Exhibit (c)(3)

CONFIDENTIAL Project Obsidian Conflicts Committee Discussion Materials June 18, 2018

CONFIDENTIAL Disclaimer These discussion materials and any supplemental information (written or oral) or other documents provided in connection therewith (collectively the “materials”) are provided solely for the information of the Conflicts Committee of the Board of Directors (the “Committee”) of Obsidian by Tudor Pickering Holt & Co Advisors LP (“TPH”) in connection with the Committee’s consideration of a potential transaction (the “Transaction”) involving the sale of the outstanding public units of Obsidian. This presentation is incomplete without reference to, and should be considered in conjunction with, any supplemental information provided by and discussions with TPH in connection therewith. The materials are for discussion purposes only and may not be relied upon by any person or entity for any purpose without TPH’s express prior written consent. The materials were prepared for specific persons familiar with the business and affairs of Obsidian for use in a specific context and were not prepared with a view to public disclosure or to conform with any disclosure standards under any state, federal or international securities laws or other laws, rules or regulations, and neither the Board of Directors of Obsidian (the “Board”) nor TPH takes any responsibility for the use of the materials by persons other than Obsidian. The materials are provided on a confidential basis solely for the information of Obsidian and may not be disclosed, summarized, reproduced, disseminated or quoted or otherwise referred to, in whole or in part, without TPH’s express prior written consent. The materials necessarily are based on financial, economic, market and other conditions as in effect on, and the information available to TPH as of June 18, 2018 the date of the materials. Although subsequent developments may affect the contents of the materials, TPH has not undertaken, and is under no obligation, to update, revise or reaffirm the materials. The materials are not intended to provide the sole basis for evaluation of the Transaction and do not purport to contain all information that may be required. The materials do not address the underlying business decision of Obsidian or any other party to proceed with or effect the Transaction. The materials do not constitute any opinion, nor do the materials constitute a recommendation to Obsidian, any security holder of Obsidian or any other person as to how to vote or act with respect to any matter relating to the Transaction or whether to buy or sell any assets or securities of any company. TPH’s only opinion will be the opinion, if any, that is actually delivered to Obsidian in connection with the Transaction. The materials may not reflect information known to other professionals in other business areas of TPH and its affiliates. The preparation of the materials was a complex process involving quantitative and qualitative judgments and determinations with respect to the financial, comparative and other analytic methods employed and the adaptation and application of these methods to the unique facts and circumstances presented and, therefore, is not readily susceptible to partial analysis or summary description. Accordingly, the analyses contained in the materials must be considered as a whole. Selecting portions of the analyses, analytic methods and factors without considering all analyses and factors could create a misleading or incomplete view. The materials reflect judgments and assumptions with regard to industry performance, general business, economic, regulatory, market and financial conditions and other matters, many of which are beyond the control of the participants in the Transaction. Any estimates of value contained in the materials are not necessarily indicative of actual value or predictive of future results or values, which may be significantly more or less favorable. In addition, any analyses relating to the value of assets, businesses or securities do not purport to be appraisals or to reflect the prices at which any assets, businesses or securities may actually be purchased or sold. All budgets, projections, estimates, financial analyses, reports and other information with respect to operations reflected in the materials have been prepared by management of the relevant party or are derived from such budgets, projections, estimates, financial analyses, reports and other information or from other sources, which involve numerous and significant subjective determinations made by management of the relevant party and/or which such management has reviewed and found reasonable. The budgets, projections and estimates contained in the materials may or may not be achieved and differences between projected results and those actually achieved may be material. TPH has relied upon representations made by management that such budgets, projections and estimates have been reasonably prepared in good faith on bases reflecting the best currently available estimates and judgments of such management (or, with respect to information obtained from public sources, represent reasonable estimates), and TPH expresses no opinion with respect to such budgets, projections or estimates or the assumptions on which they are based. The scope of the financial analysis contained herein is based on discussions with Obsidian (including, without limitation, regarding the methodologies to be utilized), and TPH does not make any representation, express or implied, as to the sufficiency or adequacy of such financial analysis or the scope thereof for any particular purpose. TPH has assumed and relied upon the accuracy and completeness of the financial and other information provided to or reviewed by it without (and without assuming responsibility for) independent verification of such information, makes no representation or warranty (express or implied) in respect of the accuracy or completeness of such information and has further relied upon the assurances of relevant parties that they are not aware of any facts or circumstances that would make such information inaccurate or misleading. The materials are not an offer to sell or a solicitation of an indication of interest to purchase any security. The materials do not constitute a commitment by TPH or any of its affiliates to underwrite, subscribe for or place any securities, to extend or arrange credit, or to provide any other services. In the ordinary course of business, TPH and certain of its affiliates, as well as investment funds in which they may have financial interests, may acquire, hold or sell, long or short positions, or trade or otherwise effect transactions, in debt, equity, and other securities and financial instruments (including loans and other obligations) of, or investments in, one or more parties that may be involved in the Transaction and their respective affiliates or any currency or commodity that may be involved in the Transaction. TPH provides mergers and acquisitions, restructuring and other advisory services to clients. TPH’s personnel may make statements or provide advice that is contrary to information contained in the materials. TPH’s or its affiliates’ proprietary interests may conflict with Obsidian’s interests. TPH may have advised, may seek to advise and may in the future advise companies mentioned in the materials.

CONFIDENTIAL Agenda Situation Overview Financial Summary Obsidian Standalone Financial Analysis Supplemental Analysis Additional Analysis as Requested by Obsidian Conflicts Committee Note: Except otherwise noted, analysis has relied on cases provided by Management which reflects such Management’s best estimates 3 and judgment with respect to Obsidian and Onyx and is reasonable to evaluate Obsidian and Onyx’s contemplated transaction.

CONFIDENTIAL I. Situation Overview

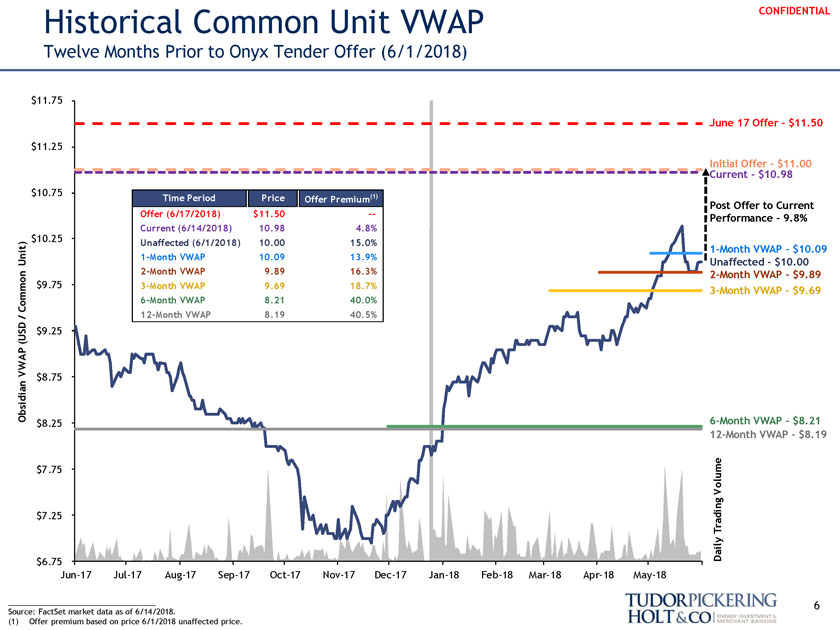

CONFIDENTIAL Situation Overview Parent increased unit ownership from 79.88% to 88.25% at average price of $8.40 on December 26, 2017 Nassef Onsi Sawiris additionally owns 1.01% Per the Amended & Restated Partnership Agreement, if the Parent holds more than 90% of the total LP interests at any time, then parent has the right to purchase all, but not less than all, of the remaining LP interests Purchase price for remaining units shall equal the greater of: The average daily closing price of the units on the NYSE for the 20 consecutive trading days immediately preceding the date that is three business days prior to the date on which the notice of the exercise of the above mentioned right is given ($10.46 as of 6/14/2018) The highest price paid by the GP or any of its affiliates for an units purchased during the 90 days preceding the date on which such notice is given (GP has not purchased any units since 12/26/2017) Tender offer of $11.00 per common unit for all remaining common units announced on June 4, 2018 Onyx Management communicated intent to increase tender offer to $11.50 per common unit on June 17, 2018 Represents a 15.0% premium over Obsidian closing price on June 1, 2018, a 13.9% premium over 1-month VWAP and a 18.7% premium over 3-month VWAP Tender offer conditioned on 90% threshold Committee required to make recommendation or state that it is neutral or unable to take a position with respect to the offer within 10 business days, or by June 18, 2018 Tender offer expires on July 2, 2018 and may be extended at Parent’s discretion Effective in 2027, methanol no longer qualifies as MLP income and Obsidian will pay a higher tax rate

Historical Common Unit VWAP CONFIDENTIAL Twelve Months Prior to Onyx Tender Offer (6/1/2018) $11.75 40, 00 June 17 Offer—$11.50 $11.25 350, 00 Initial Offer—$11.00 Current—$10.98 $10.75 (1) Time Period Price Offer Premium Post Offer to Current Offer (6/17/2018) $11.50 — 30, 00 Performance—9.8% Current (6/14/2018) 10.98 4.8% $10.25 Unaffected (6/1/2018) 10.00 15.0% t) i 1-Month VWAP—$10.09 Un 1-Month VWAP 10.09 13.9% Unaffected—$10.00 2-Month VWAP 9.89 16.3% 250, 00 2-Month VWAP—$9.89 $9.75 3-Month VWAP 9.69 18.7% Common 6-Month VWAP 8.21 40.0% 3-Month VWAP—$9.69 / 12-Month VWAP 8.19 40.5% (USD $9.25 20, 00 AP VW $8.75 n Obsidia 150, 00 $8.25 6-Month VWAP—$8.21 12-Month VWAP—$8.19 10, 00 $7.75 lume Vo 50, 00 $7.25 Trading Daily $6.75 0 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 May-18 Source: FactSet market data as of 6/14/2018. 6 (1) Offer premium based on price 6/1/2018 unaffected price.

