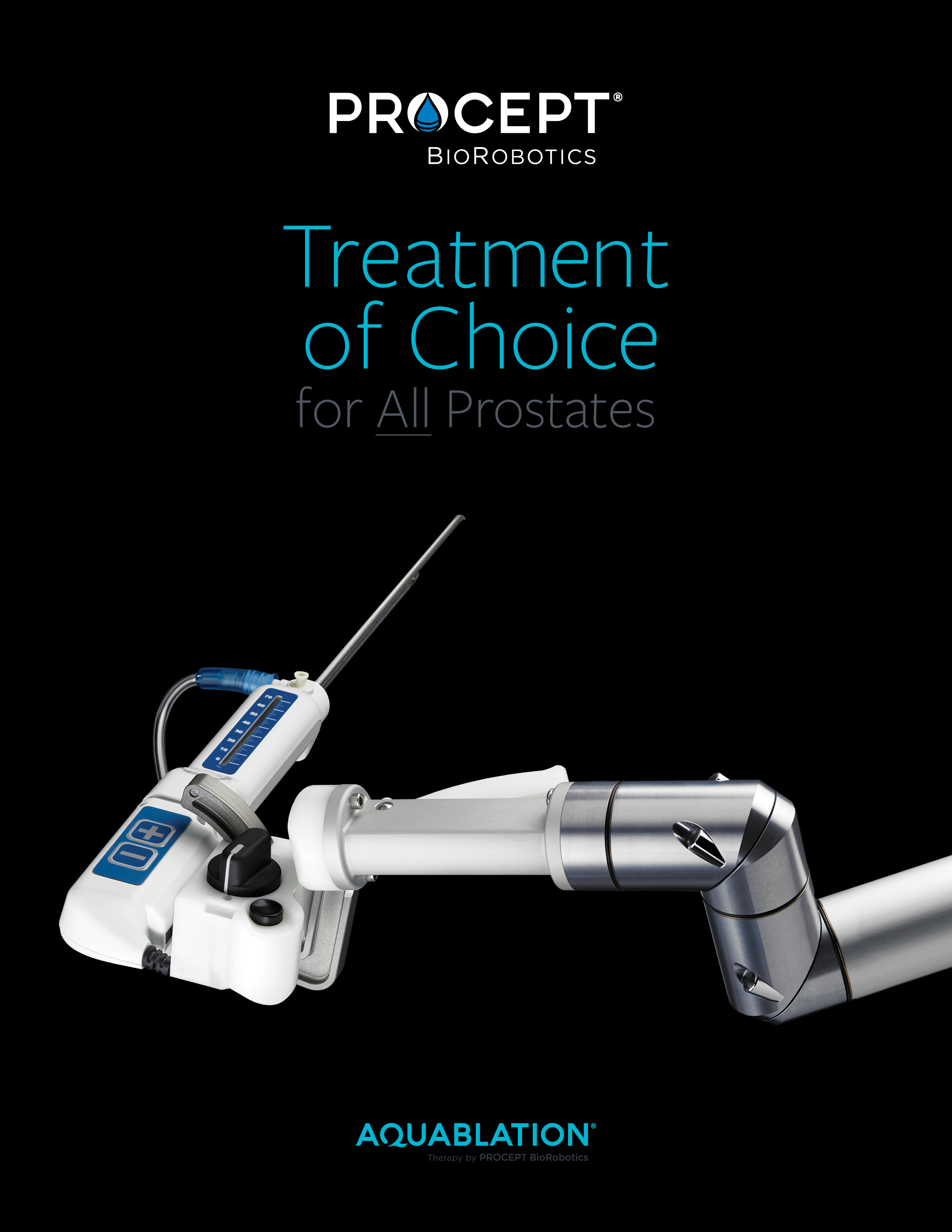

We are a commercial-stage surgical robotics company focused on advancing patient care by developing transformative solutions in urology. We develop, manufacture and sell the AquaBeam Robotic System, an advanced, image-guided, surgical robotic system for use in minimally-invasive urologic surgery with an initial focus on treating benign prostatic hyperplasia, or BPH. BPH is the most common prostate disease and impacts approximately 40 million men in the United States. Our proprietary AquaBeam Robotic System employs a single-use disposable handpiece to deliver our Aquablation therapy, which combines real-time, multidimensional imaging, personalized treatment planning, automated robotics and heat-free waterjet ablation for targeted and rapid removal of prostate tissue. We believe that Aquablation therapy represents a paradigm shift in the surgical treatment of BPH by addressing compromises associated with alternative surgical interventions to deliver effective, safe and durable outcomes that are independent of prostate size and shape or surgeon experience. We have developed a significant and growing body of clinical evidence, which includes nine clinical studies and over 100 peer-reviewed publications, supporting the benefits and clinical advantages of Aquablation therapy. As of June 30, 2021, we have an installed base of more than AquaBeam Robotic Systems, and Aquablation therapy has been utilized in the treatment of more than patients whose prostates have ranged in size from less than 30 ml to over 300 ml.

The main goal of BPH treatment is to alleviate the symptoms associated with the disease and improve the patient’s quality of life. While drug therapy is typically a first line treatment option, limited efficacy and negative side effects contribute to low compliance, high failure rates and drop outs. On the other hand, surgical intervention is proven to provide effective and durable symptom relief compared to drug therapy, but the use of surgery is significantly underpenetrated, largely due to the compromise patients must make between the incidence of irreversible side effects associated with alternative resective surgical interventions or the lower rates of efficacy and durability associated with non-resective surgical interventions. In addition, most alternative surgical interventions are limited by prostate size and shape, with no single procedure capable of effectively addressing the full range of prostate anatomies regardless of surgeon experience level.

We developed our proprietary AquaBeam Robotic System to address many of the shortcomings of alternative surgical interventions by delivering our Aquablation therapy, the first and only image-guided robotic therapy for the treatment of BPH. The AquaBeam Robotic System combines real-time image guidance, personalized treatment planning, automated robotic execution and heat-free waterjet ablation. We believe our Aquablation therapy addresses the compromise between safety and efficacy of alternative surgical interventions, providing the following unique combination of benefits:

•Significant and durable symptom relief. Aquablation therapy has demonstrated significant and long-lasting levels of symptom relief similar to those of alternative resective procedures.

•Favorable safety profile. Aquablation therapy has demonstrated low rates of irreversible complications, including urinary incontinence, erectile dysfunction and ejaculatory dysfunction, compared to published rates observed for other resective surgeries.

