UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2020

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ______________to ______________

Commission File Number 000-549995

|

I-ON DIGITAL CORP.

|

(Exact name of registrant as specified in its charter)

(formerly known as I-ON Digital Corp.)

|

Delaware

|

46-3031328

|

|

|

(State or Other Jurisdiction of Incorporation or Organization)

|

(I.R.S. Employer Identification Number)

|

|

15, Teheran-ro 10-gil, Gangnam-gu, Seoul, Korea

|

06234

|

|

|

(Address of Principal Executive Offices)

|

(Zip Code)

|

+82-2-3430-1200

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

Name of each exchange on which registered

|

|

|

Common Stock, par value $0.0001 per share

|

OTCQB

|

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act of 1934 during the past 12 months (or for such shorter period that the registrant

was required to file such reports), and (2) has been subject to such filing requirement for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12

months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers in response to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or

information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large

accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☐

|

Accelerated filer ☐

|

|

Non-accelerated filer ☒

|

Smaller reporting company ☒

|

|

Emerging growth company ☐

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to

Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of internal control over financial reporting under Section 404(b) of the

Sarbanes-Oxley Act (15 U.S.C. 7762(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

As of June 30, 2020 (the last business day of the registrant’s most recently completed second fiscal quarter), the aggregate market value of the common stock held by non-affiliates of the registrant was approximately

$2.8 million based on the closing sales price of $0.08 on the OTC Markets. All executive officers and directors of the registrant have been deemed, solely for the purpose of the foregoing calculation, to be “affiliates” of the registrant.

As of March 22, 2021, there were approximately 35,030,339 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE:

None.

|

PART I

|

Page

|

|

|

Item 1.

|

2

|

|

|

Item 1A

|

13

|

|

|

Item 1B

|

21

|

|

|

Item 2.

|

21

|

|

|

Item 3.

|

21

|

|

|

Item 4.

|

21

|

|

|

PART II

|

||

|

Item 5.

|

22

|

|

|

Item 6.

|

23

|

|

|

Item 7.

|

23

|

|

|

Item 7A

|

28

|

|

|

Item 8.

|

28

|

|

|

Item 9.

|

28

|

|

|

Item 9A

|

28

|

|

|

Item 9B.

|

28

|

|

|

PART III

|

||

|

Item 10.

|

29

|

|

|

Item 11.

|

30

|

|

|

Item 12.

|

32

|

|

|

Item 13.

|

32

|

|

|

Item 14.

|

32

|

|

|

PART IV

|

||

|

Item 15.

|

33

|

|

|

36

|

||

PART I

|

SPECIAL NOTE ON FORWARD-LOOKING STATEMENTS

The information in this report contains forward-looking statements. All statements other than statements of historical fact made in this report are forward looking. In particular, the

statements herein regarding industry prospects and future results of operations or financial position are forward-looking statements. These forward-looking statements can be identified by the use of words such as “believes,” “estimates,”

“intends”, “plans”, “could,” “possibly,” “probably,” anticipates,” “projects,” “expects,” “may,” “will,” or “should,” “designed to,” “designed for,” or other variations or similar words or language. No assurances can be given that the future

results anticipated by the forward-looking statements will be achieved. Forward-looking statements reflect management’s current expectations and are inherently uncertain. Our actual results may differ significantly from management’s

expectations.

Although these forward-looking statements reflect the good faith judgment of our management, such statements can only be based upon facts and factors currently known to us. Forward-looking

statements are inherently subject to risks and uncertainties, many of which are beyond our control. As a result, our actual results could differ materially from those anticipated in these forward-looking statements as a result of various

factors, including those set forth below under the caption “Risk Factors.” For these statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995. You

should not unduly rely on these forward-looking statements, which speak only as of the date on which they were made. They give our expectations regarding the future but are not guarantees. We undertake no obligation to update publicly or

revise any forward-looking statements, whether as a result of new information, future events or otherwise, unless required by law.

|

Organization and Corporate History

I-ON Digital Corp. (formerly known as I-ON Communications Corp.) was incorporated under the laws of the State of Delaware on June 18, 2013 as ALPINE 3 Inc. Alpine 3 Inc. was set up to serve as a vehicle to effect an

asset acquisition, merger, exchange of capital stock or other business combination with a domestic or foreign business. ALPINE 3 did not undertake any effort to cause a market to develop in its securities, either debt or equity, before it

successfully concluded a business combination. On April 4, 2014, The Michael J. Rapport Trust (the “Trust”) purchased 10,000,000 shares of common stock which was all of the outstanding shares of Alpine 3, Inc., and subsequently changed the name to

Evans Brewing Company Inc. (“EBC”) on May 29, 2014. On October 9, 2014 the Trust agreed to the cancellation of 9,600,000 of the shares of common stock that it had acquired and retained 400,000 shares of common stock.

On October 15, 2014, Bayhawk and EBC entered into an Asset Purchase and Share Exchange Agreement (the “Agreement”), subject to receiving approval of the independent Bayhawk shareholders who voted on the transaction. On

September 17, 2015, the independent Bayhawk shareholders approved the agreement and Bayhawk sold to EBC and EBC purchased from Bayhawk assets of Bayhawk, including but not limited to the assets relating to the Bayhawk Ales label and the Evans Brands

(collectively, the “Transferred Assets”). Bayhawk retained ownership of 100% of the stock in Evans Brewing Corp. (CA) (“Evans Brewing California”) which has the brewers license at City Brewery in Lacrosse, WI. Based on the affirmative vote by the

independent Bayhawk shareholders to approve the Asset Purchase transaction, EBC proceeded with the share exchange and tender offer to the Bayhawk shareholders, pursuant to which EBC offered to exchange shares of EBC common stock for shares of Bayhawk

common stock, on a one-for-one basis (the “Exchange Offer”). At the close of the share exchange on December 2, 2015, 4,033,863 Bayhawk shares were accepted and exchanged for 4,033,863 shares of EBC common stock.

On January 25, 2018, Evans Brewing Company, Inc. consummated an Agreement of Merger and Plan of Reorganization (the “Merger Agreement”), with I-ON Digital Corp.., a company organized under the laws of the Republic of

Korea (South Korea) (“I-ON”) and I-ON Acquisition Corp., a wholly-owned subsidiary of the Company (“Acquisition”). Pursuant to the terms of the Merger Agreement, Acquisition merged with and into I-ON in a statutory reverse triangular merger (the

“Merger”) with I-ON surviving as a wholly-owned subsidiary of the Registrant. As consideration for the Merger, the Registrant agreed to issue the shareholders of I-ON (the “I-ON Holders”) an aggregate of 26,000,000 shares of our Common Stock, in

accordance with their pro rata ownership of I-ON capital stock. Following the Merger, the Registrant adopted the business plan of I-ON in information technology consultancy and software development. On December 14, 2017, in connection with the

Merger, the Company’s Board of Directors approved an amendment to its Certificate of Incorporation (the “Amendment”) to change its name to I-ON Digital Corp.