CONFIDENTIAL Obsidian Ownership and Trading Overview (USD in millions, unless otherwise noted) Ownership – Top Holders (as of 3/31/2018) Daily Trading Volume as a % of Units O/S Obsidian IPO (10/3/13) to Current A B C D E Holdings Position Position % 1.0% Investor Name Style ($MM) (M shares) O/S Onyx Other Inst. $843 76,774 88.249% Morgan Stanley (Strategic Investments) Other Inst. 61 5,572 6.405% Nassef Sawiris Other Inst. 10 879 1.011% 0.8% Cowen Investment Management LLC Aggressive Growth 8 711 0.817% UBS Securities LLC Aggressive Growth 4 358 0.411% PCJ Investment Counsel Ltd. Value 2 150 0.172% Bard Associates, Inc. Aggressive Growth 2 150 0.172% 0.6% Credit Capital Investments LLC Value 1 70 0.081% Quinn Opportunity Partners LLC Value 1 69 0.080% Deutsche Asset Management Investment GmbH Aggressive Growth 0 36 0.042% Renaissance Technologies LLC Aggressive Growth 0 33 0.038% 0.4% Iconiq Capital LLC Aggressive Growth 0 18 0.021% Michael Bennett Other Inst. 0 15 0.017% Goldman Sachs & Co. LLC (Private Banking) Aggressive Growth 0 14 0.016% Worth Venture Partners LLC Growth 0 13 0.014% 0.2% Walleye Trading Advisors LLC Aggressive Growth 0 12 0.014% Deltec Asset Management LLC Aggressive Growth 0 12 0.013% Nathaniel Gregory Other Inst. 0 10 0.011% Wells Capital Management, Inc. Aggressive Growth 0 3 0.003% 0.0% Manulife Asset Management Ltd. Aggressive Growth 0 3 0.003% Oct-13 Apr-14 Oct-14 Apr-15 Oct-15 Apr-16 Oct-16 Apr-17 Oct-17 Apr-18 Merrill Lynch, Pierce, Fenner & Smith, Inc. (Invt Mgmt) Aggressive Growth 0 3 0.003% Citigroup Global Markets, Inc. (Broker) Aggressive Growth 0 2 0.002% Dod Fraser Other Inst. 0 1 0.001% 1 3 6 1 2 3 4 Since Ahmed El-Hoshy Other Inst. 0 1 0.001% Month Month Month Year Year Year Year IPO Morgan Stanley Smith Barney LLC (Private Banking) Aggressive Growth 0 0 0.000% ADTV (M Units) 24.4 16.6 56.9 32.7 29.6 38.8 40.3 71.4 Total—Top-25 Holders $932 84,907 97.597% Turnover— Total Owned by Onyx & Tenders $852 77,669 89.277% 0.0x 0.0x 0.1x 0.1x 0.2x 0.3x 0.5x 1.0x Units O/S(1) Disclosed Intent to Tender Units(2) Turnover—0.1x 0.1x 0.7x 0.8x 1.5x 3.0x 4.1x 8.6x ___________________________________ Public Float(1) Source: Company filings and FactSet market data as of 6/14/2018. Note: Ownership data sourced from quarterly filings, as of 3/31/2018. (1) Turnover represents volume traded over current outstanding / public units. 7 (2) Michael Bennett and Ahmed El-Hoshy disclosed intent to tender in 6/4/2018 Schedule TO-T and Nassef Sawiris disclosed intent to tender in 6/8/2018 Schedule TO-T/A.

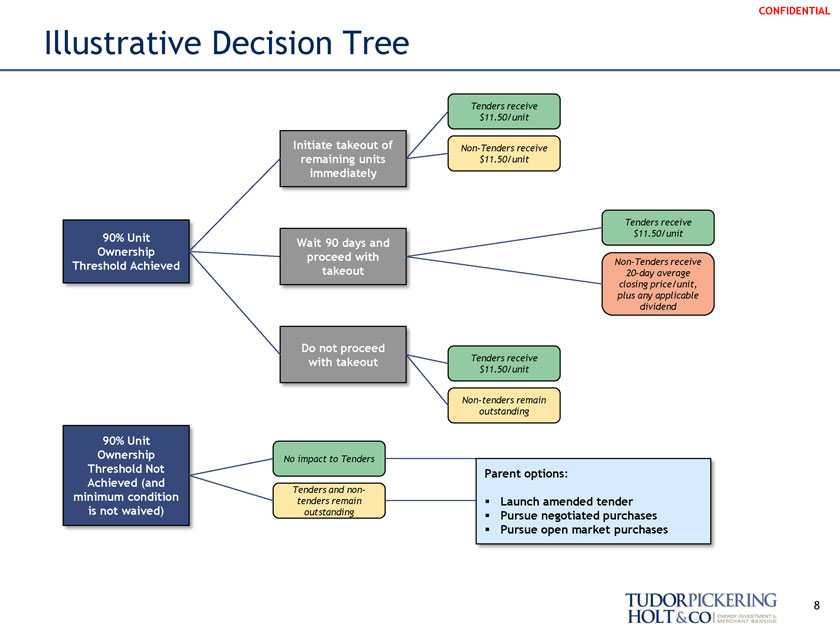

CONFIDENTIAL Illustrative Decision Tree Tenders receive $11.50/unit Non-Tenders receive 20-day average closing price/unit, plus any applicable dividend

CONFIDENTIAL II. Financial Summary

CONFIDENTIAL Summary of Model Scenarios Scenarios Shown Herein: Scenarios Provided by Onyx Management 1 Base Case Commodity Prices Reflects Management forecasts of methanol and ammonia base case pricing Consensus average commodity price forecast from 3 third-party consultants, including Argus, IHS Markit, and Methanol Market Services Asia (MMSA) Scenarios Not Provided by Onyx Management — Developed based on Discussions with Obsidian Conflicts Committee 2 Upside Commodity Prices Reflects Management’s base case methanol and ammonia price forecasts increased by 10% 3 Downside Commodity Prices Reflects Management’s base case methanol and ammonia price forecasts decreased by 10% 4 Low Utilization Reflects Management’s base case commodity price forecast and reflects a reduction in Obsidian’s methanol and ammonia capacity utilization rates via a decrease in Management’s forecasted commodity sales volumes by 10% 5 Methanol Debottlenecking Reflects Management’s base case commodity price and utilization forecasts in addition to a methanol debottlenecking project Assumes 10% increase in methanol capacity (91.25kt per year) realized in 2020E assuming same profit margin Assumes $45.6MM ($500/t) in capex funded with 5.50% debt incurred in 2019E (50% of estimated $1,000/t replacement cost) ï,§ Assumptions based on guidance from Obsidian Conflicts Committee 10 Sources: Obsidian filings, Onyx Management, investor presentations and Management model received 6/6/2018.

CONFIDENTIAL Historical and Projected Methanol Prices US Gulf Coast Spot Price Argus Methanol Contract Base Case Commodity Prices Upside Commodity Prices Downside Commodity Prices Obsidian Realized Methanol Argus Spot Argus Contract Index 5-Year 10-Year $700 Historical Historical Methanol: 2015A 2016A 2017A 2018E 2019E 2020E 2021E Average(1) Average(2) Obsidian Realized Prices(5) $325 $213 $325 $387 $352 $326 $338 $345 — Obsidian Discount to Argus Contract(5) 20% 22% 19% 18% 19% 20% 21% 16.8% — Base Case Commodity Prices — — — $473 $433 $409 $426 — — Upside Commodity Prices — — — 520 476 450 469 — — $600 Downside Commodity Prices — — — 426 390 368 383 — — Argus Spot Contract(3) $325 $224 $333 $379 $344 — — $355 $349 Argus Contract Index(4) 405 274 401 472 425 — — 429 428 $500 m t USD/ $400 $300 $200 $100 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12 Jun-13 Jun-14 Jun-15 Jun-16 Jun-17 Jun-18 Jun-19 Jun-20 Jun-21 Jun-22 Jun-23 Source: Management model received 6/6/2018, Argus and Bloomberg as of 6/14/2018. (1) 5-Year Obsidian Realized Prices and Discount to Argus Contract reflects only pricing available since the 10/3/2013 Obsidian IPO. (2) Historical Argus Contract prices reflects only pricing available since 1/1/2010. (3) Historical methanol prices reflects US Gulf Coast spot price (POLIUSGC Index). 11 Historical methanol prices reflects Argus fob US contract prices. 5-year historical average from 5/24/2013 to 5/25/2018. Forecasts reflect Base Case Commodity Prices.

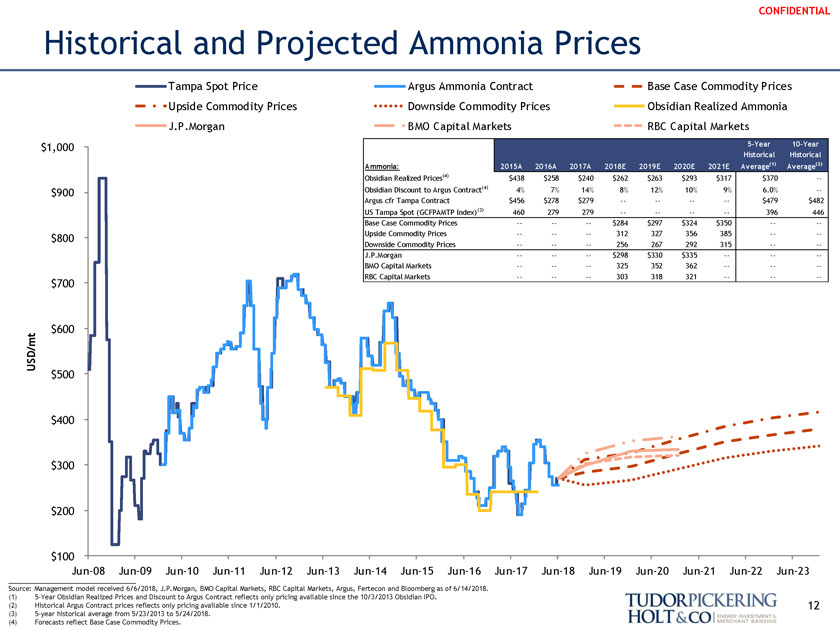

CONFIDENTIAL Historical and Projected Ammonia Prices Tampa Spot Price Argus Ammonia Contract Base Case Commodity Prices Upside Commodity Prices Downside Commodity Prices Obsidian Realized Ammonia J.P.Morgan BMO Capital Markets RBC Capital Markets $1,000 5-Year 10-Year Historical Historical Ammonia: 2015A 2016A 2017A 2018E 2019E 2020E 2021E Average(1) Average(2) Obsidian Realized Prices(4) $438 $258 $240 $262 $263 $293 $317 $370 — $900 Obsidian Discount to Argus Contract(4) 4% 7% 14% 8% 12% 10% 9% 6.0% — Argus cfr Tampa Contract $456 $278 $279 — — — — $479 $482 US Tampa Spot (GCFPAMTP Index)(3) 460 279 279 — — — — 396 446 Base Case Commodity Prices — — — $284 $297 $324 $350 — — $800 Upside Commodity Prices — — — 312 327 356 385 — — Downside Commodity Prices — — — 256 267 292 315 — — J.P.Morgan — — — $298 $330 $335 — — — BMO Capital Markets — — — 325 352 362 — — — RBC Capital Markets — — — 303 318 321 — — — $700 mt $600 U SD/ $500 $400 $300 $200 $100 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12 Jun-13 Jun-14 Jun-15 Jun-16 Jun-17 Jun-18 Jun-19 Jun-20 Jun-21 Jun-22 Jun-23 Source: Management model received 6/6/2018, J.P.Morgan, BMO Capital Markets, RBC Capital Markets, Argus, Fertecon and Bloomberg as of 6/14/2018. (1) 5-Year Obsidian Realized Prices and Discount to Argus Contract reflects only pricing available since the 10/3/2013 Obsidian IPO. (2) Historical Argus Contract prices reflects only pricing available since 1/1/2010. 12 5-year historical average from 5/23/2013 to 5/24/2018. Forecasts reflect Base Case Commodity Prices.