•Outcomes independent of prostate size and shape and surgeon experience. Aquablation therapy delivers outcomes that are effective, safe and durable across all prostate sizes and shapes. Compared to other resective procedures, we believe Aquablation therapy is relatively simple to learn, enabled by the intuitive interface of the CPU and automated robotic resection, and delivers outcomes that are independent of surgeon experience.

1

•Personalized treatment planning and improved decision-making. Aquablation therapy combines cystoscopic visualization, ultrasound imaging and advanced planning software to provide the surgeon with a multidimensional view of the treatment area and enable personalized treatment planning for the patient’s unique anatomy, improved decision-making and real-time monitoring during the procedure.

•Targeted and controlled resection with consistent resection times. Aquablation therapy utilizes automated robotic resection to remove prostate tissue using a precise, heat-free waterjet. These features enable targeted and controlled tissue removal with rapid resection times that are highly consistent across prostate sizes and shapes and surgeon experience.

In the United States, we currently sell our products to hospitals primarily through our direct sales organization. These hospitals in turn bill various third-party payors, such as commercial payors and government agencies, for treatment payment of each patient. Effective in 2021, all local Medicare Administrative Contractors, or MACs, which represent 100% of eligible Medicare patients, issued final positive local coverage determinations to provide Medicare beneficiaries with access to Aquablation therapy in all 50 states. Our strong body of clinical evidence and support from key societies, supplemented by the momentum from Medicare coverage, have led to favorable coverage decisions from several large commercial payors, including Anthem, BlueCross – Massachusetts, Emblem Health, Health Care Service Corp, and Humana. We plan to leverage these recent successes in our active discussions with commercial payors to establish additional positive national and regional coverage policies. Outside of the United States, we have ongoing efforts in key markets to expand established coverage and improve payment which we will believe will expand patient access to Aquablation therapy. We sell our products outside of the United States through both our direct sales organization and, in certain regions, our network of distribution partners.

We generated revenue of $7.7 million and a net loss of $53.0 million for the year ended December 31, 2020, compared to revenue of $6.2 million and a net loss of $$42.0 million for the year ended December 31, 2019. As of December 31, 2020, we had an accumulated deficit of $201.7 million.

Market Overview

BPH refers to the non-malignant enlargement of the prostate gland, a small gland in the male reproductive system, and in the United States is the number one reason men visit a urologist. BPH is estimated to occur in more than 50% of men in their 50s, growing to 70% of men in their 60s, and is the fourth most common diagnosed disease in men above 50 years old, ranking behind coronary artery disease, hypertension and type 2 diabetes. BPH often results in uncomfortable lower urinary tract symptoms, or LUTS, which can have a significant impact on quality of life. If left untreated, BPH may eventually lead to more serious complications.

In the United States, we estimate that approximately 40 million men are impacted by symptoms of BPH, with aging demographics expected to drive future growth. Over the next ten years, we expect that the number of men over 65 years old in the United States will double and include a corresponding increase in the number of men with enlarged prostates. Of these men, approximately 12 million are being managed by a physician for symptoms related to their disease. While drug therapy is typically a first line treatment option, limited efficacy and negative side effects contribute to low patient compliance, high failure rates and drop outs. On the other hand, surgical intervention is proven to provide effective and durable symptom relief compared to drug therapy, but the use of surgery is significantly underpenetrated largely due to the compromise patients must make between (1) the incidence of irreversible side effects associated with current resective surgical interventions, or (2) the lower rates of efficacy and durability associated with non-resective surgical interventions. Our total addressable patient population in the United States includes approximately 8.2 million patients, comprised of 6.7 million receiving drug therapy, 1.1 million who have tried but failed drug therapy and 400,000 undergoing surgical intervention each year. Based on the average selling price of our single-use handpiece, we estimate that our total addressable market opportunity is in excess of $20 billion in the United States. The global incidence of BPH among men over 50 years old is similar to that of the United States, representing a significant incremental market opportunity outside of the United States.

BPH Treatment Options and Their Limitations

The main goal of BPH treatment is to alleviate the symptoms associated with the disease and improve the patient’s quality of life. As such, a patient’s recommended course of treatment is largely based on the patient’s

2

degree of symptoms, typically measured using validated scoring systems such as International Prostate Symptom Score, or IPSS. Patients with mild symptoms who have not developed other complications of BPH may choose watchful waiting, meaning that before proceeding with active treatment, the physician and patient wait to see if symptoms get worse or if new symptoms develop. Patients who choose this approach are generally advised to implement lifestyle changes and return for yearly visits with their physician to determine if symptoms are changing. For most men, the prostate will continue to grow and symptoms will worsen. As symptoms become more bothersome, active treatment may be recommended. The two primary categories of active treatment for BPH are drug therapy and surgical intervention.

•Drug therapy. Drug therapy is often the first step in actively treating mild-to-moderate symptoms of BPH. While there is no pharmacological cure for BPH, drugs may be used to manage symptoms. Available drugs address symptoms by either shrinking (5-alpha reductase inhibitors) the prostate or relaxing (alpha blockers) muscles surrounding the prostate. In some instances, patients may be prescribed a combination of both medications. Most men with BPH who start drug therapy will need to continue it indefinitely in order to relieve symptoms, unless they choose to undergo surgical intervention. While drug therapy can provide relief for some men, two out of three patients are not satisfied with the effectiveness of their medication. In general, drug therapy provides IPSS reduction of approximately five points. Drug therapy is also often associated with negative side effects, including headaches, dizziness, nausea, erectile dysfunction, ejaculatory dysfunction, cardiac failure and dementia. These side effects often contribute to poor treatment compliance, with drug therapy failing in up to 30% of men. Furthermore, drug therapy may be costly, particularly in light of limited symptom relief. For example, a recent study has shown that payor costs for branded combination drug therapy over a two-year period was the least cost-effective of all treatment options included in the study, as drug therapy requires extended use and yields the least symptom relief.

•Surgical intervention. Surgical intervention is recommended for patients who have failed or are unwilling to consider drug therapy, or are suffering from complications due to their BPH. Although more invasive than drug therapy, surgical intervention generally provides more significant, longer-lasting symptom relief. There are two categories of surgical intervention, resective and non-resective. We estimate that approximately 400,000 BPH surgeries were performed in the United States in 2019, growing at a compounded annual growth rate, or CAGR, of 11% since 2016. We believe that growth in the use of surgical intervention over the past several years is due to the introduction of new technologies that better balance the compromise between efficacy and safety as well as growing awareness of surgical intervention an effective way to manage BPH symptoms compared to drug therapy.