At the effective time of the Merger, our board of directors and officers were reconstituted by the appointment of Jae Cheol James Oh as Chairman, Chief Executive Officer, and Chief Financial Officer, Hong Rae Kim as

Executive Director and Jae Ho Cho as Director. Michael Rapport resigned as President, Chief Executive Officer, and Chairman in connection with the Transaction and Evan Rapport resigned as Vice President and Director, Kenneth Wiedrich resigned as

Chief Financial Officer and Director and Kyle Leingang resigned as Secretary. Roy Robertson, Mark Lamb, Joe Ryan, and Kevin Hammons resigned as members of the Board of Directors and their respective committees.

On March 21, 2019, the Company’s Board of Directors approved an amendment to the Company’s Certificate of Incorporation to change the name of the Company to I-ON Digital Corp. The Company filed a Certificate of

Amendment to effectuate the name change on or about April 2, 2019.

I-ON Digital

Following the Merger, the Company adopted the business plan of I-ON. I-ON was founded by Jae Cheol James Oh, who currently serves as CEO. The Company’s roots are in IT consultancy and software development. I-ON

services South Korea’s enterprise content management system’s (CMS) market and specializes in advancing market-leading internet software applications to capitalize on rapidly growing market sectors.

After being awarded its first of numerous international patents in 2003, I-ON has since evolved into an industry-leading and recognized software developer and provider of on-premise and cloud-based enterprise-class

unstructured data management, digital experience and digital marketing software and solutions. I-ON’s portfolio of software and solutions serves the digital marketing and technology needs of organizations, enabling clients to create, measure, and

optimizes digital experiences for their audiences across marketing channels and devices. We believe these solutions help clients reduce the cost of content management and delivery, while increasing the return on their investments in digital

communication and marketing spend. As of its founding, the Company has serviced and continues to service over 1,000 blue-chip and middle-market clients across virtually all verticals in both private and public sectors. The Company has

meaningfully expanded its reach over the past decade and now currently markets, licenses and sells its products and services directly to clients in South Korea and Japan, as well as in Singapore, Malaysia, Indonesia, Thailand, Vietnam, and the U.S.

through value-added resellers and partnerships.

I-ON currently holds 6 international and over 20 domestic patents for both products and methodologies built into the 10 product offerings the Company currently has at market. These encompass enterprise CMS, digital

experience and service delivery software, digital marketing, smart mobility and analytics tools, and, more recently, energy management solutions as well as sports software and IT convergence services. Beginning in the fourth quarter of 2018, the

Company started endorsing its 7th generation cloud based Digital Experience (DXP) platform as a service offering known as ICE, which encompasses a more feature-rich front and back end CMS. The Company has designed and developed industry-leading

technologies that are compliant with global standards including GS (Good Software) and NET (New Excellent Technology). I-ON also holds numerous domestic and global industry awards, earning high rankings and recognition from the likes of Gartner

(Magic Quadrant 2014) and Red Herring (2014 Asia Top 100 Winner), among many others.

In addition to South Korea, Japan has particularly helped fuel I-ON’s growth over the past 10 years owing to the success of an exclusive licensing deal with Ashisuto, a large Japan-based technology services firm that

employs approximately 800 technical, engineering and marketing staff across 9 office locations. Ashisuto, which has provided technology services to Japan’s enterprises and government entities since 1973, currently white labels and sells I-ON’s

core CMS offering ICS6 to over 600 clients as NOREN 6.

As a result of global enterprise digital marketing trends and I-ON’s nearly 20 -year track record in South Korea, Japan and now, Southeast Asia, the Company’s objective is to continue to gain market share in these

markets. I-ON will continue to closely engage and consult with existing and prospective clients as their subject matter expert and digital strategist of choice across multiple touchpoints in the digital marketing and technology ecosystem, helping

Chief Marketing Officers (CMO) and Chief Information Officers (CIO) drive critical change and growth for their organizations.

I-ON has invested and continues to spend substantial revenue on research and development. The Company has over 120 employees as of December 31, 2019, approximately 95% of whom are considered full-time. Research and

development typically comprises of approximately 80 junior, mid to senior level engineers and developers, most of whom are based at the Company’ headquarters located at 15 Teheran-ro 10-gil, Gangnam-gu, Seoul, South Korea, 06234.

PRODUCTS AND SERVICES

I-ON’s product line is comprised of:

|

Enterprise CMS & Digital Experience (IaaS/PaaS):

|

|

|

I-ON Content Server - ICS6

|

I-ON Content Application Framework Engine - ICAFE

|

|

I-ON Deploy Server - IDS

|

I-ON Content Ecosystem - ICE

|

|

I-ON Digital Asset Management System - IDAS

|

|

|

I-ON Web Analytics Server

|

|

Software as a Service (SaaS) :

|

Energy Management Solutions :

|

|

Distributed Repository Service - GAIA

|

Load Aggregator’s Management System - LAMS

|

|

iDrive - E-Document Management System

|

- Demand Resource Management

|

|

e.Form - mobile contract platform

Assist9 – mobile ERP dashboard

|

- DLMS/COSEM -Advanced two-way metering infrastructure

|

Sports & IT Convergence Service

Ticket Advanced Marketing Management – TAMM- pro-sports marketing & analytics

VoiceBall – Amateur League Umpire & Data Service

The following is a brief description of I-ON’s key products:

ICS6 (I-ON Content Server) – ICS6 is I-ON’s generation 6 web content management system that helps reduce burdens of complex website management by organizing vast amounts of

ever-increasing digital content and big data into physical directory and logical site structure. ICS6 is one of South Korea’s first-to-market cloud-based CMS platforms and a market share leader in both Korea & Japan.

ICE (I-ON Content Ecosystem) - ICE is I-ON’s 7th generation DXP offering that manages the digital content management lifecycle commencing from creation, registration,

distribution, deletion, billing to analytics. ICE is geared for SOs seeking ways to enhance business to business to consumer (B2B2C) value.

IDS (I-ON Deploy Server) – IDS, in conjunction with ICS6, securely, conveniently and automatically deploys files and content between servers when distribution inefficiencies and

services issues arise.

IDAS (I-ON Digital Asset Management System) – IDAS, in conjunction with ICS6, ensures a virtuous cycle of an organization’s digital assets through an integrated framework that

collects, manages, deploys and distributes content. It also provides ample storage and categorization functionalities necessary to address high multi-media content demand including high-resolution video. The software supports digital archiving,

scalability and changes in physical environment.

iCAFE (I-ON Content Application Framework Engine) – iCAFE is a content delivery platform optimized for N-Screen environments, offering a

robust wire-wireless service delivery platform for broadcasting, imaging & mobile content

e.Form – e.Form is a one-stop mobile contract solution for smartphones and tablets that digitizes and expedites document creation and execution processes for organizations. The

platform supports over 200 application programming interfaces (APIs).

iDrive – iDrive is a SaaS-based EDMS (e-document management system) which centralizes all categories of e-documents within an organization, iDrive is geared for streamlining and

managing the e-document lifecycle from creation, approval, archiving to destruction.

GAIA – GAIA is a back-end unstructured data repository platform that manages a cloud-based ecosystem that enterprises or individuals can use to build and share mobile

applications.

LAMS (Load Aggregator’s Management System) - LAMS is one of South Korea’s first Open ADR 2.0-based demand response management solutions designed to manage and reduce electricity

consumption and peak demand through demand response program participation.

