Table of Contents

As filed with the Securities and Exchange Commission on October 1, 2013.

Registration No. 333-190653

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

Amendment No. 2

to

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

SPRINGLEAF HOLDINGS, LLC

(Exact name of registrant as specified in its charter)

| Delaware | 6141 | 27-3379612 | ||

| (State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

601 N.W. Second Street

Evansville, IN 47708

(812) 424-8031

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Scott D. McKinlay, Esq.

Springleaf Holdings, LLC

601 N.W. Second Street

Evansville, IN 47708

(812) 424-8031

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

Copies to:

| Gregory A. Fernicola, Esq. Joseph A. Coco, Esq. Skadden, Arps, Slate, Meagher & Flom LLP Four Times Square New York, New York 10036-6522 (212) 735-3000 |

Richard D. Truesdell, Jr. Esq. Davis Polk & Wardwell LLP 450 Lexington Avenue New York, New York 10017 (212) 450-4000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement. þ

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer þ | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) | ||||||

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of each class of securities to be registered |

Proposed maximum aggregate offering |

Registration

Fee Amount(3) | ||

| Common Stock, $0.01 par value |

$50,000,000 | $6,820 | ||

|

| ||||

|

| ||||

| (1) | Estimated solely for the purpose of computing the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | Includes offering price of shares that the underwriters have the option to purchase pursuant to their over-allotment option. |

| (3) | A registration fee in the amount of $58,050 was previously paid by Springleaf REIT Inc., the registrant’s indirect wholly owned subsidiary, in connection with the filing of a Registration Statement on Form S-11 (Registration No. 333-174208) on May 13, 2011. Pursuant to Rule 457(p) under the Securities Act, the filing fee of $58,050 previously paid by Springleaf REIT Inc. is being used to offset the filing fee of $6,820 required for the filing of this Registration Statement. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We and the selling stockholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED OCTOBER 1, 2013

PRELIMINARY PROSPECTUS

Shares

Springleaf Holdings, Inc.

(currently named Springleaf Holdings, LLC)

Common Stock

$ Per Share

This is an initial public offering of common stock of Springleaf Holdings, Inc. (“Springleaf”) We are selling shares of our common stock. The selling stockholders identified in this prospectus are offering shares of Springleaf common stock. We will not receive any proceeds from the sale of shares of common stock by the selling stockholders. After this offering, Springleaf Financial Holdings, LLC, an entity owned primarily by a private equity fund managed by an affiliate of Fortress Investment Group LLC (“Fortress”), will own approximately % of our common stock, or % if the underwriters’ over-allotment option is fully exercised.

We expect the public offering price to be between $ and $ per share. Currently, no public market exists for the shares. We intend to apply to list our shares of common stock on the New York Stock Exchange (“NYSE”) under the symbol “LEAF.”

Investing in our common stock involves risks. See “Risk Factors” beginning on page 15 to read about certain factors you should consider before buying our common stock.

| Per Share |

Total |

|||||||

| Public Offering Price |

$ | $ | ||||||

| Underwriting Discount(1) |

$ | $ | ||||||

| Proceeds Before Expenses to Us |

$ | $ | ||||||

| Proceeds Before Expenses to the Selling Stockholders |

$ | $ | ||||||

| (1) | The underwriters will receive compensation in addition to the underwriting discount. See “Underwriting.” |

We have granted the underwriters the right to purchase up to additional shares of common stock, at the public offering price, less the underwriting discount, for the purpose of covering over-allotments.

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of common stock against payment on or about , 2013.

| BofA Merrill Lynch | Barclays | Citigroup | Credit Suisse | |||

The date of this prospectus is , 2013.

Table of Contents

| 1 | ||||

| 15 | ||||

| 38 | ||||

| 40 | ||||

| 41 | ||||

| 42 | ||||

| 44 | ||||

| 45 | ||||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

49 | |||

| 87 | ||||

| 88 | ||||

| 101 | ||||

| 127 | ||||

| 128 | ||||

| 133 | ||||

| 138 | ||||

| 144 | ||||

| Certain United States Federal Income Tax Considerations for Non-U.S. Holders of Common Stock |

146 | |||

| 148 | ||||

| 156 | ||||

| 156 | ||||

| 156 | ||||

| 156 | ||||

| Disclosure of Commission Position on Indemnification for Securities Act Liabilities |

157 | |||

| F-1 |

You should rely only on the information contained in this prospectus and any free writing prospectus prepared by us or on our behalf that we have referred you to. We, the selling stockholders and the underwriters have not authorized anyone to provide you with additional or different information. If anyone provides you with additional, different or inconsistent information, you should not rely on it. We are not making an offer of these securities in any state, country or other jurisdiction where the offer is not permitted. You should not assume that the information in this prospectus or any free writing prospectus is accurate as of any date other than the date of the applicable document regardless of its time of delivery or the time of any sales of our common stock. Our business, financial condition, results of operations or cash flows may have changed since the date of the applicable document.

Certain of the states in which we are licensed to originate loans and the state in which our insurance subsidiaries are domiciled (Indiana) have laws or regulations which require regulatory approval for the acquisition of “control” of regulated entities. Under some state laws or regulations, there exists a presumption of “control” when an acquiring party acquires as little as 10% of the voting securities of a regulated entity or of a company which itself controls (directly or indirectly) a regulated entity (the threshold is 10% under Indiana’s insurance statutes). Therefore, any person acquiring 10% or more of our common stock may need the prior approval of some state insurance and/or licensing regulators, or a determination from such regulators that “control” has not been acquired.

i

Table of Contents

NON-GAAP FINANCIAL MEASURES

As of June 30, 2013, our segments include: Consumer, Insurance, Portfolio Acquisitions, and Real Estate. Management considers Consumer, Insurance, and Portfolio Acquisitions to be our Core Consumer Operations and Real Estate as our Non-Core Portfolio.

We present pretax core earnings (loss), as described under “Prospectus Summary—Summary Historical Consolidated Financial Data,” as a non-GAAP financial measure in this prospectus. Pretax core earnings (loss) is a key performance measure used by management in evaluating the performance of our Core Consumer Operations. Pretax core earnings (loss) represents our income (loss) before provision for (benefit from) income taxes on a historical accounting basis, and excludes results of operations from our Real Estate segment and other non-core, non-originating legacy operations, restructuring expenses related to our Consumer and Insurance segments, gains (losses) associated with accelerated long-term debt repayment and repurchases of long-term debt, and impact from change in accounting estimate and results of operations attributable to non-controlling interests. Pretax core earnings (loss) is a non-GAAP measure and should be considered in addition to, but not as a substitute for or superior to, operating income, net income, operating cash flow and other measures of financial performance prepared in accordance with generally accepted accounting principles in the United States (“GAAP”). Under “Prospectus Summary—Summary Historical Consolidated Financial Data” herein, we include a quantitative reconciliation from income (loss) before provision for (benefit from) income taxes on a historical accounting basis to pretax core earnings (loss).

We also present our segment financial information on a historical accounting basis (a non-GAAP measure using the same accounting basis that we employed prior to the Fortress Acquisition (described in this prospectus)). This presentation provides us and other interested third parties a consistent basis to better understand our operating results. This presentation is not in accordance with, or a substitute for, GAAP and may be different from, or inconsistent with, non-GAAP financial measures used by other companies. See Note 24 of the Notes to Consolidated Financial Statements for the year ended December 31, 2012 and Note 17 of the Notes to Unaudited Condensed Consolidated Financial Statements for the six months ended June 30, 2013 in each case, included elsewhere in this prospectus, for reconciliations of segment information on a historical accounting basis to consolidated financial statement amounts.

