UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

For the fiscal year ended December 31 , 2021

or

For the transition period from _____ to _____

Commission file number 001-36353

(Exact name of registrant as specified in its charter)

| N/A | ||||||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

+353 1 7094000

(Address, including zip code, and telephone number, including

area code, of registrant’s principal executive offices)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | ☒ | No | ☐ | ||||||||||||||

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 of Section 15(d) of the Act. | Yes | ☐ | ☒ | ||||||||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | ☒ | No | ☐ | ||||||||||||||

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). | ☒ | No | ☐ | ||||||||||||||

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer", "accelerated filer", "smaller reporting company", and "emerging growth company" in Rule 12b-2 of the Exchange Act. | |||||||||||||||||

| ☒ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | |||||||||||||||||||||||||||

| Emerging growth company | ||||||||||||||||||||||||||||||||

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | ☐ | |||||||||||||||||||||||||||||||

| Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its audit report. | |||||||||||||||||

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). | Yes | ☐ | No | ||||||||||||||

The aggregate market value of the voting stock held by non-affiliates of the registrant, based upon the closing sale price of our ordinary shares on July 3, 2021 as reported on the New York Stock Exchange, was $6,266,348,414 . Ordinary shares held by each director or executive officer have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of February 25, 2022, the registrant had 133,784,716 outstanding ordinary shares.

PERRIGO COMPANY PLC

FORM 10-K

YEAR ENDED DECEMBER 31, 2021

TABLE OF CONTENTS

| Page No. | ||||||||

| Part I. | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Additional Item. | ||||||||

| Part II. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| Item 9C. | ||||||||

| Part III. | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| Part IV. | ||||||||

| Item 15. | ||||||||

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements in this report are “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and are subject to the safe harbor created thereby. These statements relate to future events or our future financial performance and involve known and unknown risks, uncertainties and other factors that may cause our, or our industry’s actual results, levels of activity, performance or achievements to be materially different from those expressed or implied by any forward-looking statements. In particular, statements about our expectations, beliefs, plans, objectives, assumptions, future events or future performance contained in this report, including certain statements contained in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” are forward-looking statements. In some cases, forward-looking statements can be identified by terminology such as “may,” “will,” “could,” “would,” “should,” “expect,” “plan,” “anticipate,” “intend,” “believe,” “estimate,” "forecast," “predict,” “potential” or the negative of those terms or other comparable terminology.

The Company has based these forward-looking statements on its current expectations, assumptions, estimates and projections. While the Company believes these expectations, assumptions, estimates and projections are reasonable, such forward-looking statements are only predictions and involve known and unknown risks and uncertainties, many of which are beyond the Company’s control, including: the effect of the coronavirus (COVID-19) pandemic and its variants and the associated supply chain impacts on the Company’s business; general economic, credit, and market conditions; the outbreak of war between Russian and Ukraine, including the imposition of sanctions related thereto, or escalation of conflict in other regions where we do business; future impairment charges; customer acceptance of new products; competition from other industry participants, some of whom have greater marketing resources or larger market shares in certain product categories than the Company does; pricing pressures from customers and consumers; resolution of uncertain tax positions, including the Company’s appeal of the draft and final Notices of Proposed Assessment (“NOPAs”) issued by the U.S. Internal Revenue Service and the impact that an adverse result in any such proceedings would have on operating results, cash flows, and liquidity; pending and potential third-party claims and litigation, including litigation relating to the Company’s restatement of previously-filed financial information and litigation relating to uncertain tax positions, including the NOPAs; potential impacts of ongoing or future government investigations and regulatory initiatives; potential costs and reputational impact of product recalls or sales halts; the impact of tax reform legislation and healthcare policy; the timing, amount and cost of any share repurchases; fluctuations in currency exchange rates and interest rates; the Company’s ability to achieve the benefits expected from the sale of its RX business and the risk that potential costs or liabilities incurred or retained in connection with that transaction may exceed the Company’s estimates or adversely affect the Company’s business or operations; the consummation and success of the proposed acquisition of Héra SAS and the ability to achieve the expected benefits thereof, including the risk that the parties fail to obtain the required regulatory approvals or to fulfill the other conditions to closing on the expected timeframe or at all, the occurrence of any other event, change or circumstance that could delay the transaction or result in the termination of the securities sale agreement or the risks that the Company’s synergy estimates are inaccurate or that the Company faces higher than anticipated integration or other costs in connection with the proposed acquisition; the consummation and success of other announced and unannounced acquisitions or dispositions, and the Company’s ability to realize the desired benefits thereof; and the Company’s ability to execute and achieve the desired benefits of announced cost-reduction efforts and strategic and other initiatives. An adverse result with respect to the Company’s appeal of any material outstanding tax assessments or pending litigation, including securities or drug pricing matters, could ultimately require the use of corporate assets to pay such assessments, damages from third-party claims, and related interest and/or penalties, and any such use of corporate assets would limit the assets available for other corporate purposes. These and other important factors, including those discussed in this report under “Risk Factors” and in any subsequent filings with the United States Securities and Exchange Commission, may cause actual results, performance or achievements to differ materially from those expressed or implied by these forward-looking statements. The forward-looking statements in this report are made only as of the date hereof, and unless otherwise required by applicable securities laws, we disclaim any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise.

TRADEMARKS, TRADE NAMES AND SERVICE MARKS

This report contains trademarks, trade names and service marks that are the property of Perrigo Company plc, as well as, for informational purposes, trademarks, trade names, and service marks that are the property of other organizations. Solely for convenience, certain trademarks, trade names, and service marks referred to in this report appear without the ®, ™ and SM symbols, but those references are not intended to indicate that we or the applicable owner, as the case may be, will not assert, to the fullest extent under applicable law, our or their rights to such trademarks, trade names, and service marks.

1

Perrigo Company plc - Item 1

Business Overview

PART I.

ITEM 1. BUSINESS

Perrigo Company plc was incorporated under the laws of Ireland on June 28, 2013. We became the successor registrant to Perrigo Company, a Michigan corporation, on December 18, 2013 in connection with the acquisition of Elan Corporation, plc ("Elan"). Unless the context requires otherwise, the terms "Perrigo", the "Company", "we," "our," "us," and similar pronouns used herein refer to Perrigo Company plc, its subsidiaries, and all predecessors of Perrigo Company plc and its subsidiaries.

WHO WE ARE

Our vision is to make lives better by bringing Quality, Affordable Self-Care Products that consumers trust everywhere they are sold. We are a leading provider of over-the-counter ("OTC") health and wellness solutions that are designed to enhance individual well-being and empower consumers to proactively prevent or treat conditions that can be self-managed. We are headquartered in Ireland and sell our products primarily in North America and Europe as well as in other markets around the world.

We endeavor to empower consumers’ self-care decisions, utilizing the Company’s core competencies to fully take advantage of the massive global trend towards self-care. We define self-care as not just treating disease or helping individuals feel better after taking a product, but also maintaining and enhancing their overall health and wellness. Consistent with our vision, in 2019 Perrigo’s management and board of directors launched a three-year strategy to transform the Company into a consumer self-care leader. We completed our transformation to a consumer self-care company in 2021 by reconfiguring the portfolio through the divestiture of our RX business, announcement of the acquisition of Héra SAS (“HRA Pharma”), and removal of significant uncertainty through settlement of a tax exposure. In addition, we continue to invest in growth initiatives to drive future consistent and sustainable results in line with consumer-packaged goods peers.

Segments

Our reporting and operating segments are as follows:

•Consumer Self-Care Americas ("CSCA") comprises our consumer self-care business (OTC, infant formula, and Oral care categories, our divested Animal health category, and contract manufacturing) in the U.S., Mexico and Canada.

•Consumer Self-Care International ("CSCI") comprises our consumer self-care business primarily branded in Europe and Australia, and our store brand business in the United Kingdom and parts of Europe and Asia. Our liquid licensed products business in the United Kingdom was divested on June 19, 2020.

We previously had an RX segment which was comprised of our prescription pharmaceuticals business in the U.S. and other pharmaceuticals and diagnostic businesses in Israel, which have been divested. Following the divestiture, there were no substantial assets or operations left in this segment. The RX segment was reported as Discontinued Operations in 2021, and is presented as such for all periods in this report (refer to Item 8. Note 8). Financial information related to our business segments can be found in Item 8. Note 21. Our segments reflect the way in which our management makes operating decisions, allocates resources and manages the growth and profitability of the Company.

