Digital Asset Exchanges and the digital asset industry as a whole. In particular, in the two weeks that followed the February 7, 2014 halt of Bitcoin withdrawals from Mt. Gox, the value of one Bitcoin fell on other exchanges from around $795 on February 6, 2014 to $578 on February 20, 2014. Additionally, in January 2015, Bitstamp announced that approximately 19,000 Bitcoin had been stolen from its operational or “hot” wallets. Further, in August 2016, it was reported that almost 120,000 Bitcoins worth around $78 million were stolen from Bitfinex, a large Digital Asset Exchange. The value of Bitcoin and other digital assets immediately decreased over 10% following reports of the theft at Bitfinex and the Shares suffered a corresponding decrease in value. In July 2017, the Financial Crimes Enforcement Network (“FinCEN”) assessed a $110 million fine against

BTC-E,

a now defunct Digital Asset Exchange, for facilitating crimes such as drug sales and ransomware attacks. In addition, in December 2017, Yapian, the operator of Seoul-based cryptocurrency exchange Youbit, suspended digital asset trading and filed for bankruptcy following a hack that resulted in a loss of 17% of Yapian’s assets. Following the hack, Youbit users were allowed to withdraw approximately 75% of the digital assets in their exchange accounts, with any potential further distributions to be made following Yapian’s pending bankruptcy proceedings. In addition, in January 2018, the Japanese digital asset exchange, Coincheck, was hacked, resulting in losses of approximately $535 million, and in February 2018, the Italian Digital Asset Exchange, Bitgrail, was hacked, resulting in approximately $170 million in losses. Most recently in May 2019, one of the world’s largest Digital Asset Exchanges, Binance, was hacked, resulting in losses of approximately $40 million.

Negative perception, a lack of stability in the Digital Asset Markets and the closure or temporary shutdown of Digital Asset Exchanges due to fraud, failure or security breaches may reduce confidence in the Bitcoin Network and result in greater volatility in the prices of Bitcoin. Furthermore, the closure or temporary shutdown of a Digital Asset Exchange used in calculating the Index Price may result in a loss of confidence in the Trust’s ability to determine its Digital Asset Holdings on a daily basis. These potential consequences of such a Digital Asset Exchange’s failure could adversely affect the value of the Shares.

The Index has a limited history and a failure of the Index Price could adversely affect the value of the Shares.

The Index has a limited history and the Index Price is a composite reference rate calculated using volume-weighted trading price data from various Digital Asset Exchanges chosen by the Index Provider. The Digital Asset Exchanges chosen by the Index Provider have also changed over time. For example, effective January 19, 2020, the Index Provider removed Bittrex and added LMAX Digital as part of its scheduled quarterly review. On April 6, 2020, the Index Provider removed itBit and did not add any constituents as part of its scheduled quarterly review. The Index Provider may remove or add Digital Asset Exchanges to the Index in the future at its discretion. For more information on the inclusion criteria for Digital Asset Exchanges in the Index, see “Item 1. Business—Overview of the Bitcoin Industry and Market— Bitcoin Value—The Index and the Index Price.”

Although the Index is designed to accurately capture the market price of Bitcoin, third parties may be able to purchase and sell Bitcoin on public or private markets not included among the constituent Digital Asset Exchanges of the Index, and such transactions may take place at prices materially higher or lower than the Index Price. Moreover, there may be variances in the prices of Bitcoin on the various Digital Asset Exchanges, including as a result of differences in fee structures or administrative procedures on different Digital Asset Exchanges. For example, based on data provided by the Index Provider, on any given day during the year ended December 31, 2021, the maximum differential between the 4:00 p.m., New York time spot price of any single Digital Asset Exchange included in the Index and the Index Price was 0.64% (8.50% based on Old Index Price) and the average of the maximum differentials of the 4:00 p.m., New York time, spot price of each Digital Asset Exchange included in the Index and the Index Price was 0.32% (8.47% based on Old Index Price). During this same period, the average differential between the 4:00 p.m., New York time, spot prices of all the Digital Asset Exchanges included in the Index and the Index Price was 0.0003% (0.24% based on Old Index Price). During this same period, the average differential between the 4:00 p.m., New York time spot prices of all the Digital Asset Exchanges included in the Index and the Index Price was 0.0003%. All Digital Asset Exchanges that were included in the Index throughout the period were considered in this analysis. To the extent such prices differ materially from the Index Price, investors may lose confidence in the Shares’ ability to track the market price of Bitcoins, which could adversely affect the value of the Shares.

The Index Price used to calculate the value of the Trust’s Bitcoin may be volatile, and purchasing activity in the Digital Asset Markets associated with Basket creations may affect the Index Price and Share trading prices, adversely affecting the value of the Shares.

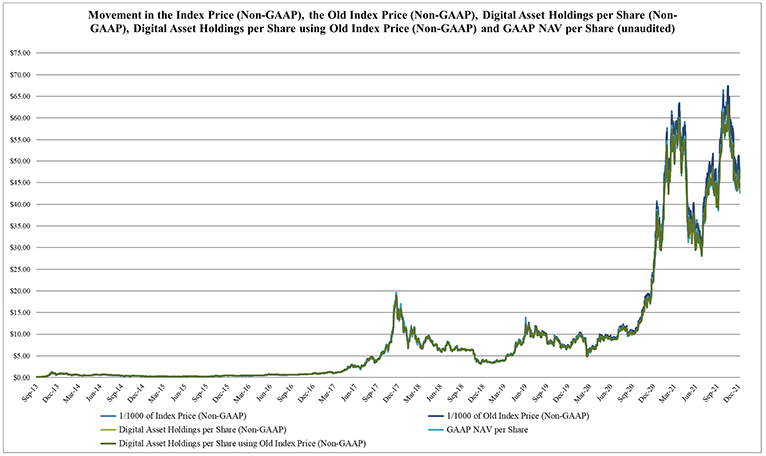

The price of Bitcoin on public Digital Asset Exchanges has a very limited history, and during this history, Bitcoin prices on the Digital Asset Markets more generally, and on Digital Asset Exchanges individually, have been volatile and subject to influence by many factors, including operational interruptions. While the Index is designed to limit exposure to the interruption of individual Digital Asset Exchanges, the Index Price, and the price of Bitcoin generally, remains subject to volatility experienced by Digital Asset Exchanges, and such volatility could adversely affect the value of the Shares. For example, since the beginning of the Trust’s operations, the Index Price ranged from $117.03 to $67,352.59 ($117.03 to $67,397.98 based on Old Index Price), with the straight average being $9,535.36 ($9,508.58 based on Old Index Price) through December 31, 2021. In addition, in the twelve months from January 1, 2021 to December 31, 2021, the Index Price ranged from $29,311.80 to $67,352.59 ($29,235.54 to $67,397.98 based on Old Index Price). The Sponsor has not observed a material difference between the Index Price and average prices from the constituent Digital Asset Exchanges individually or as a group. The price of Bitcoin more generally has experienced volatility similar to the Index Price during these periods. For additional information on movement of the Index Price and the price of Bitcoin, see “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Historical Digital Asset Holdings and Bitcoin Prices.”

Furthermore, because the number of Digital Asset Exchanges is limited, the Index will necessarily be composed of a limited number of Digital Asset Exchanges. If a Digital Asset Exchange were subjected to regulatory, volatility or other pricing issues, the Index Provider would have limited ability to remove such Digital Asset Exchange from the Index, which could skew the price of Bitcoin as represented by the Index. Trading on a limited number of Digital Asset Exchanges may result in less favorable prices and decreased liquidity of Bitcoin and, therefore, could have an adverse effect on the value of the Shares.