FORM 10-K

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

(Mark One)

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______________ to _______________ | |

Commission file number 1-36232

VALERO ENERGY PARTNERS LP

(Exact name of registrant as specified in its charter)

Delaware | 90-1006559 |

(State or other jurisdiction of | (I.R.S. Employer |

incorporation or organization) | Identification No.) |

One Valero Way | |||

San Antonio, Texas | 78249 | ||

(Address of principal executive offices) | (Zip Code) | ||

Registrant’s telephone number, including area code: (210) 345-2000 | |||

Securities registered pursuant to Section 12(b) of the Act: Common units representing limited partnership interests listed on the New York Stock Exchange.

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule12b-2 of the Exchange Act.

Large accelerated filer þ | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

The aggregate market value of the voting and non-voting common units held by non-affiliates was approximately $881.6 million based on the last sales price quoted as of June 30, 2015 on the New York Stock Exchange, the last business day of the registrant’s most recently completed second fiscal quarter.

The registrant had 36,534,211 common units, 28,789,989 subordinated units and 1,332,829 general partner units outstanding at February 1, 2016.

DOCUMENTS INCORPORATED BY REFERENCE

None

CONTENTS

PAGE | ||

i

References in this report to “Partnership,” “we,” “our,” “us,” or similar terms refer to Valero Energy Partners LP, one or more of its subsidiaries, or all of them taken as a whole. References to “our general partner” refer to Valero Energy Partners GP LLC, an indirect wholly owned subsidiary of Valero Energy Corporation. References to “Valero” refer to Valero Energy Corporation, one or more of its subsidiaries (other than Valero Energy Partners LP or Valero Energy Partners GP LLC), or all of them taken as a whole.

PART I

ITEMS 1 & 2. BUSINESS and PROPERTIES

BUSINESS

Overview

Valero Energy Partners LP is a Delaware limited partnership formed in July 2013. On December 16, 2013, we completed our initial public offering (the IPO) of 17,250,000 common units representing limited partner interests. Our common units are listed on the New York Stock Exchange (NYSE) under the symbol “VLP.” See Note 11 of Notes to Consolidated Financial Statements for further discussion of the IPO. Our company offices are located at One Valero Way, San Antonio, Texas 78249.

Our website address is www.valeroenergypartners.com. Information on our website is not part of this report. Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed with or furnished to the United States (U.S.) Securities and Exchange Commission (SEC) are available, free of charge, on our website (under Reports & SEC Filings), soon after we file or furnish such material.

We are a master limited partnership formed by Valero to own, operate, develop, and acquire crude oil and refined petroleum products pipelines, terminals, and other transportation and logistics assets. Our assets include crude oil and refined petroleum products pipeline and terminal systems in the U.S. Gulf Coast and U.S. Mid-Continent regions that are integral to the operations of the following Valero refineries:

• | Port Arthur Refinery–Port Arthur, Texas; |

• | McKee Refinery–Sunray, Texas; |

• | Three Rivers Refinery–Three Rivers, Texas; |

• | Memphis Refinery–Memphis, Tennessee; |

• | Ardmore Refinery–Ardmore, Oklahoma; |

• | St. Charles Refinery–Norco, Louisiana; |

• | Houston Refinery–Houston, Texas; and |

• | Corpus Christi East and West Refineries–Corpus Christi, Texas. |

We generate revenues by charging tariffs and fees for transporting crude oil and refined petroleum products through our pipelines and terminals. All of our revenues are derived from transactions with Valero. We expect Valero to serve as a critical source of our future growth by providing us opportunities to purchase additional transportation and logistics assets that Valero currently owns or may acquire or develop in the future. Our agreements with Valero are discussed more fully in other sections of this report.

1

Acquisitions in 2015

Effective March 1, 2015, we acquired two subsidiaries from Valero that own and operate crude oil, intermediates, and refined petroleum products terminals supporting Valero’s Houston and St. Charles Refineries (the Houston and St. Charles Terminal Services Business) for total consideration of $671.2 million.

Effective October 1, 2015, we acquired subsidiaries from Valero that own and operate crude oil, intermediates, and refined petroleum products terminals supporting Valero’s Corpus Christi East and Corpus Christi West Refineries (collectively, the Corpus Christi Terminal Services Business) for total consideration of $465.0 million.

In connection with these acquisitions, we issued common units and general partner units to Valero and entered into various agreements with Valero. These transactions and agreements are described further in Note 3 and Note 4 of Notes to Consolidated Financial Statements. The descriptions of these acquisitions and the related agreements in Notes 3 and 4 of Notes to Consolidated Financial Statements are incorporated herein by reference.

Other Developments

In November 2015, we amended and restated our senior unsecured revolving credit facility agreement (the Revolver) to, among other things, extend the maturity from December 2018 to November 2020 and increase the total commitment from $300.0 million to $750.0 million. See Note 7 of Notes to Consolidated Financial Statements for a summary of the terms of the Revolver.

During 2015, we entered into two subordinated credit agreements with Valero (the Loan Agreements) under which we borrowed $160.0 million and $395.0 million (collectively, the loans) to finance a portion of the acquisitions of the Houston and St. Charles Terminal Services Business and the Corpus Christi Terminal Services Business, respectively, as described in Note 3. The loans mature on March 1 and October 1, 2020, respectively, and may be prepaid at any time without penalty. See Note 7 of Notes to Consolidated Financial Statements for a summary of the terms of the Loan Agreements.

In November 2015, we completed a public offering (the 2015 Offering) of 4,250,000 common units at a price of $46.25 per unit and received gross proceeds of $196.6 million. After deducting the underwriting discount and other offering costs totaling $7.7 million, our net proceeds from the offering were $188.9 million. Concurrent with the offering, our general partner contributed $4.0 million in exchange for 86,735 general partner units to maintain its 2.0 percent general partner interest in the Partnership. In December 2015, we used $185.0 million of these proceeds to pay down one of our Loan Agreements as further described in Note 7 of Notes to Consolidated Financial Statements.

2

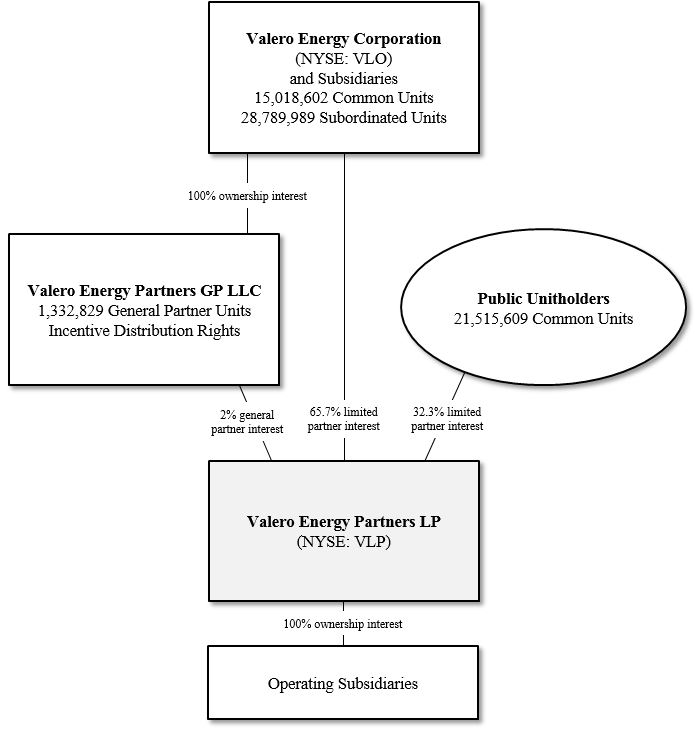

Organizational Structure

The following simplified diagram depicts our organizational structure as of February 1, 2016.

