Table of Contents

As filed with the Securities and Exchange Commission on June 8, 2015

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-22872

Steben Select Multi-Strategy Master Fund

(Exact name of registrant as specified in charter)

9711 Washingtonian Blvd.

Suite 400

Gaithersburg, Maryland 20878

(Address of principal executive offices) (Zip code)

Francine J. Rosenberger, Esq.

c/o Steben & Company, Inc.

9711 Washingtonian Blvd.

Suite 400

Gaithersburg, Maryland 20878

(Name and address of agent for service)

(240) 631-7600

Registrant’s telephone number, including area code

Date of fiscal year end: March 31

Date of reporting period: March 31, 2015

Table of Contents

Item 1. Reports to Stockholders.

Table of Contents

Steben Select Multi-Strategy Master Fund

Financial Statements

March 31, 2015

Table of Contents

Steben Select Multi-Strategy Master Fund

| Page | ||

| 1 | ||

| Financial Statements |

||

| 2 | ||

| 3 | ||

| 4 | ||

| 5 | ||

| 6 | ||

| 7-8 | ||

| 8 | ||

| 9-19 | ||

| 20 | ||

| 21-22 | ||

| 23 | ||

This report is intended for shareholders of the Funds and may not be used as sales literature unless preceded or accompanied by a current prospectus.

Table of Contents

Report of Independent Registered Public Accounting Firm

To the Board of Trustees and Shareholders of

Steben Select Multi-Strategy Master Fund:

We have audited the accompanying statement of assets and liabilities of Steben Select Multi-Strategy Master Fund (the “Master Fund”), including the schedule of investments and cash equivalents, as of March 31, 2015, and the related statements of operations and cash flows for the year then ended, the statements of changes in net assets and financial highlights for each of the periods in the two-year period then ended. These financial statements and financial highlights are the responsibility of the Master Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of March 31, 2015, by correspondence with the custodian and investees or by other appropriate auditing procedures. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Steben Select Multi-Strategy Master Fund as of March 31, 2015, the results of its operations and its cash flows for the year then ended, the changes in its net assets and the financial highlights for each of the periods in the two-year period then ended in conformity with U.S. generally accepted accounting principles.

| /s/ KPMG LLP |

| Columbus, Ohio |

| May 29, 2015 |

1

Table of Contents

Steben Select Multi-Strategy Master Fund

Statement of Assets and Liabilities

March 31, 2015

| ASSETS |

||||

| Investments in Portfolio Funds, at fair value (cost $36,550,000) |

$ | 44,073,830 | ||

| Cash Equivalents |

289,874 | |||

| Dividends receivable |

9 | |||

|

|

|

|||

| Total Assets |

44,363,713 | |||

|

|

|

|||

| LIABILITIES |

||||

| Management fees payable |

45,977 | |||

| Accrued operating services fee payable |

5,518 | |||

| Subscriptions received in advance |

220,000 | |||

|

|

|

|||

| Total Liabilities |

271,495 | |||

|

|

|

|||

| NET ASSETS |

$ | 44,092,218 | ||

|

|

|

|||

| Shares outstanding |

3,880,590 | |||

|

|

|

|||

| Net asset value per share (net assets/shares outstanding) |

$ | 11.36 | ||

|

|

|

|||

| COMPONENTS OF NET ASSETS |

||||

| Paid in capital |

$ | 40,643,389 | ||

| Accumulated net investment loss |

(3,902,170) | |||

| Accumulated net realized loss |

(172,831) | |||

| Net unrealized appreciation on investments |

7,523,830 | |||

|

|

|

|||

| Net Assets |

$ | 44,092,218 | ||

|

|

|

|||

See accompanying Notes to Financial Statements.

2

Table of Contents

Steben Select Multi-Strategy Master Fund

For the Year Ended March 31, 2015

| INVESTMENT INCOME |

||||

| Dividend income |

$ | 93 | ||

|

|

|

|||

| EXPENSES |

||||

| Management fees (Note 6) |

466,686 | |||

| Operating services fee (Note 6) |

56,009 | |||

|

|

|

|||

| Total Expenses |

522,695 | |||

|

|

|

|||

| Net Investment Loss |

(522,602) | |||

|

|

|

|||

| NET UNREALIZED GAIN (LOSS) ON INVESTMENTS |

||||

| Change in unrealized appreciation/depreciation on investments |

5,584,830 | |||

|

|

|

|||

| Net Increase in Net Assets from Operations |

$ | 5,062,228 | ||

|

|

|

|||

See accompanying Notes to Financial Statements.

3

Table of Contents

Steben Select Multi-Strategy Master Fund

Statements of Changes in Net Assets

| Year Ended March 31, 2015 |

For the Period August 1, 2014 (Commencement of Operations) through March 31, 2014 |

|||||||

| FROM OPERATIONS |

||||||||

| Net investment loss |

$ | (522,602) | $ | (174,010) | ||||

| Change in unrealized appreciation/depreciation on investments |

5,584,830 | 1,939,000 | ||||||

|

|

|

|

|

|||||

| Net Increase in Net Assets from Operations |

5,062,228 | 1,764,990 | ||||||

|

|

|

|

|

|||||

| FROM DISTRIBUTIONS |

||||||||

| Net investment income |

(2,869,136) | (336,422) | ||||||

| Net realized gain |

(172,831) | — | ||||||

|

|

|

|

|

|||||

| Net Decrease in Net Assets from Distributions |

(3,041,967) | (336,422) | ||||||

|

|

|

|

|

|||||

| FROM CAPITAL TRANSACTIONS |

||||||||

| Proceeds from sales of shares |

6,870,000 | 30,295,000 | ||||||

| Proceeds from reinvestment of distributions |

3,041,967 | 336,422 | ||||||

|

|

|

|

|

|||||

| Net Increase in Net Assets from Capital Transactions |

9,911,967 | 30,631,422 | ||||||

|

|

|

|

|

|||||

| Total Increase in Net Assets |

11,932,228 | 32,059,990 | ||||||

| NET ASSETS |

||||||||

| Beginning of period |

32,159,990 | 100,000 | ||||||

|

|

|

|

|

|||||

| End of period |

$ | 44,092,218 | $ | 32,159,990 | ||||

|

|

|

|

|

|||||

| Accumulated Net Investment Loss |

$ | (3,902,170) | $ | (510,432) | ||||

|

|

|

|

|

|||||

| SHARE TRANSACTIONS |

||||||||

| Shares sold |

618,369 | 2,937,318 | ||||||

| Shares reinvested |

283,092 | 31,811 | ||||||

|

|

|

|

|

|||||

| Total share transactions |

901,461 | 2,969,129 | ||||||

|

|

|

|

|

|||||

See accompanying Notes to Financial Statements.

4

Table of Contents

Steben Select Multi-Strategy Master Fund

For the Year Ended March 31, 2015

| CASH FLOWS FROM OPERATING ACTIVITIES |

||||

| Net increase in net assets from operations |

$ | 5,062,228 | ||

| Adjustments to reconcile net increase in net assets resulting from operations to net cash used in operating activities: |

||||

| Purchases of investments |

(6,450,000 | ) | ||

| Change in unrealized appreciation/depreciation on investments |

(5,584,830 | ) | ||

| Changes in operating assets and liabilities: |

||||

| Investments made in advance |

1,000,000 | |||

| Dividends receivable |

(1 | ) | ||

| Management fees payable |

12,442 | |||

| Accrued operating services fee payable

|

|

1,493

|

| |

|

|

|

|||

| Net Cash used in Operating Activities |

(5,958,668 | ) | ||

|

|

|

|||

| CASH FLOWS FROM FINANCING ACTIVITIES |

||||

| Proceeds from sales of shares |

6,870,000 | |||

| Distributions paid to shareholders |

(3,041,967 | ) | ||

| Proceeds from reinvestment of distributions |

3,041,967 | |||

| Change in Subscriptions received in advance |

(780,000 | ) | ||

|

|

|

|||

| Net Cash provided by Financing Activities |

6,090,000 | |||

|

|

|

|||

| Net Change in Cash and Cash Equivalents |

131,332 | |||

| CASH AND CASH EQUIVALENTS |

||||

| Beginning of period |

158,542 | |||

|

|

|

|||

| End of period |

$ | 289,874 | ||

|

|

|

|||

See accompanying Notes to Financial Statements.