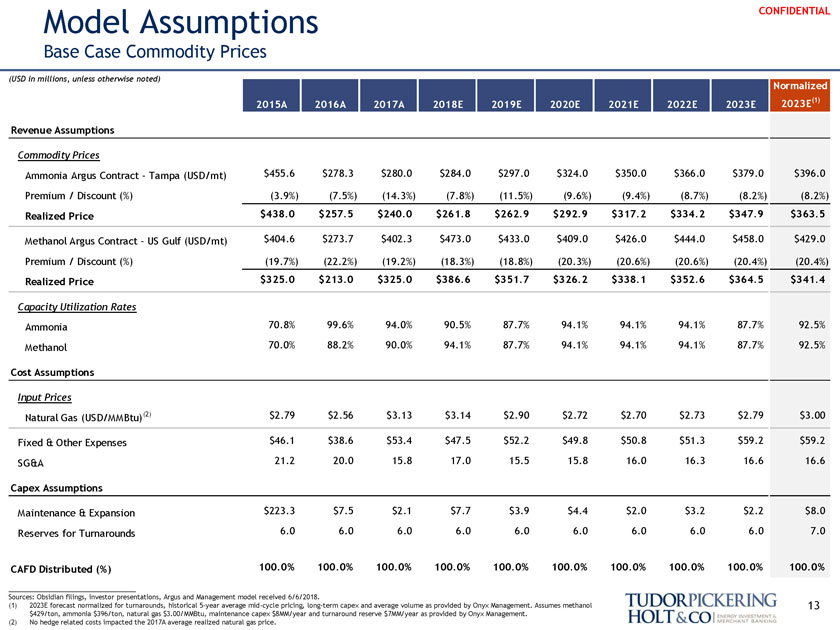

Model Assumptions CONFIDENTIAL Base Case Commodity Prices (USD in millions, unless otherwise noted) Normalized 2015A 2016A 2017A 2018E 2019E 2020E 2021E 2022E 2023E 2023E (1) Revenue Assumptions Commodity Prices Ammonia Argus Contract—Tampa (USD/mt) $455.6 $278.3 $280.0 $284.0 $297.0 $324.0 $350.0 $366.0 $379.0 $396.0 Premium / Discount (%) (3.9%) (7.5%) (14.3%) (7.8%) (11.5%) (9.6%) (9.4%) (8.7%) (8.2%) (8.2%) Realized Price $438.0 $257.5 $240.0 $261.8 $262.9 $292.9 $317.2 $334.2 $347.9 $363.5 Methanol Argus Contract—US Gulf (USD/mt) $404.6 $273.7 $402.3 $473.0 $433.0 $409.0 $426.0 $444.0 $458.0 $429.0 Premium / Discount (%) (19.7%) (22.2%) (19.2%) (18.3%) (18.8%) (20.3%) (20.6%) (20.6%) (20.4%) (20.4%) Realized Price $325.0 $213.0 $325.0 $386.6 $351.7 $326.2 $338.1 $352.6 $364.5 $341.4 Capacity Utilization Rates Ammonia 70.8% 99.6% 94.0% 90.5% 87.7% 94.1% 94.1% 94.1% 87.7% 92.5% Methanol 70.0% 88.2% 90.0% 94.1% 87.7% 94.1% 94.1% 94.1% 87.7% 92.5% Cost Assumptions Input Prices Natural Gas (USD/MMBtu) (2) $2.79 $2.56 $3.13 $3.14 $2.90 $2.72 $2.70 $2.73 $2.79 $3.00 Fixed & Other Expenses $46.1 $38.6 $53.4 $47.5 $52.2 $49.8 $50.8 $51.3 $59.2 $59.2 SG&A 21.2 20.0 15.8 17.0 15.5 15.8 16.0 16.3 16.6 16.6 Capex Assumptions Maintenance & Expansion $223.3 $7.5 $2.1 $7.7 $3.9 $4.4 $2.0 $3.2 $2.2 $8.0 Reserves for Turnarounds 6.0 6.0 6.0 6.0 6.0 6.0 6.0 6.0 6.0 7.0 CAFD Distributed (%) 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% Sources: Obsidian filings, investor presentations, Argus and Management model received 6/6/2018. (1) 2023E forecast normalized for turnarounds, historical 5-year average mid-cycle pricing, long-term capex and average volume as provided by Onyx Management. Assumes methanol 13 $429/ton, ammonia $396/ton, natural gas $3.00/MMBtu, maintenance capex $8MM/year and turnaround reserve $7MM/year as provided by Onyx Management. (2) No hedge related costs impacted the 2017A average realized natural gas price.

Forecast Detail CONFIDENTIAL Base Case Commodity Prices (USD in millions, unless otherwise noted) 2015A 2016A 2017A 2018E 2019E 2020E 2021E 2022E 2023E Ammonia Revenue $99 $84 $77 $81 $87 $98 $106 $111 $115 Methanol Revenue 210 174 267 335 284 280 290 303 294 Variable Costs (120) (179) (145) (154) (140) (138) (137) (139) (135) Fixed Costs (46) (20) (53) (47) (52) (50) (51) (51) (59) Total SG&A & Other Costs (21) (1) (16) (17) (15) (16) (16) (16) (17) EBITDA (1) $123 $59 $128 $197 $164 $174 $192 $208 $199 Normalized—Turnarounds (5) 192 172 170 187 203 207 Normalized—Turnarounds, Pricing, Capex & Volume (6) 184 Interest Expense (2) ($20) ($47) ($43) ($43) ($35) ($35) ($35) ($34) ($34) Cash Taxes Paid (0) (1) (1) (1) (1) (1) (1) (2) (2) Change in Net Working Capital (2) (49) 8 (16) (9) (8) (8) (8) (8) (8) Maintenance Capex (3) (172) (7) (2) (8) (4) (4) (2) (3) (2) Turnaround Reserve (6) (6) (6) (6) (6) (6) (6) (6) (6) Total Capex ($178) ($13) ($8) ($14) ($10) ($10) ($8) ($9) ($8) Cash Available for Distribution (4) $64 $6 $61 $130 $110 $119 $140 $155 $146 Normalized—Turnarounds (5) 125 118 115 135 150 155 Normalized—Turnarounds, Pricing, Capex & Volume (6) 125 Distributions Public Common Units $13 $1 $12 $15 $13 $14 $16 $18 $17 Onyx Common Units 51 5 49 115 97 105 123 136 129 Total Distributions $64 $6 $61 $130 $110 $119 $140 $155 $146 Common LP Units Outstanding 87.0 87.0 87.0 87.0 87.0 87.0 87.0 87.0 87.0 Cash Available for Distribution / Unit $0.73 $0.07 $0.70 $1.49 $1.26 $1.37 $1.61 $1.78 $1.68 Distributions / Unit 0.73 0.07 0.70 1.49 1.26 1.37 1.61 1.78 1.68 Net Debt $437 $457 $428 $399 $399 $399 $399 $399 $399 Net Debt / LTM EBITDA 3.6x 7.8x 3.3x 2.0x 2.4x 2.3x 2.1x 1.9x 2.0x Sources: Obsidian filings, investor presentations and Management model received 6/6/2018. (1) Adjusted to exclude the loss on disposition of fixed assets in Q4 2017. (2) Interest expense and change in net working capital per 10-K filings. (3) Reported maintenance capex assumed to include $6MM of turnaround reserve. (4) Assumes cash available for distribution equal to distributed cash per 10-K filings. (5) Forecasts normalized for turnarounds each year of projection period as provided by Onyx Management. 14 2023E forecast normalized for turnarounds, historical 5-year average mid-cycle pricing, long-term capex and average volume as provided by Onyx Management. Assumes methanol $429/ton, ammonia $396/ton, natural gas $3.00/MMBtu, maintenance capex $8MM/year and turnaround reserve $7MM/year as provided by Onyx Management.

Sensitivity Analysis CONFIDENTIAL EBITDA (USD in millions) $250 $239 $240 $249 Upside $231 Commodity Prices $229 $230 $219 Methanol $212 $211 $208 Debottlenecking $210 $201 $197 $199 Base Case $192 $192 Commodity Prices $190 $180 $174 $171 $171 $166 Low Utilization $170 $164 $163 $150 $166 Downside Commodity Prices $150 $156 $158 $141 $152 $130 $128 $136 $123 Actual $127 $110 $90 $70 $59 $50 2014A 2015A 2016A 2017A 2018E 2019E 2020E 2021E 2022E 2023E 15 Sources: Obsidian filings, investor presentations and Management model received 6/6/2018.

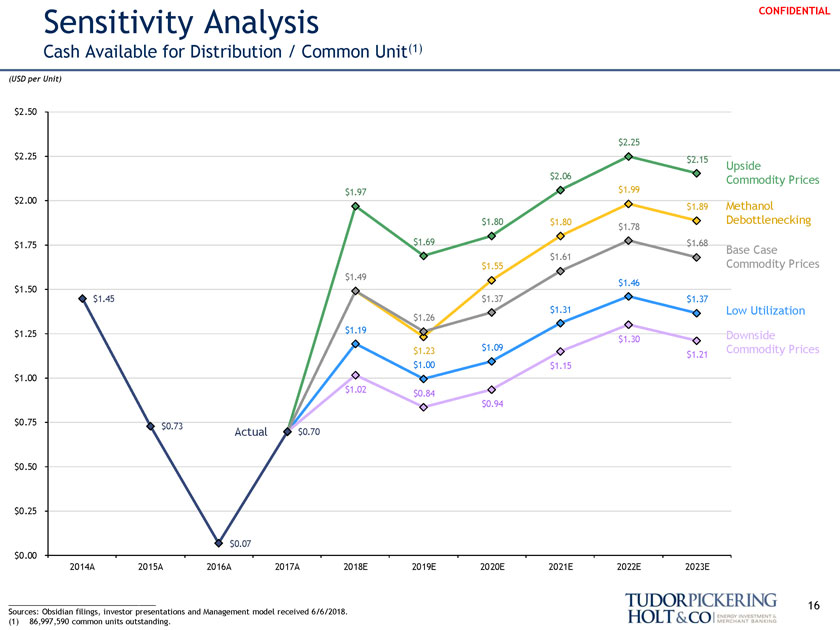

Sensitivity Analysis CONFIDENTIAL Cash Available for Distribution / Common Unit(1) (USD per Unit) $2.50 $2.25 $2.25 $2.15 Upside $2.06 Commodity Prices $1.97 $1.99 $2.00 $1.89 Methanol $1.80 $1.80 Debottlenecking $1.78 $1.75 $1.69 $1.68 Base Case $1.61 $1.55 Commodity Prices $1.49 $1.46 $1.50 $1.45 $1.37 $1.37 $1.31 Low Utilization $1.26 $1.25 $1.19 $1.30 Downside $1.23 $1.09 Commodity Prices $1.21 $1.00 $1.15 $1.00 $1.02 $0.84 $0.94 $0.75 $0.73 Actual $0.70 $0.50 $0.25 $0.07 $0.00 2014A 2015A 2016A 2017A 2018E 2019E 2020E 2021E 2022E 2023E ___________________________________ 16 Sources: Obsidian filings, investor presentations and Management model received 6/6/2018. (1) 86,997,590 common units outstanding.