We present income (loss) before provision for (benefit from) income taxes—historical basis of accounting, as described under “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” as a non-GAAP financial measure in this prospectus. Income (loss) before provision for (benefit from) income taxes—historical basis of accounting is a non-GAAP measure and should be considered in addition to, but not as a substitute for or superior to, operating income, net income, operating cash flow and other measures of financial performance prepared in accordance with GAAP. Under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” herein, we include a quantitative reconciliation from our income (loss) before provision for (benefit from) income taxes on a push-down accounting basis to income (loss) before provision for (benefit from) income taxes—historical accounting basis.

ii

Table of Contents

This summary highlights information contained elsewhere in this prospectus. It may not contain all the information that may be important to you. You should read this entire prospectus carefully, including the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and the related notes included elsewhere in this prospectus, before making a decision to purchase our common stock. Some information in this prospectus contains forward-looking statements. See “Forward-Looking Statements.”

Springleaf Holdings, Inc. (“SHI”) is a newly-formed Delaware corporation that has not, to date, conducted any activities other than those incident to its formation and the preparation of the registration statement of which this prospectus forms a part. Unless the context suggests otherwise, references in this prospectus to “Springleaf,” the “Company,” “we,” “us,” and “our” refer to Springleaf Finance, Inc. (“SFI”) and its consolidated subsidiaries prior to the consummation of the Restructuring (as defined below), and to SHI and its consolidated subsidiaries after the consummation of the Restructuring. References in this prospectus to “Fortress” refer to Fortress Investment Group LLC. All amounts in this prospectus are expressed in U.S. dollars, except where noted, and the financial statements have been prepared in accordance with GAAP.

Business Overview

Springleaf is a leading consumer finance company providing responsible loan products to customers through our nationwide branch network and through iLoan, our internet lending division. We have a nearly 100-year track record of high quality origination, underwriting and servicing of personal loans, primarily to non-prime consumers. Our deep understanding of local markets and customers, together with our proprietary underwriting process and data analytics, allow us to price, manage and monitor risk effectively through changing economic conditions. With an experienced management team, a strong balance sheet, proven access to the capital markets and strong demand for consumer credit, we believe we are well positioned for future growth.

We staff each of our 834 branch offices with local, well-trained personnel who have significant experience in the industry and with Springleaf. Our business model revolves around an effective origination, underwriting and servicing process that leverages each branch office’s local presence in these communities along with the personal relationships developed with our customers. Credit quality is also driven by our long-standing underwriting philosophy, which takes into account each prospective customer’s household budget, and his or her willingness and capacity to repay the loan. Our extensive network of branches and expert personnel is complemented by our internet lending division, known as iLoan. Formed at the beginning of this year, our iLoan division allows us to reach customers located outside our branch footprint and to more effectively process applications from customers within our branch footprint who prefer the convenience of online transactions.

In connection with our personal loan business, our two captive insurance subsidiaries offer our customers credit and non-credit insurance policies covering our customers and the property pledged as collateral for our personal loans.

In addition, we pursue strategic acquisitions of loan portfolios through our Springleaf Acquisitions division, which we service through our centralized servicing operation. As part of this strategy, we recently acquired, through a joint venture in which we own a 47% equity interest, a $3.9 billion consumer loan portfolio from HSBC Finance Corporation and certain of its affiliates (collectively, “HSBC”), which we refer to as the “SpringCastle Portfolio.” Through the acquisition of the SpringCastle Portfolio and other similar acquisitions, we expect to achieve a meaningful return on our investment as well as receive a stable servicing fee income stream. We also intend to pursue fee-based opportunities in servicing loans for others through our centralized servicing operation.

1

Table of Contents

Industry and Market Overview

We operate in the consumer finance industry serving the large and growing population of consumers who have limited access to credit from banks, credit card companies and other lenders. According to Experian PLC, as of June 30, 2013, the U.S. consumer finance industry has grown to approximately $2.9 trillion of outstanding borrowings in the form of personal loans, vehicle loans and leases, credit cards, home equity lines of credit and student loans. According to the Federal Deposit Insurance Corporation, there were approximately 51 million adults living in under-banked households in the United States in 2011. Furthermore, difficult economic conditions in recent years have resulted in an increase in the number of non-prime consumers in the United States.

This industry’s traditional lenders have recently undergone fundamental changes, forcing many to retrench and in some cases to exit the market altogether. Tightened credit requirements imposed by banks, credit card companies, and other traditional lenders that began during the recession of 2008-2009 have further reduced the supply of consumer credit for non-prime borrowers. In addition, we believe that recent regulatory developments create a dis-incentive for these lenders to resume or support these lending activities. As a result, while the number of non-prime consumers in the United States has grown in recent years, the supply of consumer credit to this demographic has contracted. We believe this large and growing number of potential customers in our target market, combined with the decline in available consumer credit, provides an attractive market opportunity for our business model.

Installment lending to non-prime consumers is one of the most highly fragmented sectors of the consumer finance industry. We believe that installment loans made by competitors that we track are presently provided through approximately 5,000 individually-licensed finance company branches in the United States. We are one of the few remaining national participants in the consumer installment lending industry still servicing this large and growing population of non-prime customers. Our iLoan division, combined with the capabilities resident in our national branch system, provides an effective nationwide platform to efficiently and responsibly address this growing market of consumers. We believe we are, therefore, well-positioned to capitalize on the significant growth and expansion opportunity created by the large supply-demand imbalance within our industry.

Competitive Strengths

Extensive Branch Network. We believe that our branch network is a major competitive advantage and distinguishes us from our competitors. We operate one of the largest consumer finance branch networks in the United States, serving our customers through 834 branches in 26 states. Our branch network is the foundation of our relationship-driven business model and is the product of decades of thoughtful market identification and profitability analysis. It provides us with a proven distribution channel for our personal loan and insurance products, allowing us to provide same-day fulfillment to approved customers and giving us a distinct competitive advantage over many industry participants who do not have—and cannot replicate without significant investment—a similar nationwide footprint.

High Quality Underwriting Supported by Proprietary Analytics. Our branch managers have on average 12 years of experience with us and, together with their branch staff, have substantial local market knowledge and experience to complement their long-term relationships with millions of our current and former customers. We believe the loyalty and tenure of our employees have allowed us to build a consistent and deeply-engrained underwriting culture that produces consistently well-underwritten loans. In addition, we support and leverage the knowledge that our employees have accumulated about our customers through our proprietary technology, data analytics and decisioning tools, which enhance the quality of our lending and servicing processes. Since the decentralized branch network introduces the potential for greater variation in the application of the Company’s underwriting guidelines, we place district and regional managers in the field to review branch loan underwriting decisions to minimize variations among branches and reduce the potential for heightened delinquencies and charge-offs.

2

Table of Contents

High-Touch Relationship-Based Servicing. Our extensive branch network enables high-touch, relationship-based loan servicing, which we believe is a major component of superior loan performance. Our branch office employees typically live and work in the communities they serve and are often on a first-name basis with our customers. We believe that this high-touch, relationship-based servicing model distinguishes us from our competitors and allows us to react more quickly and efficiently in the event a borrower shows signs of financial or other distress.