Segments

Our operations consist of one reportable segment and are conducted solely in the U.S. All of our assets are located in the U.S. See Item 8., “Financial Statements and Supplementary Data” for financial information about our operations and assets.

3

Our Assets and Operations

The following sections describe our assets and the related services that we provide.

Port Arthur Logistics System

Our Port Arthur logistics system includes our Lucas crude system and our Port Arthur products system.

Lucas Crude System. Our Lucas crude system supports diverse and flexible crude oil supply options for Valero’s Port Arthur Refinery. Our Lucas crude system comprises the following assets:

• | Lucas Terminal. Our Lucas terminal is located 12 miles from Valero’s Port Arthur Refinery on 495 acres. The facility consists of seven storage tanks with an aggregate of 1.9 million barrels of storage capacity. The Lucas terminal receives crude oil through our Nederland pipeline, which connects to the Sunoco Logistics Partners L.P. marine terminal in Nederland, Texas, as well as through connections to the Cameron Highway crude oil pipeline and Enterprise’s Beaumont marine terminal. The terminal connects to TransCanada’s Cushing MarketLink pipeline via our TransCanada connection and to the Seaway crude oil pipeline via our Seaway connection. The Lucas terminal delivers crude oil to Valero’s Port Arthur Refinery through our Lucas pipeline. |

• | Lucas Pipeline. Our Lucas pipeline is a 12-mile, 30-inch pipeline with 400,000 barrels per day of capacity that delivers crude oil from our Lucas terminal to Valero’s Port Arthur Refinery. |

• | Nederland Pipeline. Our Nederland pipeline is a five-mile, 32-inch pipeline with 600,000 barrels per day of capacity that delivers crude oil to our Lucas terminal from the Sunoco Logistics Nederland marine terminal. |

• | TransCanada Connection. Our TransCanada connection has 400,000 barrels per day of capacity and connects our Lucas terminal to TransCanada’s Cushing MarketLink pipeline. |

• | Seaway Connection. Our Seaway connection has 750,000 barrels per day of capacity and connects our Lucas terminal to the Seaway crude oil pipeline. |

Port Arthur Products System. Our Port Arthur products system transports refined petroleum products from Valero’s Port Arthur Refinery to major third-party pipeline systems, including the Explorer, Colonial, Sunoco Logistics MagTex and Enterprise TE Products refined petroleum products pipeline systems, for delivery to various marketing outlets, and to Enterprise’s Beaumont marine terminal for exports.

Our Port Arthur products system comprises the following assets:

• | Port Arthur Products Pipelines (PAPS – El Vista). Our Port Arthur products pipelines consist of a four-mile, 20-inch pipeline with 144,000 barrels per day of capacity that delivers gasoline from Valero’s Port Arthur Refinery to our El Vista terminal and a three-mile, 20-inch pipeline with 216,000 barrels per day of capacity that delivers diesel from Valero’s Port Arthur Refinery to our Port Arthur Products Station (PAPS) terminal. |

• | 12-10 Pipeline. Our 12-10 pipeline consists of 13 miles of 12-inch and 10-inch pipeline with 60,000 barrels per day of capacity that delivers refined petroleum products from Valero’s Port Arthur Refinery to the Enterprise TE Products pipeline connection, the Sunoco Logistics MagTex pipeline connection, and Enterprise’s Beaumont marine terminal. |

4

• | PAPS and El Vista Terminals. Our PAPS terminal consists of eight tanks with 821,000 barrels of diesel storage capacity, and our El Vista terminal consists of eight tanks with 1.2 million barrels of gasoline storage capacity. Our PAPS terminal also contains storage tanks owned by Colonial, which serves as the operator of our PAPS terminal. Each party owns its own tanks at the PAPS terminal and its own external pipelines connecting to the terminal, but certain equipment and improvements located at and serving the terminal are jointly owned. We own all of the El Vista terminal assets. |

McKee Logistics System

Our McKee logistics system is a crude oil and refined petroleum products pipeline and terminal system supporting Valero’s McKee Refinery. Our McKee logistics system includes our McKee crude system and McKee products system.

McKee Crude System. Our McKee crude system supplies crude oil to Valero’s McKee Refinery. The system has a throughput capacity of approximately 72,000 barrels per day and consists of 145 miles of pipelines located in the Texas panhandle and western Oklahoma, 20 crude oil truck unloading sites with lease automatic custody transfer units, and approximately 240,000 barrels of storage capacity.

McKee Products System. Our McKee products system transports refined petroleum products from Valero’s McKee Refinery to our refined petroleum products terminal in El Paso, Texas and on to Kinder Morgan’s SFPP system for marketing in the southwest U.S. We own a 33⅓ percent undivided interest in the system. Capacity on the McKee products system is allocated between the other interest owner and us according to our respective ownership interests.

Our McKee products system comprises the following assets:

• | McKee to El Paso Pipeline. Our McKee to El Paso pipeline consists of 408 miles of 10-inch pipeline that delivers diesel and gasoline produced at Valero’s McKee Refinery to our El Paso terminal. The pipeline has a total capacity of 63,000 barrels per day (of which 21,000 barrels per day of capacity are allocable to our 33⅓ percent undivided interest). |

• | SFPP Pipeline Connection. Our SFPP pipeline connection consists of 12 miles of 16- and 8-inch pipelines that deliver diesel and gasoline from our El Paso terminal to Kinder Morgan’s SFPP system. The SFPP pipeline connection has 98,400 barrels per day of capacity (of which 33,000 barrels per day of capacity are allocable to our 33⅓ percent undivided interest). |

• | El Paso Terminal. Our El Paso terminal is located on 117 acres and consists of 10 storage tanks with 499,000 barrels of storage capacity (of which 166,000 barrels of capacity are allocable to our 33⅓ percent undivided interest). The El Paso terminal receives refined petroleum products delivered to the terminal through our McKee to El Paso pipeline and delivers refined petroleum products to our four-bay truck rack at our El Paso terminal and to Kinder Morgan’s SFPP system through our SFPP pipeline connection. Our El Paso terminal truck rack has 30,000 barrels per day of capacity (of which 10,000 barrels per day of capacity are allocable to our 33⅓ percent undivided interest). |

5

Memphis Logistics System

Our Memphis logistics system includes our Collierville crude system and our Memphis products system.

Collierville Crude System. Our Collierville crude system is the primary crude oil supply source for Valero’s Memphis Refinery, delivering crude oil from the Capline pipeline.

Our Collierville crude system comprises the following assets:

• | Collierville Pipeline System. Our Collierville pipeline system consists of 52 miles of 10- to 20-inch pipelines with 210,000 barrels per day of capacity that deliver crude oil to Valero’s Memphis Refinery. We lease an approximate 13 mile portion of this pipeline, which runs from the Mississippi state line to the Memphis Refinery, from Memphis Light, Gas and Water (MLGW). The initial term of the lease, along with renewal periods available at our option, extend through 2046. |

• | Collierville Terminal. Our Collierville terminal is located in Byhalia, Mississippi on 60 acres. The facility consists of three storage tanks with 975,000 barrels of storage capacity. The Collierville terminal receives crude oil delivered to the terminal through the Capline pipeline. |

• | St. James Crude Tank. We own a 330,000 barrel crude oil storage tank in St. James, Louisiana located on land we lease from Shell. The tank is used to aggregate crude oil volumes to batch deliveries through the Capline pipeline to our Collierville terminal. |

Memphis Products System. Our Memphis products system is the primary outlet for refined petroleum products produced at Valero’s Memphis Refinery. Distribution of these products occurs through our Memphis truck rack and our terminal in West Memphis, Arkansas, for further distribution via truck and barge to marketing outlets along the central Mississippi River, to Exxon’s Memphis refined petroleum products terminal, and to the Memphis International Airport.