5

Table of Contents

Steben Select Multi-Strategy Master Fund

Schedule of Investments and Cash Equivalents

March 31, 2015

| Redemptions | ||||||||||||||||

| Investments in Portfolio Funds(1): | Percentage of Net Assets |

Cost | Fair Value | Frequency | Notice Period No. of Days | |||||||||||

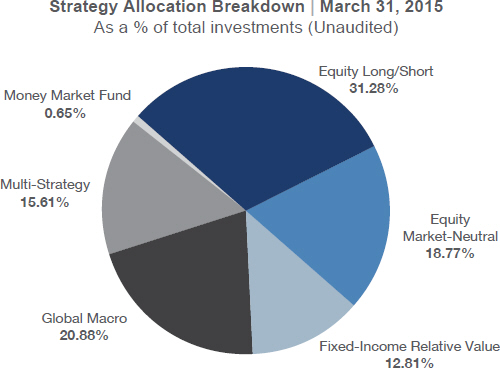

| Equity Long/Short Strategy: |

||||||||||||||||

| The Collectors’ Fund LP |

8.04 % | $ | 3,000,000 | $ | 3,547,209 | Quarterly | 45 | |||||||||

| Marshall Wace Eureka Fund Class B2 |

10.61 | 4,000,000 | 4,677,054 | Monthly | 30 | |||||||||||

| Visium Global Fund, LP |

12.82 | 5,250,000 | 5,654,049 | Monthly | 30 | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| 31.47 | 12,250,000 | 13,878,312 | ||||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Equity Market-Neutral Strategy: |

||||||||||||||||

| Voloridge Trading Fund LP |

18.89 | 6,500,000 | 8,328,343 | Monthly | 5 | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Fixed-Income Relative Value Strategy: |

||||||||||||||||

| The Obsidian (Offshore) Fund – Class V Series (2) |

12.89 | 5,100,000 | 5,683,162 | Monthly | 60 | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Global Macro Strategy: |

||||||||||||||||

| AHL (Cayman) SPC, Class A1 Evolution USD (2) |

10.76 | 3,500,000 | 4,742,769 | Monthly | 5 | |||||||||||

| Graham Absolute Return Ltd.(2) |

10.25 | 3,700,000 | 4,518,473 | Monthly | 30 | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| 21.01 | 7,200,000 | 9,261,242 | ||||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Multi-Strategy: |

||||||||||||||||

| Stratus Feeder Ltd. C USD 1.5 Leverage (2) |

15.70 | 5,500,000 | 6,922,771 | Monthly | 60 | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total Investments in Portfolio Funds: |

99.96 | 36,550,000 | 44,073,830 | |||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Cash Equivalents: |

||||||||||||||||

| Money Market Fund: |

||||||||||||||||

| Fidelity Institutional Money Market Portfolio – |

0.66 | 289,874 | 289,874 | |||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total Investments in Portfolio Funds and Cash Equivalents |

100.62 % | $ | 36,839,874 | $ | 44,363,704 | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| (1) | All Portfolio Funds are non-income producing. |

| (2) | Offshore Portfolio Fund. |

| (3) | 7-Day Yield. |

| (4) | Income Producing. |

See accompanying Notes to Financial Statements.

6

Table of Contents

Steben Select Multi-Strategy Master Fund

(Unaudited)

7

Table of Contents

Steben Select Multi-Strategy Master Fund

Portfolio Fund Strategies

(Unaudited)

8

Table of Contents

Steben Select Multi-Strategy Master Fund

March 31, 2015

(1) ORGANIZATION

Steben Select Multi-Strategy Master Fund (the “Master Fund”) is a Delaware statutory trust registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a non-diversified closed-end management investment company and serves as a master fund in a master-feeder structure. Steben Select Multi-Strategy Fund serves as a feeder fund in the master-feeder structure. The Master Fund has authorized unlimited common shares of beneficial interest (“Shares”), which may be issued in more than one class or series. Shares in the Master Fund are issued solely in private placement transactions that do not involve any “public offering” within the meaning of Section 4(2) of, and/or Regulation D under the Securities Act of 1933 (“Securities Act”). Investments in the Master Fund generally may be made only by U.S. and foreign investment companies or other investment vehicles that include persons who are “accredited investors” (“Shareholders”), as defined in Regulation D under the Securities Act.

The Master Fund’s investment objective is to seek capital appreciation with low long-term correlation to traditional public equity and fixed income markets. The Master Fund is a “fund of funds” and seeks to achieve its investment objective, primarily by allocating its assets, directly or indirectly, among investment partnerships, managed funds, securities, swaps and other assets held in segregated accounts and other investment funds, which may include investment funds commonly referred to as hedge funds, (collectively, “Portfolio Funds”) that are managed by third-party investment managers (“Portfolio Fund Managers”) that employ a variety of alternative investment strategies.

The Board of Trustees (the “Board” and each member a “Trustee”) is authorized to engage an investment adviser and it has selected Steben & Company, Inc. (the “Investment Manager”), to manage and oversee the Master Fund’s portfolio and operations, pursuant to an investment management agreement (the “Investment Management Agreement”). The Investment Manager is a Maryland corporation that is registered as an investment adviser under the Investment Advisers Act of 1940, as amended, and is registered with the Commodity Futures Trading Commission (the “CFTC”) as a commodity pool operator and a swap firm, and is a member of the National Futures Association as well as with the Securities and Exchange Commission (the “SEC”) as a broker-dealer. Under the Investment Management Agreement, the Investment Manager is responsible for developing, implementing, and supervising the Master Fund’s investment program subject to the supervision of the Board.

Under the Master Fund’s organizational documents, the Master Fund’s Trustees and officers are indemnified against certain liabilities arising out of the performance of their duties to the Master Fund. In the normal course of business, the Master Fund enters into contracts with service providers, which also provide for indemnifications by the Master Fund. The Master Fund’s maximum exposure under these arrangements is unknown, as this would involve any future potential claims that may be made against the Master Fund.

(2) SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES AND PRACTICES

(a) BASIS OF ACCOUNTING

The accounting and reporting policies of the Master Fund conform with U.S. generally accepted accounting principles (“U.S. GAAP”). The Master Fund is an investment company and follows accounting and reporting guidance under Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, “Financial Services-Investment Companies”.

9

Table of Contents

Steben Select Multi-Strategy Master Fund

Notes to Financial Statements

March 31, 2015

(b) VALUATION

Share Valuation

The Master Fund will calculate its Net Asset Value (“NAV”) as of the close of regular trading on the New York Stock Exchange (ordinarily 4:00 P.M.) on the last business day of each calendar month and such other dates as the Board may determine, including in connection with repurchase of Shares, in accordance with the procedures and policies established by the Board. The NAV of the Master Fund will equal the value of the total assets of the Master Fund, less all of its liabilities, including accrued fees and expenses.

Investment Valuation

The Investment Manager’s Valuation Committee implements the valuation of the Master Fund’s investments, including interests in the Portfolio Funds, in accordance with written policies and procedures (the “Valuation Procedures”) that the Board of the Master Fund has approved for purposes of determining the value of securities held by the Master Fund, including the fair value of the Master Fund’s investments in Portfolio Funds. The Investment Manager’s Valuation Committee consists of members of the Board, additional officers of the Master Fund, and one or more representatives of the Investment Manager.