Industry-Leading Loan Performance. We believe that we have historically experienced lower default and delinquency rates than the non-prime consumer finance industry as a whole. This superior level of loan performance has been achieved through the consistent application of time-tested underwriting standards, leveraging the relationships between our branch employees and our customers, and fostering a business owner mindset among our branch managers. In addition, we utilize highly effective, internally developed proprietary risk scoring models and monitoring systems. These models and systems have been developed using performance and customer data from our long history of lending to millions of consumers.

Proven Access to Diversified Funding Sources. We have the proven ability to finance our businesses from a diversified source of capital and funding, including cash flow from operations and financings in the capital markets in the form of personal loan and mortgage loan securitizations. Earlier this year we demonstrated the ability to attract capital markets funding for our personal loan business by completing two securitizations, a first for our industry in 15 years. We expect to continue to expand this securitization program that locks in our funding for loan originations for multiple years. Over the last several years, we have also demonstrated the ability to replace maturing unsecured debt with lower-cost, non-recourse securitization debt backed by our legacy real estate loan portfolio. We further expanded our available financing alternatives in May 2013 by re-entering the unsecured debt market, our first unsecured note issuance in six years. In addition, we have significant unencumbered assets to support future corporate lines of credit giving us added financial flexibility. Finally, we have one of the largest equity capital bases of any U.S. consumer finance company not affiliated with a bank or an auto or equipment manufacturer, which positions us well to continue the growth in our business and to make appropriate investments in technology, compliance and data analytics.

Experienced Management Team. Our management team consists of highly talented individuals with significant experience in the consumer finance industry. Their industry experience and complementary backgrounds have enabled us to grow revenue from our Core Consumer Operations (defined in “—Summary Historical Consolidated Financial Data”) by 63% during the first half of 2013 compared to the same period in 2012. Our Chief Executive Officer, Jay Levine, has 29 years of experience in the finance industry, and our senior management team has on average over 25 years of experience across the financial services and consumer finance industries.

Our Strategy

The retreat of banks and other consumer finance companies from the non-prime consumer lending industry positions us as one of the few remaining large independent consumer finance companies able to capitalize on those opportunities. We intend to grow our consumer loan portfolio, expand our products and channels and develop additional portfolio acquisition and servicing fee opportunities. Our growth strategy centers around three broad initiatives:

Drive Revenue Growth through our Extensive Branch Network. We intend to continue increasing same-store revenues by capitalizing on opportunities to offer our existing customers new products as their credit needs evolve and by refining our existing marketing programs and actively developing new marketing channels, particularly online search and social media. We will continue to expand “turn-down” programs with higher credit-tier lenders to refer to us certain applicants who do not meet the requirements of their underwriting programs, and we will continue growing our successful merchant referral program under which we provide an incentive to retailers for referring customers to us for loans to purchase goods or services.

3

Table of Contents

Drive Revenue Increases through New Channels and Acquisitions. Through the introduction of new channels and portfolio acquisitions, we seek to grow our loan originations and revenue.

| — | Internet Lending. In 2013, we expanded our business model and began originating personal loans on a centralized basis through iLoan, our internet lending division, which allows us to reach customers outside of our current geographic footprint. In addition to reaching new customers, the internet channel allows us to more effectively serve customers who are accustomed to the convenience of online transactions. Once fully developed, we expect iLoan to be able to provide internet lending access on a 24/7 basis in 46 states. |

| — | Portfolio Acquisitions. To build our consumer loan portfolio beyond our branch and internet businesses, we formed Springleaf Acquisitions, a separate division focused on the strategic acquisition of consumer loan portfolios that meet our investment return thresholds. We have a broad range of relationships with institutional sellers, Wall Street intermediaries and financial sponsors, including Fortress, through which we receive numerous requests to review potential acquisition opportunities. We expect to make additional acquisitions similar to our recent acquisition of the $3.9 billion SpringCastle Portfolio. |

Pursue Fee Income Opportunities. Our centralized servicing operation, known as Springleaf Servicing Solutions, gives us a dynamic platform covering all 50 states with which to pursue additional fee opportunities servicing the loans of others. We believe we are among a few platforms with nation-wide coverage offering third-party fee-based servicing for consumer loans. With the increasing cost of regulatory compliance in the consumer finance sector, we expect smaller third-party servicers will be challenged to make the necessary investments in technology and compliance. Finally, by combining the capital commitment capability of Springleaf Acquisitions with the servicing capability of Springleaf Servicing Solutions, we are able to offer third parties a greater alignment of interests. We expect, therefore, to be able to leverage our recent SpringCastle Portfolio acquisition into additional servicing fee opportunities.

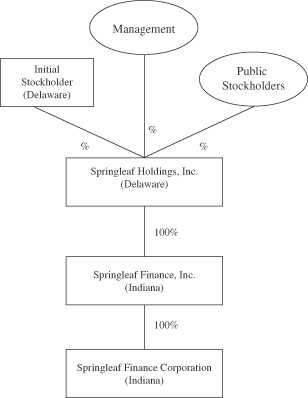

Our History and Corporate Information

In November 2010, an affiliate of Fortress indirectly acquired an 80% economic interest in SFI from an affiliate of American International Group, Inc. (“AIG”). This transaction is referred to in this prospectus as the Fortress Acquisition. AIG indirectly retained a 20% economic interest in SFI. All of the common stock of Springleaf Finance Corporation (“SFC”) is owned by SFI.

SFC was incorporated in Indiana in 1927 as successor to a business started in 1920. SFI was incorporated in Indiana in 1974. SHI (currently named Springleaf Holdings, LLC) was recently organized in Delaware for the purpose of effecting this offering. Prior to the completion of this offering, through a series of restructuring transactions, Springleaf Financial Holdings, LLC (the “Initial Stockholder”) and certain of our executive officers (the “selling stockholders”) will own 100% of the equity interests in SHI, the issuer of the common stock offered hereby, and SHI will own 100% of the equity interests of SFI (the “Restructuring”).

As part of a strategic effort to reposition the company and to renew focus on the personal loan business, we initiated a number of restructuring activities during the first half of 2012, including the following: (1) ceased originating real estate loans nationwide and in the United Kingdom; (2) ceased retail sales financing; (3) consolidated certain branch operations resulting in closure of 231 branch offices. As a result of these initiatives, we reduced our workforce in our branch operations and at our Evansville, Indiana headquarters, and operations in the United Kingdom by 820 employees.

4

Table of Contents

Our executive offices are located at 601 N.W. Second Street, Evansville, Indiana 47708, and our telephone number is (812) 424-8031. Our website address is www.SpringleafFinancial.com. The information on our website is not a part of this prospectus.

Our Principal Stockholders

Immediately following the completion of this offering, the Initial Stockholder will own approximately % of our outstanding common stock, or % if the underwriters’ over-allotment option is fully exercised. This level of share ownership is sufficient to control the vote on matters and transactions requiring stockholder approval. The Initial Stockholder is owned primarily by a private equity fund managed by an affiliate of Fortress, a leading global investment manager that offers alternative and traditional investment products, and by a subsidiary of AIG. See “Risk Factors—Risks Related to Our Organization and Structure” and “Principal Stockholder.”

Ownership Structure

Set forth below is the ownership structure of Springleaf Holdings, Inc. and its subsidiaries upon consummation of the Restructuring and this offering.