Our Memphis products system comprises the following assets:

• | Shorthorn Pipeline System. Our Shorthorn pipeline system consists of seven miles of 14-inch pipeline that delivers diesel and gasoline produced at Valero’s Memphis Refinery to our West Memphis terminal and two miles of 12-inch pipeline that delivers diesel and gasoline from our West Memphis terminal and Valero’s Memphis Refinery to Exxon’s Memphis refined petroleum products terminal. We lease the 14-inch pipeline from MLGW. The initial term of the lease, along with renewal periods available at our option, extend through 2046. The Shorthorn pipeline system has a total capacity of 120,000 barrels per day. |

• | Memphis Airport Pipeline System. Our Memphis Airport pipeline system consists of a nine-mile, six-inch pipeline that delivers jet fuel produced at Valero’s Memphis Refinery to the Swissport Fueling, Inc. terminal located at the Memphis International Airport and a two-mile, six-inch pipeline that delivers jet fuel from Valero’s Memphis Refinery to the FedEx jet fuel terminal located at the Memphis International Airport. The Memphis Airport pipeline system has a total capacity of 20,000 barrels per day. Both six-inch pipelines are owned by MLGW and we have an agreement with MLGW under which we are the exclusive operator of both pipelines. Our agreement with MLGW automatically renews and MLGW does not have a right to terminate. |

6

• | West Memphis Terminal. Our West Memphis terminal is located in West Memphis, Arkansas on 75 acres. The facility consists of 18 storage tanks with over one million barrels of storage capacity, a truck rack, and a barge dock on the Mississippi River. Our West Memphis terminal receives refined petroleum products through our Shorthorn pipeline system and through a biodiesel truck unloading rack located at the terminal. The terminal delivers refined petroleum products to the five-bay, 50,000 barrels per day truck rack at the terminal, our two-berth, 4,000 barrels per hour barge dock on the Mississippi River, and our Shorthorn pipeline system for deliveries to Exxon’s Memphis terminal. |

• | Memphis Truck Rack. Our Memphis truck rack is located on five acres of land adjacent to Valero’s Memphis Refinery. The facility consists of a high-capacity seven-bay truck rack and five biodiesel storage tanks with 8,000 barrels of storage capacity. The truck rack has a capacity of 110,000 barrels per day. |

Three Rivers Crude System

Our Three Rivers crude system supports Valero’s Three Rivers Refinery and is located in the Eagle Ford shale region in South Texas. The system consists of 11 crude oil truck unloading sites with lease automatic custody transfer units and three 1-mile, 12-inch pipelines with a capacity of 110,000 barrels per day. The system delivers crude oil received from the truck unloading sites and pipeline connections to tanks at Valero’s Three Rivers Refinery. The system also receives locally produced crude oil via connections to the Harvest Arrowhead pipeline system and the Plains Gardendale pipeline for processing at the Three Rivers Refinery or for shipment through third-party pipelines to Valero’s refineries in Corpus Christi, Texas. The system has a connection to the EOG Eagle Ford West Pipeline and supporting pipeline infrastructure, which segregate and connect Eagle Ford crude oil production to Valero’s Three Rivers Refinery.

Wynnewood Products System

The Wynnewood products system is the primary distribution outlet for refined petroleum products from Valero’s Ardmore Refinery. The system consists of a 30-mile, 12-inch refined petroleum products pipeline with 90,000 barrels per day of capacity and two tanks with a total of 180,000 barrels of storage capacity. The system connects Valero’s Ardmore Refinery to the Magellan refined products pipeline system.

Houston Terminal

Our Houston terminal is a crude oil, intermediates, and refined petroleum products terminal that supports Valero’s Houston Refinery. The terminal is located on the Houston ship channel and has storage tanks with 3.6 million barrels of storage capacity. The terminal receives waterborne crude oil via the refinery’s docks and the terminal’s connection to Houston Fuel Oil Terminal Company (HFOTCO), and receives pipeline crude oil through the Magellan and Seaway systems. The terminal can distribute refined petroleum products across the refinery’s docks and into the Magellan South Pipeline system. Also, the terminal can access the Colonial, TEPPCO, and Explorer pipeline systems via the Kinder Morgan Pasadena terminal.

St. Charles Terminal

Our St. Charles terminal is a crude oil, intermediates, and refined petroleum products terminal that supports Valero’s St. Charles Refinery. The terminal is located on the Mississippi River and has storage tanks with 10 million barrels of storage capacity. The terminal receives crude oil via the refinery’s docks and from Louisiana Offshore Oil Port (LOOP) via the Clovelly pipeline. The terminal can distribute refined petroleum products across the refinery’s docks and into the Plantation (via Parkway) and Colonial (via Bengal) pipeline systems.

7

Corpus Christi Terminals

Our Corpus Christi terminals are engaged in the business of terminaling crude oil, intermediates, and refined petroleum products in Corpus Christi, Texas.

• | Corpus Christi East Terminal. Our Corpus Christi East terminal supports Valero’s Corpus Christi East Refinery. The Corpus Christi East terminal is located on the Corpus Christi ship channel and has storage tanks with 6.2 million barrels of storage capacity. |

• | Corpus Christi West Terminal. Our Corpus Christi West terminal supports Valero’s Corpus Christi West Refinery. The Corpus Christi West terminal is located on the Corpus Christi ship channel and has storage tanks with 3.8 million barrels of storage capacity. |

Our Corpus Christi terminals are connected via pipeline. The terminals can receive crude oil via the refineries’ docks, the Eagle Ford Pipeline LLC pipeline, the North Beach terminal owned by NuStar Logistics, L.P. (NuStar), and NuStar’s Eagle Ford pipelines. The terminals can distribute products across their docks and through NuStar’s South Texas pipeline network.

8

Pipelines

The following table summarizes information with respect to our pipelines described above:

Pipeline | Diameter (inches) | Length (miles) | Throughput Capacity (thousand barrels per day) | Commodity | Associated Valero Refinery | Significant Third-party System Connections | ||||||

Port Arthur logistics system | ||||||||||||

Lucas crude system | ||||||||||||

Lucas pipeline | 30 | 12 | 400 | crude oil | Port Arthur | Sunoco Logistics Nederland; Enterprise Beaumont; Cameron Highway; TransCanada Cushing MarketLink | ||||||

Nederland pipeline | 32 | 5 | 600 | crude oil | Port Arthur | Sunoco Logistics Nederland | ||||||

Port Arthur products system | ||||||||||||

20-inch gasoline pipeline | 20 | 4 | 144 | gasoline | Port Arthur | Explorer; Colonial | ||||||

20-inch diesel pipeline | 20 | 3 | 216 | diesel | Port Arthur | Explorer; Colonial | ||||||

12-10 pipeline | 12, 10 | 13 | 60 | refined petroleum products | Port Arthur | Sunoco Logistics MagTex; Enterprise TE Products; Enterprise Beaumont | ||||||

McKee logistics system | ||||||||||||

McKee crude system | multiple segments | 145 | 72 | crude oil | McKee | — | ||||||

McKee products system | ||||||||||||

McKee to El Paso pipeline | 10 | 408 | 21(1) | refined petroleum products | McKee | — | ||||||

SFPP pipeline connection | 16, 8 | 12 | 33(2) | refined petroleum products | McKee | Kinder Morgan's SFPP System | ||||||

Memphis logistics system(3) | ||||||||||||

Collierville crude system | ||||||||||||

Collierville pipeline | 10-20 | 52 | 210 | crude oil | Memphis | Capline | ||||||

Memphis products system | ||||||||||||

Shorthorn pipeline system | 14, 12 | 9 | 120 | refined petroleum products | Memphis | Exxon Memphis | ||||||

Memphis Airport pipeline system | 6 | 11 | 20 | jet fuel | Memphis | Memphis International Airport | ||||||