2

Perrigo Company plc - Item 1

Business Overview

MAJOR DEVELOPMENTS IN OUR BUSINESS

Sale of Generic RX Pharmaceuticals Business

On March 1, 2021, we announced a definitive agreement to sell our RX business to Altaris Capital Partners, LLC ("Altaris"). On July 6, 2021, we completed the sale of the RX business for aggregate consideration of $1.55 billion, subject to customary adjustments for cash, debt, working capital and certain transaction expenses. The consideration includes approximately $53.3 million of reimbursements which Altaris will be required to deliver in cash to Perrigo pursuant to the terms of the Agreement. The sale resulted in a pre-tax gain, net of professional fees, of $47.5 million recorded in Other (income) expense, net on the Consolidated Statement of Operations for discontinued operations. The gain included a $159.3 million increase from the write-off of foreign currency translation adjustment from Accumulated other comprehensive income. The sale of the RX business helped establish Perrigo as a pure-play consumer self-care company, and was an essential milestone in our transformation plan.

HRA Pharma Acquisition Agreement

On September 8, 2021, we and our wholly-owned subsidiary Habsont Unlimited Company (the "Purchaser"), entered into a Put Option Agreement to acquire certain holding companies holding all of the outstanding equity interests of HRA Pharma from funds affiliated with private equity firms Astorg and Goldman Sachs Asset Management (collectively, the "Sellers"). Pursuant to the Put Option Agreement, following completion of the works council consultation process required under French law, the selling shareholders exercised their put option right under the Put Option Agreement and, on October 20, 2021, the Company, the Purchaser and the Sellers entered into a Securities Sale Agreement in the form previously agreed by the parties (the “Purchase Agreement”). Pursuant to the terms and subject to the conditions set forth in the Purchase Agreement, the Purchaser has agreed to acquire certain holding companies holding all of the outstanding equity interests of HRA Pharma from the Sellers for cash. The transaction values HRA Pharma at approximately €1.8 billion, or approximately $2.1 billion based on exchange rates as of the date of the Put Option Agreement, on an enterprise value basis and using a lockbox mechanism set forth in the Purchase Agreement. In September 2021, we entered into two non-designated currency option contracts to hedge the foreign currency exposure of the euro-denominated purchase price for HRA Pharma (refer to Item 8. Note 11).

The proposed final transaction is expected to close in the first half of 2022, subject to the satisfaction of customary closing conditions, including regulatory approvals. We intend to pay the purchase price using a combination of cash on hand and, depending upon market conditions, either funds available under our current credit facility or funds from new debt financing. HRA Pharma is one of the fastest growing OTC companies globally, with three category-leading self-care brands in blister care (Compeed®), women’s health (ellaOne®) and scar care (Mederma®), and brings expertise in prescription-to-OTC switches. This acquisition is expected to strengthen our presence in Europe, improve our financial profile and margins, and build on our transformation to a consumer self-care company. Operating results are expected to be reported within both our CSCA and CSCI segments.

Impact of COVID-19 Pandemic

We have been impacted by the coronavirus (COVID-19) global pandemic and the responses by government entities to combat the virus. We currently continue to operate in all our jurisdictions and are complying with the rules and guidelines prescribed in each jurisdiction. Refer to Item 7. Management's Discussion and Analysis - Executive Overview for a detailed discussion of the impact of the COVID-19 pandemic to our business.

Tribunal Ruling in Claim Arising from the Omega Acquisition

As previously disclosed, we were involved in arbitration in Belgium related to our claims of fraud in connection with the Omega acquisition. The Tribunal panel, as described in more detail under Claim Arising from the Omega Acquisition in Item 8. Note 19, found fraud by the sellers of Omega in a ruling on August 27, 2021 and awarded Perrigo approximately €355.0 million ($417.6 million at the time of cash receipt) including fees and costs. The panel also ruled against the sellers and in favor of Perrigo on all the counterclaims. The sellers have paid all amounts owed under the award, and the arbitral proceedings have now ended. The arbitration proceedings remain confidential as required by the Share Purchase Agreement dated November 6, 2014 ("SPA") and the rules of Belgian Centre for Arbitration and Mediation ("CEPANI"). We recorded the cash receipt as a reduction to Operating Expenses on the Consolidated Statements of Operations.

3

Perrigo Company plc - Item 1

Business Overview

Tax Updates

As described in Item 7. Management’s Discussion and Analysis – Recent Developments, Item 1A. Risk Factors - Tax Related Risks, and Item 8. Note 17, we are engaged in tax disputes in several jurisdictions. The following update notes certain material developments in such disputes since December 31, 2020, and makes use of certain terms defined in Item 8. Note 17.

•IRS Audit (2013-2015 Tax Years). On January 13, 2021, the IRS issued a 30-day letter proposing, among other modifications, certain transfer pricing adjustments regarding our profits from the distribution of omeprazole during our 2013 to 2015 tax years in the aggregate amount of $141.6 million. We timely filed a protest on February 26, 2021, on the grounds that certain of the government’s positions are currently the subject of pending litigation in the Western District of Michigan with respect to refund requests relating to our 2009 through 2012 tax years. We believe that we should prevail on the merits on the issues being contested. However, we have reserved for taxes and interest payable on a 5.24% deemed royalty on omeprazole, which we have conceded, through the tax year ended December 31, 2018.

In addition, the 30-day letter for the 2013-2015 tax years expanded on a Notice of Proposed Adjustment ("NOPA") issued on December 11, 2019 and proposed to disallow adjustments to gross sales income on the sale of prescription products to wholesalers for accrued wholesale customer pipeline chargebacks where the prescription products were not re-sold by such wholesalers to covered retailers by the end of the tax year for the 2013-2015 tax years. We filed a protest on February 26, 2021 to request IRS Appeals consideration. On January 20, 2022, the IRS responded to our Protest with its Rebuttal and reiterated its position in the NOPA that the accrued chargebacks are not currently deductible in the tax year accrued because all events have not occurred to establish the fact of the liability in the year deducted. If the IRS were to prevail in its proposed adjustment, we estimate a payment of approximately $18.0 million, excluding interest and penalties for the 2013-2015 tax years. In addition, we expect the IRS to seek similar adjustments for future years. If those future adjustments were to be sustained, based on preliminary calculations and subject to further analysis, we estimate this would result in a payment not to exceed $7.0 million through tax year ended December 31, 2021, excluding interest and penalties. We have fully reserved for this issue. We strongly disagree with the IRS’s proposed adjustment and will pursue all available administrative and judicial remedies necessary.

•IRS NOPA (Interest Deductibility for 2014-2015 Tax Years). On January 13, 2021, we received a Revenue Agent Report (“RAR”) for our 2013-2015 tax years, which retains the adjustment from the previously disclosed NOPA dated May 7, 2020, which disallowed interest expense deductions of $414.7 million on $7.5 billion in debts owed by Perrigo U.S. to Perrigo Company plc for the 2014 and 2015 tax years. We timely filed a protest to the RAR with the IRS. The RAR caps the interest rate on the debt for U.S. federal income tax purposes at 130.0% of the Applicable Federal Rate on the stated grounds that the loans were not negotiated on an arm's-length basis. The IRS advised on May 3, 2021, that it changed its policy for all taxpayers and will no longer pursue the default interest of 130.0% of AFR. However, on January 20, 2022, the IRS responded to our Protest, which we filed on February 26, 2021, with its Rebuttal, and revised its position on this interest rate issue by reasserting that implicit parental support considerations are necessary to determine the arm's length interest rate and proposed revised interest rates that are higher than the interest rates proposed under its 130% of AFR assertion. The blended interest rate proposed by the IRS Rebuttal is 4.36%, an increase from the blended interest rate in the RAR of 2.57%, and lower than the stated blended interest rate of the loans of 6.8%. We will pursue all available administrative and judicial remedies necessary to defend the deductibility of the interest expense on this indebtedness.

•Irish Revenue NoA. On November 4, 2020, the Irish High Court ruled that the NoA did not violate our constitutional rights and legitimate expectations as a taxpayer. The Irish High Court did not review the technical merits of the NoA under Irish law. Elan Pharma pursued further challenges in the Irish Tax Appeals Commission, which scheduled a hearing for late 2021. Prior to the scheduled hearing, on September 29, 2021, Elan Pharma and Irish Revenue agreed to a full and final settlement of the NoA on the following terms: (i) on a 'without prejudice basis' and, for purposes of the settlement, an alternative basis of taxation was applied, (ii) Irish Revenue to take no further action in relation to the NoA or any Tysabri related income or transactions, (iii) no interest or penalties applied, (iv) a total tax of €297.0 million charged as full and final settlement of all liabilities arising from the sale of the Tysabri patents for the fiscal years 2013 to 2021, and (v) after Irish Revenue credited taxes already paid and certain unused R&D credits against the €297.0 million charged settlement amount, the total cash payment of €266.1 million ($307.5 million) was made on

4

Perrigo Company plc - Item 1

Business Overview

October 5, 2021. We recorded the payment as a component of income tax expense on the Consolidated Statements of Operations.