Investments are carried at fair value. As a general matter, the fair value of the Master Fund’s investment in a Portfolio Fund represents the amount that the Master Fund can reasonably expect to receive if the Master Fund’s investment was sold at its reported NAV. Determination of fair value involves subjective judgment and amounts ultimately realized may vary from estimated values. The fair value of the Portfolio Funds has been estimated using the NAV as reported by the Portfolio Fund Managers of the respective Portfolio Funds. FASB guidance provides for the use of NAV as a “Practical Expedient” for estimating fair value of the Portfolio Funds. NAV reported by each Portfolio Fund is used as a practical expedient to estimate the fair value of the Master Fund’s interest therein and their classification within Level 2 or 3 is based on the Master Fund’s ability to redeem its interest in the near term and liquidate the underlying portfolios.

Certain securities and other financial instruments in which the Portfolio Funds invest may not have readily ascertainable market prices and will be valued by the Portfolio Fund Managers. Such valuations generally will be conclusive with respect to the Master Fund, even though a Portfolio Fund Manager may face a conflict of interest in valuing the securities, as their value will impact the Portfolio Fund Manager’s compensation. Generally, neither the Investment Manager nor the Board will be able to confirm independently the accuracy of the valuations made by the Portfolio Fund Managers. The net asset values or other valuation information received by the Investment Manager from the Portfolio Funds will typically be estimates only, subject to revision through the end of each Portfolio Fund’s annual audit. The valuations reported by the Portfolio Fund Managers, upon which the Master Fund will calculate its NAV, may be subject to later adjustment based on information reasonably available at that time. To the extent that subsequently adjusted valuations or revisions to Portfolio Fund net asset values adversely affect the Master Fund’s NAV, the outstanding Shares of the Master Fund will be adversely affected by prior repurchases to the benefit of Shareholders who previously had Shares repurchased at a NAV per share higher than the adjusted amount. Conversely, any increases in the net asset value resulting from such subsequently adjusted valuations will be entirely for the benefit of the outstanding Shares and to the detriment of Shareholders who previously had Shares repurchased at a NAV per share lower than the adjusted amount.

10

Table of Contents

Steben Select Multi-Strategy Master Fund

Notes to Financial Statements

March 31, 2015

Under the Valuation Procedures, if the Master Fund, acting reasonably and in good faith, determines that a Portfolio Fund Manager cannot provide valuation of a Portfolio Fund or if the Master Fund determines that the valuation provided by a Portfolio Fund Manager does not represent the fair value of the Master Fund’s interest in a Portfolio Fund, the Master Fund may utilize any other reasonable valuation methodology to determine the fair value of the Portfolio Fund. Although redemptions of interests in Portfolio Funds normally are subject to advance notice requirements, Portfolio Funds typically will make available NAV information to holders representing the price at which, even in the absence of redemption activity, the Portfolio Fund would have effected a redemption if any such requests had been timely made or if, in accordance with the terms of the Portfolio Fund’s governing documents, it would be necessary to effect a mandatory redemption. In the absence of specific transaction activity in interests in a particular Portfolio Fund, the Master Fund would consider whether it was appropriate, in light of all relevant circumstances, to value such a position at its NAV as reported by the Portfolio Fund, or whether to adjust such value to reflect a premium or discount to such NAV.

In making a fair value determination, the Master Fund will consider all appropriate information reasonably available to it at the time and that the Investment Manager believes to be reliable. The Master Fund may consider factors such as, among others: (i) the price at which recent purchases for or redemptions of the Portfolio Fund’s interests were effected; (ii) information provided to the Master Fund by a Portfolio Fund Manager, or the failure to provide such information as the Portfolio Fund Manager agreed to provide in the Portfolio Fund’s offering materials or other agreements with the Master Fund; (iii) relevant news and other sources; and (iv) market events. In addition, when a Portfolio Fund imposes extraordinary restrictions on redemptions, or when there have been no recent subscriptions for Portfolio Fund interests, the Master Fund may determine that it is appropriate to apply a discount to the NAV reported by the Portfolio Fund. The Board reviews all valuation adjustments, which would be undertaken pursuant to the Board-approved policy and procedures.

To the extent that the Investment Manager invests the assets of the Master Fund in securities or other instruments that are not investments in Portfolio Funds (e.g., directly or through separate accounts), the Master Fund will generally value such assets as described below. Securities traded: (1) on one or more of the U.S. national securities exchanges or the OTC Bulletin Board will be valued at their last sales price; and (2) on the NASDAQ Stock Market will be valued at the NASDAQ Official Closing Price (“NOCP”), at the close of trading on the exchanges or markets where such securities are traded for the business day as of which such value is being determined. Securities traded on the NASDAQ Stock Market for which the NOCP is not available will be valued at the mean between the closing bid and asked prices in this market. Securities traded on a foreign securities exchange will generally be valued at their closing prices on the exchange where such securities are primarily traded and such valuations translated into U.S. dollars at the current exchange rate. If an event occurs between the close of the foreign exchange and the computation of the Master Fund’s NAV that would materially affect the value of the security, the value of such security will be adjusted to its fair value. Except as specified above, the value of a security, derivative, or synthetic security that is not actively traded on an exchange shall be determined by an unaffiliated pricing service that may use actual trade data or procedures using market indices, matrices, yield curves, specific trading characteristics of certain groups of securities, pricing models, or combinations of these. The Investment Manager’s Valuation Committee will monitor the value assigned to each security by the pricing service to determine if it believes the value assigned to a security is correct. If the Investment Manager’s Valuation Committee believes that the value received from the pricing service is incorrect, then the value of the security will be its fair value as determined in accordance with the Valuation Procedures.

11

Table of Contents

Steben Select Multi-Strategy Master Fund

Notes to Financial Statements

March 31, 2015

(c) CFTC REGULATION

On August 13, 2013, the CFTC adopted rules to harmonize conflicting SEC and CFTC disclosure, reporting and recordkeeping requirements for registered investment companies that do not meet an exemption from the definition of commodity pool. The harmonization rules provide that the CFTC will accept the SEC’s disclosure, reporting, and recordkeeping regime as substituted compliance for substantially all of the otherwise applicable CFTC regulations as long as such investment companies meet the applicable SEC requirements.

Previously, in November 2012, the CFTC issued relief for fund of fund operators, including advisers to registered investment companies that may otherwise be required to register with the CFTC as commodity pool operators but do not have access to information from the investment funds in which they are invested in order to determine whether such registration is required. This relief delayed the registration date for such operators until the later of June 30, 2013 or six months from the date the CFTC issues revised guidance on the application of certain thresholds with respect to investments in commodities held by funds of funds.

In July 2013, the Investment Manager claimed no-action relief from the CFTC registration with respect to its operation of the Master Fund. Although the CFTC now has adopted harmonization rules applicable to investment companies that are deemed to be commodity pools, the CFTC has not yet issued guidance on how funds of funds are to determine whether they are deemed to be commodity pools. As of March 31, 2015, the Master Fund is not considered a commodity pool and continues to rely on the fund of fund no-action relief.

(d) CASH EQUIVALENTS

The Master Fund considers all unpledged temporary cash investments of sufficient credit quality with a maturity date at the time of purchase of three months or less to be cash equivalents. The Master Fund considers U.S. regulated money market funds to be cash equivalents.

(e) SECURITY TRANSACTIONS AND INVESTMENT INCOME RECOGNITION

Purchases and sales of securities are recorded on a trade-date basis. For investments in securities, interest income is recorded on the accrual basis and dividends are recorded on the ex-dividend date. Realized gains or losses on the disposition of investments are accounted for based on the specific identification method. Investments that are held by the Master Fund are marked to fair value at the date of the financial statements, and the corresponding change in unrealized appreciation/depreciation is included in the Statement of Operations.