TAMM (Ticket Admission Marketing Management) - TAMM is a mobile B2B2C platform that integrates and manages the professional sports event experience from marketing and promotion

and ticket purchases and reservations to the delivery of a mobile analytics dashboard for followers. Event organizers/sponsors have included, among others, the LPGA Hana Bank Championship and SK Telecom Open. I-ON acquired the core TAMM developers

and intellectual property from South Korea-based MoceanPeople in March 2016.

Assist9 – Assist9 is a mobile all-in-one work flow process and data management dashboard geared towards small and medium-sized businesses and startups. Core functions revolve

around ERP, PMS, SFA, HR, and e-approval – with up to fifteen others- and are designed to improve operational efficiencies and provide CEOs with greater analytical insight into their businesses.

ADDRESSABLE MARKETS

South Korea, Japan and Southeast Asia

Econsultancy and Adobe reported in recent studies that less than 15% of CMO respondents identified as working for digital-first organizations, despite a study by Forrester Research that indicated 51% of B2B enterprises

were ratcheting up digital marketing initiatives in 2018 and into 2019. A key driver of I-ON’s ability to tap further into existing and future addressable markets, the Company believes, will depend on how quickly mid to large enterprises can adopt a

digital-first mindset through continued client engagement.

According to many industry researchers, such as Forrester and Gartner, the combined enterprise digital marketing and CMS sector in South Korea and Japan is expected to generate a high single digit compounded annual

growth rate to over $800 million by 2020.

Given its market share-leading in both South Korea and Japan, I-ON remains uniquely positioned to serve as a localized partner and to address the evolving marketing needs of mid to large enterprises. CMOs continue to

seek new and innovative ways to analyze, improve return on investment (ROI) and justify the value of increased digital marketing spending.

According to numerous industry sources, including Forbes, South Korea has emerged as one of Asia’s fastest growing technology startup hubs, attracting increasing investment from domestic funds and foreign investment.

Today, South Korea remains the eleventh largest economy in the world and, with 51 million people, the twenty-eighth largest population in the world, while boasting the world’s highest broadband penetration at 97%.

South Korea was recently highlighted in Bloomberg’s list of most innovative countries, owing to the country’s research and development intensity, as well as productivity and educational standards. Home to Samsung, Hyundai and over 10 other Fortune

500 companies, South Korea, for the past several decades, has also been on a path pivoting from big industry and manufacturing to transformative technology, thanks to government and private/public partnership initiatives. Favorable policy

initiatives have recently led to larger budget allocation towards science and technology, matching funds with international investors, establishing international entrepreneurship programs at universities, opening up many of the country’s research

institutes, and providing safety nets for technologists and scientists that take capital risk.

Similarly, Japan remains the third largest economy and second largest developed economy in the world, the third largest automobile manufacturing, and the largest electronics goods industry in the world. Despite being

home to over 50 Fortune 500 companies, and facing growing competition from China and South Korea, manufacturing and investment in Japan have also pivoted toward software development, high-technology, and precision goods sectors, such as robotics and

optical instruments.

Asia-Pacific and Global

Across not only South Korea and Japan, but the entire Asia-Pacific region, businesses and consumers today increasingly demand personalized content and experiences in their online interactions, across multiple digital

channels and devices. This is accelerating growth in the CMS and digital marketing arenas as well demand from marketers seeking solutions that optimize customers’ experiences, demonstrate the success of their programs with objective metrics, and

deliver the greatest return on their marketing spend.

According to Gartner, the enterprise CMS market across the Asia-Pacific region, which includes China, South Korea, Hong Kong, Japan, Indonesia, Malaysia, Singapore and Vietnam – exceeded $700 million in 2016, up

significantly from $500 million in 2014 and is projected to exceed $900 million by 2019, reflecting a compounded annual growth rate of at least 12%. Malaysia, Indonesia and Singapore collectively generated $180 million in enterprise CMS revenue last

year and Gartner projects a 16% annual growth rate into 2020.

In North America, aggregate digital marketing spend, which includes CMS for both products and professional services by both mid and large-sized enterprises, exceeded $135 billion in 2016 from approximately $95 billion

in 2014, and according to forecasts from both IDC and Statista, is projected to grow 18% annually to over $225 billion by 2019.

Globally, sources such as the CMO Council and Gartner estimate the current web and mobile digital marketing industry size at $450 billion, while forecasting a high single digit 5 year compounded annual growth rate to

over $600 billion by 2019.

MARKETING AND GROWTH STRATEGY

Growth in omni-channel DXP, digital marketing and big data

CMS and digital marketing budgets at global brands continue to increase relative to traditional marketing dollars, according to Gartner and many CMO surveys, which describe a general atmosphere keen on shifting

marketing dollars towards ROI enhancing tools such as audience analytics and curation, consumer engagement, smart mobility and artificial intelligence. In South Korea, existing and prospective clients across many sectors are often consulting with

I-ON on how best to integrate disparate and increasingly complex needs, which may for example apply digital asset management, e-commerce, sports software and SaaS capabilities. As competition has been intensifying, the pace of overall M&A

activity has also been accelerating as small and mid-size players such as I-ON, seek to diversify and address the trends and demands. Accordingly, enterprise CMS globally is being viewed less as tools for building web pages and standard analytics,

but more so as vital software and value-added solutions that can help drive the effectiveness of often complex, data driven and expensive digital strategies and marketing campaigns. Interoperability remains a key differentiator across the dynamic

South Korean and East Asian markets. Companies small and large, particularly those with intricate distribution and supply chain responsibilities, not only require a portal for their intranet for external needs, but demand that their CMS software

facilitate a real-time connection between the business, people and things that allow all to communicate, transact and even negotiate with each other across all touch points. As a result, I-ON also intends to play further into the unstructured and

big data, analytics, e-commerce and smart mobility arenas as part of its DXP offering.

Defining Value Proposition

I-ON believes it remains uniquely positioned to address the evolving digital experience and marketing needs of medium to large enterprises. Given the growth across the global enterprise digital marketing spectrum and

I-ON’s 19-year track record serving a marquee clientele in South Korea, Japan, and parts of Southeast Asia, I-ON’s objective is to continue to aggressively gain market share by closely engaging with existing and prospective clients, while driving

sales for both its core CMS offering and complementary solutions that enable organizations to transform traditional marketing initiatives into analytics and data-driven strategies vital to delivering measurable results.

I-ON believes that its software products and solutions will continue to be a primary revenue source for the Company over time and that its growing portfolio of products may generate profitable demand for associated

maintenance, support, implementation, consulting, and training services that the Company, and a channel of licensees and value-added resellers (VARs), can provide.

Near-term, I-ON intends to do the following to drive organic growth:

| ∙ |

Continue to leverage knowledge and experience into new or enhanced solutions and products

|

| ∙ |

Continue to deploy secure pilot environments for prospective customers to evaluate and envision additional uses for customized application development

|

| ∙ |

Continue to procure contracts directly, via strategic partnerships and increasing sales personnel

|

| ∙ |

Recruit seasoned executives as well as younger talent to utilize unique training model that addresses resource shortages

|

| ∙ |

Incubate and build-out focused profitable technology practices

|

| ∙ |

Continue to participate in multi-lateral joint research and development projects in concert with its partners across many different countries

|

South East Asia

According to Gartner, Malaysia, Indonesia and Singapore generated $180 million in enterprise CMS revenue last year and project a 16% annual growth rate by 2020. As a result, I-ON intends to continue to build off of

its initial successes in the Southeast Asia region, which include, among other projects, the following: implementation of a fully integrated mobile/online trading solution for Malaysia’s MNC Securities; a CMS implementation for a leading USA cable

manufacturer, Commscope- supporting 13 languages to meet global standards; the implementation of a CMS solution based on CSDP (Convergence Service Delivery Platform) for Indonesia’s BOLEH Mobile; and an integration of CMS platforms for the Malaysia

Ministry of Works.