•Israeli Notice of Assessment. On December 29, 2020, we received a Stage A assessment from the Israeli Tax Authority ("ITA") for the tax years ended December 31, 2015 through December 31, 2017 in the amount of $63.8 million relating to attribution of intangible income to Israel, income qualifying for a lower preferential rate of tax, exemption from capital gains tax, and deduction of certain settlement payments. We timely filed our protest on March 11, 2021 to move the matter to Stage B of the assessment process. Through negotiations with the ITA, we resolved the audit for the tax year ended June 27, 2015 through tax year ended December 31, 2019, by agreeing to add tax year ended December 31, 2018 and tax year ended December 31, 2019 to the audit to reach an agreeable resolution to provide certainty for these additional periods. The agreement with the ITA required us to pay $19.0 million, after offset of refunds of $17.2 million, for the five taxable years. In addition, we paid $12.5 million to resolve a tax liability indemnity for the tax year ended December 31, 2017 relating to Perrigo API Ltd, which we disposed of in December 2017. We recorded the payments as a component of income tax expense on the Consolidated Statements of Operations.

•IRS NOPA (Athena IPR&D Royalty Rate). Without prejudice to pursuing other administrative and judicial remedies, on April 21 and 23, 2020, we filed requests for Competent Authority Assistance with the IRS and Irish Revenue to alleviate potential double taxation on Tysabri income for the 2011-2013 tax years followed by a supplemental request on October 20, 2020 related to a disputed litigation expense deduction involving the drug Zonegran. Both requests were accepted and are under review by the Competent Authorities of the United States and Ireland.

•IRS Audit (Omeprazole Transfer Pricing Adjustments in 2009-2012 Tax Years). A trial was held during the period May 25, 2021 to June 7, 2021 for the refund case in the United States District Court for the Western District of Michigan. Post-trial briefings were completed on September 24, 2021 and the case is now fully submitted for the court’s decision.

Securities Litigation Settlement

A settlement was reached in the case, In re Perrigo Company plc Securities Litigation as described in more detail in Item 8. Note 19 under the header In the United States (cases related to Irish Tax events). Motion papers seeking approval of the class action settlement were filed on October 4, 2021. The Court issued a preliminary approval order on October 29, 2021, which led to notices being sent to class members. The Court held a hearing on February 16, 2022 about the settlement and issued the Final Approval Order and Judgment. As a result, the settlement has been approved and the case has now ended. The settlement has been funded by insurance.

Share Repurchases

We did not purchase any shares during the year ended December 31, 2021.

Stock Exchange Listing

On November 22, 2021, we initiated steps to voluntarily delist our ordinary shares from trading on the Tel Aviv Stock Exchange (“TASE”). The delisting of our ordinary shares took effect on February 23, 2022, three months following the date of our request to the TASE pursuant to Israeli law. Our ordinary shares will continue to be listed for trading on the New York Stock Exchange (“NYSE”), and all ordinary shares that were traded on TASE were transferred to the NYSE where they continue to be traded.

Leadership Changes

Effective October 5, 2021, Jim Dillard was named Executive Vice President ("EVP") and President of our CSCA segment. Mr. Dillard's supply chain, manufacturing, R&D, innovation, and regulatory experience, along with his proven leadership skills, make him qualified to lead this segment. Before this role, Mr. Dillard served as Perrigo's EVP and Chief Scientific Officer.

5

Perrigo Company plc - Item 1

Business Overview

NEW PRODUCTS

We consider a product to be new if it (i) was reformulated, (ii) was a product line extension due to changes in characteristics such as strength, flavor, or color, (iii) had a change in product status from "prescription only" ("Rx") to OTC, (iv) was a new store brand or branded launch, (v) was provided in a new dosage form or (vi) was sold to a new geographic area with different regulatory authorities, in all cases, within 12 months prior to the end of the period for which net sales are being measured. During the year ended December 31, 2021, new product sales were $130.0 million.

CONSUMER SELF-CARE AMERICAS

Overview

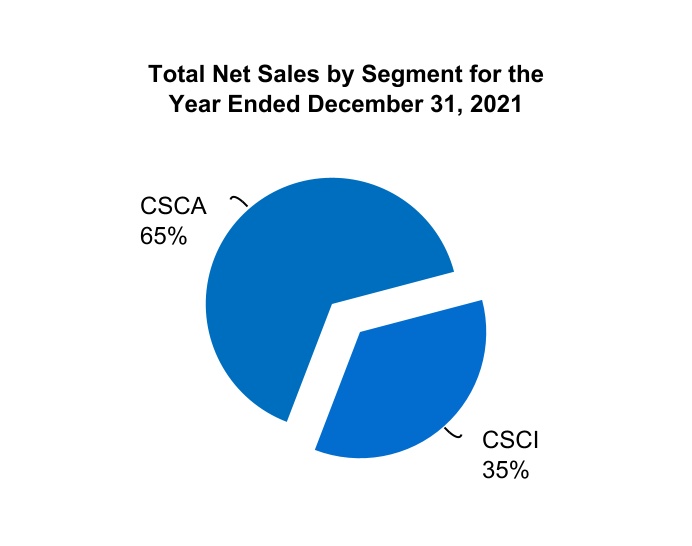

The CSCA segment is focused primarily on the sale of self-care products that help to grow our customers' overall self-care portfolio in categories including Upper respiratory, Pain and sleep-aids, Digestive health, Nutrition, Vitamins, minerals and supplements ("VMS"), Healthy lifestyle, Skincare and personal hygiene, and Oral care in the U.S., Mexico, Canada, and South America. We are a leading provider of self-care products sold to consumers via store brands. Consumer awareness and knowledge of the quality, value and efficacy of our products continues to grow due to efforts made by our retailers and wholesalers. We provide our customers self-care products under both their own brands and our brands, which are sold to consumers in store at shelf, store pickup and online. During the year ended December 31, 2021, our CSCA segment represented approximately 65% of consolidated net sales.

The CSCA segment develops, manufactures, and markets store brand self-care products that are comparable in quality and effectiveness to national brands. Store brand products must meet the same stringent U.S. Food and Drug Administration ("FDA") requirements as national brands within the U.S. and the requirements of comparable regulatory bodies outside the U.S. In most instances, our product packaging is designed to invite and reinforce comparison to national brand products, while communicating store brand value to consumers.

The cost of store brand and our branded products to retailers is significantly lower than that of comparable nationally advertised brand name products. Generally, retailers’ dollar profit per unit of store brand product is greater than the dollar profit per unit of the comparable national brand product. The retailer, therefore, can price a store brand product below the competing national brand product and realize a greater profit margin. The consumer benefits by receiving a high-quality product at a price below the comparable national brand product. As a result, our business model results in consumers saving money on their self-care needs.

We are dedicated to continuing to be the leader in developing and marketing new store brand and our branded products and have a research and development ("R&D") staff that we believe is one of the most experienced in the industry at developing products comparable in formulation and quality to national brand products. In order to offer consumers product features or benefits that national brand companies do not offer, we have implemented a product development strategy to differentiate store brand and our branded products from national brands. Our R&D team also responds to changes in existing national brand products by reformulating existing products. For example, in the OTC pharmaceutical market, certain new products are the result of changes in product status from Rx-to-OTC. These “Rx-to-OTC switches” require FDA approval through a process initiated by the drug innovator. The drug innovator usually begins the process by filing a New Drug Application ("NDA"), which is often followed by a competitor filing an Abbreviated New Drug Application ("ANDA"). Global regulatory agencies highly scrutinize any product application submitted to switch a product from physician prescribed Rx to OTC. New drugs are also marketed through the FDA's OTC monograph process, which allows us to produce drugs that are generally recognized as safe and effective without pre-marketing approval. In the Oral care category, we focus on creating products that are equivalent to the national brands, and also partner with our customers to create exclusive brands and differentiated products. We rely on both internal R&D and strategic product development agreements with outside sources to develop new products.

The CSCA segment also develops, manufactures, and distributes certain branded products, which are consistent with the segment's self-care strategy. Our branded products sold under brand names include Prevacid®24HR, Good Sense®, Zephrex D®, ScarAway®, Plackers®, Rembrandt®, Steripod®, Firefly®, REACH®, Dr. Fresh® , and Burt's Bees®.