5

Table of Contents

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL DATA

The following tables summarize the consolidated financial information of SFI. SHI is a newly-formed Delaware corporation that has not, to date, conducted any activities other than those incident to its formation and the preparation of the registration statement of which this prospectus forms a part, which have been deemed immaterial and therefore are not presented in the summary historical consolidated financial data. Upon completion of the Restructuring, SHI will own 100% of the equity interests in SFI. The summary consolidated statement of operations data for the eleven months ended November 30, 2010, for the one month ended December 31, 2010 and for the years ended December 31, 2011 and 2012 and the summary consolidated balance sheet data as of December 31, 2011 and 2012 have been derived from our audited financial statements included elsewhere in this prospectus. The consolidated balance sheet data as of December 31, 2010 has been derived from our audited financial statements not included in this prospectus. The summary consolidated statement of operations data for the six months ended June 30, 2012 and 2013 and the summary consolidated balance sheet data as of June 30, 2013 have been derived from our unaudited financial statements included elsewhere in this prospectus.

The unaudited financial statements have been prepared on the same basis as the audited financial statements and, in the opinion of our management, include all adjustments necessary for a fair presentation of the information set forth herein. Operating results for the six months ended June 30, 2013 are not necessarily indicative of the results that may be expected for the year ending December 31, 2013 or for any future period. Results for the six months ended June 30, 2013 include the SpringCastle Portfolio, which we acquired on April 1, 2013 through a newly-formed joint venture in which we own a 47% equity interest and consolidate in our financial statements. The summary financial data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our audited and unaudited consolidated financial statements and related notes included elsewhere in this prospectus.

As a result of the Fortress Acquisition, a new basis of accounting was established and, for accounting purposes, the old entity (the “Predecessor Company”) was terminated and a new entity (the “Successor Company”) was created. This distinction is made throughout this prospectus through the inclusion of a vertical black line between the Successor Company and the Predecessor Company columns. Due to the nature of the Fortress Acquisition, we revalued our assets and liabilities based on their fair values at the date of the Fortress Acquisition in accordance with business combination accounting standards (“push-down accounting”), which resulted in a $1.5 billion bargain purchase gain for the one month ended December 31, 2010. Push-down accounting also affected and continues to affect, among other things, the carrying amount of our finance receivables and long-term debt, our finance charges on our finance receivables and related yields, our interest expense, our allowance for finance receivable losses, and our net charge-off and charge-off ratio. In general, on a quarterly basis, we accrete or amortize the valuation adjustment recorded in connection with the Fortress Acquisition, or record adjustments based on current expected cash flows as compared to expected cash flows at the time of the Fortress Acquisition, in each case, as described in more detail in the footnotes to the tables below and in the Notes to Consolidated Financial Statements for the year ended December 31, 2012 included elsewhere in this prospectus.

The financial information for 2010 includes the financial information of the Successor Company for the one month ended December 31, 2010 and of the Predecessor Company for the eleven months ended November 30, 2010. These separate periods are presented to reflect the new accounting basis established for our Company as of November 30, 2010.

As a result of the application of push-down accounting, the assets and liabilities of the Successor Company are not comparable to those of the Predecessor Company, and the income statement items for the one month ended December 31, 2010 and the years ended December 31, 2011 and 2012 would not have been the same as those reported if push-down accounting had not been applied. In addition, key ratios of the Successor Company are not comparable to those of the Predecessor Company, and are not comparable to other institutions due to the new accounting basis established.

6

Table of Contents

The pro forma share information in this table includes the effect of a -for-1 stock split to be effected immediately prior to the pricing of the offering.

| Successor Company | Predecessor Company |

|||||||||||||||||||||||

| Six Months Ended June 30, |

Year

Ended December 31, |

One

Month Ended December 31, 2010 |

Eleven Months Ended November 30, 2010 |

|||||||||||||||||||||

| 2013 | 2012 | 2012 | 2011 | |||||||||||||||||||||

| (in thousands, except share data) | ||||||||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||||||

| Interest income |

$993,634 | $864,313 | $1,706,292 | $1,885,547 | $181,329 | $1,688,720 | ||||||||||||||||||

| Interest expense |

468,926 | 560,273 | 1,068,391 | 1,268,047 | 118,693 | 996,469 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net interest income |

524,708 | 304,040 | 637,901 | 617,500 | 62,636 | 692,251 | ||||||||||||||||||

| Provision for finance receivable losses |

182,938 | 136,939 | 338,219 | 332,848 | 38,767 | 444,349 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net interest income after provision for finance receivable losses |

341,770 | 167,101 | 299,682 | 284,652 | 23,869 | 247,902 | ||||||||||||||||||

| Other revenues |

95,126 | 47,892 | 94,203 | 138,159 | 31,812 | 224,422 | ||||||||||||||||||

| Other expenses |

310,369 | 356,480 | 700,741 | 746,016 | 61,976 | 737,052 | ||||||||||||||||||

| Bargain purchase gain |

— | — | — | — | 1,469,182 | — | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Income (loss) before provision for (benefit from) income taxes |

126,527 | (141,487 | ) | (306,856 | ) | (323,205 | ) | 1,462,887 | (264,728 | ) | ||||||||||||||

| Provision for (benefit from) income taxes |

27,708 | (48,481 | ) | (88,222 | ) | (99,049 | ) | (1,388 | ) | (250,697 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net income (loss) |

98,819 | (93,006 | ) | (218,634 | ) | (224,156 | ) | 1,464,275 | (14,031 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Less: Net income attributable to non-controlling interests |

53,948 | — | — | — | — | — | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net income (loss) attributable to Springleaf |

$44,871 | $(93,006 | ) | $(218,634 | ) | $(224,156 | ) | $1,464,275 | $(14,031 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Share Data: |

||||||||||||||||||||||||

| Number of shares outstanding |

||||||||||||||||||||||||

| Basic and diluted |

2,000,000 | 2,000,000 | 2,000,000 | 2,000,000 | 2,000,000 | 2,000,000 | ||||||||||||||||||

| Earnings (loss) per share |

||||||||||||||||||||||||

| Basic and diluted |

$22.44 | $(46.50 | ) | $(109.32 | ) | $(112.08 | ) | $732.14 | $(7.02 | ) | ||||||||||||||

| Pro forma Share Data(1): |

||||||||||||||||||||

| Number of shares outstanding |

||||||||||||||||||||

| Basic and diluted |

||||||||||||||||||||

| Earnings (loss) per share |

||||||||||||||||||||

| Basic and diluted |

||||||||||||||||||||

| Successor Company | ||||||||||||||||||||

| June

30, 2013 |

December 31, | |||||||||||||||||||

| 2012 | 2011 | 2010 | ||||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| Balance Sheet Data: |

||||||||||||||||||||

| Net finance receivables, net of allowance |

$14,056,498 | $11,633,366 | $13,098,754 | $14,352,518 | ||||||||||||||||

| Cash and cash equivalents |

646,372 | 1,554,348 | 689,586 | 1,397,563 | ||||||||||||||||

| Total assets |

16,042,293 | 14,673,515 | 15,494,888 | 18,260,950 | ||||||||||||||||

| Long-term debt* |

13,470,413 | 12,596,577 | 13,070,393 | 15,168,034 | ||||||||||||||||

| Total liabilities |

14,318,567 | 13,473,388 | 14,131,984 | 16,650,652 | ||||||||||||||||

| Springleaf shareholder’s equity |

1,238,216 | 1,200,127 | 1,362,904 | 1,610,298 | ||||||||||||||||

| Non-controlling interests |

485,510 | — | — | — | ||||||||||||||||

| Total equity |

1,723,726 | 1,200,127 | 1,362,904 | 1,610,298 | ||||||||||||||||

7

Table of Contents

| * | Long-term debt comprises the following: |

| June

30, 2013 |

December 31, | |||||||||||||||

| 2012 | 2011 | 2010 | ||||||||||||||

| (in thousands) | ||||||||||||||||

| Long-term debt: |

||||||||||||||||

| Secured term loan |

$2,042,370 | $3,765,249 | $3,768,257 | $3,033,185 | ||||||||||||

| Securitization debt: |

||||||||||||||||

| Real estate |

3,528,440 | 3,120,599 | 1,385,847 | 1,526,770 | ||||||||||||

| Consumer |

823,003 | — | — | — | ||||||||||||

| SpringCastle Portfolio |

2,018,486 | — | — | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total securitization debt |