Three Rivers crude system | ||||||||||||

Three Rivers crude system | 12 | 3 | 110 | crude oil | Three Rivers | Harvest Arrowhead, Plains Gardendale, and EOG Eagle Ford West | ||||||

Wynnewood products system | ||||||||||||

Wynnewood refined products pipeline | 12 | 30 | 90 | refined petroleum products | Ardmore | Magellan | ||||||

_____________

(1) | Capacity shown represents our 33⅓ percent undivided interest in the pipeline. Total capacity for the pipeline is 63,000 barrels per day. |

(2) | Capacity shown represents our 33⅓ percent undivided interest in the pipeline connection. Total capacity for the pipeline connection is 98,400 barrels per day. |

(3) | Portions of our Memphis logistics system pipelines are owned by MLGW, but they are operated and maintained exclusively by us under long-term arrangements with MLGW. |

9

Terminals

The following table summarizes information with respect to our terminals described above:

Terminal | Tank Storage Capacity (thousands of barrels) | Throughput Capacity (thousand barrels per day) | Commodity | Associated Valero Refinery | Significant Third-party System Connections | |||||

Port Arthur logistics system | ||||||||||

Lucas crude system | ||||||||||

Lucas terminal | 1,915 | — | crude oil | Port Arthur | Sunoco Logistics Nederland; Enterprise Beaumont; Cameron Highway; TransCanada Cushing MarketLink; Seaway | |||||

TransCanada connection | — | 400 | crude oil | Port Arthur | TransCanada Cushing MarketLink | |||||

Seaway connection | — | 750 | crude oil | Port Arthur | Seaway | |||||

Port Arthur products system | ||||||||||

PAPS terminal | 821 | — | diesel | Port Arthur | Explorer; Colonial | |||||

El Vista terminal | 1,210 | — | gasoline | Port Arthur | Explorer; Colonial | |||||

McKee logistics system | ||||||||||

McKee crude system | ||||||||||

Various terminals | 240 | — | crude oil | McKee | — | |||||

McKee products system | ||||||||||

El Paso terminal | 166 (1) | — | refined petroleum products | McKee | Kinder Morgan SFPP System | |||||

El Paso terminal truck rack | — | 10 (2) | refined petroleum products | McKee | — | |||||

Memphis logistics system | ||||||||||

Collierville crude system | ||||||||||

Collierville terminal | 975 | — | crude oil | Memphis | Capline | |||||

St. James crude tank | 330 | — | crude oil | Memphis | Capline | |||||

Memphis products system | ||||||||||

West Memphis terminal | 1,080 | — | refined petroleum products | Memphis | Exxon Memphis; Enterprise TE Products | |||||

West Memphis terminal truck rack | — | 50 | refined petroleum products | Memphis | — | |||||

West Memphis terminal dock | — | 4 (3) | refined petroleum products | Memphis | — | |||||

Memphis truck rack | 8 | 110 | refined petroleum products | Memphis | — | |||||

Wynnewood products system | ||||||||||

Wynnewood terminal | 180 | — | refined petroleum products | Ardmore | Magellan | |||||

Houston terminal | 3,642 | — | crude oil and refined petroleum products | Houston | HFOTCO, Magellan, Seaway | |||||

St. Charles terminal | 10,004 | — | crude oil and refined petroleum products | St. Charles | LOOP, Plantation, Colonial | |||||

10

Terminal | Tank Storage Capacity (thousands of barrels) | Throughput Capacity (thousand barrels per day) | Commodity | Associated Valero Refinery | Significant Third-party System Connections | |||||

Corpus Christi terminals | ||||||||||

Corpus Christi East terminal | 6,241 | — | crude oil and refined petroleum products | Corpus Christi East | Eagle Ford Pipeline LLC; NuStar North Beach terminal, Eagle Ford pipelines, and South Texas pipeline network | |||||

Corpus Christi West terminal | 3,835 | — | crude oil and refined petroleum products | Corpus Christi West | (same as Corpus Christi East terminal) | |||||

_____________

(1) | Capacity shown represents our 33⅓ percent undivided interest in the terminal. Total storage capacity is 499,000 barrels. |

(2) | Capacity shown represents our 33⅓ percent undivided interest in the truck rack. Total capacity is 30,000 barrels per day. |

(3) | Dock throughput is reflected in thousands of barrels per hour. |

Our Commercial Agreements with Valero

General

We have a master transportation services agreement with Valero with respect to our pipelines and a master terminal services agreement with Valero with respect to our terminals. Each of our pipelines and terminals is covered by a services schedule under these agreements. The services schedules prescribe rates, commitments, and other terms and conditions applicable to the respective pipelines and terminals. Under these agreements and schedules, we provide transportation and terminaling services to Valero, and Valero pays us for minimum quarterly throughput volumes of crude oil and refined petroleum products, regardless of whether such volumes are physically delivered by Valero in any given quarter. These services schedules have initial 10-year terms from inception, and, with the exception of certain assets, Valero has the option to renew the agreements for one additional five-year term.

Minimum Quarterly Throughput Commitments and Tariff Rates—Pipelines

Under our master transportation services agreement, Valero is obligated to transport minimum volumes of crude oil and refined petroleum products on our pipeline systems and pay a tariff rate with respect to such volumes. Tariff rates with respect to our pipeline systems may be adjusted annually at our discretion in accordance with the Federal Energy Regulatory Commission’s (FERC) indexing methodology. For any pipelines that may be subject to a jurisdictional tariff, we and Valero have agreed not to commence or support any tariff filing, application, protest, complaint, petition, motion, or other proceeding before FERC for the purpose of requesting that FERC accept or set tariff rates that would be inconsistent with the terms of the master transportation services agreement, provided that Valero will continue to have the right under FERC regulations to challenge any proposed changes in our base tariff rates to the extent the changes are inconsistent with FERC’s indexing methodology or other rate changing methodologies, or to the extent the challenge is in response to any proceeding brought against us by a third party that could affect our ability to provide transportation services to Valero under our master transportation services agreement or the applicable tariff.

Minimum Quarterly Throughput Commitments and Fees—Terminals

Under the master terminal services agreement relating to our terminals, Valero is obligated to throughput minimum volumes of crude oil and refined petroleum products and pay us throughput fees, as well as fees for providing related ancillary services such as ethanol, biodiesel and renewable diesel blending, and additive injection (except at the Wynnewood terminal, where Valero agrees to pay us a monthly fee as a base storage charge whether or not Valero actually uses any of the storage or other services made available by us at the

11

terminal). Valero provides and pays for its own inventory of ethanol, biodiesel and renewable diesel blending, and additives to be blended or injected at the terminals, where applicable. Throughput fees with respect to our terminals (or the base storage charge, with respect to our Wynnewood terminal) will be increased on July 1 of each year during the term of the applicable terminal service schedule, and other fees with respect to our terminals may be increased annually at our discretion, in each case by a percentage not to exceed the corresponding percentage change in the applicable inflation index during the 12-month period ending on March 31 of such year. If such index decreases during any period, we are not required to reduce our fees, but any subsequent increases in fees based on an increase in the index will be limited to the amount by which such increase exceeds the aggregate amount of cumulative decreases during the intervening periods.

Quarterly Deficiency Payments

If Valero fails to meet its minimum quarterly throughput commitments under our commercial agreements in any given quarter, it is obligated to pay a deficiency payment equal to the volume deficiency multiplied by the applicable tariff and/or fee with respect to such asset. We refer to this payment as a “quarterly deficiency payment.” Quarterly deficiency payments may be applied as a credit for amounts owed on throughput volumes in excess of Valero’s minimum quarterly throughput commitment with respect to such asset during any of the following four quarters, after which time any unused credits will expire. Upon the expiration of our commercial agreements, Valero may apply any such remaining credit amounts with respect to such asset until the completion of any such four-quarter period against any throughput volumes on such asset in excess of the minimum quarterly throughput commitment that was in place during the term of the agreement with respect to such asset.