CONFIDENTIAL III. Obsidian Standalone Financial Analysis

CONFIDENTIAL Illustrative Analysis at Various Unit Prices (USD in millions, except per unit (share) data) Unaffected Current Offer Obsidian Unit Price $10.00 $10.98 $11.50 Selected Obsidian Comparables Groups Implied Premium / (Discount) to Unaffected 0.0% 9.8% 15.0% Publicly Held Units 10.2 10.2 10.2 Publicly Held Equity Value $102 $112 $118 Total Units Outstanding 87.0 87.0 87.0 Implied Total Equity Value $870 $955 $1,000 Net Debt 399 399 399 Implied Enterprise Value $1,269 $1,354 $1,399 Trading Median Metric Base Case Commodity Prices Methanol / Nitrogen Methanex Transaction Median EV / 2018E EBITDA $197 6.4x 6.9x 7.1x 10.7x 7.1x 7.6x EV / 2019E EBITDA 164 7.7x 8.3x 8.5x 7.7x 8.0x — Price / 2018E CAFD $130 6.7x 7.4x 7.7x 6.9x 6.5x — Price / 2019E CAFD 110 7.9x 8.7x 9.1x 7.6x 7.1x — 2018E Yield $1.49 14.9% 13.6% 13.0% 2.7% 1.9% — 2019E Yield 1.26 12.6% 11.5% 11.0% 2.7% 2.0% — Upside Commodity Prices EV / 2018E EBITDA $239 5.3x 5.7x 5.9x — — 7.6x EV / 2019E EBITDA 201 6.3x 6.7x 7.0x — — — Price / 2018E CAFD $171 5.1x 5.6x 5.8x — — — Price / 2019E CAFD 147 5.9x 6.5x 6.8x — — — 2018E Yield $1.97 19.7% 18.0% 17.1% — — — 2019E Yield 1.69 16.9% 15.4% 14.7% — — — Downside Commodity Prices EV / 2018E EBITDA $156 8.1x 8.7x 9.0x — — 7.6x EV / 2019E EBITDA 127 10.0x 10.7x 11.0x — — — Price / 2018E CAFD $88 9.8x 10.8x 11.3x — — — Price / 2019E CAFD 73 12.0x 13.1x 13.7x — — — 2018E Yield $1.02 10.2% 9.2% 8.8% — — — 2019E Yield 0.84 8.4% 7.6% 7.3% — — — Low Utilization EV / 2018E EBITDA $171 7.4x 7.9x 8.2x 10.7x 7.1x 7.6x EV / 2019E EBITDA 141 9.0x 9.6x 9.9x 7.7x 8.0x — Price / 2018E CAFD $104 8.4x 9.2x 9.6x 6.9x 6.5x — Price / 2019E CAFD 87 10.0x 11.0x 11.5x 7.6x 7.1x — 2018E Yield $1.19 11.9% 10.9% 10.4% 2.7% 1.9% — 2019E Yield 1.00 10.0% 9.1% 8.7% 2.7% 2.0% — Sources: Management model received 6/6/2018, company filings, investor presentations, Wall Street equity research and median Wall Street consensus estimates 18 as compiled by FactSet as of 6/14/2018.

Selected Public Trading Comparables CONFIDENTIAL Methanol and Nitrogen Peers | Forecasts Normalized for Turnarounds (USD in millions, except per unit (share) data) A B C D E F G H I J K L M N O Unit (Share) Equity Price / Enterprise Value / Net Debt / EV / Price @ Market Enterprise CAFD (CF) / Unit (Share) EBITDA Distribution (Dividend) Yield 2018E Capacity Company 6/14/18 Value Value 2017A 2018E 2019E 2017A 2018E 2019E Current 2018E 2019E EBITDA ($/mt/year) CF Industries Holding, Inc. $44.92 $10,535 $17,751 6.4x 8.7x 8.1x 15.0x 13.3x 10.9x 2.7% 2.7% 2.7% 3.1x $890 LSB Industries, Inc. 5.15 158 736 61.7x 6.6x 1.8x 18.6x 11.5x 5.4x 0.0% NA NA 6.0x 521 Methanex Corporation 68.40 5,710 7,193 8.5x 6.5x 7.1x 10.1x 7.1x 8.0x 1.9% 1.9% 2.0% 1.1x 846 CVR Partners, LP 2.78 315 880 NM 7.1x 10.7x 13.4x 9.9x 7.3x 0.0% 5.8% 14.0% 6.4x 373 Median $3,012 $4,037 8.5x 6.9x 7.6x 14.2x 10.7x 7.7x 1.0% 2.7% 2.7% 4.6x $684 Mean 4,179 6,640 25.5x 7.2x 6.9x 14.3x 10.5x 7.9x 1.2% 3.5% 6.2% 4.2x $657 Minimum $158 $736 6.4x 6.5x 1.8x 10.1x 7.1x 5.4x 0.0% 1.9% 2.0% 1.1x $373 Maximum 10,535 17,751 61.7x 8.7x 10.7x 18.6x 13.3x 10.9x 2.7% 5.8% 14.0% 6.4x $890 Obsidian—Unaffected Price (6/1/18) $10.00 $870 $1,269 14.3x 9.9x 15.2% $1,020 Base Case Commodity Prices(1) 7.0x 7.4x 6.6x 7.4x 14.3% 13.6% 2.1x Low Utilization(1) 8.8x 9.3x 7.6x 8.6x 11.4% 10.8% 2.4x Obsidian—Current Price (6/14/18) $10.98 $955 $1,354 15.7x 10.5x 13.8% $1,089 Base Case Commodity Prices(1) 7.7x 8.1x 7.0x 7.9x 13.0% 12.4% 2.1x Low Utilization(1) 9.7x 10.2x 8.1x 9.1x 10.4% 9.8% 2.4x Sources: Management model received 6/6/2018, company filings, investor presentations, Wall Street equity research and median Wall Street consensus 19 estimates as compiled by FactSet as of 6/14/2018. (1) Forecasts normalized for turnarounds each year of projection period as provided by Onyx Management.