(f) FEDERAL INCOME TAXES

The Master Fund intends to continue to qualify as a Regulated Investment Company (“RIC”) by complying with the provisions available to certain investment companies, as defined in Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”), and to make distributions from net investment income and from net realized capital gains sufficient to relieve it from all, or substantially all, federal income and excise taxes. Investments in foreign securities may result in foreign taxes being withheld by the issuer of such securities.

The Master Fund has a tax year end of October 31st.

The Master Fund has adopted financial reporting rules regarding recognition and measurement of tax positions taken or expected to be taken on a tax return. Management has reviewed all open tax years and major jurisdictions and concluded that no provision for income tax would be required in the Master Fund’s financial

12

Table of Contents

Steben Select Multi-Strategy Master Fund

Notes to Financial Statements

March 31, 2015

statements. The Master Fund’s Federal and state income and Federal excise tax returns for tax years for which the applicable statutes of limitations have not expired are subject to examination by the Internal Revenue Service and state departments of revenue.

As of October 31, 2014 (the Master Fund’s tax year end), the tax cost of securities and components of distributable earnings on a tax basis were as follows:

| Cost basis of investments for federal income tax purposes |

$ | 36,182,799 | ||

|

|

|

|||

| Gross tax unrealized appreciation |

4,078,432 | |||

| Gross tax unrealized depreciation |

(2,788,382) | |||

|

|

|

|||

| Net tax unrealized appreciation |

1,290,050 | |||

|

|

|

|||

| Undistributed ordinary income |

1,921,376 | |||

|

|

|

|||

| Total distributable earnings |

$ | 3,211,426 | ||

|

|

|

At October 31, 2014, the Master Fund had no capital loss carry forwards.

Under current law, capital losses and specified ordinary losses realized after October 31 and non-specified ordinary losses incurred after December 31 (ordinary losses collectively known as “qualified late year ordinary loss”) may be deferred and treated as occurring on the first business day of the following fiscal year.

The Master Fund had no deferred losses at October 31, 2014.

The Master Fund distributed $336,422 of ordinary income during the period November 1, 2013 through October 31, 2014, and made no distributions for the period August 1, 2013 (commencement of operations) through October 31, 2013.

(g) USE OF ESTIMATES

The preparation of the financial statements in accordance with U.S. GAAP requires management to make estimates and assumptions relating to the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expense during the reporting period. Actual results could differ from those estimates and such differences may be significant.

(h) FUND EXPENSES

Pursuant to the Operating Services Agreement with the Master Fund, the Investment Manager has contractually agreed to pay all of the Master Fund’s ordinary operating expenses so long as Steben & Company, Inc. remains the Investment Manager, including the Master Fund’s organizational and offering expenses but not the following Master Fund expenses: the Management Fee, borrowing costs, interest expenses, brokerage commissions and other transaction and investment-related costs, portfolio fund and portfolio fund manager fees and expenses, taxes and governmental fees, acquired fund fees and expenses, shareholder servicing fees, litigation and indemnification expenses, judgments and other extraordinary expenses not incurred in the ordinary course of the Master Fund’s business. The Operating Services Agreement may be terminated at any time by the Board or upon 60 days written notice by the Master Fund or the Investment Manager. See Note 6 – Related Party Transactions.

U.S. Bancorp Fund Services, LLC provides accounting, administrative and transfer agency services to the Master Fund. U.S. Bank, N.A. provides custodian services to the Master Fund.

13

Table of Contents

Steben Select Multi-Strategy Master Fund

Notes to Financial Statements

March 31, 2015

(i) SHAREHOLDER ACCOUNTS

Issuance of Shares

All purchases accepted by the Master Fund are accepted at the end of the month, and the NAV of Shares is determined as of the close of business on the last day of that month. Purchases accepted by the Master Fund become effective as of the opening of business on the first calendar day of the month based on the previous month-end NAV of the Master Fund Shares.

Prior to the end of each month, the Master Fund receives Shareholder contributions with an effective subscription date of the first day of the following month. The Master Fund, in turn, makes contributions to certain Portfolio Funds, which have effective subscription dates of the first day of the following month. These amounts are reported as “Subscriptions received in advance” and “Investments made in advance”, respectively.

The Master Fund reserves the right to reject in whole or in part, in its sole discretion, any request to purchase Shares at any time.

Repurchase of Shares

No Shareholder will have the right to require the Master Fund to redeem his, her or its Shares (or any portion thereof). The Master Fund from time to time may offer to repurchase Shares pursuant to written tenders by the Shareholders. These repurchases are made at such times and on such terms as may be determined by the Board from time to time in its sole discretion. With respect to any future repurchase offer, Shareholders tendering Shares for repurchase must do so by a date specified in the notice describing the terms of the repurchase offer, which will generally be approximately 75 days prior to the date that the Shares to be repurchased are valued by the Master Fund (the “Valuation Date”). The Master Fund may elect to repurchase less than the full amount that a Shareholder requests to be repurchased. If a repurchase offer is oversubscribed by Shareholders who tender Shares, the Master Fund may repurchase a pro rata portion of the Shares tendered by each Shareholder, extend the repurchase offer, or take any other action with respect to the repurchase offer permitted by applicable law. In addition, the Master Fund has the right to repurchase Shares of Shareholders if the Master Fund determines that the repurchase is in the best interest of the Master Fund or upon the occurrence of certain events specified in the Master Fund’s Declaration of Trust.

(j) DIVIDENDS AND DISTRIBUTIONS TO SHAREHOLDERS

Dividends will generally be paid at least annually on the Master Fund’s Shares in amounts representing substantially all of the net investment income, if any, earned each year. Payments will vary in amount, depending on investment income received and expenses of operation. It is likely that many of the Portfolio Funds in whose securities the Master Fund invests will not pay any dividends, and this, together with the Master Fund’s expenses, means that there can be no assurance the Master Fund will have substantial income or pay dividends.

It is anticipated that any gains or appreciation in the Master Fund’s investments will be treated as ordinary income or long term capital gains. Such amounts will generally be distributed at least annually and such distributions would be taxed as ordinary income dividends or long term capital gains to Shareholders that are subject to tax.

14

Table of Contents

Steben Select Multi-Strategy Master Fund

Notes to Financial Statements

March 31, 2015

It is anticipated that substantially all of any taxable net capital gain realized on investments will be paid to Shareholders at least annually. The NAV per share (or portion thereof) that a Shareholder owns will be reduced by the amount of the distributions or dividends that the Shareholder actually or constructively receives from that share (or portion thereof).

Pursuant to a dividend reinvestment plan established by the Master Fund (the “Dividend Reinvestment Plan”), each Shareholder will automatically be a participant under the Dividend Reinvestment Plan and have all income distributions, whether dividend distributions and/or capital gains distributions, automatically reinvested in additional Shares. Election not to participate in the Dividend Reinvestment Plan and to receive all income distributions, whether dividend distributions or capital gain distributions, in cash may be made by notice to a Shareholder’s intermediary (who should be directed to inform the Master Fund). A Shareholder is free to change this election at any time. If, however, a Shareholder requests to change its election within 95 days prior to a distribution, the request will be effective only with respect to distributions after the 95-day period. A Shareholder whose Shares are registered in the name of a nominee (such as an Intermediary) must contact the nominee regarding its status under the Dividend Reinvestment Plan, including whether such nominee will participate on such Shareholder’s behalf as such nominee will be required to make any such election.

Generally, for U.S. federal income tax purposes, Shareholders receiving Shares under the Dividend Reinvestment Plan will be treated as having received a distribution equal to the amount payable to them in cash as a distribution had the Shareholder not participated in the Dividend Reinvestment Plan.