6,369,929 | 3,120,599 | 1,385,847 | 1,526,770 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Retail notes |

413,434 | 522,416 | 587,219 | 815,437 | ||||||||||||

| Medium-term notes |

4,064,927 | 4,162,674 | 5,999,325 | 7,850,175 | ||||||||||||

| Euro denominated notes |

408,195 | 854,093 | 1,158,223 | 1,770,965 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total unsecured senior debt |

4,886,556 | 5,539,183 | 7,744,767 | 10,436,577 | ||||||||||||

| Junior subordinated debt |

171,558 | 171,546 | 171,522 | 171,502 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$13,470,413 | $12,596,577 | $13,070,393 | $15,168,034 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Successor Company | Predecessor Company |

|||||||||||||||||||||||

| Six Months

Ended June 30, |

Year

Ended December 31, |

One

Month Ended December 31, 2010 |

Eleven Months Ended November 30, 2010 |

|||||||||||||||||||||

| 2013 | 2012 | 2012 | 2011 | |||||||||||||||||||||

| (in thousands) | ||||||||||||||||||||||||

| Other Financial Data: |

||||||||||||||||||||||||

| Cash flows from operating activities |

$118,888 | $163,976 | $215,898 | $180,606 | $(110,808 | ) | $383,554 | |||||||||||||||||

| Cash flows from investing activities |

(2,249,594 | ) | 657,350 | 1,433,964 | 1,540,673 | 140,994 | 3,198,343 | |||||||||||||||||

| Cash flows from financing activities |

1,224,248 | (92,163 | ) | (788,049 | ) | (2,430,367 | ) | (122,712 | ) | (3,402,963 | ) | |||||||||||||

8

Table of Contents

As of June 30, 2013, our segments include: Consumer, Insurance, Portfolio Acquisitions and Real Estate. Management considers Consumer, Insurance, and Portfolio Acquisitions to be our Core Consumer Operations and Real Estate as our Non-Core Portfolio.

| At or for the Six Months Ended June 30, |

At or for the Year Ended December 31, | |||||||||||||||||||

| 2013 | 2012 | 2012 | 2011 | 2010 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| Selected Data—Historical Accounting Basis:(2) |

||||||||||||||||||||

| Core Consumer Operations |

||||||||||||||||||||

| Pretax core earnings (loss)(3) |

$164,746 | $39,159 | $87,847 | $47,439 | $(50,099 | ) | ||||||||||||||

| Consumer |

||||||||||||||||||||

| Pretax operating income (loss) |

$92,755 | $2,077 | $33,461 | $33,621 | $(107,097 | ) | ||||||||||||||

| Average net finance receivables—personal |

2,609,480 | 2,366,672 | 2,426,968 | 2,337,210 | 2,527,999 | |||||||||||||||

| Yield |

25.49 | % | 23.75 | % | 24.10 | % | 22.88 | % | 21.70 | % | ||||||||||

| Gross charge-off ratio(4) |

5.50 | % | 4.39 | % | 4.63 | % | 5.09 | % | 7.26 | % | ||||||||||

| Recovery ratio(5) |

(3.22 | )% | (1.30 | )% | (0.99 | )% | (1.14 | )% | (1.12 | )% | ||||||||||

| Net charge-off ratio(4)(5) |

2.28 | % | 3.09 | % | 3.64 | % | 3.95 | % | 6.14 | % | ||||||||||

| Delinquency ratio(6) |

1.92 | % | 2.43 | % | 2.75 | % | 2.98 | % | 3.67 | % | ||||||||||

| Insurance |

||||||||||||||||||||

| Pretax operating income |

$24,415 | $23,861 | $44,402 | $53,753 | $56,998 | |||||||||||||||

| Portfolio Acquisitions |

||||||||||||||||||||

| Pretax operating income |

$100,024 | N/A | N/A | N/A | N/A | |||||||||||||||

| Pretax operating income attributable to Springleaf |

46,076 | N/A | N/A | N/A | N/A | |||||||||||||||

| Average net finance receivables—SpringCastle Portfolio |

2,865,605 | N/A | N/A | N/A | N/A | |||||||||||||||

| Yield |

23.31 | % | N/A | N/A | N/A | N/A | ||||||||||||||

| Net charge-off ratio |

2.48 | % | N/A | N/A | N/A | N/A | ||||||||||||||

| Delinquency ratio |

4.70 | % | N/A | N/A | N/A | N/A | ||||||||||||||

| Non-Core Portfolio |

||||||||||||||||||||

| Real Estate |

||||||||||||||||||||

| Pretax operating loss |

$(137,760 | ) | $(90,038 | ) | $(64,060 | ) | $(257,203 | ) | $(230,981 | ) | ||||||||||

| Average net finance receivables — real estate |

10,245,790 | 11,510,840 | 11,183,176 | 12,596,103 | 13,974,060 | |||||||||||||||

| Provision for finance receivable losses(7) |

149,624 | 81,545 | 51,130 | 249,268 | 315,018 | |||||||||||||||

| Loss ratio(8) |

2.13 | % | 2.80 | % | 2.73 | % | 3.22 | % | 3.39 | % | ||||||||||

| Total Company (including non-controlling interests) |

||||||||||||||||||||

| Income (loss) before provision for (benefit from) income taxes(2) |

$84,300 | $(73,263 | ) | $(53,387 | ) | $(164,053 | ) | $(288,474 | ) | |||||||||||

Notes:

| (1) | Pro forma Share Data gives retroactive effect to the contemplated -for-1 stock split to be effected immediately prior to the pricing of the offering. |

9

Table of Contents

| (2) | Historical accounting basis is a non-GAAP measure using the same accounting basis that we employed prior to the Fortress Acquisition. Due to the nature of the Fortress Acquisition, we revalued our assets and liabilities based on their fair values at November 30, 2010, the date of the Fortress Acquisition. This revaluation continues to affect, among other things, interest income, interest expense, provision for finance receivable losses and amortization of other intangible assets. This historical accounting basis presentation provides us and other interested third parties a consistent basis to better understand our operating results. This measure is not in accordance with, or a substitute for, GAAP and may be different from, or inconsistent with, non-GAAP financial measures used by other companies. See Note 24 of the Notes to Consolidated Financial Statements for the year ended December 31, 2012 and Note 17 of the Notes to Unaudited Condensed Consolidated Financial Statements for the six months ended June 30, 2013, included elsewhere in this prospectus, for reconciliations of segment information on a historical accounting basis to consolidated financial statement amounts. |

| The following is a reconciliation of income (loss) before provision for (benefit from) income taxes from push-down accounting basis to the historical accounting basis. |

| Successor Company | Predecessor Company |

|||||||||||||||||||||||

| Six Months Ended June 30, |

Year Ended December 31, |

One Month Ended December 31, 2010 |

Eleven Months Ended November 30, 2010 |

|||||||||||||||||||||

| 2013 | 2012 | 2012 | 2011 | |||||||||||||||||||||

| (in thousands) | ||||||||||||||||||||||||

| Income (loss) before provision for (benefit from) income taxes—push-down accounting basis |