We manufacture a significant portion of our CSCA segment's products at our plants located in the U.S., Mexico, and China, and we source the remaining materials and products from third parties. In addition, in order to

6

Perrigo Company plc - Item 1

CSCA

maximize both our capacity and sales of proprietary formulas, we engage in contract manufacturing, which involves producing unique ANDAs and monograph products through partnerships with major pharmaceutical and direct-to-consumer companies.

We believe the increasing age of the global population, continued rising healthcare costs, and consumers who proactively prevent or treat conditions will drive the need for the enhanced value that our products provide to consumers, which creates strong dynamics for U.S. OTC market growth. Another level of growth includes share gains against store brand competitors and store brand penetration gains versus national brands. In addition, we believe that new products, including new product innovation and products switching from Rx-to-OTC status (as described above) will continue to drive demand for our products and market growth within the segment.

Recent Trends and Developments

•During the third quarter of 2021, supply chain disruptions, including a significant shortage of truck drivers in the U.S. and record delays at global shipping ports, led to higher unfulfilled customer orders and higher input costs compared to the prior year. In the fourth quarter of 2021, we took a series of actions to improve the situation, including reconfiguring our distribution system for short term shipments, outsourcing highly complex product lines to a third party logistic provider, adding regional carriers for challenged shipping lanes, hiring additional distribution center personnel, and increasing the purchase cycle as it relates to the manufacturing process. While we believe supply chain disruptions will continue in the near-term, we are expecting to continue to see improvements throughout 2022.

•During the first half of 2021, net sales of cough and cold products decreased as a result of the very low incidence of cough and cold related illness, which we believe is attributed to social distancing and mask mandates put in place to combat the spread of COVID-19. However, increased consumer takeaway at our retail customers, starting in May 2021, suggested normalizing consumer purchasing routines could be expected in the second half of 2021. In the third quarter, we experienced higher demand for cough, cold and pain products due primarily to the higher incidences of cough and cold illness as society returned to in-person activities. Consumer take away continued to remain strong during the fourth quarter and, as such, we expect sales of cough, cold and pain products to continue to increase, depending on the trajectory of the COVID-19 pandemic moving forward (refer to Item 7. Management's Discussion and Analysis - Executive Overview).

•On May 18, 2021, we announced a definitive agreement to sell our Latin American businesses to Advent International. This transaction is part of our margin improvement program and Project Momentum cost savings initiative and is expected to close in the first half of 2022. We determined that the carrying value of these businesses exceeded their fair value less cost to sell, resulting in an impairment charge of $162.2 million allocated to goodwill and assets held for sale (refer to Item 8. Note 9).

7

Perrigo Company plc - Item 1

CSCA

Products

Our CSCA segment offers products in the following categories:

| Product Category | Description | |||||||

| Pain and sleep-aids | Products comprised of pain relievers, fever reducers and sleep-aids. | |||||||

| Upper respiratory | Products that relieve upper respiratory symptoms, including cough suppressants, expectorants, sinus and allergy relief. | |||||||

| Digestive health | Products such as antacids, anti-diarrheal, and anti-heartburn that relieve symptoms associated with digestive issues. | |||||||

| Nutrition | Infant formulas and nutritional beverages. | |||||||

| Healthy lifestyle | Products that help consumers live a healthy lifestyle such as smoking cessation, diabetes care, and well-being products. | |||||||

| Skincare and personal hygiene | Products for the face and body such as dermatological care, scar management, lice treatment, and other products for various skin conditions. | |||||||

| Oral care | Products used for oral care, including toothbrushes, toothbrush replacement heads, floss, flossers, whitening products and toothbrush covers. | |||||||

| Vitamins, minerals, and supplements | Vitamins, minerals, and supplements. | |||||||

| Other | Diagnostic products and other miscellaneous self-care products. | |||||||

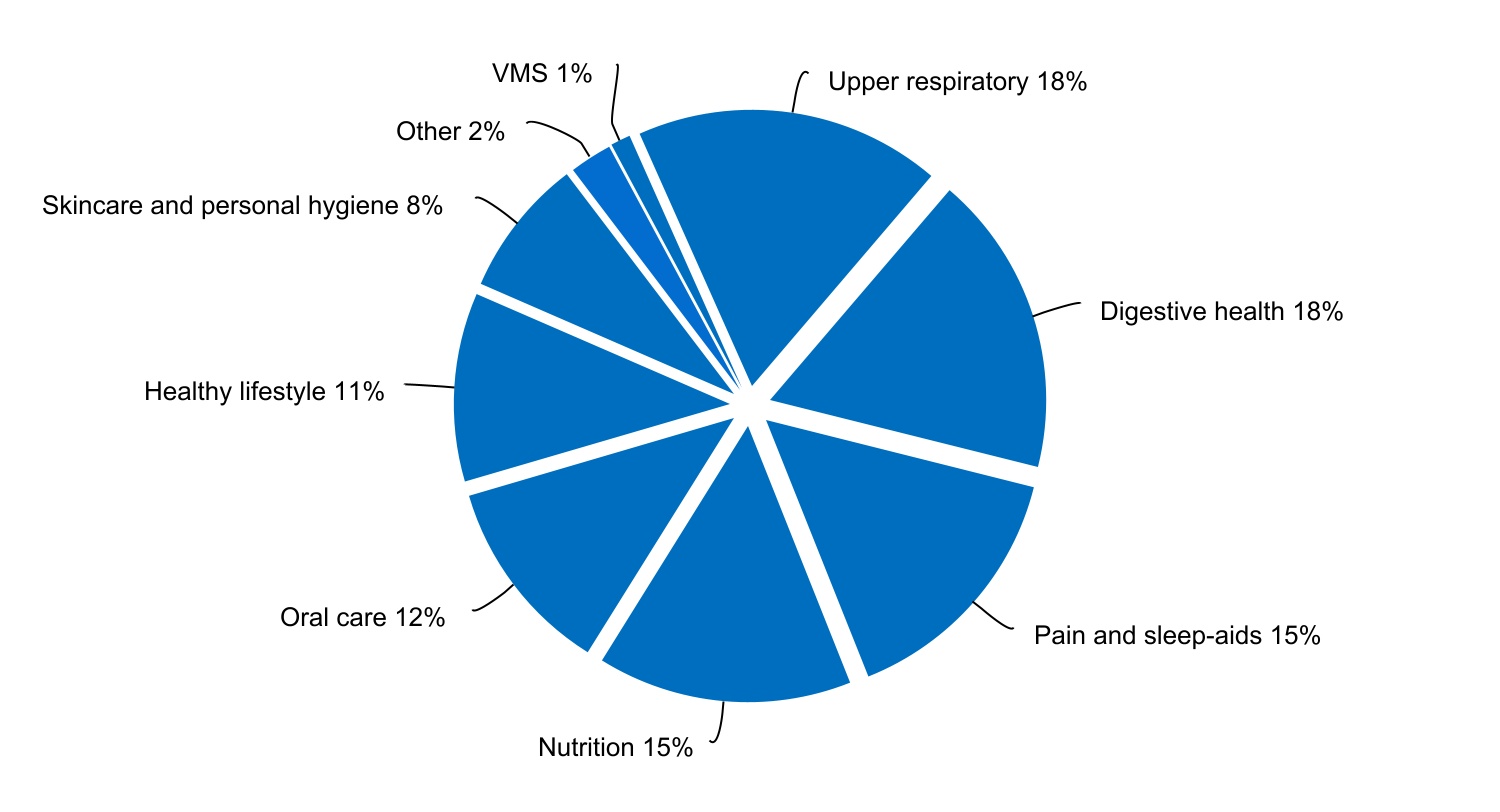

The chart below reflects net sales by product category in the CSCA segment, which includes net sales from our OTC contract manufacturing business for the year ended December 31, 2021.

We launched several new CSCA products in the year ended December 31, 2021, most notably a store brand hypoallergenic infant formula, Diclofenac sodium topical gel 1%, and Esomeprazole Mini. During the year ended December 31, 2021, new product sales in the CSCA segment were $56.1 million.

We, on our own or in conjunction with partners, received final FDA approval for one new product within the CSCA segment in the year ended December 31, 2021, and as of December 31, 2021, we had eight new product applications pending FDA approval.

8

Perrigo Company plc - Item 1

CSCA

Sales and Marketing

Our customers include major global, national, and regional retail drug, supermarket, and mass merchandise chains such as Walmart, Costco, CVS, Target, Walgreens Boots Alliance, Kroger, Dollar General, Sam’s Club, Topco, Padagis e-commerce stores including Amazon, and major wholesalers, including McKesson, Amerisource Bergen, and Cardinal Health.