Shares will be issued pursuant to the dividend reinvestment plan at their NAV determined on the next valuation date following the record date (the last date of a dividend period on which an investor can purchase Shares and still be entitled to receive the dividend). There is no sales load or other charge for reinvestment. A request must be received by the Master Fund before the record date to be effective for that dividend or capital gain distribution. The Master Fund may terminate the Dividend Reinvestment Plan at any time upon written notice to the participants in the Dividend Reinvestment Plan. The Master Fund may amend the Dividend Reinvestment Plan at any time upon 30 day’s written notice to the participants. Any expenses of the Dividend Reinvestment Plan will be borne by the Master Fund.

(3) INVESTMENTS

The Master Fund follows fair valuation accounting standards which establish an authoritative definition of fair value and set out a hierarchy for measuring fair value. These standards require additional disclosures about the various inputs and valuation techniques used to develop the measurements of fair value and a discussion in changes in valuation techniques and related inputs during the period. These standards define fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The fair value hierarchy is organized into three levels based upon the assumptions (referred to as “inputs”) used in pricing the asset or liability. These standards state that “observable inputs” reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from independent sources and “unobservable inputs” reflect an entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability. These inputs are summarized in the three broad levels listed below:

Level 1 - Unadjusted quoted prices in active markets for identical investments and registered investment companies where the value per share (unit) is determined and published and is the basis for current transactions for identical assets or liabilities at the valuation date.

15

Table of Contents

Steben Select Multi-Strategy Master Fund

Notes to Financial Statements

March 31, 2015

Level 2 - Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly or investments that can be fully redeemed at the NAV in the “near term”. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level 3 - Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Master Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available or investments that cannot be fully redeemed at the NAV in the “near term”; these are investments that generally have one or more of the following characteristics: gated redemptions, suspended redemptions, or have lock-up periods greater than quarterly.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in these securities.

The Master Fund invests in Portfolio Funds, and classifies those investments as Level 2 or Level 3 depending on the Master Fund’s ability to redeem its interest in the near term. Portfolio Fund investments for which the Master Fund can liquidate its investment within 90 days are classified as Level 2.

The following are the classes of investments grouped by the fair value hierarchy for those investments measured at fair value on a recurring basis at March 31, 2015. The Portfolio Funds below were valued using the NAV as the practical expedient:

| Description |

(Level 1) | (Level 2) | (Level 3) | Total | ||||||||||||

| Investments in Portfolio Funds |

||||||||||||||||

| Equity Long/Short Strategy |

$ | — | $ | 13,878,312 | $ | — | $ | 13,878,312 | ||||||||

| Equity Market-Neutral Strategy |

— | 8,328,343 | — | 8,328,343 | ||||||||||||

| Fixed-Income Relative Value Strategy |

— | 5,683,162 | — | 5,683,162 | ||||||||||||

| Global Macro Strategy |

— | 9,261,242 | — | 9,261,242 | ||||||||||||

| Multi-Strategy |

— | 6,922,771 | — | 6,922,771 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total Investments in Portfolio Funds |

— | 44,073,830 | — | 44,073,830 | ||||||||||||

| Cash Equivalents |

||||||||||||||||

| Money Market Fund |

289,874 | — | — | 289,874 | ||||||||||||

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total Investments in Portfolio Funds and Cash Equivalents |

$ | 289,874 | $ | 44,073,830 | $ | — | $ | 44,363,704 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

The Master Fund discloses transfers between levels based on valuations at the end of the reporting period. For the year ended March 31, 2015, there were no transfers in or out of Level 1, Level 2 or Level 3 of the fair value hierarchy. Transfers between Levels 2 and 3 in the fair value hierarchy generally relate to changes in liquidity provisions of the Portfolio Funds.

16

Table of Contents

Steben Select Multi-Strategy Master Fund

Notes to Financial Statements

March 31, 2015

In May 2015, the FASB issued ASU No. 2015-07 “Disclosures for Investments in Certain Entities That Calculate Net Asset Value per Share (or Its Equivalent).” ASU No. 2015-07 states that investments measured using net asset value per share (or its equivalent) as a practical expedient shall not be categorized within the fair value hierarchy and the reporting entity shall provide the amount measured using the net asset value per share (or its equivalent) practical expedient to permit reconciliation of the fair value of investments included in the fair value hierarchy to the line items presented in the statement of financial position. ASU No. 2015-07 also requires a reporting entity to disclose information that helps users to understand the nature, characteristics, and risks of the investments by class and whether the investments, if sold, are probable of being sold at amounts different from net asset value per share. The changes to disclosures are required for annual reporting periods beginning after December 15, 2015 and interim periods within those annual periods. Management is currently evaluating the potential impact of these new disclosures on the Master Fund’s financial statements.

(4) INVESTMENT RISKS AND UNCERTAINTIES

Portfolio Funds consist of non-traditional, not readily marketable investments, some of which may be structured as offshore limited partnerships, venture capital funds, hedge funds, private equity funds and common trust funds. The underlying investments of such funds, whether invested in stock or other securities, are generally not currently traded in a public market and typically are subject to restrictions on resale. Values determined by Portfolio Fund Managers and general partners of underlying securities that are thinly traded or not traded in an active market may be based on historical cost, appraisals, a review of the investees’ financial results, financial condition and prospects, together with comparisons to similar companies for which quoted market prices are available or other estimates that require varying degrees of judgment.

Investments are carried at fair value provided by the respective Portfolio Fund Managers. Because of the inherent uncertainty of valuations, the estimated fair values may differ from the values that would have been used had a ready market for such investments existed or had such investments been liquidated, and those differences could be material.

(5) CONCENTRATION, LIQUIDITY AND OFF-BALANCE SHEET RISK

The Master Fund invests primarily in Portfolio Funds that are not registered under the 1940 Act and invest in actively traded securities, illiquid securities, derivatives and other financial instruments using different strategies and investment techniques, including leverage, which may involve significant risks. These Portfolio Funds may invest a high percentage of their assets in specific sectors of the market in order to achieve a potentially greater investment return. As a result, the Portfolio Funds may be more susceptible to economic, political, and regulatory developments in a particular sector of the market, positive or negative, and may experience increased volatility of the Portfolio Funds’ net asset value.

Various risks are also associated with an investment in the Master Fund, including risks relating to the fund-of-funds structure of the Master Fund, risks relating to compensation arrangements and risks relating to limited liquidity, as described below.

Redemption restrictions exist for Portfolio Funds whereby the Portfolio Fund Managers may suspend redemption either in their sole discretion or other factors. Such factors include the magnitude of redemptions requested, portfolio valuation issues or market conditions.

17

Table of Contents

Steben Select Multi-Strategy Master Fund

Notes to Financial Statements

March 31, 2015

In the normal course of business, the Portfolio Funds in which the Master Fund invests trade various financial instruments and enter into various investment activities with off-balance sheet risk. These include, but are not limited to, short selling activities, writing option contracts, contracts for differences, and interest rate, credit default and total return equity swap contracts. The Master Fund’s risk of loss in these Portfolio Funds is limited to the value of its own investments reported in these financial statements by the Master Fund. The Master Fund itself does not invest directly in securities with off-balance sheet risk.

(6) RELATED PARTY TRANSACTIONS

(a) INVESTMENT MANAGEMENT FEE

Under the terms of the Investment Management Agreement between the Investment Manager and the Master Fund, the Investment Manager is entitled to receive a management fee at an annualized rate, based on the month-end net assets of the Master Fund of 1.25%, accrued and payable monthly. For the year ended March 31, 2015, the Master Fund incurred $466,686 in management fees.

(b) OPERATING SERVICES FEE

The Master Fund pays to the Investment Manager, as compensation for the services provided by the Investment Manager and its agents under the Operating Services Agreement, an annualized fee of 0.15%, which is paid monthly, based on the month-end net assets of the Master Fund. For the year ended March 31, 2015, the Master Fund incurred $56,009 in operating services fees.