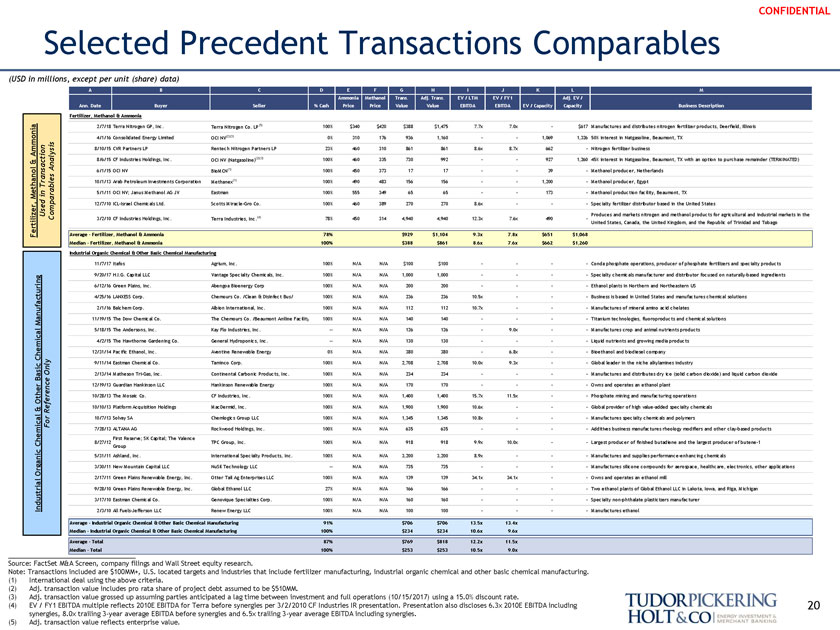

CONFIDENTIAL Selected Precedent Transactions Comparables (USD in millions, except per unit (share) data) A B C D E F G H I J K L M Ammonia Methanol Trans. Adj. Trans. EV / LTM EV / FY1 Adj. EV / Ann. Date Buyer Seller % Cash Price Price Value Value EBITDA EBITDA EV / Capacity Capacity Business Description Fertilizer, Methanol & Ammonia 2/7/18 Terra Nitrogen GP, Inc. Terra Nitrogen Co. LP (5) 100% $340 $420 $388 $1,475 7.7x 7.0x - $617 Manufactures and distributes nitrogen fertilizer products, Deerfield, Illinois 4/1/16 Consolidated Energy Limited OCI NV (2)(3) 0% 310 176 936 1,160 - - 1,069 1,326 50% interest in Natgasoline, Beaumont, TX 8/10/15 CVR Partners LP Rentech Nitrogen Partners LP 23% 460 310 861 861 8.6x 8.7x 662 - Nitrogen fertilizer business 8/6/15 CF Industries Holdings, Inc. OCI NV (Natgasoline) (2)(3) 100% 460 335 730 992 - - 927 1,260 45% interest in Natgasoline, Beaumont, TX with an option to purchase remainder (TERMINATED) 6/1/15 OCI NV BioMCN (1) 100% 450 373 17 17 - - 39 - Methanol producer, Netherlands 10/1/13 Arab Petroleum Investments Corporation Methanex (1) 100% 490 483 156 156 - - 1,200 - Methanol producer, Egypt 5/1/11 OCI NV; Janus Methanol AG JV Eastman 100% 555 349 65 65 - - 173 - Methanol production facility, Beaumont, TX 12/7/10 ICL-Israel Chemicals Ltd. Scotts Miracle-Gro Co. 100% 460 389 270 270 8.6x - - - Specialty fertilizer distributor based in the United States Produces and markets nitrogen and methanol products for agricultural and industrial markets in the 3/2/10 CF Industries Holdings, Inc. Terra Industries, Inc. (4) 78% 450 314 4,940 4,940 12.3x 7.6x 490 - United States, Canada, the United Kingdom, and the Republic of Trinidad and Tobago Average—Fertilizer, Methanol & Ammonia 78% $929 $1,104 9.3x 7.8x $ 651 $1,068 Median—Fertilizer, Methanol & Ammonia 100% $388 $861 8.6x 7.6x $ 662 $1,260 Industrial Organic Chemical & Other Basic Chemical Manufacturing 11/7/17 Itafos Agrium, Inc. 100% N/A N/A $100 $100 - - - - Conda phosphate operations, producer of phosphate fertilizers and specialty products 9/20/17 H.I.G. Capital LLC Vantage Specialty Chemicals, Inc. 100% N/A N/A 1,000 1,000 - - - - Specialty chemicals manufacturer and distributor focused on naturally-based ingredients 6/12/16 Green Plains, Inc. Abengoa Bioenergy Corp 100% N/A N/A 200 200 - - - - Ethanol plants in Northern and Northeastern US 4/25/16 LANXESS Corp. Chemours Co. /Clean & Disinfect Bus/ 100% N/A N/A 236 236 10.5x - - - Business is based in United States and manufactures chemical solutions 2/1/16 Balchem Corp. Albion International, Inc. 100% N/A N/A 112 112 10.7x - - - Manufactures of mineral amino acid chelates 11/19/15 The Dow Chemical Co. The Chemours Co. /Beaumont Aniline Facility 100% N/A N/A 140 140 - - - - Titanium technologies, fluoroproducts and chemical solutions 5/18/15 The Andersons, Inc. Kay Flo Industries, Inc. — N/A N/A 126 126 - 9.0x - - Manufactures crop and animal nutrients products 4/2/15 The Hawthorne Gardening Co. General Hydroponics, Inc. — N/A N/A 130 130 - - - - Liquid nutrients and growing media products 12/31/14 Pacific Ethanol, Inc. Aventine Renewable Energy 0% N/A N/A 380 380 - 6.8x - - Bioethanol and biodiesel company 9/11/14 Eastman Chemical Co. Taminco Corp. 100% N/A N/A 2,708 2,708 10.0x 9.3x - - Global leader in the niche alkylamines industry 2/13/14 Matheson Tri-Gas, Inc. Continental Carbonic Products, Inc. 100% N/A N/A 234 234 - - - - Manufactures and distributes dry ice (solid carbon dioxide) and liquid carbon dioxide 12/19/13 Guardian Hankinson LLC Hankinson Renewable Energy 100% N/A N/A 170 170 - - - - Owns and operates an ethanol plant 10/28/13 The Mosaic Co. CF Industries, Inc. 100% N/A N/A 1,400 1,400 15.7x 11.5x - - Phosphate mining and manufacturing operations 10/10/13 Platform Acquisition Holdings MacDermid, Inc. 100% N/A N/A 1,900 1,900 10.6x - - - Global provider of high value-added specialty chemicals 10/7/13 Solvay SA Chemlogics Group LLC 100% N/A N/A 1,345 1,345 10.8x - - - Manufactures specialty chemicals and polymers 7/28/13 ALTANA AG Rockwood Holdings, Inc. 100% N/A N/A 635 635 - - - - Additives business manufactures rheology modifiers and other clay-based products First Reserve; SK Capital; The Valence 8/27/12 TPC Group, Inc. 100% N/A N/A 918 918 9.9x 10.0x - - Largest producer of finished butadiene and the largest producer of butene-1 Group 5/31/11 Ashland, Inc. International Specialty Products, Inc. 100% N/A N/A 3,200 3,200 8.9x - - - Manufactures and supplies performance-enhancing chemicals 3/30/11 New Mountain Capital LLC NuSil Technology LLC — N/A N/A 735 735 - - - - Manufactures silicone compounds for aerospace, healthcare, electronics, other applications 2/17/11 Green Plains Renewable Energy, Inc. Otter Tail Ag Enterprises LLC 100% N/A N/A 139 139 34.1x 34.1x - - Owns and operates an ethanol mill 9/28/10 Green Plains Renewable Energy, Inc. Global Ethanol LLC 27% N/A N/A 166 166 - - - - Two ethanol plants of Global Ethanol LLC in Lakota, Iowa, and Riga, Michigan 3/17/10 Eastman Chemical Co. Genovique Specialties Corp. 100% N/A N/A 160 160 - - - - Specialty non-phthalate plasticizers manufacturer 2/3/10 All Fuels-Jefferson LLC Renew Energy LLC 100% N/A N/A 100 100 - - - - Manufactures ethanol Average—Industrial Organic Chemical & Other Basic Chemical Manufacturing 91% $706 $706 13.5x 13.4x Median—Industrial Organic Chemical & Other Basic Chemical Manufacturing 100% $234 $234 10.6x 9.6x Average—Total 87% $769 $818 12.2x 11.5x Median—Total 100% $253 $253 10.5x 9.0x Source: FactSet M&A Screen, company filings and Wall Street equity research. Note: Transactions included are $100MM+, U.S. located targets and industries that include fertilizer manufacturing, industrial organic chemical and other basic chemical manufacturing. (1) International deal using the above criteria. (2) Adj. transaction value includes pro rata share of project debt assumed to be $510MM. (3) Adj. transaction value grossed up assuming parties anticipated a lag time between investment and full operations (10/15/2017) using a 15.0% discount rate. (4) EV / FY1 EBITDA multiple reflects 2010E EBITDA for Terra before synergies per 3/2/2010 CF Industries IR presentation. Presentation also discloses 6.3x 2010E EBITDA including 20 synergies, 8.0x trailing 3-year average EBITDA before synergies and 6.5x trailing 3-year average EBITDA including synergies. (5) Adj. transaction value reflects enterprise value.

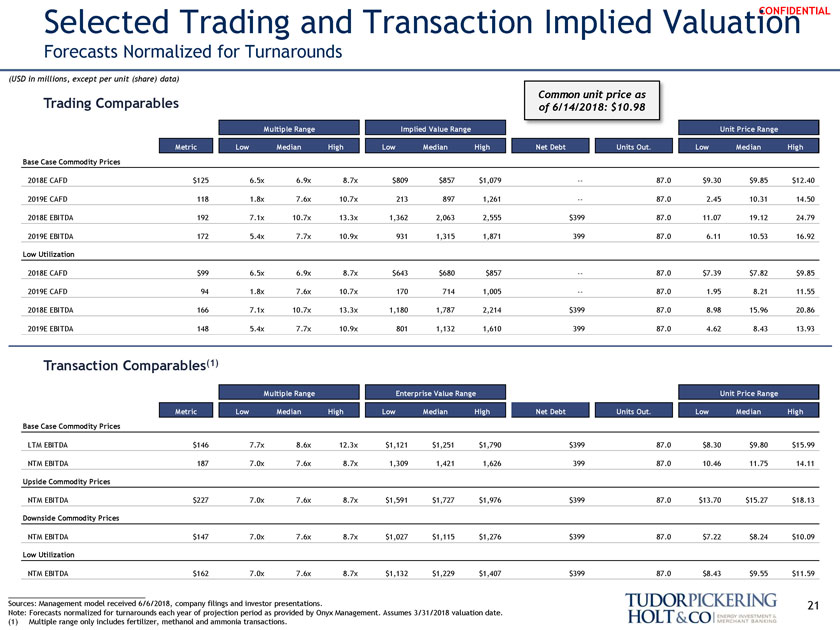

Selected Trading and Transaction Implied Valuation CONFIDENTIAL Forecasts Normalized for Turnarounds (USD in millions, except per unit (share) data) Common unit price as Trading Comparables of 6/14/2018: $ 10.98 Multiple Range Implied Value Range Unit Price Range Metric Low Median High Low Median High Net Debt Units Out. Low Median High Base Case Commodity Prices 2018E CAFD $125 6.5x 6.9x 8.7x $809 $857 $1,079 — 87.0 $9.30 $9.85 $12.40 2019E CAFD 118 1.8x 7.6x 10.7x 213 897 1,261 — 87.0 2.45 10.31 14.50 2018E EBITDA 192 7.1x 10.7x 13.3x 1,362 2,063 2,555 $399 87.0 11.07 19.12 24.79 2019E EBITDA 172 5.4x 7.7x 10.9x 931 1,315 1,871 399 87.0 6.11 10.53 16.92 Low Utilization 2018E CAFD $99 6.5x 6.9x 8.7x $643 $680 $857 — 87.0 $7.39 $7.82 $9.85 2019E CAFD 94 1.8x 7.6x 10.7x 170 714 1,005 — 87.0 1.95 8.21 11.55 2018E EBITDA 166 7.1x 10.7x 13.3x 1,180 1,787 2,214 $399 87.0 8.98 15.96 20.86 2019E EBITDA 148 5.4x 7.7x 10.9x 801 1,132 1,610 399 87.0 4.62 8.43 13.93 Transaction Comparables(1) Multiple Range Enterprise Value Range Unit Price Range Metric Low Median High Low Median High Net Debt Units Out. Low Median High Base Case Commodity Prices LTM EBITDA $146 7.7x 8.6x 12.3x $1,121 $1,251 $1,790 $399 87.0 $8.30 $9.80 $15.99 NTM EBITDA 187 7.0x 7.6x 8.7x 1,309 1,421 1,626 399 87.0 10.46 11.75 14.11 Upside Commodity Prices NTM EBITDA $227 7.0x 7.6x 8.7x $1,591 $1,727 $1,976 $399 87.0 $13.70 $15.27 $18.13 Downside Commodity Prices NTM EBITDA $147 7.0x 7.6x 8.7x $1,027 $1,115 $1,276 $399 87.0 $7.22 $8.24 $10.09 Low Utilization NTM EBITDA $162 7.0x 7.6x 8.7x $1,132 $1,229 $1,407 $399 87.0 $8.43 $9.55 $11.59 Sources: Management model received 6/6/2018, company filings and investor presentations. 21 Note: Forecasts normalized for turnarounds each year of projection period as provided by Onyx Management. Assumes 3/31/2018 valuation date. (1) Multiple range only includes fertilizer, methanol and ammonia transactions.