We seek to establish customer loyalty through superior customer service by providing a comprehensive assortment of high quality, affordable products; timely processing, shipment and delivery of orders; assistance in managing customer inventories; and support in managing and building the customer’s self-care market portfolio including their store brand business, trade and digital marketing activities. The CSCA segment employs its own sales force to service larger customers and uses industry brokers for other customers. Field sales employees, with support from marketing and customer service team members, are assigned to specific customers in order to work most effectively with the customer. The commercial organization provides our customers with customized in-store and digital marketing programs for all products we supply in the customers' self-care market portfolio.

The primary objective of this management approach is to enable our retail, e-commerce, and wholesale customers to increase sales and market share of their overall self-care portfolio. We partner with our retailers to provide customized store brand and branded products that provide quality and value to consumers. We invite comparison of store brand and our branded products to national brand products. Our sales and marketing personnel assist customers in the development and introduction of new store brand and our branded products, and in the promotion of customers’ existing store brand and our branded products by providing market information; establishing individualized promotions and marketing programs, which may include floor displays, bonus sizes, coupons, rebates, store signs, and promotional packs; and performing consumer research. During the year we saw consumers seeking more of their self-care product needs online, in part due to the COVID-19 pandemic, resulting in the growth of e-commerce as a consumer channel for our products. We have developed resources, programs and tools to be a strategic marketing partner for our customers’ digital marketing efforts. This provides our customers with a holistic campaign to convert shoppers to store brand whether they shop in-store or online.

In contrast to national brand manufacturers, which incur considerable advertising and marketing expenditures targeted directly to the end user or consumer, the CSCA segment’s primary marketing efforts are channeled through retailers and wholesalers and reach the consumer through our customers’ in-store marketing programs and our digital media programs. Because the retail profit margin for store brand and our branded products is generally higher than national brand products, retailers and wholesalers often commit funds for additional promotions.

In addition to in-store marketing programs, team members in our nutrition category market products directly to consumers and healthcare professionals.

Competition

The markets for our self-care products are highly competitive and differ for each product line and geographic region. Our primary competitors include manufacturers, such as Dr. Reddy's Labs, LNK International, Inc., PL Developments, Aurobindo and Sun Pharmaceuticals, and brand-name pharmaceutical and consumer product companies, such as Johnson & Johnson, Procter & Gamble, Reckitt Benckiser, Abbott Nutrition, Bayer AG, Sanofi and Philips. The various major categories of our CSCA business each have certain key competitors, such that a competitor generally does not compete across all product lines. However, some competitors do have larger sales volumes in certain of our categories. Additionally, national brand companies tend to have more resources committed to marketing their products and could in the future manufacture store brand versions of their products at lower prices than their national brand products. Competition is based on a variety of factors, including price, quality, assortment of products, customer service, marketing support, and approvals for new products. Refer to Item 1A. Risk Factors - Operational Risks for additional information and risks associated with competition.

9

Perrigo Company plc - Item 1

CSCI

CONSUMER SELF-CARE INTERNATIONAL

Overview

The CSCI segment is comprised of our consumer self-care business outside of North America, including our branded business in Europe and Australia and our store brand businesses in the United Kingdom and parts of Europe and Asia. The CSCI segment develops, manufactures, markets, and distributes many well-known European consumer self-care brands in the Upper respiratory, Pain and sleep-aids, Digestive health, VMS, Healthy lifestyle, Skincare and personal hygiene, and Oral care categories. The segment leverages its broad regulatory, sales, and distribution infrastructure to innovate new products and brands, in-license and expand product lines, and sell and distribute third-party brands. The CSCI segment sells these products through an extensive network of customers including pharmacies, wholesalers, drug and grocery store retailers, and para-pharmacies in more than 23 countries, primarily in Europe. Many CSCI products have leading positions in the markets in which they compete. During the year ended December 31, 2021, the CSCI segment represented approximately 35% of consolidated net sales.

Through continued investment in R&D partnerships and new technologies, the CSCI segment strives to offer high quality self-care products that meet consumers' needs. Internal R&D, new product development, insourcing, acquisitions, and partnerships support the new product pipeline, both in terms of brand extensions and product improvements. In the U.K., R&D focuses on the development of both store brand and branded products. Additional R&D centers are located in France, Sweden, Austria, Belgium, China, the Netherlands, and Germany. In the rest of Europe, most R&D is performed by external partners with oversight from our teams. The segment has seven plants dedicated to manufacturing certain of its products.

The CSCI segment primarily focuses on building local and regional brands sold through mass merchandisers, drug stores, individual and chain pharmacies, and e-commerce channels.

While the CSCI segment sells approximately 220 brands, we primarily concentrate our resources on "Focus Brands", consisting of approximately 50 key brands and sub-brands. These are selected on the basis of their current sales and growth potential in the self-care market. Additional resources, including R&D investments, are allocated to these Focus Brands to strengthen their market position in high opportunity profit categories while leveraging the same R&D efforts under smaller local brands.

Recent Trends and Developments

•During the first half of 2021, net sales of cough and cold products decreased as a result of the very low incidence of cough, cold and flu related illness this year. We believe the very low incidence of cough, cold and flu related illness was attributed to COVID-19 social distancing and mask requirements. During the second half of 2021, we experienced higher demand for cough and cold, and pain products due primarily to the higher incidences of cough, cold and flu illness as society returned to in-person activities. The spread of certain COVID-19 variants may have contributed to these higher incidences as their symptoms can be similar. Further, consumer take away remained strong during the second half of 2021 led by cough and cold, and pain products, and we expect further normalizing of consumer purchasing routines moving forward depending on the trajectory of the COVID-19 pandemic. Refer to Item 7. Management's Discussion and Analysis - Executive Overview.

•During the third quarter, a number of EU regulators requested recalls, some at the consumer level, due to the detection of 2-chloroethanol (“2-CE”). 2-CE has been associated with the presence of ethylene oxide, a constituent in pesticides, which is not permitted for use in food products under food regulations in the EU. Due to the potential presence of ethylene oxide in certain of our vitamin, minerals and supplements ("VMS") products, we initiated recalls. We have since secured alternate sourcing of the raw material. During the year ended December 31, 2021, these recalls resulted in a decrease in net sales of $2.6 million and a decrease in gross profit of $5.5 million, which included obsolete inventory.

10

Perrigo Company plc - Item 1

CSCI

Products

Our CSCI segment offers products and Focus Brands in the following categories:

| Product Category | Description | Focus Brands | ||||||||||||

| Pain and sleep-aids | Products comprised of pain relievers, fever reducers and sleep-aids. | Solpadeine® Nytol® | ||||||||||||

| Upper respiratory | Products that relieve upper respiratory symptoms, including cough suppressants, expectorants, sinus and allergy relief. | Aflubin® Bronchenolo®/Bronchostop® Physiomer® Phytosun® Coldrex® Prevalin®/Beconase® | ||||||||||||

| Digestive health | Products such as antacids, anti-diarrheal, and anti-heartburn that relieve symptoms associated with digestive issues. | |||||||||||||

| Healthy lifestyle | Products that help consumers live a healthy lifestyle such as smoking cessation, weight management, diabetes care, and well-being products. | NiQuitin® XLS (Medical)® Yokebe® | ||||||||||||

| Skincare and personal hygiene | Products for the face and body such as dermatological care, sun protection, scar management, lice treatment, insect repellents, and other products for various skin conditions. | ACO® Biodermal® Canoderm® Dermalex® Lactacyd® Wartner® Jungle Formula® Paranix® Pencivir® | ||||||||||||

| Oral care | Products used for oral care, including toothbrushes, toothbrush replacement heads, floss, flossers, and whitening products. | Plackers® | ||||||||||||

| VMS | Vitamins, minerals, and supplements. | Abtei® Arterin® Davitamon® Granufink® Zaffranax® Probify® | ||||||||||||

| Other | Diagnostic products and other miscellaneous self-care products. | |||||||||||||