Two factors that surgeons and patients commonly consider when evaluating surgical intervention are efficacy and safety. Efficacy is generally measured by symptom relief as well as durability of relief, and safety by the occurrence of irreversible complications such as urinary incontinence, erectile dysfunction and ejaculatory dysfunction. We believe that alternative surgical interventions for BPH require patients to compromise between efficacy and safety. Alternative interventions either provide significant symptom relief with a heightened risk of irreversible complications or a lower risk of complications with significantly less symptom relief. In addition, most alternative surgical interventions are limited by prostate size and shape, with no single procedure capable of effectively addressing the full range of prostate anatomies regardless of surgeon experience level. We believe that the compromise and limitations associated with alternative surgical interventions have contributed to the relatively low penetration rate of surgical intervention.

Our Solution

We have developed the AquaBeam Robotic System, an advanced, image-guided, surgical robotic system for use in minimally invasive urologic surgery. Our proprietary AquaBeam Robotic System delivers our Aquablation therapy, the first and only image-guided robotic therapy for the treatment of BPH. We market the AquaBeam Robotic System in the United States pursuant to FDA 510(k) clearance.

3

The AquaBeam Robotic System combines the following highly differentiated features that enable Aquablation therapy to deliver effective, safe and durable outcomes that are consistent across all prostate sizes and shapes and independent of surgeon experience:

•Real-time image guidance. Intraoperative ultrasound imaging combined with cystoscopic visualization provide a multidimensional view of the treatment area, enabling improved decision-making and real-time treatment monitoring.

•Personalized treatment planning. Using ultrasound imaging integrated with advanced planning software, the surgeon is able to map the treatment contour that precisely targets the resection area, personalizing the optimal tissue removal plan based on each patient’s unique anatomy.

•Automated robotic execution. Once the treatment plan is finalized, the robot automatically executes the plan, guiding the precisely calibrated waterjet with speed and accuracy while the surgeon monitors.

•Heat-free waterjet resection. Utilizing the unique power of a pulsating waterjet near the speed of sound, Aquablation therapy removes prostatic tissue with a heat-free waterjet, minimizing the risk of complications arising from prolonged thermal injury.

Our Success Factors

We believe the continued growth of our company will be driven by the following success factors:

•First and only image-guided, heat-free robotic therapy for BPH that addresses the compromise between safety and efficacy of alternative surgical interventions. We believe that alternative surgical interventions for BPH have a number of shortcomings which require patients to compromise between safety and efficacy, either providing significant symptom relief but with a heightened risk of irreversible complications or a lower risk of complications but with significantly less symptom relief. Aquablation therapy represents a paradigm shift in the surgical treatment of BPH by addressing this compromise and delivering effective, safe and durable outcomes that are consistent across all prostate sizes and shapes and independent of surgeon experience.

•Large, growing and underpenetrated market opportunity. Based on the average selling price of our single-use handpiece and the approximately 8.2 million BPH patients in the United States, we estimate that our total U.S. addressable market opportunity is in excess of $20 billion. The global incidence of BPH among men over 50 years old is similar to that of the United States, representing a significant incremental market opportunity outside of the United States.

•Significant and growing body of clinical evidence and strong support from key opinion leaders, or KOLs, resulting in the inclusion of Aquablation therapy into societal guidelines and rapid expansion of positive reimbursement coverage policies. Our robust clinical evidence includes nine clinical studies and more than 100 peer-reviewed publications, and demonstrates the efficacy, safety and durability of Aquablation therapy, consistent across all prostate sizes and shapes and independent of surgeon experience. Additionally, we have established strong relationships with KOLs within the urology community and collaborated with key urological societies in global markets. This support has been instrumental in facilitating broader acceptance and adoption of Aquablation therapy.

•Compelling value proposition and benefits to hospitals, surgeons and patients. We designed our AquaBeam Robotic System to enable consistent and reproducible BPH surgery outcomes that are independent of surgeon experience and require minimal training. Furthermore, the AquaBeam Robotic System is highly mobile and compact, requiring no retrofitting of the operating room, and we believe is competitively priced compared to other robotic systems and capital equipment devices. For patients, Aquablation therapy offers significant and durable symptom relief with an attractive safety profile.

•Recurring revenue model. We generate revenue primarily from hospitals making capital purchases of our AquaBeam Robotic System and purchasing our single-use handpieces for individual patient use. We also

4

generate revenue by providing post-warranty service for the AquaBeam Robotic System. We believe our business model of selling capital equipment that generates corresponding disposables utilization and post-warranty service contracts provides a path to predictable, recurring revenue.

•Broad research and development capabilities and a robust intellectual property portfolio. We have invested in establishing strong research and development capabilities for over a decade, including in surgical robotics and imaging-enabled surgery as well as integrating hardware and software to create an exceptional user and patient experience. We believe our focus on this experience will allow us to continue to bring new upgrades, capabilities and products to market, allowing us to innovate and maintain our competitive positioning, and that our intellectual property and know-how present a significant barrier to entry for our competitors.

•Proven leadership team and board members with deep industry experience. We are led by a highly experienced management team and board with a successful track record of building businesses by identifying and providing solutions for underserved markets in the medical device industry.

Our Growth Strategy

Our mission is to establish Aquablation therapy as the surgical standard of care for BPH. The key elements of our growth strategy are:

•Grow our installed base of AquaBeam Robotic Systems by driving adoption of Aquablation therapy among urologists. In the United States, we are initially focused on driving adoption of Aquablation therapy among urologists that perform hospital-based resective BPH surgery. We are initially targeting 860 high-volume hospitals that we estimate perform, on average, more than 200 resective procedures annually and account for approximately 70% of all hospital-based resective procedures. We also intend to increase awareness of Aquablation therapy by continuing to publish clinical data in various industry and scientific journals, present our clinical data at various industry conferences and sponsor peer-to-peer education programs and proctorships.

•Increase system utilization by establishing Aquablation therapy as the surgical treatment of choice for BPH. Once we place a system within a hospital, our objective is to establish Aquablation therapy as the surgical treatment of choice for BPH. Within each hospital, we are initially focused on targeting urologists who perform medium-to-high volumes of resective procedures and converting their resective cases to Aquablation therapy. Over time, we intend to leverage our relationships with urologists to drive utilization of Aquablation therapy beyond the current surgical market.