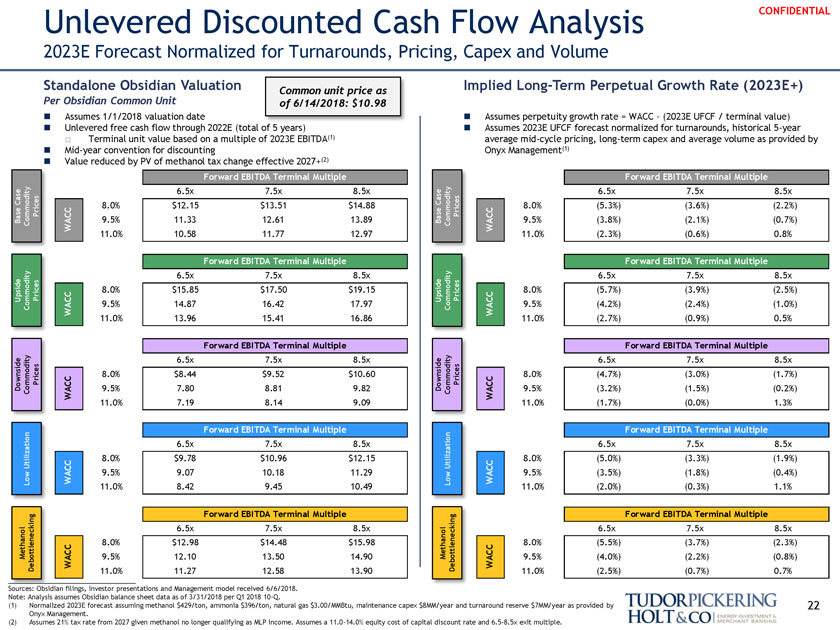

Unlevered Discounted Cash Flow Analysis CONFIDENTIAL 2023E Forecast Normalized for Turnarounds, Pricing, Capex and Volume Standalone Obsidian Valuation Common unit price as Implied Long-Term Perpetual Growth Rate (2023E+) Per Obsidian Common Unit of 6/14/2018: $10.98 Assumes 1/1/2018 valuation date Assumes perpetuity growth rate = WACC – (2023E UFCF / terminal value) Unlevered free cash flow through 2022E (total of 5 years) Assumes 2023E UFCF forecast normalized for turnarounds, historical 5-year Terminal unit value based on a multiple of 2023E EBITDA(1) average mid-cycle pricing, long-term capex and average volume as provided by Mid-year convention for discounting Onyx Management(1) Value reduced by PV of methanol tax change effective 2027+(2) Forward EBITDA Terminal Multiple Forward EBITDA Terminal Multiple 6.5x 7.5x 8.5x 6.5x 7.5x 8.5x 8.0% $12.15 $13.51 $14.88 8.0% (5.3%) (3.6%) (2.2%) Base Case Commodity Prices WA CC 9.5% 11.33 12.61 13.89 Base Case Commodity Prices WA CC 9.5% (3.8%) (2.1%) (0.7%) 11.0% 10.58 11.77 12.97 11.0% (2.3%) (0.6%) 0.8% Forward EBITDA Terminal Multiple Forward EBITDA Terminal Multiple 6.5x 7.5x 8.5x 6.5x 7.5x 8.5x 8.0% $15.85 $17.50 $19.15 8.0% (5.7%) (3.9%) (2.5%) Upside Commodity Prices WACC 9.5% 14.87 16.42 17.97 Upside Commodity Prices WACC 9.5% (4.2%) (2.4%) (1.0%) 11.0% 13.96 15.41 16.86 11.0% (2.7%) (0.9%) 0.5% Forward EBITDA Terminal Multiple Forward EBITDA Terminal Multiple 6.5x 7.5x 8.5x 6.5x 7.5x 8.5x 8.0% $8.44 $9.52 $10.60 8.0% (4.7%) (3.0%) (1.7%) Downside Commodity Prices W ACC 9.5% 7.80 8.81 9.82 Downside Commodity Prices W ACC 9.5% (3.2%) (1.5%) (0.2%) 11.0% 7.19 8.14 9.09 11.0% (1.7%) (0.0%) 1.3% Forward EBITDA Terminal Multiple Forward EBITDA Terminal Multiple 6.5x 7.5x 8.5x 6.5x 7.5x 8.5x 8.0% $9.78 $10.96 $12.15 8.0% (5.0%) (3.3%) (1.9%) Low Utilization WA CC 9.5% 9.07 10.18 11.29 Low Utilization WA CC 9.5% (3.5%) (1.8%) (0.4%) 11.0% 8.42 9.45 10.49 11.0% (2.0%) (0.3%) 1.1% Forward EBITDA Terminal Multiple Forward EBITDA Terminal Multiple 6.5x 7.5x 8.5x 6.5x 7.5x 8.5x 8.0% $12.98 $14.48 $15.98 8.0% (5.5%) (3.7%) (2.3%) Methanol Debottlenecking W ACC 9.5% 12.10 13.50 14.90 Methanol Debottlenecking W ACC 9.5% (4.0%) (2.2%) (0.8%) 11.0% 11.27 12.58 13.90 11.0% (2.5%) (0.7%) 0.7% Sources: Obsidian filings, investor presentations and Management model received 6/6/2018. Note: Analysis assumes Obsidian balance sheet data as of 3/31/2018 per Q1 2018 10-Q. (1) Normalized 2023E forecast assuming methanol $429/ton, ammonia $396/ton, natural gas $3.00/MMBtu, maintenance capex $8MM/year and turnaround reserve $7MM/year as provided by 22 Onyx Management. (2) Assumes 21% tax rate from 2027 given methanol no longer qualifying as MLP income. Assumes a 11.0-14.0% equity cost of capital discount rate and 6.5-8.5x exit multiple.

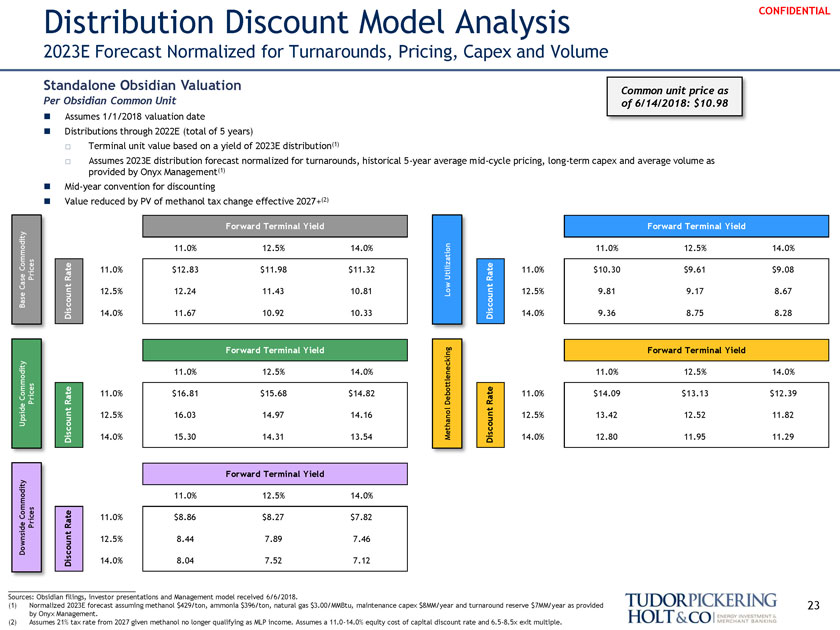

Distribution Discount Model Analysis CONFIDENTIAL 2023E Forecast Normalized for Turnarounds, Pricing, Capex and Volume Standalone Obsidian Valuation Common unit price as Per Obsidian Common Unit of 6/14/2018: $10.98 Assumes 1/1/2018 valuation date Distributions through 2022E (total of 5 years) Terminal unit value based on a yield of 2023E distribution(1) Assumes 2023E distribution forecast normalized for turnarounds, historical 5-year average mid-cycle pricing, long-term capex and average volume as provided by Onyx Management(1) Mid-year convention for discounting Value reduced by PV of methanol tax change effective 2027+(2) Forward Terminal Yield Forward Terminal Yield 11.0% 12.5% 14.0% 11.0% 12.5% 14.0% 11.0% $12.83 $11.98 $11.32 11.0% $10.30 $9.61 $9.08 12.5% 12.24 11.43 10.81 12.5% 9.81 9.17 8.67 Base Case Commodity Prices D is co u nt Ra t e 14.0% 11.67 10.92 10.33 Low Utilization D is co u nt Ra t e 14.0% 9.36 8.75 8.28 Forward Terminal Yield Forward Terminal Yield 11.0% 12.5% 14.0% 11.0% 12.5% 14.0% 11.0% $16.81 $15.68 $14.82 11.0% $14.09 $13.13 $12.39 12.5% 16.03 14.97 14.16 12.5% 13.42 12.52 11.82 Upside Commodity Prices D i s co unt Rat e 14.0% 15.30 14.31 13.54 Methanol Debottlenecking D i s co unt Rat e 14.0% 12.80 11.95 11.29 Forward Terminal Yield 11.0% 12.5% 14.0% 11.0% $8.86 $8.27 $7.82 12.5% 8.44 7.89 7.46 Downside Commodity Prices Disco u nt Rat e 14.0% 8.04 7.52 7.12 Sources: Obsidian filings, investor presentations and Management model received 6/6/2018. (1) Normalized 2023E forecast assuming methanol $429/ton, ammonia $396/ton, natural gas $3.00/MMBtu, maintenance capex $8MM/year and turnaround reserve $7MM/year as provided 23 by Onyx Management. (2) Assumes 21% tax rate from 2027 given methanol no longer qualifying as MLP income. Assumes a 11.0-14.0% equity cost of capital discount rate and 6.5-8.5x exit multiple.