11

Perrigo Company plc - Item 1

CSCI

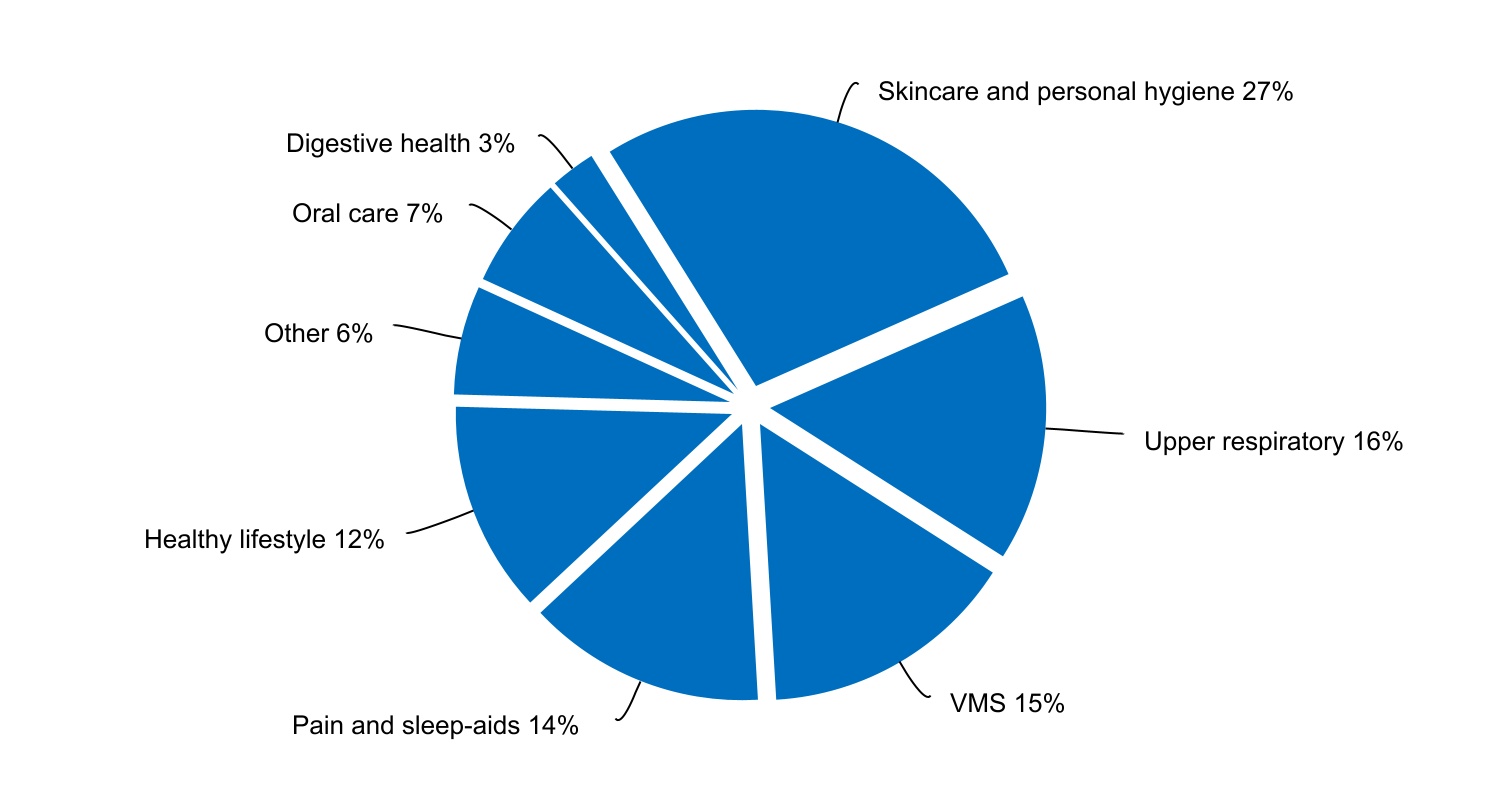

The chart below reflects net sales by product category in the CSCI segment for the year ended December 31, 2021.

We launched a number of new CSCI products in the year ended December 31, 2021, most notably some line extensions in the XLS weight management brand and ACO® brands in the Healthy lifestyle and Skincare and personal hygiene categories, respectively. In addition, we launched various VMS line extensions and a pan European probiotic mix under the new brand Probify®. During the year ended December 31, 2021, new product sales in the CSCI segment were $73.9 million.

The CSCI segment has new product development across all categories, with each of its Focus Brands having a three to five-year innovation master plan.

Sales and Marketing

Our products are sold to customers including pharmacies as well as, drug, grocery, and e-commerce stores located primarily in Europe, such as Walgreens Boots Alliance, McKesson, AS Watson, Tesco, ASDA, DM, Rossman, Carrefour, and Amazon. The CSCI segment continues to align its sales and marketing organization with current market trends by significantly increasing resources towards e-commerce and key account management. The segment sells its products primarily through an established pharmacy sales force to an extensive network of individual pharmacists. Our sales representatives visit pharmacists frequently, ensuring strong in-store visibility of our brands and facilitating pharmacist education programs. Our sales, marketing, and regulatory teams use training/merchandising teams who work in conjunction with local sales representatives to improve our brands' presence and recognition. During the COVID-19 pandemic, we have combined our traditional sales efforts with telesales to find the optimal sales model and to keep employees and customers safe. We seek to attract key talent from leading OTC, Fast Moving Consumer Goods ("FMCG"), and retailer companies to build strong local teams throughout the countries in which the CSCI segment operates.

The CSCI segment markets products using intensive broadcast and digital advertising as well as point-of-sale promotional spending to enhance brand equity. Key marketing communication tools for the CSCI segment include television and digital commercials, consumer leaflets, product websites, targeted promotional campaigns and communication programs for health care professionals.

12

Perrigo Company plc - Item 1

CSCI

Competition

The competitive landscape of the European consumer products market in the categories in which we compete is highly fragmented, as local companies often hold leadership positions in individual product lines in particular countries. As a result, the relevant competition in each of the CSCI segment's markets is both local and global. Global competitors include GSK, Sanofi, Bayer, Johnson & Johnson, Reckitt Benckiser, Teva, Viatris, Stada, Novartis, Procter & Gamble and e-commerce companies, as well as additional regional competitors. We believe our key advantage lies in our unique combination of best practices in sales, marketing, and product development. Refer to Item 1A. Risk Factors - Operational Risks for additional information and risks associated with competition.

INFORMATION APPLICABLE TO ALL REPORTABLE SEGMENTS

Trademarks, Patents and Licensing Agreements

While we own certain trademarks and patents, neither our business as a whole, nor any of our segments, is materially dependent upon our ownership of any one trademark, or patent, or group of trademarks or patents.

Materials Sourcing

Affordable, high-quality raw materials and packaging components are essential to all of our business units due to the nature of the products we manufacture. Raw materials and packaging components are generally available from multiple suppliers. Supplies of certain raw materials and packaging components, due to their technical specifications and product delivery systems, may be more limited, as they are available from one or only a few suppliers and may require extensive compatibility testing before we can use them.

Historically, we have been able to react effectively, yet not always immediately, to situations that require alternate sourcing. Should such alternate sourcing be necessary, FDA requirements placed on products approved through the ANDA or NDA process could substantially lengthen the approval of an alternate source and adversely affect financial results. We believe we have good, cooperative working relationships with our suppliers and have historically been able to capitalize on economies of scale in the purchase of materials and supplies due to our volume of purchases. Refer to Item 1A. Risk Factors - Operational Risks for risks associated with materials sourcing. Refer to Item 7. Management's Discussion and Analysis - Executive Overview for a detailed discussion of the impact of the COVID-19 pandemic on our material sourcing.

Manufacturing and Distribution

Our primary manufacturing facilities are in the U.S. We also have manufacturing facilities in the U.K., Belgium, France, Germany, Austria, Mexico, China, and Australia, along with a joint venture in China. Refer to Item 1A. Risk Factors - Operational Risks for risks associated with our manufacturing facilities. We supplement our production capabilities with the purchase of products from outside sources. The capacity of some facilities may be fully utilized at certain times for various reasons, such as customer demand, the seasonality of certain product categories (for example, our cough/cold/flu and allergy products), and new product launches. We may utilize available capacity by performing contract manufacturing for other companies. We have logistics facilities in the U.S., Mexico, Australia, and numerous locations throughout Europe. We use contract freight and common carriers to deliver our products. Refer to Item 7. Management's Discussion and Analysis - Executive Overview for a detailed discussion of the impact of the COVID-19 pandemic on our manufacturing and distribution.

Significant Customers

We have one significant customer that represents approximately 14% of our consolidated net sales. While we have other important customers, no other individual customer represents more than 10% of net sales. However, the loss of one or more of our customers could be material. We believe we generally have good relationships with our customers. Refer to Item 1A. Risk Factors - Operational Risks for risks associated with customers.

13

Perrigo Company plc - Item 1

Environmental

Our facilities and operations are subject to various environmental laws and regulations. We undergo periodic internal audits relating to environmental, health and safety requirements in order to maintain compliance with applicable laws and regulations in each of the jurisdictions in which we operate. We have made, and continue to make, expenditures necessary to comply with applicable environmental laws; however, we do not believe that the costs for complying with such laws and regulations have been or will be material to our business. We do not have any material remediation liabilities outstanding.