•Continue to broaden private payor coverage. We plan to leverage our recent successes, including the addition of Aquablation therapy to American Urological Association clinical guidelines in May 2019 and the final positive local coverage determinations by all local MACs to provide Medicare beneficiaries with access to Aquablation therapy in all 50 states, in our active discussions with private payors to establish additional positive national and regional coverage policies. We believe that additional private payor coverage will contribute to increasing utilization of our system over time. Outside of the United States, we have ongoing efforts in key markets to expand established coverage and further improve patient access to Aquablation therapy.

•Build upon our strong base of clinical evidence. We are committed to continuing to build upon our foundation of clinical evidence, which we believe will help drive increased awareness and adoption of our products. We also plan to further build our base of clinical evidence by supporting new clinical studies intended to support commercial, regulatory and reimbursement efforts.

•Invest in research and development to drive continuous improvements and innovation. We are currently developing additional and next generation technologies to support and improve Aquablation therapy to further satisfy the evolving needs of surgeons and their patients as well as to further enhance the usability and scalability of the AquaBeam Robotic System. We also plan to leverage our treatment data and software

5

development capabilities to integrate artificial intelligence and machine-learning to enable computer-assisted anatomy recognition and improved treatment planning and personalization.

•Drive increased awareness of Aquablation therapy beyond the urology community. As we expand our network of urologists and grow our installed base, we intend to increase awareness and brand recognition of Aquablation therapy beyond urologists, primarily among primary care physicians who manage BPH patients. To achieve this objective, we will invest in marketing initiatives direct at primary care physicians in order to optimize referral pathways and expand networks for BPH patients to visit a urologist.

•Further penetrate and expand into existing and new international markets. While the United States remains our primary focus in the near-term, we are growing our existing presence in the large European markets by continuing to promote the clinical benefits of Aquablation therapy, supporting investments in clinical studies to improve coverage and reimbursement and fostering relationships with KOLs. In addition, we intend to expand our reach to selected new markets in the Asia-Pacific region over time.

Summary Risk Factors

We are subject to a number of risks, including risks that may prevent us from achieving our business objectives or that may adversely affect our business, financial condition and results of operations. You should carefully consider the risks discussed in the section titled “Risk Factors,” including the following risks, before investing in our common stock:

•We are an early-stage company with a history of significant net losses, we expect to continue to incur operating losses for the foreseeable future and we may not be able to achieve or sustain profitability.

•Our revenue is primarily generated from sales of our AquaBeam Robotic System and the accompanying single-use disposable handpieces, and we are therefore highly dependent on the success of those products.

•Our quarterly and annual operating results may fluctuate significantly and may not fully reflect the underlying performance of our business. This makes our future operating results difficult to predict and could cause our operating results to fall below expectations or any guidance we may provide.

•Even if this offering is successful, we may need additional funding beyond the proceeds of this offering to finance our planned operations, and may not be able to raise capital when needed, which could force us to delay, reduce or eliminate one or more of our product development programs and future commercialization efforts.

•The commercial success of our AquaBeam Robotic System and Aquablation therapy will depend upon the degree of market acceptance of our products among hospitals, surgeons and patients.

•We have limited experience in training and marketing and selling our products and we may provide inadequate training, fail to increase our sales and marketing capabilities or fail to develop and maintain broad brand awareness in a cost-effective manner.

•We face competition from many sources, including larger companies, and we may be unable to compete successfully.

•We have limited experience manufacturing our products in large-scale commercial quantities and we face a number of manufacturing risks that may adversely affect our manufacturing abilities which could delay, prevent or impair our growth.

•We depend upon third-party suppliers, including contract manufacturers and single source suppliers, making us vulnerable to supply shortages and price fluctuations that could negatively affect our business, financial condition and results of operations.

6

•If we receive a significant number of warranty claims or our AquaBeam Robotic Systems require significant amounts of service after sale, our operating expenses may substantially increase and our business and financial results will be adversely affected.

•Our business, financial condition, results of operations and growth have been adversely impacted by the effects of the COVID-19 pandemic and may continue to be adversely impacted.

•We may encounter difficulties in managing our growth, which could disrupt our operations.

•Our internal computer systems, or those used by our contractors or consultants, may fail or suffer security breaches, and such failure could negatively affect our business, financial condition and results of operations.

•The sizes of the addressable markets for our AquaBeam Robotic System have not been established with precision and our potential market opportunity may be smaller than we estimate and may decline.

•Until we are able to achieve broader market acceptance of our AquaBeam Robotic System and Aquablation therapy, we may face risks associated with a more concentrated customer base.

•We are highly dependent on our senior management team and key personnel, and our business could be harmed if we are unable to attract and retain personnel necessary for our success.

•Our products and operations are subject to extensive government regulation and oversight both in the United States and abroad, and our failure to comply with applicable requirements could harm our business.

•If we are unable to adequately protect our intellectual property rights, or if we are accused of infringing on the intellectual property rights of others, our competitive position could be harmed or we could be required to incur significant expenses to enforce or defend our rights.

•We have identified a material weakness in our internal control over financial reporting and may identify additional material weaknesses in the future or otherwise fail to maintain effective internal control over financial reporting, which may result in material misstatements of our financial statements or cause us to fail to meet our periodic reporting obligations.

Our business also faces a number of other challenges and risks discussed throughout this prospectus. You should read the entire prospectus carefully, including the sections titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our consolidated financial statements and related notes included elsewhere in this prospectus, before deciding to invest in our common stock.

Our Corporate Information

We were incorporated in Delaware in April 2021 when our predecessor, PROCEPT BioRobotics Corporation, a California corporation, merged with and into us, and we continued as the surviving entity.

Our principal executive office is located at 900 Island Drive, Redwood City, CA, 94065 and our telephone number is (650) 232-7200. Our website address is www.procept-biorobotics.com. The information contained on, or that can be accessed through, our website is not incorporated by reference into, and is not a part of, this prospectus or the registration statement of which this prospectus forms a part. We have included our website in this prospectus solely as an inactive textual reference. Investors should not rely on any such information in deciding whether to purchase our common stock.

Implications of Being an Emerging Growth Company and a Smaller Reporting Company

We qualify as an “emerging growth company” as defined in Section 2(a) of the Securities Act of 1933, as amended, or the Securities Act, as modified by the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. As an emerging growth company, we may take advantage of specified reduced disclosure and other requirements

7

that are otherwise applicable, in general, to public companies that are not emerging growth companies. These provisions include:

•the option to present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations in this prospectus;

•not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002;

•reduced disclosure obligations regarding executive compensation in our periodic reports, proxy statements and registration statements; and

•exemptions from the requirements of holding nonbinding, advisory stockholder votes on executive compensation or on any golden parachute payments not previously approved.