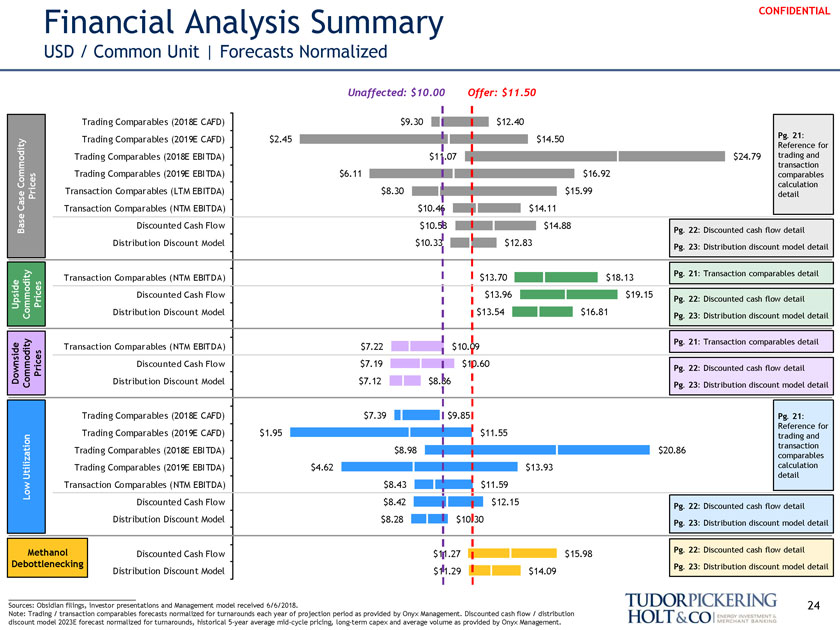

Financial Analysis Summary CONFIDENTIAL USD / Common Unit | Forecasts Normalized Unaffected: $10.00 Offer: $11.50 Trading Comparables (2018E CAFD) $9.30 $12.40 Trading Comparables (2019E CAFD) $2.45 $14.50 Pg. 21: Reference for Trading Comparables (2018E EBITDA) $11.07 $24.79 trading and transaction Trading Comparables (2019E EBITDA) $6.11 $16.92 comparables Commodity calculation Transaction Comparables (LTM EBITDA) $8.30 $15.99 Case Prices detail Transaction Comparables (NTM EBITDA) $10.46 $14.11 Discounted Cash Flow $10.58 $14.88 Base Pg. 22: Discounted cash flow detail Distribution Discount Model $10.33 $12.83 Pg. 23: Distribution discount model detail Transaction Comparables (NTM EBITDA) $13.70 $18.13 Pg. 21: Transaction comparables detail Discounted Cash Flow $13.96 $19.15 Upside Prices Pg. 22: Discounted cash flow detail Commodity Distribution Discount Model $13.54 $16.81 Pg. 23: Distribution discount model detail Pg. 21: Transaction comparables detail Transaction Comparables (NTM EBITDA) $7.22 $10.09 Discounted Cash Flow $7.19 $10.60 Prices Pg. 22: Discounted cash flow detail Downside Commodity Distribution Discount Model $7.12 $8.86 Pg. 23: Distribution discount model detail Trading Comparables (2018E CAFD) $7.39 $9.85 Pg. 21: Reference for Trading Comparables (2019E CAFD) $1.95 $11.55 trading and transaction Trading Comparables (2018E EBITDA) $8.98 $20.86 comparables Trading Comparables (2019E EBITDA) $4.62 $13.93 calculation Utilization detail Low Transaction Comparables (NTM EBITDA) $8.43 $11.59 Discounted Cash Flow $8.42 $12.15 Pg. 22: Discounted cash flow detail Distribution Discount Model $8.28 $10.30 Pg. 23: Distribution discount model detail Methanol Discounted Cash Flow $11.27 $15.98 Pg. 22: Discounted cash flow detail Debottlenecking Pg. 23: Distribution discount model detail Distribution Discount Model $11.29 $14.09 ___________________________________ Sources: Obsidian filings, investor presentations and Management model received 6/6/2018. 24 Note: Trading / transaction comparables forecasts normalized for turnarounds each year of projection period as provided by Onyx Management. Discounted cash flow / distribution discount model 2023E forecast normalized for turnarounds, historical 5-year average mid-cycle pricing, long-term capex and average volume as provided by Onyx Management.

CONFIDENTIAL IV. Supplemental Analysis

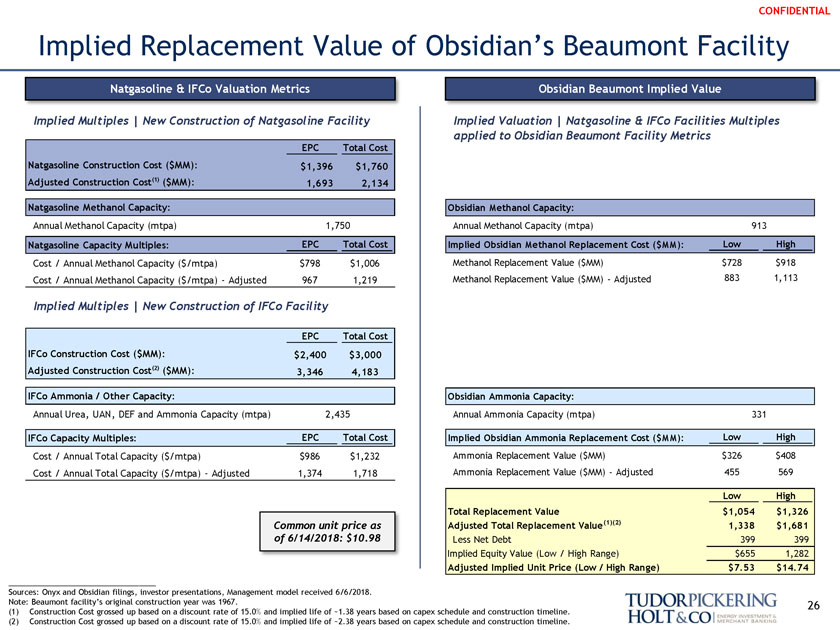

CONFIDENTIAL Implied Replacement Value of Obsidian’s Beaumont Facility Natgasoline & IFCo Valuation Metrics Obsidian Beaumont Implied Value Implied Multiples | New Construction of Natgasoline Facility Implied Valuation | Natgasoline & IFCo Facilities Multiples applied to Obsidian Beaumont Facility Metrics EPC Total Cost Natgasoline Construction Cost ($MM): $1,396 $1,760 Adjusted Construction Cost(1) ($MM): 1,693 2,134 Natgasoline Methanol Capacity: Obsidian Methanol Capacity: Annual Methanol Capacity (mtpa) 1,750 Annual Methanol Capacity (mtpa) 913 Natgasoline Capacity Multiples: EPC Total Cost Implied Obsidian Methanol Replacement Cost ($MM): Low High Cost / Annual Methanol Capacity ($/mtpa) $798 $1,006 Methanol Replacement Value ($MM) $728 $918 Cost / Annual Methanol Capacity ($/mtpa)—Adjusted 967 1,219 Methanol Replacement Value ($MM)—Adjusted 883 1,113 Implied Multiples | New Construction of IFCo Facility EPC Total Cost IFCo Construction Cost ($MM): $2,400 $3,000 Adjusted Construction Cost(2) ($MM): 3,346 4,183 IFCo Ammonia / Other Capacity: Obsidian Ammonia Capacity: Annual Urea, UAN, DEF and Ammonia Capacity (mtpa) 2,435 Annual Ammonia Capacity (mtpa) 331 IFCo Capacity Multiples: EPC Total Cost Implied Obsidian Ammonia Replacement Cost ($MM): Low High Cost / Annual Total Capacity ($/mtpa) $986 $1,232 Ammonia Replacement Value ($MM) $326 $408 Cost / Annual Total Capacity ($/mtpa)—Adjusted 1,374 1,718 Ammonia Replacement Value ($MM)—Adjusted 455 569 Low High Total Replacement Value $1,054 $1,326 Common unit price as Adjusted Total Replacement Value(1)(2) 1,338 $1,681 of 6/14/2018: $10.98 Less Net Debt 399 399 Implied Equity Value (Low / High Range) $655 1,282 Adjusted Implied Unit Price (Low / High Range) $7.53 $14.74 Sources: Onyx and Obsidian filings, investor presentations, Management model received 6/6/2018. Note: Beaumont facility’s original construction year was 1967. 26 (1) Construction Cost grossed up based on a discount rate of 15.0% and implied life of ~1.38 years based on capex schedule and construction timeline. (2) Construction Cost grossed up based on a discount rate of 15.0% and implied life of ~2.38 years based on capex schedule and construction timeline.

CONFIDENTIAL V. Additional Analysis as Requested by Obsidian Conflicts Committee

CONFIDENTIAL Methanex Equity Research Commentary year declines from ~$100/t total to ~ 75/t total before prices level off in Q4. No and 2019 We now model 2019E methanol ASP of $346/t versus $337/t previously.” “OCI’s Natgasoline plant is expected to start up imminently with spot product expected in the market mid-summer, which is when we begin to model lower methanol prices. It’s possible our price forecasts prove conservative though considering” — BMO Capital Markets (May 31, 2018) creased average price in 2018 and 2019 to $ and $ , respectively. This is up from $377/mt for 2018 and $363/mt for 2019.” — Cowen and Company (June 7, 2018) “Pricing resilient thus far, but expected fade as supply improves—While ipate as these plants restart and new greenfield capacity comes online in the US.” — Raymond James (April 27, 2018) our 2019E EBITDA forecast using the year average realized methanol price (a slight premium to Methanex’s 10-year average EV/forward EBITDA multiple of ~6.7x).” — RBC Capital Markets (June 5, 2018) “Methanol prices have moderat start , and the impact of new/expanded olefins capacity on the U.S. Gulf Coast on methanol-to-olefins (MTO) economics/operating rates.” — TD Securities (April 27, 2018) “The main driver near term has been continued strong MTO dem in ) as capacity comes online in the US and potential output from Iran.” — UBS Research (April 25, 2018) Forecasted Methanol Price (USD/mt) 2018E 2019E 2018E 2019E Broker (1) (1) Contract Contract Realized Realized BMO Capital Markets $463 $421 $375 $346 Cowen and Company -—- 388 370 Raymond James 427 370 366 320 RBC Capital Markets 451 453 383 385 Scotiabank GBM 454 390 385 337 TD Securities 447 407 383 350 UBS Research -—- 366 — Broker Median $451 $407 $383 $348 Obsidian (Base) $473 $433 $387 $352 Obsidian (Upside) 520 476 425 387 Obsidian (Downside) 426 390 348 317 Source: Wall Street equity research. (1) Reflects U.S. Gulf Coast or North American contract price.