Minimum Capacity

Under each of our commercial agreements, we are obligated to provide Valero access to capacity of at least the minimum quarterly throughput commitment for our assets. If the minimum capacity of any of our assets falls below the level of Valero’s minimum quarterly throughput commitment at any time due to events affecting such assets (whether planned or unplanned) or if capacity on any of our assets is required to be allocated among users because volume nominations exceed available capacity, Valero’s minimum quarterly throughput commitments with respect to such assets may be proportionately reduced during the period for which capacity is less than Valero’s minimum quarterly throughput commitment.

Product Gains and Losses

Under each of our commercial agreements, other than those commercial agreements covering assets that may be subject to a jurisdictional tariff or are operated by a third party and such tariff or third-party operating agreement specifically provides otherwise, we have no liability for physical losses except to the extent such losses result from our gross negligence or willful misconduct. In the event a terminal or pipeline asset is equipped to measure volume gains and losses through the installation of custody transfer meters and we begin to accept third-party volumes for throughput, we are required to negotiate provisions regarding loss allowance and allocate gains and losses among us and our customers in accordance with standard industry practices.

Termination and Suspension

Valero is permitted under our commercial agreements to suspend, reduce, or terminate its obligations under certain circumstances. If Valero determines to totally or partially suspend refining operations at a refinery that is supported by our assets for a period of at least 12 consecutive months, we and Valero are required to negotiate in good faith to agree upon a reduction of Valero’s minimum quarterly throughput commitments under the applicable commercial agreement(s), and if we are unable to agree to an appropriate reduction,

12

then after Valero has made a public announcement of such suspension, Valero may terminate the applicable agreement(s) upon 12 months’ notice to us (unless in the interim Valero publicly announces its intent to resume operations at the refinery, in which case its termination notice is deemed revoked). If a force majeure event with respect to our assets prevents us from performing any of our obligations under a commercial agreement, Valero’s obligations with respect to the affected assets under the applicable commercial agreement, including its minimum quarterly throughput commitments, will be suspended to the extent we cannot perform our obligations. In addition, if a force majeure event prevents Valero from fulfilling any of its obligations under our commercial agreements for more than 60 days, Valero’s applicable obligations with respect to the affected assets, including its minimum quarterly throughput commitments, under our commercial agreements will be suspended for the remainder of the force majeure event.

Turnarounds or other planned outages at a refinery are not force majeure events. If a force majeure event prevents any party from performing its obligations under a commercial agreement for a period of more than 12 consecutive months, then either party may terminate the agreement with respect to the affected assets. If Valero elects to terminate or suspend any of our commercial agreements, our financial condition, results of operations, cash flows, and ability to make distributions to our unitholders may be materially and adversely affected. We cannot assure you that Valero will continue to use our assets or that we will be able to generate additional revenues from third parties.

Reimbursements of Capital Expenditures

Our commercial agreements provide that, if we agree to make any capital expenditures at Valero’s request, Valero is required to reimburse us for the expenditures; the reimbursements may be recovered through tariff and/or fee increases in certain cases.

Effects of New Laws or Regulations

If new laws or regulations are enacted or promulgated or if existing laws or their interpretations are materially changed, and if such new or changed laws or regulations will have a material adverse economic impact on either us or Valero, then either of us, acting in good faith, may request to renegotiate the relevant provisions of the affected commercial agreement(s) relating to the parties’ future performance. In such event, we and Valero are required to negotiate in good faith amendments to the affected agreement(s) to conform them to the new or changed laws or regulations while preserving our economic, operational, commercial, and competitive arrangements in accordance with the understandings set forth in the applicable agreement(s).

Alternative Arrangements

Under our commercial agreements, if Valero restructures its operations at a refinery that is supported by our assets in such a manner that materially and adversely affects the economics of Valero’s performance under the applicable commercial agreement, we and Valero are required to negotiate in good faith an alternative arrangement that is no worse economically for us, and that may include a substitution of new minimum quarterly throughput commitments for Valero on other assets owned or to be acquired or constructed by us.

Our Relationship with Valero

Valero is an international manufacturer and marketer of transportation fuels, other petrochemical products, and power. Valero’s assets include 15 petroleum refineries located in the U.S., Canada, and the United Kingdom, with a combined total throughput capacity of approximately 3.0 million barrels per day. Valero also has a substantial portfolio of transportation and logistics assets.

13

We are dependent upon Valero as our only customer and the loss of Valero as a customer would have a material and adverse effect on us. For the years ended December 31, 2015, 2014, and 2013, Valero accounted for all of our revenues. We expect to continue to derive substantially all of our revenues from Valero for the foreseeable future.

Valero owns 100 percent of our general partner, a 65.7 percent limited partner interest in us, and all of our incentive distribution rights. We believe Valero will promote and support the successful execution of our business strategies given its significant ownership in us, the importance of our assets to Valero’s refining and marketing operations, and its stated intention to use us as its primary vehicle to expand the transportation and logistics assets supporting its business.

In addition to our commercial agreements with Valero, we entered into several agreements with Valero in connection with the IPO, many of which we have amended in connection with subsequent acquisitions. These agreements include an amended and restated omnibus agreement, an amended and restated services and secondment agreement, a tax sharing agreement, and several lease and access agreements. These agreements are described in Note 4 of Notes to Consolidated Financial Statements, and the descriptions of these agreements in Note 4 are incorporated herein by reference.

Pipeline Control Operations

Our pipeline systems, other than the El Paso pipeline operated by NuStar, are operated from a central control room located in San Antonio, Texas. The control center operates with a supervisory control and data acquisition system equipped with computer systems designed to monitor operational data continuously. Monitored data includes pressures, temperatures, gravities, flow rates, and alarm conditions. The control center operates remote pumps, motors, and valves associated with the receipt and delivery of crude oil and refined petroleum products, and provides for the remote-controlled shutdown of pump stations on the pipeline system. A fully functional back-up operations center is also maintained and routinely operated throughout the year to ensure safe and reliable operations.

Seasonality

The volumes of crude oil and refined petroleum products transported in our pipelines and stored in our terminals are directly affected by the levels of supply and demand for crude oil and refined petroleum products in the markets served directly or indirectly by our assets. Demand for gasoline is generally higher during the summer months than during the winter months due to seasonal increases in motor vehicle traffic. As a result, Valero’s operating results are generally lower for the first and fourth quarters of each year. Unfavorable weather conditions during the spring and summer months and a resulting lack of the expected seasonal upswings in traffic and sales could adversely affect Valero’s business, financial condition, and results of operations, which may adversely affect our business, financial condition, and results of operations. However, many effects of seasonality on our revenues will be substantially mitigated through the use of our fee-based commercial agreements with Valero that include minimum quarterly throughput commitments.

Competition

As a result of our contractual relationship with Valero under our commercial agreements and our direct connections to nine of Valero’s refineries, we believe that our pipelines and terminals will not face significant competition from other pipelines and terminals for Valero’s crude oil or refined petroleum products transportation requirements to and from the refineries we support.

If Valero’s customers reduce their purchases of refined petroleum products from Valero due to the increased availability of less expensive products from other suppliers or for other reasons, Valero may ship only the

14

minimum volumes through our pipelines (or pay the shortfall payment if it does not ship the minimum volumes), which would cause a decrease in our revenues. Valero competes with integrated petroleum companies, which have their own crude oil supplies and distribution and marketing systems, as well as with independent refiners, many of which also have their own distribution and marketing systems. Valero also competes with other suppliers that purchase refined petroleum products for resale. Competition in any particular geographic area is affected significantly by the volume of products produced by refineries in that area and by the availability of products and the cost of transportation to that area from distant refineries.