We will remain an emerging growth company until the earliest to occur of: (i) the last day of the first fiscal year in which our annual gross revenue exceeds $1.07 billion; (ii) the date that we become a “large accelerated filer,” with at least $700 million of equity securities held by non-affiliates as of the end of the second quarter of that fiscal year; (iii) the date on which we have issued, in any three-year period, more than $1.0 billion in non-convertible debt securities; and (iv) the last day of the fiscal year ending after the fifth anniversary of the completion of this offering.

We have elected to take advantage of certain of the reduced disclosure obligations in the registration statement of which this prospectus is a part and may elect to take advantage of other reduced reporting requirements in future filings with the U.S. Securities and Exchange Commission, or the SEC. As a result, the information that we provide may be different than the information you receive from other public companies in which you hold stock.

Emerging growth companies can also take advantage of the extended transition period provided in Section 13(a) of the Securities Exchange Act of 1934, as amended, or the Exchange Act, for complying with new or revised accounting standards. In other words, an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. As a result of these elections, some investors may find our common stock less attractive than they would have otherwise. The result may be a less active trading market for our common stock, and the price of our common stock may become more volatile.

We have elected to avail ourselves of this exemption and, therefore, for new or revised accounting standards applicable to public companies, we will be subject to an extended transition period until those standards would otherwise apply to private companies. As a result, our consolidated financial statements may not be comparable to companies that comply with new or revised accounting pronouncements as of public company effective dates.

We are also a “smaller reporting company” as defined in the Exchange Act. We may continue to be a smaller reporting company even after we are no longer an emerging growth company. We may take advantage of certain of the scaled disclosures available to smaller reporting companies and will be able to take advantage of these scaled disclosures for so long as our voting and non-voting common stock held by non-affiliates is less than $250.0 million measured on the last business day of our second fiscal quarter, or our annual revenue is less than $100.0 million during the most recently completed fiscal year and our voting and non-voting common stock held by non-affiliates is less than $700.0 million measured on the last business day of our second fiscal quarter.

8

The Offering

| Common stock offered by us | shares. | ||||

Option to purchase additional shares | We have granted the underwriters an option exercisable for a period of 30 days to purchase up to additional shares of our common stock at the public offering price, less the underwriting discounts and commissions. | ||||

| Common stock to be outstanding immediately after this offering | shares (or shares if the underwriters exercise their option to purchase additional shares of common stock in full). | ||||

| Use of proceeds | We estimate that the net proceeds to us from this offering will be approximately $ million, or approximately $ million if the underwriters exercise their option to purchase additional shares in full, based upon an assumed initial public offering price of $ per share, which is the midpoint of the estimated price range set forth on the cover page of this prospectus, and after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. | ||||

| We currently intend to use the net proceeds from this offering, together with our existing cash and cash equivalents, to hire additional sales and marketing personnel and expand marketing programs both in the United States and in Europe, to fund product development and research and development activities and the remainder for working capital and other general corporate purposes. See the section titled “Use of Proceeds.” | |||||

| Risk factors | Investing in our common stock involves a high degree of risk. See the section titled “Risk Factors” for a discussion of factors you should carefully consider before investing in our common stock. | ||||

| Proposed Nasdaq Global Market symbol | “PRCT” | ||||

The number of shares of common stock to be outstanding after this offering is based on shares of common stock outstanding as of June 30, 2021 (including the conversion of all outstanding shares of our redeemable convertible preferred stock into shares of our common stock immediately prior to the completion of this offering), and excludes the following:

• shares of our common stock issuable upon the exercise of options outstanding as of June 30, 2021, with a weighted-average exercise price of $ per share;

• shares of our common stock issuable upon the exercise of options granted after June 30, 2021, with a weighted-average exercise price of $ per share;

• shares of our common stock that remain available for issuance under our Amended and Restated 2008 Stock Plan, or 2008 Plan, as of June 30, 2021;

• shares of our common stock reserved for future issuance under our Plan, or 2021 Plan, which will become effective in connection with this offering (and which excludes any potential annual evergreen increases pursuant to the terms of the 2021 Plan); and

• shares of our common stock reserved for future issuance under our 2021 Employee Stock Purchase Plan, or ESPP, which will become effective in connection with this offering (and which excludes any potential annual evergreen increases pursuant to the terms of the ESPP).

Unless otherwise indicated, this prospectus reflects and assumes the following:

•a -for- reverse stock split of our common stock, which was effected on , 2021;

9

•the issuance of shares of Series E redeemable convertible preferred stock upon the exercise for cash, at an exercise price of $2.89 per share, of warrants to purchase our redeemable convertible preferred stock outstanding as of June 30, 2021, prior to the warrants expiration upon the completion of this offering;

•the conversion of all outstanding shares of our redeemable convertible preferred stock into shares of our common stock immediately prior to the completion of this offering;

•the adoption, filing and effectiveness of our amended and restated certificate of incorporation and the adoption and effectiveness of our amended and restated bylaws immediately after the completion of this offering;

•no exercise of the outstanding options referred to above; and

•no exercise by the underwriters of their option to purchase additional shares of our common stock.

10

Summary Consolidated Financial Data

The following tables summarize our historical consolidated financial data for the periods and as of the dates indicated. We derived our summary consolidated statements of operations data for the years ended December 31, 2019 and 2020 and our summary consolidated balance sheet data as of December 31, 2020 from our audited consolidated financial statements included elsewhere in this prospectus. Our historical results are not necessarily indicative of the results to be expected in the future. You should read the following information in conjunction with the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes included elsewhere in this prospectus. Our historical results are not necessarily indicative of our future results.