(7) COMPENSATION FOR TRUSTEES

The independent Trustees are paid annual compensation for service on the Board and its Committees for the portfolios overseen in the complex of funds advised by the Investment Manager “SCI Advised Funds” in an annual amount of $15,000 each. Such compensation encompasses attendance and participation at Board and Committee meetings, including telephonic meetings, if any. There are currently two independent Trustees. The Audit Committee Chairman and the Audit Committee Financial Expert also receives an annual amount of $15,000. In the interest of recruiting and retaining independent Trustees of high quality, the Board intends to periodically review such compensation and may modify it as the Board deems appropriate. In addition, through the Operating Services Agreement, the Investment Manager reimburses each independent Trustee for travel and other expenses incurred in connection with attendance at such meetings. Other Officers (apart from the CCO) and Trustees of the Master Fund who are “interested persons” by virtue of their affiliation with the Investment Manager receive no compensation in such role.

(8) INVESTMENT TRANSACTIONS

During the year ended March 31, 2015 (excluding short-term securities), the aggregate purchases of investments were $6,450,000 and sales of investments were $0. The Master Fund did not purchase long-term U.S. Government securities as a part of its investment strategy during the year ended March 31, 2015.

(9) SUBSEQUENT EVENTS

The Master Fund offered to repurchase Shares in an amount up to 20% of the net assets of the Master Fund, calculated as of June 30, 2015 (the “Repurchase Valuation Date”), and each Share tendered for repurchase will be purchased at the net asset value per Share calculated on that date. Shareholders desiring to tender Shares

18

Table of Contents

Steben Select Multi-Strategy Master Fund

Notes to Financial Statements

March 31, 2015

for repurchase had to do so by 12:00 midnight, Eastern Time on April 24, 2015 (the “Notice Date”). Shareholders had the right to change their minds and withdraw any tenders of their Shares until 12:00 midnight, Eastern Time on April 24, 2015 (the “Expiration Date”). If the Master Fund accepts the tender of the Shareholder’s Shares, the Master Fund will make payment for the Shares it repurchases within 30 days of the Repurchase Valuation Date.

No shares were repurchased during the year ended March 31, 2015, and no requests for repurchase were received by the Expiration Date.

The Master Fund has adopted financial reporting rules regarding subsequent events, which requires an entity to recognize in the financial statements the effects of all subsequent events that provide additional evidence about conditions that existed at the date of the balance sheet. Management has evaluated the Master Fund’s related events and transactions that occurred subsequent to March 31, 2015 and determined that there were no additional significant subsequent events that would require adjustment to or additional disclosure in these financial statements.

19

Table of Contents

Steben Select Multi-Strategy Master Fund

| Year Ended March 31, 2015 |

For the Period August 1, 2013 (Commencement of Operations) through March 31, 2014 |

|||||||

| PER SHARE OPERATING PERFORMANCE |

||||||||

| Net Asset Value, beginning of period |

$ | 10.80 | $ | 10.00 | ||||

|

|

|

|

|

|||||

| Income (loss) from investment operations: |

||||||||

| Net Investment Loss |

(0.16) (1) | (0.10) (1)(2) | ||||||

| Net Unrealized Gain on Investments |

1.64 | 1.04 | ||||||

|

|

|

|

|

|||||

| Total From Investment Operations |

1.48 | 0.94 | ||||||

|

|

|

|

|

|||||

| Less distributions: |

||||||||

| From net investment income |

(0.87) | (0.14) | ||||||

| From net realized gains |

(0.05) | — | ||||||

|

|

|

|

|

|||||

| Total distributions |

(0.92) | (0.14) | ||||||

|

|

|

|

|

|||||

| Net Asset Value, end of period |

$ | 11.36 | $ | 10.80 | ||||

|

|

|

|

|

|||||

| TOTAL RETURN |

14.26% | 9.35%(3) | ||||||

| RATIOS/SUPPLEMENTAL DATA |

||||||||

| Net Assets, end of period ($000’s) |

$ | 44,092 | $ | 32,160 | ||||

| Portfolio Turnover |

0.00% | 0.00% (3) | ||||||

| Ratio of Net Investment Loss to Average Net Assets |

(1.40)% (4) | (1.40)% (4)(5) | ||||||

| Ratio of Expenses to Average Net Assets |

1.40% (4)(6) | 1.40% (4)(5)(6) | ||||||

| (1) | Net investment loss per share represents net investment loss divided by the average shares outstanding throughout the period. |

| (2) | Due to the timing of capital share transactions, the per share amount of loss from investment operations varies from amounts shown in the statement of operations. |

| (3) | Not Annualized. |

| (4) | Ratios are calculated by dividing the indicated amount by average net assets measured at the end of each month during the period. |

| (5) | Annualized. |

| (6) | The ratio of expenses to average net assets does not include expenses of the Portfolio Funds that are paid indirectly by the Master Fund as a result of its ownership of the Portfolio Funds. |

See accompanying Notes to Financial Statements.

20

Table of Contents

Steben Select Multi-Strategy Master Fund

Trustee and Officer Information

(Unaudited)

The Master Fund’s operations are managed under the direction and oversight of the Master Fund’s Board. Each Trustee serves for an indefinite term or until he or she reaches mandatory retirement, if any, as established by the Board. The Board appoints officers of the Master Fund who are responsible for the Master Fund’s and day-today business decisions based on policies set by the Board. Biographical information for the current Trustees and Officers, including age, principal occupations for the past five years, the length of time served as Trustee, the number of portfolios overseen in the complex of funds advised by the Investment Manager (“SCI Advised Funds”) and any public Director/Trusteeships is set forth below. The Statement of Additional Information includes additional information about Trustees and Officers and is available, without charge by visiting www.steben.com.

Independent Trustees*

| Name and Age | Position(s) with Fund |

Number of

|

Principal Occupation(s) During the Past 5 Years |

Other Directorships During the Past 5 Years | ||||

| George W. Morriss#

Age: 67 |

Trustee (Since 2013) | 3 | Adjunct Professor, Columbia University School of International and Public Affairs, since October 2012; formerly, Executive Vice President and Chief Financial Officer, People’s Bank, Connecticut (a financial services company), from 1991 to 2001. | Trustee of Neuberger & Berman Funds complex (which consists of 55 funds), since 2007; formerly, Manager, Larch Lane Multi-Strategy Fund complex (which consisted of three funds), 2006 to 2011; formerly, Member, NASDAQ Issuers’ Affairs Committee, 1995 to 2003; Steben Select Multi-Strategy Fund and Steben Select Multi-Strategy Master Fund (investment companies)(two funds). | ||||

| Mark E. Schwartz#

Age: 67 |

Trustee (Since 2013) | 3 | President, TriCapital Advisors, Inc., since 2006. | Steben Select Multi-Strategy Fund and Steben Select Multi-Strategy Master Fund (investment companies)(two funds). | ||||

Interested Trustees*

| Name and Age |

Position(s) with Fund |

Number of Portfolios in SCI Advised Fund Complex Overseen by Trustee

|

Principal Occupation(s) During the Past 5 Years |

Other Directorships During the Past 5 Years | ||||

| Kenneth E. Steben**

Age: 60 |

Trustee and Chief Executive Officer (Since 2013) |

3 | President and Chief Executive Officer since 1989 of Steben & Company, Inc. | Steben Select Multi-Strategy Fund and Steben Select Multi-Strategy Master Fund (investment companies)(two funds). | ||||

| * | There is no stated term of office for the Fund’s Trustees. Each Trustee serves until his or her successor is elected and qualifies or until his or her death, resignation, or removal as provided in the Declaration of Trust, Bylaws or by statute. |

| ** | Mr. Steben is an “interested person”, as defined in the Investment Company Act, due to his position as President and Chief Executive Officer of the Investment Manager. |

| # | Member of the Audit Committee and the Governance and Nominating Committee. |