Environmental Matters

Our operations are subject to extensive environmental regulations by governmental authorities relating to the discharge and remediation of materials in the environment, greenhouse gas emissions, waste management, pollution prevention, species and habitat preservation, pipeline integrity, and other safety-related regulations, and characteristics and composition of fuels. Because environmental laws and regulations are becoming more complex and stringent and new environmental laws and regulations are continuously being enacted or proposed, the level of future expenditures required for environmental matters could increase in the future. In addition, any major upgrades in any of our operating facilities could require material additional expenditures to comply with environmental laws and regulations.

There are existing remedial obligations at some of our assets including our West Memphis terminal and our Lucas terminal. These existing environmental conditions are retained obligations of the prior operators of these facilities and Valero has agreed to indemnify us with respect to such conditions under the terms of our omnibus agreement. For additional information regarding our environmental matters, please see Note 6 of Notes to Consolidated Financial Statements.

Rate and Other Regulations

FERC and Common Carrier Regulations

We own pipeline assets in Texas, New Mexico, Tennessee, Mississippi, Arkansas, and Oklahoma, and we provide both interstate and intrastate transportation services. Our common carrier pipeline systems are subject to regulation by various federal, state, and local agencies.

FERC regulates interstate transportation on our common carrier pipeline systems under the Interstate Commerce Act (ICA), the Energy Policy Act (EPAct), and the rules and regulations promulgated under those laws. FERC regulations require that rates for interstate service pipelines that transport crude oil and refined petroleum products (collectively referred to as petroleum pipelines) and certain other liquids, be just and reasonable and must not be unduly discriminatory or confer any undue preference upon any shipper. FERC’s regulations also require interstate common carrier petroleum pipelines to file with FERC and publicly post tariffs stating their interstate transportation rates and terms and conditions of service. Under the ICA, FERC or interested persons may challenge existing or changed rates or services. FERC is authorized to investigate such charges and may suspend the effectiveness of a new rate for up to seven months. A successful rate challenge could result in a common carrier paying refunds together with interest for the period that the rate was in effect. FERC may also order a pipeline to change its rates, and may require a common carrier to pay shippers reparations for damages sustained for a period up to two years prior to the filing of a complaint.

Intrastate services provided by certain of our pipeline systems are subject to regulation by state regulatory authorities, such as the Texas Railroad Commission (TRRC), which currently regulates our portion of the McKee to El Paso pipeline. The TRRC uses a complaint-based system of regulation, both as to matters involving rates and priority of access. FERC and state regulatory commissions generally have not investigated

15

rates, unless the rates are the subject of a protest or a complaint. However, FERC or a state commission could investigate our rates on its own initiative or at the urging of a third party.

If our rate levels were investigated by FERC or a state commission, the inquiry could result in a comparison of our rates to those charged by others or to an investigation of our costs. We do not anticipate any complaints against our rates or any investigation by FERC or a state regulatory commission related to our rates or terms of service. Valero has agreed not to contest our tariff rates or terms of service for the term of our transportation services agreements, provided that our tariff changes and rate increases are consistent with the terms of the transportation services agreements. Even so, FERC or a state commission could order us to change our rates or terms of service or require us to pay shippers reparations, together with interest and subject to the applicable statute of limitations, if it were determined that an established rate or terms of service were unjust or unreasonable.

Pipeline Safety

Our assets are subject to increasingly strict safety laws and regulations. The transportation and storage of crude oil and refined petroleum products involve a risk that hazardous liquids may be released into the environment, potentially causing harm to the public or the environment. In turn, such incidents may result in substantial expenditures for response actions, significant government penalties, liability to government agencies for natural resources damages, and significant business interruption. The Department of Transportation (DOT) and Pipeline and Hazardous Materials Safety Administration have adopted safety regulations with respect to the design, construction, operation, maintenance, inspection, and management of our assets. These regulations contain requirements for the development and implementation of pipeline integrity management programs, which include the inspection and testing of pipelines and necessary maintenance or repairs. These regulations also require that pipeline operation and maintenance personnel meet certain qualifications and that pipeline operators develop comprehensive spill response plans.

Product Quality Standards

Refined petroleum products that we transport are generally sold by Valero for consumption by the public. Various federal, state, and local agencies have the authority to prescribe product quality specifications for products. Changes in product quality specifications or blending requirements could reduce our throughput volumes, require us to incur additional handling costs, or require capital expenditures. For example, different product specifications for different markets affect the fungibility of the products in our system and could require the construction of additional storage. If we are unable to recover these costs through increased revenues, our cash flows and ability to make distributions could be adversely affected. In addition, changes in the product quality of the products we receive on our product pipeline systems or at our terminals could reduce or eliminate our ability to blend products.

Security

We are also subject to Department of Homeland Security Chemical Facility Anti-Terrorism Standards, which are designed to regulate the security of high-risk chemical facilities, and to the Transportation Security Administration’s Pipeline Security Guidelines. We have an internal program of inspection designed to monitor and enforce compliance with all of these requirements. We believe that we are in material compliance with all applicable laws and regulations regarding the security of our facilities.

While we are not currently subject to governmental standards for the protection of computer-based systems and technology from cyber threats and attacks, proposals to establish such standards are being considered by the U.S. Congress and by U.S. Executive Branch departments and agencies, including the Department of Homeland Security, and we may become subject to such standards in the future. We are currently

16

implementing our own cybersecurity programs and protocols; however, we cannot guarantee their effectiveness. A significant cyber-attack could have a material effect on our operations and those of our customer.

Employees

Neither we nor our general partner has any employees. We are managed by the board of directors and executive officers of our general partner. All of the personnel that conduct our business are employed by Valero, and their services are provided to us pursuant to our omnibus agreement and services and secondment agreement with Valero.

PROPERTIES

The location and general character of our pipeline and terminal systems and other principal properties are described above under “Our Assets and Operations” and are incorporated herein by reference. We believe that our properties and facilities are generally adequate for our operations and that our facilities are maintained in a good state of repair. As of December 31, 2015, we were the lessee under a number of cancelable and noncancelable leases for certain properties. Our leases are discussed more fully in Notes 4, 7, and 8 of Notes to Consolidated Financial Statements.

Utilization of Our Facilities

Operating highlights for our pipelines and terminals–including pipeline transportation revenues, pipeline transportation throughput volumes, terminaling revenues, terminaling throughput volumes, and storage revenues–for the years ended December 31, 2015, 2014, and 2013 are described in Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations—2015 Compared to 2014” and “—2014 Compared to 2013,” and are incorporated herein by reference.

Title to Properties and Permits

Substantially all of our pipelines are constructed on rights-of-way granted by the apparent record owners of the property and in some instances these rights-of-way are revocable at the election of the grantor. In many instances, lands over which rights-of-way have been obtained are subject to prior liens that have not been subordinated to the right-of-way grants. We have obtained permits from public authorities to cross over or under, or to lay facilities in or along, watercourses, county roads, municipal streets, and state highways and, in some instances, these permits are revocable at the election of the grantor. We have also obtained permits from railroad companies to cross over or under lands or rights-of-way, many of which are also revocable at the grantor’s election. In some states and under some circumstances, we have the right of eminent domain to acquire rights-of-way and lands necessary for our common carrier pipelines.

Under our omnibus agreement, Valero will indemnify us for certain title defects and for failures to obtain certain consents and permits necessary to conduct our business. Although title to these properties is subject to encumbrances in some cases, such as customary interests generally retained in connection with acquisition of real property, liens that can be imposed in some jurisdictions for government-initiated action to clean up environmental contamination, liens for current taxes and other burdens, and easements, restrictions, and other encumbrances to which the underlying properties were subject at the time of acquisition, we believe that none of these burdens should materially detract from the value of these properties or from our interest in these properties or should materially interfere with their use in the operation of our business.