$126,527 | $(141,487 | ) | $(306,856 | ) | $(323,205 | ) | $1,462,887 | $(264,728 | ) | ||||||||||||||

| Adjustments: |

||||||||||||||||||||||||

| Interest income |

(103,532 | ) | (94,590 | ) | (197,981 | ) | (261,490 | ) | (36,663 | ) | — | |||||||||||||

| Interest expense |

70,187 | 125,238 | 220,969 | 339,022 | 28,809 | — | ||||||||||||||||||

| Provision for finance receivable losses |

7,250 | 22,023 | 185,859 | 79,287 | (1,488 | ) | — | |||||||||||||||||

| Repurchases and repayments of long-term debt |

(21,316 | ) | 10,967 | 39,411 | — | — | — | |||||||||||||||||

| Amortization of other intangible assets |

2,718 | 5,555 | 13,618 | 41,085 | 3,797 | — | ||||||||||||||||||

| Bargain purchase gain |

— | — | — | — | (1,469,182 | ) | — | |||||||||||||||||

| Other |

2,466 | (969 | ) | (8,407 | ) | (38,752 | ) | (11,906 | ) | — | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Income (loss) before provision for (benefit from) income taxes – historical accounting basis |

$84,300 | $(73,263 | ) | $(53,387 | ) | $(164,053 | ) | $(23,746 | ) | $(264,728 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

10

Table of Contents

| (3) | The following is a reconciliation from income (loss) before provision for (benefit from) income taxes on a historical accounting basis to pretax core earnings (loss): |

| Six Months Ended June 30, | Year Ended December 31, | |||||||||||||||||||

| 2013 | 2012 | 2012 | 2011 | 2010 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| Income (loss) before provision for (benefit from) income taxes—historical accounting basis |

$84,300 | $(73,263 | ) | $(53,387 | ) | $(164,053 | ) | $(288,474 | ) | |||||||||||

| Adjustments: |

||||||||||||||||||||

| Pretax operating loss—Non-Core Portfolio |

137,760 | 90,038 | 64,060 | 257,203 | 230,981 | |||||||||||||||

| Pretax operating (income) loss—Other/non-originating legacy operations |

(4,866 | ) | 9,163 | 67,190 | (5,776 | ) | 7,394 | |||||||||||||

| Restructuring expenses—Core Consumer Operations |

— | 15,863 | 15,863 | — | — | |||||||||||||||

| (Gain) loss from accelerated repayment/repurchase of debt—Consumer |

1,500 | (2,642 | ) | (5,879 | ) | — | — | |||||||||||||

| Impact from change in accounting estimate—Consumer(a) |

— | — | — | (39,935 | ) | — | ||||||||||||||

| Pretax operating income attributable to non-controlling interests |

(53,948 | ) | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Pretax core earnings (loss) |

$164,746 | $39,159 | $87,847 | $47,439 | $(50,099 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (a) | Impact from change in accounting estimate – Consumer represents a change from a migration analysis to a roll rate-based model for purposes of calculating allowance for finance receivable losses for the Consumer segment. |

| Pretax core earnings (loss) is a key performance measure used by management in evaluating the performance of our Core Consumer Operations. Pretax core earnings (loss) represents our income (loss) before provision for (benefit from) income taxes on a historical accounting basis and excludes results of operations from our non-core portfolio (Real Estate segment) and other non-originating legacy operations, restructuring expenses related to Consumer and Insurance segments, gains (losses) associated with accelerated long-term debt repayment and repurchases of long-term debt, impact from change in accounting estimate and results of operations attributable to non-controlling interests. Pretax core earnings (loss) provides us with a key measure of our Core Consumer Operations’ performance as it assists us in comparing its performance on a consistent basis. Management believes pretax core earnings (loss) is useful in assessing the profitability of our core business and uses pretax core earnings (loss) in evaluating our operating performance. Pretax core earnings (loss) is a non-GAAP measure and should be considered in addition to, but not as a substitute for or superior to, operating income, net income, operating cash flow and other measures of financial performance prepared in accordance with GAAP. |

| (4) | Represents annualized charge-offs as a percentage of the average of net finance receivables at the beginning of each month in the period—Consumer. Reflects $14.5 million of additional charge-offs recorded in March 2013 (on a historical accounting basis) related to our change in charge-off policy for personal loans effective March 31, 2013. Excluding these additional charge-offs, our Consumer segment gross charge-off ratio would have been 4.39% for the six months ended June 30, 2013. |

| (5) | Reflects $25.4 million of recoveries on charged-off personal loans resulting from a sale of our charged-off finance receivables in June 2013. Excluding these recoveries, our Consumer segment recovery ratio would have been (1.28)% for the six months ended June 30, 2013. Excluding the impacts of the $14.5 million of additional charge-offs and the $25.4 million of recoveries on charged-off personal loans, our Consumer segment net charge-off ratio would have been 3.11% for the six months ended June 30, 2013. |

| (6) | Represents unpaid principal balance (“UPB”) of 60 days or more past due as a percentage of UPB. |

11

Table of Contents

| (7) | Reflects the impact from change in accounting estimate for the year ended December 31, 2012, from a switch from a migration analysis to a roll rate-based model for purposes of calculating allowance for finance receivable losses for the Real Estate segment. |

| (8) | Represents the sum of annualized net charge-offs, writedowns and net gain (loss) on sales of, and operating expenses related to real estate owned as a percentage of the average of net finance receivables—Real Estate. |

12

Table of Contents

The Offering

| Common stock we are offering |

shares. |

| Common stock the selling stockholders are offering |

shares |

| Common stock to be issued and outstanding after this offering |

shares ( shares if the underwriters exercise their over-allotment option in full). |

| Common stock to be owned by the Initial Stockholder after this offering |

shares ( shares if the underwriters exercise their over-allotment option in full). |

| Use of proceeds |

We currently intend to use the net proceeds from this offering to repay or repurchase outstanding indebtedness, which may include (i) our senior secured term loan facility, (ii) SFC’s 6.90% medium term notes, Series J, due 2017 or (iii) certain of our as yet unfunded private securitization transactions to the extent we draw down amounts thereunder, as well as other general corporate purposes, including originations of new personal loans and potential portfolio acquisitions, and to satisfy working capital obligations. We will not receive any proceeds from the sale of shares of common stock by the selling stockholders. |

| Dividend Policy |

We do not currently anticipate paying dividends on our common stock. Any declaration and payment of future dividends to holders of our common stock will be at the sole discretion of our board of directors and will depend on many factors, including our financial condition, earnings, capital requirements, level of indebtedness, statutory and contractual restrictions applicable to the payment of dividends and other considerations that our board of directors deems relevant. Because we are a holding company and have no direct operations, we will only be able to pay dividends from our available cash on hand and any funds we receive from our subsidiaries. Our insurance subsidiaries are subject to regulations that limit their ability to pay dividends or make loans or advances to us, principally to protect policyholders, and certain of our debt agreements limit the ability of certain of our subsidiaries to pay dividends. See “Dividend Policy.” |

| Risk factors |

See “Risk Factors” for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

| NYSE Symbol |

“LEAF.” |

13

Table of Contents

Except as otherwise indicated, all of the information in this prospectus:

| — | gives retroactive effect to a -for-1 stock split to be effected immediately prior to the pricing of the offering; |

| — | assumes no exercise of the underwriters’ option to purchase up to additional shares of common stock; and |

| — | assumes an initial offering price of $ per share, which is the midpoint of the offering price range set forth on the cover page of this prospectus. |

14

Table of Contents

Investing in our common stock involves a high degree of risk. You should carefully consider the following risk factors, as well as other information contained in this prospectus, before deciding to invest in our common stock. The occurrence of any of the following risks could materially and adversely affect our business, prospects, financial condition, results of operations and cash flow, in which case, the trading price of our common stock could decline and you could lose all or part of your investment.