While we believe that climate change could present risks to our business, including increased operating costs due to additional regulatory requirements, physical risks to our facilities, water limitations, and disruptions to our supply chain, we do not believe these risks are material to our business in the near term.

Human Capital Resources

We are passionate about making lives better. At Perrigo, we believe that the continuous personal and professional development of our people is an important component of our ability to attract, retain, and motivate top talent, which are all important aspects of our self-care strategy. Our global workforce consists of more than 9,900 full time and part time employees spread across 34 countries, of which approximately 21% were covered by collective bargaining agreements as of December 31, 2021. We continuously endeavor to provide a diverse, inclusive, and safe work environment so our colleagues can bring their best to work, every day. We are all responsible for upholding Perrigo’s Core Values - Integrity, Respect, and Responsibility - in addition to the Perrigo Code of Conduct which, together, form the foundation of all our policies, procedures, and practices. Together, we drive Perrigo forward to deliver on our vision to make lives better by bringing Quality, Affordable Self-Care Products that consumers trust everywhere they are sold.

Diversity and Inclusion

We strive for our workforce to represent the diverse consumer base we wish to serve enabling us to continue to deliver on our self-care promise. We believe diverse representation and practicing inclusion creates lasting benefits for Perrigo colleagues, our customers, consumers, and shareholders through enhanced team performance, innovation, and profitable growth. To accomplish this objective, we rolled out a three-year strategy at the beginning of 2020 that focuses on three key diversity and inclusion areas:

•Educating our workforce on our diversity and inclusion strategy and initiatives;

•Strengthening our talent management practices through a lens of equity and inclusion; and

•Creating diversity and inclusion governance and accountability to establish our foundation and help us monitor progress.

Perrigo is committed to the well-being of the communities we serve and the individuals who work with us. Accordingly, we continue to take action to help address oppression and inequality based on multiple aspects of diversity. We understand the devastating impact that systemic oppression, injustice, and acts of violence have on underrepresented communities. Murray Kessler, President and CEO, has encouraged all Perrigo colleagues to stand united and take responsibility to learn how each of us can play a role in promoting inclusion and fighting both discrimination and implicit bias in the workplace and in our society as a whole. These efforts include open dialogues between our Board of Directors and Executive Operating Committee on topics including diversity, equity and inclusivity. Our Perrigo colleagues, including senior management, continually receive educational resources and information on how to best serve as allies in support of underrepresented groups and to learn how we can contribute to healing our society's divisions. All colleagues are encouraged to practice self-care and are provided support resources such as our global Employee Assistance Program that includes staff members who identify with various underrepresented communities and speak multiple languages.

Compensation, Benefits, Health, Safety, and Well-being

Perrigo’s commitment to self-care starts with our own team. Our top priority during the global COVID-19 pandemic has been, and continues to be, the safety of our colleagues. When faced with the challenges of this pandemic, we focused on understanding and supporting each diverse individual and the unique circumstances impacting their ability to serve as an essential worker. We have implemented safety measures to protect our on-site essential colleagues, while asking those who can safely work from home to do so. On-site, we've implemented a

14

Perrigo Company plc - Item 1

multi-step pre-screening process before entry into any facility, deep-cleaning protocols, and other safety precautions, all consistent with the rules and guidelines in each jurisdiction.

We strive to provide pay, benefits and services that support the total well-being of our people. Our total rewards package delivers competitive pay, broad-based stock grants, cash-based annual incentives, healthcare, retirement benefits, paid time off, and on-site services, among other benefits.

Perrigo’s total rewards complement a strong health and safety culture that continues with our global well-being program designed to inspire colleagues to maintain and improve their health. Launched in 2016, Perrigo’s "HEALTHYyou" well-being program continues to support colleagues and their families as they navigate their own self-care and well-being journeys. Our colleagues highly value this program and it continues to be recognized externally by receiving the Best and Brightest in Wellness™ Award in each year since 2017.

Growth, Development, and Engagement

We are committed to engaging our colleagues and fostering a belonging culture, where our people feel enabled to contribute their best to Perrigo's self-care transformation. This includes initiatives supporting overall job satisfaction, diversity and inclusion, personal and professional skill development, work/life balance, and an environment that encourages good health and safety, while upholding our core values of Integrity, Respect, and Responsibility.

Perrigo regularly conducts global engagement surveys to gather feedback from colleagues to identify strengths and opportunities within our culture. We have implemented a competency model to clarify the behaviors that reinforce our culture and lead to success at Perrigo. Additionally, we use a variety of channels to facilitate open and direct communication, including regular open forums and town hall meetings with our executive leadership team.

Our development philosophy focuses on a 70-20-10 approach, which provides a practical, blended framework for learning to support individual long-term success (where individuals obtain 70% of their knowledge from job-related experiences, 20% from interactions with others, and 10% from formal educational events). We have significantly expanded our learning capabilities by providing access to extensive on-demand self-study content to colleagues. We believe this model enables our people to deliver on our self-care vision by empowering them to be their best and make a difference to Perrigo Colleagues, Customers, Consumers, Communities, and Shareholders.

Corporate Social Responsibility

We are committed to doing business in a socially, environmentally and fiscally responsible manner. That commitment is reflected in our well-established governance, corporate responsibility and sustainability programs, as well as by our board oversight of governance and sustainability. A summary of our environmental and social initiatives is below, and additional details can be found in our 2021 Corporate Social Responsibility (“CSR”) Report available on our website. In 2020, we adopted the United Nations Sustainable Development Goals (“UN SDG”) as a global framework and committed to six goals within the UN SDG framework. In 2021, we set new specific objectives and targets for the next five years related to each of these goals, which are detailed in our 2021 CSR report. Our progress towards achieving these goals and objectives will be updated in our subsequent CSR reports on an annual basis.

•Environmental: we are committed to manufacturing our products responsibly, supporting the global drive to reduce carbon emissions and minimize our impact on the climate. We formalized our commitment to sustainability in 2015 by establishing a corporate sustainability strategy focused on reducing the environmental impact of our operations, product packaging, and supply chain. In 2020, we enhanced that strategy by committing to Goal 12: Responsible Production and Consumption and Goal 13: Climate Action, of the UN SDG.

•Social: Our vision is to make lives better, by bringing quality affordable self-care products that consumers trust, everywhere they are sold. This puts the social impact of our business front and center. We are proud to maintain goals and programs relating to Diversity and Inclusion, Human Capital Management, Human Rights, and Community Engagement and Giving. In 2020, as part of our social initiatives, we committed to Goal 3: Good Health and Well-being, Goal 4: Quality Education, Goal 5: Gender Equality, and Goal 10: Reducing Inequality, of the UN SDG.

15

Perrigo Company plc - Item 1

Regulation

GOVERNMENT REGULATION AND PRICING

The manufacturing, processing, formulation, packaging, labeling, testing, storing, distributing, advertising, and selling of our products are subject to regulation by a variety of agencies in the localities in which our products are sold. In addition, we manufacture and market certain of our products in accordance with standards set by various organizations. We believe that our policies, operations, and products comply in all material respects with existing regulations to which we are subject. Refer to Item 1A. Risk Factors - Operational Risks for related risks.

United States Regulation

U.S. Food and Drug Administration

The FDA has jurisdiction over OTC drug products, API, medical devices and Infant Formula products. The FDA’s jurisdiction extends to the manufacturing, testing, labeling, packaging, storage, distribution, and promotion of these products. We are committed to consistently providing our customers with high quality products that adhere to "current Good Manufacturing Practices" ("cGMP") regulations promulgated by the FDA. If the FDA or comparable regulatory authority becomes aware of new safety information about any of our products, these authorities may require further inspection, enhancement to manufacturing controls, labeling changes, additional testing method requirements, restrictions on indicated uses or marketing, post-approval studies or post-market surveillance.

OTC

All facilities where OTC products are manufactured, tested, packaged, stored, or distributed for the U.S. market must comply with FDA cGMPs and regulations promulgated by competent authorities in the countries, states and localities where the facilities are located. All of our drug products are manufactured, tested, packaged, stored, and distributed according to cGMP regulations. The FDA performs periodic audits to ensure that our facilities remain in compliance with all appropriate regulations.

Many of our OTC products are regulated under the OTC monograph system and subject to certain FDA regulations. Under this system, selected OTC drugs are generally recognized as safe and effective and do not require the approval of an ANDA or NDA prior to marketing. Products marketed under the OTC monograph system must conform to specific quality, formula, and labeling requirements, including permitted indications, required warnings and precautions, allowable combinations of ingredients, and dosage levels. It is generally less costly to develop and bring to market a product regulated under the OTC monograph system.