17

Item 1A. RISK FACTORS

You should carefully consider each of the following risks and all of the other information contained in this Annual Report on Form 10-K in evaluating us and our common units. Some of these risks relate principally to our business and the industry in which we operate, while others relate principally to the business and operations of Valero, tax matters, ownership of our common units, and securities markets generally.

Our financial condition, results of operations, and cash flows and our ability to make distributions to our unitholders could be materially and adversely affected by these risks, and, as a result, the trading price of our common units could decline.

Risks Related to Our Business

Valero accounts for all of our revenues. Therefore, we are subject to the business risks associated with Valero’s business. Furthermore, if Valero changes its business strategy, is unable for any reason, including financial or other limitations, to satisfy its obligations under our commercial agreements or significantly reduces the volumes transported through our pipelines or terminals, our revenues would decline and our financial condition, results of operations, cash flows, and ability to make distributions to our unitholders would be materially and adversely affected.

For the years ended December 31, 2015, 2014, and 2013, Valero accounted for all of our revenues. We expect to continue to derive a substantial amount of our revenues from Valero for the foreseeable future, and as a result, any event, whether in our areas of operation or elsewhere, that materially and adversely affects Valero’s business may adversely affect our financial condition, results of operations, and cash flows and our ability to make distributions to our unitholders. Accordingly, we are indirectly subject to the operational and business risks of Valero, the most significant of which include the following:

• | disruption of Valero’s ability to obtain crude oil; |

• | interruptions at Valero’s refineries and other facilities; |

• | any decision by Valero to temporarily or permanently curtail or shut down operations at one or more of its refineries or other facilities and reduce or terminate its obligations under our commercial agreements; |

• | competitors that produce their own supply of feedstocks, have more extensive retail outlets, or have greater financial resources may have a competitive advantage over Valero; |

• | the ability to obtain credit and financing on acceptable terms, which could also adversely affect the financial strength of business partners; |

• | the costs to comply with environmental laws and regulations; |

• | significant losses resulting from the hazards and risks of operations may not be fully covered by insurance, and could adversely affect Valero’s operations and financial results; |

• | large capital projects can take many years to complete, and market conditions could deteriorate significantly between the project approval date and the project startup date, negatively impacting project returns; |

• | interruptions of supply and increased costs as a result of Valero’s reliance on third-party transportation of crude oil and refined petroleum products; |

18

• | potential losses from Valero’s derivative transactions; and |

• | the effects of changing commodity and refined product prices. |

The volumes of crude oil and refined petroleum products that we transport and terminal depend substantially on Valero’s refining margins. Refining margins are dependent both upon the price of crude oil or other refinery feedstocks and refined petroleum products. These prices are affected by numerous factors beyond our or Valero’s control, including the global supply and demand for crude oil, gasoline and other refined petroleum products, competition from alternative energy sources, and the impact of new and more stringent regulations affecting the energy industry. A material decrease in the refining margins at Valero’s refineries supported by our assets could cause Valero to reduce the volumes we transport and terminal for Valero, which could materially and adversely affect our financial condition, results of operations, and ability to make distributions to our unitholders.

We may not have sufficient distributable cash flow following the establishment of cash reserves and payment of fees and expenses, including cost reimbursements to our general partner and its affiliates, to enable us to pay minimum quarterly distributions to our unitholders.

We may not generate sufficient cash flows each quarter to enable us to pay minimum quarterly distributions. The amount of cash we can distribute on our units principally depends upon the amount of cash we generate from our operations, which will fluctuate from quarter to quarter based on, among other things, our throughput volumes, tariff rates and fees, and prevailing economic conditions. In addition, the actual amount of cash flows we generate will also depend on other factors, some of which are beyond our control, including:

• | the amount of our operating expenses and general and administrative expenses, including reimbursements to Valero, which are not subject to any caps or other limits, in respect of those expenses; |

• | the amount and timing of capital expenditures and acquisitions we make; |

• | our debt service requirements and other liabilities, and restrictions contained in our revolving credit facility; |

• | fluctuations in our working capital needs; and |

• | the amount of cash reserves established by our general partner. |

If we are unable to obtain needed capital or financing on satisfactory terms to fund expansions of our asset base, our ability to make quarterly distributions may be diminished or our financial leverage could increase. We do not have any commitment with any of our affiliates to provide any direct or indirect financial assistance to us.

If we do not make sufficient or effective expansion capital expenditures, we will be unable to expand our business operations and may be unable to maintain or raise the level of our quarterly distributions. We will be required to use cash from our operations, incur borrowings or access the capital markets in order to fund our expansion capital expenditures. Our ability to incur indebtedness or access the capital markets may be limited by our financial condition at such time as well as the covenants in our debt agreements, general economic conditions and contingencies, and uncertainties that are beyond our control. The terms of any such financing could also limit our ability to make distributions to our common unitholders. Incurring additional debt may significantly increase our interest expense and financial leverage, and issuing additional limited partner interests may result in significant common unitholder dilution and increase the aggregate amount of cash required to maintain the then-current distribution rate, which could materially decrease our ability to pay distributions at the then-current distribution rate.

19

If Valero satisfies only its minimum quarterly throughput commitments under, or if Valero terminates or we are unable to renew or extend, our commercial agreements with Valero, our ability to make distributions to our unitholders will be reduced.

Valero is not obligated to use our services with respect to volumes of crude oil or refined petroleum products in excess of the minimum quarterly throughput commitments under our commercial agreements. During refinery turnarounds, which typically last 30 to 60 days and are performed every four to five years, we expect that Valero will satisfy only its minimum quarterly throughput commitments under our commercial agreements. Our commercial agreements with Valero generally have initial terms of 10 years from the date of acquisition of the related asset (the earliest of which begin to expire in 2023), and with the exception of certain assets, Valero has the option to renew the agreements for one additional five-year term. If Valero fails to use our facilities and services after expiration of those agreements and we are unable to generate additional revenues from third parties, our ability to make distributions to our unitholders will be reduced.

Further, Valero may suspend, reduce or terminate its obligations under our commercial agreements if certain events occur, such as Valero’s determination to totally or partially suspend refining operations at one of its refineries that our assets support for a period that will continue for at least 12 months, or a force majeure event that impacts one of Valero’s refineries for more than 60 days. Any such reduction, suspension, or termination of Valero’s obligations would have a material and adverse effect on our financial condition, results of operations, and cash flows and our ability to make distributions to our unitholders.

We may not be able to obtain third-party revenues due to competition and other factors, which could limit our ability to grow and may extend our dependence on Valero.

Since our initial public offering, we have not generated any revenues from third parties. Our ability to obtain third-party revenues is subject to numerous factors beyond our control, including competition from third parties and the extent to which we have available capacity when third-party shippers require it. We can provide no assurance that we will be able to attract material third-party revenues. Our efforts to establish our reputation and attract new unaffiliated customers may be adversely affected by our relationship with Valero and our desire to provide services pursuant to fee-based contracts. Our potential customers may prefer to obtain services under contracts through which we could be required to assume direct commodity exposure.

Our ability to acquire transportation and logistics assets from Valero is subject to risks and uncertainty, and ultimately we may not further acquire any assets from Valero.

Our present growth strategy depends significantly on acquiring assets from Valero. The consummation and timing of any future acquisitions will depend upon, among other things, Valero’s willingness to offer assets for sale, our ability to negotiate acceptable purchase agreements and commercial agreements with respect to such assets, and our ability to obtain financing on acceptable terms. We have no control over Valero’s decision to offer us the ability to acquire any of its assets. We can provide no assurance that we will be able to successfully consummate any future acquisitions from Valero, and Valero is under no obligation to accept any offer that we may choose to make. In addition, we may decide not to acquire additional assets from Valero, and any such decision will not be subject to unitholder approval. In addition, our right of first offer with respect to certain of Valero’s assets under our omnibus agreement may be terminated by Valero at any time in the event that it no longer controls our general partner.