Announced on October 1, 2018, I-ON and Singapore-based Hyper Resources Interactive Pte Ltd. executed an MoU whereby Hyper Resources will assist with marketing and utilize I-ON’s core CMS suite of ICS6, IDAS, IDS, ICS

and eForm solutions to address the needs of Singaporean enterprises. I-ON will assist with operational and technical support as well as solutions training.

Sports ICT

I-ON absorbed the TAMM team and technology in 2016. Currently the exclusive and secure web and mobile payment gateway provider for the KLGPA and technology partners with most of the major sponsors of the events, TAMM

and its next generation omni-channel sports data management solution are well-positioned to address the $5 billion global sports software market, which is projected to increase at a 13% CAGR through 2024. Significant global investment in sports

infrastructure including stadiums, complexes and leagues has been the leading driver of sports software development and implementation, which helps organizers automate various administrative functions, ticket sales, promotions, as well as player and

game management utilizing both cloud-based and on-premise technology. North America currently holds a market share of close to 60% and is expected to continue its dominant trend through 2024, according to Hexa Research.

As announced in 2018, I-ON formed a partnership with the Ministry of Culture, Sports and Tourism and the Korea Institute of Sports Science to develop a domestic multi-sport marketing and analytics platform addressing

amateur and pro golf and baseball participants and engagement. The initiative also integrates reputable University research and high-tech private sector resources. More recently in January 2019, I-ON announced a letter of intent, subject to a

multi-year framework, with California-based Pacific Pro Football league, a new amateur-pro D-league targeting future NFL recruits, which is led by a distinguished team of former NFL executives, players and coaches. The engagement represents I-ON’s

initial foray into the US market with respect to TAMM and sports software initiatives. I-ON’s scope of service is broad, but entails building out the league’s CMS infrastructure while serving as their digital strategist of choice leading up to the

2020 league launch and well beyond. This could be in association with Pacific Pro’s exclusive sponsor Adidas.

Energy ICT

In early 2018, I-ON and its various partners including Japan-based TIS INTEC Group – a leading systems integrator- began a deeper dive on how to best address the fast-growing need for distributed energy management and

virtual power plant (VPP) solutions for grid connected renewable energy sources in hopes of delivering an enhanced, reliable energy and cost-efficient product offering to East Asia markets. By employing key components of I-ON’s energy management

system to address the demand response needs of power grid companies, I-ON intends to introduce its own proprietary next generation VPP solution that operate within cloud-based service environments to address the energy management needs of

enterprises.

Popular in the U.S. and Europe, but a rapidly emerging sector in Japan and across East Asia, VPP is a cloud-based distributed power plant that aggregates the capacities of energy resources at the requests of power

transmission and distribution service providers for the purposes of enhancing power generation more reliably. VPP typically integrates small-scale power plants or energy storage facilities for residential settings, buildings, factories and

incorporates them into a remotely controlled virtual power station using a sophisticated set of software and IT systems. These systems tap into existing grid networks to tailor electricity supply and demand services under changing load conditions

both quickly and in real time, thus maximizing value for both the power generator and end user. Most industry observers currently peg the global VPP industry at $8-$12 billion -- double from just a few years ago -- and forecast the industry will

grow annually at a mid to high double-digit rate through 2025, driven by investment in the U.S., Europe and Australia with South Korea and Japan leading the way in East Asia.

Announced on November 21, 2018, Sweden-based Telenor Connexion and I-ON formed a collaboration agreement in order to provide South Korean customers in the energy sector with high-value and quality IoT solutions and

services by utilizing I-ON’s capabilities in data management, smart mobility, and advanced analytics.

Acquisition Strategy

I-ON intends to continue to leverage its international partnerships and ongoing success in enterprise CMS to move upstream, cross-sell, and serve clients more directly as either their digital strategist of choice

and/or by acquiring businesses with (i) a revenue producing platform with existing enterprise clients, (ii) subject matter expertise and or (iii) rights to intellectual property in at least one of the following digital marketing-related disciplines:

predictive analytics, smart mobility, marketing automation, search engine optimization (SEO), enterprise resource planning (ERP), workflow automation, and eCommerce. I-ON has already identified multiple compelling acquisition opportunities within

these domains, particularly in South Korea and Japan. However, there can be no assurance that I-ON will be able to acquire one or more of these businesses or that it will be able to do so on terms that are favorable to I-ON.

Notably, I-ON believes that overall macro conditions that drive consolidation and acquisitions also remain ideal including the historical low interest rate environment, a large, evolving and fragmented technology

services and solutions market across South Korea and East Asia, and the relatively low organic growth opportunities that ordinarily may not exist for smaller businesses. These existential conditions could enable I-ON to identify and purchase

compelling assets inexpensively.

Expand Product Offering and Geographic Coverage over the long-term

Over the next 5 years, I-ON’s growth strategy is to significantly expand its client base in South Korea, Japan, and Southeast Asia, while also expanding into new geographic areas, such as the U.S. and Europe to provide

clients with global coverage and around the clock services that CMS and digital marketing requires. I-ON’s continued business model is to allow its work and unique technical skills to attract new clients as well as win repeat projects with past and

current clients. At the same time, ION intends to expand its core offerings and increase brand awareness with new service capabilities and software products that produce significant value for clients.

PATENTS AND TRADEMARKS

Key Patents:

| ∙ |

Integrated certification system using electronic contract #10-1132672

|

| ∙ |

Website construction and management methodology #0457428

|

| ∙ |

Website integrated management system and management methodology #10-0764690

|

| ∙ |

Internet Reaction application reaction survey methodology and systems #0366708

|

| ∙ |

Modification and restoration methodology on comment utilizing digital items #10-0634047

|

| ∙ |

Power Quantity Reduction Compensation System management method #10-1046943

|

| ∙ |

Mobile Chat Systems for Supporting Cartoon Story-Style Communication on Webpage #9973458

|

| ∙ |

Enhancement to Sports Game Assistance System #10223448

|

| ∙ |

I-ON holds over 20 additional domestic patents

|

Key Certifications:

| ∙ |

I-ON e.Form Server Green Technology Certificate #GT-12-00040

|

| ∙ |

I-ON Content Server v6.1 Certificate of Software Quality – GS (Good Software) #14-0017

|

| ∙ |

DRMS OpenADR 2.0a/b Certificate of System Conformance

|

| ∙ |

Certificate for Company Research Institute #20022427

|

AWARDS AND INDUSTRY RECOGNITION HISTORY

|

∙

|

Selected to participate in ‘IP-Star Company development’ project by Seoul Business Agency (2013)

|

|

∙

|

Designated as Best Small and Medium Company Workplace by Small and Medium Business Corporation (2012-2014)