21

Table of Contents

Steben Select Multi-Strategy Master Fund

Officers of the Fund Who Are Not Trustees

| Name and Age | Position(s) with Fund |

Principal Occupation(s) During the Past 5 Years

| ||

| Francine J. Rosenberger Age: 47 |

Chief Compliance Officer (“COO”) and Secretary (Since 2013)

|

General Counsel, SCI, since January 2013; Partner, K&L Gates LLP (law firm) from 2003 to January 2013. | ||

| Carl Serger Age: 55 |

Chief Financial Officer (Since 2013) |

Chief Financial Officer, SCI, since December 2009; Senior VP, CFO and COO, Peracon, Inc. (electronic transactions platform) from 2007 to 2009; Independent Consultant in 2007; Senior VP and CFO, Ebix (software company) from 2006 to 2007; CFO, Senior VP and Treasurer, Finetre Corporation (financial technology platform company) from 1999 to 2006.

| ||

22

Table of Contents

Steben Select Multi-Strategy Master Fund

(Unaudited)

Proxy Voting Policies and Procedures

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities, as well as information on how the Fund voted proxies (if any) relating to portfolio securities during the most recent 12-month period ended June 30 after commencement of operations will be available on Form N-PX without charge by calling 1.800.726.3400, or on the SEC’s website at http://www.sec.gov.

Portfolio Holdings Disclosure

The Fund will file its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q will be available on the SEC’s website at www.sec.gov, and may also be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1.800.732.0330.

Privacy Policy

The Fund collects non-public information about you from the following sources:

| • | information we receive about you on applications or other forms; |

| • | information you give us orally; and |

| • | information about your transactions with us or others. |

We do not disclose any non-public personal information about our customers or former customers without the customer’s authorization, except as required by law or in response to inquiries from governmental authorities. We also disclose that information is provided to unaffiliated third parties (such as to the investment advisor to the Fund, and to brokers and custodians) only as permitted by law and only as needed for them to assist us in providing agreed services to you. All shareholder records will be disposed of in accordance with applicable law. We maintain physical, electronic and procedural safeguards to guard your nonpublic personal information.

In the event that you hold shares of the Fund through a financial intermediary, including, but not limited to, a broker-dealer, bank or trust company, the privacy policy of your financial intermediary would govern how your non-public personal information would be shared by those entities with nonaffiliated third parties.

23

Table of Contents

Steben Select Multi-Strategy Fund

For More Information

| Investment Adviser

Steben & Company, Inc. 9711 Washingtonian Blvd., Suite 400 Gaithersburg, MD 20878

|

Fund Administrator, Transfer Agent and Fund Accountant

U.S. Bancorp Fund Services, LLC 615 East Michigan St. Milwaukee, WI 53202

| |

| Custodian

U.S. Bank, N.A. Custody Operations 1555 North RiverCenter Dr., Suite 302 Milwaukee, WI 53212

|

Distributor

Foreside Fund Services, LLC Three Canal Plaza, Suite 100 Portland, ME 04101

| |

| Independent Registered Public Accounting Firm

KPMG LLP 191 W Nationwide Blvd., Suite 500 Columbus, OH 43215

|

Fund Counsel

K&L Gates, LLP State Street Financial Center One Lincoln Street Boston, MA 02111

| |

24

Table of Contents

Item 2. Code of Ethics.

The registrant has adopted a code of ethics that applies to the registrant’s principal executive officer and principal financial officer. The registrant has not made any amendments to its code of ethics during the period covered by this report. The registrant has not granted any waivers from any provisions of the code of ethics during the period covered by this report. A copy of the registrant’s Code of Ethics is filed herewith.

Item 3. Audit Committee Financial Expert.

The registrant’s Board of Trustees has determined that there is at least one audit committee financial expert serving on its audit committee. George Morriss is the “audit committee financial expert” and is considered to be “independent” as each term is defined in Item 3 of Form N-CSR.

Item 4. Principal Accountant Fees and Services.

The registrant has engaged its principal accountant to perform audit services, audit-related services, tax services and other services during the year ended March 31, 2015 and the period August 1, 2013 (commencement of operations) through March 31, 2014. “Audit services” refer to performing an audit of the registrant’s annual financial statements or services that are normally provided by the accountant in connection with statutory and regulatory filings or engagements for those fiscal years. “Audit-related services” refer to the assurance and related services by the principal accountant that are reasonably related to the performance of the audit. “Tax services” refer to professional services rendered by the principal accountant for tax compliance, tax advice, and tax planning. “All other fees” refer to the aggregate fees billed for products and services provided by the principal accountant other than “Audit fees”, “Audit-related fees” and “Tax fees”. The following table details the aggregate fees billed or expected to be billed for each of the last two fiscal years for audit fees, audit-related fees, tax fees and other fees by the principal accountant.

| FYE 3/31/2015 | FYE 3/31/2014 | |||

| Audit Fees |

$20,750 | $24,750 | ||

| Audit-Related Fees |

$4,200 | $8,000 | ||

| Tax Fees |

$9,400 | $8,500 | ||

| All Other Fees |

$0 | $0 |

The audit committee has adopted pre-approval policies and procedures that require the audit committee to pre-approve all audit and non-audit services of the registrant, including services provided to any entity affiliated with the registrant.

The percentage of fees billed by KPMG LLP applicable to non-audit services pursuant to waiver of pre-approval requirement were as follows:

| FYE 3/31/2015 | FYE 3/31/2014 | |||

| Audit-Related Fees |

0% | 0% | ||

| Tax Fees |

0% | 0% | ||

| All Other Fees |

0% | 0% |

Table of Contents

All of the principal accountant’s hours spent on auditing the registrant’s financial statements were attributed to work performed by full-time permanent employees of the principal accountant.

The following table indicates the non-audit fees billed or expected to be billed by the registrant’s accountant for services to the registrant and to the registrant’s investment adviser (and any other controlling entity, etc.—not sub-adviser) for the last two years. The audit committee of the Board of Trustees has considered whether the provision of non-audit services that were rendered to the registrant’s investment adviser is compatible with maintaining the principal accountant’s independence and has concluded that the provision of such non-audit services by the accountant has not compromised the accountant’s independence.

| Non-Audit Related Fees | FYE 3/31/2015 | FYE 3/31/2014 | ||

| Registrant |

$9,400 | $8,500 | ||

| Registrant’s Investment Adviser |

$0 | $0 |

Item 5. Audit Committee of Listed Registrants.

Not applicable to registrants who are not listed issuers (as defined in Rule 10A-3 under the Securities Exchange Act of 1934).

Item 6. Investments.

Schedule of Investments is included as part of the report to shareholders filed under Item 1 of this Form.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

The Master Fund invests a substantial portion of its assets in securities of Portfolio Funds. These securities do not typically convey traditional voting rights to the holder and the occurrence of corporate governance or other notices for this type of investment is substantially less than that encountered in connection with registered equity securities. However, Steben & Company, Inc. (the “Investment Manager”) and/or the Master Fund may, under some circumstances, receive proxies from certain Portfolio Funds and other issuers. The Board of Trustees has delegated to the Investment Manager authority to vote all proxies relating to the Master Fund’s portfolio securities pursuant to the Statement of Policies and Procedures for Proxy Voting set out in the Master Fund’s Registration Statement filed July 31, 2014. Information on how the Master Fund voted proxies (if any) relating to portfolio securities during the most recent 12-month period ending June 30, 2015 will be available on Form N-PX without charge by calling 800-726-3400, or on the SEC’s website at http://www.sec.gov.