20

If we are unable to make acquisitions on economically acceptable terms from Valero or third parties, our future growth would be limited, and any acquisitions we may make may reduce, rather than increase, our cash flows and ability to make distributions to unitholders.

Our strategy to grow our business and increase distributions to unitholders is dependent in part on our ability to make acquisitions that result in an increase in distributable cash flow per unit. Our growth strategy is based in part on our expectation of ongoing divestitures by industry participants, including our right of first offer from Valero. The consummation and timing of any future acquisitions will depend upon, among other things, whether:

• | we are able to identify attractive acquisition candidates; |

• | we are able to negotiate acceptable purchase agreements; |

• | we are able to obtain financing for these acquisitions on economically acceptable terms; and |

• | we are outbid by competitors. |

We can provide no assurance that we will be able to consummate any future acquisitions, whether from Valero or any third parties. If we are unable to make future acquisitions, our future growth and ability to increase distributions will be limited. Furthermore, even if we do consummate acquisitions that we believe will be accretive, they may in fact result in a decrease in distributable cash flow per unit as a result of incorrect assumptions in our evaluation of such acquisitions, unforeseen consequences, or other external events beyond our control. Acquisitions involve numerous risks, including difficulties in integrating acquired businesses, inefficiencies, and unexpected costs and liabilities.

Our ability to expand may be limited if Valero does not grow its business.

Our growth strategy depends in part on the growth of Valero’s business. We believe our growth will be driven in part by identifying and executing organic expansion projects that will result in increased throughput volumes from Valero and third parties. If Valero focuses on other growth areas or does not make capital expenditures to fund the growth of its business, we may not be able to fully execute our growth strategy.

Our and Valero’s operations are subject to many risks and operational hazards. If a significant accident or event occurs that results in a business interruption or shutdown for which we are not adequately insured, our financial condition, results of operations, and cash flows and our ability to sustain or increase distributions to our unitholders could be materially and adversely affected.

Our operations are subject to all of the risks and operational hazards inherent in transporting, terminaling, and storing crude oil and refined petroleum products, including:

• | damages to facilities, equipment, and surrounding properties caused by third parties, severe weather, natural disasters, and acts of terrorism; |

• | maintenance, repairs, mechanical or structural failures at our or Valero’s facilities or at third-party facilities on which our or Valero’s operations are dependent, including electrical shortages, power disruptions, and power grid failures; |

• | damages to and loss of availability of interconnecting third-party pipelines, terminals, and other means of delivering crude oil, feedstocks, and refined petroleum products; |

• | disruption or failure of information technology systems and network infrastructure due to various causes, including unauthorized access or attack; |

21

• | curtailments of operations due to severe seasonal weather; and |

• | riots, work stoppages, slowdowns or strikes, as well as other industrial disturbances. |

These risks could result in substantial losses due to personal injury and/or loss of life, severe damage to and destruction of property and equipment, and pollution or other environmental damage, as well as business interruptions or shutdowns of our facilities. Any such event or unplanned shutdown could have a material and adverse effect on our financial condition, results of operations, and cash flows and our ability to make distributions to our unitholders. In addition, Valero’s refining operations supported by our assets, on which our operations are substantially dependent and over which we have no control, are subject to similar operational hazards and risks inherent in refining crude oil.

Our insurance policies do not cover all losses, costs, or liabilities that we may experience, and insurance companies that currently insure companies in the energy industry may cease to do so or substantially increase premiums.

We do not maintain insurance coverage against all potential losses and could suffer losses for uninsurable or uninsured risks or in amounts in excess of existing insurance coverage. We maintain insurance policies for certain property damage, business interruption, and third-party liabilities, which includes pollution liabilities, and are subject to policy limits under these policies. The occurrence of an event that is not fully covered by insurance or failure by one or more insurers to honor its coverage commitments for an insured event could have a material and adverse effect on our financial condition, results of operations, and cash flows and our ability to make distributions to our unitholders. Insurance companies may reduce the insurance capacity they are willing to offer or may demand significantly higher premiums or deductibles to cover these facilities. If significant changes in the number or financial solvency of insurance underwriters for the energy industry occur, we may be unable to obtain and maintain adequate insurance at a reasonable cost. We cannot provide assurance that our insurers will renew our insurance coverage on acceptable terms, if at all, or that we will be able to arrange for adequate alternative coverage in the event of non-renewal. The unavailability of full insurance coverage to cover events in which we suffer significant losses could have a material and adverse effect on our financial condition, results of operations, and cash flows and our ability to make distributions to our unitholders.

We are exposed to the credit risks, and certain other risks, of our customers, and any material nonpayment or nonperformance by our customers could reduce our ability to make distributions to our unitholders.

We may in the future grow our customer base beyond Valero. We are subject to the risks of loss resulting from nonpayment or nonperformance by our customers, including Valero. If Valero or any other significant customer defaults on its obligations to us, our financial results could be adversely affected. Our customers may be highly leveraged and subject to their own operating and regulatory risks. Any material nonpayment or nonperformance by our customers could reduce our financial condition, results of operations, and cash flows and our ability to make distributions to our unitholders.

Our expansion of existing assets and construction of new assets may not result in revenue increases and will be subject to regulatory, environmental, political, legal, and economic risks, which could adversely affect our operations and financial condition.

In order to optimize our existing asset base, we intend to evaluate and capitalize on organic opportunities for expansion projects in order to increase revenues on our pipelines and terminals. The expansion of existing pipelines or terminals, such as by adding horsepower, pump stations, or loading racks, or the construction or expansion of new transportation and logistics assets, involves numerous regulatory, environmental, political, and legal uncertainties, most of which are beyond our control. If we undertake these projects, they

22

may not be completed on schedule or at all or at the budgeted cost. Moreover, we may not receive sufficient long-term contractual commitments from customers to provide the revenues needed to support such projects and we may be unable to negotiate acceptable interconnection agreements with third-party pipelines to provide destinations for increased throughput. Even if we receive such commitments or make such interconnections, we may not realize an increase in revenues for an extended period of time. As a result, new facilities may not be able to attract enough throughput to achieve our expected investment return, which could materially and adversely affect our financial condition, results of operations, and cash flows and our ability in the future to make distributions to our unitholders.

We do not own all of the land on which our assets are located, which could result in disruptions to our operations.

We do not own all of the land on which our assets are located, and we are, therefore, subject to the possibility of more onerous terms and increased costs to retain necessary land use if we do not have valid leases or rights-of-way or if such rights-of-way lapse or terminate. We obtain the rights to construct and operate our assets on land owned by third parties and governmental agencies, and some of our agreements may grant us those rights for only a specific period of time. Our loss of these rights, through our inability to renew leases, right-of-way contracts or otherwise, could have a material and adverse effect on our financial condition, results of operations, and cash flows and our ability to make distributions to our unitholders.

We are dependent upon third parties to operate some of our facilities.

Our McKee products system is operated by NuStar, which owns a 66⅔ percent undivided interest in the system. If NuStar fails to operate any portion of the McKee products system in accordance with the terms of our operating agreement with them, such failure could result in our inability to meet our commitments to Valero, which in turn could result in a reduction in our revenues, or in us becoming liable to Valero for any losses it may sustain by reason of our failure to comply, which losses may not be recoverable by us from NuStar. Similarly, our PAPS terminal is operated by Colonial, and any failure by Colonial or any successor-operator to comply with the terms of our operating agreement could result in our inability to meet our commitments to Valero with respect to our Port Arthur products system, which in turn could result in a reduction in our revenues, or in us becoming liable to Valero for any losses it may sustain by reason of our failure to comply, which losses may not be recoverable by us from the operator.

Restrictions in our revolving credit facility and subordinated credit agreements with Valero could adversely affect our business, financial condition, results of operations, ability to make distributions to our unitholders, and the value of our units.