|

|

∙

|

Designated as Global Small Giant Company by Small and Medium Business Administration (2012-2014)

|

|

∙

|

Grand prize at New Software Solution in General Software section by Ministry of Knowledge Economy (2012)

|

|

∙

|

Designated as top Promising Future-Leading Company by Money Today (Economic newspaper 2012)

|

|

∙

|

Certified ‘Promising Export Firm’ by Small and Medium Business Administration (2011-2013)

|

|

∙

|

KOSA (Korea Software Industry Association)

|

|

∙

|

Best prize at 11th Korean Software Companies’ Competitiveness Award - Mobile SW section (2012)

|

|

∙

|

Best prize at 10th Korean Software Companies’ Competitiveness Award– KMS/EMC/BMP section (2011)

|

| ∙ |

Best prize at SoftBank Mobile Solution Contest in Japan (2011)

|

| ∙ |

Citation of Prime Minister awarded on the SW Industrial Day (2011)

|

| ∙ |

Tower of million USD exports award (2007)

|

| ∙ |

Grand prize in Internet Service Section (oneul.com) (2012)

|

| ∙ |

Winner of Brand Service Section (Lotte Duty Free) (2012)

|

| ∙ |

Grand prize in Business Improvement section (e.Form) (2012)

|

| ∙ |

Grand Prize in Information Management (Real-time Power demand resources Operation System) (2012)

|

| ∙ |

Grand Prize in Location Based System (LBS) (Lucky Bird) (2012)

|

| ∙ |

Grand Prize in Product brand (Catch Chevrolet) (2011)

|

| ∙ |

Grand Prize eBook (Kyowon Aesop) (2011)

|

CUSTOMERS

Because organizations in virtually every sector of the economy perform or need the functions I-ON supports, the Company has successfully deployed its software solutions to over 1,000 blue-chip and middle-market

enterprises across virtually all industries and verticals in both the private and public sectors. Such industries include but are not limited to financial services, banking, informational technology services, teleDigital, internet, automotive,

healthcare, publishing, media, education, energy, logistics, retail, consumer and business services, as well as government institutions. Over 400 enterprise clients in South Korea, 500 in Japan, and 100 across Southeast Asia and globally currently

utilize I-ON products, solutions and professional services capabilities.

Given its current foothold, I-ON believes it remains uniquely positioned to address the evolving marketing needs of medium to large enterprises as CMOs continue to lack the wherewithal to analyze, improve ROI, and

justify the value of increased digital marketing spend. I-ON’s diversified product suite, introduction of new products, tools and data sources, combined with media consumption devices such as mobile and tablets have created an environment that’s

been uncharted by numerous enterprise marketers and their CMOs, particularly in South Korea, Japan, Southeast Asia and China.

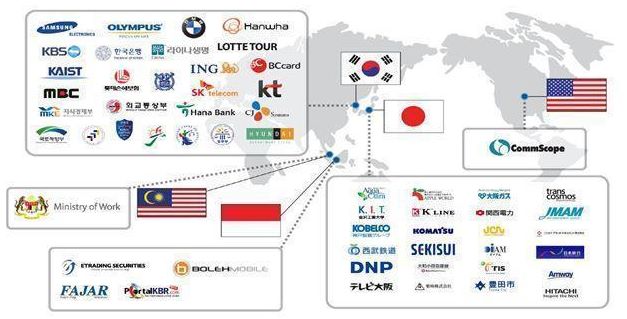

Below is a sample of I-ON’s clientele based on region.

Entry into new markets combined with relevant new product introductions has also enabled I-ON to diversify its client mix, thereby minimizing client concentration risk as reflected by the decline in top 10 client

contribution since 2013.

Below highlights I-ON’s top 10 clients as percentage of total revenue (Fiscal Years 2017-2020):

|

2017

|

2018

|

2019

|

2020

|

||||||||||||||||||

|

JoongAng Ilbo

|

8.6

|

%

|

KEPCO

|

10.1

|

%

|

SBDC

|

10.8

|

%

|

Samsung SDS

|

18.6

|

%

|

||||||||||

|

KBS

|

6.7

|

%

|

K.K. I-ON

|

7.7

|

%

|

Kyowon Creative

|

8.8

|

%

|

LG CNS

|

12.9

|

%

|

||||||||||

|

Hyundai Auto

|

6.3

|

%

|

Samsung Electro

|

6.5

|

%

|

Finger

|

8.8

|

%

|

K.K I-ON

|

9.7

|

%

|

||||||||||

|

Samsung Electro

|

6.0

|

%

|

SBDC

|

6.5

|

%

|

Amore Pacific

|

7.0

|

%

|

SBDC

|

5.8

|

%

|

||||||||||

|

KTDS

|

5.7

|

%

|

Finger

|

6.3

|

%

|

K.K I-ON

|

6.0

|

%

|

Kyowon Creative

|

5.3

|

%

|

||||||||||

|

K.K. I-ON

|

5.5

|

%

|

Mnwise

|

5.9

|

%

|

SG Tech

|

5.9

|

%

|

SK

|

4.7

|

%

|

||||||||||

|

Jeju Tourism

|

4.8

|

%

|

K.K. Ashisuto

|

4.7

|

%

|

Samsung SDS

|

5.3

|

%

|

Samsung Card

|

3.2

|

%

|

||||||||||

|

KLPGA

|

4.2

|

%

|

Shinhan Card

|

4.7

|

%

|

Seoul School Safety Mutual Aid Association

|

5.3

|

%

|

Shinhan Card

|

3.0

|

%

|

||||||||||

|

YTN

|

4.0

|

%

|

Samsung SDS

|

4.1

|

%

|

Penta Breed

|

3.2

|

%

|

NEO B&S

|

2.6

|

%

|

||||||||||

|

CJ Digital Music

|

3.9

|

%

|

Jeju Tourism

|

3.9

|

%

|

SBS

|

3.0

|

%

|

Finger

|

1.9

|

%

|

||||||||||

|

55.7

|

%

|

60.4

|

%

|

63.4

|

%

|

67.6

|

%

|

||||||||||||||

MARKETING, SALES AND DISTRIBUTION

I-ON relies both on inside and outside sales efforts as well as value-added resellers based in specific geographies to drive a bulk of their business development efforts. The Company has over 100 partners, formal and

informal, across 28 countries that provides client leads The Company also relies on client references and its track record and regularly attends reputable industry and technology conferences internationally.

COMPETITION

The market for I-ON’s products and solutions, primarily in South Korea, Japan and Southeast Asia is competitive but not considerably fragmented. We compete primarily with digital marketing agencies, systems consulting

firms and boutique consulting firms, that maintain specialized skills or products or are geographically focused, and clients’ own IT firms. Many of the firms we compete with have longer operating histories and are more developed than we are. The

principal competitive factors in these addressable markets include the ability to solve problems; the ability to deliver creative concepts and solutions; expertise and talent with advanced technologies; availability of resources; the quality and

speed of solutions; a deep understanding of user experiences; and the price of solutions. I-ON competes favorably when considering these factors and believes that its ability to deliver business innovation and outstanding value to its clients on

time and on budget, along with its successful track record, distinguishes them from competitors.