Year Ended December 31, | |||||||||||

2019 | 2020 | ||||||||||

(in thousands, except share and per share data) | |||||||||||

Consolidated Statements of Operations Data: | |||||||||||

Revenue | $ | 6,169 | $ | 7,717 | |||||||

Cost of sales | 8,054 | 8,972 | |||||||||

Gross profit | (1,885) | (1,255) | |||||||||

| Gross margin | -31 | % | -16 | % | |||||||

Operating expenses: | |||||||||||

Research and development | 13,147 | 16,275 | |||||||||

Selling, general and administrative | 28,518 | 30,272 | |||||||||

Total operating expenses | 41,665 | 46,547 | |||||||||

Loss from operations | (43,550) | (47,802) | |||||||||

Interest expense | (724) | (5,261) | |||||||||

Interest and other income, net | 2,299 | 44 | |||||||||

Net loss | $ | (41,975) | $ | (53,019) | |||||||

Net loss per share, basic and diluted(1) | $ | (4.00) | $ | (3.05) | |||||||

Weighted-average common shares used to compute net loss per share attributable to common shareholders, basic and diluted(1) | 10,486 | 17,398 | |||||||||

| Pro forma (unaudited): | |||||||||||

Net loss per share, basic and diluted | $ | ||||||||||

Weighted-average common shares used to compute pro forma net loss per share attributable to common shareholders, basic and diluted | |||||||||||

__________________

(1)See Note 2 to our consolidated financial statements included elsewhere in this prospectus for an explanation of the method used to calculate our historical basic and diluted net loss per share.

As of December 31, 2020 | |||||||||||||||||

Actual | Pro Forma(1) | Pro Forma As Adjusted(2)(3) | |||||||||||||||

| (unaudited) | |||||||||||||||||

(in thousands) | |||||||||||||||||

Consolidated Balance Sheet Data: | |||||||||||||||||

Cash and cash equivalents | $ | 100,130 | $ | $ | |||||||||||||

Working capital(4) | 95,614 | ||||||||||||||||

Total assets | 126,087 | ||||||||||||||||

Total liabilities | 65,127 | ||||||||||||||||

Redeemable convertible preferred stock | 243,854 | ||||||||||||||||

Total stockholders’ (deficit) equity | (182,894) | ||||||||||||||||

11

_________________

(1)The pro forma column in the consolidated balance sheet data table above gives effect to the conversion of outstanding shares of our redeemable convertible preferred stock as of December 31, 2020 into an aggregate of shares of common stock immediately prior to the completion of this offering.

(2)The pro forma as adjusted column in the consolidated balance sheet data table above gives effect to (i) the pro forma adjustments described in footnote (1) above and (ii) the sale and issuance by us of shares of common stock in this offering at the assumed initial public offering price of $ per share, which is the midpoint of the price range set forth on the cover page of this prospectus, after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us.

(3)Each $1.00 increase or decrease in the assumed initial public offering price of $ per share, which is the midpoint of the price range set forth on the cover page of this prospectus, would increase or decrease, as applicable, the pro forma as adjusted amount of each of our cash and cash equivalents, working capital, total assets and total stockholders’ equity by approximately $ , assuming that the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. Similarly, each increase or decrease of 1.0 million shares in the number of shares offered by us at the assumed initial public offering price would increase or decrease, as applicable, each of our cash and cash equivalents, working capital, total assets and total stockholders' equity by approximately $ , assuming the shares of our common stock offered by this prospectus are sold at the assumed initial public offering price of $ per share and after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. The pro forma as adjusted information discussed above is illustrative only and will be adjusted based on the actual initial public offering price, the number of shares we sell and other terms of this offering that will be determined at pricing.

(4)We define working capital as current assets less current liabilities. See our consolidated financial statements and related notes included elsewhere in this prospectus for further detail regarding our current assets and current liabilities.

12

RISK FACTORS

Investing in our common stock involves a high degree of risk. You should consider and read carefully all of the risks and uncertainties described below, as well as other information included in this prospectus and the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our consolidated financial statements and related notes included elsewhere in this prospectus, before making an investment decision. The risks described below are not the only ones facing us. The occurrence of any of the following risks or additional risks and uncertainties not presently known to us or that we currently believe to be immaterial could materially and adversely affect our business, financial condition or results of operations. In such case, the trading price of our common stock could decline, and you may lose all or part of your investment. This prospectus also contains forward-looking statements and estimates that involve risks and uncertainties. Our actual results could differ materially from those anticipated in the forward-looking statements as a result of specific factors, including the risks and uncertainties described below.

Risks Related to Our Limited Operating History, Financial Condition and Capital Requirements

We are an early-stage company with a history of significant net losses, we expect to continue to incur operating losses for the foreseeable future and we may not be able to achieve or sustain profitability.

We have incurred significant net losses in each reporting period since our inception. For the years ended December 31, 2019 and 2020, we had a net loss of $42.0 million and $53.0 million, respectively. For the six months ended June 30, 2020 and 2021, we had a net loss of $37.9 million and $ million, respectively. We expect to continue to incur additional losses in the future. As of June 30, 2021, we had an accumulated deficit of $ million. To date, we have financed our operations primarily through net proceeds from the sale of our redeemable convertible preferred stock in private placements, indebtedness, including our loan and security agreement, and, to a lesser extent, product revenue from sales of our AquaBeam Robotic System and single-use disposable handpieces. The losses and accumulated deficit have primarily been due to the substantial investments we have made to develop our products, costs related to our sales and marketing efforts, including costs related to clinical and regulatory initiatives to obtain marketing approval, and infrastructure improvements.

We may also encounter unforeseen expenses, difficulties, complications, delays and other known and unknown factors and risks frequently experienced by early-stage medical technology companies in rapidly evolving fields. In addition, as a public company, we will incur significant legal, accounting and other expenses that we did not incur as a private company. Accordingly, we expect to continue to incur significant operating losses for the foreseeable future and we cannot assure you that we will achieve profitability in the future or that, if we do become profitable, we will sustain profitability. Our failure to achieve and sustain profitability in the future will make it more difficult to finance our capital requirements needed to operate our business and accomplish our strategic objectives, which would have a material adverse effect on our business, financial condition and results of operations and cause the market price of our common stock to decline.

Our revenue is primarily generated from sales of our AquaBeam Robotic System and the accompanying single-use disposable handpieces, and we are therefore highly dependent on the success of those products.

To date, substantially all of our revenue has been derived, and we expect it to continue to be substantially derived, from sales of our AquaBeam Robotic System and its accompanying single-use disposable handpieces. Our products deliver our Aquablation therapy, the first and only image-guided, heat-free robotic therapy for BPH. We began commercializing our products in the United States in 2017 and physician awareness of, and experience with, our products has been and is currently limited. As a result, our products have limited product and brand recognition within the medical industry for the treatment of BPH. We do not have a long history operating as a commercial company, and the novelty of our products, together with our limited commercialization experience, makes it difficult to evaluate our current business and predict our future prospects with precision. These factors also make it difficult for us to forecast our financial performance and future growth, and such forecasts are subject to a number of uncertainties, including those outside of our control.