Table of Contents

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

|

Investment Committee Member / Portfolio Manager |

Type of Accounts | Total # of Accounts Managed |

Total Assets (000,000’s omitted) |

# of Advisory |

Total Assets for which Advisory Fee is Based on Performance (000,000’s omitted) | |||||

| Kenneth E. Steben |

Registered Investment Companies |

3 | $131 | 0 | $0 | |||||

| Other Pooled Investment Vehicles | 3 | $827 | 0 | $0 | ||||||

| Other Accounts | 0 | $0 | 0 | $0 | ||||||

| Michael Bulley |

Registered Investment Companies |

3 | $131 | 0 | $0 | |||||

| Other Pooled Investment Vehicles | 3 | $827 | 0 | $0 | ||||||

| Other Accounts | 0 | $0 | 0 | $0 | ||||||

| John Dolfin |

Registered Investment Companies |

3 | $131 | 0 | $0 | |||||

| Other Pooled Investment Vehicles | 3 | $827 | 0 | $0 | ||||||

| Other Accounts | 0 | $0 | 0 | $0 | ||||||

| Basak Akiska |

Registered Investment Companies |

3 | $131 | 0 | $0 | |||||

| Other Pooled Investment Vehicles | 3 | $827 | 0 | $0 | ||||||

| Other Accounts | 0 | $0 | 0 | $0 |

Biographical Information

Kenneth E. Steben is the President and Chief Executive Officer of the Investment Manager. Mr. Steben received his Bachelor’s Degree in Interdisciplinary Studies, with a concentration in Accounting in 1979 from Maharishi University of Management. He holds his Series 3, 5, 7, 24, 63 and 65 FINRA licenses, and has been a CFTC listed Principal and registered as an Associated Person of the Investment Manager since March 15, 1989.

Michael D. Bulley is Senior Vice President of Research and Risk Management, and a Director. He received his Bachelor’s degree in Electrical Engineering from the University of Wisconsin – Madison in 1980 and his Master’s in Business Administration with a concentration in Finance from Johns Hopkins University in 1998. Mr. Bulley is a CAIASM designee and Member of the Chartered Alternative Investment Analyst Association®. Mr. Bulley joined the Investment Manager in November 2002, and holds Series 3, 7, 28 and 30 FINRA licenses. Mr. Bulley has been a CFTC listed Principal since February 11, 2003 and registered as an Associated Person of the Investment Manager since January 18, 2003.

John Dolfin is Director of Research at the Investment Manager. Mr. Dolfin earned a Bachelor’s degree in Philosophy, Politics and Economics from Oxford University in 1993, and a Masters in

Table of Contents

Economics from Yale University in 1996. Previously, he served as Director and Head of Macro and CTA Strategies at Merrill Lynch Wealth Management, a financial advisory firm, from July 2006 to June 2010. More recently, he served as Managing Director in the Liquid Strategies Group at SAFANAD Inc., an investment management firm, from June 2010 to February 2011. From March to July 2011, he was engaged in various personal projects. Mr. Dolfin has been a CFA charter holder since 2005 and has been a CFTC listed Principal of the Investment Manager since July 2, 2012.

Basak Akiska is Director of Operational Due Diligence at the Investment Manager. Ms. Akiska earned a Bachelor’s degree in Management from University of Massachusetts Amherst in 1999 and a Masters in Accounting from University of Virginia in 2000. Previously, she served as Senior Due Diligence Analyst at FRM/MAN Investments, a financial advisory firm, from June 2006 to February 2013. Prior to that, Ms. Akiska served as an Internal Audit Manager at XL Capital, and as an Audit Manager at Ernst & Young LLP., an independent public accounting firm. Ms. Akiska acquired her CPA license in 2004 (currently inactive).

Securities Ownership of Investment Committee Members

No member of the Investment Committee owns shares of the Steben Select Multi-Strategy Master Fund.

Conflicts of Interest of the Investment Manager

As an investment adviser and fiduciary, the Investment Manager owes its clients and shareholders an undivided duty of loyalty. The Investment Manager recognizes that conflicts of interest are inherent in its business and accordingly has developed policies and procedures (including oversight monitoring) reasonably designed to detect, manage and mitigate the effects of actual or potential conflicts of interest in the area of employee personal trading, managing multiple accounts for multiple clients, including the Master Fund, and allocating investment opportunities. Investment professionals, including the Portfolio Managers and research analysts, are subject to the above-mentioned policies and oversight monitoring to ensure that all clients are treated equitably. The Investment Manager places the interests of its clients first and expects all of its employees to meet their fiduciary duties.

Employee Personal Trading. The Investment Manager has adopted a Code of Ethics that is designed to detect and prevent conflicts of interest when investment professionals and other personnel of the Investment Manager own, buy or sell securities that may be owned by, or bought or sold for, clients. Personal securities transactions by an employee may raise a potential conflict of interest when an employee owns or trades in a security that is owned or considered for purchase or sale by a client, or recommended for purchase or sale by an employee to a client. Subject to the reporting requirements and other limitations of its Code of Ethics, the Investment Manager permits its employees to engage in personal securities transactions, and also allows them to acquire investments in certain funds managed by the Investment Manager. The Investment Manager’s Code of Ethics requires disclosure of all personal accounts and maintenance of brokerage accounts with designated broker-dealers approved by the Investment Manager.

Managing Multiple Accounts for Multiple Clients. The Investment Manager has compliance policies and oversight monitoring in place to address conflicts of interest relating to the management of multiple accounts for multiple clients. Conflicts of interest may arise when an

Table of Contents

investment professional has responsibilities for the investments of more than one account because the investment professional may be unable to devote equal time and attention to each account. These conflicts increase where, as here, an investment professional receives performance-based compensation from some accounts but not from others, or receives asset-based compensation from accounts with different advisory fees. The investment professional or investment professional teams for each client may have responsibilities for managing all or a portion of the investments of multiple accounts with a common investment strategy, including other registered investment companies and unregistered investment vehicles, such as hedge funds. Among other things, investment professional compensation reflects a broad contribution in multiple dimensions to long-term investment success for our clients and is generally not tied specifically to the performance of any particular client’s account, nor is it generally tied directly to the level or change in level of assets under management.

Allocating Investment Opportunities. The investment professionals at the Investment Manager routinely are required to select and allocate investment opportunities among accounts. The Investment Manager has adopted policies and procedures intended to address conflicts of interest relating to the allocation of investment opportunities. These policies and procedures are designed to ensure that information relevant to investment decisions is disseminated promptly within its portfolio management teams and investment opportunities are allocated equitably among different clients. The policies and procedures require, among other things, objective allocation for limited investment opportunities (e.g., on a rotational basis), and documentation and review of justifications for any decisions to make investments only for select accounts or in a manner disproportionate to the size of the account. Portfolio holdings, position sizes, and industry and sector exposures tend to be similar across similar accounts, which minimize the potential for conflicts of interest relating to the allocation of investment opportunities. Nevertheless, access to Portfolio Funds or other investment opportunities may be allocated differently among accounts due to the particular characteristics of an account, such as size of the account, cash position, tax status, risk tolerance and investment restrictions or for other reasons.

The Investment Manager’s procedures are also designed to address potential conflicts of interest that may arise when the Investment Manager has a particular financial incentive, such as a performance-based management fee, relating to an account. An investment professional may perceive that he or she has an incentive to devote more time to developing and analyzing investment strategies and opportunities or allocating securities preferentially to accounts for which the Investment Manager could share in investment gains.

Performance Fees. An Investment Committee Member may advise certain accounts with respect to which advisory fees are based entirely or partially on performance. Performance fee arrangements may create a conflict of interest for the Investment Committee Member in that the Member may have an incentive to allocate the investment opportunities that he or she believes might be the most profitable to such other accounts instead of allocating them to the Master Fund.

Compensation to Investment Committee Members

The Investment Manager’s compensation program for investment professionals is designed to be competitive and effective in order to attract and retain the highest caliber employees. The compensation program for investment professionals is designed to reflect their ability to generate long-term investment success for the Investment Manager’s clients, including

Table of Contents

shareholders of the Master Fund. Except as described below, investment professionals do not receive any direct compensation based upon the investment returns of any individual client account.