Under the Federal Food, Drug and Cosmetic Act, as amended ("FFDCA") (the Hatch-Waxman amendments), a company submitting an NDA can obtain a three-year period of marketing exclusivity for an OTC product if it performs a clinical study that is essential to FDA approval. Longer periods of exclusivity are possible for new chemical entities, orphan drugs (those designated under section 526 of the FFDCA) and drugs under the Generating Antibiotic Incentives Now Act. During this exclusivity period, the FDA cannot approve any ANDAs for a similar or equivalent generic product, which can preclude another party from marketing a similar product during this period. A company may obtain an additional six months of exclusivity if it conducts pediatric studies requested by the FDA on the product. This exclusivity can delay both the FDA approval and sales of certain products.

Under certain circumstances, the first filer of an ANDA may be entitled to a 180-day generic exclusivity period for certain products. This exclusivity period often follows a patent certification and litigation process whereby the product innovator may sue for infringement. The legal action does not ordinarily result in material damages, but it generally triggers a statutorily mandated delay in FDA approval of the ANDA for a period of up to 30 months from when the innovator was notified of the patent challenge.

The Food and Drug Administration Safety and Innovation Act ("FDASIA") was signed into law on July 9, 2012. The law established, among other things, new user fee statutes for generic drugs and biosimilars, FDA authority concerning drug shortages, and changes to enhance the FDA's inspection authority of the drug supply chain. The FDASIA also reduced the time required for FDA responses to generic-blocking citizen petitions. We implemented new systems and processes to comply with the new facility self-identification and user fee requirements of the FDASIA, and we monitor facility self-identification and fee payment compliance to mitigate the risk of potential supply chain interruptions or delays in regulatory approval of new applications.

The FDA Reauthorization Act of 2017 created a pathway by which the FDA may, at the request of an applicant, designate a drug with “inadequate generic competition” as a Competitive Generic Therapy ("CGT"). At the

16

Perrigo Company plc - Item 1

Regulation

request of the applicant, the FDA may expedite the development and review of an ANDA for a drug designated as a CGT. The first approved application for a drug with a CGT designation for which there are no unexpired patents or exclusivities listed in the Orange Book at the time of original submission of the ANDA may be eligible for 180 days of generic exclusivity.

Active Pharmaceutical Ingredients

Third parties develop and manufacture APIs for use in certain of our pharmaceutical products that are sold in the U.S. and other global markets. API manufacturers typically submit a drug master file to the regulatory authority that provides the proprietary information related to the manufacturing process. The FDA inspects the manufacturing facilities to assess cGMP compliance, and the facilities and procedures must be cGMP compliant before API may be exported to the U.S.

Medical Devices

We are subject to the Medical Device Amendments of 1976 to the FFDCA and its subsequent amendments in the US. The regulations issued thereunder provide for regulation by the FDA of the design, manufacture and marketing of medical devices, including some of our products marketed under our oral care and OTC businesses. All of our current medical devices fall under Class I or Class II of the regulations. These products do not require premarket approval but may or may not require a 510(k) premarket notification depending on whether or not the product is 510(k) exempt. These devices are also subject to other general controls established by the FDA, such as registration, listing, labeling, and reporting obligations.

Infant Formula

The FDA’s Center for Food Safety and Applied Nutrition is responsible for the regulation of infant formula. The Office of Nutrition, Labeling and Dietary Supplements ("ONLDS") has labeling responsibility for infant formula, while the Office of Food Additive Safety ("OFAS") has program responsibility for food ingredients and packaging. The ONLDS evaluates whether an infant formula manufacturer has met the requirements under the FFDCA and consults with the OFAS regarding the safety of ingredients in infant formula and of packaging materials for infant formula.

All manufacturers of pediatric nutrition products must begin with safe food ingredients, which are either generally recognized as safe or approved as food additives. The Infant Formula Act provides specific requirements for infant formula to ensure the safety and nutrition of infant formulas, including minimum and, in some cases, maximum levels of specified nutrients.

Before marketing a particular infant formula, the manufacturer must provide regulatory agencies assurance of the nutritional quality of that particular formulation consistent with the FDA’s labeling, nutrient content, and manufacturer quality control requirements. A manufacturer must notify the FDA at least 90 days before the marketing of any infant formula that differs fundamentally in processing or in composition from any previous formulation produced by the manufacturer. We actively monitor this process and make the appropriate adjustments to remain in compliance with recent FDA rules regarding cGMP, quality control procedures, quality factors, notification requirements, and reports and records for the production of infant formulas.

In addition, the FFDCA requires infant formula manufacturers to test product composition during production and shelf-life; to keep records on production, testing, and distribution of each batch of infant formula; to use cGMP and quality control procedures; and to maintain records of all complaints and adverse events, some of which may reveal the possible existence of a health hazard. The FDA conducts yearly inspections of all facilities that manufacture infant formula, inspects new facilities during early production runs, and collects and analyzes samples of infant formula. Our infant formula manufacturing facilities have been inspected by the FDA with no corrective actions required from the most recent inspections.

Our infant and toddler beverages are subject to the Food Safety Modernization Act ("FSMA"), which protects the safety of U.S. foods by mandating comprehensive, prevention-based controls within the food industry. Under FSMA, the FDA has mandatory recall authority for all food products and greater authority to inspect food producers and is taking steps toward product tracing to enable more efficient product source identification in the event of a safety issue.

17

Perrigo Company plc - Item 1

Regulation

U.S. Department of Agriculture

The Organic Foods Production Act enacted under Title 21 of the 1990 Farm Bill established uniform national standards for the production and handling of foods labeled as "organic." Our infant formula manufacturing sites in Vermont and Ohio adhere to the standards of the U.S. Department of Agriculture ("USDA") National Organic Program for production, handling, and processing to maintain the integrity of organic products and are USDA-certified, enabling them to produce and label organic products for U.S. and Canadian markets.

U.S. Environmental Protection Agency

The U.S. Environmental Protection Agency ("EPA") is the main regulatory body in the United States governing environmental regulation. Laws administered by the EPA, often in partnership with state agencies, include but are not limited to the Clean Air Act; the Clean Water Act; the Resource Conservation and Recovery Act; the Comprehensive Environmental Response, Compensation and Liability Act; and the Federal Insecticide, Fungicide, and Rodenticide Act.

U.S. Drug Enforcement Administration

The U.S. Drug Enforcement Administration ("DEA") regulates certain drug products containing controlled substances, and List I chemicals, such as pseudoephedrine, pursuant to the federal Controlled Substances Act ("CSA") and the Substance Use-Disorder Prevention that Promotes Opioid Recovery Treatment for Patients and Communities Act ("SUPPORT Act"). The CSA and DEA regulations impose registration, security, record keeping, suspicious order monitoring, reporting, storage, manufacturing, distribution, importation and other requirements upon legitimate handlers under the oversight of the DEA. The DEA categorizes controlled substances into Schedules I, II, III, IV, or V, with varying qualifications for listing in each schedule. We are subject to the requirements regarding List I chemicals. Our facilities that manufacture, distribute, import, or export any List 1 Chemicals must register annually with the DEA.

The DEA inspects all registered facilities to review security, record keeping, reporting, and handling prior to issuing a controlled substance registration, and it also periodically inspects facilities for compliance with the CSA and its regulations. Failure to maintain compliance with applicable requirements, particularly as manifested in the loss or diversion of DEA regulated substances, can result in enforcement action, such as civil penalties, refusal to renew necessary registration, or the initiation of proceedings to revoke those registrations. In certain circumstances, violations could lead to criminal prosecution. We are also subject to state laws regulating the manufacture and distribution of certain products.

Federal Healthcare Programs and Drug Pricing Regulation

In the U.S., government healthcare programs such as Medicaid are important third-party payers for patients treated with our products. While these programs may cover OTC products under some circumstances, utilization of our products under these programs is limited. When covering our products, these programs regulate the amount pharmacies and other healthcare providers are paid for our products. We participate in the following programs, and are subject to associated price reporting, payment, and other compliance obligations:

•Medicaid Drug Rebate Program (“MDRP”)—We are required to report pricing data to the Centers for Medicare & Medicaid Services (“CMS”) on a monthly and quarterly basis, and to pay rebates to state Medicaid programs on units of our drugs covered by such programs.

•340B Drug Pricing Program—We are required to charge certain healthcare providers, known as 340B “covered entities,” no more than the statutorily-defined 340B “ceiling price” for our covered outpatient drugs, and must report the 340B ceiling price to the government.