13

Our quarterly and annual operating results may fluctuate significantly and may not fully reflect the underlying performance of our business. This makes our future operating results difficult to predict and could cause our operating results to fall below expectations or any guidance we may provide.

Our quarterly and annual results of operations, including our revenue, profitability and cash flow, may vary significantly in the future, and period-to-period comparisons of our operating results may not be meaningful. Accordingly, the results of any one quarter or period should not be relied upon as an indication of future performance. Our quarterly and annual operating results may fluctuate significantly as a result of a variety of factors, many of which are outside our control and, as a result, may not fully reflect the underlying performance of our business. Such fluctuations in quarterly and annual operating results may decrease the value of our common stock. Because our quarterly operating results may fluctuate, period-to-period comparisons may not be the best indication of the underlying results of our business and should only be relied upon as one factor in determining how our business is performing. These fluctuations may occur due to a variety of factors, many of which are outside of our control, including, but not limited to:

•the level of surgeon and hospital adoption and demand for our products and Aquablation therapy;

•changes in reimbursement rates by government or commercial payors;

•positive or negative coverage in the media or clinical publications, or changes in public, patient and/or physician perception, of our products or competing products and treatments, including our brand reputation;

•the degree of competition in our industry and any change in the competitive landscape, including consolidation among competitors or future partners;

•any safety, reliability or effectiveness concerns that arise regarding our products or other procedures to treat BPH;

•unanticipated pricing pressures in connection with the sale of our products and downward pressure on healthcare costs in general;

•the effectiveness of our sales and marketing efforts, including our ability to deploy a sufficient number of qualified sales representatives to sell and market our products;

•the timing of customer orders or medical procedures using our products and the number of available selling days in any quarterly period, which can be impacted by holidays, the mix of products sold and the geographic mix of where products are sold;

•unanticipated delays in product development or product launches;

•the cost of manufacturing our products, which may vary depending on the quantity of production and the terms of our agreements with third-party suppliers;

•our ability to raise additional capital on acceptable terms, or at all, if needed to support the commercialization of our products;

•our ability to achieve and maintain compliance with all regulatory requirements applicable to our products and services;

•our ability to obtain, maintain and enforce our intellectual property rights;

•our ability and our third-party suppliers’ ability to supply the components of our products in a timely manner, in accordance with our specifications, and in compliance with applicable regulatory requirements; and

•introduction of new products, technologies or alternative treatments for BPH that compete with our products.

14

The cumulative effects of these factors could result in large fluctuations and unpredictability in our quarterly and annual operating results. If our assumptions regarding the risks and uncertainties we face, which we use to plan our business, are incorrect or change due to circumstances in our business or our markets, or if we do not address these risks successfully, our operating and financial results could deviate materially from our expectations and our business could suffer.

This variability and unpredictability could also result in our failure to meet the expectations of industry or financial analysts or investors for any period. If our revenue or operating results fall below the expectations of analysts or investors or below any forecasts we may provide to the market, it will negatively affect our business, financial condition and results of operations.

The terms of our loan and security agreement require us to meet certain operating and financial covenants and place restrictions on our operating and financial flexibility. If we raise additional capital through debt financing, the terms of any new debt could further restrict our ability to operate our business.

As of June 30, 2021, we had outstanding in the form of a term loan under our loan and security agreement with Oxford Finance LLC, which was entered into in September 2019. The loan is secured by substantially all of our assets, including all of the capital stock held by us, if any. The loan and security agreement contains a number of restrictive covenants, and the terms may restrict our current and future operations, particularly our ability to respond to certain changes in our business or industry, or take future actions. See the section of this prospectus titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Indebtedness.”

The loan and security agreement contains customary representations and warranties and affirmative covenants and also contains certain restrictive covenants, including, among others, limitations on: the incurrence of additional debt, liens or other encumbrances on property, acquisitions and investments, loans and guarantees, mergers, consolidations, liquidations and dissolutions, asset sales, dividends and other payments in respect of our capital stock, prepayments of certain debt, transactions with affiliates and changes to our type of business, management of the business, control of the business or business locations. The loan and security agreement also includes financial covenants that require us to, among other things, meet certain revenue targets detailed in an approved forecast. The loan and security agreement also contains customary events of default. If we fail to comply with such covenants, payments or other terms of the agreement, our lender could declare an event of default, which would give it the right to declare all borrowings outstanding, together with accrued and unpaid interest and fees, to be immediately due and payable. In addition, our lender would have the right to proceed against the assets we provided as collateral pursuant to the loan and security agreement. If the debt under the loan and security agreement were accelerated, we may not have sufficient cash or be able to sell sufficient assets to repay this debt, which would harm our business and financial condition.

Even if this offering is successful, we may need additional funding beyond the proceeds of this offering to finance our planned operations, and may not be able to raise capital when needed, which could force us to delay, reduce or eliminate one or more of our product development programs and future commercialization efforts.

Since our inception, we have incurred significant net losses and expect to continue to incur net losses for the foreseeable future. Since our inception, our operations have been financed primarily by net proceeds from the sale of our redeemable convertible preferred stock in private placements, indebtedness and, to a lesser extent, product revenue from sales of our AquaBeam Robotic System and single-use disposable handpieces. As of June 30, 2021, we had $ million in cash and cash equivalents, and an accumulated deficit of $ million. Based on our current operating plan, we currently believe that our cash and cash equivalents, anticipated revenue and available debt financing arrangements, together with the net proceeds from this offering, will be sufficient to meet our capital requirements and fund our operations through at least the next 12 months from the date of this prospectus. However, we have based these estimates on assumptions that may prove to be wrong, and we could utilize our available capital resources sooner than we currently expect. Changing circumstances could result in lower revenues or cause us to consume capital significantly faster than we currently anticipate, and we may need to raise capital sooner or in greater amounts than currently expected because of circumstances beyond our control.