Interoperability has emerged as a key differentiator in I-ON’s addressable markets, as CMS is now seldom viewed as a stand-alone system for an enterprise’s online presence. Large enterprises and to a growing extent

small and middle market companies, particularly those with complex distribution and supply chain issues, not only require a portal for their intranet for external needs, but expect CMS platforms to allow for a real-time connection between the

business, people, behavior and things that allow all to communicate, transact and even negotiate with each other. Thus, in order to be better served and remain competitive in their own circles, clients are increasingly looking to I-ON to consult

with and integrate disparate and increasingly complex systems.

In addition to holding a first mover advantage, I-ON has been able to compete by offering flexible and often less expensive pricing, offering time-tested & proven licensing joint venture partnerships such as with

Ashisuto in Japan and focusing on R&D to drive product upgrade cycles such as ICE and introduce new products built off existing technology related to sports, energy and mobile. From a domestic DXP front, I-ON competes with companies such as

deCos Interactive and contentWise. Much larger competitors such as Adobe, Stellent, and IBM which service at significantly higher prices and complexity, lack mid-market cachet, are not built locally for scale, or are merely focused on other

disciplines. Opensource models tend to have a truer SME focus, are vague & lack vendor responsibilities, and do not address the needs of complex large to blue-chip enterprises.

RESEARCH AND DEVELOPMENT

Because the verticals in which I-ON competes are characterized by rapid technological change, the Company’s ability to compete successfully depends upon maintaining and enhancing expertise in its core business segments

and product lines. As a result, I-ON has reinvested and continues to spend substantial revenue on research and development. The Company currently employs over 100 junior, mid to senior level engineers and developers, most of whom are based at the

Company’s headquarters in Seoul. In order enable its employees to provide expert, timely, competitive services to the marketplace, I-ON also provides ongoing training and sponsors advanced university education to enhance employee skills and

knowledge of all current and future product offerings.

MANAGEMENT AND EMPLOYEES

As of December 31, 2020, I-ON has 127 full time and 1 part time employees. We believe we enjoy good employee relations. None of our employees are members of any labor union, and we are not a party to any collective

bargaining agreement.

PROPERTIES

The Company does not own any physical location. I-ON currently leases its corporate headquarters and other offices in Seoul, South Korea which expires on December 31, 2021. I-ON’s lease for its Tokyo, Japan office

expires on May 25, 2021. We believe that our current offices are sufficient in size for current and future operations.

POTENTIAL FUTURE PROJECTS AND CONFLICTS OF INTEREST

Members of the Company’s management may serve in the future as an officer, director or investor in other entities. Neither the Company nor any of its shareholders would have any interest in these other companies’

projects. Management believes that it has sufficient resources to fully discharge its responsibilities for all current and future projects.

GOVERNMENT REGULATION

We believe we are in compliance with applicable federal, state and other regulations and that we have compliance programs in place to ensure compliance going forward. There are no regulatory notifications or actions

pending.

LEGAL MATTERS

None.

RELATED PARTY TRANSACTIONS

The Company receives loan guarantees from the chief executive officer with regards to its long-term borrowing, and the Company’s restricted cash provided as collateral to the Company’s chief executive officer’s loans.

Available Information

We will make available free of charge any of our filings as soon as reasonably practicable after we electronically file these materials with, or otherwise furnish them to, the Securities and Exchange

Commission (“SEC”). We are not including the information contained in our website as part of, or incorporating it by reference into, this report on Form 10-K.

The public may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Room 1580, Washington, D.C. 20002. The public may obtain information on the

operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC at

http://www.sec.gov.

Within our website’s “Investor” section, “SEC Filings” tab, all of our filings with the Commission and all amendments to these reports are available as soon as reasonably practicable after filing.

Website

Our website address is www.i-on.net.

Our Information

Our principal executive offices are located at 15, Teheran-ro 10-gil, Gangnam-gu, Seoul, Korea 06234 and our telephone number is 82-2-3430-1200. We can be contacted by email at ir@i-on.net.

Our business, financial condition, operating results and prospects are subject to the following risks. Additional risks and uncertainties not presently foreseeable to us may also impair our business

operations. If any of the following risks actually occurs, our business, financial condition or operating results could be materially adversely affected. In such case, the trading price of our common stock could decline, and our stockholders may lose

all or part of their investment in the shares of our common stock.

This Form 10-K contains forward-looking statements that involve risks and uncertainties. These forward-looking statements can be identified by the use of words such as “believes,” “estimates,”

“intends”, “plans”, “could,” “possibly,” “probably,” anticipates,” “projects,” “expects,” “may,” “will,” or “should,” “designed to,” “designed for,” or other variations or similar words or language. Actual results could differ materially from those

discussed in the forward-looking statements as a result of certain factors, including those set forth below and elsewhere in this Form 10-K.

Risks Related to Pandemics

The recent COVID-19 coronavirus pandemic may adversely affect our business, results of operations, financial condition, liquidity, and cash flow.

While the impact on our business from the recent outbreak of the COVID-19 coronavirus is unknown at this time and difficult to predict, various aspects of our business could be

adversely affected by it.

As of the date of this Annual Report, COVID-19 coronavirus has been declared a pandemic by the World Health Organization, has been declared a National Emergency by the United States

Government and has resulted in several states being designated disaster zones. COVID-19 coronavirus caused significant volatility in global markets, including the market price of our securities. The spread of COVID-19 coronavirus has caused public

health officials to recommend precautions to mitigate the spread of the virus, especially as to travel and congregating in large numbers. In addition, certain states and municipalities have enacted, and additional cities are considering,

quarantining and “shelter-in-place” regulations which severely limit the ability of people to move and travel, and require non-essential businesses and organizations to close.

It is unclear how such restrictions, which will contribute to a general slowdown in the global economy, will affect our business, results of operations, financial condition and our

future strategic plans.

Shelter-in-place and essential-only travel regulations have negatively impacted many of our customers. In addition, while our digesters are manufactured in the United States, we

still could experience significant supply chain disruptions due to interruptions in operations at any or all of our suppliers’ facilities. If we experience significant delays in receiving our products we will experience delays in fulfilling orders

and ultimately receiving payment, which could result in loss of sales and a loss of customers, and adversely impact our financial condition and results of operations.

In addition, our headquarters are located in Seoul, South Korea which was also subject to large COVID-19 outbreak requiring its government to enact travel and work restrictions.

While these restrictions were lessened as of the date of this Annual Report, it is unclear at this time how these restrictions will affect our operations and revenues.

Risks Specific to Our Business

Our proprietary software or service delivery may not operate properly, which could damage our reputation, give rise to claims against us, or divert application of our resources

from other purposes, any of which could harm our business and operating results.

We may encounter human or technical obstacles that prevent our proprietary applications from operating properly. If our applications do not function reliably or fail to achieve customer expectations in terms of

performance, customers could assert liability claims against us or attempt to cancel their contracts with us. This could damage our reputation and impair our ability to attract or maintain customers. We provide a limited warranty, have not paid

warranty claims in the past, and do not have a reserve for warranty claims.