Risks Relating to Our Business

Our consolidated results of operations and financial condition and our borrowers’ ability to make payments on their loans have been, and may in the future be, adversely affected by economic conditions and other factors that we cannot control.

Uncertainty and negative trends in general economic conditions in the United States and abroad, including significant tightening of credit markets and a general decline in the value of real property, historically have created a difficult operating environment for our businesses and other companies in our industries. Many factors, including factors that are beyond our control, may impact our consolidated results of operations or financial condition and/or affect our borrowers’ willingness or capacity to make payments on their loans. These factors include: unemployment levels, housing markets, energy costs and interest rates; events such as natural disasters, acts of war, terrorism, catastrophes, major medical expenses, divorce or death that affect our borrowers; and the quality of the collateral underlying our receivables. If we experience an economic downturn or if the U.S. economy is unable to continue or sustain its recovery from the most recent economic downturn, or if we become affected by other events beyond our control, we may experience a significant reduction in revenues, earnings and cash flows, difficulties accessing capital and a deterioration in the value of our investments. We may also become exposed to increased credit risk from our customers and third parties who have obligations to us.

Moreover, a substantial majority of our customers are subprime or non-prime borrowers. Accordingly, such borrowers have historically been, and may in the future become, more likely to be affected, or more severely affected, by adverse macroeconomic conditions. If our borrowers default under a finance receivable held directly by us, we will bear a risk of loss of principal to the extent of any deficiency between the value of the collateral, if any, and the outstanding principal and accrued but unpaid interest of the finance receivable, which could adversely affect our cash flow from operations. In addition, foreclosure of a real estate loan (part of our legacy real estate portfolio) is an expensive and lengthy process that can negatively affect our anticipated return on the foreclosed loan. The cost to service our loans may also increase without a corresponding increase in our finance charge income.

If aspects of our business, including the quality of our finance receivables portfolio or our borrowers, are significantly affected by economic changes or any other conditions in the future, we cannot be certain that our policies and procedures for underwriting, processing and servicing loans will adequately adapt to such changes. If we fail to adapt to changing economic conditions or other factors, or if such changes affect our borrowers’ willingness or capacity to repay their loans, our results of operations, financial condition and liquidity would be materially adversely affected.

As part of our growth strategy, we have committed to building our consumer lending business. If we are unable to successfully implement our growth strategy, our results of operations, financial condition and liquidity may be materially adversely affected.

We believe that our future success depends on our ability to implement our growth strategy, the key feature of which has been to shift our primary focus to originating consumer loans as well as acquiring portfolios of consumer loans, such as our SpringCastle Portfolio that we recently acquired through our Springleaf Acquisitions division. In connection with this revised focus, we have also recently expanded into internet lending through our iLoan division.

15

Table of Contents

We may not be able to implement our new strategy successfully, and our success depends on a number of factors, including, but not limited to, our ability to:

| — | address the risks associated with our new focus on personal loan receivables, including, but not limited to consumer demand for finance receivables, and changes in economic conditions and interest rates; |

| — | address the risks associated with the new centralized method of originating and servicing our internet loans through iLoan, which represents a departure from our traditional high-touch branch-based servicing function and includes the potential for higher default and delinquency rates; |

| — | integrate, and develop the expertise required to capitalize on, our iLoan internet lending division; |

| — | comply with regulations in connection with doing business and offering loan products over the internet, including various state and federal e-signature rules mandating that certain disclosures be made and certain steps be followed in order to obtain and authenticate e-signatures, with which we have limited experience; and |

| — | successfully source, underwrite and integrate new acquisitions of loan portfolios and of other businesses. |

In order for us to realize the benefits associated with our new focus on originating and servicing consumer loans and grow our business, we must implement our strategic objectives in a timely and cost-effective manner as well as anticipate and address any risks to which we may become subject. If we are not able to do so, or if we do not do so in a timely manner, our results of operations, financial condition and liquidity could be negatively affected which would have a material adverse effect on business.

We recently ceased real estate lending and the purchase of retail finance contracts and are in the process of liquidating these portfolios, which subjects us to certain risks which if we do not manage could adversely affect our results of operations, financial condition and liquidity.

In connection with our plan for strategic growth and new focus on consumer lending, we engaged in a number of restructuring initiatives, including but not limited to, ceasing real estate lending, ceasing purchasing retail sales contracts and revolving retail accounts from the sale of consumer goods and services by retail merchants, closing certain of our branches and reducing our workforce.

Since terminating our real estate lending business, which historically accounted for in excess of 50% of the interest income of our business, and ceasing retail sales purchases, we have begun the multi-year process of liquidating these legacy portfolios. However, notwithstanding our decision to exit real estate lending and retail sales and the liquidating status of these portfolios, as of June 30, 2013 we owned $9.9 billion in UPB of real estate loans. The continuation or worsening of volatility in residential real estate values could continue to adversely affect our business and results of operations, and such adverse conditions could result in significant write-downs in the future. Similarly, due to the fact that we are no longer able to offer our legacy real estate lending customers the same range of loan restructuring alternatives in delinquency situations that we may historically have extended to them, such customers may be less able, and less likely, to repay their loans.

We may be unable to efficiently manage our restructuring and the liquidation of our legacy portfolios. In particular, we may not achieve the cost-savings and operational synergies expected as a result of closing certain of our branches and reducing personnel. Similarly, we may be unable to originate or acquire new consumer loans via our branches and over the internet at a level that is sufficient to offset the impact that liquidating our real estate and retail sales portfolios may have on our financial condition. If we fail to realize the anticipated benefits of the restructuring of our business and associated liquidation of our legacy portfolios, we may experience an adverse effect on our results of operations, financial condition and liquidity.

16

Table of Contents

There are risks associated with the acquisition of large loan portfolios, such as the SpringCastle Portfolio, including the possibility of increased delinquencies and losses, difficulties with integrating the loans into our servicing platform and disruption to our ongoing business, which could have a material adverse effect on our results of operations, financial condition and liquidity.