15

Even after the consummation of this offering, we may require additional capital in the future as we expect to continue to invest in clinical trials and registries that are designed to provide clinical evidence of the safety and efficacy of our products, expanding our sales and marketing organization, and research and development of product improvements and future products. Moreover, we expect to incur additional expenses associated with operating as a public company, including legal, accounting, insurance, exchange listing and SEC compliance, investor relations and other expenses. To the extent additional capital is necessary, there are no assurances that we will be able to raise additional capital on favorable terms or at all, and therefore we may not be able to execute our business plan. Our future funding requirements will depend on many factors, including:

•the degree and rate of market acceptance of our current and future products and Aquablation therapy;

•the scope and timing of investment in our sales force and expansion of our commercial organization;

•the impact on our business from the ongoing and global COVID-19 pandemic and the end of the COVID-19 pandemic, or any other pandemic, epidemic or outbreak of an infectious disease;

•the scope, rate of progress and cost of our current or future clinical trials and registries;

•the cost of our research and development activities;

•the cost and timing of additional regulatory clearances or approvals;

•the costs associated with any product recall that may occur;

•the costs associated with the manufacturing of our products at increased production levels;

•the costs of attaining, defending and enforcing our intellectual property rights;

•whether we acquire third-party companies, products or technologies;

•the terms and timing of any other collaborative, licensing and other arrangements that we may establish;

•the emergence of competing technologies or other adverse market developments; and

•the rate at which we expand internationally.

We may seek to raise additional capital through equity offerings or debt financings and such additional financing may not be available to us on acceptable terms, or at all. In addition, any additional equity or debt financing that we raise may contain terms that are not favorable to us or our stockholders. For example, if we raise funds by issuing equity or equity-linked securities, the issuance of such securities could result in dilution to our stockholders. Any equity securities issued may also provide for rights, preferences or privileges senior to those of holders of our common stock. In addition, the issuance of additional equity securities by us, or the possibility of such issuance, may cause the market price of our common stock to decline, and the price per share at which we sell additional shares of our common stock, or securities convertible into or exercisable or exchangeable for shares of our common stock, in future transactions may be higher or lower than the price per share paid by investors in this offering.

In addition, the terms of debt securities issued or borrowings could impose significant restrictions on our operations including restrictive covenants, such as limitations on our ability to incur additional debt or issue additional equity, limitations on our ability to pay dividends, limitations on our ability to acquire or license intellectual property rights, and other operating restrictions that could adversely affect our ability to conduct our business. For example, our current loan and security agreement prohibits us from incurring additional indebtedness without the prior written consent of our lender. In the event that we enter into collaborations or licensing arrangements to raise capital, we may be required to accept unfavorable terms, such as relinquishment or licensing of certain technologies or products that we otherwise would seek to develop or commercialize ourselves, or reserve for future potential arrangements when we might otherwise be able to achieve more favorable terms. In addition, we

16

may be forced to work with a partner on one or more of our products or market development programs, which could lower the economic value of those programs to us.

If we are unable to obtain adequate financing on terms satisfactory to us when we require it, we may be required to terminate or delay the development of one or more of our products, delay clinical trials necessary to market our products, or delay establishment of sales and marketing capabilities or other activities necessary to commercialize our products. If this were to occur, our ability to grow and support our business and to respond to market challenges could be significantly limited, which could have a material adverse effect on our business, financial condition and results of operations.

Risks Related to Our Business and Industry

The commercial success of our AquaBeam Robotic System and Aquablation therapy will depend upon the degree of market acceptance of our products among hospitals, surgeons and patients.

Our success will depend, in large part, on the acceptance of our AquaBeam Robotic System as safe, effective, reliable and durable and, with respect to hospitals, healthcare providers and patients, as cost-effective. We believe Aquablation therapy represents a new approach for treating BPH, employing a computer-assisted patient-specific visualization system, a heat-free waterjet and automated robotic system to target and remove prostate tissue. We believe that market acceptance will be driven primarily by surgeons and hospitals, and if they do not adopt the concept of computer-assisted robotics-enabled technology and perceive such technology as having significant advantages over other surgical alternatives, patients will be less likely to accept or be offered Aquablation therapy and we will fail to meet our business objectives. Surgeons’ and hospitals’ perceptions of such technology having significant advantages are likely to be based on a determination that, among other factors, our products are safe, cost-effective and represent acceptable methods of treatment. Even if we can prove the effectiveness of Aquablation therapy through clinical trials, there may not be broad adoption and use of our products and surgeons may elect not to use our products for any number of other reasons, including:

•lack of experience with our products and concerns that we are relatively new to market;

•perceived liability risk generally associated with the use of new products and treatment options;

•lack or perceived lack of sufficient clinical evidence, including long-term data, supporting clinical benefits or the cost-effectiveness of our products over existing treatment alternatives;

•the failure of key opinion leaders to provide recommendations regarding our products, or to assure surgeons, patients and healthcare payors of the benefits of our products as an attractive alternative to other treatment options;

•perception that our products are unproven;

•long-standing relationships with companies and distributors that sell other products or treatment options for BPH;

•concerns over the capital investment required to purchase our AquaBeam Robotic System and perform Aquablation therapy procedures;

•lack of availability of adequate third-party payor coverage or reimbursement;

•pricing pressure, including from Group Purchasing Organizations, or GPOs, and Integrated Delivery Networks, or IDNs, seeking to obtain discounts on our AquaBeam Robotic System based on the collective buying power of the GPO and IDN members;

•competitive response and negative selling efforts from providers of alternative treatments;

•limitations or warnings contained in the labeling cleared or approved by the FDA or other authorities.

17

Even if our AquaBeam Robotic System achieves widespread market acceptance, it may not maintain such level of market acceptance over the long term if competing products or technologies, which are more cost-effective or received more favorably, are introduced. In addition, our limited commercialization experience makes it difficult to evaluate our current business and predict our future prospects. We cannot predict how quickly, if at all, hospitals, surgeons and patients will accept our AquaBeam Robotic System or, if accepted, how frequently it will be used. Failure to achieve or maintain market acceptance and/or market share could materially and adversely affect our ability to generate revenue and would have a material adverse effect on our business, financial condition and results of operations.

We have limited experience in training and marketing and selling our products and we may provide inadequate training, fail to increase our sales and marketing capabilities or fail to develop and maintain broad brand awareness in a cost-effective manner.

We have limited experience marketing and selling our products. We currently rely on our direct sales force and distributors to sell our products in targeted geographic regions and territories, and any failure to maintain and grow our direct sales force and distributor relationships could harm our business. The members of our direct sales force are adequately trained and possess technical expertise, which we believe is critical in driving the awareness and adoption of our products. The members of our U.S. sales force are at-will employees. The loss of these personnel to competitors, or otherwise, could materially harm our business. If we are unable to retain our direct sales force personnel or replace them with individuals of comparable expertise and qualifications, or if we are unable to successfully instill such expertise in replacement personnel, our product sales, revenues and results of operations could be materially harmed.