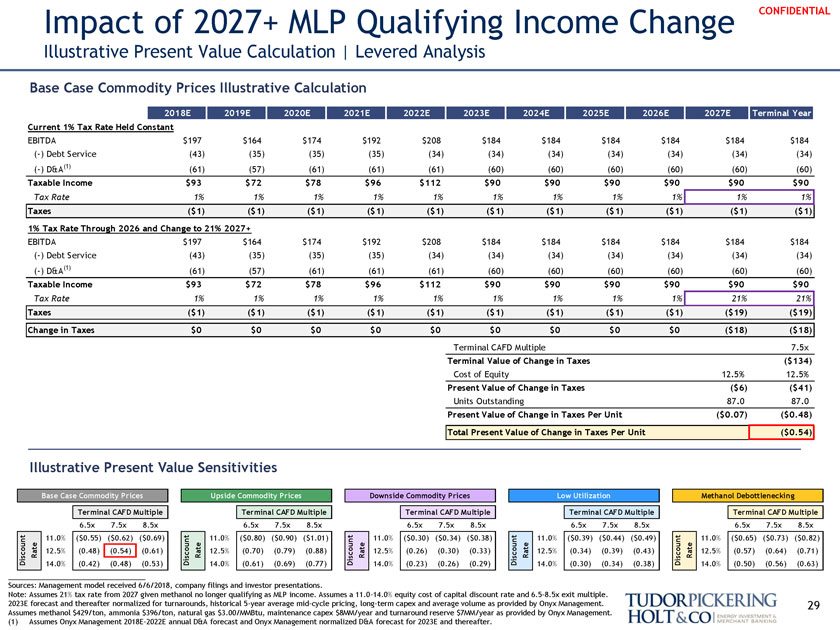

Impact of 2027+ MLP Qualifying Income Change CONFIDENTIAL Illustrative Present Value Calculation | Levered Analysis Base Case Commodity Prices Illustrative Calculation 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E 2026E 2027E Terminal Year Current 1% Tax Rate Held Constant EBITDA $197 $164 $174 $192 $208 $184 $184 $184 $184 $184 $184 (-) Debt Service (43) (35) (35) (35) (34) (34) (34) (34) (34) (34) (34) (-) D&A (1) (61) (57) (61) (61) (61) (60) (60) (60) (60) (60) (60) Taxable Income $93 $72 $78 $96 $112 $90 $90 $90 $90 $90 $90 Tax Rate 1% 1% 1% 1% 1% 1% 1% 1% 1% 1% 1% Taxes ($1) ($1) ($1) ($1) ($1) ($1) ($1) ($1) ($1) ($1) ($1) 1% Tax Rate Through 2026 and Change to 21% 2027+ EBITDA $197 $164 $174 $192 $208 $184 $184 $184 $184 $184 $184 (-) Debt Service (43) (35) (35) (35) (34) (34) (34) (34) (34) (34) (34) (-) D&A (1) (61) (57) (61) (61) (61) (60) (60) (60) (60) (60) (60) Taxable Income $93 $72 $78 $96 $112 $90 $90 $90 $90 $90 $90 Tax Rate 1% 1% 1% 1% 1% 1% 1% 1% 1% 21% 21% Taxes ($1) ($1) ($1) ($1) ($1) ($1) ($1) ($1) ($1) ($19) ($19) Change in Taxes $0 $0 $0 $0 $0 $0 $0 $0 $0 ($18) ($18) Terminal CAFD Multiple 7.5x Terminal Value of Change in Taxes ($134) Cost of Equity 12.5% 12.5% Present Value of Change in Taxes ($6) ($41) Units Outstanding 87.0 87.0 Present Value of Change in Taxes Per Unit ($0.07) ($0.48) Total Present Value of Change in Taxes Per Unit ($0.54) Illustrative Present Value Sensitivities Base Case Commodity Prices Upside Commodity Prices Downside Commodity Prices Low Utilization Methanol Debottlenecking Terminal CAFD Multiple Terminal CAFD Multiple Terminal CAFD Multiple Terminal CAFD Multiple Terminal CAFD Multiple 6.5x 7.5x 8.5x 6.5x 7.5x 8.5x 6.5x 7.5x 8.5x 6.5x 7.5x 8.5x 6.5x 7.5x 8.5x 11.0% ($0.55) ($0.62) ($0.69) 11.0% ($0.80) ($0.90) ($1.01) 11.0% ($0.30) ($0.34) ($0.38) 11.0% ($0.39) ($0.44) ($0.49) 11.0% ($0.65) ($0.73) ($0.82) Discount Ra t e 12.5% (0.48) (0.54) (0.61) Discount Ra t e 12.5% (0.70) (0.79) (0.88) Discount Ra t e 12.5% (0.26) (0.30) (0.33) Discount Ra t e 12.5% (0.34) (0.39) (0.43) Discount Ra t e 12.5% (0.57) (0.64) (0.71) 14.0% (0.42) (0.48) (0.53) 14.0% (0.61) (0.69) (0.77) 14.0% (0.23) (0.26) (0.29) 14.0% (0.30) (0.34) (0.38) 14.0% (0.50) (0.56) (0.63) Sources: Management model received 6/6/2018, company filings and investor presentations. Note: Assumes 21% tax rate from 2027 given methanol no longer qualifying as MLP income. Assumes a 11.0-14.0% equity cost of capital discount rate and 6.5-8.5x exit multiple. 2023E forecast and thereafter normalized for turnarounds, historical 5-year average mid-cycle pricing, long-term capex and average volume as provided by Onyx Management. 29 Assumes methanol $429/ton, ammonia $396/ton, natural gas $3.00/MMBtu, maintenance capex $8MM/year and turnaround reserve $7MM/year as provided by Onyx Management. (1) Assumes Onyx Management 2018E-2022E annual D&A forecast and Onyx Management normalized D&A forecast for 2023E and thereafter.

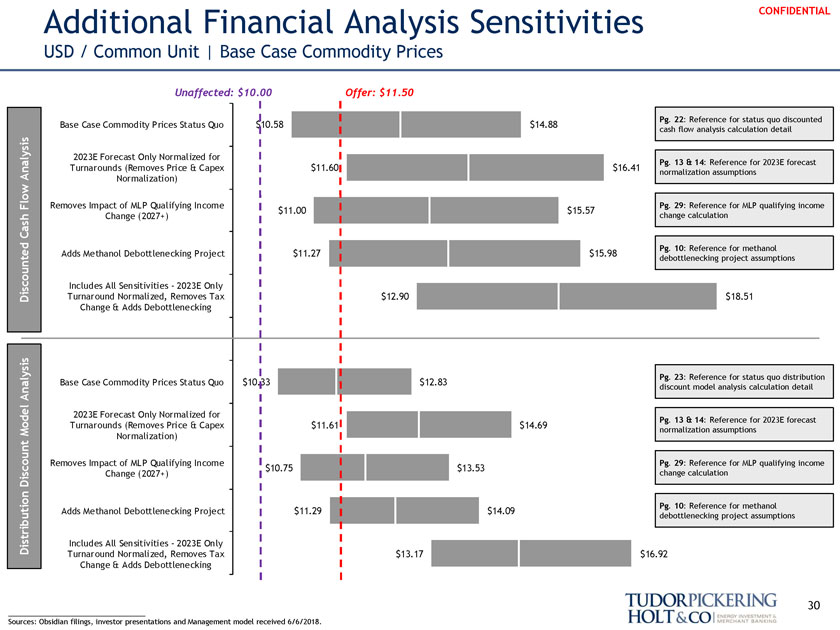

Additional Financial Analysis Sensitivities CONFIDENTIAL USD / Common Unit | Base Case Commodity Prices Unaffected: $10.00 Offer: $11.50 Pg. 22: Reference for status quo discounted Base Case Commodity Prices Status Quo $10.58 $14.88 cash flow analysis calculation detail 2023E Forecast Only Normalized for Pg. 13 & 14: Reference for 2023E forecast Turnarounds (Removes Price & Capex $11.60 $16.41 Analysis normalization assumptions Normalization) Flow Removes Impact of MLP Qualifying Income Pg. 29: Reference for MLP qualifying income Cash Change (2027+) $11.00 $15.57 change calculation Pg. 10: Reference for methanol Adds Methanol Debottlenecking Project $11.27 $15.98 debottlenecking project assumptions Includes All Sensitivities—2023E Only Discounted Turnaround Normalized, Removes Tax $12.90 $18.51 Change & Adds Debottlenecking Pg. 23: Reference for status quo distribution Base Case Commodity Prices Status Quo $10.33 $12.83 Analysis discount model analysis calculation detail 2023E Forecast Only Normalized for Pg. 13 & 14: Reference for 2023E forecast Turnarounds (Removes Price & Capex $11.61 $14.69 Model normalization assumptions Normalization) Removes Impact of MLP Qualifying Income Pg. 29: Reference for MLP qualifying income $10.75 $13.53 Discount Change (2027+) change calculation Pg. 10: Reference for methanol Adds Methanol Debottlenecking Project $11.29 $14.09 debottlenecking project assumptions Distribution Includes All Sensitivities—2023E Only Turnaround Normalized, Removes Tax $13.17 $16.92 Change & Adds Debottlenecking 30 ___________________________________ Sources: Obsidian filings, investor presentations and Management model received 6/6/2018.

About The Firm Tudor, Pickering, Holt & Co. is an integrated energy investment and merchant bank, providing high quality advice and services to institutional and corporate clients. Through the company’s two broker- dealer units, Tudor, Pickering, Holt & Co. Securities, Inc. (TPHCSI) and Tudor Pickering Holt & Co Advisors LP (TPHCA), members FINRA, together with affiliates in the United Kingdom and Canada, the company offers securities and investment banking services to the energy community. Perella Weinberg Partners Capital Management LP is an SEC registered investment adviser that delivers a suite of energy investment strategies. The firm, headquartered in Houston, Texas, has approximately 170 employees and offices in Calgary, Canada; Denver, Colorado; New York, New York; and London, England. Contact Us Houston (Research, Sales and Trading): 713-333-2960 Houston (Investment Banking): 713-333-7100 Houston (Asset Management): 713-337-3999 Denver (Sales): 303-300-1900 Denver (Investment Banking): 303-300-1900 New York (Investment Banking): 212-610-1660 New York (Research, Sales): 212-610-1600 London: +011 44(0) 20 7268 2800 Calgary: 403-705-7830 www.TPHco.com Copyright 2018 — Tudor, Pickering, Holt & Co. CONFIDENTIAL Disclosure Statement Tudor, Pickering, Holt & Co. does not provide accounting, tax or legal advice. In addition, we mutually agree that, subject to applicable law, you (and your employees, representatives and other agents) may disclose any aspects of any potential transaction or structure described herein that are necessary to support any U.S. federal income tax benefits, and all materials of any kind (including tax opinions and other tax analyses) related to those benefits, with no limitations imposed by Tudor, Pickering, Holt & Co. The information contained herein is confidential (except for information relating to United States tax issues) and may not be reproduced in whole or in part. Tudor, Pickering, Holt & Co. assumes no responsibility for independent verification of third-party information and has relied on such information being complete and accurate in all material respects. To the extent such information includes estimates and forecasts of future financial performance (including estimates of potential cost savings and synergies) prepared by, reviewed or discussed with the managements of your company and/ or other potential transaction participants or obtained from public sources, we have assumed that such estimates and forecasts have been reasonably prepared on bases reflecting the best currently available estimates and judgments of such managements (or, with respect to estimates and forecasts obtained from public sources, represent reasonable estimates). These materials were designed for use by specific persons familiar with the business and the affairs of your company and Tudor, Pickering, Holt & Co. materials. Under no circumstances is this presentation to be used or considered as an offer to sell or a solicitation of any offer to buy, any security. Prior to making any trade, you should discuss with your professional tax, accounting, or regulatory advisers how such particular trade(s) affect you. This brief statement does not disclose all of the risks and other significant aspects of entering into any particular transaction. Tudor, Pickering, Holt & Co. operates in the United Kingdom under the trading name Perella Weinberg Partners UK LLP (authorized and regulated by the Financial Conduct Authority), and in Canada through its affiliate, Tudor, Pickering, Holt & Co. Securities – Canada, ULC, located in Calgary, Alberta.