On April 1, 2013, we acquired the SpringCastle Portfolio, a $3.9 billion consumer loan portfolio consisting of over 415,000 unsecured loans and loans secured by subordinate residential real estate mortgages (which we service as unsecured loans due to the fact that the liens are subordinated to superior ranking security interests). We acquired the portfolio from HSBC through a newly-formed joint venture in which we own a 47% equity interest. In the future, we may acquire additional large portfolios of finance receivables either through the direct purchase of such assets or the purchase of the equity of a company with such a portfolio. Since we will not have originated or serviced the loans we acquire, including the SpringCastle Portfolio, we may not be aware of legal or other deficiencies related to origination or servicing, and our review of the portfolio prior to purchase may not uncover those deficiencies. Further, we may have limited recourse against the seller of the portfolio.

The ability to integrate and service the SpringCastle Portfolio successfully will depend in large part on the success of our development and integration of expanded servicing capabilities, including additional personnel, with our current operations. Similar integration issues are likely to occur with future large portfolio acquisitions. We may fail to realize some or all of the anticipated benefits of the transaction if the integration process takes longer, or is more costly, than expected. Our failure to meet the challenges involved in successfully integrating the SpringCastle Portfolio with our current business or otherwise to realize any of the anticipated benefits of the transaction, could impair our operations. In addition, we anticipate that integration will be a complex, time-consuming and expensive process that, without proper planning and effective and timely implementation, could significantly disrupt our business.

Potential difficulties we may encounter during the integration process with the SpringCastle Portfolio or future acquisitions include, but are not limited to, the following:

| — | the integration of the portfolio into our information technology platforms and servicing systems; |

| — | the quality of servicing during any interim servicing period after we purchase the portfolio but before we assume servicing obligations from the seller or its agents; |

| — | the disruption to our ongoing businesses and distraction of our management teams from ongoing business concerns; |

| — | incomplete or inaccurate files and records; |

| — | the retention of existing customers; |

| — | the creation of uniform standards, controls, procedures, policies and information systems; |

| — | the occurrence of unanticipated expenses; and |

| — | potential unknown liabilities associated with the transactions, including legal liability related to origination and servicing prior to the acquisition. |

For example, it is possible that the SpringCastle Portfolio data we acquire upon assuming the direct servicing obligations for the loans may not transfer from the HSBC platform to our systems properly. This may result in data being lost, key information not being locatable on our systems, or the complete failure of the transfer. In addition, in some cases loan files and other information related to the SpringCastle Portfolio (including servicing records) are incomplete or inaccurate. If our employees are unable to access customer

17

Table of Contents

information easily, or if we are unable to produce originals or copies of documents or accurate information about the loans, collections could be affected significantly, and we may not be able to enforce our right to collect in some cases. Similarly, collections could be affected by any changes to our collections practices, the restructuring of any key servicing functions, transfer of files and other changes that occur as a result of the transfer of servicing obligations from HSBC to us.

The anticipated benefits and synergies from the acquisition and servicing of the SpringCastle Portfolio assume, and our future acquisitions will assume, a successful integration, and are or will be based on projections, which are inherently uncertain, as well as other assumptions. Even if integration is successful, anticipated benefits and synergies may not be achieved.

There are risks associated with our ability to expand our centralized loan servicing capabilities through the acquisition and integration of the servicing facility in London, Kentucky which could have a material adverse effect on our results of operations, financial condition and liquidity.

A key part of our efforts to expand our centralized loan servicing capacity will depend in large part on the success of management’s efforts to integrate the acquisition of a servicing facility in London, Kentucky that we acquired from a subsidiary of HSBC (the “Kentucky Facility”) on September 1, 2013 and its personnel with our current operations following the completion of the transaction. We may fail to realize some or all of the anticipated benefits of the transaction if the integration process takes longer, or is more costly, than expected. Our failure to meet the challenges involved in successfully integrating the Kentucky Facility with our current business or otherwise to realize any of the anticipated benefits of the transaction, including additional revenue opportunities, could impair our operations and our ability to support additional servicing requirements from acquisitions including our acquisition of the SpringCastle Portfolio. In addition, we anticipate that integration will be a complex, time-consuming and expensive process that, without proper planning and effective and timely implementation, could significantly disrupt our business. Potential difficulties we may encounter during the integration process may include, but are not limited to, the following:

| — | the integration of the personnel with certain of our management teams, strategies, operations, products and services; |

| — | the integration of the physical facilities with our information technology platforms and servicing systems; |

| — | the disruption to our ongoing businesses and distraction of our management teams from ongoing business concerns; and |

| — | the retention of key employees, especially former employees of the seller who are familiar with the portfolio and systems, along with the integration of corporate cultures and maintenance of employee morale. |

If our estimates of finance receivable losses are not adequate to absorb actual losses, our provision for finance receivable losses would increase, which would adversely affect our results of operations.

We maintain an allowance for finance receivable losses. To estimate the appropriate level of allowance for finance receivable losses, we consider known and relevant internal and external factors that affect finance receivable collectability, including the total amount of finance receivables outstanding, historical finance receivable charge-offs, our current collection patterns, and economic trends. Our methodology for establishing our allowance for finance receivable losses is based on the guidance in Accounting Standards Codification (ASC) 450 and, in part, on our historic loss experience. If customer behavior changes as a result of economic conditions and if we are unable to predict how the unemployment rate, housing foreclosures, and general economic uncertainty may affect our allowance for finance receivable losses, our provision may be inadequate. Our allowance for finance receivable losses is an estimate, and if actual finance receivable losses are materially greater than our

18

Table of Contents

allowance for finance receivable losses, our results of operations could be adversely affected. Neither state regulators nor federal regulators regulate our allowance for finance receivable losses. Additional information regarding our allowance for finance receivable losses is included in the section captioned “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Allowance for Finance Receivable Losses.”

Our risk management efforts may not be effective.

We could incur substantial losses and our business operations could be disrupted if we are unable to effectively identify, manage, monitor, and mitigate financial risks, such as credit risk, interest rate risk, prepayment risk, liquidity risk, and other market-related risks, as well as operational risks related to our business, assets and liabilities. To the extent our models used to assess the creditworthiness of potential borrowers do not adequately identify potential risks, the valuations produced would not adequately represent the risk profile of the borrower and could result in a riskier finance receivable profile than originally identified. Our risk management policies, procedures, and techniques, including our scoring technology, may not be sufficient to identify all of the risks we are exposed to, mitigate the risks we have identified or identify concentrations of risk or additional risks to which we may become subject in the future.

Our branch loan approval process is decentralized, which may result in variability of loan structures, and could adversely affect our results of operations, financial condition and liquidity.

Our branch finance receivable origination system is decentralized. We train our employees individually on-site in the branch to make loans that conform to our underwriting standards. Such training includes critical aspects of state and federal regulatory compliance, cash handling, account management and customer relations. Subject to approval by district managers and/or directors of operations in certain cases, our branch officers have the authority to approve and structure loans within broadly written underwriting guidelines rather than having all loan terms approved centrally. As a result, there may be variability in finance receivable structure (e.g., whether or not collateral is taken for the loan) and loan portfolios among branch offices or regions, even when underwriting policies are followed. Moreover, we cannot be certain that every loan is made in accordance with our underwriting standards and rules and we have in the past experienced some instances of loans extended that varied from our underwriting standards. The nature of our approval process could adversely affect our operating results and variances in underwriting standards and lack of supervision could expose us to greater delinquencies and charge-offs than we have historically experienced, which could adversely affect our results of operations, financial condition and liquidity.

Changes in market conditions, including rising interest rates, could adversely affect the rate at which our borrowers prepay their loans and the value of our finance receivables portfolio, as well as increase our financing cost, which could negatively affect our results of operations, financial condition and liquidity.