Moreover, information services as complex as those we offer have in the past contained, and may in the future develop or contain, undetected defects or errors. We cannot assure you that material performance problems or

defects in our products or services will not arise in the future. Errors may result from receipt, entry, or interpretation of customer information or from interface of our services with legacy systems and data that we did not develop and the function

of which is outside of our control. Despite testing, defects or errors may arise in our existing or new software or service processes. These defects and errors and any failure by us to identify and address them could result in loss of revenue or

market share, liability to customers or others, failure to achieve market acceptance or expansion, diversion of development resources, injury to our reputation, and increased service and maintenance costs. Defects or errors in our software might

discourage existing or potential customers from purchasing our products and services. Correction of defects or errors could prove to be impossible or impracticable. The costs incurred in correcting any defects or errors or in responding to resulting

claims or liability may be substantial and could adversely affect our operating results.

If our security measures are breached or fail and unauthorized access is obtained to a customer’s data, our service may be perceived as insecure, the attractiveness of our

services to current or potential customers may be reduced, and we may incur significant liabilities.

Our services involve the web-based storage and transmission of customers’ proprietary information. We rely on proprietary and commercially available systems, software, tools and monitoring, as well as other processes,

to provide security for processing, transmission and storage of such information. Because of the sensitivity of this information and due to requirements under applicable laws and regulations, the effectiveness of our security efforts is very

important. If our security measures are breached or fail as a result of third-party action, acts of terror, social unrest, employee error, malfeasance or for any other reasons, someone may be able to obtain unauthorized access to customer data.

Improper activities by third-parties, advances in computer and software capabilities and encryption technology, new tools and discoveries and other events or developments may facilitate or result in a compromise or breach of our security systems. Our

security measures may not be effective in preventing unauthorized access to the customer data stored on our servers. If a breach of our security occurs, we could face damages for contract breach, penalties for violation of applicable laws or

regulations, possible lawsuits by individuals affected by the breach and significant remediation costs and efforts to prevent future occurrences. In addition, whether there is an actual or a perceived breach of our security, the market perception of

the effectiveness of our security measures could be harmed and we could lose current or potential customers.

Disruptions in Internet or telecommunication service or damage to our data centers could adversely affect our business by reducing our customers’ confidence in the reliability of

our services and products.

Our information technologies and systems are vulnerable to damage or interruption from various causes, including acts of God and other natural disasters, war and acts of terrorism and power losses, computer systems

failures, internet and teleDigital or data network failures, operator error, losses of and corruption of data and similar events. Data regarding our business and our customers’ insurance claims and encounters resides on computer hardware located

domestically and abroad. Although we conduct business continuity planning to protect against fires, floods, other natural disasters and general business interruptions to mitigate the adverse effects of a disruption, relocation or change in

operating environment at our data centers, the situations we plan for and the amount of insurance coverage we maintain may not be adequate in any particular case. In addition, the occurrence of any of these events could result in interruptions,

delays or cessations in service to our customers. Any of these events could impair or prohibit our ability to provide our services, reduce the attractiveness of our services to current or potential customers and adversely impact our financial

condition and results of operations.

In addition, despite the implementation of security measures, our infrastructure, data centers, or systems that we interface with or utilize, including the internet and related systems, may be vulnerable to physical

break-ins, hackers, improper employee or contractor access, computer viruses, programming errors, denial-of-service attacks or other attacks by third-parties seeking to disrupt operations or misappropriate information or similar physical or

electronic breaches of security. Any of these can cause system failure, including network, software or hardware failure, which can result in service disruptions. As a result, we may be required to expend significant capital and other resources to

protect against security breaches and hackers or to alleviate problems caused by such breaches.

We depend on key information systems and third party service providers.

We depend on key information systems to accurately and efficiently transact our business. These systems and services are vulnerable to interruptions or other failures resulting from, among other things, natural

disasters, terrorist attacks, software, equipment or teleDigital failures, processing errors, computer viruses, other security issues or supplier defaults. Security, backup and disaster recovery measures may not be adequate or implemented properly to

avoid such disruptions or failures. Any disruption or failure of these systems or services could cause substantial errors, processing inefficiencies, security breaches, inability to use the systems or process transactions, loss of customers or other

business disruptions, all of which could negatively affect our business and financial performance.

As cybersecurity attacks continue to evolve and increase, our information systems could also be penetrated or compromised by internal and external parties’ intent on extracting confidential information, disrupting

business processes or corrupting information. These risks could arise from external parties or from acts or omissions of internal or service provider personnel. Such unauthorized access could disrupt our business and could result in the loss of

assets, litigation, remediation costs, damage to our reputation and failure to retain or attract customers following such an event, which could adversely affect our business.

We may be unable to adequately establish, protect or enforce our intellectual property rights.

Our success depends in part upon our ability to establish, protect and enforce our intellectual property and other proprietary rights. If we fail to establish, protect or enforce our intellectual property rights, we

may lose an important advantage in the market in which we compete. We rely on a combination of trademark, copyright and trade secret law and contractual obligations to protect our key intellectual property rights, all of which provide only limited

protection. Our intellectual property rights may not be sufficient to help us maintain our position in the market and our competitive advantages.

We hold several patents and also rely on trade secrets to protect certain of our proprietary technology. However, trade secrets may not be protectable if not properly kept confidential. We strive to enter into

non-disclosure agreements with our employees, customers, contractors and business partners to limit access to and disclosure of our proprietary information. However, the steps we have taken may not be sufficient to prevent unauthorized use of our

technology, and adequate remedies may not be available in the event of unauthorized use or disclosure of our trade secrets and proprietary technology. Moreover, others may reverse engineer or independently develop technologies that are competitive to

ours or infringe our intellectual property.

Accordingly, despite our efforts, we may be unable to prevent third-parties from using our intellectual property for their competitive advantage. Any such use could have a material adverse effect on our business,

results of operations and financial condition. Monitoring unauthorized uses of and enforcing our intellectual property rights can be difficult and costly. Legal intellectual property actions are inherently uncertain and may not be successful, and

may require a substantial amount of resources and divert our management’s attention.

Claims by others that we infringe their intellectual property could force us to incur significant costs or revise the way we conduct our business.

Our competitors protect their proprietary rights by means of patents, trade secrets, copyrights, trademarks and other intellectual property. We have not conducted an independent review of patents and other intellectual

property issued to third-parties, who may have patents or patent applications relating to our proprietary technology. We may receive letters from third parties alleging, or inquiring about, possible infringement, misappropriation or violation of

their intellectual property rights. Any party asserting that we infringe, misappropriate or violate proprietary rights may force us to defend ourselves, and potentially our customers, against the alleged claim. These claims and any resulting lawsuit,

if successful, could subject us to significant liability for damages and/or invalidation of our proprietary rights or interruption or cessation of our operations. Any such claims or lawsuit could:

|

●

|

be time-consuming and expensive to defend, whether meritorious or not;

|

| ● |

require us to stop providing products or services that use the technology that allegedly infringes the other party’s intellectual property;

|

| ● |

divert the attention of our technical and managerial resources;

|

| ● |

require us to enter into royalty or licensing agreements with third-parties, which may not be available on terms that we deem acceptable;

|

| ● |

prevent us from operating all or a portion of our business or force us to redesign our products, services or technology platforms, which could be difficult and expensive and may make the performance or value of our product or service

offerings less attractive;

|

| ● |

subject us to significant liability for damages or result in significant settlement payments; or

|

| ● |

require us to indemnify our customers.

|

Furthermore, during the course of litigation, confidential information may be disclosed in the form of documents or testimony in connection with discovery requests, depositions or trial testimony. Disclosure of our

confidential information and our involvement in intellectual property litigation could materially adversely affect our business. Some of our competitors may be able to sustain the costs of intellectual property litigation more effectively than we can

because they have substantially greater resources. In addition, any litigation could significantly harm our relationships with current and prospective customers. Any of the foregoing could disrupt our business and have a material adverse effect on

our business, operating results and financial condition.

The continued success of our business model is heavily dependent upon our offshore operations, and any disruption to those operations will adversely affect us.

The majority of our operations, including the development and maintenance of our Web-based platform and our customer support services, are performed by our highly educated workforce of approximately 120 employees in

South Korea which may experience unrest due to the threats posed by North Korea. The performance of our operations in South Korea, and our ability to maintain our offshore offices, is an essential element of our business model, as South Korea is a

tech hub for Enterprise CMS/Digital marketing as well as all of our senior leadership are located in South Korea. Our competitive advantage will be greatly diminished and may disappear altogether if our operations in South Korea are negatively

impacted.

Our offshore operations expose us to additional business and financial risks which could adversely affect us and subject us to civil and criminal liability.

The risks and challenges associated with our operations outside the United States include laws and business practices favoring local competitors; compliance with multiple, conflicting and changing governmental laws and

regulations, including employment and tax laws and regulations; and fluctuations in foreign currency exchange rates. Foreign operations subject us to numerous stringent U.S. and foreign laws, including the Foreign Corrupt Practices Act, or FCPA, and

comparable foreign laws and regulations that prohibit improper payments or offers of payments to foreign governments and their officials and political parties by U.S. and other business entities for the purpose of obtaining or retaining business.

Safeguards we implement to discourage these practices may prove to be less than effective and violations of the FCPA and other laws may result in severe criminal or civil sanctions, or other liabilities or proceedings against us, including class

action lawsuits and enforcement actions from the SEC, Department of Justice and overseas regulators.

Future product development is dependent upon access to and reliability of third party software products and open source software.

Certain of our software products contain components developed and maintained by third party software vendors. We expect that we may have to incorporate software from third party vendors in our future

products. We also incorporate open source software in certain of our software products. We may not be able to replace the functionality provided by the third party or open source software currently offered with our products if that software becomes

obsolete, defective, non-compliant with third party patent restrictions or incompatible with future versions of our products or is not adequately maintained or updated, or if our relationship with the third party vendor terminates. In addition, we

must carefully monitor and manage our use of, and compliance with the licensing requirements of, open source software. Any significant interruption in the availability of these third party software products on commercially acceptable terms, defects

in these products, non-compliance with third party patent restrictions or our inability to comply with the licensing terms of either third party commercial software or open source software could delay development of future products or enhancement of

future products and could have a material adverse effect on our business, financial condition, operating results and cash flows.

Future product development is dependent on adequate research and development resources.

In order to remain competitive, we must continue to develop new products and enhancements to our existing products. This is particularly true as we further expand our cloud and SaaS offerings and

capabilities. Maintaining adequate research and development resources to meet the demands of the market is essential, and failure to do so could present an advantage to our competitors. If we are unable to develop products due to certain constraints,

such as high employee turnover, lack of management ability or a lack of other development resources, including through third party outsourcing firms, our competitiveness could be harmed.

Discovery of errors in our software could adversely affect our earnings.

The software products we offer are inherently complex. Despite testing and quality control, we cannot be certain that errors will not be found in current versions, new versions or enhancements of our

products after commencement of commercial delivery. If new or existing customers have difficulty deploying our products or require significant amounts of customer support, our operating margins could be harmed. Moreover, we could face possible claims

and higher development costs if our software contains undetected errors or if we fail to meet our customers’ expectations. With our BSM strategy, these risks increase because we are combining already complex products to create solutions that are even

more complicated than the aggregation of their product components. Significant technical challenges could also arise with our products because our customers purchase and deploy our products across a variety of computer platforms and integrate them

with a number of third party software applications and databases. These combinations increase our risk further because in the event of a system-wide failure, it may be difficult to determine which product is at fault; thus, we may be harmed by the

failure of another supplier’s products.

As a result of the foregoing, we could experience loss of or delay in revenue and loss of market share; loss of customers; damage to our reputation; failure to achieve market acceptance; diversion of

development resources; increased service and warranty costs; legal actions by customers against us which could, whether or not successful, increase costs and distract our management; and increased insurance costs.

Risks Related to Securities Markets and Investments in Our Securities

General securities market uncertainties resulting from the COVID-19 pandemic.

Since the outset of the pandemic the US and worldwide national securities markets have undergone unprecedented stress due to the uncertainties of the pandemic and the resulting

reactions and outcomes of government, business and the general population. These uncertainties have resulted in declines in all market sectors, increases in volumes due to flight to safety and governmental actions to support the markets. As a

result, until the pandemic has stabilized, the markets may not be available to the Company for purposes of raising required capital. Should we not be able to obtain financing when required, in the amounts necessary to execute on our plans in full,

or on terms which are economically feasible we may be unable to sustain the necessary capital to pursue our strategic plan and may have to reduce the planned future growth and scope of our operations.

Our executive officers and certain stockholders possess the majority of our voting power, and through this ownership, control our Company and our corporate actions.

Our current executive officers, directors and largest stockholders of the Company, hold approximately 37% of the voting power of the outstanding shares as of December 31, 2020. These officers,

directors and certain stockholders have a controlling influence in determining the outcome of any corporate transaction or other matters submitted to our stockholders for approval, including mergers, consolidations and the sale of all or

substantially all of our assets, election of directors, and other significant corporate actions. The interests of our executive officers and certain shareholders may give rise to a conflict of interest with the Company and the Company’s

stockholders. For additional details concerning voting power please refer to the section below entitled “Description of Securities.”

Liquidity of our common stock has been limited.

Our common stock is quoted on OTC Markets under the symbol “IONI”. The liquidity of our common stock is very limited and is affected by our limited trading market. The OTC Markets is an inter-dealer

market much less regulated than the major exchanges, and is subject to abuses, volatilities and shorting. There is currently no broadly followed and established trading market for our common stock. An established trading market may never develop or

be maintained. Active trading markets generally result in lower price volatility and more efficient execution of buy and sell orders. Absence of an active trading market reduces the liquidity of the shares traded.

The trading volume of our common stock may be limited and sporadic. This situation is attributable to a number of factors, including the fact that we are a small company that is relatively unknown to

stock analysts, stock brokers, institutional investors and others in the investment community that generate or influence sales volume, and that even if we came to the attention of such persons, they may tend to be risk-averse and would be reluctant

to follow an unproven company such as ours or purchase or recommend the purchase of our shares until such time as we became more seasoned and viable. As a consequence, there may be periods of several days or more when trading activity in our shares

is minimal, as compared to a seasoned issuer that has a large and steady volume of trading activity that will generally support continuous sales without an adverse effect on share price. We cannot give any assurance that a broader or more active

public trading market for our common stock will develop or be sustained, or that current trading levels will be sustained. As a result of such trading activity, the quoted price for our common stock while on the OTC Markets may not necessarily be a

reliable indicator of its fair market value.

Because we became public by means of a “reverse business combination,” we may not be able to attract the attention of major brokerage firms.